Embed Size (px)

Citation preview

FATCA CHANGES IN 2015/16 Fund boards may have considered FATCA all done and dusted in 2014/15 but 2015/16 sees the following significant changes:

1. All US investors are now reportable under US FATCA so funds who took advantage of the exemptions in 2014 will no

longer be able to do so.

2. All UK investors are also reportable for funds domiciled in the UK, crown dependencies and overseas territories such as

Gibraltar, Cayman and BVI under CDOT or “UK FATCA”.

3. Some entities that were exempt under US-FATCA will become reportable under the Common Reporting Standard (CRS)

and their classifications should be reviewed now.

4. Sponsored entities under FATCA will need to register in their own right under CRS

5. Investors domiciled outside of the CRS countries will become Passive NFFEs and must identify their UBOs.

A REMINDER OF FATCA

FATCA required all reportable funds to identify their US investors and report them to the local tax authority by mid 2015. This

broke down into four stages:

• Classification: Determine whether each entity in a fund structure required to register with the IRS and report on their investors. • Registration: Register each entity with the IRS and obtain a Global Intermediary ID number (GIIN). • Investigation: Update Due Diligence on each investor to determine whether they have a US connection and are therefore reportable. • Reporting: Report the US investors to the local tax authority of the fund by mid 2015.

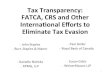

2016 CHANGES AND REQUIREMENTS

2016 sees the expansion of Tax Information Exchange to include UK FATCA and then a

further expansion in 2017 to the Common Reporting Standard. Reportable investors will

therefore include both US and UK persons for the calendar year ended 31/12/2015. By

2017 the 56 countries signed up to the Common Reporting Standard effectively make

almost all investors reportable.

Key dates:

31/05/2016 Reporting Deadline for UK funds

30/06/2016 Reporting Deadline for non-UK funds and Due Diligence deadline for all investors.

WHAT TO DO NOW

Fund managers should consider:

1. Can you effectively report all reportable investors in XML across all relevant jurisdictions?

2. Have you sufficient information to determine the reporting status of each investor and UBO where needed?

3. Have you reviewed the classification of each entity under CDOT and CRS?

56 Nations

UK

Investors

UK

Investors

US

Investors

US

Investors

US

Investors

2015 2016 2017

Reporting Due In