Embed Size (px)

Citation preview

Factors Weighing on Credit Recovery in Croatia—Pintarić

Comments by O'Callaghan

1. Context—the story is very interesting2. The Data—are worth closer examination3. Methodology—a "disequilibrium" approach

recognises that debt stocks adjust very slowly4. Lessons—some shared and some not5. Summary—don't be afraid to break the mould

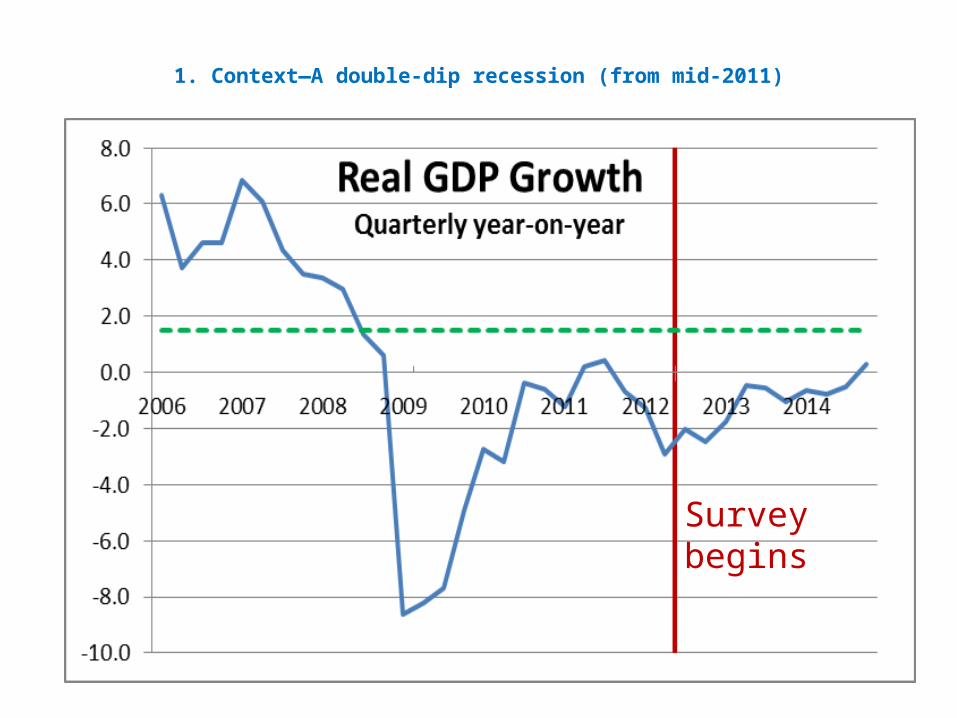

1. Context—A double-dip recession (from mid-2011)

Survey begins

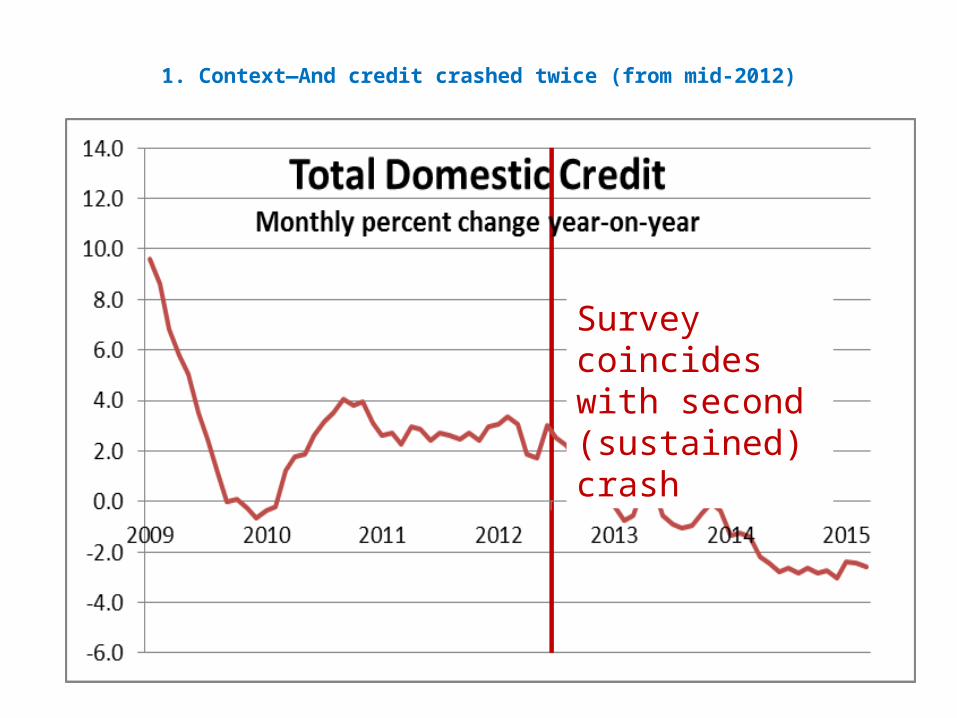

1. Context—And credit crashed twice (from mid-2012)

Survey coincides with second (sustained) crash

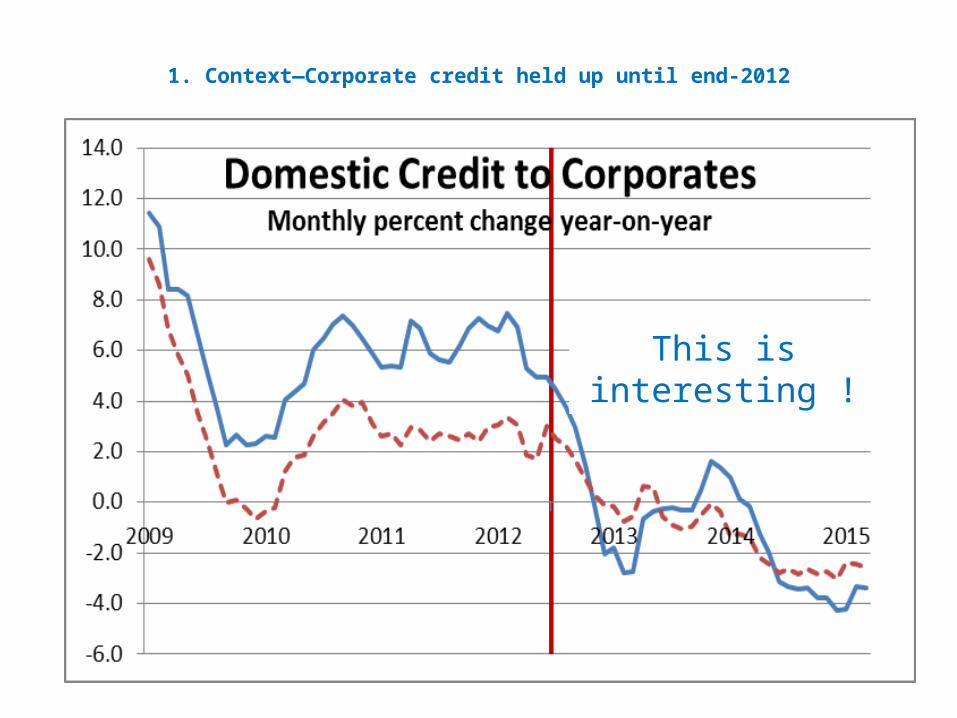

1. Context—Corporate credit held up until end-2012

This is interesting !

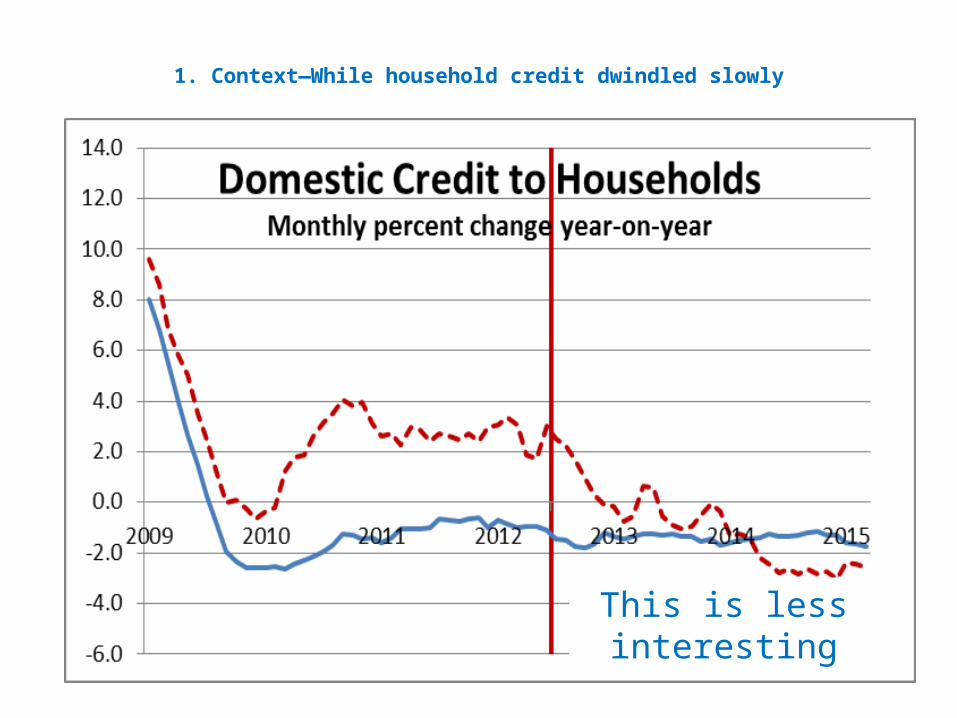

1. Context—While household credit dwindled slowly

This is less interesting

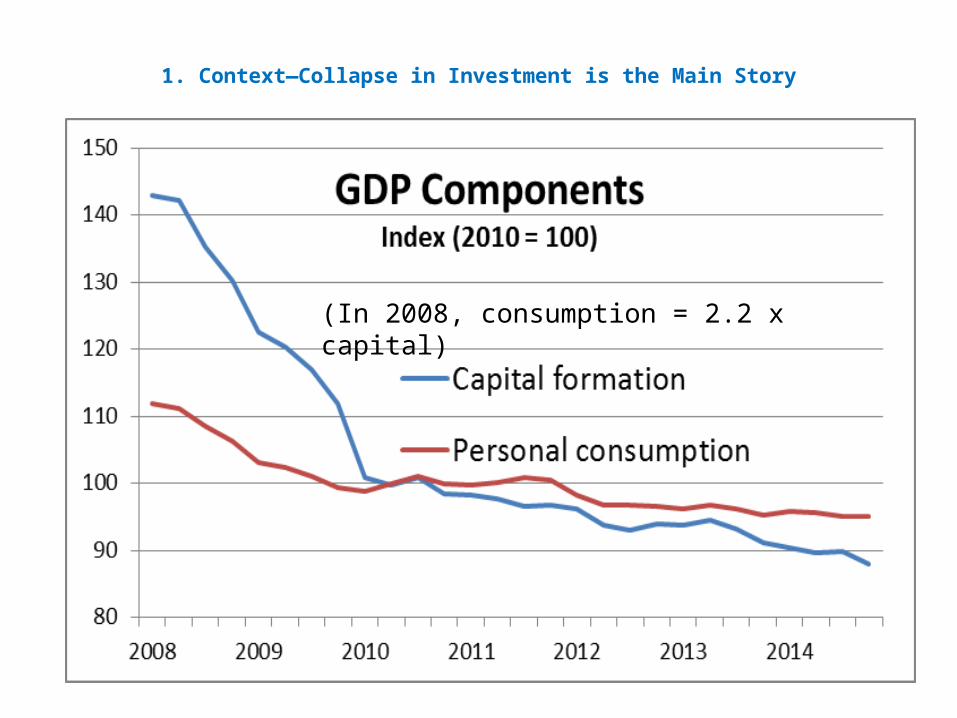

1. Context—Collapse in Investment is the Main Story

Survey begins

(In 2008, consumption = 2.2 x capital)

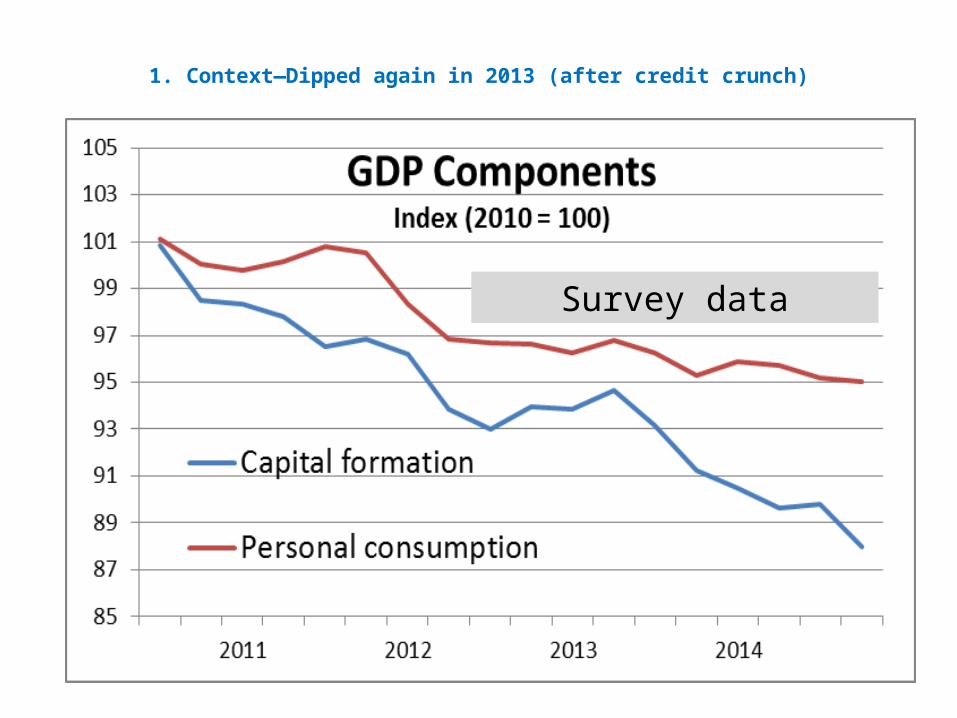

1. Context—Dipped again in 2013 (after credit crunch)

Survey begins

(In 2008, consumption = 2.2 x capital)Survey data

1. Context—Corporate credit held up until end-2012

This is really interesting !

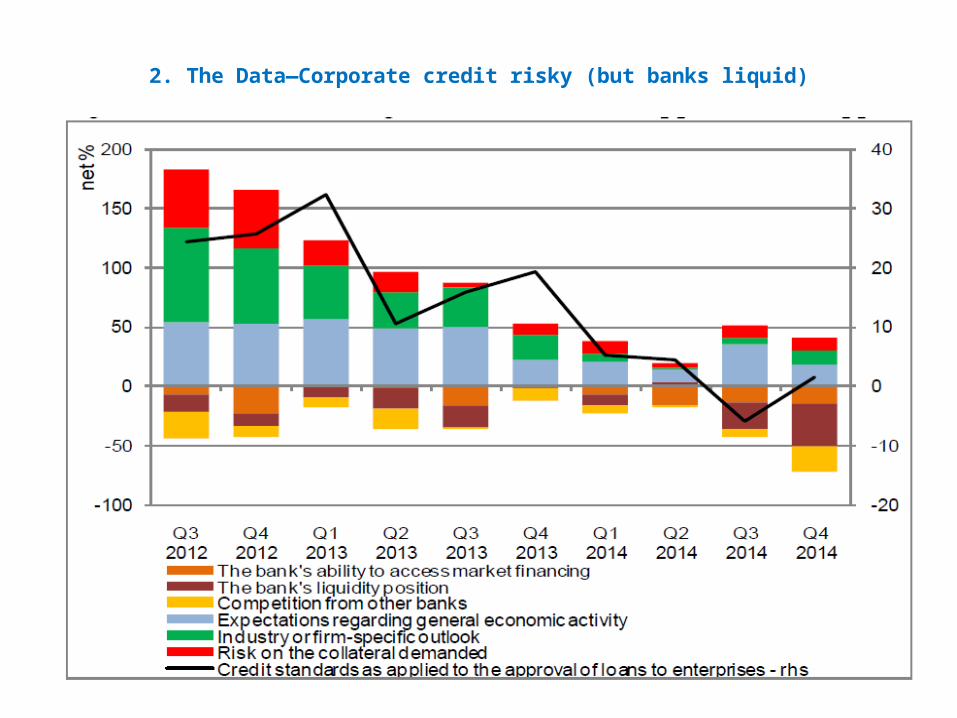

2. The Data—Corporate credit risky (but banks liquid)

Survey begins

2. The Data—Corporates want to survive/restructure

Survey begins

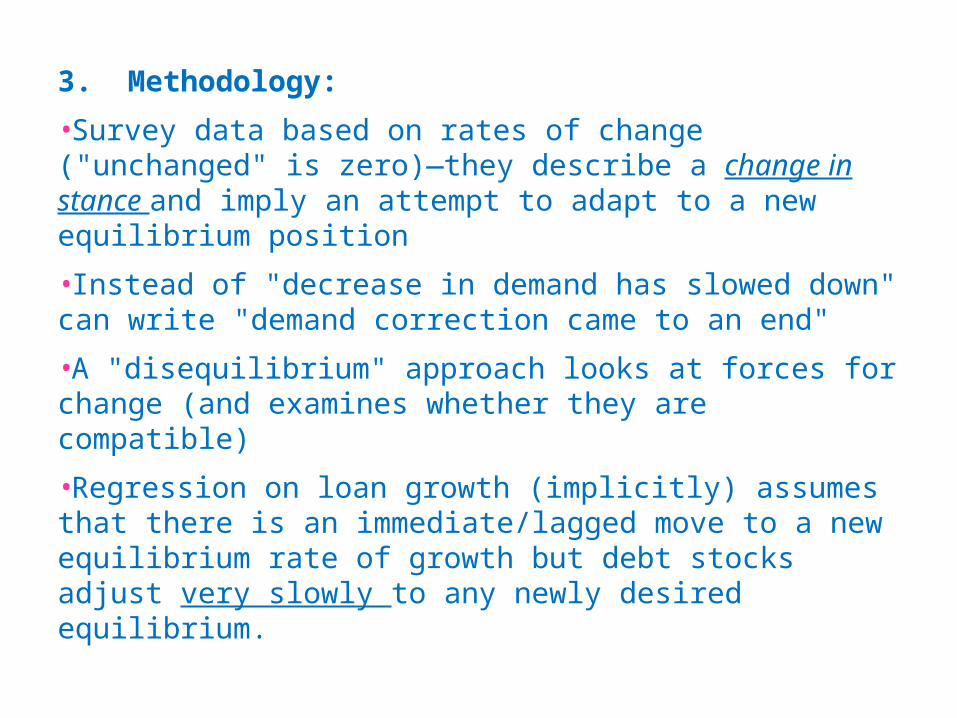

3. Methodology:

•Survey data based on rates of change ("unchanged" is zero)—they describe a change in stance and imply an attempt to adapt to a new equilibrium position

•Instead of "decrease in demand has slowed down" can write "demand correction came to an end"

•A "disequilibrium" approach looks at forces for change (and examines whether they are compatible)

•Regression on loan growth (implicitly) assumes that there is an immediate/lagged move to a new equilibrium rate of growth but debt stocks adjust very slowly to any newly desired equilibrium.

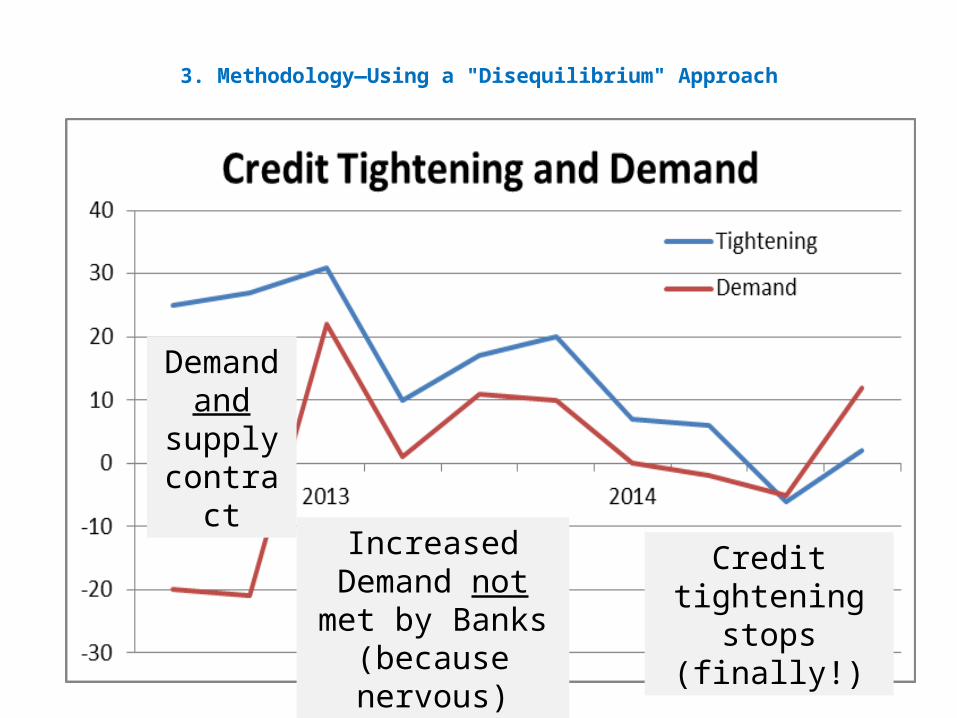

3. Methodology—Using a "Disequilibrium" Approach

Survey beginsIncreased Demand not met by Banks (because nervous)

Demand and

supply contract

Credit tightening stops (finally!)

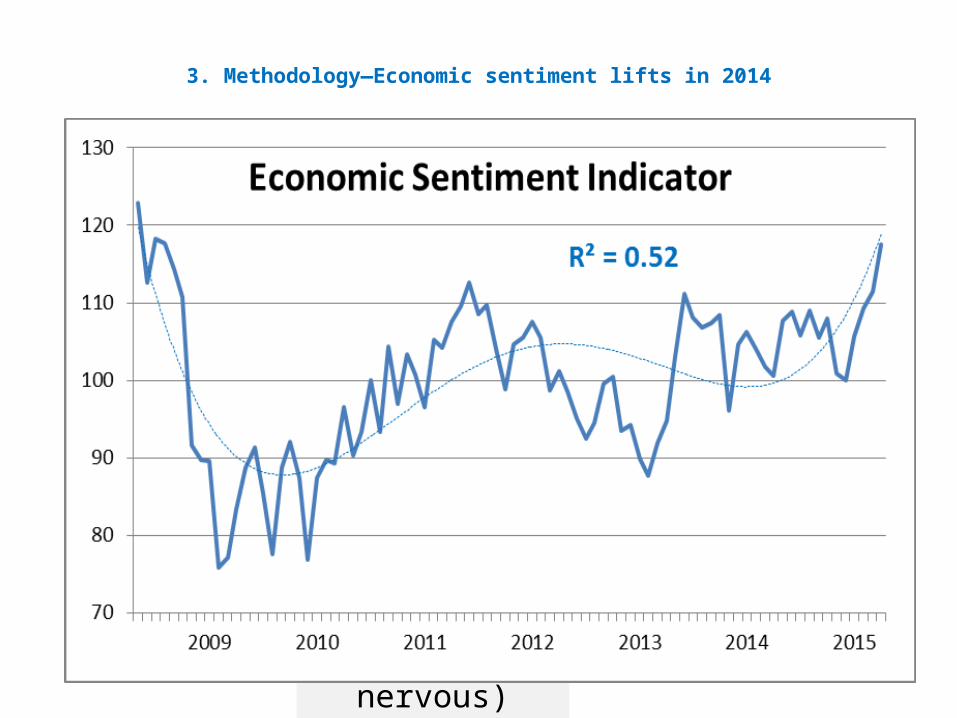

3. Methodology—Economic sentiment lifts in 2014

Survey beginsIncreased Demand not met by Banks (because nervous)

Demand and Supply contract

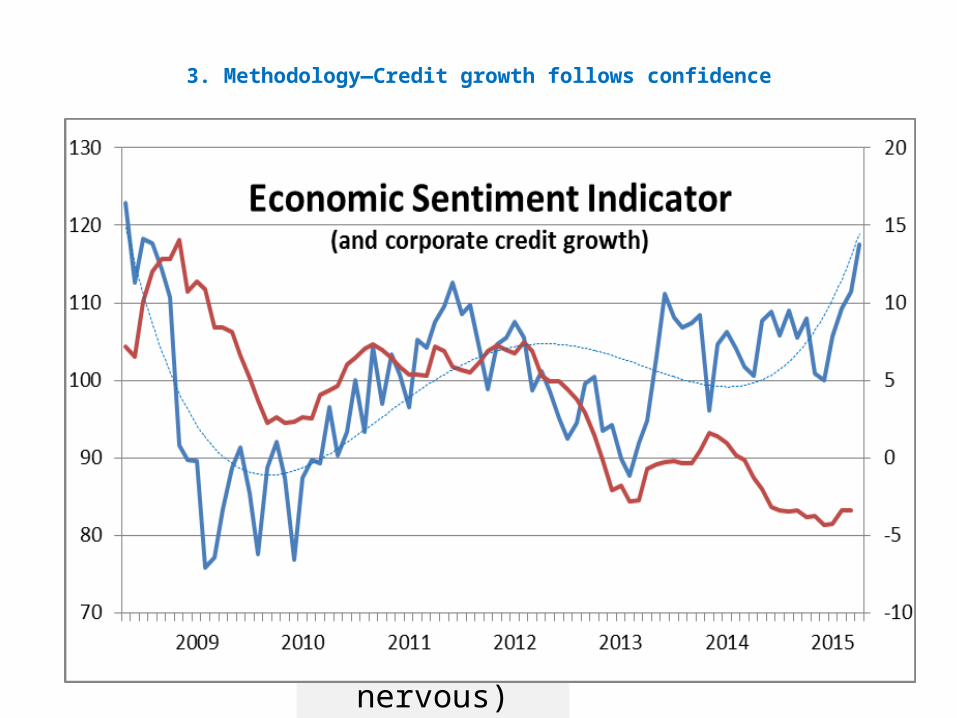

3. Methodology—Credit growth follows confidence

Survey beginsIncreased Demand not met by Banks (because nervous)

Demand and Supply contract

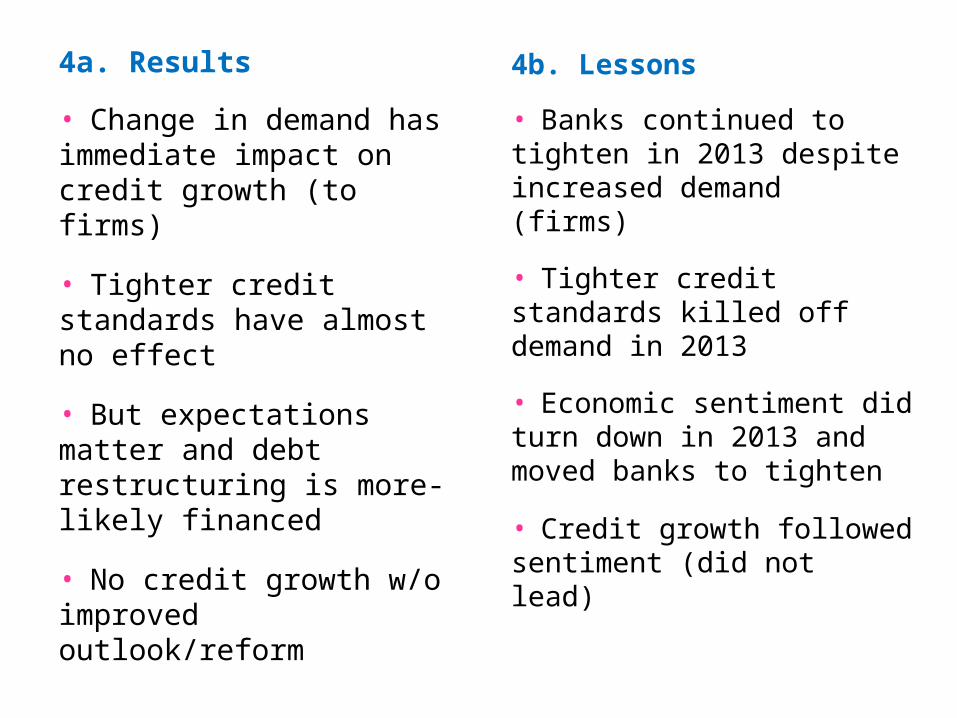

4b. Lessons

• Banks continued to tighten in 2013 despite increased demand (firms)

• Tighter credit standards killed off demand in 2013

• Economic sentiment did turn down in 2013 and moved banks to tighten

• Credit growth followed sentiment (did not lead)

4a. Results

• Change in demand has immediate impact on credit growth (to firms)

• Tighter credit standards have almost no effect

• But expectations matter and debt restructuring is more-likely financed

• No credit growth w/o improved outlook/reform

Summary•Limited data set and eager to exploit for insights—understandable and in line with other studies

•But shouldn't lose sight of the overall context (there may be more to say than first thought)

•In particular, insight into second credit crunch (and the second dip in the recession) is very important

•And enterprises/investment are the real story

•Could summarise story from aggregate data

•Value to regression and "disequilibrium" approach

•Banks dented nascent recovery but sentiment is up!