Embed Size (px)

Citation preview

Feedstock Challenges and Innovative Routes to

Feedstock

6th Indian Oil Petrochemical Conclave – 2017

Balasubramaniam Ramani, Senior Consultant,

ICIS Analytics & Consulting

1

2

Agenda

ICIS Consulting

Context Setting

• Ethylene Feedstock sources & recent developments

• Propylene Feedstock sources & recent developments

Global Petrochemical feedstock scenario & outlook

• Ethylene Feedstock sources

• Propylene Feedstock sources

• Supply-Demand Gap

• Potential future options for India

Indian Petrochemical feedstock scenario & outlook

Conclusion

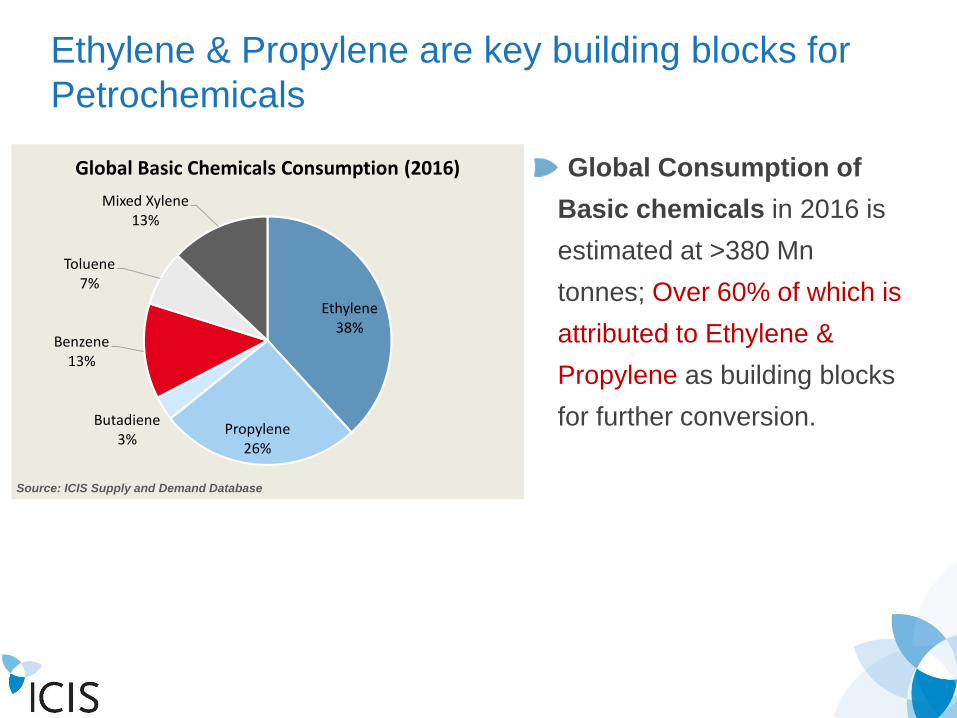

Ethylene & Propylene are key building blocks for

Petrochemicals

Global Consumption of

Basic chemicals in 2016 is

estimated at >380 Mn

tonnes; Over 60% of which is

attributed to Ethylene &

Propylene as building blocks

for further conversion.

Ethylene38%

Propylene26%

Butadiene3%

Benzene13%

Toluene7%

Mixed Xylene13%

Global Basic Chemicals Consumption (2016)

Source: ICIS Supply and Demand Database

4

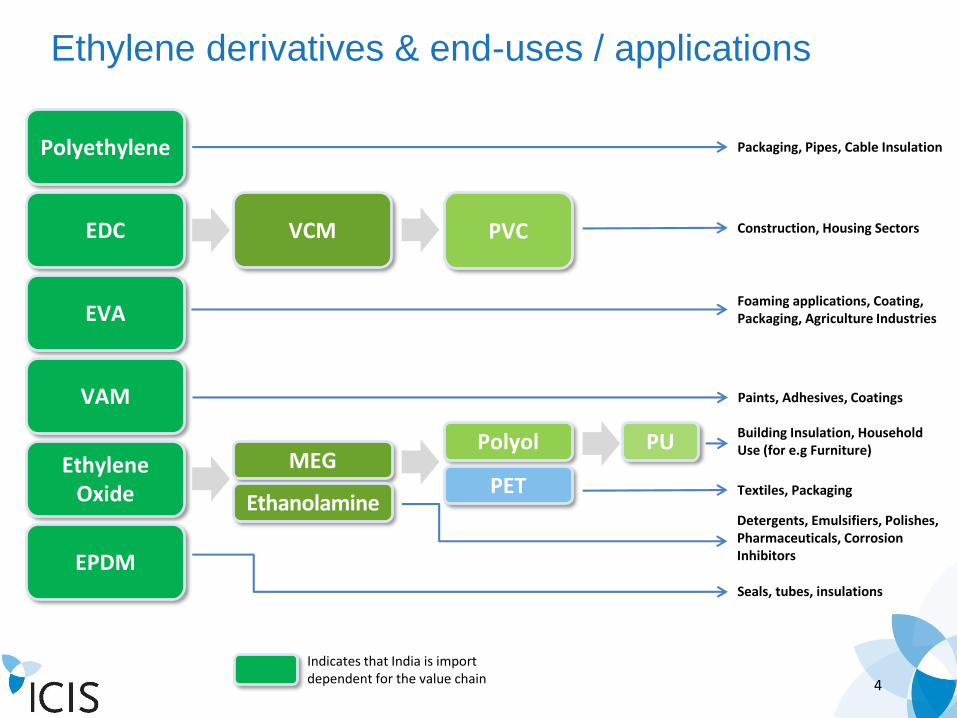

Ethylene derivatives & end-uses / applications

Polyethylene

EDC

EVA

VAM

Ethylene Oxide

EPDM

Packaging, Pipes, Cable Insulation

VCM PVC Construction, Housing Sectors

Foaming applications, Coating, Packaging, Agriculture Industries

Paints, Adhesives, Coatings

MEG

Ethanolamine

Polyol

PET

PUBuilding Insulation, Household Use (for e.g Furniture)

Textiles, Packaging

Detergents, Emulsifiers, Polishes, Pharmaceuticals, Corrosion Inhibitors

Seals, tubes, insulations

Indicates that India is import dependent for the value chain

5

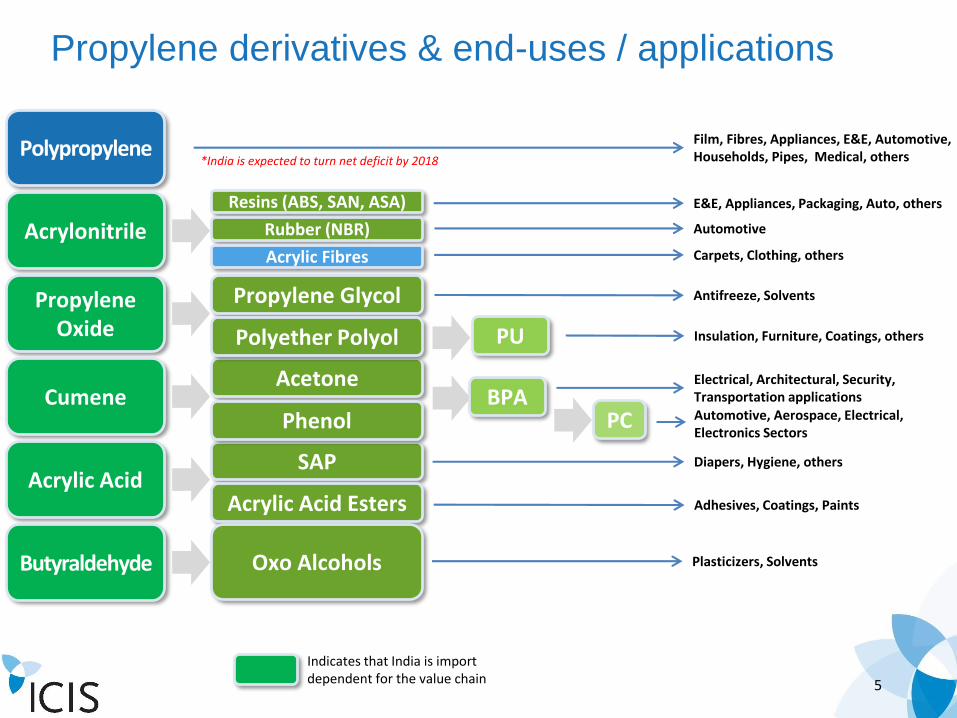

Polypropylene

Acrylonitrile

Propylene Oxide

Cumene

Acrylic Acid

Butyraldehyde

Resins (ABS, SAN, ASA)

Propylene Glycol

Acetone

Rubber (NBR)

Acrylic Fibres

SAP

Acrylic Acid Esters

Oxo Alcohols

Film, Fibres, Appliances, E&E, Automotive, Households, Pipes, Medical, others

E&E, Appliances, Packaging, Auto, others

Automotive

Carpets, Clothing, others

Antifreeze, Solvents

Insulation, Furniture, Coatings, others

Diapers, Hygiene, others

Adhesives, Coatings, Paints

Plasticizers, Solvents

Propylene derivatives & end-uses / applications

Polyether Polyol PU

PhenolBPA

PC

Electrical, Architectural, Security, Transportation applicationsAutomotive, Aerospace, Electrical, Electronics Sectors

Indicates that India is import dependent for the value chain

*India is expected to turn net deficit by 2018

6

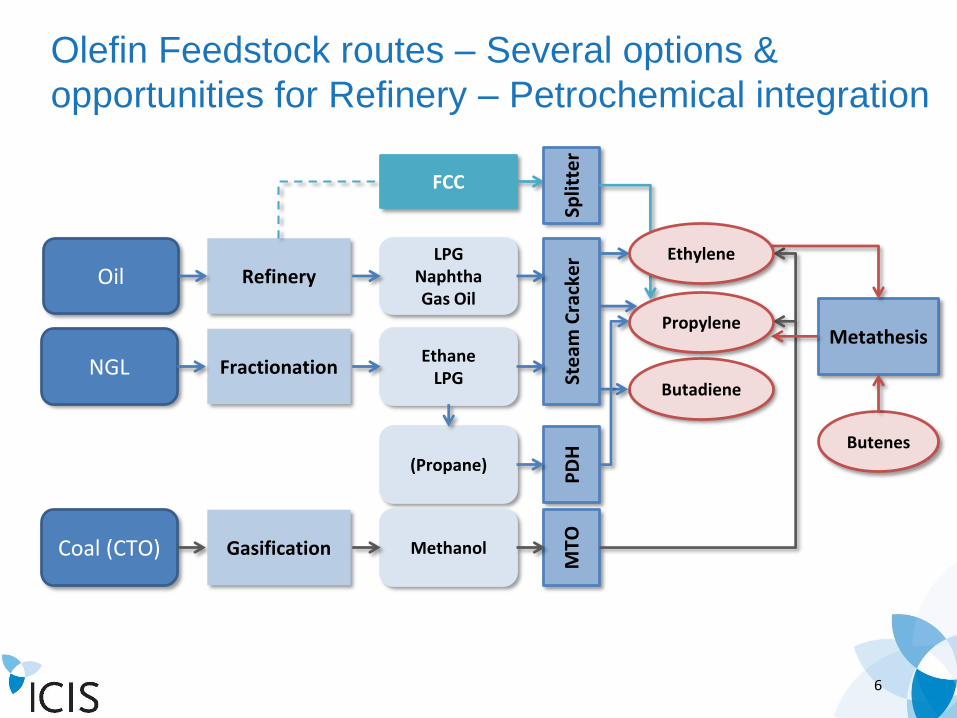

Olefin Feedstock routes – Several options &

opportunities for Refinery – Petrochemical integration

NGL

Oil

Coal (CTO)

RefineryLPG

NaphthaGas Oil

FractionationEthane

LPG Ste

am C

rack

er

PD

H

(Propane)

MTO

Butadiene

Metathesis

Butenes

Gasification Methanol

FCC

Split

ter

Ethylene

Propylene

7

Agenda

ICIS Consulting

Context Setting

• Ethylene Feedstock sources & recent developments

• Propylene Feedstock sources & recent developments

Global Petrochemical feedstock scenario & outlook

• Ethylene Feedstock sources

• Propylene Feedstock sources

• Supply-Demand Gap

• Potential future options for India

Indian Petrochemical feedstock scenario & outlook

Conclusion

8

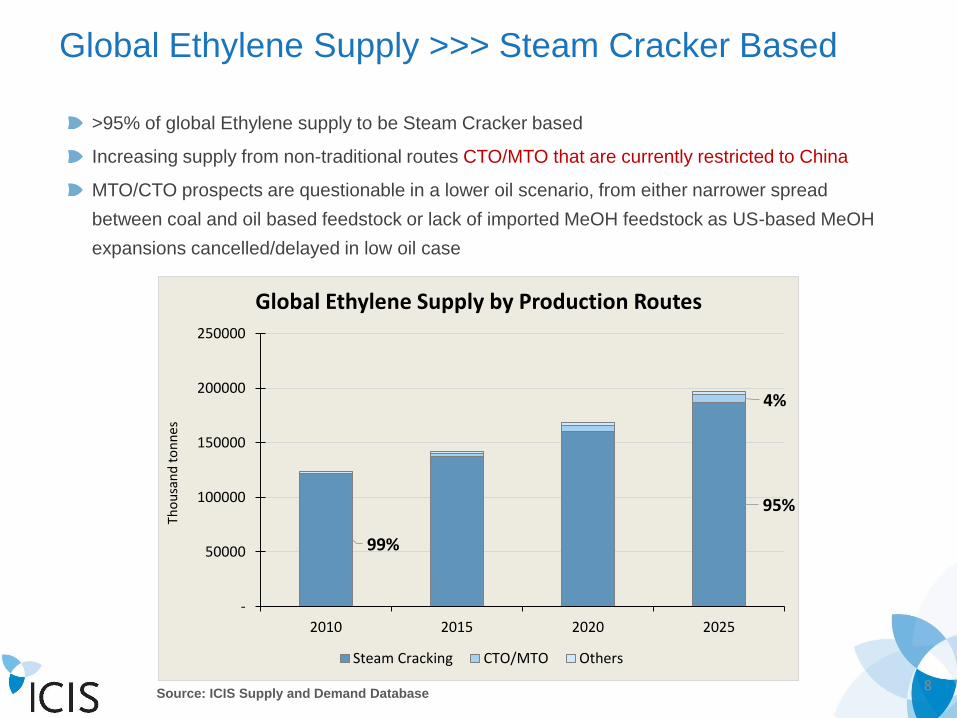

Global Ethylene Supply >>> Steam Cracker Based

Source: ICIS Supply and Demand Database

99%

95%

4%

-

50000

100000

150000

200000

250000

2010 2015 2020 2025

Tho

usa

nd

to

nn

es

Global Ethylene Supply by Production Routes

Steam Cracking CTO/MTO Others

>95% of global Ethylene supply to be Steam Cracker based

Increasing supply from non-traditional routes CTO/MTO that are currently restricted to China

MTO/CTO prospects are questionable in a lower oil scenario, from either narrower spread

between coal and oil based feedstock or lack of imported MeOH feedstock as US-based MeOH

expansions cancelled/delayed in low oil case

9

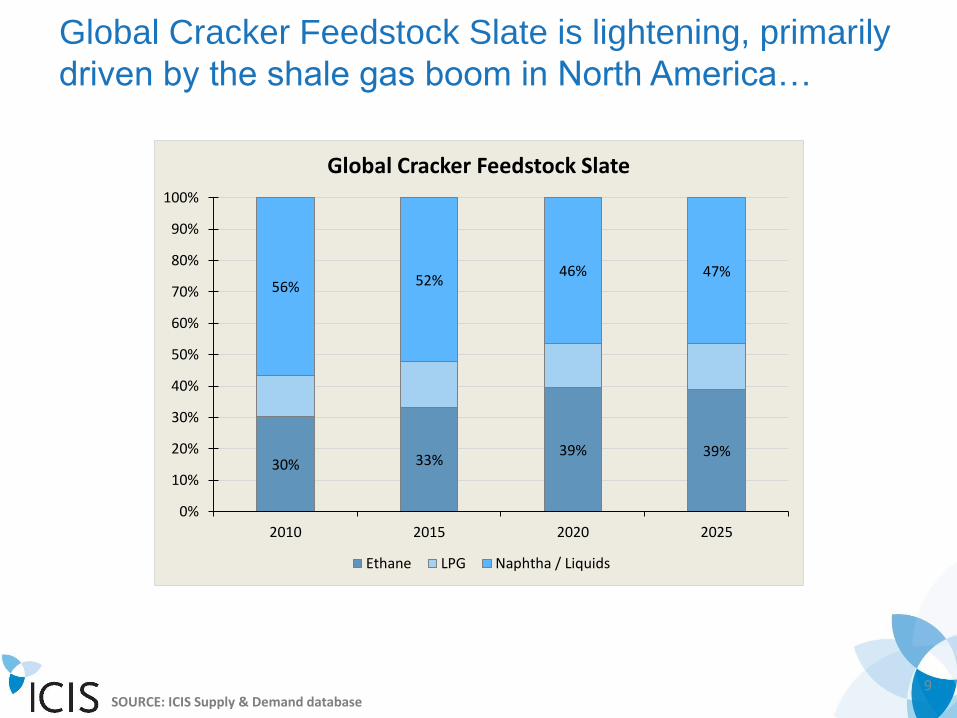

Global Cracker Feedstock Slate is lightening, primarily

driven by the shale gas boom in North America…

SOURCE: ICIS Supply & Demand database

30% 33%39% 39%

56% 52%46% 47%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2015 2020 2025

Global Cracker Feedstock Slate

Ethane LPG Naphtha / Liquids

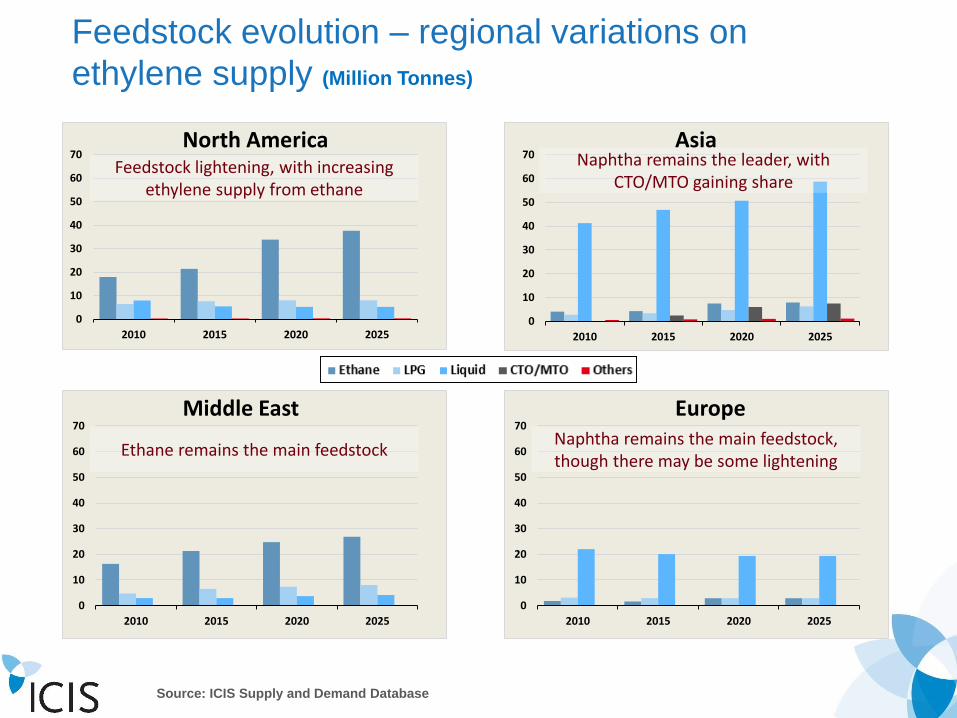

Feedstock evolution – regional variations on

ethylene supply (Million Tonnes)

0

10

20

30

40

50

60

70

2010 2015 2020 2025

North America

0

10

20

30

40

50

60

70

2010 2015 2020 2025

Asia

0

10

20

30

40

50

60

70

2010 2015 2020 2025

Middle East

Source: ICIS Supply and Demand Database

0

10

20

30

40

50

60

70

2010 2015 2020 2025

Europe

Feedstock lightening, with increasing ethylene supply from ethane

Naphtha remains the leader, with CTO/MTO gaining share

Ethane remains the main feedstockNaphtha remains the main feedstock, though there may be some lightening

11

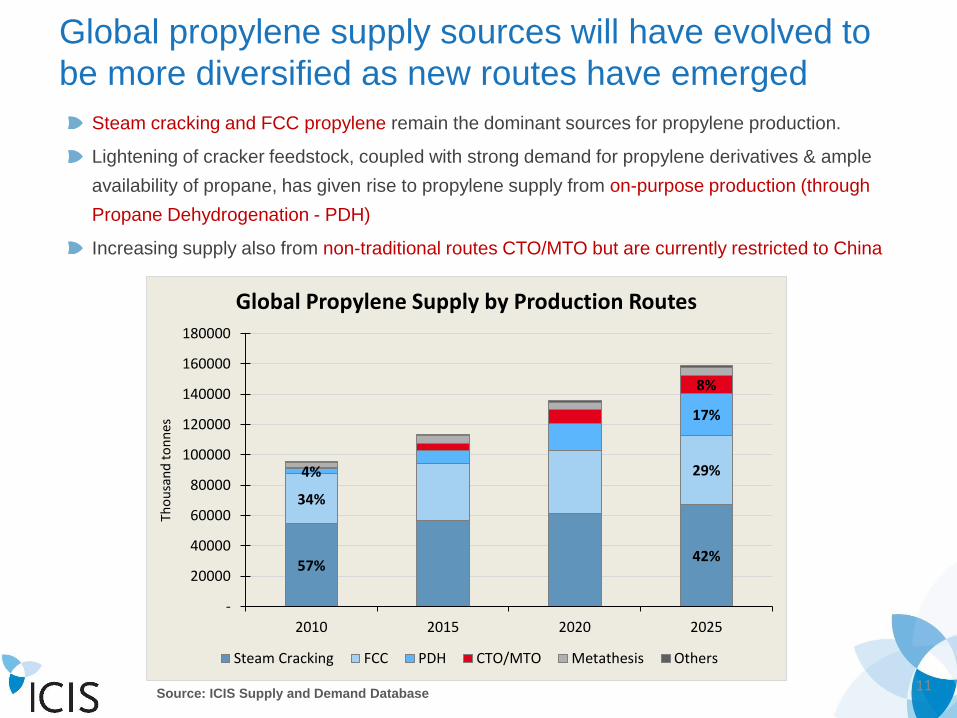

Global propylene supply sources will have evolved to

be more diversified as new routes have emerged

Source: ICIS Supply and Demand Database

Steam cracking and FCC propylene remain the dominant sources for propylene production.

Lightening of cracker feedstock, coupled with strong demand for propylene derivatives & ample

availability of propane, has given rise to propylene supply from on-purpose production (through

Propane Dehydrogenation - PDH)

Increasing supply also from non-traditional routes CTO/MTO but are currently restricted to China

57%42%

34%

29%4%

17%

8%

-

20000

40000

60000

80000

100000

120000

140000

160000

180000

2010 2015 2020 2025

Tho

usa

nd

to

nn

es

Global Propylene Supply by Production Routes

Steam Cracking FCC PDH CTO/MTO Metathesis Others

Source: ICIS Supply and Demand Database

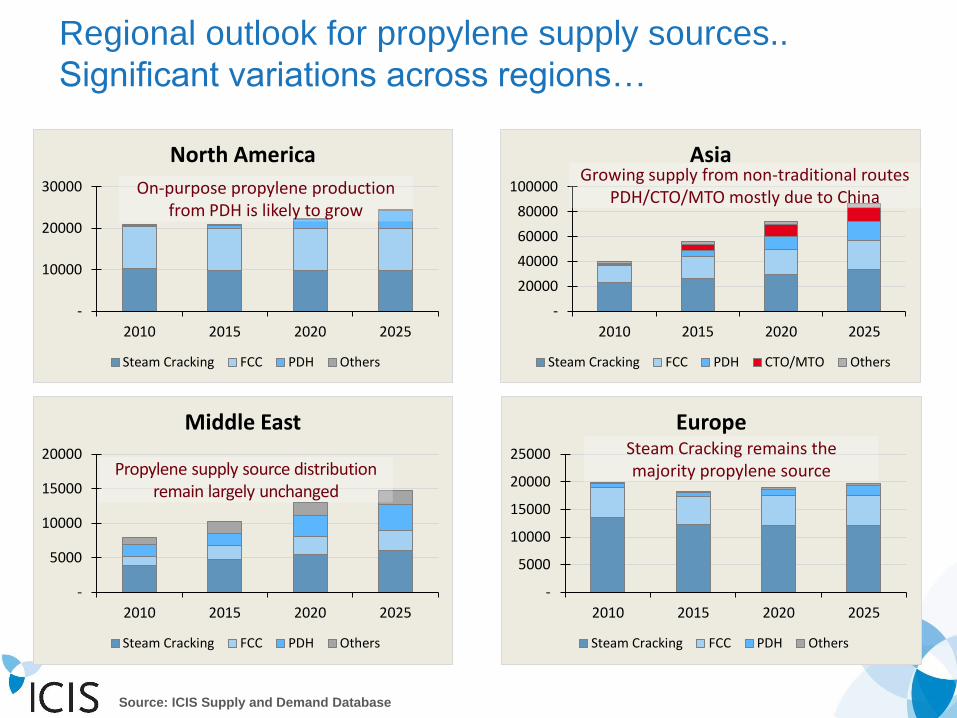

Regional outlook for propylene supply sources..

Significant variations across regions…

-

10000

20000

30000

2010 2015 2020 2025

North America

Steam Cracking FCC PDH Others

-

5000

10000

15000

20000

2010 2015 2020 2025

Middle East

Steam Cracking FCC PDH Others

-

5000

10000

15000

20000

25000

2010 2015 2020 2025

Europe

Steam Cracking FCC PDH Others

-

20000

40000

60000

80000

100000

2010 2015 2020 2025

Asia

Steam Cracking FCC PDH CTO/MTO Others

Growing supply from non-traditional routes PDH/CTO/MTO mostly due to ChinaOn-purpose propylene production

from PDH is likely to grow

Steam Cracking remains the majority propylene sourcePropylene supply source distribution

remain largely unchanged

13

Agenda

ICIS Consulting

Context Setting

• Ethylene Feedstock sources & recent developments

• Propylene Feedstock sources & recent developments

Global Petrochemical feedstock scenario & outlook

• Ethylene Feedstock sources

• Propylene Feedstock sources

• Supply-Demand Gap

• Potential future options for India

Indian Petrochemical feedstock scenario & outlook

Conclusion

14

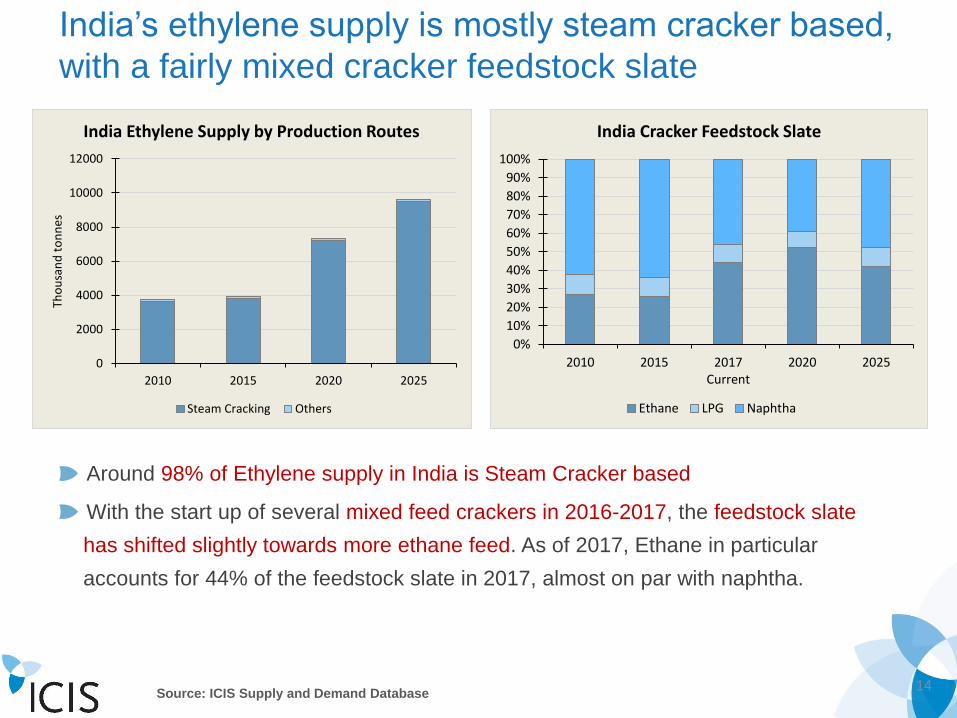

India’s ethylene supply is mostly steam cracker based,

with a fairly mixed cracker feedstock slate

Source: ICIS Supply and Demand Database

Around 98% of Ethylene supply in India is Steam Cracker based

With the start up of several mixed feed crackers in 2016-2017, the feedstock slate

has shifted slightly towards more ethane feed. As of 2017, Ethane in particular

accounts for 44% of the feedstock slate in 2017, almost on par with naphtha.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2015 2017Current

2020 2025

India Cracker Feedstock Slate

Ethane LPG Naphtha

0

2000

4000

6000

8000

10000

12000

2010 2015 2020 2025

Tho

usa

nd

to

nn

es

India Ethylene Supply by Production Routes

Steam Cracking Others

15

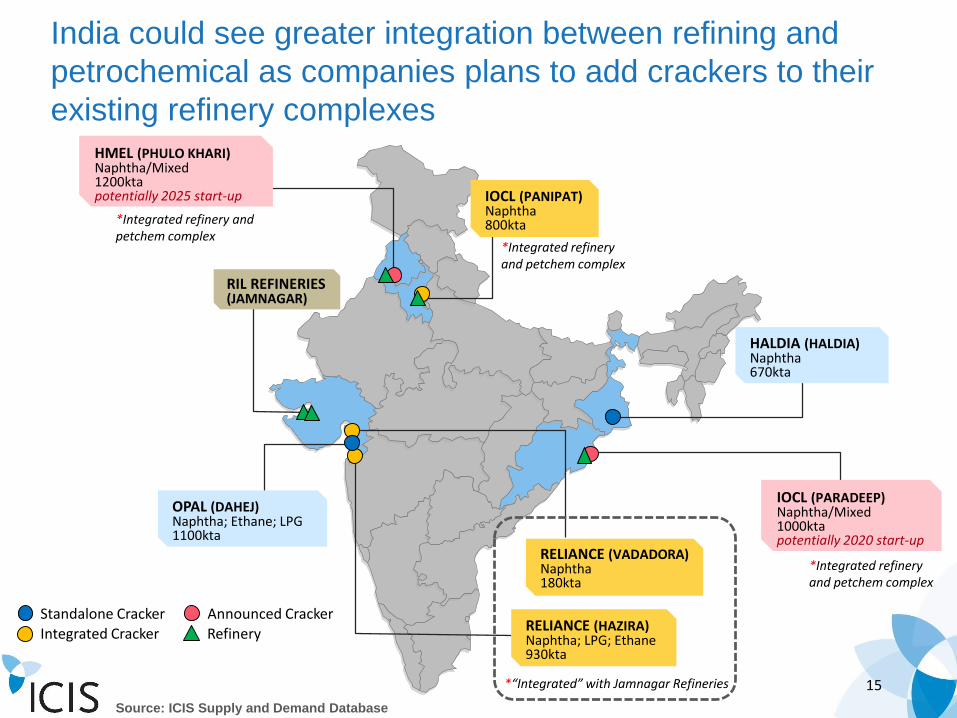

India could see greater integration between refining and

petrochemical as companies plans to add crackers to their

existing refinery complexes

RELIANCE (HAZIRA)Naphtha; LPG; Ethane930kta

RELIANCE (VADADORA)Naphtha180kta

*“Integrated” with Jamnagar Refineries

IOCL (PANIPAT)Naphtha800kta

*Integrated refinery and petchem complex

RIL REFINERIES (JAMNAGAR)

HALDIA (HALDIA)Naphtha670kta

Integrated Cracker RefineryStandalone Cracker Announced Cracker

IOCL (PARADEEP)Naphtha/Mixed1000ktapotentially 2020 start-up

HMEL (PHULO KHARI)Naphtha/Mixed1200ktapotentially 2025 start-up

*Integrated refinery and petchem complex

*Integrated refinery and petchem complex

OPAL (DAHEJ)Naphtha; Ethane; LPG1100kta

Source: ICIS Supply and Demand Database

16

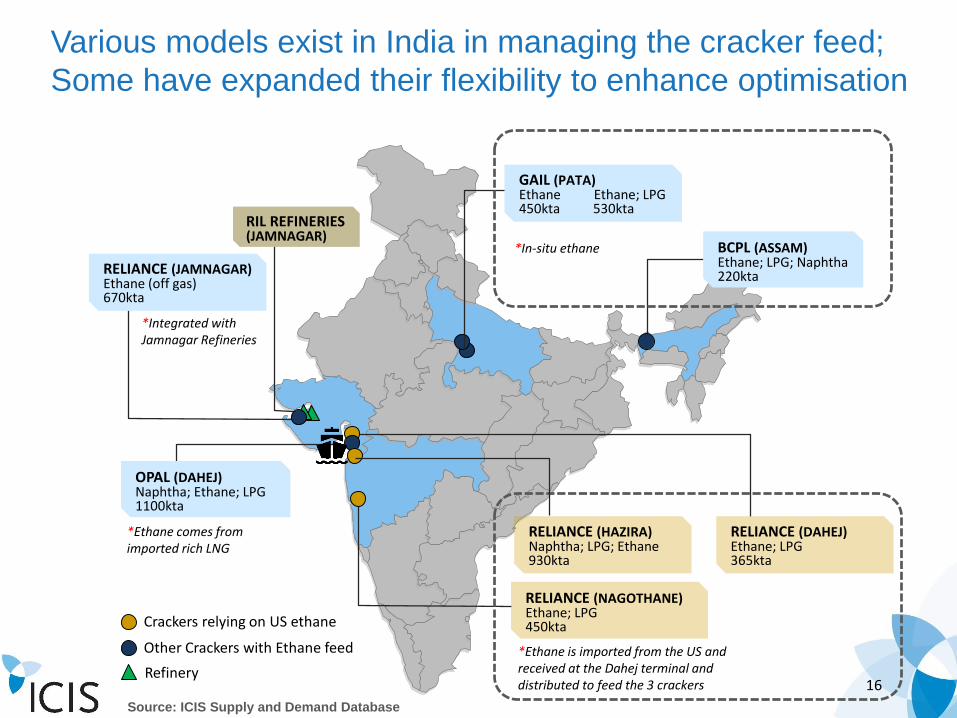

Various models exist in India in managing the cracker feed;

Some have expanded their flexibility to enhance optimisation

RELIANCE (NAGOTHANE)Ethane; LPG450kta

RELIANCE (DAHEJ)Ethane; LPG365kta

RIL REFINERIES (JAMNAGAR)

BCPL (ASSAM)Ethane; LPG; Naphtha220kta

GAIL (PATA)Ethane Ethane; LPG 450kta 530kta

RELIANCE (JAMNAGAR)Ethane (off gas)670kta

*Integrated with Jamnagar Refineries

*Ethane is imported from the US and received at the Dahej terminal and distributed to feed the 3 crackers

*In-situ ethane

*Ethane comes from imported rich LNG

RELIANCE (HAZIRA)Naphtha; LPG; Ethane930kta

OPAL (DAHEJ)Naphtha; Ethane; LPG1100kta

Crackers relying on US ethane

Refinery

Other Crackers with Ethane feed

Source: ICIS Supply and Demand Database

17

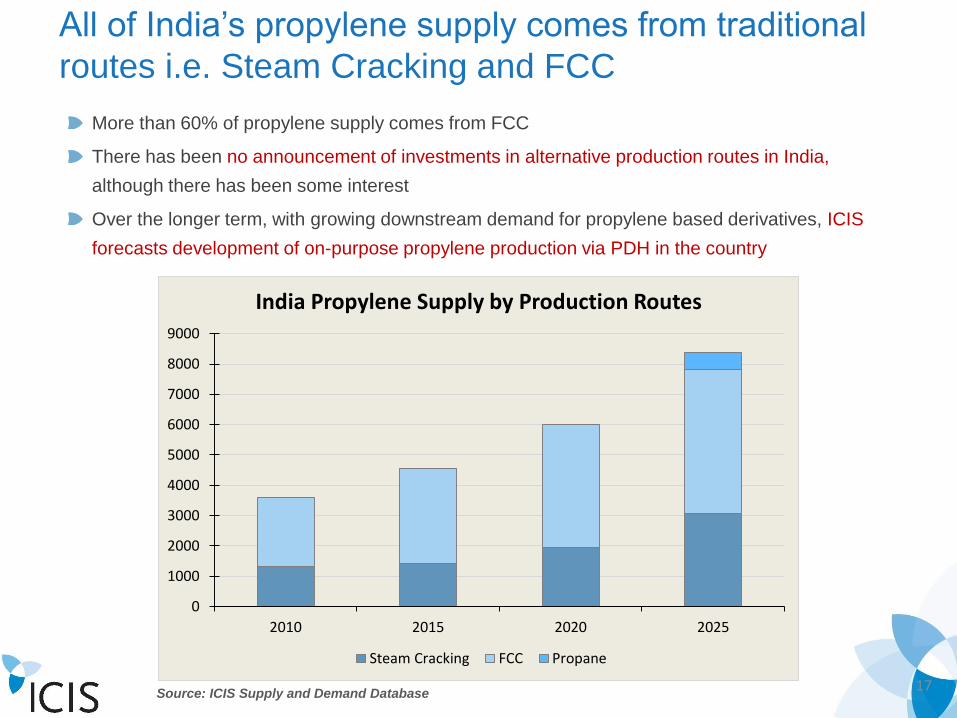

All of India’s propylene supply comes from traditional

routes i.e. Steam Cracking and FCC

Source: ICIS Supply and Demand Database

More than 60% of propylene supply comes from FCC

There has been no announcement of investments in alternative production routes in India,

although there has been some interest

Over the longer term, with growing downstream demand for propylene based derivatives, ICIS

forecasts development of on-purpose propylene production via PDH in the country

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2010 2015 2020 2025

India Propylene Supply by Production Routes

Steam Cracking FCC Propane

18

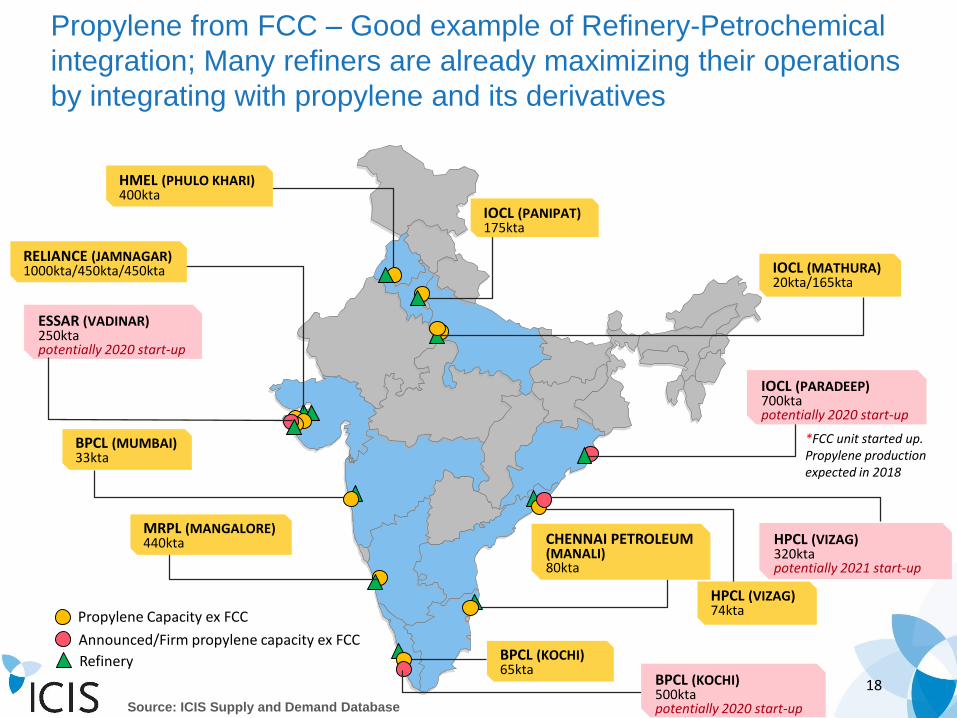

IOCL (PANIPAT)175kta

HMEL (PHULO KHARI)400kta

Propylene from FCC – Good example of Refinery-Petrochemical

integration; Many refiners are already maximizing their operations

by integrating with propylene and its derivatives

BPCL (KOCHI)65kta

BPCL (MUMBAI)33kta

CHENNAI PETROLEUM (MANALI)80kta

IOCL (MATHURA)20kta/165kta

MRPL (MANGALORE)440kta

RELIANCE (JAMNAGAR)1000kta/450kta/450kta

IOCL (PARADEEP)700ktapotentially 2020 start-up

Propylene Capacity ex FCC

Refinery

Announced/Firm propylene capacity ex FCC

*FCC unit started up. Propylene production expected in 2018

ESSAR (VADINAR)250ktapotentially 2020 start-up

HPCL (VIZAG)74kta

HPCL (VIZAG)320ktapotentially 2021 start-up

BPCL (KOCHI)500ktapotentially 2020 start-upSource: ICIS Supply and Demand Database

19

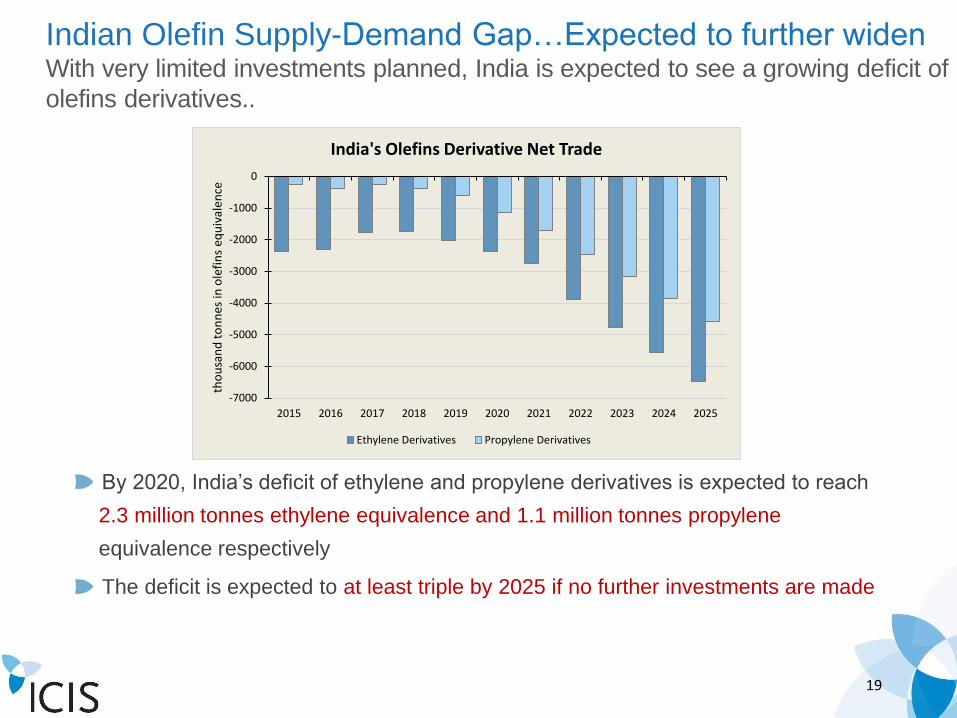

Indian Olefin Supply-Demand Gap…Expected to further widenWith very limited investments planned, India is expected to see a growing deficit of

olefins derivatives..

By 2020, India’s deficit of ethylene and propylene derivatives is expected to reach

2.3 million tonnes ethylene equivalence and 1.1 million tonnes propylene

equivalence respectively

The deficit is expected to at least triple by 2025 if no further investments are made

-7000

-6000

-5000

-4000

-3000

-2000

-1000

0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

tho

usa

nd

to

nn

es in

ole

fin

s eq

uiv

alen

ce

India's Olefins Derivative Net Trade

Ethylene Derivatives Propylene Derivatives

20

Indian Olefin Supply-Demand Gap…Expected to further widenWith very limited investments planned, India is expected to see a growing deficit of

olefins derivatives..

Investment OPPORTUNITIES remain untapped…But what options could India explore to fill this gap?

• Steam Cracking – Naphtha / Mixed feed?• Propane Dehydrogenation (PDH)?• Methanol to Olefin (MTO)?• Coal to Olefin (CTO)?

Could India be more competitive than China for these new business / feedstock models?

21

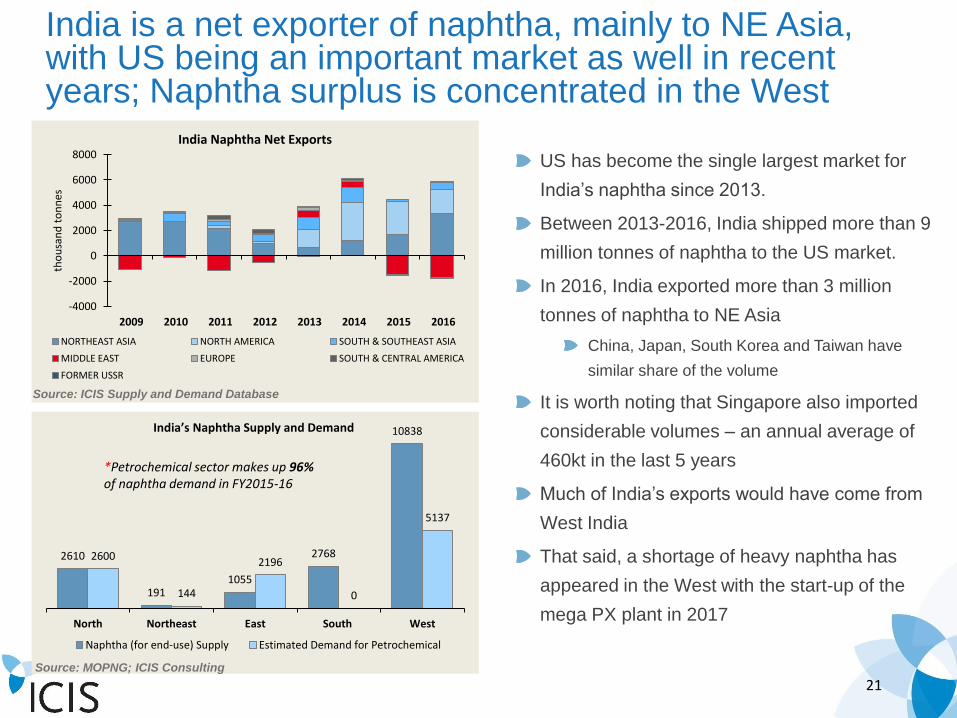

India is a net exporter of naphtha, mainly to NE Asia, with US being an important market as well in recent years; Naphtha surplus is concentrated in the West

US has become the single largest market for

India’s naphtha since 2013.

Between 2013-2016, India shipped more than 9

million tonnes of naphtha to the US market.

In 2016, India exported more than 3 million

tonnes of naphtha to NE Asia

China, Japan, South Korea and Taiwan have

similar share of the volume

It is worth noting that Singapore also imported

considerable volumes – an annual average of

460kt in the last 5 years

Much of India’s exports would have come from

West India

That said, a shortage of heavy naphtha has

appeared in the West with the start-up of the

mega PX plant in 2017

2610

1911055

2768

10838

2600

144

2196

0

5137

North Northeast East South West

India’s Naphtha Supply and Demand

Naphtha (for end-use) Supply Estimated Demand for Petrochemical

*Petrochemical sector makes up 96%of naphtha demand in FY2015-16

Source: MOPNG; ICIS Consulting

-4000

-2000

0

2000

4000

6000

8000

2009 2010 2011 2012 2013 2014 2015 2016

tho

usa

nd

to

nn

es

India Naphtha Net Exports

NORTHEAST ASIA NORTH AMERICA SOUTH & SOUTHEAST ASIA

MIDDLE EAST EUROPE SOUTH & CENTRAL AMERICA

FORMER USSR

Source: ICIS Supply and Demand Database

22

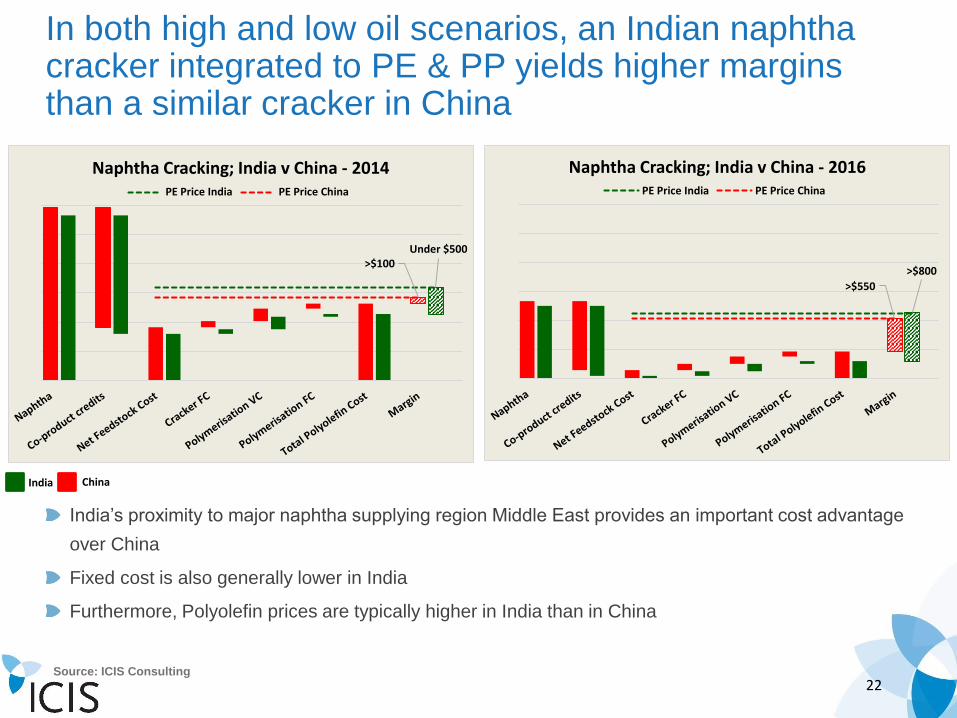

In both high and low oil scenarios, an Indian naphtha cracker integrated to PE & PP yields higher margins than a similar cracker in China

India’s proximity to major naphtha supplying region Middle East provides an important cost advantage

over China

Fixed cost is also generally lower in India

Furthermore, Polyolefin prices are typically higher in India than in China

Source: ICIS Consulting

>$100Under $500

Naphtha Cracking; India v China - 2014PE Price India PE Price China

>$550

>$800

Naphtha Cracking; India v China - 2016PE Price India PE Price China

India China

23

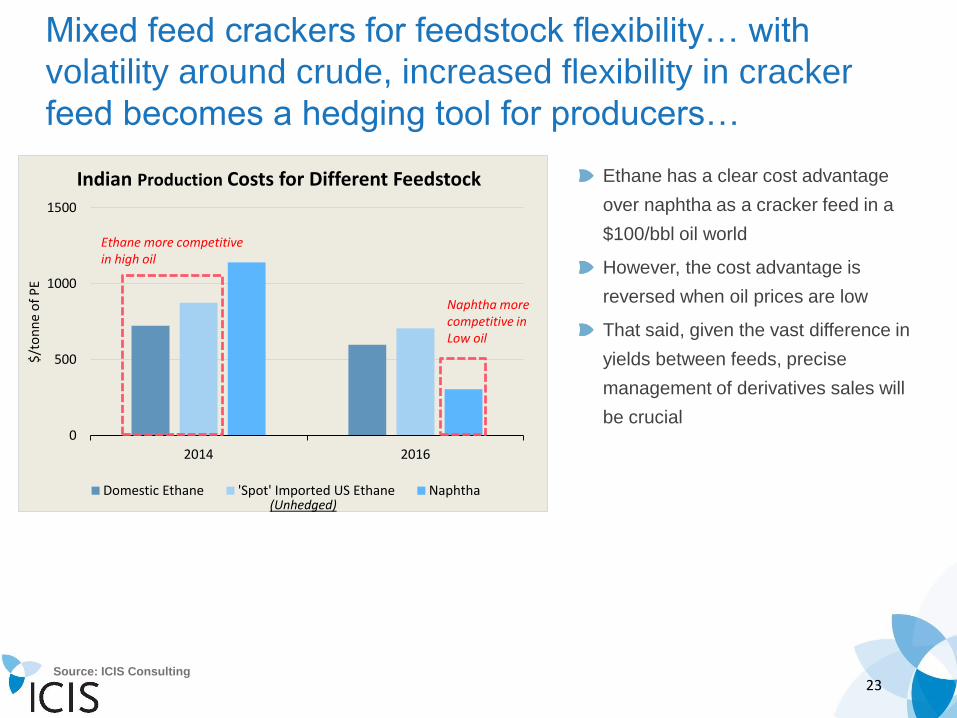

Mixed feed crackers for feedstock flexibility… with

volatility around crude, increased flexibility in cracker

feed becomes a hedging tool for producers…

Ethane has a clear cost advantage

over naphtha as a cracker feed in a

$100/bbl oil world

However, the cost advantage is

reversed when oil prices are low

That said, given the vast difference in

yields between feeds, precise

management of derivatives sales will

be crucial

Source: ICIS Consulting

0

500

1000

1500

2014 2016

$/t

on

ne

of

PE

Indian Production Costs for Different Feedstock

Domestic Ethane 'Spot' Imported US Ethane Naphtha

Ethane more competitive in high oil

Naphtha more competitive in Low oil

(Unhedged)

24

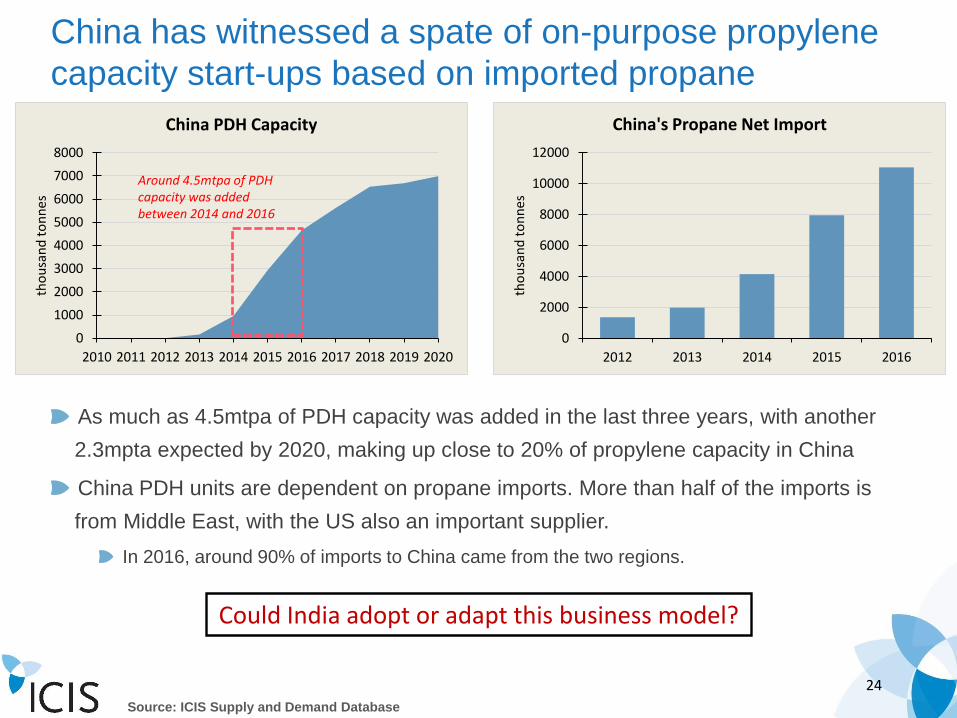

China has witnessed a spate of on-purpose propylene

capacity start-ups based on imported propane

As much as 4.5mtpa of PDH capacity was added in the last three years, with another

2.3mpta expected by 2020, making up close to 20% of propylene capacity in China

China PDH units are dependent on propane imports. More than half of the imports is

from Middle East, with the US also an important supplier.

In 2016, around 90% of imports to China came from the two regions.

0

1000

2000

3000

4000

5000

6000

7000

8000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

tho

usa

nd

to

nn

es

China PDH Capacity

Around 4.5mtpa of PDH capacity was added between 2014 and 2016

0

2000

4000

6000

8000

10000

12000

2012 2013 2014 2015 2016

tho

usa

nd

to

nn

es

China's Propane Net Import

Source: ICIS Supply and Demand Database

Could India adopt or adapt this business model?

25

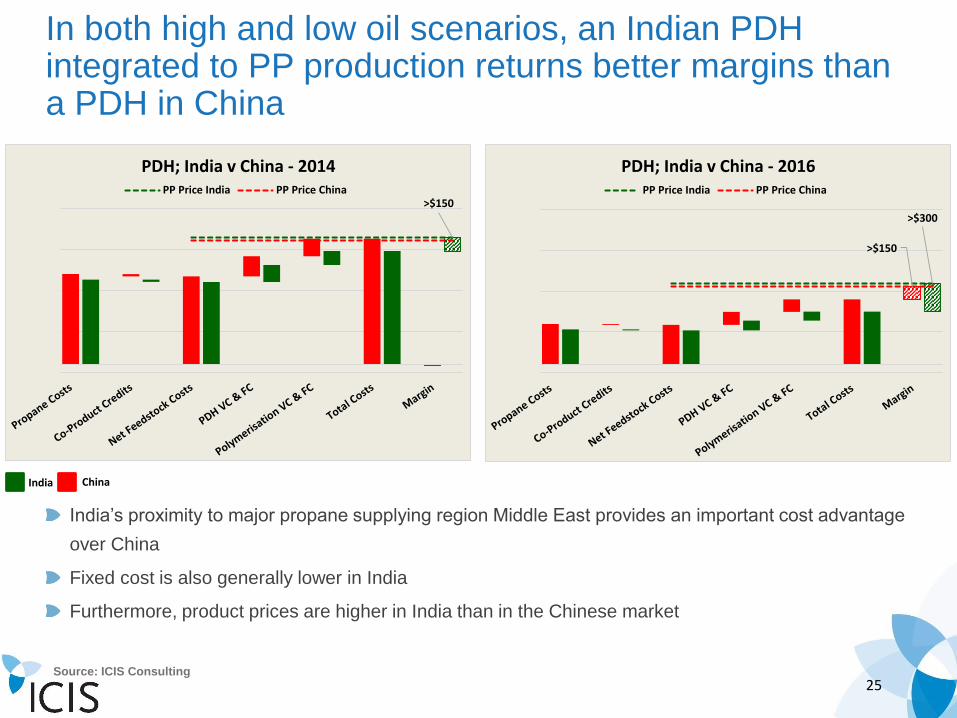

In both high and low oil scenarios, an Indian PDH integrated to PP production returns better margins than a PDH in China

India’s proximity to major propane supplying region Middle East provides an important cost advantage

over China

Fixed cost is also generally lower in India

Furthermore, product prices are higher in India than in the Chinese market

Source: ICIS Consulting

>$150

PDH; India v China - 2014PP Price India PP Price China

>$150

>$300

PDH; India v China - 2016PP Price India PP Price China

India China

26

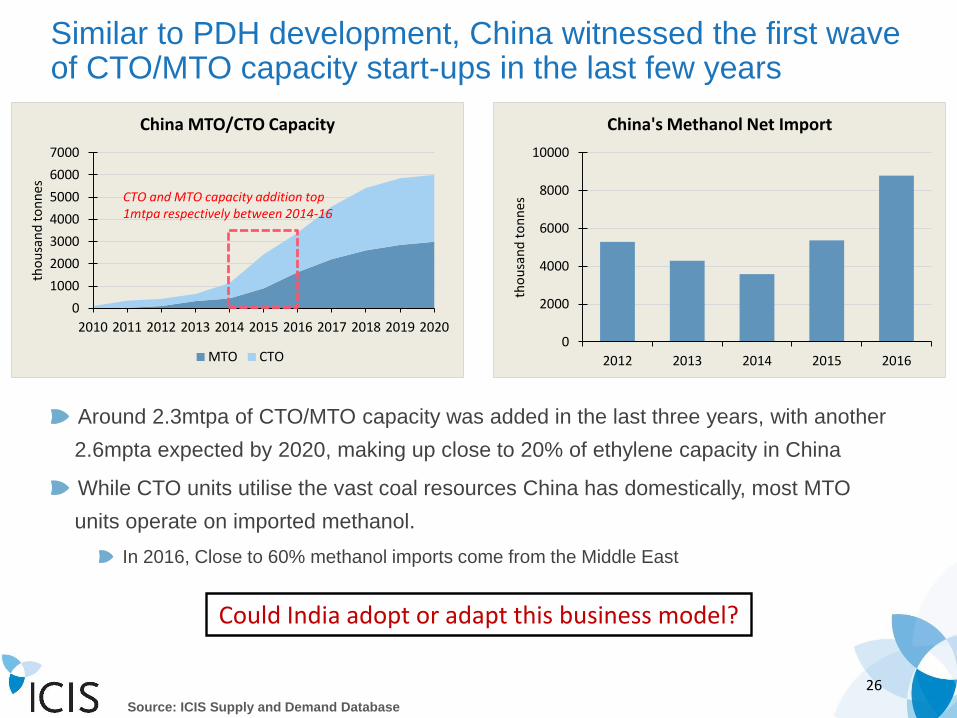

Similar to PDH development, China witnessed the first wave of CTO/MTO capacity start-ups in the last few years

Around 2.3mtpa of CTO/MTO capacity was added in the last three years, with another

2.6mpta expected by 2020, making up close to 20% of ethylene capacity in China

While CTO units utilise the vast coal resources China has domestically, most MTO

units operate on imported methanol.

In 2016, Close to 60% methanol imports come from the Middle East

Source: ICIS Supply and Demand Database

Could India adopt or adapt this business model?

0

1000

2000

3000

4000

5000

6000

7000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

tho

usa

nd

to

nn

es

China MTO/CTO Capacity

MTO CTO

CTO and MTO capacity addition top 1mtpa respectively between 2014-16

0

2000

4000

6000

8000

10000

2012 2013 2014 2015 2016

tho

usa

nd

to

nn

es

China's Methanol Net Import

27

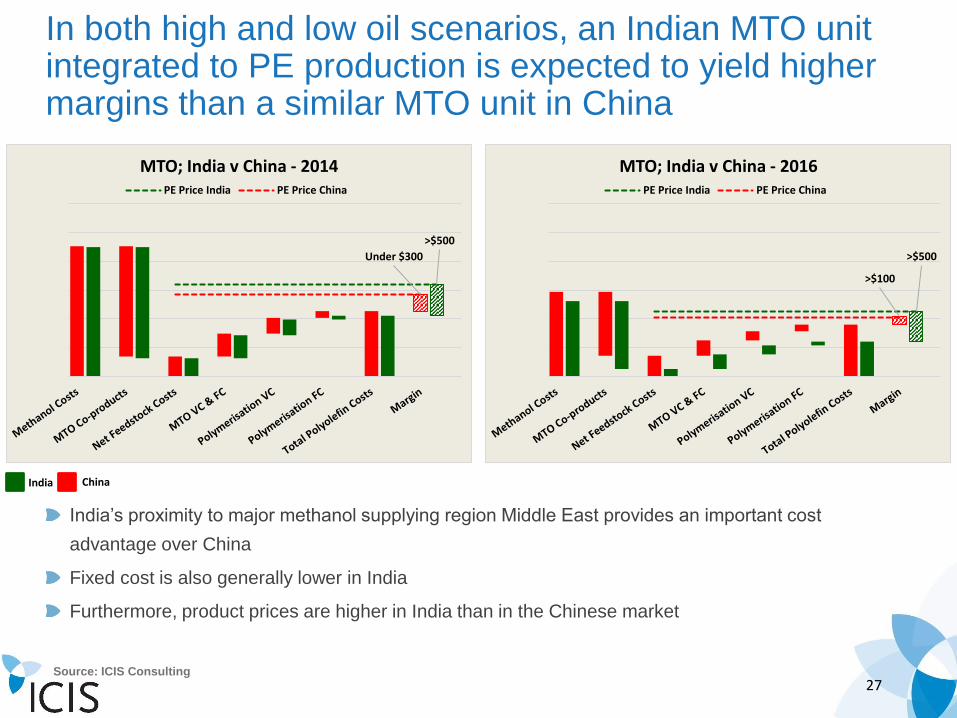

In both high and low oil scenarios, an Indian MTO unit integrated to PE production is expected to yield higher margins than a similar MTO unit in China

India’s proximity to major methanol supplying region Middle East provides an important cost

advantage over China

Fixed cost is also generally lower in India

Furthermore, product prices are higher in India than in the Chinese market

Source: ICIS Consulting

India China

Under $300

>$500

MTO; India v China - 2014PE Price India PE Price China

>$100

>$500

MTO; India v China - 2016PE Price India PE Price China

28

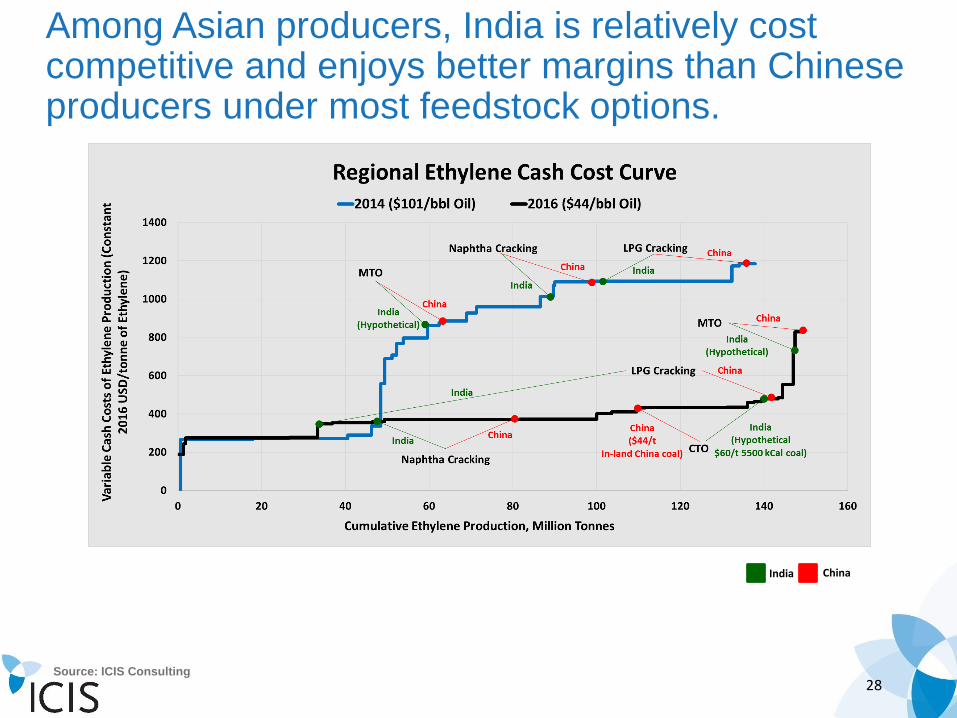

Among Asian producers, India is relatively cost competitive and enjoys better margins than Chinese producers under most feedstock options.

Source: ICIS Consulting

India China

29

Agenda

ICIS Consulting

Context Setting

• Ethylene Feedstock sources & recent developments

• Propylene Feedstock sources & recent developments

Global Petrochemical feedstock scenario & outlook

• Ethylene Feedstock sources

• Propylene Feedstock sources

• Supply-Demand Gap

• Potential future options for India

Indian Petrochemical feedstock scenario & outlook

Conclusion

30

Conclusion

Strong demand fundamentals shall drive future investments in India

Refinery-Petrochemical integration will further enhance competitiveness for

Indian producers

Traditional steam cracking shall remain evergreen

Mixed feed crackers allow for feedstock flexibility

Well diversified business model due to better product mix

Competitiveness further enhanced in the Low-oil environment prevailing

However, huge CAPEX involved

Investments into Non-traditional business modes will also be required

PDH based cluster to facilitate downstream investment into Propylene

derivatives

MTO project based on merchant methanol from Middle east with potential

Back-integration to Methanol in Middle east in future

CTO project based on imported / domestic coal