Embed Size (px)

Citation preview

t , I kD Ir -

FILE COPY ERM-112

INT WATIO11AL BANK VOR RECONTSTRUCTIONT AND DEVTIUOPMiJT

ECOINOMIC DEPARTIET

WORLD COTTOT PRODUCTION, CONSTURMPTION AND TRADE

Prepared by: Maurice F. PerkinsEconomic DepartmentAgriculture, Forest±r and Fisheries Section July 1948

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

TABIE OF CONTENTTS

Page No.Summary

I Climatic Conditions cnd Methods of Production 1 - 3

II Different Growiths of Cotton and Their Relative Prices 3 - 5

III The iaerket for Cotton 5 - 11

IV World Consumption and Trade 11 - 14

V Developments in WJorld Cotton Production 14 - 19

VI Probable Future Pattern of Cotton Production,Consunmtion and Trade 19 - 26

Appendix - Cotton Statistics and Sources

Table A _ World lviill Consumption of Cotton

Table 13 - World Cotton Production

Table C - Average Exoorts from Specified Countries

Table D - Averege Exoorts from Snecified Countries to Specified Importers

Table B - Average Imnorts into Snecified Countries

Tasble F Average Imports to Specified Countries from Specified Exporters

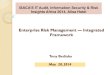

Chart _ Indices of World Mill Consumption of Cotton Related toWorld Population

WORLD COTTON PRODUCTION, CONSUMPTION AND TRADE

SUMMARY

The prime requisite for the nroduction of cotton in most countries is a

supply of cheap labor; this is the chief factor determining the location of

cotton growing areas within the limits set by the temperature and rainfall re-

quirements of the cotton rlants. The quality and thus the price of cotton is

chiefly determined by its staple length.

World cotton mill consumption, since the beginning of the present century,

has been increasing at a proportional rate fo the increase in world ponulation.

During the neriod betwee'n the two World Wars, the oatterns of cotton

production, trade and consumption have shownrn marked changes. There has been a

decrease in United States' production and exports and increases elsewhere, es-

pecially in India, Egypt, Brazil, and Peru, though the United States is still

the worldts largest producer and exporter of cotton. This decline in the relative

position of the United States was caused in the 1920's by the effects of the boll

weavil on production; in the 1930's, the causes wrere much more complicated being

a combination of exchange and trade restrictions, state encouragement abroad

and restriction in the United States, colonial preference systems, etc.

During World War II, disruptions in trade caused a piling up of stocks

and a reduction in world production. Following the war, demand for cotton/et-

panded at a greater rate than production which was held back by the need for

expansion in food acreage. In consequence, prices rose and stocks have declined.

Under circumstances of large-scale international trade there is little likelihood

of a s'.rx'lus supply position in the short-run, although prices will decline as

production expands and excessive demand subsides.

The long-run outlook for cotton, however, is not too clear owing to the

possibility of serious com-oetition from rayon and possibly other synthetic fibers.

The full force of rayon competition has not yet been experienced owing to wartime

disruption of. production and the present excessive demand for textiles.. In the

near future, however, rayon capacity will be of sufficient magnitude to impose

serious competition.

The outcome will likely be determined largely by the relative possibilities

of lowering costs.. In this respect, cotton production in the long-run may wJe.l

trove to be more elastic. Although large-scale mechanized methods are now being

developed in the United States, their applicability over large areas of production

have not been proven; in practice, the introduction of more efficient methods of

nroduction on a world-wide basis is likely to take place slowly and to consist in

a gradual improvement in the techniques of cotton production and the introduction

of more mechanized means of production than is nowi in use.

Whatever the outcome as to the absolute level of world procduction, forces

have been at work which are likely to affect the long-run pattern of cotton pro-

duction and trade amongst individual producing countries. An expansion or even

a maintenance of United States' exports is denendent upon the attainment of a

system of relatively free trade. The pressure of population upon the food supply

will likely have important effects upon India's ability to expand acreage to

even recapture nrewar prod:uction levels unless yields increase or alternate

sources of food surpljy are obtainable abroad. China has suitable land and labor

to permit a considerable expansion in production, but is handicapped by poor trans-

portation facilities. Brazil is potentially a larger producer with the further

development of her transportation system. Tn Egypt, a lackc of irrigated laid

definitely limits acreage exnoansion. Future increases in output amongst minor

producers and in colonial areas is likely. There is a great potential for an

increase in wforld oroduction on a stationarj or even declining acreage by a

general increase in yields through the use of larger quentities of fertilizer.

WORLD COTTON PRODUCTION, CONSUMPTION AND TRADE

I. CLIMATIC CO01DITIONS AND METHODS OF PRODUCTION

Cotton is a subtropical crop produced in the subhumid regions of the world

lying between the 25 and 35 degrees of latitude, north and south of the equator,

although it is nroduced in the USSR as far north as 48 degrees. Cotton requires

a frost-free growing season of 200 days, a minimum of either 20 inches of annual

rainfall with 7 to 8 inches during the growing season, a hot summer, and a fairly

dry harvesting season. Within these zones of latitude there are two general

types of conditions under which cotton is grown: areas requiring irrigation

where rainfall is deficient, and non-irrigated or rain-grown areas.

The chief areas of nroduction are as follows:

Table 1.WORLD COTTON ACERAGE 1909/1944

(thousand acres)

Average Average Average Average Average Average Averte1909/13 1914/18 1920/24 1925/29 1930/34 1935/39 1940/44

United States 34,152 34,616 33,900 42,600 34,658 27,788 22,072India 22,492 22,071 22,405 25,814 23,258 24,204 - 19,270USSR .. . 511 2,017 4,885 5,087China & Manchuria 5,461 5,563 6,451 7,038Brazil 504 584 1,436 1,492 2,446 5,562 5,312Egypt 1,743 1,576 1,748 1,828 1,734 1,821 1,163Peru 163 163 274 304 428 428 356

Total 65,735 79,618 73,860 71,928World Total 68,390 84.410 79,407 81,148

Percentage ofListed Countriesto World Total 96 94 93 89

The worldts seven largest producers of cotton ranked in terms of the size of their

production over the period 1935/39 have controlled 90 percent or better of the

world's acreage and two of them--the United States and India--have contained 64

percent or more.

Within this vast area, production conditions vary to a considerable degree.

The land used may require irrigating--either natural, as in Egept and the Sudan,

or artificial, such as in the arid areas of Peru, the central Asiatic areas of

the USSR or in California--or natural rainfall conditions may prevail, such as in

Brazil, China and Manchuria and most narts of the United States' cotton belt.

hiethods of production also show an infinite degree of variation. The

cotton nlant requires a great deajl more labor in its rroduction than most other

crops, particulerly for thinning, cultivation and harvesting. In the United

States cotton requires five times as much labor as ;,heat and about three and a

half times as much as corn to produce a given gross income. Man-hour requirements

oer acre of cotton account for more than 50 percent of the cost of production.

For this reason, cotton tends to be located in those areas of the w}orld, within

the soil and climatic limits of cultivation, where there is an abundance of cheap

labor. Within this. broad generalization, however, there are variations in the

proportions of land, labor and caipital used, depeniding upon their relative costs.

In Egypt, where high-priced cotton is produced upon high-rent land, the input of

labor reaches its maximum and the yields per acre and quality of the cotton are

amongst the highest in the wsorld. On the other hand, cotton is produced in the

southwestern United States, where labor costs are relatively high, with the ex-

tensive use of mechanized equipment.

An consequence of these and other factors, cotton yields vary considerably:

Table 2YIELDS OF GIfNlED COTTOT PER ACRB 1935/39

pounds)

United States 225.4India 106.1USSR 322.3China and Mlanchuria 193.9Brazil 168.1EgEyt 496.9Peru 428.9

The most important other factors which affect yields are: use of fertilizer,

soil fertility, insect and plant disease, climatic variations, methods of

harvesting. and the productive skills of the farmer. Probably the worst conditiorT

of cultivation are exemplified by India where over large areas the soils are -poor,

practically no fertilizer is applied, low quality seed is used, nests and nlant

diseases are rife and the plant is cultivated with little regard to its natur-l

requirements. Under such conditions, low yields are inevitable and 'productionl is

only profitable in consequence of the extremely cheap labor available.

Any estimate of the cost of production of lint cotton is complicated by

the fact that a valuable by-product,-cottonseed-.is produced at the same time.

Data for the chief producing countries are practically non-existent, except in

the case of the United States.

II. DITFERENT GROWTHS OF COTTON AID THEIR REIATXVE PRICES

Table 3 shows the prices of various types of growths of cotton at Liverpool

over the period 1906 to 1938 converted to U.S4 currency. These types are repre-

sentative of the vast majority of cotton entering into world trade.

The prices over a period of years show a uniformity of movement and a

fairly stable relationship to American middling with the exception of Egyptian

and Indian in the period 193 0/34 and indicate that broad general factors wihich havy

influenced the world cotton market over the period covered have had somewhat simi-

lar effects in each individual cotton marlet. The changes in the premitm or dis-

count to American middling is due to a variety of factors: chaniges in the supply

relationship in respect to demand for each particular growth, cianges in exchcange

rates relative to the pound, government cotton price policies, differential

freight rate changes, etc.

The fact that each particular growth maintains a relatively stable premium

and discount relationship to other growths is a reflection of the differing charac-

teristics of each particular growth and the uises'to wrhich they are put. Cotton

can broadly be divided iinto four groups depending on the length of the fiber or

"istaple":

- 4 -

(1) Very short staole cotton' - not more than 3/4 inch in length.

This cotton is mostly unspinnable and finds its main use in batting

and wadding. The harsh type is used in the nap of cotton blankets. The chief

source of export supply for this type of cotton is India, with China a secondary

source. large ouantities are also produced in the USSR, Netherlands East Indies,

Korea, Persia, and in Asia lMinor; in fact, it is the prevailing characteristic

of all Far Eastern cotton.

(2) Short-staple cotton - 3/4 inch and more, but less than 1 1/8 inches.

(3) Ordinary long-staple cotton - 1 1/8 inches and more, but less than1 3/8 inches.

These two groups of cotton constitute the bulk of world production

and are produced almost exclusively in the United States and South Brazil; large

quantities are also produced in the USSR and in other parts of the world--Upper

Egypt, Peru, Mexico, Africa, etc. India prod-aces large amounts of the short-staple

varieties. These cottons make un the bulk of the raw material for cotton goods and

are most widely used where the characteristics of very short or extra long staple

cotton are not re,quired. Peruvian "Tanguis" is used in spinning asbestos yarns

and mixed wool yarns on account of its roughness.

(4) Extra long-stavle cotton - 1 3/8 inches alnd longer.

This type of cotton is used chiefly in fine thread and for woven

fabrics, knit goods and lace. It is the finest type of cotton and commands the

highest -rice. The chief sources of exoort supply are Lower Egypt, the Anglo-

Egyptian Sudan and Peru, though it is produced in the United States in smell quan-

tities and in Niorthern Brazil, Tanganyika, Uganda, and the British West Indies.

In addition to "1staple length", cotton is also classified on the basis of

"tgrade" (color, brightness, foreign matter, and ginning preparation) and

"character" (diameter, strength, body, maturity, uniformity, and smoothness).

These factors are important in determining the selection of cotton for a particu-

lar purpose but are not as important as `staple length".

- 5 -

Table 3COTTON1: SPOT PRICE PER POUND OF SPECIFIED GROWFTHS, LIVERPOOL

(U.S. cents per pound)

Egyptian IndianPeriod American Brazilian Peruvian Salellaridis Oomra #1

Middling Sao Paulo Tanguis P..G,P. Fi.ne

1906/09 av. 13.02 .. 14.55 19.79 10.651910/14 av. 13.81 ,. 16.36 22.60 11.891915/19 av. 33.04 , 41.07 57.90 29.101920/24 av. 25.74 24.95 - 31.75 42.16 19.991925/29 av. 20.17 19.05 24.45 35.46 16.131930/34 av. 10.88 10.72 13.05 15.02 6.471935/38, av. 12.15 11.85 15.13 19.41(a) 9.19

(a) 1935/37 average.

(premium or discount over American - cents per pound)

1906/o9 av. ,, ; 1-53 , 6.77 - 3.371910/14 av. .- 1 3.55 1 8.79 - 1.921915/19 av. .. # 8.03 I 24.86 _ 3.941920/24 av. - 0.79 $ 6.01 o 16.42 -5.751925/29 av. _ 1.12 , 4.28 1 15.29 - 4.041930/34 av. 0.16 $ 2.17 3.14 - 4.411935/38 av. - 0,30 $ 2.98 , 6 . 6 0(a) 2.96

(a) 1935/37 average.

(percent of American)

1906/09 av. .. 110.2 151.9 81.81910/14 av. .. 118.3 163.8 86.o1915/19 av. . 124.2 175.2 88.01920/24 av. 97.0 123.2 163,8 77.?1925/29 av. 94.6 121.4 176,0 80.21930/34 av. 98.6 120.0 138.1 59.51935/38 av. 97.5 124.8 151.5 75.6

III. THE MARKET FOR COTTON

As is shown by Table 4 and Chart, world mill consumption of raw cotton

from 1904 to date, offset somewhat for periods of war and depression, has shotim ar

increasing upward trend at a similar rate to the growth in world population,

-6_

Table 411OPFJD.POPULA-TION AND MIILL CONTSUiPTION OF COTTON

* P-o2p0 ation _ Itlill ConsumptionYear Millions Index Period. Million Index

_____ ____ _ (1907 = .1o0) 3aBlea (1905/09 = 100)

1907 3587 100 1905/09 av. 18.5 1001912 1637 103 1910/14 av. 20.6 1111917 1716 los 1915/19 av. 19.7 1071922 1866 118 1920/24 av. 20.0 10o1927 1946 123 1925/29 av. 25.2 136

1932 2043 129 1930/34 av. 24.2 1311937 2092 132 1935/39 av. 28.5 1541942 2176 137 1940/44 av. 24.0 1301946 2251 143 1946 26.o 141

Cotton fiber constitutes the chief source of textile raw material; wool,

rayon and silk are tlae other important textile fibers, although jute, flax, hemp,

abaca, sisal, heneouen, ramie, and a few other 'minor fibers including naner and

synthetics, compete with cotton as sources of supply, chiefly in the industrial

field, for such uses as bagging, ropes and twine, etc.

Table 5WORLD PRCODUCTION\T OF FiOUR TEXTILE FI3ERS

Average Cotton Ral,on Wvool Silk Total(million p;ounds)

1910/134 10,306 20 2,918 55 13,2991915/19 9,502 24 2,810 58 12,3941920/24 9,732 80 3,050 85 12,94?1925/29 12,793 299 2,143 119 15,3541930/34 12,364 603 2,181 124 15,2721935/39 14,820 1,684 2,297 121 18,9221940/44 12,970 2,529 2,488 80 18.067

(percent)1910/14 78 - 22 - 1001915/19 77 - 23 - 1001920/24 75 0.5 24 0.5 1001925/29 83 2 14 1 1001930/34 81 4 14 1 1001935/39 78 9 12 1 1001940/44 72 14 14 - loo

Index (1910/14 = 100)1910/14 100 100 100 100 1001915/19 92 120 96 105 931920/24 94 400 105 155 971925/29 124 1,495 73 216 1151930/34 119 3,015 75 226 1151935/39 143 8,420 79 220 1421940/44 125 12.645 8- 145 136

- 7 -

From Table 5 it is aponarent that cotton has represented from 72 to 83 percent of

the worldts textile fiber supply. The rapid increase in rayon output, however,

particulnrly since 1935, is reducing the promortion of cotton to the totel.

Data available for the United Statest market (including production for

exp,ort) are illustrative of cotton's position in major end use markets in relation

to other fibers.

Table 6ESTIMATELD COSWSUIPTIOIT OF COTTON MI-WD OT-HER iMAATERIALS

BY MAJOR UiNITFD STATESI' mm-USE MARUETS, 1939(thousand cotton bale equivalents - data rounded)

X, j -,. , *, .AZ'llEnd Use Market Total Cotton Rayo. lWool Silk Jute Paper Other

AMnrelMen's, Youths',Boys' 2,108 1,653 46(a) 345(c) 1 - 2 61

Women's, Misses',Juniorst 1,808 791 409(b) 341(f) 235(i) - 10 22

Children's,Infants' 351 288 16 46 1 - 1 _

TOTAJ. 4.267 2.731 470 732 237 - 13 83-Household Uses 2,761 1,990 71(c) 329(g) 1 203(k) 60(n) 10?Industrial Uses 6,638 2,848 46(d) 123(h) 2 669(m) 592(p) 2,358

GRAND TOTAL 13,666 7,569 586 ' 1,184 241 872 665 2,54?(a) Chiefly hosiery, suits and trousers.(b) Chiefly dresses, blouses, hosiery, underwear, najamas, sportswear.(c) Chiefly draperies, upholstery, blankets.(d) Tire cord and luggage.(e) Chiefly suits, coats and jacklets, overcoats, sweaters, trousers, gloves,

hosiery, underwear.(f) Chiefly coats and jackets, sportswear, sweaters.(g) Rugs, carnets and mats, blankets, drapery and upholstery.(h) Automobile upholstery and lining.(i) Hosiery and underwear.(k) Rugs and carpets.(m) Automobile upholstery and lining, bags, cordage and twine.(n) -Table cloths and napkins, towels and towelling, window shades.(p) Bags, medical supplies, nlastic laminates.,

Tables 6 and 7 reveal that in the United States fibers competing with cotton are

entrenched in certain fairly well-defined end-use markets, Paper is chiefly com-

petitive in towiels, nankins, bags, and medical supplies; jute, in rugs and caroets,

cordage and twine, bags, and automobile upholstery and lining; silk, in woments

- 8 -

Table 7COMIRTITIOi'T FROM OTHFR FIBERS IN THIRTY PRINCIPAL COTTON

GOODSUSES, UJNITED STATES,. 139

CottontUse Consumed Competition

(thousand bales)

10 leading a-pnarel uses

1. Shirts 464 Moderate: rayons, espec. sports5me2. Piece goods 332 Considerable: rayons, synthetics3. Trousers 285 Considerable: rayons, blends4. men's overalls 232 NTegligible5. iNien's underwear 210 Moderate: rayons6. Wo,nen's dresses 175 Considerable: rayons, synthetics7. Women's underwear 104 Considerable: rayons, synthetics8. Men s hosiery 98 Considerable: rayons, wools9. Men's nightwear 75 Moderate: rayons

10. ifen's work gloves 62 Negligible

10 leading household uses

1. Sheets 433 Fegligible2. Towels 303 Considerable: anaper3. Blankets 180 Considerable: wool, rayon, blends4. Drapery, upholstery 154 Considerable: rayon, synthetics,

glass, fiber, and jute5. Pugs, carpets 149 ovonsiderable: flax, jute, paper,

others6. Curtains 130 Considerable: rayons, synthetics?. Bedspreads 94 Moderate: rayons8. Pillowcases 75 Negligible9. Bed tickings 73 Negligible

10. Oil cloths 63 Negligible

10 leadina industrial uses

1. Automobiles 707 Considerable: high tenacity,rayon, synthetics

2. Bags 473 Considerable: burlap, paper3. Cordage, twine 248 Considerable: jute, hemp, sisal,

synthetics4. Laundry 131 Negligible5. Shoes 128 Negligible6. Thread 120 Considerable: flax,.silk, synthetinm7. Electric insulation 83 Coisl.derable: glass fiber, silk8. Artificial leather 63 Nlegligible9. Belts (machinery) 61 Considerable: leather10. Hose 40 Considerable: flax

hosiery and underwear; wool, in suits, sweaters and other outer garments, ru s,

carpets and mats; and rayon, in men's hosiery and women's dresses, blouses, under-

wear, and nightwear.. It is apparent, therefore, that in most fields cotton is

faced with a considerable array of competition on the United Statesl market. The

30 items listed in Table 7 consumed, in 1939, 5.7 million bales of cotton or

78 percent of the total market. Of this last figure, 22 percent of the uses wras

faced with negligible competition, 15 percent, with moderate and 63 percent, with

considerable competition; thus, only 22 percent of the cotton goods market i

could be regarded as definitely safe from comipetitive inroads,

The coarse fibers (jute, hemp, sisal, etc.), whose nature limits them to

such uses as bags, bagging, cordage, twine, etc., represent the least competition,

not because they compete in unimroortant marlkets, but because their future com-

petitive expansion possibilities are not very great. Paper, on the other hand.,

represents a more formidable competitor in that it is rapidly exvcanding into new

markets through new nroducts each year.

Competition is evident both on a price and quality basis; thus, rayon has

recently taken over the automobile tire-cord market on a quality basis, whereas,

in the bag markcet, the relative nrice of paper, jute, etc., is the all-important

item. The prices of fibers over a number of years are given below:

Table 8AVRAGE SPOT PRICES OF COTTON, WOOL, SILK, MID RAYON

IN THE NITITED STATES(dollars per pound)

Rayon Rayon StanlePeriod Raw Scoured Raw -Filament Fiber

Cotton Raw Wool Silk Yarn (viscose)

1915/19 .265 1.35 6.35 3.64*1920/24 .256 1.36 7.64 3.001925/29 .193 1.15 5.64 1.621930/34 .097 .67 2.05 .73 .481935/39 .109 .84 1.93 .56 .281940/44 .170 1.12 .. .54 .251945 .226 1.18 .. .55 .251946 .306 1.03 6.79(a) .56 .251947 0351 1.22 4.55 .67. .32.(a) July/December only.

- 10 -

The extent of rayon substitution for cotton, its rapid increase in pro-

duction over recent years and its price relative to cotton, mark it as the most

important of competitors. The price of rayon staple fiber, which is most directly

competitive with cotton is now below cotton prices, particularly when it is con-

sidered that the 1)rice represents absolutely clean fiber, whereas the price of

cotton is on a gross weight basis and includes a 15 percent loss on the bagF_, g

ties and waste in cleaning. Moreover, rayon being a manufactured product can be

cut to whatever staple length is desired without additional cost (wrhich is not

true of cotton where extra staple lengths command high premiums). From the stand-

point of quality, rayon has undergone a complete transformation. "A notoriously

poor quality fiber a few years ago, rayon is now cotton's chief competitor on

quality marlets".

This challenge of rayon is not entirely confined to the United Statest

market; in fact, in Germany and Italy it was in the process of replacing cotton

prior to Wlorld War II.

Table 9WORID PRODUCTION OF RAYON (FIBER AND FILAMENT YARN)

(million pounds)

CottonPeriod USA Ger- Italy Great France Other Japan All World Equiv.

man; Britain Eurone Other Total (OOC bales)

1910 .. , - .. 18 411915 4 2 .. 4 1 - 7(a) 19 441920/24 av. 24 12 8 14 7 .. 1 14 (a) 80 1881925/29 av. 82 40 50 40 26 45 12 4 299 7031930/34 av. 168 73 81 69 54 67 83 8 603 14181935/39 av. 312 359 238 147 71 105 427 25 1684 39311940/44 av. 613 797 281 141 94 253 303 47 2529 59551945 792 190 7 144 49 150 28 56 1416 33301946 854 108 95 183 68 237 30 63 1638 383501947 975 .. ,. 203 125 .. 35 662(b) 2000 4700

(a) Includes "Other Eurone".(b) Includes countries for which individual date not available.

Production of rayon in Germany, Japan and Italy on a cotton equivalent basis ex,

panded from 19 million bales in 1935 to 4.5 million in 1939.

It is yet too early to say what the precise effect of rayon (and. other

synthetic fibers, e.g. nylon) will have on the cotton market, but it is bouTd to

be considerable, particularly when it is considered that the price is now belowr

that of cotton in the United States and rmay fall still further in the long run.

IV. WORLD CONSUKPTIO0\ AiD TRADE

Table A in the Appendix and. Table 10 below show world mill consumption

from 1911 to date by country and area. With the exception of war, postwar anid

depression years, world consumotion has showm an increasing trend of about 2.2

million bales each decade. During the period covered, however, the geographical

pattern of consumption has shown a marked clhange.

Table 10WOBID MILL COiTSUIPTIONT OF RAW COTTON

BY MAJOR CONStUI4ING COUi,TT2IES A;0 AREAS

(thousand bales) (percent)1911/ 1920/ 1925/ 1930/ 1935/ 1911/ 1920/ 1925/ 1930/ 1935/

Colintry 1913 1924 1929 1934 1939 ' 1913 1924 1929 1934 1939

United States 5306 5869 6735 5465 6938 23.8 28.6 27.1 22.6 24.1United Kingdom 4456 2886 3024 2447 2836 1 20.0 14.1 12.2 10.1 9.8Cont. Europe 6006 4590 5867 5462 5569 t 26.9 22.4 23.6 22.6 19.3USSR 2001 727 1741 1844 3305(a)l 9.0 3.6 7.0 7.6 11.4Orient 3137(b) -5357 6475 7913 8554 1 )20.3 26.2 26.1 32.6 29.6Other 1392(c) 1050 1009 1085 1674 ' ) 5.1 4.0 L! 5.8

TOTAL 22298 20479 24851'24216 28876 ' 100.0 100.0 100.0 100.0 1020,(a) Four_year average.(b) Excludes China and M4anchuria.(c) Includes China and Manchuria,

Consumption in the United Kingdom has been halved; Continental Europe has suffered

a much smaller shrinkage, largely in Germany (which has been more than offset by

increased usage of rayon). The United States and the USSR have largely retained

their pre-World War I proportionate nosition. The Orient, particularly Japan,

has enjoyed the largest increases both relatively and absolutely and can thus be

said to have fallen heir to the chief proportion of the shrinikage in the United

Kingdom, Germany and a few other European countries. This has primarily occurred

in the manufacture of the cheaper types of cotton textiles where labor skills are

at a minimum.

- 12 -

Data on cotton exports by countries representing a large proportion of

world trade is given in Table C in the Appendix and Table 11 below.

Table 11 -

AVERAGE WORLD COTTON EXPORTS BY CROP YEARS(percent of total)

ExportingCountry 1910/14 1915/19 1920/24 1925/29 1930/34 1935/39 1940/44

United States 69.9 61.6 56.8 60.1 58.5 43.2 27.2India 15.6 18.8 24.6 20.6 18.7 20.4 12.9Egypt 11.2 12.0 11.4 10.4 11.9 13.5 14.9Brazil 0.8 0.3 0.8 0.8 1.8 8.6 14.3Peru 0.7 1.2 1.6 1.5 2.0 2.6 3.9Other 1.8 6.1 4.8 _6.6 7,1 11.7 26.8

TOTAL 100.0 100.0 100.0 100.0 100.0 100.0 100.0

A comparison with the tables on cotton production reveals that two large

cotton producers are relatively small exporters, namely; China and the USSR, the

bulk of their production being consumed domestically.

As the relative position of the United States declined, different competi-

tors improved their position at different times. During the 1920's, India and a

number of minor producers--including the Sudan, Uganda, the Belgian Congo--e_pande

their exports. During the 1930's, this role was enjoyed by Brazil, Peru, Egypt,

Argentina, Uganda, and the Belgian Congo.

Table D in the Appendix gr,ives exports from the major exporting countries

to the chief importing countries over a 30-year period. It shows that the decline

in United States' export trade during 1935/39 "as confined largely.to Europe,-the

United Kingdom, Germany, France, and Italy, nrimarily; exnorts to Japan were main-

tained. The Indian market largely centered on Japan, but a strong position in

Europe, particularly in the United Kingdom, was maintained, though trade with

Germany and. Italy fell off. The Egyptian market was centered on the United

Kingdom and other Euronean countries where fine quality cottons were required;

though the British market weakened, this was more than offset in other European

markets and her over-all position was improved somewhat. Brazil was the large

- 13 -

gainer in exv,ort trade during 1935/39 in all countries, particularly Europe and

eslnecially the United Kingfom and Germany; there is not much doubt that the

Bra.zilian gains were made almost entirely at the expense of the United States,

as the-qualities of their cottons are directly competitive. The Peruvian market

was lrimarily in the United Xingdom wihere her position was largely maintained;

considerable geins were made on the German market in 1935/39, though exnorts to

the United States shrank. The importance of minor producing countries has been

steadily increasing.

Data on cotton imports by countries representing most of world trade is

given in Table B in the Appendix and Table 12 below:

Table 12AVERA.G. COTTONT IMPORTS BY CALEiDAR YERS MOR PRINCIPAL COUNTTRIES

(percent of total)

ImportingCountry 1909/13 1920/23 1925|29, __ 1930/34 1932539

United Kingdom 30.2 26.4 21.6 18.7 22.2Germany 16.4 9.7 10.2 11.0 9.3France lo.4 10.8 11.0 9.9 9.4Italy 6.2 7.5 7.2 6.7 5.0Other Rurope 23.1 12.2 19.3 17.0 17.4

Total Eurone 86.3 66.6 69.3 63.3 63.3Japan 10.2 22.6 20.8 24.8 26.7China *3 3.9 4i3 6.6 2.8India .4 '5 1.1 2.2 3.4Cana da 1.1 2.1 1.9 1.8 2.4United States 1.7 4.3 2.6 1.3 1.4

TOTAL(a) 100.0 100.0 100.0 100.0 100.0(a) Excludes minor non-Euronean countries.

Prior to World W-1ar I, Europe plus Japan constituted almost the whole world import

market for raw cotton. This is also true prior to World War II, but the pattern

changed: Japan more than doubled her rela.tive pronortion of the market, whilst

the position of Europe, particularly the United Kingdom and Germany, suffered a

decline both relatively and absolutely. The absolute quantity of trade eccluding

periods of post-war recovery and depression has remained fairly stationary with

a slight upward movement. An analysis of the trade patterns by individual

- 14 -

importing countries given in Table F in the Appendix shows the same trend as

described above in the analysis by exnorters. The advance in the Japanese te:;tile

industry benefited India on account of the proximity of the market and the type

and cheapness of the cotton relative to the bulk of Japanese output of chealp cotton

goods. The largest portion of the increased output of Brazil wJent into ?.uxro7e as

a replacement of American cotton. Though the United States increased its markletings

of cotton in Japan, this did not offset the decrease in Europe. Finally, exoorts

from the smaller producing couwtries increased, particularly to Europe. The united

Kingdom absorbed the expanded output of its colonies, particularly the Sudan and

British East Africa (Uganda and KIenya esnecially), thoueh in the late 1930's India

became the important market for the latter area.

V. DEVELOPMENTS IN WORLD COTTON PRODUCTION1

Probably the most interesting develorment in world cotton production has

been the rise and relative decline in the position of the United States as the

world's leading cotton producer--a position she still maintains?

Table 13WORLD COTTON PRODUCTION

Includes Non-Commercial Production(thousand bales)

United Other Countries WorldPeriod States Excl. China Incl. China Exci. China Incl,. China

1891/94 av. 8,282 3,618 .. 11,9001895/99 av. 9,444 4,176 .. 13,6201900/04 av. 10,710 5,150 .. 15,8601905/09 av. 11,640 6,140 o. 17,7801910/14 av, 14,254 7,306 .. 21,5601915/19 av. 11,467 6,612 ,. 18,0791920/24 av. 10,980 6,974 9,380 17,954 20,3601925/29 av. 15,268 9,330 11,882 24,598 27,1501930/34 av. 13,343 9,721 12,451 23,o64 25,7941935/39 av. 13,149 15,714 18,569 28,863 31,7181940/44 av. 11,957 .. 15,082 27,0391945/46 9,015 10,510 12,330 19,525 21,3451946/47 8,640 10,930 12,855 19,570 21,4951947/48 11,508 12,462 14,612 23,970 26,120

- 15 -

Since the advent of cotton as a raw material on a large scale to the Western world

in the 18th century, the United States has been the nrincipal supplier and, with

the exception of short war T)eriods and periods of depression, cotton production

exnanded up to 1926; since then a marked downward movement has occurred. From at

least the beginning oI this century, however, expansion in production outside the

United States has been proceeding at a greater rate, as the nroportion of United

States' to world poroduction has been falling.

Table 14PROPORTION OF UIThITbD STAT.Ss PRODUCTION TO TOTAL

11ORLD COTTON PRODUCTION(percent)

Excluding Excluding InclueingPeriod China Period China China

1891/94 av. 70 1920/24 av. 61 531895/99 av. 70 1925/29 av. 62 56

1900/04 av. 68 1930/34 av. 58 521905/09 av. 66 1935/39 av. 46 411910/14 av. 66 1940/44 av. .. 441915/19 alr. 63 1945/46 46 42

1946147 44 401947/48 48 44

This decline in United States'nroduction, therefore, is a phenomenon of the

period beginning with W;[orld W4ar I and extending to the present.

The first n,hase of this decline which terminated in the middle 1920ts was

entirely due to the depredations of the boll weavil which reduced yields and in-

creased costs. The reduction occurred at a time when other producers were unable

to expand p)roduction sufficiently to bridge the gap and world mill consumption on

the average exceeded commercial production over a ten-year period. In consequence,

prices on the average remained relatively high. These high prices polus the evolu-

tion of means to combat the boll weavil in the United States resulted in an e:-

pansion of acreage and production, both in the United States and elsewhere during

the last half of the 1920 1 s. The world commercial position during this pneriod in

relation to prices is shown in Table 15 below.

Table 15WORLD COTTON COEvE=RCIAL STOCKS, PRODUCTION, CONSUMPTION

AUD UNITED STATESI PRICES

Mill Diff. be- Price ofPeriod Stocks Pro- Total Con- tween pro- 7/811 midd_-duction Supply sumption duction & ling (cents

(million balee)1905/09 av. .. 18.2 .. 18.5 0 0.3 11.791910/14 av . *-. t'3 .. 20.6 , 0.7 12.021915/19 2V. . 18.8 .. 19.7 - 0.9 25.561920/24 av. 10.3 19.5 29.8 20.0 - 0.5 22.991925/29 av. 10.5 26.o 36.5 25.2 , 0.8 17.651930/34 av. 15.9 24.9 40.8 24.2 , 0.7 9.161935/39 av. 17.3 29.7 47.0 28.5 $ 1.2 10.301940/44 av. 22.2 25.1 47.3 24.0 $ 1.1 17.621945/46 26.5 20.3 46.8 23.5 - 3.2 24.381946/47 23.1 21.0 44.1 26.0 - 5.0 33.331947/48 17.9 24.4 42.3 32.09(a)

(a) Nine-month average.

A second neriod of declining United States' production was ushered in by theGreat Depression following 1929. Cotton prices declined and remained low for over

a decade. United Statest acreage dropped persistently until, in 1945, it was at

the level of 1892. Production did not fall off to the same extent as yields in-

creased with the withdrawal of low-yielding marginal land, the increased use of

fertilizer and other improvements. This second period contains several interesting

developments. A fundamental shift in the agriculture of the South had apparently

begun.

Cotton acreage, besides declining'in toto, shifted westward to the Mississippi

and the plains area of Texas, Oklahoma and Arizona where newer and cheaper methods

of cultivation could be used: the Old South moved more towards a diversified agri-

culture, particularly into livestock, Secondly, the Federal Government intervened

in the nroduction and marketing !rocess in an endeavor to support prices. Un-

doubtedly, this helped. to encourage the shift outlined above; it also helped in

maintaining world cotton prices at levels which encouraged expansion abroad, a

decline in United States' trade and an accumulation of stocks.

- 17 -

Table 16COMERCIAL STOCKS AITD COISUMPTION OF AMEICAI1 COTTONi

(million bales)

0pening Stocks Mill ConsurotionPeriod Held in' the Held In the

TTnited Staten Elsehwere TTnitpti St-xt0. 71 ab#rh

1920/24 av. 2.1 3.4 5.6 6.2l125/2 9 av. 2.6 2.7 6.4 8.31930/34 av. 7.2 3.0 5.3 7,31935/39 av. 8.3 1.7 6.8 5.31940/44 av. 10.8 1.1 10.2 1.51945/46 11.1 1.1 9.0 2. 11946/47 7.1 2.7 ,9.7 3.31947/48 2,4 2.9

For the first time in any continuous period, the United States' domestic market

became the premier market for its own cotton. During VWorld WJar II, a continuing

decline in acreage occurred through a shift in farm labor into the armed forces

and into better paying industrial occupations.

Although the story of the ezpansion in cotton production outside the United

States begins in the nineteenth century, its effective challenge to United States$

supremacy began after World lJar I. Total non-United States' production, excluding

China and Mianchuria, fluctuated between 6 and 7 million bales from 1905/09 to

1920/24; in 1935/39, it had exceeded 15 million bales. World production, includ-

ing non-commercial supplies, is given in the Appendix, Table B.

As has been outlined above, production was expanded during the 1920's

chiefly under the encouragement of high prices caused by low United StatesO pro-

duction until 1925, and by an active world demand thereafter.

- 18 -

Table 17CHAIGES IN WORLD COTTON PRODUCTION

Change in thousand bales1920/24 1925/29 1930/34 1935/39 1940o/44over over over over over

1909/13 1920/24 1925/29 1930/34 3.935/29

United States - 2053 L 4288 - 1925 194 - 1192Five Otiher Major

Producers(b) $ 280 $ 1818 $ 344 , 4832 - 3209Ten MinorProducers (b) $ 204 $ 472 $ 217 $ 950 $ 60

All OtUr _ _, 215 , 8 A 336 - 338WORILD T0TA:..(1) Excl. U.S.A. $ 702 $ 2505 L 569 A 6118 - 3487(2) Inel. U.S.A. - l351(a) A 6793 _ 1356 A 5924 - 4679

(a) Including 1916/18 data for China,(b) For individual countries see more complete data. in Apnendix.

Du-ring 1920/24, significant gains in produption occurred in Ind.ia, Brazil, China,

Peru, Korea, and Uganda, wzhich were considerably offset, however, by reductions

in the USSR, due to civil strife and in Egypt, due to declining yields. M'lore sig-

nificant gains were made during the period 1925/29 in all countries except Brazil

where a small decline occurred due to favorable coffee prices. Iarge increases

occurred in the USSR, under the Five"Year Plan; in India, where ctto-n priowes were

relatively feavorable compared wlith comneting crons (as was the case in most other

countries); and in Egypt, where yields recovered.- The period 1930/34 showred the

smallest net gains, due to low cotton prices and. restricted markets during the de-

rPression. In India, cotton had declined in price relative to other commodities

and a considerable reduction in production occurred; the same was true of Egypt

where cotton competes with grain; in Brazil, production increased at the expense of

coffee due to relatively lower coffee prices; the USSR continued its expansion of

acreage and production under a planned economy. The period. 1935/39 v;itnessed the

largest increase in output, particularly in the USSR, India,.Brazil, and Egypt,

amongst the major nrotucers, and in Iran, Turkey, ]siexico, the Belgian Congo, Peru,

the Sudan, and Argentina, amongst the minor producers, though all increased their

- 19 -

production. With the exception of the USSR, the chief reason for this was not so

much the increase in nrice of cotton compared with 1930/34 as its relati7e favor-

ableness to competing nroducts for land. This is most evident in the case of

3razil where coffee prices were exceedingly low. However, other factors were

present of wrhich the most important was state aid and encouragement to the cotton

producer, This aspect is seen in the case of the African colonies, Uganda, the

Sudan, the Belgian Congo, French Equatorial Africa where nroduction has been con-

sistently advancing up to World VWar II as integral parts of colonial e:mansion

progrr'ms.

During the war years,.:a reduction in output occurred a.s a direct result of

war devastation, in the USSR and China; as a result of the loss of markets, in the

case of the African colonial areas; and as a result of the necessity of increasing

the production of food, in India, Egypt and other areas.

VI. PROBABLE FUTURE PATTERN OF COTTOIT PRODUCTIO1N, COiJSUI4PTION AM TRIDE

By way of summary of the above discussion, world cotton production and. con-

sumntion have shown an advancing trend, marred by periods of war and denression,

somewhat similar to the increase in world population. The nosition of the United

States, the world's larger nrod.ucer, however, has declined from roughly 60 1nercent

of the total at the beginning of the century to 40 percent nrior to World War 1.

Trade between the two World Wars, excluding the 1920/24 postwar neriod, has

fluctuated around the 1909/13 level of 13.8 million bales. Thus, trade has remained

stationary whilst production, consumntion and stocks have increased. A larger pro,-

nortion of raw cotton has been manufactured in countries in which it was produced.

The pattern of world trade, however, has shifted considerably. The U-nited

States' share in world export markets has declined from a ore-World WIar I average of

70 percent to 43 percent in 1935/39, Other major producers, India, Brazil, Egypt,

Pera, and a host of minor producers have expanded their exnorts to fill the gap.

- 20 -

On the import side of trade, Europe-particularly the United King-don and

Germany--have become of relatively less import,nce as markets whilst still absorbing

about two-thirds of total world imports. Japan, on the other hand, has increased

her share of world imports from roughly 10 rercent prior to World 'ar I to 27 per-

cent on the average for the reriod 1935/39. China, India and Canada have made

moderate absolute but substantial relative gains as imoorters.

Federal Government intervention in the United Statesl cotton market through

price supporting and acreage restriction programs had an influence in restricting

acreage, output and trade. But the cost element relative to competing products wias

influential also: at prevailing market prices during the 1930's relative to the

prices of competing farm products, cotton production and acreage was reduced in the

United States, whilst producers in competing countries were willing to exoand out-

put. State intervention outside the United States, however, was active in encourag-

ing production in various ways and thus accounted for some of the increase which

took place. Apart from these factors, the shortage of United States, foreign ex-

change worked particularly to the disadvantage of cotton especially in those coun-

tries which exercised exchange rationing controls and barter-agreements as tne

exchange was expended on those commodities which could not readily be obtained else-

where. Increased production of rayon particularly in Germany, Italy and Janan also

contributed to an absolute decrease in imports of cotton. From the trade roint of

view, it was estimated in 1936 for Japan "in each dollar's worth of cotton goods

exported the cost of imported raw materials was about 43 cents, whereas for each

dollar's worth of rayon textiles the cost in foreign exchange was only about 10

cents."

During World War II, the production and marketing of cotton once more was

disrupted. Isolation from markets, food and la.bor slhortages resulted in a reduction

of cotton production. Similarly, lack of labor and raw materials and, in some coun-

tries, destruction of textile equipment reduced cotton consumption; stocks of raw

cotton increased to record proportions.

- 21 -

Following the termination of the war, demand expanded faster than production

and stocks were drawn upon heavily to fill the gap; prices rose. By the summer of

1947, however, it was becoming apparent that for financial reasons the rate of ex-

pansion was slowing up; this may be offset by the passage of ERP. Meanwhile, pro-

duction has started to increase, though the relationship of cotton to food prices

is not favorable to cotton at present; unless production revives significantly in

the next two years stocks will be approaching a minimum. In this respect, the

cotton situation is anproaching the position,of wheat two years ago--surplus stocks

which had accumulated prior to and during the war will have been consumed.

On the demand side, a commercial consumption of 28 million bales is below

world requirements in view of the increase in nopulation which has taken place dur-

ing the past ten years, the tattered condition of the worldls wardrobe and the

present relatively low level of rayon production in Europe and Japan.

The conclusion which anpears to emerge from the above analysis over the

short-run would appear to be, in the absence of depression and financial stringen*

cies, that consumption of raw cotton would tend to remain high; that until the

world. food situation becomes easier and prices subside, and agricultural labor

supplies become more plentiful, an over-all surplus production position is unlikely,

though the gap between production and consumption will narrow or be entirely

eliminated and prices will decline. This would. not nreclude stocks increasing in

any one producing country, i.e., the United States on account of trade restrictions.

With regard to the long-run rnrospects, there is no doubt that the world de-

mand for textiles in general will increase during periods of good business condi-

tions. Wihat this will mean in terms of an increase in cotton consumption, however,

is nroblematical due to the threat of increasing competition from rayon and other

substitutes.

In 1947, the w!orld production of rayon was equivalent to 4.7 million bales

of cotton (peak prod.uction was reached in 1941 with an equivalent of 6.7 million

- 22 -

bales) at a time when -production in Germany, Italy and Japan was at a fraction of

Drewar and wartime peaks. World caracity in 1948 is estimated by the ".Ra7yon

Organon't at 7.8 million bales. Should the above-mentioned three countries recover

their nroduction cspacity and other countries continue to expand output, a poten-

tial production of rayon equivalent to 10 million bales of cotton by 1950 would not

be too high; this would be greater than one-third of -prewar cotton mill consumption.

What effect would such an outnut have on the demand. for cotton?

In this connection, some interesting estimates a.s to cotton consumption in

the United States in 1950 compared w;ith 1939 were given in the hearings during

1947 before the Subcommittee on Cotton, House of Representatives. Under the as-

sumntions of moderate prosperity and relative Prices between cotton and competing

commodities as existed at the beginning of 1946 (cotton 25 cents i9er pound), the

estimated consumption of cotton and competing materials was zas follows:

19 50

Cotton (thousand bales) 7569 7684Percent of Total 55.4 45.4

Competing Materials(thousand bale equiv.) 6096 9254

Percent of Total 44.6 54.6

On the basis of a varying price for cptton with the prices of compDeting pro4tacts

remaining fixed as above, the consumption of cotton in 1950 is esti.mated:

At 12 cents per pound - 9559 (thousand bales)At 25 cents ner pound - 7684 (thousand bales)At 40 cents per pound - 5186 (thiousand bales)

Thus, an increasing consumption of cotton in the United States under conditions of

moderate prosperity would depend upon the relative price of cotton being much lower

than competing products, particularly rayon.

There is no doubt that the advent of rayon and other substitutes vill slow

down the rate of expansion in world cotton demand unless costs of prodcuction of

cotton are lowered. As it is unlikely that wages and the rent of la.nd can be re-

duced substantially owing to competitive uses, this would necessitate the

- 23 -

introduction of more efficient methods of production. Already, a start in this

direction is being made in the United States through the evolution of mechanized

means of pl2.nting, cultivating and picking. The technique is etill in the early

stages of development. The reduction in labor costs in the United States clpaimed

by the newPr methods are revea.ling.

"Under the man-mule system in the Miississippi Delta, a total of 141.1hours of labor are needed to procluce an acre of cotton. However, whentwo-row tractor equipment and mechanical pickers are used, the man-hourrequirement drops to 43.7 and when full four-row equipment and mechan-ical pickers are used, the man-hours are further lowered to 27.6. Inthe High Plains area of Texas and Oklahoma, mechanization has advancedto such a state that the man-mule svstem is almost completely antiquated.Currently, thle man hours needed for production of an acre of cotton,using two,-row equinm.ent and hand-snarping, total 21.9. Use of four-rowtractor equinment and machine strippers reduces the hours of labor tothe almost incredible low of 6.9 per acre."

Mechanization, however, particularly in backw;ard and primitive areas should

not be conceived in terms of ca.terpillar tractors, mechanical cotton pickers and -

flame cultivators. These ex-ensive items of capital equipment are likely to be

restricted to areais of rnredominant commercial farming on a large-scale basis where

the land is suitable and canital available. Mechpnization is a matter of deegree

and in most cotton areas of the world any reduction in costs is likely, on a

nractical basis, to be achieved by a slow gradlual initroeuction of better machinery

and equipment and an imnrovement in techniques of cotton -;rowing over the pr-mitive

methods now in use. As has been demonstrated. in the United States in recent years,

a considerable increase in yields can be obtained through the a-oplication of larger

amounts of fertilizer.

It is evident, with the rise of substitutes--particularly rayon--as relative.

ly new factors in the textile situation, that the future of cotton is somewhat in

doubt.. The situation is still too fluid to allow an accurate appraisal as to what

can be expected in the future, though it is reasonable to exnect a long-run increase

in world demand. Cotton possesses a number of characteristics wrhich have not yet

been duplicated by substitutes; synthetics are likely to makce their greatest gains

during the early reriods of develoioment and then fit into a more stable relation-

shipn with the established fibers. Moreover, in the long-run the cost situation

for cotton is likely to prove more fluid than is the case for synthetics..

Wrhiatever the outcome of this competitive situation, the pattern of wrorld

cotton production in the future is likely to undergo changes equally as significant

as those vihich have occurred during the period between the twro World Wars. The

controlling factors in this respect are likely- to be: future relative developments

in the cost structure in the cotton industry, the repercussions of the changed

structure of nostllar trade patterns, the pressure of an increasing population on

food supplies, and the availability of supplies of labor and capital in areas where

an expansion in production is rhysically feasible.

Probably the most difficult problem to analyze in this respect is the future

role of the United States as a nrodv.cer. Undoubtedly, the new techniques will have

their greatest influence in this area during the next twenty years. The ex,oansion

of fully mechanized farming in and west of the iHississippi and a more modest im-

provement in techniques in the older nrodulcing areas will most certainly lower

costs of rroduction. But will this increase the market for United Statesl cotton?

Under the most optimistic assumptions, it is unlikely that domestic cotton consump-

tion will exceed 10 million bales, which is below present levels of production.

Any increase in production, therefore., will have to come as a result of an exr)ansion

in foreign markets. The prime prerequisite for such a situation would be a reversal

of a restricted international trade pattern such as existed in the 1930's and a

relative freedom in exrchange convertibility with the dollar. Should the dollar be-

come a chronic hard currency, and this is by no means an unlikely possibility,

importing countries would hardly nermit their dollars to be used for the purchase

of American cotton, if surpl4es could be obtained elsewhere. In such a situation,

the tendency wrould be for United States' nroduction to shrink to the level of

domestic consumption.

- 25 -

In most other producing areas, there is considerable room for improvement

in yields through the adoption of better methods of cultivation, the use of ferti-

lizers, insecticides and. weed killers as well as mechanization which would provide

for significant increases in output on a stationary acreage. Sucha improvement,

however, is bound. to be slow and as thlere is a large number of non-economic factors

inresent it is likely to involve a considerable exiieniditure of funds for state aid

in such things as experiment stations, educational facilities, the dissemination

of better seed, etc., as well as the provision of various forms of credit.

In India, the chief difficulty in the way of an expansion in acreage is

the pressure of the population on the food supply which is likely to make food pro-

duction a relatively more attractive price proposition. Should imports of food.be

made available at low costs and internal agricultural facilities such as irrigation

be improved, a larger acreage could be devoted to cotton. Much could be done in

India to increase nroduction by the improvement of yields which are exceedingly low,

The expansion in cotton acreage is likely to continue in the USSR as new

irrigetion facilities in the cotton growing regions are completed. On the basis of

a rapidly growing population and the need for an increase in per capita consumption,

it is unlikely that the USSR will become a large exporter.

The situation in China is somewhat similar to that of India with regard to

food supplies. However, adequate suprlies of labor are on hand to permit an ex-

pansion in production; if an adequate transportation system could be developed,

a considerable increase in cotton acreage could be expected.

Brazil has areas of land in the south where the climate is suitable for the

production of cotton; even if only a small proportion of it were physically suitable

for cotton, a doubling of nresent acreage would likely be possible. Under present

methods of production, however, exy.ansion in acreage is limited by the existing

transportation facilities and the labor supply. The utilization of mechanized

.- 26 -

methods is one solution to this latter problem, but it is not known whether they

would prove adaptable to the hilly nature of the terrain. Increased yields, how-

ever, could most certainly be obtained throiugh better growing methods.

lack of available irrigated land is the problem restricting the extension

of cotton in Egypt; cultivation is definitely limited to the delta and valley of

the iTile and under present production conditions very little in the way of acreage

exnansion can be looked for.

Among the minor producers increasing output trends will undoubtedly proceed.

Colonial expansion will be rushed as fast as the limitation in labor supply and its

canabilities will permit. Argentina has a large area in the Chaco where production

can be expanded; the soil is fertile but there is a lack of labor and transporta-

tion facilities. The flat terrain is suited to the use of mechanized techniques.

In a number of these -oroclucing areas ¶ihere the textile industry is in a developing

stage, the market for cotton is likely to be maintained as a matter of policy irre_.

spective of the urice of comneting substitutes, particularly synthetics, which-would

have to be imported from more industrialized areas.

In view of the imponderables involved in the above discussion as to the

future of cotton, any prediction as to the probable pattern of production and trade

is subject to a wide margin of error. Granted the continued scarcity of dollar ex-

change on foreign markets, the expansion of improved production techniques elsewhere

and an exnansion in world demand for cotton, likely prospects are for a maintenance

or a further reduction in American output and an increase in production elsewhere.

There is no large area existing in the world today which has marked advantages over

other countries and where cotton could be produced by the simple expedient of moving

onto the land. In all areas, there exist problems--transportation, labor, capital,

etc.--which require solution before any considerable expansion in output can take

place; Any increase in world supplies of cotton likely to be required in the future,

therefore, will take place in a number of sources of supply as it becomes feasible

to extend the margin of extensive and intensive cultivation,

APPBfDIX

COTTON STATISTICS AfD SOURCES

The statisti6al data contained in this repwort were collected from a

number of government and trade sources. Thus, there exist certain differences

for any particular year depending on the source. Historical data prior to 1920

were tal;en largely from "The Book of the World Cotton Conference, 192101, except

for trade statistics. Material on world commercial production stocks and mill

consumnntion after 1920 came from the New Y'ork Cotton 1lxchange. Data on total

world production and trade are from the United States DeDartments of Agriculture

and Commerce. With regard to world production, a difference exists between world

commercial production and total wTorld production; the latter includes estimates

for non-commercial procucvioln in India, China and a number of other Asiatic coun-

tries where neasant production exists. Export statistics for most countries as

collected by the U.S. Department of Agriculture is on a crop year basis beginning

with August; import trade, however, is largely on a calendar year basis.

TABLE AWORLD MILL COITSUKPTION OF COTTOIT

- (thousand bales)

Country 1911/13 1920/24 1925/29 1930/?4 1935/39 1940/44 1944/45 1945/46 1946/47

United States 5306 5869 6735 5465 6938 10301 9568 9163 10025Great Britain 4456 2886 3024 2447 2836 2044 1570 1600 1737Continental Europe

Austria & Fungary 836 110 147 189 257(a) (Belgium 233 242 389 309 287(a) (Czechoslovakia (b) 348 497 335 399(c) CDenmark 25 19 21 30 36(a) (Finland 34 30 37 42 62(a) (France 1037 1038 1218 1096 1217(a) (Germany 1775 1035 1390 1243 1200(a) (Holland 84 98 175 175 247(a) ( Not availableItaly 8°2 857 989 848 661(a) (Norway & Sweden 123 88 107 123 150(a) (Poland 421 }90 272 258 297(a) (Portugal 73 84 86 75 90(a) (Spain 371 343 409 428 135(a) (Switzerland 112 108 130 109 129(a) (Other Continent n.a. n.a. n.a. 202 352(a) C

Total 6o06 4590 5867 5462 5569(d) .3599(e) 1175 2810 3801USSR 2001 727 1741 1844 3305(a) (f) 2200 1850 1865Orient

China 1448 1983 2420 1995 936 600 650 1570India 1795 1;27 1834 2206 2715 3763 3927 3700 3102Japan 1342 2082 2658 3016 3243 640 150 200 625Other .. .. 271 601 647 - 430 438 490

Total 3137 5357 6475 7913 8554 5986 5107 4988 5787Elsewhere -

Brazil 573 501 472 408 706 .843 985 1055 1014Canada 120 160 223 219 294 .403 .353 330 342Other Countries 700 389 314 458 674 1272 1246 1314 .1322

_Total 1393 1050 1009 1085 1674 2518 2584L 2699 2678WORID TOTAL 22299 20479 24851 24216 28876 24448 22204 23110 25893

(a) 1935-38 average. (b) Included in Austria, (c) 1935-37 avera,e. (d) 1935-39 average. (e) Includes USSR.(f) Included in Continental Europe.

TABLE BWORID C)TTONT FRODUCTIOiT

(thousand bales - including non-commercial production)

Total Total -World Totals % of six Ma-Period United Six TaJor Ten Minor Excluding Including jor Pro5ucers

States India USSR China Brazil gypt Proc'cers Producers Other China China of Total

1909/13 av. 13033 3583 763 *- 282 1451 ,. .. . 195521914/18 av. 12424 3591 955 2159(a) 312 1136 20577 .. .. 18844 21003 97.701920/24 av. 10980 4121 161 2406 547 1281 19496 735 129 17954 20360 95.751925/29 av. 15268 4666 1022 2552 504 1587 25599 1207 344 24598 27150 94.281930/34 av. 13343 3929 1764 2730 772 1480 24013 1424 352 23064 25794 93.111935/39 P.m 13149 5373 3430 2855 1956 1893 28656 2374 688 28863 31718 90-341940/44 av. 11957 4469 ! ' 2170 1243 24959 2430 350 . 270391945/L6 9015 3530 1700 1820 1350 1082 18497 2288 560 19525 21345 86.651946147 8640 3417 2200 1925 1300 1252 18734 .. 693 19570 21495 87.151947/48 11508 3300 2935 2150 2000 1252 23155 .. 1191 23970 26120 88.64

Ten Minor Producers

Anglo- Fr. Equa- T Ten MiinorPeriod Egyptian Belgian torial Producers

Peru Mexico Argentina Uganda Tulrkey Suadan Korea Conro Iran Africa of Total

1909/13 av. 120 202 3 20 114(b) 12 26 - .. -1914/18 av. 130 152 9 23 *- 15 55 - *1920/24 av. 198 180 39 91 49 30 104 9 34 1 3.611925/29 av. 246 253 115 131 89 126 138 26 31 2 4.441930/34 av. 298 195 191 206 112 159 145 71 33 14 5.521935/39 tav. 834 334 289 281 275 248 180 172 171 40 7.481940/44 av. *20 424 396 198 290 244 201 181 91 85 8.981945/46 329 434 285 191 301 204 163 174 92 115 10.711946/47 294 46o -01 183 271 226 90 179 641947/48 350 464 400 200 o. 90 190 80

(a) 1916/18 only.(b) 1909/10 only.

TABIE CCOTTOIT: EXPORTS FROM SPEC IF ED COUITTRIES

CROP WMaS (BEGIWNIIT AIJUUST 1) - S YEAR AVERAGE TO 1944(thousand bales)

Countries(h) 1910-14 1915-19 1920-24 1925-29 1930-34 1935-39 1940-44 1945-46 1946-47

United States 9298 5704 6277 8576 7645 5589 1378 3613 3544India 2069 1740 2721 2929 2440 2645 657 849 837Egypt 1485 1112 1263 1479 1560 1744 760 860' 1471Brazil 102 25 85 119 234 1112 727 1462 1529Peru 89 114 180 219 259 338 197 424 361Anglo-Egyptian Sudan .. 15(a) 28 123 121 252 283 280 205Argentina- - (f) 24 94 118 217 61(a)- 125 57China 242 266 217 289 187 274 162 -U.S.S.R. (b) 9(c) - 13(i) 74 58 ...Mexico (b) 239(e) 87 97 21 98 49 275 212Turkey. .. .. 52(c) 74 69 69 44 _ _Uganda 19(a) 21(a) 67 142 186 286 211 247 194Belgian Congo - - 3 24 62 147 149(a) 173 20-3Iran 34 81 99 73 * - 9Other Countries(t F). -

Total (excl. TJ.S.A.) 4006 3543 476i 5683 5429 7313 3300 4695 5078All Countries ShowJn 13304 9245 11038 14259 13Q7j 12902 4678 8308 8622.WORLD TOTAL 12951(i) 5096(i) 9286 9621

(a) Four-year average.(b) Less than 500 bales.(c) Two-year average.(d) One year only.(e) Three-year average.-(f) Small,.if any.(g) Includes U.S.S.R.(h) African countries are on calendar years, others on crop years.() 'Includes 21 countries, representing most of waorld trade.

TA3IZ DAVtRAGiL E-'-RTS OF COTTOIT FROM Sz5CIFIED COu:7.YRI.ES TO SPECIFIED IMPORTERS

(thousand, bales)

Exporting United UnitedCountries Total Jar}an Zingdom GermanLy France Italy China India States Ganada Others(a)

United States1910/14 8840 297 `509 2515 1087 501 13 (b) - 153 7651924/25-1928/29 8816 1205 ?164 2051 933 763 159 81 _ 240 12201934/35-1938/39 5296 1271 1097 579 589 430 55 89 - 261 925

India1910/14 2014 847 103 293 91 195 26 - 7 (b) 4521924/25-1928/29 2937 1455 150 194 148 319 308 _ 39 (b) 3241934/35-1938/39 2746 1372 376 163 125 133 64(c) - 55(c) (b) 458

E.rPt1910/14 1446 7 680 129 128 49 22 2 148 (b) 2811924/25-1928/29 1486 62 620 87 193 95 - 2 236 10(d) 1811934/35-1938/39 1747 149 554 176 215 115 22(d) 102(e) 51(c) 8(d) 357

Brazil1910/14 83 - 67 2 3 - - - _ _ 11

1925/29 109 - 85 4 7 - (b) (b) _ (b) 131935/39 1077 216 219 328 94 39 (b) (b) - (b) 181

Peru1910/14 83 - 63 1 5 - - 10 4 11924/28 205 - 179 9 - - 17 -

1934/38 331 24 168 95 8 3 (b) (b) 1 (b) 32

(a) Largely European countries.(b) Included in "Others"f, if any.(c) Average 1934/35-1937/38.(d) Imports into country specified.(e) 1934/37 average.

TA3LBE BCOTTOIT: IMPOMTS I'TO SPEICIFIED COTIJYTRIES

FIVE-ThA-R AVERAGE TO 1914(thousand bales)

Couantries 1909-13 1915-19 1920-23 1925-29 1930-34 1935-39 1940-44 1945-46(b) 1946/47(b)Europe:United Kingdom 4163.7 3797.1 2?26.2 3208.2 2486.7 2795.6 2178.5 1877 1818Germany 2257.6 .. 1001.0 1514.5- 1455.2 1172-.3 20.6 165 550France 1434.7 1031.1 1119.7 1638.6 1320.O 1187.7(a) 28.0 '1265 903Italy 856.5 911.6 771.5 1070.9 896.4 632.5(a) 13.2 600 1130Spain 365.7 419.8(e) 362.3 372.8 445.3 *. 17.2 332 337Czechoslovakia - - .. 555.8 392.5 392.0 .. 140 267Poland and Danzig .. .. 185.9 239.7 2613(a) 327.9 .. 265 295Belgium 627.2 .. 426.8 391.2 368.1 512.7 * 325 620USSR 847.3 .. .. 593.9 169.1(a) 114.7lUetherlands 264.5 134.3 113.6 178.8 185.1 235.2 . 200 350Sweden 89.2 158.5 80.3 103.7 117.1 161.7 11.2Switzerland 113.1 103.2 107.7 141.5 119.7 142.9Austria 866.4(f) .. .. 154.3 113.7(a) 174.9Portugal - _ 74.3 89.9 112.2 112.1Total ofCo,untries Shown 11885.9 6555.;6 6895.0 10298.2 8420.0 7962.3 23808 6055(c) 7128(c)

Ahs ia.Japan 1404.5 2067.3 2334.7 3038.1 3288.8 3354.1 1258.8 194 741China 43.2 83.6 401.4 635.9 S78.1 .346.1 ,, 1200 853British India 57.5 13.6 56.o 168.7 287.8 429.4 452.8 502 546

Total ofCountries Shown 1505.2 2164.5 2792.1 3892.7 4454.7 4129.6 1711.6 1896 2140

llorth America:United States 229.9 308.6 443.3 392.9 168.5 174.1 262.5 343 270Canada , 150.6(4) 193.7 212.5 280.6 232.6 302.3 445.6 393 413

Total'ofCountries Shown 380.5 502.3 _6 8 7401.1 . 4764 708.1 736 5683GRAID TOTAL OFCOUMTTRIES SHOWIT 137711.6 9222.4- 10342.9 .14864.4 13275.8 i2568.3 4800..5 8687 9951

(a) Four-year average. (d) '.S, exports only (running bales>(b) 'Crop years. (e) Three-year average.(c) Includes allowances for missing data. (f) Austria-Hungary..

TaZFAT-2'^AG3 IMaI-ORTS OF COTTOI' TIO S-iCCIFIED COUiThRIES FROM SIECIFID EXPCRTERS

(thousand bales)

Importing United Countries Total States Indla. zgYat Brazil Peru Chi-xna Others

Japan1909/13 1404 306 838 29 _ - 205 261924/28 3067 1256 1402 66 - _ 257 261934/37 3555 1413 1549 144 114(b) 25(b) 176 134

United KinPdom1909/13 4748 3574 155 836(a) .63 55 5 601924/28 3460 2105 172 663 51 183 (c) 2861934/38 2907 1196 400 577 236 173 (c) 325

Germany

1909/13(d) 2258 1722 306 187 2 3 15 231924/28 1706 1412 169 84 3 6 6 261934/38 1253 411 129 182 248 81 11 191

France1909/13 1435 1120 107 112 2 1 2 911924/28 1578 1004 176 195 6 l(b) (c) 1961934/38 1235 652 202 223 72 25(b) (c) 61

Italy1909/13 857 591 195 49 - - 1 211924/28 1032 715 213 85 - (c) (c) 191934/38 702 433 89 123 31(g) (c) (c) 26

(a) Includes the Sudan.(b) Erports from country specified.(c) If any, included in "Othersa.(d) Special trade.

INDICES OF WORLD MILL CONSUMPTION OF COTTONRELATED TO WORLD POPULATION

1904= 100 a180 180

160 160

140 WORLD MILL CONSUMPTION OF COTTON 1ItACTUALto\

z s / s / -~~~~~~~~--- WORLD POPULATION

120 120

100 100

801 18 01904 1910 1920 1930 1940 1946

I.B R D - Economic Dept