Embed Size (px)

Citation preview

Fastnet Oil & Gas Plc

Proactive Presentation Manchester 29.10.14

www.fastnetoilandgas.com 2

Disclaimer

This document is confidential and is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published in whole or in part, for any purpose. In particular, neither this document nor any copy of it (or any part of it) may be sent to or taken into the United States, Canada, Australia, Republic of South Africa or Japan (or any of their respective territories or possessions, or to any resident thereof or any other corporation, partnership or other such entity created or organised under the law thereof), nor may it be distributed to or for the account or on behalf of any US person (within the meaning of regulation S under the US Securities Act of 1933, as amended). The distribution of this presentation in other jurisdictions may also be restricted by law and persons into whose possession this presentation comes (or a copy hereof) should inform themselves about, and observe, any such restriction. Any failure to comply with these restrictions may constitute a violation of the laws of any such other jurisdiction.

This document does not constitute or form any part of any offer or invitation or other solicitation or recommendation to purchase any securities and contains information designed only to provide a broad overview for discussion purposes. As such, all information and research material provided herein is subject to change and this document does not purport to provide a complete description of the investment opportunity. All expressions of opinion are subject to change without notice and do not constitute advice and should not be relied upon. Fastnet Oil & Gas plc (the “Company”) does not undertake any obligation to update or revise the information in or contents of this document. Recipients of this document who may consider acquiring shares in the Company are reminded that any such acquisition should not be made on the basis of the information contained in this document.

This document is being distributed in the UK only to, and is directed only at persons who are: (i) investment professionals as defined in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) FPO 2005 (“the Promotion Order”); (ii) are persons of a kind described in Article 49(2) of the Promotion Order; (iii) are persons to whom this document may otherwise lawfully be issued or passed on and/or (iv) persons outside the United Kingdom (in accordance with any applicable legal requirements) (all such persons together being referred to as “Relevant Persons”). Any person who is not a Relevant Person should not act or rely on this presentation or any of its contents and any investment or investment activity to which it relates will only be available to Relevant Persons. Any person who is unsure of their position should seek independent advice. This communication is exempt from the financial promotion restriction in section 21 of the Financial Services and Markets Act 2000 (“FSMA”) on the basis that it is only directed at and being sent to the categories of investor described above. This communication has not been approved by a person authorised by the Financial Services Authority under FSMA.

This document is being distributed in Ireland only to and is directed only at persons who are “qualified investors” within the meaning of the Prospectus (Directive 2003/71/EC) Regulations 2005 of Ireland.

Neither the Company, nor its employees, advisers or representatives nor any other person makes any guarantee, representation, undertaking or warranty, express or implied as to the accuracy, completeness, correctness or fairness of the information and opinions contained in this document (or as to the reasonableness of any assumptions on which any of the same is based or the use of any of the same), nor does the Company nor its employees, advisers or representatives nor any other person accept any responsibility or liability whatsoever for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

The information set out herein may be subject to updating, completion, revision, verification and amendment and such information may change materially. If you rely on this communication to make an investment you may be exposed to a significant risk of losing all of your investment. This communication does not constitute either advice or a recommendation regarding any securities. Any person who is in any doubt about the subject matter of this communication should consult a duly authorised person specialising in advising on such investments.

This communication includes forward-looking statements. These forward-looking statements include all matters that are not historical facts, statements regarding the Company's intentions, beliefs or current expectations concerning, among other things, the Company's results of operations, financial condition, prospects, growth, strategies, and the industry in which the Company operates. By their nature, forward-looking statements involve risks and uncertainties. You are cautioned that forward-looking statements are not guarantees of future performance and that the Company's actual results of operations, financial condition and the development of the industry in which the Company operates may differ materially from those made in or suggested by the forward-looking statements contained in this communication. Past performance is not a guide to future performance.

Company Overview

Moroccan Assets

Irish Assets

Outlook

Company Overview

Irish Assets

Moroccan Assets

Outlook

www.fastnetoilandgas.com 4

Overview and Company Funding

• 25,053 sq. km. under licence onshore and offshore Morocco and offshore Ireland with 16 primary exploration and appraisal

prospects matured for drilling

• Cash balance USD 20 mm at 31 July 14

• Running costs – general and administration – USD 2.6 mm p.a

• Fully funded to meet all current licence phase commitments - monetisation through farm down and recovery of past costs

• Quality Partners – Kosmos Energy, BP, SK

• Celtic Sea farm out process well underway. Internal technical work continues to enhance value with completion of 3D

interpretation. Offers expected Q4.

• Tendrara Lakbir well planning on schedule. Farmout process ongoing.

• FA-1 well reached TD May 14, under budget. Numerous oil and gas shows encountered in well. FA-1 results have

significantly de-risked the Foum Assaka license area.

OVERVIEW

www.fastnetoilandgas.com 5

Business Model Health Check

ACQUIRE

• 25,053 sq. km. under licence and exclusive options

• New niche opportunities being reviewed in onshore East Africa

ANALYSE

• 1,910 sq. km. of 3D seismic acquired in Ireland

• 488 sq. km. of 3D seismic reprocessed onshore Morocco

• Up to 5,000 sq. km. of 3D seismic acquired/reprocessed offshore Morocco

FARM DOWN

• Foum Assaka farmed out to SK Innovation – carry in up to 2 wells plus back costs

• Total cost to Fastnet from licence acquisition to completion of the FA-1 well was USD 2.75m

• Celtic Sea and Tendrara Farmouts well underway – 9 front-runners

EXPLORE

• FA-1 first well tested the high risk, deepwater, acreage in the portfolio

• De-risked petroleum system – oil shows encountered, sand presence confirmed but thickness/quality remains issue

• Tendrara Lakbir well planning under way and on track

• Celtic Sea 3D Interpretation has defined and de-risked very large potential oil and gas prospects

MONETISE

• FA-1 encountered non-commercial hydrocarbons, derisked elements of petroleum system for future prospect evaluation.

• Tendrara – Lakbir drilling programme offers next near-term opportunity for monetisation

• Deep Kinsale and Mizzen prospects offer medium term potential for monetisation following farm-down/drilling

OVERVIEW

ACQUIRE

ANALYSE

FARM DOWN

EXPLORE

MONETISE

www.fastnetoilandgas.com 6

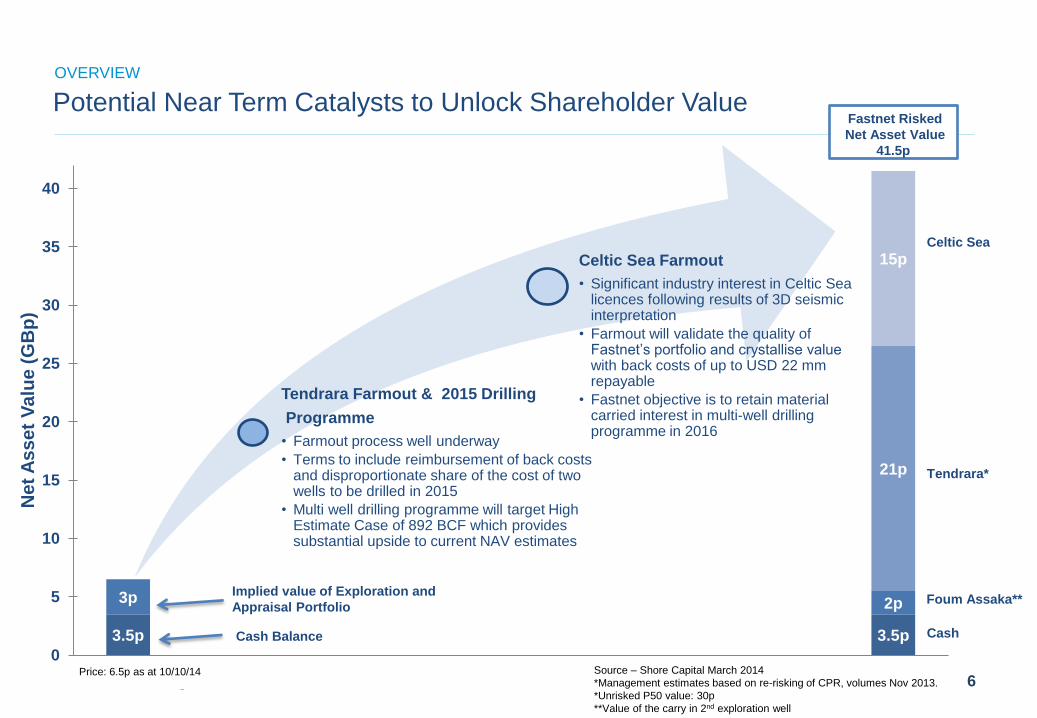

3.5p 3.5p

3p 2p

21p

15p

0

5

10

15

20

25

30

35

40

Ne

t A

ss

et

Va

lue

(G

Bp

)

Potential Near Term Catalysts to Unlock Shareholder Value

Tendrara Farmout & 2015 Drilling

Programme

• Farmout process well underway

• Terms to include reimbursement of back costs and disproportionate share of the cost of two wells to be drilled in 2015

• Multi well drilling programme will target High Estimate Case of 892 BCF which provides substantial upside to current NAV estimates

Celtic Sea Farmout

• Significant industry interest in Celtic Sea licences following results of 3D seismic interpretation

• Farmout will validate the quality of Fastnet’s portfolio and crystallise value with back costs of up to USD 22 mm repayable

• Fastnet objective is to retain material carried interest in multi-well drilling programme in 2016

Source – Shore Capital March 2014

*Management estimates based on re-risking of CPR, volumes Nov 2013.

*Unrisked P50 value: 30p

**Value of the carry in 2nd exploration well

Tendrara*

Celtic Sea

Foum Assaka**

Cash

Implied value of Exploration and

Appraisal Portfolio

Cash Balance

Fastnet Risked

Net Asset Value

41.5p

OVERVIEW

Price: 6.5p as at 10/10/14

Experienced Board & Senior Management

Paul Griffiths, Managing Director CEO of Island Oil & Gas Plc until its acquisition by San Leon

Energy Plc in 2009

Built and sold 3 oil and gas companies between 1999-2012

Senior geophysicist for Gulf Oil Corporation for Europe and

Mediterranean Region and Gulf R&D in Pittsburgh

Carol Law, Executive Director Former Exploration Manager, Anadarko East Africa

Responsible for the play finding Prosperidade gas complex in

Rovuma Area 1, offshore Mozambique

Also member of teams responsible for discoveries in Ghana

(Jubilee), Brazil (multiple Campos Basin discoveries)

Cathal Friel, Executive Chairman Managing Director and one of the founders of Raglan Capital in

2007

Former founding partner and Director of Merrion Capital

MBA from University of Ulster

Will Holland, Chief Financial Officer Former Associate Director at Macquarie bank where he originated,

structured and managed equity and debt investments in small-cap

E&P companies.

Previously worked at Halliburton Energy Services in various

technical & business development roles based in Africa & Europe

MBA from Heriot-Watt University

Michael Nolan, Non-Executive Director Former Founder and Group Finance Director of Cove Energy PLC

Currently CFO of Discover Exploration and Non-executive director

of Rathdowney Resources plc and Orogen Gold plc

Fellow of the Chartered Accountants Ireland

Value Creation

Sold IPDL to DNO ASA, after

reverse takeover of

Providence Resources Plc

collapsed in 2002, for an exit

price of $34 mm after

investing approx. $1.5 mm

100 TCF +

Carol led the Anadarko team

that discovered over 100 TCF

of natural gas in the Area 1

Block, Offshore Mozambique

100%

100% exploration

success rate offshore

Ireland with Island Oil &

Gas: 4 wells drilled, two

commercial gas fields

$2.64 billion

Sale price of a 10%

stake in Anadarko’s

Area 1 Block, Offshore

Mozambique

38+ years

Experience in oil

and gas exploration

and near term field

appraisal

30 years

Experience in oil

and gas industry

25+ years

Managerial

Corporate Finance

experience

20+ years

Experience in oil

and gas industry

€100 million

One of the founding directors

of Merrion Capital, where he

was part of the small team

that built the business and

sold it for c. €100m in 2006

$2.5 billion

Value of successful

corporate transactions

on which Cathal has

advised

+$110 million

Managed Macquarie interest

in over $110 million of debt

and equity investments

Internal Control

Lead teams of internal

auditors at Halliburton

assessing accounting &

operation risks

THE TEAM

18+ years

Experience in

resource

exploration sector

+1900%

Share price increase between

the Cove Energy IPO in June

2009 and its sale in Aug 2012

$1.9 billion

Cove Energy was sold

to PTTEP in Aug 2012

after a competitive

auction process

Company Overview

Moroccan Assets

Irish Assets

Outlook

Company Overview

Irish Assets

Moroccan Assets

Outlook

www.fastnetoilandgas.com 9

Celtic Sea Offshore

Highly prospective basin

capable of delivering significant

near-term production

• Attractive petroleum geology with

major reserves potential: largest

producing gas field at Kinsale

Head, large prospects with well-

understood large-field analogues

and existing infrastructure

• Underexplored, applying new

technologies to de-risk by analogy

with surrounding oil and gas

discoveries

• Shallow water prospects: easier to

monetise than deepwater Irish

Atlantic Margin

• Largest ever 3D seismic survey

undertaken in Summer 2013

(1,910km2)

- Mizzen 1,400km2

- Kinsale 510km2

DEEP

KINSALE

MOLLY

MALONE

MIZZEN &

Mizzen East

SHANAGARRY BLOCK 49/13

AREA 285 km2 648 km2 1942 km2 881 km2 272 km2

WATER DEPTH c. 100 m c. 100 m c. 100 m c. 100 m c. 100 m

FASTNET INTEREST 60% 100% 100% 82.35% 85%

IRELAND

www.fastnetoilandgas.com 10

Deep Kinsale - Large Untested Closure Below Shallow Producing Gas Field IRELAND

Prospect E

Deep Kinsale Primary

Prospect “A”

49/9-2 “Helvick” Oil & Gas Play

Base Chalk

Upper Purbeck Sands

Middle Wealden

Upper Jurassic

Upper-Middle Jurassic

Mounding in Upper Purbeck

Northern Bounding Fault Kinsale Field 1.7 TCF Gas

MFS

48/25-1 Discovery

Southern Bounding Fault

Source

Reservoir Prone

Deep Liassic Source?

Approx. Licence Limit (4000ft)

North

SE

North South East

Potential reservoir bearing packages thicken into active Late Jurassic to Early Cretaceous Faults

www.fastnetoilandgas.com 11

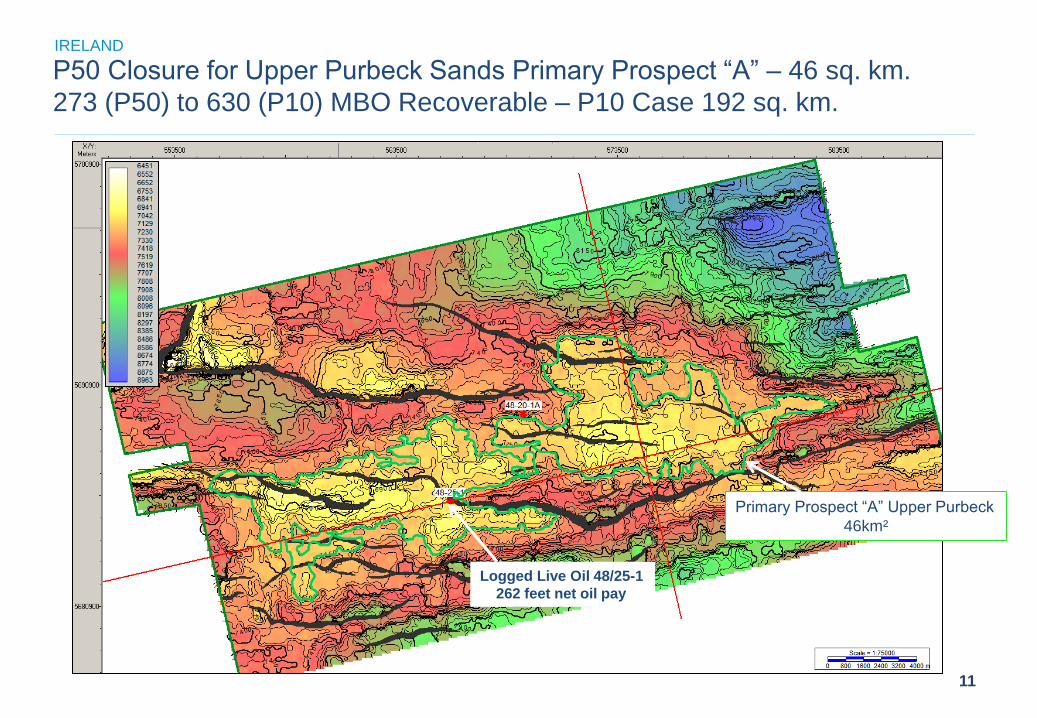

P50 Closure for Upper Purbeck Sands Primary Prospect “A” – 46 sq. km.

273 (P50) to 630 (P10) MBO Recoverable – P10 Case 192 sq. km.

Primary Prospect “A” Upper Purbeck

46km²

Logged Live Oil 48/25-1

262 feet net oil pay

IRELAND

www.fastnetoilandgas.com 12

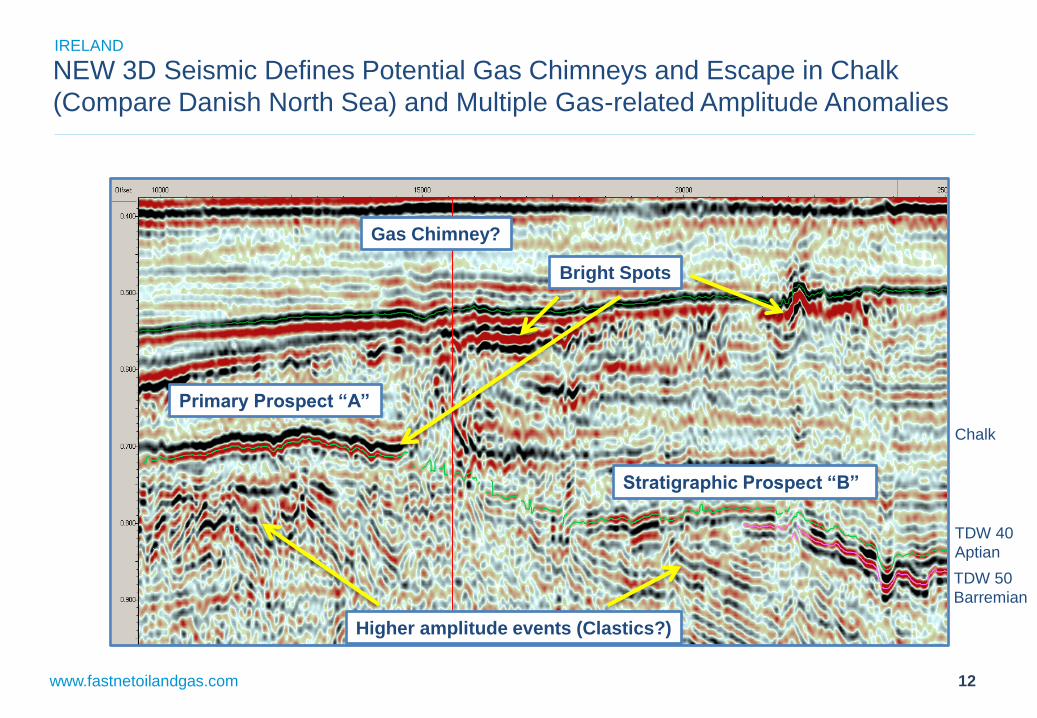

NEW 3D Seismic Defines Potential Gas Chimneys and Escape in Chalk

(Compare Danish North Sea) and Multiple Gas-related Amplitude Anomalies

Gas Chimney?

Bright Spots

Stratigraphic Prospect “B”

TDW 40

Aptian

TDW 50

Barremian

Chalk

Primary Prospect “A”

Higher amplitude events (Clastics?)

IRELAND

Company Overview

Moroccan Assets

Irish Assets

Outlook

Company Overview

Irish Assets

Moroccan Assets

Outlook

www.fastnetoilandgas.com 14

Energy Prices and Fiscal Regime

MOROCCO

• The gas and oil prices in Morocco are indexed to international prices.

• The gas price at the Morocco - Algerian border is 10 to 11 USD per a million BTU.

• The selling price of the produced gas from Moroccan wells is between 2 and 3 MAD/m3.

Fiscal Incentives

• 25% State participation

• Royalty: Oil 10%; Gas 5%

• 10 year corporate tax holiday on discovery

Profit Value of 1bbl of Oil in Morocco

• Producing 1bbl of oil in Morocco is equivalent to

• 13bbl in Algeria

• 7bbl in Nigeria

Morocco Canada

Argentina UK

Libya Egypt

Norway Indonesia

0% 20% 40% 60% 80% 100%

Gov’t Take (%)

Morocco Algeria Nigeria Egypt

Source: EY Global oil and gas tax guide, 2013

www.fastnetoilandgas.com 15

Tendrara Lakbir Option

MOROCCO

Overview

• 14,548 sq. km. Over entire

prospective Missour-Tendrara Basin

• Material, near-development gas

project – clear pathway to early

monetisation

• 7 wells drilled on licence – 6

encountered gas

Equity & Partners

• Pathfinder (subsidiary of Fastnet):

50% net equity

• Oil and Gas Investments Funds

(OGIF): 25%

• ONHYM: 25%

www.fastnetoilandgas.com 16

Tendrara Lakbir Exploration History: 6 wells discovered gas of 7 wells drilled MOROCCO

• TE-5 Gas Structure (red) 488 sq. km. 3D & 4,110 kms. 2D seismic

3 month EWT – no pressure depletion in TAGI I Formation damage – stabilised rate 1.5 mm cfgpd

Legacy Prospectivity (2000-2008)

• TE-3 & TE-4 Structure (red hatched) TAGI tight gas reservoir

Gas shows in Lias limestone and Carboniferous

• TE-2 Structure (red outline) TAGI tight gas reservoir

• SBK-1 Gas Discovery (red) TAGI II tested at 5 mm cfgpd

Declined to 2.5 mm cfgpd (fault barrier/no 3D) Condensate shows in Lias dolomites & Trias basalts 300 bcf GIIP Best Estimate

• TAGI Prospects (yellow) Structural & Stratigraphic Pinchout

• TE-1 (1966) logged gas Possible downdip extension TE-5 Structure

Additional Untested Upside

• Cambro-Ordovician NE area of the Block

• Carboniferous Basinwide

• Unconventional Shale Gas Carboniferous – basin centre play

62 TCF (Source ONHYM) Silurian/Tannezuft – NE area

NW-SE LINE OF SECTION Legacy 2D Seismic

www.fastnetoilandgas.com 17

Fastnet TAGI I Depth Map (At Seismic Reference Datum)

P50 CLOSURE: 40 sq. km. GAS-DOWN-TO 2451 meters subsea 88 meters gross gas column in TE-5

No water leg encountered Meskala Field pressure data supports single column

FAULT “A” MAY EXTEND ENE AS SHOWN BELOW

Fault “A”

o

o

Provisional TE-6 Testing 10 sq. km. updip 350 BCF GIIP

Provisional TE-7 Testing P50 40 sq. km. 1.4 TCF GIIP

TE-5 P90 35 BCF GIIP from EWT interpretation Radius of investigation < 1 sq. km.

TE-1 New Petrophysical Analysis

43.8 meters of gas pay now recognised Upside to Extend TE-5 Gas Column 400 meters Downdip

MOROCCO

• Legacy 2D seismic

processing (depth mapping

in progress on reprocessed

seismic data)

• TE-6 to test deliverability

and TE-7 to Test P50 GIIP

Volumes

www.fastnetoilandgas.com 18

Fastnet Independent Reservoir Engineering Study

(Case “A” 9.1 mm cfgpd with all zones in 22.5m perforated; S = 0) A

( Original Well Test k – Only top 11.5m contributing; S = 30)

(EWT Well Test k – Only top

11.5m contributing; S = 0)

MOROCCO

TE-5 Well – inflow Performance Rates

TE-6 Well to test well deliverability case “A” – 9mm cfgpd

www.fastnetoilandgas.com 19

Offshore Morocco Play Fairway Analysis

MOROCCO

• FA-1 well trade value is being used to

give valuable insight into an ongoing

analysis of the potential of the under-

explored offshore

• Deep Secondary Target favoured by

Fastnet and a target for Chevron and

BP offshore Nova Scotia remains a key

target in Foum Assaka following the FA-

1 well

• Exploration drilling offshore Morocco

has historically focused on the

Carbonate Shelf with no commercial

discoveries as yet

Analysis of 32 Wells drilled in Morocco

FA-1 Well

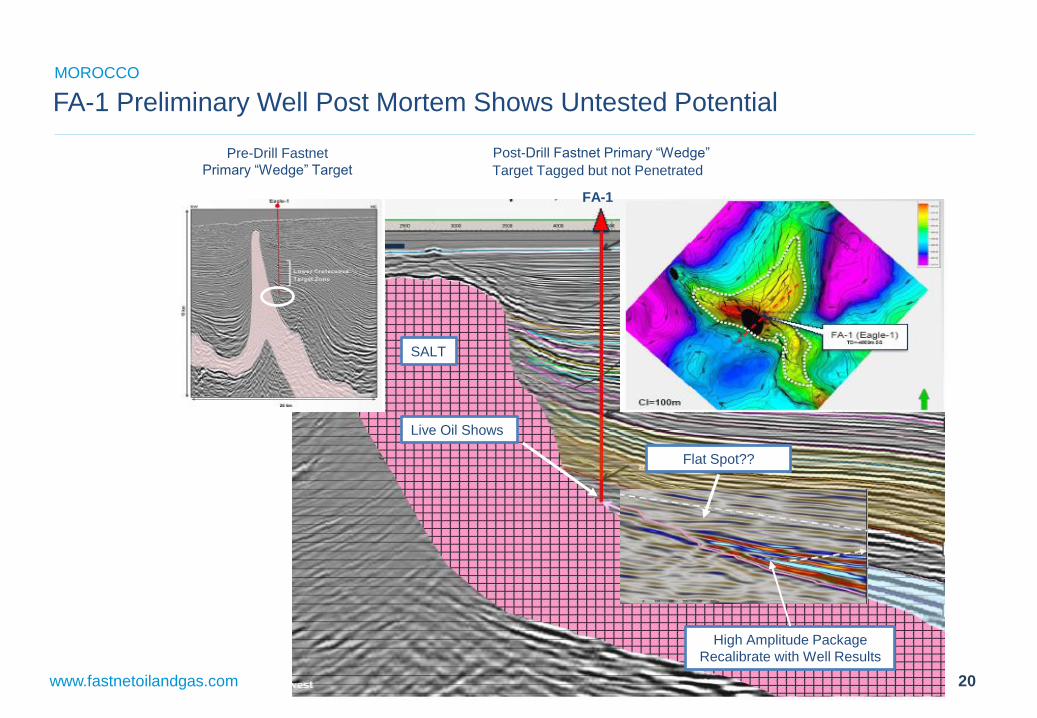

www.fastnetoilandgas.com 20

Flat Spot??

Pre-Drill Fastnet

Primary “Wedge” Target

Post-Drill Fastnet Primary “Wedge”

Target Tagged but not Penetrated

FA-1

Live Oil Shows

High Amplitude Package

Recalibrate with Well Results

SALT

MOROCCO

FA-1 Preliminary Well Post Mortem Shows Untested Potential

www.fastnetoilandgas.com 21

MOROCCO

FA-1 Sidewall Cores – Live Oil Under UV Light

Source: CoreLab

www.fastnetoilandgas.com 22

Company Overview

Irish Assets

Moroccan Assets

Outlook

www.fastnetoilandgas.com 23

OUTLOOK

Prospect Activity 2014 2015

Q2 Q3 Q4 Q1 Q2 Q3 Q4

ONSHORE

MOROCCO

(Tendrara Lakbir)

Farmout

Exercising Option Agreement (Dec 2014)

Rig contract

Drilling preparation EIS Study

Complete seismic pre-stack depth migration

mature prospect portfolio

Drill first appraisal well

Drill second non obligatory appraisal

well/POD submission

OFFSHORE

MOROCCO

(Foum Assaka)

Drill first well

Evaluate FA-1 well results

Drill second FA-1 carried well subject to

partners approving location & timing

Evaluate well results

OFFSHORE

IRELAND

(Celtic Sea)

Celtic Sea Farmout/workshop

(Joint Initiative by Celtic Sea operators)

3D Seismic Interpretation/AVO Processing

Stage 1 & Stage 2 Farmouts

Multi-Well programme planning for 2016

Forward Work Programme

www.fastnetoilandgas.com 24

THANK YOU

Thank You