Embed Size (px)

Citation preview

FINAL OFFICIAL STATEMENT DATED FEBRUARY 26, 2013 NEW ISSUES Moody’s Rated “Aa1” Non Bank Qualified In the opinion of Quarles & Brady LLP, Bond Counsel, assuming continued compliance with the requirements of the Internal Revenue Code of 1986, as amended, under existing law Interest on the Tax-Exempt Bonds and Tax-Exempt Notes is excludable from gross income and is not an item of tax preference for federal income tax purposes. See "TAX STATUS" herein for a more detailed discussion of some of the federal income tax consequences of owning the Tax-Exempt Bonds and Tax-Exempt Notes. Interest on the Taxable Notes is included in gross income for federal income tax purposes. See "TAX STATUS" herein. The Securities are NOT designated as "qualified tax-exempt obligations". The interest on the Securities is not exempt from present Wisconsin income or franchise taxes.

RACINE COUNTY, WISCONSIN $14,880,000 General Obligation Refunding Bonds $6,000,000 General Obligation Promissory Notes

$1,020,000 Taxable General Obligation Promissory Notes

Dated: March 19, 2013 Due: As shown herein The $14,880,000 General Obligation Refunding Bonds (the “Tax-Exempt Bonds”), the $6,000,000 General Obligation Promissory Notes (the “Tax-Exempt Notes”), and the $1,020,000 Taxable General Obligation Promissory Notes (the “Taxable Notes”), (collectively, the “Securities”), will be dated March 19, 2013 and will be in the denomination of $5,000 each or any multiple thereof. The Tax-Exempt Bonds will mature serially on March 1 of the years 2014 through 2026 as shown herein. The Tax-Exempt Notes will mature serially on March 1 of the years 2014 through 2015, and 2017 through 2023 as shown herein. The Taxable Notes will mature serially on March 1 of the years 2014 through 2023 as shown herein. Interest on the Securities shall be payable commencing September 1, 2013 and semiannually thereafter on each March 1 and September 1. Associated Trust Company, National Association, Green Bay, Wisconsin will serve as escrow agent for the advanced refunded obligations. The Securities are being issued pursuant to Chapter 67 of the Wisconsin Statutes. The Securities will be general obligations of Racine County, Wisconsin (the “County”) for which its full faith and credit and taxing powers are pledged which taxes may, under current law, be levied without limitation as to rate or amount. The proceeds from the sale of the Tax-Exempt Bonds will be used for the public purpose of current and advance refunding certain outstanding obligations of the County, including interest on them. (See “THE FINANCING PLAN” herein.) The proceeds from the sale of the Tax-Exempt Notes will be used for the public purposes, including financing capital projects included in the County's 2013 budget. (See “THE FINANCING PLAN” herein.) The proceeds from the sale of the Taxable Notes will be used for public purpose of financing the County's revolving loan fund for the Racine County Economic Development Corporation. (See “THE FINANCING PLAN” herein.) The Tax-Exempt Bonds maturing March 1, 2024 and thereafter are subject to call and prior redemption on March 1, 2023 or any date thereafter as described herein. (SEE “REDEMPTION PROVISIONS” herein.) The Tax-Exempt Notes maturing March 1, 2021 and thereafter are subject to call and prior redemption on March 1, 2020 or any date thereafter as described herein. (SEE “REDEMPTION PROVISIONS” herein.) The Taxable Notes maturing March 1, 2021 and thereafter are subject to call and prior redemption on March 1, 2020 or any date thereafter as described herein. (SEE “REDEMPTION PROVISIONS” herein.) The Securities will be issued only as fully registered Securities and will be registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York ("DTC"). DTC will act as the securities depository of the Securities. Individual purchases will be made in book-entry form only in denominations of $5,000 principal amount or any integral multiple thereof. Purchasers of the Securities will not receive certificates representing their interest in the Securities purchased. (See "BOOK-ENTRY-ONLY SYSTEM" herein.) The County’s Securities are offered when, as and if issued subject to the approval of legality by Quarles & Brady LLP, Milwaukee, Wisconsin, Bond Counsel. The anticipated settlement date for the Securities is on or about March 19, 2013.

BAIRD

2

MATURITY SCHEDULES

$14,880,000 General Obligation Refunding Bonds Dated: March 19, 2013 - Due: March 1 of the years 2014 through 2026

Callable: March 1, 2023

CUSIP (1) CUSIP (1)

Base Base (March 1) Amount Rate Yield 749845 (March 1) Amount Rate Yield 749845

2014 $285,000 2.00% 0.40% PZ0 2021 $1,145,000 4.00% 1.90% QG1 2015 545,000 3.00 0.51 QA4 2022 1,195,000 4.00 2.11 QH9 2016 1,010,000 3.00 0.64 QB2 2023 1,245,000 4.00 2.35 QJ5 2017 1,720,000 3.00 0.83 QC0 2024 1,300,000 4.00 2.53 QK2 2018 1,500,000 3.00 1.10 QD8 2025 1,355,000 4.00 2.61 QL0 2019 1,065,000 3.00 1.36 QE6 2026 1,415,000 4.00 2.72 QM8 2020 1,100,000 3.00 1.66 QF3

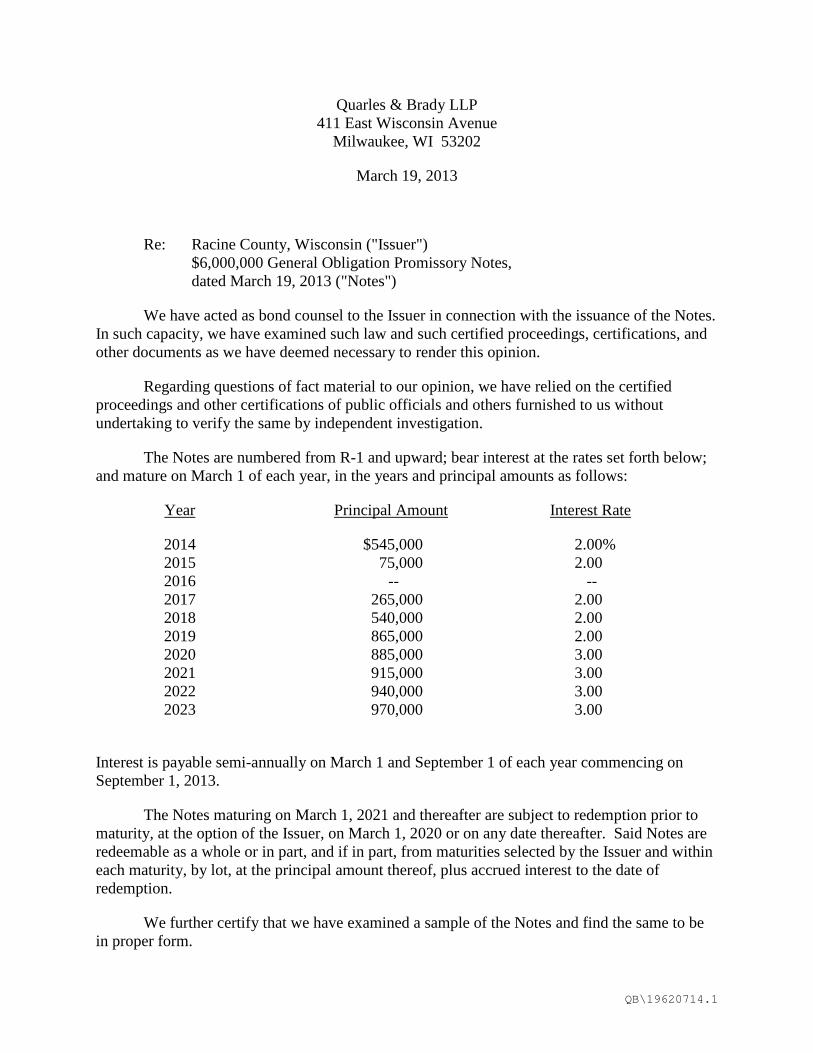

$6,000,000 General Obligation Promissory Notes

Dated: March 19, 2013 - Due: March 1 of the years 2014 through 2015 and 2017 through 2023 Callable: March 1, 2020

CUSIP (1)

Base (March 1) Amount Rate Yield 749845

2014 $545,000 2.00% 0.40% QN6 2015 75,000 2.00 0.51 QP1 2016 — — — — 2017 265,000 2.00 0.85 QQ9 2018 540,000 2.00 1.12 QR7 2019 865,000 2.00 1.36 QS5 2020 885,000 3.00 1.66 QT3 2021 915,000 3.00 1.93 QU0 2022 940,000 3.00 2.16 QV8 2023 970,000 3.00 2.40 QW6

$1,020,000 Taxable General Obligation Promissory Notes

Dated: March 19, 2013 - Due: March 1 of the years 2014 through 2023 Callable: March 1, 2020

CUSIP (1)

Base (March 1) Amount Rate Yield 749845

2014 $95,000 0.50% 0.50% QX4 2015 95,000 0.75 0.75 QY2 2016 100,000 0.90 0.90 QZ9 2017 100,000 1.05 1.05 RA3 2018 100,000 1.49 1.49 RB1 2019 100,000 1.69 1.69 RC9 2020 105,000 2.00 2.00 RD7 2021 105,000 2.20 2.20 RE5 2022 110,000 2.39 2.39 RF2 2023 110,000 2.59 2.59 RG0

(1) CUSIP data herein provided by Standard & Poor’s CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. Copyright 2013. American Bankers Association.

3

RACINE COUNTY

WISCONSIN

COUNTY BOARD OF SUPERVISORS

Peter L. Hansen, Chairperson Russell (Rusty) A. Clark, Vice-Chairperson

Gilbert Bakke Robert N. Miller Katherine Buske Ronald Molnar David J. Cooke Monte G. Osterman

Edward (Mike) Dawson Thomas Pringle Mark M. Gleason Q.A. Shakoor II Robert D. Grove Daniel F. Sharkozy

Jeff Halbach Donnie Snow Kenneth Hall Pamela Zenner-Richards

Kiana K. Johnson John Wisch Kenneth Lumpkin

ADMINISTRATION

James A. Ladwig, County Executive Daniel J. Eastman, Finance Director Wendy Christensen, County Clerk Jane F. Nikolai, County Treasurer

Karen Galbraith, Human Resources Director Jonathan F. Lehman, Corporation Counsel

Terry DeBrabander, Information System Director

PROFESSIONAL SERVICES

Underwriter: Robert W. Baird & Co., Milwaukee, Wisconsin

Bond Counsel: Quarles & Brady LLP, Milwaukee, Wisconsin

Paying Agent Contact: Finance Director, Racine County, Wisconsin*

Escrow Agent: (For the advance refunded obligations)

Associated Trust Company, National Association, Green Bay, Wisconsin

Mathematical Verification: Grant Thornton, LLP, Minneapolis, Minnesota

*The contact person for paying agent matters is Daniel Eastman, Finance Director

4

REGARDING USE OF THIS OFFICIAL STATEMENT

This Official Statement is being distributed in connection with the sale of the Securities referred to in this Official Statement and may not be used, in whole or in part, for any other purpose. No dealer, broker, salesman or other person is authorized to make any representations concerning the Securities other than those contained in this Official Statement, and if given or made, such other information or representations may not be relied upon as statements of Racine County, Wisconsin (the "County"). This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Securities by any person in any jurisdiction in which it is unlawful to make such an offer, solicitation or sale. Unless otherwise indicated, the County is the source of the information contained in this Official Statement. Certain information in this Official Statement has been obtained by the County or on its behalf from The Depository Trust Company and other non-County sources that the County believes to be reliable. No representation or warranty is made, however, as to the accuracy or completeness of such information. Nothing contained in this Official Statement is a promise of or representation by Robert W. Baird & Co. Incorporated (the "Underwriter"). The Underwriter has provided the following sentence of inclusion in this Official Statement. The Underwriter has reviewed the information in this Official Statement in accordance with, and as part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. The information and opinions expressed in this Official Statement are subject to change without notice. Neither the delivery of this Official Statement nor any sale made under this Official Statement shall, under any circumstances, create any implication that there has been no change in the financial condition or operations of the County or other information in this Official Statement, since the date of this Official Statement. This Official Statement contains statements that are “forward-looking statements” as that term is defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. When used in this Official Statement, the words “estimate,” “intend,” “project” or “projection,” “expect” and similar expressions are intended to identify forward-looking statements. Forward-looking statements are subject to risks and uncertainties, some of which are discussed herein, that could cause actual results to differ materially from those contemplated in such forward-looking statements. Investors and prospective investors are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of this Official Statement. This Official Statement should be considered in its entirety. No one factor should be considered more or less important than any other by reason of its position in this Official Statement. Where statutes, ordinances, reports or other documents are referred to in this Official Statement, reference should be made to those documents for more complete information regarding their subject matter. The Securities will not be registered under the Securities Act of 1933, as amended, or the securities laws of any state of the United States, and will not be listed on any stock or other securities exchange. Neither the Securities and Exchange Commission nor any other federal, state, municipal or other governmental entity shall have passed upon the accuracy or adequacy of this Official Statement. IN CONNECTION WITH THE OFFERING OF THE SECURITIES, THE UNDERWRITER MAY OR MAY NOT OVERALLOT OR EFFECT TRANSACTIONS THAT STABILIZE OR MAINTAIN THE MARKET PRICES OF THE SECURITIES AT LEVELS ABOVE THOSE WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME WITHOUT NOTICE. THE PRICES AND OTHER TERMS RESPECTING THE OFFERING AND SALE OF THE SECURITIES MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITER AFTER THE SECURITIES ARE RELEASED FOR SALE AND THE SECURITIES MAY BE OFFERED AND SOLD AT PRICES OTHER THAN THE INITIAL OFFERING PRICES, INCLUDING SALES TO DEALERS WHO MAY SELL THE SECURITIES INTO INVESTMENT ACCOUNTS.

5

TABLE OF CONTENTS Page MATURITY SCHEDULES ..................................................................................................................................... 2 COUNTY BOARD OF SUPERVISORS................................................................................................................. 3 ADMINISTRATION ................................................................................................................................................ 3 PROFESSIONAL SERVICES ............................................................................................................................... 3 REGARDING USE OF THIS OFFICIAL STATEMENT ......................................................................................... 4 SUMMARY-TAX-EXEMPT BONDS ...................................................................................................................... 6 SUMMARY-TAX-EXEMPT NOTES ....................................................................................................................... 7 SUMMARY-TAXABLE NOTES ............................................................................................................................. 8 INTRODUCTORY STATEMENT ........................................................................................................................... 9 THE FINANCING PLAN ........................................................................................................................................ 9 ESTIMATED SOURCES AND USES .................................................................................................................. 10 REDEMPTION PROVISIONS ............................................................................................................................. 11 CONSTITUTIONAL AND STATUTORY CONSIDERATIONS AND LIMITATIONS CONCERNING THE COUNTY'S POWER TO INCUR INDEBTEDNESS .................................................................................. 11 PROPERTY TAX LEVY LIMITS .......................................................................................................................... 12 SALES TAX ......................................................................................................................................................... 13 THE RESOLUTIONS ........................................................................................................................................... 14 RACINE COUNTY ............................................................................................................................................... 15 GENERAL INFORMATION ................................................................................................................................. 18 DEMOGRAPHIC AND ECONOMIC INFORMATION .......................................................................................... 19 TAX LEVIES, RATES AND COLLECTIONS ....................................................................................................... 22 EQUALIZED VALUATIONS ................................................................................................................................ 22 TAX INCREMENT DISTRICTS ........................................................................................................................... 23 INDEBTEDNESS OF THE COUNTY .................................................................................................................. 24 FINANCIAL INFORMATION ................................................................................................................................ 26 GENERAL FUND SUMMARY FOR YEARS ENDED DECEMBER 31 ............................................................... 27 UNDERWRITING ................................................................................................................................................ 28 RATING .............................................................................................................................................................. 28 TAX STATUS ....................................................................................................................................................... 28 NON QUALIFIED TAX-EXEMPT OBLIGATIONS ............................................................................................... 29 CONTINUING DISCLOSURE ............................................................................................................................. 29 BOOK-ENTRY-ONLY SYSTEM .......................................................................................................................... 30 LITIGATION ......................................................................................................................................................... 31 MATHEMATICAL VERIFICATION ...................................................................................................................... 32 LEGAL MATTERS ............................................................................................................................................... 32 MISCELLANEOUS .............................................................................................................................................. 32 AUTHORIZATION ............................................................................................................................................... 33 Appendix A: Basic Financial Statements and Related Notes for the year ended December 31, 2011 Appendix B: Form of Continuing Disclosure Certificates Appendix C: Form of Legal Opinions

6

SUMMARY-TAX-EXEMPT BONDS

County: Racine County, Wisconsin.

Issue: $14,880,000 General Obligation Refunding Bonds (the “Tax-Exempt Bonds”).

Dated Date: March 19, 2013.

Interest Due: Commencing September 1, 2013 and semi-annually thereafter on March 1 and September 1 of each year. Interest on the Tax-Exempt Bonds will be computed on the basis of a 30-day month and a 360-day year.

Principal Due: March 1 of the years 2014 through 2026.

Redemption Provision: The Tax-Exempt Bonds maturing on and after March 1, 2024 shall be subject to call and prior payment on March 1, 2023 or on any date thereafter at par plus accrued interest. The amounts and maturities of the Tax-Exempt Bonds to be redeemed shall be selected by the County. If less than the entire principal amount of any maturity is to be redeemed, the Tax-Exempt Bonds of that maturity which are to be redeemed shall be selected by lot. Notice of such call shall be given by sending a notice thereof by registered or certified mail, facsimile or electronic transmission or overnight express delivery at least thirty (30) days nor more than sixty (60) days prior to the date fixed for redemption to the registered owner of each Tax-Exempt Bond to be redeemed at the address shown on the registration books. (See ‘REDEMPTION PROVISONS” herein.)

Security: The full faith, credit and resources of the County are pledged to the payment of the principal of and the interest on the Tax-Exempt Bonds as the same become due and, for said purposes, there are levied without limitation on all the taxable property in the County, direct, annual irrepealable taxes in each year and in such amounts which will be sufficient to meet such principal and interest payments when due. Under current law, such taxes may be levied without limitation as to rate or amount.

Purpose: The proceeds from the sale of the Tax-Exempt Bonds will be used for the public purpose of current and advance refunding certain outstanding obligations of the County, including interest on them. (See “THE FINANCING PLAN” herein.)

Tax Status: Interest on the Tax-Exempt Bonds is excludable from gross income for federal income tax purposes. (See “TAX STATUS” herein.)

Bank Qualification: The Tax-Exempt Bonds shall NOT be designated "qualified tax-exempt obligations."

Credit Rating: This issue has been assigned a “Aa1” rating by Moody’s Investors Service, Inc. (See “RATING” herein.)

Record Date: The 15th day of the calendar month next preceding each interest payment date.

Information set forth on this page is qualified by the entire Official Statement. A full review of the entire Official Statement should be made by potential investors.

7

SUMMARY-TAX-EXEMPT NOTES

County: Racine County, Wisconsin.

Issue: $6,000,000 General Obligation Promissory Notes (the “Tax-Exempt Notes”).

Dated Date: March 19, 2013.

Interest Due: Commencing September 1, 2013 and semi-annually thereafter on March 1 and September 1 of each year. Interest on the Tax-Exempt Notes will be computed on the basis of a 30-day month and a 360-day year.

Principal Due: March 1 of the years 2014 through 2015 and 2017 through 2023.

Redemption Provision: The Tax-Exempt Notes maturing on and after March 1, 2021 shall be subject to call and prior payment on March 1, 2020 or on any date thereafter at par plus accrued interest. The amounts and maturities of the Tax-Exempt Notes to be redeemed shall be selected by the County. If less than the entire principal amount of any maturity is to be redeemed, the Tax-Exempt Notes of that maturity which are to be redeemed shall be selected by lot. Notice of such call shall be given by sending a notice thereof by registered or certified mail, facsimile or electronic transmission or overnight express delivery at least thirty (30) days nor more than sixty (60) days prior to the date fixed for redemption to the registered owner of each Tax-Exempt Note to be redeemed at the address shown on the registration books.

Security: The full faith, credit and resources of the County are pledged to the payment of the principal of and the interest on the Tax-Exempt Notes as the same become due and, for said purposes, there are levied without limitation on all the taxable property in the County, direct, annual irrepealable taxes in each year and in such amounts which will be sufficient to meet such principal and interest payments when due. Under current law, such taxes may be levied without limitation as to rate or amount.

Purpose: The proceeds from the sale of the Tax-Exempt Notes will be used to raise funds for public purposes, including financing capital projects included in the County's 2013 budget. (See “THE FINANCING PLAN” herein.)

Tax Status: Interest on the Tax-Exempt Notes is excludable from gross income for federal income tax purposes. (See “TAX STATUS” herein.)

Bank Qualification: The Tax-Exempt Notes shall NOT be designated "qualified tax-exempt obligations."

Credit Rating: This issue has been assigned a “Aa1” rating by Moody’s Investors Service, Inc. (See “RATING” herein.)

Record Date: The 15th day of the calendar month next preceding each interest payment date.

Information set forth on this page is qualified by the entire Official Statement. A full review of the entire Official Statement should be made by potential investors.

8

SUMMARY-TAXABLE NOTES

County: Racine County, Wisconsin.

Issue: $1,020,000 Taxable General Obligation Promissory Notes (the “Taxable Notes”).

Dated Date: March 19, 2013.

Interest Due: Commencing September 1, 2013 and semi-annually thereafter on March 1 and September 1 of each year. Interest on the Taxable Notes will be computed on the basis of a 30-day month and a 360-day year.

Principal Due: March 1 of the years 2014 through 2023.

Redemption Provision: The Taxable Notes maturing on and after March 1, 2021 shall be subject to call and prior payment on March 1, 2020 or on any date thereafter at par plus accrued interest. The amounts and maturities of the Taxable Notes to be redeemed shall be selected by the County. If less than the entire principal amount of any maturity is to be redeemed, the Taxable Notes of that maturity which are to be redeemed shall be selected by lot. Notice of such call shall be given by sending a notice thereof by registered or certified mail, facsimile or electronic transmission or overnight express delivery at least thirty (30) days nor more than sixty (60) days prior to the date fixed for redemption to the registered owner of each Taxable Note to be redeemed at the address shown on the registration books.

Security: The full faith, credit and resources of the County are pledged to the payment of the principal of and the interest on the Taxable Notes as the same become due and, for said purposes, there are levied without limitation on all the taxable property in the County, direct, annual irrepealable taxes in each year and in such amounts which will be sufficient to meet such principal and interest payments when due. Under current law, such taxes may be levied without limitation as to rate or amount.

Purpose: The proceeds from the sale of the Taxable Notes will be used for the public purpose of financing the County's revolving loan fund for the Racine County Economic Development Corporation (the "Project"). (See “THE FINANCING PLAN” herein.)

Tax Status: Interest on the Taxable Notes is included in gross income for federal income tax purposes. (See “TAX STATUS” herein.)

Credit Rating: This issue has been assigned a”Aa1” rating by Moody’s Investors Service, Inc. (See “RATING” herein.)

Record Date: The 15th day of the calendar month next preceding each interest payment date.

Information set forth on this page is qualified by the entire Official Statement. A full review of the entire Official Statement should be made by potential investors.

9

INTRODUCTORY STATEMENT

This Official Statement presents certain information relating to Racine County, Wisconsin (the "County" and the "State" respectively) in connection with the sale of the County's $14,880,000 General Obligation Refunding Bonds (the “Tax-Exempt Bonds”), the $6,000,000 General Obligation Promissory Notes (the “Tax-Exempt Notes”) and $1,020,000 Taxable General Obligation Promissory Notes (the “Taxable Notes”) (collectively, the “Securities”). The Securities are issued pursuant to the Constitution and laws of the State and the resolutions (the "Resolutions") adopted by the County Board of Supervisors (the “County Board”) and other proceedings and determinations related thereto. All summaries of statutes, documents and the Resolutions contained in this Official Statement are subject to all the provisions of, and are qualified in their entirety by reference to such statutes, documents and the Resolutions, and references herein to the Securities are qualified in their entirety by reference to the form thereof included in the Resolutions. Copies of the Resolutions may be obtained from the Underwriter upon request.

THE FINANCING PLAN The Tax-Exempt Bonds will be issued for the purpose of advance refunding portions of the following issues (the “2006 Bonds”, the “2007 Notes” and the “2008 Notes”):

Issue

Original Amount

Call Price

Call Date

Maturities to be

Refunded

Amount of Principal Refunded

Balance after Refunding

(March 19, 2013) General Obligation Law Enforcement Center Bonds, Dated March 15, 2006 $18,970,000 100% 3/01/16 2017-2026 $11,865,000 $2,650,000 General Obligation Promissory Notes, Dated June 7, 2007 $2,155,000 100% 6/01/14 2015-2017 $805,000 $485,000 General Obligation Promissory Notes, Dated June 17, 2008 $3,795,000 100% 6/01/15 2016-2018 $1,365,000 $1,220,000

A portion of the proceeds of the Tax-Exempt Bonds will be irrevocably deposited in an escrow account, invested in U.S. Government Securities and used to advance refund the 2006 Bonds, the 2007 Notes and the 2008 Notes. See "MATHEMATICAL VERIFICATION" herein. A portion of the Tax-Exempt Bonds will be issued for the purpose of current refunding the following issue (the “2006 Notes”):

Issue

Original Amount

Call Price

Call Date

Maturities to be

Refunded

Amount of Principal Refunded

Balance after Refunding

March 29, 2013 General Obligation Promissory Notes Dated July 18, 2006 $2,065,000 100% 03/29/2013 2014-2016 $785,000 $0

Proceeds of the Bonds will be deposited in a segregated account and used to current refund the 2006 Notes. The proceeds from the sale of the Tax-Exempt Notes will be used for public purposes, including financing capital projects included in the County's 2013 budget. The proceeds from the sale of the Taxable Notes will be used for the public purpose of financing the County's revolving loan fund for the Racine County Economic Development Corporation.

10

ESTIMATED SOURCES AND USES

Tax-Exempt Bonds

Sources of Funds Par Amount of Bonds $14,880,000.00 Reoffering Premium 1,607,081.60 Transfers from Prior Issue Debt Service Funds 122,448.14 Total Sources $16,609,529.74

Uses of Funds Deposit to Net Cash Escrow Account $15,607,538.06 Deposit to Current Refunding Fund 787,616.64 Cost of Issuance (including underwriter's discount) and Rounding 214,375.04 Total Uses $16,609,529.74

Tax-Exempt Notes

Sources of Funds Par Amount of Notes $6,000,000.00 Reoffering Premium 305,223.00 Total Sources $6,305,223.00

Uses of Funds Deposit to Project Construction Fund $5,999,233.00 Bid Premium Available for Deposit to Debt Service Fund 232,740.00 Cost of Issuance (including underwriter's discount) and Rounding 73,250.00 Total Uses $6,305,223.00

Taxable Notes

Sources of Funds Par Amount of Notes $1,020,000.00 Total Sources $1,020,000.00

Uses of Funds Deposit to Project Construction Fund $1,000,000.00 Cost of Issuance (including underwriter's discount) and Rounding 20,000.00 Total Uses $1,020,000.00

11

REDEMPTION PROVISIONS

Tax-Exempt Bonds The Tax-Exempt Bonds maturing March 1, 2024 and thereafter are subject to call and prior redemption on March 1, 2023 or any date thereafter. Tax-Exempt Notes The Tax-Exempt Notes maturing March 1, 2021 and thereafter are subject to call and prior redemption on March 1, 2020 or any date thereafter. Taxable Notes The Taxable Notes maturing March 1, 2021 and thereafter are subject to call and prior redemption on March 1, 2020 or any date thereafter.

CONSTITUTIONAL AND STATUTORY CONSIDERATIONS AND LIMITATIONS

CONCERNING THE COUNTY'S POWER TO INCUR INDEBTEDNESS The Constitution and laws of the State limit the power of the County (and other municipalities of the State) to issue obligations and to contract indebtedness. Such constitutional and legislative limitations include the following, in summary form and as generally applicable to the County. Purpose The County may not borrow money or issue notes or bonds therefor for any purpose except those specified by statute, which include among others the purpose for which the Securities are being issued. Bond or Note Anticipation Notes In anticipation of issuing general obligation bonds or notes, the County is authorized to borrow money using bond or note anticipation notes. The bond or note anticipation notes shall in no event be general obligations of the County, and do not constitute an indebtedness of the County only from (a) proceeds of the bond or note anticipation notes set aside for payment of interest on the bond or note anticipation notes as they become due, and, (b) proceeds to be derived from the issuance and sale of general obligation bonds or notes which proceeds are pledged for the payment of the principal of and interest on the bond or note anticipation notes. The maximum term of any bond or note anticipation notes (including any refunding) is five years. General Obligation Bonds The principal amount of every sum borrowed by the County and secured by an issue of bonds may be payable at one time in a single payment or at several times in two or more installments; however, no installment may be made payable later than the termination of twenty years immediately following the date of the bonds. The County Board is required to levy a direct, annual, irrepealable tax sufficient in amount to pay the interest on such bonds as it falls due and also to pay and discharge the principal thereof at maturity. Bonds issued by the County to refinance or refund outstanding notes or bonds issued by the County may be payable no later than twenty years following the original date of such outstanding notes or bonds. Promissory Notes In addition to being authorized to issue bonds, the County is authorized to borrow money using notes for any public purpose. To evidence such indebtedness, the County must issue to the lender its promissory notes (with interest) payable within a period not exceeding ten years following the date of said notes. Such notes constitute a general obligation of the County. Notes may be issued to refinance or refund outstanding notes. However, such notes may be payable no later than twenty years following the original date of such outstanding notes.

12

Refunding Bonds In addition to being authorized to issue bonds, the County is authorized to borrow money using refunding bonds for refunding existing debt. To evidence such indebtedness, the County must issue to the lender its refunding bonds (with interest) payable within a period not exceeding twenty years following the initial date of the debt to be refunded. Such refunding bonds constitute a general obligation of the County. Refunding bonds are not subject to referendum. Debt Limit The County has the power to contract indebtedness for purposes specified by statute so long as the principal amount thereof does not exceed five percent of the equalized value of taxable property within the County. For information with respect to the County's percent of legal debt incurred, see the caption "INDEBTEDNESS OF THE COUNTY-Debt Limit," herein.

PROPERTY TAX LEVY LIMITS

Property Tax Levy Rate Limit Limits have been imposed on the property tax levy rates for Wisconsin counties. There are separate limits for the operating levy and the debt service levy. The baseline for the limits is the actual 1992 tax rate adopted for the 1993 budget. The operating levy rate and the debt levy rate cannot exceed the baseline rates unless the county qualifies for one of the exceptions allowed under the statute, as described below. The statute establishes specific penalties for failure to meet the freeze requirements. Among the penalties for exceeding the limits is reduction of state shared revenues and transportation aids. The operating levy rate can be exceeded only if responsibility for services is transferred to the county from another governmental unit (transfers by the county to other governmental units reduce the maximum rate) or if an increase in the maximum rate is approved at referendum. The debt service rate limit can be exceeded to the extent necessary to pay debt service on obligations authorized or issued prior to the effective date of the State's 1993-95 budget bill (August 12, 1993). Additional general obligation bonds or notes can be issued only if one of the following conditions is met: (a) the bonds or notes are approved at a referendum, (b) the county board adopts a resolution that sets forth its reasonable expectation that the issuance will not cause the county to exceed its debt levy rate limit, (c) the debt is issued for regional projects, (d) the debt is issued to refund existing debt or (e) the resolution authorizing the debt is approved by a vote of at least 3/4 of the members-elect of the county board. In addition, counties generally are prohibited from using the proceeds of general obligation bonds or notes to fund the operating expenses of the general fund of the county or to fund the operating expenses of any special revenue fund of the county that is supported by property taxes, although this prohibition does not apply to notes issued to pay unfunded prior service liability contributions. The Tax-Exempt Bonds are being issued to refund existing debt. Therefore, the taxes levied to pay debt service on the Tax-Exempt Bonds are not subject to the debt levy rate limit. In connection with the Tax-Exempt Notes and the Taxable Notes, the Resolutions authorizing the Tax- Exempt Notes and the Taxable Notes will be adopted by a ¾ vote of the County Board. Therefore, taxes levied to pay debt service on the Tax-Exempt Notes and the Taxable Notes are not subject to the tax levy rate limit. Levy Limits

Section 66.0602 of the Wisconsin Statutes imposes a limit on property tax levies by cities, villages, towns and counties. No city, village, town or county is permitted to increase its tax levy by a percentage that exceeds its valuation factor (which is defined as a percentage equal to the greater of the percentage change in the political subdivision's January 1 equalized value due to new construction less improvements removed or zero percent). The base amount in any year to which the levy limit applies is the actual levy for the immediately preceding year. This levy limitation is an overall limit, applying to levies for operations as well as for other purposes.

13

A political subdivision that did not levy its full allowable levy in the prior year can carry forward the difference between the allowable levy and the actual levy, up to a maximum of 0.5% of the prior year's actual levy.

Special provisions are made with respect to property taxes levied to pay general obligation debt service. Those are described below. In addition, the statute provides for certain other exclusions from and adjustments to the tax levy limit. Among the items excluded from the limit are amounts levied for any revenue shortfall for debt service on a revenue bond issued under Section 66.0621. Among the adjustments permitted is an adjustment applicable when a tax increment district terminates, which allows an amount equal to the prior year's allowable levy multiplied by 50% of the political subdivision's percentage growth due to the district's termination.

With respect to general obligation debt service, the following provisions are made:

(a) If a political subdivision's levy for the payment of general obligation debt service, including debt

service on debt issued or reissued to fund or refund outstanding obligations of the political subdivision and interest on outstanding obligations of the political subdivision, on debt originally issued before July 1, 2005, is less in the current year than in the previous year, the political subdivision is required to reduce its levy limit in the current year by the amount of the difference between the previous year's levy and the current year's levy.

(b) For obligations authorized before July 1, 2005, if the amount of debt service in the preceding year is

less than the amount of debt service needed in the current year, the levy limit is increased by the difference between the two amounts. This adjustment is based on scheduled debt service rather than the amount actually levied for debt service (after taking into account offsetting revenues such as sales tax revenues, special assessments, utility revenues, tax increment revenues or surplus funds). Therefore, the levy limit could negatively impact political subdivisions that experience a reduction in offsetting revenues.

(c) The levy limits do not apply to property taxes levied to pay debt service on general obligation debt

authorized on or after July 1, 2005.

The Securities will be authorized after July 1, 2005.

SALES TAX Under Wisconsin Statutes, counties may charge a 1/2 of 1% sales tax. Collection and administrative functions are performed by the State. The Board of Supervisors has not approved a County sales tax.

14

THE RESOLUTIONS The following is a summary of certain provisions of the Resolutions adopted by the County Board of Supervisors (the “Board”) pursuant to the procedures prescribed by Wisconsin Statutes. Reference is made to the Resolutions for a complete recital of their terms. Tax-Exempt Bonds By way of a Resolution adopted on February 26, 2013 (the “Award Resolution for the Tax-Exempt Bonds”), the County Board authorized the issuance of the Tax-Exempt Bonds, awarded the sale of the Tax-Exempt Bonds to the Underwriter, provided the details and form of the Tax-Exempt Bonds, and set out certain covenants with respect thereto. The Award Resolution for the Tax-Exempt Bonds pledges the full faith, credit and resources of the County to payments of the principal of and interest on the Tax-Exempt Bonds. Pursuant to the Award Resolution for the Tax-Exempt Bonds, the amount of direct, annual, irrepealable taxes levied for collection in the years 2013 through 2026 which will be sufficient to meet the principal and interest payments on the Tax-Exempt Bonds when due will be specified (or monies otherwise appropriated). The Award Resolution for the Tax-Exempt Bonds establishes separate and distinct from all other funds of the County a debt service fund with respect to payment of principal of and interest on the Tax-Exempt Bonds. Tax-Exempt Notes By way of a Resolution adopted on February 26, 2013 (the “Award Resolution for the Tax-Exempt Notes”), the County Board authorized the issuance of the Tax-Exempt Notes, awarded the sale of the Tax-Exempt Notes to the Underwriter, provided the details and form of the Tax-Exempt Notes, and set out certain covenants with respect thereto. The Award Resolution for the Tax-Exempt Notes pledges the full faith, credit and resources of the County to payments of the principal of and interest on the Tax-Exempt Notes. Pursuant to the Award Resolution for the Tax-Exempt Notes, the amount of direct, annual, irrepealable taxes levied for collection in the years 2013 through 2023 which will be sufficient to meet the principal and interest payments on the Tax-Exempt Notes when due will be specified (or monies otherwise appropriated). The Award Resolution for the Tax-Exempt Notes establishes separate and distinct from all other funds of the County a debt service fund with respect to payment of principal of and interest on the Tax-Exempt Notes. Taxable Notes By way of a Resolution adopted on February 26, 2013 (the “Award Resolution for the Taxable Notes”), the County Board authorized the issuance of the Taxable Notes, awarded the sale of the Taxable Notes to the Underwriter, provided the details and form of the Taxable Notes, and set out certain covenants with respect thereto. The Award Resolution for the Taxable Notes pledges the full faith, credit and resources of the County to payments of the principal of and interest on the Taxable Notes. Pursuant to the Award Resolution for the Taxable Notes, the amount of direct, annual, irrepealable taxes levied for collection in the years 2013 through 2023 which will be sufficient to meet the principal and interest payments on the Notes when due will be specified (or monies otherwise appropriated). The Award Resolution for the Taxable Notes establishes separate and distinct from all other funds of the County a debt service fund with respect to payment of principal of and interest on the Taxable Notes.

15

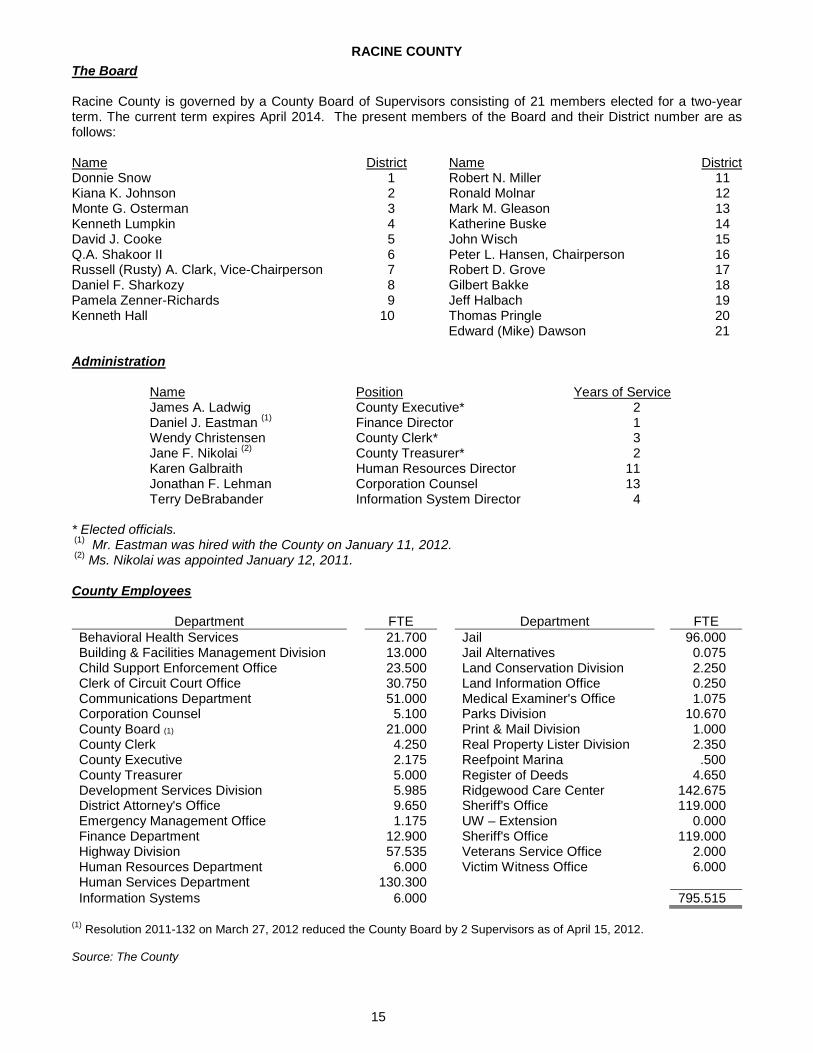

RACINE COUNTY

The Board Racine County is governed by a County Board of Supervisors consisting of 21 members elected for a two-year term. The current term expires April 2014. The present members of the Board and their District number are as follows: Name District Name District Donnie Snow 1 Robert N. Miller 11 Kiana K. Johnson 2 Ronald Molnar 12 Monte G. Osterman 3 Mark M. Gleason 13 Kenneth Lumpkin 4 Katherine Buske 14 David J. Cooke 5 John Wisch 15 Q.A. Shakoor II 6 Peter L. Hansen, Chairperson 16 Russell (Rusty) A. Clark, Vice-Chairperson 7 Robert D. Grove 17 Daniel F. Sharkozy 8 Gilbert Bakke 18 Pamela Zenner-Richards 9 Jeff Halbach 19 Kenneth Hall 10 Thomas Pringle 20 Edward (Mike) Dawson 21 Administration

Name Position Years of Service James A. Ladwig County Executive* 2 Daniel J. Eastman (1) Finance Director 1 Wendy Christensen County Clerk* 3 Jane F. Nikolai (2) County Treasurer* 2 Karen Galbraith Human Resources Director 11 Jonathan F. Lehman Corporation Counsel 13 Terry DeBrabander Information System Director 4

* Elected officials. (1) Mr. Eastman was hired with the County on January 11, 2012. (2) Ms. Nikolai was appointed January 12, 2011. County Employees

Department FTE Department FTE Behavioral Health Services 21.700 Jail 96.000 Building & Facilities Management Division 13.000 Jail Alternatives 0.075 Child Support Enforcement Office 23.500 Land Conservation Division 2.250 Clerk of Circuit Court Office 30.750 Land Information Office 0.250 Communications Department 51.000 Medical Examiner's Office 1.075 Corporation Counsel 5.100 Parks Division 10.670 County Board (1) 21.000 Print & Mail Division 1.000 County Clerk 4.250 Real Property Lister Division 2.350 County Executive 2.175 Reefpoint Marina .500 County Treasurer 5.000 Register of Deeds 4.650 Development Services Division 5.985 Ridgewood Care Center 142.675 District Attorney's Office 9.650 Sheriff's Office 119.000 Emergency Management Office 1.175 UW – Extension 0.000 Finance Department 12.900 Sheriff's Office 119.000 Highway Division 57.535 Veterans Service Office 2.000 Human Resources Department 6.000 Victim Witness Office 6.000 Human Services Department 130.300 Information Systems 6.000 795.515

(1) Resolution 2011-132 on March 27, 2012 reduced the County Board by 2 Supervisors as of April 15, 2012. Source: The County

16

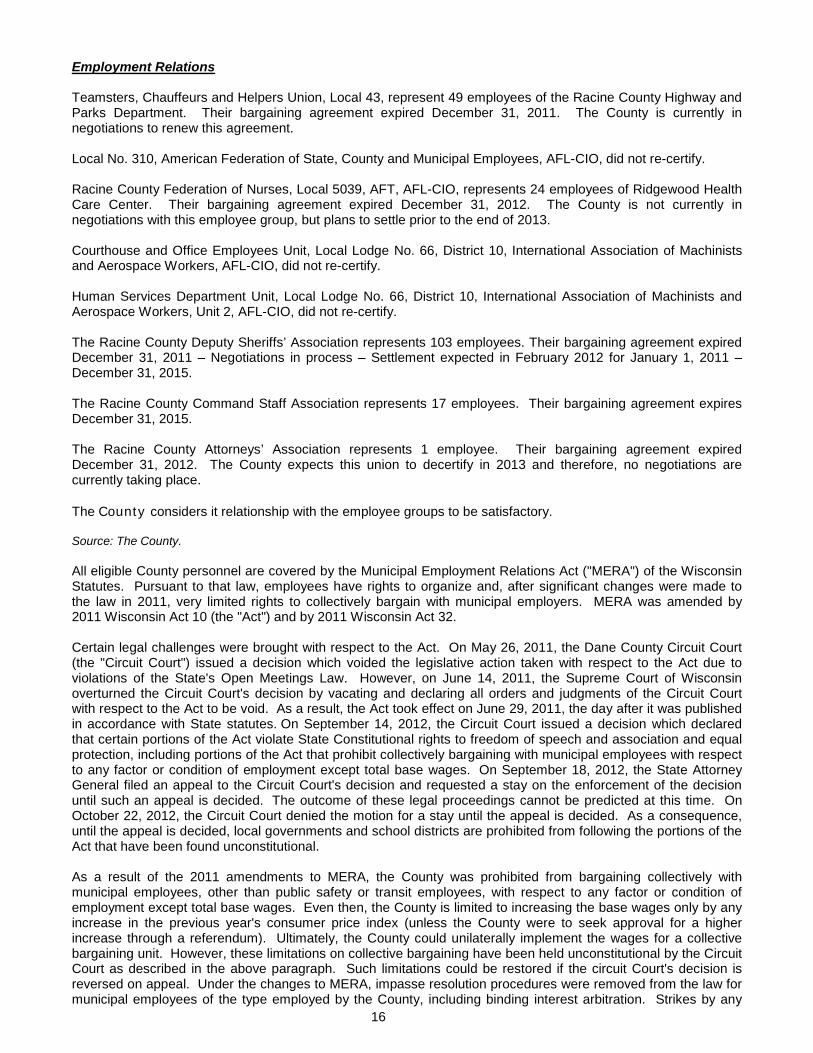

Employment Relations Teamsters, Chauffeurs and Helpers Union, Local 43, represent 49 employees of the Racine County Highway and Parks Department. Their bargaining agreement expired December 31, 2011. The County is currently in negotiations to renew this agreement. Local No. 310, American Federation of State, County and Municipal Employees, AFL-CIO, did not re-certify. Racine County Federation of Nurses, Local 5039, AFT, AFL-CIO, represents 24 employees of Ridgewood Health Care Center. Their bargaining agreement expired December 31, 2012. The County is not currently in negotiations with this employee group, but plans to settle prior to the end of 2013. Courthouse and Office Employees Unit, Local Lodge No. 66, District 10, International Association of Machinists and Aerospace Workers, AFL-CIO, did not re-certify. Human Services Department Unit, Local Lodge No. 66, District 10, International Association of Machinists and Aerospace Workers, Unit 2, AFL-CIO, did not re-certify. The Racine County Deputy Sheriffs’ Association represents 103 employees. Their bargaining agreement expired December 31, 2011 – Negotiations in process – Settlement expected in February 2012 for January 1, 2011 – December 31, 2015. The Racine County Command Staff Association represents 17 employees. Their bargaining agreement expires December 31, 2015. The Racine County Attorneys’ Association represents 1 employee. Their bargaining agreement expired December 31, 2012. The County expects this union to decertify in 2013 and therefore, no negotiations are currently taking place. The County considers it relationship with the employee groups to be satisfactory. Source: The County. All eligible County personnel are covered by the Municipal Employment Relations Act ("MERA") of the Wisconsin Statutes. Pursuant to that law, employees have rights to organize and, after significant changes were made to the law in 2011, very limited rights to collectively bargain with municipal employers. MERA was amended by 2011 Wisconsin Act 10 (the "Act") and by 2011 Wisconsin Act 32. Certain legal challenges were brought with respect to the Act. On May 26, 2011, the Dane County Circuit Court (the "Circuit Court") issued a decision which voided the legislative action taken with respect to the Act due to violations of the State's Open Meetings Law. However, on June 14, 2011, the Supreme Court of Wisconsin overturned the Circuit Court's decision by vacating and declaring all orders and judgments of the Circuit Court with respect to the Act to be void. As a result, the Act took effect on June 29, 2011, the day after it was published in accordance with State statutes. On September 14, 2012, the Circuit Court issued a decision which declared that certain portions of the Act violate State Constitutional rights to freedom of speech and association and equal protection, including portions of the Act that prohibit collectively bargaining with municipal employees with respect to any factor or condition of employment except total base wages. On September 18, 2012, the State Attorney General filed an appeal to the Circuit Court's decision and requested a stay on the enforcement of the decision until such an appeal is decided. The outcome of these legal proceedings cannot be predicted at this time. On October 22, 2012, the Circuit Court denied the motion for a stay until the appeal is decided. As a consequence, until the appeal is decided, local governments and school districts are prohibited from following the portions of the Act that have been found unconstitutional. As a result of the 2011 amendments to MERA, the County was prohibited from bargaining collectively with municipal employees, other than public safety or transit employees, with respect to any factor or condition of employment except total base wages. Even then, the County is limited to increasing the base wages only by any increase in the previous year's consumer price index (unless the County were to seek approval for a higher increase through a referendum). Ultimately, the County could unilaterally implement the wages for a collective bargaining unit. However, these limitations on collective bargaining have been held unconstitutional by the Circuit Court as described in the above paragraph. Such limitations could be restored if the circuit Court's decision is reversed on appeal. Under the changes to MERA, impasse resolution procedures were removed from the law for municipal employees of the type employed by the County, including binding interest arbitration. Strikes by any

17

municipal employee or labor organization are expressly prohibited. As a practical matter, it is anticipated that strikes will be rare. Furthermore, if strikes do occur, they may be enjoined by the courts. Additionally, because the only legal subject of bargaining is the base wage rates, all bargaining over items such as just cause, benefits, and terms of conditions of employment are prohibited and cannot be included in a collective bargaining agreement. Other Post Employment Benefits The County provides "other post-employment benefits" ("OPEB") (i.e., post-employment benefits, other than pension benefits, owed to its employees and former employees) through a single-employer defined benefit plan to employees who have terminated their employment with the County and have satisfied specified eligibility standards. Membership of the plan consisted of 548 retirees receiving benefits and 710 active plan members as of January 1, 2011, the date of the latest actuarial valuation. OPEB calculations are required to be updated every [two/three] years and prepared in accordance with Statement No. 45 of the Governmental Accounting Standards Board (“GASB 45”) regarding retiree health and life insurance benefits, and related standards. An OPEB study for the County was last completed as of December 31, 2011

County made changes effective January 1, 2013 that would impact below info, however it is unquantifiable at this time.

The information summarized in the remainder of this section, below, is taken from the County’s audited financial statements for the year ended December 31, 2011 ("Fiscal Year 2011"). Potential investors should note that, per the above-described changes limiting eligibility for post-employment health benefits, the County anticipates that the annual required contribution and actuarial accrued liability for benefits described below will decrease.

The County is required to expense the estimated yearly cost of providing post-retirement benefits representing a level of funding that, if paid on an ongoing basis, is project to cover costs and amortize unfunded actuarial liabilities over an a given period not to exceed 30 years. Such annual accrual expense is referred to as the "annual required contribution." As shown in the County’s Financial Statements for Fiscal Year 2011, the County’s annual required contribution was $16,212,518. For Fiscal Year 2011, contributions to the plan totaled $6,951,765, which was 42.9% of the annual required contribution. The County’s funding practice has been to fully fund the yearly amount of benefit premiums on a "pay-as-you-go-basis." The plan's ratio of actuarial value of assets to actuarial accrued liability for benefits (the "Funded Ratio") as of the most recent actuarial valuation date, was 0%. As of December 31, 2011 the actuarial accrued liability was $258,502,255, and the actuarial value of assets was $0, resulting in an unfunded actuarial accrued liability of $258,502,255. For more information, see Note IV.E. in "Appendix A - Basic Financial Statements and Related Notes for the Year Ended December 31, 2011" attached hereto.

18

GENERAL INFORMATION

Location Racine County is located in southeastern Wisconsin, approximately 30 miles south of Milwaukee and 60 miles north of Chicago and is bounded on the east by Lake Michigan. The County encompasses an area of 337 square miles and consists of two cities, seven villages and nine towns. Interstate Highway 94 links Racine County with Milwaukee and Chicago, while U.S. Highway 45 and State Highways 11, 20, 31, 32, 36, 38 and 83 intersect the County. Racine is located along the Lake Michigan shoreline, between the Milwaukee and Chicago Metropolitan areas. A picturesque lakefront and harbor make Racine not only pleasurable, but a rewarding, relaxing and recreational place to visit. History Woodland Indians and their descendants were early inhabitants of Racine County. In the latter half of the 17th Century, French fur traders and missionaries, such as Nicholas Perrot and Fathers Claude Allouez and Jacques Marquette, found predominately Miami Indians inhabiting the lands along Racine's Root River. By 1720, the Miami tribe had moved on and the area became the home of the Potawatomi Indians. It was with the Potawatomi at Skunk Grove that Jacques Vieaux and Louis Vieaux set up fur trade in the Old Northwest Territory in the late 1820's. A historic marker has been placed at the site of the Vieaux's fur-trading post in the Town of Mount Pleasant. Following the Black Hawk War in 1832, "Wisconsin fever" enticed many pioneers from Western New York State, rural New England and Britain including Captain Knapp who founded the settlement of Port Gilbert at the junction of the Root River and Lake Michigan. The name Port Gilbert never gained acceptance over the earlier Indian designation of Chippecotton (Root River) or its French version Racine and, in 1841, the community was incorporated as Racine. The railroads came and continued to serve in transporting the diverse products of Racine County's industries: auto parts, engines, foundry products, printed materials, household and personal care products, garden equipment, machine parts and scores of others. The earliest schools were private, the first opening in 1836. In 1837, Racine County was divided into school districts and the first public school was constructed in 1842 on part of the present site of the award winning County Court House. The first high school was built by Lucas Bradley in 1853 in this area and produced the first high school graduates in the State. Education Thirteen school districts serve the County, educating students in kindergarten through the twelfth grade. The Racine Unified School District is the largest district in the County, with an estimated enrollment for the 2012-2013 school year of 21,691 students. Higher Education Higher education is available at the following post-secondary educational facilities located within 30 miles of the County: Alverno College, Medical College of Wisconsin, Cardinal Stritch College, Carthage College, Concordia College, Gateway Technical College, Marquette University, Milwaukee School of Engineering, Mount Mary College, University of Wisconsin - Milwaukee, the University of Wisconsin – Parkside and Wisconsin Lutheran College. Health Facilities A complete range of health facilities and professionals serves Racine County communities. Four hospitals provide expert care to county residents: The A-Center, St. Luke's Memorial Hospital, St. Mary's Medical Center, Racine, and Memorial Hospital, Burlington. Also five clinics provide a variety of health services for area communities. Of special interest is the New Medico Rehabilitation Center of Wisconsin, a residential community re-entry program for head-injured individuals, located in the Town of Dover. Finally, St. Luke's Memorial Hospital, Racine, provides landing facilities for the "Flight for Life" helicopter. This helicopter is specially staffed and equipped to provide airborne emergency service to critically ill or injured patients.

19

DEMOGRAPHIC AND ECONOMIC INFORMATION Population

Racine County Estimate, 2012 195,386 Estimate, 2011 195,225 Census, 2010 195,408 Estimate, 2009 196,380 Estimate, 2008 196,321

Source: Wisconsin Department of Administration, Demographic Services Center. Per Return Adjusted Gross Income

State of Racine Wisconsin County

2010 $46,958 $47,358 2009 45,372 46,215 2008 47,046 50,061 2007 48,985 49,266 2006 48,107 48,154

Source: Wisconsin Department of Revenue, Division of Research and Policy. Unemployment Rate

State of Racine Wisconsin County December, 2012 6.5% 8.3% December, 2011 6.6 7.9 Est. Average 2012 6.9% 8.5% Average, 2011 7.5 9.1 Average, 2010 8.1 9.7 Average, 2009 8.5 10.1 Average, 2008 4.7 5.6

Source: Wisconsin Department of Workforce Development.

20

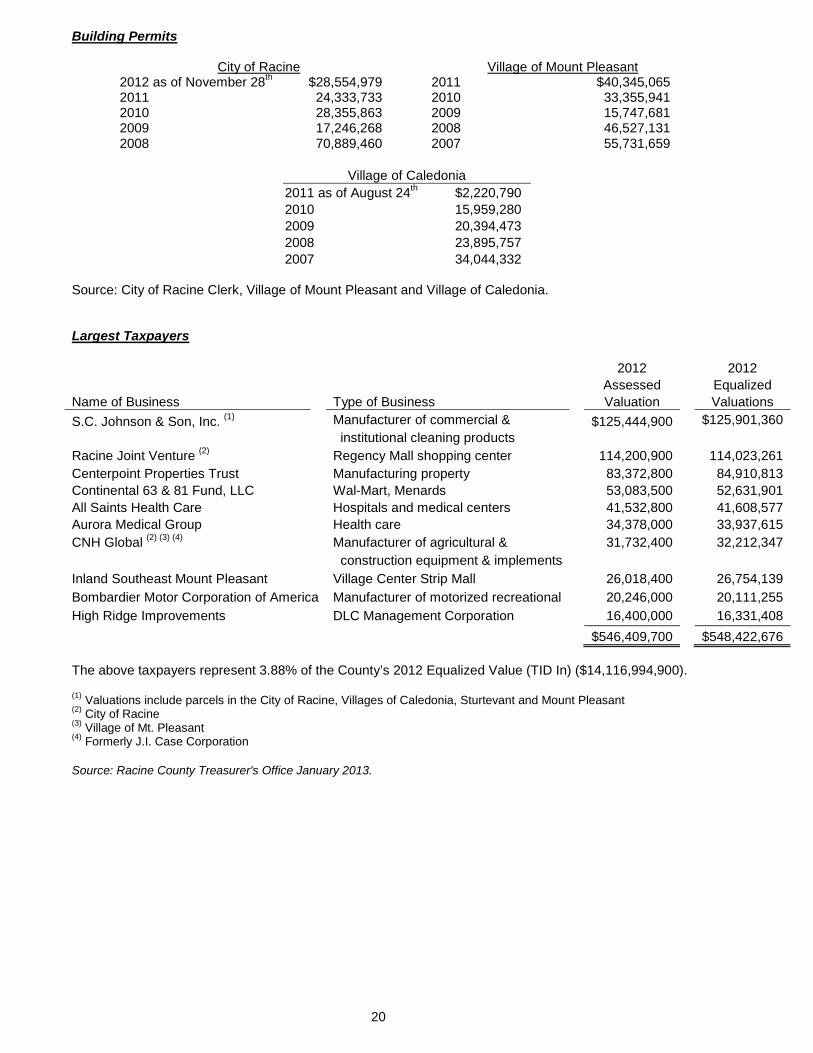

Building Permits

City of Racine Village of Mount Pleasant 2012 as of November 28th $28,554,979 2011 $40,345,065 2011 24,333,733 2010 33,355,941 2010 28,355,863 2009 15,747,681 2009 17,246,268 2008 46,527,131 2008 70,889,460 2007 55,731,659

Village of Caledonia

2011 as of August 24th $2,220,790 2010 15,959,280 2009 20,394,473 2008 23,895,757 2007 34,044,332

Source: City of Racine Clerk, Village of Mount Pleasant and Village of Caledonia. Largest Taxpayers

2012

2012

Assessed

Equalized

Name of Business

Type of Business

Valuation

Valuations S.C. Johnson & Son, Inc. (1)

Manufacturer of commercial &

$125,444,900

$125,901,360

institutional cleaning products

Racine Joint Venture (2)

Regency Mall shopping center

114,200,900

114,023,261 Centerpoint Properties Trust

Manufacturing property

83,372,800

84,910,813

Continental 63 & 81 Fund, LLC

Wal-Mart, Menards

53,083,500

52,631,901 All Saints Health Care

Hospitals and medical centers

41,532,800

41,608,577

Aurora Medical Group

Health care

34,378,000

33,937,615 CNH Global (2) (3) (4)

Manufacturer of agricultural &

31,732,400

32,212,347

construction equipment & implements

Inland Southeast Mount Pleasant

Village Center Strip Mall

26,018,400

26,754,139 Bombardier Motor Corporation of America Manufacturer of motorized recreational

20,246,000

20,111,255

High Ridge Improvements

DLC Management Corporation

16,400,000

16,331,408

$546,409,700

$548,422,676

The above taxpayers represent 3.88% of the County’s 2012 Equalized Value (TID In) ($14,116,994,900). (1) Valuations include parcels in the City of Racine, Villages of Caledonia, Sturtevant and Mount Pleasant (2) City of Racine (3) Village of Mt. Pleasant (4) Formerly J.I. Case Corporation Source: Racine County Treasurer's Office January 2013.

21

Largest Employers Listed below are the largest employers in the Racine County area. Number of Employer Name Type of Business Employees All Saints Health Care Center Health care services 2,701 CNH Global(1) Manufacturer of agricultural and construction equipment and implements 2,650 Racine School District Education 2,625 SC Johnson & Son, Inc. Manufacturer of commercial and institutional cleaning products 1,496 Wheaton Franciscan Healthcare Hospital 1,079 Gateway Technical College (2) Vocational education 1,042 In-Sink-Erator Division, Manufacturer of household and commercial Emerson Electric Company disposer systems, hot water dispensers 1,000 Twin Disc Inc. Manufactures hydraulic torque converters 802 Racine County Government 795 City of Racine Municipal government 790 Modine Manufacturing Heat exchanger manufacturing 650 Wal-Mart Retail Stores in Racine & Burlington 500-998 BRP US Inc Manufactures engine equipment 500 Rudd Lighting Manufactures industrial, commercial & 450 residential lighting fixtures

(1) Formerly known as J.I. Case Corporation. (2) Includes full and part-time. Source: 2012 Wisconsin Manufacturers and 2012 Business Service Directories. WI WorkNet website and January 2013 Direct Employer Inquiries.

22

TAX LEVIES, RATES AND COLLECTIONS In November of each year, the County Board adopts an annual budget for the ensuing calendar year. At that time levies on real estate and personal property for county taxes are set which, when collected in the ensuing year, will be sufficient to cover budgeted operating expenses, debt service, contingency fund and other expenditures of the County. Taxes on real estate and personal property become due on January 1 of each year and become delinquent after the first day of February of each year. A taxpayer may elect, as is his right, to pay his annual real estate property taxes in two installments. The first installment becomes delinquent after January 31, and the last installment becomes delinquent after July 31 of each year. Special assessment taxes must be paid in full by January 31 of each year. The towns, villages and cities in Racine County turn over uncollected real estate and special assessment taxes to Racine County on February 15 of each year. Racine County reimburses the municipalities 100% for postponed and delinquent real estate taxes. Delinquent personal property taxes are collected by the towns, villages and cities. Set forth below are tax levies for County purposes and the tax rate per $1,000 equalized valuation on all taxable property in Racine County for collection years 2009-2013:

Total Uncollected Taxes Percent of

Levy

Collection

County County County-wide As of Levy Year

Year

Tax Rate Levy* Levy* December 31, 2012 Collected

2012

2013

$3.54 $51,011,985 $338,189,017 -To Be Collected- 2011

2012

3.38 50,900,547 329,272,692 $7,358,848 97.77%

2010

2011

3.48 50,831,349 322,502,719 3,864,358 98.80 2009

2010

3.34 50,939,395 318,063,935 1,900,577 99.40

2008

2009

3.31 50,786,176 305,393,464 724,233 99.76 * Includes County, Cities, Villages, Towns, School Districts, and Technical College Districts net of State Tax Credits. These figures do not include special assessments or charges or special tax districts not subject to a mill rate. Source: The County.

EQUALIZED VALUATIONS All equalized valuations of property in the State of Wisconsin are determined by the State of Wisconsin, Department of Revenue, Supervisor of Assessments Office. Equalized valuations are the State's estimate of full market value. The State determines assessed valuations of all manufacturing property in the State. Assessed valuations of residential and commercial property are determined by local assessors. Residential and commercial property located within the County are assessed annually by the local assessors. At hearings held each year a taxpayer may appeal the assessment of his property to the Board of Review of the local municipality. The Board of Review consists of local assessors and local officials. The assessors do not have a vote on final determinations. Set forth in the table below are equalized valuations of all property located within the County for the years 2008 through 2012. The County's Equalized Valuation has decreased by 11.73 percent since 2008 with an annual average decrease of 3.07 percent

Year

Equalized Valuation (TID-IN)

Equalized Valuation (TID-OUT)

2012

$14,116,994,900

$13,463,629,150 2011

15,041,416,400

14,418,248,850

2010

15,228,632,600

14,597,854,550 2009

15,912,047,700

15,216,512,450

2008

15,992,707,300

15,327,604,350 Source: Wisconsin Department of Revenue.

23

The equalized valuation by class in the County for 2012 is as follows:

Amount

Percent of Total

Real Estate Residential

$10,554,091,100

74.76% Commercial

2,538,531,400

17.98

Manufacturing

430,052,000

3.05 Agricultural, Forest, Other

284,344,700

2.01

Total Real Estate

$13,807,019,200

97.80% Total Personal Property

$309,975,700

2.20%

Total

$14,116,994,900

100.00% Source: Wisconsin Department of Revenue.

TAX INCREMENT DISTRICTS Seven municipalities in the County have created Tax Increment Districts (TIDs) under Wisconsin Statute 66.1105. TID valuations totaling $653,365,750 have been excluded from the County’s tax base for 2012.

(2012)

TID

Year

Base

Current

Municipality

Number

Created

Value

Increment

Value Village of Mount Pleasant

01

2006

$4,292,700

$42,534,500

$46,827,200

Village of Mount Pleasant

02

2007

99,636,000

57,139,900

156,775,900

Village of Sturtevant

03

1994

9,157,700

163,664,800

172,822,500

Village of Union Grove

03

2001

1,882,400

7,433,000

9,315,400 Village of Union Grove

04

2006

31,932,700

*

30,406,000

Village of Waterford

02

2000

13,788,800

30,302,300

44,091,100

City of Burlington

03

1992

131,478,900

170,311,700

301,790,600 City of Burlington

001E

2010

1,753,900

$1,913,400

3,667,300

City of Racine

02

1983

2,394,700

31,186,500

33,581,200 City of Racine

05

1985

0

16,329,100

16,329,100

City of Racine

06

1987

21,660,400

21,386,500

43,046,900 City of Racine

07

1989

1,899,600

41,465,900

43,365,500

City of Racine

08

1990

11,338,350

21,576,950

32,915,300 City of Racine

09

2000

877,600

29,693,500

30,571,100

City of Racine

10

2003

1,180,400

*

787,300 City of Racine

11

2005

3,179,700

*

2,529,200

City of Racine

12

2006

378,000

6,341,200

6,719,200 City of Racine

13

2006

312,300

9,472,800

9,785,100

City of Racine

14

2006

4,103,200

$342,700

4,445,900 City of Racine

15

2006

0

*

0

City of Racine

16

2009

38,217,400

2,271,000

40,488,400

Village of Caledonia

01

2007

14,038,300

*

12,651,600 Village of Caledonia

02

2007

337,500

*

300,400

Village of Caledonia

03

2011

28,644,200

*

27,939,500

TOTAL

$318,556,050

$653,365,750

$1,071,151,700

* Per the Wisconsin Department of Revenue, this District has a zero or negative increment. Source: Wisconsin Department of Revenue.

24

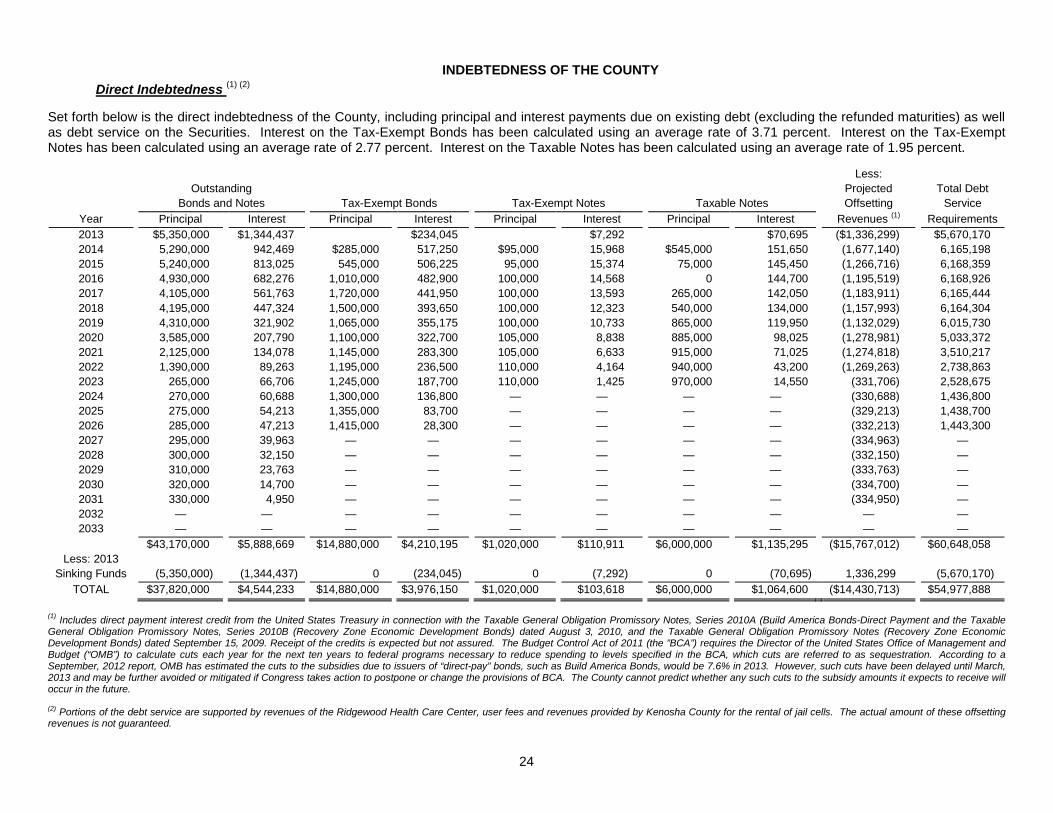

INDEBTEDNESS OF THE COUNTY

Direct Indebtedness (1) (2)

Set forth below is the direct indebtedness of the County, including principal and interest payments due on existing debt (excluding the refunded maturities) as well as debt service on the Securities. Interest on the Tax-Exempt Bonds has been calculated using an average rate of 3.71 percent. Interest on the Tax-Exempt Notes has been calculated using an average rate of 2.77 percent. Interest on the Taxable Notes has been calculated using an average rate of 1.95 percent.

Less: Outstanding Projected Total Debt Bonds and Notes Tax-Exempt Bonds Tax-Exempt Notes Taxable Notes Offsetting Service

Year Principal Interest Principal Interest Principal Interest Principal Interest Revenues (1) Requirements 2013 $5,350,000 $1,344,437 $234,045 $7,292 $70,695 ($1,336,299) $5,670,170 2014 5,290,000 942,469 $285,000 517,250 $95,000 15,968 $545,000 151,650 (1,677,140) 6,165,198 2015 5,240,000 813,025 545,000 506,225 95,000 15,374 75,000 145,450 (1,266,716) 6,168,359 2016 4,930,000 682,276 1,010,000 482,900 100,000 14,568 0 144,700 (1,195,519) 6,168,926 2017 4,105,000 561,763 1,720,000 441,950 100,000 13,593 265,000 142,050 (1,183,911) 6,165,444 2018 4,195,000 447,324 1,500,000 393,650 100,000 12,323 540,000 134,000 (1,157,993) 6,164,304 2019 4,310,000 321,902 1,065,000 355,175 100,000 10,733 865,000 119,950 (1,132,029) 6,015,730 2020 3,585,000 207,790 1,100,000 322,700 105,000 8,838 885,000 98,025 (1,278,981) 5,033,372 2021 2,125,000 134,078 1,145,000 283,300 105,000 6,633 915,000 71,025 (1,274,818) 3,510,217 2022 1,390,000 89,263 1,195,000 236,500 110,000 4,164 940,000 43,200 (1,269,263) 2,738,863 2023 265,000 66,706 1,245,000 187,700 110,000 1,425 970,000 14,550 (331,706) 2,528,675 2024 270,000 60,688 1,300,000 136,800 — — — — (330,688) 1,436,800 2025 275,000 54,213 1,355,000 83,700 — — — — (329,213) 1,438,700 2026 285,000 47,213 1,415,000 28,300 — — — — (332,213) 1,443,300 2027 295,000 39,963 — — — — — — (334,963) — 2028 300,000 32,150 — — — — — — (332,150) — 2029 310,000 23,763 — — — — — — (333,763) — 2030 320,000 14,700 — — — — — — (334,700) — 2031 330,000 4,950 — — — — — — (334,950) — 2032 — — — — — — — — — — 2033 — — — — — — — — — —

$43,170,000 $5,888,669 $14,880,000 $4,210,195 $1,020,000 $110,911 $6,000,000 $1,135,295 ($15,767,012) $60,648,058 Less: 2013

Sinking Funds (5,350,000) (1,344,437) 0 (234,045) 0 (7,292) 0 (70,695) 1,336,299 (5,670,170) TOTAL $37,820,000 $4,544,233 $14,880,000 $3,976,150 $1,020,000 $103,618 $6,000,000 $1,064,600 ($14,430,713) $54,977,888

(1) Includes direct payment interest credit from the United States Treasury in connection with the Taxable General Obligation Promissory Notes, Series 2010A (Build America Bonds-Direct Payment and the Taxable General Obligation Promissory Notes, Series 2010B (Recovery Zone Economic Development Bonds) dated August 3, 2010, and the Taxable General Obligation Promissory Notes (Recovery Zone Economic Development Bonds) dated September 15, 2009. Receipt of the credits is expected but not assured. The Budget Control Act of 2011 (the ”BCA”) requires the Director of the United States Office of Management and Budget (“OMB”) to calculate cuts each year for the next ten years to federal programs necessary to reduce spending to levels specified in the BCA, which cuts are referred to as sequestration. According to a September, 2012 report, OMB has estimated the cuts to the subsidies due to issuers of “direct-pay” bonds, such as Build America Bonds, would be 7.6% in 2013. However, such cuts have been delayed until March, 2013 and may be further avoided or mitigated if Congress takes action to postpone or change the provisions of BCA. The County cannot predict whether any such cuts to the subsidy amounts it expects to receive will occur in the future. (2) Portions of the debt service are supported by revenues of the Ridgewood Health Care Center, user fees and revenues provided by Kenosha County for the rental of jail cells. The actual amount of these offsetting revenues is not guaranteed.

25

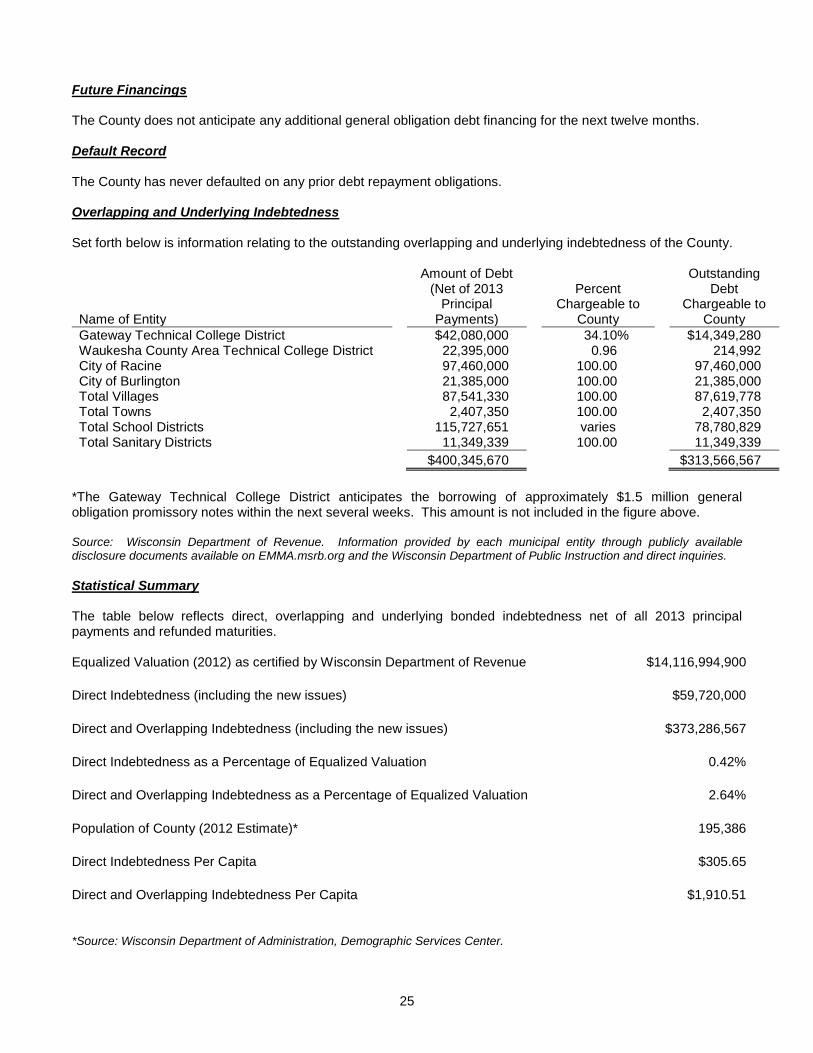

Future Financings The County does not anticipate any additional general obligation debt financing for the next twelve months. Default Record The County has never defaulted on any prior debt repayment obligations. Overlapping and Underlying Indebtedness Set forth below is information relating to the outstanding overlapping and underlying indebtedness of the County.

Name of Entity

Amount of Debt (Net of 2013

Principal Payments)

Percent Chargeable to

County

Outstanding Debt

Chargeable to County

Gateway Technical College District

$42,080,000

34.10%

$14,349,280 Waukesha County Area Technical College District

22,395,000

0.96

214,992

City of Racine

97,460,000

100.00

97,460,000 City of Burlington

21,385,000

100.00

21,385,000

Total Villages

87,541,330

100.00

87,619,778 Total Towns

2,407,350

100.00

2,407,350

Total School Districts

115,727,651

varies

78,780,829 Total Sanitary Districts

11,349,339

100.00

11,349,339

$400,345,670

$313,566,567

*The Gateway Technical College District anticipates the borrowing of approximately $1.5 million general obligation promissory notes within the next several weeks. This amount is not included in the figure above. Source: Wisconsin Department of Revenue. Information provided by each municipal entity through publicly available disclosure documents available on EMMA.msrb.org and the Wisconsin Department of Public Instruction and direct inquiries. Statistical Summary The table below reflects direct, overlapping and underlying bonded indebtedness net of all 2013 principal payments and refunded maturities. Equalized Valuation (2012) as certified by Wisconsin Department of Revenue $14,116,994,900

Direct Indebtedness (including the new issues) $59,720,000

Direct and Overlapping Indebtedness (including the new issues) $373,286,567

Direct Indebtedness as a Percentage of Equalized Valuation 0.42%

Direct and Overlapping Indebtedness as a Percentage of Equalized Valuation 2.64%

Population of County (2012 Estimate)* 195,386

Direct Indebtedness Per Capita $305.65

Direct and Overlapping Indebtedness Per Capita $1,910.51

*Source: Wisconsin Department of Administration, Demographic Services Center.

26

Debt Limit As described under the caption "CONSTITUTIONAL AND STATUTORY CONSIDERATIONS AND LIMITATIONS CONCERNING THE COUNTY'S POWER TO INCUR INDEBTEDNESS--Debt Limit," the total indebtedness of the County may not exceed five percent of the equalized value of property in the County. Set forth in the table below is a comparison of the outstanding indebtedness of County as of the closing of the Securities and net of refunded maturities, as a percentage of the applicable debt limit. Equalized Valuation (2012) as certified by Wisconsin Department of Revenue

$14,116,994,900

Legal Debt Percentage Allowed

5.00%

Legal Debt Limit

$705,849,745

General Obligation Debt Outstanding (including new issues)

$62,675,000

Unused Margin of Indebtedness

$643,174,745

Percent of Legal Debt Incurred

8.88%

Percentage of Legal Debt Available

91.12%

FINANCIAL INFORMATION The financial operations of the County are conducted primarily through its general fund. Most taxes and non-tax revenues (such as license fees, fines and costs and user's fees) are paid into the general fund and current operating expenditures are made from the general fund pursuant to appropriations made by the County Board of Supervisors. Budgeting Process The County is required by State law to annually formulate a budget and to hold public hearings thereon prior to the determination of the amounts to be financed, in whole or in part, by general property taxes, funds on hand or estimated revenues from other sources. The budget must list all existing indebtedness of the County and include anticipated revenues from all sources during the ensuing year, and must list all proposed appropriations for each department, activity and reserve account during the ensuing year. The budget must show actual revenues and expenditures for not less than the first six months of the current year and estimated revenues and expenditures for the balance of the current year. As part of the budgeting process, public hearings are held on the proposed budget, at which time any resident or taxpayer in the County may be heard. At an annual budget meeting in November of each year the County Board adopts the final budget for the succeeding year and levies taxes based on equalized valuations of property less any increment attributable to Tax Increment Districts. The amounts of taxes so levied and the amounts of the various appropriations in the final budget (after any alterations made pursuant to public hearings) may not be changed unless authorized by a vote of two-thirds of the entire membership of the County Board. Failure to publish notice of any such alteration within ten days thereafter shall preclude any change in the budget. Financial Records The County maintains its financial records on a calendar year basis. Appendix A hereto sets forth the financial statements of the County for the year ended December 31, 2011, which have been audited by CliftonLarsonAllen LLP, Certified Public Accountants and Consultants, Racine, Wisconsin (formerly Clifton Gunderson LLP). The County did not ask CliftonLarsonAllen LLP to perform any additional procedures in connection with this Official Statement.

27

__________________________________________________________________________________________ GENERAL FUND SUMMARY

FOR YEARS ENDED DECEMBER 31 _______________________________________________________________________________________________________________

2013

2012

2011

2010

2009

BUDGET

ESTIMATE

ACTUAL

ACTUAL

ACTUAL

Revenues Taxes $44,656,736

$44,519,373

$44,543,689

$44,272,047

$44,337,375

Intergovernmental 11,167,078

11,737,298

14,715,210

12,374,871

11,784,258 Fines and fees 8,037,612

7,706,755

7,660,295

7,545,658

6,961,700

Interest 214,401

813,893

4,120,323

3,316,144

3,278,222 Other 3,664,500

3,434,671

896,613

675,787

635,188

Total Revenues $67,740,327

$68,211,990

$71,936,130

$68,184,507

$66,996,743

Expenditures General government $15,080,476

$15,967,794

$15,726,460

$14,054,302

$19,873,265

Public safety 32,764,211

30,341,289

32,962,956

29,558,926

26,553,273 Health and social services 6,048,769

5,538,009

5,764,829

6,210,916

3,386,866

Education and recreation 4,181,055

4,592,255

4,151,309

4,093,839

4,095,969 Development 1,381,804

3,015,718

2,725,818

1,647,439

1,715,127

Highway and streets (Public Works) 848,600

936,413

629,808

684,656

— Capital Projects 2,687,090

2,812,523

—

—

—

Capital Outlay —

—

1,976,519

1,568,306

600,170

Total Expenditures $62,992,005