Embed Size (px)

Citation preview

VFF

September 2017

Execution in post MiFID II environment

Espen Andersen

Head of Electronic Execution Services

Market structure and Execution under MiFID I

• Expansion in number of trading «venues»:

• MTF – Multilateral Trading Facility

• BCN – Broker Crossing Network

• Internal markets

• Increase in «dark» execution:

• Regulated Markets (RM)

• MTF – Multilateral Trading Facility

• BCN – Broker Crossing Network

2

DNB dark

volumeTrade category break down

OBX -FY 2015

Source: Fidessa Fragmentation Index

Venue market share

OBX - FY 2015

Source: Fidessa Fragmentation Index

Market structure and trading under MiFID I

• Liquidity no longer available at the exchange. How to consolidate the market?

• Smart Order Router (SOR)

• Execution algorithms

3

Client S

O

R

Algo

DMA

Sell side

Care

Internal

market

Introduction to Execution under MiFID II

• The intention of new regulation is to bringing as much trading as possible on to

regulated markets to participate in the price formation process.

• New best-ex regulation mandating more documentation, more reporting and the need

for continuous monitoring for both buy- and sell-side

• Massive increase in data points for both trade porting and transaction reporting with

new reporting obligations for the buy-side.

• Market structure and execution possibilities to change with the introduction of new

venue types (SI), capping of dark pools (BCN) and new order types.

4

Trading obligation

• “Investment firms will be required to trade shares that are admitted to trading on a

RM or traded on a trading venue on a RM, MTF or SI”

• Double volume caps

• 4% and 8% volume caps on RPW and NTW (liquid instruments) means trading in BCNs will come to a

halt

5

Best Ex requirements

• From all «reasonable steps» to «all sufficient steps»

• Participants need to measure execution quality and

document «all sufficient steps» on a continues bases

• Execution policy must be a «living document»

• Even though all clients are not «caught» in MiFID II

Investment firm definition => «sell sides» are.

6

DNB

Transaction Cost Analysis

DNB Order Performance Monitor

Conditional orders

• Indicative orders can be represented in

multiple systems at once, sending a firm

order into a specific system only when a

counterparty is found.

7

Conditional orders

• Turquoise Plato Block

Discovery

• Bats LIS

• POSIT Conditional Orders

Large In Scale (LIS) waiver post MiFID II

Periodic auctions

• Order books holding very short regular

auctions with prices within the EBBO.

• Indicative price/size of each auction is

published, so it is considered pre-trade

transparent and the caps do not apply.

• Some also offering broker preference

8

Periodic auctions

• Bats Europe Periodic

Auctions

• Nasdaq Auction on

Demand

• Sigma X Auction Book

Order book LIS

• Block orders above LIS

executed with different

order entry

mechanisms.

9

Order book LIS

• UBS MTF Large in scale trades

• Most of the mechanics of the MTF remain unchanged, but trades that meet the LIS

size requirements are consummated under the LIS waiver.

• Euronext Block MTF

• London-based dark MTF that will be revamped into a new block-trading MTF

• LIS on SETS order book

• Hidden orders within the LSE SETS lit order book, with peg option.

• Deutsche Borse volume discovery orders

• Iceberg order type to allow execution of large orders within the Xetra book

• Nasdaq Nordic LIS Block

• Hidden orders integrated within the Nasdaq Nordic lit order books

Systematic Internaliser (SI)

• Classified as a «Venue» under MiFID II

• Do not have to comply with Tick size regime

• Timing of trade publication (up to 1 min)

• Pre-trade transparency 10% of SMS public

• Can provide «private quotes»

to predetermined

client groups

• Must operate on risk

10

Dark distribution

pre/post MiFID II?

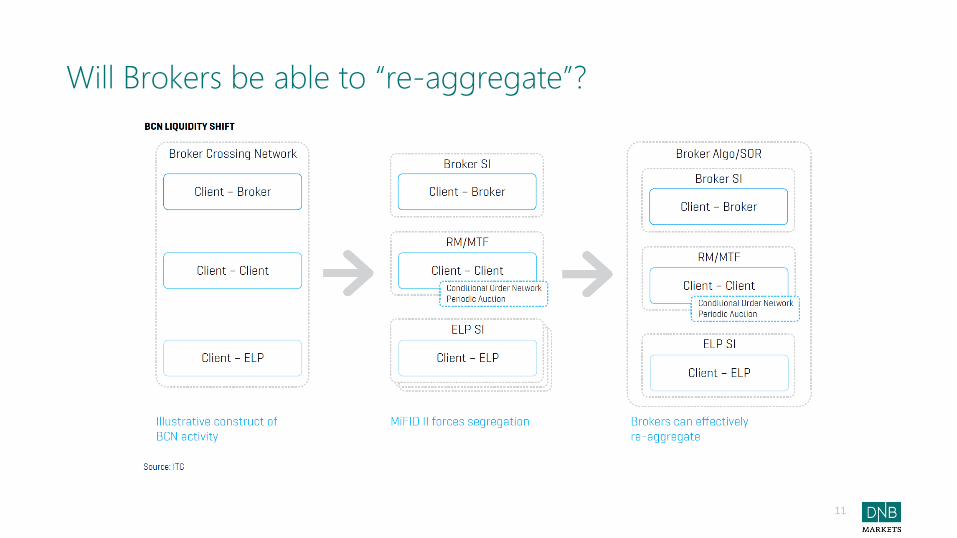

Will Brokers be able to “re-aggregate”?

11

The end of “Old school upstairs-crossing”?

• No, the regulators intention is not to stop

matching of block trades – but it might get a

bit more complicated

• Local knowhow and client familiarity still

matters

12

Disclaimer

This presentation is strictly confidential and prepared exclusively for the benefit and internal use of our client to whom it is directly addressed and delivered (including such

client’s subsidiaries, the “Company”) and not for distribution or publication. The information may not be reproduced without the consent of DNB Markets.

The information in this presentation is based upon any management forecasts supplied to us by the Company and publicly available information. We have relied upon and

assumed, without independent verification, the accuracy and completeness of all information available. DNB Markets opinions and estimates constitute DNB Markets’ judgment

and should be regarded as indicative, preliminary and for illustrative purposes only. Statements in the presentation reflect prevailing conditions and DNB Markets’ opinion at the

date the presentation was prepared, all of which are accordingly subject to change. DNB Markets does not warrant that the information in the presentation is exact, correct or

complete. The presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, oral briefing provided by DNB

Markets.

Our research are not and do not purport to be appraisals of the assets, shares, or business of the Company or any other entity. DNB Markets makes no representation as to the

actual value which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Unless expressly contemplated

hereby, the information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control,

which may have significant valuation and other effects.

This presentation is not an offer or a recommendation to purchase or sell financial instruments or assets, and does not constitute a commitment by DNB Markets to underwrite,

subscribe for or place any securities or to extend or arrange credit to or to provide any other services. DNB Markets does not accept any responsibility for direct or indirect losses

that are due to the interpretation, and/or use, of this presentation.

DNB Bank ASA and/or other companies in the DNB group or employees and/or officers in the group may be market makers, trade or hold positions in instruments referred to or

connected therewith, or provide financial advice and banking services in this connection.

Rules regarding confidentiality and other internal rules limit the exchange of information between different units in DNB Bank. Employees in DNB Markets who have prepared this

presentation are therefore prevented from using, or being aware of, information in DNB Bank and other companies in the DNB group which may be relevant to this presentation.

This presentation has been prepared in accordance with the general business terms of DNB Markets, a division of DNB Bank ASA, available at dnb.no/markets.

CONFIDENTIAL

13

![MiFID II - Key Impacts & Considerations Sell-Side Firms · “[T]he MiFID II best execution regime does not require a fundamental review of firm’s existing arrangements where they](https://img.dokumen.tips/doc/110x75/5ec9ea40753764113717a2af/mifid-ii-key-impacts-considerations-sell-side-firms-aoethe-mifid-ii-best.jpg)