Embed Size (px)

Citation preview

Report No. 526a-IND FILE CP YlDAppraisal ofBank Pembangunan Indonesia(Bapindo)

October 22, 1974

East-Asia and Pacific Projects Departments

Not for Public Use

Document of the International Bank for Reconstruction and DevelopmentInternational Development Association

This report was prepared for official use only by the Bank Group. It may notbe published, quoted or cited without Bank Group authorization. The Bank Group doesnot accept responsibility for the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

US$1 a Rp 415Rp 1 = US$0.0024Rp 1 million = US$2,410Rp 1 billion - US$2.41 million

ABBREVIATIONS

ADB - Asian Development BankASKRINDO - Asuransi Credit IndonesiaBAPINDO - Bank Pembangunan IndonesiaBI - Bank IndonesiaBMI - Belgique Maatschappij voor InvesteeringEXIM - Bank Ekspor-Impor IndonesiaGOI - Government of IndonesiaICB - Investment Coordinating BoardIDA - International Development AssociationIDFC - Indonesian Development Finance CompanyINVESTASI - Investment Credit ProgramKfW - Kreditanstalt fur WiederaufbauMCD - Maritime Credit DepartmentPANN - National Fleet Development CorporationPDFCI - Private Development Finance Company of IndonesiaPELNI - Pelayaran Nasional IndonesiaPWCL - Permanent Working Capital LoanRDB - Regional Development BankREPELITA I - First Five-Year Development PlanREPELITA II - Second Five-Year Development PlanRLS - Regular Inter-Island Liner ServiceUNDP - United Nations Development ProgramWBG - World Bank Group

FISCAL YEAR

January 1 - December 31

INDONESIA

APPRAISAL OF BANK PEMBANGUNAN INDONESIA (BAPINDO)

Table of Contents

Page No.

BASIC DATA

SUMMARY, RECOMMENDATIONS, AND UNDERSTANDINGS REACHED .... i - iii

I. INTRODUCTION ............................................ 1

II. ECONOMIC, INDUSTRIAL AND FINANCIAL ENVIRONMENT .......... 2

Economic Environment .............. ................... . 2Industrial Environment ..... ....................... 3Financial Environment ......................... ... 5Financing for Small-Scale Industry ......... ........ 7I.nflation ......................................... 7Interest Rates .............. . ................ 8

III. INSTITUTIONAL ASPECTS ............... 9

BAPINDO Act ............ o ................... 9Policy Statement ...... ................ -.... . 9Organization Structure ....... . .......... . 9Supervisory Board, Management, and Staff ...... ...... 10Procedures .... o .................. ........... 12

r,V. OPERATIONS AND FINANCIAL CONDITION ._o............... 13

Summary of Operations ...... ........................ 13Industrial Loans .......... ...... . 14Maritime Sector Loans .. ............. o .............. 16Raw Cotton Loans ...... ............................ 17Equity Financing ...... o_ ......................... 17Resources .......................................... 18Financial Position . ............................... 18Profitability ....... .............................. 18Quality of Portfolio ... .......... ....... 19

This report was prepared by Messrs. Zamir Hasan, Promodh Malhotra, and Rainer 11.Ullmann, following their appraisal mission to BAPINDO in April 1974.

-2-

Page No.

V. PROSPECTS ....................................... 21

General Outlook ... ................................... 21BAPINDO's Business Forecasts ....................... 22Resource Requirements ............................ 23Projected Financial Position . ..... ........ 24Proposed Loan .................... ................... 24

LIST OF ANNEXES

1. Approvals and Implementation of Foreign Investment Projects bySector, 1967-1973

2. Approvals of Domestic Investment Projects by Sector, 1968-1973

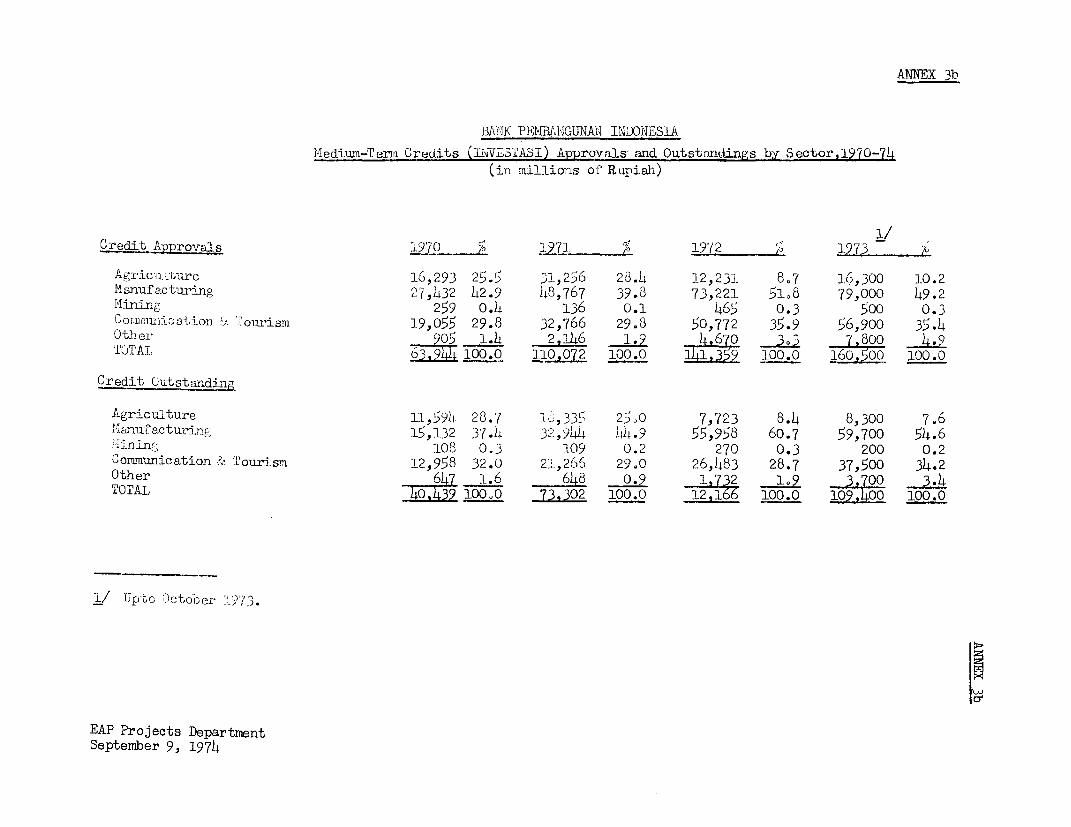

3. Medium-Term Investment Credit Program (INVESTASI)

3a. Medium-Term Credits (INVESTASI), 1970 - January 1974

3b. Medium-Term Credits (INVESTASI), Approvals and Outstandings by Sector,1970-1974

4. Development Banks in Indonesia

5. The Money and Capital Market in Indonesia

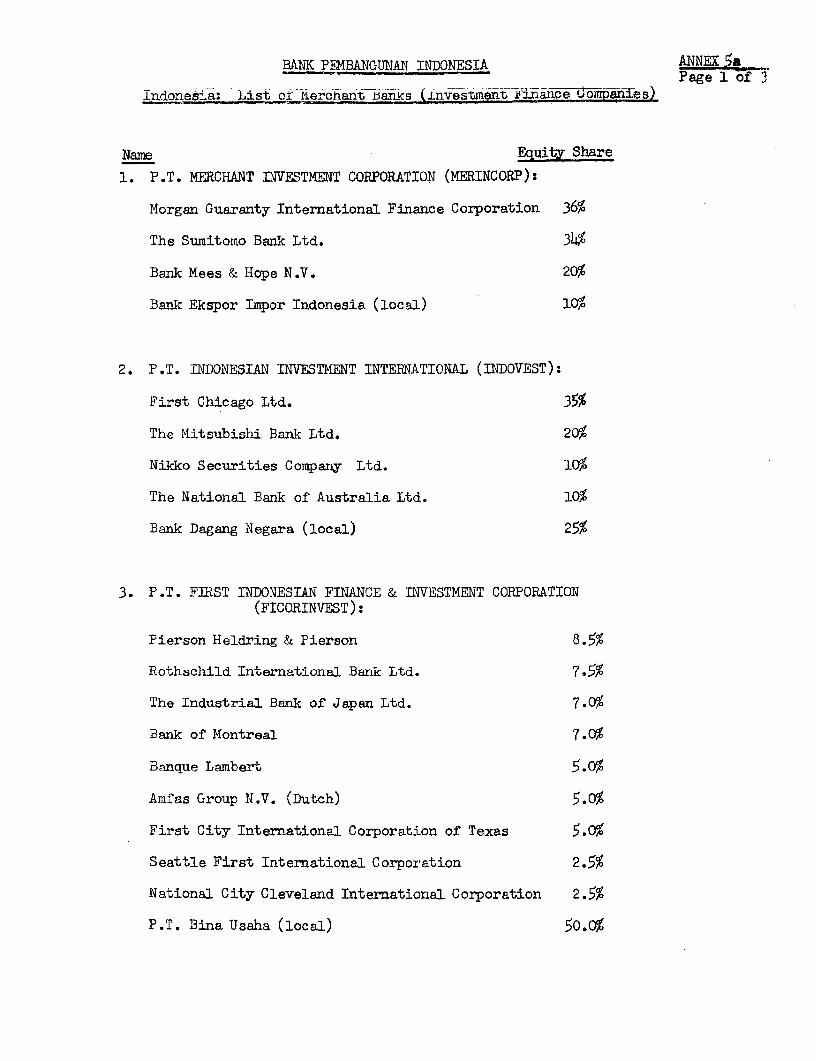

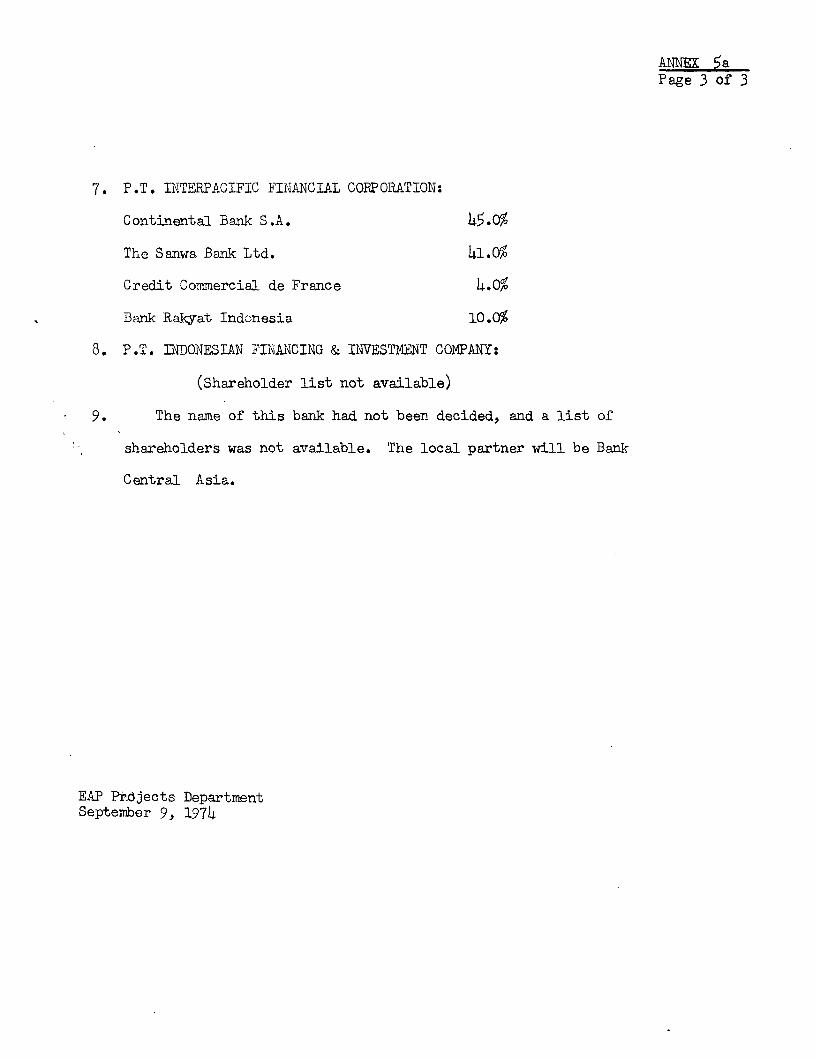

5a. List of Merchant Banks (Investment Finance Companies)

6. Interest Rate Structure of State Commercial Banks

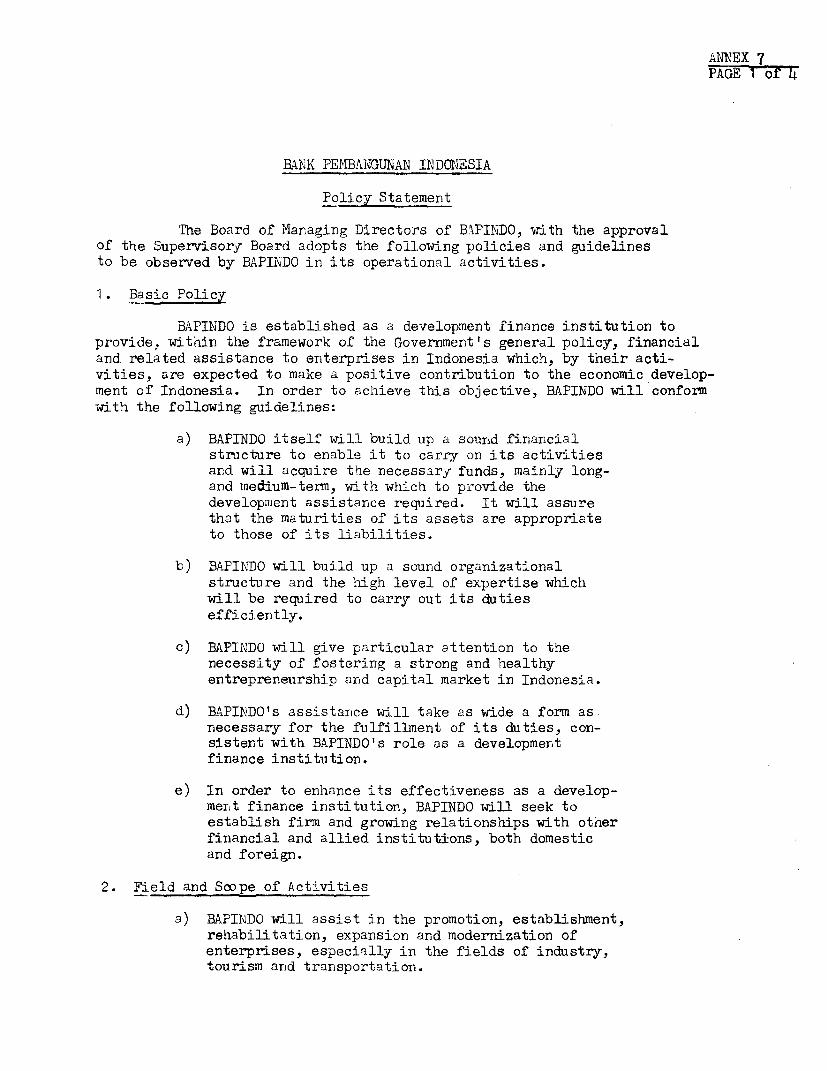

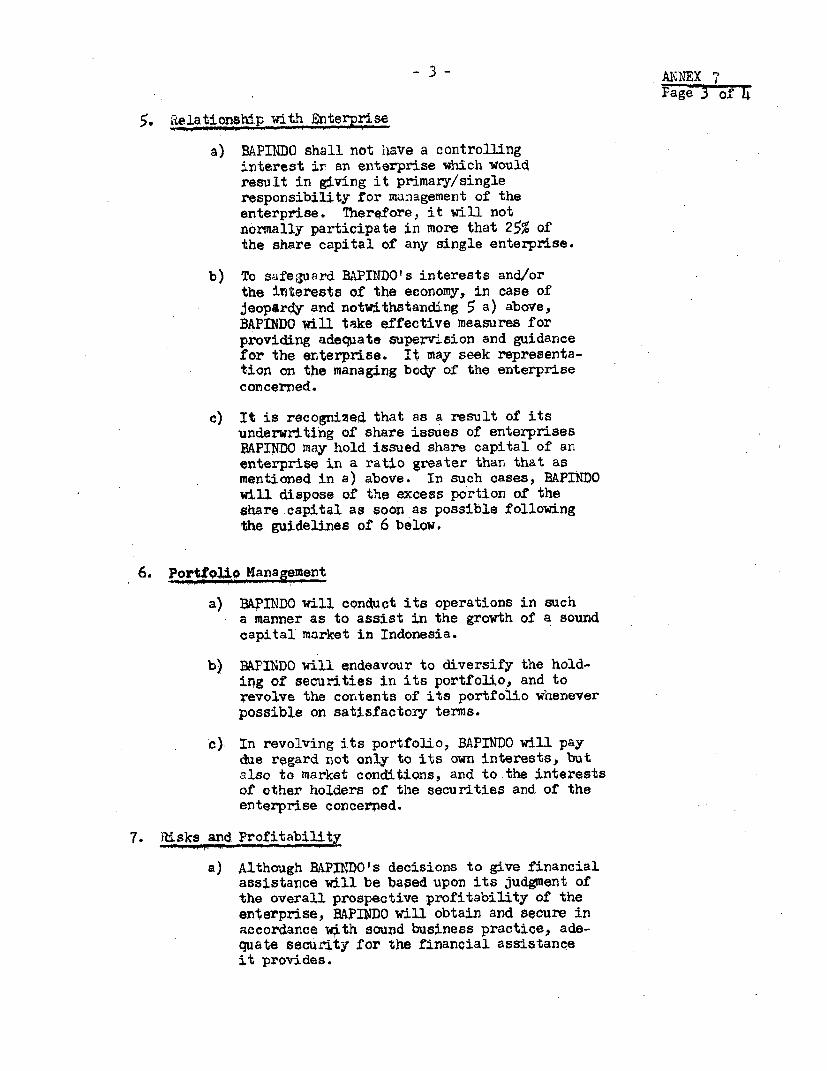

7. Policy Statement

S. Summary of Loan Operations, 1971-1973

9. Investment Loan Commitments by Industry, 1971-1973

10. Analysis of Medium- and Long-Term Loan Commitments, according to Size,Location and Maturity

11. Permanent Working Capital Loan Commitments by Industry, 1971-1973

12. Small Business Co-Financing with Regional Development Banks

13. Maritime Sector Loan Commitments, 1971-1973

14. Summarized Audited Balance Sheets, 1970-1973

15. Summarized Audited Income Statements, 1970-1973

16. Analysis of Loan Arrears as of December 21, 1972 and 1973

17. Analysis of Medium/Long-Term Loan Portfolio as of December 31, 1973

18. Forecast of Approvals, Commitments and Disbursements, 1974-1978

19. Projected Balance-Sheets, 1974-1978

20. Projected Income Statements, 1974-1978

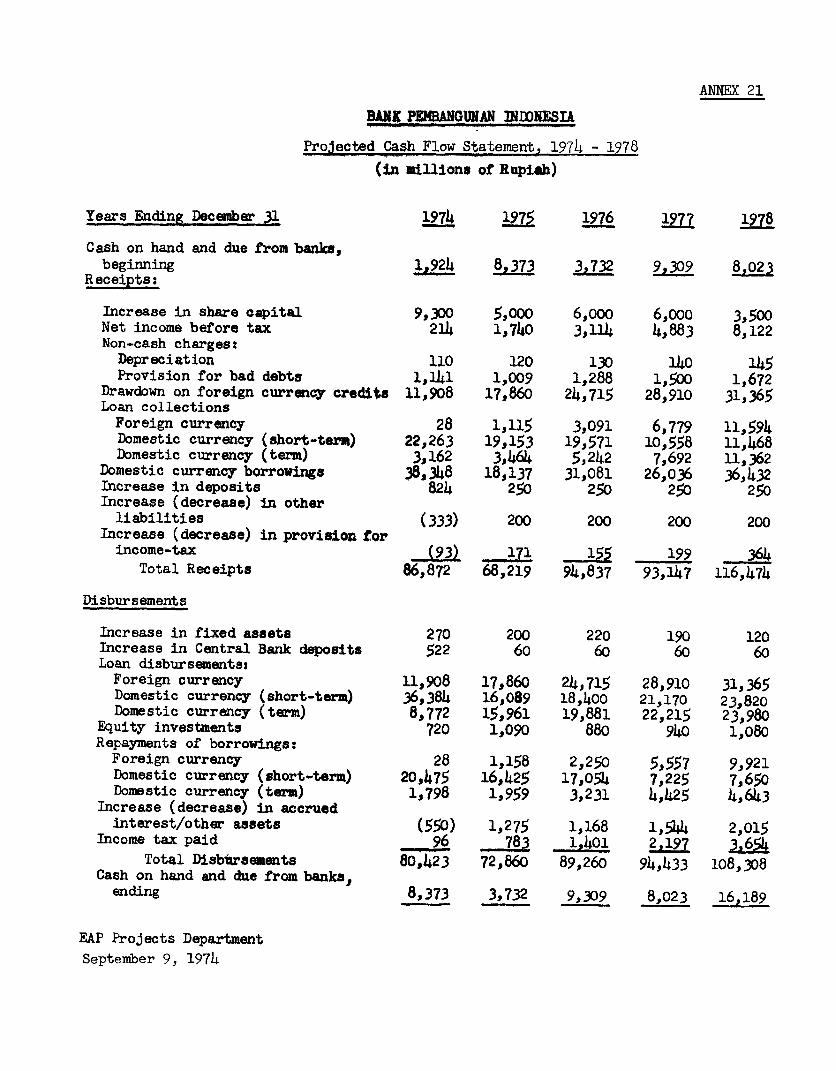

21. Projected Cash Flow Statements, 1974-1978

22. Projected Financial Ratios, 1974-1978

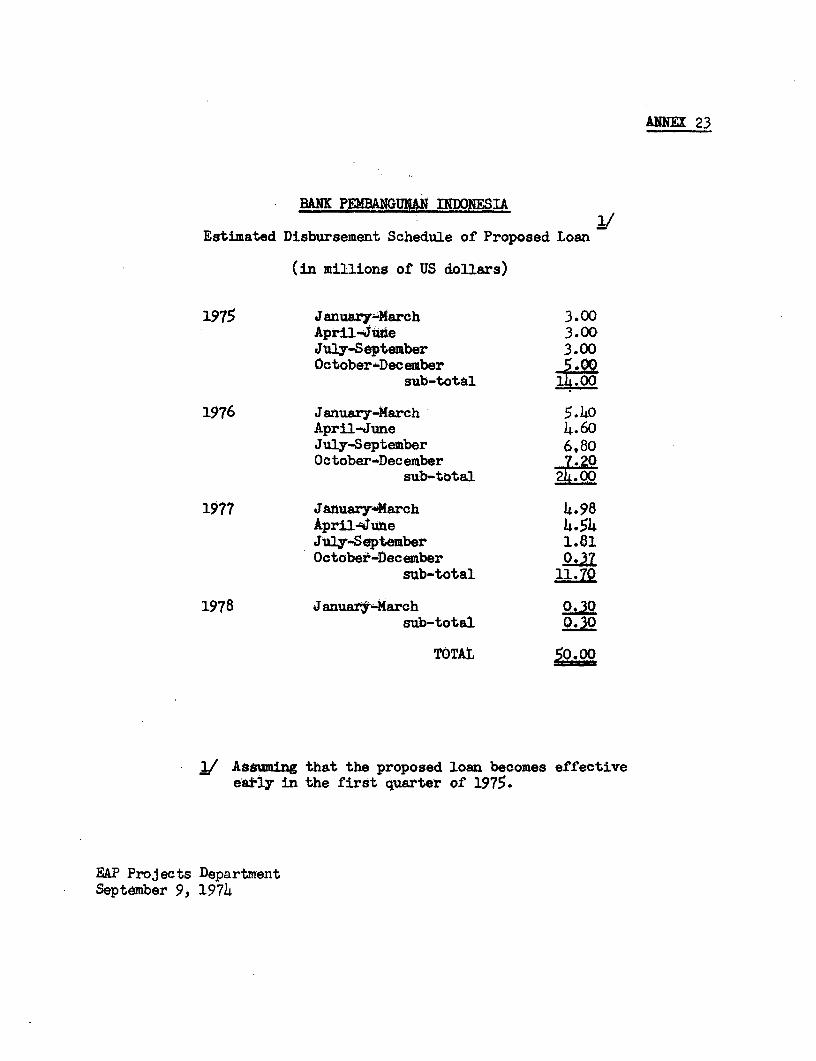

23. Schedule of Estimated Disbursements

CHARTS

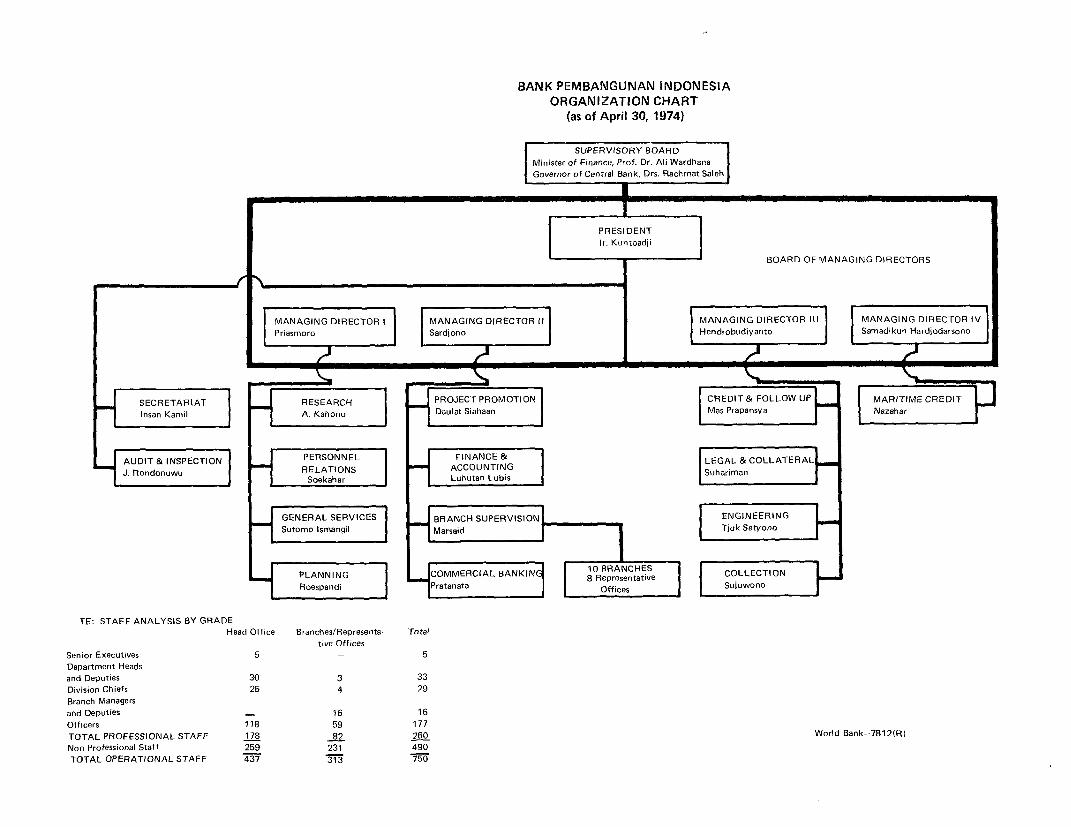

Organization ChartLocation of Branches

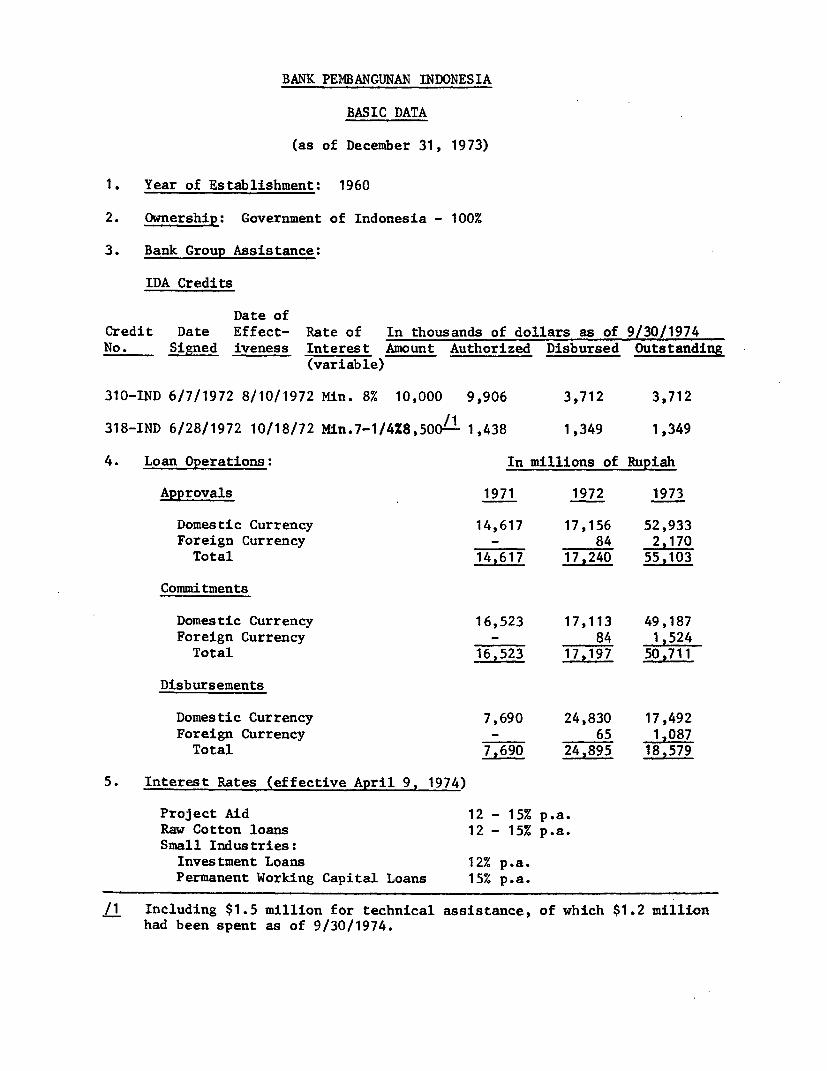

BANK PEMBANGUNAN INDONESIA

BASIC DATA

(as of December 31, 1973)

1. Year of Establishment: 1960

2. Ownership: Government of Indonesia - 100%

3. Bank Group Assistance:

IDA Credits

Date ofCredit Date Effect- Rate of In thousands of dollars as of 9/30/1974

No. Signed iveness Interest Amount Authorized Disbursed Outstanding(variable)

310-IND 6/7/1972 8/10/1972 Min. 8% 10,000 9,906 3,712 3,712

/1318-IND 6/28/1972 10/18/72 Min.7-1/4X8,500/--- 1,438 1,349 1,349

4. Loan Operations: In millions of Rupiah

Approvals 1971 1972 1973

Domestic Currency 14,617 17,156 52,933Foreign Currency - 84 2,170

Total 14,617 17,240 55,103

Commitments

Domestic Currency 16,523 17,113 49,187Foreign Currency - 84 1,524

Total 16,523 17,197 50,711

Disbursements

Domestic Currency 7,690 24,830 17,492Foreign Currency - 65 1,087

Total 7,690 24,895 18,579

5. Interest Rates (effective April 9, 1974)

Project Aid 12 - 15% p.a.

Raw Cotton loans 12 - 15% p.a.

Small Industries:Investment Loans 12% p.a.Permanent Working Capital Loans 15% p.a.

/1 Including $1.5 million for technical assistance, of which $1.2 millionhad been spent as of 9/30/1974.

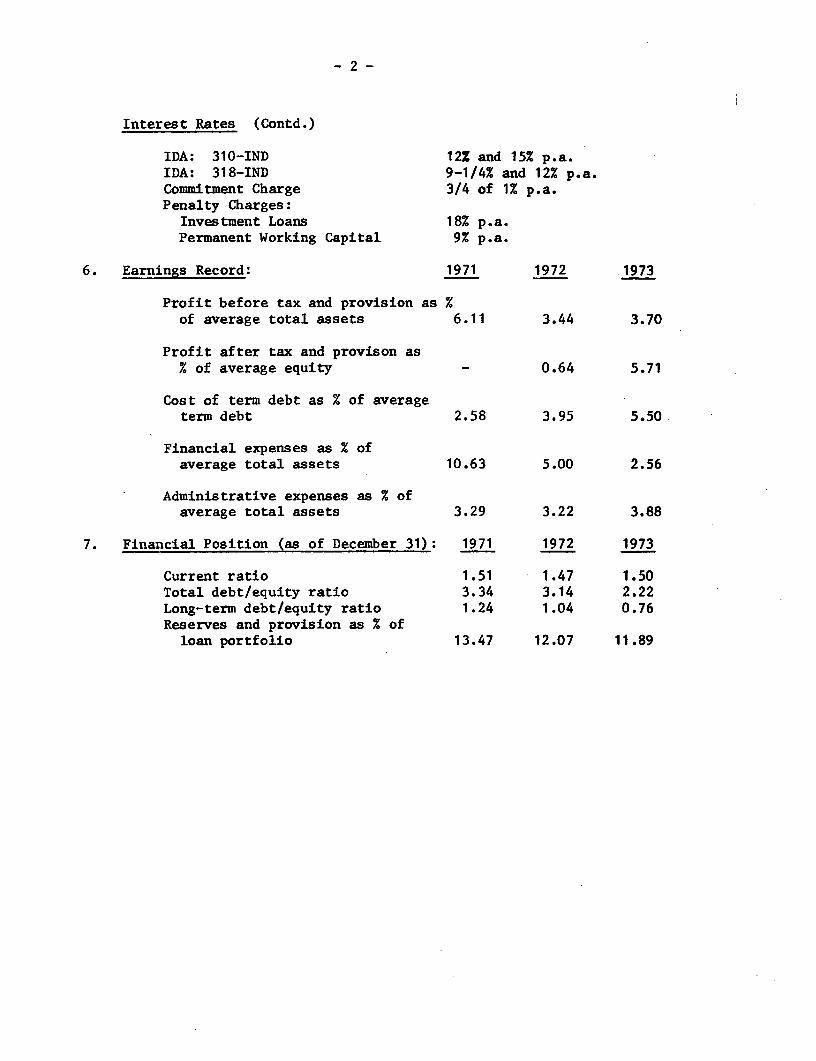

-2-

Interest Rates (Contd.)

IDA: 310-IND 12% and 15% p.a.IDA: 318-IND 9-1/4% and 12% p.a.Commitment Charge 3/4 of 1% p.a.Penalty Charges:

Investment Loans 18% p.a.Permanent Working Capital 9% p.a.

6. Earnings Record: 1971 1972 1973

Profit before tax and provision as %of average total assets 6.11 3.44 3.70

Profit after tax and provison as% of average equity - 0.64 5.71

Cost of term debt as % of averageterm debt 2.58 3.95 5.50

Financial expenses as % ofaverage total assets 10.63 5.00 2.56

Administrative expenses as % ofaverage total assets 3.29 3.22 3.88

7. Financial Position (as of December 31): 1971 1972 1973

Current ratio 1.51 1.47 1.50Total debt/equity ratio 3.34 3.14 2.22Long-term debt/equity ratio 1.24 1.04 0.76Reserves and provision as % of

loan portfolio 13.47 12.07 11.89

INDONESIA

APPRAISAL OF BANK PEMBANGUNAN INDONESIA (BAPINDO)

SUMMARY, RECOMMENDATIONS, AND UNDERSTANDINGS REACHED

i. The World Bank Group's (WBG's) association with Bank PembangunanIndonesia (BAPINDO) dates back to 1969. A detailed examination in Decemberof that year, made by a Bank mission at the request of the Government (GOI),revealed that BAPINDO was organizationally weak, grossly under-capitalized,with a portfolio of dubious quality, and with unacceptably low standards ofappraisal and follow-up. In June 1970, GOI and WBG agreed on a reorganizationand financial restructuring of BAPINDO, as part of a rationalization ofthe institutional arrangements for providing long-term capital for industry.BAPINDO was to become the main domestic source of long-term capital for theprivate sector.

ii. Since June 1970 considerable progress has been made in implementingthe agreed reorganization, helped by close cooperation among the Government,WBG, and BAPINDO. BAPINDO's management was strengthened; its capital basewas improved by the conversion of Government loans into equity, and by freshinfusions of cash; its portfolio was analysed, a part was transferred out ofBAPINDO's responsibility, and substantial provisions were made against doubt-ful debts on the remainder; and its accounts were audited by outside in-dependent auditors. BAPINDO also engaged six Advisors, selected and recom-mended by WBG. In December 1971, after sufficient progress had been made,Bank Indonesia (BI) rescinded its earlier prohibition against BAPINDO'smaking loans to new clients, and in May 1972 the International DevelopmentAssociation (IDA) made a Credit of $10 million to BAPINDO. In June 1972 IDAmade a second credit of $8.5 million 1/ for the rehabilitation of inter-islandregular liner service (RLS), when the Government designated BAPINDO the bankfor handling credits for the shipping sector.

iii. Progress made by BAPINDO since the first Credit was made has beenremarkable. The Board of Managing Directors, with the help of the Advisorsand continuing advice from WBG, has worked hard to streamline the organization,improve appraisal standards, bring order into the portfolio inherited fromthe past and, particularly from the second half of 1973, to increase thevolume of new business. For its part, GOI has continued its active help andcooperation; since the first Credit was made, GOI has paid an additionalamount of Rp 11.3 billion into BAPINDO's capital to strengthen its equity,and to enable it to undertake a growing volume of business. Two of the moresignificant developments in 1973 were a retrenchment of about 40% of its staff(from 1263 to 750), and the closing of 8 uneconomic branches (out of a totalof 18), and their conversion into representative offices; both these actionsrepresented implementation of understandings reached earlier with WBG.

1/ This amount included $1.5 million for technical assistance.

- ii -

iv. As a result of the improvements between 1971 and 1973, BAPINDO isnow a far more effective institution than it was in 1969, with a sense ofcorporate purpose and direction, and growing confidence in its ability to ful-fill its role. For the first time in BAPINDO's history, external auditorsgave it an unqualified report on its azcounts, (for the year ended December 31,1973). During 1973, it committed 163 loans for a total of Rp 50.7 billion.More significantly, the proportion of long-term loans to total commitmentsincreased substantially. BAPINDO's commitments in 1974 have shown furthergrowth, and with the transfer of raw cotton loan business to Bank Ekspor-Impor, BAPINDO will now concentrate on providing long-term capital, the roleconceived for it by GOI and WBG in 1970.

v. Notwithstanding the remarkable progress already made by BAPINDO,there is both scope and need for further improvement. BAPINDO's Board ofSupervisors needs to be enlarged and made more effective; and BAPINDO'sauthorized capital needs to be increased in view of its growing operations.Internally, appraisal standards need to be improved further, particularlyto analyze more fully the economic aspects of projects. BAPINDO also needsto institute an effective system of project supervision. These and otherweaknesses are recognized by the management and remedial actions are beingtaken. Currently the emphasis is on staff training and improvement, andrecently three senior officials received training for up to three monthseach in three of the more experienced DFCs associated with WBG; the trainingprograms were arranged by the Bank.

vi. The economic, industrial, and financial environment in which BAPINDOoperates offers good prospects for BAPINDO's continued growth. The investmentneeds of the private sector are large and continuing, and the shortage oflong-term capital continues. BAPINDO estimates that its commitments for thethree years, ending December 1976, would amount to Rp 151 billion, includingan estimated Rp 53 billion for foreign exchange commitments for the last twoquarters of 1974, 1975 and 1976. These foreign exchange commitments, theequivalent of US$100 million, would involve imports. The estimated commitments,although justified and achievable if viewed from the demand side, may appearsomewhat optimistic from the point of view of BAPINDO's current processingcapacity.

vii. BAPINDO's domestic currency resources would be provided principallyby GOI in the form of equity, loans and refinance, and also through net col-lections and retained earnings. Foreign currency needs in the immediatefuture would be met from the proposed Bank loan, as BAPINDO does does nothave any other foreign currency resources. The Bank has suggested, andBAPINDO is exploring, raising loans from other sources, including KfW, whichis considering making a DM 22 million loan.

viii. The proposed Bank loan would continue the Bank Group's support ofthe industrial sector in Indonesia. It would also provide continuity in WBG'sinstitution-building role which began in 1969, and which will continue to be

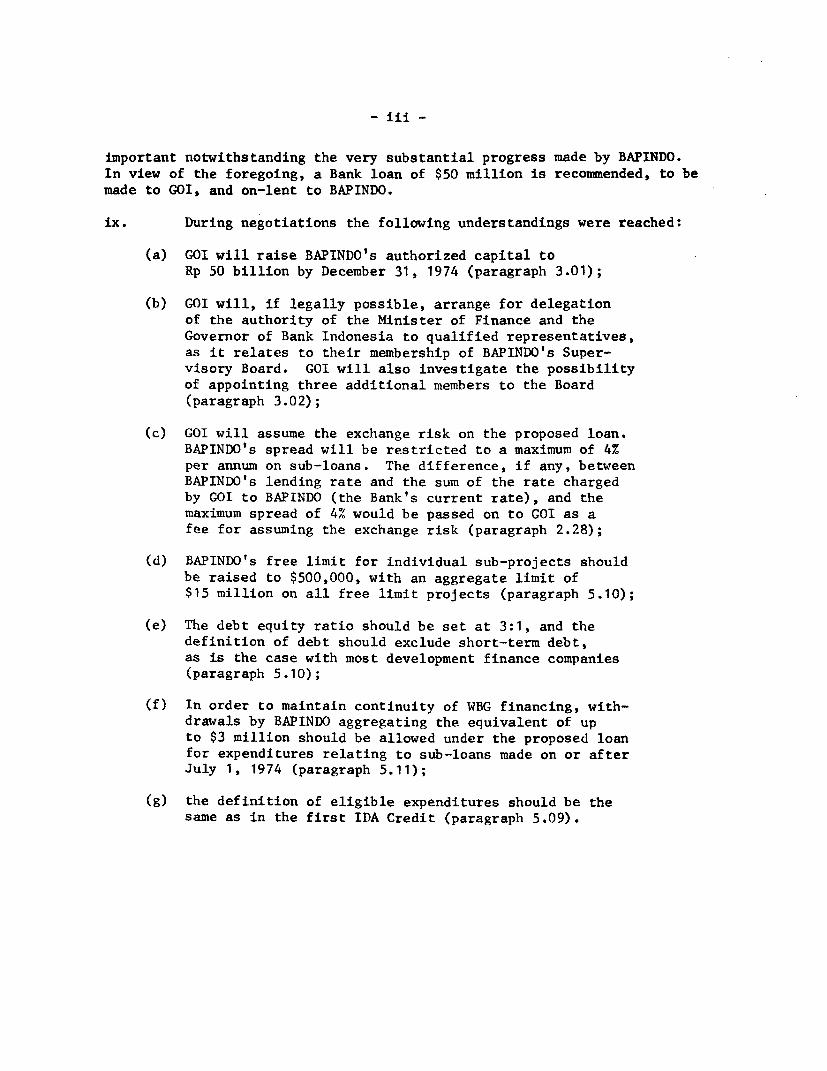

- iii -

important notwithstanding the very substantial progress made by BAPINDO.In view of the foregoing, a Bank loan of $50 million is recommended, to bemade to GOI, and on-lent to BAPINDO.

ix. During negotiations the following understandings were reached:

(a) GOI will raise BAPINDO's authorized capital toRp 50 billion by December 31, 1974 (paragraph 3.01);

(b) GOI will, if legally possible, arrange for delegationof the authority of the Minister of Finance and theGovernor of Bank Indonesia to qualified representatives,as it relates to their membership of BAPINDO's Super-visory Board. GOI will also investigate the possibilityof appointing three additional members to the Board(paragraph 3.02);

(c) GOI will assume the exchange risk on the proposed loan.BAPINDO's spread will be restricted to a maximum of 4%per annum on sub-loans. The difference, if any, betweenBAPINDO's lending rate and the sum of the rate chargedby GOI to BAPINDO (the Bank's current rate), and themaximum spread of 4% would be passed on to GOI as afee for assuming the exchange risk (paragraph 2.28);

(d) BAPINDO's free limit for individual sub-projects shouldbe raised to $500,000, with an aggregate limit of$15 million on all free limit projects (paragraph 5.10);

(e) The debt equity ratio should be set at 3:1, and thedefinition of debt should exclude short-term debt,as is the case with most development finance companies(paragraph 5.10);

(f) In order to maintain continuity of WBG financing, with-drawals by BAPINDO aggregating the equivalent of upto $3 million should be allowed under the proposed loanfor expenditures relating to sub-loans made on or afterJuly 1, 1974 (paragraph 5.11);

(g) the definition of eligible expenditures should be thesame as in the first IDA Credit (paragraph 5.09).

INDONESIA

APPRAISAL OF BANK PEMBANGUNAN INDONESIA (BAPINDO)

I. INTRODUCTION

1.01 Since 1969 the World Bank Group (WBG) has worked with the Govern-ment of Indonesia (GOI) to improve the institutional arrangements for theprovision of finance for medium- and long-term investment in the industrialsector in Indonesia. The government-owned Bank Pembangunan Indonesia(BAPINDO) has been and remains an important focal point of the joint effortsof the Government and the WBG. By May 1972 progress in reorganizing andstrengthening BAPINDO had reached the stage at which the Association wasable to make BAPINDO a Credit of $10 million. It was followed in June 1972by an additional Credit of $8.5 million to finance a rehabilitation programfor inter-island shipping.

1.02 The WBG has continued, since the first two Credits were made, tofollow BAPINDO's progress closely and to assist it whenever possible. Aswill be detailed later in this report, BAPINDO's progress has been remark-able, although there still remains room for much improvement. The WBGintends to continue to make available to BAPINDO such advice and guidanceas BAPINDO considers it needs and the WBG considers it can offer. On thebasis of the WBG's experience with BAPINDO over the past five years, thereis good reason to believe that BAPINDO will make substantial further pro-gress. The effects of that progress should carry beyond BAPINDO itself.Paragraphs 2.24, 4.06 and 4.07 below, with respect to BAPINDO's appraisalof and lending to Regional Development Banks in Indonesia, give an interestinginsight into the "multiplier" effect that the WBG's transfer of expertiseto an important financial institution in a member country can have. Sincethe quality of the advice that BAPINDO is able to offer to the RegionalDevelopment Banks will depend on the standards of performance BAPINDO isable to achieve for itself, the continuance of BAPINDO's close associationwith the WBG should have far-reaching, beneficial effects.

1.03 The recent growth of industry in Indonesia has exceeded expectations,and the combined efforts of Indonesian term lending institutions have notbeen adequate to meet the growing demand for investment funds. As a result,foreign financial sources have been called on for significant investment inIndonesia. In 1973, GOI decided that BAPINDO should henceforth concentrateprimarily on making loans to medium- and large-scale industrial enterprises,and made arrangements for BAPINDO's lending to small-scale enterprise to besupplemented by other sources of finance. With these considerations in mind,and on the basis of the appraisal contained in this report, a Bank loan forBAPINDO of $50 million is recommended.

-2-

II. ECONOMIC, INDUSTRIAL AND FINANCIAL ENVIRONMENT

Economic Environment

2.01 The performance and prospects of the Indonesian economy weredescribed in: "The Indonesian Economy: Recent Developments and Prospectsfor 1974/75", November 26, 1973, 286-IND. A Basic Economic Mission assessedIndonesia's longer term development prospects and policies during October1974; its findings are not yet available.

2.02 Repelita I. The First Five-Year Development Plan (Repelita I) ranfrom April 1, 1969 to March 31, 1974. During this period, substantial im-provements were made in rehabilitating the infrastructure, laying the founda-tion for further development of the economy. GDP rose at an average rateof 7% per annum. The share of the agricultural sector fell from 47.7% to40.2% of GDP, while the industrial sector's share rose from 9.3% to 9.8%of GDP. The agricultural sector grew by 3% per annum, mainly because ofincreased rice production; the industrial sector grew at over 11% per annum,following large domestic and foreign investment. Gross domestic capitalformation increased at an average rate of around 25% in real terms (34%at current prices). The share of gross investment in GDP increased from8.8% in 1968-69 to 17.7% in 1973-74, and foreign resources made a significantcontribution to this growth.

2.0:3 Repelita II. The Second Five-Year Development Plan (Repelita II)which will run from April 1, 1974 to March 31, 1979, aims at a more equit-able distribution of development benefits through the expansion of socialwelfare activities, and the creation of greater employment opportunities.Real GDP is projected to rise at 7.5% per annum, and per capita income byabout 5.7% per annum, despite an estimated population increase of 2.3% perannum. Total investment is expected to rise by 13.2% per annum in real terms(23.4% at current prices). The proportion of gross investment to GDP willrise from 17.7% in 1973/74 to 22.9% in 1978/79. Agriculture is expected togrow at 4.6% per annum, but its contribution to GDP will fall from 40.2% in1973/74 to 35.6% in 1978/79. The industrial sector is expected to grow at13%, and its share of GDP will rise from 9.8% in 1973/74 to 12.5% in 1978/79.

2.04 Further expansion is projected for industries which process domesticraw materials, effect import substitution or are export-oriented. The small-scale sector will receive special attention because of its potential forincreasing employment. Exports of crude oil, timber, agricultural productsand other minerals are expected to continue their recent rapid growth. Importpolicies will give priority to capital goods and industrial raw materials.Substantial expenditures will be made on regional development to achieve amore balanced growth. Policies relating to foreign and domestic investmentwill aim at encouraging the growth of local industries, especially in thesmall scale sector.

-3-

2.05 A total investment of Rp 11,023.4 billion is expected to be made;the contribution of foreign resources to total investment is expected todecline from 39% in 1974/75 to 22% in 1978/79. Government development ex-penditures will rise to 45.6% of total investment in 1978/79, compared with42.7% in 1974/75. Some of these figures and targets have, however, beenrendered obsolete by the jump in export earnings from oil, which alreadytotalled $1.724 billion for the first five months of 1974, exceeding the$1.708 billion earned from oil exports during the entire year 1973. ThePlan's basic strategy, which was designed to reduce dependence on foreignaid will, however, remain intact.

Industrial Environment

2.06 Features of Industrialization. Indonesia is still at the thresh-old of industrialization. The manufacturing sector is relatively undeveloped;its share of GDP is lower than that usual in a country at a similar stage ofdevelopment, and of a comparable domestic market size. The estimated annualvalue-added per capita by this sector is only $5.88; and the industry mix isstill dominated by consumer goods. Indonesia's industrialization processexhibits the following broad features: (a) a domestic market orientation,encouraged by a large population; (b) increasing participation by foreignprivate capital, following generous incentives and a favorable investmentclimate; (c) an apparent persistence of excess capacity in certain sectorssuch as textiles, cigarettes and matches, due to such problems as inputshortages, shortage of working capital, and lack of effective demand; (d)low efficiency and productivity of public sector manufacturing enterprises,primarily due to poor management; (e) a geographical concentration in Java,particularly in and around Jakarta; and (f) a small but heavily promotedindigenous manufacturing sector. There is a new sense of urgency, sharedby both GOI and the private sector, in stepping up the pace of industrialdevelopment, and large investments have been made during recent monthswhich will greatly extend the size and range of the manufacturing sector.

2.07 Industrial Structure. Reliable statistical data are not easilyavailable. Some light was shed on the broad structure of the industrialsector by the 1970 Industrial Survey, which found consumer goods, particularlyfood products (including tobacco), contributing 62% of total manufacturingoutput in 1969. The food processing, textiles, apparel, footwear and trans-port equipment (assembly and repair) industries predominated. Intermediateand capital goods industries are only recently making their appearance.Industrial chemicals, including fertilizer and petro-chemicals, are in anearly stage of development. Several small steel mills exist, producing itemsmainly for the construction industry; additional steel capacity is beingmobilised.

2.08 According to the 1970 Survey of Large- and Medium-Scale Manufac-turing Industries, medium- and large-scale enterprises 1/ numbered 17,900 in

1/ The Survey defined "large" establishments as those having 100 workersor more without power equipment or 50 workers or more with power equip-ment. The "medium" establishments were defined as those having 50-99workers without power equipment or 5-49 workers with power equipment.

-4-

1969. Large-scale firms accounted for only 11% of total industrial establish-ments. Firms in the 'food and beverage' industry accounted for 35%, and thosein the 'textile' industry for 27%, of the total number of large- and medium-scale enterprises. No reliable data are available regarding the structuralcharacteristics of the small-scale sector.

2.09 In 1969, medium- and large-scale firms in the food processing in-dustry employed more than one-third of the total labor force in the medium-and large-scale sectors. Tobacco and textile industries were next in im-portance. Medium- and large-scale enterprises together employed 849,000workers, or about 3.7% of Indonesia's total labor force. Large-scale firmsemployed on average 302 workers per plant, while medium-scale firms averagedabout 16 workers per plant. As stated earlier (paragraph 2.07), intermediateand capital goods industries are only recently making an appearance; theircontribution to employment and output is still small.

2.10 Industrial development is concentrated on Java, which has 782 ofexisting medium- and large-scale firms, and 86% of total manufacturing em-ployment. Java also has the largest scale of production with an averageof 53 workers per plant. Jakarta accounts for 11% of firms located, and 7%of total industrial employment, in Java. Industrial activity also tends tobe concentrated in and around large cities elsewhere in the Indonesianarchipelago.

2.11 Industrial Investment. From January 1967 through December 1973the value of approved foreign investment projects, in sectors other thanpetroleum and banking, amounted to $3.1 billion. 1/ Major shares wereas follows: $1.2 billion or 38.7% in manufacturing, $959.9 million or30.6% in mining and quarrying, and $497.8 million or 15.8% in forestry.In 1973 the value of foreign investments approved reached $615.8 million,compared with $522.0 million in 1972. Approvals in the manufacturing sectorrose sharply to $455.5 million, mainly due to a $235.1 million share forthe textile and leather industries. The "implementation" of approvals(expenditures) at end 1973 was, however, estimated at only $1.1 billion,or 35'c of total approvals. Implementation dropped to $319 million in 1973,compared to $344 million in 1972, mainly due to projects with slow gestationin the mining and quarrying sectors. To improve efficiency, GOI set up theInvestment Coordinating Board (ICB) in June 1973, replacing the TechnicalCommittee on Capital Investment, and its subcommittees, the Foreign InvestmentBoard and the Domestic Investment Board. Various concerned ministries arerepresented on ICB, and applicants both foreign and domestic need now dealonly with one agency.

2.12 Domestic investment approvals also grew rapidly; 1816 projects,envisaging a total investment of Rp 1,236 billion, were approved fromNovember 1968 through December 1973 2/. In 1973 total approvals reached

1/ See Annex 1.

2/ See Annex 2.

- 5 -

Rp 569.4 billion, compared with Rp 297.6 billion in 1972. The share ofdomestic investment approvals in total approvals rose from 28% in 1972to 69% in 1973.

2.13 Some important investment regulations were amended in early 1974.New foreign investments are allowed only in the form of joint ventures, onthe understanding that the Indonesian share be increased to 51% within aspecified period, usually ten years. Some tax incentives have been reduced,the list of industries closed to foreign investors expanded, and a largernumber o' Indonesians are to be employed in foreign or joint-venture enter-prises. Regulations regarding domestic investment were also revised to en-sure greater participation by "indigenous" Indonesians. Effective February1974, only indigenous or "pribumi" 1/ enterprises are allowed access to themedium-term credit facilities under the INVESTASI program 2/. It is tooearly to assess the effects of these changes on both foreign and domesticinvestment, but the momentum of industrial growth is not expected to besignificantly diminished.

2.14 Obstacles to Further Growth. There have been marginal improve-ments in removing the following major impediments to further rapid industrialgrowth: (a) the lack of adequate public infrastructure of all kinds; (b)the scarcity of entrepreneurship, and of a broad range of business and manage-ment skills; (c) administrative and bureaucractic obstacles which cause in-vestors considerable delays and difficulties in getting decisions and obtain-ing interpretation of laws; and (d) the scarcity of equity capital and offinance for current assets. The Government recognizes these impedimentsand remedial actions on a broad front have been taken or are being taken.However, these are basic problems and solutions will emerge only over a longperiod.

Financial Environment

2.15 Banking Structure. The banking network consists of the CentralBank, Bank Indonesia (BI); five large state-owned commercial banks; a stateDevelopment Bank (BAPINDO); two joint-venture development banks, 3/ IndonesianDevelopment Finance Company (IDFC) and the Private Development Finance Com-pany of Indonesia (PDFCI); 26 regional development banks; 128 small domesticprivate banks; and branches of 11 foreign banks. There are also about 9,000savings and village banks, but their assets are relatively insignificant. BIand the state banks predominate, accounting for almost 90% of total outstand-ing bank credit; domestic and foreign private banks account for the larger

1/ Indigenous or "pribumi" enterprises are those companies in which in-digenous entrepreneurs control either 75% of the equity, or 50% of theequity and key management positions.

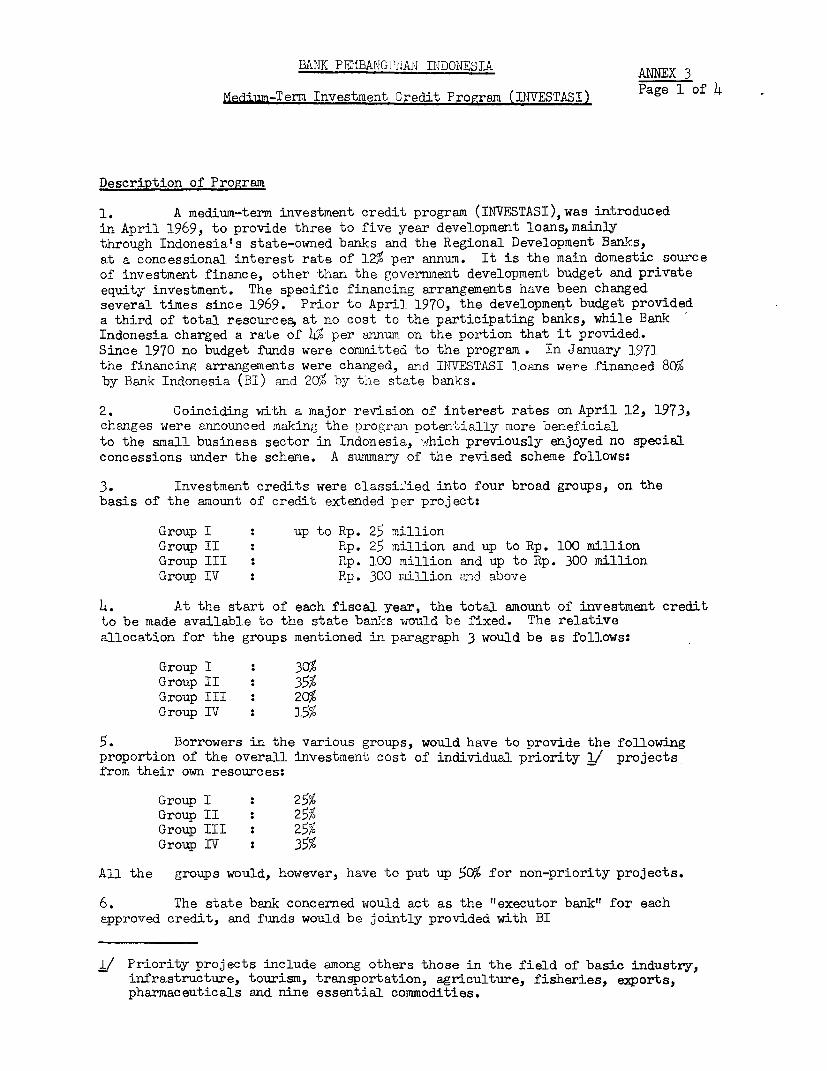

2/ See Annex 3 for a description of the INVESTASI Program.

3/ See Annex 4 for details of ownership.

-6-

part of the remainder. Foreign bank branches have grown rapidly in the lastfew years, and are now larger and more important than local private banks.

2.16 The five State commercial banks have for historical reasonsspecialized in providing finance for particular sectors, although there issome overlapping 1/.

2.17 Money and Capital Markets. Money and capital markets are in avery early stage of development. G0I created the Agency for Money andCapital Market Development in January 1972, which is currently working on,among other proposals, the establishment of a securities and exchange ad-ministration. Nine merchant banks (joint-ventures between foreign andlocal banks) were given licenses during 1973/74 to help develop the moneyand capital market. It is too soon to say how successful they will be inmeeting their objective 2/. At present they deal in short-term commercialpaper, real estate, and act as local agents for their parent banks in ob-taining foreign currency loans for their clients. There is a small stockexchange that deals mainly in shares of previously Dutch-owned pre-war en-terprises, now largely owned by the State and recently converted into limitedliability companies. An important obstacle to rapid development of thecapital market is the weak financial position of most Indonesian companies.

2.18 Short-Term Credit. Short-term credit is extended by banks forperiods of up to one year; most loans are for three or six months duration,and can be renewed depending upon the bank/borrower relationship. There isno broad, well-developed bill market for discounting trade paper, and workingcapital is generally hard to obtain.

2.19 Medium- and Long-Term Credit. Term credit for industrial projectsis available from all banks, although foreign banks must obtain BI's approvalto make loans for more than a year. No state banks, except BAPINDO, can makeloans for periods beyond five years. Term finance, except that part extendedby local institutions out of foreign currency lines of credit, is largelyextended under the INVESTASI program (Annex 3) introduced by the Governmentin 1969. The total amount of loans approved under this program up toJanuary 31, 1974 was Rp 167.8 billion, and total disbursements stood atRp 116.1 billion. The private sector received Rp 91.1 billion or 78.5% oftotal disbursements, and Rp 25.0 billion or 21.5% went to the public sector.

1/ Bank Negara Indonesia, 1946 (industry, transport, agriculture and export);Bank Bumi Daya (mining, export, estates);Bank Rakjat Indonesia (agriculture, rural projects);Bank Dagang Negara (mining and exports);Bank Expor-Impor Indonesia (exports, imports).

2/ For a fuller treatment of the money and capital market, see Annex 5.

-7 -

2.20 One of the major institutional developments during 1973 was thesetting up, with active WBG assistance, of P.T. Private Development FinanceCompany of Indonesia (PDFCI), a privately-owned development finance company.PDFCI, in addition to making term loans, will actively seek equity invest-ments and will also play a role in promoting new enterprises.

2.21 With the establishment of PDFCI there are now three domesticspecialized institutions for providing long-term capital. BAPINDO is by farthe largest. PDFCI's initial resources amount to $21 million equivalent,and it is yet to enter the operational phase; IDFC had total outstandingresources of less than $10 million equivalent. BAPINDO is, and will continueto be, the principal domestic source of medium- and long-term capital for theprivate industrial sector.

Financing for Small-Scale Industry

2.22 Until early 1973 most loans under the INVESTASI scheme had beendirected to medium or large industrial enterprises. In April 1973 theGovernment announced that 65% of future assistance under the INVESTASIprogram would be reserved for small loans. During 1973, the Governmentalso established a new agency, P.T. Bahana, for making equity investmentsin, and providing management assistance to, small businesses. The Govern-ment had also earlier set upP.T. Asuransi Kredit Indonesia (ASKRINDO) toinsure bank loans made to small business up to certain limits, to encour-age banks to increase their lending to this sector.

2.23 ASKRINDO's program was expanded in December 1973; medium-term andworking capital loans to small industry are now automatically insured up to75% of total risk. This change accompanied an expanded INVESTASI program ofassistance to small businesses, under which an amount of Rp 12 billion wasset aside for such loans made through the state banks, including BAPINDO.An overall limit of Rp 2 billion was initially set for each state bank.Maximum amounts that can be borrowed by each customer are Rp 5 million forinvestment loans, and a similar amount for permanent working capital.

2.24 To reach a larger number of small borrowers and to improve theinstitutional arrangements for financing small borrowers, BAPINDO instituteda new co-financing scheme with selected Regional Development Banks (RDBs).Under this program BAPINDO appraises the RDBs, and extends them a line ofcredit. The agreement provides for BAPINDO's financing in each sub-projectto be limited to 10% of the total loan for fixed assets, and 20% of the totalloan for working capital; BI provides 80% and 70% respectively, and the balanceof 10% is provided by the RDBs. BAPINDO has appraised and entered into agree-ments with 8 RDBs. BAPINDO's plans call for 5 more appraisals during 1975.

Inflation

2.25 Indonesia achieved a remarkable degree of price stability during1969-71. However, the inflation rate which had declined to 2.6% in 1971 shot

-8-

up to 25.7% in 1972, largelybecause of an increase in rice prices followinga serious drought. Strong inflationary pressures continued during 1973 andthe early part of 1974, caused by domestic demand, fueled by a sizeablecredit expansion, the strong rise in export prices (particularly oil) andthe increase in prices of imported goods and raw materials used by domesticindustries. The Jakarta consumer price index rose by 27% during 1973, andby a further 16% in the first quarter of 1974. Prices rose by 472 over thetwelve-month period ended March 1974, compared to a 21% increase in theprevious comparable period. Alarmed by the rapid inflation, the Governmentannounced a package of strong anti-inflationary measures on April 9, 1974,including credit rationing and changes in interest rates. The inflationrate for the period April-July 1974 has already been contained to about 5.6%,and the months of August and September have shown a further reduction.

Interest Rates

2.26 Current interest rates and changes made in the recent past aregiven in Annex 6. Interest rates for all state banking institutions areprescribed by BI.

2.27 In the 60's when inflation in Indonesia was very high, the Governmentfollowed a policy of high interest rates as part of the economic stabilizationprogram. By the beginning of the new decade, GOI was able to bring inflationarypressures under control, and interest rates were reduced across the board inMay 1972 and again in April 1973. However, the long-term lending rate, alreadylow, remained unchanged at 12%. When inflationary pressures developed onceagain in 1973 and the early months of 1974, the Government increased interestrates on most loans and deposits. The term lending rate was also increasedto 15% p.a. (The rate for loans not exceeding Rp. 100 million, however,remained unchanged at 12%). In relation to inflation during the last 12 to15 months, the interest rate for term loans is negative. Simply raising theinterest rate would not help, however, because policy objectives are complexand would be affected differently by such a change. Formulation of an interestrate policy is made more difficult by the fact that the country has a freeforeign exchange system, and medium-term capital is freely available fromoverseas capital markets, currently at rates around 12%. These foreign marketshave been tapped mainly by joint-venture companies and Indonesian businessmenof Chinese origin who have long established contacts overseas. This causespolitical and social strains since indigenous entrepreneurs are at a dis-advantage, paying rates of interest on locally borrowed funds higher thanthose available to competitors with access to foreign capital markets. Allfactors considered, the 15% rate appears reasonable. If the recent containmentof price pressures proves short-lived, and inflationary trends re-emerge, GOIwill need to review its interest rate policy. In the past, the Governmenthas been quite sensitive to monetary developments which threaten price stability.

2.28 In 1972 and 1973, when IDA made the first Credits to BAPINDO andPDFCI, GOI insisted on assuming the exchange risk itself on the grounds that

-9-

the Indonesian Rupiah was a relatively stable currency, and that most sub-borrowers were not sophisticated enough to understand the complexities ofmultiple currency exchange risks. The Bank has accepted GOI's view that it,rather than the ultimate borrower, should assume the exchange risk under theproposed loan. However, the spread allowed to BAPINDO would be restrictedto a maximum of 4%, as in the case of the first Credit. The difference, ifany, between the final on-lending rate and the sum of the rate charged by GOIto BAPINDO (the Bank's current rate) and the maximum spread of 4%, would bepassed on to GOI as a fee for assuming the exchange risk.

III. INSTITUTIONAL ASPECTS

BAPINDO Act

3.01 The draft of a new BAPINDO Act had been agreed upon by the Associa-tion, GOI and BAPINDO in 1972. Two key provisions were: (a) increasing theauthorized capital from Rp 60 million to Rp 20 billion, and (b) expanding theSupervisory Board to a minimum of four members, including persons with expe-rience in industry and finance. The new Act was expected to be passed promptlyby the legislature. In the event, the revised Act has not yet been passedby the legislature because of a crowded schedule. GOI has now concluded thatthe procedure of using a separate Act of Parliament to establish or amend thecharter of a state bank is too cumbersome, and that it should control thefunctions of banks like BAPINDO through the provisions of the existing Banking

Act. GOI, therefore, does not intend to press Parliament for passage of thedraft BAPINDO Act, but will take administrative steps to implement the mainchanges contained in the Act. BAPINDO's authorized capital will be increasedto Rp 50 billion by end December 1974. Arrangements will also be made forappropriate changes relating to BAPINDO's Supervisory Board (see paragraph 3.06).

Policy Statement

3.02 BAPINDO's operations are guided by a policy statement 1/, draftedin consultation with the Association, adopted by its Board of Managing Directors,and approved by the Supervisory Board early in 1972. It is similar in mostrespects to policy statements adopted by other development finance companiesassociated with the WBG, and is acceptable to the Bank. No change has beenmade in the statement since its adoption, and none appears necessary at thepresent time.

Organization Structure

3.03 Head Office. In mid-1971, the Association agreed with the Govern-ment and BAPINDO on a scheme for a radical reorganization of BAPINDO. By

early 1972, sufficient progress had been made to justify a first Credit to

1/ See Annex 7.

- 10 -

BAPINDO. BAPINDO's capital structure had been greatly improved, the seniormanagement had been strengthened and BAPINDO had engaged four competentAdvisors recommended by WBG. The selection of managers for, and allocationof staff to, different departments had been completed, except for the MaritimeCredit Department (MCD) which became operational in mid-1973; two additionalAdvisors, recommended by WBG, were also attached to MCD. Since then, thedepartments have settled down and are working fairly smoothly. Better inter-action is needed between the Research Department, which does the economicwork for BAPINDO, and the Credit and Follow-Up Department, and BAPINDO'smanagement is seeking to bring about the required improvement. The ProjectPromotion Department spends most of its time supervising problem loans, insteadof doing its stated job of project promotion. This anomaly has been recognized,and BAPINDO's management expects that a modest beginning in project promotionwill be made in the near future, without detriment to the supervision of pro-blem loans.

3.04 Branches. In 1972 BAPINDO had agreed with the Association that itwould close down uneconomic branches. During 1973, 8 out of 18 branches weretransformed into Representative Offices, each with a reduced staff. Theseoffices will concentrate on developing new business and supervising existingprojects.

3.05 General performance at the branches has been weak. The best avail-able talent has become concentrated at Head Office, although the branchesstill perform important operational work. The weakness of the branches slowsdown the overall pace of activity. The branches also feel isolated from thebroad currents of activity at Head Office. BAPINDO is trying to correct thesituation through a systematic training program conducted at the Head Officefor staff from the branches, regular rotation of assignments, and by frequentHead Office staff visits to the branches. This approach seems appropriateand should gradually bring about improvement in the efficiency of the branches.

Supervisory Board, Management and Staff

3.06 Supervisory Board. The present BAPINDO Act designates the Ministerof Finance and the Governor, Bank Indonesia, as the two members of the Super-visory Board. The preoccupation of its members with state business hasprevented them from effectively supervising, and providing policy guidanceto, BAPINDO's Board of Managing Directors. GOI has agreed that, if legallypossible, the Minister of Finance and the Governor of Bank Indonesia willdelegate their authority to qualified representatives who will have more timeto oversee BAPINDO's operations. GOT will also investigate the possibilityof appointing three additional members to the Board, under the provisions ofthe original BAPINDO Act. An enlarged, effective, Supervisory Board wouldbetter represent BAPINDO's interests in the councils of Government, as alsoin the financial and business communities.

3.07 Board of Managing Directors. BAPINDO's Board of Managing Directorsis composed of a President and four Managing Directors. Except for one mem-ber promoted from within, all other members, including the President, were

new to development banking, when they were appointed. They drew heavily onAdvisors (see the following paragraph) and outside consultants for specifictasks, and on the WBG for advice. They have all worked hard and learnedquickly, gaining experience and with it confidence. During 1972 and 1973their attention was focussed on implementing the reorganization and improv-ing internal procedures, so that BAPINDO could effectively take on newbusiness. This preoccupation with internal reorganization, required byBAPINDO's specific situation, resulted in insufficient attention to long-range planning and operational planning systems. The management has nowstarted to remedy these deficiencies, in particular in the area of longer-term financial planning. The WBG will continue to assist BAPINDO's manage-ment in whatever way it can.

3.08 Advisors. As part of the reorganization, four Advisors wereappointed, in 1971 and early 1972, togrovide support to BAPINDO's newmanagement. Two more advisors were appointed in late 1972 when the MaritimeCredit Department was established. All the Advisors were selected and recom-mended to BAPINDO by the WBG. The contracts of all the Advisors were due toexpire between May and October 1974, prompting, earlier this year, a thoroughevaluation of their performance. BAPINDO and the WBG concluded that theAdvisors had collectively contributed significantly to BAPINDO's developmentand improved performance. It was agreed with BAPINDO that the time had cometo start a gradual reduction in the number of Advisors. Accordingly, thecontract of one Advisor was allowed to expire in May 1974, and that of anotherwas renewed until December 1974. The contracts of two others have beenextended, one to expire in the summer of 1975 and the other in 1976. Requiredchanges in the terms of reference have been agreed upon. The contracts ofthe Maritime experts will be renewed for one more year up to October 1975;the need for continuing their services beyond this period will be reviewed insummer 1975. UNDP and the Governments of Japan and Australia have contributedtowards meeting the cost of these technical experts.

3.09 Staff. One of BAPINDO's achievements during 1973 was a 40% reduc-tion in total staff, both at Head Office and at the branches (from more than1,263 to 750). The retrenchment mainly covered clerical and lower supportstaff, whose numbers were bloated beyond BAPINDO's needs in the past. BAPINDOhandled the reduction imaginatively and compassionately, in close cooperationwith the Department of Manpower. Major results of this staff reduction havebeen a general organizational streamlining, a sense of renewed purpose amongthe retained staff, and marked improvement in efficiency.

3.10 BAPINDO's staff at the professional level is generally well quali-fied. Following the resumption of lending activity in early 1972, technicalassistance from the Advisors, the Association's extension of two Credits in1972, adoption of systematic training methods, a significant reduction instaff numbers, and improvements in compensation, staff morale and motivationhave improved visibly. BAPINDO needs to hire some economists (see paragraph3.12) and engineers, particularly in the Maritime Credit Department. BAPINDO's

- 12 -

Personnel Department has drawn up a long-term staff development plan and,

significantly, the training budget for 1974 was increased by 80%, reflectingthe high priority accorded this activity.

Procedures

3.11 Appraisal. BAPINDO's appraisal standards have improved consider-

ably over the last two years, in part because of the efforts of the Advisors,

and in part because of the priority BAPINDO's management assigned to staff-

training in project appraisal work. Appraisals are now undertaken in a

systematic manner, and the financial and technical aspects are usually handled

satisfactorily. The Management and Advisors are conscious of the need to

continue improving appraisal work, and two senior officials from BAPINDO made

4-month visits this year to the Industrial Mining and Development Bank of

Iran and the Korea Development Finance Corporation, under a UNDP project forwhich the Bank is Executing Agency, for further study in appraisal techniques.

3.12 BAPINDO's appraisals are less satisfactory in covering marketing

and economic aspects. Reliable statistics are hard to come by in Indonesia,and this problem is compounded by the fact that most of BAPINDO's clients

are not sophisticated enough to undertake detailed market studies on their

own. Emphasis in BAPINDO's economic appraisal is given to partial indica-

tors and effective rates of protection, but economic rates of return are not

calculated. BAPINDO has agreed to upgrade its capability in this area, and

to develop a suitable methodology with the WBG's assistance.

3.13 Supervision. A separate division to concentrate on supervisionactivity was not set up until late 1973. Follow-up work done so far has been

largely in conjunction with processing of applications for rescheduling old

loans, or making additional loans to old customers. One of the major diffi-culties encountered was inadequate past appraisals. Supervision work must

now be concentrated at the branches; this is where the actual supervision

takes place. BAPINDO is currently actively engaged in drawing up a practicalsupervision manual, and has sent one of its senior officials to the Private

Development Corporation of the Philippines to study its supervision procedures,at the WBG's suggestion.

3.14 Procurement and Disbursement. BAPINDO's guidelines for procurement

appear satisfactory but implementation in the past was not strict, (e.g. for

imported items the requirement that the applicant obtain several quotations

was not always followed), and depended on the initiative of the engineerconcerned, varying considerably from project to project. Branch staff werelax in following procedures, but the Engineering Advisor has now worked out

clearer procedures which are expected to make procurement more efficient.IDA's comments on subprojects also helped tighten procedures.

3.15 Loan disbursements for imported items are made after checkingappropriate documents, including suppliers' invoices and bills of lading.

- 13 -

Loan disbursements for local expenditures are made on the basis of physicalinspection and verification of documents supporting expenditures. Disburse-ment procedures are satisfactory, and no problems exist in following WBGprocedures.

3.16 Internal Control and Accounting. BAPINDO hired outside consultantsto improve its internal control and accounting systems. Their recommendationsreceived in August 1973 are currently being implemented throughout the organi-zation. The shift to the new system was completed at Head Office and Jakartabranch by August 1974, and should be in place throughout the institution bymid-1975. Retraining of staff and upgrading of procedures is proceedingsimultaneously. The transition to the new system has been smooth and imple-mentation is currently ahead of schedule.

IV. OPERATIONS AND FINANCIAL CONDITION

Summary of Operations

4.01 BAPINDO's operations fall into three distinct categories: (i) in-dustrial loans, (ii) maritime sector loans, and (iii) short-term raw cottonloans. Industrial lending was BAPINDO's original function, with the emphasisalternating between medium-term lending and short-term lending. Within thedesign of institutional financing arrangements agreed upon by GOI and the WBG,BAPINDO was to concentrate on medium- and long-term financing; it, therefore,gave up short-term lending in 1972. It has however continued to finance per-manent working capital and to make short-term loans to its term loan clients.Maritime sector lending commenced in 1972 when BAPINDO was designated as thechannel for foreign credits to the maritime sector. Lending for raw cottonstarted in 1967 when BAPINDO was designated administrator for importing rawcotton under US PL 480 agreements, for distribution to selected spinning mills,at prices subsidized by GOI.

4.02 Except for making raw cotton loans, BAPINDO was relatively inactiveduring 1971, because GOI had stopped it from making new loans in late 1970,and before that it did not have adequate resources. It restarted operationsin 1972, after the reorganization had made some progress. A summary ofBAPINDO's loan operations is given in Annex 8, and commitments for 1972 and1973 are shown below:

- 14 -

Commitments(Amounts in Rp. millions)

1972 1973

No. Amount No. Amount

Industrial Loans/1 44 2,773 105 9,933

Maritime sector loans 3 64 40 2,244

Raw cotton loans 19 14,360 18 38,538

Total 66 17,197 163 50,715

/1 Including Investment and Permanent Working Capital Loans.

During most of 1972 BAPINDO was still preoccupied with reorganizing andsorting out the weak portfolio inherited from the past. It was not until1973 that BAPINDO began to operate more normally, and was better gearedto handle an increasing volume of new business.

Industrial Loans

4.03 Investment Loans. -/ BAPINDO made commitments for 53 investmentloans for Rp 7.3 billion in 1973, compared with 26 loans for Rp 2.1 billionin 1972. Total commitments as of December 31, 1973 amounted to 165 loanstotalling Rp 19.5 billion. Textile projects took 41% of cumulative commit-ments, reflecting the predominance of this sector in Indonesia's industrialstructure. The next largest sectors were rubber processing with 14% andtourism with 13% of total commitments. Most loans for rubber processingwere made between 1969 and 1971, when BAPINDO was administrator of'a spe-cial GOI loan program for this sector.

4.04 The average size of BAPINDO's commitments in 1973 was Rp 133 mil-lion 2/ ($320,000), a substantial increase over the comparable figure ofRp 80 million ($193,000) in 1972. The larger size of loans mainly reflectedworldwide inflation, and involvement in textile projects of relatively largersize. The average loan size, other than textiles, rose only marginally fromRp 61 million to Rp 68 million between 1971 and 1973. About 60% of BAPINDO 'sloans were below $200,000 equivalent, and only 5 out of a total of 165 invest-ment loans were for more than the equivalent of $1 million. 70% of cumulative

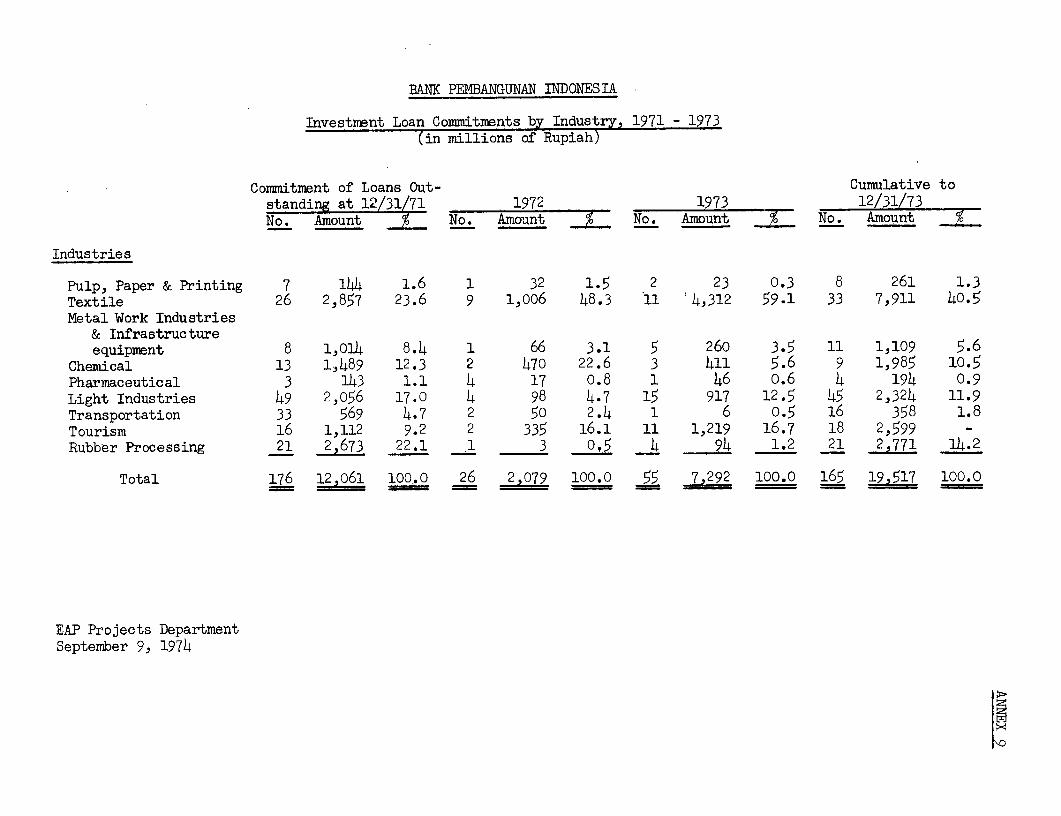

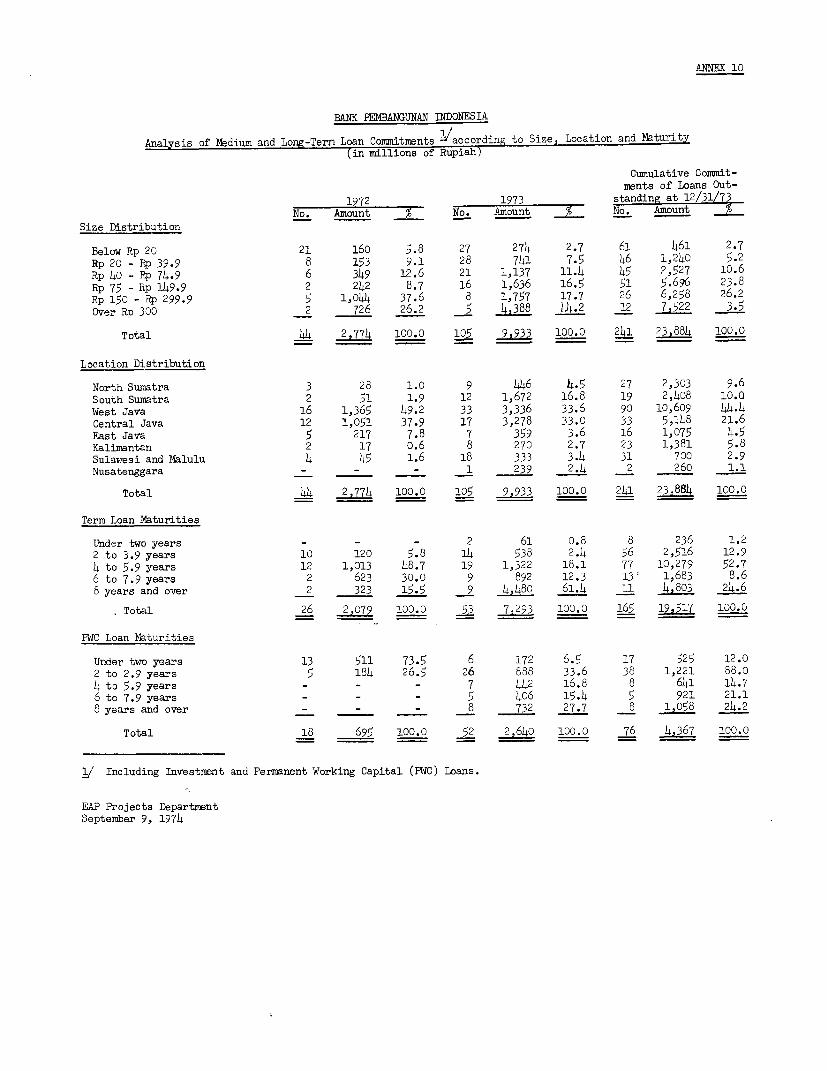

1/ Data on Investment Loan Commitments by size, duration, geographicallocation, and by industry are shown in Annexes 9 and 10.

2/ Because BAPINDO finances, on average, about 75% of total project cost,its share reflects a total average project cost of about Rp 177 million.

- 15 -

commitments at year-end 1973 were made to clients in Java, reflecting thegeographic concentration of 78% of all medium- and large-scale enterprisesin that island. Within Java, however, commitments in Central Java rose to21% of total commitments in 1972 and 1973 compared to 8%in 1971. BAPINDO'sloans committed during 1973 had an average repayment period of between fiveand six years, while nine out of a total of 53 loans were made for more thanan eight-year period. There has been a visible lengthening of loan maturities,which is par'tly a result of comments made by the WBG on BAPINDO's generallyover-optimistic estimates of the repayment capacity of sub-projects it pro-posed to finance.

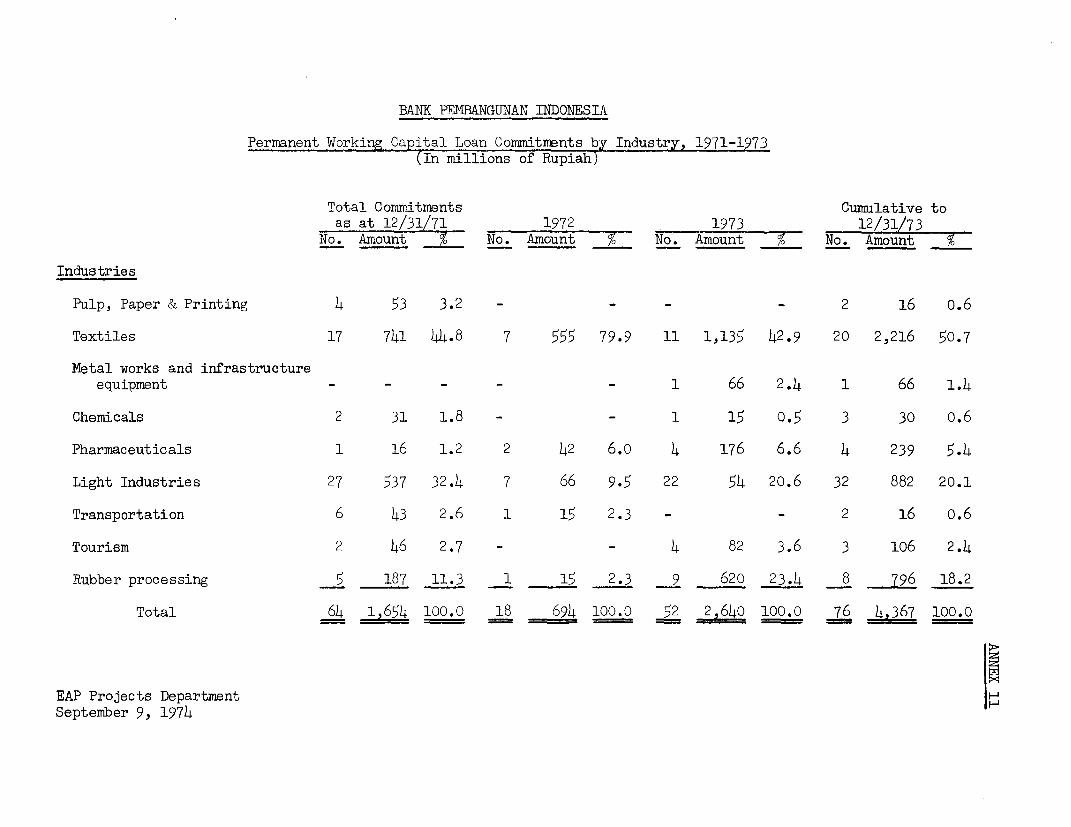

4.05 Permanent Working Capital'Loans (PWCL). -/ BAPINDO's PWCL's areextended to its term loan clients, and accounted for about 25% of totalindustrial lending in 1973 (52 loans for Rp 2.6 billion). Until mid-1973,PWCLs were usually made for one year and were renewed every year. Sincemid-1973, however, repayment schedules have been fixed according to theestimated debt servicing capacity of customers. In 1973, PWCLs had anaverage repayment period of between four and five years. The industrialdistribution of PWCLs was similar to that of equipment loans, with textilesaccounting for 51% of cumulative commitments. PWCLs were also concentratedin Java (69%). In 1973, the average size of PWCLs was Rp 50 million, doublethe 1971 size, but only half the average size of investment loans.

4.06 Small Business Co-Financing with Regional Development Banks. Agood example of BAPINDO's growing confidence and ability to innovate isthe co-financing scheme set up with selected Regional Development Banks(RDB's) 2/. BAPINDO has been actively concerned with increasing its assist-ance to small-scale industry. In 1973, two pilot projects were set up withthe RDB's of Central Java and Bali jointly to finance small-scale enterprises.BAPINDO set up lines of credit of Rp 50 million each, to be used by the RDB'sto extend investment loans and PWCLs not exceeding Rp 5 million each forindividual customers. Arrangements were made for,P.T. ASKRINDO to insure 80%of the loan risk, the balance being borne by BAPINDO and the RDB in proportionto their share in the sub-loan. Following changes in the constitutionalstructure of the RDB's late in 1973, which freed them from direct interferenceby provincial Governors, Bank Indonesia brought this co-financing scheme withinthe ambit of the INVESTASI program (see Annex 3). This provided BAPINDO witha welcome additional source of funds. By April 1974, BAPINDO had added threemore RDB's to this scheme, and revised its earlier agreements to bring itstotal lines of credit to,RDB's to Rp 1.05 billion. Four more agreementshave been signed since that date.

1/ Data on PWCLs by size, duration, geographical location and by industryare shown in Annexes 10 and 11.

2/ Further details of this scheme are provided in Annex 12.

- 16 -

4.07 Before extending lines of credit to the RDB's, BAPINDO made care-ful appraisals of each institution. A program for correcting organizationaldeficiencies was agreed upon with each RDB's management. Selected RDB offi-cials are already attending training courses at BAPINDO, and officials fromBAPINDO are expected to be deputed for tours of duty with the RDB's. BAPINDOdoes not involve itself in sub-project appraisals, but those exceedingRp 2 million require ASKRINDO's prior approval.

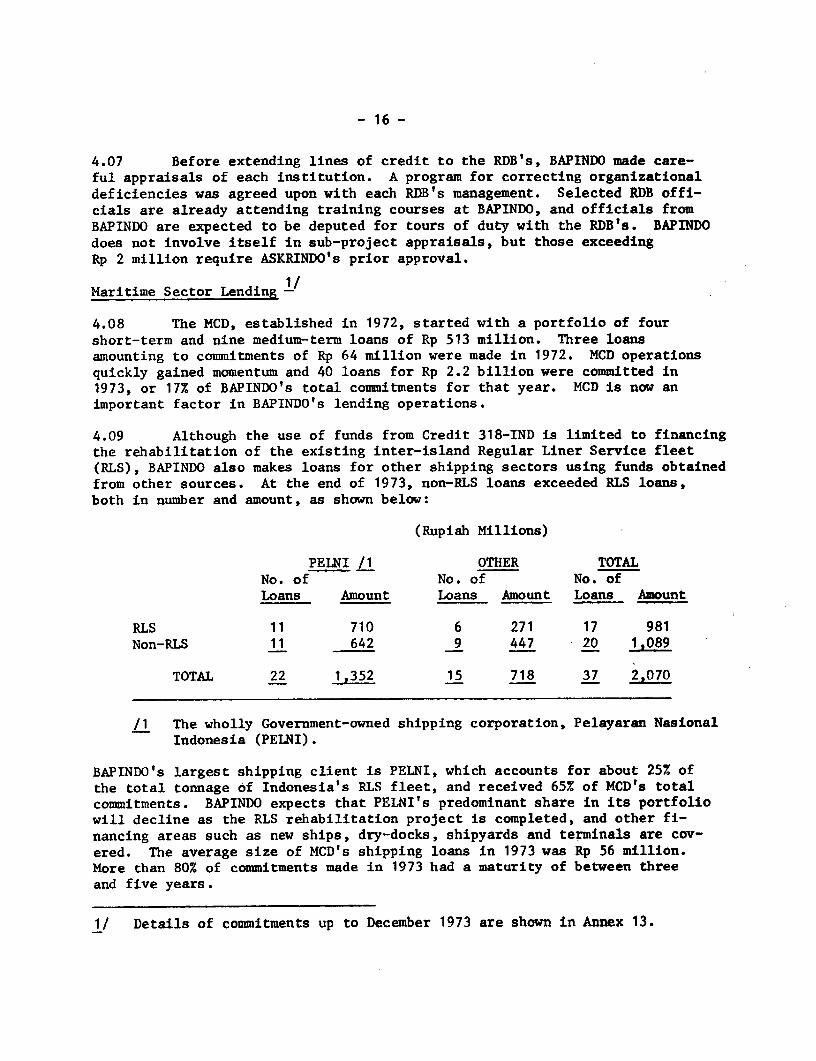

Maritime Sector Lending -/

4.08 The MCD, established in 1972, started with a portfolio of fourshort-term and nine medium-term loans of Rp 513 million. Three loansamounting to commitments of Rp 64 million were made in 1972. MCD operationsquickly gained momentum and 40 loans for Rp 2.2 billion were committed in1973, or 17% of BAPINDO's total commitments for that year. MCD is now animportant factor in BAPINDO's lending operations.

4.09 Although the use of funds from Credit 318-IND is limited to financingthe rehabilitation of the existing inter-island Regular Liner Service fleet(RLS), BAPINDO also makes loans for other shipping sectors using funds obtainedfrom other sources. At the end of 1973, non-RLS loans exceeded RLS loans,both in number and amount, as shown below:

(Rupiah Millions)

PELNI /1 OTHER TOTALNo. of No. of No. ofLoans Amount Loans Amount Loans Amount

RLS 11 710 6 271 17 981Non-RLS 11 642 9 447 20 1,089

TOTAL 22 1,352 15 718 37 2,070

/1 The wholly Government-owned shipping corporation, Pelayaran NasionalIndonesia (PELNI).

BAPINDO's largest shipping client is PELNI, which accounts for about 25% ofthe total tonnage of Indonesia's RLS fleet, and received 65% of MCD's totalcommitments. BAPINDO expects that PELNI's predominant share in its portfoliowill decline as the RLS rehabilitation project is completed, and other fi-nancing areas such as new ships, dry-docks, shipyards and terminals are cov-ered. The average size of MCD's shipping loans in 1973 was Rp 56 million.More than 80% of commitments made in 1973 had a maturity of between threeand five years.

1/ Details of commitments up to December 1973 are shown in Annex 13.

- 17 -

Raw Cotton Loans

4.10 The unsettled state of BAPINDO's organization during 1971-72did not affect its raw cotton business, because it did not appraise theseshort-term loans. GOI identifies borrowers, indicates amounts to be loaned,and BAPINDO acts only as an executing agency, concerned with opening LC's,handling documents, and collecting repayments. Bank Indonesia providesBAPINDO with the major part of funds for financing the import of cotton.BAPINDO finances freight and other local currency costs from its own funds(about Rp 10.5 billion or 20% of ttal raw cotton loans in 1972 and 1973).The raw cotton loans are usually for a period of one year.

4.11 Raw cotton commitments totalled 11 loans for Rp 13,062 million in1971, 10 loans for Rp 14,360 million in 1972, and 18 loans for Rp 38,538million in 1973. The sharp increase in average loan size from Rp 755 millionin 1972 to Rp 2,141 million in 1973, reflected increased world market pricesfor cotton, and reduction (subsequently abolition in 1973), of governmentexchange rate subsidies for raw cotton imports.

4.12 In 1972, the Association had agreed with GOI and BAPINDO that rawcotton lending would be phased out and that BAPINDO would concentrate onmaking medium- and long-term loans. A sudden termination of.raw cotton lend-ing was not envisaged, as this would have affected BAPINDO's-profitabilityadversely. Term lending operations have now developed sufficiently so thatan end to raw cotton lending should not seriously impair BAPINDO's financialstability. GOI has decided to transfer, by the end of 1974, the raw cottonimport lending to Bank Ekspor-Impor (EXIM) with which BAPINDO already sharesthis business. One textile mill importer's account will remain with BAPINDO,because it is also a long-term loan client.

Equity Financing

4.13 BAPINDO had not made any equity investments before mid-1974, whenit agreed to invest up to 40% of the proposed equity of the newly establishedNational Fleet Development Corporation (PANN). The WBG did not earlierencourage such investments because BAPINDO had still to demonstrate the organi-zational competence to undertake an adequate appraisal of such operationsinherently more risky than lending. With the recent improvements in itsorganizational structure and appraisal capability, it should now considermaking modest equity investments. It should thus play a role in implementingGOI's decision to encourage the growth of "pribumi" entrepreneurs. One wayof converting "non-pribumi" customers t a "pribumi" status would be for BAPINDOto buy a share of the equity of such companies, for later resale to Indonesianprivate individuals or companies. GOI also plans to use BAPINDO as a channelfor equity investments in joint-venture companies to ensure that such com-panies achieve the required minimum Indonesian participation. BAPINDO isnot expected to assuime the risk for such investments, and will be suppliedwith the required funds by GOI. Guidelines for such investments are presentlybeing formulated by GOI.

- 18 -

Resources

4.14 For the bulk of its domestic currency resources BAPINDO is, andwill continue to be, dependent on the Government. Funds are provided inthe form of increases in its share capital, through'Bank Indonesia in theform of refinance facilities (INVESTASI), and through long-term loans. During1973 when BAPINDO's liquidity position was good, Bank Indonesia withdrewthe refinance facility; but this will be restored in late 1974 with thequickening pace of BAPINDO's commitments.

4.15 BAPINDO's foreign exchange resources consist of the two IDA Creditsmade in 1972. The general industrial credit has been almost fully comnitted;the maritime credit had an uncommitted balance of $5.6 million as ofSeptember 30, 1974. Because BAPINDO continues conditionally to approveprojects which it plans to finance from the proposed Bank loan, it has askedfor a relaxation of the "90 day rule", covering commitments made prior tothe effectiveness of the loan. The request is acceptable since it is desirableto maintain the continuity of Bank Group financing (paragraph 5.11).

Financial Position

4.16 BAPINDO's December 31 summary balance sheets for 1970, 1971, 1972and 1973 are given in Annex 14.

4.17 In the two years following the lifting of the restriction on termlending in 1971, BAPINDO's total assets grew by 16.8%. Significant changeswere a 15.3% increase in the raw cotton loan portfolio to Rp 15.2 billion,and a 29.5% increase in the portfolio of medium- and long-term investmentloans to Rp 14.4 billion. BAPINDO's loan portfolio, including investmentloans, raw cotton loans and working capital loans, rose from 80.8% of totalassets in 1971, to 84.1% of total assets in 1973. The loan portfolio andtotal assets grew in spite of massive write-offs amounting to Rp 1.86 billionduring 1972 and 1973. Write-offs of such magnitude are not expected in thefuture.

4.18 BAPINDO's financial position has improved significantly duringthe last two years, mainly due to the conversion of Rp 6.5 billion GOI loansinto equity in 1971, and the receipt of cash towards additional equity ofRp 4 billion during 1972 and 1973. The Government paid in an additional amounttotalling Rp 9.3 billion during the first quarter of 1974. The provision fordoubtful debts is now considered adequate by BAPINDO's auditors; for thefirst time in its history, BAPINDO's 1973 financial statements received anunqualified opinion and clean report from its auditors. As of December 31,1973, BAPINDO's debt/equity ratio was 2.2:1, well within the maximum 3:1stipulated in the IDA Project Agreement.

Profitability

4.19 Summary income statements for the years ended December 31, 1970,1971, 1972 and 1973, are given in Annex 15. BAPINDO had a spread of about

- 19 -

7% on its loan operations in 1972 and 1973. Despite the high spread, itsprofitability was poor. In 1973 it made a net after-tax profit of Rp 608million, as compared to a negligible profit of Rp 54 million in 1972. The1973 profit would have been Rp 1,023 million, but for the extraordinary ex-pense of Rp 415 million, incurred on severance pay under the massive re-trenchment program. The poor profit performance in the past was largelydue to sizeable provisions for losses on the older portion of its loan port-folio, and also to its administrative and personnel expenses, high in rela-tion to a somewhat stagnant portfolio. These factors will be less impor-tant in coming years, because the staff has already been considerably re-duced and the loan portfolio will grow rapidly.

4.20 The raw cotton loan portfolio has been crucial to BAPINDO'sprofitability. Thp income from this activity was Rp 832 million in 1973;without it BAPINDO would have made a loss of Rp 577 million for the year.It is expected that increasing income from the fast growing medium- andlong-term portfolio, will adequately compensate for the loss of incomefrom raw cotton loan operations after 1974.

4.21 BAPINDO is not expected to pay dividends to its sole owner, GOI,and profits, after adjustments, will be retained.

Quality of Portfolio -

4.22 In assessing the quality of BAPINDO's loan portfolio, due consid-eration has to be given to the fact that the loan repayment record has beengenerally unsatisfactory in Indonesia. All financial institutions sufferfrom this problem; some seriously. In BAPINDO's case, the situation hasimproved considerably since 1972, although arrears 2/ are still quite high,as the following table shows:

1/ Annex 16 gives an analysis of BAPINDO's loans in arrears.

2/ BAPINDO considers loans to be in arrears on the day an instalmentbecomes due, and no allowance is made for a grace period or for atransit period between branches and Head Office. In measuring thequality of BAPINDO's portfolio, arrears of more than six months havebeen considered. If arrears of more than 3 months were to be con-sidered, the 1973 percentages would change from 15% to 20% and 36% to 53%for medium- and long-term loans, from 59% to 61% and 60% to 62% forshort-term loans. Percentages for raw cotton loans would remainunchanged.

- 20 -

As percentage oftotal loans outstanding

Loans Outstanding Principal Principal Outstanding(Rp million) In Arrears Affected by Arrears

1972 1973 1972 1973 1972 1973December 31

Medium & long-term 13,118 16,193 28 15 62 36

Short-term industrialloans /1 704 386 74 59 74 60

Maritime loans 576 1,810 53 11 75 13

Raw cotton loans 17,752 15,295 5 1 33 24

Total 32,150 33,684 16 12 46 30

/1 These loans were made before 1971 (BAPINDO no longer makes short-termloans), and BAPINDO does not have any leverage unless a new loan issought. These clients are still being pursued with the hope thatsome part of these loans may be recovered.

4.23 The maritime and raw cotton loan portfolios are in much bettercondition than the industrial loan portfolio. The maritime portfolio im-proved dramatically after PELNI, the largest maritime client, cleared itsarrears, following a reorganization required by BAPINDO as a condition ofcontinued financial assistance. Raw cotton loan clients always had a strongincentive not to default, in order to remain eligible for the followingyear's cotton quota; textile mills are also relatively more profitable. Inthe industrial loan portfolio, textiles, tourism and pharmaceuticals projectshad relatively good records; while metal works, pulp, paper and printing,transportation and rubber processing were among the group of troublesomeprojects.

4.24 As of December 31, 1973, BAPINDO undertook an account by accountanalysis which resulted in the following qualitative classification of thetotal medium- and long-term loan portfolio:

- 21 -

(% of total amount outstanding)

Good loans /a 36.9Slow loans lb 16.7Problem loans /c 34.6Bad loans /d 11.8

100.0

/a Payments regular and on time.

/b Payments regular, but often late.

/c Projects needing special attention, with active BAPINDO involvmentaimed at improving repayment records.

/d Companies in, or close to liquidation, with no reasonable hope of resump-tion of regular payments.

One of the more important reasons for high arrears is inadequate pastappraisals which stipulated unrealistically short repayment schedules, sincethe INVESTASI program did not allow a repayment period exceeding 5 years.Many customers, with otherwise satisfactory growth and pr4fit performance,found themselves unable to repay term debt without adversely affecting opera-tions, because of a general shortage of working capital. Some arrears alsoresulted from genuine financial difficulties due to technical, marketing ormanagement reasons.

4.25 BAPINDO is acutely conscious of the need to upgrade the loan port-folio through both better appraisals and greatly strengthened supervisionwork at Head Office and branches. The arrears situation should improvesubstantially as a result. However, following the recent imposition of asevere credit squeeze as part of GOI's anti-inflationary measures, a slowdownin repayments may result for the entire banking system, and BAPINDO cannothope to be an exception. The provision for bad debts, however, appears tobe adequate.

V. PROSPECTS

General Outlook

5.01 Indonesia's overall economic prospects remain bright. DuringRepelita II (see paragraph 2.03) total gross investment is expected to risefrom Rp 1,100 billion or 17.7% of GDP in fiscal 1974 to Rp 3,150 billion or23% of GDP in fiscal 1979. The share of the industrial sector is expected togrow from 9.8% of GDP in fiscal 1974 to 12.5% in fiscal 1979; the growth rateof the industrial sector is expected to average 13% annually during the Planperiod. Within the industrial sector, GOI is committed to a policy of giving

- 22 -

full scope and encouragement to the private sector, and to developing indigenousIndonesian enterprise. Despite the obstacles mentioned in paragraph 2.14,the recent growth of industry has resulted in an investment demand which thelocal term lending institutions have not been able to fulfill; reliance hashad to be placed on private external financial institutions to make up thedifference. In the foreseeable future, as in the past, BAPINDO's businesswill be limited by its own processing capacity rather than by a lack of demand;the needs for long-term capital are large and continuing.

BAPINDO's Business Forecasts

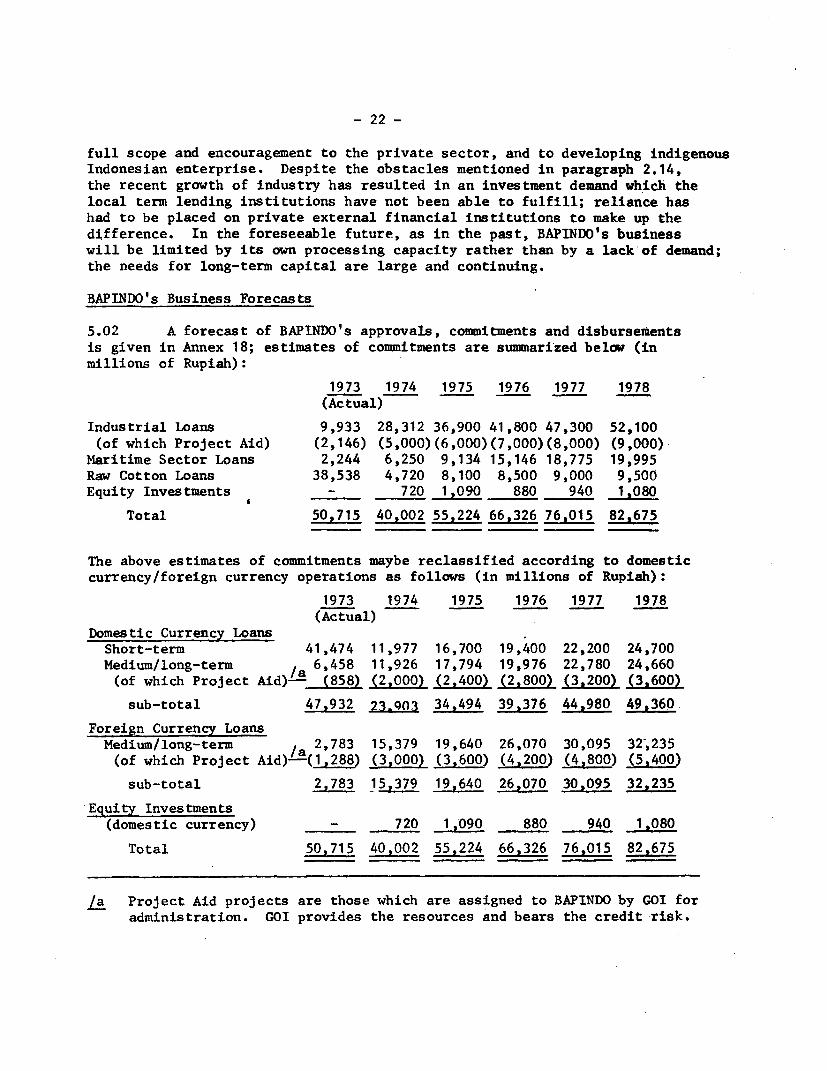

5.02 A forecast of BAPINDO's approvals, commitments and disburserentsis given in Annex 18; estimates of commitments are summarized below (inmillions of Rupiah):

1973 1974 1975 1976 1977 1978(Actual)

Industrial Loans 9,933 28,312 36,900 41,800 47,300 52,100(of which Project Aid) (2,146) (5,000)(6,000)(7,000)(8,000) (9,000)

Maritime Sector Loans 2,244 6,250 9,134 15,146 18,775 19,995Raw Cotton Loans 38,538 4,720 8,100 8,500 9,000 9,500Equity Investments - 720 1,090 880 940 1,080

Total 50,715 40,002 55,224 66,326 76,015 82,675

The above estimates of commitments maybe reclassified according to domesticcurrency/foreign currency operations as follows (in millions of Rupiah):

1973 1974 1975 1976 1977 1978(Actual)

Domestic Currency LoansShort-term 41,474 11,977 16,700 19,400 22,200 24,700Medium/long-term /a 6,458 11,926 17,794 19,976 22,780 24,660(of which Project Aid) - (858) (2,000) (2,400) (2,800) (3,200) (3,600)

sub-total 47,932 23,q93 34.494 39,376 44,980 49,360

Foreign Currency LoansMedium/long-term / 2,783 15,379 19,640 26,070 30,095 32,235(of which Project Aid) -(1,288) (3,000) (3,600) (4,200) (4,800) (5,400)

sub-total 2,783 15,379 19,640 26,070 30,095 32,235

Equity Investments(domestic currency) - 720 1,090 880 940 1,080

Total 50,715 40,002 55,224 66,326 76,015 82,675

/a Project Aid projects are those which are assigned to BAPINDO by GOI foradministration. GOI provides the resources and bears the credit risk.

- 23 -

5.03 BAPINDO's past performance is not a good indicator of its potentialfor the future. The above projections appear optimistic but are fullyjustifiable from the point of view of the demand, and are backed up by astrong pipeline of pending loan applications (Rp 61 billion as of April 1,1974). The projections indicate that the proportion of short-term loans intotal commitments will decline significantly, from about 75% in 1973 to about30% throughout the projected period. This is because while medium- andlong-term loans increase much more rapidly than in the past, (a) raw cottonloan business is being transferred to EXIM and (b) BAPINDO has restrictedshort-term lending to its term clients. With the single exception noted inparagraph 4.13 above, BAPINDO has not made equity investments in the pastbut expects to make a start in 1974. Maritime sector operations will accountfor 20-25% of total estimated commitments. An analysis of the pipelineindicates that the textile industry could account for about a third ofBAPINDO's industrial lending followed by the chemical industry (about afourth) in the next two years.

Resource Requirements

5.04 Domestic Currency. Other than retained earnings, deposits andcollections, BAPINDO is completely dependent on the Government for domesticcurrency resources. As of January 1, 1974, BAPINDO had a surplus of Rp 2.8billion on a disbursement basis. However, BAPINDO had a deficit of Rp 3.8billion if undisbursed commitments are also taken into account. Domesticcurrency resources needed to meet new commitments, including Project Aidprojects, stated in paragraph 5.02 would amount to about Rp 98 billion for1974, 1975 and 1976. Including the deficit as of January 1, 1974, totalresource requirements for the three years 1974-76 would be about Rp 102 billion(including Rp 7 billion for Project Aid projects) on a commitment basis. Ofthis amount, Rp 20 billion are estimated to be provided by net collections,deposits and internal cash generation. The balance of Rp 82 billion wouldhave to be provided by the Government. BAPINDO has assumed that its capitalwill be increased by Rp 20 billion during 1974-76, and that the balance willbe provided in the form of loans and INVESTASI refinance facility. Consider-ing the amounts of funds provided by the Government in the past, it is notunrealistic for BAPINDO to expect Rp 82 billion in a three year period. Earlyin 1974 GOI paid more than Rp 9 billion in equity funds. During the negotia-tions for the proposed loan, understanding was reached with GOI that it wouldcontinue to provide BAPINDO with the rupiah resources needed by the latter,either in the form of equity or loans, to allow it to effectively carry outits rations.

Foreign Currency. BAPINDO's only foreign currency resources aretwo IDA Credits made in 1972. Credit 310-IND is almost fully committed;

Credit 318-IND still has a balanc?'o75.6 million but its use is restrictedto financing of RLS clients. For its estimated commitments during remainingmonths of 1974, 1975 and 1976, BAPINDO would need about Rp 53 billionequivalent (including about Rp 11 billion for Project Aid projects). TheBank has informed BAPINDO that it cannot continue to be its sole source of

- 24 -

foreign exchange funds. Kreditanstalt fur Wiederaufbau (KfW) will send anappraisal mission to BAPINDO in late November this year for a proposed DM 22million loan. BAPINDO is also exploring the possibility of securing financialassistance from Belgique Maatschappij voor Investeering (BMI) and the AsianDevelopment Bank (ADB). It is recommended that the Bank consider $50 millionfor the proposed loan which would account for about one-half of BAPINDO'sforeign exchange resource requirements (excluding Project Aid projects forwhich the Government provides the needed resources) for the period endingDecember 1976.

Projected Financial Position