Embed Size (px)

Citation preview

1planetretail.net

European Retail TrendsRetailing in Europe and Country Profiles

Nice, 26 February 2015 Niklas ReineckeRetail Analyst

PRESENTATION FOR PLMA‘s Roundhouse Conference

David GrayRetail Analyst

Ageing Society, Single Households, Individualisation, Urbanisation, Mobilisation, Transparency in

Production, Loss of Loyalty, Online Shopping, Two Nations Effect, Lifestyle, Situational Usage,

Economisation, Cocooning, Smart and Hybrid Shopping, Sustainability, Technological Progress,

Energy Saving, Regional Sourcing, Faster Innovation Cycles, Renovation Cycles, Rise of Independent Shopkeepers, Proximity Retailing, Energy Costs,

Rising Food Prices, Direct-to-Consumer, Demand for Protection, Verticalisation, Cartel Control,

Oligopolisation, Discounting, Multichannel Shopping, Event Shopping, Foodservice, Complexity!

Europe from a Macro Perspective

4

A few markets in CEE see very high levels of modern food retail similar to Western European markets.

Europe from a Macro Perspective - Share of Modern Food Retail Format Sales

Source: Planet Retail.

Europe: 2014 (%)

5

Economic recovery is not universal. Markets are in different stages.

Europe from a Macro Perspective – GDP Real Growth

Serbia

Russia

Azerbaijan

Armenia

Georgia

Ukraine

Belarus

MoldovaRomania

Hungary

Poland

Bulgaria

Greece

Cyprus

Macedonia

Albania

Bosnia & Herzegovina

CroatiaSlovenia

Italy

Slovakia

Czech RepGermany

Sweden

Lithuania

Latvia

Estonia

Finland

Norway

FranceAustria

Switzerland

Belgium

Netherlands

SpainPortugal

UnitedKingdom

Ireland

Denmark

+5.0%

+3.2%+4.5%

+2.7%

+8.9%

+3.0%

+3.4%

+0.2%

+0.7%

+1.1%

+2.1%

+1.4%

+0.4%

-0.2%

-1.1%

Source: Planet Retail.

+1,2%

+3.2%

+2.4%+2.8%

+2.4%

+1.0.%

+1.4%

+1.2%

+1.8%

+1.0%

+1.5%

-0.8%

-0.2%

Europe: GDP Real Growth 2014 (%)

+0.7%

+2.5%

+0.6%

+3.6%

+0.6%

+1.0%

-0.5%+1.3%

+2.1%

-6.5%

+3.2%

6

Europe from a Macro Perspective - Modern Food Retail Format Sales

Despite a current slowdown of the Russian economy, Eastern Europe will see a higher MFRF sales CAGR than Central Europe over the next five years.

0

200

400

600

800

1,000

1,200

1,400

1,600

2014e 2019f

Western Europe

Central Europe

Eastern Europe

Mo

der

n F

oo

d R

etai

l Sal

es

(EU

R b

n)

Europe: Modern Food Retail Format Sales, 2014-2019f (EUR bn)

Note: f – forecastSource: Planet Retail

In Western Europe, poorly-performing retailers such as Metro Group are contributing to the slow growth.

Central Europe

8

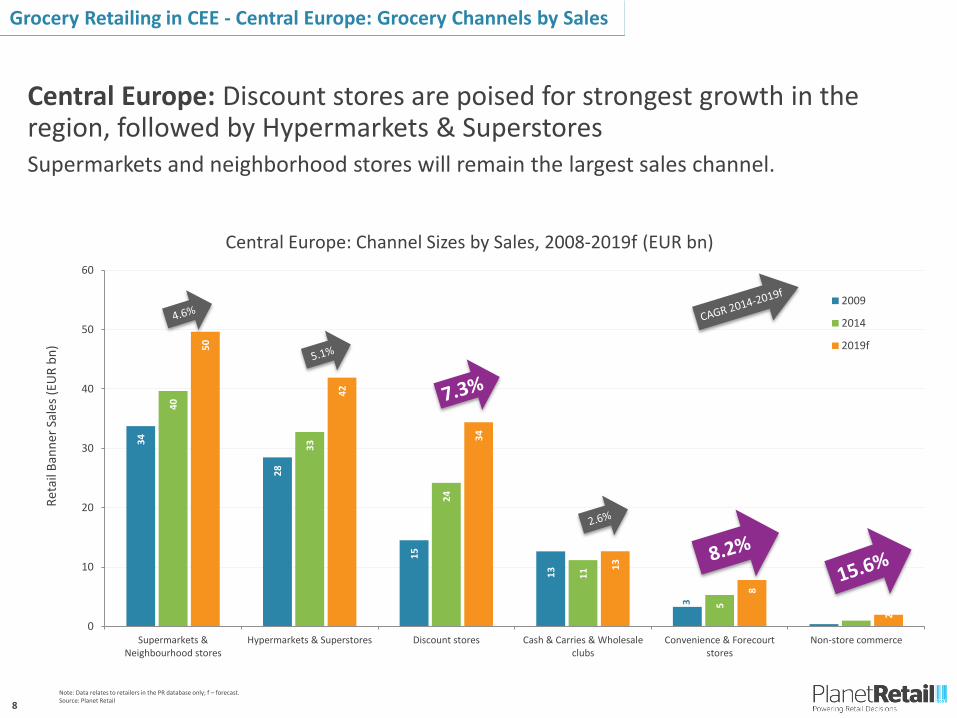

Central Europe: Discount stores are poised for strongest growth in the region, followed by Hypermarkets & SuperstoresSupermarkets and neighborhood stores will remain the largest sales channel.

Grocery Retailing in CEE - Central Europe: Grocery Channels by Sales

34

28

15

13

3

0

40

33

24

11

5

1

50

42

34

13

8

2

0

10

20

30

40

50

60

Supermarkets &Neighbourhood stores

Hypermarkets & Superstores Discount stores Cash & Carries & Wholesaleclubs

Convenience & Forecourtstores

Non-store commerce

Re

tail

Ban

ner

Sal

es (

EUR

bn

)

2009

2014

2019f

Note: Data relates to retailers in the PR database only; f – forecast.Source: Planet Retail

Central Europe: Channel Sizes by Sales, 2008-2019f (EUR bn)

9

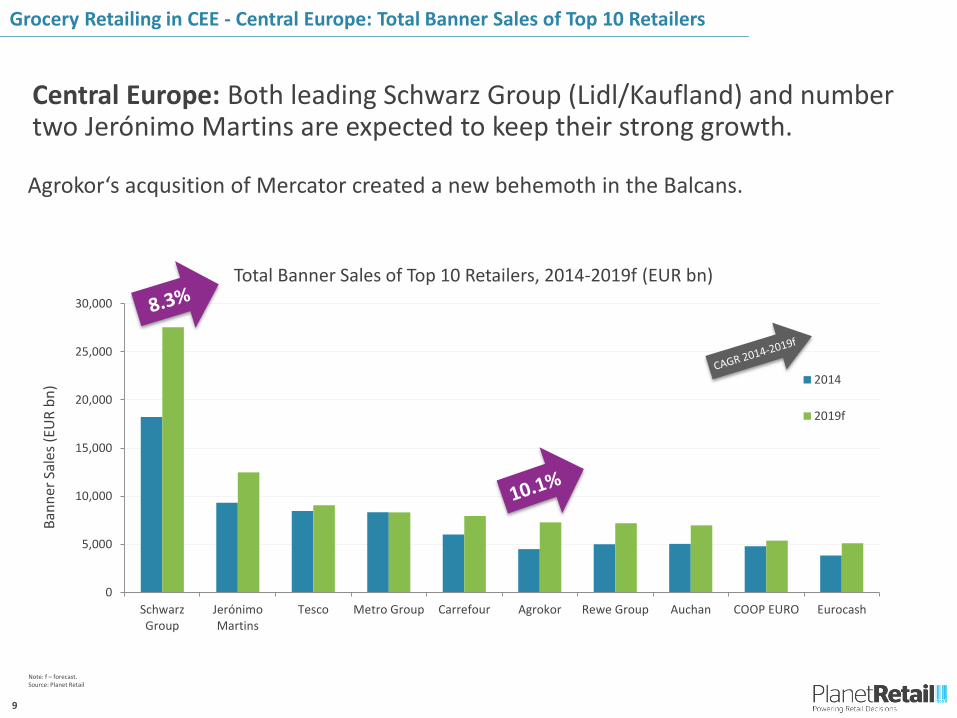

Grocery Retailing in CEE - Central Europe: Total Banner Sales of Top 10 Retailers

Central Europe: Both leading Schwarz Group (Lidl/Kaufland) and number two Jerónimo Martins are expected to keep their strong growth.

Agrokor‘s acqusition of Mercator created a new behemoth in the Balcans.

0

5,000

10,000

15,000

20,000

25,000

30,000

SchwarzGroup

JerónimoMartins

Tesco Metro Group Carrefour Agrokor Rewe Group Auchan COOP EURO Eurocash

Ban

ner

Sal

es

(EU

R b

n)

Total Banner Sales of Top 10 Retailers, 2014-2019f (EUR bn)

2014

2019f

Note: f – forecast.Source: Planet Retail

10

Poland enjoys growing food retail sales per capita, despite demographic challenges.

In terms of consumer spending, leading Polish cities promise a market size equivalent to some of the smaller Central European countries.

1,8092,926

Warsaw Lodz

Metropolitan Food Retail Sales per capita, 2014f (EUR)

Warsaw Katowice

3.0 2.6

Population, 2014f (million)

1.4

Lodz

1,968

Katowice

1. Country Overview

Note: f – forecastSource: Planet Retail

6259

43

26 26

13 12

0

10

20

30

40

50

60

70

Hungary Warsaw Slovakia Katowice Croatia Lódz Cyprus

Co

nsu

mer

sp

end

ing

(EU

R b

n)

Central Europe: Consumer Spending in Selected Polish Cities vs. Central European markets, 2014f (EUR bn)

11

0

10

20

30

40

50

60

70

80

90

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Foo

d R

etai

l (%

)

Hypermarkets & Superstores Supermarkets & Neighbourhood Stores Discount Stores Others

Fast channel change in CEE: e.g. Poland’s discount share of food retail is the largest in the CEE region.

POLAND: Channel Development in Food Retail, 2000-2020 (%)

Source: Planet Retail

Grocery Retailing in CEE - Poland

12

2. Competitive Environment

Eurocash

Eurocash partners with nearly 10,000 retail stores across the country.

Creating synergies with Tradis and its partners like the Lewiatan network is the main priority. It is also investing in the outlet expansion of its own banners like Groszek.

Eurocash acquired two convenience store chains in 2014, Inmedio and 1 minute. Inmedio also operates Inmedio Café.

In Q3 2014, Eurocash launched e-grocery site frisco.pl.

A partnership with independent franchise network abc is expanding fast, currently consisting of 6,170 stores. The network introduced abc Mini Bistro in 2013, a concept strategy suggested by Eurocash.

Eurocash became the largest wholesaler in Poland after acquiring Tradis Distribution in 2012. It is also increasingly experimenting with convenience stores channel.

Abc Mini Bistro in an abcstore offering snacks and beverages. It is currently available in 300 stores.

© E

uro

cash

© C

arim

ali

Inmedio Café allows shoppers to read their newspapers as they have a hot drink or a snack.

Eurocash cash & carry is still the core business of Eurocash Group.

13

99% Turnover from discount channel

2,587Discount Stores

Biedronka in Poland

Grocery Retailing in CEE - Competitive Environment

Notes: e- estimate, f – forecastSource: Planet Retail

• EUR800 million investment in 300 new stores in Poland from 2015-2017

• More proximity penetration, battling with Zabka

• Calls for massive investment into logisitics

• Mulling over online grocery operation in Poland

• Internationalisation on the agenda: Romania, Russia, Ukraine and Turkey

EUR9.3 billionBanner Sales

in Poland

Biedronkadiscount stores

99%

Drugstores1%

Biedronka in Poland: Total Banner Sales per channel, 2014e

Eastern Europe

15

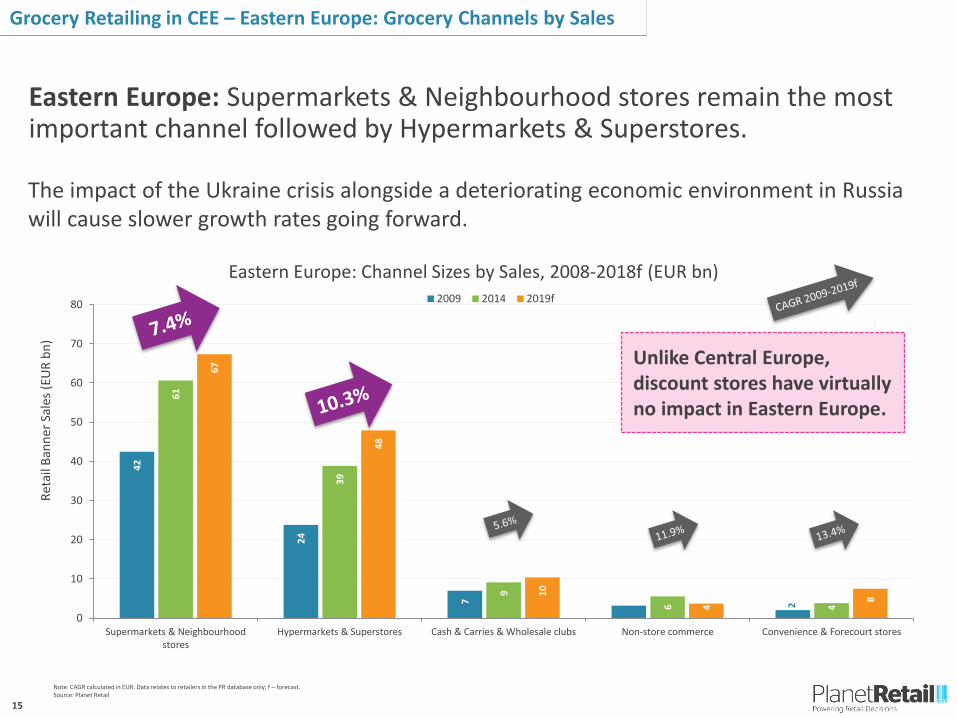

Eastern Europe: Supermarkets & Neighbourhood stores remain the most important channel followed by Hypermarkets & Superstores.

Grocery Retailing in CEE – Eastern Europe: Grocery Channels by Sales

42

24

7

3

2

61

39

9

6 4

67

48

10

4

8

0

10

20

30

40

50

60

70

80

Supermarkets & Neighbourhoodstores

Hypermarkets & Superstores Cash & Carries & Wholesale clubs Non-store commerce Convenience & Forecourt stores

Re

tail

Ban

ner

Sal

es (

EUR

bn

)

2009 2014 2019f

Note: CAGR calculated in EUR. Data relates to retailers in the PR database only; f – forecast.Source: Planet Retail

Eastern Europe: Channel Sizes by Sales, 2008-2018f (EUR bn)

The impact of the Ukraine crisis alongside a deteriorating economic environment in Russia will cause slower growth rates going forward.

Unlike Central Europe, discount stores have virtually no impact in Eastern Europe.

16

Grocery Retailing in CEE – Eastern Europe: Total Banner Sales of Top 10 Retailers

Eastern Europe: All top 10 retailers are expected to generate growth with some of them even at double digit CAGRs.

Importance of Russia is illustrated by the fact that three of the top 5 players in the region come from Russia.

0

5,000

10,000

15,000

20,000

25,000

30,000

Magnit X5 RetailGroup

Auchan Dixy Group MetroGroup

Lenta O'Key M.video ATB Market Adeo

Ban

ner

Sal

es

(EU

R b

n)

Total Banner Sales of Top 10 Retailers, 2014-2019f (EUR bn)

2014

2019f

Source: Planet Retail Worth mentioning is the absence of the discount players including giant Lidl.

17

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

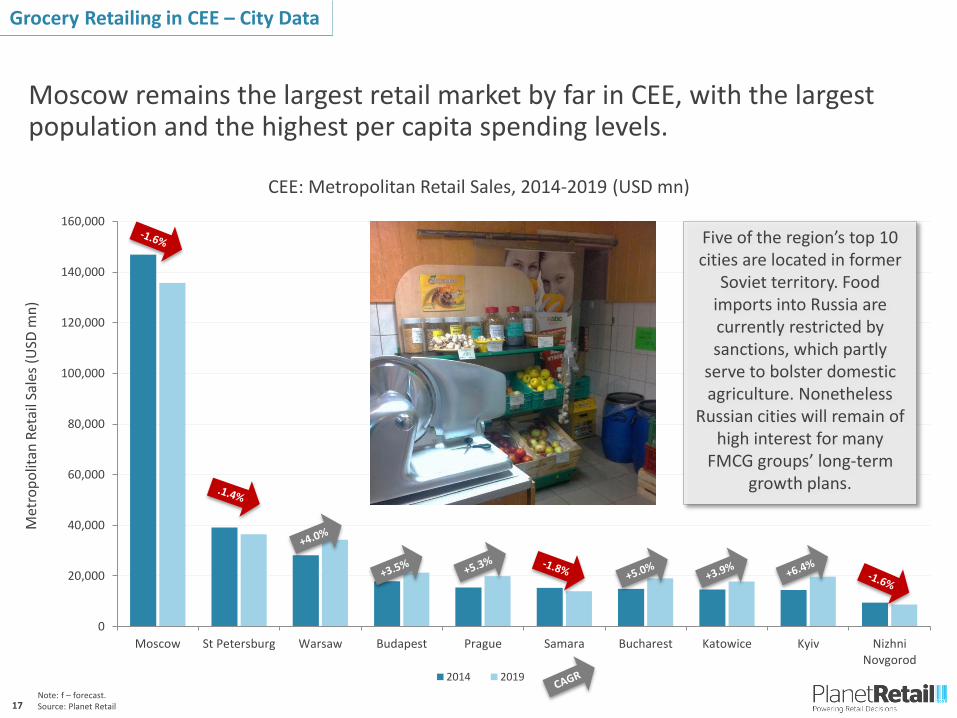

Moscow St Petersburg Warsaw Budapest Prague Samara Bucharest Katowice Kyiv NizhniNovgorod

Met

rop

olit

an R

etai

l Sal

es (

USD

mn

)

2014 2019

CEE: Metropolitan Retail Sales, 2014-2019 (USD mn)

Note: f – forecast.Source: Planet Retail

Moscow remains the largest retail market by far in CEE, with the largest population and the highest per capita spending levels.

Five of the region’s top 10 cities are located in former

Soviet territory. Food imports into Russia are currently restricted by sanctions, which partly

serve to bolster domestic agriculture. Nonetheless

Russian cities will remain of high interest for many

FMCG groups’ long-term growth plans.

Grocery Retailing in CEE – City Data

18

Store numbers increased from 4,055 in 2009 to 9,711 in 2014f.

Far ahead closest rival X5 Retail Group (5,483 stores in 2014).

31.6% year-on-year sales growth for 2014.

present in seven federal districts and 2,108 cities in Russia with 9,711 stores.

2015 capex is RUB65 billion*, mostly scheduled for store expansion.

The retailer recorded 14.5% like-for-like sales growth in 2014, together with a 4.5% rise in traffic generation.

Magnit operates supermarkets & neighbourhood stores, hypermarkets and drugstores across Russia.

Magnit became the grocery market leader in Russia in 2013.

3. Competitive Environment

Magnit investment budget, 2014$1.9 bn

“Enjoy…”

SERGEY GALITSKIY Founder & CEO, Magnit

(on H1 2014 results)

Magnit’s strict financial control is the backbone of its ambitious expansion drive, with a strong focus on efficiency.

*USD/RUB= 34.4 (2014)

© M

agn

it

19

National and international suppliers (1,000 in total) contribute 55-60% of Magnit’s product assortment.

Private label assortment of 605 SKUs:

The majority being food items.

11% private label sales share.

Curated product assortment across regions:

Ambient food in less wealthy regions

Emphasising fresh produce in more affluent cities.

Magnit is renowned for running all its operations in-house, from logistics to agricultural production units. Centralisation rate is 86%.

1. Corporate Overview

5,938company-owned trucks, 2014

27distribution centres, 2014

4,000local suppliers working with Magnit

20

Strategic Initiatives

Magnit’s regional conquest: Founded in Southern Russia 20 years ago, the retailer is currently in almost every region in Russia.

South: 1,980

N. Cacausus: 343

Central: 3,000

Volga: 2,698

North-West: 520

Urals: 936

Siberia: 234

Note: Map as of Q3 2014Source: Company Reports/ Planet Retail

Channel Trends

22

C-STORES

HYPERMARKETS

DISCOUNTERSE-COMMERCE

Big Box servicing online home delivery, Click & Collect, Drive formats.

Hypermarkets opening dedicated discount areas and formats.

Discounters opening more convenience-based formats.

C-stores as E-commerce fulfillment outlets.

4. Retail Trends: Channel proliferation and convergence

23

4. Discount Stores

-> Discounters need new ideas for impulse and convenience products!

24

Fighting Convenience Stores

City centre locations; instore bakeries; food-to-go;

premium food; pre-selection, quick shopping.

Fighting Cash & Carries

Ambient staples for bulk buying, multi packs, no

services, no frills environment.

Fighting Supermarkets

New categories and extended specialist food ranges, fresh fish, more

brands and selected services.

Fighting Hypermarkets

Adding non-food and deli food categories on an opportunistic basis.

Discounters - How do they grow?

The all-purpose grocers skimming off the cream.

Fighting Online?

4. Discount Stores

25

Aldi Nord/Süd and Lidl remain the most important discount operators.

Consolidation process.

From hard to smart discounting.

Adaptations to national demands.

Proximity retailing.

E-commerce challenging for discounters.

Partly investment in own production!

Brand listings at Aldi!

Discounters are shifting from hard to smart discounting - broadening their offers but staying loyal to their buttress of success.

4. Discount Stores

26

4. Supermarkets & Neighbourhood Stores

27

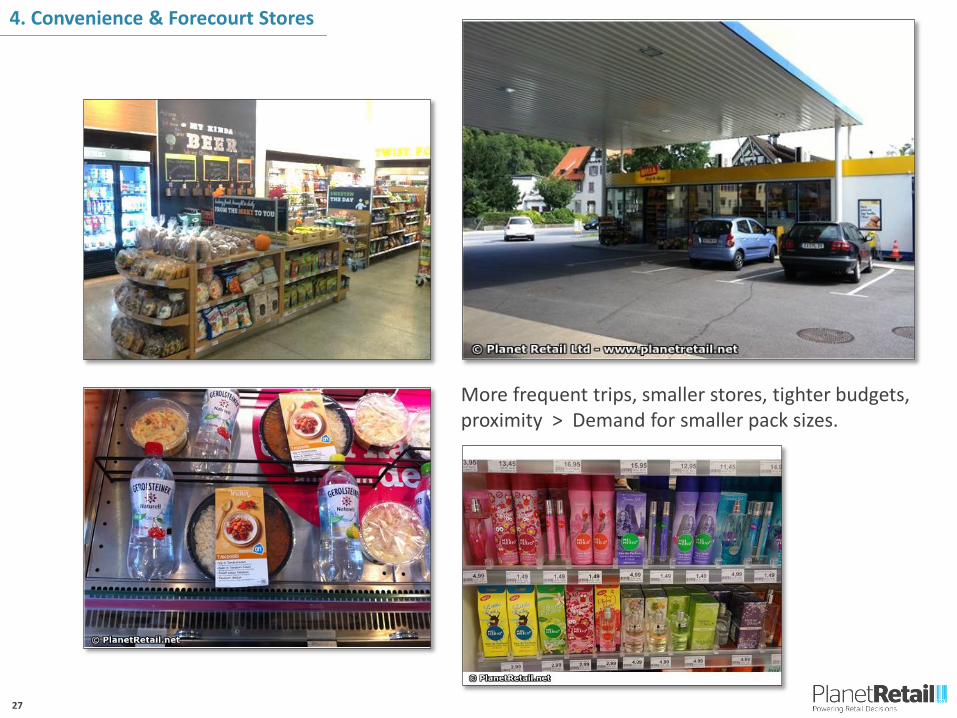

4. Convenience & Forecourt Stores

More frequent trips, smaller stores, tighter budgets, proximity > Demand for smaller pack sizes.

28

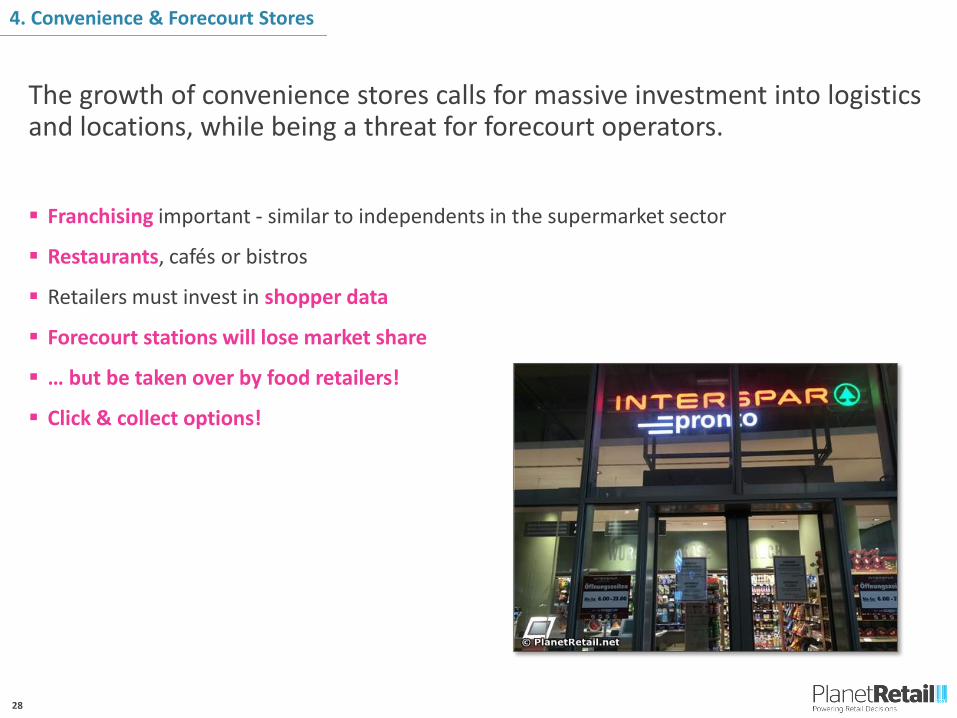

Franchising important - similar to independents in the supermarket sector

Restaurants, cafés or bistros

Retailers must invest in shopper data

Forecourt stations will lose market share

… but be taken over by food retailers!

Click & collect options!

The growth of convenience stores calls for massive investment into logistics and locations, while being a threat for forecourt operators.

4. Convenience & Forecourt Stores

29

4. Hypermarkets & Superstores

Hypermarkets are readjusting non-food assortments

30

Europe cannot be viewed as one market.

Channels blurring.

Proximity rising.

E-commerce growing.

Discounters softening.

Hypermarkets specialising, readjusting non-food ranges: increase productivity; increase format profitability; scale back less profitable ranges.

STORES BECOMING SMALLERin food and non-food:

Demand for smaller pack sizes.

Still growth in big box.

Broad traditional sector.

Shift to modern trade at varying speed.

6. Key Findings

![훼밀리인터네셔널(Family International) | [Cott] plma brochures nov 2011](https://img.dokumen.tips/doc/110x75/55a3b2dc1a28abff678b4730/family-international-cott-plma-brochures-nov-2011.jpg)