Embed Size (px)

Citation preview

Factors that contribute to customer satisfaction in guesthouses in Gauteng Province

By

Margarita Popova (809529820)

A dissertation submitted to the Faculty of Management, University of Johannesburg in fulfilment for a Masters of

Technology in Business Administration

March 2006

Supervisor: Dr NC Bresler Co- supervisor: Prof. J Spowart

1

Acknowledgements I wish to pay tribute to and acknowledge the contribution of the following people

who made this thesis possible:

• Friends and family who supported and inspired me.

• Doctor NC Bresler and Professor J Spowart, my academic supervisors for

guiding me and giving me invaluable advise.

• Alison Chambers for proofreading my work.

• Guest house owners and their customers who participated in the survey.

2

Title of the thesis: Factors that contribute to customer satisfaction in guest

houses in Gauteng Province

Summary: Guest houses operate in a highly competitive arena and aim to satisfy the

customer needs and to differentiate their product from the ones of competitors. In

order for these establishments to provide a product which satisfies the patrons,

guest house owners have to know everything they can about the customers –

what they want, what they think, how they make decisions, what influences their

decisions. To gain a better understanding of these influences on customers’

satisfaction, the study included information collected by primary and secondary

data. The secondary data provided literature on the notion and significance of

customer satisfaction, analysed the guest house product, customer behaviour

and service quality. It also provided guidelines on the type of primary data that

had to be acquired. The primary data was obtained in the form of questionnaires

completed by 65 managers and 169 customers of guest houses in the province.

The questionnaires were distributed during December 2004 and February to May

2005. The findings indicated that the factors that contribute to customers’

satisfaction in guest houses in Gauteng Province are: the warm and friendly

hospitality of the host and staff; the friendly environment; the feeling of being

home away from home; the neatness, comfort and hygiene; the great service;

walking the extra mile to meet the customer needs; attention to detail; complete

package; value for money and best security. In other words it is the personalised

service offered at the guest houses that customers choose over other types of

available accommodation.

3

Declaration

I, Margarita N. Popova, hereby declare that:

I understand that plagiarism means presenting the ideas and words of someone

else as my own, without appropriate recognition of the source.

I confirm that the work that I submit for assessment is my own, except where I

explicitly indicate otherwise.

I have fully acknowledged all words, ideas and results from other sources that I

have used in this research study through a generally accepted style of quotes,

references and bibliography.

I am aware that the University views plagiarism as a serious offence punishable

by a disciplinary committee.

Margarita N. Popova

4

Table of Content

LIST OF FIGURES 8

LIST OF TABLES 9

LIST OF ABBREVIATIONS 11

1. INTRODUCTION, STATEMENT OF PROBLEM, OBJECTIVES AND .......12

1.1 Background to problem.........................................................................12

1.2 Statement of problem ............................................................................14

1.3 Research objectives ..............................................................................14

1.4 Review of related literature ...................................................................15

1.5 Limitations ..............................................................................................18

1.6 Significance and contribution of the study..........................................19

1.7 Research design and methodology......................................................19

1.8 Outline of the proposed study ..............................................................20

1.9 Preview of the following chapters ........................................................21

2. LITERATURE REVIEW – THE GUEST HOUSE PRODUCT ......................23

2.1 Introduction ............................................................................................23

2.2 International tourism .............................................................................24

2.3 Tourism in South Africa.........................................................................27

2.4 The accommodation industry in South Africa.....................................32

2.5 The guest house sector in South Africa...............................................34 2.5.1 Historical background........................................................................35 2.5.2 Guest house management................................................................36

2.6 The guest house product offering ........................................................38 2.6.1 The guest house product offering characteristics..............................39 2.6.2 Differentiating the guest house offerings...........................................42

5

2.6.3 Guest house grading schemes – method of differentiating ...............43 guest houses...................................................................................................43 2.6.4 The guest house marketing mix ........................................................44

2.7 Hospitality management........................................................................45 2.7.1 Objectives of managers ....................................................................45 2.7.2 Unique challenges in accommodation management.........................46

2.8 Summary.................................................................................................49

3. LITERATURE REVIEW – CUSTOMER BEHAVIOUR ................................50

3.1 Introduction ............................................................................................50

3.2 The customer as an individual..............................................................51 3.2.1 Customer needs and motivation .......................................................51 3.2.2 Personality and self-concept .............................................................54 3.2.3 Perception.........................................................................................55 3.2.4 Learning process ..............................................................................57 3.2.5 Involvement theory............................................................................58 3.2.6 Attitudes ............................................................................................59 3.2.7 Customer expectations .....................................................................60 3.2.8 Customer satisfaction and loyalty .....................................................62

3.3 Social and cultural dimensions of consumer behaviour ....................63 3.3.1 Reference groups .............................................................................63 3.3.2 Family influence ................................................................................64 3.3.3 Social class .......................................................................................66 3.3.4 Culture ..............................................................................................66

3.4 Decision-making ....................................................................................67 3.4.1 Need recognition...............................................................................68 3.4.2 Information search ............................................................................68 3.4.3 Evaluation of service alternatives......................................................69 3.4.4 Service purchase and consumption ..................................................69 3.4.5 Post purchase evaluation..................................................................71

3.5 Summary.................................................................................................72

4 LITERATURE REVIEW – SERVICE QUALITY...........................................73

4.1 Introduction to service quality ..............................................................73

4.2 Customer satisfaction and service quality ..........................................73

4.3 Service quality dimensions...................................................................75

6

4.4 Measuring service quality .....................................................................77

4.5 Service quality gaps ..............................................................................78

4.6 Summary.................................................................................................82

5. RESEARCH METHODOLOGY ...................................................................83

5.1 Introduction ............................................................................................83

5.2 Statement of the problem......................................................................83

5.3 Research objectives ..............................................................................83

5.4 Collection of data ...................................................................................84

5.5 The sample .............................................................................................85

5.6 Distribution and response rate .............................................................86

5.7 Analysis method ....................................................................................87

5.8 Problems experienced during the collection of data ..........................88

5.9 Reliability and validity of the research data.........................................89

5.10 Significance and contribution of the study..........................................90

5.11 Summary.................................................................................................90

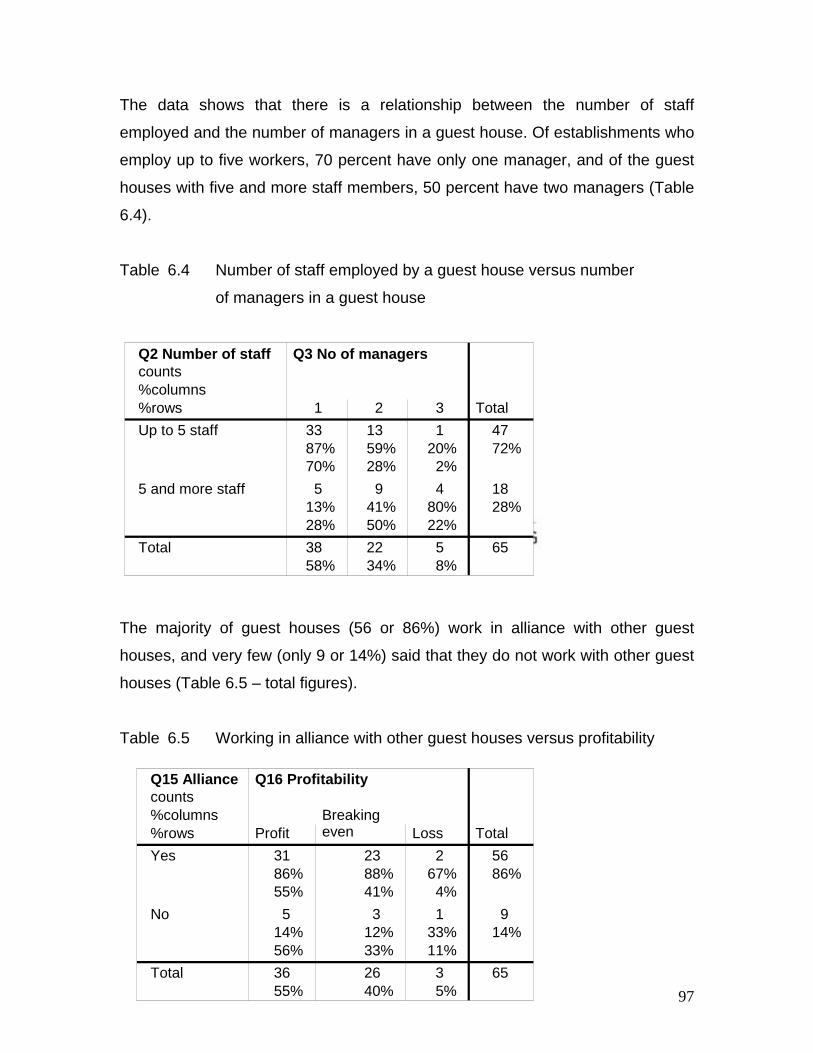

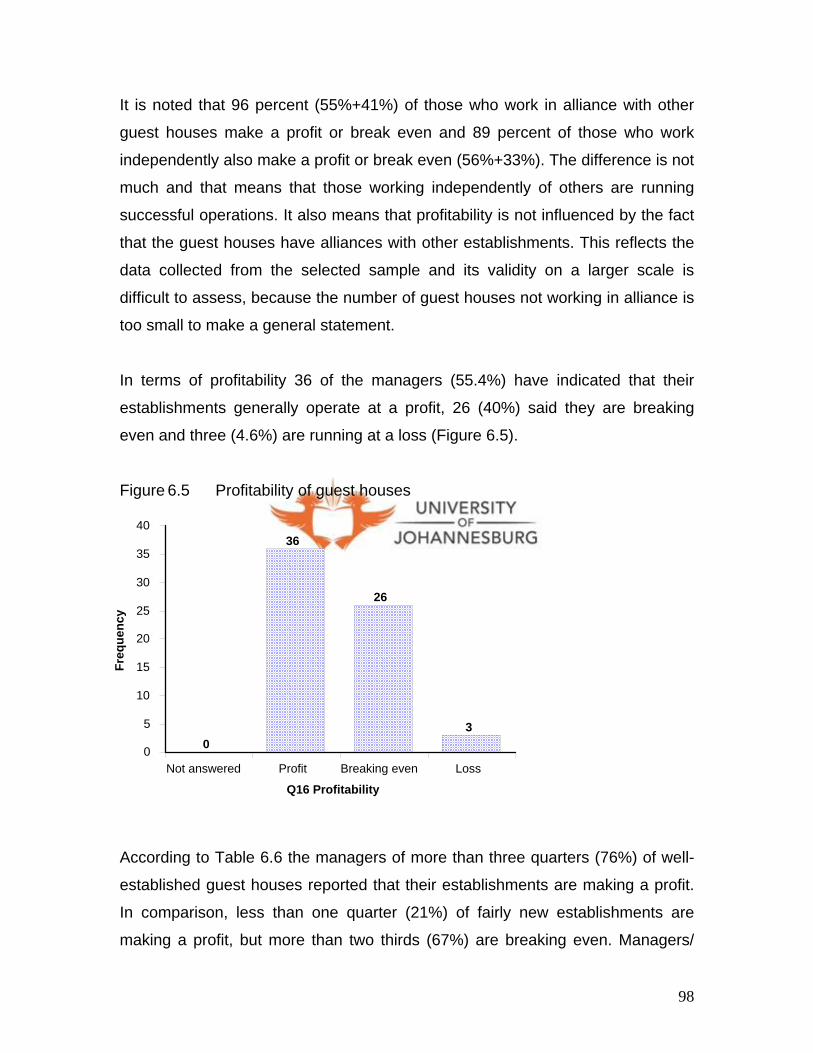

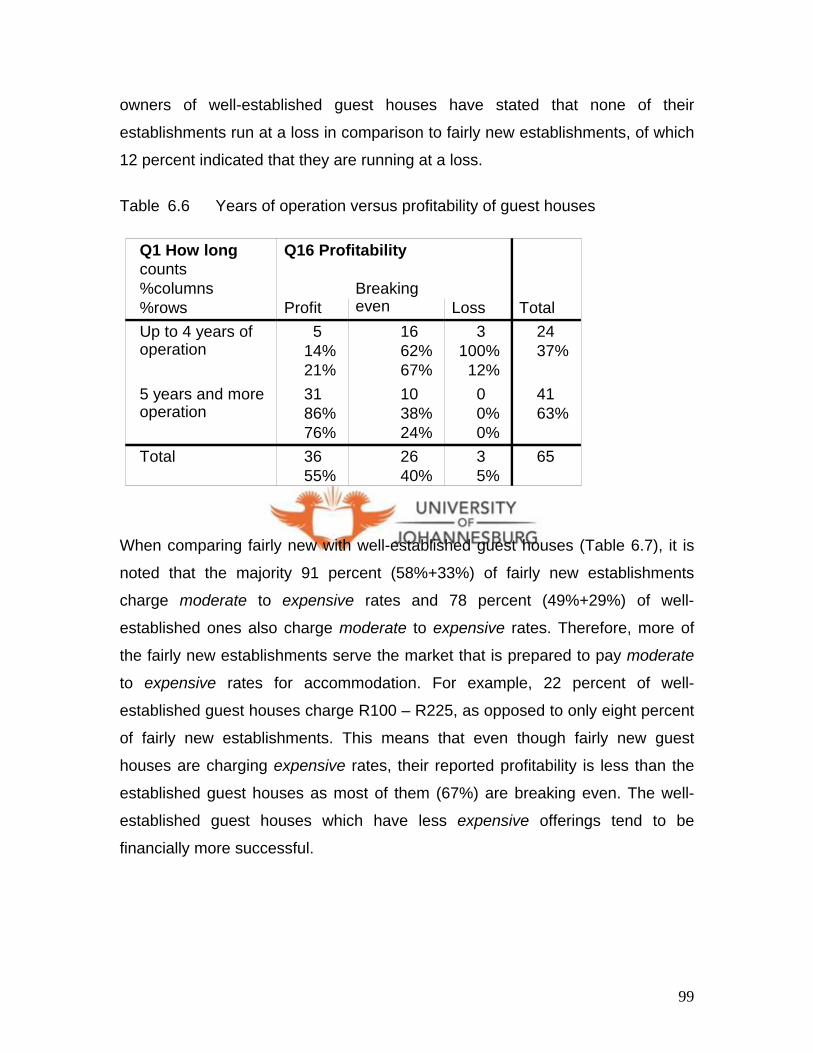

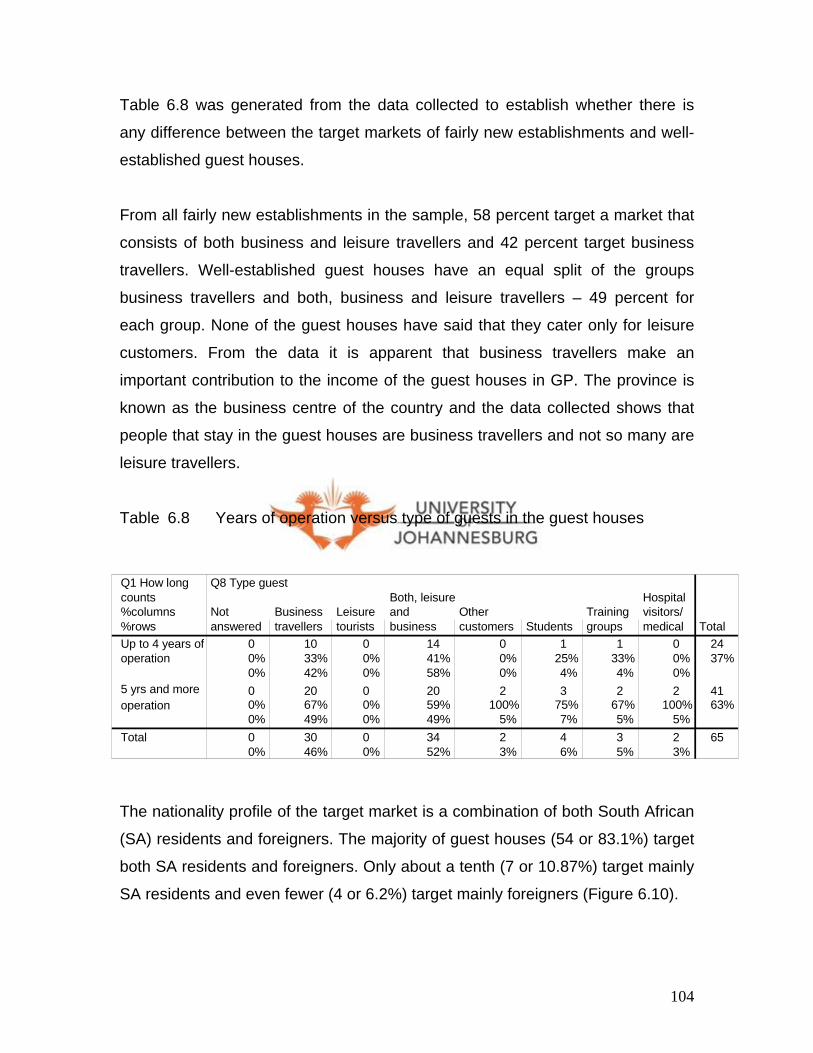

6. REPORT ON DATA AND ANALYSIS.........................................................91

6.1 Introduction ............................................................................................91

6.2 Management questionnaires.................................................................92 6.2.1 The guest houses .............................................................................92 6.2.2 Demand ..........................................................................................100 6.2.3 Target market..................................................................................103 6.2.4 Services offered by the guest houses .............................................105 6.2.5 Meals ..............................................................................................107 6.2.6 Advertising ......................................................................................108 6.2.7 Management comments..................................................................110

6.3 Customer questionnaires ....................................................................112 6.3.1 How customers perceive the guest houses.....................................112 6.3.2 Satisfaction with the overall experience ..........................................118 6.3.3 Uniqueness of guest houses...........................................................120 6.3.4 Matters to be improved upon ..........................................................123

7

6.3.5 Nationality profile of customers .......................................................126 6.3.6 Business versus leisure profile........................................................135 6.3.7 How the customers evaluated the questionnaire ............................144

6.4 Summary...............................................................................................145

7. SUMMARY OF FINDINGS, CONCLUSIONS AND RECOMMENDATIONS 146

7.1 Introduction ..........................................................................................146

7.2 Summary of findings from management questionnaires .................146

7.3 Summary of findings from customer questionnaires .......................151 7.3.1 How customers perceive the guest houses.....................................151 7.3.2 South African residents versus foreigners.......................................155 7.3.3 Business versus leisure profile........................................................157

7.4 Conclusion............................................................................................158

7.4 Recommendations ...............................................................................165

BIBLIOGRAPHY 168

ANNEXURE 1 178

MANAGEMENT QUESTIONNAIRE.................................................................178

ANNEXURE 2 181

CUSTOMER QUESTIONNAIRE.......................................................................181

ANNEXURE 3 184

LIST OF GUEST HOUSES THAT PARTICIPATED IN THE STUDY...............184

8

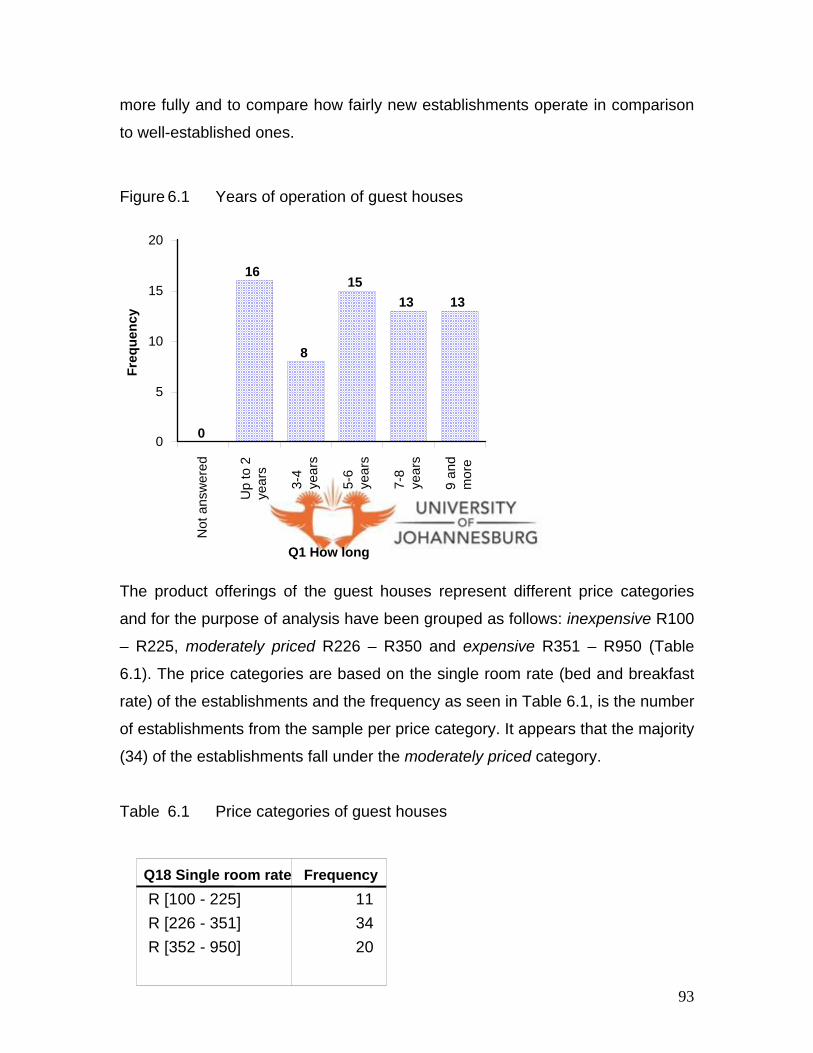

List of Figures Figure 6.1 Years of operation of guest houses 93

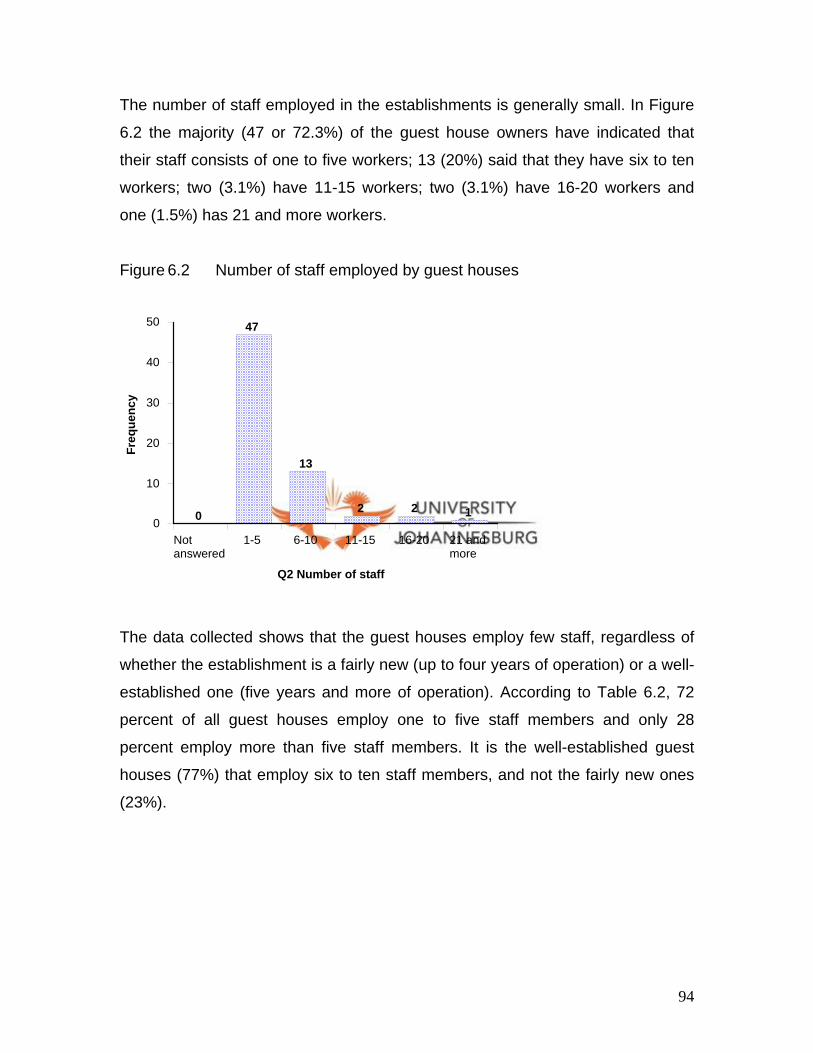

Figure 6.2 Number of staff employed by guest house 94

Figure 6.3 Staff turnover 95

Figure 6.4 Number of managers in a guest house 96

Figure 6.5 Profitability of guest houses 98

Figure 6.6 Months of high demand 101

Figure 6.7 Average weekly occupancy rates in high demand season 102

Figure 6.8 Average weekly occupancy rates in percentage during low

demand season 102

Figure 6.9 Types of guests in the guest houses 103

Figure 6.10 Nationality of market targeted by guest house owners 105

Figure 6.11 Business services offered at guest houses 106

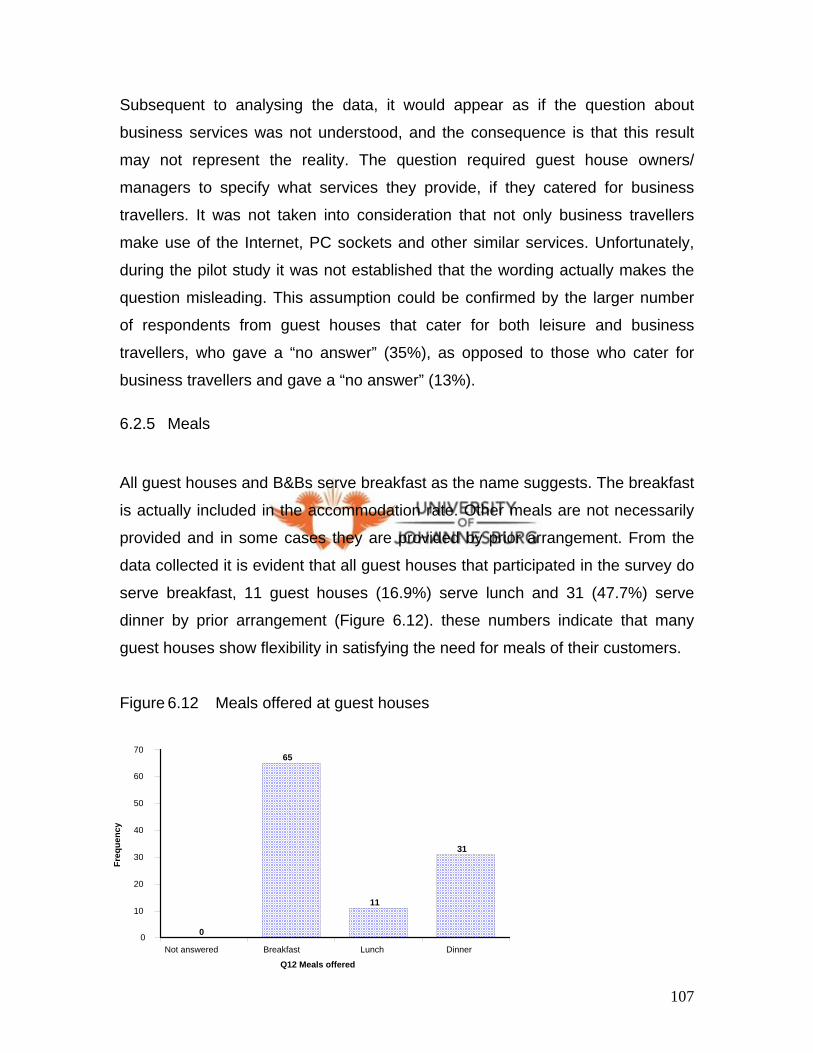

Figure 6.12 Meals offered at guest houses 107

Figure 6.13 Advertising media 109

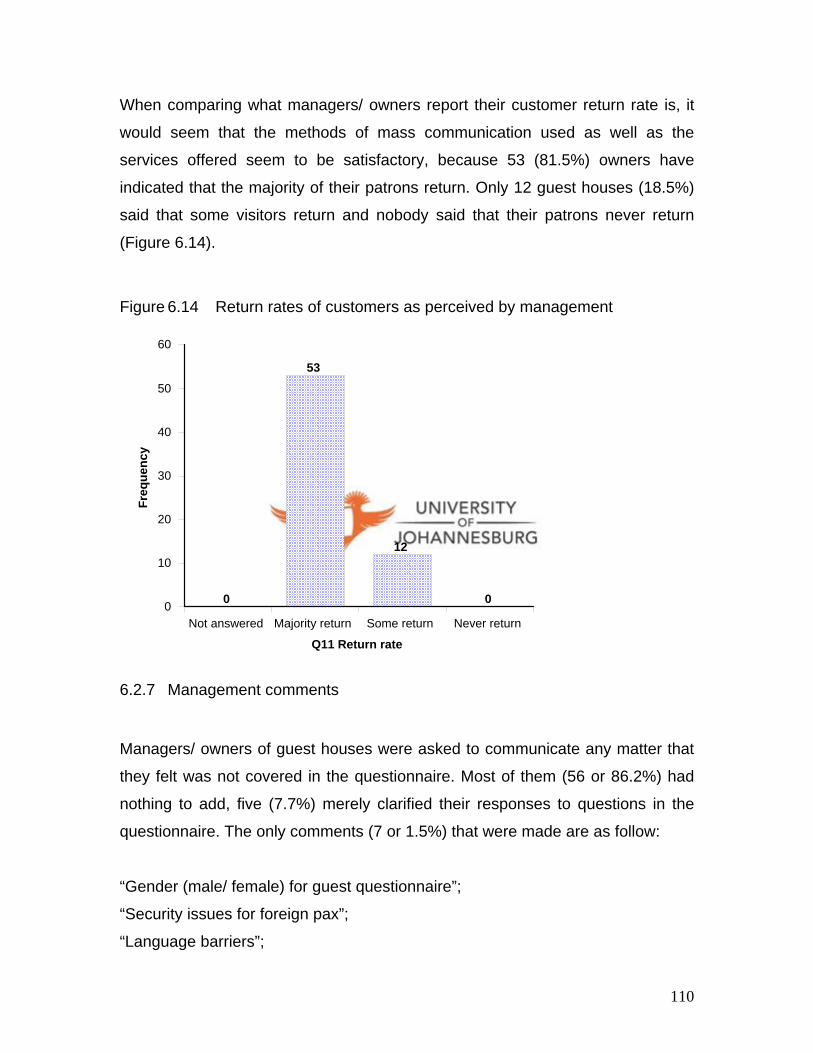

Figure 6.14 Return rates of customers as perceived by management 110

Figure 6.15 Matters that managers/ owners feel are not

covered in the questionnaire 111

Figure 6.16 Most important aspects/ characteristics of service 113

Figure 6.17 Most important aspects/ characteristics of the guest house 114

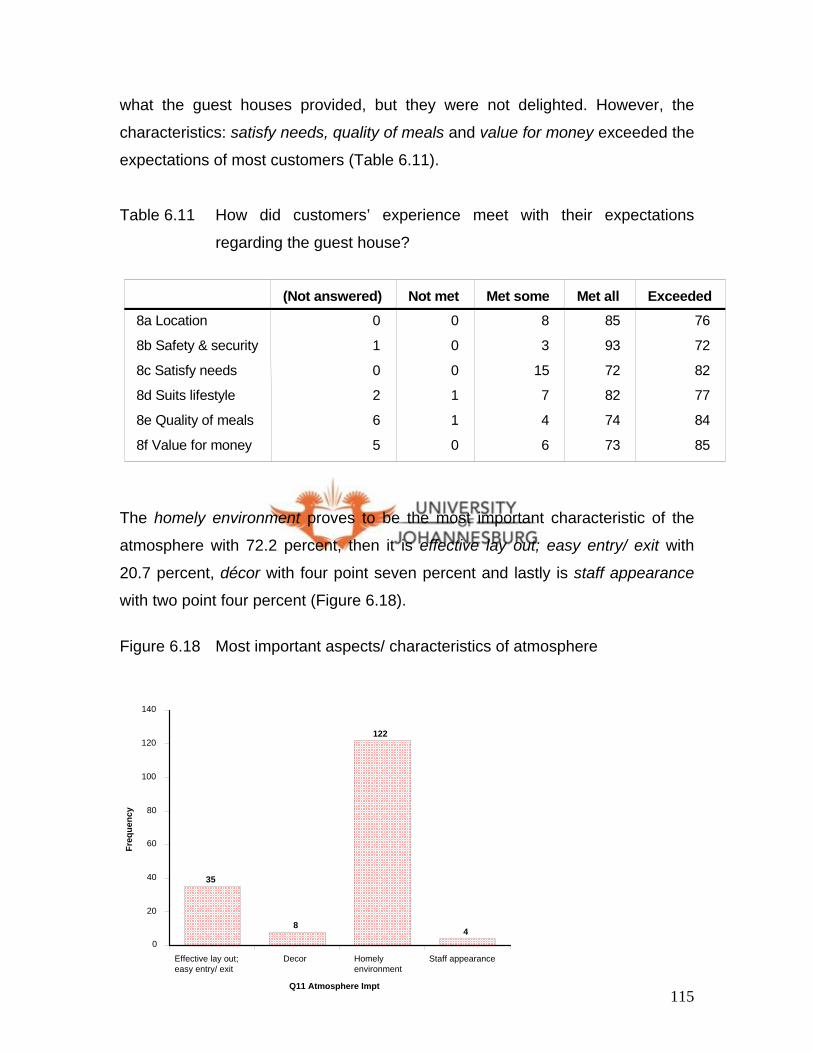

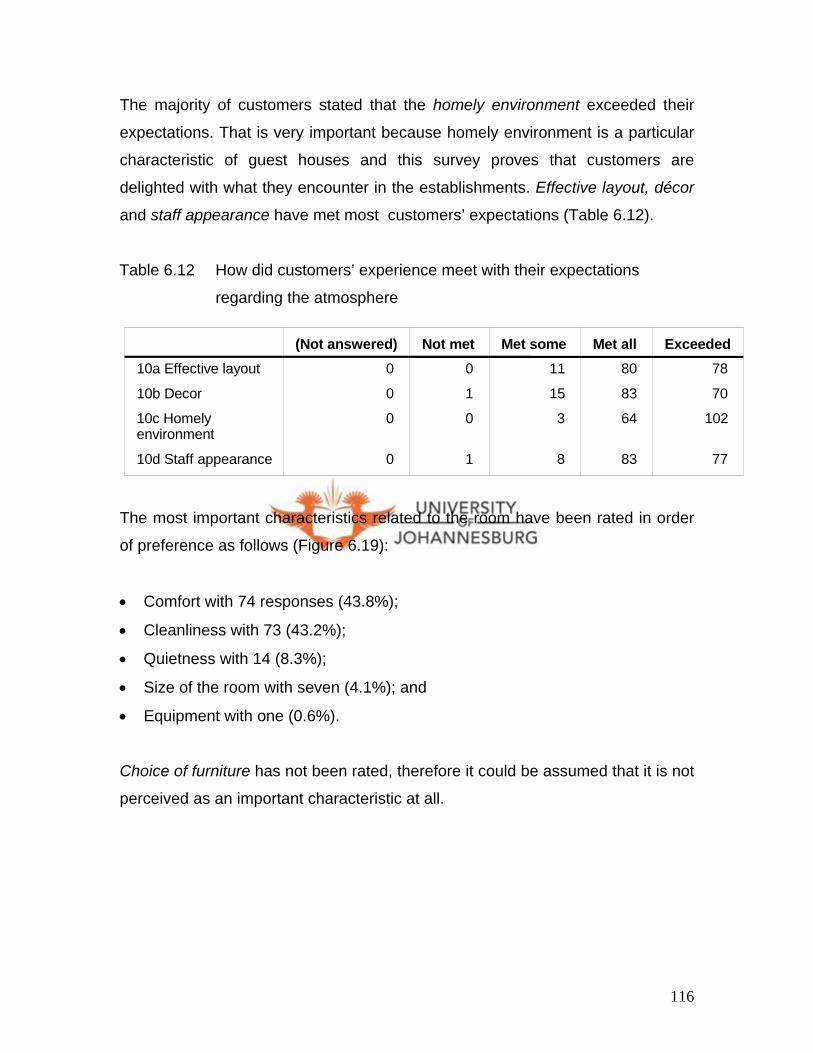

Figure 6.18 Most important aspects/ characteristics of atmosphere 115

Figure 6.19 Most important aspects/ characteristics of the room 117

Figure 6.20 How satisfied are customers with whole experience 118

Figure 6.21 Would customers come back to guest house? 119

Figure 6.22 Would customers recommend the guest house? 119

Figure 6.23 What impressed customers the most? 121

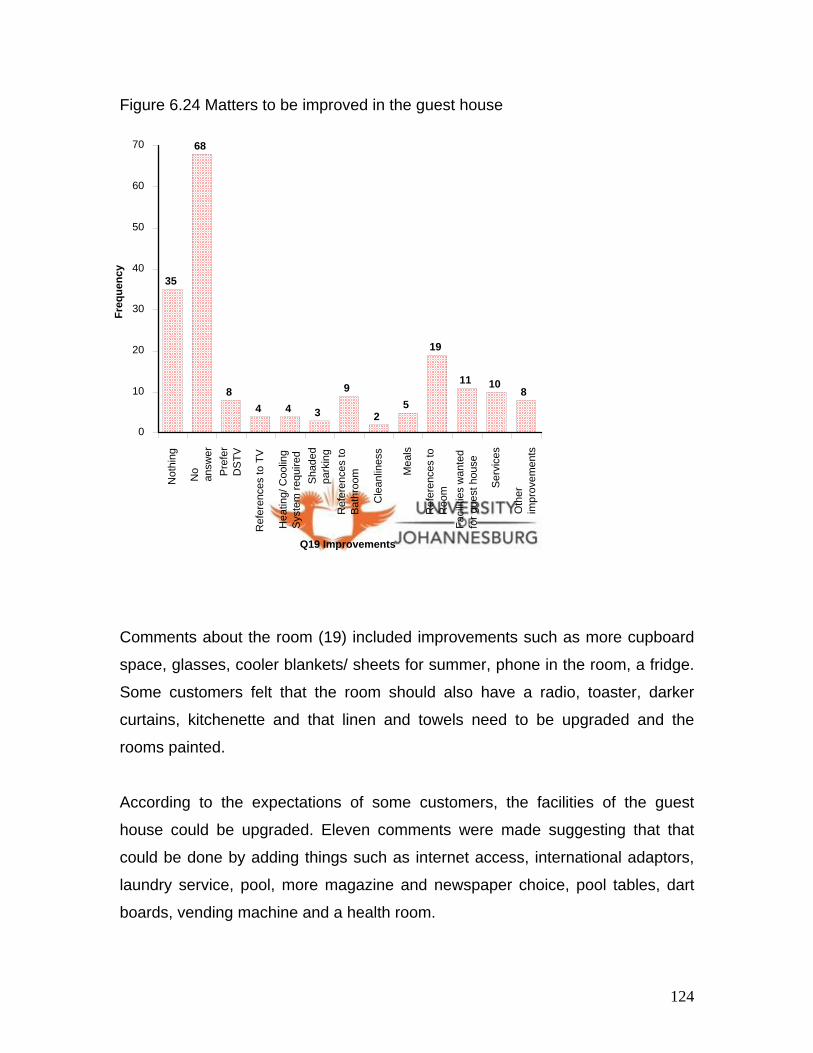

Figure 6.24 Matters to be improved in the guest house 124

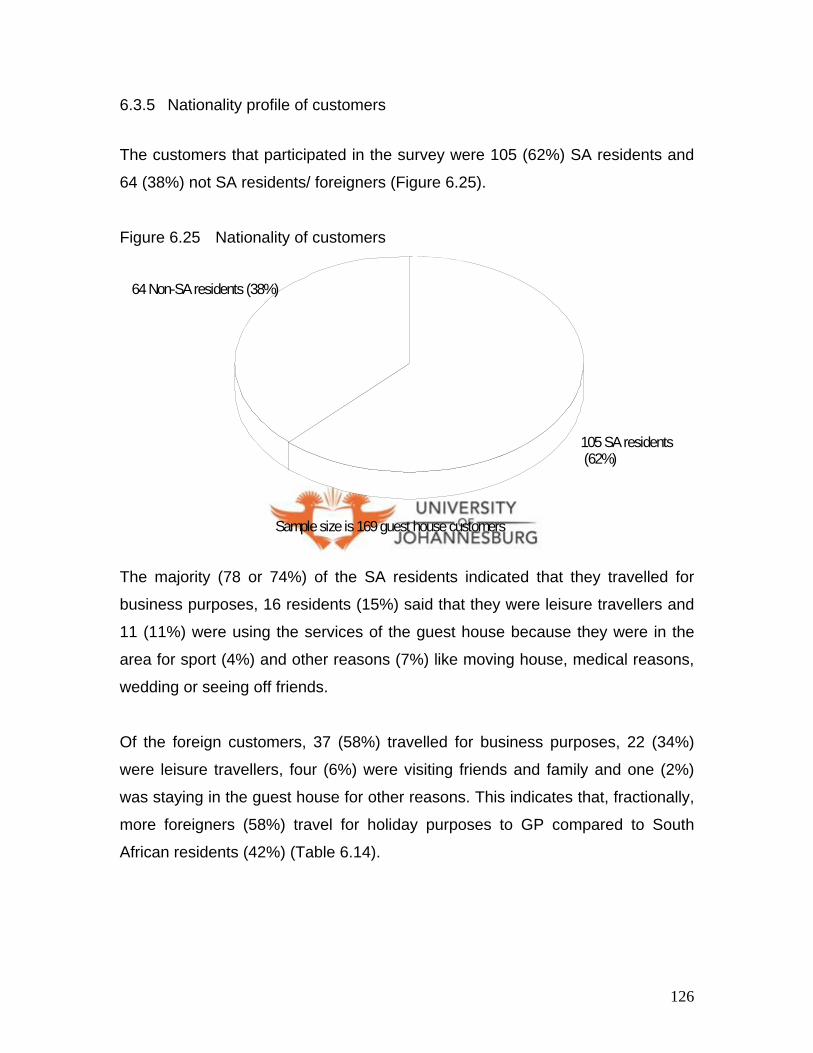

Figure 6.25 Nationality of customers 126

Figure 6.26 Reasons for stay in the guest house 135

Figure 6.27 Customer comments 145

9

List of Tables

Table 6.1 Price categories of guest houses 93

Table 6.2 Years of operation versus number of staff employed 95

Table 6.3 Years of operation versus number of managers in a

guest house 96

Table 6.4 Number of staff employed by guest house versus

number of managers in a guest house 97

Table 6.5 Working in alliance with other guest houses versus

profitability 97

Table 6.6 Years of operation versus profitability of guest houses 99

Table 6.7 Single room rates versus years of operation of guest house 100

Table 6.8 Years of operation versus types of guests in the

guest houses 104

Table 6.9 Types of guests in the guest house versus business

services offered at the guest houses 106

Table 6.10 How did customers’ experience meet with their

expectations regarding the service? 113

Table 6.11 How did customers’ experience meet with their

expectations regarding the guest house? 115

Table 6.12 How did customers’ experience meet with their

expectations regarding the atmosphere? 116

Table 6.13 How did customers’ experience meet with their

expectations regarding the room? 117

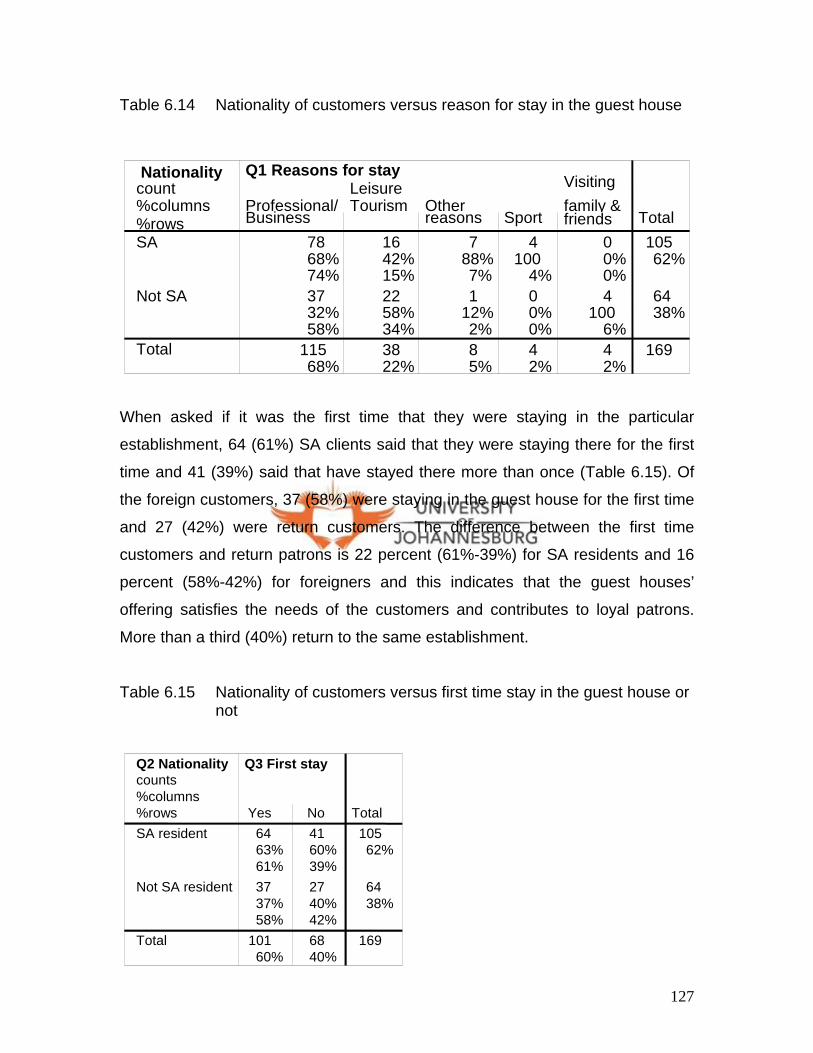

Table 6.14 Nationality of customers versus reason for stay in the

guest house 127

Table 6.15 Nationality of customers versus first time stay in

the guest house or not 127

Table 6.16 Number of times stayed in the guest house versus

nationality of customers 128

10

Table 6.17 How customers heard of particular guest house versus

nationality of customers 130

Table 6.18 Nationality of customers versus most important aspects/

characteristics of the service 131

Table 6.19 Nationality of customers versus most important aspects/

characteristics of the guest house 132

Table 6.20 Nationality of customers versus most important aspects/

characteristics of the atmosphere 133

Table 6.21 Nationality of customers versus most important aspects/

characteristics of the room 134

Table 6.22 Nationality of customers versus age group 134

Table 6.23 Reasons for stay in the guest house versus nationality

of customers 136

Table 6.24 Years of operation of guest house versus reason for

stay in the guest house 137

Table 6.25 How did customers hear about the guest house versus

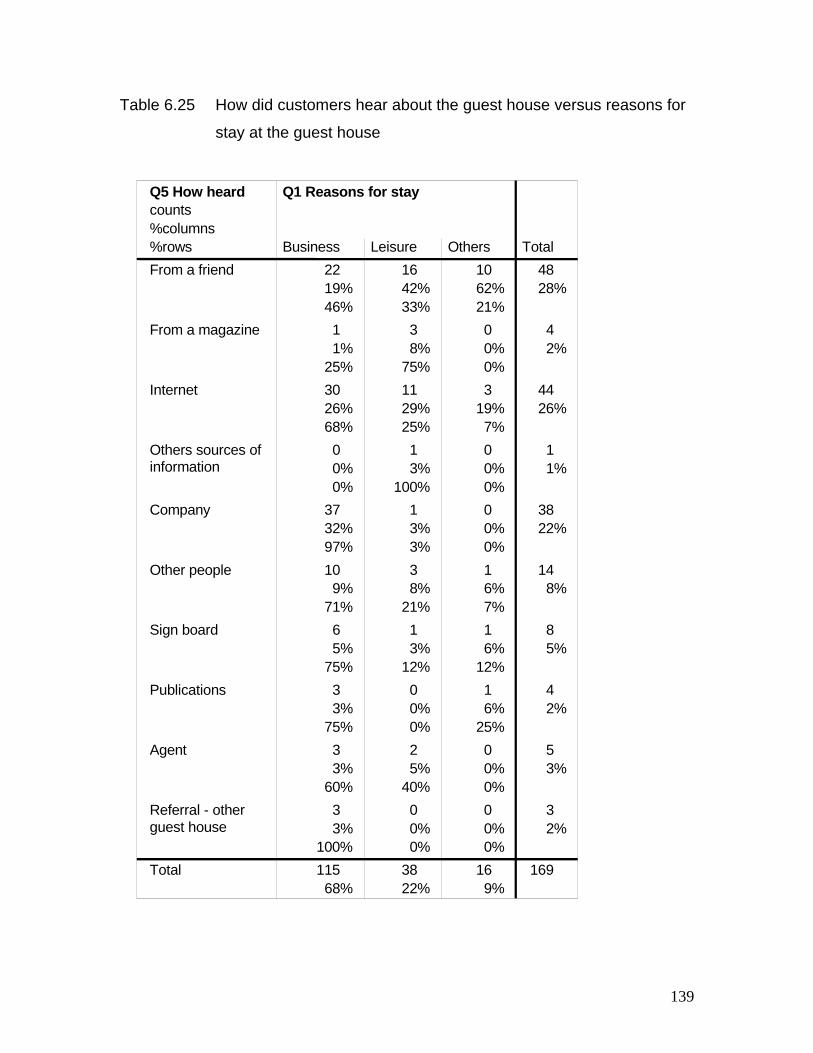

reason for stay at the guest house 139

Table 6.26 Reason for stay at the guest house versus most important

aspects/ characteristics of the service 140

Table 6.27 Reason for stay at the guest house versus most important

aspects/ characteristics of the guest house 141

Table 6.28 Reason for stay at the guest house versus most important

aspects/ characteristics of the atmosphere 142

Table 6.29 Reason for stay at the guest house versus most important

aspects/ characteristics of the room 143

Table 6.30 Reason for stay at the guest house versus age group 143

11

List of Abbreviations AA Automobile Association ANC African National Congress B & B Bed and Breakfast establishment BEE Black Economic Empowerment CBD Central Business District DSTV Digital Satelite Television DVD Digital Video Disc Four Ps Product, Price, Promotion, Place GHASA Guest House Association of South Africa GP Gauteng Province GSA General Sales Agent Km Kilometres PC Personal Computer SA South African SAA South African Airways SADC Southern African Developing Countries SERVQUAL Service Quality model of Parasuraman, Zeithaml and Berry (1988)SQGs Service Quality Gaps TGCSA Tourism Grading Council of South Africa TV Television WTO World Tourism Organisation

12

1. INTRODUCTION, STATEMENT OF PROBLEM, OBJECTIVES AND

METHODOLOGY OF THE STUDY

1.1 Background to problem The tourism industry in South Africa has been growing in the past few years

(Henning & Willemse, 1999b: 11). Several well-known international hotel chains

have established successful accommodation premises in the country and

dominate the tourism markets. However, many tourists choose the services

offered by small, privately run accommodation providers, rather than those

offered by the recognised hotels. This led to the creation of the guest house

sector of the Tourism Industry in South Africa, which has been growing since

1995 (Jordaan, 2001: 171).

The guest house business is considered a home business, as people generally

start one in their homes by either restoring or altering the existing facilities to suit

their needs, or alternatively building one from scratch. Beginning such an activity

could be for the purpose of acquiring a primary income or a second income,

when retiring and needing something to fill the quiet times. Guest houses are run

by a family or a manager with a few staff members. The owners do not

necessarily have any experience in the hospitality industry, and the success and

survival depends on their good business sense, managerial skills and expertise

(Henning & Willemse, 1999a: 4).

As mentioned by the Guest House Association South Africa (GHASA), a small

number of guest houses are listed with their association while the majority of

these establishments operate independently from GHASA. Only in recent years,

guest houses were taken into consideration when statistical data, financial or

trading reports were prepared for the hospitality industry.

13

The guest house concept originated in Europe. In South Africa it started as far

back as 1991, but the real growth has taken place only since 1995 (Jordaan,

2001: 171). The guest house industry today is highly competitive (Henning &

Willemse, 1999a: v) in terms of services and quality offered to its customers. The

customers’ overall satisfaction with the service of the organisation is based on all

their encounters/ experiences with that organisation (Sureshchandar, Rajendran

& Anantharaman, 2002: 364). The continued and profitable existence of a guest

house and any other business depends on how effectively it is marketed.

Marketing a product or a service entails making sure that the potential customer

has sufficient information to make an informed decision. It is necessary for guest

house owners to appreciate the needs of their guests and direct their marketing

efforts towards satisfying those needs, so that maximum customer satisfaction

and service quality can be obtained.

Customer satisfaction is considered a prerequisite for customer retention and

loyalty (Sureshchandar, Rajendran & Anantharaman, 2002: 364). Loyal

customers help to promote the establishment; they provide strong word of mouth

advertising and become a marketing force by recommending the guest house to

other customers (Bowen & Chen, 2001: 213). Positive word of mouth is regarded

to be the best advertising a company can get (Bowen & Chen, 2001: 213).

The criteria that count in evaluating service quality are defined by customers.

Service quality is more difficult for customers to evaluate than goods quality.

Therefore, the criteria customers use to evaluate service quality might be more

difficult for the marketer, and especially for a guest house owner with no previous

experience in the hospitality services, to comprehend (Zeithaml, Parasuraman &

Berry, 1999: 16). It is therefore important for guest house owners to have a good

knowledge of customers’ expectations and perceptions of the service offered at

the establishments. From these a need is generated to determine what makes

visitors stay at guest houses and to identify the specific elements that contribute

to their satisfaction in order to provide them with the quality desired.

14

1.2 Statement of problem

The primary objective of service providers and marketers is to develop and

provide products and services that satisfy customers’ needs and expectations,

thereby ensuring their own economic survival. To achieve this objective, service

providers need to understand how consumers choose and evaluate their service

offering (Zeithaml & Bitner, 2003: 35). Owing to the fact that the guest house

sector in South Africa only came into existence in the past decade there is a

limited amount of literature published on customer satisfaction in guest houses.

There are, except for generic SERVQUAL dimensions by Zeithaml, Parasuraman

and Berry (1990), no clear criteria of what factors contribute to customer

satisfaction in guest houses. Thus there is a need to establish:

• what are customers looking for when selecting a guest house in order to

be satisfied;

• the customers’ specific needs; and

• the level of quality offered in guest houses

in order to help managers/ owners of guest houses provide the quality of services

that their customers expect.

1.3 Research objectives

In the past few years the guest house sector has grown rapidly, which can be

associated with high demand for the services of such establishments (Henning &

Willemse, 1999a: v). Many owners of guest houses are not equipped with the

necessary skills and experience to adequately interpret customers’ expectations

and perceptions in order to provide the quality of services required and to ensure

that the customers will return to or promote their establishment. Therefore the

research aims to:

15

• describe the notion and significance of customer satisfaction;

• establish what attracts customers to guest houses;

• establish the guest houses’ customers’ needs;

• analyse the quality of services in the guest houses;

• determine the rate of return of customers;

• analyse occupancy reports of the individual guest houses; and

• develop a framework of criteria that are associated with customers’

choices of guest house accommodation to ensure their satisfaction.

1.4 Review of related literature

The South African hotel industry is recognised as one of the most important

sectors of the domestic economy, said Jordaan (2001: 151). It is characterised

by the presence of many of the world’s most well-known brands including Holiday

Inn, Sheraton, Hyatt, Hilton, Inter- Continental and Radison (Jordaan, 2001: 151).

The author adds that home grown brands such as Southern Sun, Protea Hotels

& Inns, City Lodge, Sun International and others offer a further glimpse of the

diversity available in South Africa. While hotels have traditionally offered a full

range of services to the travelling public, the industry now provides for all types of

needs and expectations (Jordaan, 2001: 156).

The nature of accommodation supplied at a destination is mainly a function of

demand – in other words, it is tourists who determine what type of

accommodation will be established at the destination area. Some prefer the full-

amenity type of accommodation, whilst others are content with the bare

essentials (Jordaan, 2001: 36).

In the past decade a growing trend towards guest house type of accommodation

has been noted, as it was mentioned in Paragraph 1.1. Many foreign guests

prefer to stay in a guest house, because it gives them an opportunity to meet the

local people and talk to them about various aspects, whereas in larger,

16

commercial operations they feel they do not get to know the country’s people,

Jordaan (2001: 173) stated. The author added that travellers seek the homely

environment, where they can walk on the grounds, or have a braai outside;

because it is something they would have done if they were at home (Jordaan,

2001: 173).

Customer satisfaction has an important role in the hospitality industry. It has a

direct influence on the existence, survival and success of the hospitality service

providers, and on a larger scale, has an impact on the economy of a country.

Customer satisfaction is the extent to which a firm fulfils a consumer’s needs,

desires, and expectations. Customers find it satisfactory – and even desirable –

to permit businesses to cater to them and even to stimulate wants (Perreault, Jr.

& McCarthy, 1999: 640). Businesses exist at the discretion of the consumers – if

the products and services offered satisfy the customers, then the firms will

continue to operate.

Satisfied customers are those who have received an excellent service. Excellent

service might seem like an intangible goal, because service can only be

assessed to be good or bad according to the personal satisfaction of the guest.

There are, however tangible means by which it can be achieved. People can see,

taste and appreciate the effects of good service (Henning & Willemse, 1999b:

11). Excellent service pays off because it creates true customers – customers

who are glad they selected a firm after the service they experienced; customers

who will use the firm again and sing the firm’s praises to others (Zeithaml,

Parasuraman & Berry, 1990: 9). Positive word of mouth increases the

accommodation establishment’s reliability and decreases customer’s perceived

risk (Bowen & Chen, 2001: 216). When a product is complex and difficult to

evaluate, and there is risk involved in the decision to buy it – as is the case with

many services – consumers most often look to others for advice on which

provider to consider (Zeithaml & Bitner, 2003: 162). A small increase in customer

satisfaction boosts customer loyalty dramatically, and in addition to benefiting

17

from the extremely satisfied customers’ repeat patronage, the hotel managers

can save their marketing expenses, because of the extremely satisfied

customers’ marketing power (Bowen & Chen, 2001: 215).

Establishing the level of customer satisfaction in the tourism industry is a

challenging process. This is due to the classification of customers into several

categories. A tourist can be, amongst others:

• a business person;

• a holiday maker;

• someone visiting friends and family; and

• someone pursuing special interests.

All of the above could be domestic or international tourists, who travel for

different purposes and have different expectations and behaviours. Consumer

behaviour as defined by Wilkie (in Williams, 2002: 8) is, the mental, emotional

and physical activities that people engage in when selecting, purchasing, using

and disposing of products and services so as to satisfy needs and desires.

In order to determine what factors contribute to a customer’s satisfaction, it is

necessary to examine the different needs, tastes, expectations and behaviours of

customers. At the same time the quality of the services offered should be

assessed, so that a clearer picture of what makes the customer select a specific

tourist establishment can be formulated.

In assessing the services offered, management must consider that there could

be service quality gaps, or discrepancies between the expectations of the guests

and the actual services provided (Zeithaml & Bitner, 2003: 113). For that to be

possible one would have to identify and relate those key elements that require

systematic management attention (Candido & Morris, 2000: 464). The elements

include: management perceptions of customer expectations; the vision, the

18

mission and the service strategy; the quality specifications and service design;

the financial and human resources; the external communication system and the

service delivery system, as stated by Candido and Morris (2000: 464).

The service quality approach starts with the assumption that the level of service

quality experienced by customers is critically determined by the gap between

their expectations of service and their perceptions of what they actually receive

from a specific service provider (Donnelly & Shiu, 1999: 500). Their perceptions

are based on dimensions, which are used to evaluate the service quality, and

include:

• tangibles - the physical appearances;

• reliability of the staff;

• responsiveness of the staff;

• assurance that the employees convey; and

• the empathy that the company provides.

It is important for any business to be able to develop a quality service strategy

that balances all the above elements and dimensions successfully. Formulation

and implementation of such, requires understanding and elimination of the

service quality gaps and commitment at all times to become a “customer-driven”

or a “customer-centred organisation” (Massnick, 1997: 9).

1.5 Limitations Acquiring of information about the topic has proven to be difficult due to the

limited statistical data about guest houses. The research will be conducted

amongst visitors to and managers of guest houses in Gauteng Province;

therefore the findings will be relevant only to guest houses in the province.

19

1.6 Significance and contribution of the study

This research will provide a framework of criteria associated with the factors that

contribute to customer satisfaction in guest houses in the Gauteng Province.

Information will be distributed to guest house owners to assist them in

understanding the expectations and perceptions of customers in order to provide

the quality of services required.

1.7 Research design and methodology

The research design and methodology will be the following:

• The term guest houses in this research will represent guest houses and Bed

and Breakfast establishments, due to the similarity of these two

accommodation providers. Their alike characteristics are further discussed in

Paragraph 2.5.

• Secondary research will include review of national and international literature and articles related to the topic. The review of literature will provide a

guideline on what primary data should be collected.

• Collection of primary data will be in the form of a two-phased study. The first

phase will be the pilot stage and will include interviews with five guest house

owners and their customers, which will help to acquire useful information on

which the questionnaires for the second phase will be based. A qualitative

approach will be used to establish the right questions for the questionnaires

and to create a perspective needed for interpreting the data. The second

phase will be obtaining information through self-administered questionnaires

from guest house owners and their customers. A quantitative approach will be

20

used with the purpose to quantify customer satisfaction, the extent of service

quality gaps and the perception of value.

• This research will be an exploratory and descriptive study, which will not

include correlation analysis. The analytical methods used will be cross-

tabulations, bar charts, pie charts, intervals and descriptive measures like

mode for most frequently occurring values, range for difference between the

largest and smallest observations and mean for average values.

• The population (universe) in the study will include guest houses in Gauteng

Province. The sampling unit is 65 guest houses and the respondents will be

65 owners/ managers of the guest houses and 325 guests if guest house

owners allow and succeed to interest five of their guests to complete the

questionnaires.

• The parameters of the research will cover guest houses located within a 70

kilometres (km) radius from the Johannesburg Central Business District

(CBD).

• Guest houses serving different target markets will be included in the sample,

such as those with different pricing categories.

1.8 Outline of the proposed study

The outline of the chapters is a generic one and details will unfold as the

research progresses.

Chapter 1 Introduction

Chapter 2 Literature review – The guest house product

Chapter 3 Literature review – Consumer behaviour

Chapter 4 Literature review – Service quality

Chapter 5 Research methodology

21

Chapter 6 Report on data and analysis

Chapter 7 Summary of findings, conclusion and recommendations

1.9 Preview of the following chapters

Chapter two, Literature review – The guest house product, presents a description

of international tourism, a brief historic background of the development of South

African tourism and some current tourism trends and developments. It then

presents information about guest houses in the country and their product

offering, followed by a section on hospitality management.

Chapter three, Literature review – Customer behaviour, presents why it is

important for marketers to study and understand customer behaviour. It then

describes characteristics of the behaviour of the customer as an individual, the

social and cultural dimensions of consumer behaviour and the decision-making

process that customers follow.

Chapter four, Literature review – Service quality, presents a brief overview of

what is quality in the service industry and how it is related to customer

satisfaction. It then explains what factors contribute to the evaluation of service

quality, how the service quality could be measured and what discrepancies could

arise between customers’ expectations and their perceptions of the service they

receive from the service provider.

Chapter five, Research methodology, is a chapter that describes the steps taken

during the execution of the research study.

Chapter six, Report on data and analysis, provides an analysis of the collected

data from the questionnaires. The results are illustrated in the form of figures and

tables and represent the answers of the owners/ managers of the guest houses

in Gauteng Province and some of their guests.

22

Chapter seven, Summary of findings, conclusion and recommendations, provides

a statement of the main points established in Chapter six. It then presents the

final conclusion of the research, based on the literature reviewed and all the data

collected during the study; and some recommendations for guest house owners.

23

2. LITERATURE REVIEW – THE GUEST HOUSE PRODUCT

2.1 Introduction

The guest house sector in South Africa is a relatively new one in the hospitality

industry. It only became prominent in the nineties. Guest houses are privately run

accommodation establishments and their exact contribution to the hospitality

industry is difficult to assess. However, they are participants in the tourism

industry and in order to portray a clearer picture of them, the following issues are

discussed in this chapter: International tourism, tourism in South Africa, the

accommodation industry in South Africa, the guest house sector in South Africa

and hospitality management.

The discussion on international tourism presents an overview of tourism on a

global scale. It includes reasons why people travel, role players in the tourism

industry and the effect of globalisation on tourism.

The section on tourism in South Africa provides a brief history of the

development of tourism in the country. It introduces current tourist trends and

current developments in the domestic market.

The section on the accommodation industry in South Africa presents the various

types of accommodation available to tourists. It also describes customer trends

and statistical figures related to accommodation in recent years.

The section on the guest house sector in South Africa provides general

information about guest houses. It also includes a detailed analysis of the guest

house product. Further information about guest houses will be obtained through

questionnaires and reported on at a later stage in the study.

24

The section on hospitality management defines the process of hospitality

management and explains the role of managers in the industry.

2.2 International tourism

Tourism is the term given to the activity that occurs when tourists travel. This

encompasses everything from the planning of the trip, the travelling to the place,

and the stay itself, to the return, and the reminiscences afterwards. It includes the

activities the traveller undertakes as part of the trip, the purchases made and the

interactions that occur between guest and host. In summary, it is all the activities

and impacts that occur when a visitor travels (Mill & Morrison, 1992: 9).

Tourism has grown enormously in the last half century and has become the

world’s largest industry (Wahab & Cooper, 2001:70). This growth can be

associated with the increase of the world’s population, the increase in individuals’

earnings, changes in society, emerging technologies and widely available

information, changes in political and legal environments, the increase in

international investments and the global economy. Globalisation has offered

endless opportunities and at the same time has made the world a highly

competitive arena. People are changing their life styles in order to survive or be

successful in this competitive environment. They are becoming more aware of

their limited time and are looking for both value for time and value for money

(Wahab & Cooper, 2001:70). This indicates that the tourism demand is

undergoing a transformation from holiday products, which were “mass,

standardised and rigidly packaged”, at reasonable prices due to economies of

scale, towards “independent or semi – independent trips” (Wahab & Cooper,

2001: 77; Keyser, 2002: 109-111). In other words, people are moving away from

perceived mass tourism destinations.

Travellers are motivated by a wide range of desires. The World Tourism

Organisation (WTO) recognises six main purposes for travelling (Keyser, 2002:

45):

25

• Leisure, recreation and holidays – these include sightseeing, shopping,

attending sport events, recreational and cultural activities, cruises, gambling,

relaxing and honeymooning.

• Visiting friends or relatives – such as visiting family and friends, weddings,

funerals, care for invalids or ill members of the family.

• Business – includes meetings, sales for foreign enterprises, conferences,

educational courses, giving lectures or concerts and government missions.

• Health – for example health treatments, spas, fitness and other medical

treatments.

• Religion – involves attending religious events.

• Other – like transit activities or other unknown activities.

Tourism is about people: tourists interacting with other people, undergoing

experiences that may influence their own or the host community’s attitudes,

expectations, opinions and, ultimately, lifestyles. Tourism being such a diverse

activity makes it difficult for individual tourist outlets to satisfy the needs and

desires of all travellers. Wahab and Cooper (2001: 70) suggest that the 4S

framework for urban tourism is shifting from “Sightseeing – Shopping – Shows –

Short breaks” to “Segmentation – Specialisation – Sophistication – Satisfaction”.

This framework guides tourism managers in the interpretation of the demand

trends and in the development of products that will best satisfy the chosen

segment of the market. The advantage of accommodation establishments, such

as guest houses, is that the management and staff are in constant interaction

with their customers. This interaction provides a better opportunity for guest

house managers to acquire customer knowledge, than any researcher or

26

database could provide (Middleton & Clarke, 2001: 183). This also helps guest

house owners to identify which segment of the market is most likely to be

attracted to their product offering so that they can concentrate their marketing

efforts on that specific market segment. Ultimately, these processes of

segmenting the market and meeting customers needs through customised

service, lead to satisfied customers.

The demand for tourism is met by the concentrated marketing efforts of a wide

variety of tourist services. Together, these services form the world’s largest and

fastest growing industry (Holloway, 1998: 67). The travel and tourism industry

comprises of the tourist and the producers of the tourism product, which are the

transport providers; the accommodation providers, such as hotels, guest houses,

lodges and so forth; and attractions and support services. The producers could

be from the private sector or the public sector, and the success of the industry

depends on the close working partnership between the two sectors. Additionally,

there are other factors that influence travel and tourism. The World Tourism

Organisation has identified the most important ones as economic and political

factors, the influence of technology, demographics, the effect of globalisation,

localisation, growing socio-environmental awareness, living and working

environment, a change from “service” to “experience” economy, advances in

marketing and travel and personal safety (Lubbe, 2003: 64).

Globalisation of the media and easy access to information has contributed to the

fact that people are becoming more educated and their interests are shifting to

different destinations. They seek to experience more adventurous and enriching

tourist products and also more personal service, such as the service that a guest

house could offer them. The sophistication in their needs, leads to the necessity

to develop sophisticated products, which are to be delivered at the appropriate

time and price (Wahab & Cooper, 2001: 85). This requires a specialisation of the

products and destinations. Tourism enterprises are in a situation where they

have to identify their competitive advantage and market the products to the

27

consumers in the best possible way. Since tourists no longer have single,

standardised and rigidly packaged wants, segmentation offers the opportunity to

provide appealing tourism products to well-defined markets (Wahab & Cooper,

2001: 88). The powerful immediacy of customer contact in guest houses,

provides a knowledge not only of what customers want and expect from the

product offering, but also of what type of customers are looking for that offering.

Appropriate segmentation ensures that the right type of consumer is attracted to

the destination and ultimately it has an impact on the experience of the tourists

and their perception of the product. The tourist experience is a complex amalgam

of factors, which shape the tourist’s feelings and attitudes towards his or her visit

(Page, 1995: 24; Bennett, Joste & Strydom, 2005: 91). If the consumers are

satisfied with their experience it means that their needs and expectations were

met. It also suggests that they will probably return to the destination and/ or will

share their experience with friends and family. Then these friends and family may

become potential customers, because the place was recommended by

somebody that has been there. Word of mouth advertising is considered to be a

very powerful marketing tool in the service industry, especially when dealing with

international markets.

2.3 Tourism in South Africa

In South Africa, the historical background of the country has played an important

part in the development of the tourism industry. In the 19th century, owing to its

climate conditions, South Africa became famous as a health destination and it

was marketed in Britain as the ”health resort of Europe”. Domestic tourism also

occurred at this time as the farming community went on holidays by ox-wagon

(Lubbe, 2003: 26). Many attractions were established and opened their doors to

welcome the tourists.

During the First and Second World wars, South Africa experienced difficulties in

promoting tourism to the country. In the late sixties, the World Bank established a

Tourism Projects Department to help finance the development of tourism.

28

“However, in the seventies and eighties the apartheid regime slowed down the

growth of tourism. South Africa became isolated from the rest of the world. Harsh

economic and other sanctions were imposed, including measures to discourage

citizens of foreign countries from visiting South Africa. South Africans were also

denied the opportunity to visit some foreign countries. This resulted in major

restrictions on the activities of the South African Tourism Board. Offices in some

countries had to be closed, and South Africa was regarded as an undesirable

and unmarketable destination. Some newspapers refused to accept

advertisements that promoted South Africa. To counter this, the Tourism Board

was obliged to expand on the use of direct marketing campaigns. Local tourism

was also encouraged to help ensure the survival of the industry. Discriminatory

legislation was gradually abolished and new markets and marketing opportunities

opened up. However, South Africa remained isolated from the rest of the world”

(Bresler, 2005: 120).

On 2 February 1990, President F.W. de Klerk announced the unbanning of the

African National Congress (ANC) and other freedom organisations, and also the

release of all political prisoners, amongst them the ANC leader, Mr Nelson

Mandela (Bresler, 2005: 120). The sanctions were lifted and many opportunities

opened up for South Africa. The country was positively marketed internationally

as a tourist destination, more airlines started flying to South Africa and co-

operation between the Southern African countries increased (Lubbe, 2003: 27).

South Africa was exposed again to international markets. Overseas tourists were

once again encouraged to visit South Africa, and South African citizens were free

to visit overseas destinations that had previously been closed to them. The first

democratic elections held in April 1994 also impacted profoundly on the tourist

industry. Although many foreign tourists avoided the country at the time of the

elections, thousands of international journalists and observers injected millions of

rand into the local tourist industry (Bresler, 2005: 120).

29

After 1994 tourist activity increased considerably. The figures of total foreign

visitors, as recorded by South African Tourism (2005b), prove the tourism growth

experienced in the country and they are as follows:

Year – Total foreign visitors

1994 – 3 896 547

1995 – 4 684 064

1996 – 5 186 221

1997 – 5 170 096

1998 – 5 898 236

1999 – 6 026 086

2000 – 6 000 538

2001 – 5 908 024

2002 – 6 549 916

2003 – 6 504 890

2004 – 6 677 839

In the past eleven years tourism in South Africa has been expanding and working

towards optimising its potential. Today, South Africa probably has the best

accommodation facilities and transport infrastructure in all of Africa (Bresler,

2005: 117). The tourist arrival statistics for 2002 confirmed that South Africa is

the fastest growing tourist destination in the world (South African Tourism, 2003)

and that the country has a lot to offer in terms of genuine warmth and hospitality,

diverse cultures and heritages, wildlife, scenic beauty and adventurous

opportunities, conference facilities and eco-tourism.

Recently, a new tourist trend has become evident in the country. A company,

Master Currency, undertook a survey, which established that 69 percent of airline

passengers to Johannesburg are either returning emigrants or people coming to

shop (South Africa Travel Guide Online 2004). Puk, chief executive officer of

Sure Travel, stated in the South African Travel Guide Online that many people

30

that used to go to Dubai to shop in bulk quantities are now coming to South

Africa instead. Shopping is the second most common reason amongst

foreigners, after holiday reasons, for coming to Gauteng (South African Tourism,

2005c: 12). This has further contributed to increasing the popularity of the

country. Another event that needs to be mentioned is South Africa winning the

bid for the 2010 Soccer World Cup. This means that the tourism industry of the

country will benefit enormously from all the opportunities that will arise from

hosting such an event and South Africa stands a good chance of becoming an

even more popular tourist destination.

Perceptions of high crime rates in South Africa and other Southern African

countries have, however, significantly deterred international tourists from visiting

(George, 2001: 44). Tourists could be particularly sensitive towards travelling to

destinations that might put them at risk. That is why ensuring safety and security

has become very important for all tourism service providers.

The domestic tourist market plays an important role in the South African

economy. It was valued at R47 billion for the period 2002/3, as opposed to the

international market value of R53.9 billion, and research indicates that there is

opportunity for further growth (Department of Environmental Affairs and Tourism,

2004). In 2003 South Africans undertook over 49 million domestic trips, of which

64 percent was to visit friends and family, 16 percent for holiday, almost 11

percent for religious purposes, 6.2 percent for business and 16 percent for

medical reasons (South African Tourism, 2004b: 1). Domestic tourism is driven

by school holidays with the largest number of trips taken in December (summer

holiday), then in July (winter holiday) and April (Easter holiday). In terms of

provincial popularity, Kwazulu- Natal received the biggest share of domestic trips

– 13,9 million trips, followed by Gauteng – 8.6 million, Eastern Cape – 7.5 million,

Western Cape – 5.2 million, Limpopo – 4.6 million, Free State – 3.3 million,

Northwest – 3 million, Mpumalanga – 2.5 million and Northern Cape – 0.8 million

trips (South African Tourism, 2004b: 4).

31

Tourism in South Africa is currently undergoing transformation. A lot of emphasis

is being placed on internal marketing. Internal marketing is promotion of the firm

and its products to the firm’s employees. Through it the company’s staff become

educated, aligned and motivated in achieving the company’s objectives, said

Crick (2003: 161). The author added that on a larger scale, the successful

implementation of a tourism programme depends on the internal marketing of

tourism to the community. In other words, internal marketing of tourism is in fact

development of domestic tourism. The government is putting programmes in

place to assist the emerging entrepreneurs in the tourism sector. An emphasis is

placed on educating and involving local communities and previously

disadvantaged groups to participate in the tourism value chain. The

transformation of the industry is also involved in encouraging local South Africans

to travel more and see the country. Currently, only 30 percent (14 million) of the

population of the country take trips for holiday purposes (Department of

Environmental Affairs and Tourism, 2004) and the majority of domestic travellers

stay with friends and family, rather than using the services of guest houses,

hotels or other accommodation providers (South African Tourism, 2005d: 9).

High importance is placed on capturing a bigger share of the black market.

Abrahamse in Ludski (2001) identified a need to develop an understanding of the

needs of the local tourists in order to draw black South Africans into the market. It

is critical that all people of a country support the tourism industry, because

growth in the domestic market will increase the value of the market and will help

combat issues of seasonality, geographic spread and limited trip expenditure.

Further development of domestic tourism will lead to improvement in the quality

of the products and services, will increase the confidence of international tourists

about coming to South Africa, will secure stable occupancy levels and will create

job opportunities (Department of Environmental Affairs and Tourism, 2004).

32

2.4 The accommodation industry in South Africa

The nature of accommodation supplied at a destination is mainly a function of

demand – in other words, it is tourists who determine what type of

accommodation will be established at the destination area. Some prefer the full-

amenity type of accommodation, whilst others are content with the bare

essentials (Jordaan, 2001: 36).

Tourist accommodation includes all establishments offering overnight

accommodation on a commercial basis. Accommodation is part of the tourism

product that provides a support service for a wider motivation, which has brought

a visitor to a specific destination (Bresler, 2005: 198). For business travellers,

accommodation is a necessary facility that makes it possible, convenient and

comfortable to engage in the primary reason for travel – i.e. business. For leisure

travellers, accommodation is integrally related to the attractions of a destination

and it is also a part of the facilities (Middleton & Clarke, 2001: 390). When

selecting a holiday destination, the image and quality of the accommodation

might have a strong influence on the choice.

In South Africa the list of types of accommodation that the travellers can choose

from is considerably long. It includes: hotels, motels, B&Bs, guest houses,

cottages, lodges, mountain huts, flats, rooms, rondavels, caravan parks, time

share accommodation, accommodation for back packers, resorts and others. In

Paragraph 1.4 it was established that the South African hotel industry is

recognised as one of the most important sectors of the domestic economy. It is

characterised by the presence of many of the world’s best-known brands

including Holiday Inn, Sheraton, Hyatt, Hilton, Inter- Continental, Radison and

home grown brands such as Southern Sun, Protea Hotels & Inns, City Lodge,

Sun International and others (Jordaan, 2001: 151). While hotels have traditionally

33

offered a full range of services to the travelling public, the industry now provides

for all types of needs and expectations (Jordaan, 2001: 156).

In 2000 and 2001, the accommodation industry of South Africa had relatively

stable occupancy rates. In 2002 and 2003 the country received increased global

exposure due to the United Nations World Summit (in 2002) and the Cricket

World Cup (in 2003), which were held in South Africa. This resulted in a sharp

increase of the occupancy rates for these two years (Koumelis, 2004). Foreign

travellers perceived the country as a value-for-money destination, because in the

past years the weaker rand made it possible for tourists to enjoy high-class

holidays for less money, as compared to prices in other countries. Recently,

however, South African hotels’ occupancy rates have been falling and Koumelis

(2004) attributes it to the stronger South African currency that the country has

been experiencing since the beginning of 2004. Today the stronger rand implies

that foreigners will have to pay more, in terms of their home currency, in order to

come to South Africa for a holiday. This resulted in a decline of over two million

bed nights sold in 2004 as compared to 2003 (South African Tourism, 2005a:

62), and over six billion rand decline of Total Foreign Direct Spent in South Africa

(South African Tourism, 2005b: cover page). There was a further decrease in

bed nights sold in 2005, as the figures for the second quarter are 11.9 percent

less than the first quarter (Statistics South Africa, 2005b: 2). Additionally, the

most common length of stay of domestic tourists for the first quarter of 2005 was

only two nights (South African Tourism, 2005d: 9) and for foreigners in 2004 was

also only two nights (South African Tourism, 2005b: 83).

The country has also been experiencing airline capacity problems for the past

few years. South African Airways (SAA) has been criticised by the government

for not keeping pace with the growing tourism demand (Hicks, 2003). However,

the Tourism Authorities are committed to increasing the air access to the country

(Koumelis, 2004). This will help to bring more people to the country and through

increased availability of flights to South Africa, the cost of travel to the country

34

could be decreased. This would contribute positively to restoring the value-for-

money perception of tourists and would also favour tourism growth and

accommodation providers.

The stronger rand creates an advantageous situation for small establishments

like guest houses. In general guest houses are more cost effective for tourists as

compared to hotels. The average cost of hotel accommodation tends to be

around R400 a night, while an average guest house charges between R200 and

R250 a night (Gillingham, 2004). The hotel charge may or may not include

breakfast, while almost all guest houses include breakfast in their tariff. In other

words, by using guest houses, organisations or travellers can cut their

accommodation bills almost in half (Gillingham, 2004). However, guest house

managers/ owners should take into consideration that the hotels generally have

more financial resources available and could use tactical price cuts in the form of

sales promotions in order to attract as many tourists as possible. Guest houses

on the other hand, might not be in a financial position to reduce their prices, and

this might lead to hotels and guest houses offering accommodation at similar

prices. In such a situation of increased competition, it would be of great

importance to guest houses and other small-scale operation establishments to

know what their customers expect from the service provider. Having this

knowledge, guest houses would be able to provide a satisfactory service offering

to their customers and would be able to attract and retain customers.

2.5 The guest house sector in South Africa

A guest house, as defined by the Tourism Grading Council of South Africa

(TGCSA, 2002), is either a converted house adapted to accommodate overnight

guests or it may be a purpose-built facility. A guest house is run as a commercial

operation and it is often owner-managed. It has public areas, which are for the

exclusive use of the guests. The owner/ manager either lives off-site, or in a

separate area on the property.

35

Guest houses generally compete for a share of the tourist market with all kinds of

accommodation providers, however, they are in direct competition with Bed and

Breakfast (B&B) establishments, which offer similar services. Owing to the

similarity of the two, B&Bs will be included in the study and when the term guest

house is used it would represent guest houses and B&B establishments. Bed

and Breakfast accommodation, according to TGCSA, is usually provided in a

family (private) home and the owner/ manager lives in the house or on the

property. Breakfast is usually served. Bathroom facilities may or may not be en-

suite and/ or private. In general, the guests share the public areas with the host

family.

2.5.1 Historical background

In this section, the information provided on guest houses explains how they came

about, what they are and what they offer to their guests.

In the past decade a growing trend towards guest and country house type of

accommodation has emerged. The guest house concept originated in Europe. In

South Africa the first guest houses became evident in 1991, but the real growth

only took place since 1995 (Jordaan, 2001: 171). In Gauteng there are 115

registered guest houses and 203 registered B&B establishments and they

provide 1774 rooms and 3648 beds for travellers (City of Johannesburg official

website, 2005).

The guest house industry today is highly competitive, as it was previously

discussed in Paragraph 1.1, and the different guest houses compete in terms of

the services and quality offered to their customers. Initially guest houses started

as a source of second income and in some instances as the only income. Until

recently the guest house sector was regarded as dominated by white people, but

today more and more black people are following the same example and are

offering to their customers the experience of traditional customs and cuisine

(South African Tourism, 2004a). Many foreign guests feel that in large

36

commercial operations they do not have enough contact with the country’s

people, therefore they choose to stay in a guest house, where they are in a

homely atmosphere and in close interaction with the guest house owners and

their staff and where they can learn more about the traditions and the customs of

the country (Paragraph 1.4). From the foreigners that make use of the services of

guest houses, European tourists seem to be frequenting those establishments

much more than their African, Indian and Australian counterparts (South African

Tourism, 2005b: 91). However, South African Tourism (2005b: 14) established

that the largest share of foreign tourists to South Africa is land-based travel from

neighbouring Southern African Developing Countries (SADC). Short haul visitors

to SA from SADC, Central and East Africa made up 69 percent of visitors to the

country in 2004 and long haul visitors from overseas and North Africa made up

31 percent (South African Tourism, 2005b: 14). It was also established that

tourists from these countries stay mostly at hotels or with friend and family.

Therefore these customers represent an opportunity for a target market for guest

houses.

2.5.2 Guest house management

The management of the guest houses is usually done by the owners or,

alternatively, they employ a manager. The owners do not necessarily have any

experience in the hospitality industry, but the success and survival of their

establishments depend on their good business sense, managerial skills and

expertise (Henning & Willemse, 1999a: 4). It is important to recognise that a

distinct and significant range of management issues confront small hospitality

firms (Morrison & Thomas, 1999: 149). Managers are challenged with balancing

and satisfying needs of consumers, owners or operating companies and

employees (Jayawardena & Haywood, 2003: 195). Marketing an establishment

involves some kind of research into customer needs, a marketing plan and

choosing the correct promotional methods in order to reach the target market.

Advertising is also expensive for small companies (Misner, 1994: 37) and guest

37

houses might not have surplus funds to employ in order to reach their customers.

Guest house owners, as mentioned in paragraph 2.2, have the advantage of

being in contact with their guests, which allows them to detect customer needs,

behaviour and satisfaction or complaints (Middleton & Clarke, 2001: 183). Their

customer knowledge is better than hotel’s customer knowledge, because they

receive customer feedback on a daily basis and this is why guest houses could

satisfy customers better. This is also why guest house owners who have some

management and marketing knowledge and know how to use the feedback from

the customers would successfully reach their target market.

Quality management is also an issue by means of which, if addressed efficiently

and effectively by the manager, a guest house could gain advantages over its

competitors and achieve a more secure financial future. The owner/ manager

should be able to promote a preventative system of quality control. Furthermore,

the owner/ manager should be an entrepreneur. As Morrison and Thomas (1999:

153) state, many of the management challenges confronting small hospitality

firms have the potential to be addressed through entrepreneurial practices.

“Because tourism is a relatively new industry, communications and access to

information is the major obstacle to growth and development,” said Abrahamse in

Koumelis (2003: 1). She also stated that many entrepreneurs recognise the

opportunity to become involved in tourism, but are having difficulty in

understanding what they need to have in place in order to be a player in the

industry. Additionally, small, family-run accommodation establishments rarely

take steps to acquire information and skills that do not have immediate

application to the solution of a specific technical or managerial problem (Bresler,

2005: 200). This is why the study could provide useful guidelines on customer

expectations, perceptions and behaviour, which would help guest house

managers/ owners to satisfy customer needs and would contribute to successful

operation of their business.

38

Some guest houses have started to work together and form their own guest

house networks. They are also building relationships with other suppliers, like car

rental companies, tour operators, travel agents and tourist information centres.

Networking helps to reach a broader field of clients, to ensure more stable

occupancy rates and also to save on marketing costs.

High crime figures in any country represent a threat to the hospitality industry. In

South Africa tourists and travellers are encouraged to be aware and cautious

when exploring the attractions offered at destinations. Hospitality services

providers are also urged to ensure the safety of their patrons. Guest houses are

small establishments, therefore it is easier to control the safety and security of

their guests. It is more difficult for an intruder to walk unnoticed into a small

establishment than a large one, where the front office staff is often busy (Callan

& Fearon, 1997: 170).

2.6 The guest house product offering

The product offering of a guest house is part of its marketing mix. For an

organisation to be successful with its marketing mix, it has to develop a

differential advantage, which will distinguish the organisation’s product offering

from that of the competitors (Cooper, Fletcher, Gilbert, Shepherd & Wanhill,

1998: 411). A differential advantage could only be achieved in certain areas of

the hospitality product. What is the guest house product? A product, as defined

by Kotler, Bowen and Makens (1996: 274), is anything that can be offered to a

market for attention, use or consumption that might satisfy a want or a need. It

includes physical objects, services, places, organisations and ideas. In terms of

hospitality and tourism, the product is a combination of the core product, the

facilitating product, the supporting product and the augmented product.

The core product is the basic need function served by the generic product

(Seaton & Bennett, 1996: 121). For guest houses the core benefits offered are

shelter and rest. The facilitating products are those services or goods that must

39

be present for the guest to use the core product (Kotler et al., 1996: 275). A

guest house, for example, has a reception area where the guests can check in

and out, telephones, a dining room where breakfast and dinner are served, and

parking facilities as facilitating products. Core products require facilitating

products, but do not always require supporting products. Supporting products are

those that add extra value to the core product and help to differentiate it from the

competition. Examples of supporting products in guest houses are: shampoo and

shower gel in the bathroom or a bottle of mineral water in the room. An example

of a supporting service is the opportunity for foreign guests to communicate in

their home language with the owners. Many guest house owners speak German

or French or Italian or languages other than English. This facilitates foreign

travellers and provides added benefits to the product. The distinction between

supporting and facilitating products is not always clear. Sometimes, depending

on their personal needs, customers could see the supporting product as

facilitating and vice versa. Seaton and Bennett (1996: 121) grouped the

facilitating and supporting products in one and called them the tangible/formal

products. The authors have further defined them as the specific features and

benefits residing in the product itself – like styling, quality, brand name, design

and others. The augmented products are the add-ons that are extrinsic to the

product itself, but which may influence the decision to purchase. They include

accessibility, atmosphere, customer interaction with the service organisation,

customer participation and customers’ interaction with each other (Kotler et al.,

1996:276). In other words the augmented service offering combines what is

offered and how it is delivered.

2.6.1 The guest house product offering characteristics

Quality is an important contributor to a differential advantage of a guest house. A

customer who receives quality for his money would leave the establishment

satisfied and would talk to friends and family about his experience. He will

promote the guest house to others by word of mouth, which is a powerful

40

marketing tool. A satisfied customer would bring repeat business for the guest

house and would help to generate new customers. Word-of-mouth advertising

could be more effective than any paid advertising the firm might use (Zeithaml &

Bitner, 2003: 162).

Quality, as Fontaine stated (in Hall, 1990: viii), means each person doing his or

her job correctly each and every time. Defining quality in the service industry is

not straightforward and obvious owing to the fact that human interaction is more

complex compared to the other industries, where the products are physical

goods rather than services. In the manufacturing industry, the customers

evaluate the quality provided by evaluating the goods purchased, on the basis of

whether they work as effectively as advertised. The contact with the seller is

limited to obtaining information about the product and then selecting to purchase

it, or not. The quality is then evaluated on the properties of the actual goods. The

service offering or the guest house offering in this case, however, has unique

characteristics. They are:

• Intangibility

Hospitality services cannot be seen, tasted, felt, heard or smelled before

being bought – they are intangible. That means that customers are unsure of

what exactly they are purchasing and an element of risk is present, because

they cannot evaluate or test the service beforehand. That is why customers

rely on word of mouth communication from people that have experienced the

service offering (George, 2001: 20).

• Inseparability

The guest house offering is sold first, then produced and consumed at the

same time. Therefore the way that the offering is delivered is crucial and the

service providers, the staff, become part of the offering. Additionally, other

consumers also become part of the offering, as they can affect the overall

experience in a positive or a negative way.

41

• Variability (Heterogeneity)

Tourism offerings and experiences vary according to a given situation. The

service providers are not all the same, they are human beings, and they

deliver different levels of service. Similarly, no two consumers are precisely

the same – they have different demands, expectations, tastes, moods,

perceptions and emotions (George, 2001: 21).

• Perishability

The guest house offering cannot be saved, stored, resold or returned – the

product is perishable. If a hotel room is not sold, the revenue for that day is

lost and cannot be recovered.

In the service industry the products are intangible and the evaluation of the

quality is based on the continuous interaction of people with people. The quality

of the interaction can rarely be standardised to ensure uniformity. The process

starts from the point of acquiring information about a destination, then making a

reservation, travelling, arriving, the actual stay and then getting back home.

Throughout the process the customer forms subconscious expectations, which

are compared with the actual experience. These are used as criteria when

evaluating the quality of the performance received. The criteria to evaluate the

performance are complex and depend on each individual’s perception and

expectation. At the same time the performance varies from producer to producer,

from customer to customer, from day to day and from situation to situation.

It is imperative that guest houses deliver to their customers the highest standard

of quality desired. Guest house owners/ managers should learn how customers

evaluate and what they expect from the service offering, so that they can ensure

that their product will generate the ultimate customer satisfaction. They must also

use this knowledge to attract similar customers to their establishment. Customers

42

with similar needs would have more in common and this would enhance their

experience at the guest house.

2.6.2 Differentiating the guest house offerings