Embed Size (px)

Citation preview

European Commission /

Taxation and Customs Union

Taxation trends in the

European Union

Edition 2010

Marco FantiniHead of Sector “Quantitative Analysis of Taxation”

Taxation and Customs Union DGEuropean Commission

European Commission /

Taxation and Customs Union

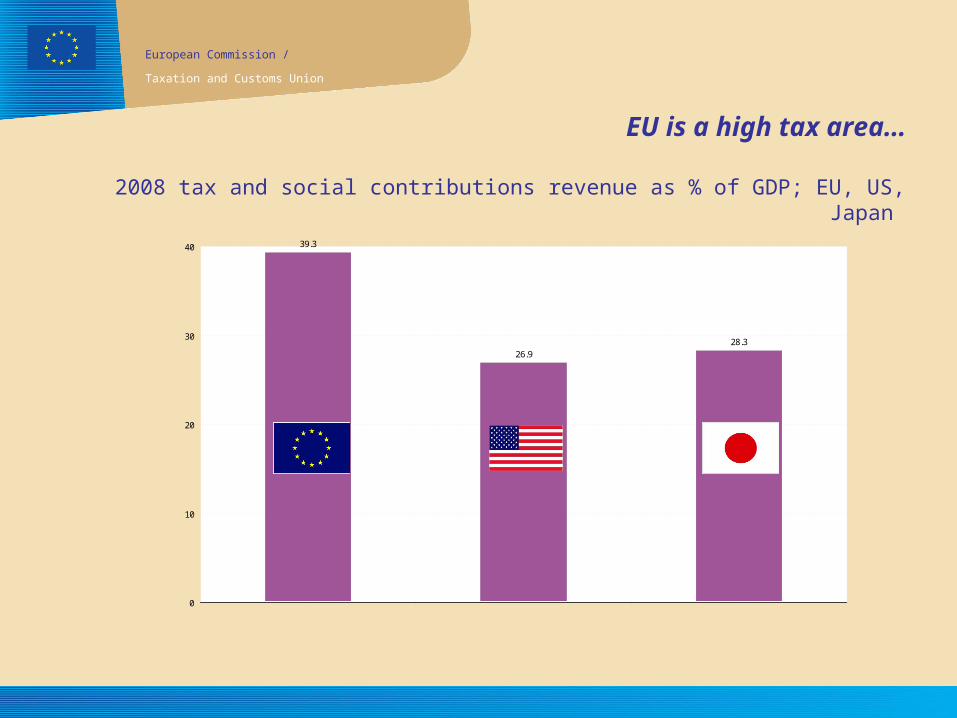

EU is a high tax area…

2008 tax and social contributions revenue as % of GDP; EU, US, Japan

39.3

26.928.3

0

10

20

30

40

E U -2 7 U S JP

European Commission /

Taxation and Customs Union

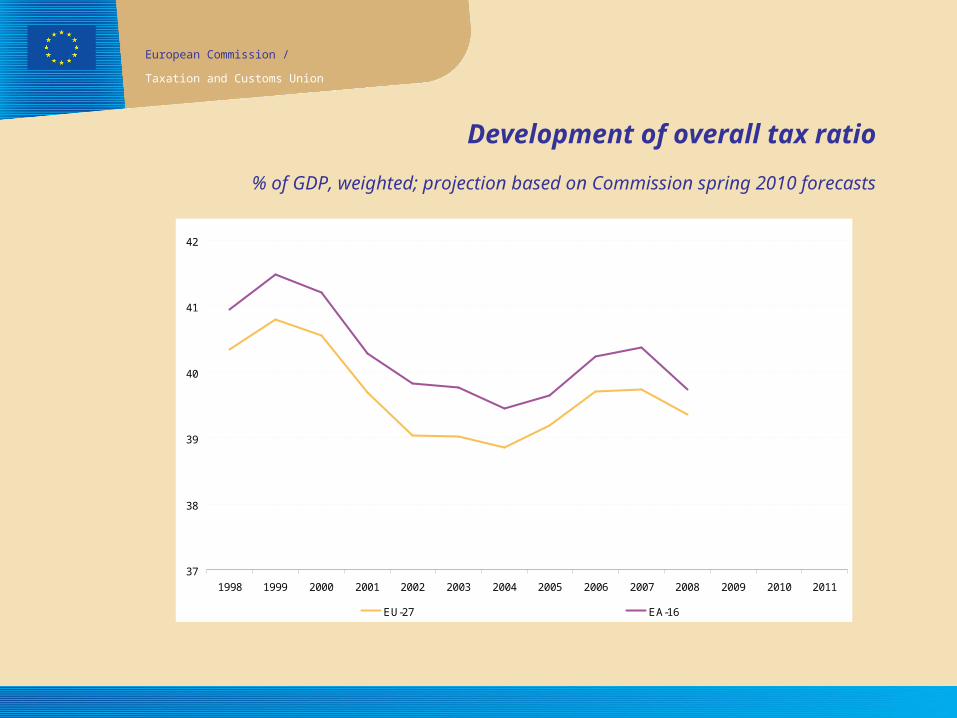

Development of overall tax ratio

% of GDP, weighted; projection based on Commission spring 2010 forecasts

37

38

39

40

41

42

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

EU-27 EA-16

%

European Commission /

Taxation and Customs Union

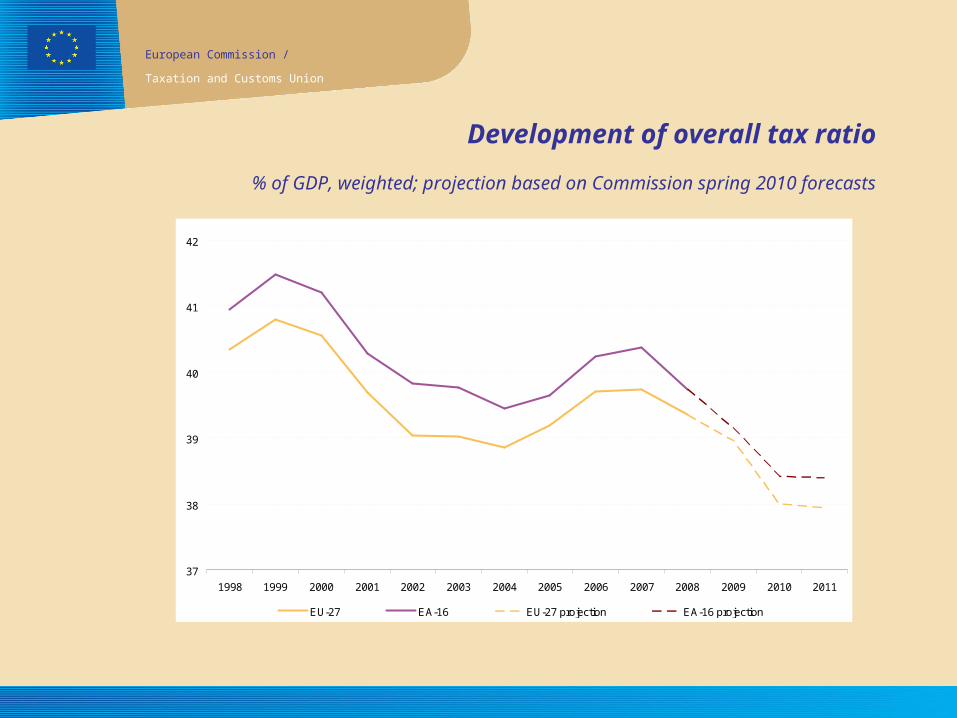

Development of overall tax ratio

% of GDP, weighted; projection based on Commission spring 2010 forecasts

37

38

39

40

41

42

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

EU-27 EA-16 EU-27 projection EA-16 projection

%

European Commission /

Taxation and Customs Union

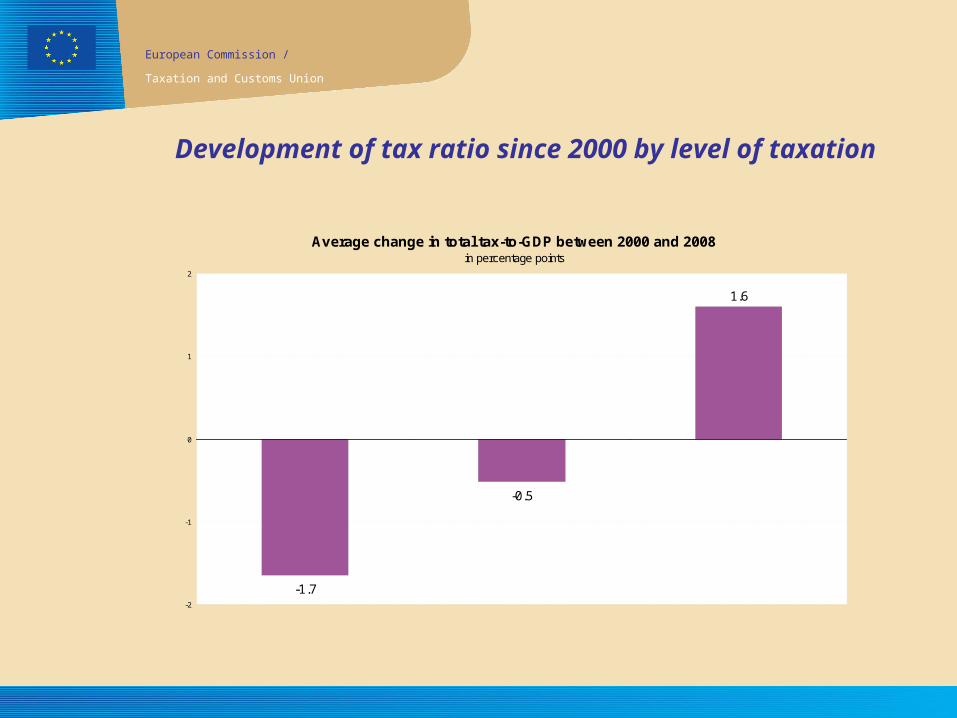

Development of tax ratio since 2000 by level of taxation

Average change in total tax-to-GDP between 2000 and 2008in percentage points

-1.7

-0.5

1.6

-2

-1

0

1

2

Medium tax countries

Low tax countries

High tax countries

European Commission /

Taxation and Customs Union

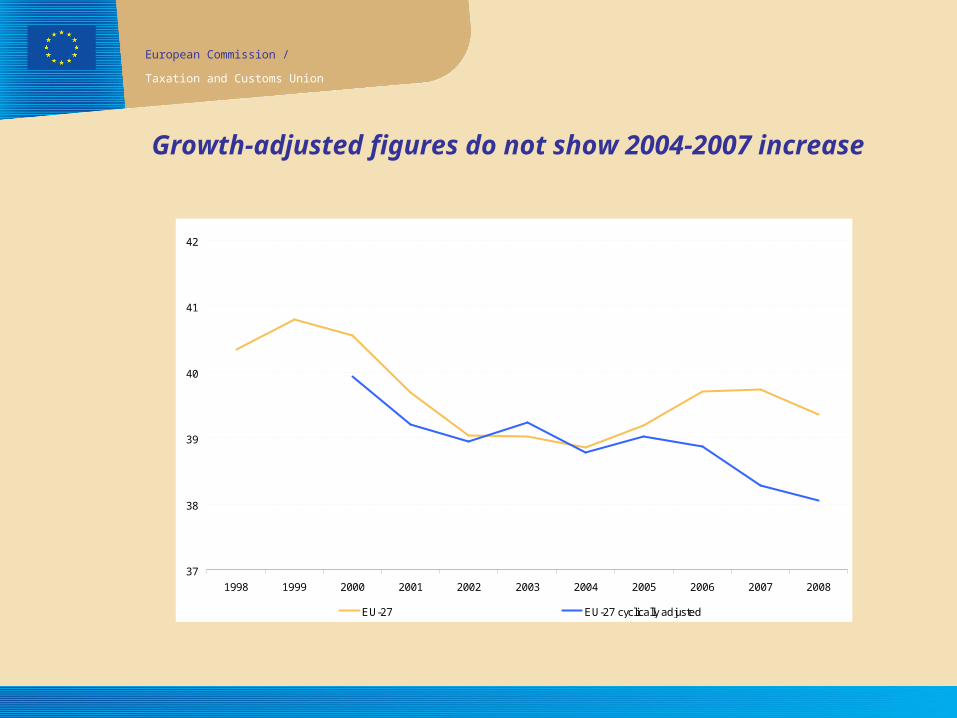

Growth-adjusted figures do not show 2004-2007 increase

37

38

39

40

41

42

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

EU-27 EU-27 cyclically adjusted

%

European Commission /

Taxation and Customs Union

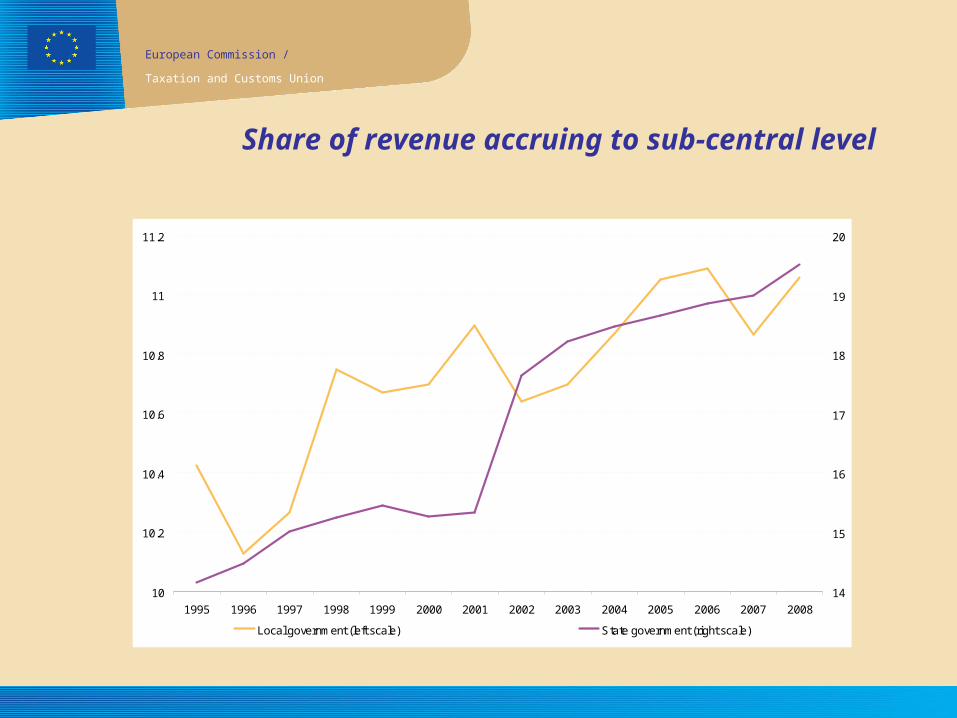

Share of revenue accruing to sub-central level

10

10.2

10.4

10.6

10.8

11

11.2

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 200814

15

16

17

18

19

20

Local government (left scale) State government (right scale)

European Commission /

Taxation and Customs Union

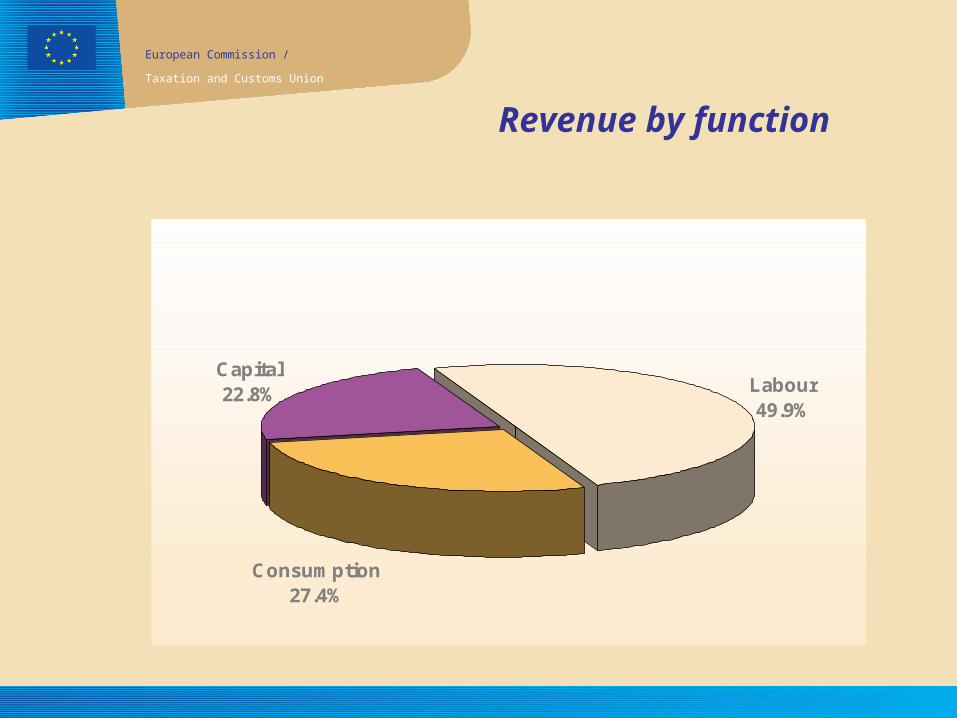

Revenue by function

Capital22.8% Labour

49.9%

Consumption27.4%

2008

European Commission /

Taxation and Customs Union

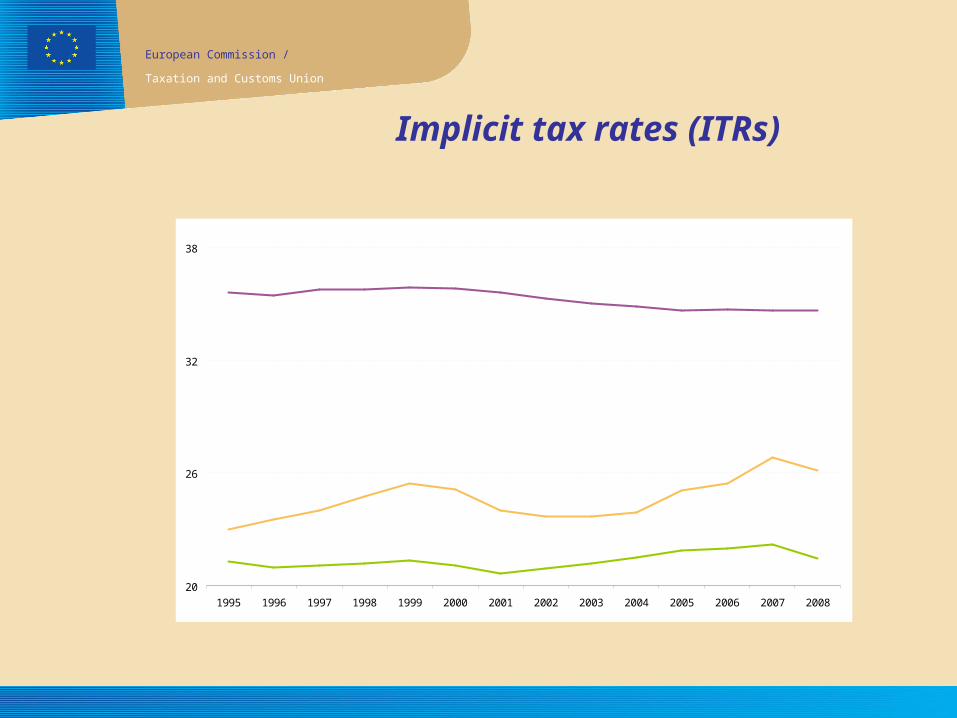

Implicit tax rates (ITRs)

20

26

32

38

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

%

ITR Capital

ITR Consumption

ITR Labour

European Commission /

Taxation and Customs Union

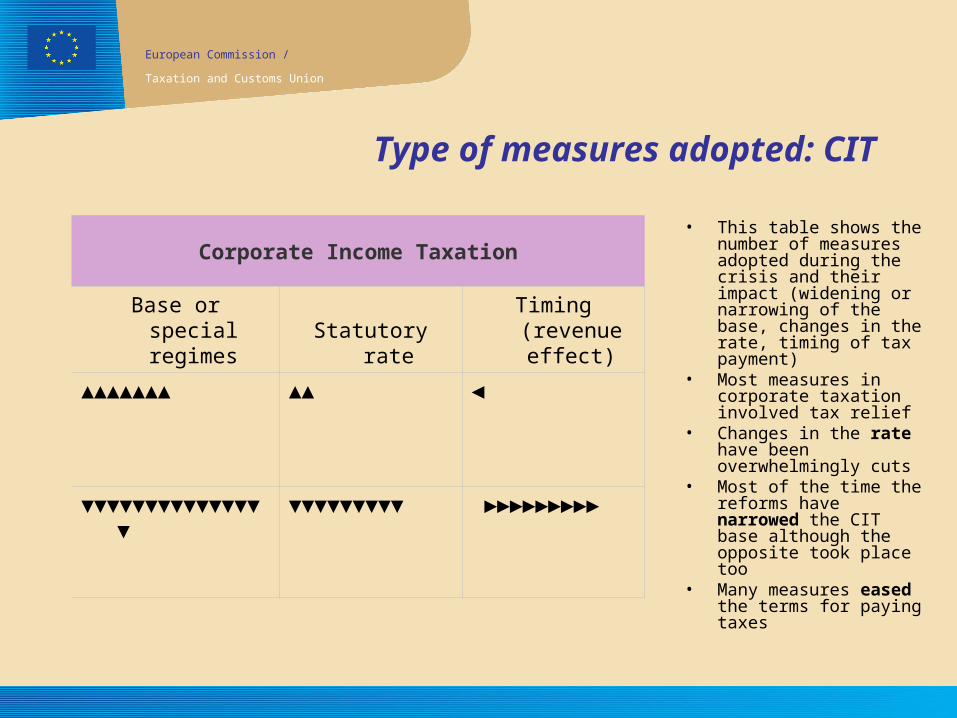

Type of measures adopted: CIT

Corporate Income Taxation

Base or special regimes Statutory rate

Timing (revenue effect)

▲▲▲▲▲▲▲ ▲▲ ◄

▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼

▼▼▼▼▼▼▼▼▼

►►►►►►►►►

• This table shows the number of measures adopted during the crisis and their impact (widening or narrowing of the base, changes in the rate, timing of tax payment)

• Most measures in corporate taxation involved tax relief

• Changes in the rate have been overwhelmingly cuts

• Most of the time the reforms have narrowed the CIT base although the opposite took place too

• Many measures eased the terms for paying taxes

European Commission /

Taxation and Customs Union

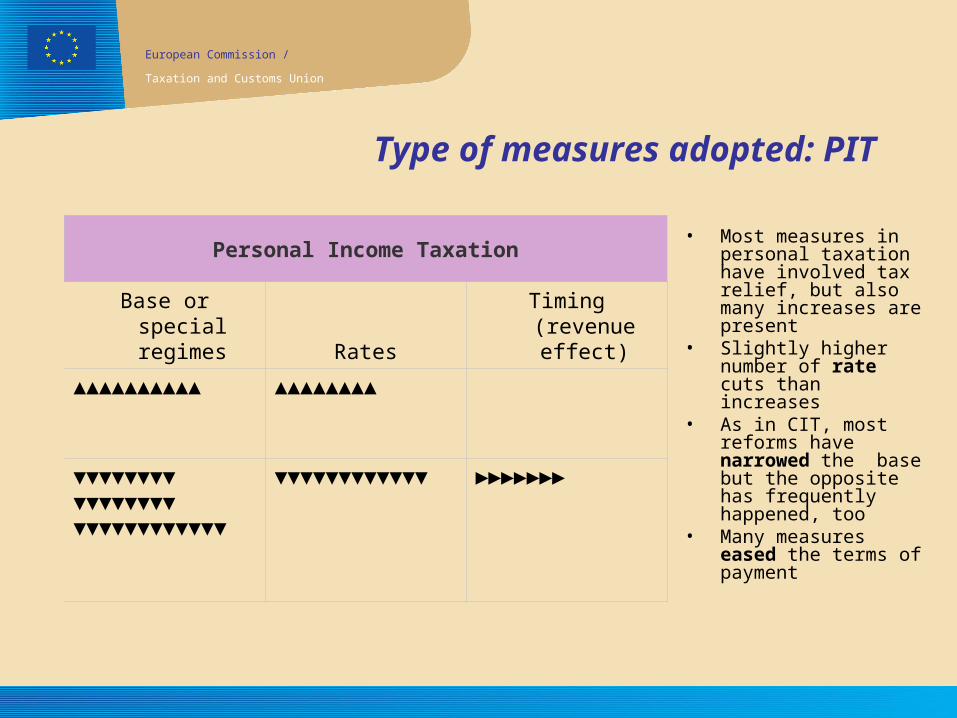

Type of measures adopted: PIT

• Most measures in personal taxation have involved tax relief, but also many increases are present

• Slightly higher number of rate cuts than increases

• As in CIT, most reforms have narrowed the base but the opposite has frequently happened, too

• Many measures eased the terms of payment

Personal Income Taxation

Base or special regimes Rates

Timing (revenue effect)

▲▲▲▲▲▲▲▲▲▲

▲▲▲▲▲▲▲▲

▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼

▼▼▼▼

▼▼▼▼▼▼▼▼▼▼▼▼

►►►►►►►

European Commission /

Taxation and Customs Union

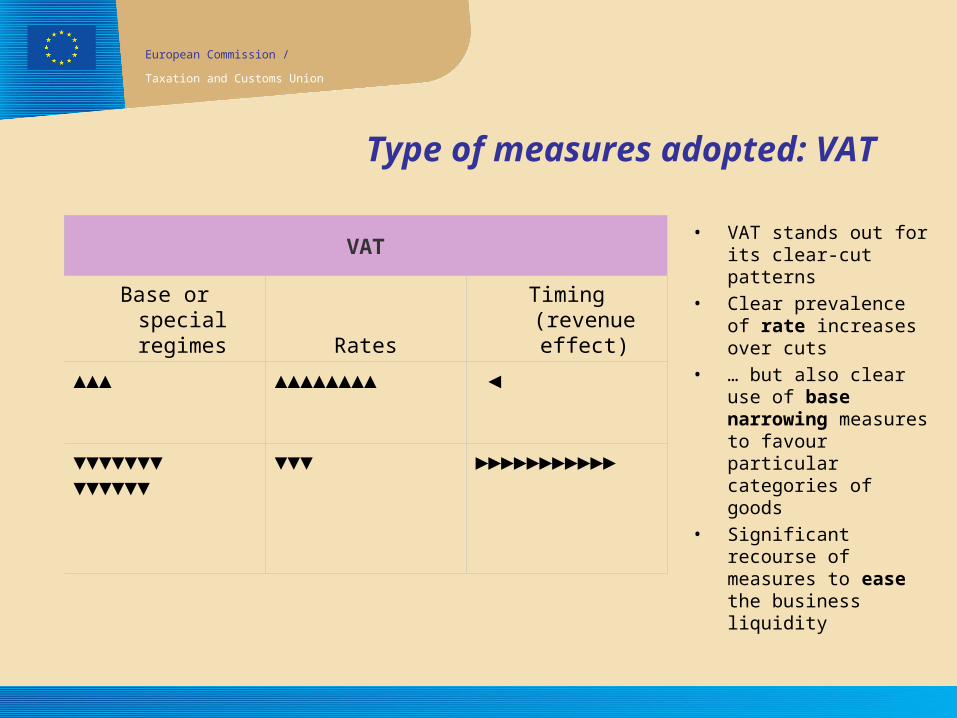

Type of measures adopted: VAT

• VAT stands out for its clear-cut patterns

• Clear prevalence of rate increases over cuts

• … but also clear use of base narrowing measures to favour particular categories of goods

• Significant recourse of measures to ease the business liquidity

VAT

Base or special regimes Rates

Timing (revenue effect)

▲▲▲ ▲▲▲▲▲▲▲▲ ◄

▼▼▼▼▼▼▼▼▼▼▼▼▼

▼▼▼ ►►►►►►►►►►►

European Commission /

Taxation and Customs Union

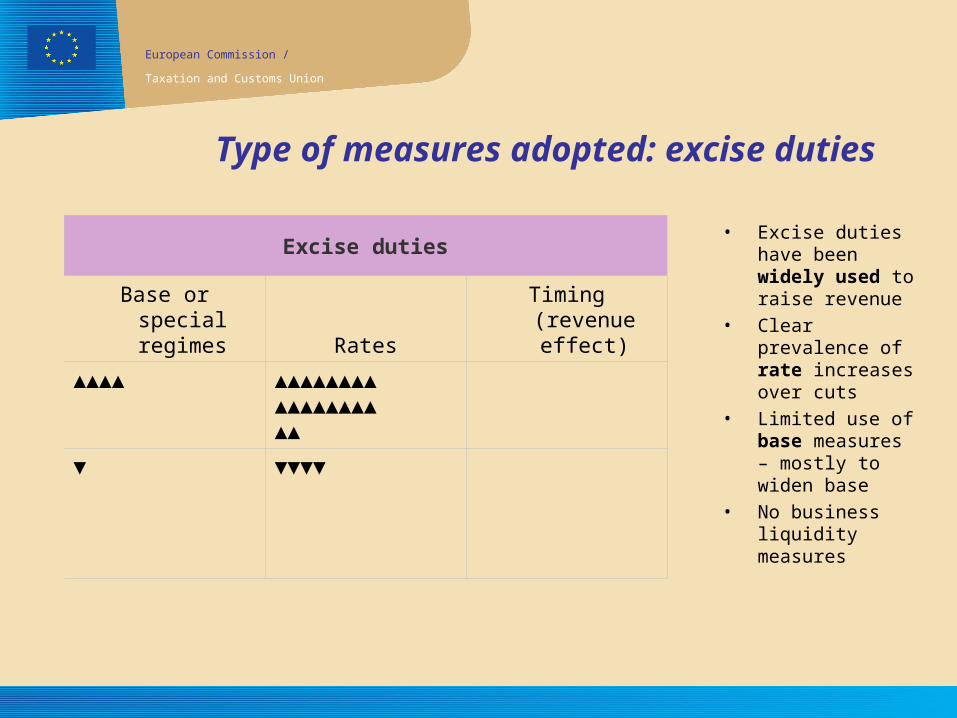

Type of measures adopted: excise duties

• Excise duties have been widely used to raise revenue

• Clear prevalence of rate increases over cuts

• Limited use of base measures – mostly to widen base

• No business liquidity measures

Excise duties

Base or special regimes Rates

Timing (revenue effect)

▲▲▲▲ ▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲

▼ ▼▼▼▼

European Commission /

Taxation and Customs Union

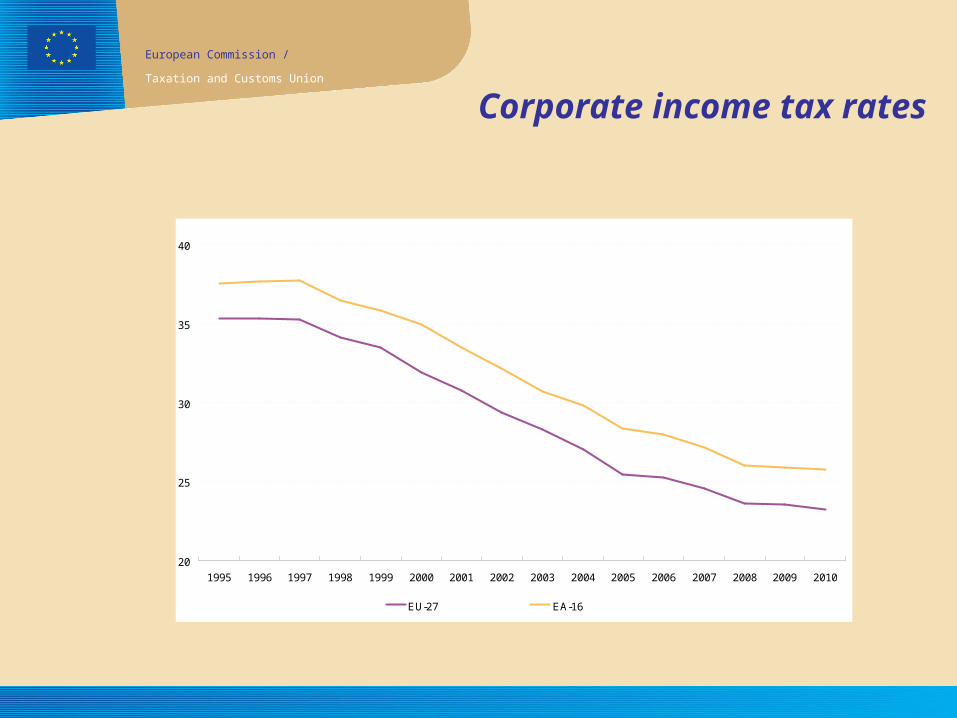

Corporate income tax rates

20

25

30

35

40

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

EU-27 EA-16

European Commission /

Taxation and Customs Union

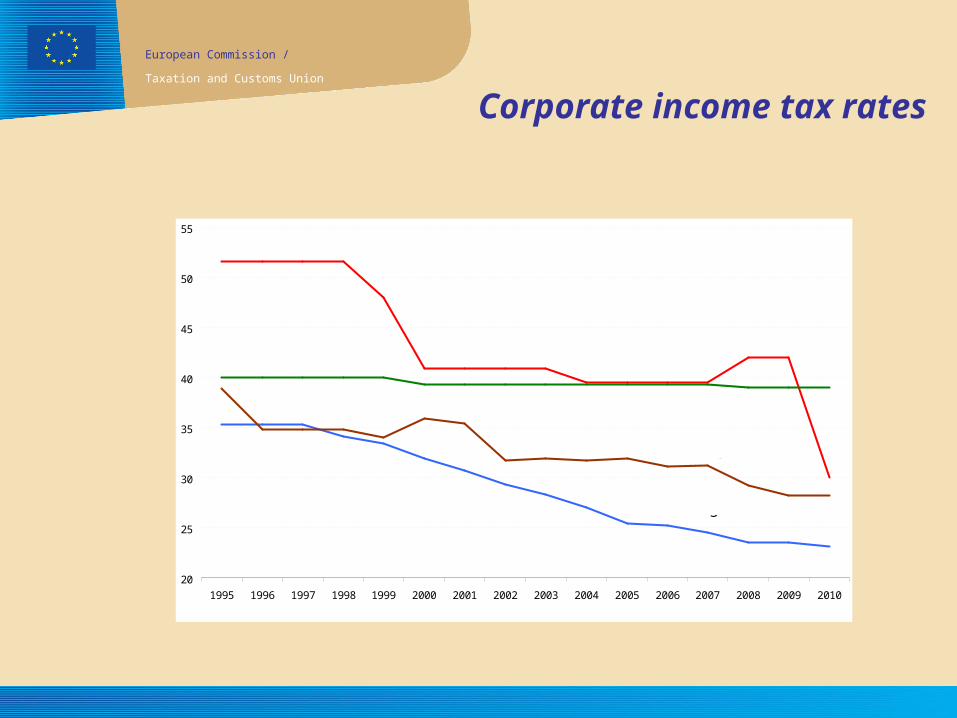

Corporate income tax rates

20

25

30

35

40

45

50

55

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

United States

BRIC average

EU average

J apan

European Commission /

Taxation and Customs Union

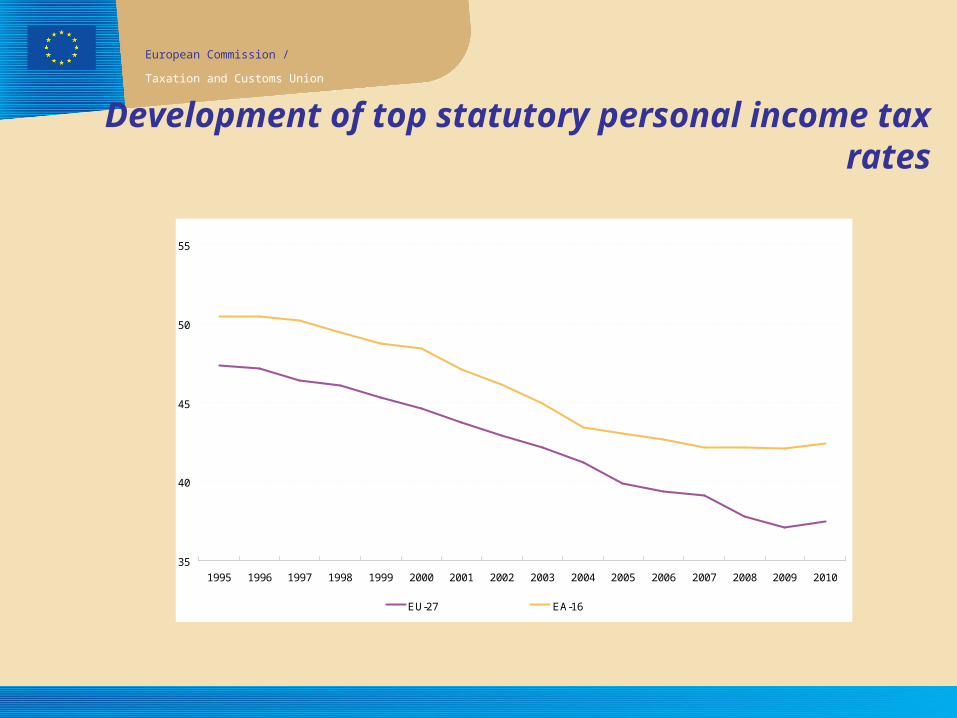

Development of top statutory personal income tax rates

35

40

45

50

55

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

EU-27 EA-16

European Commission /

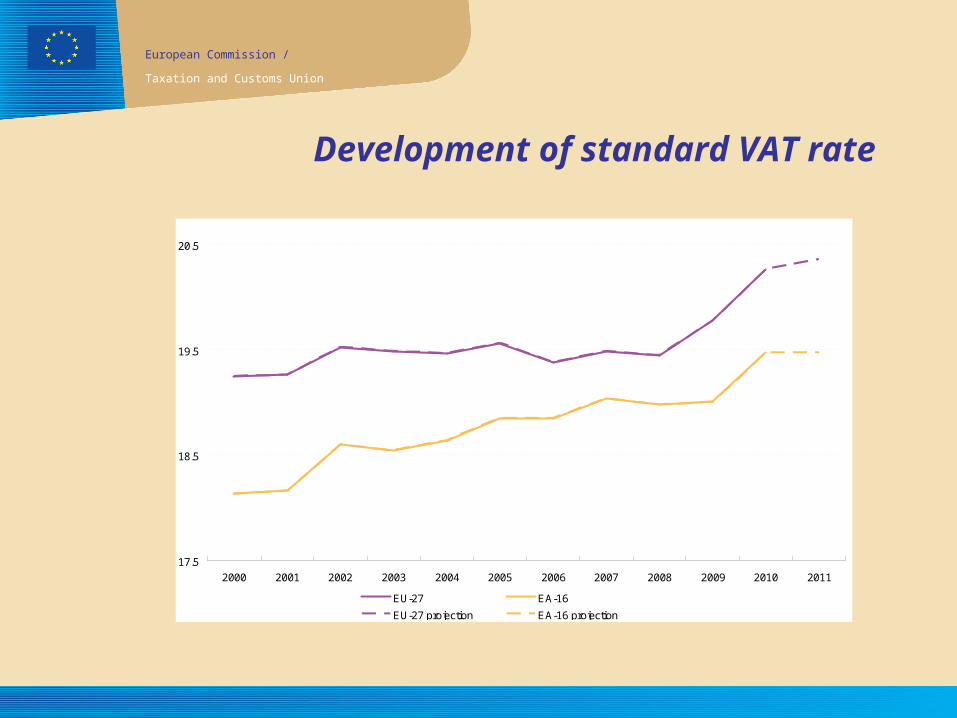

Taxation and Customs Union

Development of standard VAT rate

17.5

18.5

19.5

20.5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

EU-27 EA-16

EU-27 projection EA-16 projection

European Commission /

Taxation and Customs Union

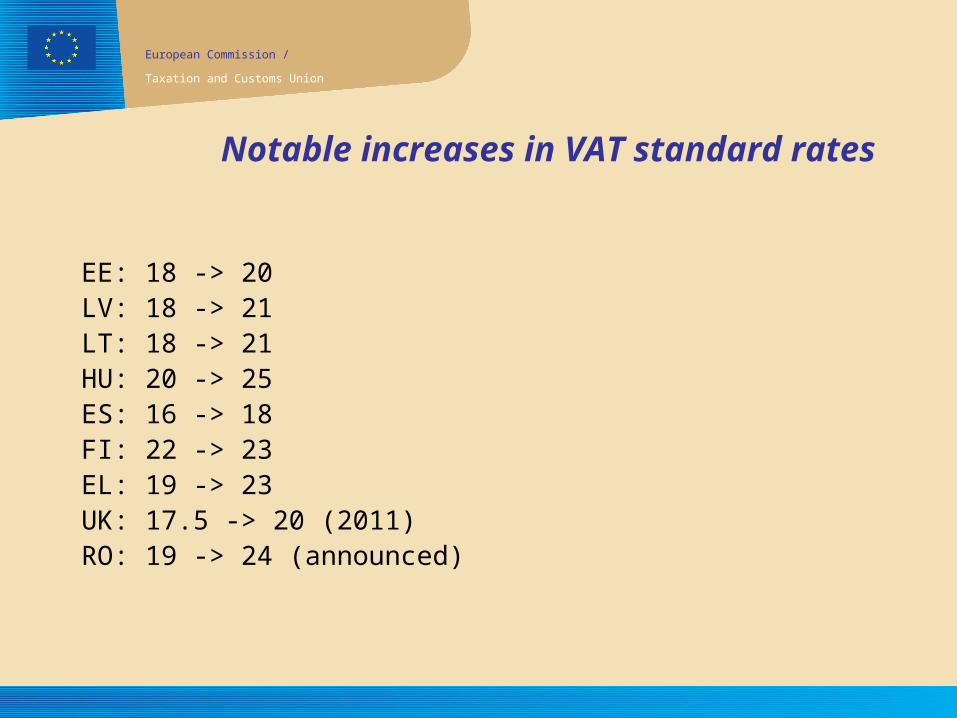

Notable increases in VAT standard rates

EE: 18 -> 20LV: 18 -> 21LT: 18 -> 21HU: 20 -> 25ES: 16 -> 18FI: 22 -> 23EL: 19 -> 23UK: 17.5 -> 20 (2011)RO: 19 -> 24 (announced)

European Commission /

Taxation and Customs Union

Additional information

• The full report and an executive summary are available at the following address:

• http://ec.europa.eu/taxtrends