Embed Size (px)

Citation preview

European Electricity Markets Structure and Trading

Phase I: Retail Competition and Crossborder Mergers

Modelling and Managing Competitive Electricity Markets

30 September – 3 October 2003

John Bower

Europe I 2John Bower

Overview

European electricity market overview

The Directive and retail supply competition

Unresolved regulatory issues

BREAK

Transmission economics

Measuring market integration

Transmission pricing solutions

Case Study

Europe I 3John Bower

European electricity market overviewFour coordinated AC transmission grids linked by DC lines define market boundary….

TRANSMISSION SYSTEMS IN THE EUROPEAN ELECTRICITY MARKET

Source: UCTE

Europe I 4John Bower

European electricity market overview…. owned by 45 separate entities spread across 28 countries coordinated by ETSO

EUROPEAN TRANSMISSION SYSTEM OPERATORS (ETSO) MEMBERS

• TSOI, the association of TSOs in Ireland: Irish Republic (ESB), Northern Ireland, (NIE)

• UKTSOA, the United Kingdom TSO association:England & Wales (NGC), Scottish Power (S. Scotland), N. Scotland, (Scottish Hydro)

• NORDEL, the Nordic TSOs: Norway (Statnett), Sweden (Svenska Kraftnat), Finland (Fingrid), W. Denmark (Eltra), E. Denmark (Elkraft)

• UCTE, the Union for the Co ordination of Transmission of Electricity, association of TSOs of the Continental countries of Western and Central Europe: Belgium (Elia SA/NV), Germany (Bewag AG, Energie Baden Württemberg AG, E.On Netz GmbH, Hamburgische Electrizitäts-Werke AG, RWE Net AG, Vereinigte Energiewerke AG), Spain (Red Eléctrica de España S.A., France (EdF Gestionnaire du Réseau de Transport d´Electricité), Greece (Hellenic Transmission System Operator),Italy (Gestore della Rete di Transmissione Nazionale), Slovenia (Elektro Slovenija), Croatia (Hrvatska Elektroprivreda, FRJ, EP CG, Elektroprivreda Crne Gore, Elektroprivreda Srbije), FYROM (Elektrostopastvo na Makedonija), Bosnia –Herzegovina (Joint Power Coordination Center), Luxembourg (Compagnie Grand Ducale d'Electricité du Luxembourg), Netherlands, TenneT bv), Austria (Tiroler Wasserkraftwerke AG, Verbund - Austrian Power Grid, Vorarlberger Kraftwerke AG), Portugal (Rede Eléctrica Nacional, S.A.), Switzerland (Aare-Tessin Ltd. for Electricity, BKW FMB Energie AG / BKW FMB Energie S.A., Elektrizitäts-Gesellschaft Laufenburg Grid AG/ Electricité de, Laufenbourg Grid AG, S.A., Energie Ouest Suisse, Etrans Ltd., Nordostschweizerische Kraftwerke AG), Czech Republic (CEPS), Hungary (Magyar Villamos Müvek Rt.), Poland (Polskie Sieci Elektroenergetyczne SA), Slovak Republic(Slovenské Elektrárne, a.s., Prenosova sústava)

Europe I 5John Bower

European electricity market overviewMarket serves 460 million people with peak load of 400 GW using 2784TWh per year

EUROPEAN ELECTRICITY MARKET STATISTICS

Country Area Population

Installed Generation

CapacityMaximum

System LoadTotal Net

Generation

Pump Storage

ConsumptionTotal

Consumption Net Importskm2 million MW MW GWh GWh GWh GWh

Austria 83900 8.10 13517 7728 54068 1986 50718 -1364Belgium 30500 10.20 14088 12291 80162 1639 82851 4328Czech Republic 78866 10.30 13746 8744 67741 749 56974 -10018Denmark 43000 5.30 12544 6284 34230 2148 32748 666Finland 338000 5.20 16143 12700 67113 2901 76093 11881France 544000 58.60 108291 66863 503998 6604 427471 -69923Germany 357000 82.00 107769 74300 496588 5789 493953 3154Great Britain 243300 59.00 69866 51000 359637 3497 370312 14172Hungary 93030 10.10 7847 5543 32420 0 35858 3438Croatia 56538 4.70 3601 2430 9829 18 13763 3952Greece 132000 10.50 9401 7699 45208 585 44617 -6Ireland 70300 3.70 4165 21634 449 21283 98Italy 301300 57.60 65513 49019 262426 9177 297706 44457Luxembourg 2600 0.40 0 888 1145 1022 5834 5711Netherlands 41500 15.60 14210 12255 52910 0 71824 18914Norway 324000 4.50 27622 20420 137000 10256 107721 -19023Poland 120728 38.60 30135 21836 144681 2790 135517 -6374Portugal 92400 9.90 9784 6022 37573 560 37949 936Slovakia 48845 5.40 7832 4149 28718 392 25653 -2673Slovenia 20253 2.00 2400 1698 12529 0 11180 -1349Spain 504800 39.70 44921 32430 195372 4908 194905 4441Sweden 450000 8.90 32934 26000 139994 11707 132974 4687Switzerland 50000 8.90 14606 9027 65392 1974 56401 -7017Total 4026860 459.2 630935 439326 2850368 69151 2784305 3088

Europe I 6John Bower

SING

LE EN

ERG

Y M

AR

KET

The Directive and retail supply competitionNew EU Directives give all electric (gas) consumers right to choose supplier by 1 July 07

1985

SINGLEEUROPEAN

ACT

1990 1995 2000 2005

Transp-arency

Directive

TransitDirective

MAIN EU LEGISLATION ON SINGLE MARKET FOR ENERGY

Electricity

Directive

Gas

Directive

30% 33% 100%Electricity Consumption

20%Gas Consumption 28%

Electricity

Directive

II

Gas

Directive

II

100%

Europe I 7John Bower

The Directive and retail supply competition…. with energy market liberalisation also being driven by economic / technical pressures

FORCES FOR CHANGE IN CROSS-BORDER ELECTRICITY TRADE

IN

EUROPEAN ELECTRICITY

MARKET EVOLUTION

DEREGULATI

ONRI O

NALCI OTY

F

NATI

ELECTM

ARKETS

INCREASEDEFFICIENCY ANDREDUCED SCALE

OF POWERPLANT

CREASECD

SIZE OF D

TRANSMISSION

CABLES

INCREASPE

ED

SED AND

REDUCED COST

OF COMPUTING

DER F

EG NAU TI

O S ET

LATI

ON

O MNA

LG

AAR

KS

Europe I 8John Bower

The Directive and retail supply competitionThe Directive guarantees competition in supply with transmission / distribution access.

KEY PROVISIONS OF THE ELECTRICITY DIRECTIVE

• Unbundling of accounts– Prevents subsidisation and distortion of competition in vertically integrated firms

• Competition in construction and operation of new plant– Authorisation procedure allows market to determine investment criteria – Tendering procedure allows central planner to determine when/where to build capacity

• Open access to transmission (and distribution) networks– Independent Transmission System Operator (TSO) must be appointed– Tariffs for connection and carriage must be transparent and non-discriminatory– Reciprocity clause and system reliability issues allows countries to bar access

• Right of consumers to choose their supplier– Increasing number of consumers should be authorised to choose their suppliers

Europe I 9John Bower

The Directive and retail supply competitionAbout 70% of electricity retail market volume is now eligible for supply competition and…

PERCENTAGE OF ELECTRICITY CONSUMPTION ELIGIBLE TO CHOOSE SUPPLIER

Source: European Commission DG Energy and Transport

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

France

Greece

Denmark

Irelan

d

Italy

Portugal

Belgium

SpainLuxe

mbourgNeth

erlan

dsAustr

iaFinlan

dGerm

any

Norway

Sweden

Net

con

sum

ptio

n op

en to

sup

ply

com

petit

ion

2002

2005

Europe I 10John Bower

The Directive and retail supply competition…. about 80% of gas retail market volume.

PERCENTAGE OF GAS CONSUMPTION ELIGIBLE TO CHOOSE SUPPLIER

Source: European Commission DG Energy & Transport

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Portugal

France

Greece

Denmark

Sweden

Belgium

Netherl

ands

Luxembourg

Spain

Irelan

d

Italy

Austria

Finland

German

y

Net

con

sum

ptio

n op

en to

sup

ply

com

petit

ion

2002

2005

Europe I 11John Bower

Unresolved regulatory issuesIn reality State and Federal policy objectives are interdependent and often in conflict

LIBERALISATION CONFLICTS

• Security

– Concern about dependence on other countries for generation capacity– Concern about dependence on other countries for generation fuels– Concern about dependence on other countries for gas / electricity transmission routes

• Competition

– Conflict between capital market and public service obligations– Access rights to transmission/ distribution and pricing of transmission– Increasing industry concentration through mergers and acquisitions

• Environment

– EUETS (CO2) and LCPD (NOx, SOX, particulate) costs versus lower prices– Renewables versus Combined Cycle Gas Turbines (CCGT)– NIMBY delays on approval of transmission routes / generation site licences

Europe I 12John Bower

Unresolved regulatory issuesLiberalisation means wholesale / retail markets replace government control and ….

STRUCTURE OF A LIBERALISED ELECTRICTY MARKET

Generators

Transmission

Consumers

Suppliers

Distribution

RETAIL MARKET

WHOLESALE MARKET

Physical Electricity Flow

Contract Flow

Europe I 13John Bower

Unresolved regulatory issues…. with new entrants and increased efficiency reducing prices….

IMPACT OF LIBERALISATION IN ENGLAND & WALES 1990 - 2003

Oligopoly

RPI-X RPI-X

Generators

Transmission

Consumers0% / -17%

Suppliers

Distribution

RETAIL MARKET

-14%

WHOLESALE MARKET

Physical Electricity Flow

Competitive

MonopolyMonopoly

Contract Flow

Europe I 14John Bower

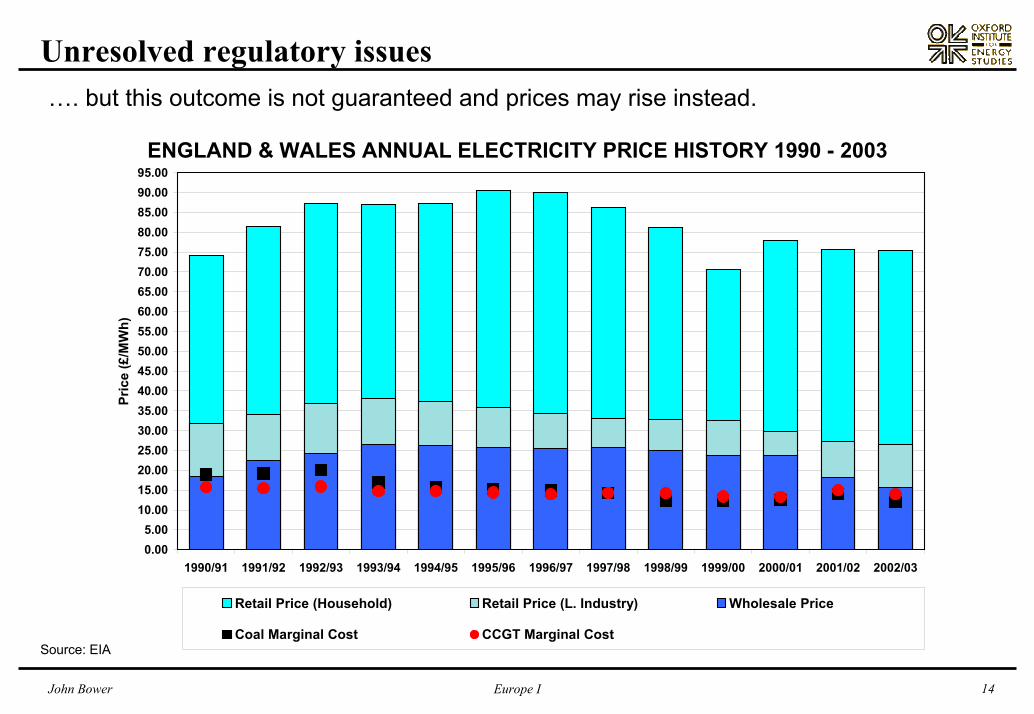

Unresolved regulatory issues…. but this outcome is not guaranteed and prices may rise instead.

ENGLAND & WALES ANNUAL ELECTRICITY PRICE HISTORY 1990 - 2003

Source: EIA

0.005.00

10.0015.0020.0025.0030.0035.0040.0045.0050.0055.0060.0065.0070.0075.0080.0085.0090.0095.00

1990/91 1991/92 1992/93 1993/94 1994/95 1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02 2002/03

Pric

e (£

/MW

h)

Retail Price (Household) Retail Price (L. Industry) Wholesale Price

Coal Marginal Cost CCGT Marginal Cost

Europe I 15John Bower

Unresolved regulatory issuesNational regulation is still required to create and maintain a competitive industry…

SHARE OF COAL GENERATION CAPACITY IN ENGLAND & WALES

Source: EIA

0%

20%

40%

60%

80%

100%

Apr-90

Oct-90

Apr-91

Oct-91

Apr-92

Oct-92

Apr-93

Oct-93

Apr-94

Oct-94

Apr-95

Oct-95

Apr-96

Oct-96

Apr-97

Oct-97

Apr-98

Oct-98

Apr-99

Oct-99

Apr-00

Oct-00

Apr-01

Oct-01

Shar

e of

Coa

l Gen

erat

ion

Cap

acity

NationalPowerBEGL

InternationalPowerInnogy

AES

TXU/Eastern

EdF

AEP

Edison

PowerGen

ScottishPowerALCAN

Europe I 16John Bower

Unresolved regulatory issues…. but many countries still pursue the ‘national champion’ objective….

EU GENERATION CAPACITY CONCENTRATION RATIO (3 FIRM) 2001

SOURCE: European Commission, Company Accounts, OIES estimates

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gre

ece

Fran

ce

Irela

nd

Bel

gium

Port

ugal

Italy

Spai

n

Swed

en

Den

mar

k

Finl

and

Aus

tria

Net

herla

nds

Ger

man

y

Nor

way UK

Shar

e of

Tot

al N

et S

uppl

y (%

)

Europe I 17John Bower

Unresolved regulatory issues… and vertical integration between concentrated generation sector and monopoly ‘wires’

Control Areas of the German Transmission System Operators as at 1 Jan 2000

Control Areas of the German Transmission System Operators as at 1 Jan 2001

Source: Source: DVG (Deutsche Verbundbesellschaft) http://www.dvg-heidelberg.de/extern/DVG/res.nsf/files/Regelzonen2001-GB.pdf/$file/Regelzonen2001-GB.pdf

Europe I 18John Bower

Unresolved regulatory issuesCross-border mergers may now be preventing access to transmission / distribution ….

EUROPEAN INVESTMENTS OF EDF (APR 2002)

5

6,18

9

1 7,8,15

10, 11, 13

2, 143, 16, 17

4

12

1. Estag 25% 15. Bert 89%

2. Elcogas 29.1% 16. Italenergia 18%

3. ISE 30% 17. Montedison 97%

4. Pego 10% 18. ATEL 13%

5. Graningue 36%

6. Motor Colombus 20%

7. Edasz 29%

8. Demasz 50.0%

9. Ech 58%

10. London Elec. 100%

11. SWEB 100%

12. EnBW 34%

13. Seaboard 100%

14. Hidrocantabrico 59%

Europe I 19John Bower

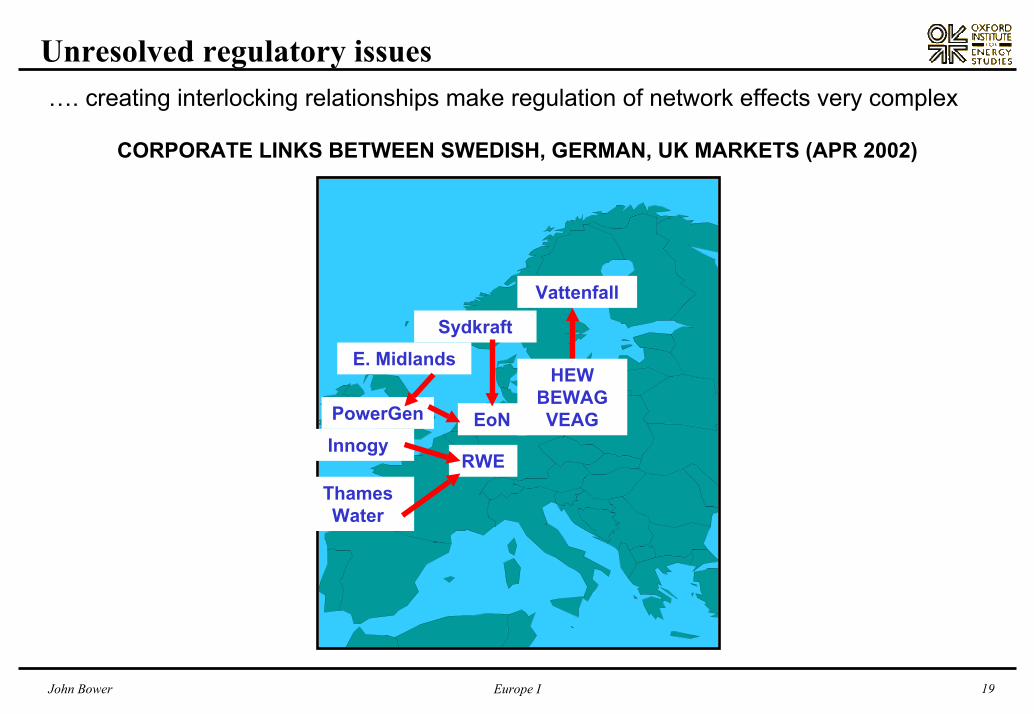

Unresolved regulatory issues…. creating interlocking relationships make regulation of network effects very complex

CORPORATE LINKS BETWEEN SWEDISH, GERMAN, UK MARKETS (APR 2002)

Sydkraft

Vattenfall

PowerGen

HEW BEWAG VEAGEoN

E. Midlands

InnogyRWE

Thames Water

Europe I 20John Bower

Unresolved regulatory issuesAll national governments want to intervene to set national energy policy….

RECENT BRITISH ENERGY HEADLINES

28 Aug 02 British Energy drained by low prices-minister

01 Sep 02 British Energy ponders US sale

06 Sep 02 Nuclear firm British Energy begs for bailout

07 Sep 02 British Energy shares suspended as company warns of insolvency

08 Sep 02 Ministers offers £410 million loan to British Energy

09 Sep 02 British Energy falls almost 80 pct after LSE lifts trading curbs

26 Sep 02 Ministers extend loan to British Energy and increase it to £500

18 Sep 03 Government sets deadline on British Energy restructuring

22 Sep 03 Nuclear plants may get new lease of life

02 Oct 03 ??????

Europe I 21John Bower

Unresolved regulatory issues… usually under the guise of energy security…

GENERATION TECHNOLOGY CAPACITY SHARE IN ENGLAND & WALES (Apr 1990 – Mar 2004)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Apr-90

Oct-90

Apr-91

Oct-91

Apr-92

Oct-92

Apr-93

Oct-93

Apr-94

Oct-94

Apr-95

Oct-95

Apr-96

Oct-96

Apr-97

Oct-97

Apr-98

Oct-98

Apr-99

Oct-99

Apr-00

Oct-00

Apr-01

Oct-01

Apr-02

Oct-02

Apr-03

Oct-03

Cap

acity

Sha

re b

y Fu

el a

nd G

ener

atio

n Te

chno

logy

OCGT

Oil

Pump Store

Small Coal

Medium Coal

CCGT

Large Coal

Magnox

AGR/PWR

Hydro

Europe I 22John Bower

Unresolved regulatory issues…but is in conflict with the environmental objectives of EUETS and LCPD…

EU EMISSIONS TRADING SCHEME AND LARGE COMBUSTION PLANT DIRECTIVES

Precursor

2003 – 2004

National Plan

Formulation

Phase I

2005 – 2007

CO2 only

Allocation only

Phase II

2008 – 2012

CO2 + other gases

Allocation + Auctions

EU

Emissions Trading Scheme

Phase I

2004 – 2007

SOx, NOx, dust

ELV or NP

Derogation Phase

2008 – 2015

SOx, NOx, dust

ELV or 20k hr derogation

Precursor

2002 - 2003

National Plan

Formulation

EU

Large Combustion

Plant Directive

Source: EIA

Europe I 23John Bower

Unresolved regulatory issues…even the EU Renewables Directive 10% target by 2010 is really about energy security

EUROPEAN ELECTRICITY GENERATION OUTPUT 2000

Source: EIA

0

100

200

300

400

500

600

700

800

900

Rus

sia

Ger

man

yU

KIta

lyPo

land

Spai

nTu

rkey

Ukr

aine

Net

herla

nds

Cze

ch R

epub

licFr

ance

Gre

ece

Kaz

akhs

tan

Uzb

ekis

tan

Bel

gium

Rom

ania

Port

ugal

Den

mar

kB

elar

usFi

nlan

dIre

land

Hun

gary

Yugo

slav

iaB

ulga

riaA

zerb

aija

nA

ustr

iaTu

rkm

enis

tan

Slov

akia

Esto

nia

Mac

edon

ia, T

FYR

Bos

nia

and

HG

Swed

enC

roat

iaSl

oven

iaM

oldo

vaA

rmen

iaLi

thua

nia

Mal

taG

eorg

iaLa

tvia

Kyr

gyzs

tan

Switz

erla

ndO

ther

Nor

way

Tajik

ista

nA

lban

iaIc

elan

d

Ann

ual G

ener

atio

n O

utpu

t (TW

h)

Thermal Nuclear Hydro Geothermal and Other

Europe I 24John Bower

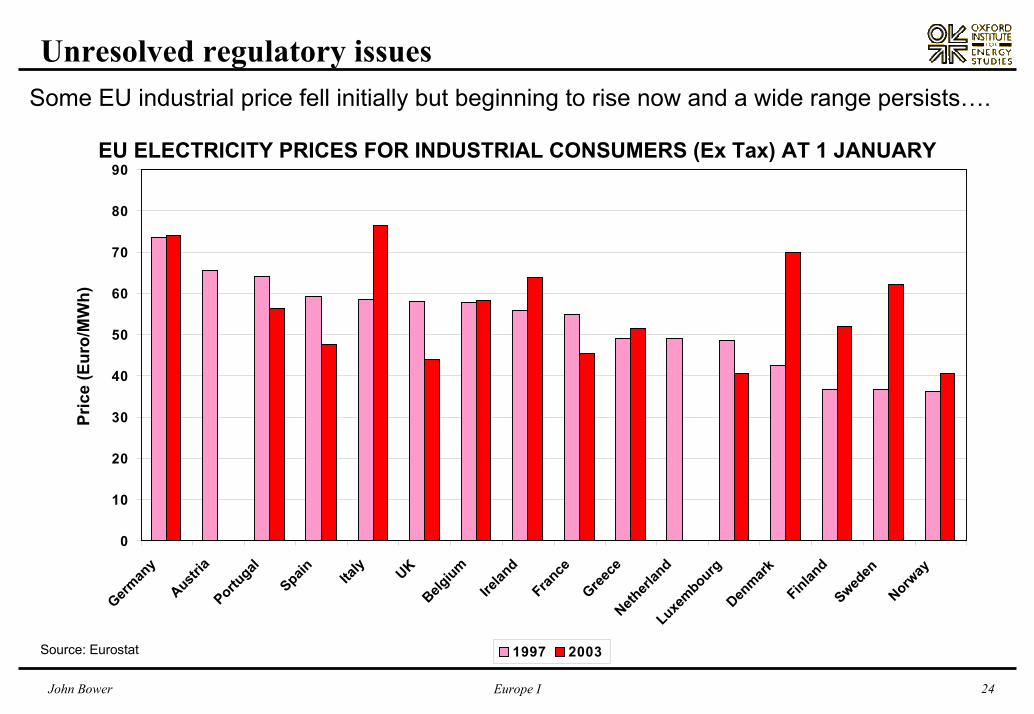

Unresolved regulatory issuesSome EU industrial price fell initially but beginning to rise now and a wide range persists….

EU ELECTRICITY PRICES FOR INDUSTRIAL CONSUMERS (Ex Tax) AT 1 JANUARY

Source: Eurostat

0

10

20

30

40

50

60

70

80

90

German

y

Austria

Portugal

Spain Italy UK

Belgium

Irelan

d

France

Greece

Netherl

and

LuxembourgDen

markFinlan

dSwed

enNorw

ayPr

ice

(Eur

o/M

Wh)

1997 2003

Europe I 25John Bower

Unresolved regulatory issues…. while household prices only fell a little overall and went up a lot in Scandinavia

EU ELECTRICITY PRICES FOR HOUSEHOLD CONSUMERS (Ex Tax) AT 1 JANUARY

Source: Eurostat

0

20

40

60

80

100

120

140

160

Italy

German

yPortu

galBelg

iumLuxe

mbourg

Austria

France

Spain UKNeth

erlan

d

Irelan

dGree

ceSwed

enNorw

ayFinlan

dDen

markPr

ice

(Eur

o/M

Wh)

1997 2003

Europe I 26John Bower

Speaker

John Bower is a Senior Research Fellow at the Oxford Institute for Energy Studies which is an independent research charity affiliated to Oxford University and dedicated to advanced research in the social science aspects of energy. John joined OIES in November 2001 and his research interest is in the emergence and evolution of integrated cross-border electricity and gas markets. Specifically; the development of efficient pricing and investment mechanisms for energy, transmission capacity, and emissions.

Before joining the OIES, John completed his PhD at London Business School and his previous career was in the commodity industry. His experience ranges from energy trading, at Marc Rich & Co, to risk management consultancy, with Coopers & Lybrand, advising commodity traders, producers and processors in base metal, precious metal, ‘softs’ and energy markets. Immediately prior to his PhD he was Global Controller Metals/Commodities at Deutsche Morgan Grenfell.

Oxford Institute for Energy Studies

57 Woodstock Road

Oxford OX2 6FA

United Kingdom

Telephone: +44 (0)1865 889 125

Facsimile: +44 (0)1865 310 527

Email: [email protected]

URL: http://www.oxfordenergy.org