Embed Size (px)

Citation preview

EU-ASEAN BUSINESS NETWORKS

Your Gateway to South-East Asia

European Association for Business and Commerce in Thailand

GATEWAY TO ASEAN

1999

1998

1997

1996

1995

1967

1977

1984

1993

2003

2007

2008

2009

2015

ASEAN formedIndonesiaMalaysia

PhilippinesSingapore

Thailand

Free flow ofGoodsServicesInvestmentSkilled labourFreer flow of capital

ASEAN Economic Community (AEC)

ASEAN Charter

PTA

Myanmar and Laos joined

AFTA

Vietnam joined

AFAS

Brunei Darussalam joined AIABali Concord II

Cebu Declaration

Cambodia joined

The Association of Southeast Asian Nations (ASEAN)

GATEWAY TO ASEAN

ASEAN Population: 625 million (9% of the world's population); Median age: 28 years EU Population: 500 million (7.3% of the world’s population); Median age: 40 years in EU

ASEAN GDP: USD 3.3 trillion; GDP Growth (2013): 5.2%EU GDP: USD 16.6 trillion; GDP Growth (2013): 0.1%

Foreign Direct Investment (FDI): US$115 billion The EU is the biggest provider of Foreign Direct Investment into ASEAN. EU FDI is 22% of the total in 2013

ASEAN Economic Community (AEC): moving towards a single market4 Pillars: Single Market and Production Base, Competitive Economic Region, Equitable Economic Development , Integration into the Global Economy

Free Trade Agreements in place: China (ACFTA), Japan (AJCEP), Korea (AKFTA), India (AITIG), Australia-NZ (AANZFTA), and EU has concluded a FTA with Singapore and is negotiating FTAs with several other ASEAN countries (Vietnam, Thailand, Malaysia, Indonesia)

ASEAN key facts

GATEWAY TO ASEAN

Year of entry into ASEAN

Population

Million

GDP

$Billion

GDP per capita

% of US level

Real growth of GDP, 2003 – 13

%

Brunei 1984 0.4 17 78 1.1

Cambodia 1999 15.1 15.5 2 7.8

Indonesia 1967 249.9 868.3 7 5.8

Laos 1997 6.8 10.9 3 7.8

Malaysia 1967 29.7 312.4 20 5

Myanmar 1997 62.8 59 2 8.6

Philippines 1967 98.4 272 5 5.4

Singapore 1967 5.4 295.7 103 6.3

Thailand 1967 67 387.2 11 3.8

Vietnam 1995 91.7 171.2 4 6.4

ASEAN key facts

Source: HIS, McKinsey Global Institute Analysis

GATEWAY TO ASEAN

ASEAN key economics

GATEWAY TO ASEAN

EU - ASEAN trade performance

GATEWAY TO ASEAN

EU - ASEAN Business Networks

European Association for Business and Commerce in Thailand

WHO &

WHERE

EU BUSINESS NETWORKS IN THE REGION

Attracting EU businesses into the region and supporting them in their market entry activities; Increasing EU Business’ leverage towards the ASEAN Governments.The projects

Increase and improve export and investment of EU businesses to the ASEAN regional market.Objectives

European businesses in Europe, in particular SMEs, with an interest in ASEAN markets. Existing European companies in ASEAN which need to increase their presence and visibility.

Target group

WHAT

Joint expertise, knowledge and experience of well-established European business support organizations with an extensive network in ASEAN and the EU.Expertise

ASEAN ROADSHOWVILNIUS, LITHUANIAMAY 12, 2015

PHILIPPINES – THE RISING TIGER OF ASIA

Philippines - Country facts

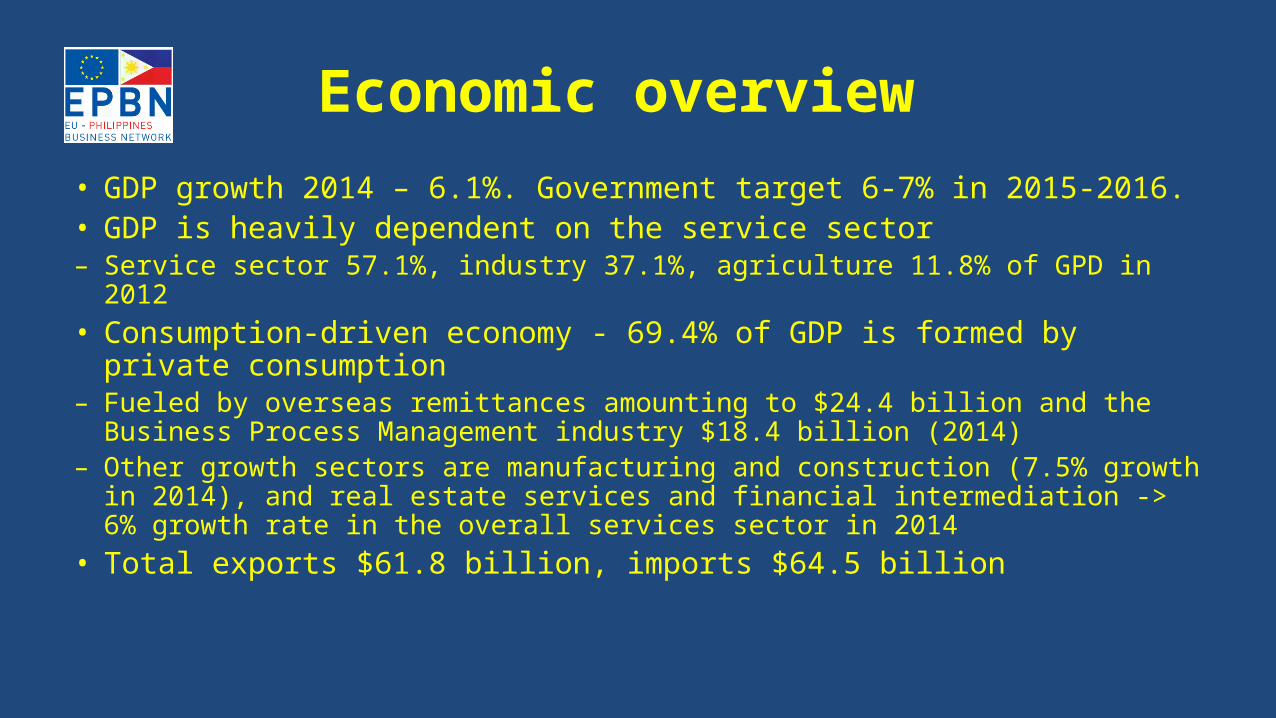

Economic overview

• GDP growth 2014 – 6.1%. Government target 6-7% in 2015-2016.

• GDP is heavily dependent on the service sector– Service sector 57.1%, industry 37.1%, agriculture 11.8% of GPD in 2012• Consumption-driven economy - 69.4% of GDP is formed by

private consumption– Fueled by overseas remittances amounting to $24.4 billion and the

Business Process Management industry $18.4 billion (2014)– Other growth sectors are manufacturing and construction (7.5% growth

in 2014), and real estate services and financial intermediation -> 6% growth rate in the overall services sector in 2014

• Total exports $61.8 billion, imports $64.5 billion

Investment climate

• Investment grade ratings (Fitch, S&P, Moody’s, Japan, Korea)

• FDI $6.2 billion in 2014, six times higher than in 2010 • Government incentives– Board of Investment - Investment Priority Plan– Philippine Economic Zone Authority (PEZA) for export-oriented

activities

• Foreign ownership– Foreigners can invest up to 100% equity in corporations,

partnerships and other entities in the Philippines, except in areas included in the Foreign Investments Negative List (FINL)

Lithuania-Philippines Bilateral Trade

Areas of opportunity• Energy/Renewables & Environmental technologies• ICT & IT/BPM• Food/Agriculture• Infrastructure & Transport • Maritime• Tourism• Healthcare/Medical & Pharmaceuticals• Consumer Goods/Retail• Financial Services• Manufacturing• Mining• Automotive

Areas of opportunity• Information Technology and Business Process Management

– Philippines is world no. 1 in voice services, no. 2 in non-voice services– Metro Manila region world no. 2 outsourcing/offshoring destination after

Bangalore– One of the fastest growing industries in the Philippines, CAGR 26% (2006-

2013)

• Environment / Renewable Energy– National Renewable Energy Program aims to triple the yearly production

capacity of renewable energy by 2030, currently 5030 MW. Program relies heavily on private sector.

– Solid waste management systems being developed according to the implemented act RA 9003. Aim to reach recycling ratio of 25 percent.

– Lots of untapped potential in the treatment of hazardous and medical waste.

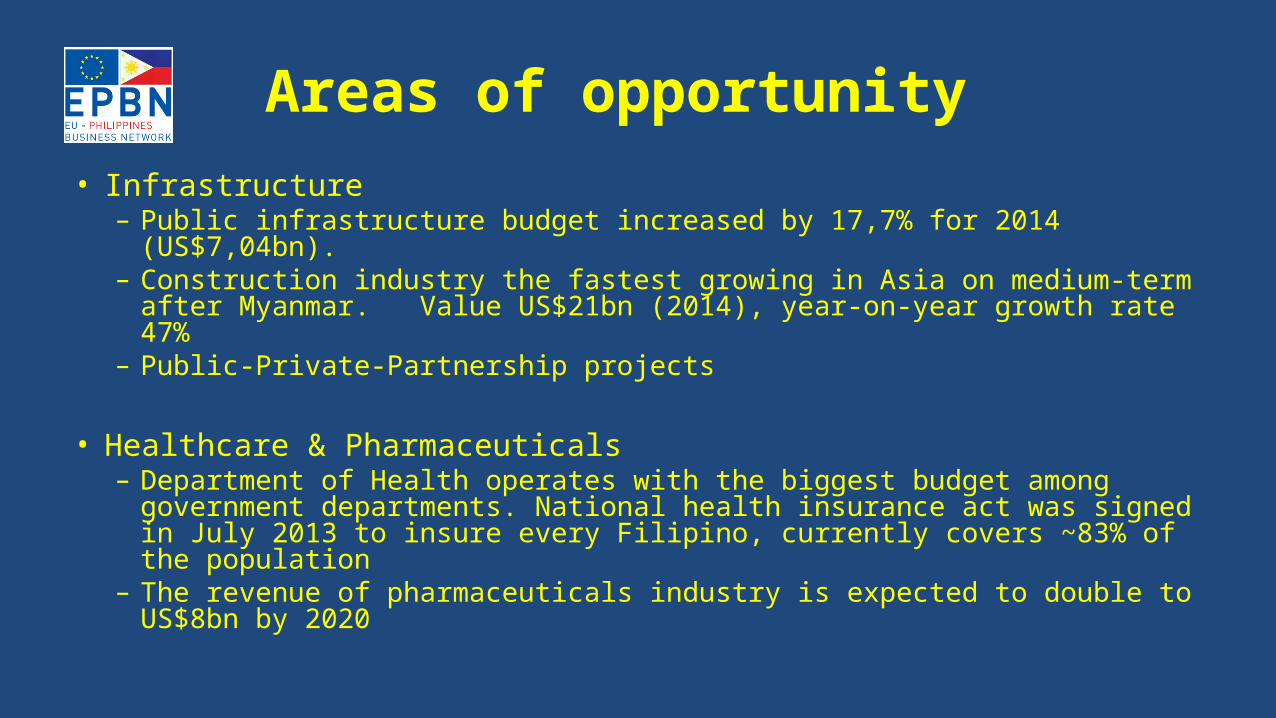

Areas of opportunity• Infrastructure

– Public infrastructure budget increased by 17,7% for 2014 (US$7,04bn). – Construction industry the fastest growing in Asia on medium-term after

Myanmar. Value US$21bn (2014), year-on-year growth rate 47%– Public-Private-Partnership projects

• Healthcare & Pharmaceuticals– Department of Health operates with the biggest budget among

government departments. National health insurance act was signed in July 2013 to insure every Filipino, currently covers ~83% of the population

– The revenue of pharmaceuticals industry is expected to double to US$8bn by 2020

Doing business in the Philippines

• Strengths– Strong macroeconomic

fundamentals– Educated, young, and

English-speaking labor force

– Improving governance– Renaissance of

manufacturing– Overseas remittances– Strategic geographic

location: launching pad for AEC

Doing business in the Philippines

• Strengths– Strong macroeconomic

fundamentals– Educated, young, and

English-speaking labor force

– Improving governance– Renaissance of

manufacturing– Overseas remittances– Strategic geographic

location: launching pad for AEC

• Challenges– Corruption– Red tape and Bureaucracy– High rate of poverty– Inefficient infrastructures– Low rates of investments

to GDP – Low Foreign Direct

Investments

EU-Philippines Business Network

• Partnership of eight chambers of commerce operating in Manila

EPBN Services

• Advocacy and market access– 14 industry-led sector committees & ad hoc support

• Business support–Market studies, business matching, new market entry

support, business development• Business missions–Ministerial & private sector business delegations

• Government relations– Embassies and Philippine government agencies