Embed Size (px)

Citation preview

Demir BektićDeka Investment GmbH & IQ-KAP

Northfield's 29th Annual Research Conference

Stowe, March 20th – 22nd, 2017

Extending Fama-French Factors To Corporate Bond Markets

Source: D. Bektic, J.-S. Wenzler, M. Wegener, D. Schiereck and T. Spielmann, 2016, SSRN Working Paper 2715727

Disclosures

‡ This presentation was produced solely by Demir Bektić. The opinions and statements expressed herein arethose of the authors and do not necessarily reflect those of Deka Investment GmbH or its employees.

‡ The information contained herein is only as current as of the date indicated, and may be superseded by

subsequent market events or for other reasons. Charts and graphs provided herein are for illustrative

purposes only. The information in this presentation has been developed internally and/or obtained from

sources believed to be reliable; however, neither Deka Investment nor the speaker guarantees the

accuracy, adequacy or completeness of such information. Nothing contained herein constitutes investment,

legal, tax or other advice nor is it to be relied on in making an investment or other decision.

‡ There can be no assurance that an investment strategy will be successful. Historic market trends are not

reliable indicators of actual future market behavior or future performance of any particular investment

which may differ materially, and should not be relied upon as such. Target allocations contained herein are

subject to change. There is no assurance that the target allocations will be achieved, and actual

allocations may be significantly different than that shown here. This presentation should not be viewed as

a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any

investment strategy.

2

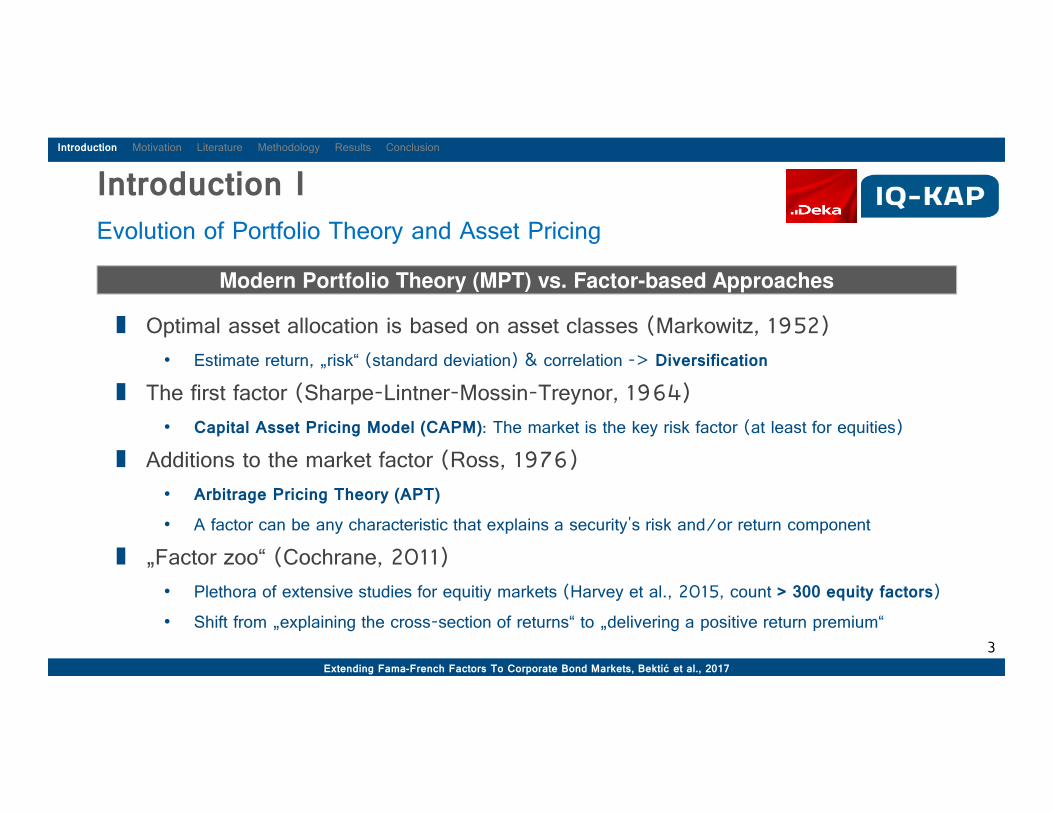

Introduction I

Evolution of Portfolio Theory and Asset Pricing

Modern Portfolio Theory (MPT) vs. Factor-based Approaches

‡ Optimal asset allocation is based on asset classes (Markowitz, 1952)

• Estimate return, „risk“ (standard deviation) & correlation -> Diversification

‡ The first factor (Sharpe-Lintner-Mossin-Treynor, 1964)

• Capital Asset Pricing Model (CAPM): The market is the key risk factor (at least for equities)

‡ Additions to the market factor (Ross, 1976)

• Arbitrage Pricing Theory (APT)

• A factor can be any characteristic that explains a security's risk and/or return component

‡ „Factor zoo“ (Cochrane, 2011)

• Plethora of extensive studies for equitiy markets (Harvey et al., 2015, count > 300 equity factors)

• Shift from „explaining the cross-section of returns“ to „delivering a positive return premium“

Introduction Motivation Literature Methodology Results Conclusion

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

3

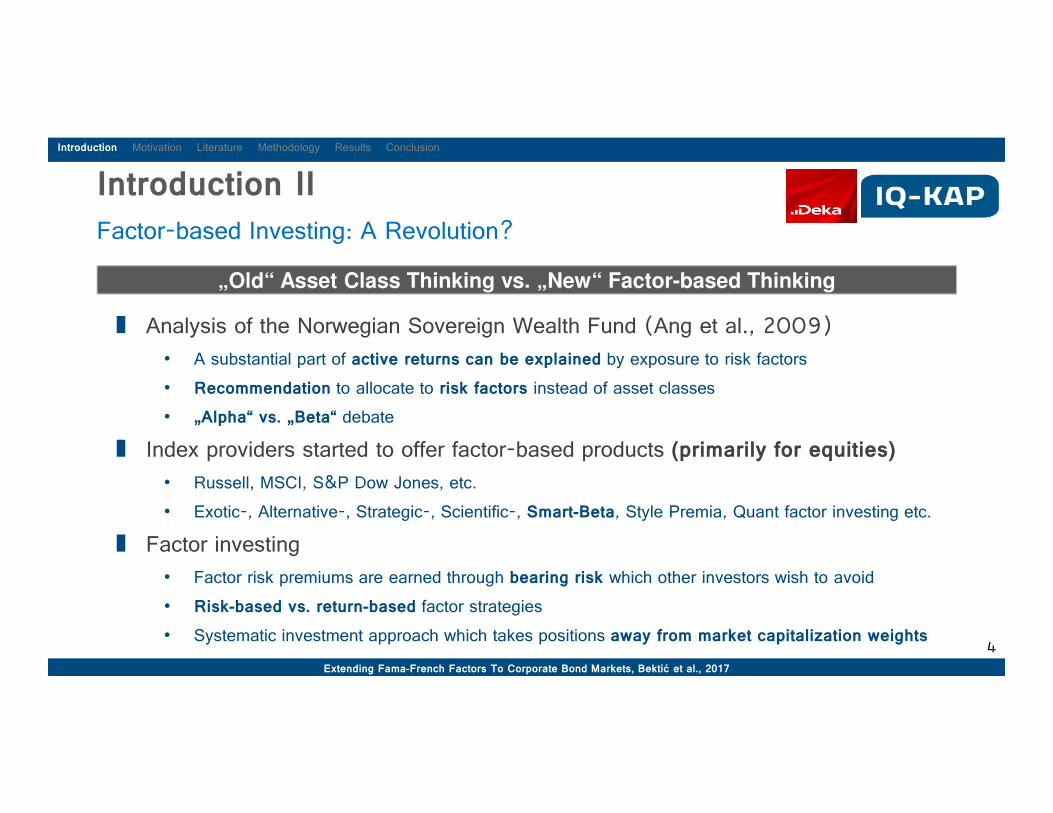

Introduction II

Factor-based Investing: A Revolution?

„Old“ Asset Class Thinking vs. „New“ Factor-based Thinking

‡ Analysis of the Norwegian Sovereign Wealth Fund (Ang et al., 2009)

• A substantial part of active returns can be explained by exposure to risk factors

• Recommendation to allocate to risk factors instead of asset classes

• „Alpha“ vs. „Beta“ debate

‡ Index providers started to offer factor-based products (primarily for equities)

• Russell, MSCI, S&P Dow Jones, etc.

• Exotic-, Alternative-, Strategic-, Scientific-, Smart-Beta, Style Premia, Quant factor investing etc.

‡ Factor investing

• Factor risk premiums are earned through bearing risk which other investors wish to avoid

• Risk-based vs. return-based factor strategies

• Systematic investment approach which takes positions away from market capitalization weights4

Introduction Motivation Literature Methodology Results Conclusion

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Motivation I

Shortcomings of Typical Bond Indices

Equities vs. Bonds I

Introduction Motivation Literature Methodology Results Conclusion

5

‡ Motivation for factor-based solutions comes from shortcomings of bond indices

‡ Greatest deficits are:

� Market-capitalization weighting suboptimal for diversification and unwanted risk-exposures (e.g., PIIGS)

� Lack of investability and replicability

• Benchmarks usually include a large number of bonds

• Many bonds are not sufficiently liquid

‡ Main conditions for the success of factor-based bond products are

� To provide investable solutions

� To offer better diversification

� To offer better risk-exposures

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Motivation II

Market-capitalization Weighting

Equities vs. Bonds II

Introduction Motivation Literature Methodology Results Conclusion

6

‡ Equities: Market-capitalization weighting = Most valuable company has greatest weight

‡ Bonds: Market-capitalization weighting = Largest borrower has greatest weight

‡ Issuers with highest amount outstanding constitute greatest portion of the index

‡ Index funds are forced to buy bonds of these issuers and drive up prices

‡ Therefore, yields of these bonds are declining

� As a result, these issuers can borrow money at even lower rates

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

30%

40%

50%

60%

70%

Index w

eight(ER00)

Euro Financial Euro Non-Financial

Motivation III

What is a „good“ factor?

Risk premium or just data mining?

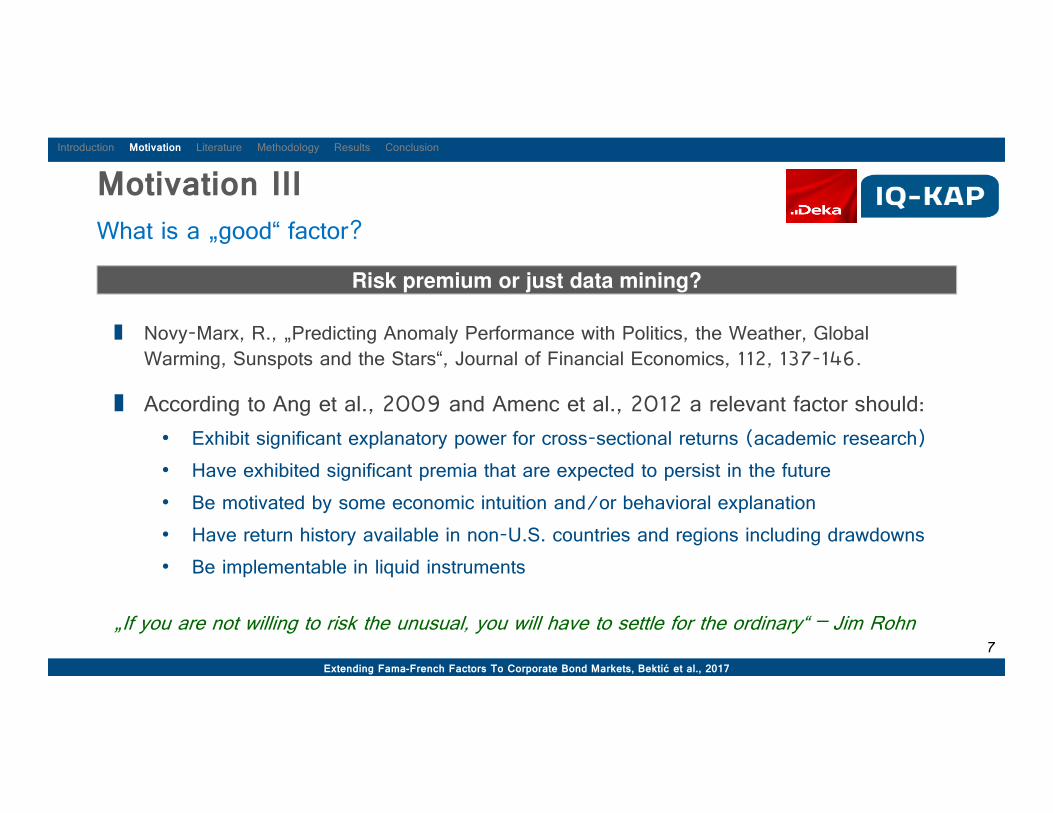

‡ Novy-Marx, R., „Predicting Anomaly Performance with Politics, the Weather, Global

Warming, Sunspots and the Stars“, Journal of Financial Economics, 112, 137-146.

‡ According to Ang et al., 2009 and Amenc et al., 2012 a relevant factor should:

• Exhibit significant explanatory power for cross-sectional returns (academic research)

• Have exhibited significant premia that are expected to persist in the future

• Be motivated by some economic intuition and/or behavioral explanation

• Have return history available in non-U.S. countries and regions including drawdowns

• Be implementable in liquid instruments

„If you are not willing to risk the unusual, you will have to settle for the ordinary“ – Jim Rohn7

Introduction Motivation Literature Methodology Results Conclusion

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Related Literature I

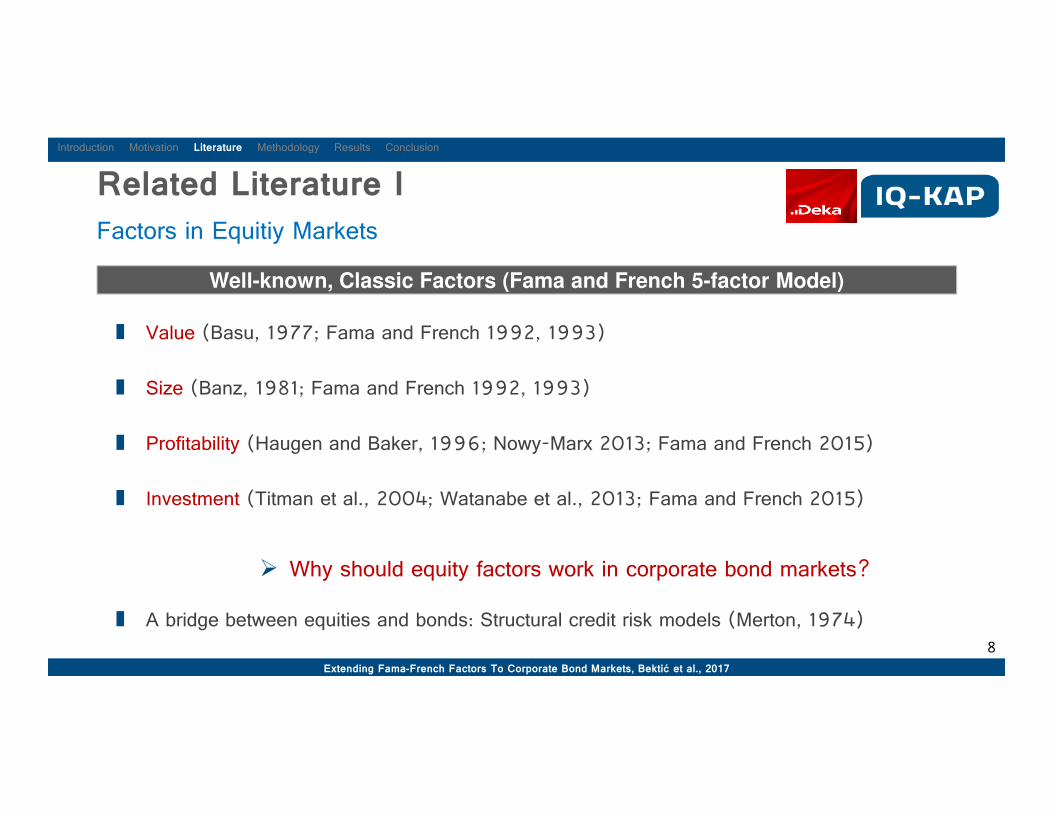

Factors in Equitiy Markets

Well-known, Classic Factors (Fama and French 5-factor Model)

‡ Value (Basu, 1977; Fama and French 1992, 1993)

‡ Size (Banz, 1981; Fama and French 1992, 1993)

‡ Profitability (Haugen and Baker, 1996; Nowy-Marx 2013; Fama and French 2015)

‡ Investment (Titman et al., 2004; Watanabe et al., 2013; Fama and French 2015)

� Why should equity factors work in corporate bond markets?

‡ A bridge between equities and bonds: Structural credit risk models (Merton, 1974)

Introduction Motivation Literature Methodology Results Conclusion

8

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Related Literature II

Option Pricing Theory

Black and Scholes (1973)

‡ To relate equity and debt in the Merton model, equity is valued as a call option on the value of assets V

� Applying the put-call parity yields the value of debt D and equity E as E + D = V, where

Introduction Motivation Literature Methodology Results Conclusion

9

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

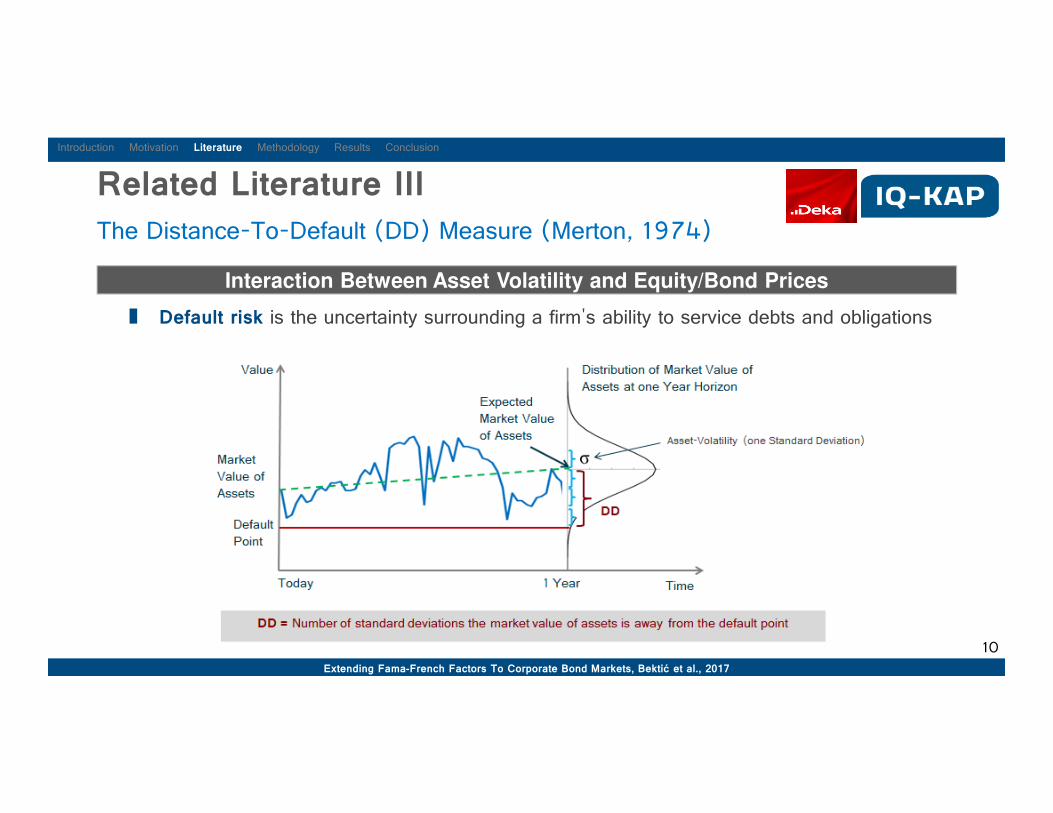

‡ P represents the nominal value of liabilities.

‡ According to the model the spread between risky credit debt and risk-free debt is the value of the put option.

Related Literature III

The Distance-To-Default (DD) Measure (Merton, 1974)

Interaction Between Asset Volatility and Equity/Bond Prices

Introduction Motivation Literature Methodology Results Conclusion

‡ Default risk is the uncertainty surrounding a firm's ability to service debts and obligations

10

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

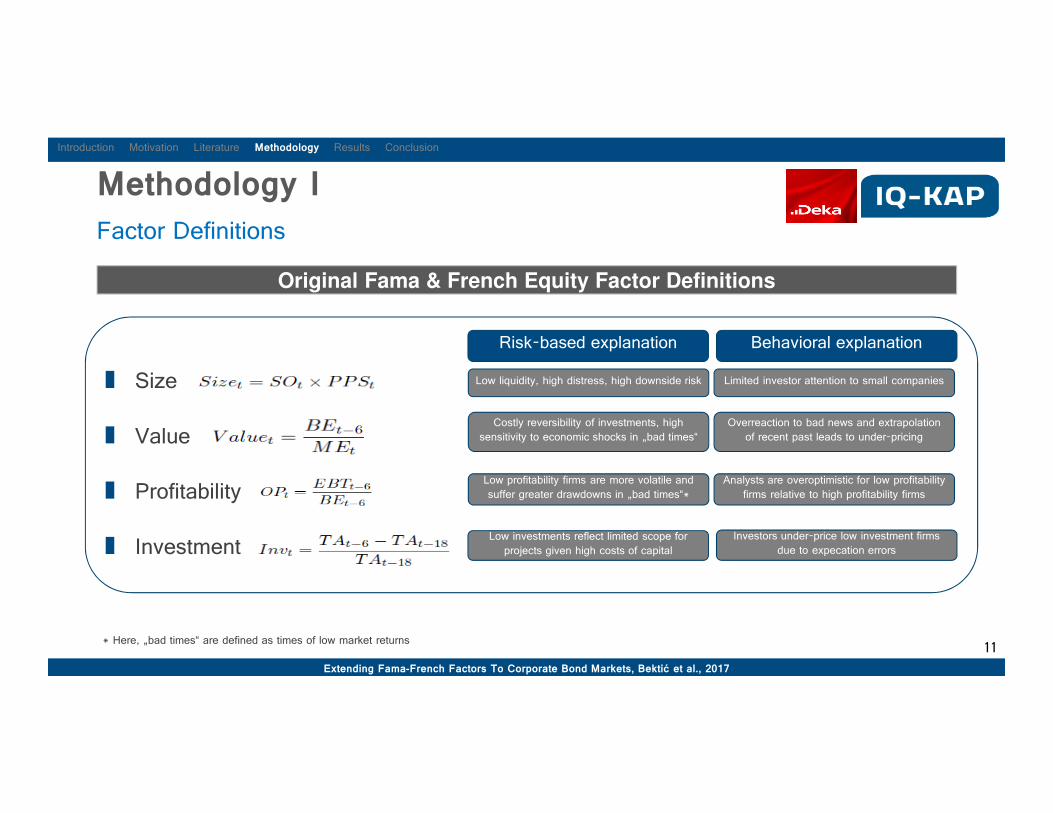

Methodology I

Factor Definitions

Original Fama & French Equity Factor Definitions

‡ Size

‡ Value

‡ Profitability

‡ Investment

Introduction Motivation Literature Methodology Results Conclusion

Risk-based explanation Behavioral explanation

Low liquidity, high distress, high downside risk

Costly reversibility of investments, high

sensitivity to economic shocks in „bad times“

Low profitability firms are more volatile and

suffer greater drawdowns in „bad times“*

Low investments reflect limited scope for

projects given high costs of capital

Limited investor attention to small companies

Overreaction to bad news and extrapolation

of recent past leads to under-pricing

Analysts are overoptimistic for low profitability

firms relative to high profitability firms

Investors under-price low investment firms

due to expecation errors

* Here, „bad times“ are defined as times of low market returns11

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Methodology II

Data

Bank of America Merrill Lynch (BAML) Global Corporate & High Yield Index (GI00)

‡ Monthly data of all senior U.S. High Yield (HY), U.S. Investment Grade (IG) and European

IG corporate bonds

‡ U.S. Data from December 1996 to December2016

‡ European Data from December 2000 to December 2016

‡ Excess returns over duration matched Treasuries

‡ Only publicly traded issuers (the four analyzed factors are based on financial statement ratios

and equity market data)

‡ We eliminate securities that have different payout characteristics compared to standard senior

coupon bonds

‡ 6-month lag (see Fama & French 1992, 1993, 2015)

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Introduction Motivation Literature Methodology Results Conclusion

12

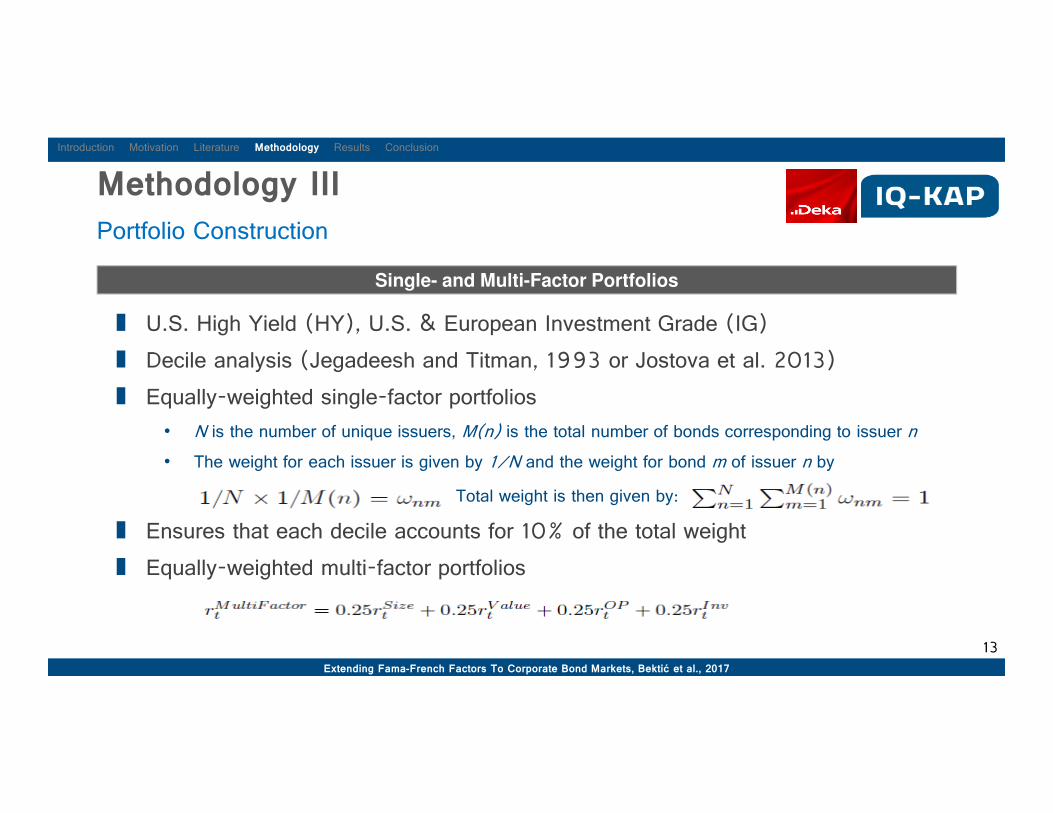

Methodology III

Portfolio Construction

Single- and Multi-Factor Portfolios

‡ U.S. High Yield (HY), U.S. & European Investment Grade (IG)

‡ Decile analysis (Jegadeesh and Titman, 1993 or Jostova et al. 2013)

‡ Equally-weighted single-factor portfolios

• N is the number of unique issuers, M(n) is the total number of bonds corresponding to issuer n

• The weight for each issuer is given by 1/N and the weight for bond m of issuer n by

‡ Total weight is then given by:

‡ Ensures that each decile accounts for 10% of the total weight

‡ Equally-weighted multi-factor portfolios

Introduction Motivation Literature Methodology Results Conclusion

13

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Empirical Results I

Excess Returns & Risk-adjusted Returns

Introduction Motivation Literature Methodology Results Conclusion

Performance Summary of Long-Only Factor Portfolios

14

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

0%

2%

4%

6%

8%

Return

U.S. HY

0.0%

0.5%

1.0%

1.5%

Return

U.S. IG

0.0%

0.5%

1.0%

1.5%

2.0%

Return

EUR IG

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Market Size Value OP Inv MF

Sharpe-Ratio

U.S. HY

0.0

0.1

0.2

0.3

0.4

Market Size Value OP Inv MF

Sharpe-Ratio

U.S. IG

0.00.10.20.30.40.50.60.70.8

Market Size Value OP Inv MF

Sharpe-Ratio

EUR IG

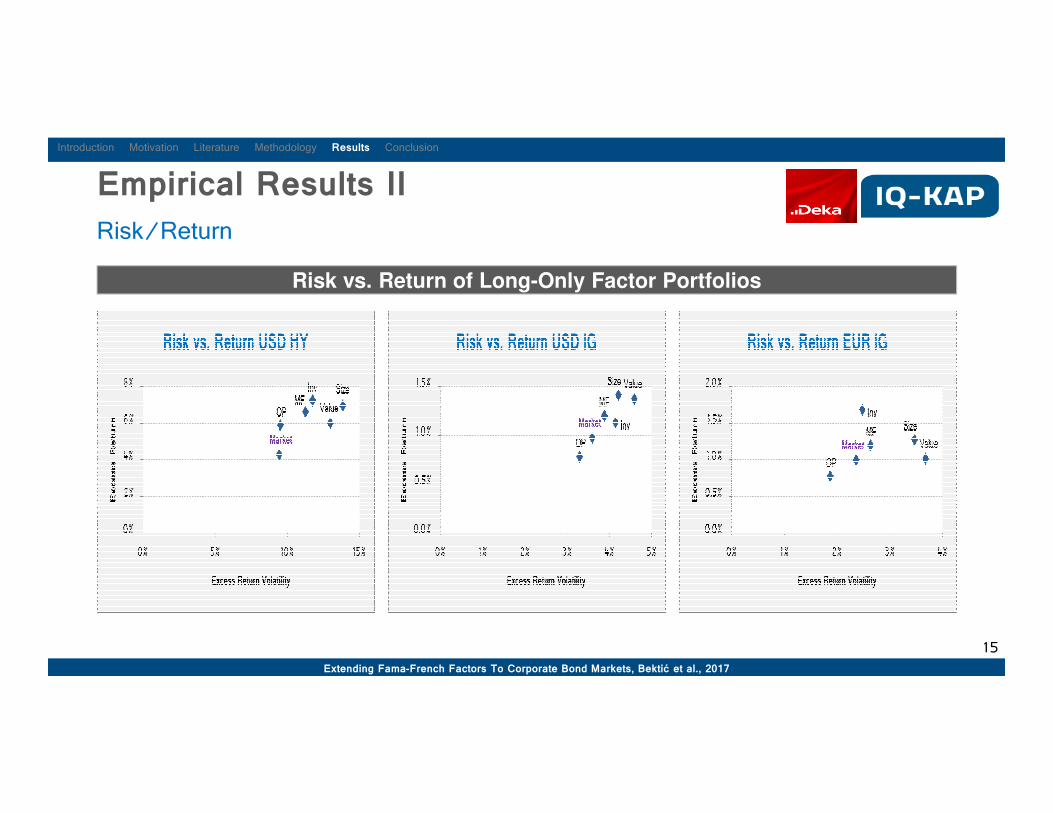

Empirical Results II

Risk/Return

Risk vs. Return of Long-Only Factor Portfolios

Introduction Motivation Literature Methodology Results Conclusion

15

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

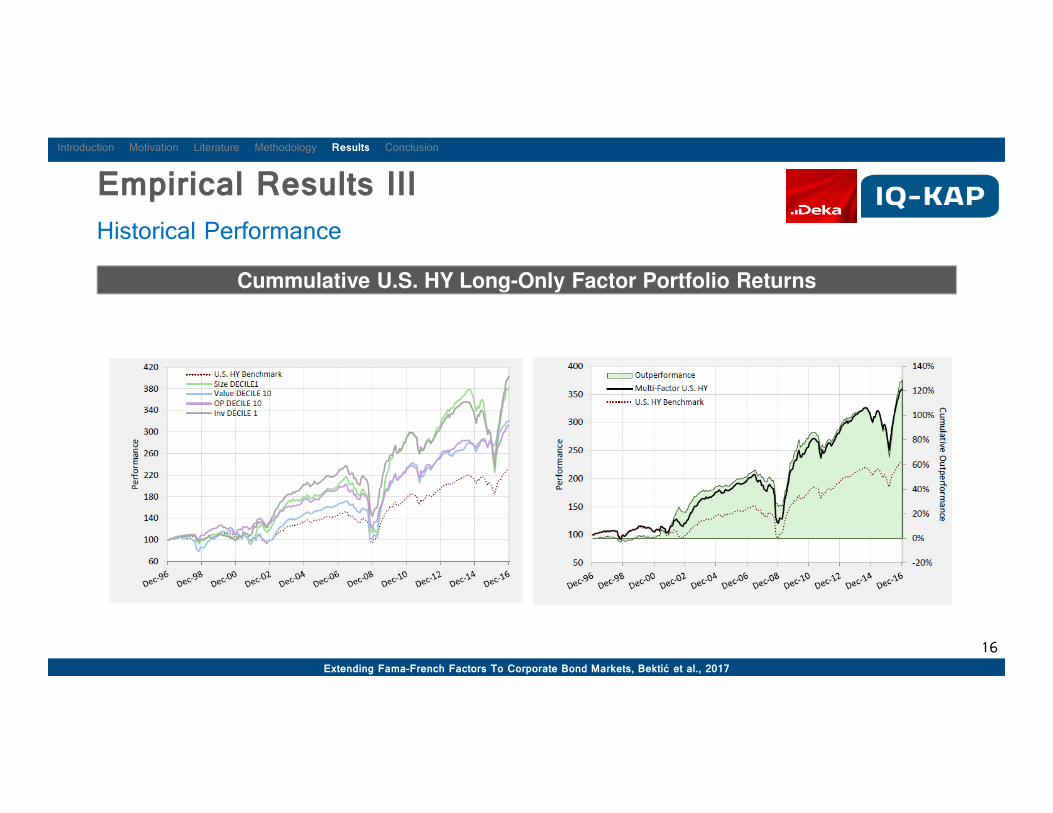

Empirical Results III

Historical Performance

Cummulative U.S. HY Long-Only Factor Portfolio Returns

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Introduction Motivation Literature Methodology Results Conclusion

16

Empirical Results III

Historical Performance

Cummulative U.S. IG Long-Only Factor Portfolio Returns

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Introduction Motivation Literature Methodology Results Conclusion

17

Empirical Results III

Historical Performance

Cummulative European IG Long-Only Factor Portfolio Returns

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Introduction Motivation Literature Methodology Results Conclusion

18

Empirical Results IV

Risk-adjusted Returns after Costs

Performance Summary after Transaction Costs (Long-Only)

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Introduction Motivation Literature Methodology Results Conclusion

19

Conclusion

The Paper in a Nutshell

Fama-French Factors in Corporate Bond Markets

‡ Results suggest that Fama & French equity factors size, value, profitability and

investment can be used for corporate bond investing

‡ BUT: These factors do not fully translate into fixed income markets• All four factors exhibit statistically significant results in U.S. HY markets (size & value for bond investors only)

• Investment statistically significant in the European IG space

‡ Multi-factor portfolios generate positive (risk-adjusted) returns in all three markets• Reduce tracking error and drawdown (higher risk-adjusted returns)

• Benefit from diversification

‡ Factor investing should be a strategic decision• Long-term allocation to factors and implementation into investable strategies is crucial

• Investors should have a clear understanding of the sources of expected returns, the stability and sustainability

of those returns, the risk exposure and risk controls as well as the liquidity demands of the strategy

Introduction Motivation Literature Methodology Results Conclusion

20

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Time Series Regressions / Asset-Pricing Tests

1)

2)

3)

Appendix

Appendix 1

Introduction Motivation Literature Methodology Results Conclusion Appendix

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

* The data on MKT, SMB, HML, RMW, and CMA is obtained from Kenneth French's website: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

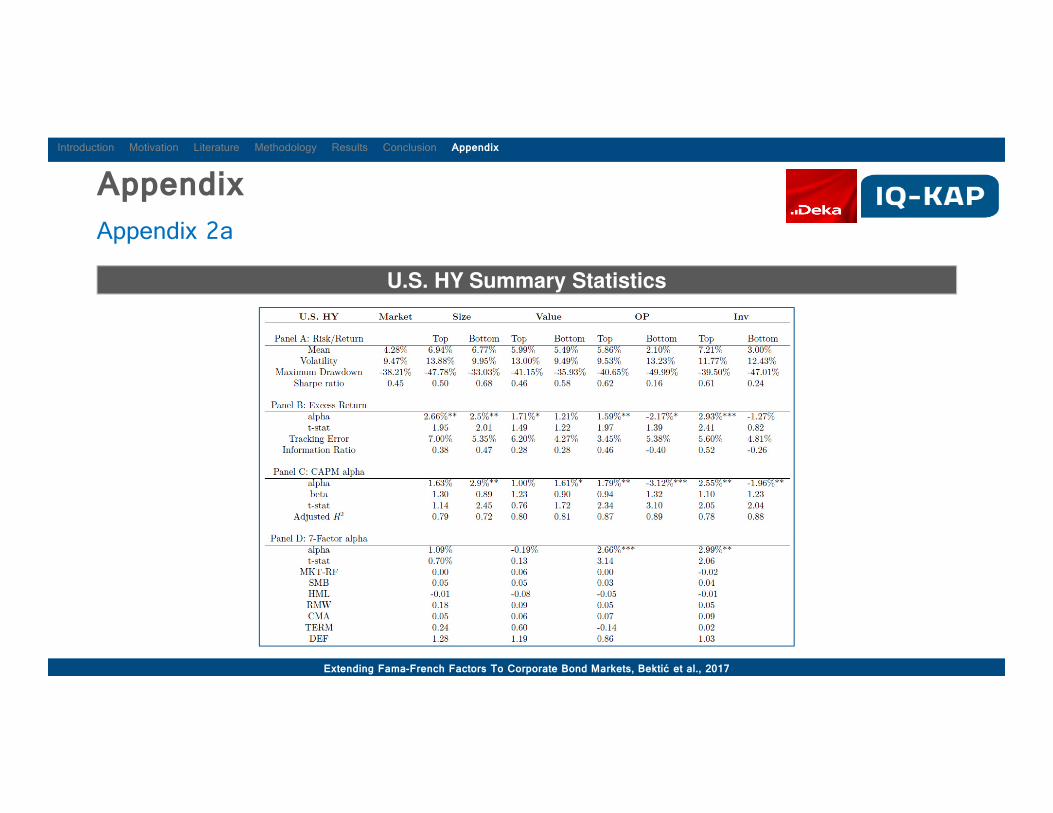

Appendix

Appendix 2a

U.S. HY Summary Statistics

Introduction Motivation Literature Methodology Results Conclusion Appendix

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Appendix

Appendix 2b

U.S. IG Summary Statistics

Introduction Motivation Literature Methodology Results Conclusion Appendix

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Appendix

Appendix 2c

European IG Summary Statistics

Introduction Motivation Literature Methodology Results Conclusion Appendix

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

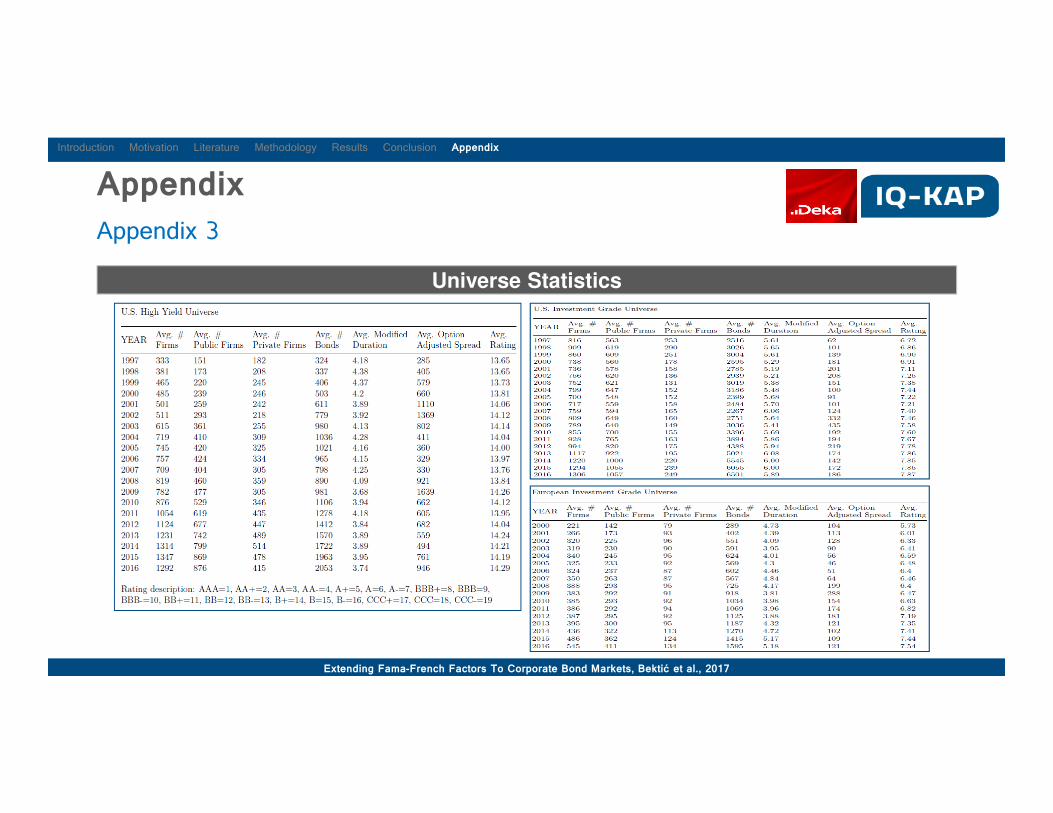

Appendix

Appendix 3

Universe Statistics

Introduction Motivation Literature Methodology Results Conclusion Appendix

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

Appendix

Appendix 4a

Long-Short Correlation Summary I (U.S. only)

Introduction Motivation Literature Methodology Results Conclusion Appendix

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017

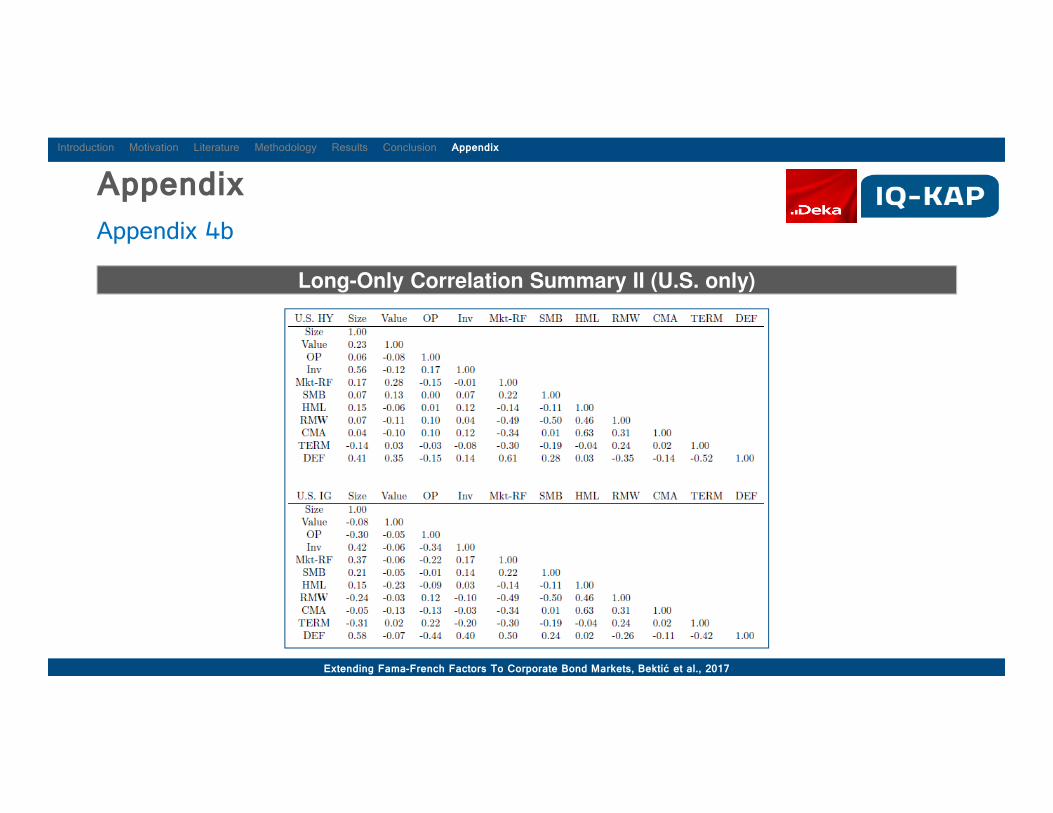

Appendix

Appendix 4b

Long-Only Correlation Summary II (U.S. only)

Introduction Motivation Literature Methodology Results Conclusion Appendix

Extending Fama-French Factors To Corporate Bond Markets, Bektić et al., 2017