Embed Size (px)

Citation preview

Finance Bill 2009 – Direct Tax Proposals

Presentation by : CA. Kapil Goel, ACA, LLBChartered AccountantNew Delhicakapilgoel @gmail.com

OBJECT/SCOPE

To deliberate upon proposals of Finance Bill 2009 ( of July 6, 2009)

3

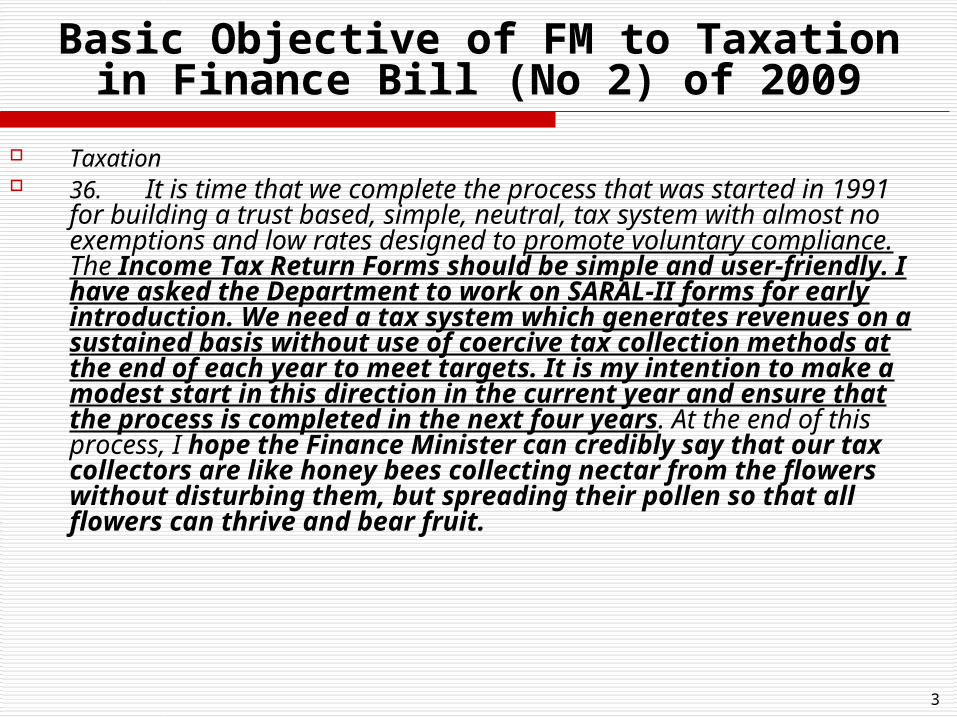

Basic Objective of FM to Taxation in Finance Bill (No 2) of 2009

Taxation 36. It is time that we complete the process that was started

in 1991 for building a trust based, simple, neutral, tax system with almost no exemptions and low rates designed to promote voluntary compliance. The Income Tax Return Forms should be simple and user-friendly. I have asked the Department to work on SARAL-II forms for early introduction. We need a tax system which generates revenues on a sustained basis without use of coercive tax collection methods at the end of each year to meet targets. It is my intention to make a modest start in this direction in the current year and ensure that the process is completed in the next four years. At the end of this process, I hope the Finance Minister can credibly say that our tax collectors are like honey bees collecting nectar from the flowers without disturbing them, but spreading their pollen so that all flowers can thrive and bear fruit.

4

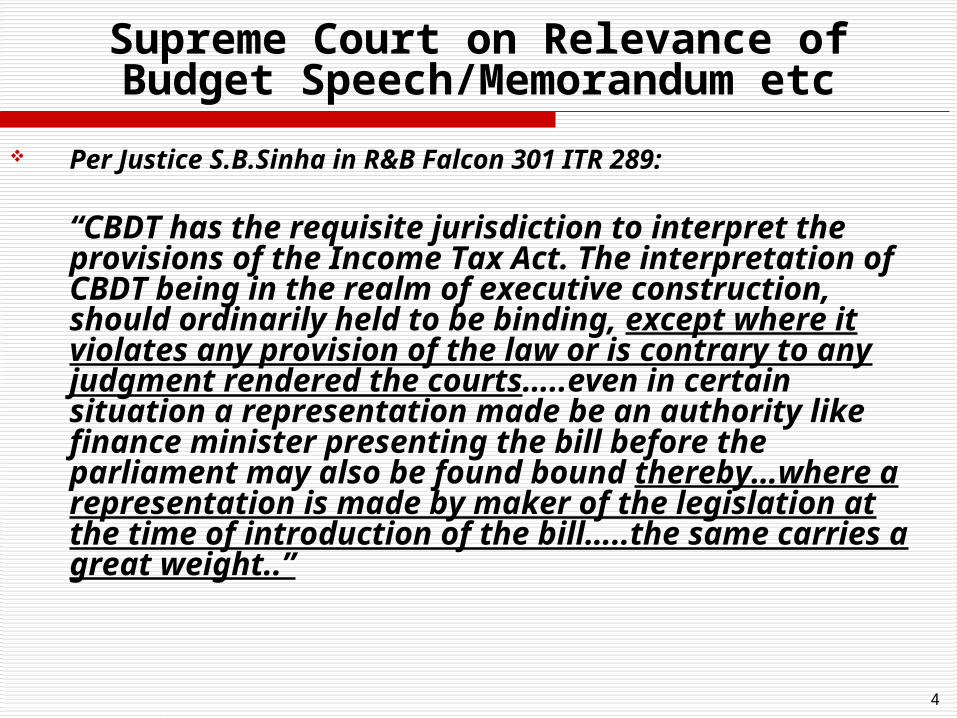

Supreme Court on Relevance of Budget Speech/Memorandum etc

Per Justice S.B.Sinha in R&B Falcon 301 ITR 289:

“CBDT has the requisite jurisdiction to interpret the provisions of the Income Tax Act. The interpretation of CBDT being in the realm of executive construction, should ordinarily held to be binding, except where it violates any provision of the law or is contrary to any judgment rendered the courts…..even in certain situation a representation made be an authority like finance minister presenting the bill before the parliament may also be found bound thereby…where a representation is made by maker of the legislation at the time of introduction of the bill…..the same carries a great weight..”

5

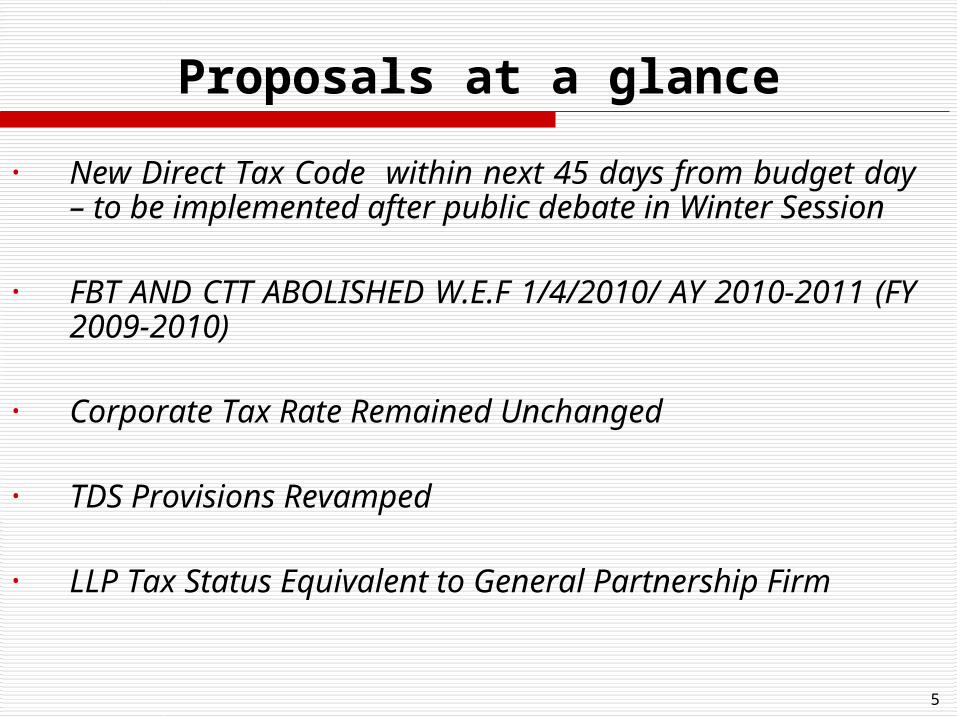

Proposals at a glance

• New Direct Tax Code within next 45 days from budget day – to be implemented after public debate in Winter Session

• FBT AND CTT ABOLISHED W.E.F 1/4/2010/ AY 2010-2011 (FY 2009-2010)

• Corporate Tax Rate Remained Unchanged

• TDS Provisions Revamped

• LLP Tax Status Equivalent to General Partnership Firm

6

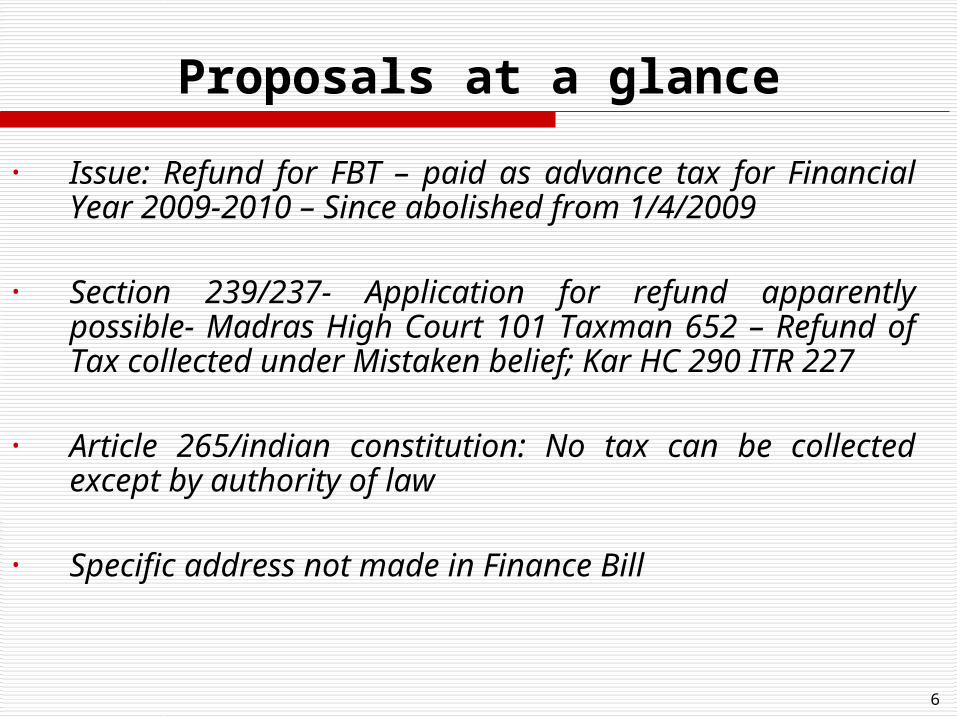

Proposals at a glance

• Issue: Refund for FBT – paid as advance tax for Financial Year 2009-2010 – Since abolished from 1/4/2009

• Section 239/237- Application for refund apparently possible- Madras High Court 101 Taxman 652 – Refund of Tax collected under Mistaken belief; Kar HC 290 ITR 227

• Article 265/indian constitution: No tax can be collected except by authority of law

• Specific address not made in Finance Bill

7

Proposals at a glance

• Personal Income Tax (Individual; HUF AOP; BOI; Artificial Juridical Person) – Basic Tax Exemption Limit (in INR- Lacs) No Surcharge on Personal Income Tax (to be removed in phased manner) (persons covered: Firm and Local Authority also) (AY 2010-2011)

Assessee Earlier (AY 2009-10) Changed (AY 2010-11)

Sr Citizen 2.25 2.40

Women 1.80 1.90

Others/individuals/HUF

1.50 1.60

8

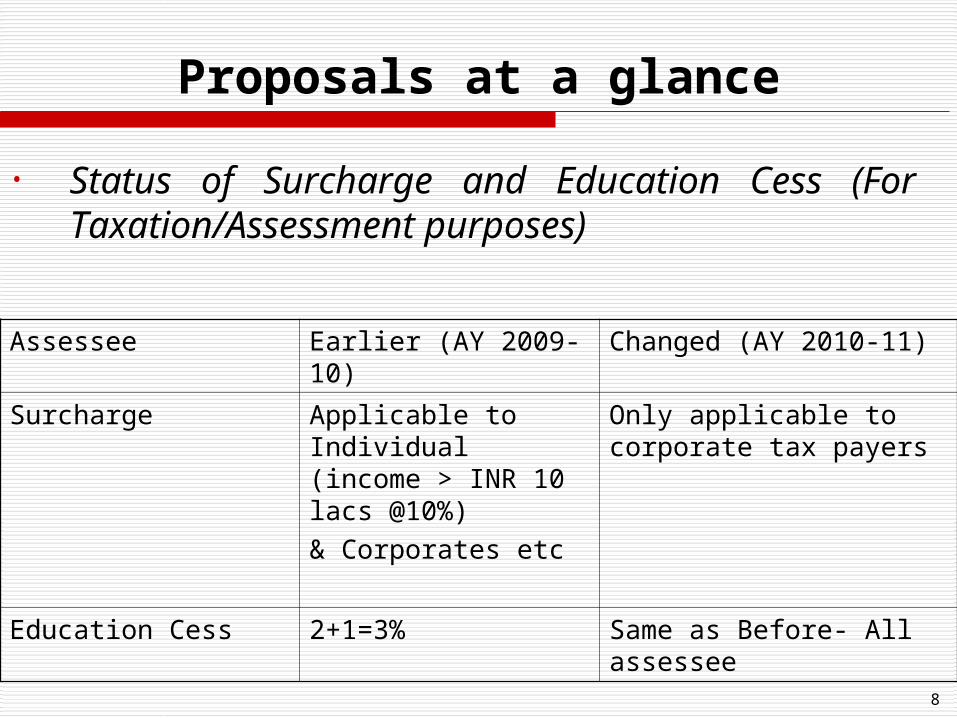

Proposals at a glance

• Status of Surcharge and Education Cess (For Taxation/Assessment purposes)

Assessee Earlier (AY 2009-10) Changed (AY 2010-11)

Surcharge Applicable to Individual (income > INR 10 lacs @10%) & Corporates etc

Only applicable to corporate tax payers

Education Cess 2+1=3% Same as Before- All assessee

9

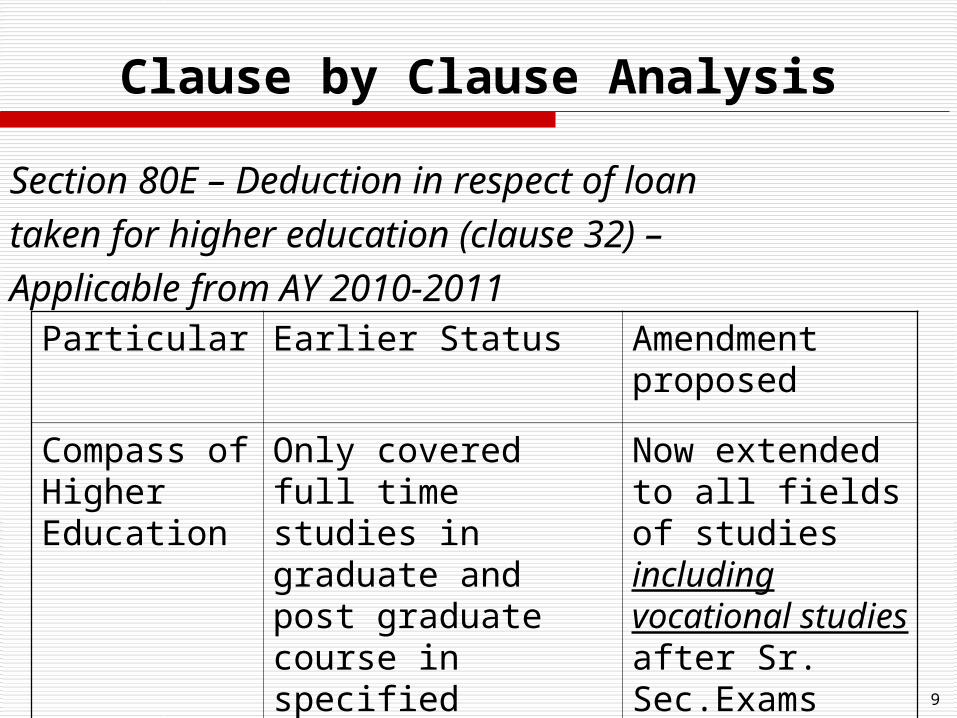

Clause by Clause Analysis

Section 80E – Deduction in respect of loan taken for higher education (clause 32) – Applicable from AY 2010-2011

Particular Earlier Status Amendment proposed

Compass of Higher Education

Only covered full time studies in graduate and post graduate course in specified subjects

Now extended to all fields of studies including vocational studies after Sr. Sec.Exams

10

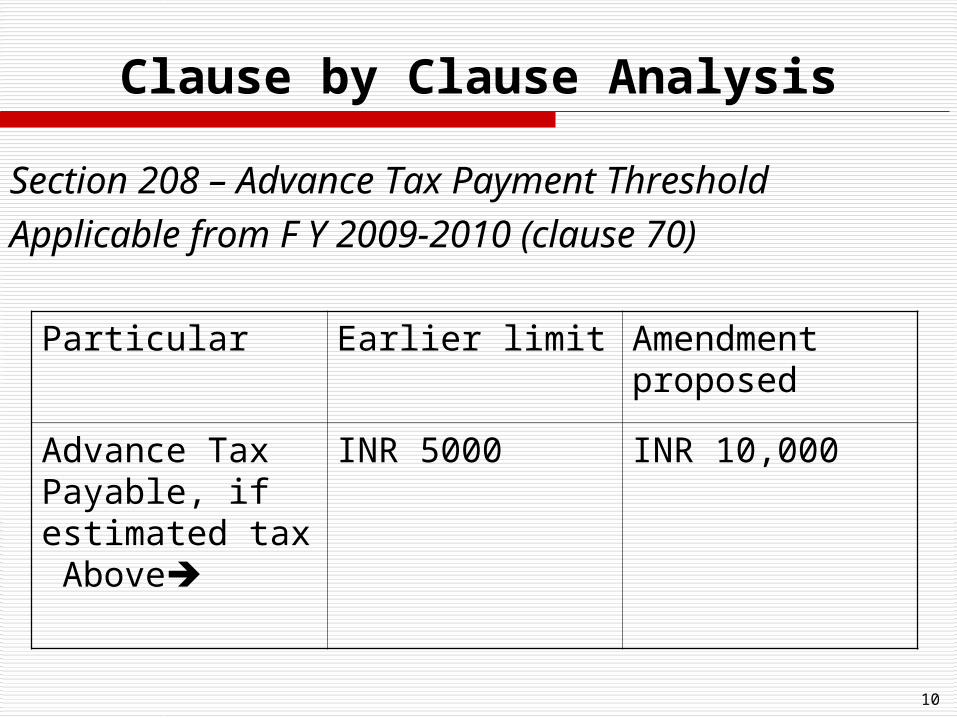

Clause by Clause Analysis

Section 208 – Advance Tax Payment ThresholdApplicable from F Y 2009-2010 (clause 70)

Particular Earlier limit Amendment proposed

Advance Tax Payable, if estimated tax Above

INR 5000 INR 10,000

11

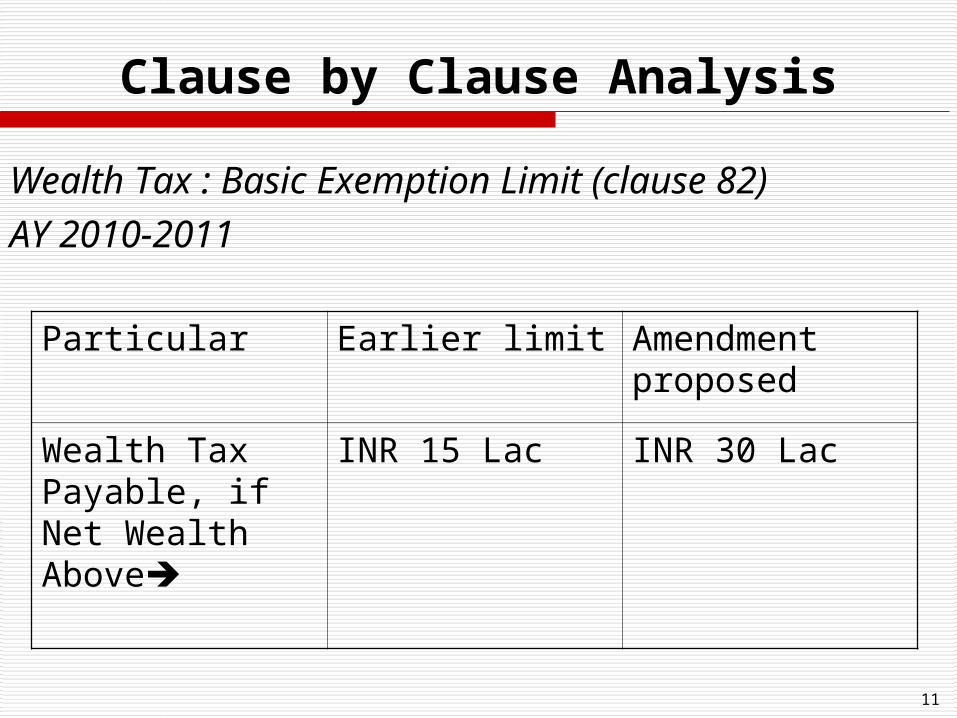

Clause by Clause Analysis

Wealth Tax : Basic Exemption Limit (clause 82) AY 2010-2011

Particular Earlier limit Amendment proposed

Wealth Tax Payable, if Net Wealth Above

INR 15 Lac INR 30 Lac

12

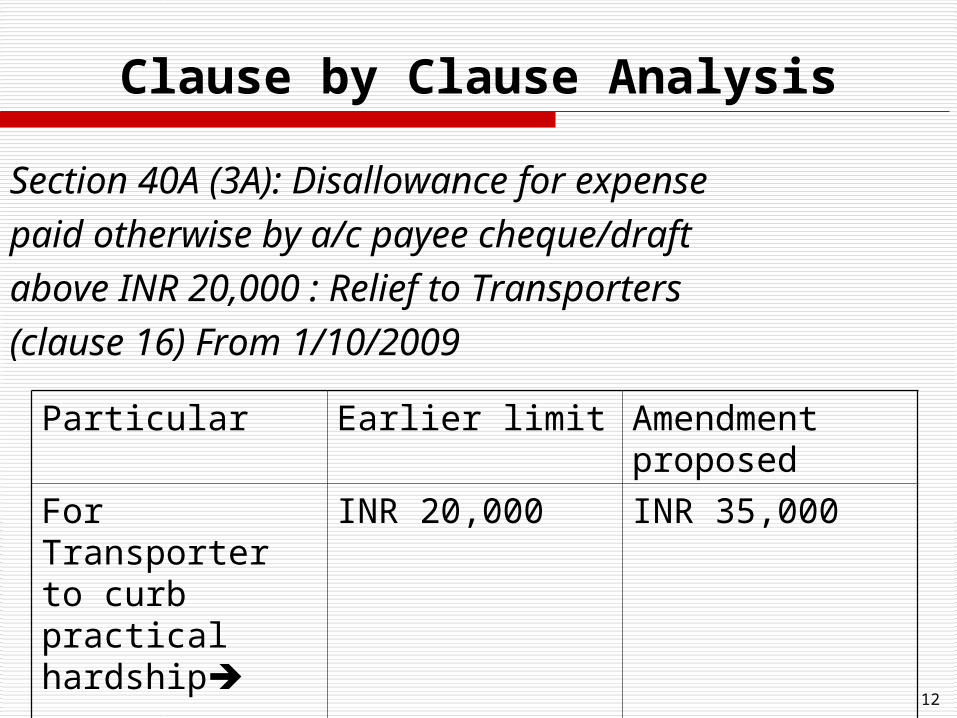

Clause by Clause Analysis

Section 40A (3A): Disallowance for expense paid otherwise by a/c payee cheque/draft above INR 20,000 : Relief to Transporters (clause 16) From 1/10/2009

Particular Earlier limit Amendment proposed

For Transporter to curb practical hardship

INR 20,000 INR 35,000

13

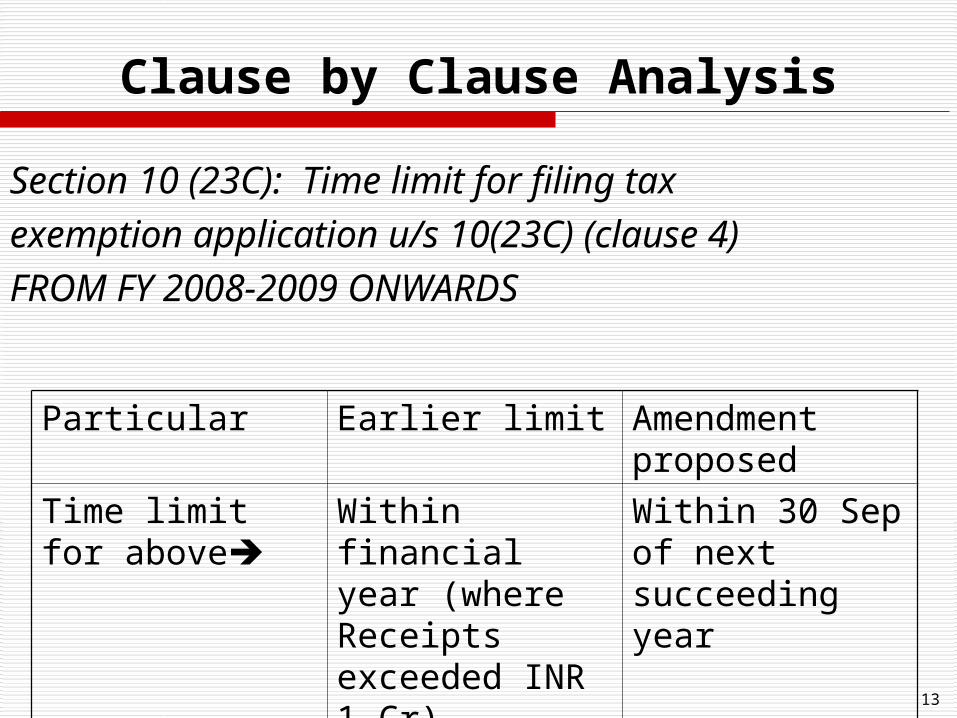

Clause by Clause Analysis

Section 10 (23C): Time limit for filing tax exemption application u/s 10(23C) (clause 4) FROM FY 2008-2009 ONWARDS

Particular Earlier limit Amendment proposed

Time limit for above

Within financial year (where Receipts exceeded INR 1 Cr)

Within 30 Sep of next succeeding year

14

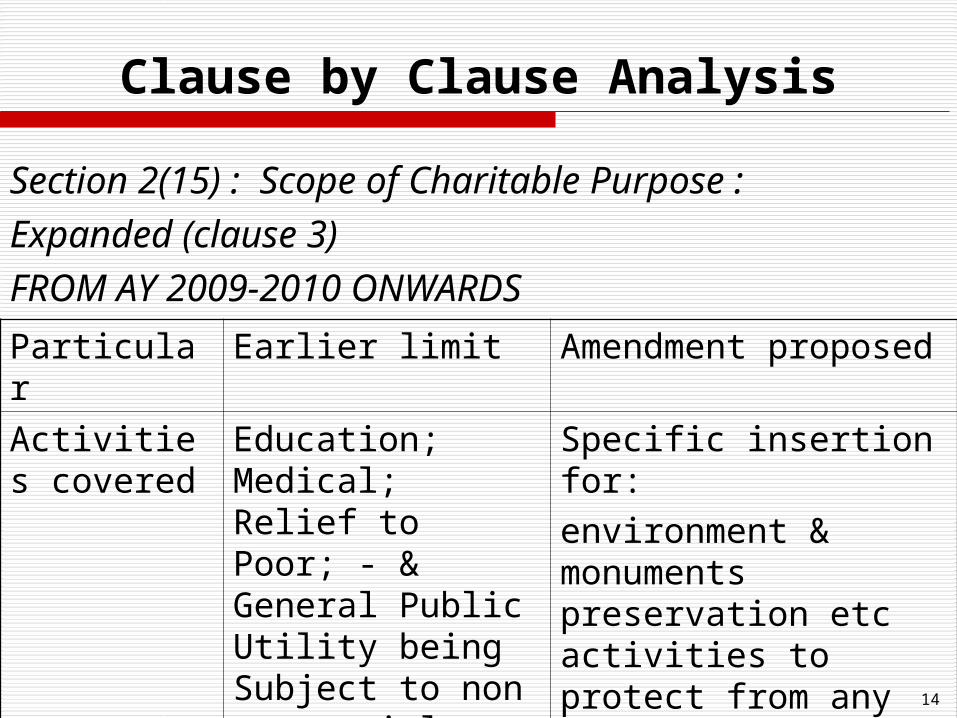

Clause by Clause Analysis

Section 2(15) : Scope of Charitable Purpose : Expanded (clause 3) FROM AY 2009-2010 ONWARDS

Particular Earlier limit Amendment proposed

Activities covered

Education; Medical; Relief to Poor; - & General Public Utility being Subject to non commercial

Specific insertion for:environment & monuments preservation etc activities to protect from any impact of Finance Act, 2008 amendment

15

Clause by Clause Analysis

Section 40(b)(v) : Remuneration to Partner’s Limit Increased (clause 15) FROM AY 2010-2011Particular Earlier limit Amendment proposed

Slab for payment of remuneration to working partner changed & alligned

Different for professional firms and others

Same for Both

In first 300,000 book profit or loss cases- INR 150,000 or 90% whichever is higher On balance= @ 60%

16

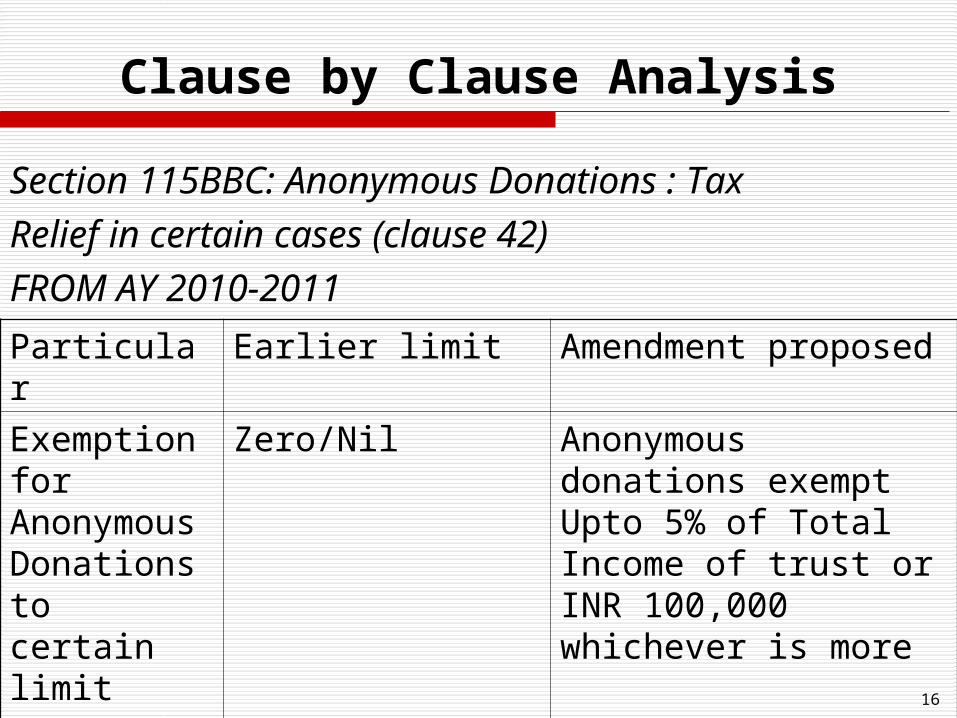

Clause by Clause Analysis

Section 115BBC: Anonymous Donations : Tax Relief in certain cases (clause 42) FROM AY 2010-2011

Particular Earlier limit Amendment proposed

Exemption for Anonymous Donations to certain limit

Zero/Nil Anonymous donations exempt Upto 5% of Total Income of trust or INR 100,000 whichever is more

17

Clause by Clause Analysis

Weighted Deduction for Inhouse Research and Development Section 35(2AB): Scope Expanded (clause 12) FROM AY 2010-2011

Particular Earlier Scope Amendment proposed

Nature of Industry Covered

Limited and Specified

Benefit extended to all manufacturing business houses except for items listed in XIth Schedule

18

Clause by Clause Analysis

Section 80G : Number of Years for which Approval u/s 80G(5)(vi) shall be applicable (clause 33)

Particular Earlier Scope Amendment proposed

Maximum Time Span in terms of Asst Years for which Approval could be given

Five Asst Years

For approval expiring after 1/10/2009 u/s 80G(5), approval will be in perpetuity – unless withdrawn by concerned CIT etc – For which expired before 1/10- once granted – perpetual force

19

Clause by Clause Analysis

Section 293C: Inserted to empower wherever in Income Tax Act an approval is required from an authority- said authority has withdrawal power Also, subject to giving hearing to concerned Assessee (clause 78)

20

Clause by Clause Analysis

Section 13B and Section 80GGB/GGC (clause 3, 4,8,34,35) – For AY 2010-2011- funding of political party- Contribution to Electoral Trust/Trust as approved by CBDT in accordance with specified scheme of Central Govt (pass through vehicle)– Eligible for 100% deduction

/for donor

- Aforesaid donations subject to tax u/s 2(24) in hands of trust; exempted u/s 13B Provided

- Said trust: functions in accordance with applicable rules to be notified &

- distributes to Political Party during concerned previous year 95% of aggregate donations as recd.to political party as registered u/s 29A (Representative of People Act)

21

Clause by Clause Analysis

Section 35AD – Investment Linked Tax Incentive for Specified Business (clause 10; 13; 17;24;28) – For AY 2010-2011 – Key Points;

for cold chain facility for specified products; for warehouse facilities for agricultural produce (business commences after 1/4/2009) and laying & operating a cross country natural gas pipeline distribution network (business commences after 1/4/2007)

For all capital expense (excl land ; goodwill and financial instrument)

loss of specified business – only adjustable against profits of the specified business – indefinite carry forward – section 73A

22

Clause by Clause Analysis

Tax Deduction at Source – TDS Law – Overhauled -a) TDS Rates – 194I- Rental (in case PAN of deductee is not there- TDS 20% applicable w.e.f 1/4/2010)

Particular Existing Rate Amendment/Proposal w.e.f 1/10/2009

Plant & Machinery 10% 2%

Land & Building- Individual/HUF Payee- Other Payee

15%

20%

10%

10%

23

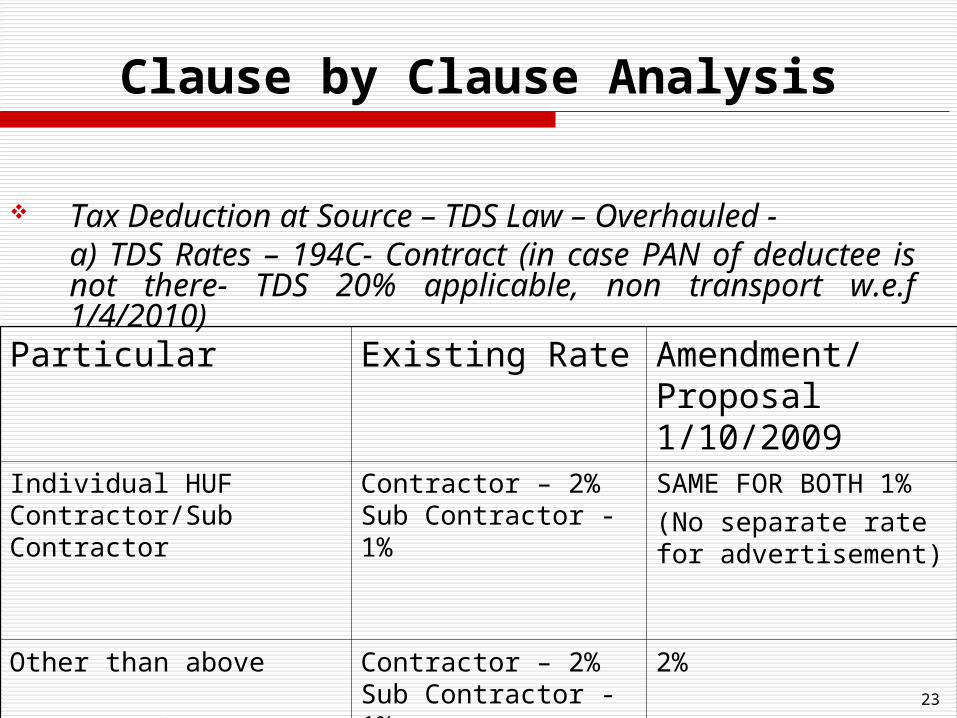

Clause by Clause Analysis

Tax Deduction at Source – TDS Law – Overhauled -a) TDS Rates – 194C- Contract (in case PAN of deductee is not there- TDS 20% applicable, non transport w.e.f 1/4/2010)

Particular Existing Rate Amendment/Proposal 1/10/2009

Individual HUF Contractor/Sub Contractor

Contractor – 2% Sub Contractor -1%

SAME FOR BOTH 1%(No separate rate for advertisement)

Other than above Contractor – 2% Sub Contractor -1%

2%

24

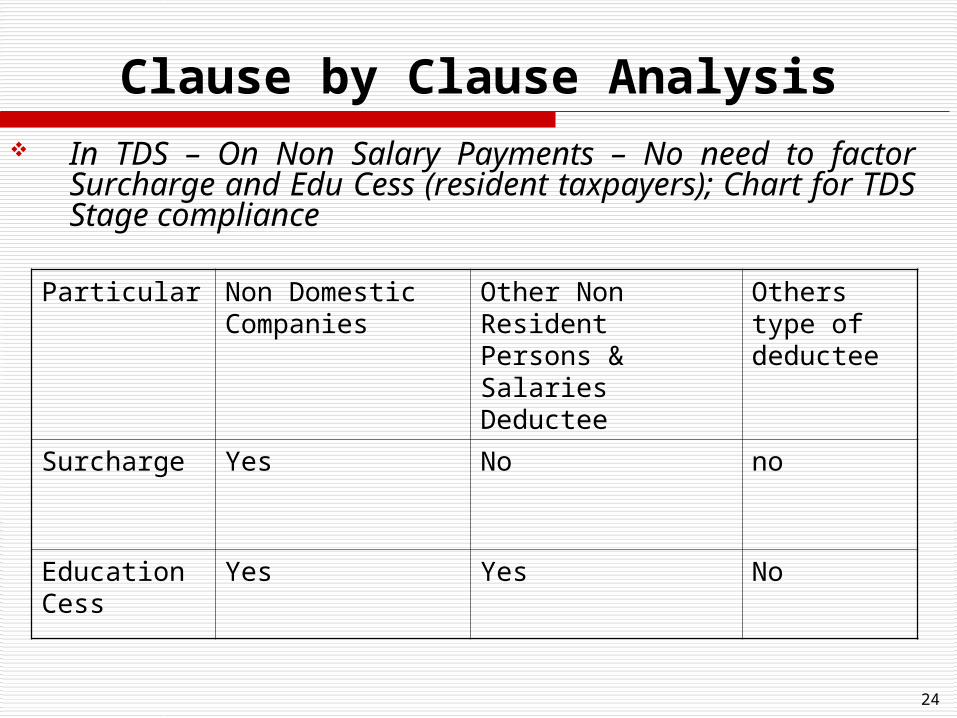

Clause by Clause Analysis In TDS – On Non Salary Payments – No need to

factor Surcharge and Edu Cess (resident taxpayers); Chart for TDS Stage compliance

Particular Non Domestic Companies

Other Non Resident Persons & Salaries Deductee

Others type of deductee

Surcharge Yes No no

Education Cess

Yes Yes No

25

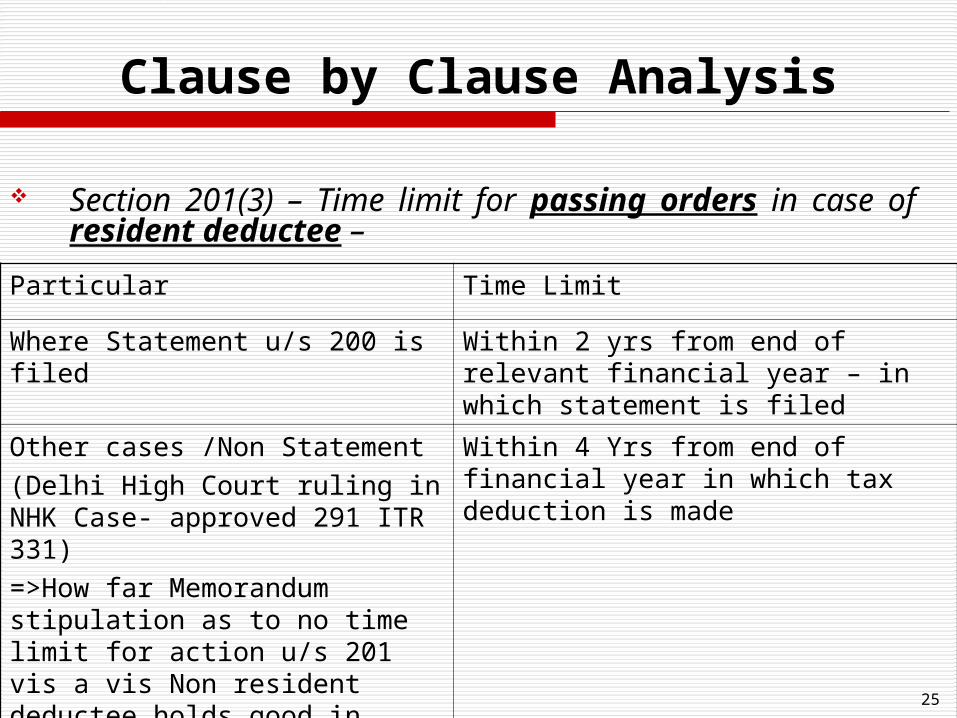

Clause by Clause Analysis

Section 201(3) – Time limit for passing orders in case of resident deductee –

Particular Time Limit

Where Statement u/s 200 is filed

Within 2 yrs from end of relevant financial year – in which statement is filed

Other cases /Non Statement(Delhi High Court ruling in NHK Case- approved 291 ITR 331)=>How far Memorandum stipulation as to no time limit for action u/s 201 vis a vis Non resident deductee holds good in light of DHC prevailing order?

Within 4 Yrs from end of financial year in which tax deduction is made

26

Clause by Clause Analysis

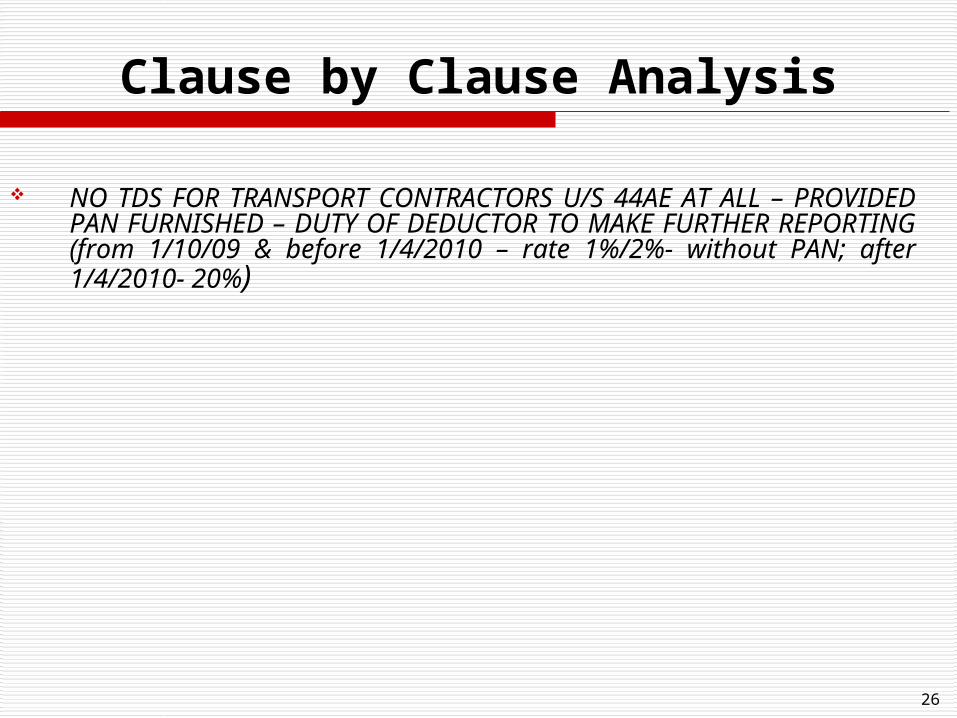

NO TDS FOR TRANSPORT CONTRACTORS U/S 44AE AT ALL – PROVIDED PAN FURNISHED – DUTY OF DEDUCTOR TO MAKE FURTHER REPORTING (from 1/10/09 & before 1/4/2010 – rate 1%/2%- without PAN; after 1/4/2010- 20%)

27

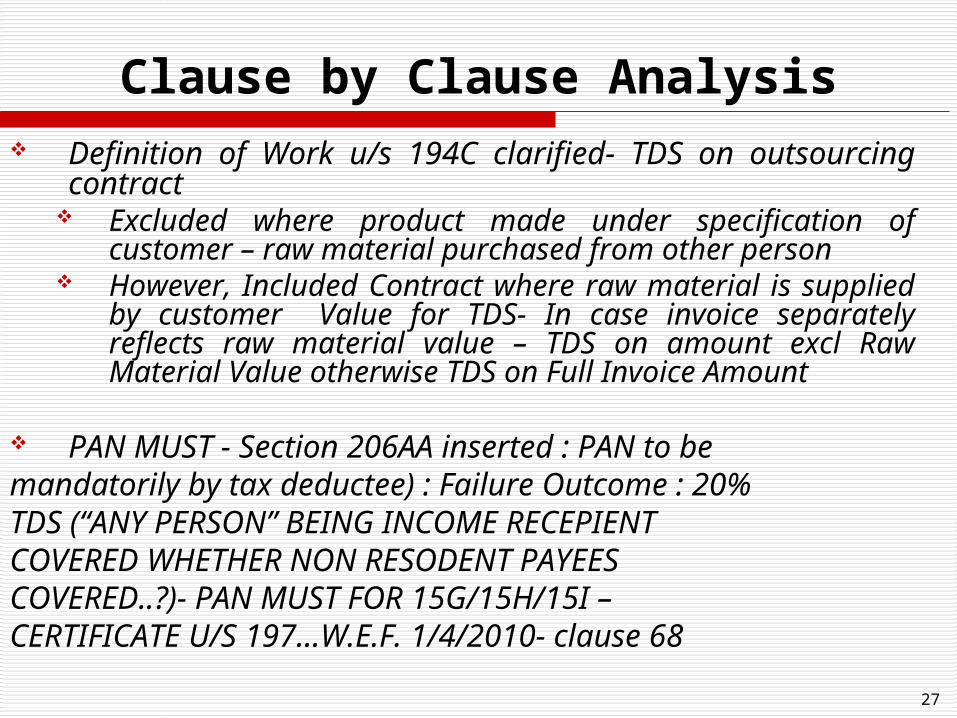

Clause by Clause Analysis Definition of Work u/s 194C clarified- TDS on

outsourcing contract Excluded where product made under specification of

customer – raw material purchased from other person However, Included Contract where raw material is

supplied by customer Value for TDS- In case invoice separately reflects raw material value – TDS on amount excl Raw Material Value otherwise TDS on Full Invoice Amount

PAN MUST - Section 206AA inserted : PAN to be mandatorily by tax deductee) : Failure Outcome : 20% TDS (“ANY PERSON” BEING INCOME RECEPIENT COVERED WHETHER NON RESODENT PAYEES COVERED..?)- PAN MUST FOR 15G/15H/15I – CERTIFICATE U/S 197…W.E.F. 1/4/2010- clause 68

28

Clause by Clause Analysis Processing of Tax Statement for TDS- Section 200A

inserted – Clause 64 From 1/4/2010 Where ever TDS statement is submitted u/s 200 – to

be processed for arithmetical error/ incorrect claim (inconsistent items etc)

Intimation to be sent for Sum Payable/Refundable to Deductor – within 1 yr from end of financial year in which statement is filed

Scheme for Centralized processing of aforesaid statement may be prescribed by CBDT

Flexibility to provide periodicity for filing tax statement u/s 200(3)- inculcated – on discretion of Govt …

29

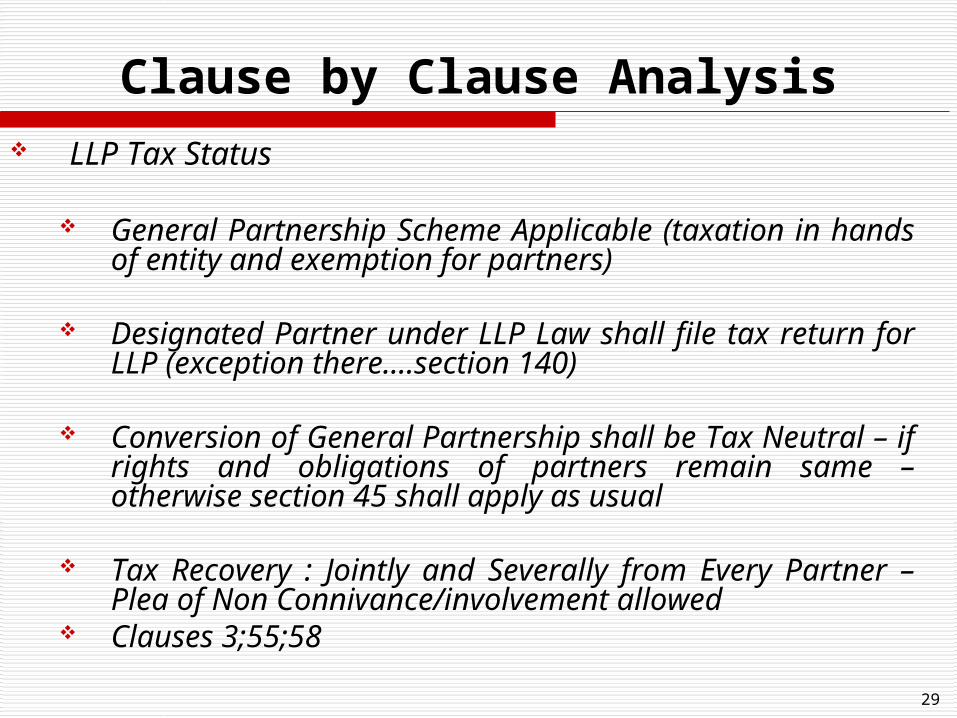

Clause by Clause Analysis LLP Tax Status

General Partnership Scheme Applicable (taxation in hands of entity and exemption for partners)

Designated Partner under LLP Law shall file tax return for LLP (exception there….section 140)

Conversion of General Partnership shall be Tax Neutral – if rights and obligations of partners remain same – otherwise section 45 shall apply as usual

Tax Recovery : Jointly and Severally from Every Partner – Plea of Non Connivance/involvement allowed

Clauses 3;55;58

30

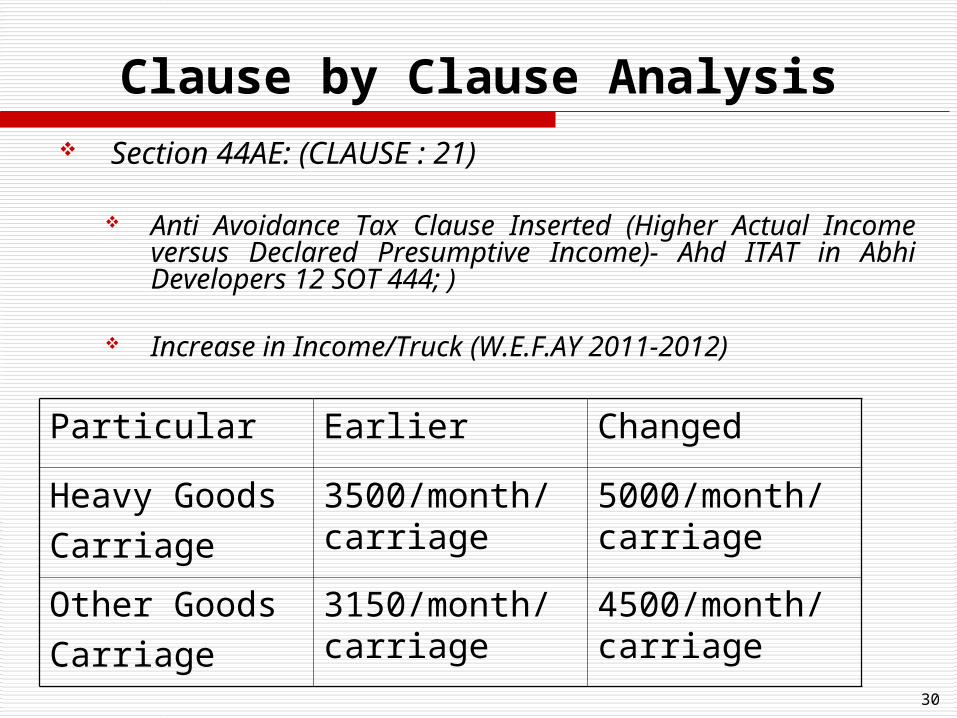

Clause by Clause Analysis Section 44AE: (CLAUSE : 21)

Anti Avoidance Tax Clause Inserted (Higher Actual Income versus Declared Presumptive Income)- Ahd ITAT in Abhi Developers 12 SOT 444; )

Increase in Income/Truck (W.E.F.AY 2011-2012)

Particular Earlier Changed

Heavy GoodsCarriage

3500/month/carriage

5000/month/carriage

Other GoodsCarriage

3150/month/carriage

4500/month/carriage

31

Clause by Clause Analysis Section 44AD: (CLAUSE : 18 TO 22)

Applicable from AY 2011-2012

Type of Assessee Eligible : Covering Individual/HUF/Firm excl LLP not claiming deduction u/s 10A/10AA/10B/10BA/CH VIA (Heading ‘C’)

Nature of Business Covered: Any Business excluding Section 44AE/Truck Operator Maximum Turnover INR 40 Lacs

Immunity from Advance Tax Payment

No Books; Audit if scheme opted (That is, In case not opted- books and audit mandatory)

TAX AUDIT SCOPE IMPLIEDLY EXTENDED?

32

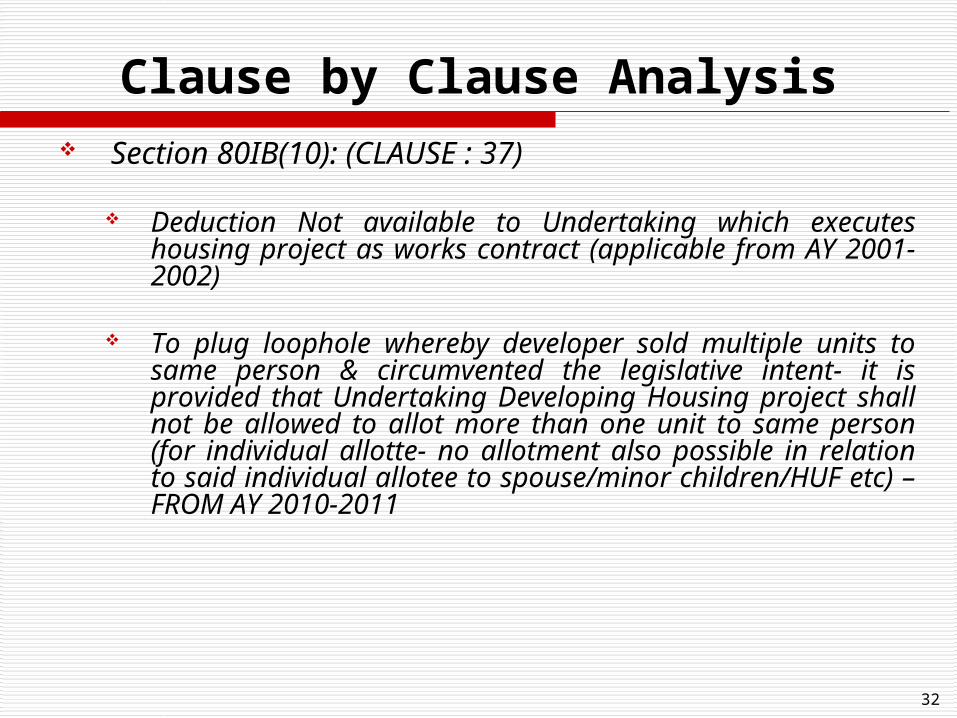

Clause by Clause Analysis Section 80IB(10): (CLAUSE : 37)

Deduction Not available to Undertaking which executes housing project as works contract (applicable from AY 2001-2002)

To plug loophole whereby developer sold multiple units to same person & circumvented the legislative intent- it is provided that Undertaking Developing Housing project shall not be allowed to allot more than one unit to same person (for individual allotte- no allotment also possible in relation to said individual allotee to spouse/minor children/HUF etc) – FROM AY 2010-2011

33

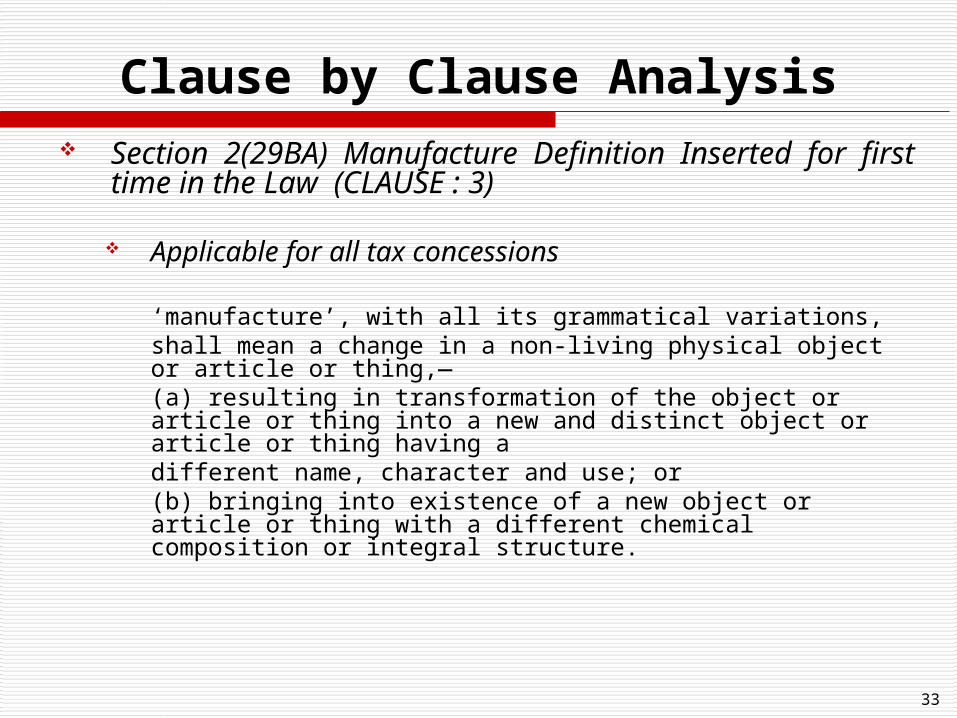

Clause by Clause Analysis Section 2(29BA) Manufacture Definition Inserted for

first time in the Law (CLAUSE : 3)

Applicable for all tax concessions

‘manufacture’, with all its grammatical variations,shall mean a change in a non-living physical object or article or thing,—(a) resulting in transformation of the object or article or thing into a new and distinct object or article or thing having adifferent name, character and use; or(b) bringing into existence of a new object or article or thing with a different chemical composition or integral structure.

34

Clause by Clause Analysis Reassessment Proceedings

Clause 57 Explanation to Section 147 inserted

Impliedly Overruled Kerala High Court in Travancore 305 ITR 170 and Delhi High Court in Jai Bharat Maruti cases ITA 501/2007 223 CTR 269

No need for separate recording of reasons on “other issues” noticed in reassessment proceedings

From AY 1989-90 ONWARDS

35

• Scope of addition on “unconnected issues” (issues other than one on which reopening is made and reasons are recorded):

• Whether addition on main/parent/original issue must – connotation of phrase “and” as connecting section 147….

• Held yes by Raj HC in Shree Ram Singh 217 CTR 345 and Dr Devender Gupta 220 CTR 629

• Fav Ker HC in Travancore Rubber 305 ITR 170 (applied by Delhi High Court in Jai Bharat Maruti) (EXPLAINED NEXT SLIDES)

• Del ITAT in Software Consultants ITA 2554/2004; CJ International ITA 2736/2006; Narayan Securities ITA 309/Del/2007;

• Asr ITAT in R.K.Kakkar 108 TTJ 1; Darshan Kaur BCAJ Sep 2008

• Jodhpur ITAT in 118 TTJ 276• Agra ITAT in Saraf Gramudyog BCAJ Jun 2007• P&HHC in Gardhara Singh 173 Taxman 46

Section 147 – Issues

36

• Scope of addition on “unconnected issues” :• Whether addition possible after making roving

and fishing enquiries Held No in • Delhi ITAT in K.G.Baliga (ITA No. 3840/2003)• Expotech (ITA 1016/2004), • Poonam Rani Singh 97 ITD 390, • Jaipur ITAT in Gyarsi Lal 95 TTJ 386, • Manoj Kr Gupta 114 TTJ 253 etc. • DHC in Jai Bharat Maruti & • Del ITAT in Ravina Associates 15 DTR 1; • Del ITAT in S Harishanker 19 DTR 72• Del ITAT in Jeevan Prakash Gupta 1016/Del/2004

• Impact of SC ruling in Alagendran Finance 293 ITR 1 stating reopening do not wash previous assessment and is open qua escaped issues

Section 147 – Issues

37

Clause by Clause Analysis Search Under Section 132 Clause 50/51

Amendment having Mass Impact : Delhi High Court in Nalini Mahajan and Pawan Gupta & All HC in Raghu Partap overruled

Provided from Retrospective Effect : Joint Director and Additional Director Had Power to Issue Warrant repc w.e.f 1/6/1994 & 1/10/1998

DHC in Capital Power and Pawan Kumar 222 CTR 36/47 & P&HHC in Vinod 252 ITR 29 & All HC in Raghu Partap 307 ITR 450 SC in Chand Vhurasia – Latest Development- revenue’s SLP notice issued

38

Clause by Clause Analysis How far retrospective validation of hitherto

adjudicated illegal exercise of power can be made?

Kar HC in 239 ITR 282 (Section 148- Thirty days time limit omission- retrospective effect – held constitutionally valid)

P&HHC in 290 ITR 15 (section 148 – limited immunity to notices not served as per section 143(2), post 148 notice return from retrospective effect to overrule Special Bench ITAT Raj Kaumar Chawla case etc- validity upheld )

39

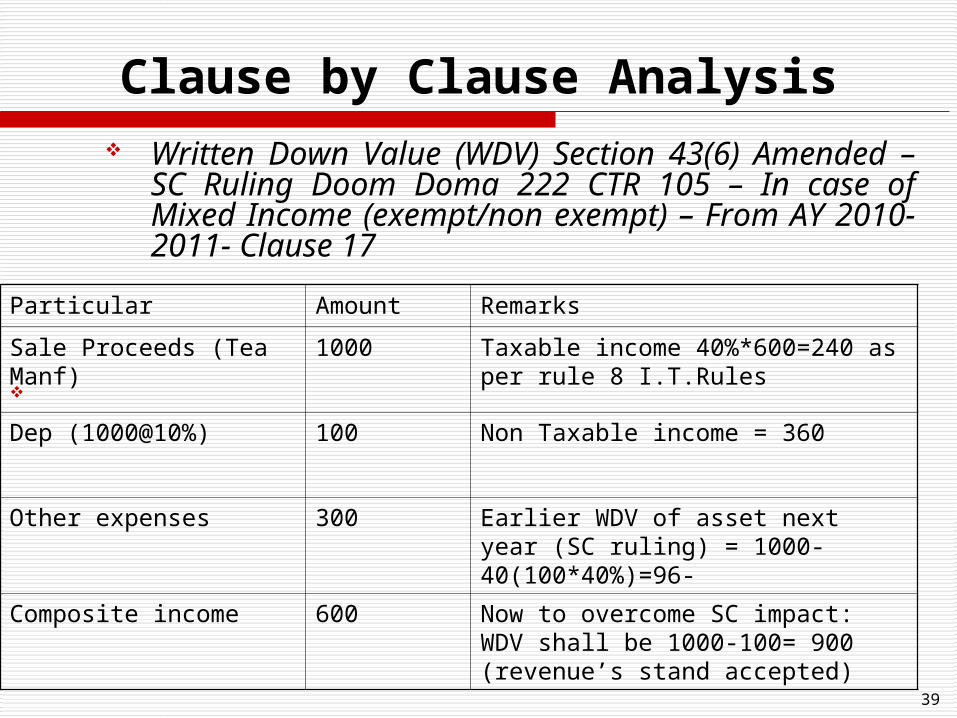

Clause by Clause Analysis Written Down Value (WDV) Section 43(6)

Amended – SC Ruling Doom Doma 222 CTR 105 – In case of Mixed Income (exempt/non exempt) – From AY 2010-2011- Clause 17

Particular Amount Remarks

Sale Proceeds (Tea Manf)

1000 Taxable income 40%*600=240 as per rule 8 I.T.Rules

Dep (1000@10%) 100 Non Taxable income = 360

Other expenses 300 Earlier WDV of asset next year (SC ruling) = 1000- 40(100*40%)=96-

Composite income 600 Now to overcome SC impact: WDV shall be 1000-100= 900 (revenue’s stand accepted)

40

Clause by Clause Analysis New Pension scheme – operation from

1/1/2004- mandatory for all Central Govt recruits- also opened for state govt/private sector and self employed ….NPT/Trust set up 27/2/2008 under Indian Trust Act- Tax Structure (EET Method followed/proposed) Section 10(44)- income recd by any person on

behalf of trust exempt from tax Dividend to NPT shall be exempt from DDT u/s 115O All purchase/sales of equity/derivative – by NPT

exempt from STT NPT shall receive all income without TDS –section

197A Benefit available u/s 80CCD on contribution to NPT

(hitherto employees included – now self employed also included)

Applicable from AY 2009-2010 ONWARDS

41

Clause by Clause Analysis Anomaly in SEZ Unit Deduction u/s 10AA

removed (Parity in Numerator and Denominator) from AY 2010- 2011

Earlier FormulaeFor Deduction Computation

Profits of business of Unit* Export Turnover of Unit/Total Turnover of Business of Assessee

Proposed LawFor Deduction Computation

Profits of business of Unit* Export Turnover of Unit/Total Turnover of Business of undertaking/unit

42

Clause by Clause Analysis Section 56(2)(vi) Transaction without

consideration/inadequate consideration (for transactions on/after 1/10/2009)- clause 26

Provided that Property recd without consideration will be included (which in turn will include immovable property; share/securities/ jewellery etc)

In case of immovable property without consideration: if stamp duty value exceeds INR 50,000 : WHOLE STAMP VALUE TAXABLE and for Inadequate consideration : Difference in stamp value and declared value taxable

For Movable Property recd without consideration: Fair Market Value shall be base of taxation (Method to be prescribed)

43

Clause by Clause Analysis Section 50C- Clause 25 for transactions

on/after 1/10/2009

Covered transactions executed through agreement to sell

Jd ITAT RULINGS IN 110 ITD 525/112 TTJ 76/ 122 TTJ 515 Impliedly Overruled

44

Clause by Clause Analysis MAT – Clause 43; 44;45

From AY 2010-2011

Rate of Taxation u/s 115JB increased from 10% to 15%

Carry Forward period u/s 115JAA(2) increased from 7 to 10 years

From AY 1998-1999: Provision for Diminution in value of asset debited to P&L – to be added back to determine taxable book profits

45

Clause by Clause Analysis Section 10(10C): Compensation on voluntary

retirement/termination of service

Clause 4; 38 from AY 2010-2011

Double Benefit Addressed – Proviso to section 89 & 10(10C) inserted

Rulings prospectively impacted Mad HC in 273 ITR 307 G.V.VENUGOPAL Kar HC in 279 ITR 402 BHC in 291 ITR 407 Mad HC 245 ITR 856

46

Clause by Clause Analysis Introduction of Document Identification

Number/DIN and facility of electronic communication

With effect from 1/10/2010

Section 282B : Every Income tax authority bound to allot a computer generated DIN for every document issued/recd by them

Document issued/recd without DIN shall be invalid

Provision for service of notice by electronic mode u/s 282 & courier service provided w.ef 1/10/2009 (for electronic service – rules to be made by CBDT)- CLAUSE 76; 77

47

Clause by Clause Analysis Concealment Penalty : Section 271(1)(c)

Explanation 5A – Clause 73’ For Search after 1/6/2007

Deemed concealment – clarified to cover where return filed before search but income found in search not included in return – deemed to be concealed (for previous year being ended before search date)- section 56(2)(viii)

48

Clause by Clause Analysis Clause 26;27 & 56 – Interest on delayed

/enhanced compensation

SC Rama bai 181 ITR 400 – Taxable on mercantile basis

Amendment proposed in section 145A : Taxable in year of receipt; irrespective of accounting method followed and under the head other sources

49

Clause by Clause Analysis Clause 40 & 41

Transfer Pricing Law

Safe Harbor Rules Concept introduced (from 1/4/2009)- to reduce the impact of judgment error in determining the transfer price

Where more than one price is determined by most appropriate method – Arm Length Price shall be Arithmetic Mean of the same (If ALP is within 5% of Transfer price as reflected by Assessee – No further adjustment required in assessee declared Transfer Price)

Kol ITAT in Development Consultants & Sony Delhi ITAT rulings apparently impacted

50

Clause by Clause Analysis

Alternate Dispute Resolution Mechanism for Person in whose case transfer pricing oder u/s 92CA(3) by TPO is passed and any foreign company

For orders passed after 1/10/2009 Draft Assessment Order to be prepared and sent to

assessee intimating proposed variations – prejudicial to assessee

Eligible Assessee can file either acceptance or his objections thereon to i) Dispute Resolution Panel and II) AO

Powers similar to CIT-A are available to Panel Dispute Resolution Panel to consist of three CIT’s

nominated by CBDT- Directions binding on revenue/AO - Assessee can Appeal to ITAT from order of AO passed in

pursuant to Panel Directions Section 144C inserted

51

Clause by Clause Analysis In case Dispute Panel do not pass directions as

per - sub-section (5)- with in nine months from the end of the month in which the draft order is forwarded to assessee- Impact? Whether Functus Officio & Deemed Acceptance of Assessee’s Objections – AllHC in context of section 12AA – 216 CTR 167

Whether procedure applicable to each tax assessment of Non resident/Foreign Company in International tax Cell? (like Vodafone Type cases?)

52

Clause by Clause Analysis Other Amendments as proposed:

Extension of Sunset clause for tax holiday u/s 80IA (TERMINAL DATE FOR COMMENCING ACTIVITY OF POWER DSITRIBUTION EXTENDED FROM 31/3/2008 TO 31/3/2011 – 80IA(4)(v)(b) & under 80IA(4)iv)- to 31.3.2011 from 31.3.2010- clause 36 Power Sector Tax Reform

Oil Refineries – Time limit u/s 80IB(9) FOR commencing operations upto 31/3/2009 extended to 31/3/2012 (both for public and private sector); Natural Gas production licensed under NELP VIIIth round bidding & beginning production after 1/4/2009 – entitled (AHD ITAT IN NIKO FOR EARLIER PERIOD? 22 DTR 225

Undertaking u/s 80IB(9) Not every well in Oil Block but all blocks under single contract of NELP- one undertaking – from AY 2000-2001

53

Clause by Clause Analysis Other Amendments as proposed:

Section 10A/10B deduction available for one more year – viz AY 2011-2012 (earlier sunset by AY 2010-2011)

Abolition of FBT Paves way for revival of old tax regime Perquisite in hands of employees (section 17(2)(vi;

vii & viii – inserted) Capital Gains taxation on ESOP’s etc

Section 36(1)(viii)- to allow National Housing Bank benefit under said section – being engaged in re-financing & financing of housing/slum projects – for words construction/purchase of residential houses; words “development of housing in India” substituted- clause 14- AY 2010-2011

54

Clause by Clause Analysis Other Amendments as proposed:

Section 2(48) Scheduled Banks incl Nationalized Banks empowered to issue ZERO coupon Bonds (earlier INFRASTRUCTURE CAPITAL CO./FUND AND PUBLIC SECTOR CO WERE ONLY EMPOWERED)

Central Govt Empowered tp enter into agreement with specified non sovereign countries- Section 90 Scope expanded Tax Information Exchange Agreement – clause 38;83—w.e.f 1/10/2009

Non Life Insurance Business – Parity introduced between IRDA Guidelines and Income Tax Act vis a vis Taxation of Income/Loss from Investment- clause 79

![KAPIL SHING ]](https://img.dokumen.tips/doc/110x75/577d27691a28ab4e1ea3dca9/kapil-shing-.jpg)