Embed Size (px)

DESCRIPTION

The Global Economic Shapshot - Macroeconomic Overview | Beginners Guide - The Different Stock Indices | India - A Growth Miracle? | Focus - The Beer Industry | Human Capital Bourse - People’s Free

Citation preview

FIN NCEL BM A G A Z I N E

S E C O N D E D i t i O N m ay 2 0 1 0

ThE GlobAl EcoNoMIc SNApShoTMacroeconomic overview

bEGINNErS GuIdEThe different Stock Indices

INdIA A growth miracle?

ThE bEEr INduSTrYFocuS

huMAN cApITAl bourSEpeople’s Free

i | Financelab MaGaZine

Financelab MaGaZine | i i

ThE lEGAcY oF ThE poSTwAr MASTEr IS up For quESTIoN

The Financial crisis will most likely not only lead to new rules in economic governance and policies, but also influence theoretical economics. The Great Depression inspired Keynes to write his influential

“General Theory of employment, interest and Money”, which has heavily impacted economic policies since the Second World War. Keynes’ primary contribution was his explicit focus on securing adequate aggre-gate demand, via encouraging governments to step in during slumps to prevent another Depression by stimulating ailing economies. Hitherto classical liberal economist had held a monopoly position, especially in the Anglo Saxon countries, but Keynes completely rewrote economics as a subject.

But Keynes’ thesis is now up for its greatest test so far. The financial Chernobyl that devastated a wide range of economics has initiated the greatest stimulus program ever seen. Governments have incurred mountains of debt to secure a fragile economy, and at first this seems to be a great success. Keynes has apparently been proved right, and thanks to his legacy the world economy is back on track. But the real threat for Keynes’ theoretical supremacy lurks if massive spending by governments initiates a second recession, as markets simply lose trust in governments’ ability to repay their enormous debts. Many prominent economists have warned that a double dip is not an unlikely scenario, and paradoxically govern-ment debt is among the chief reasons for this concern. We are already seeing tentative signs of investors losing trust in sovereign debt, for instance in Greece, but “safe heavens” such as UK and US treasuries do not look so safe anymore. If the collapse of Lehman could kick off a tidal wave of financial sell offs; how will investors react to a sudden bankruptcy of a major developed country? If such a situation comes about is it not only the world economy that will falter; Keynes’ legacy may crumple as well.

Thomas Christensen, Editor.

EdITorIAl

i i i | Financelab MaGaZine

who MAdE ThIS?EdITor Thomas christensen

TEchNIcAl dIrEcTorAndreas Thelander bertelsen

JourNAlIST TEAMdavid weinbergdaniel SchmidtMartin Frederiksen

coNTrIbuTorSAurelija AugulyteFrederik plough Søgaard

coNTENTThE GlobAl EcoNoMIc SNApShoT 1

bEGINNErS GuIdE 4

INdIA - A GrowTh MIrAclE? 6

FocuS - ThE bEEr INduSTrY 8

SuMMErY oF FINANcElAb MEETING 10

FINANcElAb cAlENdEr 11

huMAN bourSE - FrEdErIk h/S (IN dANISh) 12

MAcroEcoNoMIc ovErvIEw

Financelab MaGaZine | 1

ThE GlobAl EcoNoMIc SNApShoT

By Aurelija Augulyte, Head of Investment Panel

Euro area: bailout or let default?negotiations about the Greek bailout package

have been at the forefront of the economic agenda in the recent months. As some flesh on the spare bones have been added to the rescue plan (45bn eUR agreement), it seemed for a while that bond investors got relieved. Yet as Eurostat revised last year’s budget deficit (from 12.7% to 13.6% of GDP), Moody’s downgraded the country (from A2 to A3) and S&P made its bonds “junk” (BB+). These developments intensified the jitteriness of the mar-kets. As evidence, the euro dropped to new lows against the US, Greek bond yields surged to record levels over German bunds ever since the euro was introduced in 1999, and Greek stocks plummeted.

Other indebted euro-area countries, primarily PIGS, suffer from spillover effects, as evidenced by recent developments in bond yields, stock markets, and are also being punished by rating agencies (downgrades of Portugal and Spain). Judging from the markets (credit spreads), if Greece defaults, the next shoe to drop would be Portugal, which has the next-largest debt burden. Of course, its predicament is not as bad as Greece’s, but history shows (remember Asian crisis?) investors do not necessarily think “facts” as panic takes over.

now that Greece asked to activate the bailout pack-

age April 23rd, the support money is expected to reach the country before long. Given a huge amount (8.5bn euro) of Greek bonds maturing May 19th, the money is direly needed before.

Germany has not been very optimistic about saving Greece with German taxpayers’ money. “Why do we have to pay for Greece’s luxury pensions?” asked Bild Zeitung, Germany’s largest tabloid newspaper on its front page on April 28th. According to sur-veys, more than 50% of Germans do not want to help Greece.Support, if it comes, will not be free lunch. Accord-ing to German Chancellor A. Merkel, “Greece must do its homework first.” Likewise, German Finance

Minister W. Schaeuble warned recently that the tough restructuring of the economy is “unavoidable and an absolute prerequisite” to get aid approved by the EU. Now the question remains how tough these measures will be. Given the Greek promise to reduce budget deficit to 8.7% this year, clearly, the process will be far from pleasant for the overall economy.

Unfortunately, the bailout money won’t solve the underlying structural problems. It is simply an exer-cise of throwing good money after bad, covering old debt with new debt. Clearly, even the initial prom-ised 45bn euro will not save Greece. According to IMF, Greece might need up to 120bn euro. Some

NordEA ANAlYTIcS NordEA ANAlYTIcS

2 | FINANCELAB MAGAZINE

economists even expect this figure to reach even up to 600bn euro, which would be nearly economic madness to implement.

Maybe Germany’s unwillingness to support Greece is not without reason, after all. Yes, there will be immediate spillover effects to other PIGS countries, and some will have to leave the euro zone. And yes, many banks, including Western Europe’s, will have to suffer yet another wave of write-downs on PIGS countries’ bonds. But if Greece default is inevitable, which seems quite likely, prolonging it with a painful depression and increasing debt burden will ultimately cost more – both for Greece and the rest of euro zone, both in financial terms and in terms of reputa-tion of the European monetary union.

uS: slowly, but (so far) surelyThere have been quite a few positive US macroeco-nomic news releases in the past few weeks. The existing home sales grew at a solid 16.1% y/y in March, while the new home sales rose at the fastest pace in nearly 50 years. The durable goods orders (excl. transport) increased by 13.5% y/y, which was the fourth strong gain in the past months and the fastest pace since 2007. March retail sales came beating the expectations at 7.6% y/y, followed but previous two months’ upward revisions. The Confer-ence Board’s Consumer Confidence Index increased to pre-Lehman levels, and the Index of Leading Eco-nomic indicators revived, giving a hope of positive macro developments going forward.

While the international Monetary Fund (iMF) iMF revised euro zone’s growth forecast downwards in their recently released World economic Outlook,

the US forecast has been updated upwards: U.S. economy is expected to grow 2.3% this and 2.4% next year.

US Federal Reserve Bank (FED) governors also sounded mildly more optimistic in their meeting on April 28th. Their statement noted that the labor market is “beginning to improve” (vs. “stabilizing” in March), as well as “household spending has picked up recently” (vs. “expanding at a moderate rate” in March), and that the housing starts “edged up” (vs. “have been flat at depressed levels” in March).

One of the worrying macro news from the US lately, however, has been sentiment of small and medium sized businesses: The national Federation of inde-pendent Business’s optimism index dropped to 86.8 in March from 88 in February, hitting lowest level since summer last year. This is a disappointing de-velopment, since small businesses have historically been the backbone of US job creation, accounting for approximately 80% of all new jobs. The crisis hit them hardest as their main source of finance, banks, tightened their credit policies. Unemployment

NordEA ANAlYTIcS

FINANCELAB MAGAZINE | 3

remains the key concern in the US, and it is likely to persist for quite some time. As FED chairman B. Bernanke warned in his testimony in April, even though the risk of a double-dip recession is “cer-tainly less than it was a few months ago”, there is a “possibility” of the US unemployment rate remaining “stubbornly” high, at “around 10%”.

Having seen some signs of improvement in the US economy recently, many now fear that the recovery might lose steam as B. Obama’s stimulus package effects evaporate. Yes, it is clearly a concern, and we might see some less positive changes in the macro data in the near term, which might cause some risk aversion turning back to the stock markets. How-ever, it is highly likely to me that the worst in this economic cycle is already behind, and the recovery will continue –slowly, but surely. Yes, one should admit that the US economy faces many challenges ahead in terms of its fiscal bal-ances, health care, etc. But, again, when you invest or trade in the markets, all that matters - matters in relative terms. And those who forecast “doom and gloom” for the US, just look at the global markets: whenever bad news strikes, it is the US government bonds that everyone flights to as “safe Heaven”, and it is the US currency that strengthens, showing no sign of loss in confidence yet.

china: bubble growing, but revaluation delayed?another month and another bunch of “positive” surprises in the Chinese macroeconomic data: GDP figure released at 11.9% - higher than expected, in-dustrial production and investments came at 18.1% y/y and 26.4% y/y, respectively.

The property prices moved further into bubble-like territory with overall house prices increasing 11.7% y/y in March. Rumors are running that the situa-tion has reached the point where even taxi drivers boast being owners of several flats for speculative reasons, and that many newly built shopping malls and offices lie idle.The chinese government continues the uphill battle of trying to cool the credit markets – for example, it has recently increased the down payment ratios for some home purchases, promising that some “more forceful” steps might follow in an attempt to curb down speculation. It is very possible that China will introduce higher, maybe even U.S.-style, property taxes at some point in an attempt to clamp down the booming real estate market.

Another policy change largely expected from the Chinese officials is a revaluation of the yuan. While the US has been relatively quiet lately, and has postponed legally calling china “a currency manipu-lator” pressure is felt from other countries such as developing powers like India and Brazil. L. H. Loong, Singapore’s prime minister, expressed his country’s voice recently, claiming that it was “in China’s own interests” to get a more flexible exchange rate now that the crisis is over.

While the crisis in china seems over at least from a statistical point of view, growth has been to a large extent artificial in a sense that it was mainly sup-ported by government stimulus package. In addition to this, now the Europe’s troubles put pressure on external demand. Europe is indeed an important Chi-nese trade partner: the EU accounted for $21.45bn - the largest share of China’s $112.11bn of exports in March, outpacing even shipments to the US ($19.33 bn).

Export growth is very important for China’s mainly export-driven economy. Chinese officials have very well expressed themselves saying that before any signs of sustained global recovery they will not change their currency policy. Moreover, evidence of a “very certain” recovery, according to China’s central bank Governor Z. Xiaochuan, is needed be-fore rolling back any stimulus measures, including keeping the yuan from strengthening. Clearly, the Greek tragedy paralyzing the euro area’s growth prospects is not the sign of global recovery china is aiming for, and these developments give at least a political argument against letting the yuan stronger in the international forum.

One way or another, china has been and still re-mains a quite big risk factor going forward. Since global growth is so much dependent on emerging countries now, any further other sign of overheat-ing in china or an attempt to tighten might result in another bout of risk aversion and sell-off in global equity markets.

4 | Financelab MaGaZine

bEGINNErS GuIdElESSoN Two

by David C. Weinberg, FinanceLab Journalist Team

ThE dIFFErENT STock INdIcES

when thinking about stock exchanges and trading, most people will associate these

terms with the dow Jones, Nikkei and dAX. In order to have a proper understanding of why they exist, what they actually measure and who is present in these indices will be the topic of this month’s beginner’s guide. First, the Ameri-can indices (dow Jones, the NASdAq and the S&p500) are explained, followed by the Asian (NIkkEI 225), the European (Euro SToXX 50, dAX).

American Indices:dow JoNESThe Dow Jones (its original name is Dow Jones industrial average) is probably the most important American Index which is comprised of the 30 big-gest and most important companies like Walt Dis-ney, IBM, GM and GE. It is based in New York and acts as a role model for all other equity indices in the world. If it decreases significantly, it is very likely that the Asian and European indices go down as well. The Dow Jones can be traced back to the publisher of the same name, who also owns the Wall Street Journal. The all time high was reached at the peak of the dot.com bubble in 2000 with 11.900 points. Interestingly, in 1994 it surpassed the 4.000 points. The index is calculated by dividing the sum of the companies’ shares and divided by a so called Dow divisor (a more difficult calculation which shall not be part of this article).

NASdAqThe NASDAQ (National Association Of Securities dealers Automated quotation) is a pure american

computer based stock exchange. It was founded in 1971 and the first electronic stock exchange. The trading includes mostly companies focused on high-tech and internet development. Since it consists of the typical tech equities, they react stronger to market changes, and account for very sharp in-creases in boom times, but also for plummets when it comes to a weaker economic conditions. When the deviation from standard values is significant, and has a large magnitude we speak of a high volatility. The degree of volatility, thus, determines the risk associated with a share. Investors demand higher risk premiums.

S&p 500The Standard & Poor’s 500 consists of the 500 larg-est enterprises in the US. It shows the development of the broad US-economy and provides a more in-depth view than the Dow Jones. Many firms rebuild the S&P 500 in order to reflect the economic per-formance. This index is perceived to be more mod-ern than the Dow Jones. Closely connected to the S&P 500 is the S&P Futures which is nearly traded around the clock and provides info about the very short-term development of the US-economy

Asian Indices:NIkkEIThe NIKKEi is a Tokio based index which embraces 225 chosen companies. The method used to calcu-late it is the same as for the Dow Jones.

European Indices:Euro SToXX 50The Euro Stoxx is the European equivalent of the Dow Jones. The 50 biggest European companies are listed. It may become more relevant in the near

Financelab MaGaZine | 5

future. The companies listed are usually traditional enterprises like Daimler, BASF, but also more mod-ern and more technological oriented companies like Nokia or Philips.

dAXThe Dax is the most important German index. As the largest economy in Europe this index serves as a guideline for the european economy and its per-formance. The 30 biggest companies are part of this index. There are also other subunits of the Dax, e.g. the MDax and the SDax which comprise smaller firms. However, when speaking of the DAX, the main index is addressed. It was founded in 1988 and had a value of 1000. For being listed in the Dax, a com-pany has to have a prime standard, which means that the share has to be dispersed to at least 10%, and have to be continuously traded at the xetra (the electronic system of the German stock exchange in Frankfurt). An important event which happened in October 2008, was the skyrocketing shares of Volkswagen. Porsche secured options to purchase app. 75% of the whole company. This led to a price 8 times as high as three days before and made VW to the most expensive enterprise in the world, even ahead of Exxon Mobile. The Dax was influenced and gained 700 points. Without VW it would have made a loss of 350.

what for?As we have seen, indices reflect the development of a whole market. With a change of only one number, one can track the economy in its entirety. There are a lot more indices than those presented below. The Economist, Dow Jones and different investment banks created indices evaluating raw materials and durable goods like cars. They provide also the basis for index certificates, options and futures. The latter are for a beginner too risky to start with since win and

lose situations are decided within a narrow spread. However, if one buys an index certificate one buys the whole market and can track it easily and without much effort. Indices are also important benchmarks for hedge fund manager and private investors. If one performed better than the Dow Jones for instance, one can be proud of having “outperformed” the Dow Jones and that definitely result in joy (and bonuses) for the trader in question.

6 | FINANCELAB MAGAZINE

A GrowTh MIrAclE?

nehru and the Gandhis, who thought that economic growth, and societal justice was to be obtained via democratic socialism. Unfortunately it instead led to poverty and disillusion as the government created a leviathan state populated by a huge bureaucracy titled the “Licence Raj”. This public intrusion into the private sector is still among the greatest barriers to growth in India, as it is characterized by flourishing corruption, but things are starting to look better for the Indian economy. Current Prime Minister and then finance minister Manmohan Singh initiated in 1991 a liberalisation process to free the entrepreneurial class from the “Licence Raj”

Growth Possibilities and Investment Opportunities The greatest opportunity for growth in india emanates from the IT and communication sector. A myriad of small enterprises exist with nothing

more than a computer and a dream, but some of these small v e n t u r e s

have grown into big

enterprises, among them info-sys, which is now

among the world IT leaders. This has already attracted a herd of venture

funds, which are identifying small indian companies, and invest

with both capital and managerial skills in order to see these firms develop new

success stories. Accel, a major venture fund located in Silicon Valley, did for instance in 2008 add India to its global portfolio. Following funds such as icici Ventures and even Google Venture fund. One of the greatest barriers to successful and sustainable growth in india is to link the blos-

by Thomas christensen, Editor

INdIA

After the rise of china the world now has its eyes fixed on the other populous nation in

Asia - India. If India can copy the success story of china a whole new range of opportunities arise not just for the impoverished Indians, but also for global businesses and investors. despite their similarities such as size and loca-tion in Asia, India and china are indeed more different than alike. This makes on wonder: is it even likely that a heterogeneous, democratic state can duplicate the growth of authoritarian, homogenous china?

India’s trajectory towards growth has skipped the stage of industrialization and leaped directly into the knowledge economy, but this means that an elite of indian entrepreneurs are taking part in the global economy while the majority of the people are still living distant live in agrarian areas, secluded from the world economy. This is unsustain-able in every society, especially a democratic one.

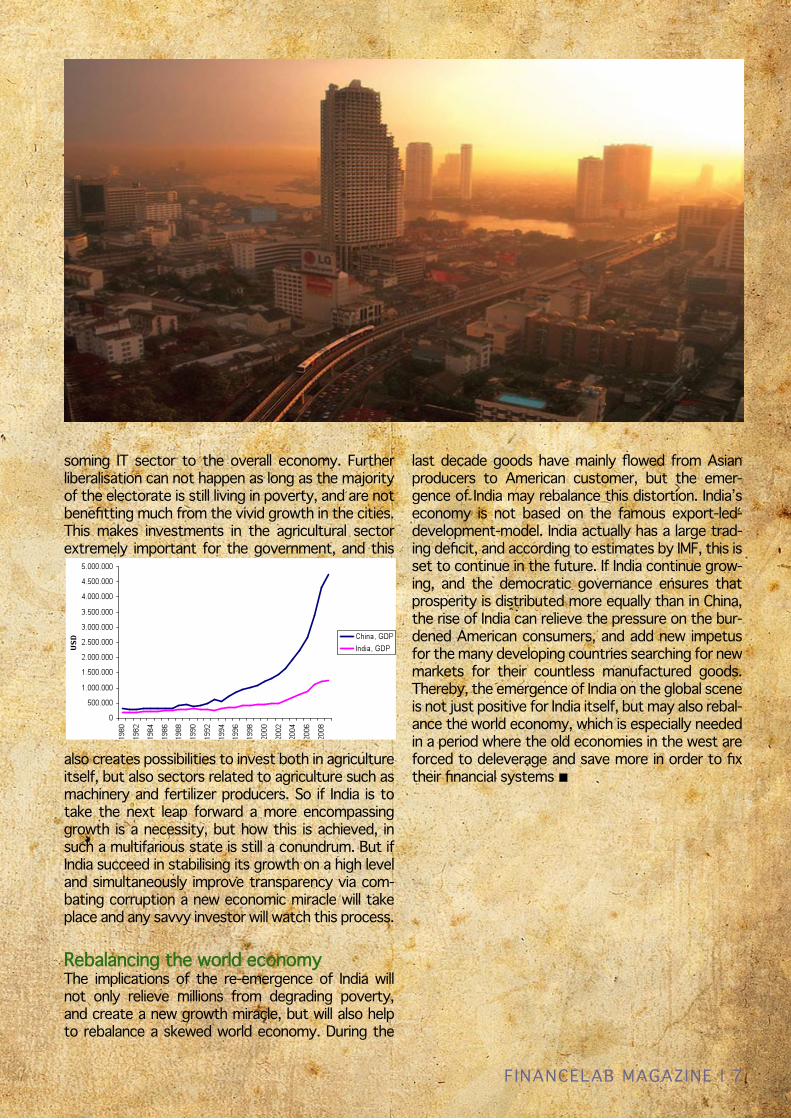

India’s contextafter india won independence from the British in 1947 most Indi-ans thought that a new golden era was to begin, and that india could retake its position as one of the largest economies in the world. India did, before the industrial revolution, constitute around 20 percent of global GPD. The period after independence was dominated by charismatic leaders such as

FINANCELAB MAGAZINE | 7

soming IT sector to the overall economy. Further liberalisation can not happen as long as the majority of the electorate is still living in poverty, and are not benefitting much from the vivid growth in the cities. This makes investments in the agricultural sector extremely important for the government, and this

also creates possibilities to invest both in agriculture itself, but also sectors related to agriculture such as machinery and fertilizer producers. So if India is to take the next leap forward a more encompassing growth is a necessity, but how this is achieved, in such a multifarious state is still a conundrum. But if india succeed in stabilising its growth on a high level and simultaneously improve transparency via com-bating corruption a new economic miracle will take place and any savvy investor will watch this process.

rebalancing the world economyThe implications of the re-emergence of india will not only relieve millions from degrading poverty, and create a new growth miracle, but will also help to rebalance a skewed world economy. During the

last decade goods have mainly flowed from Asian producers to american customer, but the emer-gence of India may rebalance this distortion. India’s economy is not based on the famous export-led-development-model. India actually has a large trad-ing deficit, and according to estimates by IMF, this is set to continue in the future. If India continue grow-ing, and the democratic governance ensures that prosperity is distributed more equally than in China, the rise of india can relieve the pressure on the bur-dened american consumers, and add new impetus for the many developing countries searching for new markets for their countless manufactured goods. Thereby, the emergence of india on the global scene is not just positive for India itself, but may also rebal-ance the world economy, which is especially needed in a period where the old economies in the west are forced to deleverage and save more in order to fix their financial systems.

8 | Financelab MaGaZine

ThE bEEr INduSTrY

by Martin Frederiksen, Journalist Team

FocuS INduSTrY oF ThE MoNTh

The beer industry is at the moment an interest-ing topic, especially in Denmark as Carlsberg is

one of the largest Danish companies. Many excit-ing opportunities and challenges are rising in Asia. At the same time, the Danish beer company has to deal with strikes from the Danish store workers. The employees do not think one beer a workday is enough and they fight for their right to three beers a workday. One may believe it is a joke, but it is not, and that is why the beer industry is an industry, you have to love: large multinational corporations and (apparently...) plenty of beers.

The most important thing about the beer industry is even not mentioned yet: The connection to foot-ball. A lot of breweries try to brand themselves as a ‘football-brand’, in order to improve their recognisa-bility. Carlsberg has long been almost synonymous with the English football club Liverpool. Newcastle United has a long-standing relationship with Scottish & Newcastle, while Heineken is identified with Cham-pions League. Finally, the English Mickey Mouse-cup, carling cup, is obviously currently sponsored by Carling. The breweries’ connection to football super-stars can end up as an important part of the entry into the Asian markets.

Isn’t one beer enough?It all began on the 7th of April. The Danish store work-ers in Fredericia and Høje Tåstrup started their strike as a consequence of a new alcohol policy, Carlsberg introduced.- It is correct that we are hit by a strike. We have made the new alcohol policy, because we noticed that only seven percent of other companies allow employees to drink alcohol during work time. That is why we have introduced our new alcohol policy, which means that our employees are only allowed to consume one beer in the canteen during lunchtime, Jens Bekke, communications director of Carlsberg, explained on the 7th of April to the Danish Newspa-per Berlingske Business. The Danish store workers fought for their right to drink three beers a day,

and it all went to a ridiculous point, where drivers and production employees in sympathy started to strike with the store workers. The delivery of beer was delayed all over Sealand, and people thirsting for carlsberg beer were forced to switch to other brands for a weekend. It could have turned out as a profound tragedy, but as the store workers went back to work on the 12th of April.

Asia – a huge market with great oppor-tunitiesEven though the strike in Denmark is an interesting topic, it is by far distanced by the current activities in Asia. As the beer market in Europe is already ma-tured, it is extremely difficult for the large breweries to earn more or gain larger market shares in the old markets. Instead of fighting for small market shares in Europe, Carlsberg, InBev, SABMilller, Heineken and the other breweries have changed their focus to the huge unexploited Asian market, which is predicted to be the most important market in the future. The rising potential of the asian markets was also reflected in Carlsberg’s report for fourth quarter of 2009.

- The Asian markets were less affected of the fi-nancial crisis, and the sale of beer continued to rise throughout the year. As the Asian market continues its growth, the region will become even more impor-tant for carlsberg in the future, carlsberg wrote in its report. The sale of beer in the Asian market was in fourth quarter of 2009 4.6 million hectolitre com-pared to only 2.7 million in fourth quarter of 2008.

Those Asian guys do not drink beer…One of the greatest challenges in asia for carls-berg and its competitors is the Asians’ abstention from drinking beer. The Indian market is on paper one of the largest markets for the breweries, but the Indians do almost not drink beer. On average, Indians only consume 1.3 litres of beer pr. year – Danes older than 14 years consume on average

Financelab MaGaZine | 9

11.7 litres of beer pr. year!

However that is not the only problem for carlsberg in India. SABMiller and a partnership between Unit-ed Breweries and Heineken dominate the indian mar-ket, and together they count for about 85 percent of the market, which leaves a maximum of 15 percent of the market to Carlsberg.

- In medium term I expect the market share of the two big ones to fall to 70 per-cent. It leaves 30 percent of the market, which we have to fight for. In the long term the big ones’ market share will fall further. Our target is to capture 15 percent of the market of mild beer and 10 percent of the strong beer market, Pradeep Gidwani, chief ex-ecutive of carlsberg india, recently said to Jyllands-Posten. Pradeep Gidwani is optimistic despite the small consumption of beer in India. As he ex-presses himself: - it can almost only develop in one direction. From one populated country to anotheranother very populated country in asia is china, and the chinese market is – similar to india – also a very attractive market for the brewery giants. It is estimated that Carlsberg has about 20 billion Danish kroner for acquisitions in Asia, and the brewery is therefore looking for possible acquisitions. Jørgen Buhl Rasmussen, chief executive of Carlsberg, con-firms.-We have regained our flexibility and we now got bigger financial strength, so if we see discovers something very interesting, there are really no limits, he says to dagbladet Børsen, before he continues:- compared to a year ago, we are in a fantastic situation, and we have bunch of options. We do not need to fight for extra time before buying another company. An acquisition can now be decided by as-sessing the attractiveness of the company, and af-

ter a consideration regarding timing, Jørgen Buhl Rasmus-sen says. According to the Danish newspaper Børsen, carlsberg has been working on increasing its share of own-ership in the chinese brewery Chongging Brewery. Another opportunity for carlsberg is to buy Yanjing, which stock exchange value is estimated to be approximately DKK 20 billion. Jørgen Buhl Rasmussen refused to comment on the rumours concerning chongging or Yanjing, but he said that carlsberg operates with a list of possible targets in the asian market.

breakthrough in AsiaOne of the most important parts of Carlsberg’s way to success in asia is the spon-sorship of football and in particular the english football club Liverpool FC. Many of the players in liverpool Fc are extremely popular in Asia, and Keld Strudahl, head of marketing of carlsberg, knows how unfortunate it was for the Danish Brewery to lose their main sponsorship of

the club. However, he does not consider the loss of the main sponsor-

ship as devastating.

- now when we are not longer paying for being on the shirt, we can spend more money on other parts of the sponsorship of Liverpool, if we want to. Cur-rently we do not consider it as necessary, as we are close to a new deal with the club, Keld Strudahl told Børsen on the 19th of April.Keld Strudahl and Carlsberg is extremely interested in a new deal with ‘The Reds’, as many of the clubs players are extremely popular in Asia, and can there-fore be used in Carlsberg’s marketing. Fernando Tor-res, Steven Gerrard and Daniel Agger are all held in high esteem by the asian supporters.

10 | Financelab MaGaZine

Summary of investment panel meeting, April 28 2010. by daniel Schmidt.

FINANcElAb INvESTMENT pANElFOLLOW THE MONEY

april 28 2010 was the date that FinanceLab In-vestment Panel started investing the funds that

are present in Denmark’s first student run invest-ment fund.

“We have been working hard and done a lot of ef-fort in making this work. Now it is reality”, Aurelija Augulyte, Head of FinanceLab Investment Panel expressed.

it was a very committed panel of students from cbS and University of copenhagen, who discussed the issues of the agenda. The panel members are all at different stages of their relative studies, but the atmosphere at the meeting was marked by a great sense of energy and knowledge sharing.The meeting was as usual initiated with a thorough overview of the hottest topics from the macro-world by Aurelija. Of course, the focus was on the debt problems in Southern europe, which may seem overwhelming, but perhaps is more aimed at the economies themselves instead of the financial mar-kets. “I don’t think that we have to be that afraid of Southern Europe. It seems like the markets don’t care anymore. Today the rating of Spain was down-graded – the markets fall, but after an hour, they were back again”, explained Marc Rasmussen, Port-folio Manager and the most experienced trader of FinanceLab Investment Panel. Furthermore, Aurelija was convinced that a Greek default is not a realistic scenario.

Take advantage of energy correlations“Oil and gas are correlated, but recent development in market prices shows a spread between the two. as a trader it is possible to take advantage of such developments, by setting up a hedged position on energy”, Aurelija explained to the panel. In this par-ticular case, the idea is to short oil and buy gas. In

that way it is possible to earn money, independent of price development, supply, and demand, as long as the spread will narrow down. Unfortunately, Fi-nanceLab Investment Panel does not have the soft-ware yet to make a hedged position on energy, and therefore, the brilliant idea was not up for voting.

Financelab likes the beersNext presentation was from the Consumer Staples and Discretionary group, who suggested investing in the Danish brewery stock Carlsberg. Carlsberg have recently been very successful in reducing their debt, and it seems like they are well structured for future challenges. Carlsberg seemed like a good invest-ment from both a technical and a fundamental point of view.

as a surprise the industry Group had a nice contribu-tion to the talk on beers: They had researched Royal Unibrew in lack of good investment opportunities within the industrial sector. The company previously had some issues and worrisome troubles, but now they seem well structured.

“looking at development in stock prices among breweries during the last couple of years, there is still much more upside potential in Unibrew, which perhaps seems to be catching up now”, Alex from industry Group told

after a long discussion on beers, growth strategies, taste of ciders, and marketing strategies of the two companies, it was time to move on to another pre-sentation, again by the Consumer group. This time the group presented and suggested ic companys, who is in the phase of a turn-around, and who has a stock on the way to the skies. The Investment Panel was uncertain that the progress could keep on, and there was an intense discussion in whether the investment would be too risky on the 2-3 month basis.

Financelab MaGaZine | 11

The last presentation and suggestion was from the energy Group who presented Vestas and the latest news about their giant order and their interim rap-port as well. The case should be seen as a long-term investment, and the energy Group convinced the panel that Vestas was just about to be even more successful.

consensusbefore the voting, the panel discussed some basic portfolio strategies, and it was agreed upon that only two stocks should be bought this month, and it should not be two brewery stocks.everyone voted for two suggestions, and it turned out that the majority saw the biggest potential in Vestas and Carlsberg. Amounts and exit strategies were discussed, and it was agreed to use 20 per-

cent of the portfolio on each of the stocks. This may sound very risky, but so far, the pool of funds is still small, and therefore, risk is a necessity.

“This was by far the best meeting until now”, was the last comment of one of the satisfied panel members.

all the presentations from the meeting can be found at FinanceLab.dk

One of the most interesting aspects regarding last meeting is that it might be the last in the current premises. After the summer break a brand new facility may be available to the members for Fi-nancelab.

FINANcElAb cAlENdErALL EVENTS CAN BE FOUND INCLUDING MORE INFORMATION ON OUR FACEBOOK GROUP AND ON OUR HOMEPAGE.

May 10 – May 12: Trading diplomaA documented step into your financial career!Through partnership with GcMS (Global capital Market Solutions), Financelab is offering the only trading diploma course in Denmark. You will attain diploma-certification in Trading Tactics, Forex Trading, Equity Derivatives, Technical Analysis and much more. Teachers with 9 years of HR- and trader-experience will be coaching you through the trading platform (Saxotrader) and different trading decisions.Sign up at FinanceLab.dk

May 14, 16.00-18.00: General Assembly in FinancelabFinanceLab will constitute the organization, agree to the statutes & member declaration, vote for board members. Everyone can attend at the general assembly, so you are welcome to bring your friends. all active members can, and indeed must, vote at the assembly. Active being defined as everyone having a financelab.dk email-account.

May 17, 18.15-20.00: Meeting at university of copenhagenAn ordinary meeting at KU with knowledge sharing as its primary purpose. Everybody is welcome. Registration: [email protected]

May 25: deadline for contributing to Financelab MagazineDo you want to write an article in the next issue of FinanceLab Magazine?Send your contribution to [email protected]

May 31, 18.00-20.00: ordinary meeting in Investment panelIf you wish to have a look or make a special visit, please contact: [email protected]

12 | FINANCELAB MAGAZINE

FrEdErIk h/S

læs tankeeksperimentet om Financelabs formand, da han som det første menneske

i verden lod sig børsnotere på københavns humankapitalbørs, people’sFree.

Da Frederik blev født havde han tre primære finansieringskilder; familien, banken og staten. alle med hvert sit incitament til at investere penge i den viden, Frederik senere skal bruge for at kunne stå på egne ben. Frederik er en ganske almindelig gennemsnitsdansker og ifølge Danmarks finansbudget for 2010 har staten allerede finansieret Frederiks og øvrige familier i Danmark med godt 32 mia. kr. Det drejer sig om barselsdagpenge, børnetilskud, børnefamilieydelse, elevstøtte/skoleydelse og 10 år i folkeskolen. Det er et krav. Men herefter er det op til Frederiks frie valg om han vil være skatteyder eller tage imod de 17,6 mia. kr., staten har investeret i, at Frederik og hans skolekammerater får en ungdomsuddannelse. Frederik ser ingen logisk grund til at afvise tilbuddet, når det er gratis.

Omkring 18-års alderen gør Frederik for første gang brug af sin tredje finansieringskilde; banken. Kreditkortet bliver hurtigt en vane, mens støtten fra familien bliver reduceret. Staten giver igen Frederik et tilbud og denne gang har staten fordoblet indsatsen. For 36 mia. kr. er Frederik og hans klassekammerater sikret uddannelsesstøtte og en gratis plads på et af Danmarks konkurrencedygtige universiteter. Frederik ser ingen logisk grund til at afvise tilbuddet, når det er gratis.

Antages de nuværende satser at gælde

bagudrettet, har Frederik i gennemsnit modtaget ca. 30.000 kr. om året fra han var 0 til 15. Under ungdomsuddannelsen fik han 107.000 kr. (inkl. familieydelser) de første to år og 127.000 kr. på det tredje år grundet SU-tillæg. Da Frederik er 18 år og netop har afsluttet sin studentereksamen, har staten samlet finansieret Frederiks familie og uddannelse for minimum 1,2 mio. kr. udtrykt i nutidsværdier (korrigeret for inflation mv.)

Frederik har bevidst sin iver og derfor er staten villig til at give ham et endnu bedre tilbud. I udlandet måtte Frederik betale 60-100.000 kr. for en højere videregående uddannelse. På copenhagen business School (cbS) ville den årlige pris være 57.000 kr. pr. studerende, hvis der blev lukket ned for statslige og private tilskud. Tillagt evt. overskud til investorer ville Frederiks CBS-uddannelse koste ham ca. 60.000 kr. om året. Men staten tilbyder igen at finansiere hans uddannelsesønsker.

Yderligere tildeles han SU-støtte som udeboende for 60.000 kr. om året. Den samlede årlige finansiering på universitetet bliver i grove træk 120.000 kr. Så når Frederik er færdig efter 5 år på CBS har staten finansieret 23 års uddannelse og SU-støtte for i alt 2,4 mio. kr. Hvis Frederik tager imod uddannelsen, må det være rimeligt, at han en dag betaler de 2,4 mio. kr. tilbage plus renter.

Men det går op for Frederik, at aftalen med staten ikke er en finansieringsaftale, hvor der kræves renter ligesom hos banken. Staten har ved at satse 2,4 mio. kr. på Frederiks viden og opvækst, ønsket at blive kompenseret med en slags ejerandel i hans viden. Frederik opfattede

by Frederik plough Søgaard, president Financelab.

humankapitalbørs, people’s Free.

FINANCELAB MAGAZINE | 13

oprindelig sig selv som en klient ligesom han er hos banken. Men ifølge statens opfattelse er han økonomisk set et investeringsaktiv, der kan skabe økonomiske fordele, som staten har medejerskab i, så der er hverken tale om finansiering eller støtte men snare en investering fra statens side.

Dette er en vigtig pointe, eftersom der ikke forelægger nogen klar investeringskontrakt mellem Frederik og staten. Aftalen trådte i kraft gennem loven i det øjeblik, Frederik blev født. Eftersom aftalen blev indgået allerede ved Frederiks fødsel, har staten formentlig taget store risici ved at investere i hans fremtid. Staten har haft en grundlæggende tillid til, at Frederik ville blive sund og rask og skabe økonomiske fordele for staten frem for at rejse væk, få dårligt helbred, ende på gaden eller dø. Med den anskuelse har Frederik, foruden de personlige værdier også haft økonomisk værdi. Økonomisk værdi er målbart og Frederik overvejer nu, hvad en højere længerevarende uddannelse i finansiering og regnskab vil betyde for hans værdi hos staten.

Med en cand merc kan Frederik forvente en gennemsnitlig årsløn på hele 500.000 kr. før skat frem til sin pension. antages staten at have ejerskab på gennemsnitligt 50 pct. af Frederiks viden (svarende til den effektive skattesats), vil Frederik indbringe staten 250.000 kr. om året ved at tage imod statens tilbud om ”gratis” uddannelse. Dette er en yderst favorabel aftale for staten. Staten har investeret 2,4 mio. kr. i Frederiks viden. Men at Frederik har kostet staten 2,4 mio. kr., svarer ikke nødvendigvis til, at han er 2,4 mio. kr. værd. Hvis et andet land ville overtage retten over Frederiks viden og livsindtægter, måtte landet betale godt 3,6 mio. kr. Dette beløb svarer netop til nutidsværdien af Frederiks fremtidige indtægtsbidrag til staten. Staten kunne således tjene 1,1 mio. kr. (3,6 - 2,4 mio. kr.) ved at sælge retten over Frederiks viden, og de deraf afledte skatteindtægter på et marked for humankapital.

Frederik har sat sig for at betale af på sin gæld til staten på 1,2 mio. kr. Sammenlignet med et almindeligt banklån med faste ydelser, må Frederik betale ca. 134.000 kr. om året plus renter på 11 pct. af restgælden. Den løsning vil resultere i, at Frederik skal betale halvdelen af sine indtægter på 500.000 kr. til staten, indtil hans 45 års fødselsdag, hvorefter satsen falder moderat.

Yderligere overvejer Frederik at indgå aftale med banken om finansiering af de næste 5 års universitetsuddannelse inkl. kostbidrag. Det vil koste yderligere 690.000 kr. Ved en annuitetsordning må han betale 30 pct. af de årlige indtægter på 500.000 kr., indtil hans 45 års fødselsdag, hvorefter satsen falder moderat.

Omlagde Frederik således sin uddannelses-finansiering fra staten til almindelige banklån, ville han samlet skulle betale 80 pct. af de 500.000 kr. i de næste 20 år af hans liv. Med

statens nuværende skattetryk på 50 pct. tyder det på, at den har

skånet ham for de dyre rentebetalinger og det kan derfor ikke betale sig at lade banken overtage gælden.

Det bekræfter vores forrige hypotese om statens e j e r s k ab s r o l l e . Årsagen til den store forskel mellem skatten og

bankudgifterne må være, at staten i

modsætning til banken har taget ejerskab i Frederiks viden som en slags

kompensation for rentebetalingerne. Dette udgør en væsentlig forskel mellem stat og bank. Frederik har ingen rentebærende gæld til staten ligesom til banken. Derimod har staten retten til at tage en fast andel af Frederiks indtægter, uanset hvad han tjener.

Da Frederik stadig er interesseret i at gøre sig uafhængig af staten, overvejer han nu mulighederne for ændring af ejerskabsforhold i stedet for ændring af låneforhold. Da statens underskud i 2010 er 85 mia. kr., får Frederik nu

14 | Financelab MaGaZine

den idé, at et ejerskabsskifte kunne hjælpe til at nedbringe statsunderskuddet. Hvor staten den ene dag køber viden, bør den også kunne sælge viden den næste dag. Hvis staten kan sælge viden til en højere pris, har den tilmed fået afkast af sin investering. Så længe staten kan skabe viden mere effektivt end andre institutioner, vil der være grundlag for et afkast.

Lad os antage, at Danmark etablerer et humankapital marked, for at udgøre et eksempel for det øvrige EU, der i nogens øjne står på renden til systemisk opbrud. På dette marked håndteres opkrævning af person-dividender frem for person-skatter, hvor opkrævningsrettighederne findes i digital papirform ligesom på aktiemarkedet. Staten navngiver disse værdipapirer Peoples Free Issues (PFI’er) for at sende et positivt signal til omverden. Med denne ordning tilbyder staten, at Frederik frit kan overdrage en andel af statens ejerskab i Frederik til andre investorer. Han kan for første gang nogensinde frit vælge sin ejermand. Dog med visse undtagelser. Frederik skal imidlertid stadigt beskattes af allerede afholdte udannelses- og familieydelser samt sundhedsvæsen, sikkerhed, visse indkomstoverførelser mv.

Via tast-selv-borger udregner Frederik en ny skattesats korrigeret for 5 års uddannelse og stipendier. Hans nye skattesats antages at være 35 pct., mens de sidste 15 pct. kan noteres som PFI’er på Copenhagen People’sFree, der er navnet på humankapitalbørsen i København. Ejeren af Frederiks PFI’er får således 15 pct. af hans månedlige indkomst i al evighed via People’sFree, mens staten får 35 pct. via SKAT.

Frederik har valgt at finansiere uddannelsen Cand. merc. i finansiering og regnskab gennem Copenhagen People’sFree. Efter Frederiks anmodning på tast-selv-borger sælger SKAT de såkaldte finans-PFI’er i Frederik til en værdi af 690.000 kr. på People’sFree. Når staten har solgt i omegnen af 112.000 PFI’er af denne type, vil statsunderskuddet i øvrigt være dækket, hvorfor staten har interesser i at markedsføre People’sFree overfor den private sektor og unge med gymnasiebaggrund. Efter et par måneders forarbejde med prospektformulering og promotion, sælger børsmægleren Frederiks PFI’er videre i mindre dele til private investorer for en samlet værdi af 720.000 kr. PeoplesFree udvikler elektroniske

handelssystemer, hvor Frederik og studerende indenfor samme uddannelseskategori, inddeles i puljer af ca. 100 studerende i hver pulje. Denne løsning er forholdsvis simpel med nutidens IT-teknologi, og snart kan Frederik se en kursgraf, der afspejler den samlede værdi på Frederik og hans medstuderendes PFI’er. Det var primært investeringsselskaber specialiseret inden for HR, der skabte efterspørgsel på PFI-markedet og det går op for mange studerende ligesom for Frederik, at PFI-modellen er attraktiv af følgende årsager:

1) Efterspørgslen på PFI’er presser prisen op og samtidig er der vækstmuligheder i Frederik. Det skaber incitament blandt investorerne til at ændre dividendepoli-tik under de halvårlige generalforsamlin-ger. Der er altså chancer for, at Frederik kan påkræves en lavere dividende-beta-ling og dermed en lavere nettoskat, hvis han børsnoterer sig.

2) Investorerne er profitmaksimerende. Derfor spekulerer og involverer de sig i højere grad i Frederiks karriere, fordi det i sidste ende kommer investorerne selv til gode. Frederiks karrieremuligheder bli-ver af den grund bedre ved notering på People’sFree.

3) Der er kort feedback-proces mellem Fre-deriks performance og reaktionerne på PFI-markedet. Stiger PFI-prisen er det tegn på tillid til Frederiks og hans med-studerendes fremtid.

4) Frederik er i højere grad motiveret til at skabe økonomiske fordele for sig selv. Med højere indkomst kan han nemlig op-købe alle PFI’er i hans eget navn og der-med købe sig selv fri af puljen. Dette er kernefilosofien bag People’sFree.

5) Markedet for PFI’er fordeler sig ud i pul-jer af mange forskellige fagkompeten-cer; håndværk, naturvidenskab, IT, hu-manistiske uddannelser mv. Det giver investorerne mulighed for at sprede sin risiko over en bred portefølje af kompe-tencer med både kort- eller langsigtede vækstudsigter.

6) Ordet vidensamfund har fået ny betyd-ning. Er indisk viden efterspurgt, kan det læses direkte af kursen på indiske PFI’er. People’sFree skaber generel synlighed og bedre målbarhed i værdien af et lands know-how.

7) Karrierevalg er interessedreven, men der er tendens til at unge også bruger infor-

Financelab MaGaZine | 15

mationen fra PFI-markedet til at træffe karrierevalg.

Efter blot 5 år har flere EU-lande kopieret modellen og PFI-markedet er rykket op i billion klassen. Det er gået op for Frederik, at børsnoteringen også havde en række bagsider. People’sFree gav Frederik frihed til at vælge sin ejer, men samtidig har valget sat ham under ekstra hårdt pres fra omverdenen.

1) Karakteroffentliggørelser, enkeltindivi-ders nye initiativer, succeser eller fiasko-er på arbejdsmarkedet er blevet gjort til hovedbegivenheder i den finansielle presse.

2) Der er informationspligt. Frederik skal der-for evaluere sin indsats via People’sFree.dk hvert semester, svarende til en års-rapportering eller årsopgørelse.

3) investorerne taber penge, hvis Frederik ikke yder sit ypperste. Det er svært at definere, hvornår Frederiks tid skaber mest værdi for investorerne. Det der for Frederik opfattes som fritid, opfattes af investorerne som råderum for merværdi.

4) Frederik bør handle i investorernes inter-esser. Det kan skabe interessekonflikter mellem Frederiks personlige behov og in-vestorernes.

5) investorerne valgte under generalfor-samlingen på Frederiks femte uddannel-sesår at hæve dividenden fra 15 til 17 pct. Dette begrænsede bl.a. Frederiks muligheder for at købe sig fri fra PFI-markedet.

6) Der er asymmetrisk information, hvorfor investorerne har ansat analytikere med speciale i psykologi til at overvåge og føre performancemåling på Frederik. Det har ofte skabt anledning til frustration og stress.

7) PFI’er har mere makroøkonomisk føl-somhed. Deres værdi reagerer på arbe-jdsmarkedsforhold, uddannelsespolitik og branchefaktorer. Som udgangspunkt betragtes PFI’er på samfunds- og natur-videnskabelige fag oftest mere sikre og mindre spekulative i forhold til PFI’er på humanistiske fag. En boble i det danske farmaceut PFI-marked, skabte i en år-række mangel på kapital til farmaceut-uddannelserne. Det øgede efterspørgs-len markant på de statsligt finansierede farmaceut-uddannelser. Og da regerin-gen imidlertid ikke havde sat ressourcer

af til at agere sikkerhedsnet, når PFI-markedet svigtede, steg adgangskarak-teren fra 7 til 10,7, hvilket var en re-kordstigning.

Omend modellen i en vis udstrækning blot var en omfordeling af Frederiks frihed, var han godt tilfreds. De samlede ressourcer til uddannelse i Danmark steg markant, fordi PFI’er også fik opbakning fra befolkningen (jf. Dansk PFI Forenings årsberetning, 2012). PFI-markedet blev ligesom boligmarkedet en aktivklasse, hvor danske familier kunne investere langsigtet og sikkert. Vigtigst af alt fik Frederik frihed til at skifte ejer uden at skulle forlade sine danske rødder.