Embed Size (px)

Citation preview

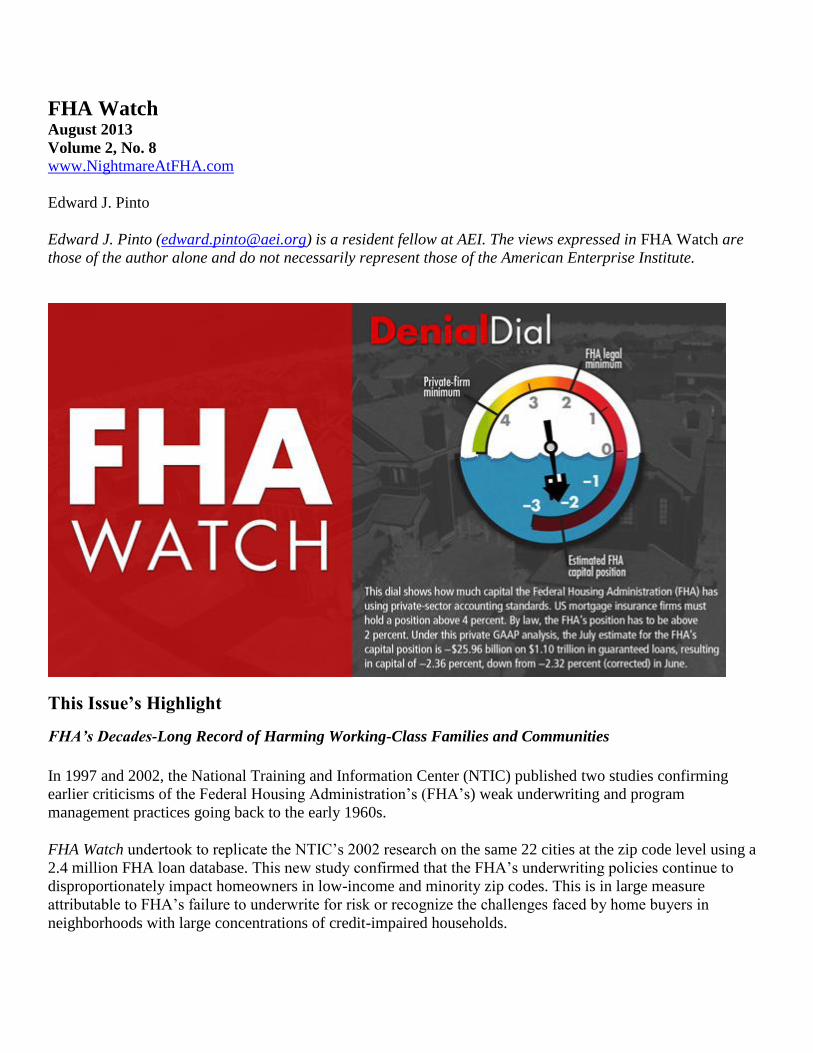

FHA Watch August 2013

Volume 2, No. 8

www.NightmareAtFHA.com

Edward J. Pinto

Edward J. Pinto ([email protected]) is a resident fellow at AEI. The views expressed in FHA Watch are

those of the author alone and do not necessarily represent those of the American Enterprise Institute.

This Issue’s Highlight

FHA’s Decades-Long Record of Harming Working-Class Families and Communities

In 1997 and 2002, the National Training and Information Center (NTIC) published two studies confirming

earlier criticisms of the Federal Housing Administration’s (FHA’s) weak underwriting and program

management practices going back to the early 1960s.

FHA Watch undertook to replicate the NTIC’s 2002 research on the same 22 cities at the zip code level using a

2.4 million FHA loan database. This new study confirmed that the FHA’s underwriting policies continue to

disproportionately impact homeowners in low-income and minority zip codes. This is in large measure

attributable to FHA’s failure to underwrite for risk or recognize the challenges faced by home buyers in

neighborhoods with large concentrations of credit-impaired households.

This Month’s Features

Spotlight on FHA’s Decades-Long Record of Harming Working-Class Families and Communities

Disproportionate Impact on Home Buyers in Low-Income and Minority Zip Codes Continues

Spotlight on Insolvency

FHA’s Estimated GAAP Net Worth Equals –$25.96 Billion, with a Capital Shortfall of $46–66 Billion

Spotlight on Delinquency

Overall Rate Decreases to 14.94 Percent in July from 15.53 Percent in June

Spotlight on Best Price Execution

FHA, VA, and USDA Pricing Dominance Declines

Spotlight on FHA’s Decades-Long Record of Harming Working-Class Families and

Communities

Disproportionate Impact on Home Buyers in Low-Income and Minority Zip Codes Continues

In 1997, the National Training and Information Center (NTIC) published The Devil’s in the Details: An

Analysis of FHA Default Concentration and Lender Performance in 20 U.S. Cities, covering the period 1992–

96.1 In 2002, the NTIC followed up with Families HUD Abandoned: An Analysis of the Federal Housing

Administration’s Loan Default Activity and Lender Performance in 22 U.S. Cities, 1996–2000.2 These studies

confirmed earlier criticisms of the FHA’s weak underwriting and program management practices going back to

the early 1960s.3

The 2002 study, which predates the housing collapse, found “vast differences in FHA default rates in low

income census tracts compared to middle income census tracts. Also, large differences exist in default rates

based on racial composition of census tracts.” Specifically, the study found:

21 of 22 cities had higher FHA loan default rates in low-income census tracts than in middle-income

census tracts.4 The exception was Newark.

19 of 22 cities had higher FHA loan default rates in minority census tracts than in white census tracts.5

The exceptions were Baltimore, Miami, and Washington, DC.

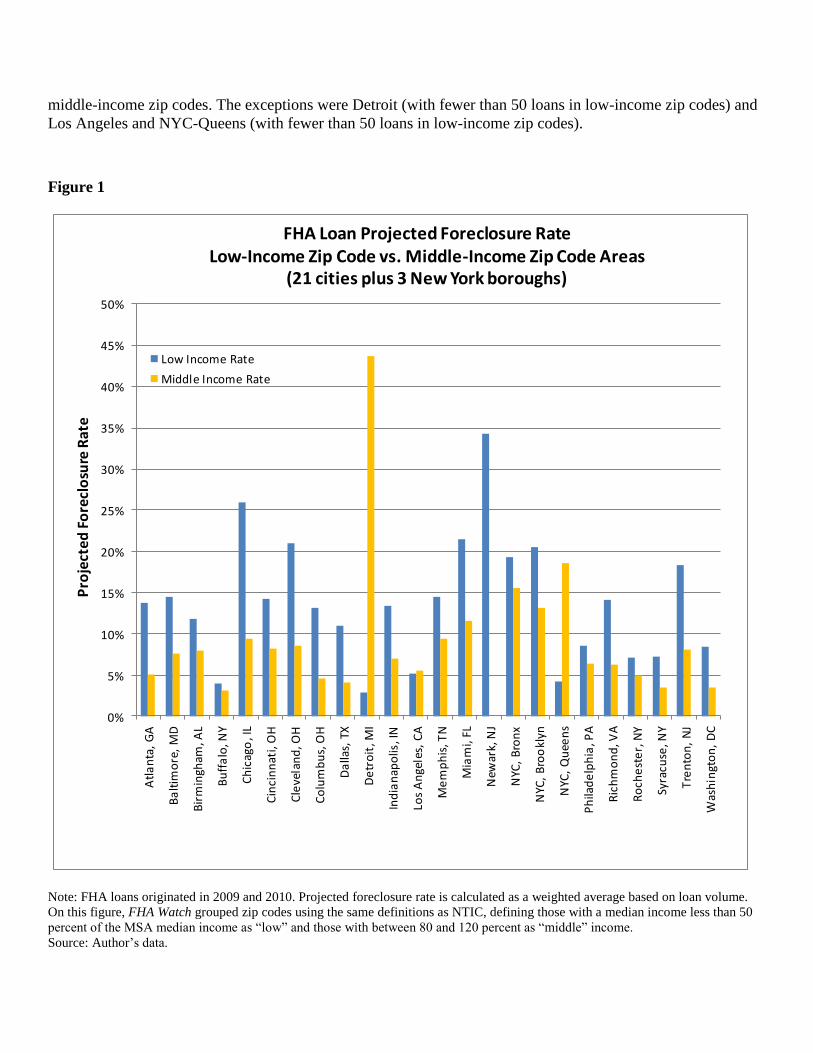

FHA Watch undertook to replicate the NTIC’s 2002 research on the same 22 cities, this time at the zip code

level using a 2.4 million FHA loan database. This new study confirmed that the FHA’s underwriting policies

continue to disproportionately impact homeowners in low-income and minority zip codes. This is in large

measure attributable to FHA’s failure to underwrite for risk or recognize the challenges faced by home buyers

in neighborhoods with large concentrations of credit-impaired households.

Figure 1 shows that little has changed since 2002 in terms of the FHA’s continuing disproportionate impact on

low-income areas. Of 22 cities, 19 had higher FHA projected foreclosure rates in low-income zip codes than in

middle-income zip codes. The exceptions were Detroit (with fewer than 50 loans in low-income zip codes) and

Los Angeles and NYC-Queens (with fewer than 50 loans in low-income zip codes).

Figure 1

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Atl

an

ta,

GA

Ba

ltim

ore

, M

D

Bir

min

gham

, AL

Bu

ffa

lo, N

Y

Ch

icag

o, I

L

Cin

cin

nat

i, O

H

Cle

vela

nd

, OH

Co

lum

bu

s, O

H

Da

llas,

TX

De

tro

it, M

I

Ind

ian

apo

lis, I

N

Los

An

gele

s, C

A

Me

mp

his

, TN

Mia

mi,

FL

New

ark,

NJ

NYC

, B

ron

x

NYC

, B

roo

klyn

NYC

, Q

uee

ns

Ph

ilad

elp

hia

, PA

Ric

hm

on

d, V

A

Ro

che

ste

r, N

Y

Syra

cuse

, NY

Tre

nto

n,

NJ

Was

hin

gto

n,

DC

Pro

ject

ed F

ore

clo

sure

Rat

e

FHA Loan Projected Foreclosure RateLow-Income Zip Code vs. Middle-Income Zip Code Areas

(21 cities plus 3 New York boroughs)

Low Income Rate

Middle Income Rate

Note: FHA loans originated in 2009 and 2010. Projected foreclosure rate is calculated as a weighted average based on loan volume. On this figure, FHA Watch grouped zip codes using the same definitions as NTIC, defining those with a median income less than 50

percent of the MSA median income as “low” and those with between 80 and 120 percent as “middle” income. Source: Author’s data.

Figure 2 shows that little has changed since 2002 in terms of the FHA’s continuing disproportionate impact on

minority areas. Of 22 cities, 19 had higher FHA loan default rates in minority zip codes than in white zip

codes.6 The exceptions were Indianapolis (with zero loans in minority zip codes), NYC–Bronx (with fewer than

50 loans in white zip codes), and Syracuse (with zero loans in minority zip codes).

Figure 2

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Atl

an

ta,

GA

Ba

ltim

ore

, M

D

Bir

min

gham

, AL

Bu

ffa

lo, N

Y

Ch

icag

o, I

L

Cin

cin

nat

i, O

H

Cle

vela

nd

, OH

Co

lum

bu

s, O

H

Da

llas,

TX

De

tro

it, M

I

Ind

ian

apo

lis, I

N

Los

An

gele

s, C

A

Me

mp

his

, TN

Mia

mi,

FL

New

ark,

NJ

NYC

, B

ron

x

NYC

, B

roo

klyn

NYC

, Q

uee

ns

Ph

ilad

elp

hia

, PA

Ric

hm

on

d, V

A

Ro

che

ste

r, N

Y

Syra

cuse

, NY

Tre

nto

n,

NJ

Was

hin

gto

n,

DC

Pro

ject

ed

Fo

recl

osu

re R

ate

FHA Loan Projected Foreclosure RateMinority Zip Code vs. White Zip Code Areas

(21 cities plus 3 New York boroughs)

Minority Rate

White Rate

Note: On this figure, FHA Watch grouped zip codes using the same definitions as NTIC: those with a minority population greater than

80 percent as “minority” and those with fewer than 20 percent as “white.”

Source: Author

The FHA Watch results show that the FHA’s underwriting policies continue to, as the 2002 NTIC report stated,

result in “vast differences in FHA default rates in low income [areas] compared to middle income [areas]. Also,

large differences exist in default rates based on racial composition of [areas].”

Why the Disproportionate Impact?

There are at least three reasons for this unchanging result over the course of many decades.

First, FHA borrowers in low-income and minority neighborhoods tend to have a higher prevalence of low FICO

scores, which generally leads to higher levels of default. For example, in Chicago’s low-income zips, 42.7

percent of FHA borrowers had a FICO score below 660 compared to 31.1 percent for middle-income zips. In

Chicago’s minority zips, 51 percent of FHA borrowers had a FICO score below 660, compared to 26.6 percent

for white zips.

Second, new research by FHA Watch found that loans to FHA borrowers in zip codes with a higher

concentration of residents with low credit scores perform worse than those to FHA borrowers in zip codes with

a low concentration of residents with low credit scores, even when risk factors such as credit score, down

payment, and debt-to-income (DTI) ratio are held constant. For example, in Chicago’s low-income zips, the

average credit score of all residents (not just those of the FHA borrowers) was 643, compared to 713 for the

residents of middle-income zips, and in Chicago’s minority zips, the average credit score for all residents was

633, compared to 729 for residents of white zips.

FHA Watch used credit risk score data [proprietary Equifax Risk Score (ERS) data] to analyze the impact that

varying concentrations of low-credit-score individuals7 in a zip code have on the performance of FHA loans

where credit risk factors were held constant. An FHA borrower living in a zip code in the fourth quartile

(containing zip codes with the lowest credit-risk scores, with mean scores ranging from 519 to 673), on average,

had a 45 percent higher likelihood of being 90+ days delinquent compared to a borrower with the same risk

characteristics living in a zip code in the first quartile (containing zip codes with the highest credit-risk scores,

with mean scores ranging from 721 to 826).

Figure 3 demonstrates that the impact on the 90+-day delinquency rates (90+ rates) was consistent across 245

risk buckets representing five loan-to-value (LTV) categories (LTV includes impact of the upfront premium

charged by the FHA), seven FICO credit score categories,8 and seven DTI categories.

Figure 3

Source: Author

Figure 4 displays the same data, smoothed using a neural net modeling methodology.

Figure 4

Source: Author

In these charts, the five LTV categories are displayed at the bottom along the x-axis. Within each LTV

category, the FICO credit score categories of <580, 580, 600, 620, 660, 680, and 720+ are displayed from left to

right on the x-axis, and the DTI categories of <23, 28, 33, 38, 43, 48, and 55 percent are displayed from bottom

to top on the y-axis. Separate results are shown for the first and fourth quartiles.

Figure 5 is a simplified version limited to the 97.5 percent LTV category to better illustrate the 49 risk buckets

based on FICO credit score and DTI. This more targeted view allows for more detailed labeling; however, the

data displayed for the 97.5 percent LTV segment are identical to figure 4.

Figure 5

Source: Author

Third, separate new research by FHA Watch found that loans to FHA borrowers in zip codes with a higher fraud

risk score perform worse than loans to FHA borrowers in zip codes with a lower fraud risk score,9 even when

risk factors such as FICO credit score, down payment, and DTI ratio are held constant. An FHA borrower living

in a zip code in the fourth quartile (the 25 percent of the zip codes with the highest fraud risk scores), on

average, had a 31 percent higher likelihood of being 90+ days delinquent compared to a borrower with the same

risk characteristics living in a zip code in the first quartile (the 25 percent of the zip codes with the lowest fraud

risk scores).

Figure 6 uses Interthinx Risk Index data to demonstrate the correlation between fraud risk score and the

performance of FHA loans. It compares 90+ rates for both the first and fourth quartiles across 245 risk buckets

representing five LTV categories (LTV includes impact of upfront premium charged by FHA), seven FICO

categories, and seven DTI categories. It was constructed using zip-code-level data from 31 major metropolitan

areas. The data have been smoothed using a neural net modeling methodology. In general, FHA loans in the

fourth quartile (zip codes with a high Interthinx Risk Index) had higher 90+ rates than loans in the first quartile

(zip codes with a lower Interthinx Risk Index), regardless of loan-level risk bucket. This correlation was

strongest for risk buckets in the lower FICO categories across all LTVs and DTIs.

Figure 6

Source: Author

In figure 6, the five LTV categories are displayed at the bottom along the x-axis. Within each LTV category, the

ERS categories of <580, 580, 600, 620, 660, 680, and 720+ are displayed from left to right on the x-axis, and

the DTI categories of <23, 28, 33, 38, 43, 48, and 55 percent are displayed from bottom to top on the y-axis.

Separate results are shown for the first and fourth quartiles.

Figure 7 relates to the Chicago metropolitan area. It illustrates the strong correlation between a zip code’s fraud

risk index and the projected foreclosure rate. At-risk zip codes are primarily ones with below-median incomes

and home prices.

Figure 7

Note: On this figure, zip codes with above-average marketplace Interthinx Fraud Risk Indices (represented by larger dots) are highly

correlated with zips having high projected foreclosure rates and both characteristics concentrated in zip codes with incomes and home

prices below the area median (lower left quadrant). The FHA’s poorly designed lending practices and misaligned incentives expose

working-class families and neighborhoods to excessive foreclosure risk.

Source: Author

Conclusion

The FHA is guilty of inflicting a scourge of foreclosures across America. Over the period 1975 to 2011, more

than 3 million, or one in eight FHA-insured families will suffer a foreclosure—an abysmal record made worse

by the fact that lower-income and minority families have suffered even higher rates of foreclosure.

The FHA has been selling hope and delivering harm. This is the result of systemic deficiencies in the FHA’s

insurance program—a lack of proper alignment of incentives, foreclosure-prone lending practices, and poor

management practices. A long history of cross-subsidizing high-risk loans with lower-risk loans has enabled the

disproportionate impact on lower income and minority families to continue. But as Irving Welfeld observed in

1992, “averaging out is not a defense.”10

What the FHA and the families and communities it serves need is common-sense reform, including the

following:

Reduce coverage below 100 percent [see Section 234 of the Protecting American Taxpayers and

Homeowners Act of 2013 (PATH)];

Advise consumer as to foreclosure risk based applicant’s risk profile (see Section 236 of PATH);

Limit seller concessions to 3 percent (see Section 263 of PATH);

Utilize residual income test (see Section 267 of PATH);

Reinstitute vetted appraisal panels with rotational assignment;

Introduce countercyclical stress test and loan-to-value ratios; and

Underwrite for risk.

Spotlight on Insolvency

FHA’s Estimated GAAP Net Worth Equals –$25.96 Billion, with a Capital Shortfall of $46–66 Billion

This month, the FHA’s private generally accepted accounting principles (GAAP) estimated net worth

deteriorated slightly. The estimate for July of the FHA’s GAAP net worth is –$25.96 billion, down from –

$25.21 billion) in June 2013, up from –$30.41 billion in September 2012, and down from –$20.87 billion in

September 2011. The capital shortfall stands at $47 billion (using a 2 percent capital ratio) and $67 billion

(using a 4 percent capital ratio). The Denial Dial was reset to −2.36 percent.

The FHA has undertaken a series of delinquent mortgage note sales that will impact its GAAP estimated net

worth. The latest sale was in June 2013, when it sold 15,470 nonperforming loans with an unpaid principal

balance of $2.4 billion. The FHA reports its month-to-month cash flow position with a lag of many months. The

impact of these sales will be incorporated as data become available.

Please see the notes to table A1 for a detailed explanation.11

Spotlight on Delinquency

Overall Rate Decreases to 14.94 Percent in July from 15.53 Percent in June

In July, 14.94 percent of all FHA loans were delinquent, down from 15.53 percent in June 2013 and down from

16.52 percent in July 2012. Total delinquencies decreased by 46,573 over June 2013 and declined by 97,353

over July 2012. This continues a slow generally downward trend in overall rate from the high of 17.79 percent,

reached in December 2011.

The serious delinquency rate decreased to 8.25 percent from 8.47 percent in June 2013 and decreased from 9.51

percent in July 2012. The month-over-month decline is presumably is because of 15,470 nonperforming loans

sold in June.

For the monthly data tabulation, see table A2 in the appendix.

Spotlight on Best Price Execution

FHA, VA, and USDA Pricing Dominance Declines

Table 1 demonstrates the pricing advantages the Ginnie/FHA, Ginnie/USDA, and Ginnie/VA divisions have

over Fannie Mae.

The best price execution calculation primarily depends on two factors.

The first is the Ginnie Mae MBS execution relative to the Fannie MBS execution. This month the Ginnie MBS

price spread widened compared to Fannie. While Ginnie’s spread advantage has been quite volatile, it has

tended to trend down. When FHA Watch first started tracking best price execution in February 2012, the

benchmark Ginnie MBS sold at a premium of 1.63 points in price over the benchmark Fannie MBS. In July

2013, it had narrowed to 0.47 points. However, August saw a strong reversal, as the Ginnie execution advantage

widened to 1.03 points. This translates into a one-month increase of $840 in Ginnie’s MBS price advantage on a

$150,000 loan.

The second is the relative cost for mortgage guaranty insurance. The FHA recently implemented a policy

change whereby annual mortgage insurance premiums generally must be paid for the life of the loan, rather than

terminating when the LTV reaches 78 percent. This increased the present value cost of the FHA mortgage

insurance premium by an estimated $2,000 on a $150,000 loan.

While these two factors partially offset each other, the net result was that the FHA’s execution worsened by

about $1,000. Compared to last month, the Fannie execution is now ahead of the FHA’s on loans C and D and

has a widened advantage on E, F, and G.

This continues a two-year trend that has seen Fannie’s price execution improve compared to the FHA’s. As

table 1 demonstrates, this advantage increases as loan risk decreases (generally represented by FICO score). As

a result, in April–June 2013 the FHA had the lowest percentage of its new business with FICO scores above 720

(26.9 percent) since January–March 2011 (37.8 percent).

Table 1. Best Price Execution (Ginnie pricing advantages in bold)

Feature Loan A Loan B Loan C Loan D Loan E Loan F Loan G

MBS coupon 4.00% 4.00% 4.00% 4.00% 4.00% 4.00% 4.00%

Term 30-yr 30-yr 30-yr 30-yr 30-yr 30-yr 30-yr

LTV 95% 96.50% 95% 95% 90% 95% 90%

FICO 620 680 680 700 700 720 740

Risk levelVery

highHigh Medium Medium Medium Medium

Medium-

low

Ginnie/FHA

Execution94.63 94.36 94.63 94.63 94.63 94.63 94.63

Ginnie/USDA

Execution100.18 100.18 100.18 100.18 100.18 100.18 100.18

Ginnie/VA

Execution102.03 101.38 102.03 102.03 102.28 102.03 102.28

Fannie Execution 92.29 93.32 95.46 95.71 97.15 97.42 98.48

Ginnie/FHA

advantage on a

$150,000 loan

compared to Fannie $3,516 $1,558 -$1,239 -$1,614 -$3,774 -$4,187 -$5,777

Ginnie/USDA

advantage on a

$150,000 loan

compared to Fannie $11,841 $10,296 $7,086 $6,711 $4,551 $4,138 $2,548

Ginnie/VA

advantage on a

$150,000 loan

compared to Fannie $14,616 $12,096 $9,861 $9,486 $7,701 $6,913 $5,698

Source: Adapted from JPMorgan’s 2012 Securitized Products Outlook, November 23, 2011, 18.

Note: Mortgage-backed securities (MBS) pricing from MBS Live, published by Mortgage News Daily. Comparison based on MBS

pricing as of August 23, 2013. On that date, a Ginnie 30-year MBS with a coupon of 4.0 percent had a price of 103.53, and a Fannie

30-year MBS with the same 4.0 percent coupon had a price of 102.81. These prices were then adjusted based on the present value

(where necessary) of applicable borrower-paid credit fees, mortgage insurance premiums, and the value of the base servicing fee.

Fannie’s guarantee fee was increased by 10 basis points effective April 2012, as mandated by Congress, and by 10 basis points again

as announced on August 31, 2012, by the Federal Housing Finance Agency. All publicly announced FHA premium increases are

included. USDA and VA premiums are unchanged.

On the whole, the five divisions of the Government Mortgage Complex (along with Freddie Mac) have

substantial pricing and underwriting advantages over the private sector. The result is that the Government

Mortgage Complex’s share of the entire first-mortgage market continues to be at 85–90 percent.

Appendix: Historical Data Tables

Table A1. Insolvency Watch ($ Billions)

Date

FHA’s

“Capital

Resources”

(Assets)

Cash Flow

since end of

fiscal year*

Estimated

Case Loss

Reserve

(Liabilities

on PMI

Basis)**

Estimated

Liability for

Excess

Upfront

Premiums

beyond

GAAP

Allowance

Current

Net

Worth

(PMI

Basis)

Require

d

Capital

Ratio

Required

Capital

Under

Applicable

Ratio***

Capital

Shortfall

(PMI

Basis)

Sept. 30, 2011 $28.18 --- $41.05 $8.00 ($20.87) 2% $18.14 ($39.02)

Sept. 30, 2011 $28.18 --- $41.05 $8.00 ($20.87) 4% $36.29 ($57.16)

Sept. 30, 2012 $25.57 --- $46.88 $9.10 ($30.41) 2% $19.43 ($49.84)

Sept. 30, 2012 $25.57 --- $46.88 $9.10 ($30.41) 4% $38.85 ($69.26)

Oct. 31, 2012 $25.57 ($0.42) $45.18 $9.35 ($29.38) 2% $19.51 ($48.90)

Oct. 31, 2012 $25.57 ($0.42) $45.18 $9.35 ($29.38) 4% $39.02 ($68.41)

Nov. 30, 2012 $25.57 ($0.85) $45.23 $9.60 ($30.11) 2% $19.51 ($49.62)

Nov. 30, 2012 $25.57 ($0.85) $45.23 $9.60 ($30.11) 4% $39.02 ($69.13)

Dec. 31, 2012 $25.57 ($1.27) $45.30 $9.60 ($30.61) 2% $19.51 ($50.11)

Dec. 31, 2012 $25.57 ($1.27) $45.30 $9.60 ($30.61) 4% $39.01 ($69.62)

Jan. 31, 2013 $25.57 ($1.70) $43.30 $9.60 ($29.03) 2% $19.56 ($48.59)

Jan. 31, 2013 $25.57 ($1.70) $43.30 $9.60 ($29.03) 4% $39.12 ($68.15)

Feb. 28, 2013 $25.57 ($2.12) $41.82 $9.60 ($27.97) 2% $19.78 ($47.74)

Feb. 28, 2013 $25.57 ($2.12) $41.82 $9.60 ($27.97) 4% $39.56 ($67.52)

Mar. 31, 2013 $25.57 ($2.54) $39.88 $9.60 ($26.45) 2% $19.96 ($46.41)

Mar. 31, 2013 $25.57 ($2.54) $39.88 $9.60 ($26.45) 4% $39.92 ($66.37)

Apr. 30, 2013 $25.57 ($2.97) $38.53 $9.60 ($25.53) 2% $20.05 ($45.58)

Apr. 30, 2013 $25.57 ($2.97) $38.53 $9.60 ($25.53) 4% $40.10 ($65.63)

May 31 2013 $25.57 ($3.39) $37.60 $9.60 ($25.02) 2% $20.10 ($45.12)

May 31 2013 $25.57 ($3.39) $37.60 $9.60 ($25.02) 4% $40.20 ($65.22)

Jun. 30 2013 $25.57 ($3.82) $38.37 $9.60 ($26.21) 2% $20.06 ($46.27)

Jun. 30 2013 $25.57 ($3.82) $38.37 $9.60 ($26.21) 4% $40.12 ($66.33)

Jul. 31 2013 $25.57 ($4.24) $38.28 $9.60 ($26.55) 2% $20.02 ($46.57)

Jul. 31 2013 $25.57 ($4.24) $38.28 $9.60 ($26.55) 4% $40.04 ($66.59)

Notes: Table A1 estimates the FHA’s current net worth and capital shortfall under accounting rules applicable to a private mortgage

insurer (PMI) such as Genworth. Estimates are based on Genworth having the FHA’s delinquent loans, risk exposure, capital

resources, and capital ratio (under both the 2 percent statutory requirement for the FHA and the 4 percent of risk-in-force requirement

applicable to a PMI). In quarter 2 of 2013, Genworth had loss reserves equaling 59 percent of its risk-in-force on 60-days-plus

delinquent loans, up 1 percent from quarter 1 of 2013. Genworth, Quarterly Financial Supplements, Delinquency Metrics-US

Mortgage Insurance Segment, 44, http://phx.corporate-ir.net/phoenix.zhtml?c=175970&p=irol-quarterlyreports

(accessed August 22, 2013).

*The FHA’s negative cash flow was $424 million per month during Q1 of FY 2013. See exhibit 10, US Department of Housing and

Urban Development, FHA Single-Family Mutual Mortgage Insurance Fund Programs, Quarterly Report to Congress, 13. The FHA

raised its upfront premium from 1 to 1.75 percent (excluding streamline refinances) effective for case numbers assigned on or after

April 9, 2012. Since under private GAAP accounting this amount would not be taken into income immediately, it will be accounted

for in the “Estimated liability for excess upfront premiums beyond GAAP allowance.” The amount of this liability was estimated at

$9.60 billion as of April 30, 2013.

** Outstanding balance of loans 60-days-plus delinquent based on loan counts on applicable date times average loan balance for loans

going to claim of $126,524. Reserve levels have been recalculated based on gross paid claim amounts derived from claim terminations

data in the report series entitled Monthly Report to the FHA Commissioner, 6,

http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/rmra/oe/rpts/com/commenu (January 2013 is the latest data

update available) and Net Loss on Claims Percentage data from the report series entitled Quarterly Report to Congress on the

Financial Status of the MMI Fund (FY 2012 Q4), Exhibit 5,

http://portal.hud.gov/hudportal/documents/huddoc?id=fhartc_q4_2013.pdf (accessed May 18, 2013). The FY 2013 Q1 report was not

used as it had a number of unique factors present. It will be reevaluated once the FY 2013 Q2 is released.

***Total based on the FHA’s total amortized risk-in-force net of loans covered by loan loss reserve.

Table A2. National Delinquency Watch

End Date 30-Days Delinquency

Rate and Number of

Loans

60-Days-Plus

Delinquency Rate

and Number of Loans

30-Days-Plus

Delinquency Rate

and Number of Loans

Serious Delinquency Total Loans

Jan. 2011 N/A N/A N/A 8.9% / 612,443 6,882,984

Mar. 2011 N/A N/A N/A 8.3% / 580,480 6,983,893

June 2011 5.79% / 411,258 10.55% / 749,204 16.62% / 1,160,462 8.34% / 592,366 7,103,531

Sept. 2011 5.70% / 413,834 11.08% / 803,899 16.78% / 1,217,733 8.77% / 636,778 7,258,328

Dec. 2011 5.72% / 421,404 12.07% / 889,602 17.79% / 1,311,006 9.73% / 716,786 7,370,426

Jan. 2012 5.35% / 397,018 12.18% / 903,748 17.53% / 1,300,766 9.92% / 735,760 7,418,830

Feb. 2012 4.78% / 355,092 11.70% / 871.870 16.47% / 1,226,962 9.73% / 725,002 7,450,480

Mar. 2012 4.57% / 341,213 11.21% / 837,472 15.78% / 1,178,685 9.47% / 707,930 7,471,708

Apr. 2012 4.77% / 358,174 11.20% / 840,803 15.97% / 1,198,977 9.42% / 707,222 7,507,031

May 2012 4.93% / 372,514 11.29% / 852,608 16.23% / 1,225,222 9.43% / 711,612 7,549,730

June 2012 5.19% / 393,894 11.43% / 867,959 16.61% / 1,261,853 9.48% / 719,984 7,594,689

July 2012 5.04% / 384,349 11.48% / 874,802 16.52% / 1,259,151 9.51% / 725,074 7,622,873

Aug. 2012 4.91% / 375,464 11.44% / 874,656 16.35% / 1,250,120 9.49% / 725,692 7,645,912

Sept. 2012 5.58% / 428,351 11.70% / 898,590 17.30% / 1,326,931 9.62% / 738,303 7,671,677

Oct. 2012 5.02% / 387,000 11.54% / 887,959 16.57% / 1,274,959 9.54% / 734,431 7.693,992

Nov. 2012 4.95% / 382,194 11.53% / 888,901 16.48% / 1,271,095 9.56% / 737,251 7,710,077

Dec. 2012 5.23% / 404,686 11.50% / 890,400 16.72% / 1,295,086 9.40% / 728,394 7,744,925

Jan. 2013 5.07% / 392,536 11.63% / 900,852 16.70% / 1,293,388 9.58% / 741,618 7,744,921

Feb. 2013 4.76% / 369,571 11.21% / 869,952 15.97% / 1,239,523 9.39% / 728,860 7,760,200

Mar. 2013 4.52% / 351,478 10.68% / 829,619 15.21% / 1,181,097 9.03% / 701,628 7,767,181

Apr. 2013 4.36% / 338,957 10.32% / 801.694 14.68% / 1,140,651 8.73% / 678,506 7,770.886

May 2013 4.39% / 341,400 10.06% / 782,193 14.46% / 1,123,593 8.45% / 656,909 7,771,948

June 2013 5.27% / 410,172 10.26% / 798,199 15.53% / 1,208,371 8.47% / 659,314 7,781,196

July 2013 4.87% / 378,903 10.10% / 782,895 14.94% / 1,161,798 8.25% / 641,808 7,776,713

Sources: US Department of Housing and Urban Development, “Neighborhood Watch,” https://entp.hud.gov/sfnw/public (Servicing

download, Excel; accessed July 15, 2013) and US Department of Housing and Urban Development, “FHA Outlook,”

http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/rmra/oe/rpts/ooe/olmenu (accessed October 21, 2012). Rates not

seasonally adjusted. Serious delinquency includes ninety-days-plus delinquency and loans in bankruptcy or foreclosure.

Notes 1 National Training and Information Center, The Devil’s in the Details: An Analysis of FHA Default Concentration and Lender

Performance in 20 U.S. Cities (Chicago: NTIC, October 1997). 2 National Training and Information Center, Families HUD Abandoned: An Analysis of the Federal Housing Administration’s Loan

Default Activity and Lender Performance in 22 U.S. Cities, 1996–2000 (Chicago: NTIC, May 2002). 3 In 1962, the FHA’s mounting foreclosures were noted by Time magazine: “Homeowners of a new and unattractive breed are

plaguing the Federal Housing Administration these days. Known as ‘the walkaways,’ they are people who find themselves unable to

meet their mortgage payments—and to solve the problem simply move out their belongings at night, drop their house key in the

mailbox and disappear. … Because it underwrites low-cost housing for high-risk groups, the FHA’s problems are particularly acute.”

(See “Credit: Beware of the Walkaways,” Time, July 27, 1962, www.time.com/time/magazine/article/0,9171,827500,00.html.)

In 1973, Brian D. Boyer chronicled “how the FHA scandal worked on a day-to-day basis [to destroy whole neighborhoods] in the big

cities of the United States.” (See Brian D. Boyer, Cities Destroyed for Cash: The FHA Scandal at HUD, Chicago: Follett Publishing

Company, 1973.)

In 1986, the New York Times noted the similarities of yet another round of FHA scandals to the horrors experienced during the 1960s

and 1970s in Brooklyn and other cities: “That scandal – as with others at the time that affected such cities as Newark, Philadelphia and

Detroit – was remarkably similar to a pattern of fraud that Federal investigators said last month that they had found in several cities,

including Camden, N.J.; Houston, Seattle and Milwaukee. … The results have been huge numbers of defaults.” (See Martin Gottlieb,

“FHA Case Recalls Bushwick in 70’s,” New York Times, February 2, 1986, www.nytimes.com/1986/02/02/nyregion/fha-case-recalls-

bushwick-in-70-s.html.)

In 1992, former HUD attorney and senior analyst Irving Welfeld summed up HUD’s history with “Mention the Department of

Housing and Urban Development and the word scandal comes to mind.” (See Irving Welfeld, HUD Scandals: Howling Headlines and

Silent Fiascos, New Brunswick, NJ: Transaction Publishers, 1992.) 4 The NTIC defined census tracts with a median income less than 50 percent of the metropolitan statistical area (MSA) median income

as “low” and those between 80 and 120 percent as “middle” income. 5 The NTIC defined census tracts with minority populations greater than 80 percent as “minority” and those with fewer than 20

percent as “white.” 6 Buffalo and Rochester each had fewer than 50 loans in minority zip codes.

7 The ERS is calculated using a proprietary model created by Equifax. The ERS uses a numerical range of 280 to 850—the lower the

score, the greater the likelihood of the consumer becoming severely delinquent. Equifax has calculated ERS for over 218 million

scorable individuals in the United States residing in over 52,000 zip codes. Using data obtained from Equifax, the average ERS for

each zip code was determined. The zip codes were rank ordered by average ERS. The data set was then divided into four equal

quartiles, each representing approximately 54 million individuals. The first quartile was assembled by starting with the zip code with

the highest average ERS (a score of 826) and proceeding downward by average ERS until zip codes with a sufficient number of scored

individuals were selected to account for one-quarter of the total 218 million ERS scored population. This first quartile had an ERS

range of 721–826. This process was repeated for the second, third, and fourth quartiles. The fourth quartile had an ERS range of 519–

673. This process allowed for each zip code to be assigned to a unique quartile. The first versus fourth quartiles were used for

purposes of the analysis, as these best demonstrate the effect of average ERS differences at the zip code level. Up to this point, no

FHA-specific information had been utilized. 8 While ERSs were used to construct the zip code quartiles, FICO credit scores were used as a risk category to define FHA loan risk

buckets at the zip code level. The FICO score (a proprietary model created by Fair Isaac Corporation) uses a numerical range of 300 to

850—again, the lower the score, the greater the likelihood of the consumer becoming severely delinquent. FICOs were the credit score

used to assign each FHA loan to a risk bucket. 9 For this research, the Interthinx Mortgage Fraud Risk Indices were used. The Fraud Risk Indices are calculated based on the

frequency with which indicators of fraudulent activity are detected in mortgage applications processed by Interthinx. The Fraud Risk

Indices consist of the property valuation, identity, occupancy, and employment/income values. 10

Welfeld, HUD Scandals. 11

January–June 2013 estimates were adjusted based on data contained in exhibits 5 and 8, US Department of Housing and Urban

Development, FHA Single-Family Mutual Mortgage Insurance Fund Programs, Quarterly Report to Congress FY 2013 Q3, 9 and 13.