Embed Size (px)

Citation preview

Exploration & Production

59

Our Goals and Agenda

Demonstrate clear progress on performance

Describe our path to become “Top Tier”

Detailed review of operations

Confirm performance expectations

60

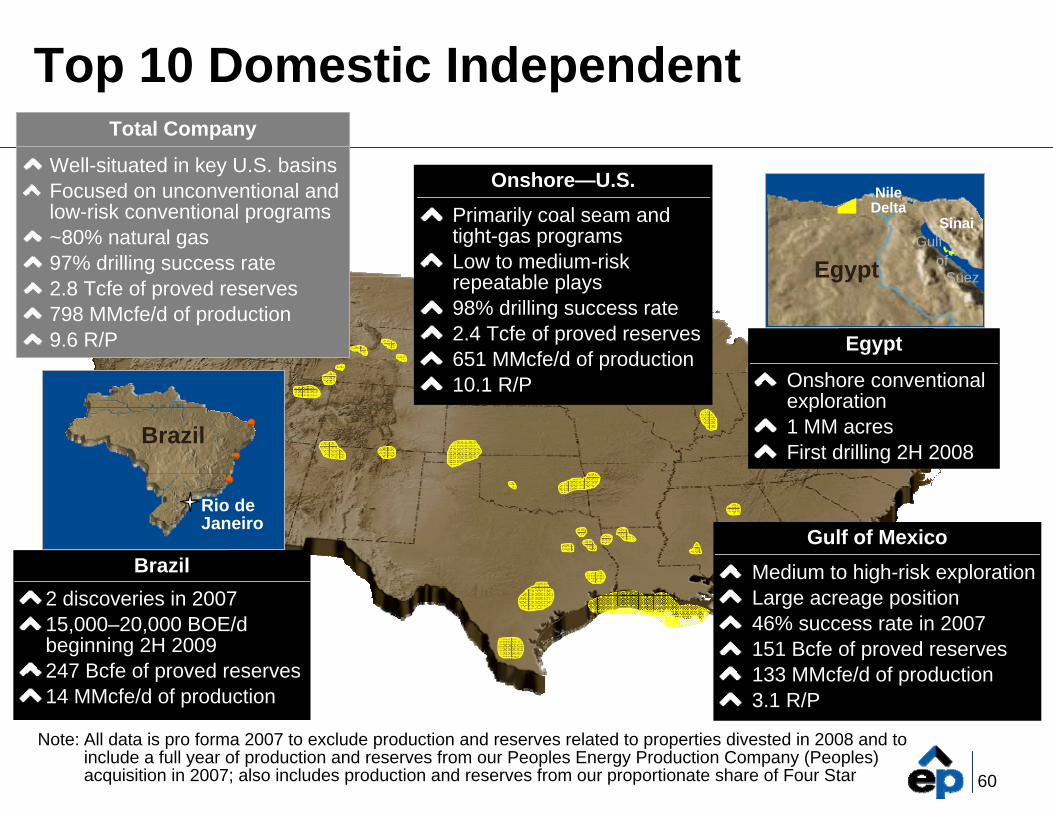

Top 10 Domestic Independent

Note: All data is pro forma 2007 to exclude production and reserves related to properties divested in 2008 and to include a full year of production and reserves from our Peoples Energy Production Company (Peoples) acquisition in 2007; also includes production and reserves from our proportionate share of Four Star

Brazil2 discoveries in 200715,000–20,000 BOE/d beginning 2H 2009247 Bcfe of proved reserves14 MMcfe/d of production

Egypt

Onshore conventional exploration1 MM acresFirst drilling 2H 2008

Egypt

NileDelta

Sinai

EgyptGulf

ofSuez

Total Company

Well-situated in key U.S. basinsFocused on unconventional and low-risk conventional programs~80% natural gas97% drilling success rate2.8 Tcfe of proved reserves798 MMcfe/d of production9.6 R/P

Onshore—U.S.Primarily coal seam and tight-gas programsLow to medium-risk repeatable plays98% drilling success rate2.4 Tcfe of proved reserves651 MMcfe/d of production10.1 R/P

Gulf of MexicoMedium to high-risk explorationLarge acreage position46% success rate in 2007151 Bcfe of proved reserves133 MMcfe/d of production3.1 R/P

Rio de Janeiro

Brazil

61

High Grading Our Portfolio

Divested 309 Bcfe of properties for $845 MM (sales price and assumed asset retirement obligation)—$2.73/Mcfe

Low inventory, high operating costs

Purchased Peoples for $887 MM

End result—more focused; more profitable, faster growing; added 450 total gross drilling locations

62

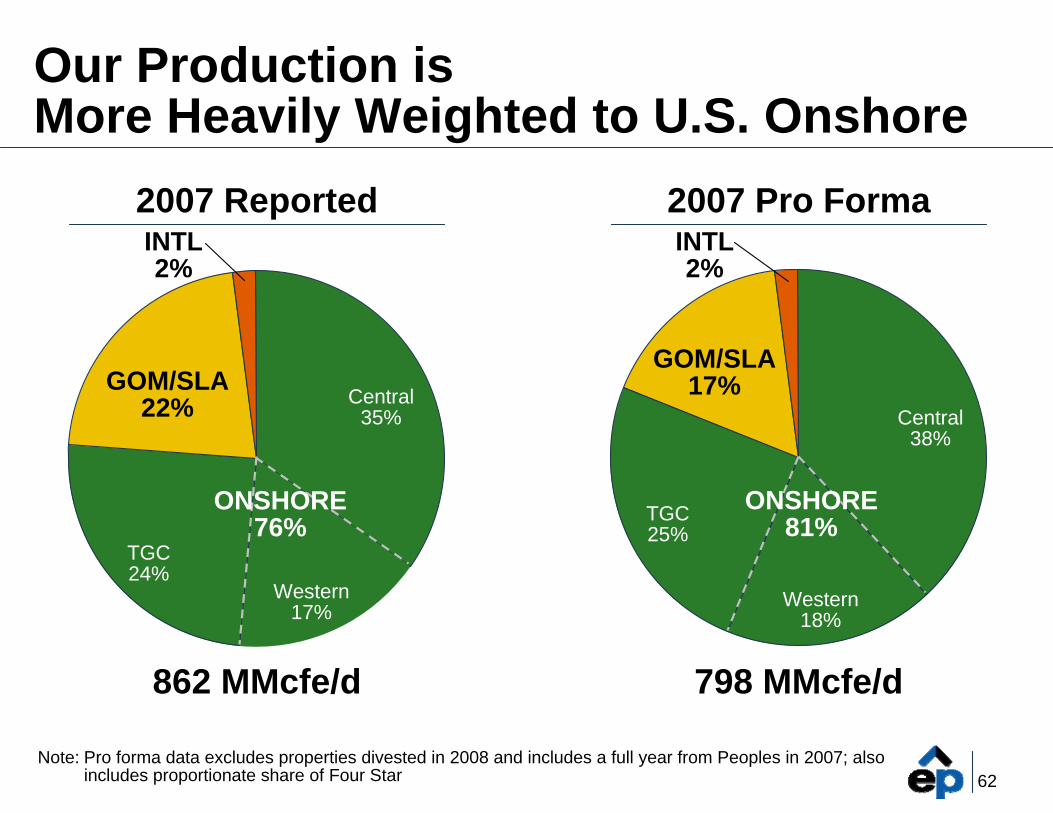

Our Production isMore Heavily Weighted to U.S. Onshore

Central 35%

Western17%

TGC24%

INTL2%

2007 Reported

862 MMcfe/d 798 MMcfe/d

2007 Pro Forma

GOM/SLA22% Central

38%

Western18%

TGC25%

GOM/SLA17%

ONSHORE76%

INTL2%

ONSHORE81%

Note: Pro forma data excludes properties divested in 2008 and includes a full year from Peoples in 2007; also includes proportionate share of Four Star

63

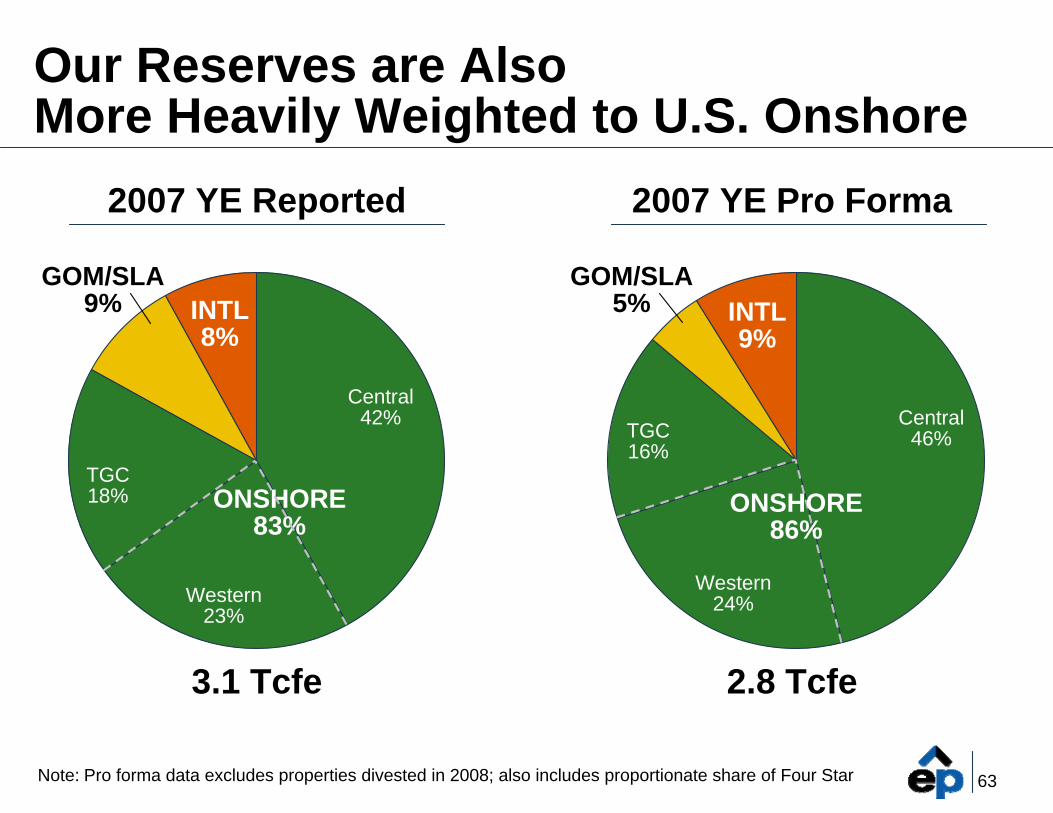

3.1 Tcfe

Our Reserves are AlsoMore Heavily Weighted to U.S. Onshore

Central42%

GOM/SLA9%

TGC18%

INTL8%

Central46%

GOM/SLA5%

TGC16%

INTL9%

2007 YE Reported 2007 YE Pro Forma

2.8 Tcfe

Western23%

Western24%

ONSHORE83%

ONSHORE86%

Note: Pro forma data excludes properties divested in 2008; also includes proportionate share of Four Star

64

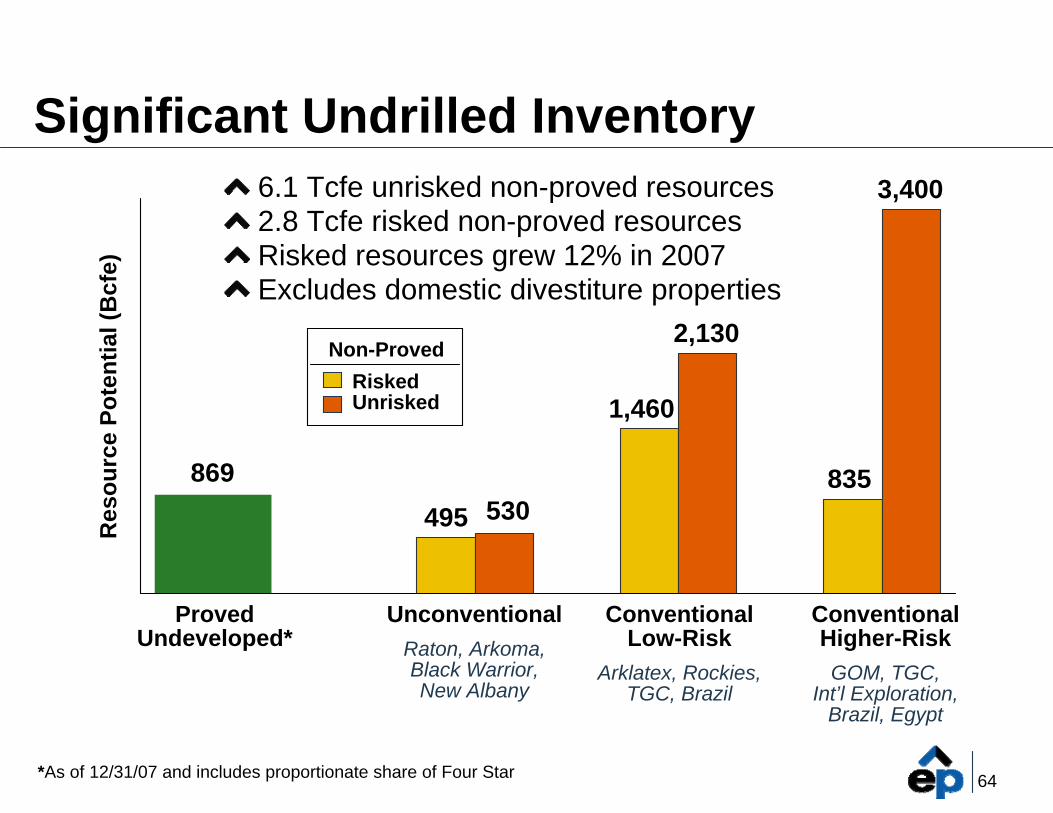

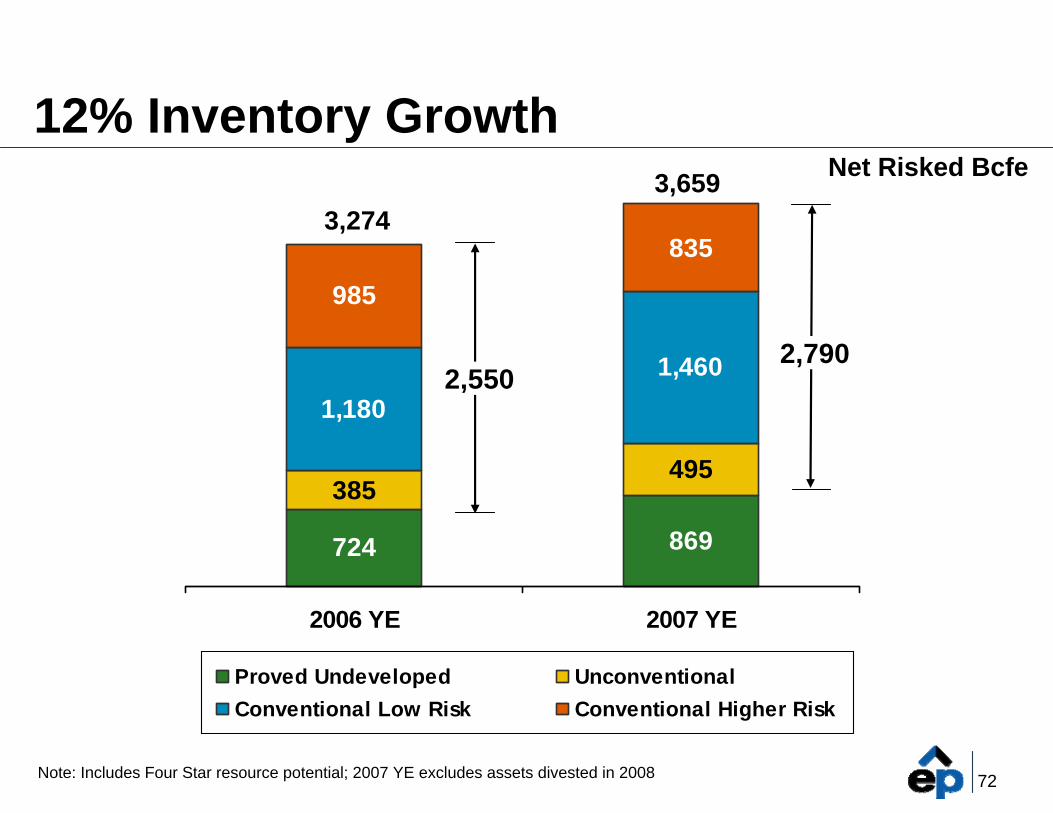

Significant Undrilled Inventory

Proved Undeveloped*

UnconventionalRaton, Arkoma,Black Warrior,New Albany

ConventionalLow-Risk

Arklatex, Rockies, TGC, Brazil

ConventionalHigher-RiskGOM, TGC,

Int’l Exploration,Brazil, Egypt

869495 530

1,460

2,130

835

3,400

*As of 12/31/07 and includes proportionate share of Four Star

Res

ourc

e Po

tent

ial (

Bcf

e)

6.1 Tcfe unrisked non-proved resources2.8 Tcfe risked non-proved resourcesRisked resources grew 12% in 2007Excludes domestic divestiture properties

RiskedUnrisked

Non-Proved

65

2007 AccomplishmentsProduction growth 8%

Reserves growth 18%

Unit LOE dropped 7%

Inventory growth of 12%

Staff rose 10%

Significant international exploration success

Portfolio high gradingPeoples acquisitionDivestitures

We delivered on our commitments

Hit our targets

Visible growth

Top quartile performance

Visible growth

Increasing capability

Pinaúna, Bia (Brazil)

More focused, faster growth, lower cost operator

66

Strategy for “Top Tier” Has Not Changed,But it is Better Defined

Build and apply competencies in assets with repeatable programs and significant project inventory

Sharpen execution skills to improve capitaland expense efficiency and maximize returns

Add assets with inventory that fit our competencies and divest assets that do not

67

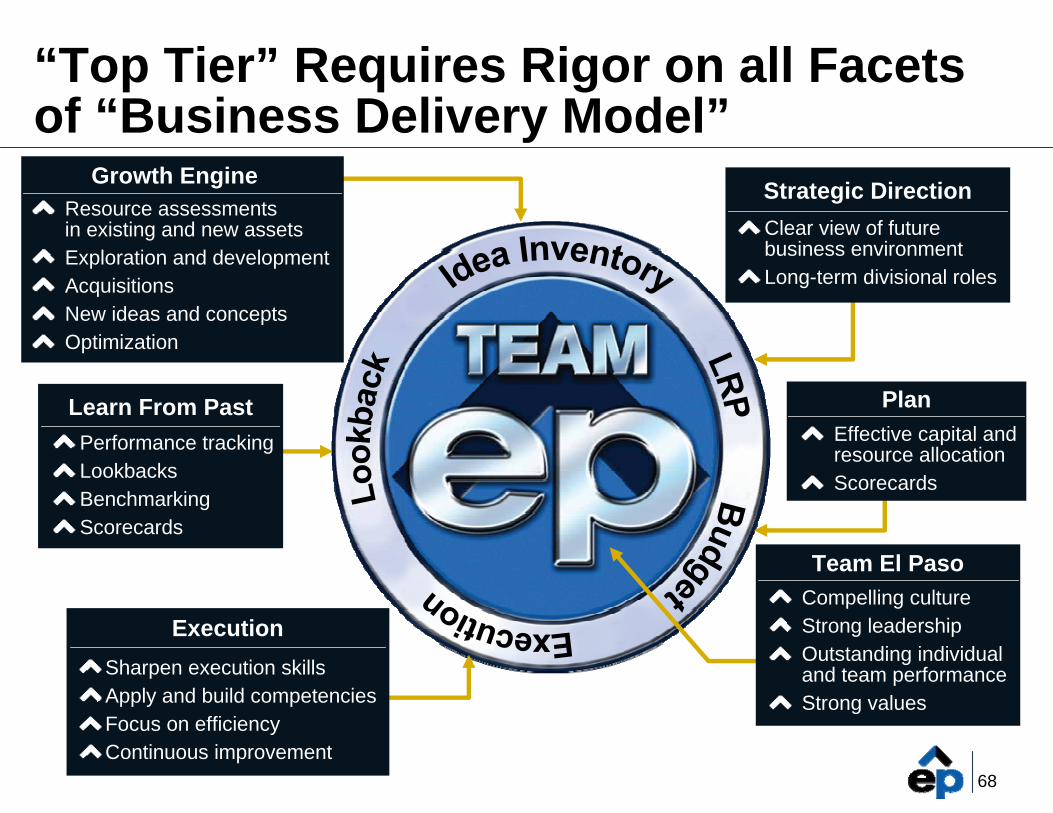

“Business Delivery Model” is the Core ofOur Approach to the Business

68

“Top Tier” Requires Rigor on all Facetsof “Business Delivery Model”

PlanEffective capital and resource allocationScorecards

Resource assessmentsin existing and new assetsExploration and developmentAcquisitionsNew ideas and conceptsOptimization

Growth Engine Strategic DirectionClear view of future business environmentLong-term divisional roles

Compelling cultureStrong leadershipOutstanding individualand team performanceStrong values

Team El Paso

Learn From PastPerformance trackingLookbacksBenchmarkingScorecards

Sharpen execution skills Apply and build competenciesFocus on efficiency Continuous improvement

Execution

69

Priority to Align Assets to Competencies

Competency

Rep

eata

bilit

y

StrengthenCompetencies

Leverage Strengths& Increase Activity

Rationalize DevelopInventory

Low

Hig

h

Weak Strong

70

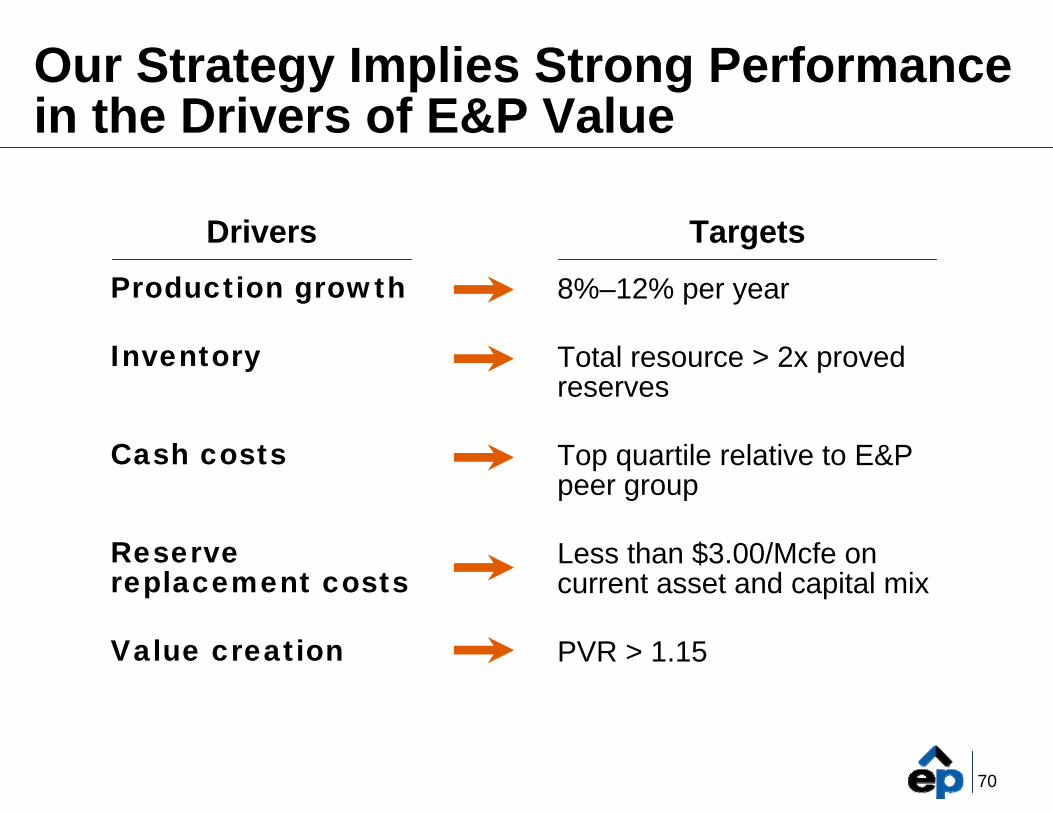

Our Strategy Implies Strong Performancein the Drivers of E&P Value

Production growth

Inventory

Cash costs

Reservereplacement costs

Value creation

8%–12% per year

Total resource > 2x proved reserves

Top quartile relative to E&Ppeer group

Less than $3.00/Mcfe oncurrent asset and capital mix

PVR > 1.15

Drivers Targets

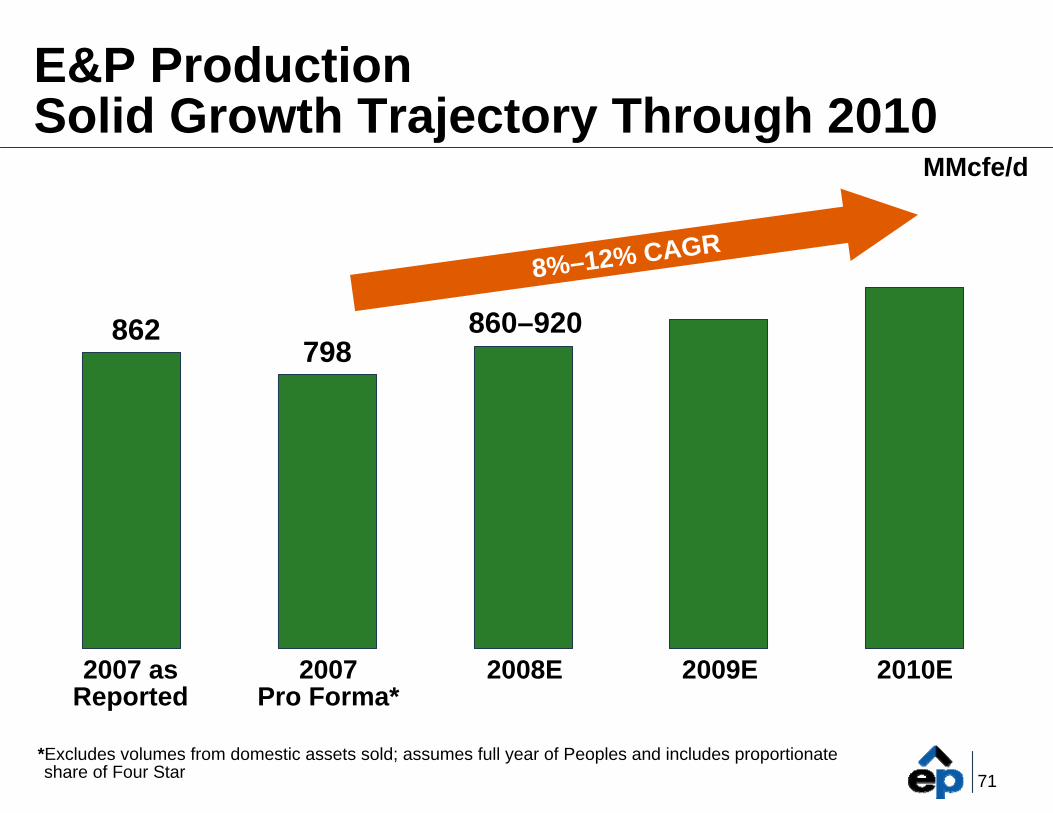

71*Excludes volumes from domestic assets sold; assumes full year of Peoples and includes proportionate share of Four Star

E&P ProductionSolid Growth Trajectory Through 2010

862798

860–920

8%–12% CAGR

2007 asReported

2007Pro Forma*

2008E 2009E 2010E

MMcfe/d

72

724 869

385495

1,1801,460

985

835

2006 YE 2007 YE

Proved Undeveloped UnconventionalConventional Low Risk Conventional Higher Risk

12% Inventory Growth

3,2743,659

2,7902,550

Note: Includes Four Star resource potential; 2007 YE excludes assets divested in 2008

Net Risked Bcfe

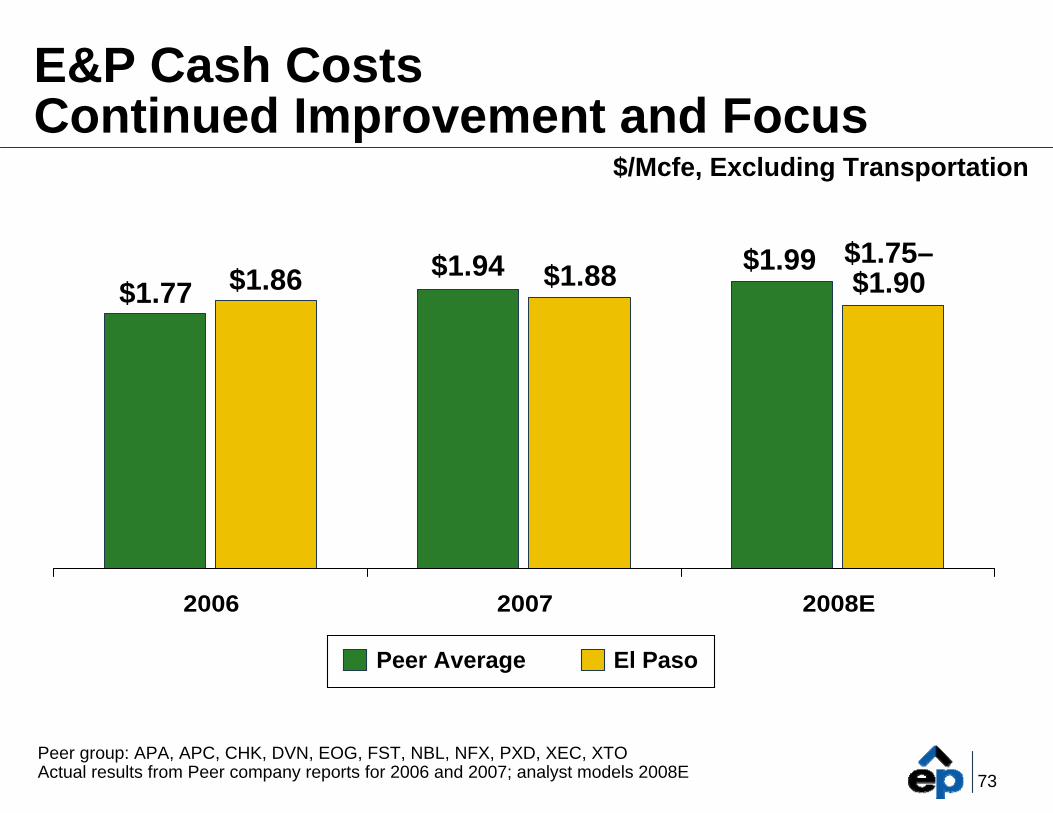

73Peer group: APA, APC, CHK, DVN, EOG, FST, NBL, NFX, PXD, XEC, XTOActual results from Peer company reports for 2006 and 2007; analyst models 2008E

2006 2007 2008E

E&P Cash CostsContinued Improvement and Focus

$1.77 $1.86 $1.94 $1.88$1.75–$1.90

$1.99

Peer Average El Paso

$/Mcfe, Excluding Transportation

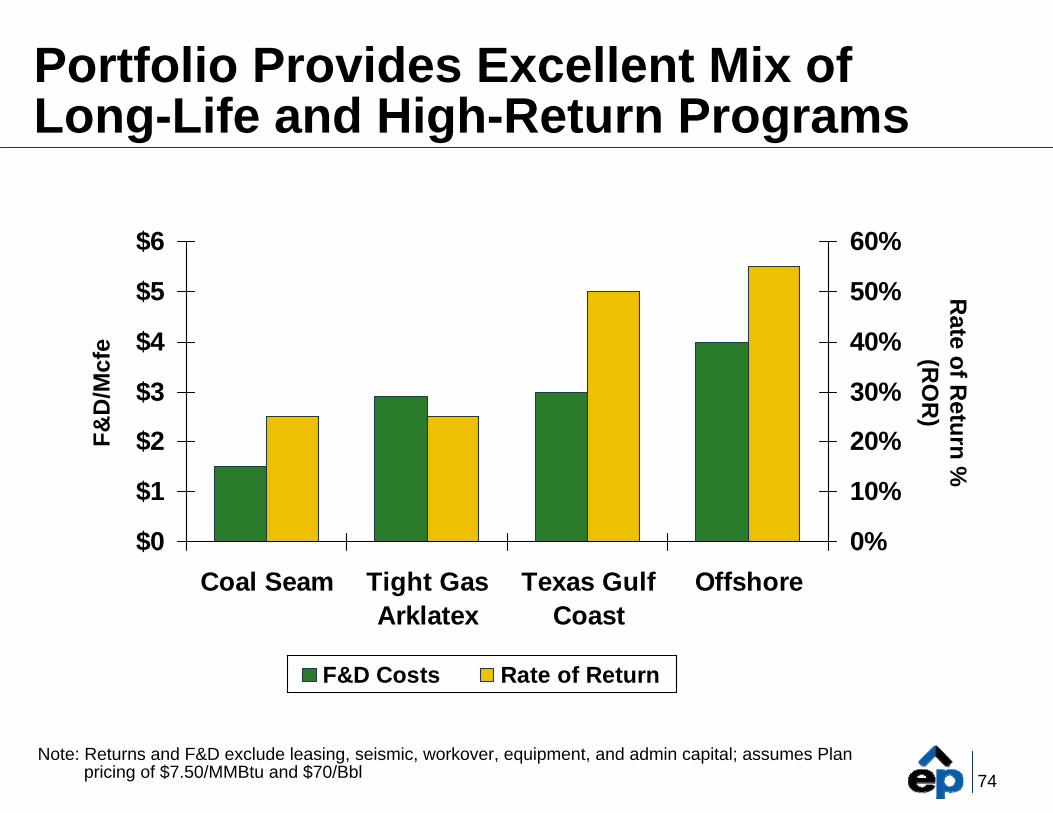

74Note: Returns and F&D exclude leasing, seismic, workover, equipment, and admin capital; assumes Plan

pricing of $7.50/MMBtu and $70/Bbl

Portfolio Provides Excellent Mix ofLong-Life and High-Return Programs

F&D

/Mcf

e

$0

$1

$2

$3

$4

$5

$6

Coal Seam Tight GasArklatex

Texas GulfCoast

Offshore0%

10%

20%

30%

40%

50%

60%

F&D Costs Rate of Return

Rate of R

eturn %(R

OR

)

75

0

2

4

6

8

10

12

14

4 5 6 7 8 9 10 11

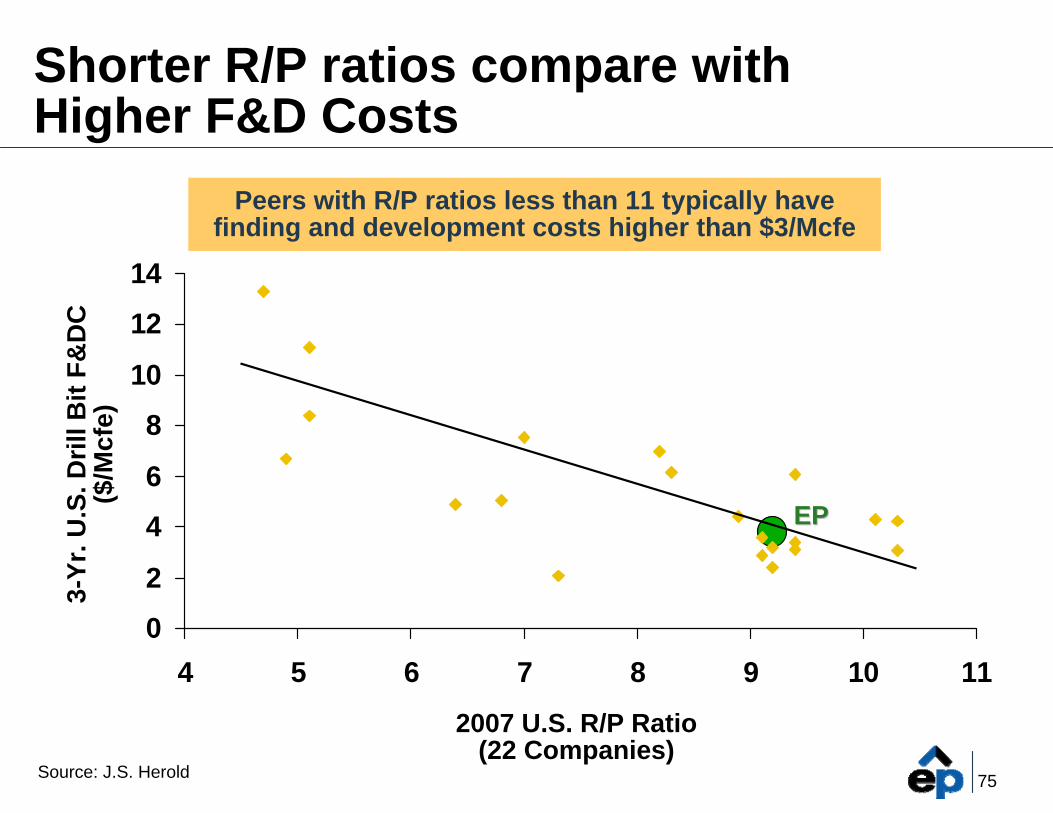

Shorter R/P ratios compare withHigher F&D Costs

EPEP

Peers with R/P ratios less than 11 typically havefinding and development costs higher than $3/Mcfe

3-Yr

. U.S

. Dril

l Bit

F&D

C($

/Mcf

e)

2007 U.S. R/P Ratio(22 Companies)

Source: J.S. Herold

76

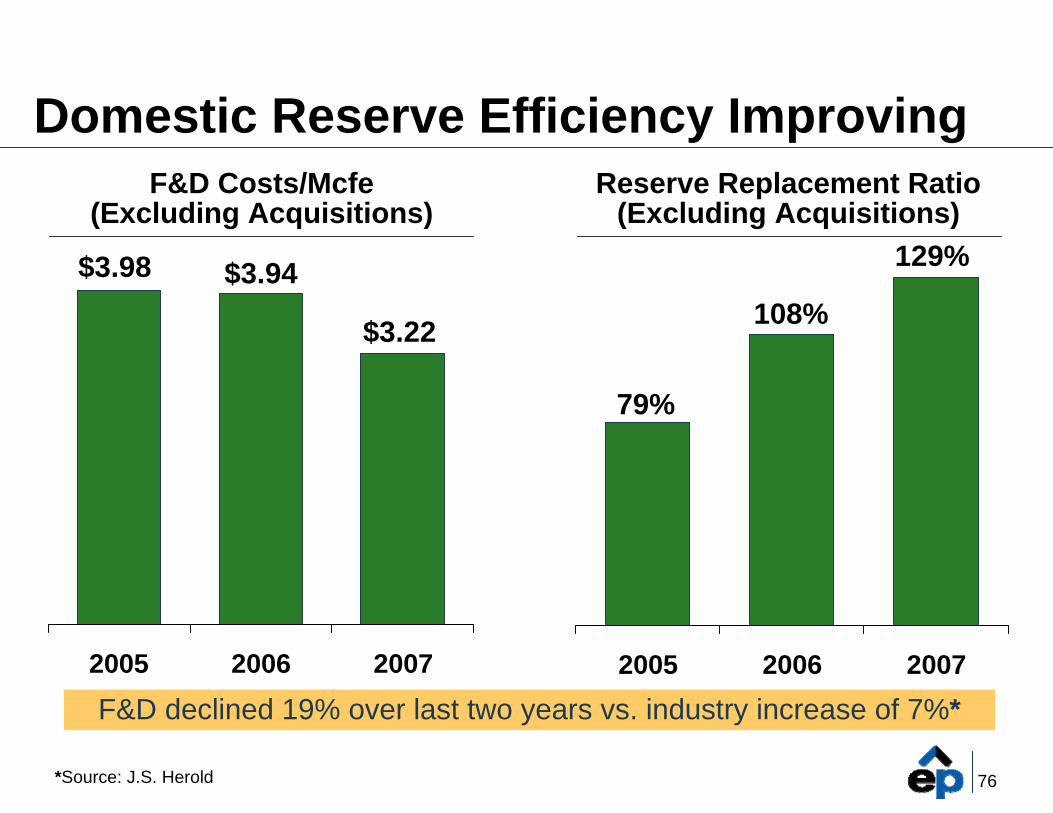

Domestic Reserve Efficiency Improving

2005 2006 2007

F&D Costs/Mcfe (Excluding Acquisitions)

$3.98 $3.94

$3.22

2005 2006 2007

Reserve Replacement Ratio (Excluding Acquisitions)

79%

108%

129%

F&D declined 19% over last two years vs. industry increase of 7%*

*Source: J.S. Herold

77

2006 2007 2008E

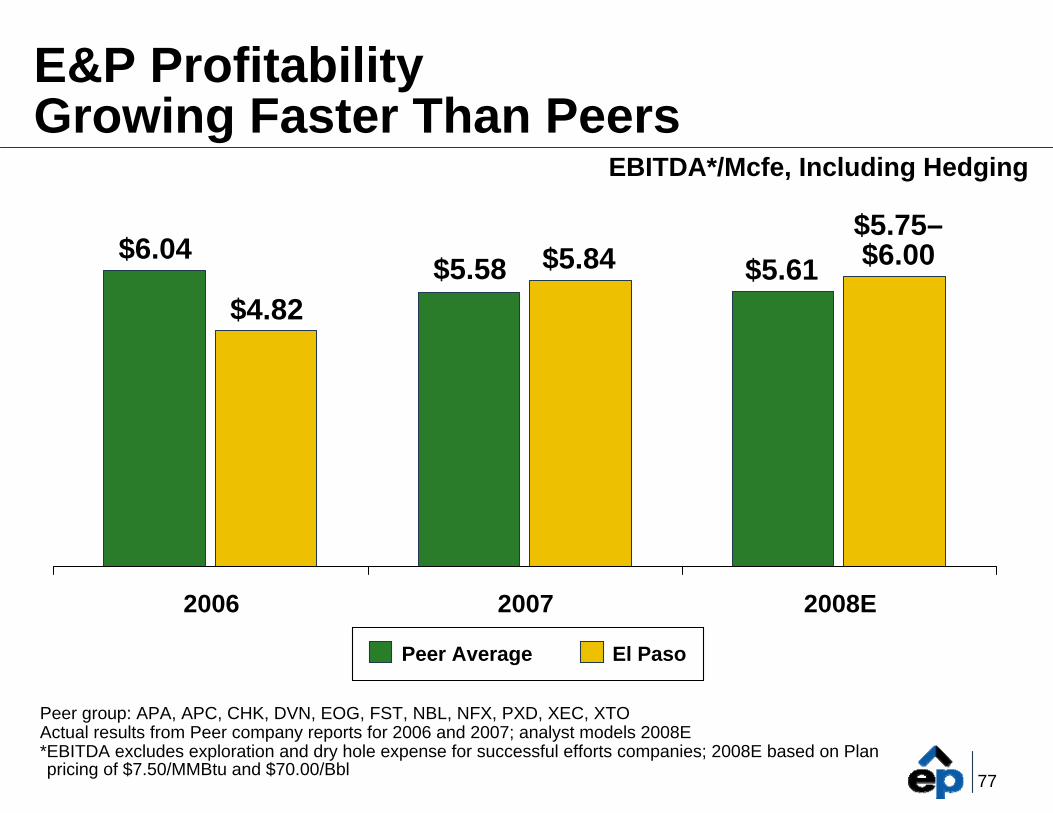

E&P ProfitabilityGrowing Faster Than Peers

$6.04

$4.82$5.58 $5.84

$5.75–$6.00

Peer group: APA, APC, CHK, DVN, EOG, FST, NBL, NFX, PXD, XEC, XTOActual results from Peer company reports for 2006 and 2007; analyst models 2008E*EBITDA excludes exploration and dry hole expense for successful efforts companies; 2008E based on Plan pricing of $7.50/MMBtu and $70.00/Bbl

$5.61

Peer Average El Paso

EBITDA*/Mcfe, Including Hedging

78

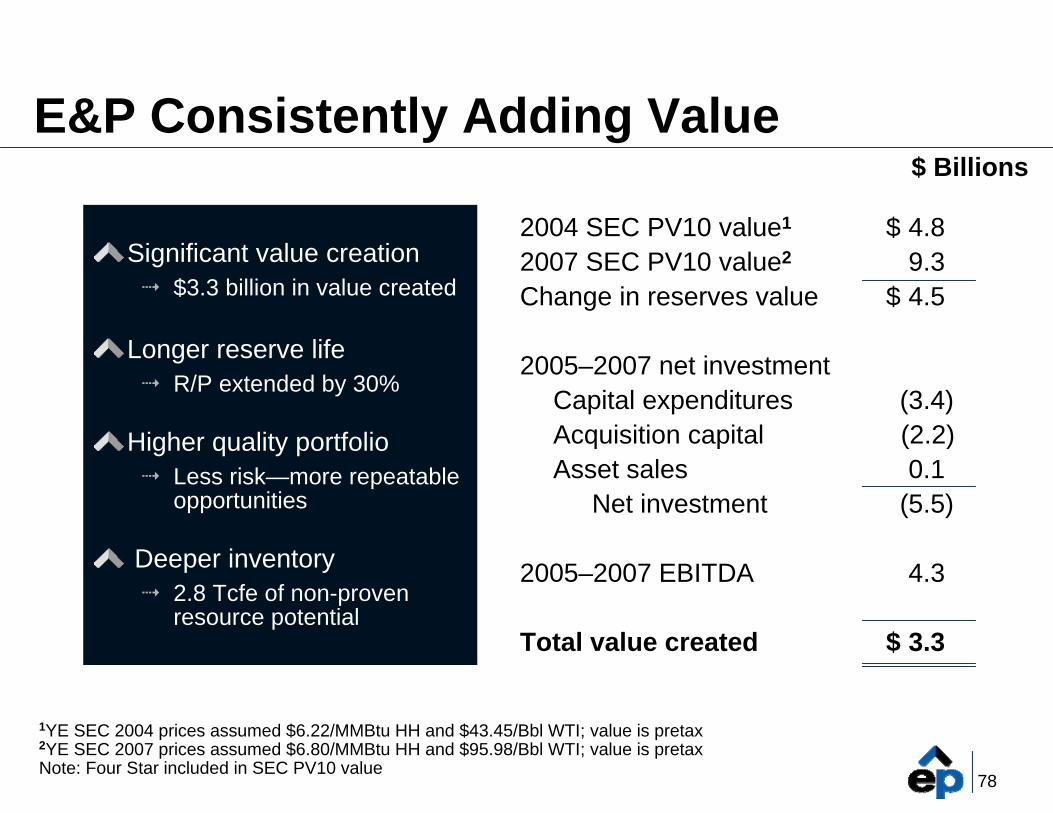

E&P Consistently Adding Value

Significant value creation$3.3 billion in value created

Longer reserve lifeR/P extended by 30%

Higher quality portfolioLess risk—more repeatable opportunities

Deeper inventory 2.8 Tcfe of non-proven resource potential

1YE SEC 2004 prices assumed $6.22/MMBtu HH and $43.45/Bbl WTI; value is pretax2YE SEC 2007 prices assumed $6.80/MMBtu HH and $95.98/Bbl WTI; value is pretaxNote: Four Star included in SEC PV10 value

2004 SEC PV10 value1

2007 SEC PV10 value2

Change in reserves value

2005–2007 net investmentCapital expendituresAcquisition capitalAsset sales

Net investment

2005–2007 EBITDA

Total value created

$ 4.89.3

$ 4.5

(3.4)(2.2)0.1

(5.5)

4.3

$ 3.3

$ Billions

79

El Paso Will Become a “Top-Tier” Performer

Performance is steadily improving

Growth strategy is rational and aligned with competencies

Significantly improved portfolio

Project inventory is high-quality and growing

Highly competent workforce

80

Program Review

81

Program Assumptions

Highlighted programs cover 85% of 2008 capitalProgram statistics are pro forma to exclude production from properties divested in 2008; includes a full year from PeoplesInventory

Locations are on gross basisResource potential is net to El PasoResource includes proved undeveloped reservesDoes not include value upside including infill drilling

EconomicsReturns assume $7.50/MMBtu Henry Hub and $70.00/Bbl WTIF&D costs = drilling and completion costsRate of return and PVR are risked; net to El Paso

82

Onshore

83

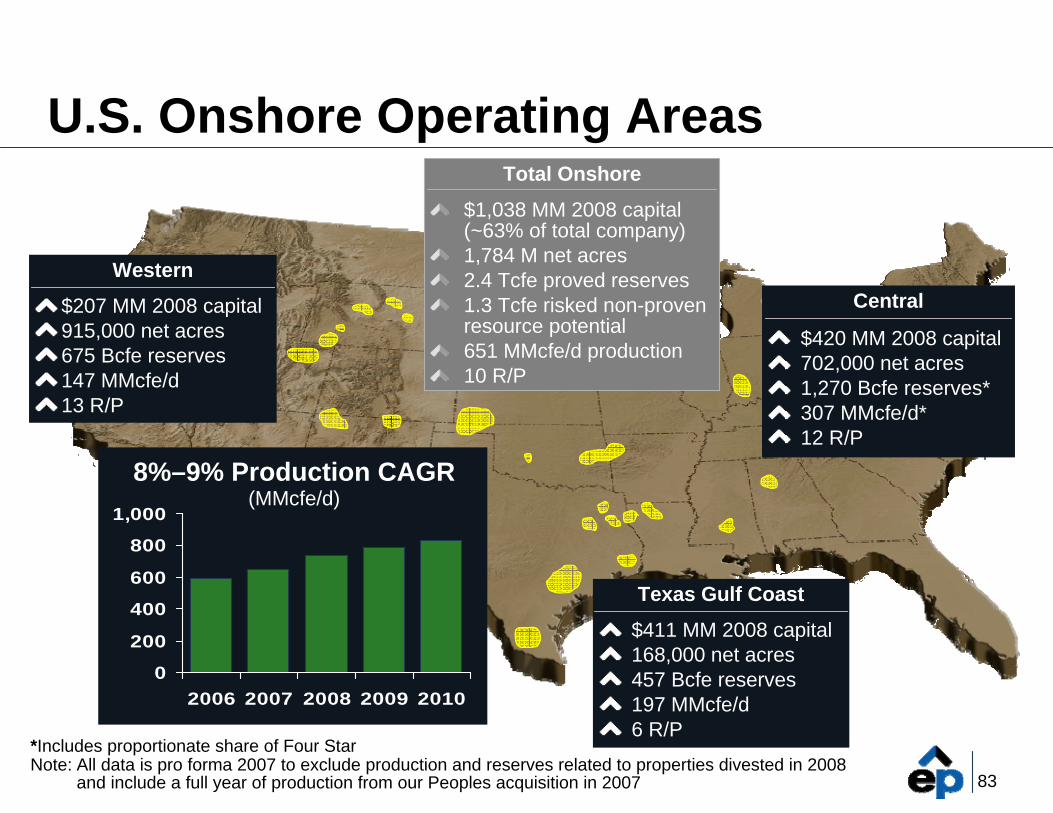

U.S. Onshore Operating Areas

Western

$207 MM 2008 capital915,000 net acres675 Bcfe reserves147 MMcfe/d13 R/P

Texas Gulf Coast

$411 MM 2008 capital168,000 net acres457 Bcfe reserves 197 MMcfe/d6 R/P

Central

$420 MM 2008 capital702,000 net acres1,270 Bcfe reserves*307 MMcfe/d*12 R/P

*Includes proportionate share of Four StarNote: All data is pro forma 2007 to exclude production and reserves related to properties divested in 2008

and include a full year of production from our Peoples acquisition in 2007

Total Onshore

$1,038 MM 2008 capital(~63% of total company)1,784 M net acres2.4 Tcfe proved reserves1.3 Tcfe risked non-proven resource potential651 MMcfe/d production10 R/P

0

200

400

600

800

1,000

2006 2007 2008 2009 2010

8%–9% Production CAGR(MMcfe/d)

84

Onshore Characterization

Targeting repeatable, low to mid-risk programsHigh-quality, concentrated asset base

Material core positions in coal seam and tight gas Multi-year project inventoryStrong positions in resource plays

Annual capital spend of $1 billion generating EBITDA of $1.3 billion–$1.4 billionPredictable, mid-single digit production growth

85

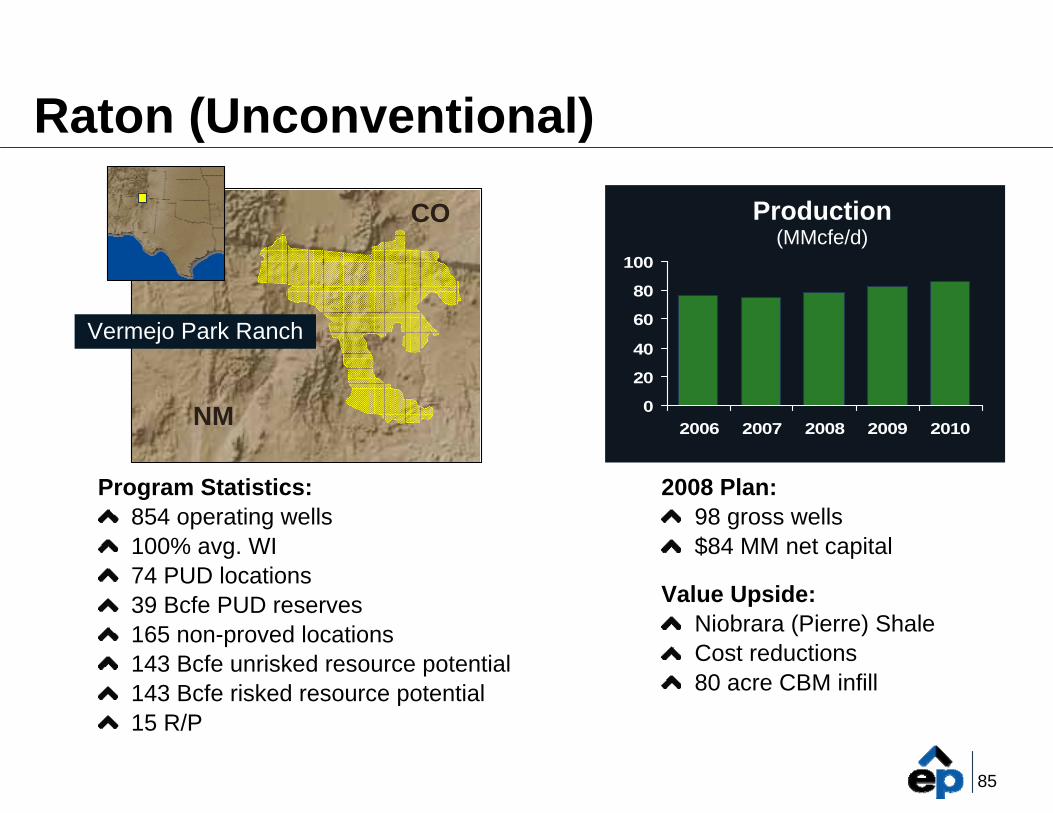

Raton (Unconventional)

Program Statistics:854 operating wells100% avg. WI74 PUD locations39 Bcfe PUD reserves165 non-proved locations143 Bcfe unrisked resource potential143 Bcfe risked resource potential15 R/P

2008 Plan:98 gross wells$84 MM net capital

Value Upside:Niobrara (Pierre) ShaleCost reductions80 acre CBM infill

0

20

40

60

80

100

2006 2007 2008 2009 2010

Production (MMcfe/d)

NM

CO

Vermejo Park Ranch

86

Raton Economics

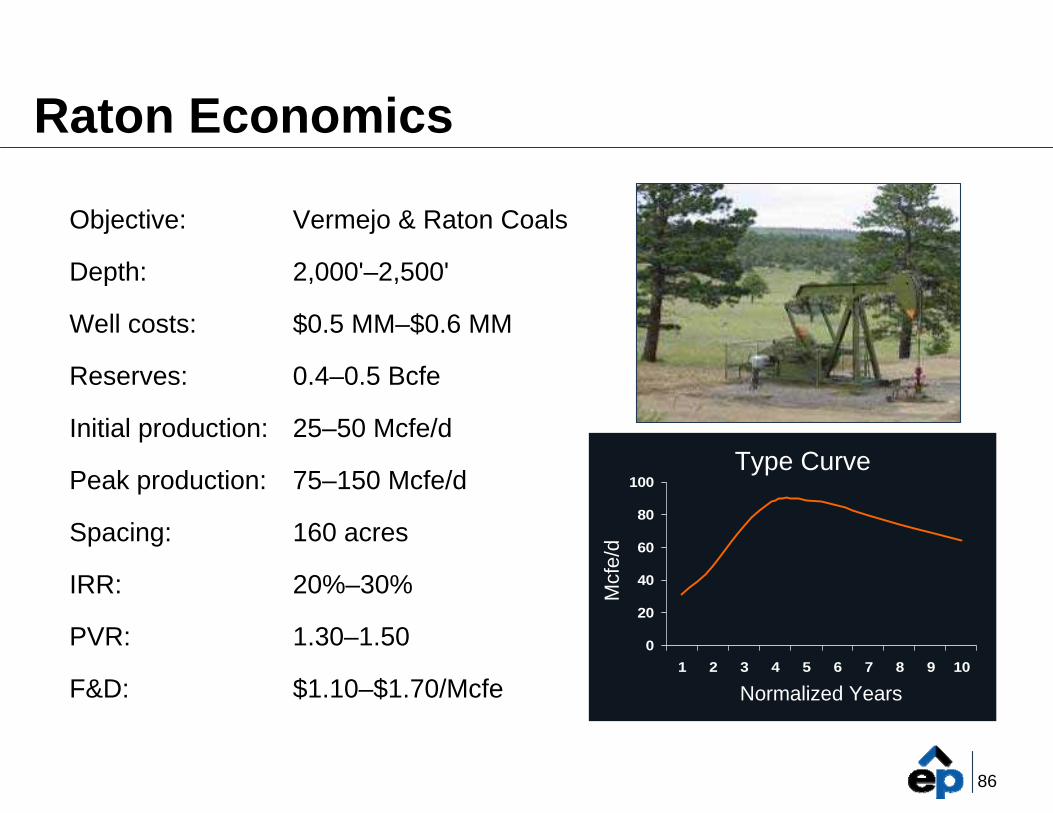

Objective:

Depth:

Well costs:

Reserves:

Initial production:

Peak production:

Spacing:

IRR:

PVR:

F&D:

Vermejo & Raton Coals

2,000'–2,500'

$0.5 MM–$0.6 MM

0.4–0.5 Bcfe

25–50 Mcfe/d

75–150 Mcfe/d

160 acres

20%–30%

1.30–1.50

$1.10–$1.70/Mcfe

0

20

40

60

80

100

1 2 3 4 5 6 7 8 9 10

Normalized Years

Mcf

e/d

Type Curve

87

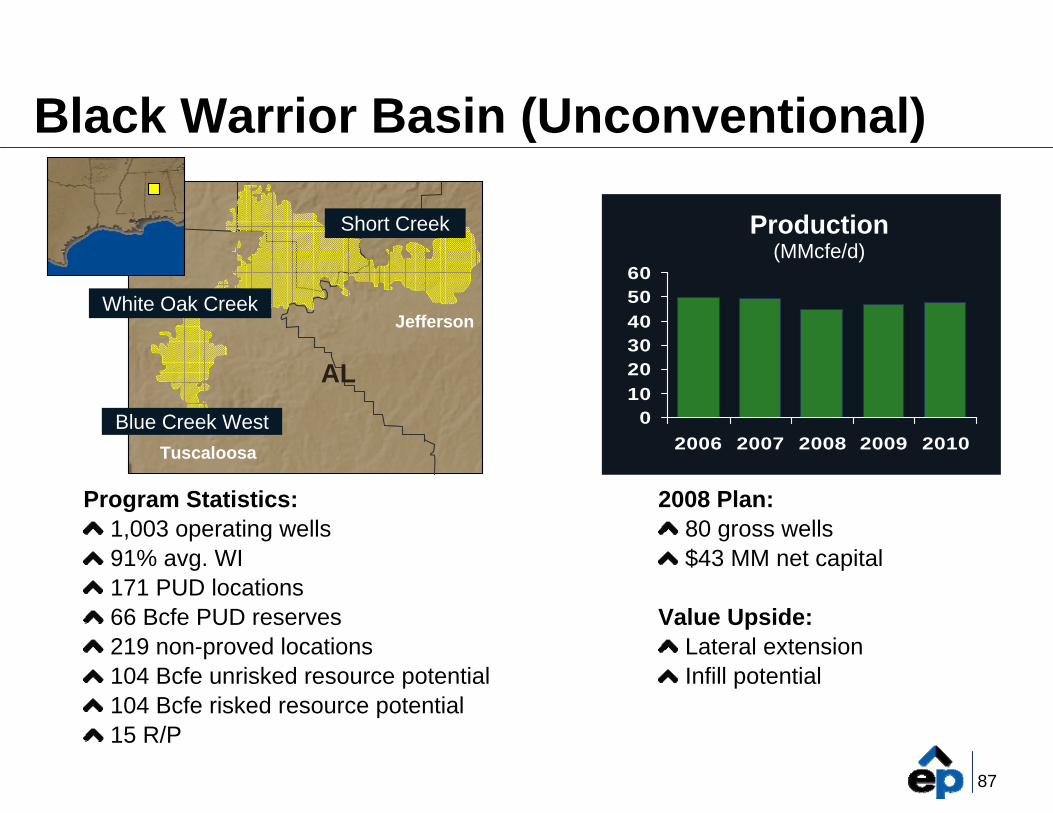

Program Statistics:1,003 operating wells91% avg. WI171 PUD locations66 Bcfe PUD reserves219 non-proved locations104 Bcfe unrisked resource potential104 Bcfe risked resource potential15 R/P

0102030405060

2006 2007 2008 2009 2010

Black Warrior Basin (Unconventional)

2008 Plan:80 gross wells$43 MM net capital

Value Upside:Lateral extensionInfill potential

Note: Excludes Brookwood

Production (MMcfe/d)

White Oak Creek

Blue Creek West

Short Creek

Jefferson

Tuscaloosa

AL

88

Normalized Years

Mcf

e/d

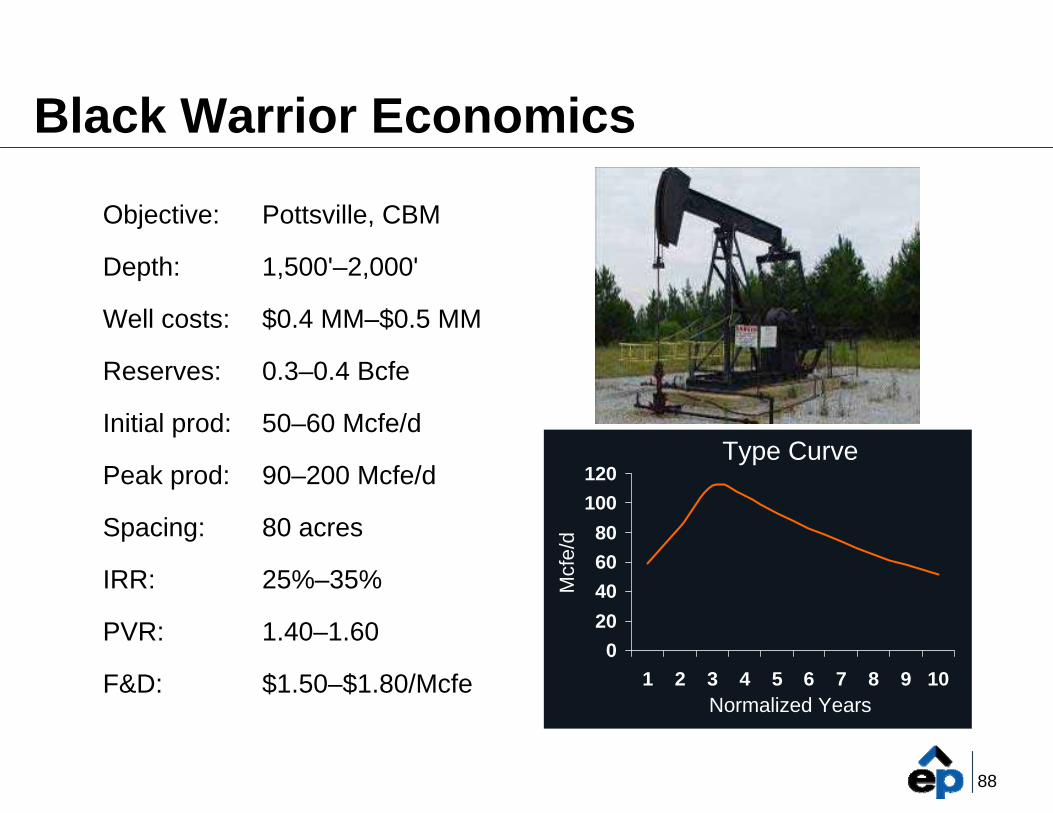

Black Warrior Economics

Objective:

Depth:

Well costs:

Reserves:

Initial prod:

Peak prod:

Spacing:

IRR:

PVR:

F&D:

Pottsville, CBM

1,500'–2,000'

$0.4 MM–$0.5 MM

0.3–0.4 Bcfe

50–60 Mcfe/d

90–200 Mcfe/d

80 acres

25%–35%

1.40–1.60

$1.50–$1.80/Mcfe

Type Curve

020406080

100120

1 2 3 4 5 6 7 8 9 10

89

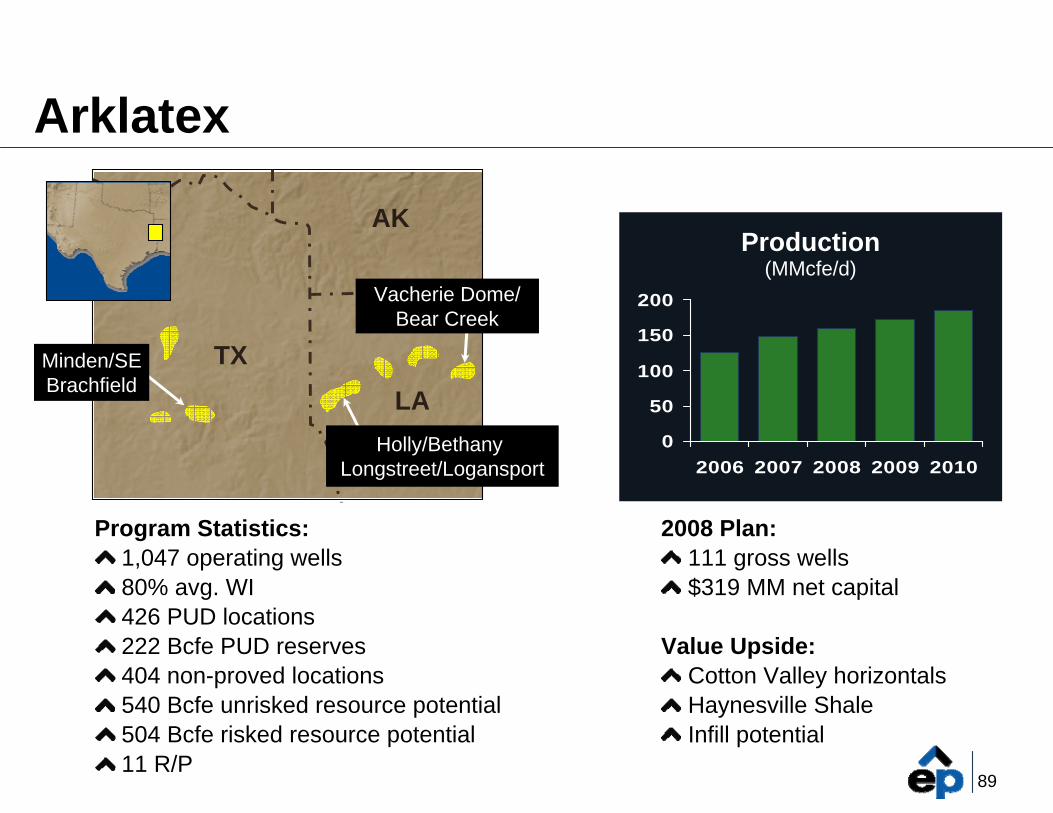

Arklatex

Program Statistics:1,047 operating wells80% avg. WI426 PUD locations222 Bcfe PUD reserves404 non-proved locations540 Bcfe unrisked resource potential504 Bcfe risked resource potential11 R/P

2008 Plan:111 gross wells$319 MM net capital

Value Upside:Cotton Valley horizontalsHaynesville ShaleInfill potential

Minden/SEBrachfield

0

50

100

150

200

2006 2007 2008 2009 2010

Production (MMcfe/d)

TX

AK

LA

Vacherie Dome/Bear Creek

Holly/Bethany Longstreet/Logansport

90

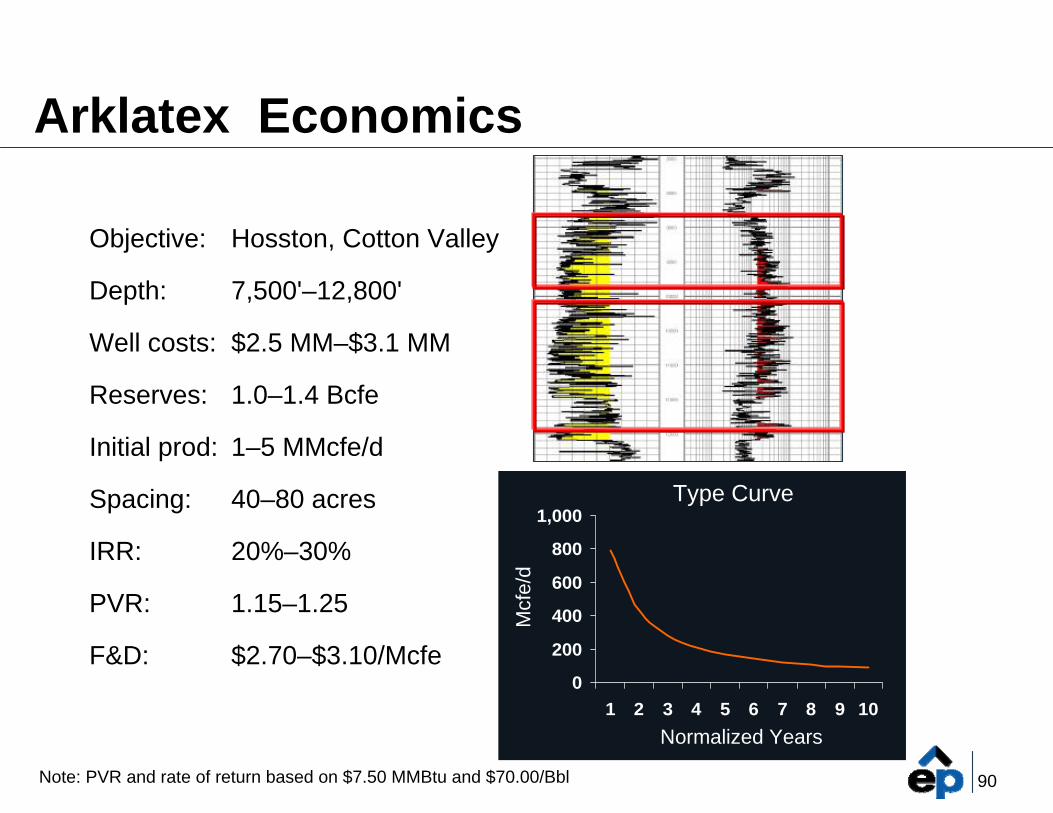

Arklatex Economics

Objective:

Depth:

Well costs:

Reserves:

Initial prod:

Spacing:

IRR:

PVR:

F&D:

Hosston, Cotton Valley

7,500'–12,800'

$2.5 MM–$3.1 MM

1.0–1.4 Bcfe

1–5 MMcfe/d

40–80 acres

20%–30%

1.15–1.25

$2.70–$3.10/Mcfe

Cotton Valley 10,500 ft.

Hosston 8,500 ft.

0

200

400

600

800

1,000

1 2 3 4 5 6 7 8 9 10

Type Curve

Normalized Years

Mcf

e/d

Note: PVR and rate of return based on $7.50 MMBtu and $70.00/Bbl

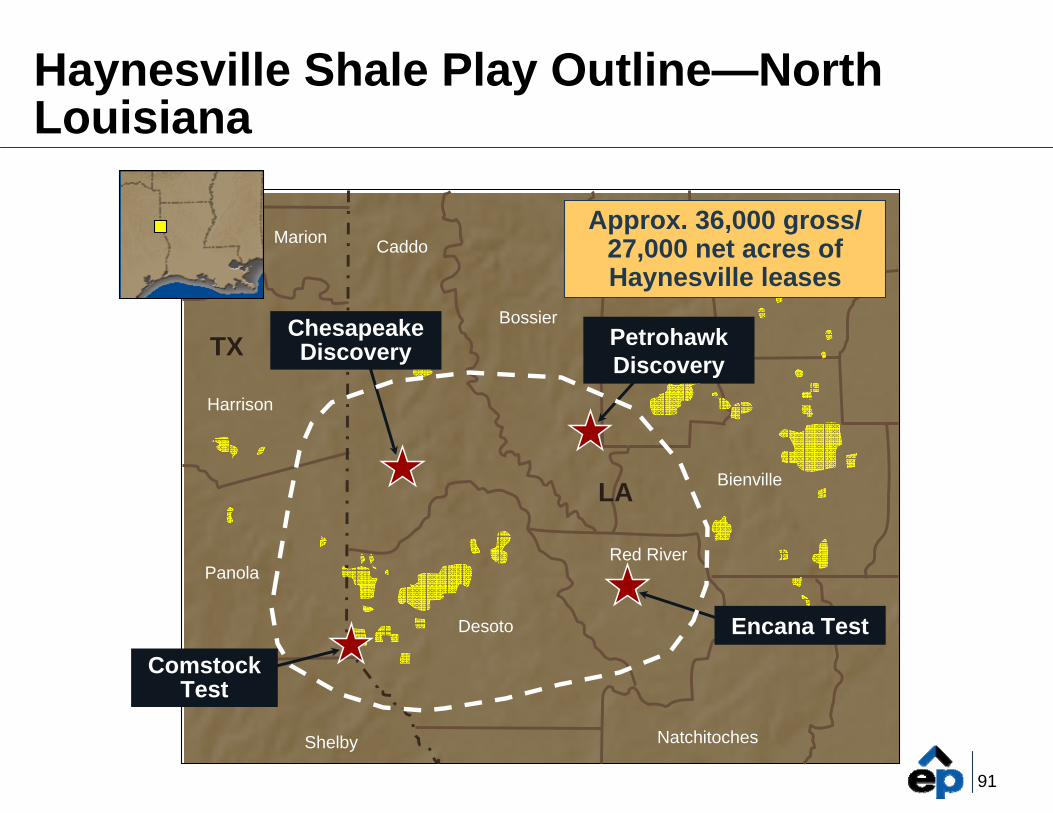

91

Haynesville Shale Play Outline—North Louisiana

Panola

Natchitoches

Marion

Bossier

Webster Claiborne

Harrison

Caddo

Shelby

Bienville

Red River

Desoto

Comstock Test

Petrohawk Discovery

Approx. 36,000 gross/ 27,000 net acres of Haynesville leases

ChesapeakeDiscovery

Encana Test

LA

TX

92

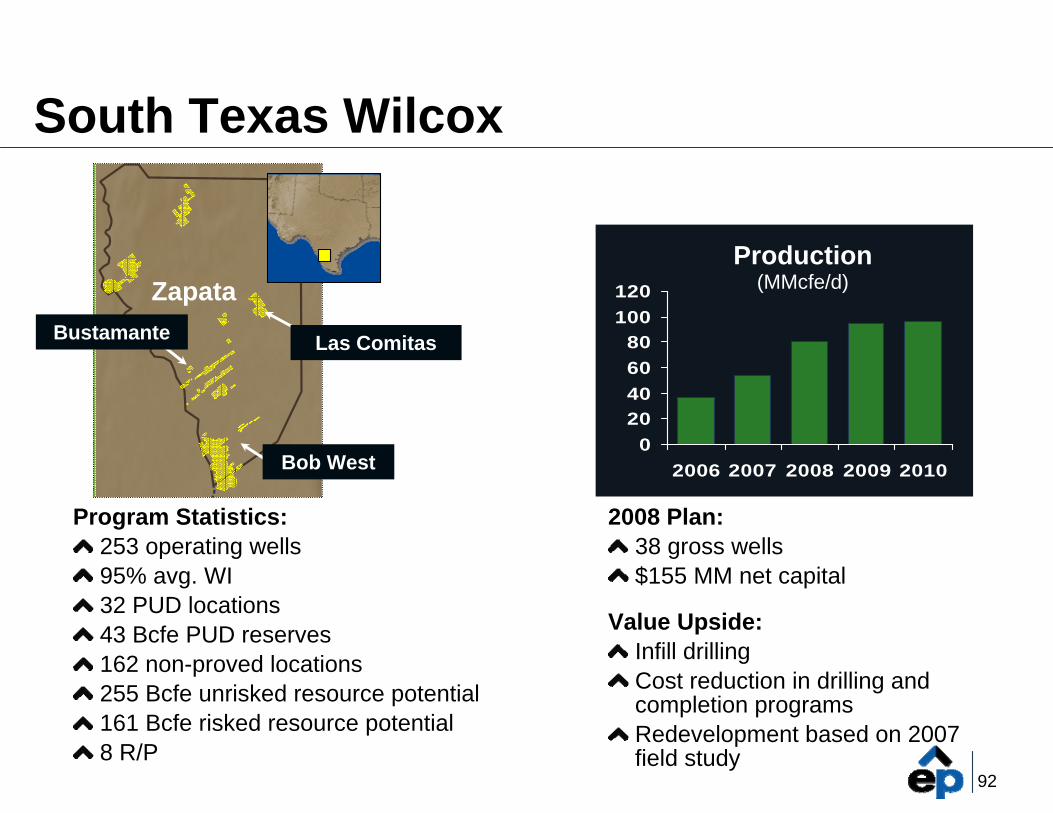

Zapata

South Texas Wilcox

Program Statistics:253 operating wells95% avg. WI32 PUD locations43 Bcfe PUD reserves162 non-proved locations255 Bcfe unrisked resource potential161 Bcfe risked resource potential8 R/P

2008 Plan:38 gross wells$155 MM net capital

Value Upside:Infill drillingCost reduction in drilling and completion programsRedevelopment based on 2007 field study

020406080

100120

2006 2007 2008 2009 2010

Production (MMcfe/d)

Las ComitasBustamante

Bob West

93

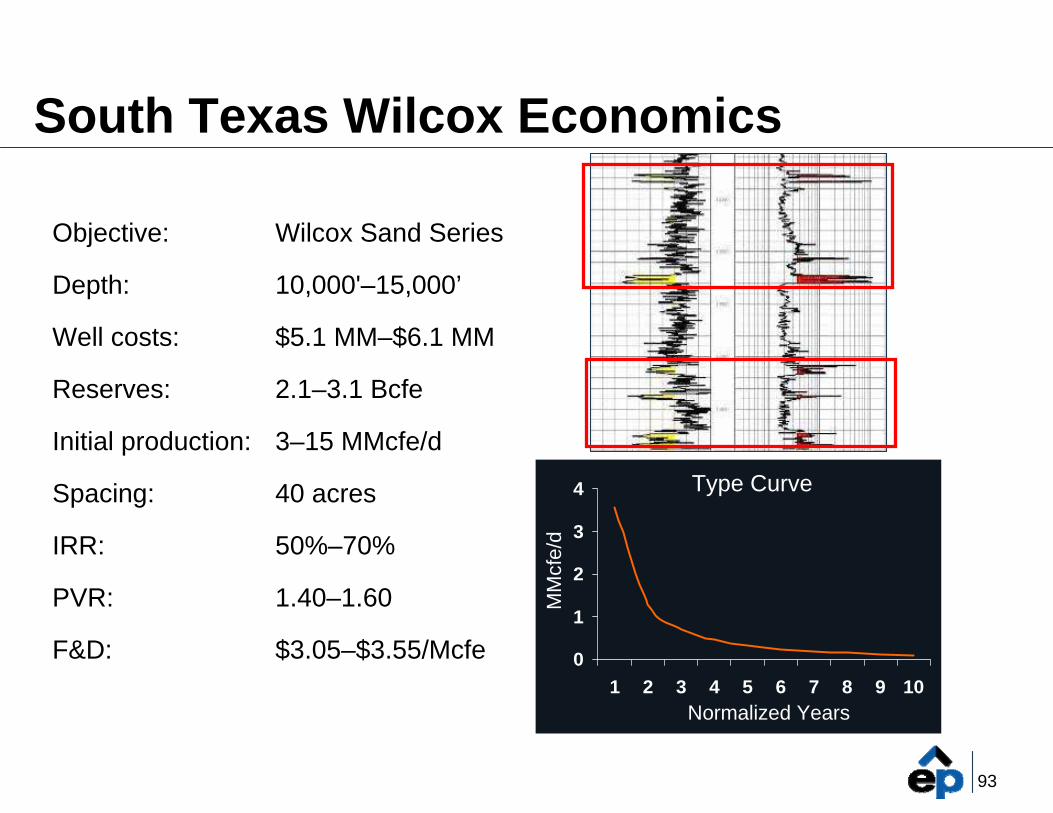

South Texas Wilcox Economics

Objective:

Depth:

Well costs:

Reserves:

Initial production:

Spacing:

IRR:

PVR:

F&D: 0

1

2

3

4

1 2 3 4 5 6 7 8 9 10

Type Curve

Wilcox Sand Series

10,000'–15,000’

$5.1 MM–$6.1 MM

2.1–3.1 Bcfe

3–15 MMcfe/d

40 acres

50%–70%

1.40–1.60

$3.05–$3.55/Mcfe

Lobo 14,000 ft.

Perdido 12,500 ft.

Normalized Years

MM

cfe/

d

94

020406080

100120

2006 2007 2008 2009 2010

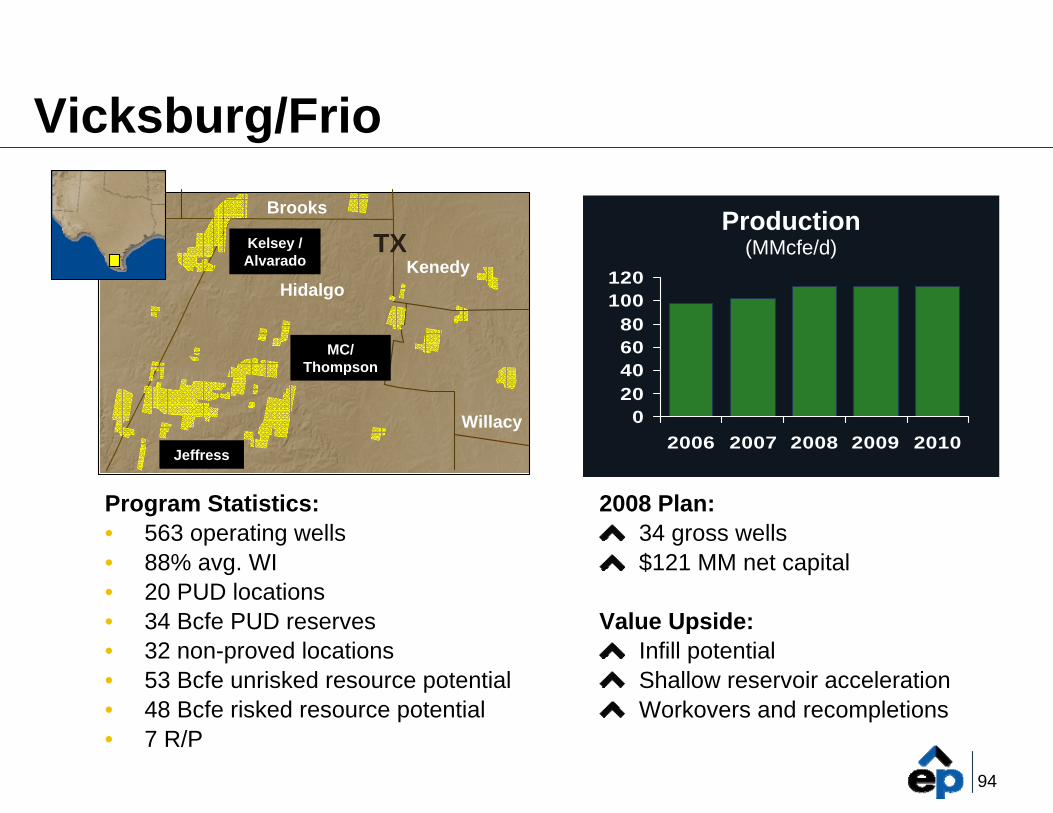

Vicksburg/Frio

Program Statistics:• 563 operating wells• 88% avg. WI• 20 PUD locations• 34 Bcfe PUD reserves• 32 non-proved locations• 53 Bcfe unrisked resource potential• 48 Bcfe risked resource potential• 7 R/P

2008 Plan:34 gross wells$121 MM net capital

Value Upside:Infill potentialShallow reservoir accelerationWorkovers and recompletions

Production (MMcfe/d)Kelsey /

Alvarado

Jeffress

MC/ Thompson

HidalgoKenedy

Willacy

Brooks

TX

95

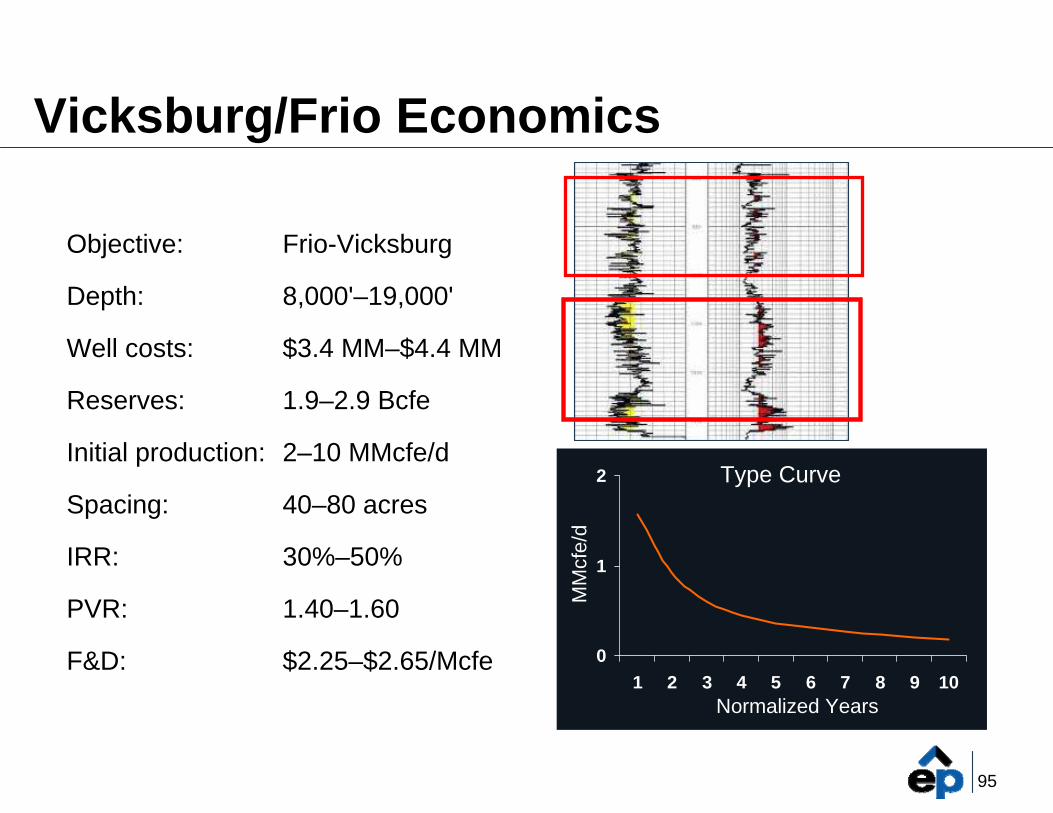

Vicksburg/Frio Economics

Objective:

Depth:

Well costs:

Reserves:

Initial production:

Spacing:

IRR:

PVR:

F&D:

Frio-Vicksburg

8,000'–19,000'

$3.4 MM–$4.4 MM

1.9–2.9 Bcfe

2–10 MMcfe/d

40–80 acres

30%–50%

1.40–1.60

$2.25–$2.65/Mcfe 0

1

2

1 2 3 4 5 6 7 8 9 10

T-Sand 13,000 ft.

S-Sand 9,000 ft.

Type Curve

Normalized Years

MM

cfe/

d

96

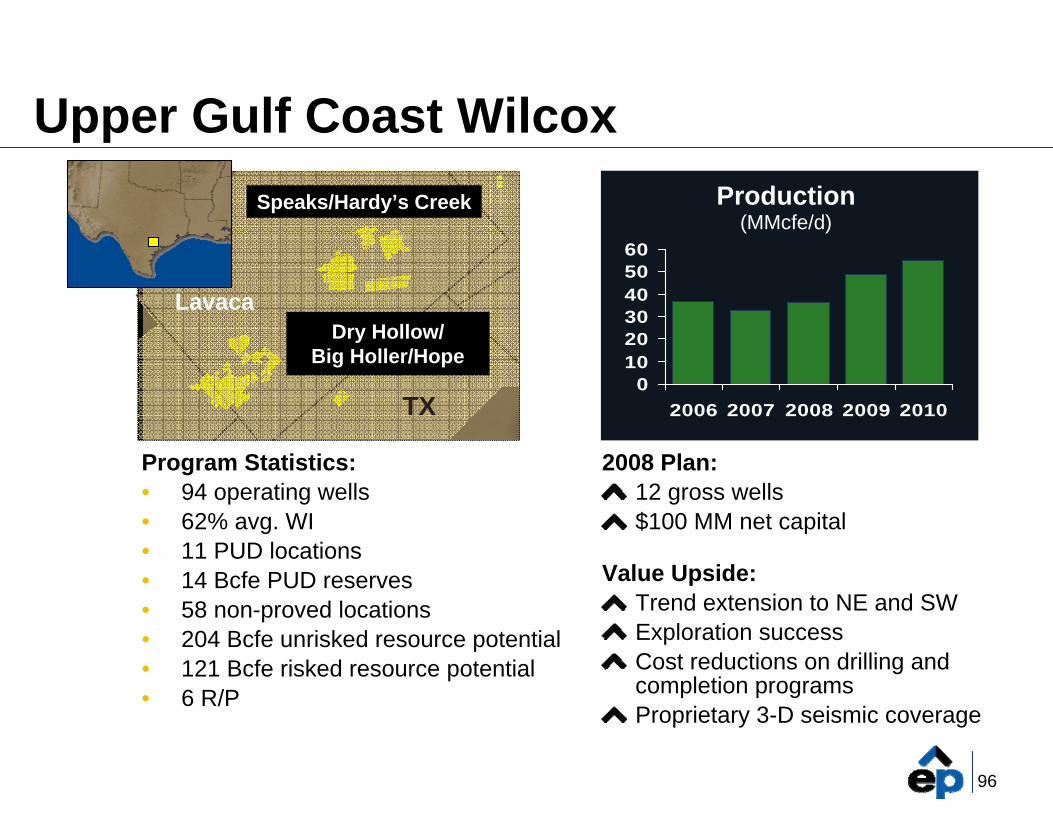

Upper Gulf Coast Wilcox

Program Statistics:• 94 operating wells• 62% avg. WI• 11 PUD locations• 14 Bcfe PUD reserves• 58 non-proved locations• 204 Bcfe unrisked resource potential• 121 Bcfe risked resource potential• 6 R/P

0102030405060

2006 2007 2008 2009 2010

2008 Plan:12 gross wells$100 MM net capital

Value Upside:Trend extension to NE and SWExploration successCost reductions on drilling and completion programsProprietary 3-D seismic coverage

Production (MMcfe/d)

Speaks/Hardy’s Creek

Dry Hollow/Big Holler/Hope

Speaks/Hardy’s Creek

LavacaDry Hollow/

Big Holler/Hope

TX

97

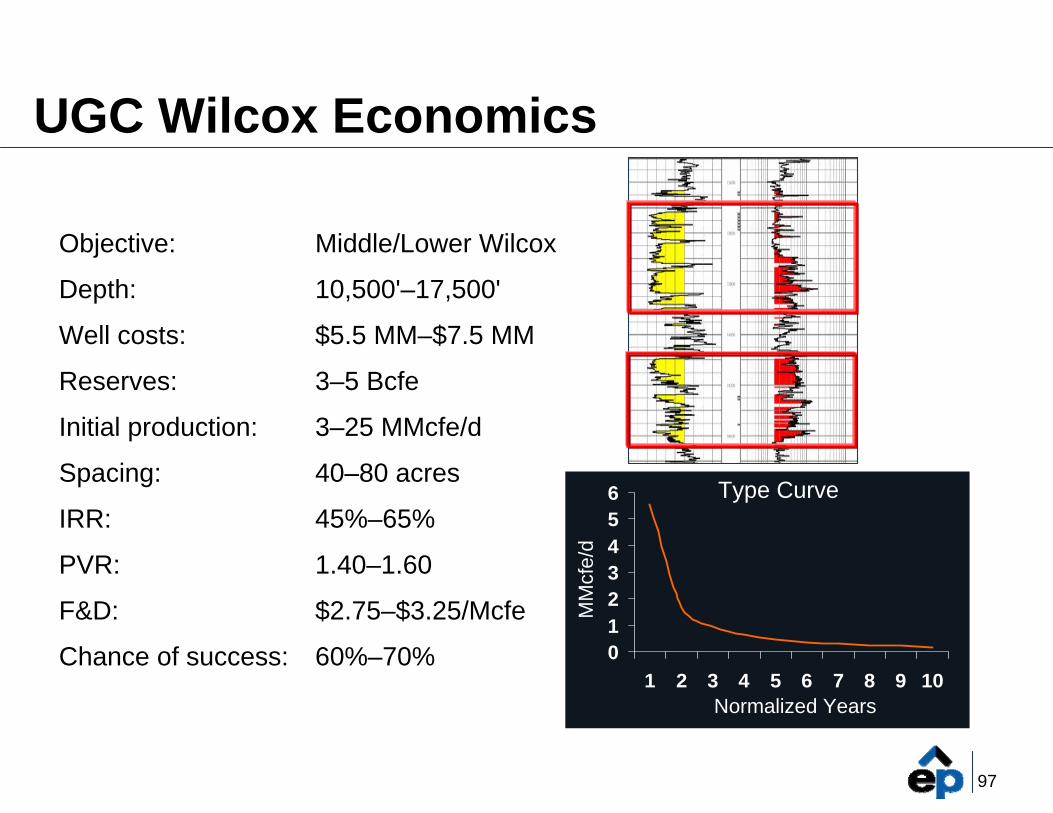

UGC Wilcox Economics

Objective:

Depth:

Well costs:

Reserves:

Initial production:

Spacing:

IRR:

PVR:

F&D:

Chance of success:

Middle/Lower Wilcox

10,500'–17,500'

$5.5 MM–$7.5 MM

3–5 Bcfe

3–25 MMcfe/d

40–80 acres

45%–65%

1.40–1.60

$2.75–$3.25/Mcfe

60%–70% 0123456

1 2 3 4 5 6 7 8 9 10

Ewers Sand 13,400 ft.

Meine Sand 14,400 ft.

Type Curve

Normalized Years

MM

cfe/

d

98

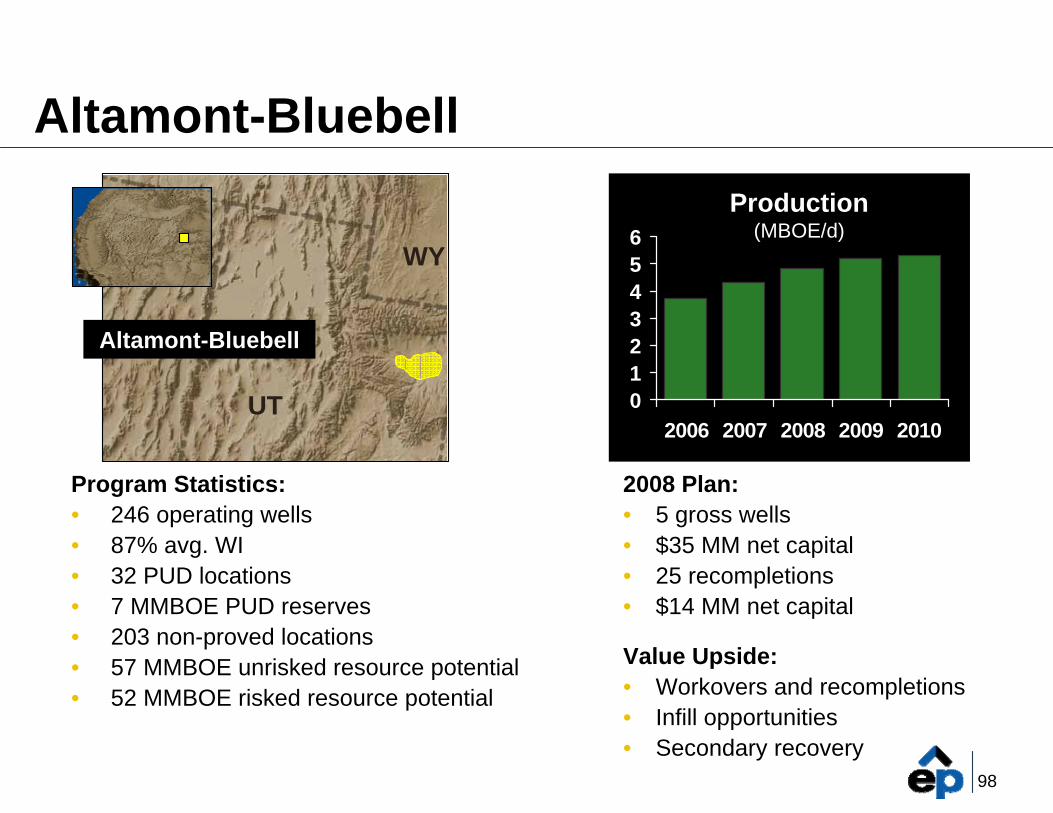

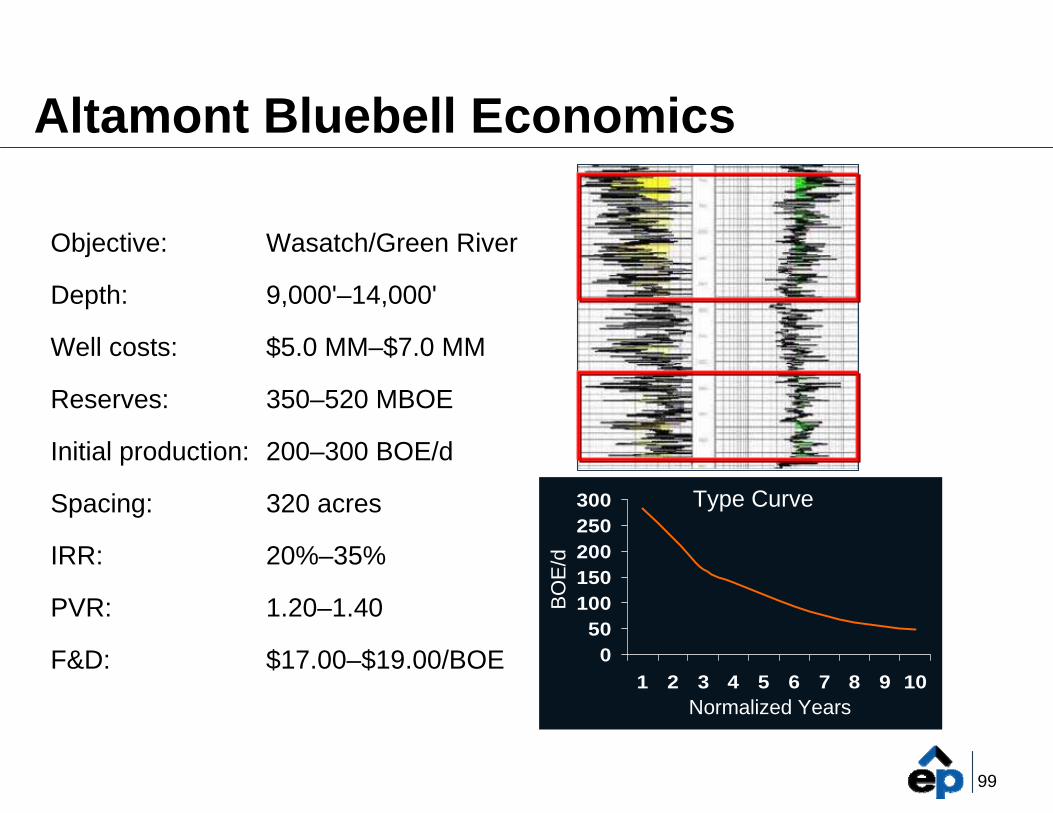

Altamont-Bluebell

Altamont-Bluebell

Program Statistics:• 246 operating wells• 87% avg. WI• 32 PUD locations• 7 MMBOE PUD reserves• 203 non-proved locations• 57 MMBOE unrisked resource potential• 52 MMBOE risked resource potential

2008 Plan:• 5 gross wells• $35 MM net capital• 25 recompletions• $14 MM net capital

Value Upside:• Workovers and recompletions• Infill opportunities• Secondary recovery

0123456

2006 2007 2008 2009 2010

Production(MBOE/d)

UT

WY

99

Type Curve

Normalized Years

Altamont Bluebell Economics

Objective:

Depth:

Well costs:

Reserves:

Initial production:

Spacing:

IRR:

PVR:

F&D:

Wasatch/Green River

9,000'–14,000'

$5.0 MM–$7.0 MM

350–520 MBOE

200–300 BOE/d

320 acres

20%–35%

1.20–1.40

$17.00–$19.00/BOE 050

100150200250300

1 2 3 4 5 6 7 8 9 10

Wasatch 9,800 ft.

Green River 7,600 ft.

BO

E/d

100

Gulf of Mexico/South Louisiana(GOM/SLA)

101

Corpus ChristiCorpus Christi

HoustonHouston

New OrleansNew OrleansLATX

Note: All data is pro forma 2007 to exclude production and reserves related to properties divested in 2008 and include a full year of production from our Peoples acquisition in 2007

Gulf of Mexico/SLA Statistics

383,000 net acres offshore21,000 net acres SLA133 MMcfe/d151 Bcfe reserves 625 Bcfe risked non-proved resource potential3 R/P

020406080

100120140

2006 2007 2008 2009 2010

Production (MMcfe/d)

GOM/SLA Position

102

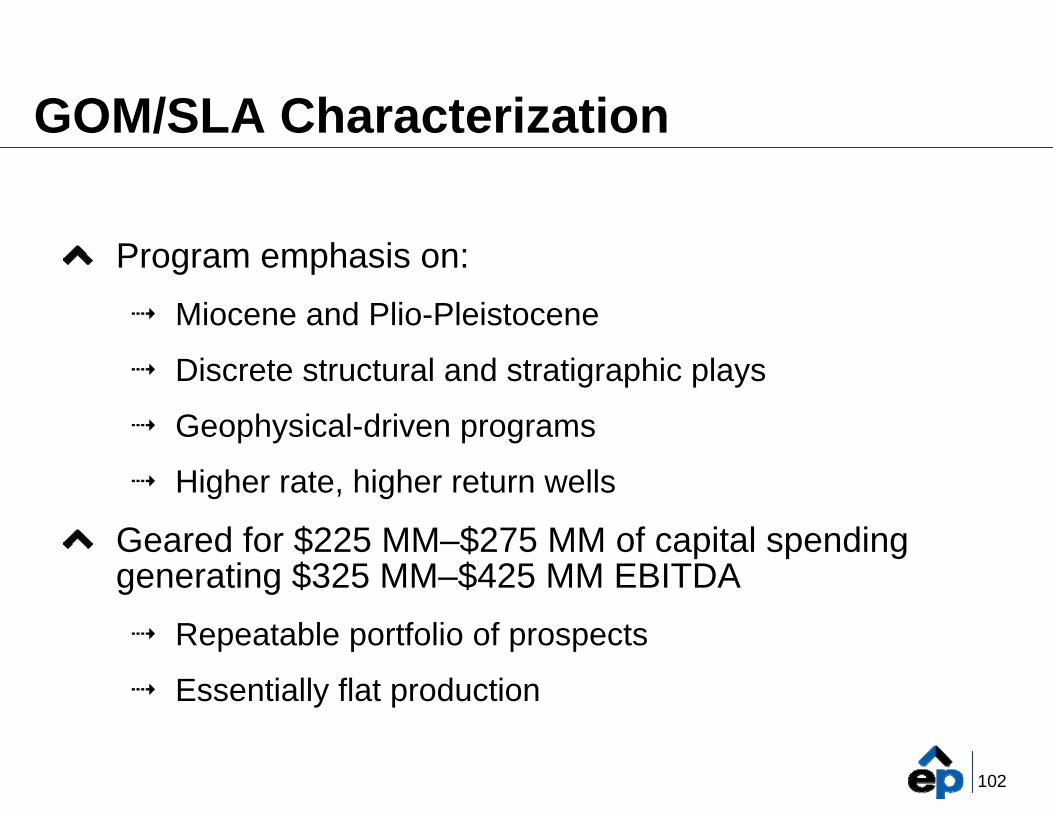

GOM/SLA Characterization

Program emphasis on:Miocene and Plio-Pleistocene

Discrete structural and stratigraphic plays

Geophysical-driven programs

Higher rate, higher return wells

Geared for $225 MM–$275 MM of capital spendinggenerating $325 MM–$425 MM EBITDA

Repeatable portfolio of prospects

Essentially flat production

103

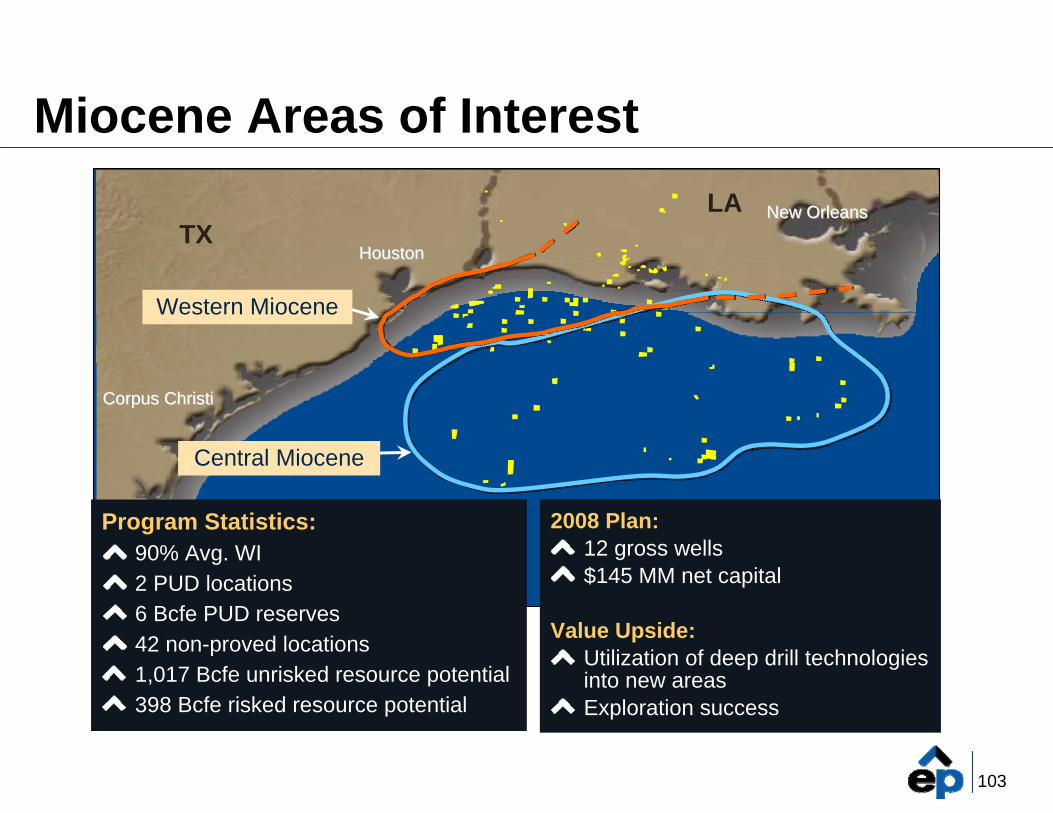

Miocene Areas of Interest

Corpus ChristiCorpus Christi

HoustonHouston

New OrleansNew Orleans

Western Miocene

Program Statistics:90% Avg. WI2 PUD locations6 Bcfe PUD reserves42 non-proved locations1,017 Bcfe unrisked resource potential398 Bcfe risked resource potential

2008 Plan:12 gross wells$145 MM net capital

Value Upside:Utilization of deep drill technologies into new areasExploration success

LATX

Central Miocene

104

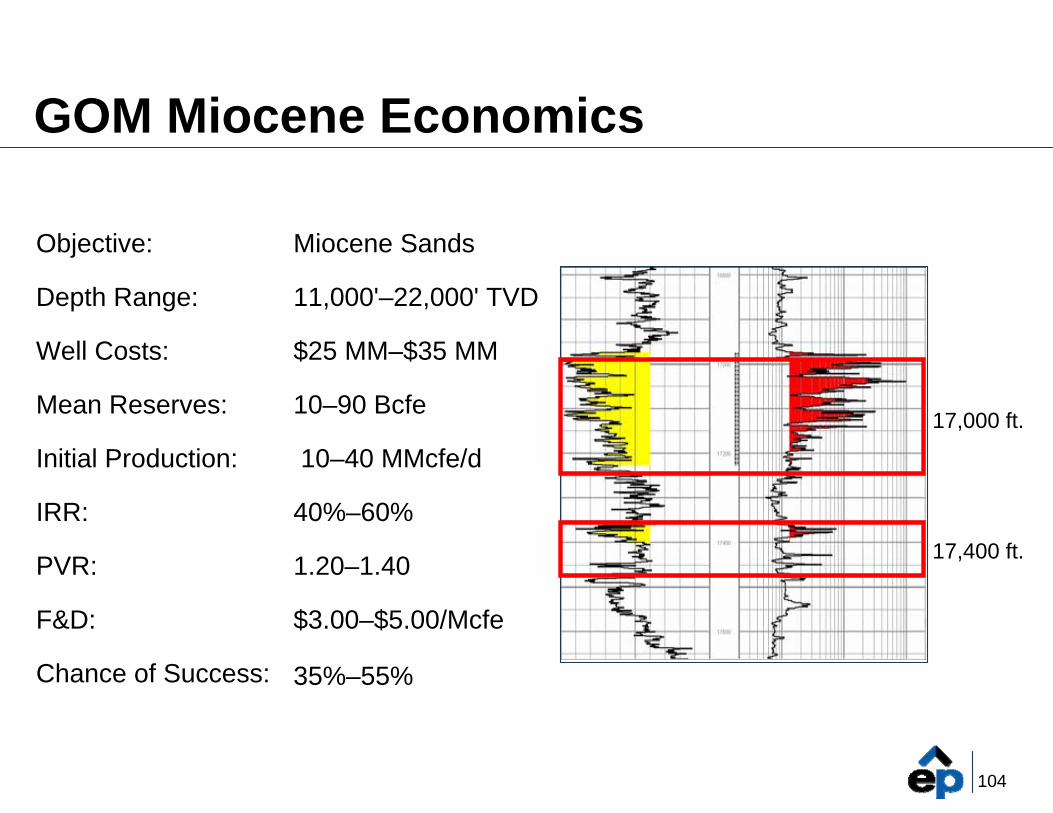

GOM Miocene Economics

Miocene Sands

11,000'–22,000' TVD

$25 MM–$35 MM

10–90 Bcfe

10–40 MMcfe/d

40%–60%

1.20–1.40

$3.00–$5.00/Mcfe

35%–55%

Objective:

Depth Range:

Well Costs:

Mean Reserves:

Initial Production:

IRR:

PVR:

F&D:

Chance of Success:

17,000 ft.

17,400 ft.

105

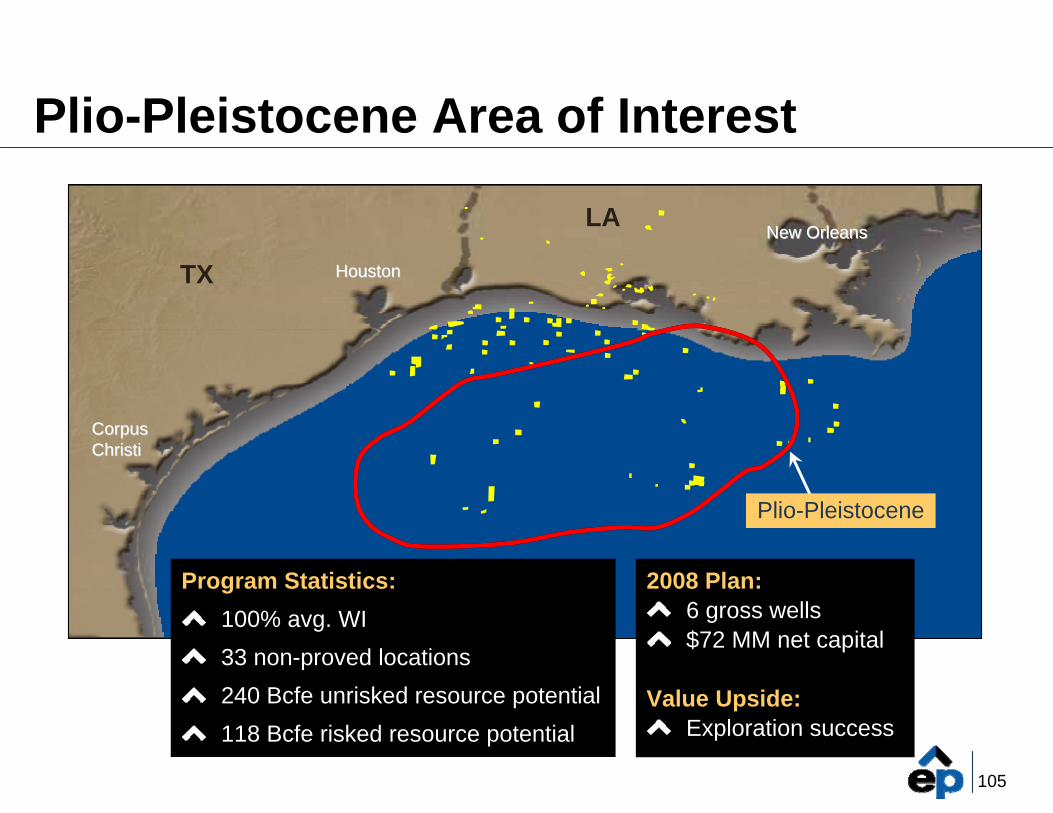

Plio-Pleistocene Area of Interest

CorpusCorpusChristiChristi

HoustonHouston

New OrleansNew Orleans

Plio-Pleistocene

Program Statistics:100% avg. WI33 non-proved locations240 Bcfe unrisked resource potential 118 Bcfe risked resource potential

2008 Plan:6 gross wells$72 MM net capital

Value Upside:Exploration success

LA

TX

106

GOM Plio-Pleistocene Economics

Plio-Pleistocene Sands

6,800'–13,500' TVD

$7 MM – $16 MM

2–12 Bcfe

2–20 MMcfe/d

50%–75%

1.4–1.6

$3.00–$4.00/Mcfe

50%–70%

Objective:

Depth Range:

Well Costs:

Mean Reserves:

Initial Production:

IRR:

PVR:

F&D:

Chance of Success:

7,000 ft.

7,600 ft.

107

International

108

International Characterization

Exploration and development opportunities inBrazil and Egypt

Bia and Pinaúna development underway (Brazil)

Risked resource potential of 1 Tcfe with more than35 prospects/leads

Up to 5 years of drilling inventory with up to 200 unrisked wells

Egypt drilling program commences 4Q 2008

Yearly capital spend of $300 MM–$350 MM overnext 3 years

Material production and reserve growth expected

109

Rio de Rio de JaneiroJaneiro

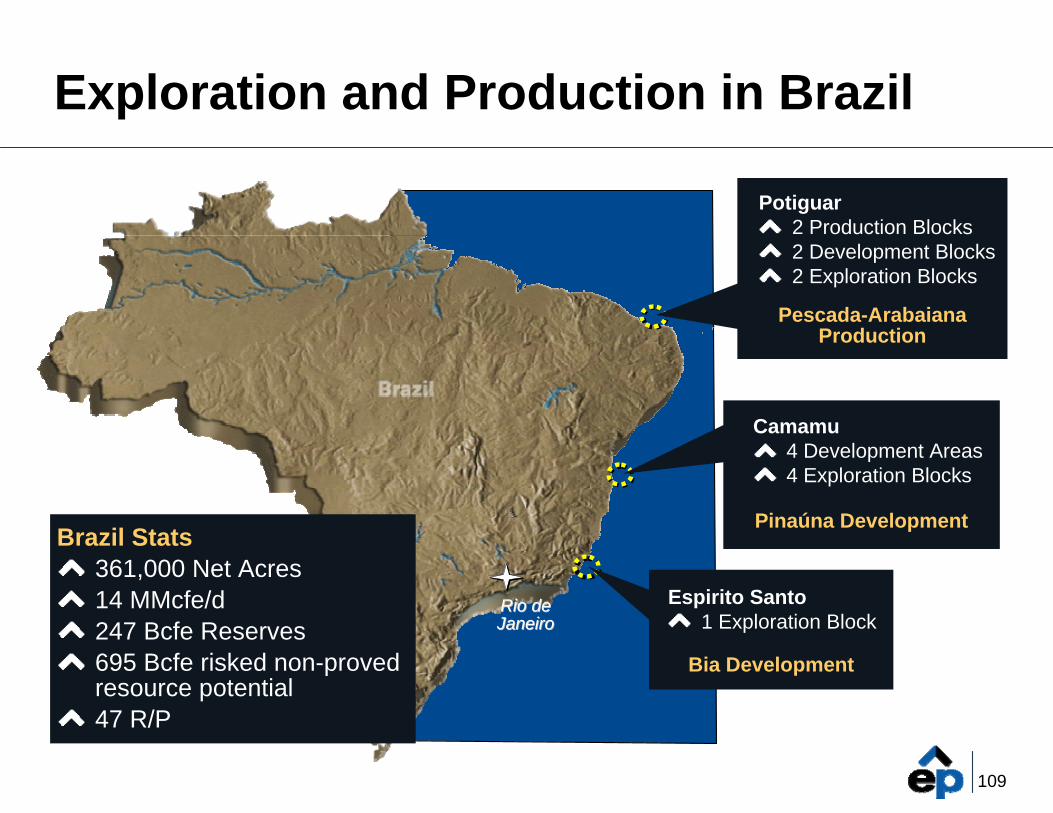

Exploration and Production in Brazil

Brazil Stats361,000 Net Acres14 MMcfe/d247 Bcfe Reserves695 Bcfe risked non-proved resource potential47 R/P

Potiguar2 Production Blocks2 Development Blocks2 Exploration Blocks

Pescada-Arabaiana Production

Camamu4 Development Areas4 Exploration Blocks

Pinaúna Development

Espirito Santo1 Exploration Block

Bia Development

110

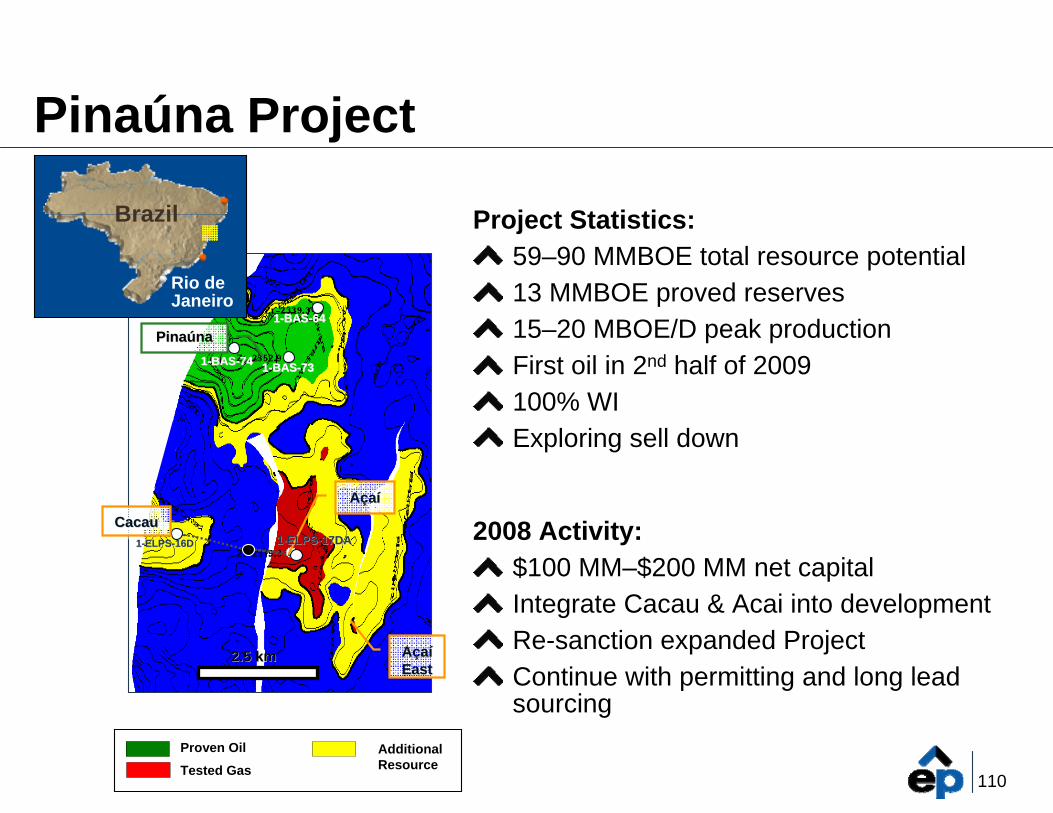

Pinaúna Project

Project Statistics:59–90 MMBOE total resource potential13 MMBOE proved reserves15–20 MBOE/D peak productionFirst oil in 2nd half of 2009100% WI Exploring sell down

2008 Activity:$100 MM–$200 MM net capitalIntegrate Cacau & Acai into developmentRe-sanction expanded ProjectContinue with permitting and long lead sourcing

11--BASBAS--737311--BASBAS--7474

11--BASBAS--6464

Resource OutlookAdditionalResource

Proven Oil

Tested Gas

2.5 km2.5 km

11--ELPSELPS--16D16D

AAççaaíí

11--ELPSELPS--17DA17DA

AAççaaííEastEast

CacauCacau

PinaPinaúúnana

Rio de Janeiro

Brazil

111

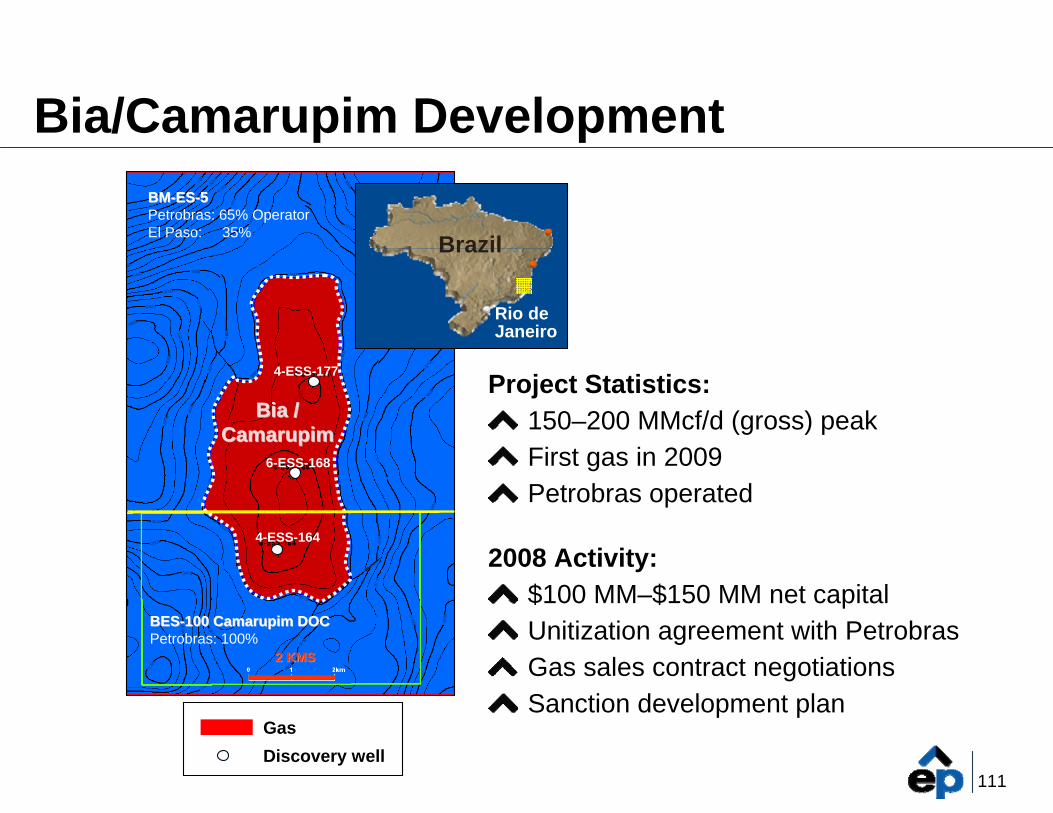

Bia/Camarupim Development

Project Statistics:150–200 MMcf/d (gross) peakFirst gas in 2009Petrobras operated

2008 Activity:$100 MM–$150 MM net capitalUnitization agreement with PetrobrasGas sales contract negotiationsSanction development plan

BESBES--100 Camarupim DOC100 Camarupim DOCPetrobras: 100%

BMBM--ESES--55Petrobras: 65% OperatorEl Paso: 35%

Gas

2 KMS2 KMS

6-ESS-168

4-ESS-164

4-ESS-177

Discovery well

Bia / Bia / CamarupimCamarupim

Rio de Janeiro

Brazil

112

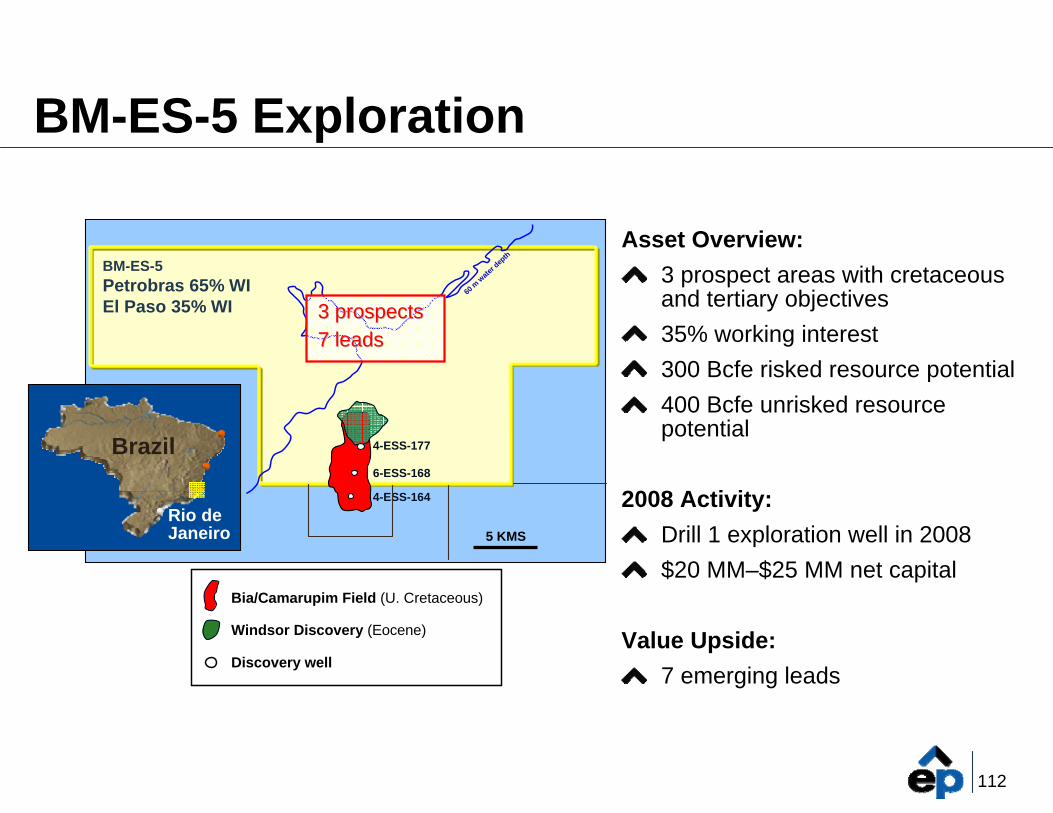

BM-ES-5 Exploration

Asset Overview:3 prospect areas with cretaceous and tertiary objectives35% working interest300 Bcfe risked resource potential400 Bcfe unrisked resource potential

2008 Activity:Drill 1 exploration well in 2008$20 MM–$25 MM net capital

Value Upside:7 emerging leads

5 KMS

60 m

wate

r dep

th

BM-ES-5Petrobras 65% WIEl Paso 35% WI

6-ESS-168

4-ESS-164

4-ESS-177

Windsor Discovery (Eocene)

Bia/Camarupim Field (U. Cretaceous)

Discovery well

Rio de Janeiro

Brazil

3 prospects3 prospects7 leads7 leads

113

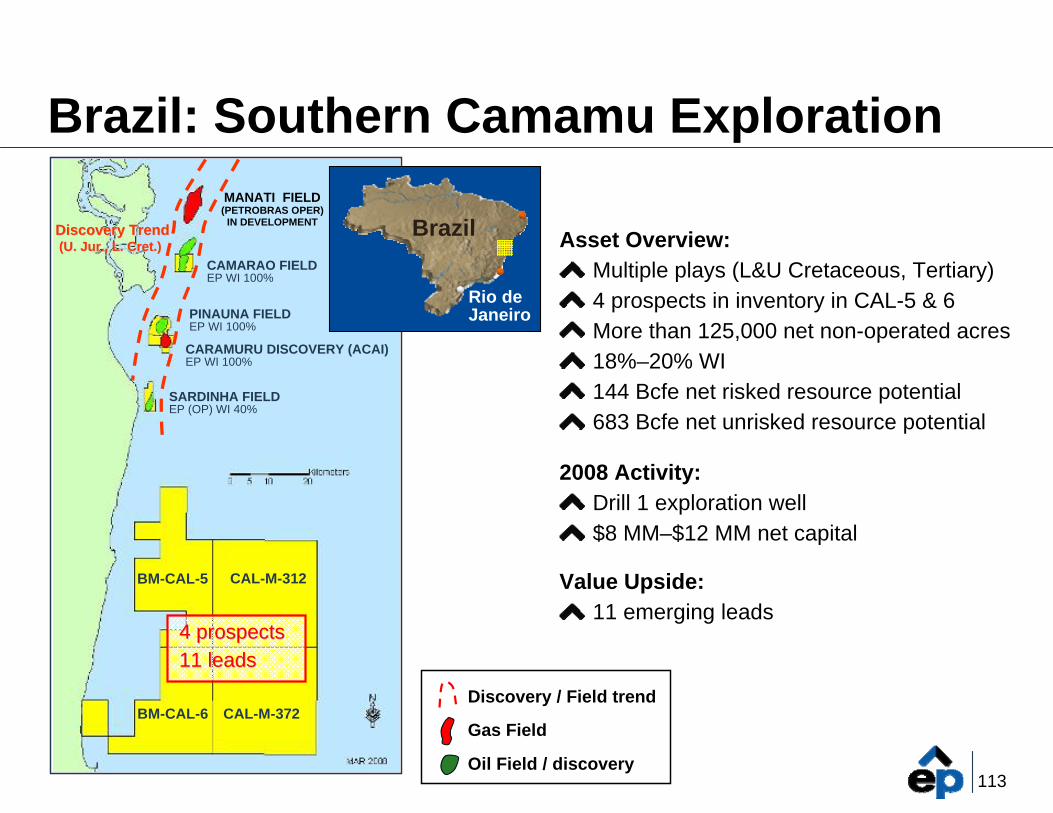

Brazil: Southern Camamu Exploration

Asset Overview:Multiple plays (L&U Cretaceous, Tertiary)4 prospects in inventory in CAL-5 & 6More than 125,000 net non-operated acres18%–20% WI144 Bcfe net risked resource potential683 Bcfe net unrisked resource potential

2008 Activity:Drill 1 exploration well$8 MM–$12 MM net capital

Value Upside:11 emerging leads

Gas Field

Oil Field / discovery

Discovery / Field trend

MANATI FIELD(PETROBRAS OPER)

IN DEVELOPMENT

CAMARAO FIELDEP WI 100%

PINAUNA FIELDEP WI 100%

SARDINHA FIELDEP (OP) WI 40%

CARAMURU DISCOVERY (ACAI)EP WI 100%

CAL-M-312

CAL-M-372

BM-CAL-5

BM-CAL-6

Discovery Trend Discovery Trend (U. Jur., L. Cret.)(U. Jur., L. Cret.)

Rio de Janeiro

Brazil

4 prospects4 prospects11 leads11 leads

114

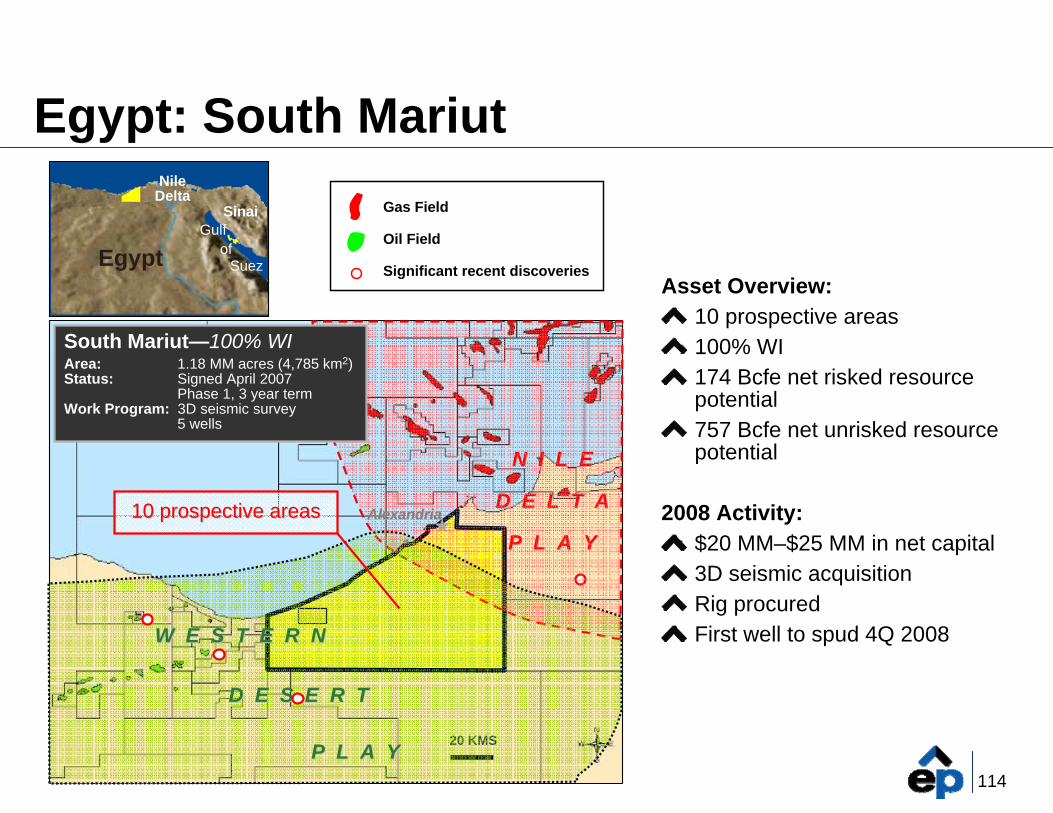

Egypt: South Mariut

Asset Overview:10 prospective areas100% WI174 Bcfe net risked resource potential757 Bcfe net unrisked resource potential

2008 Activity:$20 MM–$25 MM in net capital3D seismic acquisitionRig procuredFirst well to spud 4Q 2008

Gas Field

Oil Field

Significant recent discoveries

20 KMS

N I L E N I L E

D E L T AD E L T A

P L A Y P L A Y AlexandriaAlexandria

W E S T E R N W E S T E R N

D E S E R TD E S E R T

P L A Y P L A Y

South Mariut—100% WIArea: 1.18 MM acres (4,785 km2)Status: Signed April 2007

Phase 1, 3 year termWork Program: 3D seismic survey

5 wells

Egypt

NileDelta

Sinai

EgyptGulf

ofSuez

10 prospective areas10 prospective areas