Embed Size (px)

DESCRIPTION

bangladesh finance bill

Citation preview

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Personal Tax Page | 1

01755-621692

Abridged Version

of

Finance Bill- 2014

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Personal Tax Page | 1

01755-621692

Personal Tax

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Personal Tax Page | 1

01755-621692

PERSONAL TAX i

1. Proposed Tax rate for Non-Corporate Tax payers (Individuals & Firms):

PaP Particulars Proposed (FY 2014-15) Existing (FY 2013-14)

Slab Rate Slab Rate

On First Tk. 220,000 Nil 220,000 Nil

On Next Tk. 300,000 10% 300,000 10%

On Next Tk. 400,000 15% 400,000 15%

On Next Tk. 500,000 20% 300,000 20%

On Next Tk. 3,000,000 25% 3,000,000 25%

On Balance TK. Balance 30% Balance 25%

Non-Resident other than Bangladesh non-Residents 30% 25%

2. Proposal of Income threshold for Individual Tax-Payers:

Status Proposed

(FY 2014-15) Existing (FY 2013-14)

Tax exempted income threshold 220,000 220,000

Women and aged taxpayers (65 years of age & above) 275,000 250,000

Physically Challenged 375,000 300,000

War- wounded Gazetted Freedom Fighter 400,000 Not specified

3. Proposal of Minimum Tax for Individual Taxpayers Based on Location:

Status Proposed

(FY 2014-15) Existing

(FY 2013-14)

City Corporation Area 3,000 3,000

Paurashava 2,000 2,000

Other Areas 1,000 1,000

4. Charge of surcharge

Issues Proposed

(FY 2014-15) Existing

(FY 2013-14)

Net Wealth worth of Tk. 20 Million to Tk. 100 Million 10% 10%

Net Wealth worth of Tk. 100 Million to Tk. 200 Million 15% 15%

Net Wealth worth of Tk. 200 Million to Tk. 300 Million 20% 15%

Net Wealth exceeding Tk. 300 Million 30% 15%

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Personal Tax Page | 2

01755-621692

5. Investment allowance

An assesse would get tax rebate of 15% on lower of:

i) Actual investment, ii) 30% of total income or iii) Tk. 15 Million

6. Proposal of Tax on Investment in House/ Flat:

Location of the Property Rate on per

sq. meter

up to 200

Sq. meter

Rate on per

sq. meter

above 200 Sq. meter

Gulshan Model Town, Banani, Baridhara, Motijheel Commercial Area and Dilkusha

Commercial Area of Dhaka.

5,000/- 7,000/-

Dhanmondi Residential Area, Defence Officers Housing Society (DOHS), Mahakhali, Lalmatia Housing Society, Uttara Model Town, Bashundhara Residential Area,

Dhaka Cantonment, Kawran Bazar, Bijaynagar, Segunbagicha, Nikunja of Dhaka

and Panchlaish, Khulshi, Agrabad and Nasirabad Area of Chittagong.

4,000/- 5,000/-

Other areas of City Corporation 2,000/- 3,000/-

Paurasabha of any district headquarters 1,000/- 1,500/-

Other Areas including Upazilla 700/-

1,000/-

More than one house/flat Additional

Additional

20%

7. Proposal of Tax on Investment in House/ Flat:

Particulars Tax Rate

Tax Rate on Total Value 10%

In case of more than one Plot/Land additional tax on payable sum (20% higher

of 10% of Tax)

12%

8. Requirement of Audit for Persons:

If gross receipt or sales is more than 50 million from business or profession, the statement of Accounts

needs to be audited either by a Chartered or a Cost & Management Accountant.

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Corporate Tax Page | 1

01755-621692

Corporate Tax

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Corporate Tax Page | 2

01755-621692

CORPORATE TAX

1. Corporate Tax Rate:

Particulars Proposed (FY 2014-15)

Existing (FY 2013-14)

Publicly Traded Company (other than Bank, Insurance, Mobile Phone Operator, Cigarette Manufacturing Co), no rebate is allowed even dividend is paid more than 20% of capital

27.50% 27.50%

Publicly Traded Company pay dividend less than 10% of capital or fail to pay dividend within the specific time by BSEC

35.00% 37.50%

Non-Publicly Traded Company 35.00% 37.50%

Bank, Insurance and Financial Institution (except Merchant Bank) 42.50% 42.50%

Merchant Bank 37.50% 37.50%

Cigarette Manufacturing Company

Publicly Traded 40% 40%

Non- Publicly Traded 45% 45%

Mobile Phone Operator

Publicly Traded 40% 40%

Non- Publicly Traded 45% 45%

Dividend Income 20% 20%

Minimum Turnover Tax 0.30% 0.50%

2. Tax Holiday, Exemption & Reduction:

Issues Proposed

(FY 2014-15) Existing

(FY 2013-14)

Tax-Holiday for 17 Industrial Undertakings 30 June, 2019 30 June, 2015 Tax-Holiday for 17 Physical Infrastructure

Facilities

15% Tax on Income Derived from production of Jute goods 30 June, 2019 30 June, 2015

15% Tax on Income from Fabric, Dyeing Industry etc

30 June, 2019 30 June, 2015

50% Tax rebate on Export of Handicrafts 30 June, 2019 30 June, 2015

Tax Exemption in Poultry Sector

30 June, 2019 30 June, 2015

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Corporate Tax Page | 3

01755-621692

3. Tax Exemption Period (S - 46B):

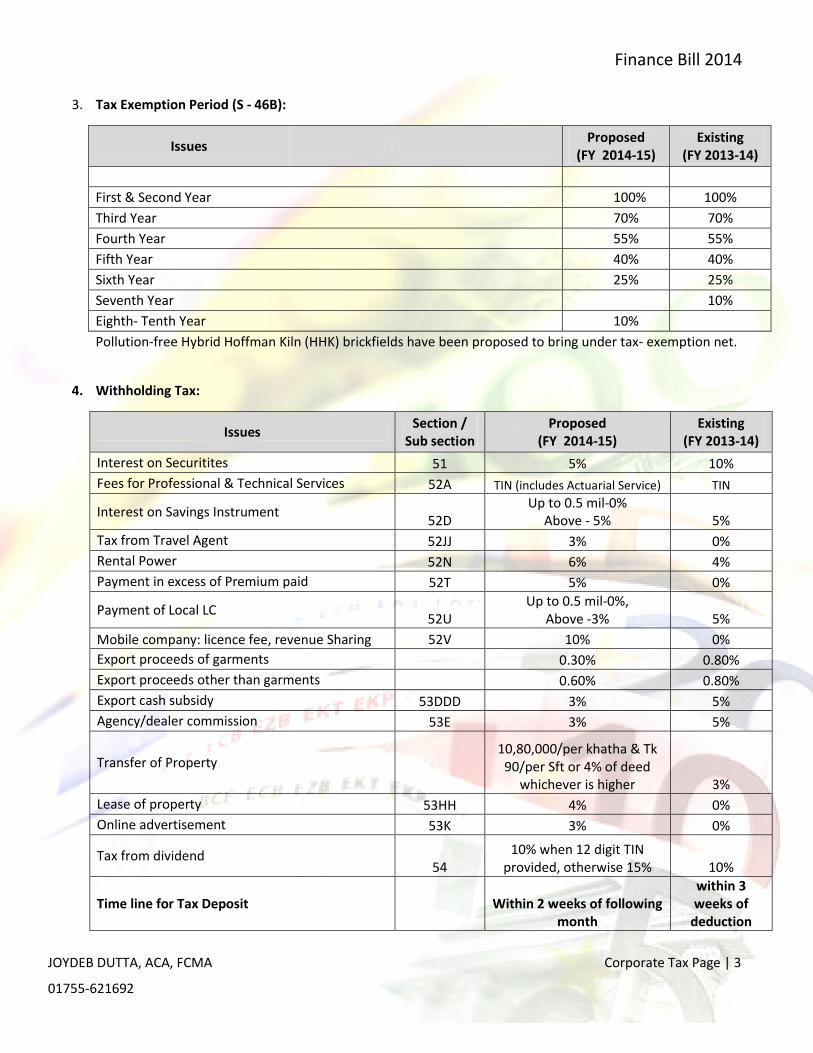

Issues Proposed

(FY 2014-15) Existing

(FY 2013-14)

First & Second Year 100% 100%

Third Year 70% 70%

Fourth Year 55% 55%

Fifth Year 40% 40%

Sixth Year 25% 25%

Seventh Year 10%

Eighth- Tenth Year 10%

Pollution-free Hybrid Hoffman Kiln (HHK) brickfields have been proposed to bring under tax- exemption net.

4. Withholding Tax:

Issues Section /

Sub section Proposed

(FY 2014-15) Existing

(FY 2013-14)

Interest on Securitites 51 5% 10%

Fees for Professional & Technical Services 52A TIN (includes Actuarial Service) TIN

Interest on Savings Instrument 52D

Up to 0.5 mil-0% Above - 5% 5%

Tax from Travel Agent 52JJ 3% 0%

Rental Power 52N 6% 4%

Payment in excess of Premium paid 52T 5% 0%

Payment of Local LC 52U

Up to 0.5 mil-0%, Above -3% 5%

Mobile company: licence fee, revenue Sharing 52V 10% 0%

Export proceeds of garments 0.30% 0.80%

Export proceeds other than garments 0.60% 0.80%

Export cash subsidy 53DDD 3% 5%

Agency/dealer commission 53E 3% 5%

Transfer of Property

10,80,000/per khatha & Tk 90/per Sft or 4% of deed

whichever is higher 3%

Lease of property 53HH 4% 0%

Online advertisement 53K 3% 0%

Tax from dividend 54

10% when 12 digit TIN provided, otherwise 15% 10%

Time line for Tax Deposit

Within 2 weeks of following month

within 3 weeks of

deduction

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Corporate Tax Page | 4

01755-621692

5. Certain Contractors excluded from final discharge of Tax Liability:

A Contractor or sub-Contractor to the contractor of an oil company

Oil Marketing Companies and its dealer or agent excluding petrol Pump station

Any Company engaged in Oil Refinery

Any Company engaged in Gas Transmission

6. Capital Market:

Withholding Tax Section /

Sub section Proposed (FY 2014-15)

Existing (FY 2013-14)

Transfer of share of shareholder of Stock Exchange

53N 15% 0%

Gains of securities traded in the Stock Exchange 53O

Company or firm 10% Others

Gain between 1 to 2 mil - 3% Above 2 mil - 5%

0%

Dividend Income 54 Exempted up to 15,000 Exempted up

to 10,000

Corporate Social Responsibility (CSR):

Propose to extend tax facility on contribution to any fund created and approved by the government to help victims of natural disaster and accidents as CSR.

Propose to raise the expenditure limit from Tk. 8o million to Tk.120 million keeping unchanged the existing condition of allowable limit at 20 percent of total income of any company.

Transfer pricing related Income Tax regulations will be come into force 1 July, 2014.

Capital Assets:

Agricultural land in Bangladesh will also be treated as Capital Assets

Method of Accounting:

For companies, financial statements have to be prepared in accordance with BAS/BFRS and audited by Chartered Accountants.

Inadmissible Deductions (S - 30)

Allowable limit of excess perquisite is increased to Tk 350,000 than earlier of Tk 250,000.

Payment of House rent other than crossed cheque or bank transfer will be disallowed.

Any expenditure exceeding 10% of net profit disclosed in the statement of accounts under head office expenses against profit.

Any expenditure by way of royalty expenses, technical services fee, technical know-how fee or technical assistance fee exceeding 8% of net profit disclosed in the statement of accounts instead of the profit.

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Corporate Tax Page | 5

01755-621692

Any expenditure by way of incentive bonus exceeding 10% of net profit disclosed in the statement of accounts instead of disclosed net profit.

Third Schedule (paragraph 3):

Normal Depreciation Allowance :

Particulars Dep Rate %

Office Equipment 10%

physical infrastructure-

(i) Bridge 2%

(ii) Road 2%

(iii) Fly over 2%

(iv) Pavement runway, taxiway 2.5%

(v) Apron, tarmac 2.5%

(vi) Boarding bridge 10%

(vii) Communication, Navigation aid and other equipments 5%

• Third Schedule (paragraph 7B): Accelerated Depreciation allowance on machinery and plant:

Industrial undertaking established between 1 July 2014 and 30 June 2019:

Particulars Dep Rate %

First Year 50%

Second Year 30%

Third Year 20%

Other Reforms

Payment of monthly house rent amounting more than Tk.25 thousand proposed to be made through banks.

Estimated income of Non Resident Contractor & Sub-contractor extended from 10% to 15%

Income from poultry industry exceeding TK 1,50,000/- an amount minimum 10% required to be invested in purchase of govt. bond & securities within 6 months and hold such bond or securities till maturity of such bond or securities;

Exemption from return submission: return submission has been exempted if assessee has not been able to earn taxable income prior to three consecutive years instead of having

Amount of tax payable on the basis of tax payable shown in return or tax payable under 16ccc whichever is higher.

Section 82BB: Tax return submitted under Universal-self will be exempted from audit if:

Certain conditions are met

20% increase in income is shown on return than last assessed income

Section 128: penalty of 10% is increased to 15%

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Corporate Tax Page | 6

01755-621692

Amortization of License Fees:

License Fees paid before July 01, 2012 included in amortization of License fees. Definition of License fees

now includes Spectrum Assignment fees, GSM License Fees, License acquisition or renewal fees.

Sixth schedule (para 48 to 52): Exclusion from total Income

Income earned in abroad are brought as foreign remittance

Donation by cross cheque to girl’s school or college

Donation to Technical and Vocational Training Institute

Donation on R&D of agriculture

Income up to ten lakh taka realized from transfer of stock or shares of public limited company

Income from agriculture will be exempted up to Tk 200,000

Tax exemption of ITES services is extended up to 2019

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Value Added Tax Page | 1

01755-621692

VALUE ADDED TAX (VAT)

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Value Added Tax Page | 2

01755-621692

VALUE ADDED TAX (VAT)

VAT Rules and Supplementary Duty Rules, 2013 have been drafted to implement VAT Act 2015 w.e.f 1 July 2015

• Online VAT registration will be kicked off from Jan 01, 2015

• Online VAT return Submission will be implemented within 30 June 2015

PROPSAL FOR REFORMS IN VDS RATE

Services Code Proposed

(FY 2014-15) Existing

(FY 2013-14)

Air Conditioned Launch S 036.10 15% 10%

Air Conditioned Bus S 036.20 15% 10%

Air Conditioned Railway S 036.20 15% 10%

Motor Garage & Workshop S 3.10 7.50% 4.50%

Dockyard S 3.20 7.50% 4.50%

Photograph Maker S 019.00 7.50% 4.50%

English Medium School S 069.00 7.50% 4.50%

Immigration Advisor S 067.00 7.50% 4.50% Transport Contractor (except Petroleum product carrying contractor @ 2.25%) services S 048.00 7.50% 4.50%

Land Development S 010.10 3% 1.50%

Jewellery Services S 026.00 3% 2.00%

General Restaurant Service (Not Air Conditioned) S 1.20 7.50% 6.00%

PROPSAL FOR REFORMS IN TRUNCATED RATE

Services Code Proposed

( FY 2014-15) Existing

(FY 2013-14)

Restaurant – Non Ac S 001.20 7.50% 6.00%

Motor garage/workshop S 003.10 7.50% 4.50%

Dockyard S 003.20 7.50% 4.50%

Land Development Org S 010.10 3% 1.50%

Building Construction Org S 010.20 3% 1.50%

Photo producer S 019.00 7.50% 4.50%

Goldsmith etc S 026.00 3% 2.00%

Carrying Contractor S 048.00 7.50% 4.50%

Immigration consultant S 067.00 7.50% 4.50%

English Medium School S 069.00 7.50% 4.50%

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Value Added Tax Page | 3

01755-621692

VAT Withdrawal

Details Code Stage

Kidney Dialysis Solution 3004.90.91 Production

Meditation service S 099.40 Service

Supplier of cow/buffalo bone to Gelatin Capsule S 037.00 Trader

Contraceptive 30.04 Trader

Crushed leather 41.04 to 41.07 Import & Production

VAT Exemption Withdrawal

Details Code Stage

Handmade biscuit and cake Production 19.05 Production

Cellular (mobile/Fixed Wireless) Telephone set 8517.12.10 Import

Ocean going vessel (above 5000 DWT) 89.01 to 89.07 Import & Production

PROPSAL FOR REFORMS IN TARIFF RATE

Details Proposed

(FY 2014-15) Existing

(FY 2013-14)

Rate/ Ton Rate/ Ton

Oils other than soya bean and palm 6,667 0

Scrap/Ship Scrap 2000 1500

HR coil to CR Coil 8250 7500

CR Coil to GP/CI Sheet, HR GP/CI Sheet 10% +

MS Product 10% +

GI Wire 10% +

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Value Added Tax Page | 4

01755-621692

Other Reforms

Issues Proposed (FY 2014-15)

Existing (FY 2013-14)

Maximum Penalty 50% of the evaded Tax Confiscation of

Goods

Environment Protection Surcharge / Green Tax for industries which pollute the Environment

1% on Ad-valorem basis on products manufactured

Health Development Surcharge 1% on imported & domestically produced Tobacco

Price of 25 sticks Non-filter Bidis BDT. 6.14

Price of 20 sticks Non-filter Bidis BDT. 6.94

Supplementary Duty Rate On Jarda And Gul Products 60% 30%

100% export oriented company will not be required to pay Input VAT on (a) procurement provider, (b) Security service, (c) Carrying contractor and (d) Import of service from outside Bangladesh

All VAT registered will be required to submit monthly VAT return. Quarterly return has been withdrawn.

ATV is not required to be paid on (a) passenger airline and its spares, (b) cargo plane, (c) certain cancer products and (d) equipment sand spares declared to the BOI.

S 007.00 (Advertising Entity) and S 014.00 (Indenting entity) have been excluded from deduction of

VAT at source

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Custom Duty Page | 1

01755-621692

Custom Duty

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Custom Duty Page | 2

01755-621692

CUSTOM DUTY

Pharmaceuticals

• Existing Duty @ 10 and 25% on 40 fundamental raw materials have been reduced to 5%

• Other duty structure will remain same

• Existing Duty @ 10 and 25% on 41 fundamental raw materials of Ayurveda medicine have been reduced to 5%

Poultry and Livestock

Duty on poultry and livestock against input and raw material has been withdrawn

Paper, Ceramic, Furniture, Plastic, Baby diaper, Electrical and other local industries

Duty @ 10% and 25% has been reduced to 5% to 10%

• Duty on import of railway Machinery and equipment has been reduced from 10% to 5%

• 5% RD will be imposed for importation of 15-16 inches bus tyre

• CD will be increased from 10 to 25% for import of by-cycle tube

• Tariff Value of crude petroleum will be increased to USD 40 from USD 32 • CD @ 5% will be payable for importation of navigation light, Broadcasting equipment and firefighting equipment

• No duty on import of dump truck

• No duty for importation of raw material for Prefabricated building, fire resistant door, emergency light, sprinkler system for RMG

• Duty on certain raw material used for RMG reduced

• Duty structure on import of vehicle has been reclassified

• 100 gm gold can be imported Duty free

• Increase of duty on iron products and withdraw duty on importation of raw materials for billet, sponge iron and reduced iron

• Change of CD from 25% to 5% on multiplexer, grand master clock for faster internet connectivity

• 15% CD on import of mobile set

• 25% CD on import of LPG Cylinder

• 25% CD on import of Energy Saving Lamp, Electric Fan Motor

• Reduction of CD from 25% to 10% for raw materials to produce diaper

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Supplementary Duty Page | 1

01755-621692

Supplementary Duty & Travel Tax

Finance Bill 2014

JOYDEB DUTTA, ACA, FCMA Supplementary Duty Page | 2

01755-621692

SUPPLEMENTARY DUTY

A telecom company will be required to pay SD of Tk 100 per SIM card during replacement

15% SD on locally produced Electric Filament Bulb has been withdrawn.

Significant Reforms have been proposed in the SD structure.

TRAVEL TAX

Details Proposed

(FY 2014-15) Existing

(FY 2013-14)

By Air North America, Europe, Africa, Australia, New Zealand or Far East 4000 3000

SAARC 1200 1000

Any Other Countries 3000 2500

By Land 500 300

By Sea 800 500

![Finance 1 FINANCE BILL 2015 - Customsgst.customs.gov.my/en/rg/SiteAssets/gst_bill/FINANCE BILL 201528BI29.pdf · Tax Act 2014 and the Promotion of Investments Act 1986. [ ] ENACTED](https://img.dokumen.tips/doc/110x75/5e5c555824bc0258b918ffcd/finance-1-finance-bill-2015-bill-201528bi29pdf-tax-act-2014-and-the-promotion.jpg)