Embed Size (px)

Citation preview

89

4. Introduction

In this chapter mobile payments are presented. What are the applications for which people pay with their mobile phone? And what is the level of trust people have towards a PIN-code when paying with their mobile?

Due to the low penetration (and therefore, low number of observations) of mobile payment in the different European countries, most results are only presented on a European level. Where possible, country specifics are given.

The input for this chapter is from the online study in which 14 countries were questioned.

90

49%

38%

35%

21%

18%

13%

24%

0% 20% 40% 60% 80% 100%

Texting in competition (at premium rate texts)

Purchasing (virtual) tickets (tube, tram, parking...)

Downloading music, ring tones…

Paying bills

Automatic vending machines

Person to person payment

Other

Applications mobile payment

4.1. Mobile payment methods in Europe: ApplicationsWhat are the applications you use mobile payments for? (base=users of mobile payment method last year, N=369)

In Europe, texting in competition is the most popular mobile payment application. About half of the respondents (49%) have used this application during the last year.

Also quite popular are the purchase of (virtual) tickets for the tram, bus or parking (38%) and downloading music or ring tones via mobile (35%).

Less used applications are person to person payment (13%) and automatic vending machines (18%).

91

8

4

3

2

1

3

20

26

27

16

24

18

14

29

27

37

55

43

39

23

24

27

18

22

28

20

4

7

9

9

19

2

3

3

3

1

6

21

30

16

12Texting in competition (N= 181)

Automatic vending machines (N=68)

Purchasing tickets (N=141)

Paying Bills (N=77)

Person to person payment (N=49)

Downloading music, … (N=128)

Other (N=88)

Daily Weekly Monthly Once every three to six months Once a year Less often

4.2. Mobile payment methods in Europe*:Frequency of usage of applications

How often do you use mobile payment solutions? (base=users of mobile payment application)

Applications of mobile payment with the highest frequency of usage on a weekly basis are texting in competition, automatic vending machines and purchasing tickets for tram or bus.

Most of the applications are mostly used on a monthly base.

*due to the low number of observations on a country level per application (N<20), results for mobile payment solutions on a country level are not presented

92

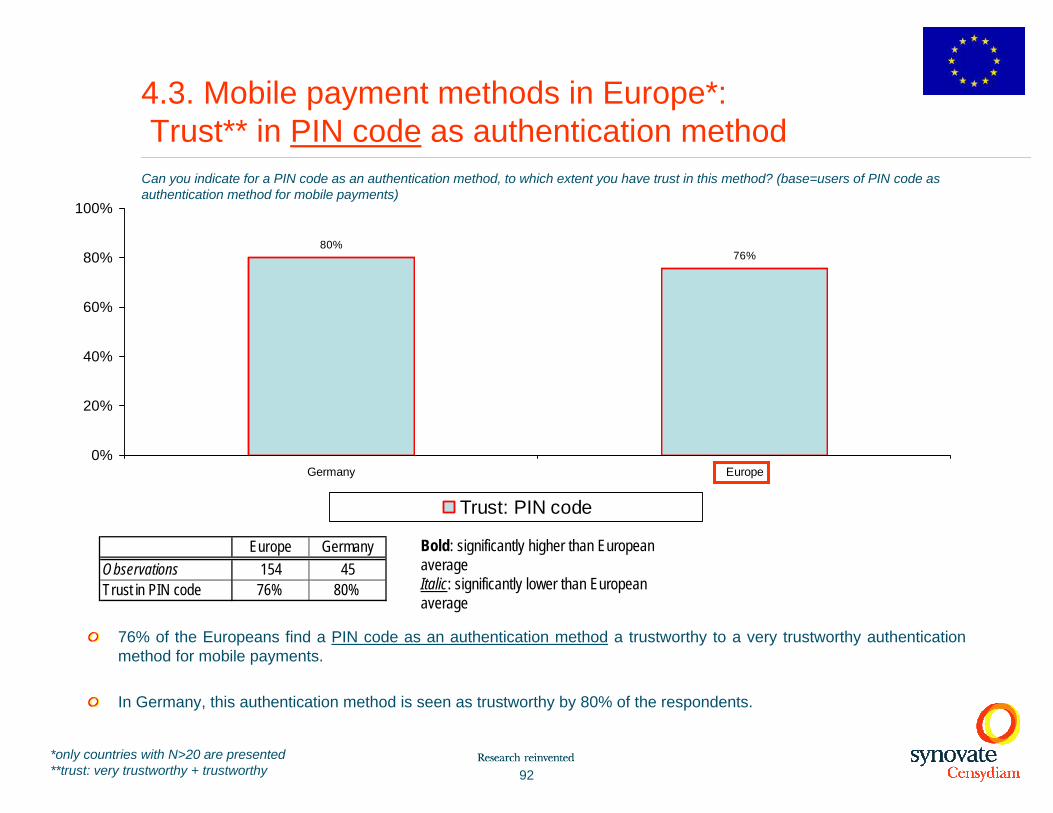

4.3. Mobile payment methods in Europe*:Trust** in PIN code as authentication method

76%80%

0%

20%

40%

60%

80%

100%

EuropeGermany

Trust: PIN code

Bold: significantly higher than European averageItalic: significantly lower than European average

76% of the Europeans find a PIN code as an authentication method a trustworthy to a very trustworthy authentication method for mobile payments.

In Germany, this authentication method is seen as trustworthy by 80% of the respondents.

Can you indicate for a PIN code as an authentication method, to which extent you have trust in this method? (base=users of PIN code as authentication method for mobile payments)

*only countries with N>20 are presented**trust: very trustworthy + trustworthy

Europe GermanyObservations 154 45Trust in PIN code 76% 80%

93

50%

46%

39%

35%

31%

27%

26%

24%

22%

21%

21%

19%

17%

16%

10%

0% 20% 40% 60% 80% 100%

Convenient

For small amounts

User-friendly

For specific applications

Trustworthy

For everyday usage

Technical

Widely spread

Anonymous

Inexpensive

Using the newest technologies

With a wide range of applications

Free of charge

For regular purchases

For larger amounts

Product features mobile payment

4.4. Mobile payment methods in Europe: Product features

Can you indicate for each of these features, if its fits your experience with mobile payment solutions? (base=users of mobile payments solutions in last year, N=369)

Mobile payment solutions are mostly seen as convenient, for small amounts and user friendly. Next to that, they are for specific applications.Mobile payments are not linked with payments of large amounts or for very regular purchases.

94

4.4. Mobile payment methods in Europan countries*: Product features

In most European countries, mobile payment is associated with the same product features. It is seen as a convenient solution and for small amounts. It is definitively not linked with larger amounts and more regular purchases.

Can you indicate for each of these features, if its fits your experience with mobile payment solutions? (base=users of mobile payment solutions in last year)

Top 5

*only countries with N>20 are presented

Europe Sweden Denmark Finland Germany Portugal Austria Italy France Spain Hungary PolandObservations 369 45 25 64 29 31 42 25 20 21 65 59Convenient 50% 56% 72% 50% 41% 52% 60% 24% 50% 52% 82% 51%For small amounts 46% 71% 56% 56% 41% 68% 71% 36% 45% 48% 48% 27%User-friendly 39% 51% 56% 27% 17% 61% 43% 68% 50% 43% 32% 29%For specific applications 35% 29% 44% 72% 31% 35% 38% 36% 25% 38% 26% 36%Trustworthy 31% 9% 28% 23% 31% 26% 38% 44% 15% 19% 45% 41%For everyday usage 27% 29% 32% 17% 21% 48% 33% 16% 5% 24% 32% 44%Technical 26% 29% 24% 14% 31% 19% 26% 24% 15% 24% 40% 29%Widely spread 24% 22% 36% 20% 10% 16% 21% 36% 10% 10% 34% 42%Anonymous 22% 18% 8% 9% 31% 13% 17% 16% 15% 10% 18% 36%Inexpensive 21% 29% 0% 8% 14% 39% 21% 20% 15% 10% 32% 20%Using the newest technologies 21% 24% 20% 31% 14% 26% 17% 24% 15% 29% 25% 15%With a wide range of applications 19% 16% 40% 19% 7% 16% 12% 24% 10% 14% 15% 27%Free of charge 17% 18% 8% 3% 14% 16% 17% 8% 15% 24% 9% 20%For regular purchases 16% 13% 20% 6% 3% 16% 24% 20% 5% 24% 9% 22%For larger amounts 10% 0% 0% 2% 7% 3% 2% 4% 0% 5% 3% 22%

95

Summary: Mobile payments

• Convenient• For small amounts• User-friendly• For specific applications• Trustworthy• Europe: 76%

• Germany: 80%

Top 5 product features mobile payment

Trustworthiness PIN code

• Purchasing tickets for tram or bus.• Automatic vending machines• Texting in competition

Applications weekly plus

96

Content

Section 1: Objectives & Methodology

Section 2: Authentication methods of card payments

Section 3: Authentication methods of online payments

Section 4: Authentication methods of mobile payments

Section 5: Innovative authentication methods and e-environment solutions

Section 6: Conclusions

97

Learnings

Two innovative authentication methods (Biometry, RFID) and one innovative e-environmentapplication (iDTV) were tested on appeal and willingness to use.

– Biometry• Appeal: 65%• Willingness to use: 69%

– RFID• Appeal: 34%• Willingness to use: 29%

– iDTV• Appeal: 26%• Willingness to use: 22%

There are some countries that have a more progressive attitude towards these new concepts, namely: Italy, Poland and Spain. Countries that are more conservative are Finland, Germany and Austria.

98

5. Introduction

In the following section, the focus lies on new and innovative authentication methods for cashless payments. The following applications are presented:

– Biometry: is a user identification method that may allow users to improve payments’security (e.g. fingerprint, eye recognition)

– RFID (Radio Frequency Identification): is a user identification method which uniquely identifies an object or person, when the person passes through places where antennas catch their data by means of a chip that the person wears somewhere on him (her)

Next to that a future e-environment or new interface to the internet was tested, namely:– iDTV: is an application that will allow you to do payments via interactive television

For each of these applications, the appeal and the intention to use will be shown. Results in chapter 5 will be presented on a European (weighted) level. Information on a country level (unweighted) are added in the annex (section E).

The input for this chapter is the online questionnaire among internet payment users in 14 countries.

99

33

11

8

32

23

19

19

23

30

25

28 16

9 7

18

Biometry

RFID

IDTV

Very appealing Appealing Somewhat appealing Not appealing Not appealing at all

5.1. Biometry, RFID and iDTV: AppealTo what extent do you find the following concepts appealing? (base=2880)

In Europe, biometry is seen as the most appealing innovative authentication method. 65% find this concept appealing to very appealing. As for RFID, 43% find this concept not appealing.

The appeal of iDTV is comparable. 44% find this e-environment concept not appealing.

100

16%

24%

15%19%

26%26%

47%45%

24%19%21%

27%28%22%

37%33%34%32%

63%

49%

57%58%59%59%60%60%61%64%66%65%

80%80%86%86%

15%18%25%

25%33%

42%

55%

28%31%

43%

54%

0%

20%

40%

60%

80%

100%

FinlandBelgiumAustriaUKGermanyFranceSwedenNetherlandsHungaryDenmarkEuropePolandPortugalItalySpain

IDTV RFID Biometry

5.1. Biometry, RFID and iDTV: Appeal*

Bold: significantly higher than European average Italic: significantly lower than European average

*appeal: very appealing + appealing

Looking at the different innovative concepts, biometry is seen as the most appealing in all countries. RFID comes in second (except in Hungary, Sweden, Belgium, Portugal and Spain).Countries that find these concepts more appealing that the European average are Spain, Italy, Portugal and Poland. Countries with a more reserved attitude are Finland, Belgium, Austria, the UK and Germany.

To what extent do you find biometry/RFID/iDTV appealing? (base=2880)

Europe Spain Italy Portugal Poland Denmark Hungary Netherlands France Sweden Germany UK Austria Belgium FinlandObservations 2880 213 202 206 211 200 200 203 200 205 211 201 213 216 199Appeal biometry 65% 86% 86% 80% 80% 66% 64% 61% 60% 60% 59% 59% 58% 57% 49%Appeal RFID 34% 54% 63% 32% 43% 33% 31% 37% 28% 22% 27% 28% 21% 19% 24%Appeal IDTV 26% 55% 45% 47% 42% 26% 33% 19% 25% 25% 18% 15% 15% 24% 16%

101

30

9

6

39

20

17

23

38

43

17

20

4

16

15

4Biometry

RFID

IDTV

Would definitely use it Would use it Not sure if I would use it Would not use it Would definitely not use it

5.2. Biometry, RFID and iDTV: Intention to useTo what extent would you be willing to use these methods as user identification system/e-environment application? (base=2880)

Comparing both verification methods (RFID and biometry), biometry gets the highest ratings: 69% would be willing to use biometry.

As for iDTV only 23% would be willing to use this innovative interface for the internet.

102

12%

21%20%

45%

26%

17%

26%

36%32%31%

38%

61%61%63%64%65%66%67%67%69%71%77%77%80%82%82%

16% 16%

39%41%

15%13%

23%24%

22%

35%37%

26% 24% 26% 25%27%29%

36%

48%

0%

20%

40%

60%

80%

100%

NetherlandsFinlandGermanyAustriaUKSwedenBelgiumFranceEuropeHungaryDenmarkSpainPortugalPolandItaly

IDTV RFID Biometry

5.2. Biometry, RFID and iDTV: Intention to use*

Bold: significantly higher than European average Italic: significantly lower than European average

*Intention to use: would definitively use it+ would use it

Biometry is the most popular innovative identification method in Europe. In all countries this concept gets the highest preference in terms of intention to use.

Europe Italy Poland Portugal Spain Denmark Hungary France Belgium Sweden UK Austria Germany Finland NetherlandsObservations 2880 202 211 206 213 200 200 200 216 205 201 213 211 199 203Willingness to use biometry 69% 82% 82% 80% 77% 77% 71% 67% 67% 66% 65% 64% 63% 61% 61%Willingness to use RFID 29% 48% 38% 31% 36% 32% 36% 26% 17% 26% 26% 27% 24% 26% 25%Willingness to use IDTV 22% 37% 41% 45% 35% 20% 39% 21% 24% 23% 13% 15% 16% 16% 12%

To what extent would you be willing to use these methods as user identification system/e-environment application? (base=2880)

103

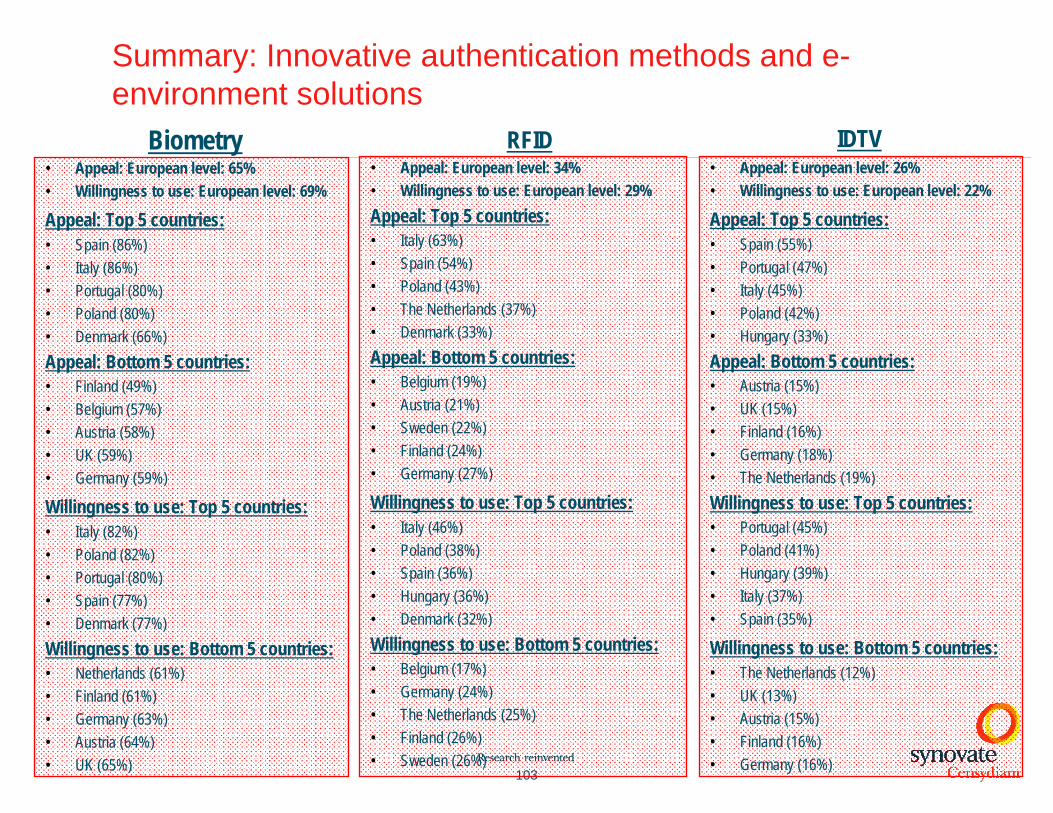

Summary: Innovative authentication methods and e-environment solutions

• Appeal: European level: 65%• Willingness to use: European level: 69%

Appeal: Top 5 countries:• Spain (86%)• Italy (86%)• Portugal (80%)• Poland (80%)• Denmark (66%)Appeal: Bottom 5 countries: • Finland (49%)• Belgium (57%)• Austria (58%)• UK (59%)• Germany (59%)

Willingness to use: Top 5 countries:• Italy (82%)• Poland (82%)• Portugal (80%)• Spain (77%)• Denmark (77%)Willingness to use: Bottom 5 countries: • Netherlands (61%)• Finland (61%)• Germany (63%)• Austria (64%)• UK (65%)

Biometry RFID IDTV• Appeal: European level: 26%• Willingness to use: European level: 22%

Appeal: Top 5 countries:• Spain (55%)• Portugal (47%)• Italy (45%)• Poland (42%)• Hungary (33%)Appeal: Bottom 5 countries: • Austria (15%)• UK (15%)• Finland (16%)• Germany (18%)• The Netherlands (19%)Willingness to use: Top 5 countries: • Portugal (45%)• Poland (41%)• Hungary (39%)• Italy (37%)• Spain (35%)

Willingness to use: Bottom 5 countries:• The Netherlands (12%)• UK (13%)• Austria (15%)• Finland (16%)• Germany (16%)

• Appeal: European level: 34%• Willingness to use: European level: 29%Appeal: Top 5 countries: • Italy (63%)• Spain (54%)• Poland (43%) • The Netherlands (37%)• Denmark (33%)Appeal: Bottom 5 countries: • Belgium (19%)• Austria (21%)• Sweden (22%)• Finland (24%)• Germany (27%)

Willingness to use: Top 5 countries:• Italy (46%)• Poland (38%)• Spain (36%)• Hungary (36%)• Denmark (32%)Willingness to use: Bottom 5 countries: • Belgium (17%)• Germany (24%)• The Netherlands (25%)• Finland (26%)• Sweden (26%)

Study on user identification methods in card payments, e-payment and mobile payments

Final study - Work Package 2Annex

105

Content

Section A: Ideal payment solution

Section B: Awareness and usage of different payment methods

Section C: Country results: Authentication methods of card payments

Section D: Country results: Authentication methods of online payments

Section E: Country results: Innovative authentication methods and

e-environment solutions

106

Learnings

The ideal payment solution should answer generic consumer’s needs: – People are looking for a practical and safe way to handle their money in daily life.– People need an uncomplicated and straightforward payment method that they can trust.– People want a comprehensible and dependable payment method which can be used every day.=> The ideal payment solution should be able to generate a sense of trust and security in every day

life, and is a reliable and straightforward application which is accessible for everyone.

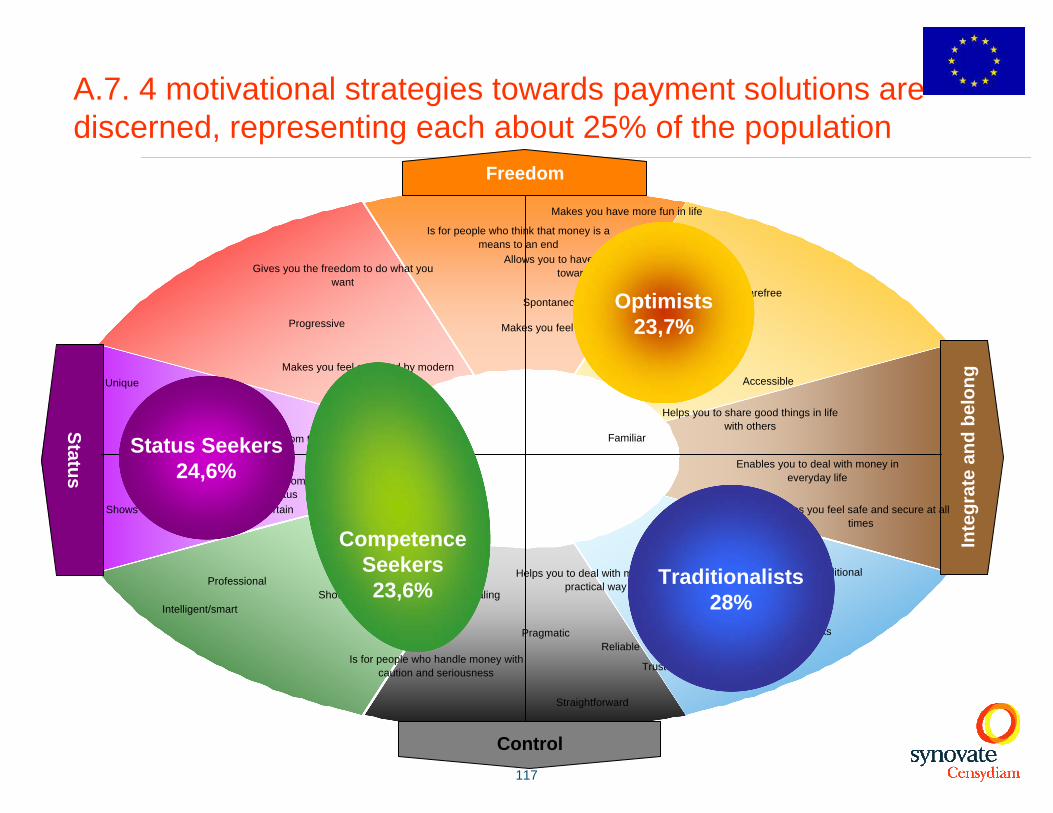

But people can also have specific expectations towards their ideal payment solution. Four different types of motivations towards payment solutions are discerned in the segmentation framework:

Freedom

Status Integrate and belong

Control

Status Seekers24,6%

Optimists23,7%

Traditionalists28%

Competence Seekers23,6%

107

A. Introduction

People can have different expectations towards their payment solutions. In this chapter the different needs and expectations towards ideal payment solutions are presented in a motivational segmentation.

Respondents were asked to describe their ideal payment solution in terms of:– Satisfaction statements– Personality statements– Product features

Personality and satisfaction statements are based on the Censydiam model.

Via clustering techniques, basic structures in the data are revealed. Based on this input, respondents were allocated to different motivational segments. Results of the qualitative phase and the quantitative study have been integrated.

108

Gives you the freedom to do what you want

Makes you feel on top of the world

Shows that you have acquired a certain position in life

Gives a sense of competence and status

Shows that you are capable of dealing with money

Makes you stand out from the crowd

Is for people who handle money with caution and seriousness

Helps you to deal with money in a practical way

Makes you feel safe and secure at all times

Helps you avoid taking risks

Enables you to deal with money in everyday life

Makes you feel accepted by modern society

Is for people who think that money is a means to an end

Helps you to share good things in life with others

Makes you have more fun in life

Allows you to have a carefree attitude towards money

Progressive

Spontaneous

Prestigious

Professional

Intelligent/smart

Unique

Pragmatic

Straightforward

Trustworthy

Reliable

Familiar

Traditional

SocialFriendly

Accessible

Carefree

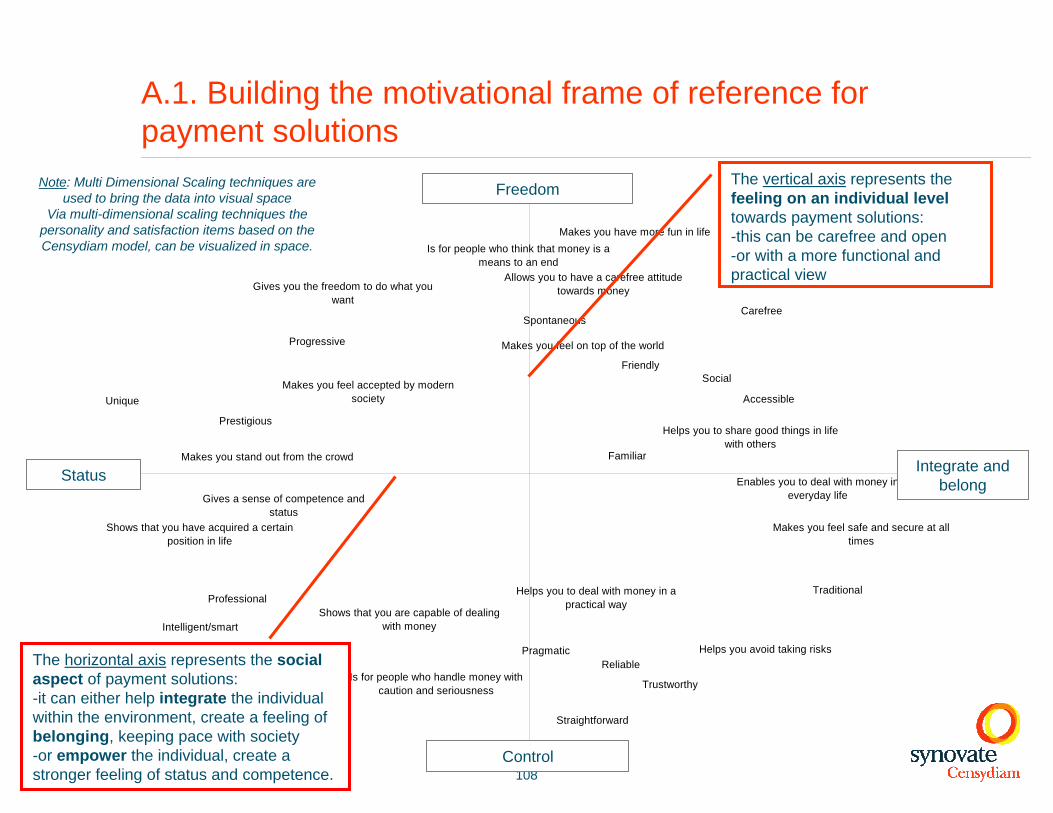

A.1. Building the motivational frame of reference for payment solutions

Freedom

Status Integrate and belong

Control

The vertical axis represents the feeling on an individual level towards payment solutions:-this can be carefree and open-or with a more functional and practical view

The horizontal axis represents the social aspect of payment solutions: -it can either help integrate the individual within the environment, create a feeling of belonging, keeping pace with society-or empower the individual, create a stronger feeling of status and competence.

Note: Multi Dimensional Scaling techniques are used to bring the data into visual space

Via multi-dimensional scaling techniques the personality and satisfaction items based on the Censydiam model, can be visualized in space.

109

Control

Status

Freedom

Inte

grat

e an

d be

long

Gives you the freedom to do what you want

Makes you feel on top of the world

Shows that you have acquired a certain position in life

Gives a sense of competence and status

Shows that you are capable of dealing with money

Makes you stand out from the crowd

Is for people who handle money with caution and seriousness

Helps you to deal with money in a practical way

Makes you feel safe and secure at all times

Helps you avoid taking risks

Enables you to deal with money in everyday life

Makes you feel accepted by modern society

Is for people who think that money is a means to an end

Helps you to share good things in life with others

Makes you have more fun in life

Allows you to have a carefree attitude towards money

Progressive

Spontaneous

Prestigious

Professional

Intelligent/smart

Unique

Pragmatic

Straightforward

Trustworthy

Reliable

Familiar

Traditional

SocialFriendly

Accessible

Carefree

The motivational frame of reference for payment solutions

110

A.2. Ideal satisfaction of payment solutionsPeople are looking for a practical and safe way to handle their money in daily life.

56%

55%

44%

42%

35%

32%

29%

24%

19%

18%

17%

16%

16%

15%

12%

8%

Enables you to deal with money in everyday life

Helps you to deal with money in a practical way

Gives you the freedom to do what you want

Makes you feel safe and secure at all times

Helps you avoid taking risks

Is for people who handle money with caution and seriousness

Shows that you are capable of dealing with money

Allows you to have a carefree attitude towards money

Makes you have more fun in life

Helps you to share good things in life with others

Makes you feel accepted by modern society

Is for people who think that money is a means to an end

Makes you feel on top of the world

Gives a sense of competence and status

Shows that you have acquired a certain position in life

Makes you stand out from the crowd

Can you indicate which feelings and emotions you IDEALLY look for in a payment method? You can mark a number from 1 to 7 where 1 means “Doesn’t fit at all” and 7 “fits perfectly”. (Top 6,7)

Total sample

Important• Dealing with money in a practical

way, in every day life • Gives you freedom• Gives you safety and security, with

low risk

Less important• Money as a means to an end• Feeling on top of the world• Source of status and distinction

Top 5

Bottom 5

111

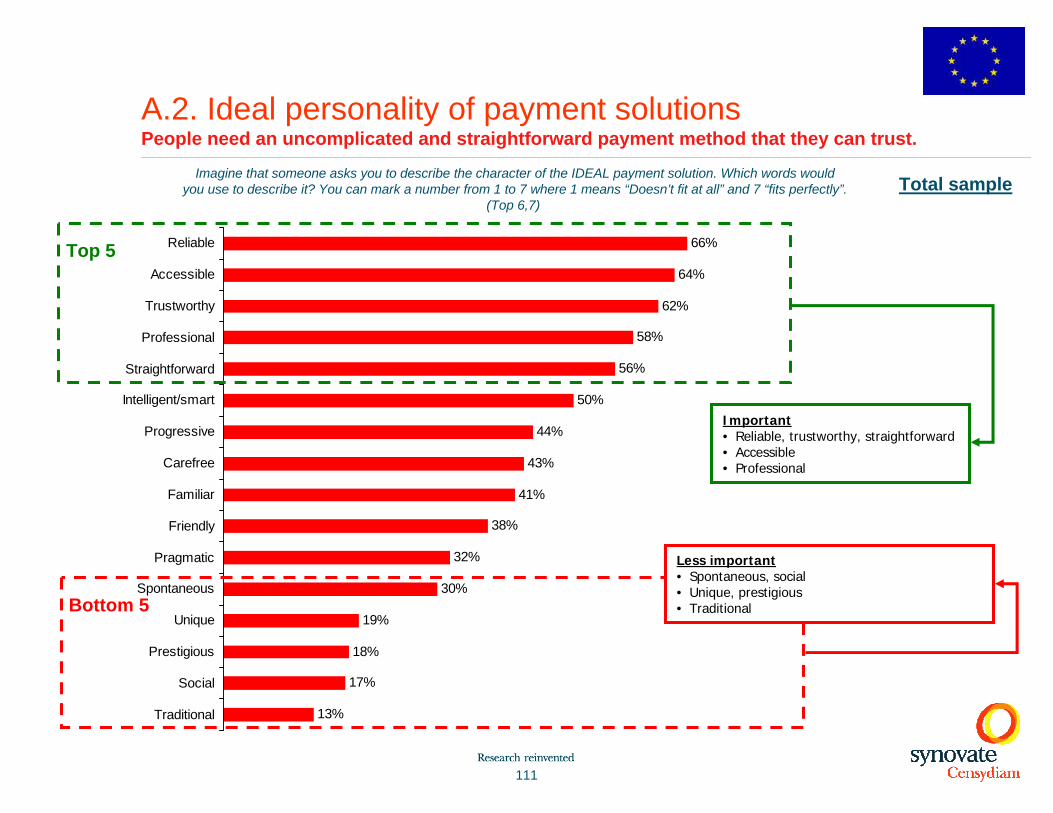

A.2. Ideal personality of payment solutionsPeople need an uncomplicated and straightforward payment method that they can trust.

66%

64%

62%

58%

56%

50%

44%

43%

41%

38%

32%

30%

19%

18%

17%

13%

Reliable

Accessible

Trustworthy

Professional

Straightforward

Intelligent/smart

Progressive

Carefree

Familiar

Friendly

Pragmatic

Spontaneous

Unique

Prestigious

Social

Traditional

Imagine that someone asks you to describe the character of the IDEAL payment solution. Which words would you use to describe it? You can mark a number from 1 to 7 where 1 means “Doesn’t fit at all” and 7 “fits perfectly”.

(Top 6,7)Total sample

Important• Reliable, trustworthy, straightforward• Accessible• Professional

Less important• Spontaneous, social• Unique, prestigious• Traditional

Top 5

Bottom 5

112

A.2. Ideal product features of payment solutionsPeople want a comprehensible and dependable payment method which can be used every day.

75%

74%

72%

71%

64%

64%

63%

63%

61%

61%

60%

59%

52%

43%

43%

41%

35%

34%

30%

Convenient

User-friendly

For everyday usage

Dependable

Free of charge

For regular purchases

With a PIN code

Helps to monitor my finances/account

Respects your privacy

Inexpensive

With a wide range of applications

Widely spread

Using the newest technologies

For larger amounts

For small amounts

Anonymous

With a signature

Technical

For specific applications

How would each of the following qualities describe your ideal payment solution? You can mark a number from 1 to 7 where 1 means “Doesn’t fit at all” and 7 “fits perfectly”. (Top 6,7)

Total sample

Important• Convenient, user-friendly• Dependable• For every day usage• Free of charge

Less important• For small amounts, specific applications• Anonymous• With a signature• Technical

Top 5

Bottom 5

113

Control

Status

Freedom

Inte

grat

e an

d be

long

Gives you the freedom to do what you want

Makes you feel on top of the world

Shows that you have acquired a certain position in life

Gives a sense of competence and status

Shows that you are capable of dealing with money

Makes you stand out from the crowd

Is for people who handle money with caution and seriousness

Helps you to deal with money in a practical way

Makes you feel safe and secure at all times

Helps you avoid taking risks

Enables you to deal with money in everyday life

Makes you feel accepted by modern society

Is for people who think that money is a means to an end

Helps you to share good things in life with others

Makes you have more fun in life

Allows you to have a carefree attitude towards money

Progressive

Spontaneous

Prestigious

Professional

Intelligent/smart

Unique

Pragmatic

Straightforward

Trustworthy

Reliable

Familiar

Traditional

SocialFriendly

Accessible

Carefree

A.3. Fundamental meaning of payment solutionsThe ideal payment solution is able to generate a sense of trust and security in every day life. It is a reliable and straightforward application which is accessible for everyone.

Top 5 satisfactions and personalities

114

In the qualitative phase 4 motivational groups towards cashless payment solutions were discerned:

– Trendsetters: impulsive achievers who want to master new technologies and be on top of the modern world

– Upgraders: ambitious individuals who want to excel and stand out from the crowd

– Traditionalists: anxious people who want to be in control over their finances and who find cashless payment a source of frustration and self-doubt

– Optimists: curious people who are optimistic about the world and like to consult other people about payment methods

A.4. Different motivations towards cashless payment solutions identified in the qualitative phase

Freedom

No limits

Control

Status

PrivilegeIntegrate and

belong

Cashless payments =Convenience,

efficiency, the new ‘norm’

Need for self-reliance, less

‘shared’ experiences

Freedom

No limits

Control

Status

PrivilegeIntegrate and

belong

Cashless payments =Convenience,

efficiency, the new ‘norm’

Need for self-reliance, less

‘shared’ experiences Traditionalists

Trendsetters

Upgraders

Optimists

Figure based on qualitative report

115

A.5. Different motivations towards cashless payment solutions identified in the quantitative phase

In the qualitative study, 4 motivational groups towards cashless were presented. The quantitative research confirms 4 different motivations (towards payment in general), however there are some differences between the groups.

The link with the qualitative motivational groups is shown hereunder:

Qualitative output Quantitative output

-Trendsetters

-Upgraders

-Traditionalists

-Optimists

-Competence Seekers

-Status Seekers

-Traditionalists

-Optimists

116

Giv

es y

ou th

e fre

edom

to d

o w

hat y

ou w

ant

Mak

es y

ou fe

el o

n to

p of

the

wor

ld

Sho

ws

that

you

hav

e ac

quire

d a

certa

in p

ositi

on in

life

Giv

es a

sen

se o

f com

pete

nce

and

stat

us

Sho

ws

that

you

are

cap

able

of d

ealin

g w

ith m

oney

Mak

es y

ou s

tand

out

from

the

crow

d

Is fo

r peo

ple

who

han

dle

mon

ey w

ith c

autio

n an

d se

rious

ness

Hel

ps y

ou to

dea

l with

mon

ey in

a p

ract

ical

way

Mak

es y

ou fe

el s

afe

and

secu

re a

t all

times

Hel

ps y

ou a

void

taki

ng ri

sks

Ena

bles

you

to d

eal w

ith m

oney

in e

very

day

life

Mak

es y

ou fe

el a

ccep

ted

by m

oder

n so

ciet

y

Is fo

r peo

ple

who

thin

k th

at m

oney

is a

mea

ns to

an

end

Hel

ps y

ou to

sha

re g

ood

thin

gs in

life

with

oth

ers

Mak

es y

ou h

ave

mor

e fu

n in

life

Allo

ws

you

to h

ave

a ca

refre

e at

titud

e to

war

ds m

oney

Pro

gres

sive

Spo

ntan

eous

Pre

stig

ious

Pro

fess

iona

l

Inte

llige

nt/s

mar

t

Uni

que

Pra

gmat

ic

Stra

ight

forw

ard

Trus

twor

thy

Rel

iabl

e

Fam

iliar

Trad

ition

al

Soc

ial

Frie

ndly

Acc

essi

ble

Car

efre

e

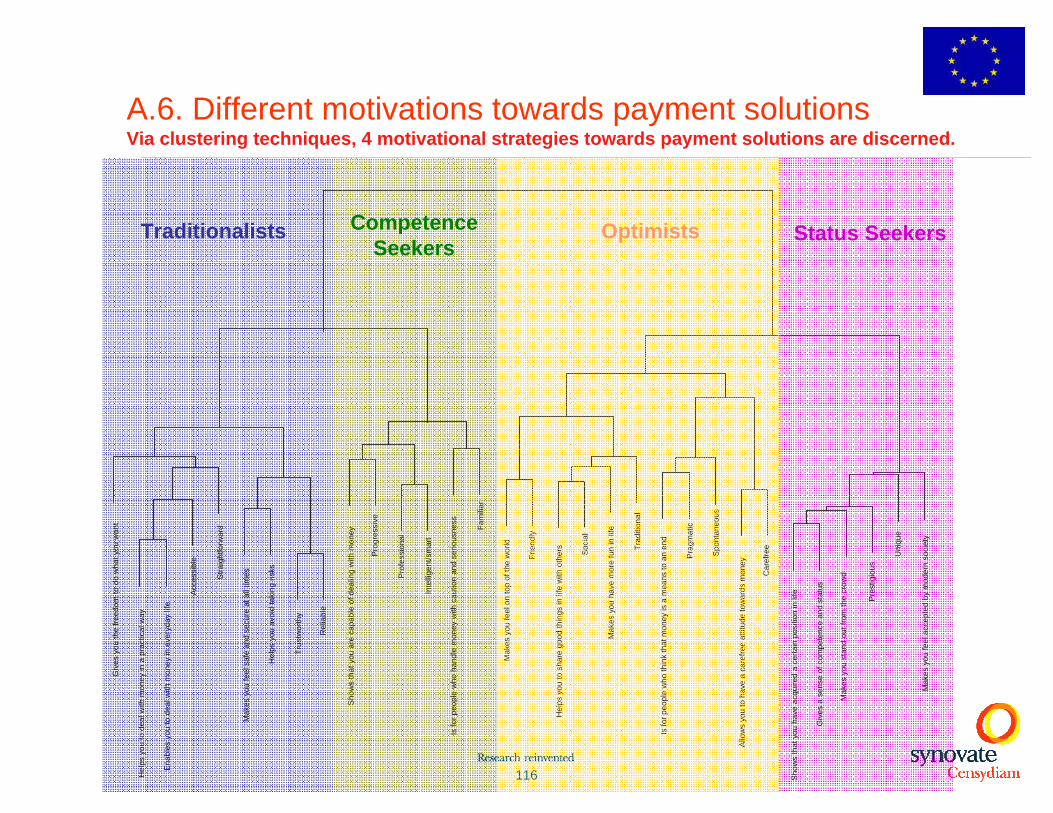

A.6. Different motivations towards payment solutionsVia clustering techniques, 4 motivational strategies towards payment solutions are discerned.

Traditionalists CompetenceSeekers

Optimists Status Seekers

117

Control

Status

Freedom

Inte

grat

e an

d be

long

Gives you the freedom to do what you want

Makes you feel on top of the world

Shows that you have acquired a certain position in life

Gives a sense of competence and status

Shows that you are capable of dealing with money

Makes you stand out from the crowd

Is for people who handle money with caution and seriousness

Helps you to deal with money in a practical way

Makes you feel safe and secure at all times

Helps you avoid taking risks

Enables you to deal with money in everyday life

Makes you feel accepted by modern society

Is for people who think that money is a means to an end

Helps you to share good things in life with others

Makes you have more fun in life

Allows you to have a carefree attitude towards money

Progressive

Spontaneous

Prestigious

Professional

Intelligent/smart

Unique

Pragmatic

Straightforward

Trustworthy

Reliable

Familiar

Traditional

SocialFriendly

Accessible

Carefree

A.7. 4 motivational strategies towards payment solutions are discerned, representing each about 25% of the population

Status Seekers24,6%

Optimists23,7%

Traditionalists28%

Competence Seekers23,6%

118

Expectations towards payment solutions

Socio-demographical profile Product features

Core (top %)

Differentiating only

Differentiating only

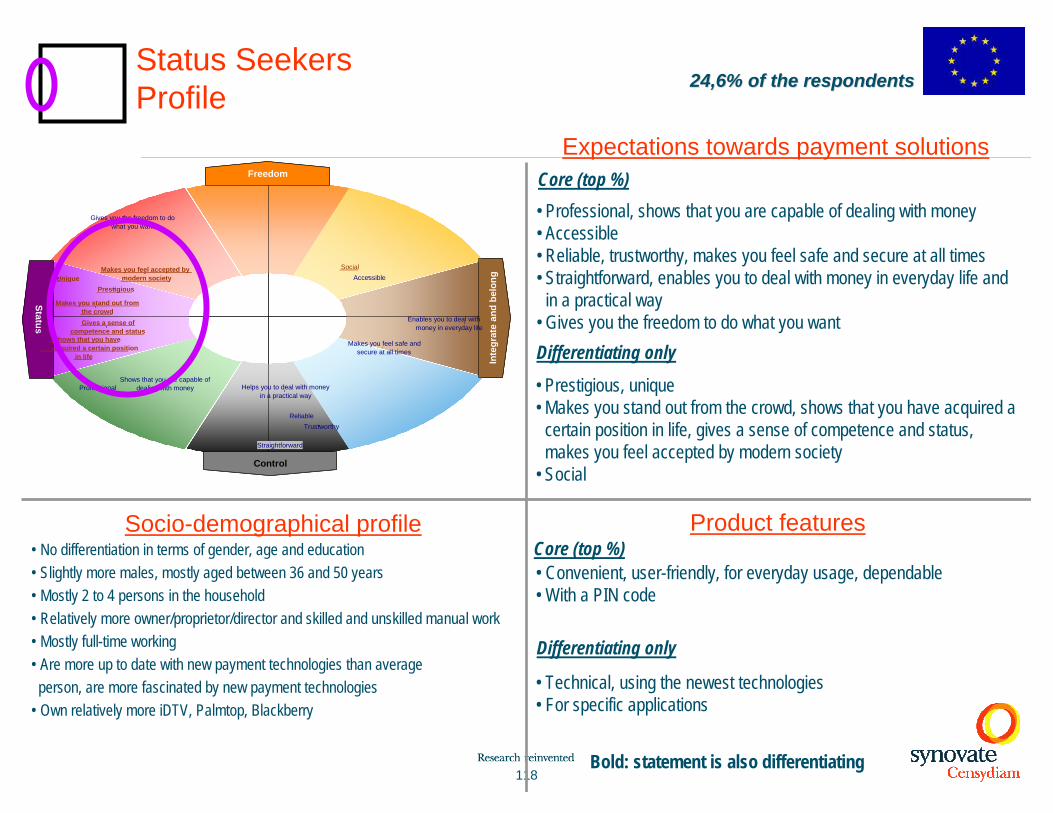

• No differentiation in terms of gender, age and education• Slightly more males, mostly aged between 36 and 50 years• Mostly 2 to 4 persons in the household• Relatively more owner/proprietor/director and skilled and unskilled manual work• Mostly full-time working• Are more up to date with new payment technologies than average

person, are more fascinated by new payment technologies• Own relatively more iDTV, Palmtop, Blackberry

Core (top %)

Bold: statement is also differentiating

24,6% of the respondents24,6% of the respondents

Control

Status

Freedom

Inte

grat

e an

d be

long

Control

Status

Freedom

Inte

grat

e an

d be

long

PrestigiousUnique

Makes you stand out from the crowd

Shows that you have acquired a certain position

in life

Gives a sense of competence and status

Makes you feel accepted by modern society

Social

ProfessionalShows that you are capable of

dealing with money

Accessible

ReliableTrustworthy

Straightforward

Enables you to deal with money in everyday life

Helps you to deal with money in a practical way

Gives you the freedom to do what you want

Makes you feel safe and secure at all times

Status Seekers Profile

• Prestigious, unique• Makes you stand out from the crowd, shows that you have acquired a

certain position in life, gives a sense of competence and status, makes you feel accepted by modern society

• Social

• Professional, shows that you are capable of dealing with money• Accessible• Reliable, trustworthy, makes you feel safe and secure at all times• Straightforward, enables you to deal with money in everyday life and

in a practical way• Gives you the freedom to do what you want

• Convenient, user-friendly, for everyday usage, dependable• With a PIN code

• Technical, using the newest technologies• For specific applications

119

•They want payment solutions that make them stand out from the crowd and make them unique. It is also about showing success in life. In that respect payment solutions can be seen as a status symbol.

•They are looking for financial freedom to be able to do what they want and as a way to be on top of the modern world.

•They see themselves as professional and successful, willing to openly embrace new technology and to be an active participant in the modern world.

•They talk about their own behavior as if having an almost ‘innate’ aptitude to relate to new payments methods, fully embracing and accepting newtechnologies in a natural way.

•They expect a hassle free, practical and user-friendly financial experience. Next to that, they are not afraid of atechnical solution that uses the newest technologies.

*Integration of qualitative and quantitative results

Status SeekersSummary

24,6% of the respondents24,6% of the respondents

120Control

Status

Freedom

Inte

grat

e an

d be

long

Status Seekers Attributes

Blue = top 5

Blue underlined = top 5 & differentiating

Brown underlined = only differentiating

Bold =Strongly differentiating

PrestigiousUnique

Makes you stand out from the crowd

Shows that you have acquired a certain position

in life

Gives a sense of competence and status

Makes you feel accepted by modern society

Social

ProfessionalShows that you are capable of

dealing with money

Accessible

ReliableTrustworthy

Straightforward

Enables you to deal with money in everyday life

Helps you to deal with money in a practical way

Gives you the freedom to do what you want

Makes you feel safe and secure at all times

121

Status SeekersExpectations towards payment solutions

7737Makes you feel safe and secure at all times

8544Gives you the freedom to do what you want

7952Helps you to deal with money in a practical way

8254Enables you to deal with money in everyday life

9153Straightforward

9058Trustworthy

8458Reliable

9060AccessibleTraditionalists

10535Shows that you are capable of dealing with money

9659ProfessionalCompetence

12320SocialOptimists

18434Makes you feel accepted by modern society

19530Gives a sense of competence and status

22626Shows that you have acquired a certain position in life

25017Makes you stand out from the crowd

17832Unique

21635PrestigiousStatus

Index %Expression of basic motivational drivers Motivational Strategy

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

122

Status SeekersProduct features payment solutions

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

11561Using the newest technologies

12542Technical

12738For specific applications

10466With a PIN code

9267Dependable

9469For everyday usage

9672User-friendly

9775Convenient

Index%

123

Status SeekersSocio-demographical profile

Index>110Index<90

124

Expectations towards payment solutions

Socio-demographical profile Product features

Core (top %)

Differentiating only

Differentiating only

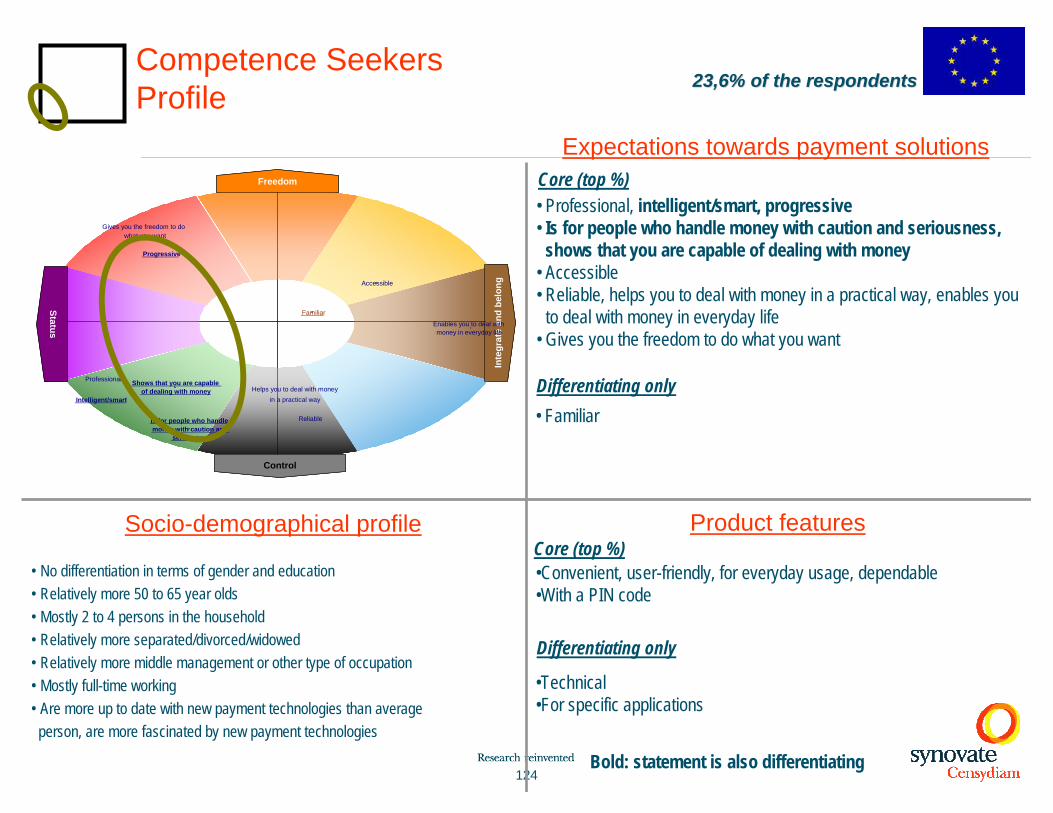

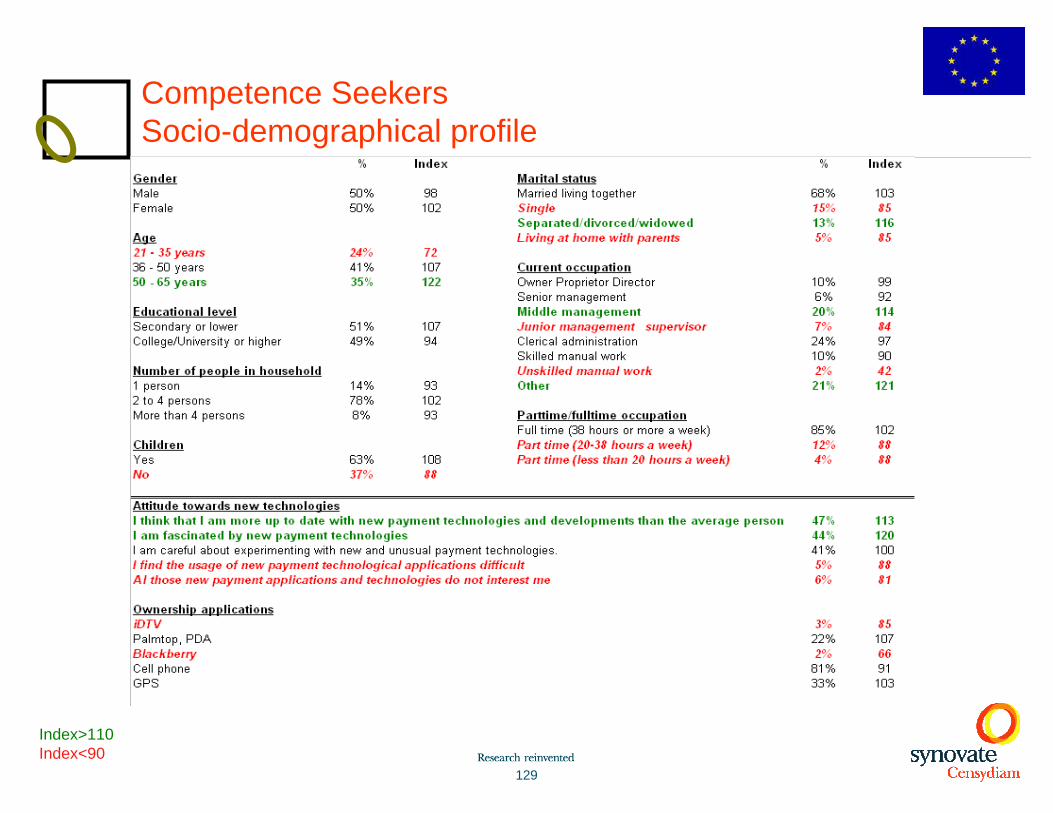

• No differentiation in terms of gender and education• Relatively more 50 to 65 year olds• Mostly 2 to 4 persons in the household • Relatively more separated/divorced/widowed• Relatively more middle management or other type of occupation• Mostly full-time working• Are more up to date with new payment technologies than average

person, are more fascinated by new payment technologies

Core (top %)

Bold: statement is also differentiating

23,6% of the respondents23,6% of the respondentsCompetence Seekers Profile

• Familiar

• Professional, intelligent/smart, progressive• Is for people who handle money with caution and seriousness,

shows that you are capable of dealing with money• Accessible• Reliable, helps you to deal with money in a practical way, enables you

to deal with money in everyday life• Gives you the freedom to do what you want

•Convenient, user-friendly, for everyday usage, dependable•With a PIN code

•Technical•For specific applications

Control

Status

Freedom

Inte

grat

e an

d be

long

Control

Status

Freedom

Inte

grat

e an

d be

long

Professional

Intelligent/smart

Progressive

Is for people who handle money with caution and

seriousness

Shows that you are capable of dealing with money

Familiar

Reliable

Accessible

Helps you to deal with money in a practical way

Enables you to deal with money in everyday life

Gives you the freedom to do what you want

125

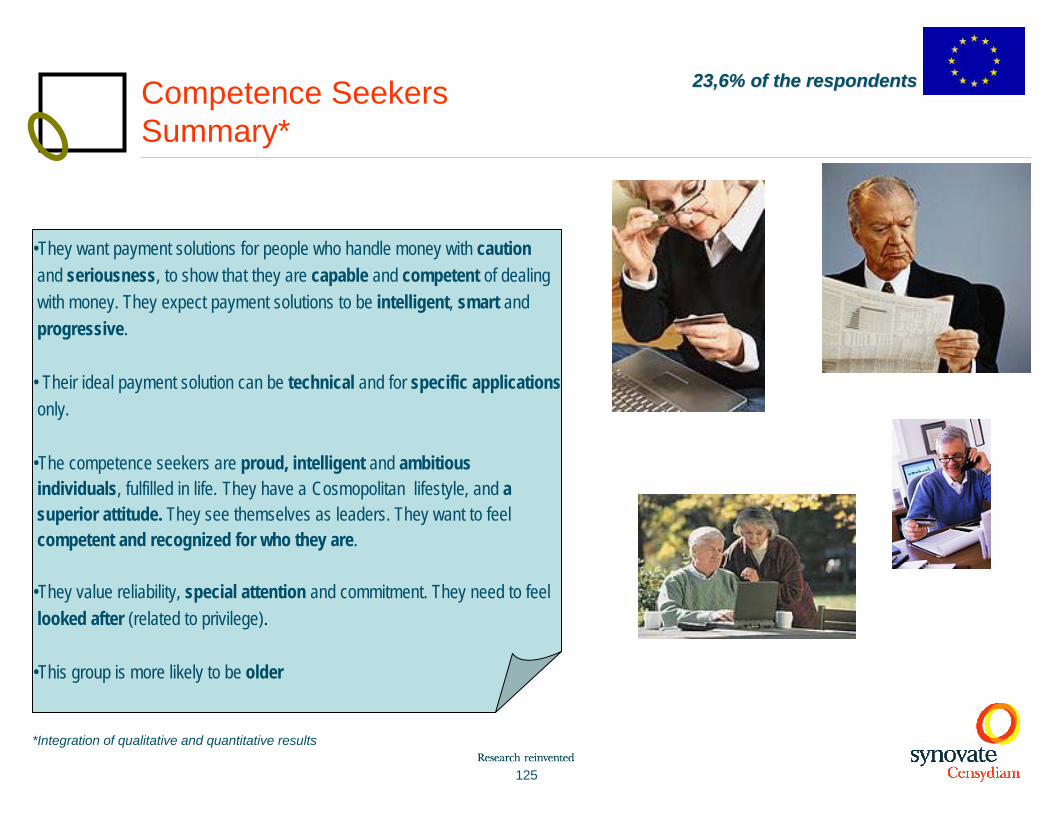

•They want payment solutions for people who handle money with cautionand seriousness, to show that they are capable and competent of dealingwith money. They expect payment solutions to be intelligent, smart and progressive.

• Their ideal payment solution can be technical and for specific applicationsonly.

•The competence seekers are proud, intelligent and ambitiousindividuals, fulfilled in life. They have a Cosmopolitan lifestyle, and a superior attitude. They see themselves as leaders. They want to feel competent and recognized for who they are.

•They value reliability, special attention and commitment. They need to feellooked after (related to privilege).

•This group is more likely to be older

*Integration of qualitative and quantitative results

Competence SeekersSummary*

23,6% of the respondents23,6% of the respondents

126

Control

Status

Freedom

Inte

grat

e an

d be

long

Blue = top 5

Blue underlined = top 5 & differentiating

Brown underlined = only differentiating

Bold =Strongly differentiating

Competence Seekers Attributes

Professional

Intelligent/smart

Progressive

Is for people who handle money with caution and

seriousness

Shows that you are capable of dealing with money

Familiar

Reliable

Accessible

Helps you to deal with money in a practical way

Enables you to deal with money in everyday life

Gives you the freedom to do what you want

127

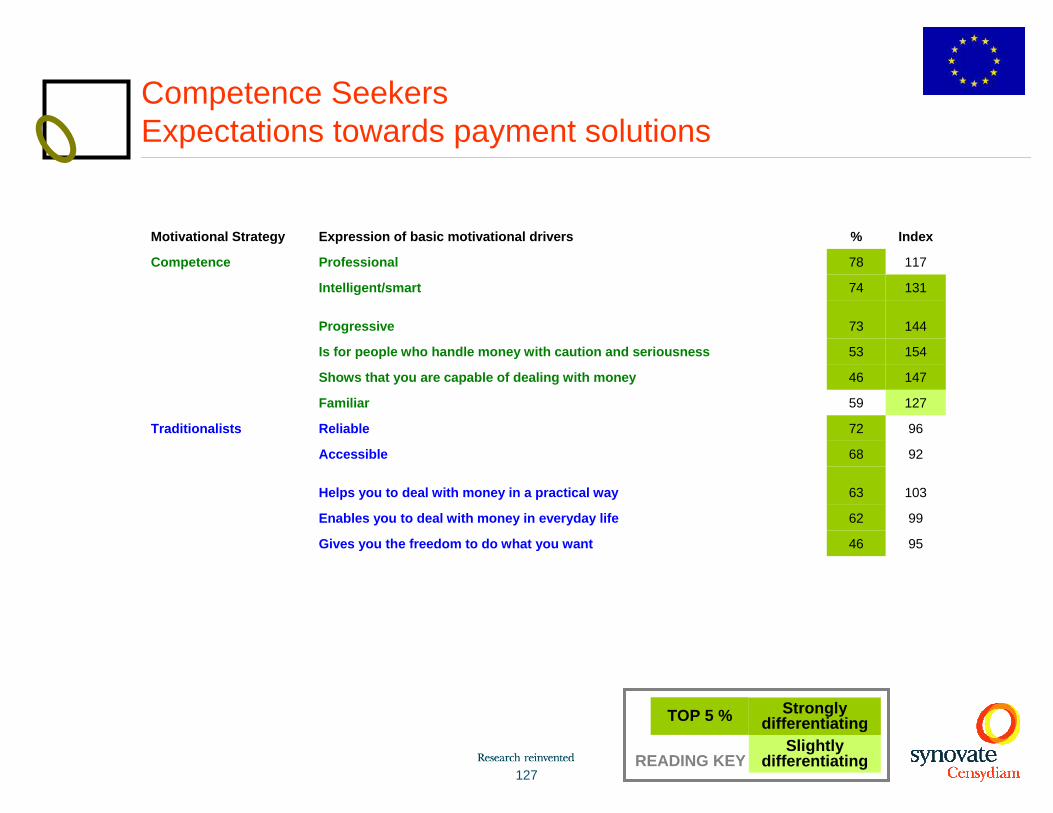

Competence SeekersExpectations towards payment solutions

9546Gives you the freedom to do what you want

9962Enables you to deal with money in everyday life

10363Helps you to deal with money in a practical way

9268Accessible

9672ReliableTraditionalists

12759Familiar

14746Shows that you are capable of dealing with money

15453Is for people who handle money with caution and seriousness

14473Progressive

13174Intelligent/smart

11778ProfessionalCompetence

Index %Expression of basic motivational drivers Motivational Strategy

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

128

Competence SeekersProduct features of payment solutions

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

11138For specific applications

11243Technical

10475With a PIN code

9679Dependable

10184For everyday usage

9985User-friendly

9987Convenient

Index%

129

Competence SeekersSocio-demographical profile

Index>110Index<90

130

Control

Status

Freedom

Inte

grat

e an

d be

long

Control

Status

Freedom

Inte

grat

e an

d be

long

Reliable

Accessible

Trustworthy

Straightforward

Helps you to deal with money in a practical way

Enables you to deal with money in everyday life

Makes you feel safe and secure at all times

Gives you the freedom to do what you want

Helps you avoid taking risks

Carefree

Professional

Expectations towards payment solutions

Socio-demographical profile Product features

Core (top %)

Differentiating only

Differentiating only

• Relatively more 21 to 35 year olds, college or university degree• Slightly more females• Relatively more living at home with parents• Relatively more senior or junior management or clerical administration• Mostly working full-time

Core (top %)

Bold: statement is also differentiating

28% of the respondents28% of the respondentsTraditionalists Profile

• Carefree

• Reliable, trustworthy, straightforward• Helps you to deal with money in a practical way and in everyday

life• Helps you avoid taking risks • Makes you feel safe and secure at all times• Accessible• Gives you the freedom to do what you want• Professional

•Convenient, user-friendly, for everyday usage, dependable•Free of charge

•Respects your privacy

131

•The traditionalists need payment solutions that are reliable and trustworthy and that help them deal with money in a practical way and in everyday life.

•Next to that, there is a strong need for control over their finances.

•They are very security minded and so look for payment solutions that reduce this risk and make them feel safe at all times.

•They see themselves as normal people who don’t wish to make a show of themselves.

•The traditionalists are looking for payment solutions that respecttheir privacy.

•The traditionalists are more likely younger people with a higher education.

*Integration of qualitative and quantitative results

TraditionalistsSummary*

28% of the respondents28% of the respondents

132

Control

Status

Freedom

Inte

grat

e an

d be

long

Reliable

Accessible

Trustworthy

Straightforward

Helps you to deal with money in a practical way

Enables you to deal with money in everyday life

Makes you feel safe and secure at all times

Gives you the freedom to do what you want

Helps you avoid taking risks

Carefree

Professional

Traditionalists Attributes

133

TraditionalistsExpectations towards payment solutions

9965ProfessionalCompetence

12458CarefreeOptimists

14255Helps you avoid taking risks

11557Gives you the freedom to do what you want

13261Makes you feel safe and secure at all times

12679Enables you to deal with money in everyday life

13283Helps you to deal with money in a practical way

12275Straightforward

12586Trustworthy

12489Accessible

12290ReliableTraditionalists

Index %Expression of basic motivational drivers Motivational Strategy

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

134

TraditionalistsProduct features of payment solutions

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

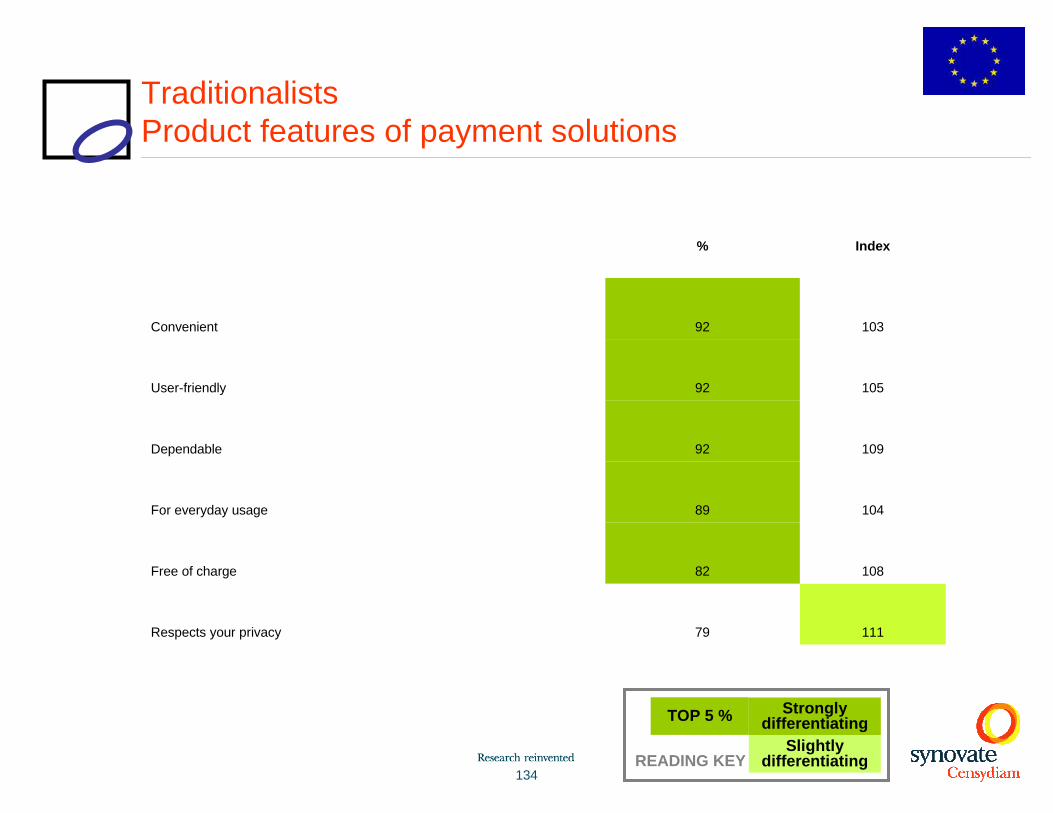

11179Respects your privacy

10882Free of charge

10489For everyday usage

10992Dependable

10592User-friendly

10392Convenient

Index%

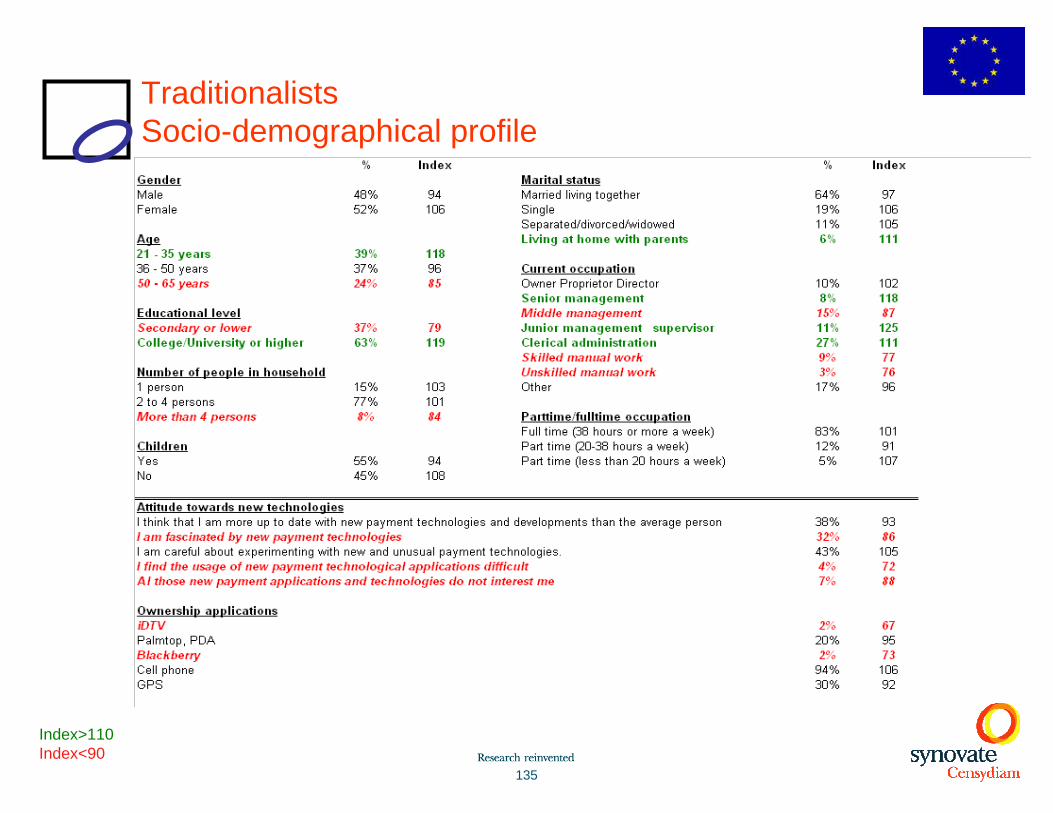

135

TraditionalistsSocio-demographical profile

Index>110Index<90

136

Control

Status

Freedom

Inte

grat

e an

d be

long

Control

Status

Freedom

Inte

grat

e an

d be

long

Carefree

Allows you to have a carefree attitude towards

money

Traditional

Social

Spontaneous

Pragmatic

Is for people who think that money is a means to an

end

Makes you feel on top of the world

Helps you to share good things in life with others

Makes you have more fun in life

Reliable

Accessible

Trustworthy

Straightforward

Enables you to deal with money in everyday life

Gives you the freedom to do what you want

Helps you to deal with money in a practical way

Makes you feel safe and secure at all times

Expectations towards payment solutions

Socio-demographical profile Product features

Core (top %)

Differentiating only

• Relatively more 21 to 35 years, secondary education or lower• Relatively more 1 or more than 4 persons in household• Relatively more singles• Relatively more skilled and unskilled manual work• Relatively more part-time working• More not interested by new payment applications and

technologies, and the usage of these new payment applications difficult

• Relatively more iDTV

Core (top %)

Bold: statement is also differentiating

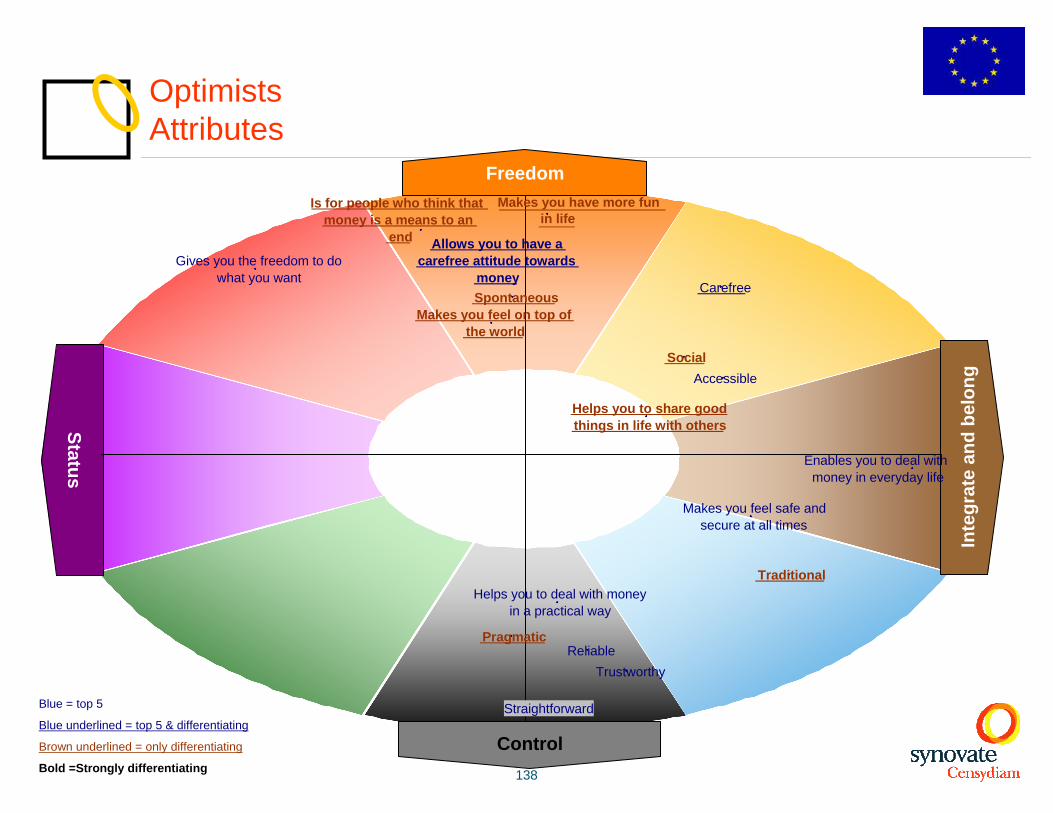

23,7% of the respondents23,7% of the respondentsOptimistsProfile

• Traditional, pragmatic• Social, spontaneous• Is for people who think that money is a means to an end• Makes you feel on top of the world• Helps you to share good things in life with others, makes you have

more fun in life

• Carefree, allows you to have a carefree attitude towards money• Reliable, trustworthy, straightforward• Enables you to deal with money in everyday life and in a practical way• Gives you the freedom to do what you want• Makes you feel safe and secure at all times• Accessible

•Convenient, user-friendly, for everyday usage, dependable•Free of charge

137

•The optimists need payment solutions that enable them to have a carefree attitude towards money. Money is seen as a means to an end: it enables one to share goodthings in life with others and make life more pleasurable.

•They have no ambition to experiment or to be seen as innovators. They are not really interested in new payment applications and technologies. They also findthese new applications difficult.

•The optimists are social, warm and open-minded people with a positive attitude towards the future.

•They need payment solutions that can make them deal with money in everyday life and in a practical, user-friendly. It should also give them the freedom to do what they want. It should also respect their privacy.

•This group is relatively more part-time working and relatively more single and young.

*Integration of qualitative and quantitative results

OptimistsSummary*

23,7% of the respondents23,7% of the respondents

138

Control

Status

Freedom

Inte

grat

e an

d be

long

OptimistsAttributes

Blue = top 5

Blue underlined = top 5 & differentiating

Brown underlined = only differentiating

Bold =Strongly differentiating

Carefree

Allows you to have a carefree attitude towards

money

Traditional

Social

Spontaneous

Pragmatic

Is for people who think that money is a means to an

end

Makes you feel on top of the world

Helps you to share good things in life with others

Makes you have more fun in life

Reliable

Accessible

Trustworthy

Straightforward

Enables you to deal with money in everyday life

Gives you the freedom to do what you want

Helps you to deal with money in a practical way

Makes you feel safe and secure at all times

139

OptimistsExpectations towards payment solutions

9332Makes you feel safe and secure at all times

8338Helps you to deal with money in a practical way

10940Gives you the freedom to do what you want

9243Enables you to deal with money in everyday life

9949Straightforward

9652Trustworthy

9253Accessible

9757ReliableTraditionalists

13019Makes you have more fun in life

15320Helps you to share good things in life with others

15518Makes you feel on top of the world

15919Is for people who think that money is a means to an end

13437Pragmatic

14137Spontaneous

14720Social

15315Traditional

14828Allows you to have a carefree attitude towards money

12647CarefreeOptimists

Index %Expression of basic motivational drivers Motivational Strategy

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

140

OptimistsProduct features of payment solutions

Strongly differentiating

Slightly differentiating

TOP 5 %

READING KEY

10962Free of charge

10064For everyday usage

10365Dependable

10066User-friendly

10068Convenient

Index%

141

OptimistsSocio-demographical profile

Index>110Index<90

142

3431303029282828

2321

1917

1515

1125

2834

1133

4715

2042

1822

815

3428

3119

2625

1037

2813

2030

5141

2217

1017

3414

1521

2924

4230

2529

Spain (N=161)Italy (N=167)

Poland (N=172)Hungary (N=183)Finland (N=185)

UK (N=150)Austria (N=193)

Portugal (N=185)France (N=171)

Germany (N=172)Netherlands (N=165)

Belgium (N=196)Sweden (N=178)

Denmark (N=177)

Status Seekers Competence Seekers Traditionalists Optimists

A.8. Motivational groups in the different European countries

In % (the number of observations per country represent the number of allocated respondents per country)

Countries with a high number of status seekers are Spain, Italy, Poland and Hungary. Countries with the highest number of competence seekers are Austria, Germany and Hungary. The highest number of traditionalists are in Sweden, Denmark and Portugal. Optimists can mainly be found in the Netherlands.

143

Content

Section A: Ideal payment solution

Section B: Awareness and usage of different payment methods

Section C: Country results: Authentication methods of card payments

Section D: Country results: Authentication methods of online payments

Section E: Country results: Innovative authentication methods and

e-environment solutions

144

Learnings

Looking at the awareness and usage of the cashless payment solutions, card payments are the most common application in the European countries.

Also in terms of trustworthiness, user friendliness and relevance in day to day life, card payments are at the top of the list but nevertheless closely followed by internet.

80% of the Europeans use a card at least once a week to pay for goods and services compared to 40% for internet payments and 4% for mobile payments.

The frequency number for internet should be nuanced: the sample consisted of people who did internet payments during the last year. Therefore this number is probably lower when taking into account the whole population (which also includes more traditional offline payment users).

Barriers towards internet payments are other payment applications that are more often used, the lack of knowledge in knowing how to use the application or the distrust behind the technology. Barriers towards mobile payment are not knowing how to make mobile payments and the technology behind the application: people don’t have the necessary technology to make payments via the mobile or don’t trust the technology behind the application.

145

B. Introduction

In the following chapter the awareness and usage of different payment methods is presented. The following applications are shown:

– Card payment (debit card, credit card, loyalty card)– Internet payment (bank transaction or purchase via internet)– Mobile payment (payment via mobile phone)

These payment applications will be assessed on:– Trust: how trustworthy is the application?– User friendliness: how easy is the application to use?– Relevance to the user: how useful is the application?

Next to that, the barriers for using new payment technologies will be shown.

The results will be presented on a total European level and on a country level. These latter findings will enable a cross country comparison.

The input for this chapter is from the online study in which 14 European countries were questioned. Results on an European level are weighted according to the relative importance of the internet population across the 14 countries. Results on country level are not weighted.

146

88%95%95%96%96%97%97%97%98%98%98%99%99%99%99%

0%

20%

40%

60%

80%

100%

NetherlandsAustriaPolandBelgiumDenmarkItalyGermanyEuropeHungarySwedenFinlandUKSpainFrancePortugal

Card payment

B.1. Awareness cashless payment methodsCard payments*

Here is a list of different methods people can use to pay for goods and services. Can you indicate which ones you know, even if only by name?

The awareness of cards (debit card, credit card, loyalty card) as a payment method is almost complete in all countries. Only in the Netherlands, the awareness is substantially lower.

*due to sampling criteria, all respondents needed to know internet payment methods. The level of awareness for internet payment was 100% and therefore not reported in this section.

Bold: significantly higher than European averageItalic: significantly lower than European average

Europe Portugal France Spain UK Finland Sweden Hungary Germany Italy Denmark Belgium Poland Austria NetherlandsObservations 2880 206 200 213 201 199 205 200 211 202 200 216 211 213 203Card payment 97% 99% 99% 99% 99% 98% 98% 98% 97% 97% 96% 96% 95% 95% 88%

147

B.1. Awareness cashless payment methodsInternet payments

Questions on awareness and usage of different cashless payment methods were asked via the internet. Due to sampling criteria, all respondents participating in the online research needed to know internet payment methods. The level of awareness for internet payment was 100% and therefore not reported in this section.

148

31%36%

44%46%48%50%51%53%54%58%60%63%

67%70%

75%

0%

20%

40%

60%

80%

100%

ItalyFranceUKSpainEuropeDenmarkNetherlandsBelgiumGermanySwedenPolandFinlandAustriaPortugalHungary

Mobile payment

B.1. Awareness cashless payment methodsMobile payments

Here is a list of different methods people can use to pay for goods and services. Can you indicate which ones you know, even if only by name?

48% of the Europeans know mobile payment. Countries like Hungary, Portugal and Austria have a higher level of awareness. Italy and France are below the European average.

Bold: significantly higher than European averageItalic: significantly lower than European average

Europe Hungary Portugal Austria Finland Poland Sweden Germany Belgium Netherlands Denmark Spain UK France ItalyObservations 2880 200 206 213 199 211 205 211 216 203 200 213 201 200 202Mobile payment 48% 75% 70% 67% 63% 60% 58% 54% 53% 51% 50% 46% 44% 36% 31%

149

33

5

1

47

35

3

12

42

8

4

14

10

4

5

1

11

2

62

1Card payment (N=2789)

Internet payment (N=2880)

Mobile payment (N=1372)

Daily Weekly Monthly Once every three to six months Once a year Less often Never

B.2. Frequency of usage of cashless payment methods in Europe

Can you indicate for each payment method, how often you use it? (base=awareness of payment method) (%)

Card payment is the most frequently used payment method in Europe. 33% of the Europeans use their card on a daily base. 47% use it once a week.Payments via the internet, are mostly done once a month (42%). 35% does this on a weekly basis.Mobile payments are less integrated. 62% never pays with their mobile.

150

Card paymentInternet payment Mobile payment

Europe 80% 40% 4%France 94% 24% 4%Finland 91% 80% 2%Denmark 88% 48% 2%Belgium 87% 60% 1%Portugal 87% 46% 6%Spain 85% 24% 5%Hungary 84% 25% 6%Poland 80% 63% 5%Sweden 81% 28% 2%Italy 80% 23% 8%Austria 79% 59% 6%UK 77% 42% 5%Germany 76% 53% 3%Netherlands 44% 32% 1%

B.2. Frequency of usage of cashless payment methods in European countries: weekly plus*

Can you indicate for each payment method, how often you use it? (base=awareness of payment method)

Countries that have the highest frequency of card usage at least once a week are France, Finland, Denmark, Belgium and Portugal. In the Netherlands, only 44% of the people use their card on a weekly basis.

Internet payments are mostly used in Finland, Belgium, Poland, Austria and Germany. Countries with a lower level of usage are Spain, Hungary, Italy and France.

Mobile payments are less frequently used in the different European countries. In Italy, 8% of the respondents use their mobile at least once a week to pay for goods and services. In Belgium and the Netherlands, only 1% uses this application weekly.

Top 5

*at least once a week (daily + weekly)

Bold: significantly higher than European averageItalic: significantly lower than European average

151

39%

16%

15%

13%

7%

4%

25%

38%

17%

9%

14%

21%

30%

I hardly ever use online payment solutions**

I do not know how to use it

I don't trust the technology behind it

I am afraid I won't retrieve my money when something goes wrong

The application is not secured enough (PIN, authentication code)

I do not have the necessary technology for it (PC, card system ofbank...)

OtherOnline payment (N=108)Mobile payment (N=851)

B.3. Barriers* of internet and mobile payment methods in Europe

What are the reasons you have used only once a year/never used internet payments/mobile payments? (base=yearly users of internet payment/non-users of mobile payments)

Barriers to use internet payments solutions are the fact that other payment solutions are used more than online solutions (39%). The fact that people do not know how to use it and the lack of trust behind the technology each account for about 16%.Barriers not to use mobile solutions are mainly related to the lack of knowledge about the application (38%) and the technology which is missing to do the transaction (21%). The lack of security and trust are more important for mobile applications than for online applications as a barrier.

*internet payment: reasons for only using online payment methods once a yearmobile payments: reasons for never trying mobile payment methods**only asked for online payment methods

152

In Spain, Sweden, UK, Germany and Portugal the main barrier for not using mobile solutions is not knowing how to use the technology. The lack of necessary technology is mainly in France and the Netherlands a barrier.Trust and security are perceived as barriers in Germany, UK, Spain and Hungary.In Austria, Hungary and Finland, other barriers are more important. However, there isn’t more information on hand on these factors.

Top 5

B.3. Barriers of mobile* payment methods in European countries

What are the reasons you have never used mobile payments? (base=non-users of mobile payments, N=min.30 per country)

Bold: significantly higher than European averageItalic: significantly lower than European average

I do not know how to use it

I do not have the necessary

technology for it (PC, card system of

bank)

I don't trust the technology behind

it

The application is not secured enough (PIN, authentication

code)

I am afraid I won't retrieve my money when something

goes wrong OtherEurope 38% 21% 17% 14% 9% 30%Spain 52% 16% 9% 13% 9% 27%Sweden 48% 12% 18% 10% 4% 36%UK 45% 15% 15% 17% 11% 23%Germany 39% 21% 28% 20% 10% 30%Portugal 37% 13% 10% 7% 8% 37%Belgium 36% 21% 18% 9% 6% 36%France 33% 35% 13% 13% 8% 21%Italy 32% 10% 19% 13% 16% 29%Denmark 30% 20% 8% 13% 3% 41%Poland 28% 17% 9% 6% 9% 39%Netherlands 28% 38% 9% 8% 3% 35%Austria 25% 9% 18% 13% 10% 54%Hungary 19% 15% 20% 15% 2% 42%Finland 18% 9% 9% 9% 3% 59%

*Due to the low number of observations per country for barriers of online payment, no country results are presented for online payment methods.

153

80

58

30

19

34

32

1

7

30

1

6 2

Card payment (N=2727)

Internet payment (N=2880)

Mobile payment (N=521)

Very easy to use Easy to use Not easy to use, not uneasy to use Not easy to use Not easy to use at all

B.4. User friendliness of cashless payment methods in Europe

Can you indicate for each payment method, how easy this method is to use? (base=users of payment method) (%)

Card payments are considered the most user-friendly cashless payment method in Europe. 80% of the Europeans find it very easy to use. In totality, almost all respondents find card payments a user friendly payment method.More than half of the Europeans (58%) find payments via the internet very easy to use. Mobile payments are considered relatively easy to use. However 8% considers this method as not easy to use and another 30% finds the application more neutral in terms of user friendliness.

154

All European countries find payment via card a user friendly payment method.

Internet payments are considered more user friendly in Portugal, UK and Finland compared to the European average. Spain, Hungary and Italy find payment via internet less user friendly than most countries in Europe.

Polish and Danish inhabitants perceive mobile payment solutions as most user friendly. French respondents are more critical towards mobile payments in terms of user friendliness.

Top 5

*user friendliness: very easy to use + easy to use

B.4. User friendliness* of cashless payment methods in European countries

Can you indicate for each payment method, how easy this method is to use? (base=users of payment method)

Card payment Internet paymentMobile

paymentEurope 99% 92% 62%Portugal 100% 98% 66%Belgium 99% 95% 57%Poland 99% 95% 85%Germany 99% 91% 55%UK 99% 98% 52%France 98% 96% 43%Austria 98% 92% 57%Finland 98% 97% 79%Denmark 98% 92% 82%Spain 98% 85% 63%Hungary 98% 85% 72%Sweden 97% 91% 70%Italy 97% 85% 66%Netherlands 97% 89% 67%

Bold: significantly higher than European averageItalic: significantly lower than European average

155

40

29

18

50

54

44

9

14

30

1

3

6 1

Card payment (N=2727)

Internet payment (N=2880)

Mobile payment (N=521)

Very trustworthy Trustworthy Not trustworthy, not untrustworthy either Untrustworthy Very untrustworthy

B.5. Trustworthiness of cashless payment methods in Europe

Can you indicate for each payment method, to which extent you have trust in this method? (base=users of payment method) (%)

Card payments enjoy a high level of trust among European card users. 90% of the European card users consider payment via card a trustworthy to very trustworthy application.Internet payments are also considered quite trustworthy. Payment via mobile is seen as trustworthy. 62% of the European mobile payment users find this application trustworthy (trustworthy + very trustworthy). About a third of the European users have a neutral opinion towards the trustworthiness of mobile payment solutions.

156

Scandinavian countries like Denmark and Finland have the highest level of trust in card payments, whereas Sweden has the lowest level of trust.

Internet payments are considered to be very trustworthy in Denmark and Finland but also in Poland.

Looking at mobile payment solutions, the Scandinavian countries Denmark and Finland have once more a high level of trust. Mobile payments generate the highest level of trust in Hungary. The lowest trust scores are once more for Sweden.

Top 5

*trustworthiness: very trustworthy + trustworthy

B.5. Trustworthiness* of cashless payment methods in European countries

Can you indicate for each payment method, to which extent you have trust in this method? (base=users of payment method)

Bold: significantly higher than European averageItalic: significantly lower than European average

Card paymentInternet payment

Mobile payment

Europe 90% 83% 62%Denmark 96% 94% 74%Finland 96% 93% 71%Portugal 96% 87% 66%Poland 95% 94% 65%Belgium 95% 85% 64%Spain 94% 73% 67%Austria 93% 88% 71%Hungary 93% 76% 79%France 92% 75% 57%Italy 92% 87% 69%Netherlands 90% 89% 67%Germany 89% 82% 62%UK 88% 84% 48%Sweden 77% 86% 51%

157

80

67

32

18

28

30

2

4

30

1

7 2

Card payment (N=2727)

Internet payment (N=2880)

Mobile payment (N=521)

Very useful Useful Not useful, not useless either Useless Very useless

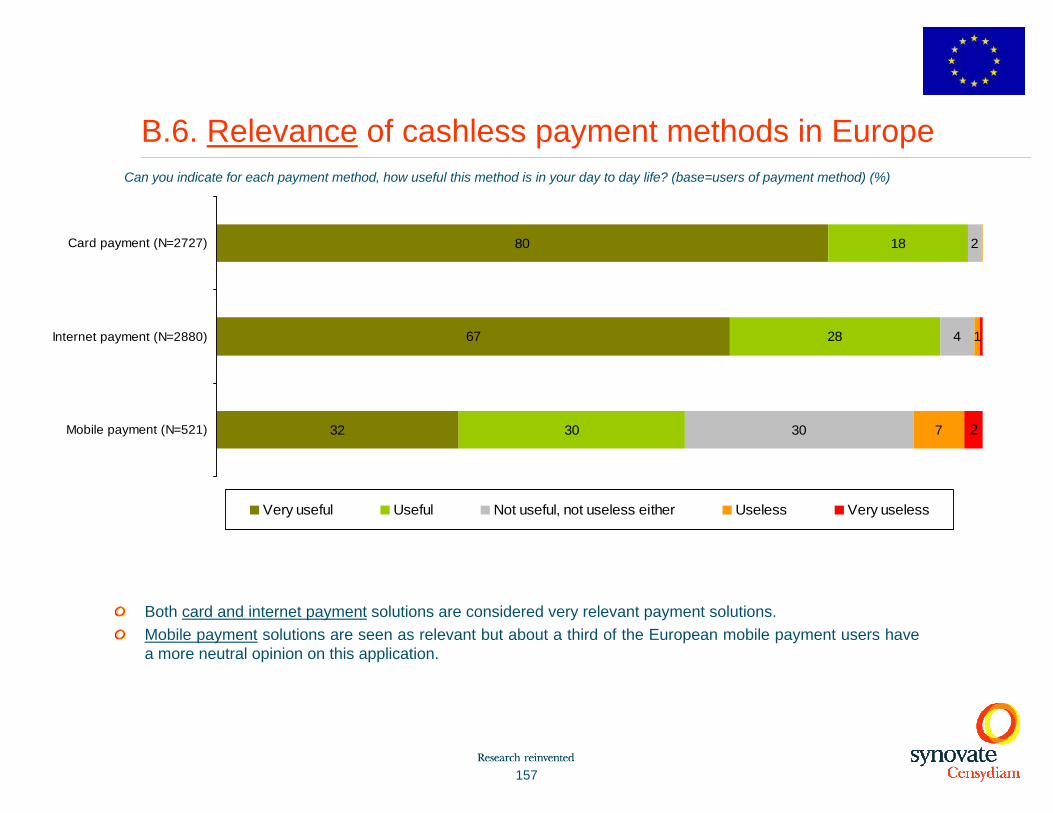

B.6. Relevance of cashless payment methods in EuropeCan you indicate for each payment method, how useful this method is in your day to day life? (base=users of payment method) (%)

Both card and internet payment solutions are considered very relevant payment solutions. Mobile payment solutions are seen as relevant but about a third of the European mobile payment users have a more neutral opinion on this application.

158

Card payments are seen as very relevant in almost all European countries.

Internet payments are considered to be very useful in Portugal and Poland. Compared to the other European countries, the Netherlands and Spain have the lowest relevance scores for internet payment.

Looking at mobile payment solutions, it is especially Finland but also France that is critical in terms of relevance. The application is seen as most relevant in Poland and Hungary.

Top 5

*relevance= very useful+ useful

Can you indicate for each payment method, how useful this method is in your day to day life? (base=users of payment method)

B.6. Relevance* of cashless payment methods in European countries

Card paymentInternet payment

Mobile payment

Europe 98% 95% 62%Portugal 100% 99% 70%Austria 99% 96% 57%Italy 99% 94% 69%Finland 99% 97% 34%Denmark 99% 95% 53%France 98% 96% 43%Poland 98% 98% 79%Belgium 98% 95% 50%Spain 98% 91% 63%Sweden 98% 97% 62%UK 98% 94% 61%Germany 97% 94% 62%Hungary 97% 94% 78%Netherlands 96% 90% 75%

Bold: significantly higher than European averageItalic: significantly lower than European average

159

Summary: awareness and usage of card payments

• Europe: 98%

Top 5 countries:• Portugal (100%)• Belgium (99%)• Poland (99%)• Germany (99%)• UK (99%)

Bottom 5 countries: • Netherlands (97%)• Italy (97%)• Sweden (97%)• Hungary (98%)• Spain (98%)

• Europe 97%

Top 5 countries: • Portugal (99%)• France (99%)• Spain (99%)• UK (99%)• Finland (98%)

Bottom 5 countries: • Netherlands (88%)• Austria (95%)• Poland (95%)• Belgium (96%)• Denmark (96%)

• Europe: 91%

Top 5 countries:• Denmark (96%)• Finland (96%)• Portugal (96%)• Poland (95%)• Belgium (95%)

Bottom 5 countries:• Sweden (77%)• UK (88%)• Germany (89%)• Netherlands (90%)• Italy (92%)

Awareness User friendliness TrustworthinessFrequency of usage

• Weekly plus Europe 80%

Top 5 countries: • France (94%)• Finland (91%)• Denmark (88%)• Belgium (87%)• Portugal (87%)

Bottom 5 countries: • Netherlands (44%)• Germany (76%)• UK (77%)• Austria (79%)• Italy (80%)

Relevance• Europe: 98%

Top 5 countries:• Portugal (100%)• Austria (99%)• Italy (99%)• Finland (99%)• Denmark (99%)

Bottom 5 countries: • Netherlands (96%)• Hungary (97%)• Germany (97%)• UK (98%)• Sweden (98%)

160

• Europe: 92%

Top 5 countries:• Portugal (98%)• UK (98%)• Finland (97%)• France (96%)• Belgium (95%)

Bottom 5 countries: • Hungary (85%)• Italy (85%)• Spain (85%)• Netherlands (89%)• Sweden (91%)

• I hardly ever use online payment solutions • I don’t know how to use it• I don’t trust the technology behind it

• Weekly plus Europe 40%

Top 5 countries: • Finland (80%)• Poland (63%)• Belgium (60%)• Austria (59%)• Germany (53%)

Bottom 5 countries: • Italy (23%)• France (24%)• Spain (24%)• Hungary (25%)• Sweden (28%)

• Europe: 83%

Top 5 countries:• Poland (94%)• Denmark (94%)• Finland (93%)• Netherlands (89%)• Austria (88%)

Bottom 5 countries:• Spain (73%)• France (75%)• Hungary (76%)• Germany (82%)• UK (84%)

Frequency of usage

Barriers top 3

User friendliness Trustworthiness Relevance• Europe: 95%

Top 5 countries:• Portugal (99%)• Poland (98%)• Finland (97%)• Sweden (97%)• France (96%)

Bottom 5 countries: • Netherlands (90%)• Spain (91%)• Hungary (94%)• Italy (94%)• Germany (94%)

Summary: awareness and usage of internet payments

161

Summary: awareness and usage of mobile payments

• Europe: 62%

Top 5 countries:• Poland (85%)• Denmark (82%)• Finland (79%)• Hungary (72%)• Sweden (70%)

Bottom 5 countries: • France (43%)• UK (52%)• Germany (55%)• Austria (57%)• Belgium (57%)

• I don’t know how to use it• I don’t have the necessary technology for it• I don’t trust the technology behind it

• Europe 48%

Top 5 countries: • Hungary (75%)• Portugal (70%)• Austria (67%)• Finland (63%)• Poland (60%)

Bottom 5 countries: • Italy (31%)• France (36%)• UK (44%)• Spain (46%)• Denmark (50%)

• Europe: 62%

Top 5 countries:• Hungary (79%)• Denmark (74%)• Austria (71%)• Finland (71%)• Italy (69%)

Bottom 5 countries:• UK (48%)• Sweden (51%)• France (57%)• Germany (62%)• Belgium (64%)

Awareness

Barriers top 3

User friendliness TrustworthinessFrequency of usage• Weekly plus Europe 4%

Top 5 countries: • Italy (8%)• Hungary (6%)• Austria (6%)• Portugal (6%)• Spain (5%)

Bottom 5 countries: • Belgium (1%)• Netherlands (1%)• Sweden (2%)• Denmark (2%)• Finland (2%)

Relevance• Europe: 61%

Top 5 countries:• Poland (79%)• Hungary (78%)• Netherlands (75%)• Portugal (70%)• Italy (69%)

Bottom 5 countries: • Finland (34%)• France (43%)• Belgium (50%)• Denmark (53%)• Austria (57%)