Embed Size (px)

Citation preview

Exploring specialty finance data

Introducing:

John Lodmell Advance America Paul DeSaulniers Experian Crissy Wallace Experian

©Experian 3

• CFPB proposal

• Data analysis

• Business impact and the market ahead

Contents

4/21/2017 Experian Public Vision 2017

©Experian 4

Live poll

4/21/2017 Experian Public Vision 2017

©Experian 5

Consumer Finance Protection Bureau Proposed payday loan rules

Paul DeSaulniers Experian

4/21/2017 Experian Public Vision 2017

©Experian 6

Two categories of loans covered:

• Term of 45 days or less

• Term greater then 45 days that total cost of credit is greater than 36%, and:

– Repaid directly from borrowers bank account or secured by borrowers vehicle

The proposed rule:

• Require lenders too make a determination that borrower has ability to repay loan

– Verify income

– Verify borrowers debt obligations using a credit report

– Verify borrowers housing cost

– Forecast reasonable living expenses

– Project borrowers net income, debt obligations and housing cost and ability to repay for the loan period

• Require lender to furnish information to registered information system (RIS)

Summary of the 1,300+ pages

4/21/2017 Experian Public Vision 2017

©Experian 7

Impact of rules, if implemented as written

4/21/2017 Experian Public Vision 2017

Significant

reduction in pay

day lending activity

• CFPB’s own

estimate would

eliminate 84% of

volume

Online and FinTech

lenders believe

proposed rules will

provide greater

opportunity to fill

void left by less

sophisticated lenders

(brick and mortar

lenders

Consumer groups

have divergent

views • Represents an

attempt to protect borrowers

• Does not go far enough

• Diminished liquidity options driving consumers to loan sharks, pawn shops or less desirable alternatives

Over one million

comments

submitted to the

CFPB

©Experian 8

• Does ability repay criteria as describe in rule predict consumer pay day loan performance

• How do traditional credit risk scores predict consumer performance in this space

• Profiles of consumers in the specialty finance consumers

What we will explore today

4/21/2017 Experian Public Vision 2017

©Experian 9

Data analysis

4/21/2017 Experian Public Vision 2017

Crissy Wallace Experian

©Experian 10

Additional data provides

better visibility to consumers

4/21/2017 Experian Public Vision 2017

©Experian 11

Currently lenders decision heavily on generic score to define risk

4/21/2017 Experian Public Vision 2017

Super Prime

Prime

Near Prime

Subprime

Deep Subprime

781-850

661-780

601-660

500-600

300-499

Low risk

High risk

©Experian 12

Traditional data Specific models Trended data

Thin file Aspirational data Specialty finance

The more we know about a consumer, the more accurately we can predict risk, using additional data

4/21/2017 Experian Public Vision 2017

©Experian 13

Low risk

High risk

Some data will increase predictability

with positive data for subprime consumers

4/21/2017 Experian Public Vision 2017

Positive examples:

Rental, telecom,

and utility

©Experian 14

Some data will increase predictability

with negative data for prime consumers

4/21/2017 Experian Public Vision 2017

Negative samples:

Short-term loans, payday,

rent-to-own

Low risk

High risk

©Experian 15

This provides increase predictability, and this data is FCRA, disputable and CAN be used for decisioning

4/21/2017 Experian Public Vision 2017

Low risk

High risk

Negative samples:

Short-term loans, payday,

rent-to-own

Positive examples:

Rental, telecom,

and utility

©Experian 16

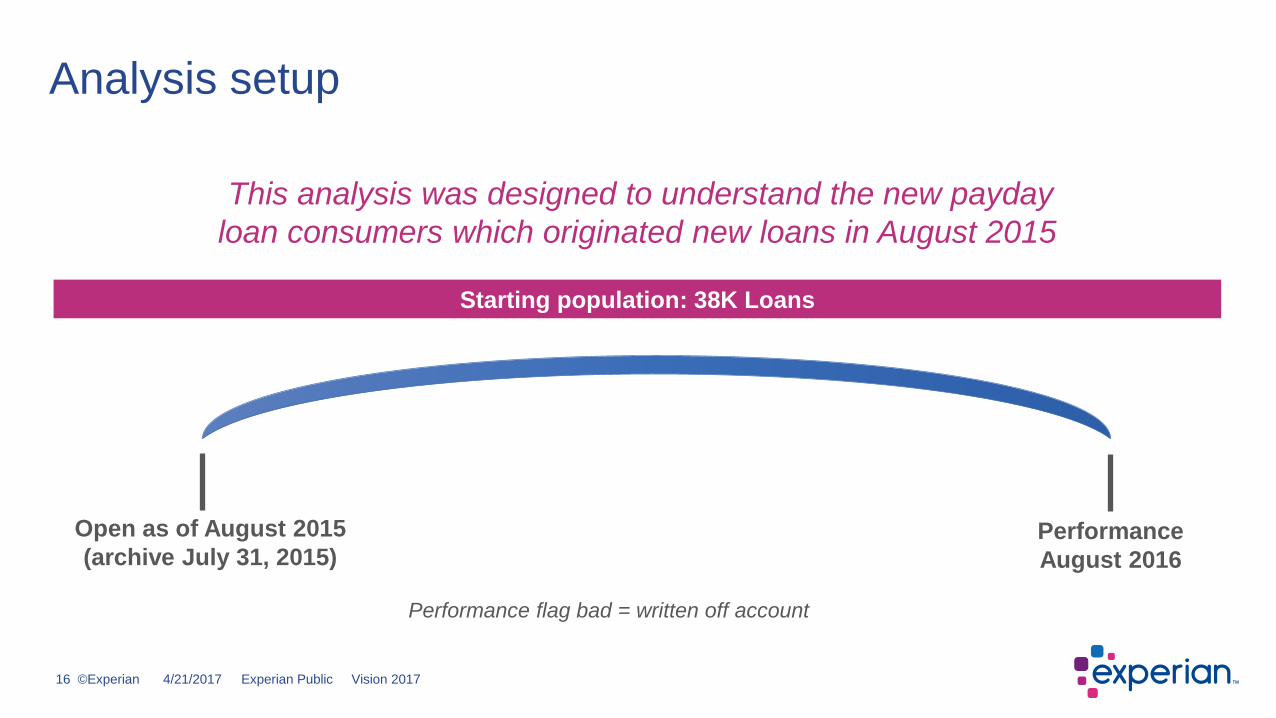

Analysis setup

4/21/2017 Experian Public Vision 2017

This analysis was designed to understand the new payday

loan consumers which originated new loans in August 2015

Open as of August 2015

(archive July 31, 2015)

Starting population: 38K Loans

Performance

August 2016

Performance flag bad = written off account

©Experian 17

Data overview Waterfall counts

4/21/2017 Experian Public Vision 2017

Input records

38,490

Unable to identify (No Hit to bureau) 1.5%

Address error <0.1%

No Pin 0.56%

Hit, but suppressed 0.91%

Consumer identified (Hit to bureau) 98.5%

Hit but no credit/scores (Collection, inquiry, public record or unscoreable)

11.5%

Thin File (1-4 trades)

39%

Thick File (5 or more trades)

48%

©Experian 18

Model performance

4/21/2017 Experian Public Vision 2017

0%

20%

40%

60%

80%

100%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70% 75% 80% 85% 90% 95% 100%

Cum

ula

tive

% o

f b

ad

acco

un

ts

Cumulative % of accounts

KS Statistic

Custom Model Score

Telecom Risk Score

TEC Connect

VantageScore V3

ExtendedView

31 25 23 23 20

KS

Custom Model Telecom Risk

VantageScore V3 EVS

TEC Connect

A statistical process called Kolmogorov-Smirnov (K-S) measures the separation of two

populations, for example ‘Goods’ versus ‘Bads’. The K-S statistic aims at measuring the

maximum difference in two populations’ cumulative distributions. The K-S measure for the

model shows the capability to distinguish ‘Good Accounts’ from ‘Bad Accounts’.

©Experian 19

Model performance

4/21/2017 Experian Public Vision 2017

15%

29%

43%

15%

28%

41%

13%

26%

39%

14%

26%

38%

14%

26%

38%

10% 20% 30%

Worst Scoring 30%

Custom Model

Telecom Risk Score

VantageScore V3

ExtendedView

TEC Connect

Pe

rcen

t o

f b

ad

acco

un

ts

Lowest scoring ranges

The ability of a model to push the largest percentage of bads

to the lowest scoring ranges is a hallmark of scorecard performance.

©Experian 20

Custom model

4/21/2017 Experian Public Vision 2017

24.8%

49.1%

58.8% 62.6%

65.6% 69.2% 67.0%

41.6%

0%

10%

20%

30%

40%

50%

60%

70%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

900-999 800-899 700-799 600-699 500-599 400-499 300-399 Exclusion Score

Write

-off r

ate

Num

be

r o

f a

cco

un

ts

Loans Writeoff Writeoff Rate

©Experian 21

Profiling specialty finance consumers

4/21/2017 Experian Public Vision 2017

What does the AVERAGE

specialty finance (payday)

consumer really look like?

Total # bankcard loans = 2 trades; $98/mo

Total # personal loans = 1 trades; $21/mo

Total # mortgage loans =

0.27 trade; $961/mo

Average debt-to-income

16% Average Vantage

Score® V3 = 536

Average Income

InsightSM $39K

Total # traditional

credit trades = 8 trades

Total # auto loans = 1 trade; 448/mo

©Experian 22

Income distributions

4/21/2017 Experian Public Vision 2017

Loans Write-off Write-off rate

52.6%

40.7%

27.1%

14.3%

46.8%

0%

10%

20%

30%

40%

50%

60%

70%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

$1-35K $35-50K $50-100K $100K+ Exclusion

Write

-off r

ate

Nu

mb

er

of a

cco

un

ts

Income InsightSM

©Experian 23

Generation segments and sample distribution

4/21/2017 Experian Public Vision 2017

Gen Z

Age 18–20

Gen Y

Younger: Age 21–27

Older: Age 28–34

Gen X

Age 35–49

Boomer

Age 50–70

Silent

Age 70+

©Experian 24

Loans by generation

4/21/2017 Experian Public Vision 2017

2.6%

19.6%

23.3%

29.0%

22.1%

3.4%

0.0%

Generation

Percent of loans by generation

Gen Z Gen YY Gen OY Gen X

Boomer Silent Unknown

Pe

rce

nt o

f a

cco

un

ts

545

525 525

533

552

576

490

500

510

520

530

540

550

560

570

580

0

2000

4000

6000

8000

10000

12000

Gen Z Gen YY Gen OY Gen X Boomer Silent

Super Prime Prime Near Prime

Subprime Deep Subprime Average VS3

Accounts by generation

and VantageScore® band

©Experian 25

File thickness overall and by generation

4/21/2017 Experian Public Vision 2017

Match but no trades

11.5%

Thin 1-4 trades 39.0%

Thick >= 5 trades 48.0%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

No bureau match

Match but no trade data

Thin 1-4 trades

Thick >=5 trades

No match /

Not scoreable 1.5%

©Experian 26

Age of oldest trade

-

1,000

2,000

3,000

4,000

5,000

6,000

Missing Gen Z Gen YY Gen OY Gen X Boomer Silent

Age of oldest trade on bureau by generation

Missing < 2 yrs 2-5 yrs 5-10 yrs 10+ yrs

Nu

mb

er

of

ac

co

un

ts

4/21/2017 Experian Public Vision 2017

©Experian 27

Number of payday loans by generation and score band

-

5,000

10,000

15,000

20,000

25,000

Super Prime Prime NearPrime Subprime Deep Subprime

1 Loan 2 Loans 3 Loans 4 Loans 5 Loans 6 to 10 Loans 11 to 15 Loans 16 to 20 Loans >20 Loans

Number of payday loans by VantageScore® band

4/21/2017 Experian Public Vision 2017

©Experian 28

More clear consumer view

By adding additional data to the

consumer profile the view of the

consumer is now much more clear

and the lenders can make more

accurate credit decisions

4/21/2017 Experian Public Vision 2017

©Experian 29

Business impact and the market ahead

4/21/2017 Experian Public Vision 2017

John Lodmell Advance America

©Experian 30

Thoughts on the market ahead…

4/21/2017 Experian Public Vision 2017

©Experian 31

Experian contact:

Paul DeSaulniers [email protected]

Crissy Wallace [email protected]

Questions and answers

4/21/2017 Experian Public Vision 2017

PaulDeSauliners @PDesaulniers

@CrissyWallace CrissyWallaceMyler

©Experian 32

Share your thoughts about Vision 2017!

4/21/2017 Experian Public Vision 2017

Please take the time now to give us your feedback about this session.

You can complete the survey at the kiosk outside.

How would you rate both the Speaker and Content?