Embed Size (px)

Citation preview

Preparing NEMS for the New Energy Market Landscape

Presented by Paul PohExecutive Vice President

Market Administration

1

Agenda

2

• Market Reform Milestones

• National Electricity Market of Singapore (NEMS)

• Lack of Investments in Other Markets

• Australia

• Europe

• What about NEMS?

Market Reform Milestones

3

May 1963Formation of Public

Utilities Board• Supplies water/electricity/gas to Singapore Mar 2000

Decision to deregulate further

Oct 1995Corporatisation of

electricity/gas

Apr 1998Formation of Singapore Electricity Pool (SEP)

Holding Company (Singapore Power)• 2 gencos (Power Senoko, Power

Seraya)• 1 T&D company (PowerGrid)• 1 electricity retail company (Power

Supply)• 1 gas supply company (PowerGas)

Temasek Holdings

•1 genco (Tuas Power)

Apr 2001Further restructuring

• PUB restructured as water authority under MEWR

• EMA to regulate electricity and gas industries

• PSO to take over system operations• EMC formed to operate and administer

wholesale electricity market

Market Reform Milestones

4

Jan 2003Commencement of NEMS• Real-time wholesale

market for electricity• Phased contestability of

consumers

2008Sale of Gencos

May 2013LNG terminal

began operation

• Mar - Tuas sold to Huaneng Group

• Oct - Senoko Power sold to Lion Power

• Dec - Power Serayasold to YTL Power

Jun 2015Launch of Electricity

Futures Market • USEP Quarterly

Base Load futures

Jan 2004• Implementation of

Vesting Contracts• Implementation of

Interruptible Load

Apr 2016Implementation of Demand Response

Programme

5

Industry Stakeholders

6

Regulator (EMA)

System Operator

(PSO)

MarketOperator

(EMC)

MSSL(SP Services)

Generators

SP PowerAssets

• Sembcorp Cogen• NEA• Keppel Merlimau Cogen• Senoko WTE

• Shell Eastern Petroleum• Keppel Seghers Tuas WTE• ExxonMobil Asia Pacific• PacificLight Power

• YTL PowerSeraya• Tuaspring• TP Utilities• Singapore Refining Company

Wholesale Traders Electricity Retailers• Diamond Energy

Managers• Pfizer Asia Pacific• MSD International

GmbH• Banyan Utilities• Green Power Asia• Singapore LNG• GSK• ECO Special Waste

Management

• CGNPC• Sunseap Leasing• LYS Genco Beta• Solar C&I• Singapore District Cooling• Nanyang Technological

University• GreenSync Holdings• Sun Electric Energy Assets• Air Liquide Singapore• Changi Mega Solar

• Keppel Electric• Sembcorp Power• Senoko Energy Supply• Seraya Energy• Tuas Power Supply• Diamond Energy

Merchants• PacificLight Energy• Hyflux Energy• Red Dot Power• Buri Energy

• Sun Electric Power• Sunseap Energy• Best Electricity Supply• I Switch• Charis Electric• Environmental Solutions• Union Power• Just Electric• Cleantech Solar Management• Energy Supply Solutions

Non-Contestable Consumers Contestable Consumers

Products Traded

• Real-time spot market (half-hourly trading intervals)

• Energy

• 3 classes of reserves (can be provided by gencos and load)• Primary (8-second)• Secondary (30-second)• Contingency (10-minute)

• Regulation

• Procured contracts (annually)• Black-start ancillary services

7

Location Map of NEMS Generators (Existing & Upcoming, excluding EG)

Electricity interconnectionwith Malaysia

Keppel Cogen

▲ Represents incineration plants

Note: The Locations indicated on this map have been approximated and stylised. They do not accurately represent the actual physical location of individual facilities

Embedded generators and small generators (below 10MW) are not depicted in this map.

Senoko Energy

Tuas PowerGeneration PowerSeraya

SembCorp

Natural gas pipelinefrom Malaysia

Natural gas pipeline from(West Natuna)

Natural gas pipeline fromSumatra (Asamera)

PacificLight

LNG Terminal

▲ ▲▲

▲

TuaspringExxonMobil

Shell

SRC

8

Objectives• Promote competition • Efficient prices to guide investment, production and consumption

decisions

Market structure• Relatively concentrated market with a high degree of vertical

integration in generation and retail

• Vesting contracts in place to mitigate market power

Consumers• Retailers charged at Uniform Singapore Energy Price (USEP)

• Contestable consumers – buy from retailers/ MSSL (at spot prices)

• Non-contestable consumers – buy from MSSL at a regulated electricity tariff

Features of NEMS

9

Mandatory Energy-Only Real-Time Gross Pool• Spot market for 5 products - energy, 3 types of reserves and

regulation

• ½ hourly trading periods with 65 minute gate-closure

• Supply offer market with interruptible load and demand bidding being demand-side participation

• Market settled daily (20 days in arrears)

Dispatch of electricity• Market clearing engine: co-optimisation of energy, reserves and

regulation, modeling of power flows

• Locational marginal pricing, with about 860 nodes

Features of NEMS

10

Lack of Investments in Other Markets

11

Australia National Electricity Market

12

13

Annual Average Prices

• The Australia NEM has high wholesale electricity prices since 2016

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

NSW1 QLD1 SA1 TAS1 VIC1

Annual average prices by region (AU$/MWh)

2011

2012

2013

2014

2015

2016

2017

14

Electricity Prices

• Australian Energy Market Commission expects Wholesalepower costs to rise between 5% and 15% each year until2019

• Average electricity bills have more than doubled over thepast decade to about $2,020 a household, making electricitythe fastest rising household expense

15

High Electricity Prices

Issues with renewables

• Decline in traditional generation (i.e. coal-fired power plants)• Limited management of renewable energy’s intermittency• Traditional sources of energy are pertinent when renewable generation

dips• Renewables do not have characteristics to support and stabilise the

electricity system

16

High Electricity Prices

High domestic gas price

• 3 massive new LNG terminals at Gladstone contracted to supply Asiawith gas

• Exporters struggle to fulfil contracted orders written years ago - Raidgas from the domestic market to meet their contracts

• Suppliers took advantage to raise prices and place onerous conditionson buyers

• Lack of financial incentive for landowner hampers development of newgas fields to increase domestic supply

High Electricity Prices

Constrained Interconnectors

• Reliant on the Basslink interconnectorfrom Victoria

• E.g. In December 2015 (faultyinterconnector)• Tasmania could not generate

sufficient hydro power• Necessary to restart a closed gas-

fired power station and commissionemergency diesel generators

Basslink Interconnector• High penetration of wind/solar

generators led to closures ofsynchronous generators

• Became very reliant on importingenergy from Victoria

• The interconnector is required to keepthe system frequency in balance

Heywood Interconnector

17

High Electricity Prices

Issues with renewables

High domestic gas price

Constrained Interconnectors

High WholesaleElectricity Prices

Provideinvestment signal

However, investment in generation is still low! !

18

19

Lack of Generation Investment

Uncertainty of government policies

• Policy instability and uncertainty driven by numerous reviews into therenewable energy target and a lack of clarity about the policies toreduce emissions after 2020

• Overlapping renewable energy (emissions reductions) targets at thestate and federal levels

• Carbon policy indecision led to uncertainties in investment of newpower generation

20

Closure of Coal-Fired Plants

WA

NT

SA

QLD

NSW

VIC

TAS

NORTHERN

240MWClosed 2016

PLAYFORD B

240MWClosed 2012

ANGLESEA

150MWClosed 2015

MORWELL

165MWClosed 2014 HAZELWOOD

1600MWClosed 2017

WALLERAWANG1000MWClosed 2014

MUNMORAH

600MWClosed 2012

REDBANK

151MWClosed 2014

SWANBANK B

480MWClosed 2012

COLLINSVILLE

190MWClosed 2012

21

Lack of Generation Investment

Uncertainty of domestic gas prices

• Uncertainty as to whether sufficient gas will be available to meet futuredomestic demand. This is due to supplies being diverted to meetinternational LNG supply contracts.

• Low levels of exploration, restrictions on onshore exploration andinfrastructure constraints resulted in uncertainty in domestic gas supply,which ultimately creates uncertainty for investment in new powergenerations

22

Australia Energy Plan

Future Energy Plan

South Australia

In March 2017, the state government unveiled AUD550 million power plan• Build a state-owned – 250MW gas-fired power station for emergencies• Support building the nation’s largest battery to store renewal energy• Encourage the construction of a new privately-owned power station by

tendering 75% of State Government electricity over next 10 years• Giving the state energy minister powers to direct generators to operate

and NEM to control flows on the interconnector

23

Australia Energy Plan

Future Energy Plan

Australia NEM

In June 2017:• Australia’s chief scientist Dr Alan Finkel made 50 recommendations to

improve the NEM• Federal Government has agreed to 49 of the recommendations• Except for the Clean Energy target recommendation

Europe Electricity Markets

24

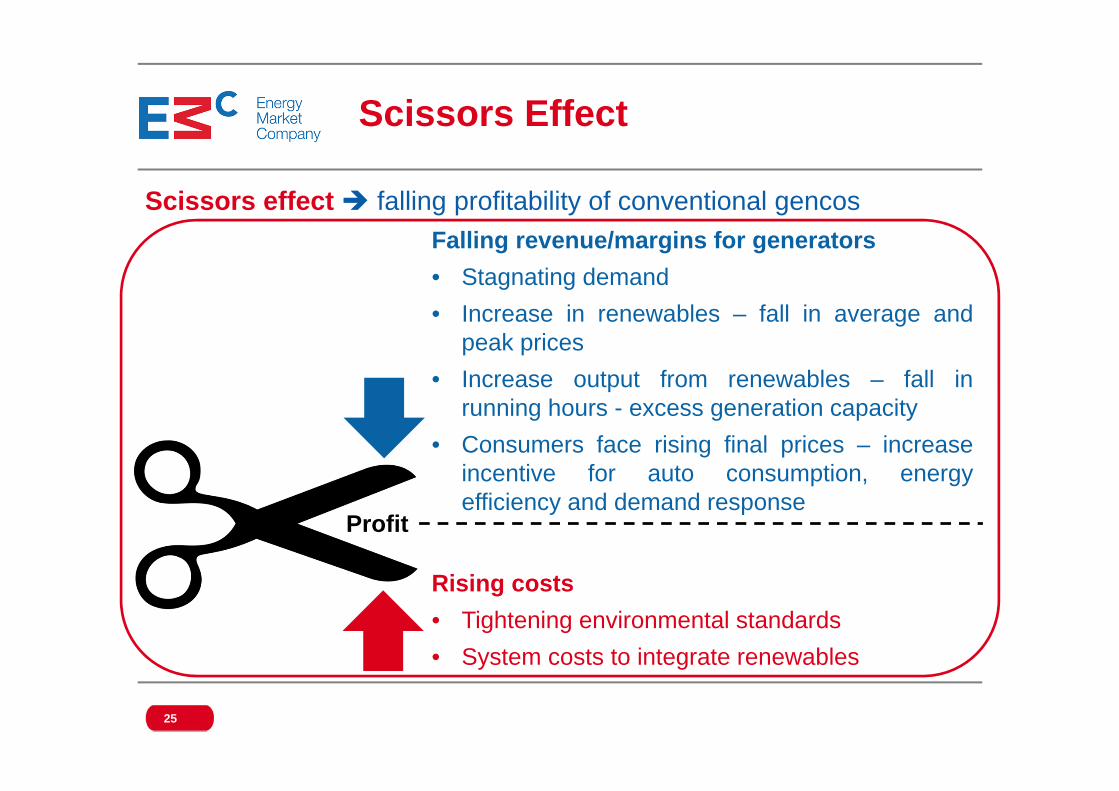

Scissors effect falling profitability of conventional gencos

Scissors Effect

Rising costs• Tightening environmental standards• System costs to integrate renewables

Falling revenue/margins for generators• Stagnating demand• Increase in renewables – fall in average and

peak prices• Increase output from renewables – fall in

running hours - excess generation capacity• Consumers face rising final prices – increase

incentive for auto consumption, energyefficiency and demand response

25

Profit

Electricity Demand in the EU-27, 2000–13

Stagnant Demand in Europe

Source: Power Statistics and Trends, Eurelectric, various years

26

Growth of renewables• Policy driven

• Has been leader in industrial development andinstallation of renewables especially wind and solar

• EU governments have levied significant funds throughelectricity tariffs to finance out-of-market payments todevelopers of renewable power

• Past 10 years, 80% of new generation capacity in OECDEurope has been renewable capacity

Renewables in Europe

27

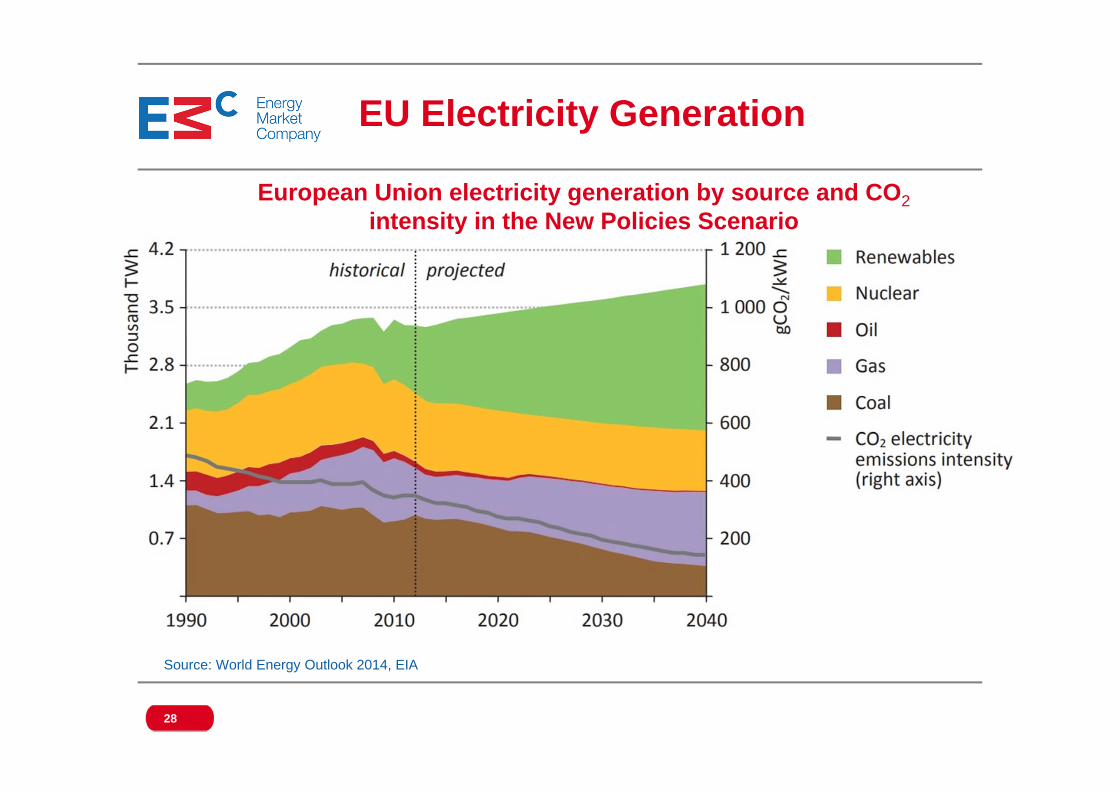

EU Electricity Generation

28

European Union electricity generation by source and CO2intensity in the New Policies Scenario

Source: World Energy Outlook 2014, EIA

EU Primary Energy Generation

29

Generation by primary energy - 2030 outlook in the EU 27

Source: Power Statistics and Trends 2013, Eurelectric

Renewables impact conventional generators’ revenue/margins

Impact of Renewables

30

Lowers average wholesale electricity prices

Peak prices falls lead to inability of conventional generatorsto recover fixed cost; as such plants rely solely on energymarket to recover their cost

Output effect – For conventional generators to recover theirfixed cost they must run sufficient hours where prices aregreater than their marginal cost. Growth of renewables haslowered capacity utilisation of conventional generators.

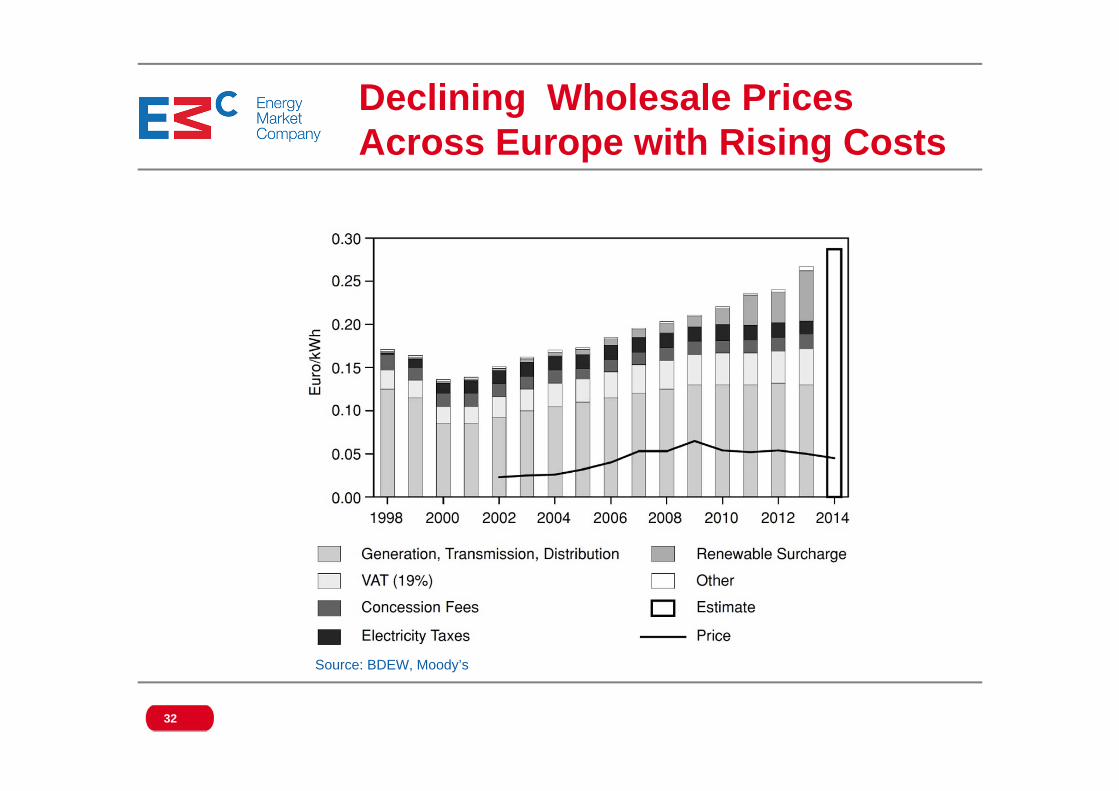

Wholesale market prices in selected EU countries, 2008-14

Falling Wholesale Prices in Europe

31

Source: OMIE, EEX

Declining Wholesale Prices Across Europe with Rising Costs

32

Source: BDEW, Moody’s

Operation of Gas Fired Plants (Spain)

Source: CNMC

Hours of effective operation of gas fired plants in Spain (2004-2014)

33

More auto consumption, energy efficiency and demandresponse lower demand and lower capacity utilisation ofconventional generators

Growth in Demand Response

34

High final prices faced by consumers incentivise autoconsumption, energy efficiency and demand response

Smart technologies reduce the cost of coordination andaggregation makes demand response more feasible

• Current electricity markets are designed for thetechnology of the 20th century

• The primary objective is to reflect the industry’s cost inprices

• Conventional plants fall naturally into a merit-orderapproach

• Low marginal cost and inflexible plants like nuclear at thebottom, high marginal cost flexible plants like OCGTs atthe top and base load plants like coal in the middle

Current Electricity Market Design

35

Stylised Merit Order

36

Source: Hunt, 2002

There is thus no incentive to invest in peaking plants orthose needed to balance the system due to variability ofrenewables’ energy output

Lack of Generation Investment

37

But increasing share of renewables in the energy mix whichdoes not have flexibility and essentially zero marginal costshas depressed both average and peak prices resulting in themissing money problem for conventional generators

Central planning and control of system – i.e.abandon liberalisation and revert to more centralisedapproaches but retain some market elements (e.g.auctions for capacity)

Potential Solutions

38

Range of potential “solutions” mooted

Refine energy only markets (e.g. introduce capacity mechanisms)

Drop out of market support for renewable resources

Investments Markets• Hive off the investment problem by creating a

market for the long term operating on the basis ofcompetitive arrangements like auctions

• Retain short-term markets along same lines aspresent

Potential Solutions

39

Introduce more flat rate or demand relatedelements into pricing (e.g. charge consumer anaccess fee to cover fixed charges and a separatemarginal cost to cover incremental cost)

A Two-Market System• Create two separate power markets for

generators

• Consumer choice between 2 different sets of supply

• As available power at relative low prices at times when sufficient supply available from low-carbon inflexible generators

• On demand power available at all times but at significant higher prices

40

Potential Solutions

X 2

41

The Two-Market System

On demand (flexible)

generators

As available intermittent generators

Support for low carbon

generators

System operator

Operator dispatches generators

Suppliers

On demand consumption

As available consumption

Electricity consumers

Income from as available

market

Income from flexibility market

Suppliers draw power

from grid

What About NEMS?

42

43

Installed Capacity

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MWInstalled Capacity (MW) CCGT/Cogen/Trigen (MW)Average Forecasted Demand (MW) Peak Forecasted Demand (MW)

44

Quarterly Average USEP vs Vesting Price, 2003 - 2016

$40

$90

$140

$190

$240

2003Q1

2004Q1

2005Q1

2006Q1

2007Q1

2008Q1

2009Q1

2010Q1

2011Q1

2012Q1

2013Q1

2014Q1

2015Q1

2016Q1

$/M

Wh

QuarterlyAverageUSEP

HedgePrice(PNG)

BVP

LVP(LNG)

2. PNG supplies

became scarce

1. Ample supply of PNGThe Lantau Group

defines three periods in NEMS

3. Increase in availability of natural gas

45

Energy-Only Market

• Generator’s sole remuneration is only from energy spot payment• In a competitive market, spot price = short run marginal cost (SRMC)• During supply scarcity, spot price > SRMC. Price spikes allow

generators to recover fixed capital costs.

Economic Theory of Energy-Only MarketEnergy-only markets with scarcity pricing provide efficient price signals for generation investments

Demand (normal)

Demand (high)

Price

Quantity (MW)

BaseloadMarginal

Cost

Peaker Marginal

Cost

• Use prices as signals• Prices spike when supply cushion is tight• Incentivise generation investment in the

long run

46

Quarterly USEP VS Estimated SRMC

0.00

50.00

100.00

150.00

200.00

250.00

300.00

$/M

Wh Quarterly

AverageUSEP

QuarterlyAverageEstimatedSRMC

2013 Q4

47

Vesting Contracts

10

20

30

40

50

60

70

Vest

ing

Con

trac

t Cov

erag

e (%

)

Year

Vesting Contract Rollback Schedule (Initial vs Actual)

InitialRollbackSchedule

ActualSchedule

48

Rise of Solar

Target of 1000MWp

>2020

0

100

200

300

400

500

600

700

800

900

1000D

ec-0

8Ju

n-09

Dec

-09

Jun-

10D

ec-1

0Ju

n-11

Dec

-11

Jun-

12D

ec-1

2Ju

n-13

Dec

-13

Jun-

14D

ec-1

4Ju

n-15

Dec

-15

Jun-

16D

ec-1

6Ju

n-17

Dec

-17

Jun-

18D

ec-1

8Ju

n-19

Dec

-19

Jun-

20D

ec-2

0

MW

pInstalled Capacity of Grid-Connected Solar PV Systems

Source: EMA Statistics

49

Demand Profile with 1000MW Solar

4500

5000

5500

6000

6500

7000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47

Dem

and

(MW

)

PeriodWeekday Weekend/ Public HolidaysNet Weekday profile (with 1000MW solar) Net Weekend profile (with 1000MW solar)

6:30am to 7:30pm (Period 14 – Period 39)

*Estimated using 2016 data

50

USEP Profile (2016)

0

10

20

30

40

50

60

70

80

90

100

1 2 3 4 5 6 7 8 9 10 111213 1415 161718 1920 212223 2425 2627 282930 3132 333435 3637 383940 4142 434445 4647 48

USE

P ($

/MW

h)

Weekday Weekend/Public Holidays

51

Carbon Pricing in Singapore

• Singapore government will introduce a carbon tax on large directemitters of greenhouse gases (GHGs) such as power stations from2019

• Singapore is looking at a carbon tax rate of $10-$20 per tonne of carbondioxide-equivalent GHG emissions

• The final tax rate (to be decided) needs to provide sufficient price signalto incentivise behavioural change and energy efficiency improvement

• Singapore has committed to reducing emissions intensity by 36% by2030 compared to 2005 levels

Thank you

52

Disclaimer:

This presentation is being made available for general information only and is subject to change without notice. While EMC has taken reasonable care EMC does not representand makes no warranty whatsoever whether express, implied or statutory that the information provided in this presentation is current, accurate, complete, fit, suitable or valid forany purpose or use whatsoever and EMC shall not be liable for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of anykind) suffered due to any omission, error, inaccuracy, incompleteness, or otherwise, and/or any reliance on such information.

Any recirculation, transmission or distribution of this presentation or any part thereof to and/or by any third party requires the prior written permission of EMC.