Embed Size (px)

DESCRIPTION

accounting

Citation preview

1

ACCY 308Course Introduction

2

Contact DetailsCourse Co-ordinator/Lecturer

Kevin Simpkins, Adjunct ProfessorRH 716 Phone: 463 9651

Email: [email protected]

LecturerDr Thu Phuong Truong, Senior Lecturer

RH 615 Phone: 463 5233 Ext 8961Email: [email protected]

Administrative Co-ordinatorLee Vassiliadis

RH708 Phone: 4635383Email: [email protected]

3

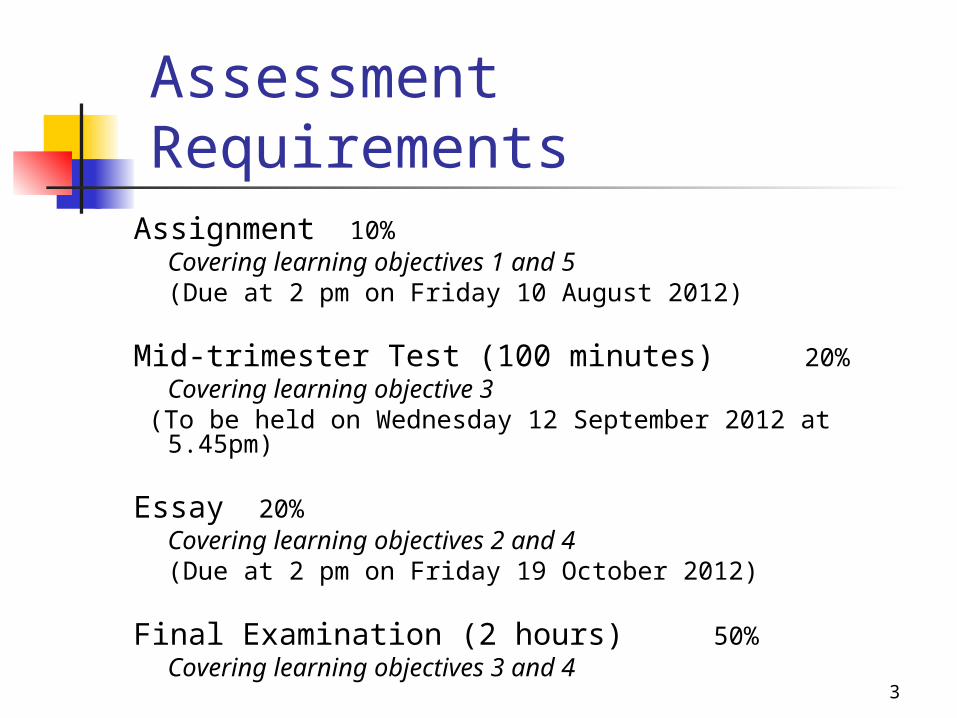

Assessment Requirements

Assignment 10%Covering learning objectives 1 and 5(Due at 2 pm on Friday 10 August 2012)

Mid-trimester Test (100 minutes)20%Covering learning objective 3

(To be held on Wednesday 12 September 2012 at 5.45pm)

Essay 20%Covering learning objectives 2 and 4(Due at 2 pm on Friday 19 October 2012)

Final Examination (2 hours) 50%Covering learning objectives 3 and 4

4

Mandatory Course Requirements

In addition to obtaining an overall course

mark of 50% or more, students must:

Attend at least 6 out of 8 tutorials; and

Make a reasonable attempt at each of the assignment and essay.

5

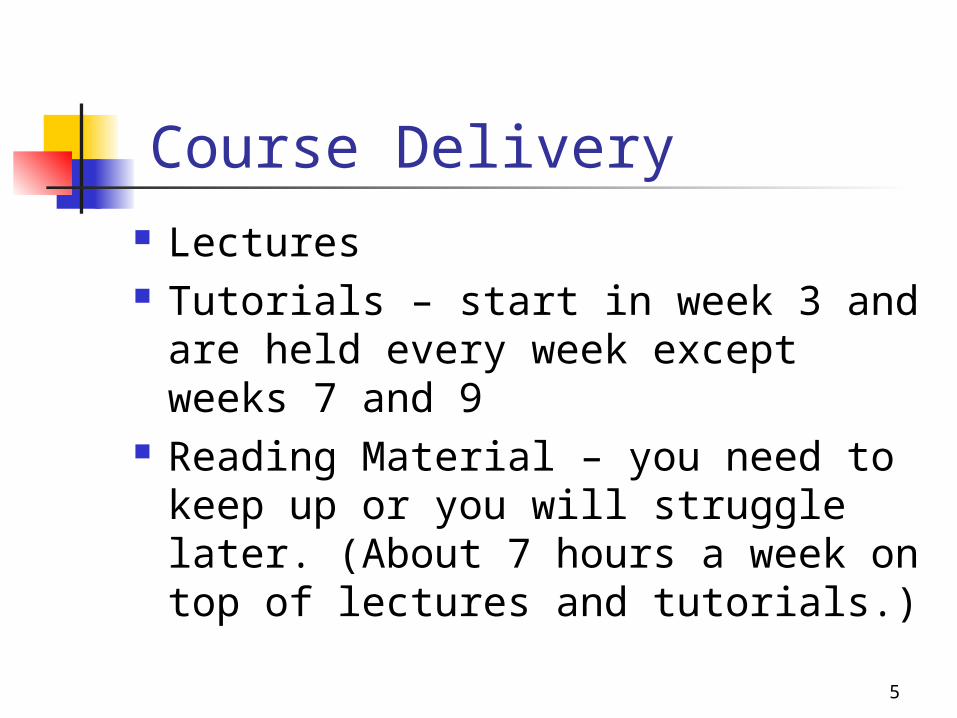

Course Delivery Lectures Tutorials – start in week 3 and are

held every week except weeks 7 and 9

Reading Material – you need to keep up or you will struggle later. (About 7 hours a week on top of lectures and tutorials.)

6

Overview of NZ Financial Reporting

Environment

7

What is GAAP?

Financial Reporting Act, s 11 states:Financial Reporting Act, s 11 states:

““The financial statements of a reporting entity must comply with generally accepted accounting practice.”.”

8

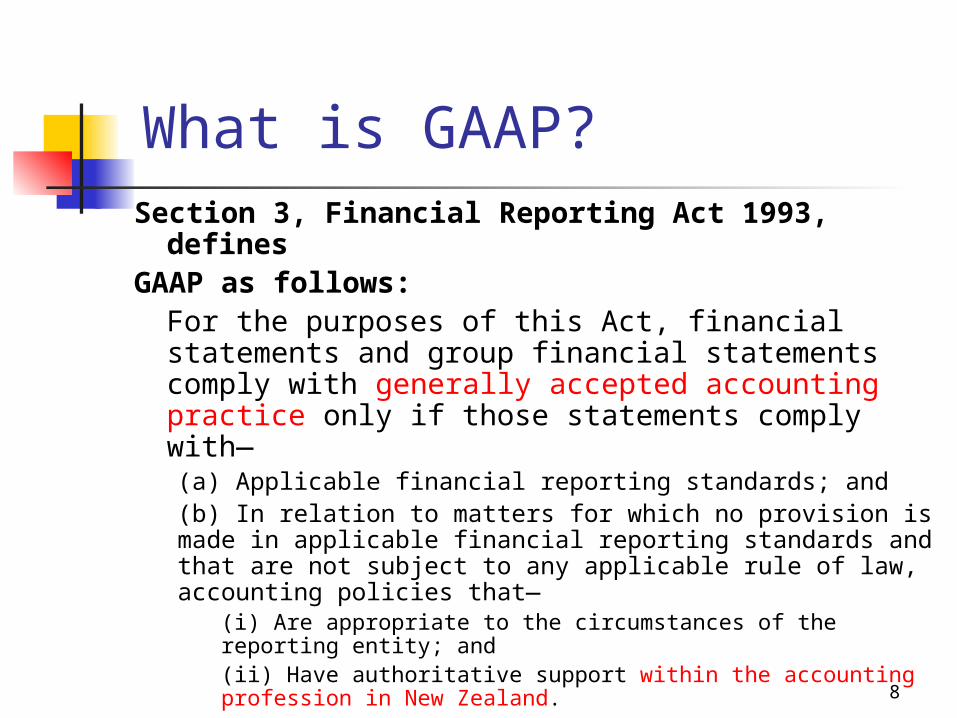

What is GAAP?Section 3, Financial Reporting Act 1993,

definesGAAP as follows:

For the purposes of this Act, financial statements and group financial statements comply with generally accepted accounting practice only if those statements comply with—(a) Applicable financial reporting standards; and(b) In relation to matters for which no provision is made in applicable financial reporting standards and that are not subject to any applicable rule of law, accounting policies that—

(i) Are appropriate to the circumstances of the reporting entity; and(ii) Have authoritative support within the accounting profession in New Zealand.

9

What is GAAP?

Aspects worth noting:Aspects worth noting:

GAAP is a _____________constructGAAP is a _____________construct

GAAP is ______________GAAP is ______________

10

A Professional Construct “Accounting has been created and

developed to accomplish various desired objectives and, therefore, it is not based on fundamental laws or absolute precepts.” (Catlett, 1960, 44)

11

Accounting – a Professional Language

“Quite simply, accounting is a language…. when you study accounting you are essentially learning this specialised language.” www.moneyinstructor.com

12

What is GAAP?

Points to note:Points to note: GAAP is a ____________ constructGAAP is a ____________ construct

GAAP is ______________GAAP is ______________ But what about ____________?But what about ____________?

13

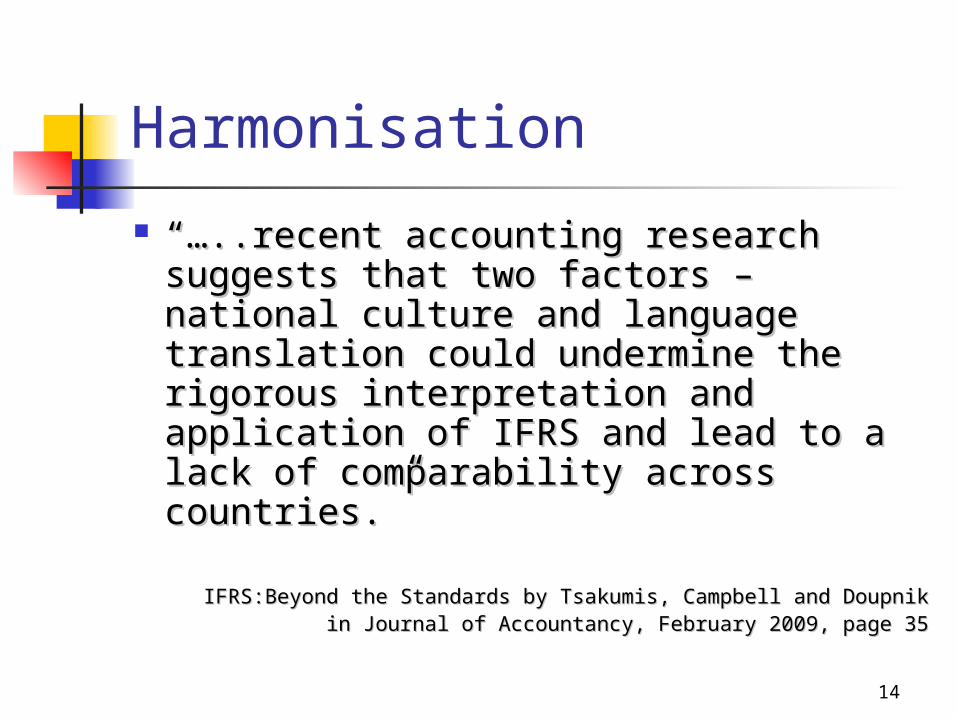

Harmonisation

Question:Question:

If accounting is a language which If accounting is a language which will develop in a jurisdictional will develop in a jurisdictional culture, what is the impact on culture, what is the impact on harmonisation of accounting?harmonisation of accounting?

(even if we have identical standards (even if we have identical standards across jurisdictions)across jurisdictions)

14

Harmonisation

“…“…..recent accounting research ..recent accounting research suggests that two factors – national suggests that two factors – national culture and language translation culture and language translation could undermine the rigorous could undermine the rigorous interpretation and application of IFRS interpretation and application of IFRS and lead to a lack of comparability and lead to a lack of comparability across countries.” across countries.”

IFRS:Beyond the Standards by Tsakumis, Campbell and DoupnikIFRS:Beyond the Standards by Tsakumis, Campbell and Doupnikin Journal of Accountancy, February 2009, page 35in Journal of Accountancy, February 2009, page 35

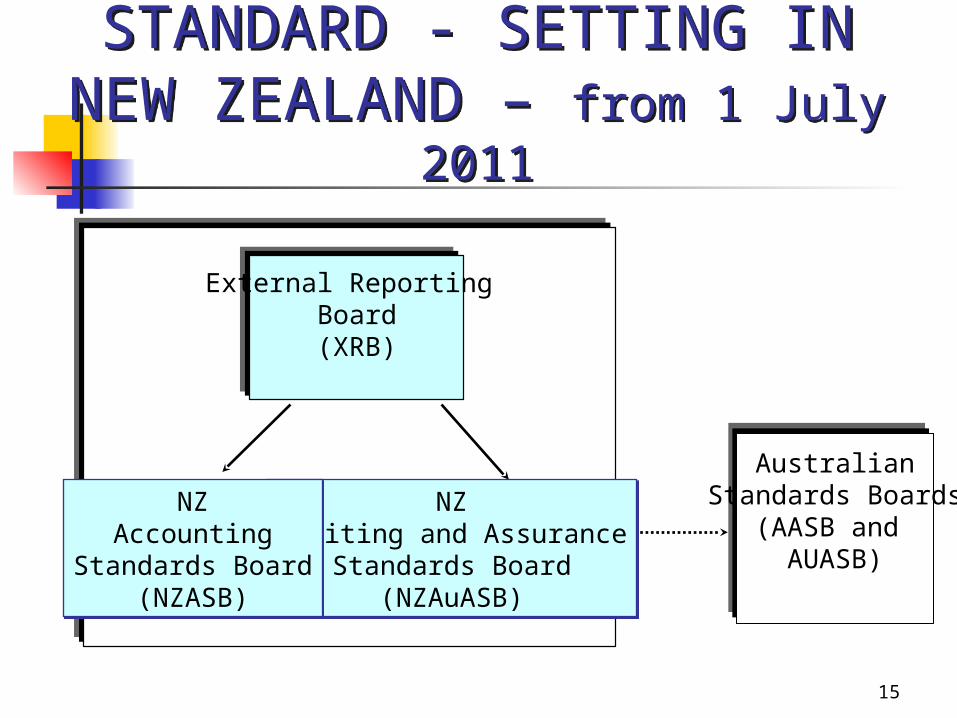

15

STANDARD - SETTING IN NEW ZEALAND – from 1 July

2011

STANDARD - SETTING IN NEW ZEALAND – from 1 July

2011

External Reporting Board(XRB)

AustralianStandards Boards

(AASB and AUASB)

NZAuditing and Assurance

Standards Board(NZAuASB)

NZAuditing and Assurance

Standards Board(NZAuASB)

NZAccounting

Standards Board(NZASB)

NZAccounting

Standards Board(NZASB)

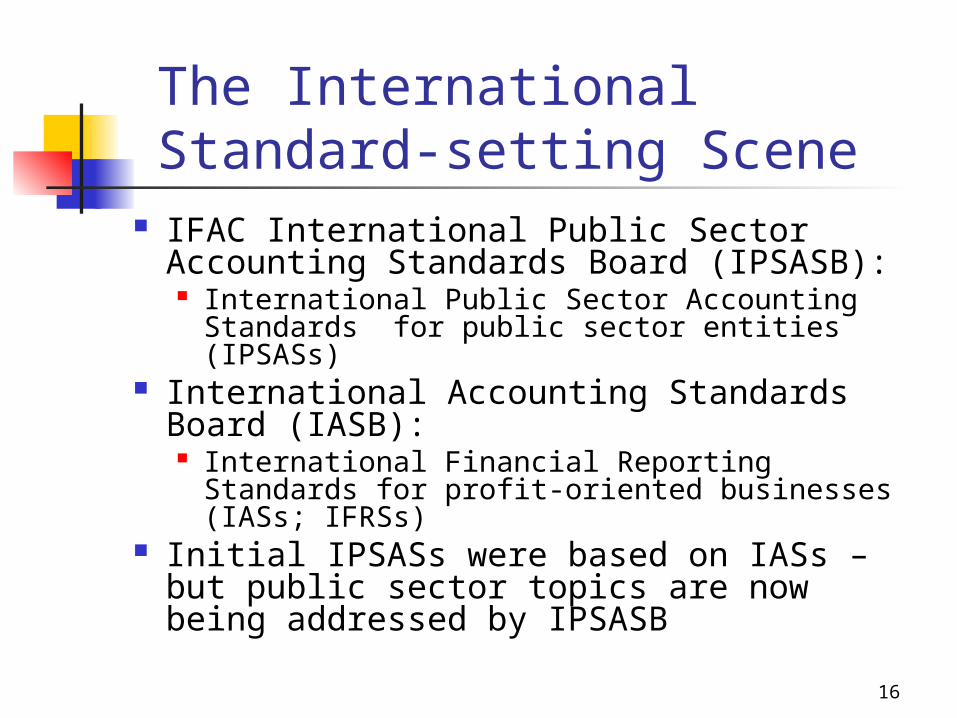

16

The International Standard-setting Scene

IFAC International Public Sector Accounting Standards Board (IPSASB): International Public Sector Accounting

Standards for public sector entities (IPSASs) International Accounting Standards

Board (IASB): International Financial Reporting Standards

for profit-oriented businesses (IASs; IFRSs) Initial IPSASs were based on IASs – but

public sector topics are now being addressed by IPSASB

17

Standards and Concepts

What is the What is the relationship relationship between the between the New Zealand New Zealand Framework and Framework and applicable applicable financial financial reporting reporting standards?standards?

Not a legal Not a legal documentdocument

In cases of In cases of conflict, the conflict, the requirements of requirements of Standards prevailStandards prevail

Standard setters Standard setters should be guided should be guided by framework in by framework in establishing establishing standards.standards.

18

Reading for Thursday Please

““Financial Accounting: In Financial Accounting: In CommunicatingCommunicating

Reality, We Construct Reality” Reality, We Construct Reality” Hines (1988)

Ask Yourself: What is Hines trying to say?Ask Yourself: What is Hines trying to say?

Identify a passage or theme that you Identify a passage or theme that you liked/disliked and note why.liked/disliked and note why.

19

Truth Statements

Are the following statements true?Are the following statements true? How do you know that they are true How do you know that they are true

or false?or false?

a) 2 + 2 = 4a) 2 + 2 = 4

b) Telecom’s profit in 2001 in New b) Telecom’s profit in 2001 in New Zealand Zealand was $642 million. was $642 million.

20

““Financial Accounting: In Financial Accounting: In CommunicatingCommunicating

Reality, We Construct Reality” Reality, We Construct Reality” Hines (1988)

Ask Yourself: What is Hines trying to say?Ask Yourself: What is Hines trying to say?

Identify a passage or theme that you Identify a passage or theme that you liked/disliked and note why.liked/disliked and note why.

21

Course Themes

22

Reporting Entity

What is an entity?What is an entity? Which entities should be required to Which entities should be required to

report?report? Should there be differences in Should there be differences in

accounting and reporting accounting and reporting requirements for different entities? On requirements for different entities? On what basis – what basis – _______________________________ etc? _______________________________ etc? If If so, why?so, why?

23

Relevance

Information is Information is relevantrelevant if it: if it:“… “… influences the economic decisions of users by influences the economic decisions of users by

helping them evaluate past, present or future helping them evaluate past, present or future events or confirming, or correcting, their past events or confirming, or correcting, their past evaluations” (Para 26, Part B of NZ Framework).evaluations” (Para 26, Part B of NZ Framework).

““RelevantRelevant financial information is capable financial information is capable of making a difference in the decisions of making a difference in the decisions made by users. Information may be made by users. Information may be capable of making a difference in a capable of making a difference in a decision even if some users choose not to decision even if some users choose not to take advantage of it or are already aware take advantage of it or are already aware of it from other sources.” (AQC6, Part A of of it from other sources.” (AQC6, Part A of NZ Framework)NZ Framework)

24

Relevance

““Financial information is capable of Financial information is capable of making a difference in decisions if it making a difference in decisions if it has _________ value, ____________ value has _________ value, ____________ value or both.”or both.”

(AQC7, Part A of NZ Framework)(AQC7, Part A of NZ Framework)

25

Reliability

NZ Framework (old, Part B): “to be useful, NZ Framework (old, Part B): “to be useful, information must also be reliable” (para B31)information must also be reliable” (para B31)

Information is reliable if it “is free from material Information is reliable if it “is free from material bias and error and can be depended upon by users bias and error and can be depended upon by users to represent faithfully that which it either purports to represent faithfully that which it either purports to represent or could reasonably be expected to to represent or could reasonably be expected to represent” (para B31)represent” (para B31)

In addition, the NZ Framework (Part B) In addition, the NZ Framework (Part B) incorporates into reliability: substance over incorporates into reliability: substance over form, neutrality, prudence and form, neutrality, prudence and completeness.completeness.

26

And now instead of reliability– Representational Faithfulness

“To be useful, financial information must not only represent relevant phenomena, but it must also faithfully represent the phenomena that it purports to represent. To be a perfectly faithful representation, a depiction would have three characteristics. It would be ________, ______and ____________.”

(AQC12, Part A of NZ Framework)(AQC12, Part A of NZ Framework)

27

Substance over Form

Defined in Para B35 of the NZ Defined in Para B35 of the NZ Framework (Part B):Framework (Part B):

““it is necessary that [transactions it is necessary that [transactions and other events] are accounted and other events] are accounted for and presented in accordance for and presented in accordance with their substance and economic with their substance and economic reality and not merely their legal reality and not merely their legal form.”form.”

28

Substance over Form – Current IASB Thinking

“Substance over form is not considered a separate component of faithful representation because it would be redundant. Faithful representation means that financial information represents the substance of an economic phenomenon rather than merely representing its legal form. Representing a legal form that differs from the economic substance of the underlying economic phenomenon could not result in a faithful representation.”

(BC3.26, Part A of NZ Framework)

29

Harmonisation

_____________ Harmonisation_____________ Harmonisation ___________Harmonisation e.g. ___________Harmonisation e.g.

Trans- TasmanTrans- Tasman __________ Harmonisation__________ Harmonisation

And how do these dimensions of harmonisation relate to our theme of the Reporting Entity?

30

Identifying our Themes

As we cover each topic ask yourself As we cover each topic ask yourself which of our themes is relevant to which of our themes is relevant to the topic and which theme(s) is/are the topic and which theme(s) is/are illuminated through the topicilluminated through the topic

Note when we highlight the themesNote when we highlight the themes Build your knowledge of these key

ideas in accounting that will give you a base from which to build future knowledge