Embed Size (px)

Citation preview

Journal of International Development

J. Int. Dev. 15, 675–692 (2003)

Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/jid.1017

FACTORS THAT INFLUENCE THEEXPANSION OF THE MICROENTERPRISE

SECTOR: RESULTS FROM THREENATIONAL SURVEYS IN ZIMBABWE

LISA DANIELS*

Department of Economics, Washington College, Chestertown, MD, USA

Abstract: Using panel data from three nationwide surveys in Zimbabwe, an error

components model is estimated to explore the factors that drive the small-enterprise sector.

Among labour-intensive industries in urban areas, entry of new enterprises appears to be

driven by surplus labour. This is supported by low barriers to entry and the negative

relationship between economic growth and entry rates. In contrast, entry in capital-intensive

industries is unrelated to economic growth and it is characterized by significant barriers to

entry, including capital, working capital, and proprietor experience. With the exception of

labour-intensive industries in rural areas, entry in all other small-enterprise industries is

positively correlated with agricultural income. Copyright # 2003 John Wiley & Sons, Ltd.

1 INTRODUCTION

Limited opportunities in the formal sector and high unemployment rates in many African

countries have led to increased attention on the micro- and small-enterprise (MSE) sector.

This is not surprising given the relatively high proportion of the population that is engaged

in MSEs in many countries. For example, the MSE sector employs 22 per cent on average

of the adult population in five southern African countries compared to only 15 per cent in

the formal sector.1 Furthermore, Mead (1993) reports that over 40 per cent of the increase

in the labour force in the 1980s was absorbed by the MSE sector in five countries in

southern and eastern Africa.

Copyright # 2003 John Wiley & Sons, Ltd.

*Correspondence to: Dr Lisa Daniels, Department of Economics, Washington College, 300 Washington Avenue,Chestertown, MD 21620, USA. E-mail: [email protected] MSE is defined as a business activity that employs 50 or fewer workers and markets at least 50 per cent of itsoutput. The adult population is defined as 15 years or older. The five countries include: Zimbabwe (Daniels,1994), Botswana (Daniels and Fisseha, 1992), Malawi (Daniels and Ngwira, 1992), Lesotho (Fisseha, 1991), andSwaziland (Fisseha and McPherson, 1991). The formal sector is defined as the set of businesses that is registered.

Because of the growing numbers of MSEs and limited employment opportunities in the

formal sector, many policy makers have turned to the MSE sector as a source of

employment creation and economic growth. The sustainability of employment in the

MSE sector, however, is uncertain. Furthermore, the relationship between economic

growth and the MSE sector is not well understood.

The lack of information on employment creation and economic growth arises from

methodological limitations of previous studies. For example, many studies have focused

on a set of firms at one point in time.2 While these studies provide valuable information on

the existing industrial structure, they do not examine entry and exit of MSEs. Furthermore,

these studies cannot document the relationship between economic growth and changes in

the MSE sector. Studies that follow a set of firms over time improve the ability to examine

changes within firms, however, they do not examine entry of new MSEs. Despite these

limitations, a limited number of studies have provided rough estimates of entry rates in

developing countries (Liedholm, 1990; Cortes et al., 1987). Liedholm estimated entry

based on existing MSEs for a one-year period in Sierra Leone. Because the estimates did

not include firms that opened and folded during the time period under examination, the

estimates had a downward bias. Cortes et al. estimated entry rates based on government

statistics for two cities in Colombia. These rates also had a downward bias, however,

because they did not include small establishments and may not have included firms that

opened and closed within the time period. Although both studies estimate entry rates, they

do not explore the factors that influence entry.

This paper addresses the limitations mentioned above by using information from three

nationwide surveys conducted in 1991, 1993 and 1998, which covered a total of 17 551

existing MSEs and 2556 closed MSEs in Zimbabwe. First, a more accurate measure of

entry is estimated based on existing and closed MSEs. Second, the determinants of entry

are explored using industrial organization theory as a conceptual framework. While this

framework has been used extensively to examine entry in industrialized countries, the

factors that drive MSE entry have not been systematically explored in developing

countries. Finally, unlike previous studies, this study measures the relationship between

MSE entry and economic growth. With this improved data set, expanded conceptual

framework, and incorporation of economic growth, an error components model is

estimated to examine the determinants of MSE entry over the ten-year period from

1988 to 1997.3 Several questions will be addressed. What is the relationship between

economic growth and the entry of MSEs? Are MSEs driven by surplus labour or market

demand? For example, do people turn to the MSE sector as a means of survival during

difficult economic times or are new firms driven by consumer demand for MSE products?

The results suggest that both labour surplus and market demand play a role in firm entry.

Among labour-intensive industries in urban areas, entry appears to be driven by an excess

supply of labour, as indicated by the negative relationship between economic growth and

entry rates.4 Furthermore, the low barriers to entry in these industries suggests that

2These studies include but are not limited to: Daniels, 1994; Daniels and Fisseha, 1992; Daniels and Ngwira, 1992;Fisseha, 1991; Fisseha and McPherson, 1991; McPherson, 1991, 1998; Parker with Torres, 1994; Daniels et al., 1995.3The microenterprises included in the three surveys comprise all business activities that employ 50 or fewerworkers and market at least 50 per cent of their output. There is no distinction made between formal or informalenterprises. Although both registered and unregistered enterprises are included in the survey, the majority ofenterprises included were not registered at the time of the survey.4An industry is defined as ‘the set of firms that produce products that are viewed as close substitutes byconsumers’ (Varian, 1987). In particular, industries within the MSE sectoer will be categorized by the standardindustrial classification four-digit codes.

676 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

they provide an alternative source of income for unskilled labour with limited access to

capital. In contrast, entry in capital-intensive industries is characterized by significant

barriers to entry, including capital (i.e., expenditures on buildings and equipment),

working capital (i.e., cash needed for weekly operating expenses) and proprietor

experience. Although entry into capital-intensive industries is not related to economic

growth, it does not appear to be driven by surplus labour. Finally, entry into all industries,

with the exception of labour-intensive industries in rural areas, is positively correlated

with agricultural income.

This paper begins with hypotheses related to MSE entry in Section 2 followed by the

sampling methods used for this study in Section 3. Section 4 describes the ten-year period

under review, including the impact of the drought and the major components of the

structural adjustment program introduced in 1991. Changes in the MSE sector from 1988

to 1997 are described in Section 5 followed by the results of the entry model in Section 6.

Finally, Section 7 offers brief conclusions.

2 HYPOTHESES RELATED TO MSE ENTRY

There are two conflicting views about the factors that drive firm entry: the market-demand

hypothesis and the labour-supply hypothesis. The market-demand hypothesis assumes that

firm entry is primarily driven by consumer demand. This hypothesis has been supported by

several studies that have shown that the demand for MSE products increases as rural

household income increases (Deb and Hossain, 1984; Hazell and Roell, 1983; King and

Byerlee, 1978). Alternatively, the labour-supply hypothesis holds that firm entry is driven

by an excess supply of labour. In this case, people enter MSE industries in search of

alternative income sources regardless of demand. Proponents of this hypothesis believe

that MSEs contribute little to the economy. While many people believe that both

hypotheses are relevant, some articles suggested a more polarized view. For example,

Biggs et al. (1988) report that ‘as agents of economic development, very small enterprises

are, to put it bluntly, of little interest’. Although the labour-supply hypothesis has not been

empirically supported, Daniels (1994) shows that the majority of MSEs in Zimbabwe are

in low-profit industries that require little skill or capital.

This paper argues that both hypotheses may be correct, but that they may apply to

different MSE industries. In particular, some industries within the MSE sector may be

driven primarily by supply factors while others may be more affected by demand factors.

Firms that are driven primarily by supply factors would most likely include labour-

intensive MSE industries that are characterized by low costs of entry. These include

industries such as basket making, vending farm products, and crocheting as illustrated in

Table 1. Limited capital, skills, or experience would be necessary to enter these industries.

Alternatively, firms driven by demand factors may would most likely include capital-

intensive industries that require large expenditures on capital and high levels of skills or

experience.5 These include industries such as general traders, grocers, auto works, and

electrical repairs.

5The chow test, which tests the hypothesis that some or all of the regression coefficients are different in subsets ofthe model, is used in the entry model presented later in the paper. The results reject the null hypothesis that thecoefficients are the same within labour- and capital-intensive industries. This suggests that entry of capital- andlabour-intensive firms is driven by different factors.

The Expansion of the Microenterprise Sector 677

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

Within the industrial organization literature, the factors that influence entry are

separated into two categories: barriers to entry and entry-inducing factors. Barriers to

entry are expected to be negatively correlated with entry. Studies in the US, Canada and

Europe indicate that significant barriers to entry include market concentration, advertising,

economies of scale, capital expenditures, human capital requirements, and government

policies (Acs and Audretsch, 1989; Duetsch, 1985; Duetsch, 1975; Gorecki, 1975;

Hamilton, 1985; Hause and Du Rietz, 1984; Khemani and Shapiro, 1986; MacDonald,

1986; Mansfield, 1962; Orr, 1974). If it is true that capital-intensive MSEs are driven by

market demand, these factors should be significant barriers to entry. Among labour-

intensive MSEs, however, barriers to entry may not exist.

Entry-inducing factors are expected to be positively correlated with entry. The primary

entry-inducing factor is high profits. Economic theory predicts that potential entrepreneurs

will be attracted to industries with high profits. The ability to enter an industry with high

profits may, however, be affected by an individual’s experience or their access to capital.

Although MSEs within capital-intensive industries generate higher profits as illustrated in

Table 1, many individuals are forced to choose labour-intensive industries that require low

start-up capital, low working capital, and can be opened within their towns or at their home.

In addition to growth within individual MSE industries, growth within the economy

should also affect entry. As the gross domestic product increases, proprietors within

labour-intensive industries may leave the MSE sector in search of formal sector jobs.

Alternatively, within capital-intensive industries, an increase in GDP may lead to higher

entry rates if these MSEs are driven by market demand.

Table 1. Capital expenditures is based on initial expenses for building and equipment

Sector Average capital expenditures Average annual profits(US dollars) (US dollars)

Capital-intensive industries

General trader 3532 5678

Grocery 876 19 250

Auto works 872 4173

Electrical repair 560 1438

Welding 315 1372

Hairdresser/barber 230 2428

Construction 161 4692

Carpentry 78 794

Tailor/dressmaker 75 599

Average 744 4491

Labour-intensive industries

Knitting 71 600

Vending drinks 63 365

Shoework/repairs 47 111

Weaving 44 736

Vending hardware 21 5063

Vending wood-based products 21 797

Vending garments 20 734

Vending food 13 386

Crocheting 6 272

Vending farm products 4 282

Grass/cane/bamboo 0 219

Average 28 870

Source: 1993 and 1998 Survey Data.

678 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

3 SAMPLING METHODS6

The data for this study were collected by three nationwide surveys of MSEs in Zimbabwe

funded by the United States Agency for International Development (McPherson, 1991;

Daniels, 1994; McPherson, 1998). An MSE was defined as any business activity that

employed 50 or fewer employees and marketed at least 50 per cent of its product.7

The sample for the 1991 survey was selected by using a stratified, one-stage cluster

sampling technique. This involved three steps. First, the country was divided into eight

strata based on population density and commercial activities. Urban areas were defined as

cities with more than 20 000 inhabitants as estimated by the 1982 census. Within the urban

areas, four strata were used: high-density areas, low-density areas, commercial districts

and industrial areas. The four strata in rural areas were small towns, growth points, district

councils, and rural councils.8 Second, a random sample of enumeration areas (EAs) within

each stratum was selected. Finally, all households, businesses, and mobile vendors in each

selected EA were interviewed. Individuals at households were also asked if they had

operated a business in the past that had folded.

In the 1993 and 1998 surveys, a subset of EAs from the 1991 study was revisited. The

reduction in the number of EAs was based on an ex-post analysis of the sample size in

1991 that indicated over-sampling in low-density areas, commercial districts, industrial

areas, and growth points and under-sampling in the remaining strata (McPherson and

Parker, 1993). A total of 17 551 proprietors from existing MSEs and 2556 folded MSEs

were interviewed in the three surveys combined.

4 DESCRIPTION OF THE TEN-YEAR PERIOD UNDER REVIEW

As described above, this paper is based on three national surveys of microenterprises

conducted in 1991, 1993 and 1998. Because the surveys also included retrospective

questions and questions about enterprises that folded prior to each survey, annual data on

entry and exit of MSEs from 1988 to 1997 can be constructed. During this period, the

growth rate of the real GDP fluctuated from a high of 7.3 per cent in 1996 to a decrease of

nine per cent in 1992 as illustrated in Table 2. These large fluctuations in real GDP growth

can be partially explained by two major events that affected not only the microenterprise

sector, but the economy as a whole: the introduction of the Economic Structural

Adjustment Program (ESAP) and the drought of the 1991–92 agricultural season. Each

of these and their potential impact on the microenterprise sector are described in this

section.

ESAP was introduced in 1991 to promote higher medium- and long-term growth and to

reduce poverty in Zimbabwe (Government of Zimbabwe, 1991). There were four primary

components of the programme: deregulation, trade liberalization, fiscal policy reforms and

monetary policy reforms. The first component, deregulation, deals with the removal of

6A complete description of the methodology used to collect this data can be found in McPherson (1991), Daniels(1994) and McPherson (1998).7Although 50 employess is high for a definition of micro and small enterprises, only 1.6 per cent of all enterpriseshad more than 10 employees. The results of the model primarily reflect, therefore, smaller enterprises with ten orfewer employees.8Growth points are towns designated by the government to promote rural development. Incentives are provided inthese towns to promote the establishment and growth of businesses. District and rural councils are administrativeareas with low population densities.

The Expansion of the Microenterprise Sector 679

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

many of the regulations controlling business activities. For example, zoning, licensing,

labour market regulations and price and marketing controls have often been cited as

impediments to MSE activities (Hess, 1993; UNIDO, 1988; Jasset and Jirira, 1987). Under

ESAP, plans to change these regulations were intended to ease the operating environment

for MSEs in Zimbabwe.

Trade liberalization, the second component of ESAP, also has implications for MSEs.

Foreign exchange allocation changes and removal of import restrictions under ESAP

could have both a positive and negative impact on MSEs. For example, foreign exchange

liberalization and removal of import restrictions should alleviate input or raw material

shortages frequently identified as a major constraint to MSE activity (Mead and Kunjeku,

1993; Zimconsult, 1992; McPherson, 1991; IMANI, 1990). Greater availability of

imported goods, however, could increase MSE failure rates.

The third component of ESAP, fiscal policy reforms, includes tax and expenditure

reductions. Corporate tax rates were 45 per cent while individual taxes were as high as 60

per cent at the beginning of ESAP. Although this tax structure has been cited repeatedly as

an impediment to MSE activity (Human Resources, 1990; USAID, 1990), tax reductions

do not have a large direct impact on the MSE community because 95 per cent of firms

report that they do not pay taxes. Furthermore, the nationwide survey in 1993 showed that

three-quarters of all firms made less than Z$4801, which was the minimum individual

taxable income in the 1992–93 tax year (Daniels, 1994). The indirect effect of high taxes

may be that firms remain unregistered in order to avoid taxes.

Under the fourth component, monetary policy reforms, interest rates were liberalized

and now play a greater role in allocating credit. Previously banks had a strong incentive to

limit credit to larger, well-established firms. With higher interest rates, investment by

larger firms may decline, but credit is now available to a wider range of firms. The

beneficiaries of this policy are more likely to be medium-sized firms rather than MSEs.

The MSE operating environment was also affected by the drought of the 1991–92

agricultural season. During this period, the southern African region experienced the worst

drought of the century. Rainfall in Zimbabwe was only 43 per cent of the average annual

rainfall from 1970 to 1991. Furthermore, the World Bank estimated that the external debt

increased to more than Z$50 billion in 1992 because of the drought (The Herald, 12 March

Table 2. Changes in the growth rate of real gross domesticproduct in Zimbabwe

Year Percentage change inreal gross domestic product(Constant 1995 US dollars)

1988 7.6

1989 5.2

1990 7.0

1991 5.5

1992 �9.0

1993 1.3

1994 6.8

1995 �0.7

1996 7.3

1997 3.2

Source: World Development Indicators.

680 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

1992). This was partly due to an 80 per cent reduction in the maize harvest and a 35 per

cent reduction in agricultural output compared with the previous year.

The MSE sector was affected by the drought through decreased income levels and

corresponding lower demand for MSE products. For example, results from the 1993

national survey showed that 76 per cent of proprietors in both urban and rural areas

reported that the volume of their business decreased because of the drought. The sector

was also affected by decreased availability of inputs in sectors tied to agriculture and a

corresponding increase in the prices of agricultural raw materials. The results from the

1993 survey showed, for example, that one quarter of all firms closed in 1992 because of

input problems, compared with only eight per cent in 1991 (Daniels, 1994).

In addition to the drought of 1992, Zimbabwe experienced a second drought in 1995.

Unlike the 1992 drought when GDP growth was a negative nine per cent, the growth rate

was negative 0.7 per cent in 1995. Because the second drought had a much smaller impact,

the economy recovered much more quickly over the following year.

5 CHANGES IN THE MSE SECTOR FROM 1988 TO 1997

Data from the three national surveys indicate that there was an 8.5 per cent increase in the

overall number of MSEs between 1991 and the 1993 surveys and an 8.7 per cent decrease

in MSEs between the 1993 and 1998 surveys. These statistics support the labour-surplus

hypothesis that MSEs are started in difficult economic times as a means of survival, since

Zimbabwe experienced the drought and the nine per cent decrease in real GDP in the 1991

to 1993 period. Examining the entry rates on an annual basis (i.e., total MSEs born in one

year divided by the number of MSEs existing at the beginning of the same year) shows,

however, that there is no correlation between the GDP and the overall entry rate of all

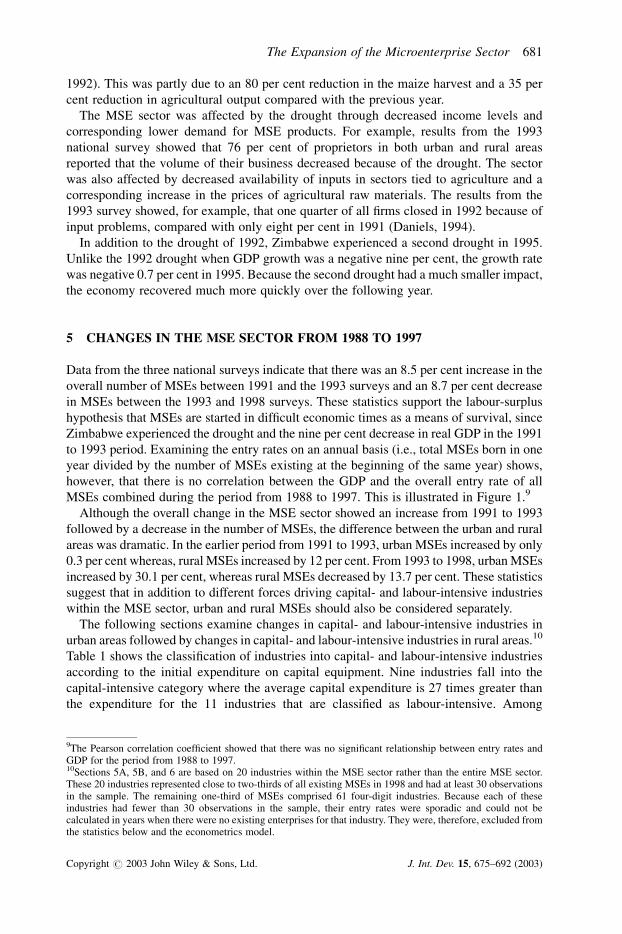

MSEs combined during the period from 1988 to 1997. This is illustrated in Figure 1.9

Although the overall change in the MSE sector showed an increase from 1991 to 1993

followed by a decrease in the number of MSEs, the difference between the urban and rural

areas was dramatic. In the earlier period from 1991 to 1993, urban MSEs increased by only

0.3 per cent whereas, rural MSEs increased by 12 per cent. From 1993 to 1998, urban MSEs

increased by 30.1 per cent, whereas rural MSEs decreased by 13.7 per cent. These statistics

suggest that in addition to different forces driving capital- and labour-intensive industries

within the MSE sector, urban and rural MSEs should also be considered separately.

The following sections examine changes in capital- and labour-intensive industries in

urban areas followed by changes in capital- and labour-intensive industries in rural areas.10

Table 1 shows the classification of industries into capital- and labour-intensive industries

according to the initial expenditure on capital equipment. Nine industries fall into the

capital-intensive category where the average capital expenditure is 27 times greater than

the expenditure for the 11 industries that are classified as labour-intensive. Among

9The Pearson correlation coefficient showed that there was no significant relationship between entry rates andGDP for the period from 1988 to 1997.10Sections 5A, 5B, and 6 are based on 20 industries within the MSE sector rather than the entire MSE sector.These 20 industries represented close to two-thirds of all existing MSEs in 1998 and had at least 30 observationsin the sample. The remaining one-third of MSEs comprised 61 four-digit industries. Because each of theseindustries had fewer than 30 observations in the sample, their entry rates were sporadic and could not becalculated in years when there were no existing enterprises for that industry. They were, therefore, excluded fromthe statistics below and the econometrics model.

The Expansion of the Microenterprise Sector 681

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

the MSEs within these industries, 68 per cent were in labour-intensive industries and

32 per cent were in capital-intensive industries.

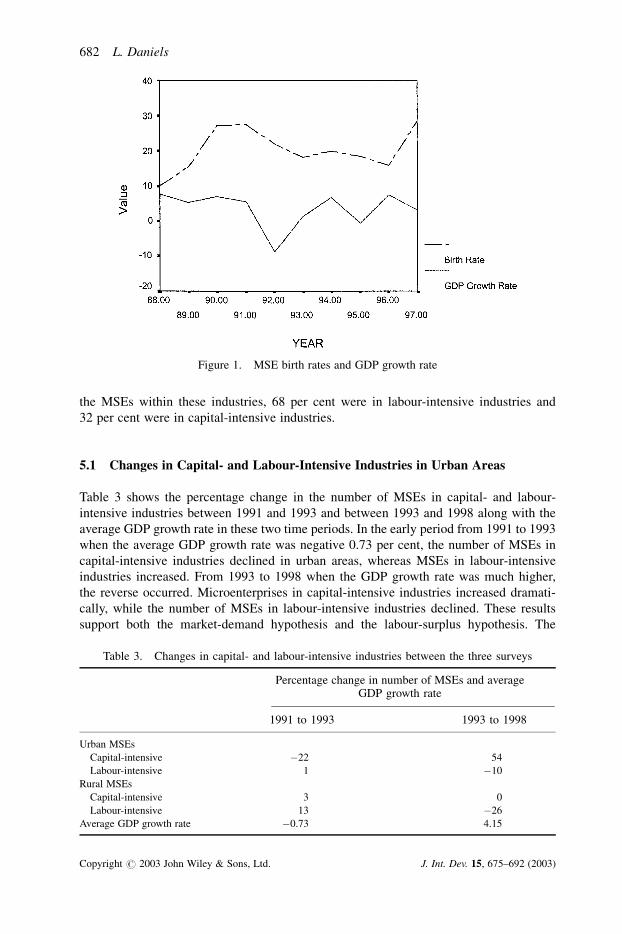

5.1 Changes in Capital- and Labour-Intensive Industries in Urban Areas

Table 3 shows the percentage change in the number of MSEs in capital- and labour-

intensive industries between 1991 and 1993 and between 1993 and 1998 along with the

average GDP growth rate in these two time periods. In the early period from 1991 to 1993

when the average GDP growth rate was negative 0.73 per cent, the number of MSEs in

capital-intensive industries declined in urban areas, whereas MSEs in labour-intensive

industries increased. From 1993 to 1998 when the GDP growth rate was much higher,

the reverse occurred. Microenterprises in capital-intensive industries increased dramati-

cally, while the number of MSEs in labour-intensive industries declined. These results

support both the market-demand hypothesis and the labour-surplus hypothesis. The

Figure 1. MSE birth rates and GDP growth rate

Table 3. Changes in capital- and labour-intensive industries between the three surveys

Percentage change in number of MSEs and averageGDP growth rate

1991 to 1993 1993 to 1998

Urban MSEs

Capital-intensive �22 54

Labour-intensive 1 �10

Rural MSEs

Capital-intensive 3 0

Labour-intensive 13 �26

Average GDP growth rate �0.73 4.15

682 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

capital-intensive industries appear to expand in good economic times, which is consistent

with the market-demand hypothesis. Alternatively, labour-intensive industries expand

during poor economic times, which is consistent with the labour-surplus hypothesis.

Figure 2 shows the annual entry rates from 1988 to 1997 for capital- and labour-

intensive industries in urban areas. While the patterns are quite similar, Figure 2 shows that

the entry rates of labour-intensive firms were much higher than capital-intensive

industries, particularly during the early 1990s, which coincides with both the drought

and the introduction of ESAP.

5.2 Changes in Capital- and Labour-Intensive Industries in Rural Areas

The percentage change in capital- and labour-intensive industries in rural areas between

1991 and 1993 and between 1993 and 1998 are shown in Table 3. The changes in the

capital-intensive industries do not follow the same patterns as the capital-intensive

industries in urban areas. Instead, capital-intensive industries grew by three per cent in

the early period from 1991 to 1993 and experienced no change in the latter period from

1993 to 1998. These results suggest that the capital-intensive industries in rural areas are

not as closely tied to overall changes in the economy as their urban counterparts.

Labour-intensive industries in rural areas followed the exact same pattern as their urban

counterparts. They expanded during poor economic times and contracted during better

economic times, consistent with the labour-surplus hypothesis.

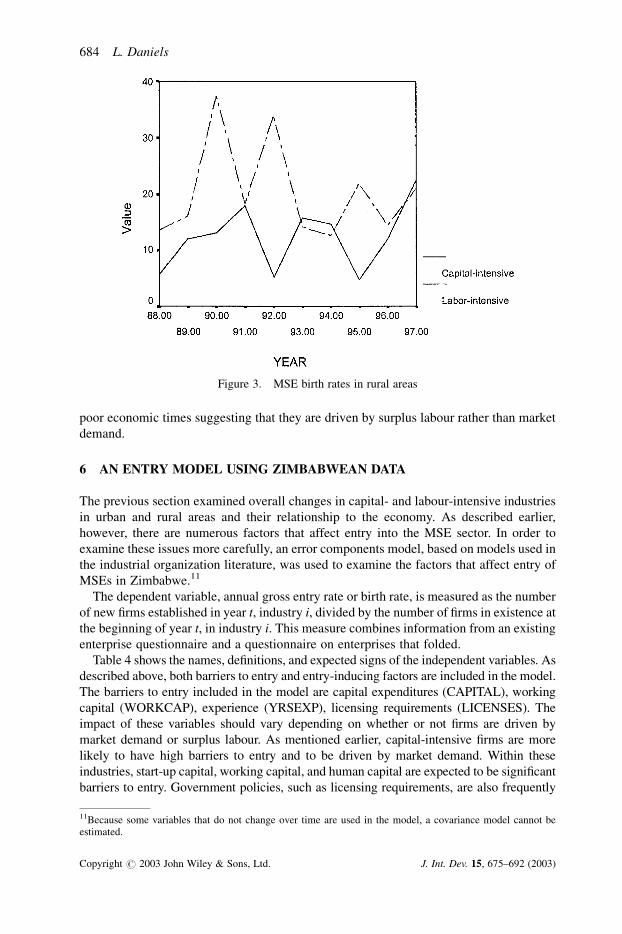

Figure 3 shows the annual entry rates from 1988 to 1997 for capital- and labour-

intensive industries in rural areas. Unlike the urban entry rates in Figure 2, the entry rates

of capital- and labour-intensive industries in Figure 3 follow almost exact opposite

patterns. Again, the labour-intensive industries appear to expand dramatically during

Figure 2. MSE birth rates in urban areas

The Expansion of the Microenterprise Sector 683

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

poor economic times suggesting that they are driven by surplus labour rather than market

demand.

6 AN ENTRY MODEL USING ZIMBABWEAN DATA

The previous section examined overall changes in capital- and labour-intensive industries

in urban and rural areas and their relationship to the economy. As described earlier,

however, there are numerous factors that affect entry into the MSE sector. In order to

examine these issues more carefully, an error components model, based on models used in

the industrial organization literature, was used to examine the factors that affect entry of

MSEs in Zimbabwe.11

The dependent variable, annual gross entry rate or birth rate, is measured as the number

of new firms established in year t, industry i, divided by the number of firms in existence at

the beginning of year t, in industry i. This measure combines information from an existing

enterprise questionnaire and a questionnaire on enterprises that folded.

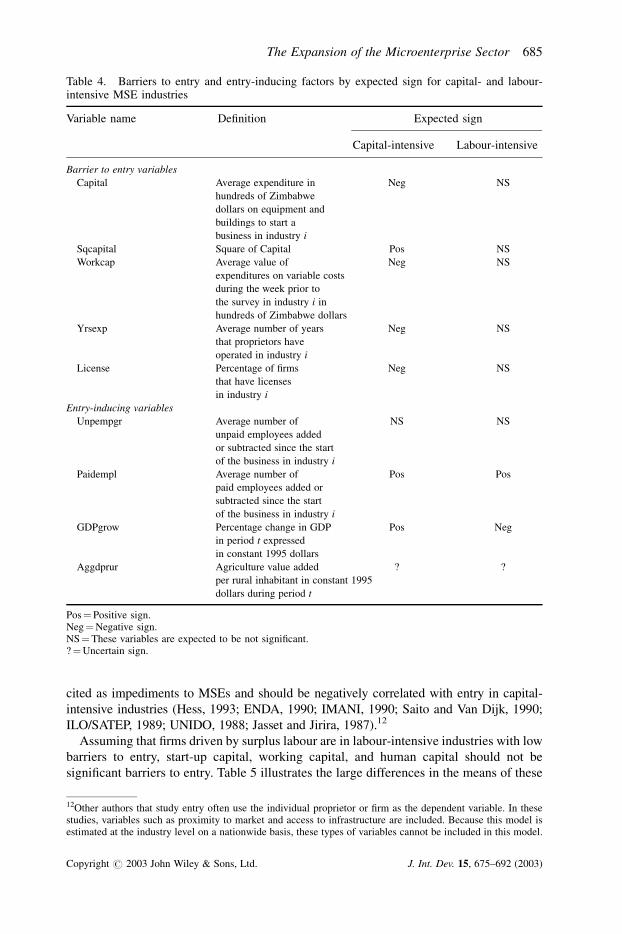

Table 4 shows the names, definitions, and expected signs of the independent variables. As

described above, both barriers to entry and entry-inducing factors are included in the model.

The barriers to entry included in the model are capital expenditures (CAPITAL), working

capital (WORKCAP), experience (YRSEXP), licensing requirements (LICENSES). The

impact of these variables should vary depending on whether or not firms are driven by

market demand or surplus labour. As mentioned earlier, capital-intensive firms are more

likely to have high barriers to entry and to be driven by market demand. Within these

industries, start-up capital, working capital, and human capital are expected to be significant

barriers to entry. Government policies, such as licensing requirements, are also frequently

Figure 3. MSE birth rates in rural areas

11Because some variables that do not change over time are used in the model, a covariance model cannot beestimated.

684 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

cited as impediments to MSEs and should be negatively correlated with entry in capital-

intensive industries (Hess, 1993; ENDA, 1990; IMANI, 1990; Saito and Van Dijk, 1990;

ILO/SATEP, 1989; UNIDO, 1988; Jasset and Jirira, 1987).12

Assuming that firms driven by surplus labour are in labour-intensive industries with low

barriers to entry, start-up capital, working capital, and human capital should not be

significant barriers to entry. Table 5 illustrates the large differences in the means of these

Table 4. Barriers to entry and entry-inducing factors by expected sign for capital- and labour-intensive MSE industries

Variable name Definition Expected sign

Capital-intensive Labour-intensive

Barrier to entry variables

Capital Average expenditure in Neg NS

hundreds of Zimbabwe

dollars on equipment and

buildings to start a

business in industry i

Sqcapital Square of Capital Pos NS

Workcap Average value of Neg NS

expenditures on variable costs

during the week prior to

the survey in industry i in

hundreds of Zimbabwe dollars

Yrsexp Average number of years Neg NS

that proprietors have

operated in industry i

License Percentage of firms Neg NS

that have licenses

in industry i

Entry-inducing variables

Unpempgr Average number of NS NS

unpaid employees added

or subtracted since the start

of the business in industry i

Paidempl Average number of Pos Pos

paid employees added or

subtracted since the start

of the business in industry i

GDPgrow Percentage change in GDP Pos Neg

in period t expressed

in constant 1995 dollars

Aggdprur Agriculture value added ? ?

per rural inhabitant in constant 1995

dollars during period t

Pos¼Positive sign.Neg¼Negative sign.NS¼These variables are expected to be not significant.?¼Uncertain sign.

12Other authors that study entry often use the individual proprietor or firm as the dependent variable. In thesestudies, variables such as proximity to market and access to infrastructure are included. Because this model isestimated at the industry level on a nationwide basis, these types of variables cannot be included in this model.

The Expansion of the Microenterprise Sector 685

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

barriers to entry among capital- and labour-intensive industries as well as the percentage

of firms with licenses. Licensing may not be a barrier to entry in labour-intensive

industries, partly due to the large numbers of MSEs in labour-intensive industries, which

makes licensing more difficult to enforce. For example, the average number of firms in a

capital-intensive industry is 19 823 compared with 35 081 in a labour-intensive industry.13

Other barriers to entry from the US, Canadian and European literature mentioned

earlier, such as market concentration, advertising and economies of scale would not be

relevant in Zimbabwe for several reasons. First, MSEs are too numerous to allow market

concentration. In 1998, there were 860 000 MSEs in Zimbabwe. Within the 20 industries

examined in this model, the average number of MSEs was 28 215. Second, while some

limited advertising may occur, it may only be within a small geographic area such as a

town. This type of advertising would not block firms from entering the industry throughout

the rest of the country. Third, most MSEs do not exhibit economies of scale. For example,

43 per cent of all firms were owned and operated by the proprietor alone and 97 per cent of

all MSEs had only one to four workers.

Entry-inducing factors are typically represented by industry employment growth. Unlike

manufacturing enterprises in industrialized countries, however, MSEs in Zimbabwe

employ both paid and unpaid employees. Unpaid employees are usually immediate family

members or relatives that may not have other employment opportunities. Because this type

of employment may not represent industry growth or positive profits, unpaid employment

(UNPEMPGR) growth is measured separately from paid employment growth (PAI-

DEMPL) to test this hypothesis. Daniels (1995) shows, for example, that profits are not

significantly correlated with unpaid employment growth using firm-level data.

In addition to growth within the industry, growth within the economy is also included in

the model as the percentage change in the real gross domestic product (GDPGROW). For

example, more individuals may turn to the MSE sector as an alternative source of income

as GDP declines, particularly in labour-intensive industries. In other words, GDP can be

considered as a proxy for wages in the formal economy. If the market-demand hypothesis

is correct, then entry should rise as GDP rises if MSEs are driven by market demand for

MSE products.

Finally, as described above, as incomes from agriculture rise, the demand for MSE

products may also rise. Alternatively, higher agricultural wages could also draw proprietors

Table 5. Values of barriers to entry for capital- and labour-intensive industries

Capital-intensive Labour-intensiveindustries industries

Capital (Mean value) Z$5,748* Z$380*

Workcap (Mean value) Z$897* Z$113*

Yrsexp (Mean value) 9 years* 8 years*

License (% of MSEs with licenses) 26%* 10%*

US$1.00¼Z$6.70.*Significant difference between capital- and labour-intensive industries at the �¼ 0.001 level.Source: 1998 Survey Data for capital, workcap, and yrsexp.1993 Survey Data for license.

13The average number of enterprises stated in this section is extrapolated to the national level. For this reason, thenumbers reported here are larger than the number of enterprises include in the survey that was mentioned in theintroduction.

686 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

away from the MSE sector. The agriculture value added per rural inhabitant (AGGDPRUR)

is therefore included in the model to test these hypotheses.

7 RESULTS

Table 6 presents the results of the entry model for capital- and labour-intensive industries

in urban and rural areas. As expected, the forces that drive entry are different for the

labour- and capital-intensive industries as well as for the same industries in the urban and

rural areas. The results are reported for the four models below.

7.1 Capital-Intensive Industries in Urban Areas

Among capital-intensive industries in urban areas, industries with higher capital expen-

ditures and working capital needs have lower entry rates. This suggests that both capital

and working capital are barriers to entry. These results are not surprising given the heavy

capital requirements of these industries. As mentioned earlier, the average capital

expenditure is 27 times greater among the capital-intensive industries compared with

the labour-intensive industries.

Despite all of the studies mentioned earlier that cite licensing in Zimbabwe as a barrier

to entry, industries with greater percentages of firms with licenses did not have lower entry

rates. Licensing may not, therefore, be a strong barrier to entry as is commonly believed.

As described earlier, human capital requirements are found to be significant barriers to

entry in much of the US, Canadian and European literature. Among capital-intensive

industries in Zimbabwean urban areas, higher levels of average proprietor experience

levels did not lead to lower entry rates. This may be due to the small range of average

Table 6. Entry model results for capital- and labour-intensive industries in urban and rural areas

Urban industries Rural industries

Capital-intensive Labour-intensive Capital-intensive Labour-intensive

Variable Coefficient Coefficient Coefficient Coefficient(t-statistic) (t-statistic) (t-statistic) (t-statistic)

Capital �0.00* (�1.77) �0.00 (�0.84) �0.00* (�1.74) �0.13 (�0.53)

Sqcapital 0.00** (1.94) 0.00 (0.57) 0.00 (1.59) 0.00 (1.07)

Workcap �0.00** (�2.13) �0.01 (�0.07) 0.00 (0.45) 0.17 (0.34)

Yrsexp �1.89 (�1.22) �7.12** (�2.05) �3.58** (�2.64) 21.51 (0.88)

License 0.01 (0.47) 0.23 (0.58) �0.14 (�0.75) 0.65 (0.10)

Paidemp 5.35 (1.01) 31.58 (1.44) 2.37 (0.54) 327.55 (0.35)

Unpempgr 13.41 (0.75) �54.55 (�1.34) �19.14 (�0.25) �33.71 (�0.11)

GDP �0.16 (�0.33) �0.81* (�1.84) �1.18 (�1.25) �8.70 (�1.27)

Aggdprur 0.37** (1.96) 0.64** (3.46) 1.07** (2.85) 0.06 (0.02)

Constant �10.12 (�0.37) 1.58 (0.05) �71.29 (�1.45) �191.15 (�0.47)

No. of observations 90 110 90 110

R-square 0.26 0.18 0.24 0.07

**¼ Significant at the �¼ 0.05 level.Source: 1991, 1993 and 1998 Survey Data.

The Expansion of the Microenterprise Sector 687

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

experience levels within the majority of these industries. For example, hair dressing and

welding have the lowest levels of proprietor experience with four to five years,

respectively. The highest level of proprietor experience is in construction with 17 years

on average. The remainder of the capital-intensive industries have experience levels that

range from eight to 12 years.

Among the entry-inducing factors, capital-intensive industries in urban areas do not

respond to the overall economy. As GDP rises, there is no impact on entry levels. If GDP

growth represents opportunities in the formal sector, these results suggest that proprietors

in capital-intensive industries in urban areas will not necessarily leave the MSE sector for

the formal sector. It also suggests that the these industries are not driven by surplus labour

as predicted by the labour-supply hypothesis. Alternatively, they may be driven by market

demand as indicated by the increased entry levels as agricultural income rises. These

results coincide with other studies that have shown that the demand for MSE products

increases as rural household income increases (Deb and Hossain, 1984; Hazell and Roell,

1983; King and Byerlee, 1978).

7.2 Labour-Intensive Industries in Urban Areas

Among the labour-intensive industries in urban areas, higher capital and working capital

needs do not lead to lower entry rates. Again, given the low capital requirements within

these industries, ranging from zero to US$71 on average, these results are not surprising. It

is surprising, however, that higher levels of proprietor experience do lead to lower entry

rates. This suggests that experience is a barrier to entry. The average level of experience

within these industries is eight years with a range of five years in vending wood-based

products, hardware, and drinks to a high of 12 years in shoe work/repairs.

Similar to capital-intensive industries in urban areas, licensing does not appear to be a

barrier to entry among labour-intensive industries. Again, this is contrary to assertions

found in numerous studies about the Zimbabwean MSE sector (Hess, 1993; ENDA, 1990;

IMANI, 1990; Saito and Van Dijk, 1990; ILO/SATEP, 1989; UNIDO, 1988; Jasset and

Jirira, 1987). In general, however, licensing would more likely be a barrier to entry among

capital-intensive industries where 26 per cent of all firms have licenses compared with

only ten per cent among labour-intensive industries.

Considering the entry-inducing factors, the entry rates of labour-intensive industries in

urban areas are negatively correlated with the growth of the GDP as predicted by the

labour-surplus theory. As the economy declines, more businesses are started, whereas

growth in the economy leads to a decline in the entry rate. Again, GDP can be considered

as proxy for wages in the formal economy. In other words, as the formal sector expands,

there is no need for individuals to turn to the MSE sector as a source of income. The

agricultural value added per rural inhabitant was positively correlated with MSE entry.

As suggested by previous studies, this indicates increases in agricultural income lead to a

greater demand for MSE products. It is not surprising that entry is negatively correlated

with GDP growth and positively correlated with agricultural value added since agriculture

represents a low proportion of GDP compared to other sub-Saharan countries. Seventy

per cent of all other sub-Saharan countries have a higher agriculture value added than

Zimbabwe with a range from 23 to 58 per cent compared to 19 per cent in Zimbabwe

(World Bank, 2000).

688 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

7.3 Capital-Intensive Industries in Rural Areas

Within the capital-intensive industries in rural areas, the model showed that capital is a

barrier to entry. Again, this is not surprising since firms within these industries require

larger capital investments than the labour-intensive industries. Considering only firms

within rural areas, the average capital expenditure among capital-intensive industries is 40

times greater than the average capital expenditure among labour-intensive industries.

Greater proprietor experience was also associated with lower entry rates suggesting that

experience is a barrier to entry. As in the urban industries, a greater proportion of firms

with licenses was not associated with lower entry rates.

Among the entry-inducing factors, the entry rates of capital-intensive industries in rural

areas are not affected by growth in GDP. Again, this suggests that these industries are not

driven by surplus labour since the entry rates do not rise as GDP falls. The entry rates are

affected, however, by changes in agricultural income. As agriculture value added rises, the

entry rates of these industries also rises. Again, this supports previous studies that show

that demand for microenterprise products rise as agricultural incomes rise.

7.4 Labour-Intensive Industries in Rural Areas

Among the labour-intensive industries in rural areas, none of the coefficients of the

independent variables was significant. This suggests that there are no significant barriers to

entry or entry-inducing factors. This is not surprising since the labour-surplus theory

suggests that proprietors can enter these industries easily. It is surprising, however, that the

entry rates of these industries are not affected by changes in the economy. The labour-

surplus hypothesis indicates that proprietors turn to these industries during difficult times,

which is illustrated only in the model for labour-intensive industries in the urban areas.

These results may reflect the fact that rural households are not as connected to the overall

economy and rely more on self employment through agriculture rather than formal or

informal sector jobs.

8 CONCLUSIONS

The labour-surplus hypothesis suggests that the number of MSEs rises and falls as a

function of labour availability. Under this hypothesis, the MSE sector should increase

during difficult times. Considering labour-intensive industries in urban and rural areas, the

number of MSEs increased from 1991 to 1993 during more difficult economic times and

decreased dramatically as the economy improved from 1993 to 1998 suggesting that these

industries are driven by surplus labour. Alternatively, capital-intensive industries in urban

areas followed the exact opposite pattern suggesting that they are not driven by surplus

labour. Instead, the change in the overall number of MSEs within these industries supports

the market-demand hypothesis, which suggests that industries are driven by market

demand for microenterprise products. Although the overall change in the number of

MSEs gives some indication of the impact of the economy on the MSE sector, the four

entry models presented in this paper provide a more detailed analysis of the forces that

drive the sector. This is done by examining individual industries within the MSE sector

and the barriers to entry and entry-inducing factors that affect each industry.

The Expansion of the Microenterprise Sector 689

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

Considering the four models, the labour-supply hypothesis is supported only by the entry

rates within labour-intensive industries in urban areas, which increase during difficult

economic times. The assumption that there are limited barriers to entry in the MSE sector

is supported only by entry rates of labour-intensive industries in rural areas. Among the

remaining categories of industries, however, there are significant barriers to entry

including capital, working capital, and experience. The relative weight of these barriers

will probably vary across industries, but they are all significant.

The market-demand hypothesis is supported in all urban-area industries and capital-

intensive industries in rural areas by the positive correlation between entry rates and

increases in agricultural incomes. None of the four models showed, however, that entry

rates are positively correlated with changes in gross domestic product. This suggests that

most industries are more closely tied to agricultural incomes rather than changes in the

overall economy.

Overall, the combined results indicate that the microenterprise sector is heterogeneous.

The forces that drive the sector vary from urban to rural areas and within capital- and

labour-intensive industries. Government and donor policies towards the MSE sector

should, therefore, reflect this heterogeneity. For example, if the government wants to

promote capital-intensive industries, it should address the barriers to entry faced by these

industries, such as capital and working capital, through credit programmes. Alternatively,

if the government wants to support labour-intensive industries where individuals may

depend on MSE income for survival, then technical training may be more appropriate

since experience was a barrier to entry, but capital was not a constraint. For example,

training in business skills or technical skills may assist proprietors to enter these industries

and improve their businesses.

Again, the results from the four models should highlight the heterogeneity of the MSE

sector and its diverse needs. The results also show the need for research that breaks down

the MSE sector into different categories based on the location of the MSEs and the level of

capital and skills requirements rather than analyzing the sector as a whole.

ACKNOWLEDGEMENTS

The funding for this work was provided by the United States Agency for International

Development through a buy-in to the Growth and Equity through Microenterprise and

Institutions (GEMINI) Project, contract number DHR-5448-Q-65-9081-00.

I am grateful for the comments of Carl Eicher, Carl Liedholm, Les Manderscheid, and

Tom Reardon on an earlier version of this paper that used the first two national data sets. I

also owe special thanks to Donald Mead for his comments on the earlier paper as well as

his participation and comments during the field research for this work. Nicholas Minot

also deserves credit for his excellent comments on both versions of this paper. The funding

for this research was provided by the United States Agency for International Development

through a buy-in to the Growth and Equity through Microenterprise and Institutions

(GEMINI) Project. Any errors in this paper should be attributed to the author.

REFERENCES

Acs Z, Audretsch D. 1989. Small-firm entry in U.S. manufacturing. Economica 56(222): 255–266.

690 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

Biggs T, Grindle M, Snodgrass D. 1988. The informal sector, policy roeform, and structural

transforamtion. In Beyond the Informal Sector: Including the Excluded in Developing Countires,

Jenkins J (ed.). Institute for Contemporary Studies Press: San Francisco.

Corte M, Berry A, Ishaq A. 1987. Success in Small and Medium-Scale Enterprises: The Evidence

from Colombia. Oxford University Press: New York.

Daniels L. 1995. Entry, exit, and growth among small-scale enterprises in Zimbabwe. Ph.D.

dissertation. Michigan State University: East Lansing, MI.

Daniels L. 1994. Changes in the small-scale enterprise sector from 1991 to 1993: results of a second

nationwide survey in Zimbabwe. GEMINI Technical Report No. 71. Development Alternatives,

Inc.: Bethesda, MD.

Daniels L, Fisseha Y. 1992. Micro- and small-scale enterprises in Botswana: results of a nationwide

survey. GEMINI Technical Report No. 46. Development Alternatives, Inc.: Bethesda, MD.

Daniels L, Mead D, Musinga M. 1995. Employment and income in micro and small enterprises in

Kenya: results of a 1995 survey. GEMINI Technical Report No. 92. Development Alternatives,

Inc.: Bethesda, MD.

Daniels L, Ngwira A. 1992. Results of a nation-wide survey on micro, small, and medium enterprises

in Malawi. GEMINI Technical Report No. 53. Development Alternatives, Inc.: Bethesda, MD.

Deb NC, Hossain M. 1984. Demand for rural industries products in Bangladesh. The Bangladesh

Development Studies XII(182): 81–99.

Duetsch L. 1975. Structure, performance, and the net rate of entry into manufacturing industries.

Southern Economic Journal 41: 450–456.

Duetsch L. 1984. Entry and the extent of multiplant operations. Journal of Industrial Economics 32:

477–487.

Environmental and Developmental Activities. 1990. Women in the informal sector: a Zimbabwean

study. ENDA: Harare, Zimbabwe.

Fisseha Y. 1991. Small-scale enterprises in Lesotho: summary of a country-wide survey. GEMINI

Technical Report No. 14. Development Alternatives, Inc.: Bethesda, MD.

Fisseha Y, McPherson M. 1991. A country-wide study of small-scale enterprises in Swaziland.

GEMINI Technical Report No. 24. Development Alternatives, Inc.: Bethesda, MD.

Gorecki PK. 1976. The determinants of entry by new and diversifying enterprises in the U.K.

Manufacturing Sector, 1958–1963: some tentative results. Applied Econometrics 7(2): 139–147.

Government of Zimbabwe. 1991. Zimbabwe, a framework for economic reform (1991–95).

Government of Zimbabwe: Harare, Zimbabwe.

Hamilton RT. 1985. Interindustry variation in gross entry rates of ‘independent’ and ‘dependent’

businesses. Applied Economics 17: 271–280.

Hause JC, Du Rietz G. 1984. Entry, industry growth, and the microdynamics of industry supply.

Journal of Political Economy 92(4): 733–757.

Hazell P, Roell A. 1983. Rural growth linkages: household expenditure patterns in Malaysia and

Nigeria. International Food Policy Research Institute (IFPRI) Research Report #41. IFPRI:

Washington, DC.

Hess R. 1993. Cost of business compliance in small scale garment and textile sector. Paper presented

at the Conference on Deregulation, Nyanga, Zimbabwe, 16–18 May, 1993.

Human Resources (PVT) Ltd. 1990. Small Business Needs Survey for the Friedrich Naumann

Foundation.

ILO/SATEP. 1989. The promotion of economic development and equity in Zimbabwe. Report to the

Government of Zimbabwe. ILO: Harare, Zimbabwe.

IMANI Development. 1990. Impediments confronting the informal sector enterprise in Zimbabwe.

IMANI: Harare, Zimbabwe.

The Expansion of the Microenterprise Sector 691

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)

Jassat EM, Jirira KO. 1987. Industrial development in Zimbabwe: the case of women in manufactur-

ing activities. Zimbabwe Institute of Development Studies: Harare, Zimbabwe (mimeo).

Khemani RS, Shapiro D. 1986. The determinants of new plant entry in Canada. Applied Economics

60(2): 1243–1257.

King RP, Byerlee D. 1978. Factor intensities and locational linkages of rural consumption patterns in

Sierra Leone. American Journal of Agricultural Economics 60(2): 197–206.

Liedholm C. 1990. The dynamics of small-scale industry in Africa and the role of policy. GEMINI

Working Paper No. 2. Development Alternatives, Inc.: Bethesda, MD.

MacDonald JM. 1986. Entry and exit on the competitive fringe. Southern Economic Journal 52:

640–652.

Mansfield E. 1962. Entry, Gibrat’s law, innovation and the growth of firms. American Economic

Review 52: 1023–1050.

McPherson M. 1991. Micro and small-scale enterprises in Zimbabwe: results of a country-wide

survey. GEMINI Technical Report 25. Development Alternatives, Inc.: Bethesda, MD.

McPherson M. 1998. Changes in Zimbabwe’s micro and small enterprise sector, 1991–1998:

evidence from a third country-wide survey. Development Alternatives, Inc.: Bethesda, MD.

McPherson M, Parker J. 1993. A manual for conducting baseline surveys of micro- and small-scale

enterprises. GEMINI Technical Note. Development Alternatives, Inc.: Bethesda, MD.

Mead D. 1993. The contribution of small enterprises to employment growth in southern Africa.

Paper presented at the African Studies Association, December, 1993.

Mead D, Kunjeku P. 1993. Business linkages and enterprise development in Zimbabwe. GEMINI

Technical Report No. 55. Development Alternatives, Inc.: Bethesda, MD.

Orr D. 1974. The determinants of entry: a study of the Canadian manufacturing industries. Review of

Economics and Statistics 56(1): 58–67.

Parker J, Torres TR. 1994. Micro- and small-scale enterprises in Kenya: results of the 1993 national

baseline survey. GEMINI Technical Report No. 75. Development Alternatives, Inc.: Bethesda,

MD.

Saito K, Van Dijk MP. 1990. The informal sector in Zimbabwe: the role of women. Environmental

and Development Activities. ENDA: Harare, Zimbabwe.

UNIDO. 1988. Human resources in Zimbabwe’s development, the current and prospective

contribution of women. UNIDO: Harare, Zimbabwe.

USAID. 1990. Country training strategy and private sector Training needs assessment: USAID/

Zimbabwe. USAID: Harare, Zimbabwe.

Varian HR. 1987. Intermediate microeconomics, a modern approach. W.W. Norton and Company:

New York.

World Bank. 2001. World Development Report 2000/2001, Attacking Poverty. World Bank:

Washington, DC.

Zimconsult. 1992. Support to Small-Scale Industries and the Enhancement of Indigenous Ownership

in Zimbabwe. UNIDO: Vienna, Austria.

692 L. Daniels

Copyright # 2003 John Wiley & Sons, Ltd. J. Int. Dev. 15, 675–692 (2003)