Embed Size (px)

Citation preview

©2009 IACPM1

Fall General Meeting

November 9-10, 2010

New York, NY

Assessing Sovereign Risk from the Bottom-Up

Edward I. Altman

New York University Stern School of Business

Director, Credit & Debt markets Research Program

www.riskmetrics.com 2

Measuring and Assessing Sovereign Risk

Some Recent Sovereign Crises

Asia – 1997

Argentina – 2000

Europe – 2010

Traditional Indicators of Risk

Macroeconomic Related Variables

Traditional Models

Statistical and Aggregative Techniques

Newer Market Based Techniques and Measures

Contingent Claims Structural Approach

Credit Default Swaps (CDS) Implied Probability of Defaults (PDs)

Corporate Statistical PD Measures to Assess Sovereign Health

The Z-Metrics Approach

A Bottom-Up analysis

(Outline for Discussion)

www.riskmetrics.com 3

Total filings and liabilities of companies filing for Chapter 11 Protection in the US: 1989-2010 (3Q)

Source: NYU Salomon Center Bankruptcy Filings Database

$0

$100

$200

$300

$400

$500

$600

$700

$800

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 (Excl. LEH

)

08 (Incl. LEH

)

09 10 (3Q)

$ B

illi

on

0

40

80

120

160

200

240

280

Pre- Petition Liabilities, in $ billions (left axis)

Number of Filings (right axis)

2009

234 filings and

liabilities of

$604.0 billion

2010 (3Q)

87 filings and

liabilities of $37.8

billion

www.riskmetrics.com 4

QUARTERLY DEFAULT RATE AND FOUR QUARTER MOVING AVERAGE

1989 – 2010 (3Q)

Source: Author’s Compilations

Default rates on high-yield bonds 1989-2010 (3Q)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1989199019911992199319941995199619971998199920002001200220032004200520062007200820092010 (3Q

)

Qu

art

erly

Def

au

lt R

ate

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

4 -

Qu

art

er M

ovin

g A

ver

age

Quarterly

Moving

www.riskmetrics.com 5

555

Par Value Par Value Default

Year Outstanding* Defaults Rates (%)

2009 $1,152,952 $124,130 10.766

2008 $1,091,000 $50,763 4.653

2007 $1,075,400 $5,473 0.509

2006 $993,600 $7,559 0.761

2005 $1,073,000 $36,181 3.372

2004 $933,100 $11,657 1.249

2003 $825,000 $38,451 4.661

2002 $757,000 $96,855 12.795

2001 $649,000 $63,609 9.801

2000 $597,200 $30,295 5.073

1999 $567,400 $23,532 4.147

1998 $465,500 $7,464 1.603

1997 $335,400 $4,200 1.252

1996 $271,000 $3,336 1.231

1995 $240,000 $4,551 1.896

1994 $235,000 $3,418 1.454

1993 $206,907 $2,287 1.105

1992 $163,000 $5,545 3.402

1991 $183,600 $18,862 10.273

1990 $181,000 $18,354 10.140

1989 $189,258 $8,110 4.285

1988 $148,187 $3,944 2.662

1987 $129,557 $7,486 5.778

1986 $90,243 $3,156 3.497

1985 $58,088 $992 1.708

2010 (3Q) $1,221,569 $8,166 0.668%

Straight Bonds Only Excluding Defaulted Issues From Par Value Outstanding, (US$ millions)

1971 – 2010 (3Q)

Historical Default Rates

Par Value Par Value Default

Year Outstandinga Defaults Rates (%)

1984 $40,939 $344 0.840

1983 $27,492 $301 1.095

1982 $18,109 $577 3.186

1981 $17,115 $27 0.158

1980 $14,935 $224 1.500

1979 $10,356 $20 0.193

1978 $8,946 $119 1.330

1977 $8,157 $381 4.671

1976 $7,735 $30 0.388

1975 $7,471 $204 2.731

1974 $10,894 $123 1.129

1973 $7,824 $49 0.626

1972 $6,928 $193 2.786

1971 $6,602 $82 1.242Standard

Deviation (%)

Arithmetic Average Default Rate

1971 to 2009 3.332% 3.226%

1978 to 2009 3.637% 3.424%

1985 to 2009 4.323% 3.550%

Weighted Average Default Rate*

1971 to 2009 4.552%

1978 to 2009 4.564%

1985 to 2009 4.601%

Median Annual Default Rate

1971 to 2009 1.896%

Source: Author’s compilation and Citigroup estimate

* Weighted by par value of amount outstanding for each year.

www.riskmetrics.com 6

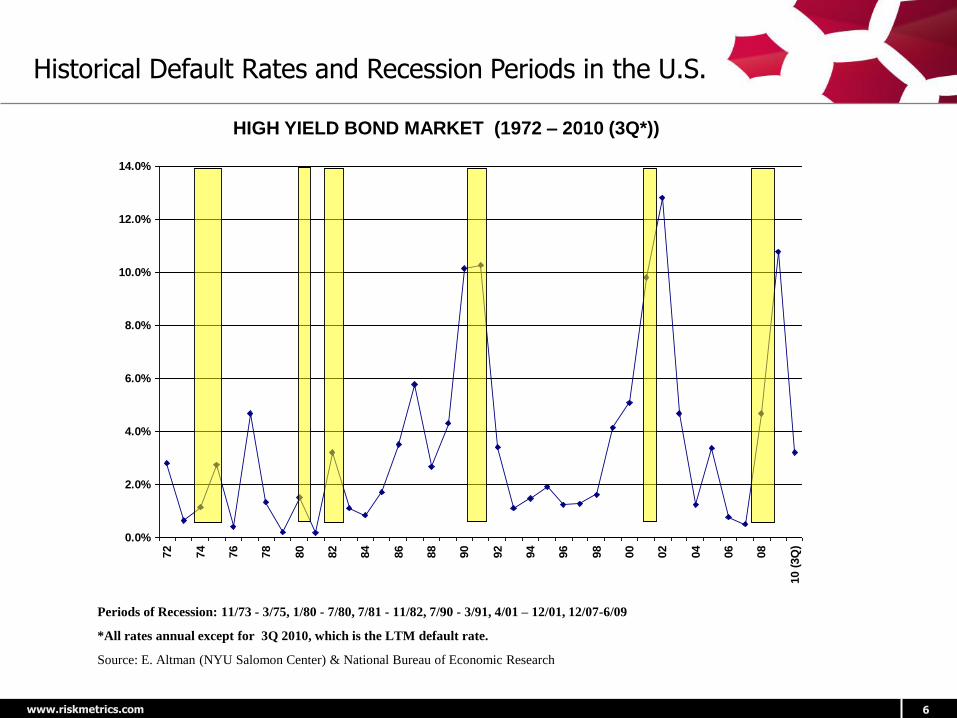

Periods of Recession: 11/73 - 3/75, 1/80 - 7/80, 7/81 - 11/82, 7/90 - 3/91, 4/01 – 12/01, 12/07-6/09

*All rates annual except for 3Q 2010, which is the LTM default rate.

Source: E. Altman (NYU Salomon Center) & National Bureau of Economic Research

HIGH YIELD BOND MARKET (1972 – 2010 (3Q*))

Historical Default Rates and Recession Periods in the U.S.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%72

74

76

78

80

82

84

86

88

90

92

94

96

98

00

02

04

06

08

10 (

3Q

)

www.riskmetrics.com 7

Objectives of our Z-Metrics™ model

To construct an accurate, logical, and robust credit-scoring model

To assign a probability of default (PD) and Z-Metrics unique credit rating over one-year and five-year horizons to non-financial firms

To provide both ―best estimate‖ as well as ―stressed‖ PDs and ratings

To create models for:

Large publicly-held firms in the U.S. and Canada (―U.S. Model‖)

Large, privately-held firms in the U.S. and Canada

Small, publicly-held firms in the U.S. and Canada

Large and small firms outside the U.S. and Canada

We expect that our U.S. model will be applicable to ex-U.S. firms

www.riskmetrics.com 8

Model characteristics

Based on over 1,000 U.S./Canadian defaulted (credit-event) non-financial firms and a control sample (~15:1) of non-defaulting observations

Credit-event date is default or bankruptcy date—whichever occurs first

Credit-event sample reduced to 638 firms in public firm sample and 802 in private firm sample after removing those with insufficient data

Sample period 1989-2008, out-of-sample tests based on two 10-year samples and 2009 credit-event firms

www.riskmetrics.com 9

Model characteristics (continued)

Over 260,000 quarterly & annual observations used to construct model

Macroeconomic factors included to capture time-series variation of default probabilities

For stressed ratings and PDs, two critical measures are examined: Share price and earnings

Final public model has 12 fundamental and market variables, including both static and trend measures plus two macroeconomic variables

www.riskmetrics.com 10

Variables assessed

Over 50 fundamental financial statement variables covering such performance characteristics as solvency, leverage, size, profitability, interest coverage, liquidity, asset quality, investment, dividend payout, and financing results

Analyzed trends in many of the fundamental variables

Included equity market price and return variables and their relative volatility patterns: typically used in structural, distance-to-default measures

Examined distribution of variable values: transformed variables to capture nature of distribution and to reduce influence of outliers

Supplemented fundamentals and market data with macroeconomic measures to adjust for macro stresses on the world’s economies

www.riskmetrics.com 11

Illustration of variable distribution

Credit-event rate as a function of Interest/EBIT for one and five year horizons(two sample periods)

credit-event (default/bankruptcy) rate

1 year horizon

0%

3%

6%

9%

12%

-4 -2 0 2 4 6

Interest/EBIT

cre

dit-e

vent

rate

1980 - 1999

2000 - 2008

credit-event (default/bankruptcy) rate

5 year horizon

0%

20%

40%

60%

-4 -2 0 2 4 6

Interest/EBIT

cre

dit-e

vent

rate

1980 - 1999

2000 - 2008

www.riskmetrics.com 12

Impact of log transformations on the distribution of credit-event rates for the variable RE/TA

one year

horizon

0%

2%

4%

6%

8%

10%

-3 -2 -1 0 1

RE/TA

cre

dit-e

vent

rate

one year

horizon

0%

2%

4%

6%

8%

10%

-1.5 -1 -0.5 0 0.5 1 1.5

-1*(ln(1 - RE/TA)

cre

dit-e

vent

rate

No transformation Log transformation

www.riskmetrics.com 13

Criteria for Variable Selection and Performance Assessment

Accuracy ratios (error rates) for credit-event prediction

Type I (Correct default prediction)

Type II (Correct non-default prediction)

Comparison of accuracy ratios to existing systems

Rating agencies, Altman’s Z-Score models

Comparison of accuracy ratios in-sample and out-of-sample

Comparison of implied Z-Metrics ratings with observed Agency ratings

Discriminatory power of model across full spectrum of ratings

One-year and five-year prediction horizons

Stability of explanatory power and parameters over time and across sectors

Macro variables that reflect timely changes in stress for firm credit-worthiness over time

Stress testing

www.riskmetrics.com 14

Case 1: Default Rate[t+1] Versus Yield Spread[t]

The regression equation is

Default Rate = - 3.25 + 1.39 * Spread

Predictor Coef SE Coef T P

Constant -3.2490 0.9072 -3.58 0.001

Spread 1.3904 0.1741 7.99 0.000

S = 1.86079 R-Sq = 69.5% R-Sq(adj) = 68.4%

Application

Applying Yield spread (12/31/2008) of 1,731 bps, PD = -3.25 + 1.39*17.31 = 20.811%

Applying Yield spread (12/31/2009) of 513 bps, PD = -3.25 + 1.39*5.13 = 3.883%

Applying Yield spread (6/30/2010) of 622 bps, PD = -3.25 + 1.39*6.22 = 5.398%

Dollar Denominated (Altman) Default Rate Predictions

www.riskmetrics.com 15

Logit model estimation

Standard logit regression functional form

CSi,t = α + ΣβXi,t + εi,t

CSi,t = Z-Metrics credit score of company i at time t

β = variable parameters (or weights)

Xi,t = set of fundamental, market based and macroeconomic variables for firm/quarter observations

εi,t = error terms (assumed to be identically and independently distributed)

CSi,t is transformed into a probability of default by

tiCStie

PD,1

1,

www.riskmetrics.com 16

Type I and Type II error rates for Agency ratings, Z-Metrics and Z’’-score Agency Equivalent (AE) ratings (1989-2008): One year prediction horizon for public firms

type I error rate (defaulters classified as non-defaulters / total defaulters)

0

0.2

0.4

0.6

0.8

1

CCC/C

C/C B

- B B+

BB-

BB

BB+

BBB-

rating class

(cutoff score = score at upper boundary of rating class N)

typ

e I e

rro

r ra

te

AE rating: Z" score

Agency rating

AE rating: Z-Metrics public one year

type II error rate

(non defaulters classified as defaulters/total non defaulters)

0

0.2

0.4

0.6

0.8

1

CCC/C

C/C B

- B B+

BB-

BB

BB+

BBB

-BBB

BBB

+ A- A A

+AA-

AA

AA/A

AA

rating class N

(cutoff score = score at upper boundary of rating class N)

typ

e II e

rro

r ra

teAE rating: Z" score

Agency rating

AE rating: Z-Metrics public one year

www.riskmetrics.com 17

Definition of Z-Metrics ratings for one and five-year horizon Public Models

% Representation % Representation

Rating Min Max 1989/2008 2008 Min Max 1989/2008 2008

High Grade ZA+ 0.00% 0.02% 3.50% 2.10% 0.00% 0.75% 3.40% 2.40%

ZA 0.02% 0.04% 5.80% 4.60% 0.75% 1.25% 7.00% 5.40%

ZA- 0.04% 0.06% 7.60% 6.10% 1.25% 1.75% 7.60% 6.40%

ZB+ 0.06% 0.09% 10.60% 10.00% 1.75% 2.50% 10.60% 9.90%

ZB 0.09% 0.14% 10.90% 11.20% 2.50% 3.50% 11.10% 11.30%

ZB- 0.14% 0.20% 8.80% 9.10% 3.50% 4.50% 8.10% 8.60%

Medium Grade ZC+ 0.20% 0.30% 9.40% 10.80% 4.50% 6.00% 8.60% 9.70%

ZC 0.30% 0.50% 10.10% 10.40% 6.00% 9.00% 11.10% 12.10%

ZC- 0.50% 1.00% 10.60% 11.40% 9.00% 14.00% 10.00% 10.30%

Low Grade ZD+ 1% 2% 7.60% 8.20% 14% 20% 6.30% 6.80%

ZD 2% 4% 5.20% 5.80% 20% 30% 6.00% 6.60%

ZD- 4% 10% 4.50% 4.70% 30% 45% 4.50% 4.90%

ZF+ 10% 25% 2.60% 2.60% 45% 65% 3.00% 3.20%

ZF 25% 50% 1.50% 1.60% 65% 80% 1.40% 1.60%

ZF- 50% 100% 1.20% 1.30% 80% 100% 1.00% 1.00%

Z-Metrics One-Year Public Model Z-Metrics Five-Year Public Model

One Year PD Five Year PD

www.riskmetrics.com 18

Default prediction examples for 2009 defaults,comparing Agency and Z-Score ratings to Z-Metrics ratings

Company Accuride General Motors Spectrum Brands

Time to Default (Months) 11 10 12

Agency rating 4 2 1

1Y Public Z-Metrics AE Rating 2 1 2

Z Score AE Rating 5 1 3

Z" score AE Rating 5 1 4

1Y Public Z-Metrics PD Values 29.80% 31.60% 14.10%

5Y Public Z-Metrics PD Values 66.80% 67.30% 47.10%

1Y Public Z-Metrics Ratings ZF ZF ZF+

5Y Public Z-Metrics Ratings ZF ZF ZF+

AE Ratings, where 1 = CCC, 2 = B-, …, 16 = AAA/AA+

www.riskmetrics.com 19

Defaulted firms’ rating comparison (Z-Metrics, Z score, Agency rating) – In sample test

Performance of Z-Metrics compared to rating agencies

Public Private Public Private Z Score Z'' Score

Average 0.62 0.05 0.6 0.15 -0.9 -0.81

Minimum 8 9 7 9 9 9

Maximum -7 -11 -5 -9 -12 -11

51% 40% 51% 40% 34% 31%

24% 34% 24% 30% 50% 50%

25% 26% 26% 30% 17% 19%

402 535 402 535 451 451

(Agency rating - AE rating) For In-Sample Period

In Sample: Issuers Defaulted 1989-2008 Z-Metrics 1Y Z-Metrics 5Y Z Score

[Agency rating] minus [AE rating]

% Firms with higher Agency rating

% Firms with lower Agency rating

% Firms with equal rating

Total number of firms

www.riskmetrics.com 20

Defaulted firms’ rating comparison (Z-Metrics, Z score, Agency rating) – Out of sample test

Performance of Z-Metrics compared to rating agencies

Out of Sample: Issuers Defaulted in 2009

Public Private Public Private Z Score Z'' Score

Average 0.5 -0.14 0.47 0.03 -1.31 -0.62

Minimum 3 2 2 3 4 3

Maximum -3 -5 -2 -2 -7 -4

50% 31% 50% 28% 17% 28%

19% 31% 16% 33% 66% 52%

31% 39% 34% 39% 17% 21%

32 36 32 36 29 29

(Agency rating - AE rating) For Out-Of-Sample Period

% Firms with equal rating

Total number of firms

Z-Metrics 1Y Z-Metrics 5Y Z Score

[Agency rating] minus [AE rating]

% Firms with higher Agency rating

% Firms with lower Agency rating

www.riskmetrics.com 21

Financial Health of the Private, Non-Financial Sector: Selected European Countries and U.S.A. in 2010/2009

(Z-Metrics PD Estimates and Implied PDs from CDS Spreads)

Z-Metrics PD Estimates: Five-Year Public Model* No. of Listed Five-Year Implied PD

Companies 2010 2009 2010 2009 from CDS Spread **† Country 2010 2009 Median PD Median PD Std. Dev. Std. Dev. 2010 2009

Netherlands 61 60 3.33% 5.62% 7.52% 9.33% 2.83% 6.06%

U.K. 442 433 3.62% 5.75% 11.60% 12.70% 6.52% 8.13%

U.S.A. 2226 2171 3.93% 6.97% 9.51% 15.15% 3.28% 4.47%

France 297 294 5.51% 7.22% 9.72% 12.34% 3.75% 4.05%

Germany 289 286 5.54% 7.34% 13.10% 15.16% 2.67% 3.66% Spain 82 78 6.44% 7.39% 9.63% 11.26% 9.39% 8.07%

Ireland 28 26 6.45% 7.46% 16.29% 16.30% 12.20% 17.00%

Italy 155 154 7.99% 10.51% 10.20% 14.11% 8.69% 11.20%

Portugal 30 30 9.36% 12.07% 7.25% 12.44% 10.90% 7.39%

Greece 79 77 10.60% 11.57% 14.40% 12.99% 24.10% 13.22%

* Based on median Z-Metrics PDs from January 1 – June 30, 2009 and January 1 – April 30, 2010.**Assuming a 40% recovery rate; based on the median CDS spread observed for first six months of 2009 and first three months of 2010.†PD Computed as 1-e(-5*s/(1-R))

Sources: RiskMetrics Group (MSCI), Markit, Compustat.

www.riskmetrics.com 22

Median Percent Change in Various Country Stock Market Index Values and Z-Metrics’ PDs

*Median of the various trading day stock index values and PDs

Sources: Z-Metrics Model calculations from RiskMetrics (MSCI) Group, Bloomberg for stock index values

(First Six Months of 2010 Vs. 2009)

Country Index

Median Percent

Change

(2010 vs. 2009)*

Median Z-Metrics

PDs: Percent Change

(2010 vs. 2009)*

France CAC40 24.1% -23.6%

Germany DAX 31.8% -24.5%

Greece ASE 5.5% -8.4%

Ireland ISEQ 26.2% -7.4%

Italy FTSEMIB 18.2% -24.0%

Netherlands AEX 34.4% -25.3%

Portugal PSI-20 17.8% -22.4%

Spain IBEX35 20.9% -12.9%

U.K. FTSE100 27.8% -37.6%

U.S.A. S&P500 31.9% -43.6%

www.riskmetrics.com 23

Five Year Implied Probabilities of Default (PD) FromCDS Spreads

Greece, Jan 2009 to Oct 2010

Source: Markit

0

10

20

30

40

50

60

1-J

an

-09

22

-Ja

n-0

9

12

-Fe

b-0

9

5-M

ar-

09

26

-Ma

r-0

9

16

-Ap

r-0

9

7-M

ay

-09

28

-Ma

y-0

9

18

-Ju

n-0

9

9-J

ul-

09

30

-Ju

l-0

9

20

-Au

g-0

9

10

-Se

p-0

9

1-O

ct-0

9

22

-Oct

-09

12

-No

v-0

9

3-D

ec-

09

24

-De

c-0

9

14

-Ja

n-1

0

4-F

eb

-10

25

-Fe

b-1

0

18

-Ma

r-1

0

8-A

pr-

10

29

-Ap

r-1

0

20

-Ma

y-1

0

10

-Ju

n-1

0

1-J

ul-

10

22

-Ju

l-1

0

12

-Au

g-1

0

2-S

ep

-10

23

-Se

p-1

0

14

-Oct

-10

Date

5 Y

ea

r P

D (

As

Pe

rce

nt)