Embed Size (px)

Citation preview

FHA TRAINING WORKBOOK

A Comprehensive Guide to FHA Lending with Finance of America

Ver 2016.10.1

LYNNE GONZALESAccount Executiveo: (925) 808.7208f: (949) [email protected] FAMWholesale.com

Finance of America Mortgage FHA Training Workbook 2016

1 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

WELCOME TO FINANCE OF AMERICA MORTGAGE FHA TRAINING

The promise of what Finance of America Mortgage offers to its valued business partners will change the landscape of our industry and transform the home mortgage experience for your customers. It is our goal to provide our third party originators with the very best in loan products, customer service levels and quality training.

This workbook outlines the FHA loan program guidelines at Finance of America and is designed to help you originate more FHA loans. We have included important information including how to submit a loan with Finance of America as well as several checklists to help you and your team process your loans quicker which will result in a timely delivery of service to your customers.

It is our goal to help you deliver positive experiences to your customers and it is the most critical focus for us at Finance of America. We thank you for the opportunity to serve you as a third party loan originator and to help your serve your customers.

ABOUT THIS WORKBOOK

This workbook is divided into sections to help you easily navigate to the information you need. At the end you will find important resource links and checklists. You can start at the beginning and work your way through the entire workbook or jump to the sections that pertain to your exact scenario. We also have additional training resources available for you at our website at www.famwholesale.com

Introduction

Finance of America Mortgage FHA Training Workbook 2016

2 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

EVERYTHING YOU NEED TO KNOW

Table of Contents

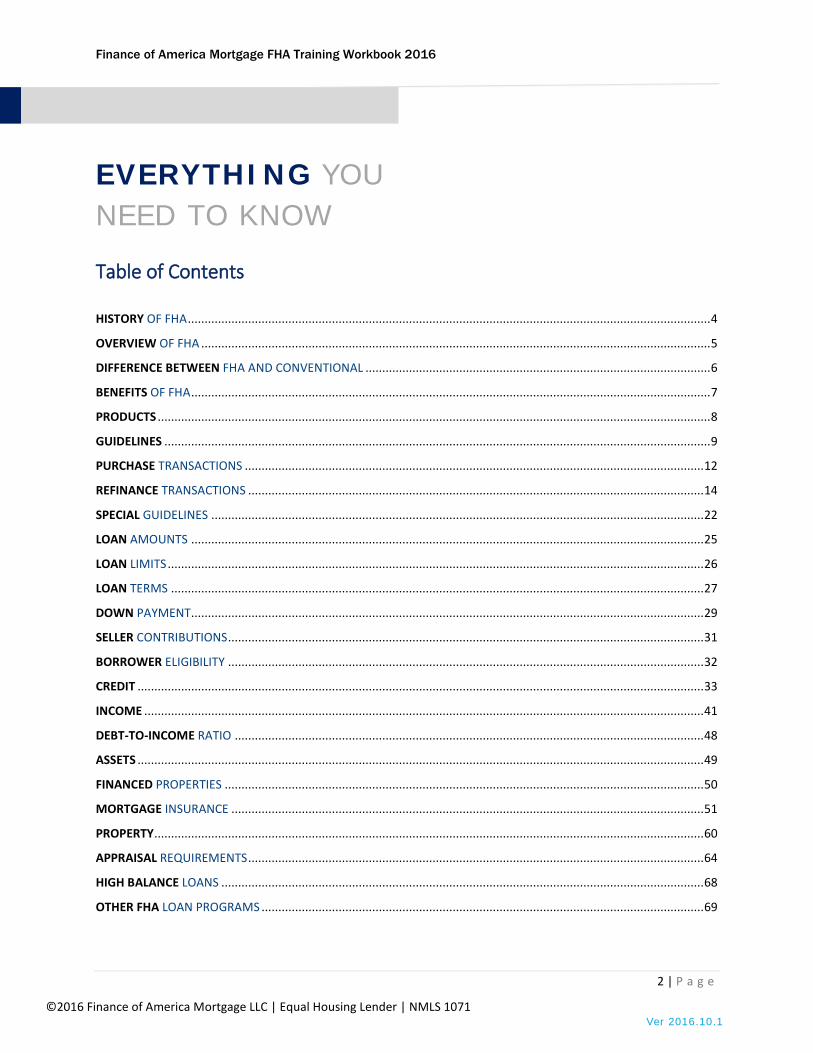

HISTORY OF FHA ............................................................................................................................................................ 4

OVERVIEW OF FHA ........................................................................................................................................................ 5

DIFFERENCE BETWEEN FHA AND CONVENTIONAL ....................................................................................................... 6

BENEFITS OF FHA ........................................................................................................................................................... 7

PRODUCTS ..................................................................................................................................................................... 8

GUIDELINES ................................................................................................................................................................... 9

PURCHASE TRANSACTIONS ......................................................................................................................................... 12

REFINANCE TRANSACTIONS ........................................................................................................................................ 14

SPECIAL GUIDELINES ................................................................................................................................................... 22

LOAN AMOUNTS ......................................................................................................................................................... 25

LOAN LIMITS ................................................................................................................................................................ 26

LOAN TERMS ............................................................................................................................................................... 27

DOWN PAYMENT ......................................................................................................................................................... 29

SELLER CONTRIBUTIONS .............................................................................................................................................. 31

BORROWER ELIGIBILITY .............................................................................................................................................. 32

CREDIT ......................................................................................................................................................................... 33

INCOME ....................................................................................................................................................................... 41

DEBT-TO-INCOME RATIO ............................................................................................................................................ 48

ASSETS ......................................................................................................................................................................... 49

FINANCED PROPERTIES ............................................................................................................................................... 50

MORTGAGE INSURANCE ............................................................................................................................................. 51

PROPERTY .................................................................................................................................................................... 60

APPRAISAL REQUIREMENTS ........................................................................................................................................ 64

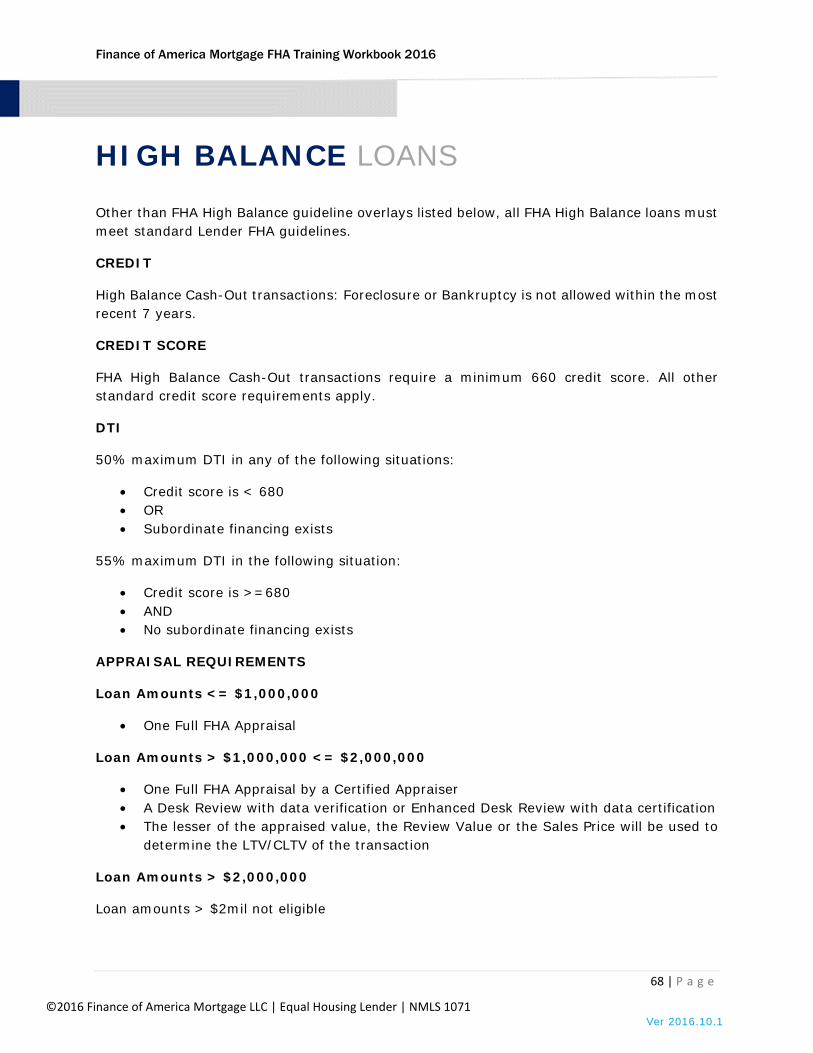

HIGH BALANCE LOANS ................................................................................................................................................ 68

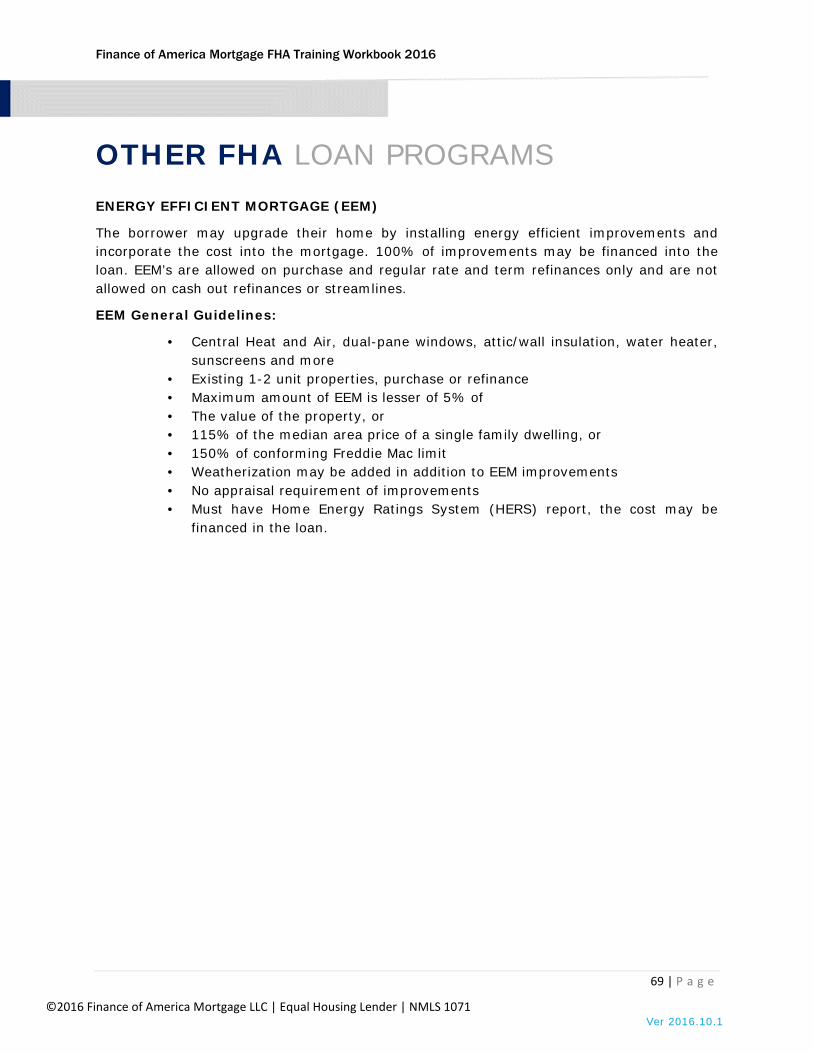

OTHER FHA LOAN PROGRAMS .................................................................................................................................... 69

Finance of America Mortgage FHA Training Workbook 2016

3 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

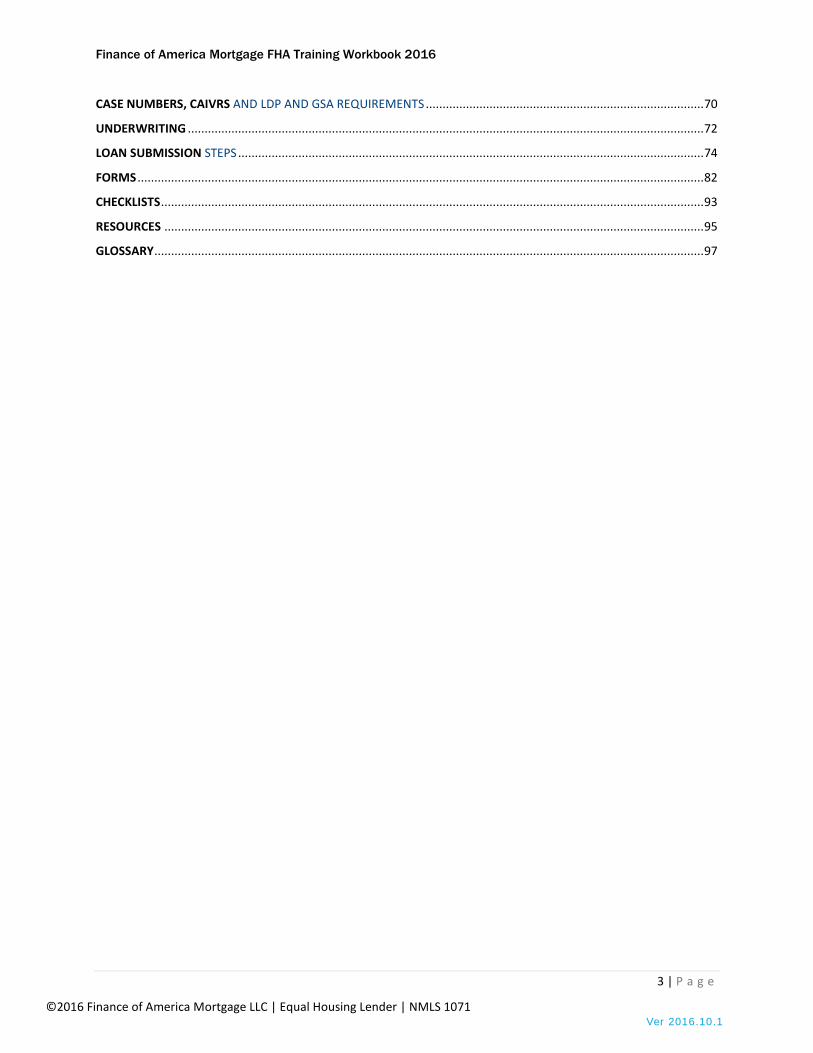

CASE NUMBERS, CAIVRS AND LDP AND GSA REQUIREMENTS ................................................................................... 70

UNDERWRITING .......................................................................................................................................................... 72

LOAN SUBMISSION STEPS ........................................................................................................................................... 74

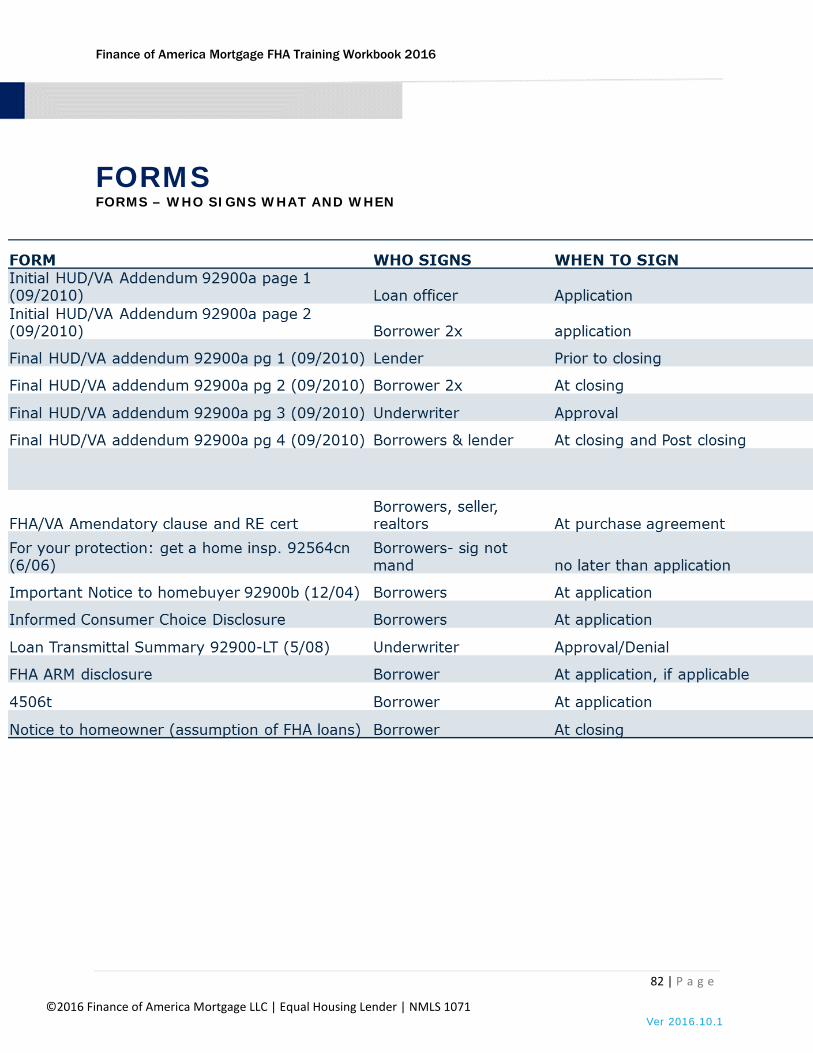

FORMS ......................................................................................................................................................................... 82

CHECKLISTS .................................................................................................................................................................. 93

RESOURCES ................................................................................................................................................................. 95

GLOSSARY .................................................................................................................................................................... 97

Finance of America Mortgage FHA Training Workbook 2016

4 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

HISTORY OF FHA THE FEDERAL HOUSING ADMINISTRATION The Federal Housing Administration (FHA) is a government corporation that was created in 1934 to help stabilize the housing market during the Great Depression. The goal was to set a standard for housing conditions and to create a financing system that would help buyers by insuring loans for them. FHA fell under the regulation of the U.S. Department of Housing and Urban Development (HUD) in 1965.

FHA insures mortgages on single family and multifamily homes including manufactured homes and hospitals. It is the largest insurer of mortgages in the world, insuring over 34 million properties since its inception in 1934.

FHA is the only government agency that operates entirely from its self-generated income and costs the taxpayers nothing. The proceeds from the mortgage insurance paid by the homeowners are captured in an account that is used to operate the program entirely. FHA provides a huge economic stimulation to the country in the form of home and community development, which trickles down to local communities in the form of jobs, building suppliers, tax bases, schools, and other forms of revenue.

Today FHA is the largest insurer of mortgages in the world, and provides an affordable way for the home buyers to own their own homes. The agency has helped to raise the number of homeowners in the nation. In fact, homeowners make up 64.9% of the nation's population today.

Finance of America Mortgage FHA Training Workbook 2016

5 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

OVERVIEW OF FHA FHA MORTGAGE FINANCING An FHA mortgage is a government-backed home loan with more flexible lending requirements than those for conventional mortgages. FHA loans are available with fixed interest rates or with adjustable rates. FHA loans have somewhat less stringent down payment and credit requirements than conventional mortgages. They require a down payment as low as 3.5% of the sales price, and borrowers may qualify even without a long standing credit history or top-notch credit scores. FHA APPROVED LENDERS FHA does not lend money. Instead, FHA, insures loans. The insurance removes or minimizes the default risk lenders face when buyers invest less than 20% down in a transaction. FHA approved lenders are authorized to:

• Take loan applications • Process loan applications • Underwrite loan files to established FHA guidelines. • Direct Endorsement (DE) allows lenders the authority to commit FHA insurance.

Finance of America Mortgage FHA Training Workbook 2016

6 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

DIFFERENCE BETWEEN FHA AND CONVENTIONAL

• FHA Specific Disclosures • Loan Transmittal Summary (LT) vs. FNMA 1008 • URLA (Uniform Residential Loan Application) vs. FNMA 1003 • Addendum to the URLA (HUD-92900-A) • Conditional Commitment DE Statement of Appraised Value (HUD-92800-5B)-FAM will

supply & complete this form • Case #s -Broker to request on FAM website • CAIVRS Database Search-FAM will complete this task • LDP & GSA Database Search-Broker to complete

FHA SPECIFIC DISCLOSURES

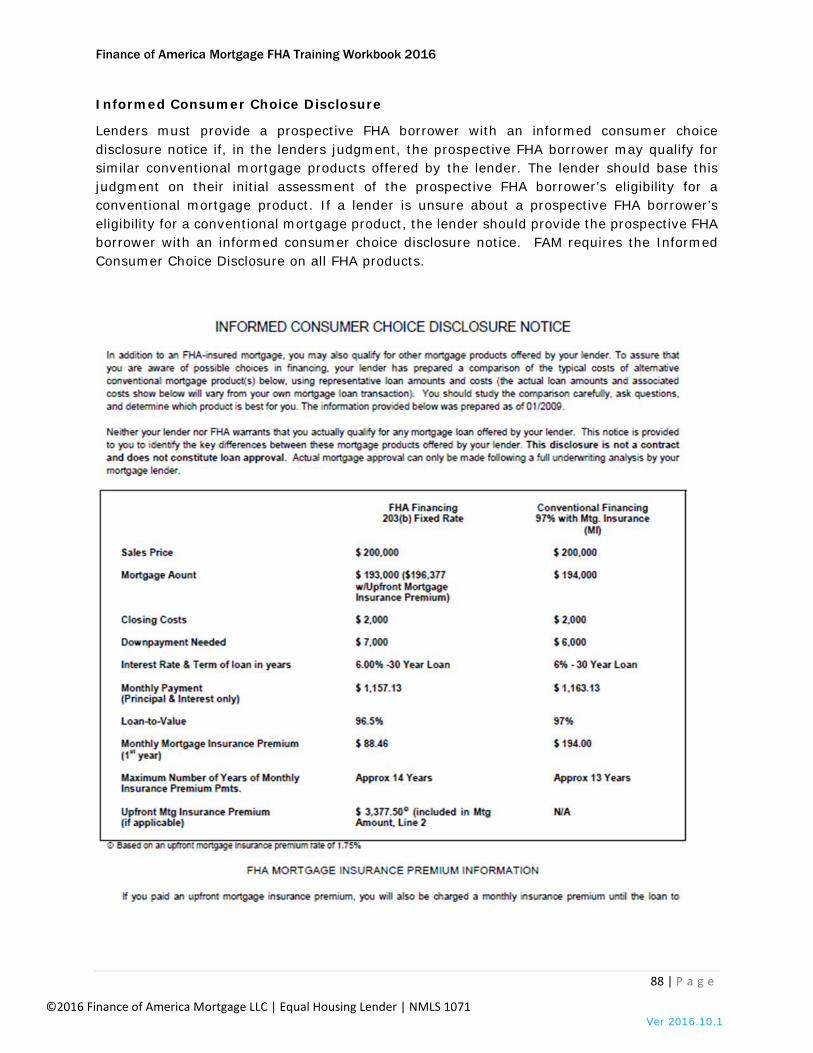

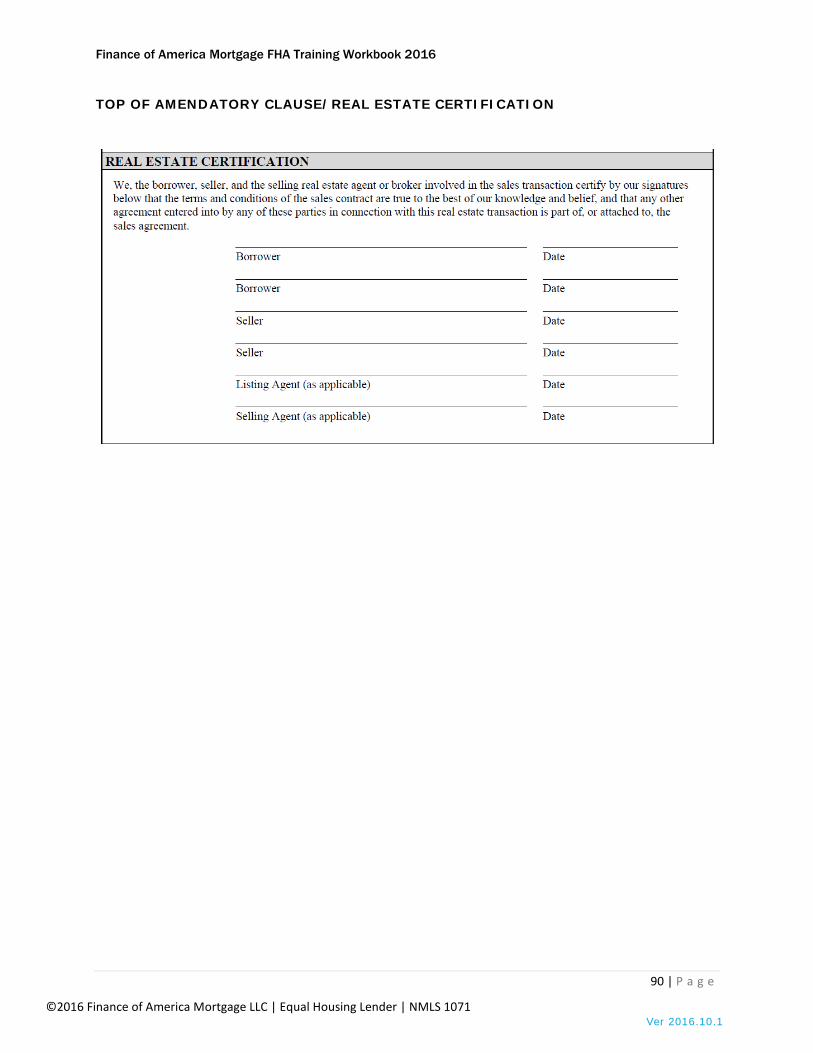

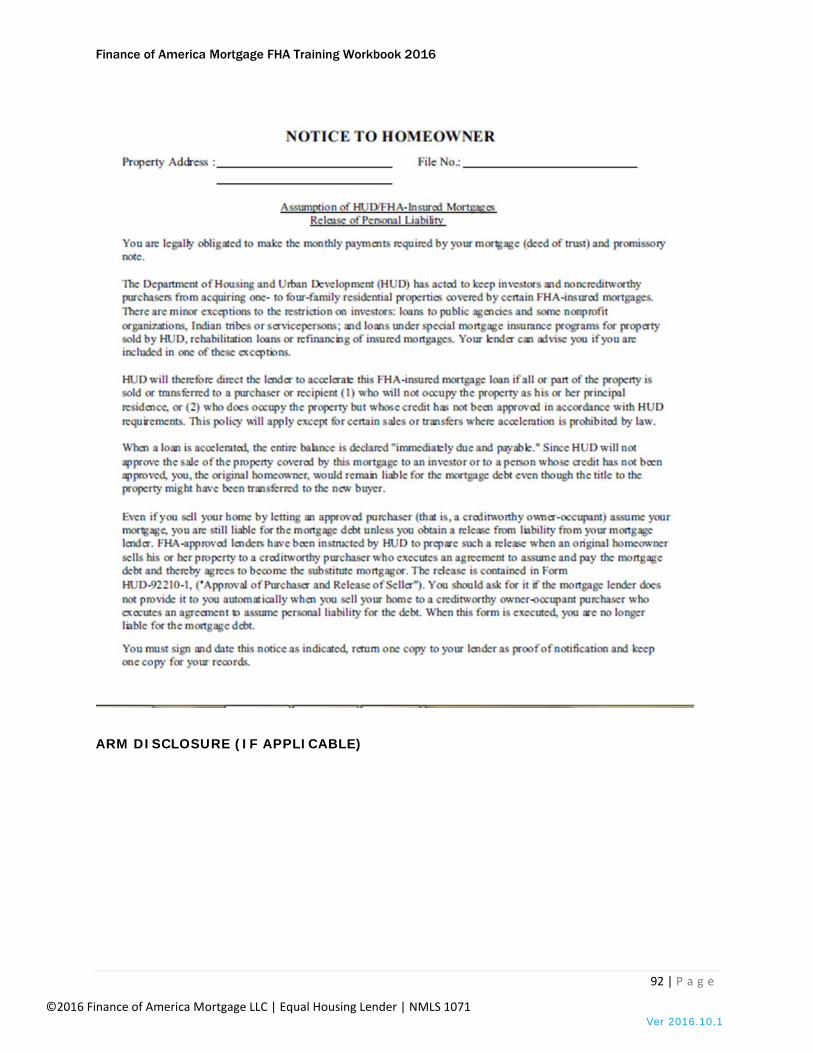

• Important Notice to Homebuyer (HUD 92900-B 11/2014) • For your Protection: Get a Home Inspection • Informed Consumer Choice Disclosure • Amendatory Clause/Real Estate Certification • Notice to Homebuyer (Assumption of HUD/FHA Mortgages) • Arm Disclosure (if applicable)

NOTE: Examples and links to FHA specific disclosures are in the resource section at the end of this workbook.

Finance of America Mortgage FHA Training Workbook 2016

7 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

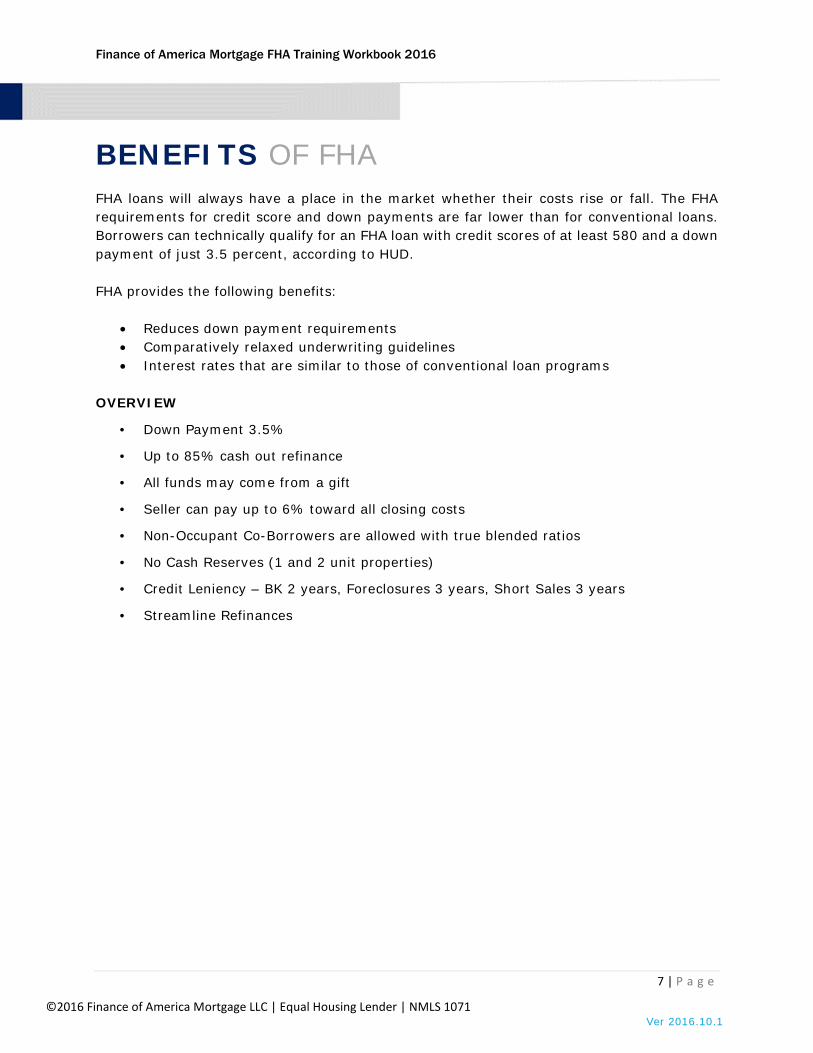

BENEFITS OF FHA FHA loans will always have a place in the market whether their costs rise or fall. The FHA requirements for credit score and down payments are far lower than for conventional loans. Borrowers can technically qualify for an FHA loan with credit scores of at least 580 and a down payment of just 3.5 percent, according to HUD.

FHA provides the following benefits:

• Reduces down payment requirements • Comparatively relaxed underwriting guidelines • Interest rates that are similar to those of conventional loan programs

OVERVIEW

• Down Payment 3.5%

• Up to 85% cash out refinance

• All funds may come from a gift

• Seller can pay up to 6% toward all closing costs

• Non-Occupant Co-Borrowers are allowed with true blended ratios

• No Cash Reserves (1 and 2 unit properties)

• Credit Leniency – BK 2 years, Foreclosures 3 years, Short Sales 3 years

• Streamline Refinances

Finance of America Mortgage FHA Training Workbook 2016

8 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

• Assumable

PRODUCTS PRODUCT NAME - FHA 203B

Purchase or Refinance of 1-4-unit primary residence

FIXED PRODUCTS

• 15 and 30 Year for standard loan amounts and

• 30 years only on high balance loan amounts

ARM PRODUCTS

• 5/1 ARMs on standard loan amounts

• 5/1 ARMs on high balance loan amounts

• 1/1/5 caps, 2.00% Margin, Index is one year US Treasury

• Not available for streamline refinances

Finance of America Mortgage FHA Training Workbook 2016

9 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

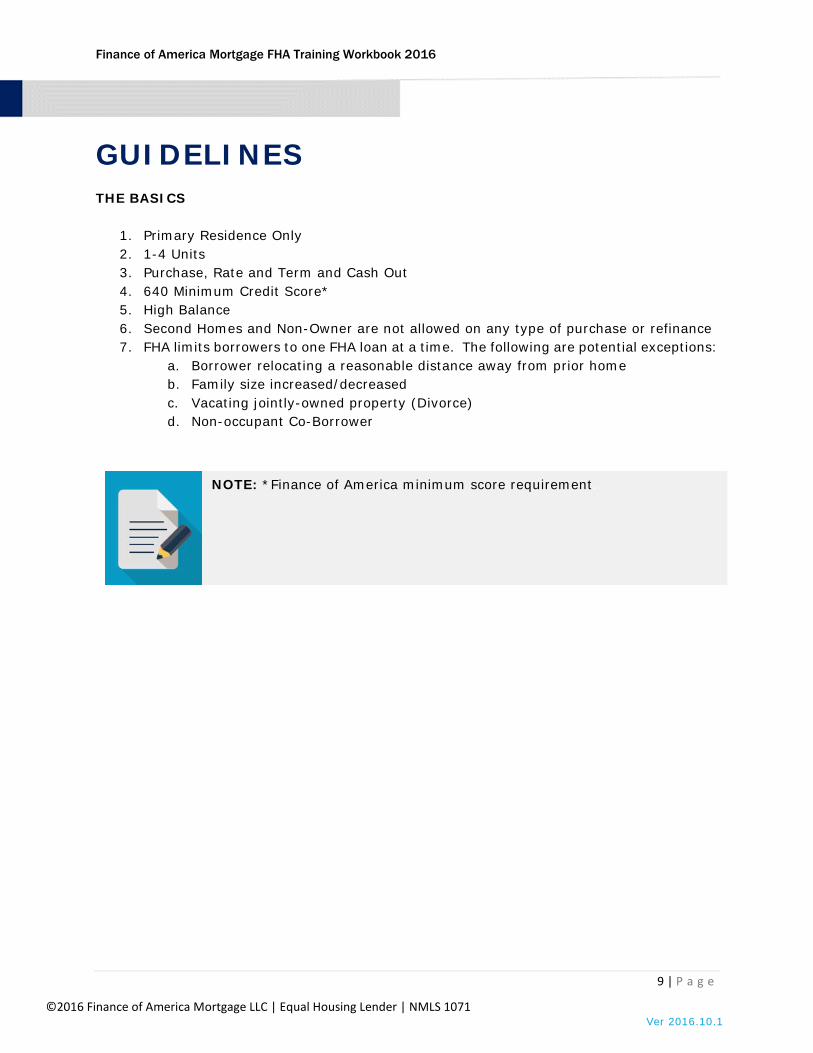

GUIDELINES THE BASICS

1. Primary Residence Only 2. 1-4 Units 3. Purchase, Rate and Term and Cash Out 4. 640 Minimum Credit Score* 5. High Balance 6. Second Homes and Non-Owner are not allowed on any type of purchase or refinance 7. FHA limits borrowers to one FHA loan at a time. The following are potential exceptions:

a. Borrower relocating a reasonable distance away from prior home b. Family size increased/decreased c. Vacating jointly-owned property (Divorce) d. Non-occupant Co-Borrower

NOTE: *Finance of America minimum score requirement.

Finance of America Mortgage FHA Training Workbook 2016

10 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

GUIDELINES TABLE

Primary Residence

Purchase

PROPERTY TYPE LTV CLTV FICO: FICO: Standard loan

amounts High Bal loan amounts

1-4 units 96.5 100 640 640

Simple Refinance1

PROPERTY TYPE LTV CLTV FICO: FICO: Standard loan

amounts High Bal loan amounts

1-4 units 97.75 97.75 640 640

Rate/Term Refinance2

PROPERTY TYPE LTV CLTV FICO: FICO: Standard loan

amounts High Bal loan amounts

1-4 units 97.75 2 97.75 2 640 640

1-4 units 85 2 85 2 640 640

Cash-Out Refinance

PROPERTY TYPE LTV CLTV FICO: FICO: Standard loan

amounts High Bal loan amounts

1-4 units 85 85 640 640

Streamline Refinance3

PROPERTY TYPE LTV CLTV FICO: FICO: Standard loan

amounts High Bal loan amounts

1-4 units See Notes4 125% 640 640

1) Simple Refinance refers to a no cash-out refinance of an existing FHA-insured Mortgage in which all proceeds are used to pay the existing FHA insured mortgage lien on the subject Property and costs associated with the transaction.

2) Rate and Term Refinance refers to a no cash-out refinance of any Mortgage in which all proceeds are used to pay existing mortgage liens on the subject Property and costs associated with the transaction.

− 97.75 percent for Principal Residences that have been owner-occupied for previous 12 months, or owner-occupied since acquisition if acquired within 12 months, at case number assignment;

− 85 percent for a Borrower who has occupied the subject Property as their Principal Residence for fewer than 12 months prior to the case number

Finance of America Mortgage FHA Training Workbook 2016

11 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

assignment date; or if owned less than 12 months, has not occupied the Property for that entire period of ownership.

3) Streamline Refinance refers to the refinance of an existing FHA-insured Mortgage requiring limited Borrower credit documentation and underwriting. There are two different streamline options available.

− Credit Qualifying • The Mortgagee must perform a credit and capacity analysis of the Borrower, but no appraisal is required.

− Non-Credit Qualifying • The Mortgagee does not need to perform credit or capacity analysis or obtain an appraisal.

4) No maximum LTV on a streamline refinance. The loan must meet Maximum Insurable Mortgage guidelines.

Finance of America Mortgage FHA Training Workbook 2016

12 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

PURCHASE TRANSACTIONS The Borrower may not receive any cash back through a purchase, other than an amount representing:

• A reimbursement for the Borrower’s overpayment of fees • Costs paid by the Borrower in advance; earnest money deposit, appraisal or

credit report fees; or • A legitimate real estate tax credit in locales where real estate taxes are paid in

arrears. • If the Borrower receives an allowable amount of cash back, the minimum

Borrower contribution must be met and verified.

Refer to Loan Amount Calculation Worksheet below.

PURCHASE LOAN CALCULATION WORKSHEET

Base Loan Amount

A $ X 96.5% =

Lesser of Sales Price or Appraised Value

Max LTV Base Loan Amount

Minimum Down Payment

B $ - $ = $

Sales Price Max Base Loan Amount Min Down Payment

Up Front MIP

C $ X 1.75* = $

Base Loan Amount (*older case # vary, see charts)

Up Front MIP

Finance of America Mortgage FHA Training Workbook 2016

13 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

Total Loan Amount

D $ + $ = $

Base Loan Amount Up Front MIP Total Loan Amount

Finance of America Mortgage FHA Training Workbook 2016

14 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

REFINANCE TRANSACTIONS NO CASH OUT REFINANCE/REGULAR REFINANCE

Below are requirements for no cash out refinances.

• The current mortgage must be a NON-FHA fixed rate or ARM. • Single Family, Owner Occupied Primary Residence Only • Maximum mortgage is the LOWER of 97.75% of appraisal or Existing Debt Calculation • Existing debt includes payoff of existing 1st, PM 2nd, jr. lien over 12 months, closing

costs, prepaid expenses, borrower paid repairs, and discount points. • If any portion of funds of equity line in excess of $1000 in last 12 months, for purposes

other than repairs and rehab. of property the line of credit may not be included. • Property owned less than 12 months, must use lesser of original purchase price +

expenditures for repairs, or current appraised value • Modified/Restructured loans are okay to be paid off, as long as the loan is not

delinquent and no late payments in past 12 months, unless AUS decision is Approve/Eligible. Current lender must supply letter that they will not file deficiency

• Proceeds to buy out ex-spouse are okay • Borrower may not receive more than $500 at closing • Non-Occupant Co-Borrower may be added • 2nd Liens may subordinate, up to 97.75% (case numbers as of 9/7/2010) • Terms of subordinate lien must not have a balloon or prepayment penalty • Payments are calculated in qualifying

Finance of America Mortgage FHA Training Workbook 2016

15 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

NO CASH OUT REFINANCE LOAN CALCULATION WORKSHEET

LTV Factor Method

A $ X 97.75% =

Appraised Value Max Mortgage #1

Existing Debt Method

B $ + $ = $

Payoff 1st, PM 2

nd or

seasoned Jr. Lien

Closing Costs -non-recurring, prepaids and discount points

Max Mortgage #2

Up Front MIP

C $ X 1.75* = $

Lower of Max #1 and Max #2

(*older case # vary, see charts)

Up Front MIP

Total Loan Amount

D $ + $ = $

Lower of Max #1 and Max #2

Up Front MIP And EEM upgrades if any

Total Loan Amount

Finance of America Mortgage FHA Training Workbook 2016

16 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

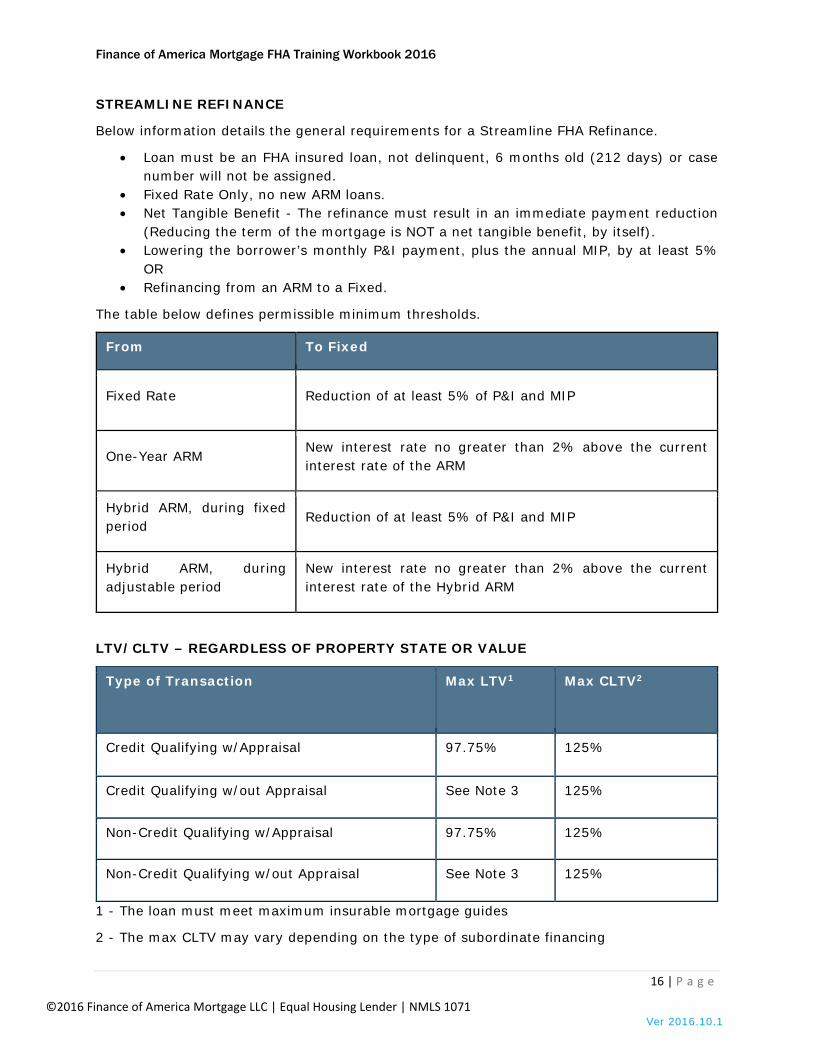

STREAMLINE REFINANCE

Below information details the general requirements for a Streamline FHA Refinance.

• Loan must be an FHA insured loan, not delinquent, 6 months old (212 days) or case number will not be assigned.

• Fixed Rate Only, no new ARM loans. • Net Tangible Benefit - The refinance must result in an immediate payment reduction

(Reducing the term of the mortgage is NOT a net tangible benefit, by itself). • Lowering the borrower’s monthly P&I payment, plus the annual MIP, by at least 5%

OR • Refinancing from an ARM to a Fixed.

The table below defines permissible minimum thresholds.

From To Fixed

Fixed Rate Reduction of at least 5% of P&I and MIP

One-Year ARM New interest rate no greater than 2% above the current interest rate of the ARM

Hybrid ARM, during fixed period

Reduction of at least 5% of P&I and MIP

Hybrid ARM, during adjustable period

New interest rate no greater than 2% above the current interest rate of the Hybrid ARM

LTV/CLTV – REGARDLESS OF PROPERTY STATE OR VALUE

Type of Transaction Max LTV1 Max CLTV2

Credit Qualifying w/Appraisal 97.75% 125%

Credit Qualifying w/out Appraisal See Note 3 125%

Non-Credit Qualifying w/Appraisal 97.75% 125%

Non-Credit Qualifying w/out Appraisal See Note 3 125%

1 - The loan must meet maximum insurable mortgage guides

2 - The max CLTV may vary depending on the type of subordinate financing

Finance of America Mortgage FHA Training Workbook 2016

17 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

3 - No maximum LTV on a streamline refinance without an appraisal. The loan must meet maximum insurable mortgage guidelines.

MAXIMUM INSURABLE MORTGAGE STREAMLINE REFINANCE WITH APPRAISAL

CREDIT QUALIFYING – MAX INSURABLE MORTGAGE IS THE LOWER OF:

• The outstanding principal balance minus the applicable refund of UFMIP, plus closing costs, prepaid items to establish the escrow account and the new UFMIP. OR

• 97.75% of appraised value of the property, plus the new UFMIP.

NON-CREDIT QUALIFYING – MAX INSURABLE MORTGAGE CANNOT EXCEED:

• The outstanding principal balance minus the applicable refund of the UFMIP, PLUS the new UFMIP.

• An appraisal may not be used to increase the insurable mortgage balance beyond the sum of the outstanding principal balance and the new UFMIP. The new loan balance may NOT include closing costs, prepaid items or other financing.

• The outstanding principal balance may include interest charged by the servicing lender when the payoff is not received on the first day of the month, but may NOT include delinquent interest, late charges or escrow shortages.

• Discount points may not be included the new mortgage.

MAXIMUM INSURABLE MORTGAGE STREAMLINE REFINANCE WITHOUT APPRAISAL

• At the time of case number, the “original value” must be obtained from FHA Connection • The maximum insurable mortgage cannot exceed:

o The outstanding principal bal. minus the applicable refund of the UFMIP, plus the new UFMIP.

o The outstanding principal balance may include interest charged by the servicing lender when the payoff is not received on the first day of the month, but may not include delinquent interest, late charges or escrow shortages.

• Condo project approval is not required. • Recently listed properties. • Listing must be cancelled at least 1 day prior to the date of the loan application. • A letter of intent to occupy from the borrower is required.

Finance of America Mortgage FHA Training Workbook 2016

18 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

MAXIMUM MORTGAGE CALCULATION WITHOUT APPRAISAL

$ _____________ Unpaid principal balance* of existing FHA loan - _____________ The LESSER of: $ ____________ Unearned UFMIP (from FHA Refinance Authorization or appropriate MIP Refund Schedule) OR $ ____________ New Estimated UFMIP = _____________ Maximum Base Loan Amount before UFMIP + _____________ New UFMIP = _____________ Total New Loan Amount including UFMIP

*May include interest charged when payoff is not received on the first day of the month. Cannot include delinquent interest, late charges or escrow shortages or MIP.

Finance of America Mortgage FHA Training Workbook 2016

19 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

MAXIMUM MORTGAGE CALCULATION WITH APPRAISAL

Calculation A:

$ ______________ Outstanding Principal Balance*

- (______________) The LESSER of: $ ____________ Unearned UFMIP (from FHA Refinance

Auth. or appropriate MIP Refund Schedule) OR $ ____________ New Estimated UFMIP + ______________ Closing costs**

+ ______________ Prepaids (includes per diem interest to end of month on new loan, hazard insurance and real estate tax deposits

needed to establish escrow account) - _______________ Lender Credit for Closing Costs and Prepaid Items

= _______________ Total A

Calculation B:

$ _______________ Total B = Appraised Value x 97.75%

Calculation C:

$ _______________ Total C = Max County Limit

New Mortgage Amount:

$ _______________ Maximum Base Mortgage (Lowest of Totals A, B and C)

+ _________ ______ New UFMIP (If financed)

$ _______________ Total New Mortgage Amount

*Outstanding Principal Balance May include Interest, but not delinquent interest, late charges or escrow shortages **Discount points may not be included in the loan amount, must be paid from borrower’s funds.

Finance of America Mortgage FHA Training Workbook 2016

20 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

CASH OUT REFINANCE

Below are details and requirements for a cash out FHA refinance:

FHA will insure a cash out refinance, up to 85% of appraised value with the following requirements:

• Properties owned 12 months or more, use current appraised value. • Properties owned less than 12 months use lesser of purchase price or appraised

value. • All Borrowers must hold title to property for at least six months. • Modified/Restructured loans are not eligible for a cash out refinance. • Borrowers whose loans are delinquent or in arrears are not eligible. • Non-Occupant Borrowers may not be added to qualify. • Existing or new subordinate financing to a maximum CLTV of 85%. • Modified subordinate financing is acceptable to a maximum CLTV of 85%. • 1 -4 units, 3-4 unit properties must pass self-sufficiency test. • Properties owned free and clear may be financed as cash-out transactions. • Listing agreements on subject property must have been cancelled 6 mos. prior

to loan application or subject to max 70% LTV/CLTV.

CASH OUT REFINANCE WORKSHEET

Max LTV Calculation

A $ X 85% =

Appraised Value Base Loan Amount

Up Front MIP

C $ X 1.75* = $

Base Loan Amount (*older case # vary, see charts)

Up Front MIP

Total Loan Amount

D $ + $ = $

Base Loan Amount Up Front MIP Total Loan Amount

Finance of America Mortgage FHA Training Workbook 2016

21 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

SPECIAL NOTE ON CALCULATING INSURANCE ON FHA REFINANCES

About Prepayment (excerpt from Important Notice to Homebuyers Disclosure):

This notice is to advise you of the requirements that must be followed to accomplish a prepayment of your mortgage, and to prevent accrual of any interest after the date of prepayment. You may prepay any or all of the outstanding indebtedness due under your mortgage at any time, without penalty. However, to avoid the accrual of interest on any prepayment, the prepayment must be received on the installment due date (the first day of the month) if the mortgagee stated this policy in its response to a request for a payoff figure. Otherwise, you may be required to pay interest on the amount prepaid through the end of the month. The mortgagee can refuse to accept prepayment on any date other than the installment due date.

NOTE: For all FHA mortgages closed on or after January 21, 2015, mortgagees may only charge interest through the date the mortgage is paid in full.

BEST PRACTICE WHEN REFINANCING AN EXISTING FHA LOAN THAT WAS ORIGINATED PRIOR TO JANUARY 21ST, 2015: ASSUME INTEREST WILL BE CHARGED

THROUGH THE END OF THE MONTH PAYOFF IS RECEIVED UNTIL OR UNLESS YOUR PAYOFF DEMAND STATES OTHERWISE.

BEST PRACTICE WHEN REFINANCING AN EXISTING FHA LOAN THAT WAS ORIGINATED PRIOR TO JANUARY 21ST, 2015: ASSUME INTEREST WILL BE CHARGED

THROUGH THE END OF THE MONTH PAYOFF IS RECEIVED UNTIL OR UNLESS YOUR PAYOFF DEMAND STATES OTHERWISE.

Finance of America Mortgage FHA Training Workbook 2016

22 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

SPECIAL GUIDELINES

IDENTITY OF INTEREST Identity of Interest is when there is a relationship between someone included in the transaction and the borrower(s). This includes family or business relationships and is limited to 85% LTV with the following exceptions:

• An employee of builder purchasing builder’s new home as primary. • A tenant purchases rented property, evidencing at least 6 months as tenant

immediately predating the sales contract. • A corporation transfers an employee, purchases that employee’s home, then sells

home to another employee. • Family member purchases another family member’s primary residence.

TRANSACTIONS AFFECTING MAXIMUM MORTGAGE There are several guidelines to be aware of that can have an effect on the FHA transaction. These guidelines include the following: Non-Occupant Co-Borrowers

• Permitted for purchases, no cash out refinances - all LTVs, and cash out refinances (must be on title, cannot add) up to 85%.

• 2-4 units max LTV is 75%. • Must be immediate family member (others, case by case) or max LTV is 75%. • Housing and obligations are included in the DTI ratios. Credit, income and assets must

be verified. • Must sign Note and Security Instrument and all other closing documents.

NOTE: If property is seller’s investment property, max mortgage is lesser of either 85% of appraised value or the appropriate LTV ratio percentage applied to sales price, plus or minus required adjustments. The 85% limit may be waived if family member has been tenant in subject property for at least 6 months.

Finance of America Mortgage FHA Training Workbook 2016

23 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

3 And 4 Unit Properties

• The maximum mortgage is limited so that the ratio of the monthly mortgage payment divided by the monthly net rental income does not exceed 100%.

o Monthly payment is principal, interest, taxes, insurance, mortgage insurance and any HOA dues.

o Net rental income is appraiser’s estimate of fair market rent from ALL units, incl. borrower’s own unit, less the appraiser’s estimate for vacancies, or 15%*, whichever is greater (Santa Ana HOC).

o The above calculations are only to determine max loan amount, borrower must still qualify as usual, and projected rent may only be used as gross income and not to offset mortgage payment.

o Borrower must have 3 months PITI reserves, cannot be a gift.

PROPERTIES UNDER CONSTRUCTION OR EXISTING LESS THAN ONE YEAR

• In these circumstances the loan is limited to 90% LTV, with the following exceptions: • Construction completed more than one-year preceding borrower’s signature on

HUD92900-A. • The dwelling’s site plans and materials were approved by VA, an eligible DE

Underwriter, or an FHA certified builder prior to construction. • Local jurisdiction issued BOTH a building permit AND a Certificate of Occupancy

or equivalent. • The dwelling is covered by a builder’s ten-year warranty plan acceptable to HUD.

PROPERTY FLIPPING

• Property flipping is when properties are purchased and resold in a short period of time for a considerable profit.

• Only owners of record may sell properties that will be financed using FHA insured mortgages. No sales or assignment of contract.

• Any resale of a property may not occur 90 or fewer days from the last sale to be eligible for financing – Exceptions to follow.

• Re-sales between 91 and 180 days where the new sales price exceeds previous price by 100% or more, additional appraisal will be required.

• FAM may require additional documentation to support resale value of property sold more than 90 days and up to 12 months.

• Restrictions do not apply to a builder selling a newly built home. • Appraisers are required to analyze prior sales of subject property. • FAM will require documentation to support increased value including any rehabilitation

or remodeling, to possibly include a second appraisal.

Finance of America Mortgage FHA Training Workbook 2016

24 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

RESALES OCCURRING 90 DAYS OR LESS – EXCEPTION If the owner sells a property within 90 days after the recorded date of acquisition, it is not eligible, unless it falls into one of the following exceptions:

o Sales by HUD of REO’s o Sales by other US Government entities o Sales by nonprofits approved by HUD o Sales acquired by inheritance o Sales by employers or relocation agencies o Sales by mortgage companies, their subsidiaries and any vendors hired by

these exempt entities o Sales by State and Federally chartered financial institutions and Government

sponsored enterprises (Fannie Mae and Freddie Mac) o Sales by local and state government agencies o Sales of properties within Presidentially-Declared Disaster Areas

Property Flipping Red Flags and Documentation Requirements

• All title transfers in the previous 12 months must be documented and reviewed in detail.

• Any increase in property value (including repairs and upgrades) in the previous 12 months must be reviewed, supported and documented by the Appraiser and Underwriter.

• A field review or second appraisal may be required at Underwriter’s discretion.

Conversion of Primary Residence to Rental Effective with Case numbers ordered on or after September 19, 2008, ML 2008-25, rental income on current primary residence being vacated, may not be considered, with the following exclusions (this applies solely to a principal residence being vacated in favor of another principal residence):

• Relocations – Homebuyer is relocating with new employer or transferring with current employer.

• Properly executed lease agreement of at least one year. • Evidence of security deposit and/or • Evidence of first month’s rent paid to homeowner. • Sufficient Equity in Vacated property. • 25% equity, determined by a current appraisal, less than 6 months old.

Rental income may NOT be derived from a family member.

NOTE: Properties acquired by individuals, investment groups, REO property-re-sellers or others whose intent is the purchase, repair and reselling of the property are not exempt from the 90-day resale restriction

Finance of America Mortgage FHA Training Workbook 2016

25 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

LOAN AMOUNTS FHA MAXIMUM LOAN AMOUNTS The National Housing Act establishes the maximum mortgage limits and the mortgage amounts for all FHA mortgage insurance programs. The limits are calculated based the median house prices in each geographic area. FHA loan limits vary based on a variety of housing types and the state and county in which the property is located, and are published annually, to be effective for each calendar year.

FHA loan limits are set by HUD, and vary from county to county. Current loan amount limits can be found online at: https://entp.hud.gov/idapp/html/hicostlook.cfm

MAXIMUM MORTGAGE CALCULATION - PURCHASE

• 96.5% of the lesser of sales price or appraised value (base loan amount) • Does not include Up Front MIP (UFMIP) • Borrower must have minimum of 3.5% down payment (Can be gift) • Closing costs may not be used in minimum 3.5% calculation • Seller Concessions maximum 6%

MAXIMUM MORTGAGE CALCULATION – REFINANCE

• No Cash Out and Streamline Refinances with appraisal 97.75% of appraised value (base loan amount).

• Cash out Refinances - 85% of appraised value.

Finance of America Mortgage FHA Training Workbook 2016

26 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

LOAN LIMITS FHA Maximum LTVs and Mortgage Insurance FHA mortgage insurance protects the lender in the event of borrower default. FHA borrowers will pay for the cost of mortgage insurance two ways: Up-Front Mortgage Insurance Premium (UFMIP) and Annual Mortgage Insurance Premium (also referred to as the periodic or monthly MIP, as the cost is assessed annually, but premiums are collected as part of the borrower’s monthly payments).

The chart below illustrates the maximum loan-to-value ratios for specific FHA transactions, and lists the UFMIP required by those programs. The UFMIP is a charge that can be financed back into the loan amount or paid in cash.

Transaction

Maximum LTV UFMIP

Purchase 96.50% (3.5% down pmt.)

1.75%

Rate-Term Refinance 97.75% if owner occupied for the previous 12 months 85% if borrower has not occupied as principal residence for <12 months prior to case number date or if owned less than 12 months and has not occupied the property for the entire period of ownership

1.75%

FHA to FHA Streamline with Appraisal

97.75% 1.75% * EXCEPT CERTAIN LOANS INSURED BEFORE 5/31/2009 – UFMIP DECREASED TO .01%

FHA to FHA Streamline without Appraisal

n/a 1.75% EXCEPT CERTAIN LOANS INSURED BEFORE 5/31/2009 – UFMIP DECREASED TO .01%

Cash-out Refinance 85% 1.75%

Finance of America Mortgage FHA Training Workbook 2016

27 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

LOAN TERMS

FIXED RATE

• 15 and 30 years

FIXED-PERIOD ADJUSTABLE-RATE MORTGAGE (ARMS)

• 30-year term only

*Due to market variances, ARM loans may be subject to additional pricing requirements.

*ARMs are not eligible for Streamline Refinances.

5/1 FIXED-PERIOD TERM

• First adjustment is 60–66 months after the first payment date. • Adjusts annually with 1% maximum increase or decrease per adjustment. • Conversion options are not allowed.

INDEX

Weekly average on U.S. Treasury securities adjusted to a constant maturity of one year.

LIFE CAP

5% above the start rate

LIFE FLOOR

5% below the start rate, but never lower than the margin

MARGIN

2.00%

PAYMENT ADJUSTMENT DATE First adjustment is the first of the month following the interest rate adjustment and every 12 months thereafter High Balance:

• 30 years • 5/1 fixed-period term − First adjustment is 60–66 months after the first payment date. − Adjusts annually with 1% maximum increase or decrease per adjustment. − ARMs are not eligible for Streamline Refinances.

Application of Unused Borrower Funds from an Escrow Account on an Existing Mortgage in FHA-Insured Refinance Transactions − Refer to the Asset section of the guidelines Standard Loan Amounts.

Maximum Base Loan Amount cannot exceed the FHA Statutory Mortgage Limits for each county and under no circumstances will a county’s mortgage limit be less than the “floor” or greater than the “ceiling” as outlined in the table below.

Finance of America Mortgage FHA Training Workbook 2016

28 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

Lowest Maximum Highest Maximum (Floor) (Ceiling)

Continental US

1-Unit $271,050 $417,000

2-Unit $347,000 $533,850 3-Unit $419,425 $645,300 4-Unit $521,250 $801,950

Alaska and Hawaii

1-Unit $271,050 $625,500

2-Unit $347,000 $800,775 3-Unit $419,425 $967,950 4-Unit $521,250 $1,202,925

HIGH BALANCE LOAN AMOUNTS Maximum Base Loan Amount cannot exceed the FHA Statutory Mortgage Limits for each county and under no circumstances will a county’s mortgage limit be less than the “floor” or greater than the “ceiling” as outlined in the table below. Lowest Maximum Highest Maximum (Floor) (Ceiling)

Continental US

1-Unit $417,001 $625,500

2-Unit $533,851 $800,775 3-Unit $645,301 $967,950 4-Unit $801,951 $1,202,925

Alaska and Hawaii

1-Unit $625,501 $938,250

2-Unit $800,776 $1,201,150 3-Unit $967,951 $1,451,925 4-Unit $1,202,926 $1,804,375

Refer to the "High Balance" section of the FHA Guidelines for additional FHA High Balance guideline overlays.

Maximum loan limits are determined by geographic areas. A complete schedule of FHA mortgage limits for all areas is available at: https://entp.hud.gov/idapp/html/hicostlook.cfm

Finance of America Mortgage FHA Training Workbook 2016

29 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

DOWN PAYMENT FHA requires a Minimum Required Investment of 3.5% of the sales price invested in the transaction.

This money must be their own funds; however, FHA considers Gift Funds to be the borrower’s own funds.

GIFT FUNDS Gifts can be in any amount and they can cover ALL or PART of the down payment required. Acceptable sources for Gift Funds include:

• Direct family members • Employers • Non-profit organizations • Someone with a “close relationship” with the borrower • A governmental agency that has a program providing homeownership assistance to

low or moderate income families or first time homebuyers

FHA has a definitive way of documenting the movement of Gift Funds.

THE FOLLOWING IS REQUIRED TO USE GIFT FUNDS

• The dollar amount • The donor’s name, address, telephone number • The Borrower must be named • The donor’s relationship to the Borrower • The donor’s signature • A statement that no repayment is required • Must contain language asserting that the funds given were not made to the donor from

any person with an interest in the sale of the property. • Gift Letter • The gift giver will need to complete a Gift Letter specifically stating that the money is

a gift and repayment of the funds is not expected. They will also need to provide documentation to prove they had the ability to give the gift to the borrower (usually in the form of a bank statement showing the funds were available at the time the gift was given.

• A copy of the gift check and proof of the borrower depositing the funds into their bank also need to be included in the file.

• “Cash on Hand” is NOT an acceptable source of Gift Funds.

Finance of America Mortgage FHA Training Workbook 2016

30 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

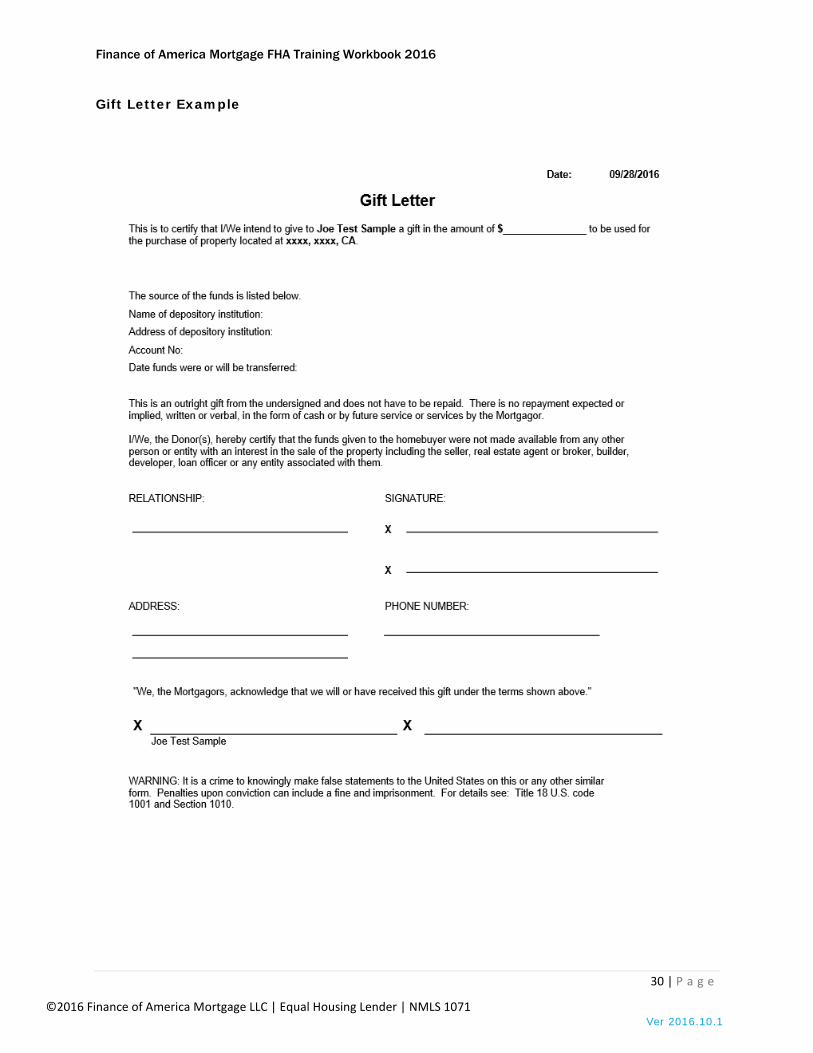

Gift Letter Example

Finance of America Mortgage FHA Training Workbook 2016

31 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

SELLER CONTRIBUTIONS INTERESTED PARTY CONTRIBUTIONS Interested parties in a real estate transaction refers to sellers, real estate agents, builders, developers or any other person or entity with an interest in the transaction. FHA limits the contributions interested parties can make to the real estate transaction.

FHA allows the interested party to contribute up to 6% of the sales price of a property towards a borrower’s closing costs, origination fees or discount points.

ADDITIONAL APPRAISAL REQUIREMENTS FOR INTERESTED PARTY CONTRIBUTIONS

• A transaction with an interested party contribution has the following (additional) appraisal requirements.

• The appraisal must indicate the amount of the contribution. • The appraiser must comment on the impact the contribution has to the final value of

the property. • The appraiser must demonstrate the effect this has on final value. • The comparable sales must be adjusted by the value of the contributions as recognized

by the market, in the appraiser’s opinion, not just dollar for dollar amount of the contribution.

• Any comparables sold with financing and/or sales concessions must reflect the difference between what the comparables actually sold for with and without concessions.

• Positive adjustments for sales or financing concessions are not acceptable.

NOTE: No portion of the seller assist can be used towards the borrower’s 3.5% down payment.

Finance of America Mortgage FHA Training Workbook 2016

32 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

BORROWER ELIGIBILITY GENERAL GUIDELINES FOR ELIGIBILITY

• U.S. Citizen • Permanent Resident Aliens • Non-Permanent Resident Aliens • All Borrowers must have a valid Social Security Number • Title must be held in individual names only

FHA will insure loans used to finance owner-occupied, 1-4 family properties. This means that a borrower taking an FHA loan is signing loan documents stating that they intend to move into the property and occupy it as their primary residence.

An FHA loan cannot be used to purchase an investment property; however, the purchase of a 2-4-unit property is allowable, provided the borrower will occupy one of the units.

While US citizenship is not required for FHA mortgage eligibility, FHA insures mortgages made to individuals with valid Social Security numbers.

Permanent resident aliens may be eligible for FHA insured financing, provided the borrower satisfies the same requirements, terms and conditions as those for US Citizens, and they are able to provide proof that they are a lawful permanent resident alien.

Non-permanent resident aliens may be eligible for FHA financing as long as the property will be their primary residence, they have a valid social security number (with exceptions for those who are employed by the World Bank, a foreign embassy, or an equivalent employer as identified by HUD), they are eligible to work in the United States and they satisfy the same requirements, terms and conditions as those for US Citizens.

Non-US Citizens without lawful residency in the United States are NOT eligible for FHA insured financing.

Eligible Borrowers Ineligible Borrowers

US Citizens Permanent Resident Aliens Non-Permanent Resident Aliens

Foreign Nationals Partnerships Corporations

Finance of America Mortgage FHA Training Workbook 2016

33 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

CREDIT CREDIT SCORES

• Finance of America’s minimum credit score on all FHA Loans is 640 • Minimum Credit Score 640 (regardless of AUS findings) • All borrowers must have a credit score

CREDIT REQUIREMENTS

• All borrowers must have at least one valid credit score. • Credit will be closely examined over past 12 – 24 months, with greater emphasis on

past 12 months. • Borrower’s housing payment history is very important. • Student loans deferred over 12 months are considered.

o The Mortgagee must include all Student Loans in the Borrower’s liabilities, regardless of the payment type or status of payments.

o If the payment used for the monthly obligation is: less than 1 percent of the outstanding balance reported on the

Borrower’s credit report, and less than the monthly payment reported on the Borrower’s credit report;

o The Mortgagee must obtain written documentation of the actual monthly payment, the payment status, and evidence of the outstanding balance and terms from the creditor.

o Regardless of the payment status, the Mortgagee must use either: the greater of:

• 1 percent of the outstanding balance on the loan; or • the monthly payment reported on the Borrower’s credit report;

or • the actual documented payment, provided the payment will fully

amortize the loan over its term • Payoff of Debt to Qualify

o Is allowed if the account is paid in full prior to closing, with a credit supplement showing a zero balance.

o Gift funds for deb payoff is acceptable. • Open 30-day charge accounts, require balance to be paid in full each month. If assets

to cover unpaid balance in addition to funds needed to close transaction, and are verified and submitted to AUS, the debt may be excluded. If sufficient assets are not verified, entire balance is included in ratios.

Finance of America Mortgage FHA Training Workbook 2016

34 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

MORTGAGE CREDIT REJECT When a Mortgage Credit Reject is in existence:

• Must be addressed on the 92900-LT and included in the loan file • May not be deleted or disregarded • Second Signature from Lender management is required

If a Mortgage Credit Reject exists on a previous Case Number Assignment for the borrower, a credit alert/warning will be noted on the current case number assignment. The Mortgage Credit Reject must also be addressed as described above. NON-TRADITIONAL CREDIT REPORTS Non-traditional Mortgage Credit Reports are not allowed. CREDIT EVALUATION CAIVRS

• All Borrower’s need to be checked through FHA’s CAIVRs system • The system checks for delinquent federal debt • Any issues will need to be cleared • FAM will access CAIVRS through the FHAC • This is informational only to you as a sponsored broker • Must be ordered on all borrowers • Any delinquency must be cleared, or not eligible for FHA loan • Should a delinquency or issued be uncovered by FAM you will be promptly notified

NON-PURCHASING SPOUSE’S CREDIT MUST BE PULLED SEPARATELY, IN COMMUNITY PROPERTY STATES

• Credit score is not to be considered, but • Debts will be considered in payments/monthly obligation • Negative credit that may impact title on subject property, may be required to be paid

Verify previous/current housing obligations Follow AUS, or for manually underwritten loans the following applies:

• Rental verification: Credit report, management service or 12 months cancelled checks.

• Mortgage Verification Credit Report, Verification of Mortgage or 12 months cancelled checks.

Finance of America Mortgage FHA Training Workbook 2016

35 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

CONSUMER CREDIT COUNSELING

• Acceptable with 12 months’ payments made on time • Need approval of CCC organization

LATE PAYMENTS AND DELINQUENT CREDIT ITEMS Any mortgage tradeline, including lines of credit, during the most recent 12 months consisting of more than one 30 days late is considered.

MORTGAGE CREDIT REJECT

• Must be addressed on the 92900-LT • May not be deleted or disregarded • Second signature from FAM Management is required

COLLECTIONS, DISPUTED ACCOUNTS & JUDGMENTS The following guidance for Collections, Disputed Accounts and Judgments must be followed for all case numbers assigned BEFORE October 15, 2013: DISPUTED TRADELINES If a credit report reveals that the borrower is disputing any credit accounts, Manual Downgrade of a TOTAL Scorecard Approve/Accept recommendation to a Manual Underwrite is not required if:

NOTE: If the borrower has privately held mortgage, FAM will require 12 months cancelled checks. NOTE: if the borrower is renting from a private party FAM will require 12 months cancelled checks.

NOTE: If risk decision was accepted and the late payments and delinquent credit items appeared on the CR & considered by AUS, manual downgrading and further documentation are not required for manual underwrites, if any of the above items appeared on the CR, the loan is ineligible.

Finance of America Mortgage FHA Training Workbook 2016

36 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

The disputed account has a zero balance OR

• The disputed account is marked as "paid in full" or "resolved“ or • The disputed account is both: • less than $500 AND • More than 24 months old, based on the date of the dispute

COLLECTION ACCOUNTS AND JUDGMENTS

• Collections are not required to be paid off as a condition of the mortgage approval. • Court-ordered judgments must be paid off.

COLLECTIONS Collection accounts of a non-purchasing spouse in a community property state are included in the cumulative balance, unless excluded by state law. All medical collections and charge off accounts are excluded from this guidance and do not require resolution. A capacity analysis of collection accounts with an aggregate balance equal to or greater than $2,000 is required. Capacity analysis includes any of the following actions:

At the time of or prior to closing, payment in full of the collection account (verification of acceptable source of funds required).

• The borrower makes payment arrangements with the creditor. If the borrower has entered into a payment arrangement with the creditor, a credit report or letter from the creditor verifying the monthly payment is required. The monthly payment must be included in the borrower’s debt-to-income ratio.

• If evidence of a payment arrangement is not available, the Underwriter must calculate the monthly payment using 5% of the outstanding balance of each collection, and include the monthly payment in the borrower’s debt-to-income ratio.

Regardless of the Accept/Approve/Refer recommendation by TOTAL Mortgage Scorecard, the Underwriter must include the payment amount in the calculation of the borrower’s debt-to-income ratio.

NOTE: The following guidance for Collections, Disputed Accounts and Judgments must be followed for all case numbers assigned ON OR AFTER October 15, 2013.

Finance of America Mortgage FHA Training Workbook 2016

37 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

DOCUMENTATION REQUIREMENTS FOR MANUAL UNDERWRITE

• The Underwriter must document reasons for approving a mortgage when the borrower has collection accounts.

• Regardless of the amount of outstanding collection accounts, the Underwriter must determine if the collection account was a result of:

o The borrower’s disregard for financial obligations OR The borrower’s inability to manage debt OR Extenuating circumstances.

o The borrower must provide a letter of explanation with supporting documentation for each outstanding collection account. The explanation and supporting documentation must be consistent with other credit information in the file.

AUTOMATED (TOTAL) UNDERWRITE There are no documentation or letter of explanation requirements for loans with collection accounts run through TOTAL Mortgage Scorecard receiving an “Accept/Approve” despite the presence of collection accounts. These accounts have been already taken into consideration in the borrower’s credit score. If TOTAL Mortgage Scorecard generates a “Refer,” the lender must manually underwrite the loan in accordance with the guidance above applicable to manually underwritten loans with collection accounts. DISPUTED ACCOUNTS Disputed derogatory credit accounts are defined as follows: Disputed charge-off accounts, Disputed collection accounts, and Disputed accounts with late payments in the last 24 months DISPUTED DEROGATORY ACCOUNTS INDICATED ON THE CREDIT REPORT If the credit report utilized by TOTAL Mortgage Scorecard indicates that the borrower is disputing derogatory credit accounts, the borrower must provide a letter of explanation and documentation supporting the basis of the dispute. The lender must analyze the documentation provided for consistency with other credit information in the file to determine if the derogatory credit account should be considered in the underwriting analysis. GUIDANCE FOR TOTAL MORTGAGE SCORECARD ACCEPT/APPROVE LOANS WITH DISPUTED ACCOUNTS Disputed Derogatory Credit Accounts greater than or equal to $1,000: If the cumulative outstanding balance of disputed derogatory credit accounts of all borrowers is equal to or greater than $1,000, the mortgage application must be downgraded to a “Refer” and a DE underwriter is required to manually underwrite the loan as described above.

Disputed Derogatory Credit Accounts less than $1,000: If the cumulative outstanding balance of disputed derogatory credit accounts of all borrowers is less than $1,000, a downgrade is not required.

Finance of America Mortgage FHA Training Workbook 2016

38 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

Excluded Accounts: Disputed medical accounts are excluded from the $1,000 limit and do not require documentation, Disputed derogatory credit accounts resulting from identity theft, credit card theft, or unauthorized use are also excluded from the $1,000 limit. However, the lender must provide in the case binder a credit report, letter from the creditor, or other appropriate documentation to support the dispute, such as a police report disputing the fraudulent charges

NON-DEROGATORY DISPUTED ACCOUNTS AND DISPUTED ACCOUNTS NOT INDICATED ON THE CREDIT REPORT

Non-derogatory disputed accounts include the following types of accounts: Disputed accounts with zero balance, disputed accounts with late payments aged 24 months or greater, and Disputed accounts that are current and paid as agreed.

If a borrower is disputing non-derogatory accounts, or is disputing accounts which are not indicated on the credit report as being disputed, the lender is not required to downgrade the application to a “Refer.” However, the lender must analyze the effect of the disputed accounts on the borrower’s ability to repay the loan. If the dispute results in the borrower’s monthly debt payments utilized in computing the debt-to-income ratio being less than the amount indicated on the credit report, the borrower must provide documentation of the lower payments.

NON-DEROGATORY DISPUTED ACCOUNTS ARE EXCLUDED FROM THE $1,000 CUMULATIVE TOTAL Disputed derogatory credit accounts of a non-purchasing spouse in a community property state are not included in the cumulative balance for determining if the mortgage application is downgraded to a “Refer”. JUDGMENTS Judgments must be paid off. An exception to the payoff of a court ordered judgment may be made if the borrower has an agreement with the creditor to make regular and timely payments. The borrower must provide a copy of the agreement and evidence that payments were made on time in accordance with the agreement, and a minimum of three months of scheduled payments have been made prior to credit approval.

Borrowers are not allowed to prepay scheduled payments in order to meet the required minimum of three months of payments. Furthermore, lenders are instructed to include the payment amount in the agreement in the calculation of the borrower’s debt-to-income ratio.

FHA requires judgments of a non-purchasing spouse in a community property state to be paid in full, or meet the exception guidance for judgments above, unless excluded by state law.

Finance of America Mortgage FHA Training Workbook 2016

39 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

DOCUMENTATION REQUIREMENTS

Manual Underwrite: The Underwriter must document reasons for approving a mortgage when the borrower has judgments.

Regardless of the amount of outstanding judgments, the Underwriter must determine if the collection account or judgment was a result of:

• The borrower’s disregard for financial obligations OR • The borrower’s inability to manage debt OR • Extenuating circumstances

The borrower must provide a letter of explanation with supporting documentation for each outstanding judgment. The explanation and supporting documentation must be consistent with other credit information in the file.

Automated (TOTAL) Underwrite: If TOTAL Mortgage Scorecard generates a “Refer,” the lender must manually underwrite the loan in accordance with the guidance above applicable to manually underwritten loans with collection accounts and judgments.

SHORT SALE Borrower is not eligible if short sale on previous residence was to:

• Take advantage of declining market conditions, and • Purchase similar or superior property within a reasonable commuting distance at a

reduced price as compared to current market value.

Borrower current at time of short sale is considered eligible for a new FHA mortgage if, from the date of application:

• All mortgage payments on the prior mortgage were made within the month due for the 12 months preceding the short sale AND

• Installment debt payments for the same time period were on time

Borrower in default at time of short sale:

• Not eligible for 3 years from the date of the pre-foreclosure sale • Exceptions may be made to the three years for isolated cases only • Default was due to circumstances beyond the borrower’s control AND • Credit was satisfactory prior to the circumstances that led to default • Loans with borrowers in default must be manually underwritten

SEASONING REQUIREMENTS FOR SHORT SALE Seasoning requirements for short sales may only be waived if all lien holders have accepted the short sale as payment in full. There can be no deficiency balance nor can any portion of any lien be converted to consumer debt.

If the short sale was greater than 3 years prior to the date of the application and AUS is an Accept, no need to manual downgrade.

Finance of America Mortgage FHA Training Workbook 2016

40 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

The credit report must reflect a zero balance on mortgage liens included in the short sale OR documentation must be obtained to support no further obligation.

BANKRUPTCY Credit report must accurately reflect bankruptcy with the correct code, or the loan must be downgraded to a manual underwrite. The code is commonly a 7 (CoreLogic, Credco and Old Republic), but may vary depending on the credit vendor. If the loan does not meet manual guidelines, the report must be corrected and the loan re-run through the AUS.

The 1003 Loan Application must reflect a “yes” response to the bankruptcy question if the borrower filed within the past 7 years.

AUS Findings must be reviewed to determine if finding is present for the BK. If not present, but credit report and 1003 reflects the BK accurately, an assumption may be made the BK was correctly read by the AUS. However, when the finding is present, but the code is not accurate, it cannot be assumed that the BK was correctly read by the AUS.

Chapter 7 must have been discharged for at least 2 years, if less, an exception may be made if over 12 months, and reason was due to documented extenuation circumstances.

Chapter 13 acceptable with minimum 12 payments made on time, and court approval for new financing.

High Balance Cash Out Transactions – no BK in past 7 years.

FORECLOSURE/DEED IN LIEU Generally, 3 years must have elapsed to qualify for a new home loan.

FORECLOSURE

• High Balance Cash Out, no foreclosures in past 7 years • Foreclosures with Accept from AUS, and greater than 3 years prior to the date of the

loan application do not require manual downgrade. • Credit Report must reflect zero balance on mortgage liens, OR documentation must be

obtained to support no further obligation. • Credit report must reflect the correct code for AUS to read foreclosure accurately, or

the loan will require a manual downgrade. The code is generally an 8 (CoreLogic, Credco and Old Republic), but may vary depending on the credit vendor. If the loan does not meet manual underwriting guidelines, the credit report must be corrected and the loan must be re-run through AUS.

• 1003 Loan Application must reflect a “yes” response to the foreclosure question. • AUS Findings must be reviewed to determine if a finding is present for foreclosure. If

not present, but the credit report and the 1003 reflect the foreclosure accurately, an assumption may be made that the foreclosure was correctly read by the AUS. In cases where the finding is present but the code is not accurate, it cannot be assumed that the foreclosure was correctly read by the AUS.

Finance of America Mortgage FHA Training Workbook 2016

41 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

INCOME CALCULATING THE BORROWER'S EFFECTIVE INCOME To be able to use a borrower’s income in the ratio calculations, it must be considered “effective”, which means it is likely to continue for at least the first three years of the mortgage, and is income that is verifiable and stable. As with other loan programs, FHA insured loans will look back at the borrower’s previous two-year employment and income history to determine whether their income is stable and likely to continue. Lenders are required to document the borrower’s income and employment history, verify the accuracy of the amounts of income being reported, and determine if the income can be considered Effective Income in accordance with FHA underwriting guidelines. Generally, income may not be used in calculating the borrower’s ratios if it comes from any source that cannot be verified, is not stable or will not continue.

Only income that is legally derived, and if required, properly claimed on the borrower’s tax returns can be considered Effective Income.

EMPLOYMENT HISTORY FHA does not require a minimum length of time that a borrower must have held a position of employment; however, the lender must document and verify the borrower’s employment for the most recent two full years. The borrower must explain any gaps in employment that span one month or more.

If a borrower indicates he or she was in school or in the military during the previous two years, and therefore not working, the borrower must provide evidence supporting this such as college transcripts or discharge papers.

FREQUENT JOB CHANGES Borrowers with frequent job changes generally may be demonstrating a lack of stability. If a borrower has changed jobs more than 3 times in the previous 12 months, or has changed lines of work, the lender must take additional steps to document that the borrower’s income is stable. The lender must obtain:

• Transcripts of training and education demonstrating qualification for the new position, or

• Employment documentation evidencing continual increases in income and/or benefits

Also, large swings or changes in income will also lead an underwriter to question the stability of the income. A borrower who changes jobs frequently within the same line of work, but

Finance of America Mortgage FHA Training Workbook 2016

42 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

continues to advance in income or benefits should not be penalized for those job changes, provided he or she has held steady employment without gaps. GAPS IN EMPLOYMENT For borrowers with a gap in employment of six months or longer, the borrower’s current income can be used as Effective Income if it can be documented that the borrower has been at their current job for at least 6 months, and a two-year work history prior to the gap in employment can be documented. CALCULATING EFFECTIVE INCOME Salary and Hourly Income: In calculating Effective Income, the underwriter will use the base salary of the borrower, as long as the income has been and will likely continue to be earned consistently. The underwriter will also look at the prior two years of W-2 to analyze the stability of the current income. If earnings are similar or increasing at a normal rate, they will use the current base income as the borrower’s Effective Income. When determining Effective Income of a borrower paid hourly, if the hours do not vary, the hourly rate will be used as Effective Income. If the hours vary, a two-year average of earnings will be used. If the hours vary and there is a documented increase in the borrower’s pay rate, a 12-month average of hours at the current rate of pay is used to determine Effective Income. Overtime and Bonus Income: Overtime and Bonus income may be used to qualify if the borrower has received the income for the past two years and it is likely to continue. Overtime and Bonus income received over a period of between one and two years may be acceptable if it has been consistently earned for at least one year and it is reasonably likely to continue. In the event that Overtime or Bonus income has declined from the previous year by 20% or more, the current year’s income must be used. The higher income from the previous year cannot be averaged in to boost the Overtime or Bonus income calculation. Part-Time Income: Part-time Employment refers to employment that is not the borrower’s primary employment and is generally performed for less than 40 hours per week. Income from part time employment can be used as Effective Income if the borrower has worked the part time job uninterrupted for the past two years and the current position is likely to continue. The Underwriter will average the income over the previous two years. If there is a documentable increase in the borrower’s rate of pay, the lender can use a 12-month average of hours at the current rate of pay. This means that if the borrower worked 20 hours a week for the first ten months of the year at a rate of $9.00 per hour, but received a pay raise to $11.00 two months ago and still works 20 hours, the income used to qualify would be the average hours worked (20) at $11.00 per hour.

Finance of America Mortgage FHA Training Workbook 2016

43 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

Seasonal Income: Seasonal employment is not year round, regardless of the number of hours per week the borrower works on the job. Income from seasonal employment can be counted as Effective Income, provided the borrower has worked in the same line of work for the previous two years and is reasonable likely to be rehired for the next season. Unemployment compensation can be included in Effective Income calculations for those with Effective income from seasonal employment. Effective Income for borrowers with seasonal employment is calculated by averaging the income over the previous two-year period. Disability Income: Disability Benefits can be received from the Social Security Administration, Department of Veterans Affairs, other public agencies, or a private disability insurance provider. Borrowers must provide documentation verifying the receipt of benefits from the provider. Disability income may be used as Effective Income, provided it will continue for the first three years of the mortgage. If the Award’s documentation does not have a defined expiration date, the lender can consider the income as likely to continue. Under no circumstances may the lender inquire into or request documentation concerning the nature of the disability or the medical condition of the borrower. The lender must use the most recent amount of benefits received to calculate Effective Income. Alimony, Child Support or Maintenance Income: Alimony, Child Support and Maintenance Income refers to income received from a former spouse or partner or from a non-custodial parent of the borrower’s minor dependent children. If listed in a final divorce decree, legal separation agreement or court order, and the borrower has received Alimony, Child Support or Maintenance Income consistently for the previous three months, the lender may use the current payment when calculating the borrower’s Effective Income. If the borrower has a voluntary payment agreement (not court ordered or listed in a legal document), the borrower must provide documentation showing receipt of the payments consistently over the previous six months in order for the payment to be used in calculating Effective Income. If the borrower cannot document consistent receipt of the income for the most recent six months, an average of the income received over the previous two years can be used to calculate Effective Income. If the income has been received for less than two years, an average of the income received over the time of receipt can be used.

Finance of America Mortgage FHA Training Workbook 2016

44 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

Government Assistance Programs: Income received under a welfare program, unemployment income, workman's compensation, payments for foster children, etc., is acceptable subject to documentation from the paying agency provided the income is expected to continue at least three years. New Job: For those borrowers about to start a new job, if the borrower has a guaranteed, non-revocable contract for the new employment that will begin within 60 days of loan closing, the income is acceptable for qualifying purposes. The lender must also verify the borrower will have sufficient income or cash reserves to support the mortgage payments and any other obligations during the interim between loan closing and the start of employment. (This may be appropriate for situations such as a teacher whose contract begins with the new school year, or a physician beginning residency after the loan is scheduled to close.) Employment in Family-Owned Businesses: Borrowers employed by businesses owned by family members are required to provide additional income documentation. These borrowers must provide the normal verification of employment and pay stubs, and also provide evidence that he or she is not an owner of the business. This may include copies of the borrower's signed personal tax returns or a signed copy of the corporate tax return showing ownership percentages. Self-Employment Income: A borrower with a 25% or greater ownership interest in a business is considered self-employed for mortgage financing purposes. Income from self-employment is considered Effective Income if the borrower has been self-employed for two years or more. For borrowers with less than two years’ self-employment, the following guidelines apply:

1. Between one and two years: Must have at least two years’ previous successful employment in that or a related occupation to be counted as Effective Income.

2. Less than one year: The income derived from self-employment may not be used as Effective Income.

If income from Self-employment is derived from a business with a greater than 20% decline in income over the analysis period, that income may not be considered Effective Income unless it can be documented that the decline in income was due to extenuating circumstances, And That the Income Has Been Stable or Increasing for The Previous 12 Months.

Commission Income: A borrower’s income is considered to be commission when he or she is paid contingent upon the conducting of a business transaction or the performance of a service. Commission income can be used as Effective Income when it has been earned for at least one year in the same or a similar line of work and it is reasonable likely to continue. Commission income is calculated by using the lesser the average net commission income earned over the previous two years or the average net commission income earned over the

Finance of America Mortgage FHA Training Workbook 2016

45 | P a g e

©2016 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Ver 2016.10.1

previous one year. Unreimbursed business expenses are to be subtracted from the gross commission income, thereby reducing the Effective Income. Rental Income: FHA considers rental income to be income received or to be received from the subject property or other real estate holdings. Rent received for properties owned by the borrower can be used as income to qualify if the lender can document that the rental income is stable. Net rental income is added to the borrower’s gross income – the borrower’s total mortgage payment is NOT reduced by the net subject property rental income. Net rental income is calculated by using the lesser of 75% of fair market rent reported by the appraiser, or 75% of the rent reflected in the lease or rental agreement. Gross rent is reduced by 25% to account for vacancies and maintenance to the property. If the borrower resides in one or more units of a multiple-unit property and charges rent to tenants of other units, that rent may be used for qualifying purposes. However, projected rent of only the additional units (not the owner-occupied unit) may be considered, and only after deducting the 25% of the gross rent to account for vacancies and maintenance to the property. Again, this may not be used as a direct offset to the mortgage payments. Net rental income is calculated by averaging the amounts listed on Schedule E of the borrower’s tax returns. Depreciation, which is a paper loss and not an actual loss, may be added back in to the net income or loss. Positive net rental income is added to the borrower’s Effective Income. Should there be a loss or negative net rental income, it is listed in the borrower’s liability. If a borrower is vacating a property and intends to hold it as a rental property and buy another property, there are guidelines about counting the rental income as Effective Income for qualification. This income may be counted when:

• The borrower is relocating the new residence is located at least 100 miles from the previous residence

• If the borrower does not have a history of rental income since the last tax filing, they must have at least 25% equity in the property. This would be proven by an appraisal; however, this appraisal does NOT need to be completed by an FHA Appraiser.