Embed Size (px)

Citation preview

Finance 431Insurance RegulationLessons from Illinois

Overview

• Historical Development– Insurance Regulation– Industry Structure– Antitrust Legislation

• Insurance Regulation in Illinois• Analysis of the Illinois Auto Experience• Generalization to Other Lines• Recent Events

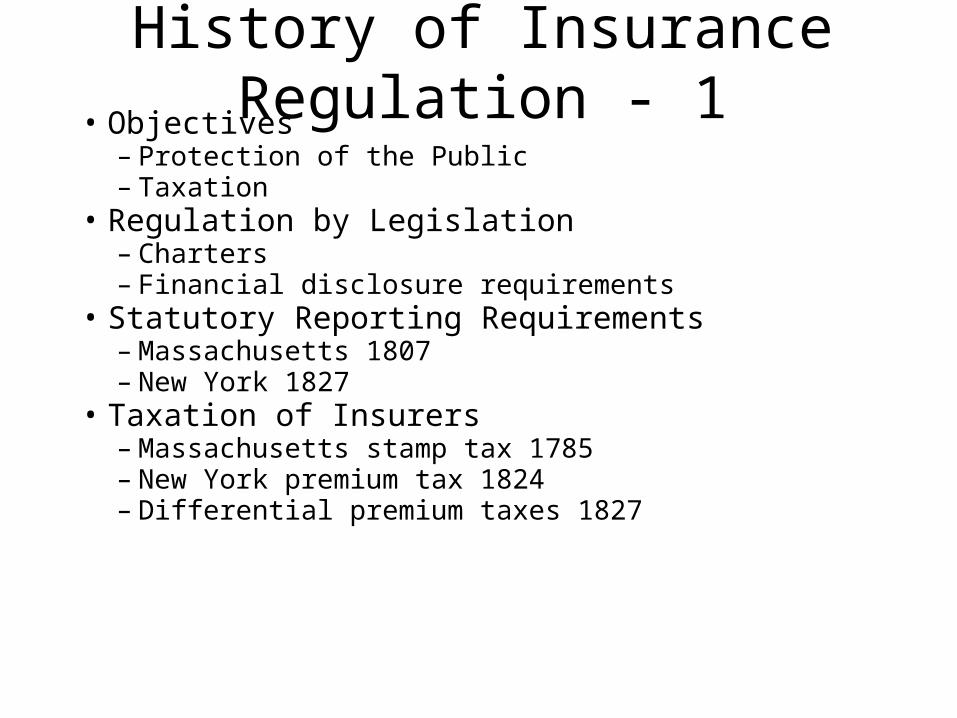

History of Insurance Regulation - 1• Objectives

– Protection of the Public– Taxation

• Regulation by Legislation– Charters– Financial disclosure requirements

• Statutory Reporting Requirements– Massachusetts 1807– New York 1827

• Taxation of Insurers– Massachusetts stamp tax 1785– New York premium tax 1824– Differential premium taxes 1827

Why Were States Regulating Insurance?

• Commerce Clause of the U. S. Constitution“Congress shall have the power ... to regulate commerce ... among

the several states”

– Limits power of states to regulate interstate business

• Paul v. Virginia 1869– Insurance is not interstate commerce

• Insurance contracts are not commerce

• Policies do not take effect until delivered, so not interstate in nature

– States could regulate (and tax) insurance

Early Structure of the Property Insurance Industry

• Primarily Fire Insurance• Adverse Effects of Competition• Rating Associations

– Local– National Board of Fire Underwriters 1866

• Catastrophic Fires– New York City 1835– Chicago 1871– Boston 1872– San Francisco 1906

• Insurance Bankruptcies

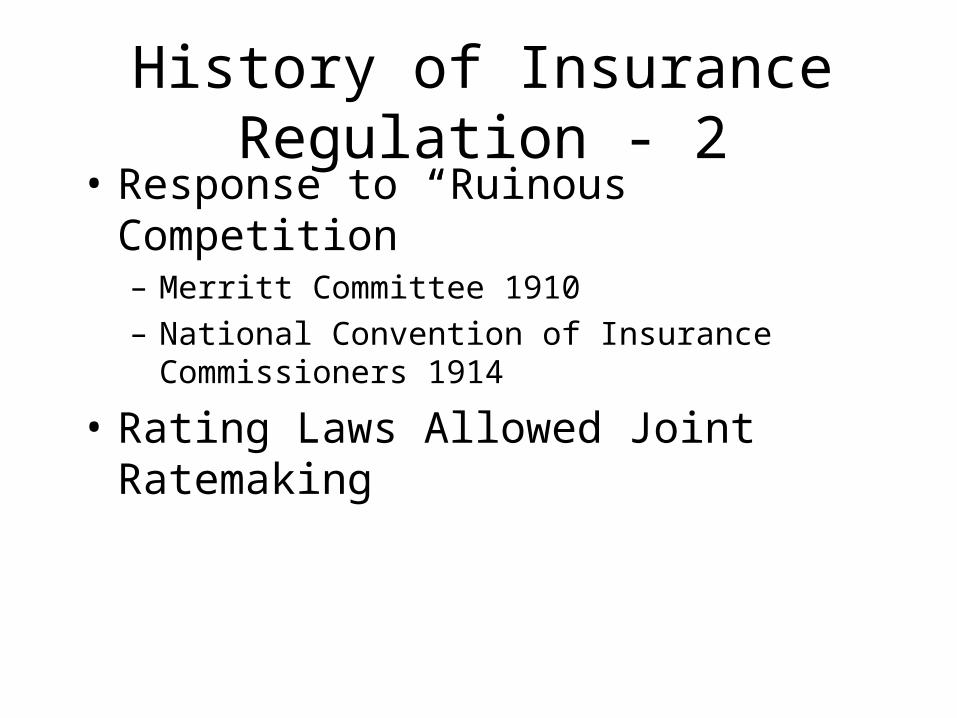

History of Insurance Regulation - 2• Response to “Ruinous Competition”

– Merritt Committee 1910

– National Convention of Insurance Commissioners 1914

• Rating Laws Allowed Joint Ratemaking

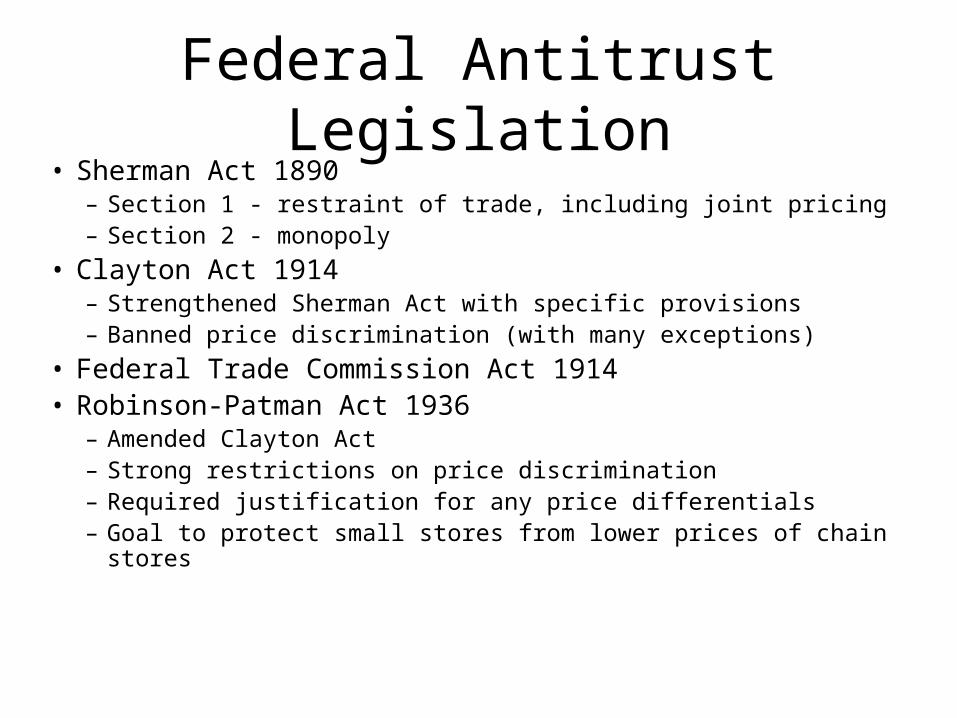

Federal Antitrust Legislation• Sherman Act 1890

– Section 1 - restraint of trade, including joint pricing– Section 2 - monopoly

• Clayton Act 1914– Strengthened Sherman Act with specific provisions– Banned price discrimination (with many exceptions)

• Federal Trade Commission Act 1914• Robinson-Patman Act 1936

– Amended Clayton Act– Strong restrictions on price discrimination– Required justification for any price differentials– Goal to protect small stores from lower prices of chain stores

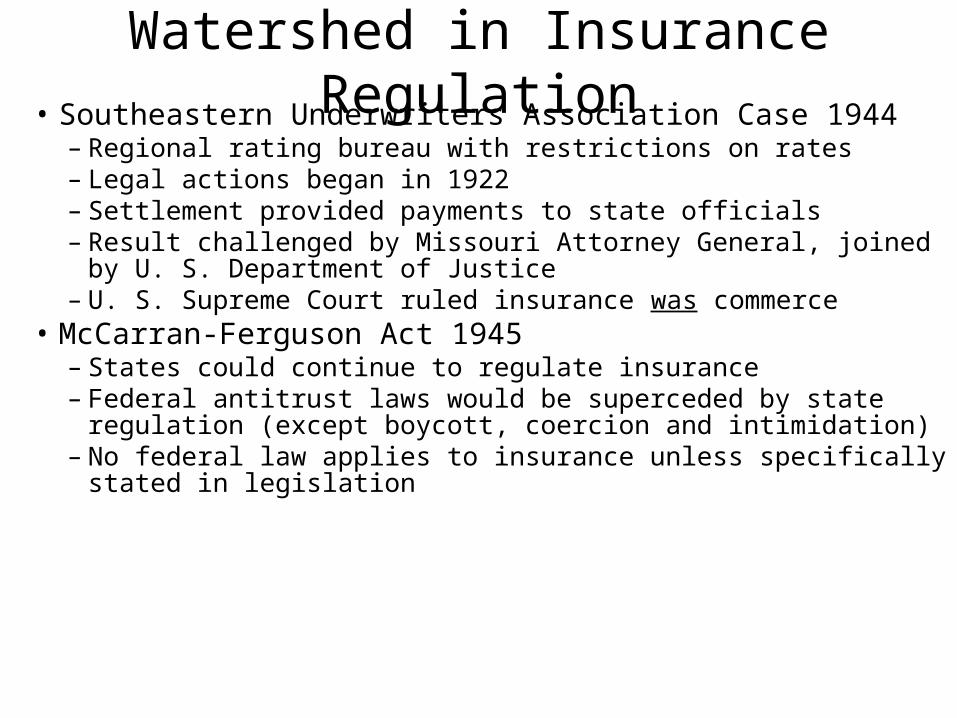

Watershed in Insurance Regulation• Southeastern Underwriters Association Case 1944

– Regional rating bureau with restrictions on rates– Legal actions began in 1922– Settlement provided payments to state officials– Result challenged by Missouri Attorney General, joined by U. S.

Department of Justice– U. S. Supreme Court ruled insurance was commerce

• McCarran-Ferguson Act 1945– States could continue to regulate insurance– Federal antitrust laws would be superceded by state regulation (except

boycott, coercion and intimidation)– No federal law applies to insurance unless specifically stated in

legislation

Insurance Rate RegulationPost-SEUA

• All states adopted rate regulatory laws to supercede federal antitrust laws – State made rates– Mandatory bureau rates– Prior approval– File-and-use– Use-and-file– Open competition

• Rates are not to be inadequate, excessive or unfairly discriminatory

Which law or court ruling currently prevents the Federal antitrust laws from being applied to the joint ratemaking activities of insurance companies?

A) Paul v. Virginia

B) Southeastern Underwriters Association

C) Sherman Act

D) McCarran-Ferguson Act

E) None of the above

The Merritt Committee report recommended that rating bureaus should be allowed, subject to state regulation, to prevent excessive competition. Which line of business did this report consider?

A) Fire

B) Workers Compensation

C) Automobile

D) Commercial General Liability

E) None of the above

Illinois Rate Regulation

• Adopted Prior Approval law 1947

• Enacted Open Competition Law effective 1970

• Open Competition Law expired in August 1971

• Illinois has no rate regulatory law for most lines of business

Illinois Statistics

• Population12,419,293 as of 4/1/2000

Fifth largest state

• Size – 55,593 sq. mi. (25th largest)

• Urban Population - 84.6%

• Per capita income $31,278 (8th)

How Is Illinois Faring without Auto Insurance Rate Regulation?

• Loss ratio - Less variable• Rate levels - Less variable• Number of insurers - Highest in nation• Premium levels - Lower than comparable areas• Uninsured drivers - Lower• Residual market size - Lower• Cost of regulation - Lower

Conclusion No need to regulate auto insurance rates

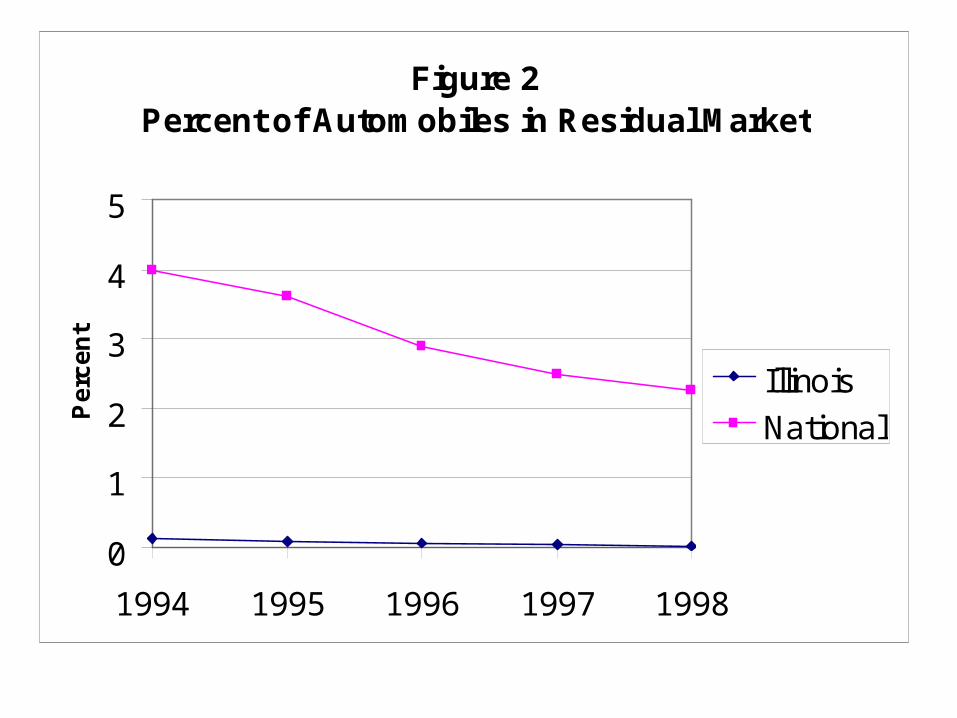

Figure 2Percent of Automobiles in Residual Market

0

1

2

3

4

5

1994 1995 1996 1997 1998

Pe

rce

nt

Illinois

National

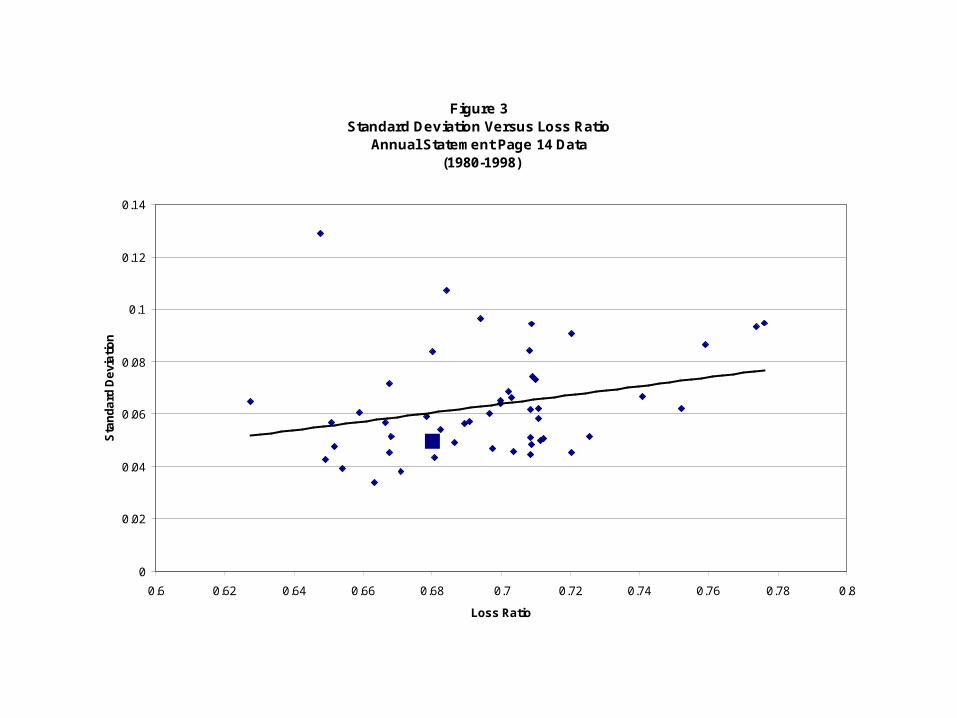

Figure 3Standard Deviation Versus Loss Ratio

Annual Statement Page 14 Data (1980-1998)

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.6 0.62 0.64 0.66 0.68 0.7 0.72 0.74 0.76 0.78 0.8

Loss Ratio

Sta

nd

ard

De

via

tio

n

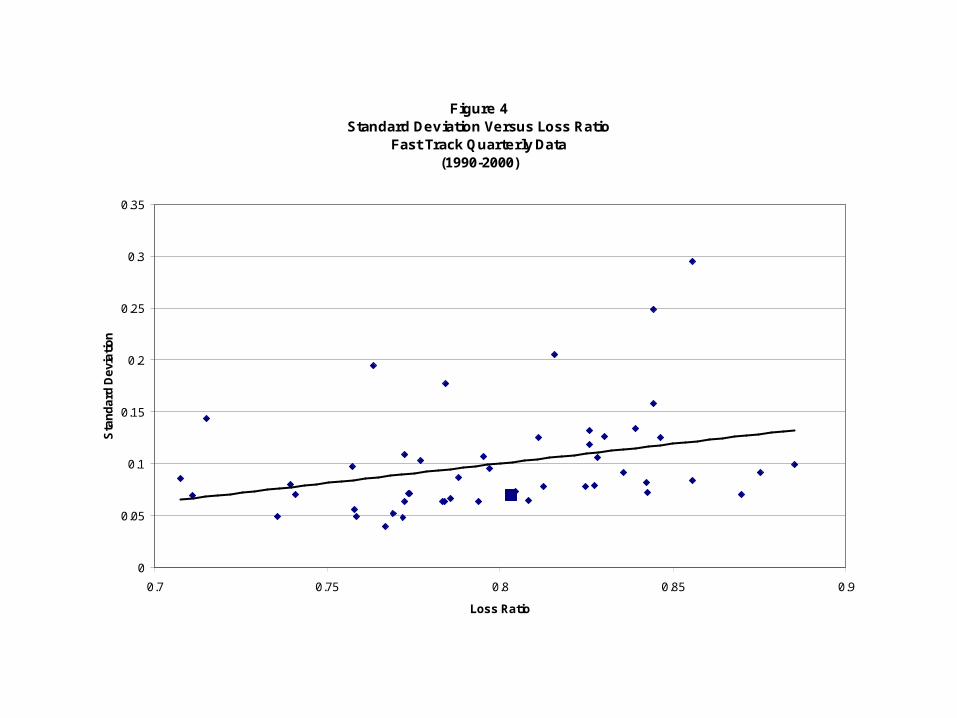

Figure 4Standard Deviation Versus Loss Ratio

Fast Track Quarterly Data (1990-2000)

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.7 0.75 0.8 0.85 0.9

Loss Ratio

Sta

nd

ard

De

via

tio

n

Figure 5Company 1 Year End Rate Levels

(12/31/89=1.000)

0.75

1

1.25

1.5

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Year

Ra

te L

eve

l

CA

CO

CT

FL

GA

IL

KY

MA

MI

MN

MO

NJ

NC

OH

OR

PA

SC

TX

VI

WI

Insurance Department Budgets as Percent of Premium VolumeSelected States

1999

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

California Illinois Massachusetts New Jersey South Carolina Countryw ide

Insurance Industry Shift• Auto Insurance is the primary line of business

– Not subject to same risk of catastrophe– Rating information needs reduced

• More competitive environment• Fire risk controlled

– Building codes– Advances in fire protection

• New catastrophe risks– Hurricane– Earthquake– Flood– Terrorism

Generalization to Other Lines• Rate regulation is not needed for any line of business

with competitive markets and minimal catastrophe risk• Regulation could be beneficial for particular lines that

are not competitive– Title insurance

• Regulation could be beneficial for coverages exposed to catastrophe risk to prevent insolvencies– Hurricanes– Earthquake– Flood– Terrorism

Recent Events - 1• Massachusetts Auto Insurance

– State made rates 1976-2007– File and use for 2008

• Reasons for change– New commissioner – Nonnie Burnes– Restricted market for coverage

• Few companies sell auto insurance• Major national insurers won’t write in Massachusetts• Setting rates under prior system was a lengthy and expensive

process

If you were the Massachusetts insurance commissioner, how would you decide if the new system is working?

A) The percent of policyholders insured through the assigned risk plan reduces.

B) Insurance rate levels decline

C) Loss ratios increase

D) More insurers enter the market in the state

E) All of the above

Recent Events - 2

• Blueprint for a Modernized Financial Regulatory Structure – Released by Treasury Secretary Henry Paulson

on March 31, 2008

– Proposes Federal insurance regulation option

– National Insurance Commissioner

– If insurer opts for a federal charter, it would not be subject to state insurance regulation (some exceptions)

Based on what you know about insurance, the public interest would be best served if what level of government regulated the insurance industry?

A) States

B) Federal

C) Both

D) Each insurer should pick whether it would be regulated by state or federal government

E) Insurance companies should not be regulated