Embed Size (px)

Citation preview

Report No. 4686-BEN F L L

BeninCountry Economic Memorandum(In Four Volumes) Volume 1: Economic Performance and Prospects

March 15, 1984

Western Africa Region

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUTIVALEINTS

Currency Unit = CFAF 1/US$1.00 CFAF 355-CFAF 1,000 US$2.81

WEIGHTS AND MEASURES

1 meter (m) - 3.28 feet (ft)1 kilometer (km) 2 0.62 mile (mi)1 square kilometer (km ) = 0.386 square mile (sq. mi.)1 metric ton (m ton) = 2,204 pounds (lb)

1 hectare (ha) 3 2.47 acres1 cubic meter (m ) 1.308 cubic yards

FISCAL YE4R

January 1 - December 31

1/ The CFA Franc (CFAF) is tied to the French Franc (FF) in theratio of FF I to CFAF 50. The French Franc is currently floating.Throughout the text the CFAF/dollar equivalents are establishedusing the rate of CFAF 355/$.

FOR OFFICIAL USE ONLYABBREVIATIONS AND ACRONYMS

AfDB African Development BankAGB Societe d'Alimentation Generale du BeninBCXAO Banque Centrale des Etats de l'Afrique de l'Ouest

BBD Banque Beninoise de DeveloppementBCB Banque Commerciale du BeninBOAD Banque Ouest Africaine de DeveloppementCAA Caisse Autonome d'AmortissementCARDER Centre d'Action Regionale pour le Developpement RuralCATS Cooperative Agricole du Type SocialistCCCE Caisse Centrale de Cooperation Economique (France)CEB Compagnie Electrique du Benin/Communaute Electrique du BgninCNCA Caisse Nationale de Credit AgricoleCPU College Polytechnique UniversitaireDEP Direction des Etudes et de la PlanificationDPE Direction de la Planification d'EtatEC European CommunitiesECOWAS Economic Community of West African StatesEDF European Development FundENU Ecole Normale SuperieureFAC Fonds d'Aide et de Cooperation (France)FAS Fonds Autonome de Stabilisation et de Soutien des Prix de

Produits AgricolesFED Fonds European de DeveloppementFLASH Faculte des Lettres, Arts et Sciences HumainesFNI Fonds National d'InvestissementFRA/GTZ The German Association for Technical Co-operationFSA Faculte des Sciences Juridiques, Economiques et PolitiquesFST Faculte des Sciences TechniquesGRVC Groupement Revolutionnaire a Vocation CooperativeIBETEX Industrie Beninoise des TextilesIDA International Development AssociationIFAD International Fund for Agricultural DevelopmentINSAE Institut Nationale de la Statistique et de l'Analyse EconomiqueINEEPS Institut National pour l'Enseignement de l'Education Physique

et SportiveINSS Institut National des Sciences de la SanteINE Institut National de l'EconomieINSJA Institut National des Sciences Juridiques et AdministrativesMDRAC Ministere du Developpement Rural et de l'Action CooperativeMPSAE Ministeredu Plan de la Statistique, et de l'Analyse EconomiqueOBEKAP Office Beninoise des Manutentions PortuairesOCBN Organisation Commune Benin-Niger des Chemins de Fer et des TransportsPAC Port Autonome de CotonouPAM Programme d'Alimentation MondialeSBEE Socigte Beninoise d'Eau et d'ElectriciteSCO Societe des Ciments d'OnigboloSNAFOR Societe Nationale pour le Developpement Forestier

This document has a restricted distribution and may be used by recipients only in the performance ofI their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

ABBREVIATIONS AND ACRONYMS (continued)

SOBEPALH Societe Beninoise de Palmiera HuileSOBEMAC Societe Beninoise des Materiaux de ConstructionSOBETEX Societe Beninoise des TextilesSONACEB Societe Nationale de Commercialisation et d'Exploration du BeninSONACI Societe Nationale des CimentsSONACOP Societe Nationale de Commercialisation des Produits PetroliersSONAFEL Societe Nationale des Fruits et LegumesSONAGRI/SONAPRA Societe Nationale pour la Production AgricoleSONAPECHE Societe Nationale drArmement et de Peche

COUNTRY DATA - BENIN page 1 of 2

AREA POPULATION 1/ DENSITY112,622 sq km 3.34 million (1979)-

Rate of growth: 2.7% (1961-79) 29.6 per sq km (1979)

POPULATION CHARACTERISTICS (1979) HEALTHCrude Birth Rate (per 1,000) 47.5 Population per physician 20.734Crude Death Rate (per 1,000) 18.5 Population per hospital bed 906Infant Mortality (per 1,000) 45.0Life Expectancy at Birth (years) 46.9

EDUCATION (1979) ACCESS TO SAFE WATERAdult literacy rate: 11.0% % of population - urban: 50Primary school enrollment: 47.0% - rural: 20

2/GNP PER CAPITA IN 1981-/: US $279

GROSS DOMESTIC PRODUCT IN 1981- : ANNUAL RATE OF GROWTH (1978 prices)

US $Mln. % 1972-76 1977-81

GDP at Market Prices 951.8 100.0 0.7 3.2Gross Domestic Investment 333.6 35.0 10.9 20.4Gross National Savings 12.5 1.3 25.8 -28.0Exports of Goods, nfs 298.9 31.4 -2.8 7.3Imports of Goods, nfs 658.0 69.1 0.2 12.0Current Account Balance -328.9 -34.6 7.3 23.4

OUTPUT, EMPLOYMENT AND PRODUCTIVITY IN 1981:

Value Added Labor Force Value Added per WorkerUS $Mln. % '000 % US $ %

Primary Production 369.8 43.7 1,253.6 73.6 245.0 59.4Secondary Production 108.0 12.8 103.9 6.1 1,039.5 209.4Services4 / 367.6 43.5 345.8 20.3 1,063.0 214.4

Total-' Average 845.4 100.0 1,703.3 100.0 496.3 100.0

GOVERNMENT FINANCE (PROVISIONAL)

CENTRAL GOVERNMENT(CFAF Billion) % of GDP

1981 1981 1976-80

Current Revenues 52.6 20.2 15.5Current Expenditures 34.8 13.4 10.7Net Lending and Transfers 3.2 1.2 2.6Current Surplus 14.6 5.6 2.3Capital Expenditures 25.1 9.7 3.7Overall Balance 10.5 04.1 -1.4External Borrowing and Grants 13.9 5.3 2.5

_/ Population Census .2/ At current exchange rates.3/ Coversions to dollars in the table are at the average exchange rate prevailing

during the period covered.4/ GDP at factor costs

COUNTRY DATA - BENIN (continued) page 2 of 2

MONEY, CREDIT AND PRICES1976 1977 1978 1979 1980 1981

(in millions CFAF outstanding end year)

Money Supply (money and quasi-money) 30,631 34,918 39,017 46,774 61,408 71,292Claims on Central Government / -7,082 -9,422 -12,917 -11,776 -17,543 -20,853Claims on the Private Sector- 32,100 38,600 47,100 59,400 85,000 87,000

(percentage or index numbers)

Money as % of GDP 22.1 23.2 23.2 23.9 28.5 27.6General Price Index 83.8 86.8 100.0 113.3 131.4 159.2

Annual Growth RatesGeneral Price Index 3.6 15.2 13.3 16.0 21.2Net Claims on Government -/ -33.0 -37.1 8.8 -49.0 -18.9Claims on the Private Sector- 20.3 22.0 26.1 43.1 2.4

BALANCE OF PAYMENTS (in US$ millions) EXTERINAL DEBT, DECEMBER 1981 (US$ millions)

1978 1979 1980 -198-1- Public debt incl. guaranteed 617.8

Export of goods, nfs 222 261 323 299 Non-guaranteed private debt

Imports of goods, nfs 370 509 703 658 Total outstanding & disbursed 617.8

Resource gap (deficit = -) -148 -207 -380 -359 2/NET DEBT SERVICE RATIO FOR 1981- (%)

Workers remittances 37 39 44 38 Public debt inclu. guaranteed 6.8

Non-guaranteed private debtNet transfers and otherToaousndg dibre

factor payments 3 -1 -2 -7 Total outstanding & disbursed

Balance current account -108 -169 -338 -328 IBRD/IDA LENDING (November 30, 1982) (US$ million)

Direct private investment 1 17 40 34 IBRD IDA

Official flowsGrants 38 64 51 85 Outstanding & disbursed -- 72.00Borrowing (net) 35 54 277 180 Undisbursed -- 63.57

Short term capital 16 14 21 12 Outstanding i. undisb. -- 135.57Other items, errors and

omissions 4 7 -46 71 RATES OF EXCHANGEIncrease in reserves (+) -22 -13 5 54 Year US$1-CFAF

Net reserves (end year) -2 -15 -10 44 1975 214.32Gross reserves (end year) 14 13 8 61 1976 238.98Equivalent months imports 0.5 0.4 0.2 1.2 1977 245.67

1979 212.721980 211.301981 217.731982 328.621983 on 355.00

1/ Includes public enterprises2/ Debt service as a percentage of exports of goods and non=factor services

Non-available

VOLUME I

BENIN: ECONOMIC PERFORMANCE AND PROSPECTS

TABLE OF CONTENTS

SUMMARY AND CONCLUSIONS .......................... 3

I. BACKGROUND. 8

II. RECENT ECONOMIC DEVELOPMENTS. .. .... 10

A. Sources of Growth .... 10B. Expenditure on Available Resources . . .. 15C. Employment, Wages and Manpower Training ... 18D. Money, Credit and Prices ... 20E. Public Finance ....................... ........ 22F. Public Enterprises .. .. ................. 25G. Balance of Payments .............................. 26H. External Debt and Foreign Aid . . .. 28

III. SECTOR PERFORMANCE AND ISSUES . . .30

A. Agriculture ................................ .. . .. . 30B. Industry ...................... 36C. Transport ... 41D. Energy ... 43E. Social Sectors ................... 44

IV. DEVELOPMENT PROSPECTS ........................... 47

A. Benin's Development Plan for the Mid-1980s .47B. Medium-Term Projections........................... 52

V. DEVELOPMENT STRATEGY ISSUES AND RECOMMENDATIONS ... 58

A. Comparative Advantage ... 58B. Public Enterprises ....... . 60C. Major Projects.... ........ ..... .. . 61D. Public Finance .. .62

E. Public Investment Constraints ..... 63F. Planning Process ..... . . 64G. Concessionary Financing . . . .66

2

PREFACE

This report is based on the findings of an economic mission that visited Beninin June 1982. The mission was composed of the following members:

Raymond Rabeharisoa, Senior Loan OfficerMaria E. Freire, EconomistDavid Bovet, Consultant (Coordinating Author)Manga Kuoh, Industrial Project Officer (Public Enterprises)Kuldeep Ohbi, Transport Economist (Transport)Peter Boone, research Assistant (Agriculture)Bill Shaw, Research Assistant (Social Sectors, Public Finance)

Mr. Robert Crown, Agricultural economist, collaborated in thepreparation of the Agriculture Chapter in Volume II.

This report is the final version of the draft discussed with the Government by aMission which visited Cotonou in late 1983*. The report includes four volumes:

Volume I: Benin: Economic Performance and ProspectsVolume II: The Economic and Social SectorsVolume III: The Public Enterprises SectorVolume IV: Statistical Appendix

* The Mission consisted of Richard Westebbe, Chief, Sven Kjellstrom, ResidentRepresentative, Manga Kuoh, Loan Officer, Emmanuel Akpa, Country Economist,Peter Boone, Consultant, Peter Ludwig, Transport, and Messrs. Marc Blanc,Henri Marticou, Eugene Sinodinos of WAPA A, Abidjan. A joint Government-World Bank communique was issued summarizing the conclusions of thediscussion.

SUMMARY AND CONCLUSIONS

1. Major changes in Benin's economic policies and performance haveoccurred over the past five years. A key decision to increase public controlover the modern sector of the economy was implemented during the second halfof the 1970s, leading to financial problems in several of the leadingindustrial and service enterprises. The First Plan (1977-1980) proposedambitious public investments in a few large projects, and these have now beenimplemented with mixed results. Rapidly-increased external debt, coupled withthe recent weakness in demand overseas and in neighboring Nigeria, has led toa difficult public finance situation at present.

2. In the face of these developments, the Government has recently takenpositive steps to eliminate economic distortions and improve the management ofpublic finance. Agricultural producer prices are being raised and inputsubsidies eliminated in a planned fashion. Pricing, personnel and managementpolicies affecting the public enterprises are being revised, and some marginalunits have been liquidated. Greater attention is being devoted to Benin'simportant economic relations with its neighbors. Assistance has been soughtto strengthen the Government's ability to manage its public finance, externaldebt and planning functions. These very recent policy changes should lay thebasis for more vigorous growth in the longer term.

Recent Economic Developments

3. Benin remains a small, poor nation, with an estimated 1981 GDP percapita of $270 for a population of 3.5 million. Three-fourths of the laborforce is engaged in traditional farming activities. The industrial sectorconsists of a few import substitution and agricultural processing plants.Recently, exploitation of local petroleum, cement and sugar resources hascommenced. Exports of these commodities--just now beginning--will faroutweigh traditional exports of oil palm products and cotton. Unofficialexports of foodcrops and re-exports of imported consumer goods to Nigeria andNiger continue. In the social sectors, education has reached many morechildren than previously, though at a sacrifice in quality terms. Healthconditions remain poor, and life expectancy at birth is 47 years.

4. Real GDP growth over the 1976 to 1981 period averaged 3.6 percent perannum, up substantially from the 0.7 percent annual trend during 1972-1976.Although Benin's economic statistics are notably weak, growth appears to havebeen particularly strong in 1977 and in 1981, when there were sharp increasesin construction, manufacturing, trade activity and public administration.This growth was linked to the heavy public investment program and to strongdemand in neighboring countries. Agriculture, on the other hand, hasconsistently grown by less than one percent per annum over the last tenyears. Traditional export crops have suffered from inadequate Governmentpricing policy, shortages of modern inputs, and poor weather conditions. TheGovernment has recently adopted a policy aimed at improving agriculturalincentives. Certain foodcrops that enjoy strong demand in Benin andneighboring markets have performed well.

4

5. The external sector has been characterized by major and risingdeficits on the current account. Substantial imports of capital goods havebeen recorded, financed by suppliers credits and official sources, in supportof the major public investment program. As gross domestic investment reachedthe very high level of 35 percent of GDP in 1981, the current account deficitincreased to 34 percent of GDP. Both investment and the current accountdeficit are expected to decline in coming years, relative to GDP. On theexport side, unrecorded exports have climbed to an estimated 86 percent oftotal exports in 1981, while recorded commodity exports declined in realberms.

6. iNet borrowing rose dramatically in 1980 and 1981, on moderatecommercial and official terms not linked to Eurodollar rates. Total debtoutstanding (including undisbursed) quadrupled from 1976 to 1981, reaching anestimated $589 million (CFAF 209 billion). Virtually all Benin's foreign debthas been contracted by the Government or is Government-guaranteed. The debtservice ratio has increased from 4 percent of exports in 1976 to 7 percent in1981, and is projected to reach 24 percent in 1983. Financial difficultieswith several of the recent large resource exploitation projects, which nowappear likely in the case of the sugar and cement projects, may impact onpublic finances since the total debt service is equivalent to 43 percent ofGovernment revenues in 1983. However, both the sugar and cement projectsinclude Nigerian Government equity participation and joint loan guarantees.

7. Public finances, after a remarkably sound performance during the mid-1970s, have recently been characterized by a declining current surplus, withthe exception of 1981. Indications are that this surplus may be seriouslyeroded in the next few years. Current revenues, over half of which are derivedfrom import duties, have accounted for about 15 percent of GDP in recentyears. These revenues were linked to imports unofficially re-exported toNigeria and to business activity related to Benin's large investmentprogram. Both sources of taxable surplus are presently diminishing. Aboutthree-fourths of current expenditures go for wages and salaries, witheducation taking a 33 percent share of the current budget. Overall, thepublic finance position after investment expenditures has been negative.

8. Public enterprise difficulties also pose a liability for Governmentfinances. Two-thirds of the 60 enterprises are in financial difficulties.Losses have been financed by the state-owned banks, rather than throughtransfers from the current budget. As many of these losses cannot now berepaid, the Government either as shareholder or as banker will have torecognize some of these deficits. Public enterprise difficulties have stemmedfrom poor initial project design, undercapitalization, inexperienced businessmanagement, inadequate Government pricing and personnel policies, and otherinefficiencies. The Government announced in 1982 a series of valuablemeasures to strengthen the public enterprises, including more realisticpricing policies, better incentives for managers and workers, toughercontrols, and the liquidation of non-viable units. These decisions are nowbeing implemented.

5

Outlook and Issues

9. Benin's economic growth will be limited by several constraints overthe medium-term which make it unlikely that GDP will grow by more than 3 to 4percent per year during the 1982-1990 period. Key constraints are:

a. Slowdown of demand in neighboring markets and the difficulties inachieving rapid gains in agriculture or implementing new industrialactivities.

b. Reduced investment levels due to lack of identified, viableprojects and borrowing capacity restricted by present debt level.

c. High recurrent costs of existing investments and policies.d. Impact of the three major projects--petroleum, sugar and cement--

on public finance.

10. These constraints make it all the more important that policy changesbe adopted to provide better incentives in agriculture and industry, and tocontrol the potential drain on public finance which would be caused by furtherpublic enterprise and major project losses. The mission estimates thatsubstantially higher economic growth can be achieved with proper policies thanunder an alternative scenario incorporating continued difficulties inagriculture, industry and trade. The debt service and public financeconstraints are serious in either case:

Best-Estimate Alternative Scenario"Favorable" Scenario "Less Favorable" Policies

----real growth rates, percent p.a., 1982-90---

GDP Growth 3.4 2.1Exports Growth 7.5 5.4Imports Growth 2.7 0.7Govt. non-debt current spending 3.7 2.7

--------- Ratios, 1990-------------------

Private consumption per capita vs.1982 96 90GDI/GDP 25 21Debt Service/Exports 23 26Debt Service/Government Revenues 55 58

11. The Benin Government has recently reviewed a number of policies inlight of national and international economic problems. The Second Plan (1983-1987) presented to donor countries in March 1983 outlines the Government'scritique of past performance and strategy for future development. Problems ofexcessive centralization, inadequate management and technical training, andthe need for better planning are discussed. And specific actions have beentaken, including price increases, cutbacks in the hiring of new collegegraduates by the civil service, a more formal project analysis procedure, andgradual elimination of agricultural subsidies. The Government has requestedassistance in the management of external debt information, in theestablishment of closer public finance controls, in the evaluation ofindustrial projects and policies, and in the strengthening of the planningfunction. The World Bank Group is prepared to support these requests.

6

12. A broad range of issues currently confronts the Government in itsdifficult tasks ahead. Critical questions include:

a. Comparative Advantage. It will be essential to focus oninvestments in economic activities that enjoy a strong demand and comparativecost advantages. Foodcrops, natural resources, and selected manufacturingactivities appear to meet these criteria. Appropriate economic incentives inagriculture and industry should be further encouraged.

b. Public Enterprises. The means to implement policy decisionsalready taken must be worked out in detail. For specific enterprises,rehabilitation plans need to be prepared based on in-depth feasibility andorganizational studies. Financial resources, domestic and foreign, will berequired to strengthen long-term viable enterprises, and the World Bank Groupis prepared to assist in this effort. The Government may wish to reduce itsrole in enterprises which are not profitable or of strategic importance.

c. Major Projects. The three large projects--petroleum, sugar andcement--represent an investment equal to 70 percent of the 1981 GDP. Problemswhich have arisen, particularly with regard to access to the Nigerian market,and high production costs in relation to current world prices, must bepromptly resolved to avoid serious impacts on Benin's economic and publicfinance position. Those projects are intended to be self-financing,profitable ventures and must be placed on this basis, as the Government'sbudget cannot underwrite losses on projects of this magnitude. NigerianGovernment equity participation in the two projects aimed at the Nigerianmarket (sugar and cement) should help to cooperatively resolve thesedifficulties.

d. Public Finance. The public finance situation is likely to bedifficult in the years ahead, due to the recurrent cost implications of recentinfrastructure investments, the need to re-finance a number of publicenterprises, the likely counterpart funding or subsidy requirements associatedwith the three major projects now coming onstream and rising debt serviceobligations. Deficiencies exist in the management of the public financeswhich must be addressed. On the revenue side, the buoyancy in import dutiesover the past few years associated with goods destined for neighboringcountries is not likely to continue in the mid-1980s. The potential forincreasing public revenues--particularly through higher import duties whichmay still be low in comparison with neighboring countries--should beassessed. The losses from public enterprises and recent large projects mustbe stemmed and reversed to avoid drains on the Treasury. Better coordinationwith the planning process is required so that the debt burden and recurrentcost implications of projects are assessed at the time of selection. Enhancedmonitoring of key revenue and expenditure indicators, and of external debttransactions, is required.

e. Investment Constraints. The present debt level is high and willconstrain further access to foreign commercial loans. However, successfulexecution of the current large projects and an enhanced capability to identifyand plan new projects can increase the volume of capital available to Benin.Access to commercial borrowing will be more difficult in the 1980s than it wasin the past five years, and preparation of sound productive sector projectswith high rates of return will be essential to tapping these funds. Projectanalysis should therefore be strengthened.

7

f. Planning Process. Further efforts are required to develop acomprehensive yet practical planning system. Criteria must be set to ensureviable investments. Policy analysis should be introduced to permit technicalcomputations to be made of the impacts of alternative policy options. Theseimpacts include the public finance implications of investments, as well as thelikely influence on GDP, the balance of payments and employment. The relativeroles of the technical ministries and the Planning Ministry in the projectplanning cycle should be examined.

12. In light of Benin's continued poverty despite its recentextraordinary development investment effort, it is recommended that foreignassistance be provided on concessionary terms. The increased debt burden dueto heavy foreign borrowing in support of key public investments will constrainfuture access to commercial-term loans. Necessary investment in economic andsocial infrastructure, agriculture, and selected industrial projects, and inthe rehabilitation of public enterprises, requires increased levels ofofficial assistance.

13. The severity and breadth of the problems now facing Benin's economyimply a need for structural adjustment measures in the future. Flexible, non-project lending by the international donor community would be an appropriateresponse. The World Bank Group's proposed public enterprise rehabilitationproject is an example of this type of operation. While the Government hasrecognized a number of its problems and is seeking advice, concrete policydecisions will need to be taken as a pre-condition for non-project lending.

8

I. BACKGROUND

Physical Characteristics

1.1 Benin is a corridor-shaped country, running 670 km from the coast ofWest Africa north to landlocked Niger. In the south, it is 120 km widebordering Togo on the west and Nigeria on the east. The land is relativelyflat or rolling, with the exception of the Atacora hills in the northwestwhich reach elevations of 750 meters. Annual precipitation is considerablyless than in other coastal West African countries, and is subject to wideannual fluctuations. In the south, rainfall averages 1,200 mm per year in tworainy seasons, diminishing to 800 mm in the north during a single wetseason. Soils are generally poor throughout the country, but populationpressure in the south has caused pockets of soil depletion. Benin enjoysdeposits of limestone in the southeast, and petroleum off the coast.

Human Resources

1.2 Benin's population is estimated at 3.5 million in 1981, based on the1979 census. The country's inhabitants are mainly rural (71 percent oftotal). In the sparsely-settled northern provinces, population density is aslow as 10 persons per square kilometer, while in the urbanized southernprovinces it is much higher, exceeding 200 people per square kilometer inAtlantique Province. The population growth rate has been increasing and isestimated at 2.7 percent per year during the 1961-1979 period. Since lifeexpectancy is still quite low (47 years at birth), the population distributionis youthful: 49 percent are below the age of fifteen. About one-fourth ofthe adult population is literate.

Political Development

1.3 Benin achieved its independence from France in 1960, when it wasknown as Dahomey. Regional and other political rivalries during the nexttwelve years led to numerous changes of government. In 1972, Colonel MathieuKerekou assumed the presidency and ushered in a new era of politicalstability. The theme of President Kerekou's administration has been one ofnational unification, the development of an independent economic and socialidentity, and increased popular participation in political life. In 1975, theParty of the People's Revolution was created and the name of Dahomey waschanged to the People's Republic of Benin. The Party and its CentralCommittee retain key policy-making authority, although the Council ofMinisters is the governing administrative group. A new constitution wasadopted in 1977, elections were held in 1979, and President Kerekou now leadsa largely civilian government.

9

Economic Background

1.4 Agriculture, supplemented by commercial activities revolving aroundBenin's traditional transit role, is the primary basis of the country'seconomy. Natural resource exploitation in the form of cement and crude oilproduction is just beginning, and existing industrial activity is limited toagricultural processing and a few import substitution activities. Per capitaGDP is estimated at US$270 in 1981. Further details on Benin's economicbackground are contained in the previous World Bank economic report, TheEconomy of Benin (Report No. 2079-BEN), reflecting data collected during a1977 economic mission.

1.5 The 1972-76 period was characterized by low economic growth, whilethe Government concentrated on revising economic institutions and preparing adevelopment program. Growth of GDP is estimated at 0.7 percent per annumduring the 1972-76 period, mainly provided by the service sector. Output ofcash crops and manufactured goods declined, and gross domestic investment wasa moderate 15 percent of GDP. A current surplus was recorded in the CentralGovernment's public finances during the 1972-76 period. Debt service remainedlow, and was only 4 percent of exports (goods and non-factor services) in1976.

1.6 Substantial changes on the economic policy and development frontswere underway, however. A basic decision was taken to exert public controlover key sectors of the economy, and this was implemented by creating publicenterprises to manage most modern-sector activities. These included clinkergrinding, textiles, and the brewery in the industrial sector; the entirebanking sector; the electric and water utility; several transport enterprises;agricultural, livestock and fishing operations; and firms dealing with theimport and distribution of various consumer goods. With a limited amount offinancial resources for expropriations of existing private-sector firms andinitial equity for newly-created enterprises (totalling about CFAF 15billion), the Government began actively managing numerous commercial andindustrial activities formerly operated by the private sector. The economicdifficulties resulting from this major change were not clear until somewhatlater, as discussed in Chapter II.

1.7 The Planning Ministry also undertook a significant nationaldevelopment planning effort in the mid-1970s. The object was to reach a broadagreement on sectoral, regional and project priorities by engaging in a multi-level planning exercise. In late 1977, the First State Plan (1977-1980) waspublished. This plan called for a sharp increase in public investment, andemphasis was concentrated upon implementing several large projects: thecreation of a complete clinker and cement production plant at Onigbolo, thecultivation and processing of sugarcane at Save, the exploitationof offshore oil near Seme, and the doubling of capacity at the port ofCotonou.

1.8 It is against this background of low economic growth and cautiouspublic finances that the ambitious Government plans and economic interventionof the mid-1970s must be viewed. The economic performance which resultedduring the 1976-1981 period is analyzed in the following chapter.

1 0

II. RECENT ECONOMIC DEVELOPMENTS

2.1 Benin's economic situation evolved favorably in several respectsduring the late 1970s. The rate of GDP growth increased, partly due to theimpact of a substantial public investment program and partly linked to theimproved economic performance of neighboring countries. Investments includedfour major development projects with broad implications for Benin's economy.These were executed beginning in 1978 and all were operating by 1983.Furthermore, the increasing role of trade helped to expand public revenues inthe form of import duties on goods destined for re-export to neighboringcountries. Output of two tradable foodcrops (maize and yams) increased inresponse to urban demand and cross-border trade with Nigeria, though otherfoodcrops declined.

2.2 However, the heavy investment effort, expansion of the role of publicenterprises, and a recent setback in the fortunes of Benin's neighbors havecombined to raise problems in the early 1980s. Benin' s external public debthas increased sharply in connection with the financing of large investmentprojects. Current low world prices for primary commodities and depresseddemand in West Africa may jeopardize the near-term export earning potential ofseveral projects in Benin, raising a potential public finance issue becausethe external debt is guaranteed by the Government. The expanded role ofpublic enterprises in the economy since the mid-1970s has led to inefficientand costly organizational structures in industry and the modern servicesector, creating claims on the banking and public finance systems. Inaddition, Benin's traditional, though modest, exports of industrial crops havedeclined over the 1976-81 period.

2.3 This chapter briefly explores recent economic developments in Benin,against a backdrop of statistics developed during the Bank's economicmission. The quality and currentness of Benin's economic data is such thatstatistical analysis must be regarded as approximate. For instance, GDPgrowth over the 1972-1976 period, now reported at 0.7 percent per annum, wasestimated at 3.0 percent in the previous World Bank economic report. Majoreconomic aggregates such as foodcrop production, cross-border exports and re-exports, balance of payments estimates, and Treasury accounts are inadequatelyquantified or out-of-date. The estimates prepared for this report arebelieved, however, to accurately represent the broad economic trends in Benin,but the margin of error may be large. Sectoral performance and issues areaddressed in greater detail in Chapter III and overall development issues inChapter V.

A. SOURCES OF GROWTH

2.4 Benin enjoyed a relatively strong growth in GDP over the 1976-1981period (see Table 2.1). Real growth of 3.6 percent per year was achieved,compared with only 0.7 percent annually during 1972-1976. Benin's growth ratein the late 1970s also compares favorably with the record of low-incomeAfrican nations as a group, which recorded average GDP growth of 1.7 percentover the 1970-1979 period. Still, Benin's GDP per capita--estimated at $270in 1981--places it close to the average of Africa's low-income countries.

2.5 Benin's large investment program and buoyant Nigerian demand were themain sources of growth during the late 1970s. Construction activities,dominated by major capital development projects, forged ahead with a 12percent growth rate during 1976-1981. Public services added employment andoutlay, resulting in an 8 percent growth rate. Commercial activities grew atabove 3 percent, with a particularly strong performance in 1981, as oil incomerose in Nigeria and uranium boosted Niger's purchases. In contrast, theprimary sector, constituting nearly half of the economy, maintained alackluster performance with average growth below one percent. Poor cash cropperformance reflected inadequate producer prices, input supply problems, andlack of extension advice. However, it is generally believed that foodcropproduction expanded more rapidly than indicated by the available statistics inTable 2.1. Total manufacturing output was the same in 1981 as it had been adecade earlier.

Table 2.1 Sources of Growth by Sector

Annual Growth Rate,% GDP Structure, %(1978 prices) (current prices)

1972-76 1976-81 1972 1981

Primary Sectgr 0.8 0.7 46.8 43.7Agriculture.- 0.9 0.9 34.1 33.2

Foodcrops 1.7 1.4 29.3 31.0Industrial Crops -3.1 -4.1 4.8 2.1

Livestock 5.6 1.3 6.8 7.2Forestry, Fisheries, Mining -6.6 -4.7 5.9 3.3

Secondary Sector -1.1 6.8 12.0 12.8Manufacturing -4.7 3.2 8.8 6.3Construction 6.2 12.2 3.2 5.8Public Utilities 3.7 3.6 0.5 0.7

Services 1.8 4.7 41.2 43.5Commerce 6.4 3.4 18.9 21.8Transport 6.9 3.6 5.8 6.8Public services -6.0 8.1 11.9 11.3Other 9.7 6.7 4.6 3.6

GDP, factor cost 0.9 3.3 100.0 100.0

GDP, market price 0.7 3.6 111.6 113.2

I/ Details by crop are provided in Table 2.2

Source: Statistical Appendix, Tables 2.1 and 2.4.

12

2.6 Trends, issues and prospects in the major sectors are discussed inChapter III. In the following section, a brief summary of production trendsin key sectors is presented.

Agriculture

2.7 Foodcrops dominate the sector, especially maize, sorghum, yams,cassava and beans. Maize is the main crop in the densely populated south,while yams and coarse grains are grown in the sparsely settled north.Marketing of these crops is carried out on the free market. Governmentsupport is limited to extension activities provided by the provincial ruraldevelopment agencies (CARDERs). The main industrial crops are cotton, oilpalm products, and groundnuts. The growing, marketing and processing of thesecrops are largely Government-controlled. Further discussion of agriculturalinstitutions and issues is presented in paras. 1.21 - 1.62 and in Volume II ofthis report.

2.8 Maize and yam production rose sharply in the late 1970s (see Table2.2). These widely-traded commodities encountered strong demand in domesticand neighboring markets, and farmers substituted from less attractivetraditional crops such as cassava, sorghum and millet. The mission was toldthat previous Government-imposed constraints on the export of fooderops toNigeria were removed in recent years, thus stimulating production. Highermaize output was partly due to introduction of new hybrid seeds. Averageyields have declined, however, for most crops over the past decade, indicatinga more extensive agriculture and a general decline in labor productivity.Shortages in modern inputs, a degradation in improved seed, and a shortage ofgood land in the south have been contributing factors. Output has beeninsufficient to meet the demand for food in the urban centers, afteraccounting for exports of about 20 percent, and cereal imports have thereforeincreased substantially--from 34,000 tons in 1976 to 110,000 tons in 1981.Subsidies on imported rice, maize, and previously wheat have also played anegative role in the urban food supply balance.

2.9 Industrial crop production--including cotton, oil palm products, andgroundnuts--has been declining steadily since the mid-1970s. Overallproduction levels now stand at about 85 percent of their decade-earlierquantities. Most of this decline has occurred since 1980, and represents ashift of resources into fooderop production and away from industrial crops.Insufficiently attractive official prices for cash crops and problems withinput supply are partly responsible for this development, since cotton andgroundnuts appear well-suited climatically to Benin's conditions. Recent IDAand IFAD-financed rural development projects which help to relieveinstitutional and financial constraints are expected to raise cottonproduction in the Zou and Borgou Provinces. The Government has also recentlytaken bold policy decisions to raise cotton producer prices and to eliminateinput subsidies. However, the low productivity and lack of competitiveadvantage evidenced in the oil palm sector is due mainly to climatic factorsthat cannot feasibly be changed. Better plantation maintenance andorganization of production could raise output, but in general oil palmproduction is likely to play a decreasing role in Benin's agriculture.

13

Table 2.2 Production Trends in Agriculture

Average Annual Growth Average AnnualRate of Production, %/year Production, tons

1969-71 to 1974-76 1974-76 to 1979-81 1979-81

FoodcropsMaize 2.1 6.2 302,000Sorghum 5.8 -3.1 59,000Yams -1.4 7.0 687,000Cassava -3.9 1.2 639,000Beans -8.1 11.1 31,100Rice 25.3 -5.2 10,200

Industrial CropsOil Palm n.a. -7.4 356,000Cotton -6.7 -5.8 18,700Groundnuts -0.3 5.6 60,150

Source: Volume II, Tables 9 and 12.

Manufacturing

2.10 Value-added in manufacturing has fluctuated from year to year, butoverall was no higher in real terms in 1981 than a decade earlier. This is adisappointing performance for a sector which is believed to hold potential forgrowth. Much of the problem was linked to the introduction of publicenterprises as the dominant organizational form in the sector. In 1982, theGovernment adopted new policies aimed at establishing economic price levels,greater management incentives, and tougher performance criteria which shouldlead to a better performance in manufacturing.

2.11 Manufacturing contributes about 6 percent of GDP, and was broughtlargely under Government control during the late-1970s as public enterpriseswere created to manage new and existing operations. Unprofitable operationsof several major enterprises have limited the sector's value-added.Manufacturing activities consist of agricultural processing, food andbeverages, textiles, cement, and assorted artisanal mechanical enterprises.

2.12 Agricultural processing has been affected by declining quantities ofraw material inputs, due to climatic problems in the case of oil palm andorganizational problems in the case of cotton. A maize mill built in 1978 inBohicon has remained idle due to difficulties in purchasing local maize atattractive prices, production problems, and market demand difficulties.Production of soap, however, based on local vegetable oils, has been quitesuccessful and capacity expansion is planned. Food and beverage output,dominated by the brewery (La Beninoise), has increased somewhat in response tostrong demand, but technical problems have held back production despitesubstantial additions to capacity.

1 4

2.13 The textile sector includes one successful and one unsuccessfulpublic enterprise. SOBETEX, printing imported cotton fabric for the local andneighboring markets, expanded production steadily until mid-1982, whenNigerian austerity measures cut demand. The firm has normally generated aconsiderable surplus. IBETEX was conceived as an integrated cotton spinning,weaving and garment-making operation aimed at the European market and usinglocal cotton. Technical, cotton quality and marketing difficulties havesharply reduced IBETEX production. The company has incurred heavy losses andis presently being reorganized. Alternative markets and products need to beexplored, in cooperation with foreign investors.

2.14 Cement output has increased in recent years, as demand rose linked tothe construction of several large projects. A second clinker grinding plantwas installed in 1978, doubling Benin's grinding capacity. Total output ofcement rose to about 270,000 tons in 1981.

2.15 Three major public investment projects have dominated the economybeginning during the late 1970s:

a. Production of cement from the limestone deposits at Onigbolocommenced in mid-1982; the plant has a capacity of 500,000 tons. Sixtypercent of the cement is destined for the Nigerian market. The Government ofNigeria is a 40 percent owner of the project and a co-guarantor of the foreignloans involved. As of early 1983, cement production had halted, because ofOnigbolo's inability to sell cement at competitive prices in Nigeria and thehigh level of unsold stocks.

b. Sugar production from irrigated canefields at Save was scheduledto begin in April 1983, with factory capacity of 47,000 tons. However, lowcane yields (75 tons per hectare) are likely to limit sugar output to 37,000tons. Eighty percent of Save's production is planned to be sold in Nigeria,but market access and pricing issues have not yet been resolved. TheGovernment of Nigeria holds 46 percent of the equity in Save.

c. Petroleum from the Seme offshore field was produced starting inearly 1983. This is a project of the Government of Benin, utilizing aNorwegian service contractor. Production is expected to reach 8,000 barrelsper day by 1985 or even earlier, and the crude oil will be entirely exported.

These very large projects did not come onstream during the periodunder review, but raise issues for the future which are discussed in ChaptersIV and V.

Construction

2.16 The construction sector has performed strongly during the 1970s,doubling its share of GDP over the ten years to 1981. This performancereflects the major public investment in infrastructure and industry duringthis period. An expansion of the Cotonou port capacity was completed in 1982,and substantial highway and rural road construction has been carried outduring recent years. Construction of the sugar, cement and petroleum projectshas also absorbed considerable labor and contributed to sectoral value-added.

15

Commerce

2.17 Commerce has traditionally been one of Benin's economic strengths,and growth in this sector matched overall GDP growth during 1976-1981. Thecommercial sector is engaged in cross-border trading activities based onexports of Benin's consumer goods (textiles and beverages) and re-exports ofimported consumer goods. Commerce also includes the marketing of foodcrops inurban centers of Benin and to neighboring countries. Activity thereforefluctuates from year to year, and the year 1981 was particularly strong forcommerce. Business volume dropped in the second half of 1982 due to slumpingNigerian demand, but commercial activity was recovering somewhat in early1983.

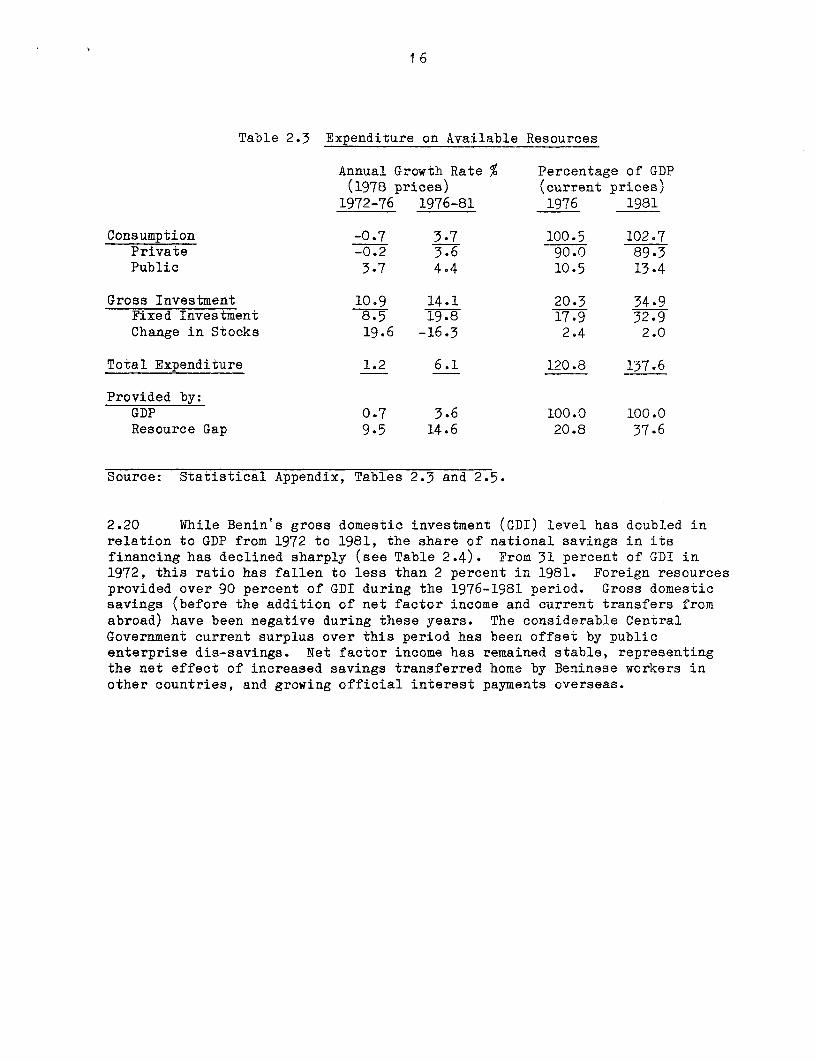

Public Services

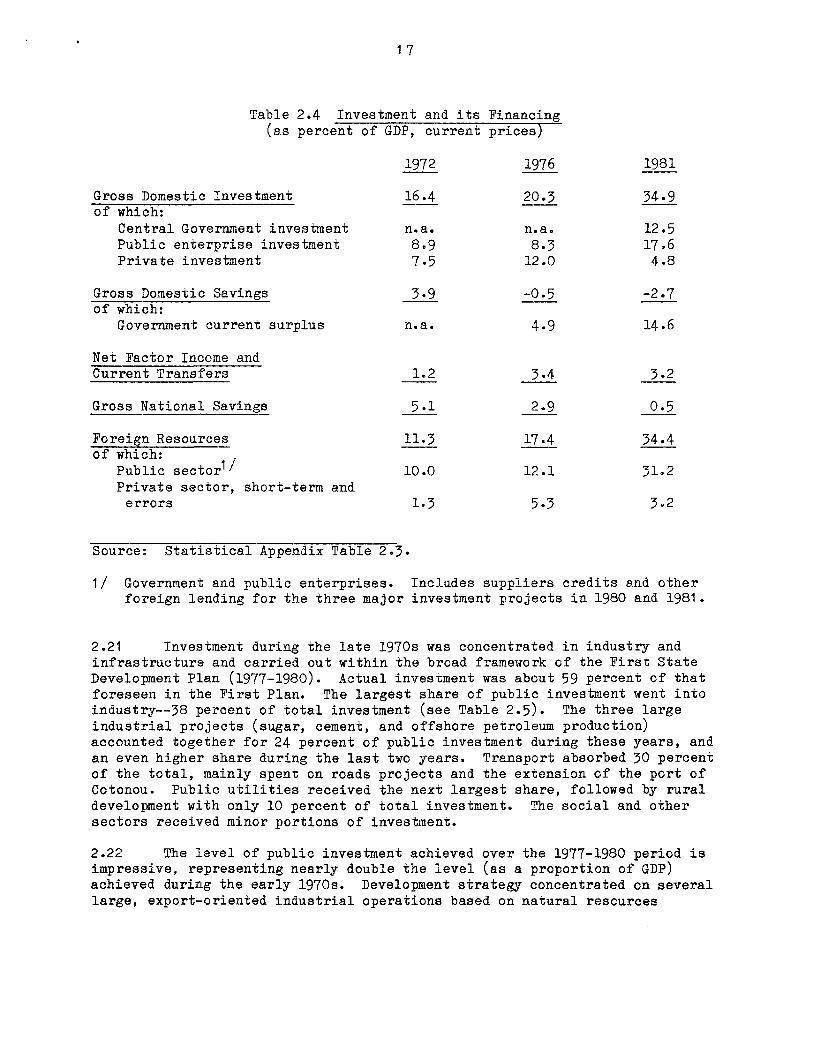

2.18 Rapid growth in civil service employment--15 percent per annum duringthe 1977-1980 period--has increased the sector's contribution to GDP in recentyears. This reverses a long period of low growth in public service activitiessince 1970. Employment in public enterprises--whose contribution is includedunder the industrial sector appropriate to each enterprise--also rose rapidlyduring the late 1970s. However, the automatic employment of college graduatesin the public sector has now been curtailed.

B. EXPENDITURE ON AVAILABLE RESOURCES

2.19 GDP growth and a sharply rising resource gap have expanded totalresources available to the economy at a high 6 percent annual growth rate(1976-1981). These resources have permitted gross domestic investment to riseto unprecedented levels in Benin, while consumption grew at 3.7 percentannually (see Table 2.3). Available resources have grown from 112 percent ofGDP in 1972 to 138 percent in 1981. Foreign resources are clearly tied to theambitious public investment program: fixed investment rose at a 20 percentreal annual rate during the 1976-1981 period, reaching the extremely highlevel of 33 percent of GDP in 1981. This is a substantial investment levelcompared to the overall average for low-income African nations: grossdomestic investment of 15 percent of GDP (in 1979) compared to Benin's 35percent rate (in 1981). Private consumption fared relatively well, recordinga per-capita real increase of nearly one percent per annum during 1976-1981,after a steep per-capita decline in the first half of the 1970s.

16

Table 2.3 Expenditure on Available Resources

Annual Growth Rate % Percentage of GDP(1978 prices) (current prices)

1972-76 1976-81 1976 1981

Consumption -0.7 3.7 100.5 102.7Private -0.2 3.6 90.0 89.3Public 3.7 4.4 10.5 13.4

Gross Investment 10.9 14.1 20.3 34.9Fixed Investment 8.5 19.8 17.9 32.9Change in Stocks 19.6 -16.3 2.4 2.0

Total Expenditure 1.2 6.1 120.8 137.6

Provided by:GDP 0.7 3.6 100.0 100.0Resource Gap 9.5 14.6 20.8 37.6

Source: Statistical Appendix, Tables 2.3 and 2.5.

2.20 While Benin's gross domestic investment (GDI) level has doubled inrelation to GDP from 1972 to 1981, the share of national savings in itsfinancing has declined sharply (see Table 2.4). From 31 percent of GDI in1972, this ratio has fallen to less than 2 percent in 1981. Foreign resourcesprovided over 90 percent of GDI during the 1976-1981 period. Gross domesticsavings (before the addition of net factor income and current transfers fromabroad) have been negative during these years. The considerable CentralGovernment current surplus over this period has been offset by publicenterprise dis-savings. Net factor income has remained stable, representingthe net effect of increased savings transferred home by Beninese workers inother countries, and growing official interest payments overseas.

17

Table 2.4 Investment and its Financing(as percent of GDP, current prices)

1972 1976 1981

Gross Domestic Investment 16.4 20.3 34.9of which:

Central Government investment n.a. n.a. 12.5Public enterprise investment 8.9 8.3 17.6Private investment 7.5 12.0 4.8

Gross Domestic Savings 3.9 -0.5 -2.7of which:

Government current surplus n.a. 4.9 14.6

Net Factor Income andCurrent Transfers 1.2 3.4 3.2

Gross National Savings 5.1 2.9 0.5

Foreign Resources 11.3 17.4 34.4of which:

Public sectorl! 10.0 12.1 31.2Private sector, short-term anderrors 1.3 5.3 3.2

Source: Statistical Appendix Table 2.3.

1/ Government and public enterprises. Includes suppliers credits and otherforeign lending for the three major investment projects in 1980 and 1981.

2.21 Investment during the late 1970s was concentrated in industry andinfrastructure and carried out within the broad framework of the First StateDevelopment Plan (1977-1980). Actual investment was about 59 percent of thatforeseen in the First Plan. The largest share of public investment went intoindustry--38 percent of total investment (see Table 2.5). The three largeindustrial projects (sugar, cement, and offshore petroleum production)accounted together for 24 percent of public investment during these years, andan even higher share during the last two years. Transport absorbed 30 percentof the total, mainly spent on roads projects and the extension of the port ofCotonou. Public utilities received the next largest share, followed by ruraldevelopment with only 10 percent of total investment. The social and othersectors received minor portions of investment.

2.22 The level of public investment achieved over the 1977-1980 period isimpressive, representing nearly double the level (as a proportion of GDP)achieved during the early 1970s. Development strategy concentrated on severallarge, export-oriented industrial operations based on natural resources

18

previously not exploited in Benin. Serious attention was also devoted to thecountry's transit role, in the form of road and port improvements. The smallshare of public investment received by rural development reflects the greatercomplexities faced in this sector, the preoccupation of planners with majorundertakings in other sectors, and the concern of external donors over pooragricultural policies.

Table 2.5 Public Investment by Sector, 1977-1980(in billions of current CFAF)

Sector Amount PercentRural Development 11.7 10.2

Industry, of which: 43.3 37.8Save sugar 12.5 11.0Onigbolo cement 9.7 8.5Seme petroleum 5.0 4.4

Public Utilities 16.7 14.6

Transport, of which: 33.9 29.7Roads 15.4 13.5Port 8.4 7.4

Commerce 1.7 1.5Tourism 3.9 3.5Education 1.8 1.6Health 1.3 1.1

TOTAL 114.3 100.0

Source: Bank Mission Estimates based on Official Data.

C. EMPLOYMENT, WAGES AND MANPOWER TRAINING

2.23 Benin's labor force remains largely agricultural. Employment in themodern sector of the economy has risen rapidly, however, absorbing part of therural-urban migration. Wages, on the other hand, have remained at lowlevels. There is no available data on income distribution in Benin, and therehave been no recent household surveys. In the past, there have beenindications that the rural-urban terms of trade did not strongly favor theurban areas, but continued migration to the large cities indicates a likelydivergence between urban and rural living standards.

1 9

Employment

2.24 The traditional agricultural sector continues to employ the greatestportion of the labor force, about 74 percent in 1980 according to Governmentestimates (see Table 2.6). Services occupy 20 percent of the workforce andindustry the remaining 6 percent, with informal activities outweighing formalemployment in both categories. Benin's informal sector is considered to bequite dynamic, and women play an important role, but little information isavailable. The formal sector employs only about 4 percent of the labor force,but employment in services grew by 15 percent per year, and by 10 percent inindustry. The public sector expanded at a more rapid rate than privateemployment in the services sector: 16 percent per year (civil service pluspublic enterprises) versus 10 percent annually for private serviceenterprises.

Table 2.6 Employment(1980, except as noted)

Thousand Informal Formal Formal SectorPersons Percent as % of as % of Annual Growth RateTotal of Total Total Total 1977-1980

Agriculture 1,220 73.6 99.6 0.4 23.7Industry 100 6.1 85.5 14.5 9.6Services 338 20.3 85.1 14.9 15.4

Total 1,659 100.0 95.8 4.2 14.6

Source: Statistical Appendix Tables 1.3 and 1.4

Wages

2.25 Wage rates have risen only slightly in nominal terms in Benin duringrecent years, and have fallen in real terms. The minimum industrial wage rateis one indicator of this trend: from 1975 to 1982, this rate declined by atotal of 43 percent in real terms. Civil service salary levels have also beenstrictly controlled, and have probably declined by a similar proportion. Thevery low wage levels in the public sector have posed a problem in retainingand motivating qualified staff, who have often been attracted by highersalaries in the parapublic and private sectors. The solution however, may beto reward efficiency rather than to raise salaries across the board. Althougheffective wage rates are not known in detail, wage levels in Benin haveclearly fallen substantially behind those of other West African nations. Forinstance, in 1970, Benin's minimum industrial wage was 22 percent less thanSenegal's, while it is now 66 percent below the Senegalese level.

20

Table 2.7 Wage Levels(minimum hourly industrial wage rate, CFAF)

1970 1975 1980 1982

Benin 39.60 45.00 51.75 51-75Ivory Coast n.a. 92.00 174.00 191.00Senegal 50.60 107.05 133.81 152.04

Source: BCEAO

Manpower and Skill Training

2.26 The future requirements for skilled workers, technicians, andprofessionals in the industrial and agricultural sectors have not beenprecisely defined. Nonetheless, it is clear that the present training systemis not well-oriented to support the development of skilled manpower for keysectors of the economy. First, the planning and administration of training isweak and employees are not sufficiently involved in formulating trainingprograms. Second, the quality of existing pre-service training programs isvery low. There is a shortage of trained teachers, a lack of essentialmaterials and equipment, and overemphasis at the lower and middle-levels ongeneral education without enough specialized training. Finally, the numbersof people trained in key fields does not correspond well to the needs. Theoutput of competent skilled workers and technicians for industry is notsufficient, for example, but there is a surfeit of graduates in the commercialfields.

D. MONEY, CREDIT AND PRICES

2.27 Benin's monetary policy is set within the context of the six-nationWest African Monetary Union (UMOA) and its common central bank, the BCEAO.The UMOA has the advantage of a convertible currency, the CFA franc, which islinked to the French franc. Policy objectives for Benin, as a member of UMOA,have been the achievement of a sustainable balance of payments and an adequatelevel of domestic economic activity.

2.28 A relatively expansionary credit policy was pursued in 1982 (Table2.8). This reflected increased demand for credit by the public enterprises tofinance losses, and by the private commercial sector due to the involuntarybuildup of stocks resulting from the slowdown in the re-export trade. Thiscredit expansion also reflected a shift in the Central Government's positiontoward the banking system. During 1981, the Government built up its depositswith domestic banks and nonbanking institutions as a result of its high fiscalsurplus. In 1982, the Government drew down its deposits with the banks bysome CFAF 9 billion, and further drawdowns are expected in 1983.

2.29 Benin's net foreign asset position also reflects the strongGovernment surplus in 1981 and subsequent weakening. Net foreign assets ofpositive CFAF 13 billion at end-1981 had declined to a negative CFAF 5 billion

221

position at end-1982, and are expected to decline futher to negative CFAF 24billion by the end of 1983.

2.30 Price inflation in Benin has been relatively moderate in recentyears, although there is no adequate price index available. The mission'sestimates of the implicit GDP deflator provide inflation levels of about 10 to12 percent annually during the 1978-1981 period. The high-income consumerprice index, prepared by one of the diplomatic missions in Cotonou, indicatessimilar levels. The devaluation of the French franc (to which the CFA francis pegged at a level of 50 to 1) in 1981, 1982 and 1983 has been reflected inthe CFAF-dollar exchange rate, which has climbed to the 400 level from arelatively stable range of 200-250 during the 1970s. This exchange rate shiftis likely to have an inflationary impact on urban consumers in Benin, althougha considerable portion of import trade is from France. In principle, thedepreciation of the CFA franc should stimulate certain exports such as cotton,whose world market price is denominated in U.S. dollars. The Governmentshould be able to substantially raise the CFAF producer price for cotton andother export crops.

22

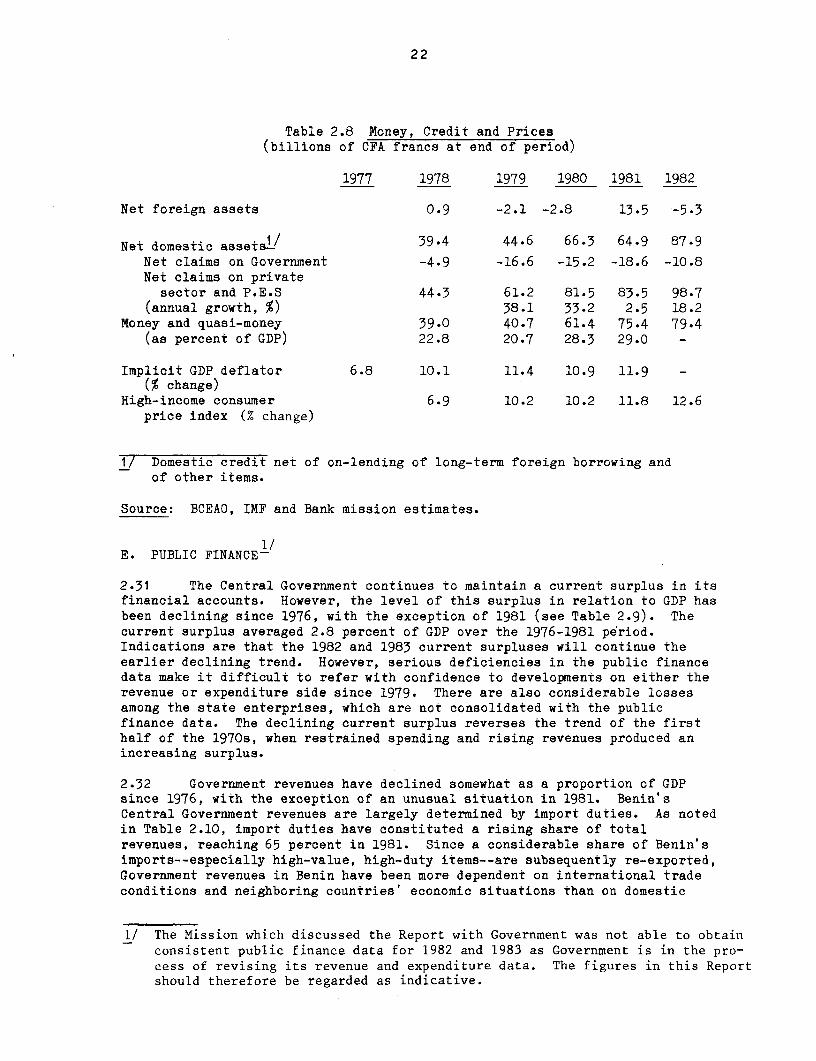

Table 2.8 Money, Credit and Prices(billions of CFA francs at end of period)

1977 1978 1979 1980 1981 1982

Net foreign assets 0.9 -2.1 -2.8 13.5 -5.3

Net domestic assets-/ 39-4 44.6 66.3 64.9 87.9Net claims on Government -4.9 -16.6 -15.2 -18.6 -10.8Net claims on private

sector and P.E.S 44.3 61.2 81.5 83.5 98.7(annual growth, %) 38.1 33.2 2.5 18.2

Money and quasi-money 39.0 40.7 61.4 75.4 79.4(as percent of GDP) 22.8 20.7 28.3 29.0 -

Implicit GDP deflator 6.8 10.1 11.4 10.9 11.9 -(% change)

High-income consumer 6.9 10.2 10.2 11.8 12.6price index (% change)

1/ Domestic credit net of on-lending of long-term foreign borrowing andof other items.

Source: BCEAO, IMF and Bank mission estimates.

I/E. PUBLIC FINANCE-

2.31 The Central Government continues to maintain a current surplus in itsfinancial accounts. However, the level of this surplus in relation to GDP hasbeen declining since 1976, with the exception of 1981 (see Table 2.9). Thecurrent surplus averaged 2.8 percent of GDP over the 1976-1981 period.Indications are that the 1982 and 1983 current surpluses will continue theearlier declining trend. However, serious deficiencies in the public financedata make it difficult to refer with confidence to developments on either therevenue or expenditure side since 1979. There are also considerable lossesamong the state enterprises, which are not consolidated with the publicfinance data. The declining current surplus reverses the trend of the firsthalf of the 1970s, when restrained spending and rising revenues produced anincreasing surplus.

2.32 Government revenues have declined somewhat as a proportion of GDPsince 1976, with the exception of an unusual situation in 1981. Benin'sCentral Government revenues are largely determined by import duties. As notedin Table 2.10, import duties have constituted a rising share of totalrevenues, reaching 65 percent in 1981. Since a considerable share of Benin'simports--especially high-value, high-duty items--are subsequently re-exported,Government revenues in Benin have been more dependent on international tradeconditions and neighboring countries' economic situations than on domestic

1/ The Mission which discussed the Report with Government was not able to obtainconsistent public finance data for 1982 and 1983 as Government is in the pro-cess of revising its revenue and expenditure data. The figures in this Reportshould therefore be regarded as indicative.

23

production. For instance, sharply higher revenues in 1981 were largely due toduties on imported goods and to taxes on Beninese manufactures, both destinedto Nigeria, in addition to taxes on income generated in the construction ofmajor projects in Benin.

Table 2.9 Central Government Finance Simmary(consolidated position)'

Average1976 1979 1980 1981 1976 1981 1976-81

Tbillions of CFAF) 7is percent of GDP)

Current Revenues 22.8 28.5 33.4 52.6 16.7 20.2 16.4Import duties 11.0 16.9 21.0 30.0 8.0 11.5 9.1Income taxes 4.2 3.5 3.4 6.8 3.1 2.6 2.4Other revenues 7.6 8.1 9.0 15.8 5.6 6.1 4.9

Current Expenditures 14.3 20.1 27.8 34.8 10.5 13.4 11.2Wages and salaries2/ 9.6 14.4 16.3 21.0 7.0 8.1 7.1

Net Lending and Transfers 3.6 5.1 4.4 3.2 2.6 1.2 2.4

Current Surplus 4.9 3.3 1.2 14.6 3.6 5.6 2.8

Investment Expenditure 2.0 7.0 16.2 25.1 1.5 9.7 4.7

Overall Balance 1.6 -3.7 -15.0 -10.5 1.2 -4.1 -1.9

Source: Statistical Appendix Tables 5.1 and 5.9.

1/ Includes Treasury, FNI, CAA and special accounts; excludes public enterprises.2/ Treasury only

2.33 Current expenditures rose to 13 percent of GDP in 1981 following avery steady proportion of 10 percent of GDP during the years 1976-1979. Innominal terms, current expenditures increased by 19 percent per year from 1976to 1981, while inflation (implicit GDP deflator) was about 10 to 15 percentannually. This spending increase is primarily attributable to higherbudgetary expenditures in 1980 and 1981 for education (expenditures have risenfrom the equivalent of 2.9% of GDP in 1978 to 4.1% in 1981) and for generalpublic services. Rapid increases were also recorded in Special Accounttransactions (pension fund payments) and in CAA expenditures (representingconsiderably higher interest payments on foreign debt). These increasesresult from economic and social priorities which are likely to continue in thefuture.

24

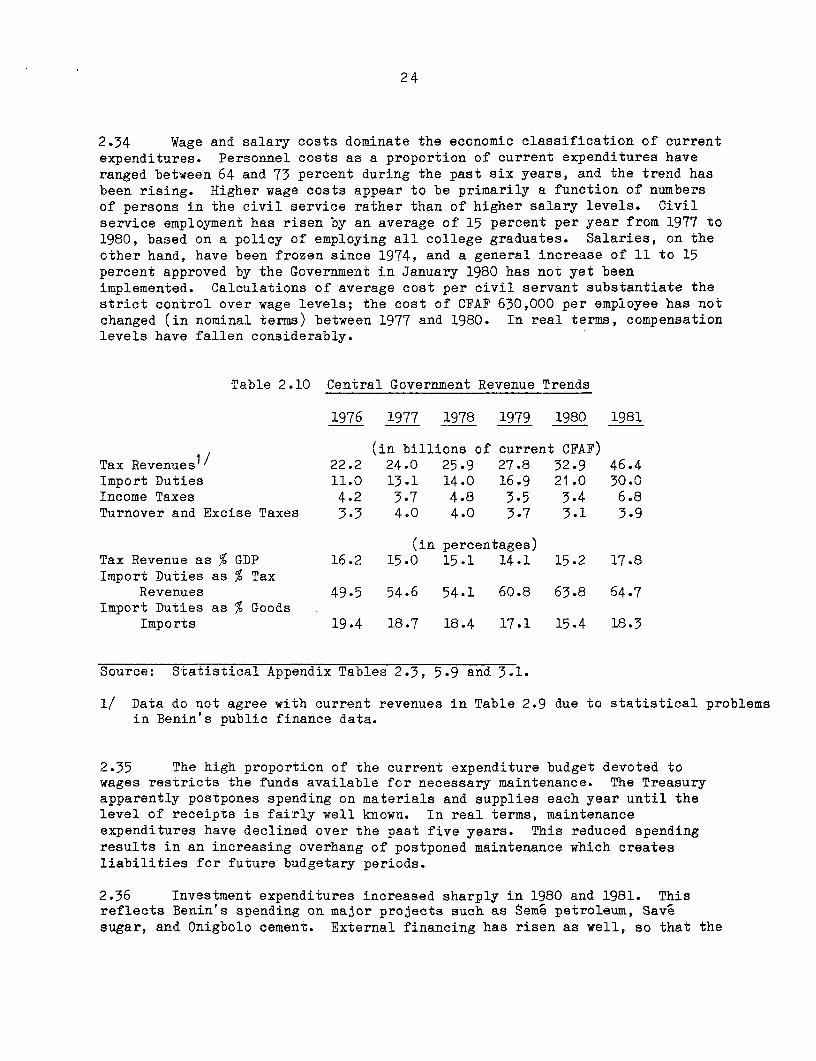

2.34 Wage and salary costs dominate the economic classification of currentexpenditures. Personnel costs as a proportion of current expenditures haveranged between 64 and 73 percent during the past six years, and the trend hasbeen rising. Higher wage costs appear to be primarily a function of numbersof persons in the civil service rather than of higher salary levels. Civilservice employment has risen by an average of 15 percent per year from 1977 to1980, based on a policy of employing all college graduates. Salaries, on theother hand, have been frozen since 1974, and a general increase of 11 to 15percent approved by the Government in January 1980 has not yet beenimplemented. Calculations of average cost per civil servant substantiate thestrict control over wage levels; the cost of CFAF 630,000 per employee has notchanged (in nominal terms) between 1977 and 1980. In real terms, compensationlevels have fallen considerably.

Table 2.10 Central Government Revenue Trends

1976 1977 1978 1979 1980 1981

(in billions of current CFAF)Tax Revenues! 22.2 24.0 25.9 27.8 32.9 46.4Import Duties 11.0 13.1 14.0 16.9 21.0 30.0Income Taxes 4.2 3.7 4.8 3.5 3.4 6.8Turnover and Excise Taxes 3.3 4.0 4.0 3.7 3.1 3.9

(in percentages)Tax Revenue as % GDP 16.2 15.0 15.1 14.1 15.2 17.8Import Duties as % Tax

Revenues 49.5 54.6 54.1 60.8 63.8 64.7Import Duties as % Goods

Imports 19.4 18.7 18.4 17.1 15.4 18.3

Source: Statistical Appendix Tables 2.3, 5.9 and 3.1.

1/ Data do not agree with current revenues in Table 2.9 due to statistical problemsin Benin's public finance data.

2.35 The high proportion of the current expenditure budget devoted towages restricts the funds available for necessary maintenance. The Treasuryapparently postpones spending on materials and supplies each year until thelevel of receipts is fairly well known. In real terms, maintenanceexpenditures have declined over the past five years. This reduced spendingresults in an increasing overhang of postponed maintenance which createsliabilities for future budgetary periods.

2.36 Investment expenditures increased sharply in 1980 and 1981. Thisreflects Benin's spending on major projects such as Seme petroleum, Savesugar, and Onigbolo cement. External financing has risen as well, so that the

2 5

proportion of investment expenditures financed by foreign borrowing hasincreased somewhat. Nevertheless, rising investment has imposed a heavyburden of counterpart financing. Net of increased foreign borrowing, thehigher investment expenditures in 1981 required CFAF 7 billion more in publiccounterpart funds than in 1979.

F. PUBLIC ENTERPRISES

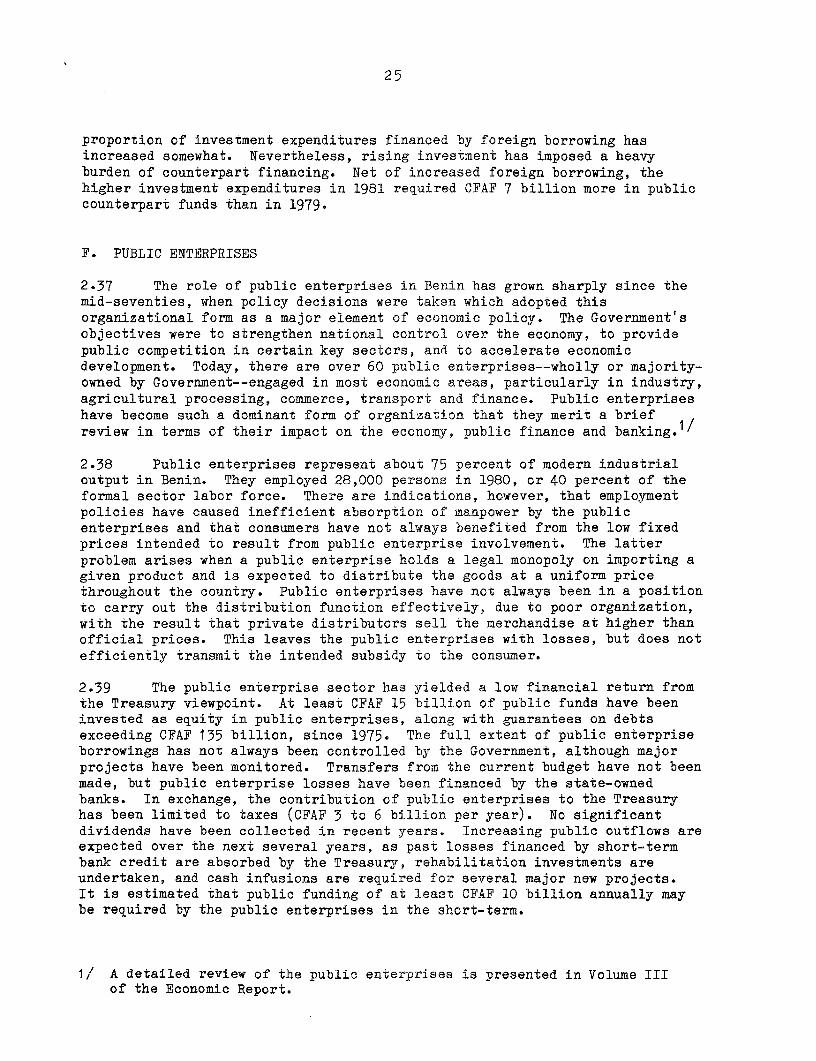

2.37 The role of public enterprises in Benin has grown sharply since themid-seventies, when policy decisions were taken which adopted thisorganizational form as a major element of economic policy. The Government'sobjectives were to strengthen national control over the economy, to providepublic competition in certain key sectors, and to accelerate economicdevelopment. Today, there are over 60 public enterprises--wholly or majority-owned by Government--engaged in most economic areas, particularly in industry,agricultural processing, commerce, transport and finance. Public enterpriseshave become such a dominant form of organization that they merit a briefreview in terms of their impact on the economy, public finance and banking.

2.38 Public enterprises represent about 75 percent of modern industrialoutput in Benin. They employed 28,000 persons in 1980, or 40 percent of theformal sector labor force. There are indications, however, that employmentpolicies have caused inefficient absorption of manpower by the publicenterprises and that consumers have not always benefited from the low fixedprices intended to result from public enterprise involvement. The latterproblem arises when a public enterprise holds a legal monopoly on importing agiven product and is expected to distribute the goods at a uniform pricethroughout the country. Public enterprises have not always been in a positionto carry out the distribution function effectively, due to poor organization,with the result that private distributors sell the merchandise at higher thanofficial prices. This leaves the public enterprises with losses, but does notefficiently transmit the intended subsidy to the consumer.

2.39 The public enterprise sector has yielded a low financial return fromthe Treasury viewpoint. At least CFAF 15 billion of public funds have beeninvested as equity in public enterprises, along with guarantees on debtsexceeding CFAF 135 billion, since 1975. The full extent of public enterpriseborrowings has not always been controlled by the Government, although majorprojects have been monitored. Transfers from the current budget have not beenmade, but public enterprise losses have been financed by the state-ownedbanks. In exchange, the contribution of public enterprises to the Treasuryhas been limited to taxes (CFAF 3 to 6 billion per year). No significantdividends have been collected in recent years. Increasing public outflows areexpected over the next several years, as past losses financed by short-termbank credit are absorbed by the Treasury, rehabilitation investments areundertaken, and cash infusions are required for several major new projects.It is estimated that public funding of at least CFAF 10 billion annually maybe required by the public enterprises in the short-term.

1/ A detailed review of the public enterprises is presented in Volume IIIof the Economic Report.

26

2.40 The banks are heavily exposed to the public enterprises, whichaccount for over 60 percent of all domestic borrowings. Arrears pose seriousproblems. Ten public enterprises maintain less-than-satisfactory bankingrelations with the commercial bank, and their total balances outstandingexceed the bank's reserves. Twelve public enterprises are in arrears to thedevelopment bank, on original loan amounts exceeding the bank's reserves.This situation has arisen in part because of the explicit or implicitGovernment guarantees involved. The sizable public finance surplus recordedin 1981 was largely deposited in the banks, and these funds assisted the banksin extending additional credit which helped finance the enterprises'deficits. In coming years, budgetary appropriations will likely be requiredto relieve the banks in the case of certain loans to public enterprises.

G. BALANCE OF PAYMENTS

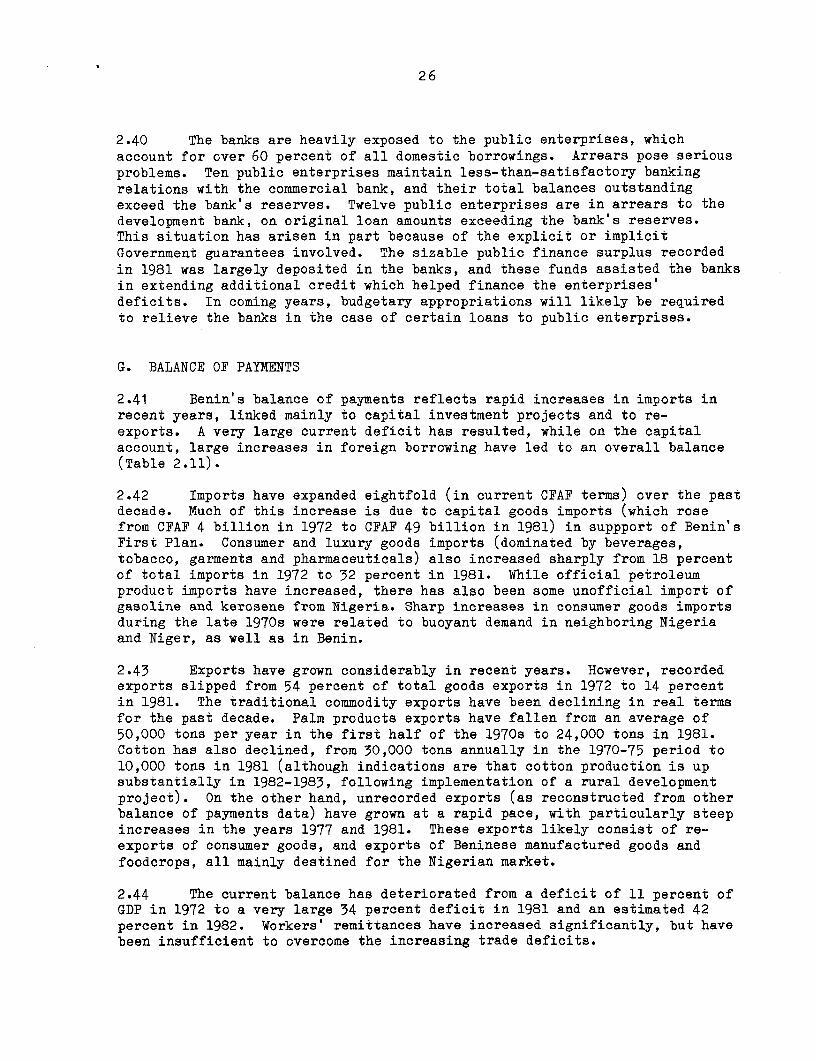

2.41 Benin's balance of payments reflects rapid increases in imports inrecent years, linked mainly to capital investment projects and to re-exports. A very large current deficit has resulted, while on the capitalaccount, large increases in foreign borrowing have led to an overall balance(Table 2.11).

2.42 Imports have expanded eightfold (in current CFAF terms) over the pastdecade. Much of this increase is due to capital goods imports (which rosefrom CFAF 4 billion in 1972 to CFAF 49 billion in 1981) in suppport of Benin'sFirst Plan. Consumer and luxury goods imports (dominated by beverages,tobacco, garments and pharmaceuticals) also increased sharply from 18 percentof total imports in 1972 to 32 percent in 1981. While official petroleumproduct imports have increased, there has also been some unofficial import ofgasoline and kerosene from Nigeria. Sharp increases in consumer goods importsduring the late 1970s were related to buoyant demand in neighboring Nigeriaand Niger, as well as in Benin.

2.43 Exports have grown considerably in recent years. However, recordedexports slipped from 54 percent of total goods exports in 1972 to 14 percentin 1981. The traditional commodity exports have been declining in real termsfor the past decade. Palm products exports have fallen from an average of50,000 tons per year in the first half of the 1970s to 24,000 tons in 1981.Cotton has also declined, from 30,000 tons annually in the 1970-75 period to10,000 tons in 1981 (although indications are that cotton production is upsubstantially in 1982-1983, following implementation of a rural developmentproject). On the other hand, unrecorded exports (as reconstructed from otherbalance of payments data) have grown at a rapid pace, with particularly steepincreases in the years 1977 and 1981. These exports likely consist of re-exports of consumer goods, and exports of Beninese manufactured goods andfoodcrops, all mainly destined for the Nigerian market.

2.44 The current balance has deteriorated from a deficit of 11 percent ofGDP in 1972 to a very large 34 percent deficit in 1981 and an estimated 42percent in 1982. Workers' remittances have increased significantly, but havebeen insufficient to overcome the increasing trade deficits.

27

2.45 Capital inflows have risen sharply, particularly during 1980 and 1981when several major investment projects were financed. Suppliers creditsprovided the bulk of these funds, on reasonable terms (7.5 to 8.0 percentinterest, 12 years maturity). Net borrowing rose from CFAF 11.4 billion in1979 to the CFAF 50 billion level in 1980 and 1981. Official grant aid anddirect foreign investment have also increased, linked to the Government'sinvestment program.

2.46 The overall balance of payments turned positive in 1980 after threeyears of modest deficits. In 1981, a major positive balance was achieved,although the source of this shift is clouded by the existence of a substantialmovement in the "other capital flows and errors" line. Recent developmentssuggest that the 1981 performance was largely based on the strong Nigeriandemand for Beninese goods and re-exports, as net reserves have again been rundown to a small negative position as at end-1982.

Table 2.11 Summary Balance of Payments(billions of current CFAF)

1972 1976 1979 1980 1981

Exportsl/ 21.6 31.5 64.2 68.3 81.2Importsl/ 32.1 60.0 108.3 148.5 178.8

Resource Balance -10.5 -28.5 -44.1 -80.2 -97.6Investment Income -0.7 0.0 -0.2 -0.5 -2.1Remittances and Private

Transfers 1.7 4.7 8.4 9.3 10.3

Current Balance -9.5 -23.8 -35.9 -71.4 -89.4Official Grant Aid 5.7 12.8 13.7 13.3 23.1Direct Investm7nt 1.2 0.6 3.6 8.4 9.2Net Borrowing2 1.5 3.1 11.4 58.7 48.9Other Capital Flows and

Errors3 2.1 8.8 4.5 -8.0 22.9

Overall Balance 1.0 1.3 -2.7 1.0 14.7Net Reserves, year-end 7.2 4.5 -3.3 -2.2 12.5

Source: Statistical Appendix Table 3.1.

1/ Goods and non-factor services.2/ Medium and long-term borrowing and other capital.3/ Net short-term capital, credit from IMF, other flows, and errors.

28

H. EXTERNAL DEBT AND FOREIGN AID

2.47 The massive public investment effort undertaken during the late 1970swas largely financed from abroad. This was reflected in sharply highercapital inflows, which were obtained on harder terms than in the past. Debtservice is rising, though much of the increase is related to major export-oriented projects. Because investment has been almost exclusively in thepublic sector, and because the CFA franc is fully convertible, debt servicingissues are essentially a question of public finance.

2.48 Benin's external debt (outstanding, including undisbursed amounts)increased from $166 million (CFAF 59 billion) at end-1976 to an estimated $589million (CFAF 209 billion) at end-1981 (see Table 2.12). Of the 1981outstanding amount, 43 percent was incurred to finance the sugar, cement, andpetroleum projects. The mix of borrowing changed as well, shifting theoutstanding debt structure from 15 percent on commercial terms in 1976 to 48percent commercial in 1981.

2.49 Debt service has increased from the $2.8 to $4.2 million level (CFAF1.0 to 1.5 billion) during 1976-80 to $17 million (CFAF 5.9 billion) in 1981and $68 million (CFAF 24 billion) projected for 1983 based on existingcommitments. Debt service in 1981 accounted for 7 percent of exports (goodsplus non-factor services), or 11 percent of Central Government revenues. Thethree major industrial projects--two of which are jointly guaranteed by theNigerian Government--account for 79 percent of the debt service due in 1983.

Table 2.12 External Debt

CFAF billions Percentage(current terms)1976 1981 1976 1981

Total Debt Outstanding 59 209 100.0 100.0

Public Creditors 50 109 85.4 52.1Multilateral 24 75 41.1 36.1Bilateral 26 34 44.3 15.9

Commercial Creditors 9 100 14.6 47.9Suppliers Credits 5 5 8.1 2.3Bank loans 4 95 6.5 45.6

Total Debt Service 1.5 5.9as X Exports (G + NFS) - - 4.2 7.3as % Govt. Revenues - - 6.6 11.2

Source: Statistical Appendix Table 4.1.

29

2.50 The present level of Benin's debt service is substantially higherthan in the past, but is linked to a major investment thrust. The country'scapacity to service this debt depends on the success of the major projects,which in turn hinges upon favorable developments in worldwide demand and inNigerian demand (in the case of sugar and cement). If the output can be soldat attractive prices, and if trade levels recover following their 1982 slumpso that Benin's import duties rise, there will not be any difficulty inservicing this debt. However, there are major questions surrounding theviability of these projects, particularly in the case of the sugar project(see para. 3.32). Benin's debt servicing capability is further assessed inChapter IV on the basis of alternative macroeconomic projections.

2.51 Concessionary aid for development in Benin has grown fairly rapidlyin the form of grants during the late 1970s, but official loans have notincreased. This means that some aid agencies may be converting their aid toBenin from loan to grant terms. The sharp increase in bilateral grantsappears to reflect improved political relations with key donor nations. Thevolume of concessionary loans, however, has not increased. This may reflectBenin's emphasis during the late 1970s on major industrial projects in whichforeign aid played little role, and the country's limited absorptive capacityfor other simultaneous new projects.

30

III. SECTOR PERFORMANCE AND ISSUES

3.1 This chapter presents summaries of the major performance trends andissues in the key sectors of Benin's economy. The material is organized asfollows:

A. AgricultureB. IndustryC. TransportD. EnergyE. Social Sectors

A. AGRICULTURE

Background

3.2 Agriculture is the most important sector of the Beninese economy. Itemploys three-fourths of the active population, and provides 40 percent of theGDP and 36 percent of the foreign exchange earnings. The sector ispredominantly fooderop oriented, producing maize, sorghum, yams, cassava,beans, and small quantities of rice. It is estimated that Benin enjoys anoverall food surplus; a significant portion of domestic foodcrop production(perhaps 20 percent) is exported to Nigeria and Niger. This offsets Benin'sfoodgrain imports, which have been rising in recent years, and which have beensubsidized by the Government through public enterprises. Benin enjoys acomparative advantage in foodcrop production which is likely to continue inthe future. The main industrial crops are palm oil, cotton, and peanuts.Efforts are underway to expand cotton output, which is well-suitedenvironmentally to conditions in northern Benin. But the oil palm sector islimited by insufficient rainfall, and will likely continue to decline invalue.

3.3 Farming patterns vary markedly by region. In the southern andcentral region, two rainy seasons permit double cropping. Land is usedintensively, and the average farm size is 1.2 ha. In the northern region withonly one rainy season, the cropping pattern is less intensive and the averagefarm size is 2.4 ha. There is an average of 3.3 farm workers per farm inBenin. Labor is mainly family labor, yet a small number of farmers fromlarger farms hire workers during peak periods, such as harvesting.Cooperatives exist throughout the country; however, individual farmers stillaccount for about 90 percent of all agricultural production in Benin. Yieldsare generally not high, due partly to low use of modern inputs (improvedseeds, fertilizer). Fertilizers are so far little used in Benin, althoughthey have been shown to improve the generally poor soils and raise yields formost crops.

31

Production Trends

3.4 Benin experienced a five-year period of stagnation in staple cropproduction prior to 1976. Production then increased (see Table 3.1) as aresult of better weather and more attractive prices to small farmers.Production of maize and yams has increased sharply during the last five yearslargely in response to increased border trade wtih Western Nigeria. Beans andcassava output has also risen during this time period. Sorghum production hasdeclined in recent years, due largely to a shifting of tastes to maize in thenorth.

Table 3.1 Selected Foodcrop Production(thousand metric tons)

1969-71 1974-76 1979-81

Maize 202 224 302Sorghum 52 69 59Yams 524 489 687Cassava 733 601 639Beans 28 18 31Rice 4 13 10

Source: Ministry of Rural Development