Embed Size (px)

Citation preview

FASB’s Accounting Standards UpdatesASUs issued during 2010 and the beginning of 2011

with permission of the Financial Accounting Foundation for use of FASB material

22

2

Course Objectives

High Level Review of FASB Accounting Standards Updates (ASUs) issued during 2010 and the beginning of 2011The main provisions and their effective dates

Update preparers of US GAAP financials, and get them up to speed

Encourage preparers to perform further research on the new accounting standards

Offer possibility to seek further guidance

33

3

Disclaimer

The contents of this coursework provided have been prepared with reasonable care, that means the author has made every attempt to provide the most accurate information available using internal and external resources to prepare this course but he makes no representations, warranties, or guarantees regarding the accuracy, correctness or completeness of any opinions, advice, statements, instructions or other information provided in or by the material or the other contents and features of the course

It is your responsibility to investigate and evaluate the accuracy, correctness, reliability or completeness of any opinions, advice, statements, instructions or request further clarification from the author

44

4

Introduction

Effective July 1, 2009, changes to the source of authoritative U.S. GAAP, the FASB Accounting Standards Codification™ (FASB Codification), are communicated through an Accounting Standards Update (Update). Updates are published for all authoritative U.S. GAAP promulgated by the FASB, regardless of the form in which such guidance may have been issued prior to release of the FASB Codification (e.g., FASB Statements, EITF Abstracts, FASB Staff Positions, etc.) Updates are also issued for amendments to the SEC content in the FASB Codification as well as for editorial changes

55

5

Introduction

An Update is a transient document that summarizes the key provisions of the project

that led to the Update, details the specific amendments to the FASB

Codification, andexplains the basis for the Board's decisions

Although ASUs will update the FASB Codification, the FASB does not consider Updates as authoritative in their own right

66

6

Introduction

1XX General Principles 8XX Broad Transactions2XX Presentation 805 Business Combinations280 Segment Reporting 810 Consolidation

3XX Assets 815 Derivatives and Hedging350 Intangibles - Goodwill and Other 820 Fair Value Measurements and Disclosures360 Property, Plant, and Equipment 825 Financial Instruments

4XX Liabilities 850 Related Party Disclosures430 Deferred Revenue 852 Reorganizations

5XX Equity 855 Subsequent Events

505 Equity 9XX Industry6XX Revenue 930 Extractive Activities - Mining605 Revenue Recognition 932 Extractive Activities - Oil and Gas

7XX Expenses 940 Financial Services - Broker and Dealers730 Research and Development 946 Financial Services - Investment Companies740 Income Taxes

77

7

Introduction1XX General Principles2XX Presentation3XX Assets310 Receivables

FASU 2011-01 Deferral of the Effective Date of Disclosures about Troubled Debt Restructurings in Update No. 2010-20

350 Intangibles - Goodwill and Other

GASU 2010-28 When to Perform Step 2 of the Goodwill Impairment Test for Reporting Units with Zero or Negative Carrying Amounts

4XX Liabilities5XX Equity505 Equity

HASU 2010-01 Accounting for Distributions to Shareholders with Components of Stock and Cash

6XX Revenue605 Revenue Recognition

IASU 2010-17 Milestone Method (Topic 605): Milestone Method of Revenue Recognition

7XX Expenses720 Other Expenses

JASU 2010-27 Fees Paid to the Federal Government by Pharmaceutical Manufacturers

88

8

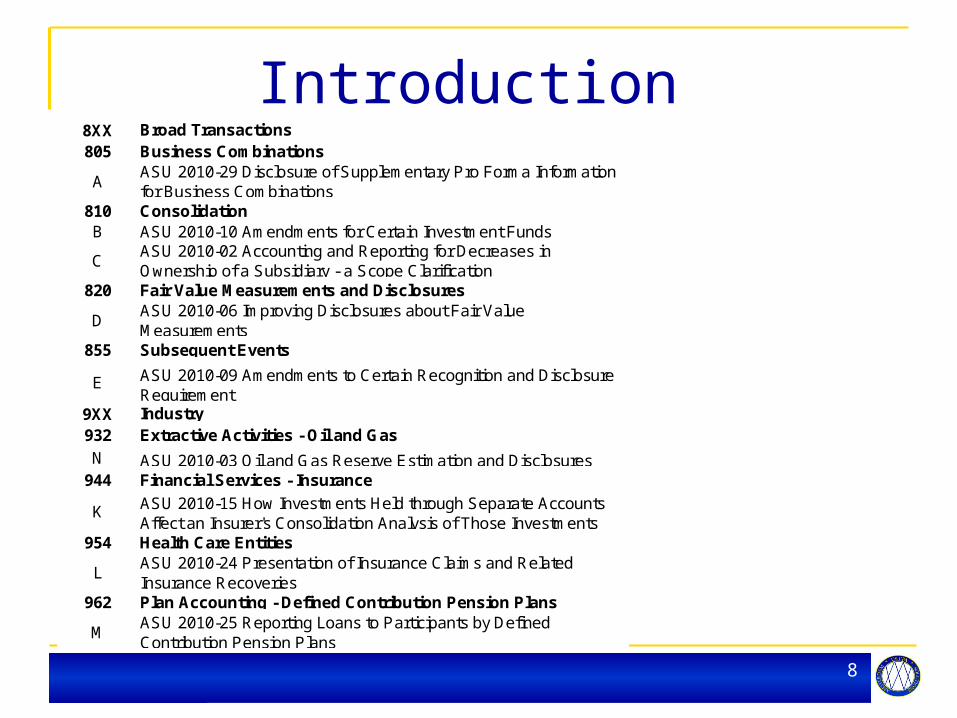

Introduction8XX Broad Transactions805 Business Combinations

AASU 2010-29 Disclosure of Supplementary Pro Forma Information for Business Combinations

810 ConsolidationB ASU 2010-10 Amendments for Certain Investment Funds

CASU 2010-02 Accounting and Reporting for Decreases in Ownership of a Subsidiary - a Scope Clarification

820 Fair Value Measurements and Disclosures

DASU 2010-06 Improving Disclosures about Fair Value Measurements

855 Subsequent Events

E ASU 2010-09 Amendments to Certain Recognition and Disclosure Requirement

9XX Industry932 Extractive Activities - Oil and Gas

N ASU 2010-03 Oil and Gas Reserve Estimation and Disclosures944 Financial Services - Insurance

K ASU 2010-15 How Investments Held through Separate Accounts Affect an Insurer's Consolidation Analysis of Those Investments

954 Health Care Entities

LASU 2010-24 Presentation of Insurance Claims and Related Insurance Recoveries

962 Plan Accounting - Defined Contribution Pension Plans

MASU 2010-25 Reporting Loans to Participants by Defined Contribution Pension Plans

99

9

A: ASU 2010-29

Update No. 2010-29 - Business Combinations (Topic 805): Disclosure of Supplementary Pro Forma Information for Business Combinations

If a public entity presents comparative financial statements, the entity shoulddisclose revenue and earningsof the combined entityas though the business combination(s) that occurred

during the current year had occurred as of the beginning of the comparable prior annual reporting period only

1010

10

A: ASU 2010-29

The amendments in this Update also expand the supplemental pro forma disclosures under Topic 805 to includea description of the nature and amountof material, nonrecurring pro forma

adjustments directly attributableto the business combination included in the

reported pro forma revenue and earnings

1111

11

A: ASU 2010-29

Effective prospectively for business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after December 15, 2010. Early adoption is permitted

IFRS 3, Business Combinations, permits, but does not require, pro forma disclosures for the comparative period. IFRS does not require a description of the nature and amount of material, nonrecurring pro forma adjustments

1212

12

B: ASU 2010-10

Update No. 2010-10 - Consolidation (Topic 810): Amendments for Certain Investment Funds

Defer the consolidation requirements in Topic 810 for a reporting entity's interest in an entity that has all of the attributes of an investment company

Effective as of the beginning of a reporting entity's first annual period that begins after November 15, 2009

1313

13

B: ASU 2010-10

The deferral would apply to:A reporting entity's interest in an entitythat is required to comply or operate in

accordance with requirementssimilar to those in Rule 2a-7 of the Investment

Company Act of 1940 for registered money market funds

These entities are variable interest entities

1414

14

C: ASU 2010-02

Update No. 2010-02 - Consolidation (Topic 810): Accounting and Reporting for Decreases in Ownership of a Subsidiary - a Scope Clarification

Effective beginning in the first interim or annual reporting period ending on or after December 15, 2009. The amendments should be applied retrospectively to the first period that an entity adopted Statement 160

The scope of the decrease in ownership provisions of the Subtopic and related guidance applies to the following:

1515

15

C: ASU 2010-02

A subsidiary or group of assets that is a business or nonprofit activity

A subsidiary that is a business or nonprofit activity that is transferred to an equity method investee or joint venture

An exchange of a group of assets that constitutes a business or nonprofit activity for a non-controlling interest in an entity (including an equity method investee or joint venture)

1616

16

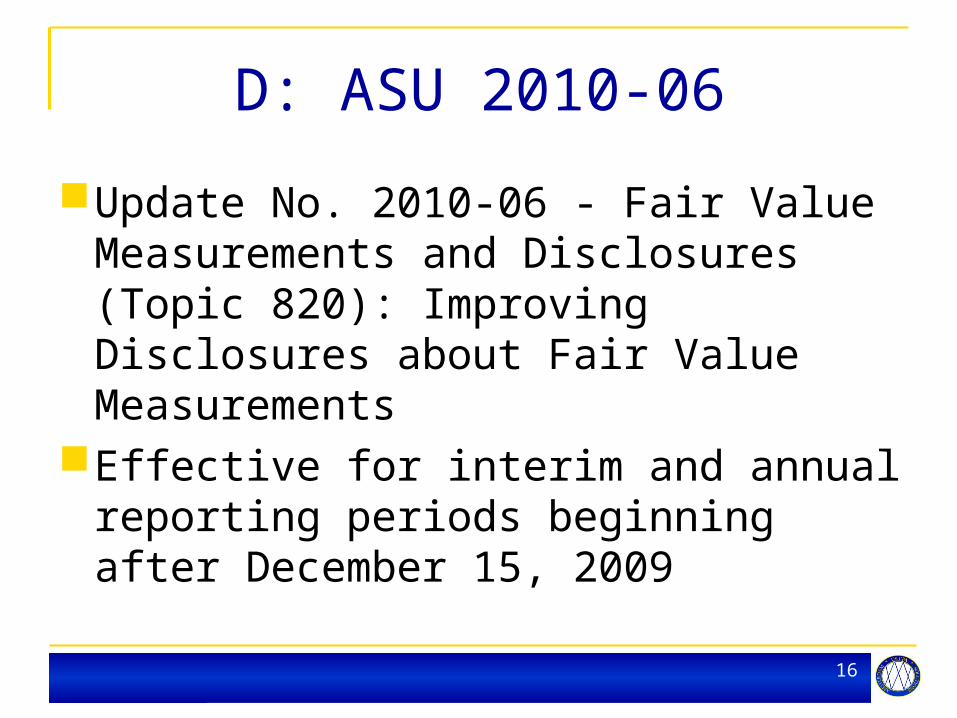

D: ASU 2010-06

Update No. 2010-06 - Fair Value Measurements and Disclosures (Topic 820): Improving Disclosures about Fair Value Measurements

Effective for interim and annual reporting periods beginning after December 15, 2009

1717

17

D: ASU 2010-06

A reporting entity should provide disclosures about the valuation techniques and inputs used to measure fair value for both recurring and nonrecurring fair value measurements in either Levels 2 and 3

1818

18

E: ASU 2010-09

Update No. 2010-09 - Subsequent Events (Topic 855): Amendments to Certain Recognition and Disclosure Requirement

Provides definition for an SEC filer:Adds the term revised financial statement

to its glossaryEffective for interim or annual periods

ending after June 15, 2010

1919

19

E: ASU 2010-09

An SEC filer is an entity that is required to file or furnish its financial

statements with either the SEC or, with respect to an entity subject to Section 12(i) of the

Securities Exchange Act of 1934, as amended, the appropriate agency under that Section

it does not include an entity that is not otherwise a SEC filer whose financial statements are included in a submission by another SEC filer

2020

20

E: ASU 2010-09

Revised financial statements include financial statements revised eitheras a result of correction of an erroror retrospective application of U.S. generally

accepted accounting principles

2121

21

E: ASU 2010-09

An entity that either(a) is a SEC filer or(b) is a conduit bond obligor for conduit debt

securities that are traded in a public market is required to evaluate subsequent events

through the date that the financial statements are issued

if an entity meets neither of those criteria, then it should evaluate subsequent events through

the date the financial statements are available to be issued

2222

22

F: ASU 2011-01

Update No. 2011-01 - Receivables (Topic 310): Deferral of the Effective Date of Disclosures about Troubled Debt Restructurings in Update No. 2010-20Update No. 2010-20 - Receivables (Topic

310): Disclosures about the Credit Quality of Financing Receivables and the Allowance for Credit Losses

The deferral in this amendment is effective upon issuance

2323

23

F: ASU 2011-01

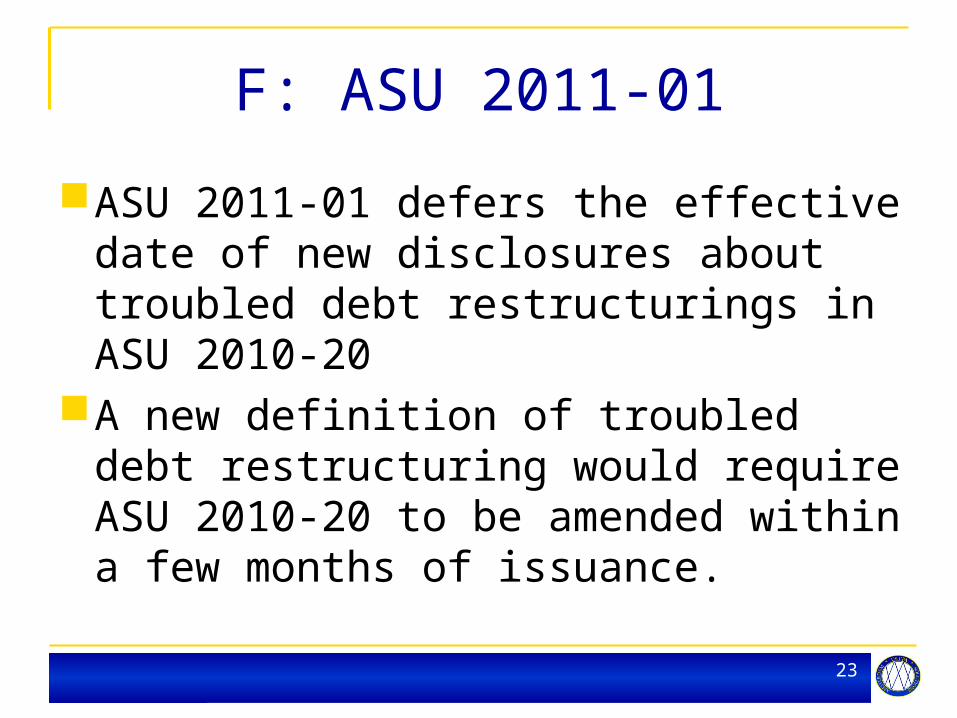

ASU 2011-01 defers the effective date of new disclosures about troubled debt restructurings in ASU 2010-20

A new definition of troubled debt restructuring would require ASU 2010-20 to be amended within a few months of issuance.

2424

24

G: ASU 2010-28

Update No. 2010-28 - Intangibles - Goodwill and Other (Topic 350):

When to Perform Step 2 of the Goodwill Impairment Test for Reporting Units with Zero or Negative Carrying Amounts

2525

25

G: ASU 2010-28

Effective after 15 December 2010 for Public companies

Eliminates an entity's ability to assert that a reporting unit is not required to perform Step 2Step 1: Carrying Value > Fair ValueStep 2: Calculate Impairment, if any

2626

26

G: ASU 2010-28

Test for reporting units with zero or negative carrying amounts

Step 1 is modified to still require performing Step 2 if qualitative factors exist that would indicate goodwill may be impaired

2727

27

G: ASU 2010-28

Impairment recorded as a cumulative-effect adjustment to beginning retained earnings in the period of adoption

Under IFRS a different impairment model, i.e. a single-step goodwill impairment test

2828

28

H: ASU 2010-01

Update No. 2010-01 - Equity (Topic 505): Accounting for Distributions to Shareholders with Components of Stock and Cash

Clarify that the stock portion of a distribution to shareholders

that allows them to elect to receive cash or stockwith a potential limitation on the total amount of cashthat all shareholders can elect to receive in the

aggregate is considered

2929

29

H: ASU 2010-01

a share issuanceEffective > December 15, 2009, applied on

a retrospective basisIFRS does not provide specific guidance

3030

30

I: ASU 2010-17

Update No. 2010-17 - Revenue Recognition - Milestone Method (Topic 605): Milestone Method of Revenue Recognition

Provides guidance on when to apply the milestone method of revenue recognition for Research and development transactions

3131

31

I: ASU 2010-17

will primarily affect entities that provide research or development deliverables

Effective > June 15, 2010 on a prospective basis for milestones achieved

Early adoption is permitted

3232

32

I: ASU 2010-17

A vendor can recognize considerationthat is contingent upon achievement of

a milestonein its entirety as revenue in the period in

which the milestone is achievedonly if the milestone meets all criteria to

be considered substantive

3333

33

I: ASU 2010-17

To be considered substantive, the consideration earned by achieving the milestone should commensurate:The vendor's performance to achieve the milestone The enhancement of the value of the item delivered

as a result of a specific outcome resulting from the vendor's performance to achieve the milestone

Relate solely to past performance Be reasonable relative to all deliverables and

payment terms in the arrangement

3434

34

I: ASU 2010-17

Additional Disclosure requirements applyA vendor may elect, but is not required, to

adopt the amendments in this Update retrospectively for all prior periods

Previously no guidance under US GAAP

3535

35

I: ASU 2010-17

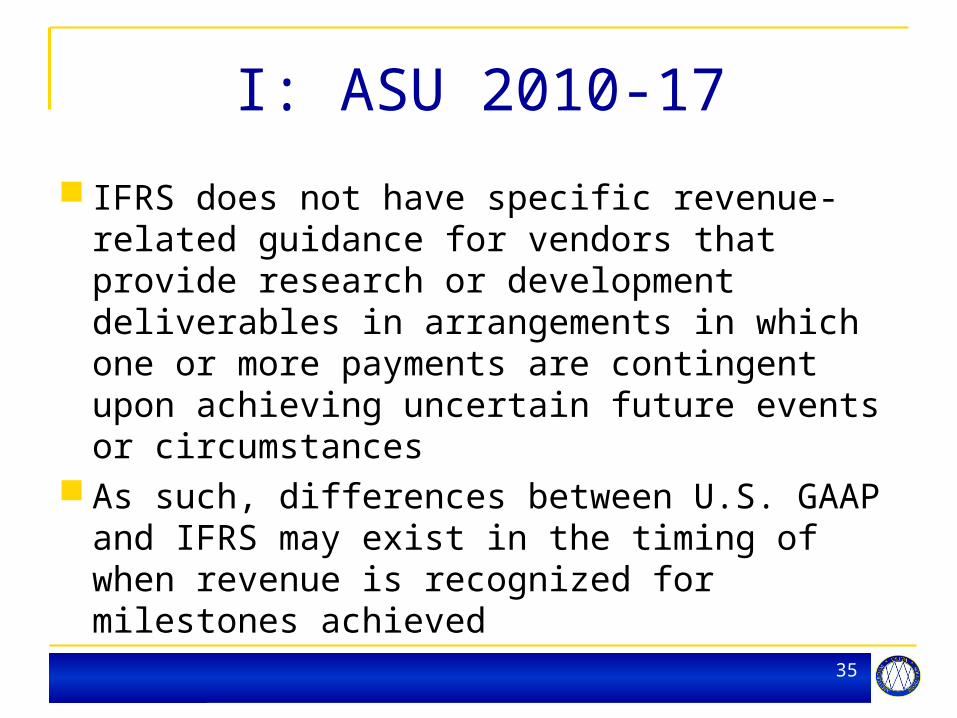

IFRS does not have specific revenue-related guidance for vendors that provide research or development deliverables in arrangements in which one or more payments are contingent upon achieving uncertain future events or circumstances

As such, differences between U.S. GAAP and IFRS may exist in the timing of when revenue is recognized for milestones achieved

3636

36

J: ASU 2010-27

Update No. 2010-27 - Other Expenses (Topic 720): Fees Paid to the Federal Government by Pharmaceutical Manufacturers

Effective for calendar years beginning after December 31, 2010

There is no specific guidance in IFRS for the fee covered by this Update

3737

37

J: ASU 2010-27

Amended Act imposes an annual fee on the pharmaceutical manufacturing industry

Annual fee ranges from $2.5 billion to $4.1 billion for all affected entities in total

Fee will be allocated to individual entities on the basis of the amount of their branded prescription drug sales for the preceding year as a percentage of the

industry's branded prescription drug sales for the same period

3838

38

J: ASU 2010-27

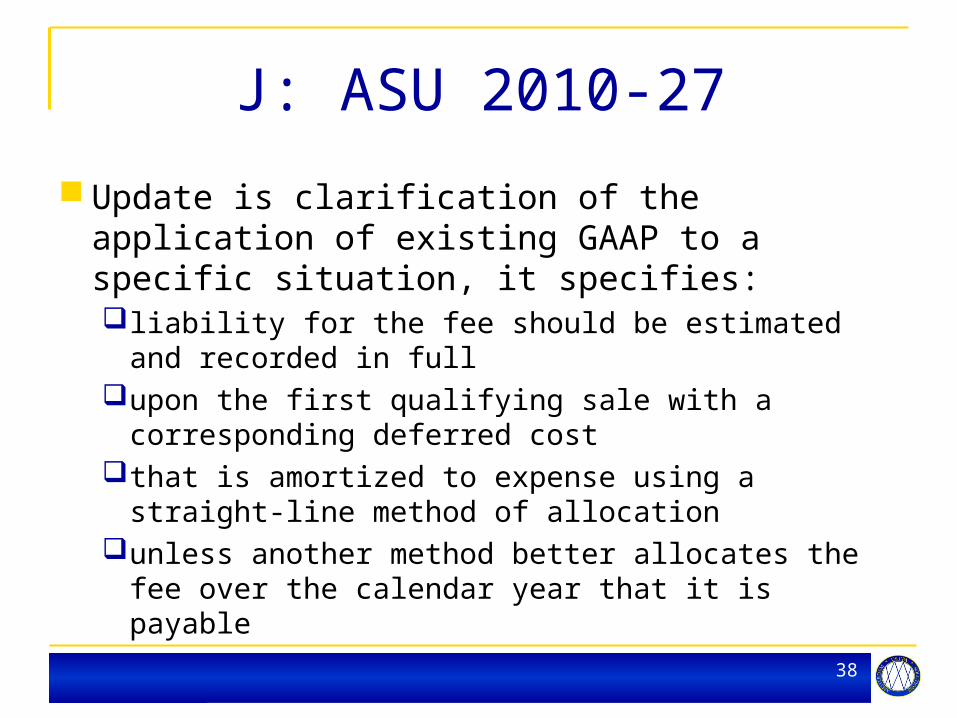

Update is clarification of the application of existing GAAP to a specific situation, it specifies: liability for the fee should be estimated and recorded

in fullupon the first qualifying sale with a corresponding

deferred costthat is amortized to expense using a straight-line

method of allocation unless another method better allocates the fee over

the calendar year that it is payable

3939

39

K: ASU 2010-15

Update No. 2010-15 - Financial Services - Insurance (Topic 944): How Investments Held through Separate Accounts Affect an Insurer's Consolidation Analysis of Those Investments

Effective > December 15, 2010 The amendments in this Update may result in

differences in accounting and reporting between GAAP and IFRS because IFRS does not specifically address the accounting by insurance entities

4040

40

K: ASU 2010-15

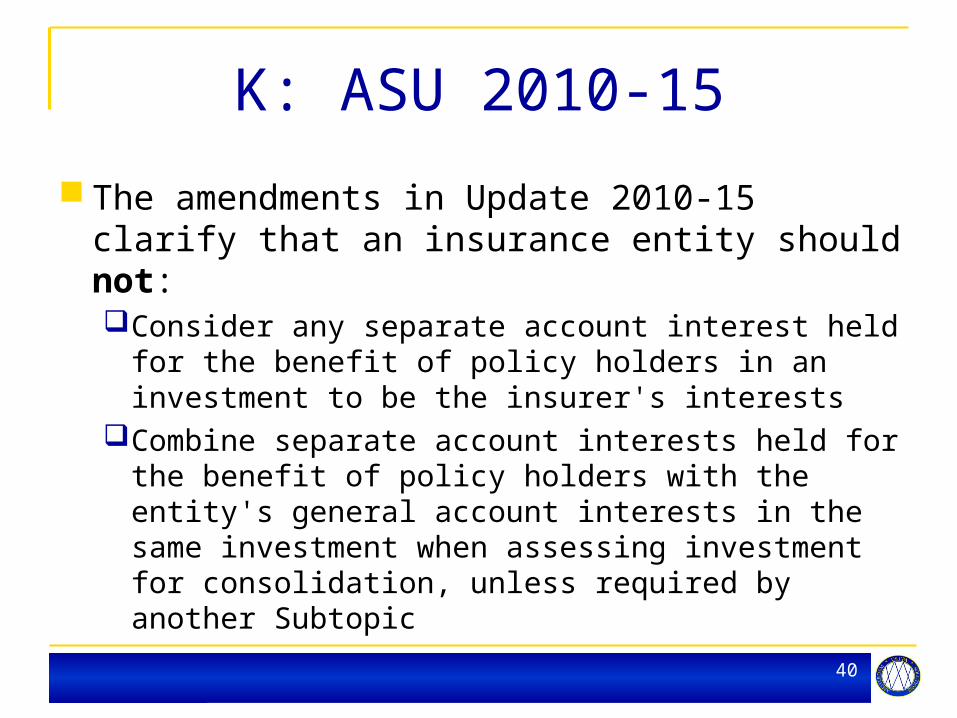

The amendments in Update 2010-15 clarify that an insurance entity should not:Consider any separate account interest held for the

benefit of policy holders in an investment to be the insurer's interests

Combine separate account interests held for the benefit of policy holders with the entity's general account interests in the same investment when assessing investment for consolidation, unless required by another Subtopic

4141

41

K: ASU 2010-15

Update 2010-15 provides amendments to Subtopic 944-80 to clarifythat for the purpose of evaluating whether the

retention of specialized accounting for investments in consolidation is appropriate,

a separate account arrangement should be considered a subsidiary

4242

42

K: ASU 2010-15

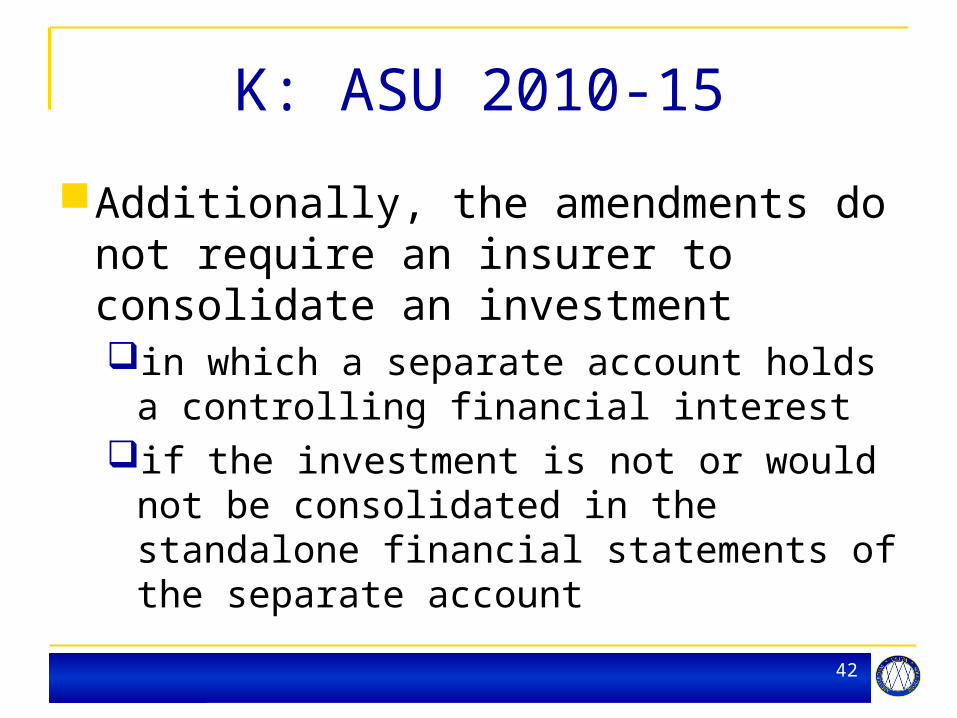

Additionally, the amendments do not require an insurer to consolidate an investmentin which a separate account holds a

controlling financial interestif the investment is not or would not be

consolidated in the standalone financial statements of the separate account

4343

43

L: ASU 2010-24

Update No. 2010-24 - Health Care Entities (Topic 954): Presentation of Insurance Claims and Related Insurance Recoveries

Effective > December 15, 2010IFRS does not permit offsetting of assets

and liabilities in the circumstances described in this Update

4444

44

L: ASU 2010-24

The amendments in this Update clarify that a health care entity should not net insurance recoveries against a related claim liability

Additionally, the amount of the claim liability should be determined without consideration of insurance recoveries

4545

45

L: ASU 2010-24

A cumulative-effect adjustment should be recognized in opening retained earnings in the period of adoption if a difference exists between any liabilities and insurance receivables recorded as a result of applying the amendments in this Update

The amendments in this Update permit retrospective application

Early application of the amendments in this Update also is permitted

4646

46

M: ASU 2010-25

Update No. 2010-25 - Plan Accounting - Defined Contribution Pension Plans (Topic 962): Reporting Loans to Participants by Defined Contribution Pension Plans

Effective > December 15, 2010Participant loans are not as commonly

observed outside the United States

4747

47

M: ASU 2010-25

Affects any defined contribution pension plan that allows participant loans

The amendments in this Update require that participant loansbe classified as notes receivable from

participants, which are segregated from plan investments

and measured at their unpaid principal balance

plus any accrued but unpaid interest

4848

48

N: ASU 2010-03

Update No. 2010-03 - Extractive Activities - Oil and Gas (Topic 932): Oil and Gas Reserve Estimation and Disclosures

Effective > December 31, 2009IFRS 6 and Topic 932 differ in areas such

as scope, measurement, and disclosuresE.g. IFRS 6 specifies the financial reporting

for mining activities, while Topic 932 does not

4949

49

N: ASU 2010-03

The changes from current GAAP improve the reserve estimation and disclosure requirements byUpdating the reserve estimation requirements

for changes in practice and technology that have occurred over the last several decades and

Expanding the disclosure requirements for equity method investments

5050

50

Need Further Guidance?

Amsterdam US CPA Solutions Phone (+31) 20 600 20 40 Fax (+31) 20 600 20 41 [email protected] Singel 540, 1017AZ

Amsterdam, The Netherlands

Expert international financial solutions in accounting, controlling, business, US auditing and US tax for entrepreneurial business leaders and investors