Embed Size (px)

Citation preview

Ethics in Banking A Human Folly or Systemic Failure

Dr Mohiuddin AlamgirFormer Director Policy and Planning United Nations International

Fund for Agricultural Development (IFAD) Rome and Former President Bangladesh Economic Association

Ethics in Banking A Human Folly or Systemic Failure

Governor Bangladesh Bank Dr Atiur RahmanDirector General Bangladesh Institute of Bank ManagementDistinguished GuestsLadies and GentlemenAssalamu Alaikum

Fourteen Distinguished public figures delivered Nurul Matin Memorial Lecture I thank BIBM Governing Board for making me the fifteenth I am not sure I am worthy of this honor From Justices to Ministers and academics all have spoken What can I add except a few words as a layman economist

I have not met Mr Nurul Matin but here I am standing before you to share my thought in memory of a distinguished banker that he was who clearly left a mark on the banking community during his life time

We are discussing ethics in banking BIBM is the right venue as I presume through its various training programs BIBM is developing characters of Bangladeshrsquos Bankers to practice ethical banking When BIBM opened its door in 1974 Bangladesh had 1512 scheduled bank branches with a total deposit of Tk 9132 crores today it is 9131 branches and Tk 6991837 crores in deposits For one in BIBM there is lot of character building exercises to keep all concerned straight The regulatory responsibility of the Bangladesh Bank has also multiplied when its regulatory authority remains truncated Both character and regulation appear out of sync with the desired optimum but there is no need to panic With Atiur at the helm of both character and regulation in his dual capacity we can rest assured that in due course we shall be able to sail through to safe waters until of course someone puts a hole in the boat and we are at the bottom of the sea Surely no one wants that to happen

1

I shall talk tonight more about principles and less about specifics on the assumption that if we get principles right anomalies in specifics of bank operations will be automatically taken care of though some gaps could still persist Gaps are good indicators of the banking systemrsquos health So though gaps are undesirable some measure of these are welcome as early warning Sounds odd but in an imperfect world it makes sense at least to me hopefully to you too

Ethics Banking and Ethics in Banking

Defining ethics banking and ethics in banking may sound straightforward but it is far from it

Let us start with ethics My preferred definition is ethics is the discipline and practice of applying value to human behavior to define the basic concepts and fundamental principles of decent human contact and conduct Then we have to explain what value is and what human behavior is Obviously value is not money value though it could be Value is a system of important and lasting beliefs pertaining to right and wrong fair and unfair good and bad and desirable and undesirable handed down in society through customs tradition religion and anchoring these families

Human behavior is expression of self (individual andor society) in action (physically andor emotionally) Values influence personal and social behavior and ethics defines what ldquogoodrdquo and ldquobadrdquo behaviors are We are still not out of the woods What is good for you may be bad for me and what is bad for me may be good for you We need to normalize across individuals and society and define ethics as the norm or value system which is acceptable to and to which the civilized society conforms to Ethics relates to values and moral principles used in communities in which a company enterprise bank operates

One of the strongest arguments for ethics that it is good business and good for business

Coming to banking it is about accepting deposits and lending both at a price called interest paid to compensate for foregone

2

consumption or charged for money which has alternative use for earning an income Dr ABM Azizul Islam in his memorial lecture summarized principal functions of bank as intermediation maturity transformation credit allocation and facilitation of payment flows In all cases banking functions are concerned with the future balancing individualsrsquo subjective time preference with individual enterprisesrsquo profit expectation in light of objective market realities in a manner such that bank itself is able to maximize profit In maximizing profit banks presumably protect shareholder interest who are owners depositors and borrowers all in the same breath creating a built in conflict of interest situation and making banking operations susceptible to the influence of unethical practices

So then what is ethics in banking It is trust efficiency openness transparency and accountability development and community involvement Trust brings savers and borrowers together through bankrsquos intermediation Trust allows banks to borrow short and lend long Trust bestows authority in banks to allocate resources to alternative uses albeit with some prompting from policy makers and supervisory authorities Trust underwrites banksrsquo role in payments and fund flow

Efficiency is at the core of sound and ethical banking Banking operations are expected to be carried out in a cost-effective way avoiding ostentatious expenditures that do not contribute to productivity Deposits are to be mobilized and deployed to alternative uses efficiently ensuring maximum possible returns to capital and owners of capital Efficiency will enhance public trust in banks

Ethical banking operations have to be open subject to legally required secrecy norm if any All payments and charges advances and investments and the like should be transparent for that matter all banking transactions should be available in public domain so

3

should annual audited financial accounts and statements Openness and transparency will enhance public trust in banks

Sound banking practices cannot grow without transparency and accountability Banking business is inherently intricate but all transactions have to be transparent so that accountability can be established without a shadow of doubt The general public is wary of the situation that banking scandals go unpunished because no one seems to be accountable for misdeeds and criminal conduct Transparency and accountability are foundations of good governance Transparency ensures timely access to good and reliable (accurate) information that is manageable and understandable and accountability establishes true hierarchy of responsibility for one set of actors to account for their action to another set Accountability is an institutionalized relationship between actors that is inherently confrontation but less so if perceived as achieving greatest good to greatest number Accountability has normative implication with the possibility of punitive action in case of non-compliance and violation of norms

Ethical banking is about inclusive growth and socioeconomic development that is environmentally sustainable In other words focus of ethical banking is on triple bottom line financial return for investors real delivered value for customers and sustainable social value for society Individual and corporate depositors expect to make a good return on their deposits and holdings of bank instruments so do borrowers from their investments financed by bank credit Both increase household corporate and government income on the income account sectoral production and value added on the production account and consumption investment exports and imports on the expenditure account The result is the same maximum possible growth of gross domestic product an outcome of banking operations supported by central bank guidance supervision and regulation as well as complementary developmental activities covering for example micro small and

4

medium enterprises sharecroppers agriculturalists and other underserved clients It is a pity one has to look through the fine prints of the Bangladesh Bank Order of 1972 amended through 2003 to look for opening for the Bangladesh Bank to indulge in development banking FOR ME THE CORE FUNCTION OF THE CENTRAL BANK IS TO PROMOTE GROWTH AND SOCIOECONOMIC DEVELOPMENT WITH FINANCIAL STABILITY Its penultimate role of lender of last resort is also geared towards growth and development with financial stability which may be threatened by run on a bank or on the banking system as a whole Financial inclusion is an inseparable corollary to financial stability Protection of the environment and preservation of the resource base is hallmark of sustainable development which has to be built into bankrsquos lending operations Hence ethics is development banking with financial stability and inclusion and environmental sustainability

Ethics is building up business environment by strengthening community bond

Ethical banking is concerned with the social and environmental impacts of Bankrsquos loans and investment Ethical banks share a common set of principles like transparency and socio-environmental aims of the projects they finance Environment is a key focus among ethical banks like green banking Banks in applying ethical principles are mindful of how the products of banks can be used unethically for example how borrowers use the money that is lent out by the bank in unethical ventures Ethically conscious banks encourage corporate practices that promote environmental stewardship consumer protection human rights and diversity avoiding businesses involved in drugs gambling weapons fossil fuel unsustainable production etc Ethical banking is what follows all rules and regulations of environment social justice and investment process maintaining good governance and not just focusing on profit alone at the cost of public interest

55

Ethical banking is about ethical bankers and ethical people Ethical banking can be managed only by people with good moral character The foundation of ethical banking is people To the extent ethics in banking is about trust between banks and clients it has to be upheld by people in banking that is bankers The quality of banking can never surpass the quality of bankers The concept of quality embodies first and foremost moral standing of bankers as people followed by efficiency effectiveness transparency accountability fairness and community involvement While systemic weaknesses can let you down as client in the ultimate analysis you are let down by people who runs banks and who supervises banks The malice in banking is malice in people in banks and linked to banks borrowers and others Unscrupulous bankers could let depositors down by poor asset choice deliberate or otherwise and borrowers could let banks down by poor project choice deliberate or otherwise This is possible because of information asymmetry which bankers and borrowers do take advantage of while depositors are caught at the short end

Let us recall what Justice Muhammad Habibur Rahman told us in his second Nurul Matin memorial lecture ldquoEthics is good behavior Laws regulations and oversight will be of little help if we do not have in the banking sector leaders with high ethical standard whose collective advice could define mores of conduct Many cases brought before the SC shows connivance between bank officials and the borrowerrdquo

Sifting through my predecessor speakers (Annex-1) I find engraved ethics in banking is the presence of and due disclosure (transparency) of fair practices with regard to terms and conditions of lending and other services No hidden charges no unannounced penalties no discrimination no foreclosure without due process no graft no favor without due process no sweeping under the rug of customer complaint no undermining of customer rights no denial of equitable treatment

6

Extending it further ethics is good investment ethics is a sound risk management system ethics helps building a cohesive society ethics is promoting democratic values ethics is promoting a pluralistic democracy ethics is promoting peace and harmony ethics is promoting tolerance ethics is promoting religious tolerance ethics is integrity not just compliance ethics is inspiration and not mere enforcement ethics is motivation and not punishment ethics is educational and not directional and finally ethics is open not secretive

What do these elements add up to A sound business environment that is good for all

We do faithfully subscribe to the ethical values in banking the real problem is with its practice We preach but shamelessly do not practice them

Ethics in Banking and Governance in Banking

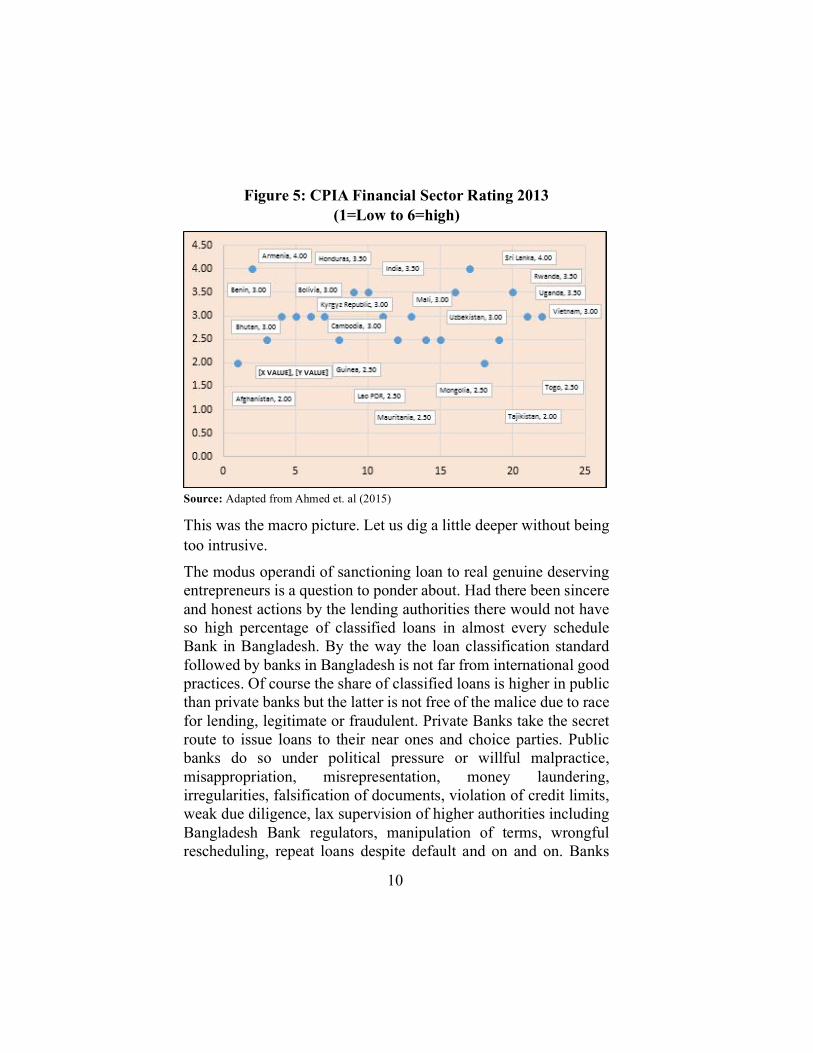

In front of this august gathering I do not want to belabor this point except pointing out that the situation is not good In NPL as well as capital adequacy Bangladesh trails behind its neighbors (Figures- 1 and 2) In a sample of 24 countries only three have worse record than Bangladesh in NPL Twenty do better (Figure-3) Among 37 countries 35 do better than Bangladesh in capital adequacy (Figure-4) In financial sector rating Bangladesh is in the middle with a score of 250 in a scale of 1 to 6 notably behind Benin Cambodia Mali and Rwanda (Figure-5) Having cited these figures I must recognize that the situation is improving by the day thanks to the Herculean efforts by Governor Atiur Rahman and colleagues in the face of lack of manpower and resources lack of independence and more important in the face of policy and political obstacles

Banks and financial institutions are controlled by parallel authorities Bangladesh bank the Banking Division of the Ministry

7

of Finance the Securities and Exchange Commission and the Microfinance Regulatory Authority and above all the Ministry of Finance This situation calls for a revisit as it is good neither for ethics in banking nor for good governance in banking

Figure 1 Bank Nonperforming Loans to Total Gross Loans 2000-2013 ()

Source Adapted from Ahmed etal (2015)

Figure 2 Bank Capital to Assets Ratio 2000-2013 ()

Source Adapted from Ahmed etal (2015)

8

Figure 3 Bank Nonperforming Loans to Total Gross Loans 2013 ()

Source Adapted from Ahmed etal (2015)

Figure 4 Bank Capital to Assets Ratio 2013

Source Adapted from Ahmed etal (2015)

9

Figure 5 CPIA Financial Sector Rating 2013 (1=Low to 6=high)

Source Adapted from Ahmed et al (2015)

This was the macro picture Let us dig a little deeper without being too intrusive

The modus operandi of sanctioning loan to real genuine deserving entrepreneurs is a question to ponder about Had there been sincere and honest actions by the lending authorities there would not have so high percentage of classified loans in almost every schedule Bank in Bangladesh By the way the loan classification standard followed by banks in Bangladesh is not far from international good practices Of course the share of classified loans is higher in public than private banks but the latter is not free of the malice due to race for lending legitimate or fraudulent Private Banks take the secret route to issue loans to their near ones and choice parties Public banks do so under political pressure or willful malpractice misappropriation misrepresentation money laundering irregularities falsification of documents violation of credit limits weak due diligence lax supervision of higher authorities including Bangladesh Bank regulators manipulation of terms wrongful rescheduling repeat loans despite default and on and on Banks

10

sanction loan against fictitious or non-existence companies with fictitious or concocted documents

State owned banks are supposed to be role models for private banks The reality is otherwise Please forgive me if I repeat a common knowledge around the world In Government Banks ruling power reigns and in private Banks rich elites reign In both cases crime is committed through falsification of documents How many times in the West and also in South Asia several years of accounts had to be revisited to put records straight Still the system is far from clean

The Bangladesh Bank is at the nerve center of banking governance The role of the Bangladesh Bank is to supervise monitor control and take punitive action against erring parties banks and defaulters alike Technically the Bangladesh Bank is doing everything by the book though sometimes inaction delayed action insufficient action inefficiency and lack of direction do creep in creating a sense of crisis that gets blown up due to over-politicization of all aspect of national life specially the Banking sector Even the Finance Minister lamented in the parliament that the main suspect in a major banking scandal could not be apprehended because of the political support he enjoyed Sceptics wonder aloud why so when Bangladesh Bank aggressively pursued the case of a Board member of a private bank to have him dismissed To be fair Bangladesh bank is now vigorously monitoring supervising and personally meeting the Board of Directors reminding them their rights and obligation and punitive action that might follow in the event of proven misconduct

Default will be less depositor interest will be protected and ethical questions will be manageable if borrowers are assisted with credit use and risk management credit use is monitored closely not just repayment records and bank itself practices sound risk management strategy and review and adjust it in light of evolving market condition

11

Banking Scandals Scams

Banking financial ethics is violated across the globe some on staggering scale Among many reasons for the 1997-1998 ethical underpinning was embodied in crony capitalism and inefficient allocation of credit to politically favored parties unethical conduct of currency speculators hot money flow into the banking system and excessive short term private borrowing to finance long term projects and poor loan quality Sounds familiar Some elements are not very far from what we are observing in Bangladesh banking in recent years

The Asian financial system and by proxy through linkages the world financial system suffered because market makers did not follow rules of the game There was human folly People let down people human beings erred to hurt other human beings And there was systemic failure as the banking system was unable to cope with the magnitude of the crisis with internal checks and balances either absent or not working effectively The crisis unfolded and played out fully under the very nose of the ministries of finance and the central banks from Thailand to Japan Korea Indonesia Malaysia Hong Kong and others All eventually abandoned closely held policies ran to the IMF to swallow the bitter pill that arguably made things worse and prolonged common manrsquos sufferings

During 2000s there have been many cases of banking improprieties which bred the ground for 2008 global financial crisis which defy logic and imagination noting the length to which individuals and enterprises would go to make illegal and immoral gains endangering the sustainability and stability of the entire financial system It is human folly and systemic failure again

People succumbed to greed and hurt other people and the system first opened up opportunities to fraud through deregulation and then failed to preempt unethical practices that ultimately hurt the unsuspecting public shaking its faith in the financial and banking

12

system as a whole Given the overwhelming reach of the financial system into our personal and corporate lives we had no place to hide but just wait for the rescue Had it not for the bailout with taxpayersrsquo money which many opposed the damage to all stakeholders would have been much more severe

The way the world financial system was brought back to life from the brink you would have thought we have learnt our lesson but not so as unethical conducts continued into the 2010s and make no mistake history will continue to repeat itself maybe damages will be more containable with stronger checks and balances If you close your eyes and reflect you will see newspaper headlines flashing events individuals and institutions associated with banking and financial system scandals

The early and mid-2000s saw the carnage brought about by leveraged borrowing by Lehman Brothers to finance housing-related assets that collapsed in value causing the largest bankruptcy filing in history with Lehman holding over $600 billion in assets The company again got caught in an accounting fraud in 2010 (Annex-2)

Then there was the massive Ponzi scheme of Bernard L Madoff Investment Securities LLC caught in 2008 with the estimated size of the fraud to be $648 billion Other notable cases include risky subprime lending by Countrywide Financial charged by SEC in 2009 and insider trading by Raj Rajaratnam indicted by a Grand Jury in 2009

A massive fraud of fake loans in Kabul Bank was reported in 2010 worth about a billion dollars with the bailout costing 5 of GDP of that war ravaged country where I worked for over six years in and out in the early 2000s Believe it or not until President Ashraf Ghani canceled his governmentrsquos partnership with Khalilullah Frozi who was supposed to be in prison for defrauding Kabul Bank a cozy business relationship was building up between Frozi and

13

government operatives over a proposed township in the heart of Kabul Mr Frozi was on national TV signing agreement on the scheme with Government Ministers This only goes to show how beholden governments sometimes are to convicted confirmed financial criminals that they are unable to cut off the umbilical cord Sounds familiar Keep guessing

In 2012 JPMorgan Chase suffered a trading loss of $58 billion Who paid for it The depositors and shareholders

One of the most unethical acts in banking history was perhaps the Libor manipulation scandal that rocked the banking industry in 2012 dragging names like the Royal Bank of Scotland HSBC Deutsche Bank JP Morgan Bank and Citibank as well as ICAP (Intercapital) in an alleged colluding scheme to manipulate the London Interbank Offered Ratendasha benchmark rate tied to financial contracts and derivatives estimated at approximately $350 trillion to gain advantage in trading position This was considered so unethical that some of the stalwarts of the banking industry itself thought it was reprehensible and that indeed the industry has an ethics problem (Irwin 2014)

Again in 2012 money laundering charges were brought against HSBC and Standard Chartered In the same year a rogue trader caused UBS a $2 billion loss SAC Capital is under Justicersquos rudder for insider trading

In September 2013 JP Morgan Chase revealed it will pay heavy fine for unfair billing practices for certain credit card lsquoadd-on productsrsquo by charging consumers for credit monitoring services that they did not receive Look out for your monthly bills if you carry a credit card issued by Chase

Globally these are only few examples but these add up to tens of billions of dollarsrsquo worth of unethical banking practices In each case unethical activities were carried out by rogue individuals and institutions under the very nose of the treasury central banks and regulatory authorities

14

Closer home we have the scams of BCI BASIC Destiny and Hallmark amounting to an estimated $14 billion which puts Bangladesh into the little league compared to the global cases I cited What makes the Bangladesh cases unique is that these not only reflect human folly and systemic failure but also more ominously connivance between the two under the very nose of the Ministry of Finance the Bangladesh Bank the management of the respective banks as well as the political leadership

A shocked Justice Shahabuddin Ahmed in his First Nurul Matin Memorial Lecture told us the story of the Bank of Commerce and Investment (BCI) Established in 1985 BCI attracted deposits on promise of high interest rates It collapsed in April 1992 with 200 crore Taka ($25 million) vanishing including Taka 2 crore and 5 lac from the High Court As the Honorable Justice said the bank had no authority from the Bangladesh Bank to do banking business yet carried on under the very nose of the Ministry of Finance and the Bangladesh Bank who blamed each other for the debacle

In these national and international banking scandals we come up against not one but two Chinese walls human folly and systemic failure

Much has been done more are being done by all concerned to remedy the situation except for the political economy of banking in Bangladesh and worldwide Facts are well documented Frustration of our Finance Minister is still echoing in the hall of the Parliament

It is not the amount of money or the innovative skills of the white collar criminals but the culture of impunity that is worrisome

No doubt we have had banking scandals all over the world But the difference is that in other countries there are strong independent and countervailing institutions capable of taking remedial action In our case such institutions are absent or are too weak

15

Loan DefaultUnethical banking does not end with large scams which are news worthy but extends to ordinary banking operations in the form of loan default that is now threatening the very foundation of the Bangladesh banking system save for the unwritten promise of state subvention and rescue In Bangladesh the question is not one of just too big to fail but also and more importantly no bank is too small to be allowed to failDefault is failure to meet the legal obligations (or conditions) of a loanThere are 178 lakh loan defaulters as of June 2015 (Source Finance Minister Muhith based on Bangladesh Credit Information Bureau as reported in Bangladesh Daily Star September 3 2015)Quoting Bangladesh Bank sources Jebun Nesa Alo in an article published in Dhaka Tribune on February 8 2015 says that 61 big borrowers owe banks Tk 53000 crore accounting for 25 of total large loans of Tk 215000 crore which is 34 of total loans and advances of Tk 634000 crore as of September 20141 According to the author ldquoOf them 21 are loan defaulters making up 25 of entire default loan valued Tk 20000 crorerdquo Though facts maybe otherwise in the eyes of public Bangladesh Bankrsquos new loan restructuring policy is designed to encourage defaulters and discourage good borrowers Some individual borrowers stand out by loan size and default Restructuring terms are 12 years for term loan and 6 years for demand loan at cost of funds plus 1 with moratorium period of 12 months Down payment is set at 1 for outstanding loans over Tk1000 crore and 2 for outstanding over Tk 500 crore The policy is inequitable because no restructuring strategy is suggested for loans below Tk 500 crore2

16

1 Dhaka Tribune February 8 2015 httpwwwdhakatribunecombanks2015 feb08 most-fortunate-borrowers-owe-banks-tk53000cr2 Terms quoted were reported in Ahmed Syed Aby Nasser Bukhtear 2015 Being a big loan defaulter pays The Daily Star February 10 2015 httpwwwthedailystarnet being-a-big-loan-defaulter-pays-64000

The Bangladesh Bank has come out defending the new loan restructuring policy on grounds of economy and employment though it has created mismatch between bank assets and liabilities as deposits are mostly short term Recently Bangladesh Bank Governor Atiur Rahman has correctly advised banks to use long term savings for big projects Nonetheless Bangladesh Bankrsquos loan restructuring policy has the unintended effect of firms not resorting to raising fund in the capital market because loans are cheaper more so in case of defaults

The loan rescheduling policy has been in the offing for some time with the Finance Minister indicating in 2009 that the Government is planning to consider rescheduling as many companies have been affected by global economic recession

Loan defaulters are barred from participating in elections but this has not been very effective in keeping defaulters from election contest on one pretext or another and the influence of business and money in the electoral process has increased rather than contained One must recognize though that this is a globally recognized dark spot on democracy The President the Chief Justice and the Daily Star have talked about it in the context of Bangladesh (Figure-6)

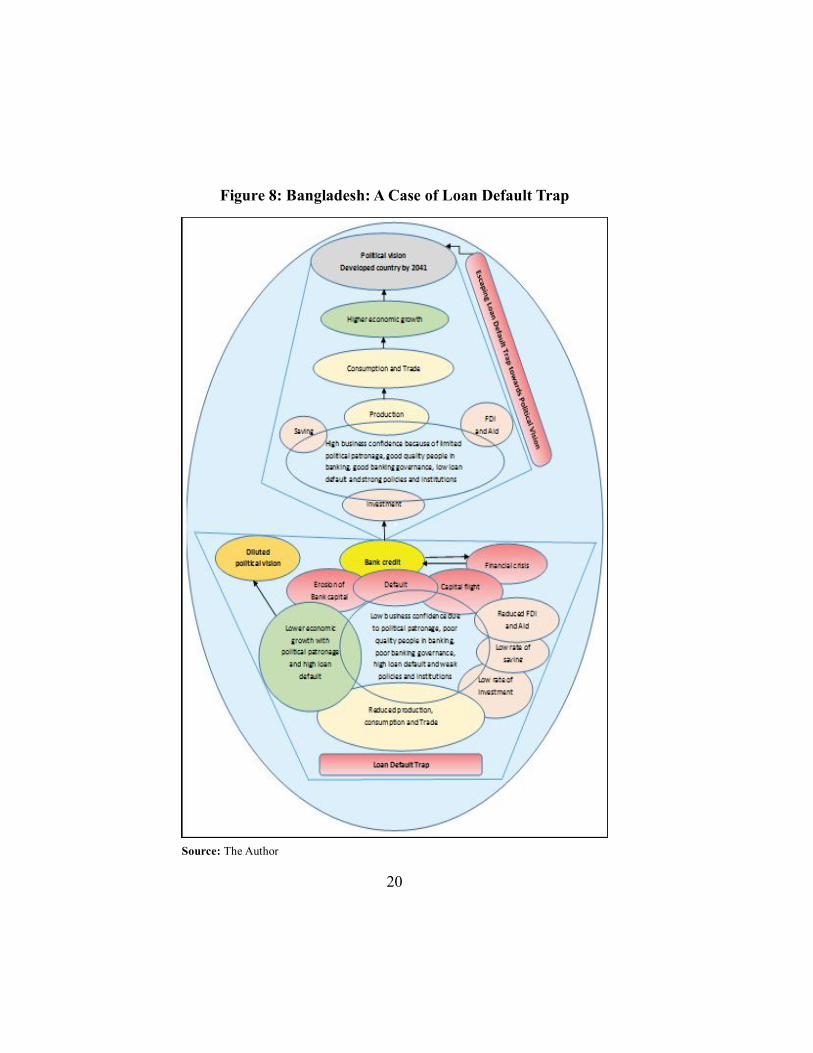

This discussion apart the greatest ethical question raised by loan defaults and how these are treated by existing legal and regulatory regime is a systemic one in what impact these have on financial and economic systems A BIBM research helps us to trace financial system impact (Figure-7) which we extend to trace economic system impact (Figure-8) showing Bangladesh caught in loan default trap which the country must escape in order to realize the political vision of developed country by 2041

17

Figure 6 Percent Businessmen Elected to the Parliament

Source The Daily Star 14 October 2015

Figure 7 Economic and Financial Implications of Non-Performing Loans (NPL)

(If NPL problem is not properly addressed it may by lead to financial crisis reducing economic growth)

Source Adapted from Adhikary Bishnu Kumar Undated Bangladesh Institute of Bank Management (BIBM) Dhaka

18

Ethics in Banking and Microcredit

Financial inclusion is ethical banking drawing in the marginal segment of the population including the poor women and the disabled into banking operations People cannot walk too far to the commercial bank branches so microcredit walks to the door step of the poor Like development banking Governor Atiur Rahman has made financial inclusion a center piece of financial development policy He has been a strong supporter of microcredit an undeniably effective instrument of financial inclusion in contrast to corruption-ridden commercial banks that tend to promote financial exclusion Bangladesh Bank has taken the lead in encouraging linking up microcredit institutionsrsquo operations with those of commercial banks I see eventual mainstreaming of all microcredit operations giving financial inclusion its true color establishing a uniform financial system governed by a common set of norms rules and regulations Already according to the annual report of the Microcredit Regulatory Authority (MRA) for 2014 bank loans accounted for Tk 515 billion or 1643 of funds of 676 microfinance institutions operating in the country as of June 2014 up from 1543 a year back (Abdullah 2015)

19

Figure 8 Bangladesh A Case of Loan Default Trap

Source The Author

20

Ethics in Banking and Interest Rate on Lending

It is banksrsquo business to lend money for investment at reasonable rate of interest covering cost of funds and plus Historically interest spread in Bangladesh has been high in excess of 5 (Figure-9) Recently interest on deposits and saving certificates have been reduced yet banks have not adjusted lending rates accordingly According to Bangladesh Bankrsquos latest loan disbursements figures of March banks are charging large and medium enterprises more than 15 percent interest for term loans Average interest rate on saving is 7 or less Commercial banks have not brought down lending rates despite a cut in interests on deposits says the Bangladesh Bank

Figure 9 Interest Rate Spread 1974-75 to 2014-15 ()

Source Bangladesh Bank

According to one news (Bangladesh Business News Monday November 23 2015- httpbusinessnews-bdcombangladeshs -interest-rate-spread-rises-slightly-in-april) in the countryrsquos banking sector overall interest rate spread moved up slightly in April 2015 as the interest rate on deposit decreased while the same on lending increased The weighted average spread between lending and deposit rates offered by the commercial banks rose to 495 in April 2015 from 487 in the previous month It was 504 in February last Deposit rate falls faster than lending rate

21

22

(Figure-10) One wonders why so Greed for profit Declining cost efficiency Increased credit demand against supply Or all

Much has been said about the relatively lsquohighrsquo interest cost of microcredit At the end it boils down to the transaction cost of enhanced improved increased financial inclusion and also market driven supply-demand factors (Figure 11)

Interest spread variation among banks is common reflecting bank policy costs and efficiency (Figure-12)

Figure 10 Lending and Deposit Rates During 2014

Source http wwwdhakatribunecom business 2015 feb 16 deposit-rate-falls-faster- lending-rate-widen-spread

Figure 11 Determination of Market and Micro Credit Interest Rate (imc and im)

Source The Author

23

Figure 12 Interest Spread by Bank September 2015 ()

Source Bangladesh Bank

24

Notwithstanding ongoing debate interest spread in Bangladesh is comparable to other developing countries3 though higher than developed countries Any attempt to influence interest spread is neutralized by countervailing action by banks Dr Manzur Hossain (2010) of BIDS thinks 4-5 interest spread is reasonable for Bangladesh considering size of its economy and profit margin of the banks He recommends focus on increasing operating efficiency in the banking sector and strengthening of capital market

Six Recommendations

I humbly submit we have to target human folly on the one hand and systemic failure on the other

For human folly I have two recommendations

1 Minimize political interference in banking operations The stronger still keep politics out of banking (Action by the political leadership)

2 Pay attention to the quality of people in banking (Action by the banking community especially the role of BIBM in developing Bankers with professional competence and good morality)

I have four recommendations to deal with systemic failure

1 Reduce the number of public banks (Policy decision by the Government)

2 Undertake significant reforms in financial and banking management which have been long overdue I echo Farashuddinrsquos recommendation that ldquoA finance and banking

3 The spread of China was 31 Vietnam 24 Indonesia 56 Malaysia 25 Pakistan 6 and Thailand 48 in 2014 (Alo 2015)

25

reforms commission may be set uprdquo (Action by the Ministry of Finance and the Bangladesh Bank)

3 Enhance Bangladesh Banks capacity for bank supervision and keep it under continuous review (Action by the Ministry of Finance and the Bangladesh Bank)

4 Strengthen three institutions to deal with corruption in banking in Bangladesh The Bangladesh Bank the Anti-Corruption Commission and the Office of the Comptroller and Auditor General (Action by the Government)

Finally I add one recommendation about BIBM communicated to me by Khalid Shams ldquoBIBM has the challenging task of building up the new generation of professionally trained bankers lsquoProfessionalism in this context should include first acquisition of the theoretical knowledge in fast developing banking field second practical hands on skills in applying that knowledge and third probably the biggest need of the hour they need to be imbibed with the ethical values that you have referred tordquo

Thank you

Annex 1 Summary of Nurul Matin Memorial Lecture

Lecture Highlights

Lecture 1 Justice Shahabuddin Ahmed

Banks have social responsibility and to be sustainable must comply with ethical standards It is important to promote ethics in banking because greed seems to have overtaken morality at all levels of governance threatening banks and the economy as well Legal framework is weak giving rise to the need for a central authority to underscore the fact that rules of business must not collide with the principles of welfare justice and fairness Bangladesh has problems with ethics in banking as manifested in the fact that demand for financial accommodation is not always subjected to professional scrutiny Governmentrsquos expression of interest to deal with loan default erring bank staff and union pressure is noted as good signs in the right direction Bank deposits are sacred trust but it got a jolt with the collapse of BCI due to unscrupulous practices MD an MP got elected again while on bail The then parliament carried a large number of loan defaulters who in the first place should not be admitted into any political party Scheme of rescheduling should not be treated as a waiver of loan default as is the practice Loans sanctioned under political pressure are vulnerable to default

Lecture 2 Justice Muhammad Habibur Rahman

Ethics is good behavior Laws regulations and oversight will be of little help if we do not have in the banking sector leaders with high ethical standard whose collective advice could define mores of conduct Law for integrity makes little sense as it must come from within Ethics has value in designing law reforms and helping to achieve its goal in search of truth Law and

26

27

ethics influences each other Law also influences ethical values as it provides a sense of what is right and what is wrong Bangladeshi bankers do not have code of ethics of their own The reference point is the 1996 BB circular in respect of responsibility powers and facilities available to bank board and management Many cases brought before the SC shows connivance between bank officials and the borrower

Lecture 3 Professor Rehman Sobhan

Ethics is trust that must be underwritten by a substructure of ethics so that a relationship of trust sustains a banking system Erosion of the relationship of trust threatens the banking system of Bangladesh Ethics is about resources being used in a just manner as justice is an integral part of the relationship of trust Banking services should be guided by economic efficiency social and political justice In reality banking is more about repayment and minimizing return to depositors than about credit use and socioeconomic development NCBs need to be partially privatized in order to make them socially accountable Banks need transparency and freedom from political pressure The logic of bank nationalization in the early 1970 lay in the need to build a democratic banking system built on principles of social justice one element of which was dispersal of banking by NCBs Justice in the banking system implies honoring of fiduciary relationship with all clients securing deposits and making just and efficient use of funds The need to democratize banking has not been accepted by banks in Bangladesh While deposit base is large lending is concentrated at both PCBs and NCBs giving way to the

28

the problem of default plaguing the banking system in Bangladesh In this environment MFIs have brought credit to the small borrowers However by and large small borrowers small industries and agriculture is underserved by the banking system in Bangladesh thereby perpetrating social injustice Inequality in bank loans reflects inefficient allocation of resources as a large proportion of borrowers are not good entrepreneurs The political influence on the banking system in Bangladesh is political injustice that along with social and economic injustices in the banking system skew benefits and exacerbate resource misuse Restoring justice in the banking system would require integration of the micro-credit and macro-credit system and expansion of the outreach of the latter to low income groups and agriculture

Lecture 4 Mr M Syeduzzaman

Ethics means choosing between what is morally good or bad the right over the wrong and fair over unfair Pillars of banking business is trust evolving as it did with codified laws governing business and regulationsregulators to enforce such laws Laws and regulations reflect the moral and ethical equivalent of the basis of banking business But honesty was the foundation leading people to say as honest as a banker which today is a paradox because the so called honest bankers are compromising public trust It is also ironical that state authorization of the Bank of England opened war chest for England while giving business to BoE which in todays mores violates dictums of socially responsible banking Through the ages banks are there for profit morality and ethics taking

29

secondary seat Ethics in banking is a part of business ethics in general which subscribes to the view that morality and ethics in banking is part of the same compact that governs the state society community business and individual life The separation of jurisdiction done here by the organizers of these lectures is nominal and not real Ethics in business banking should include accepted standards of personal integrity financial disclosure legal and regulatory compliance fulfilment of contractual obligations and observance of due diligence and prudence in the conduct of business Ethically unacceptable loans originate in lack of due diligence poor corporate governance and secrecy of private business political interference government policy and sheer corruption Ethical discipline requires adequate information flow Regulators have a strong moral and ethical responsibility to keep the banking system sound Ethics is good and independent governor and good governor is good ethics A commission to study ethics in banking is recommended

Lecture 5 Professor Wahiuddin Mahmud

Ethical values are fundamental to the functioning of the market Ethical elements enter in some measure into every contract without which no market could function Fundamental to modern day capitalism and investment mechanics is ethical standards manifested in trust Ethical lapses accentuate market failure risks like future uncertainty and informational deficiency Ethics in banking is important because banking companies are special kind of public companies securing depositors interest NCBs problem is that they

30

are far from being autonomous commercial entities besides being engulfed in incompetence and corruption and burdened with loans to SOEs Insider lending in Bangladesh banking system can be traced to expansion of private banks without adequate regulations Tightening of regulatory measures with regard to insider lending qualification of a bank director size and tenure of board and minimum required paid up capital BB taking over problem banks and government ensuring safe return of depositors money creates a moral hazard as depositors would not be selective of the bank the deal with irrespective of reputation and performance SCB problems have to be confronted head on with quality management and staff transparency and accountability The question of SCB reform boils down to political will Financial sector reforms of the World Bank and IMF shall have limited impact The Bank Companies Act 1991 requires banks to follow international accounting standards but will prove to be of little use without improved corporate governance Internal and external auditing have to be strengthened The culture of malfeasance has become entrenched in Bangladesh financial system corruption with impunity breeding corruption with impunity Big loan defaults involve irregularity concealment and corruption and collusion between borrowers and bank officials caused by lack of political will lack of prosecutorial experience with white-collar crime and lack of convictable evidence Legal reforms have yielded slow results BB has tightened loan rescheduling conditions to discourage willful or

31

habitual default The unintended consequences of market competition have to be dealt with like interest rate dividend salaries and benefits of top management interest rate which had to be moderated with selective ceilings and credit allocation (eg between exports and protected domestic industry)

Lecture 6 Professor Nurul Islam

Ethics in banking is part of ethics in economics Ethics is corporate social responsibility tending to the needs of the poor and disadvantaged and serving the community through corporate philanthropy in enlightened self-interest avoiding criticism of excessive profiteering and gaining business in the process Growth has positive moral consequences like greater opportunity tolerance of diversity social mobility and commitment to fairness and dedication to democracy Ethical considerations supplement laws and regulations and ethical conduct creates trust which is essential in banking on the part of depositors in management and on the part of management in borrowers Ethics are low cost substitute for internal control and external regulation as fraud and its monitoring and surveillance and remedial actions raise transaction costs beyond acceptable level Ethics encourages respect for law and avoidance of exploiting legal loopholes Ethics in banking is closely related to the lack of ethics in the rest of the society Banking regulations are in place in Bangladesh but these need to be strengthened in respect of licensing of banks directors chairman and top management and their relationship with directors Accounting auditing standards are being improved though it is a work in progress

32

Default problem in Bangladesh is due to politics project chosen and evolving scenario of costs and benefits willfulhabitual conduct or exposure of NCBs to SOEs and the wider problem of governance Honest supervisory and regulatory system is one answer to the loan default problem Microfinance regulatory framework is an element in this equation that may find answer to the coverage of the ultra-poor missing middle graduates etc and also of the interest charged on loans by MFIs which is higher than CBs due to cost of delivery and non-credit services The answer is full disclosure and cost saving measures Subsidized or quota based credit is not helpful to SMEs technical assistance to improve credit worthiness is

Lecture 7 Dr Bimal Jalan

Ethics is adherence to rule of law Ethics is any measure or policy decision which improves welfare of some without causing harm to anyone else Public policy should be designed to promote the greatest good of the greatest number Presumably unethical defiance of law could have significant ethical outcome (independence struggles or microcredit interest rate) Ethics in banking cannot be separated from other sectors of the economy Ethics in banking is about adhering to the best international standards and ensuring full financial disclosure of all obligations including off-balance-sheet-items

Lecture 8 Professor Muzaffer Ahmed

Ethics is the balance between right and wrong Many historical great persons have espoused the cause of right and fought wrong Ethics is rule of law and good governance

33

Lecture 9 Dr Akbar Ali Khan

The intensity of financial crisis is escalating notwithstanding surveillance and regulations aggravated by weaknesses in corporate governance and complicity of audit firms and the drive for profit maximization overshadowing the sense of right and wrong egged on by poor governance at the state level Banks thrive on the fortune probity and prudence of a particular banker Banking business is based absolutely on trust which is a relationship of mutual reliance Breach of trust creates an environment of uncertainty and suspicion Banks are highly fragile without solid ethical foundation Ethics is concerned with what is good and bad and what is right and wrong Ethics in banking should be eclectic broad and realizable Ethics can be justified as a means of good business Ethics is concerned with corporate collective and personal actors Ethics in banking comprises primary ethical obligation of ensuring the integrity of financial intermediation and the secondary ethical obligation of reducing injustice Ethical dilemma in Bangladesh comprise NPLs gap in enforcement of regulations financial swindles false expectation created by government guarantee punishment of loan defaulters and improvement of auditing standards There are internal ethical challenges emanating from collective ethical responsibility of the Board and personal ethical responsibility of staff Social micro credit is ethical commercial micro credit is not There is a problem of trust among MFIs at the grassroots in Bangladesh giving rise to unfair competition over borrowing from multiple sources and leakages to non-poor

34

Remedy lies in vigilance (by Micro Credit Regulatory Authority) collaboration and social mobilization Islamic banking has an important place in ethical banking in Bangladesh with about 15 of total deposit and credit but they are like conventional banking in terms of portfolio urban bias and support for the poor and capital adequacy Injustices in banking in Bangladesh is in flow of funds from rural to urban areas and environmental and social responsibility which need transparent guidelines

Lecture 10 Professor Muhammad Farashuddin

Ethics is the discipline that examines ones moral standards of a society It asks how these standards apply to our lives and whether these standards are reasonable - that is whether they are supported by good reasons or poor ones (Velasquez) Banking is an institution for lending borrowing exchanging issuing or storing money (Doubleday Dictionary) Ethics as an eternal source of truth and logic has remained valid since it has been codified but banks have undergone major changes in response to evolving nature and circumstances of the global economic scenario Banks would like to maximize wealth of shareholders but public sector banks go beyond profit to include social justice by providing subsidy to some clients Banks follow business ethics by avoiding violation of regulations or refraining from unacceptable actions Historically banks moved from private to corporate operations brought under regulations in 1864 in the US Banking laws and regulations appeared in various forms to ensure banks do the right thing and shy away from wrong actions that were

35

soon codified internationally for standardization under the popularly known Basel I Basel II and Basel III all aiming to ensure capital adequacy linked to three tier classification of capital (Tier I Tier II and Tier III) defining the method of calculating risk-weighted assets Basel II for example focuses on capital supervision and disclosure Internal regulations and Basel Agreement are designed to secure capital base preventing banks to pursue profit with undue risky ventures undermining depositor interests In Bangladesh commercial banking is lopsided with minority fund providers owning the bank while the interestvoice of the majority fund providers is completely bypassed even with two independentrdquo directors presumably representing their interests There is a serious ethical issue of equity shareholders taking loan from own banks The business of a bank has to be built around the trust factor Banking ethics is violated with unjustified waivers write-offs and willful defaults Further ethical violations are in loan rescheduling on soft terms and allowing the defaulter to contest elections and borrow more due to political-administrative collusion The demise of ethics is also seen in bonus without profit in SCBs One gap in ethnics is reluctance to let any bank go under The relationship between board of directors and management is problematic as the latter almost forces the former to approve multiple loan proposals under duress without board members having had the time to study each proposal closely Management supervision and assessment is inadequate by MoF and the Board from PCBs Advances for industrial purposes

36

are being diverted to stock market Future courses of action include strengthening of BB supervision establishment of Asset Management Company for NPL exposing NCBs to competition assessment of CEOs by BB limitation on non-IPO investment in stock market reduce interest spread and coordinated monetary and fiscal policy framework

Lecture 11 Dr A B Mirza Md Azizul Islam

Ethics is the study and philosophy of man with emphasis on the determination of right and wrong Simply put ethics implies the greatest good for the greatest number Principal functions of bank are intermediation maturity transformation credit allocation and facilitation of payment flows Asymmetry of information makes ethics in banking important as banks could let down depositors with poor assets and borrowers could let down banks with poor projects Four pillars of ethics in banking (i) comply with all laws rules and regulations to ensure soundness of operations (ii) fair and equitable treatment of all stakeholders (iii) full truthful and transparent disclosure of their financial health and (iv) behave as socially responsible corporate citizens

Lecture 12 Dr Yaga Venugopal Reddy

Following global financial crisis trust in banking has gone down in developed but it has gone up in developing countries In both worlds public sector banks gained in confidence of the public though shift was transitory Fixation of LIBOR and credit rating by major players did not help with confidence in the financial system nor did the mooted reaction of regulators to earlier findings of improprieties signaling failure of self-correcting power of markets and

37

weak capacity of regulatory agencies The burden of restoring maintaining and enhancing trust in financial sector has to be essentially that of financial sector and should be shared by both the regulator and the regulated The central bank is at the forefront of trust in the financial sector by maintaining financial stability on the one hand and by preserving trust in banking largely through its lender of the last resort role

Lecture 13 Professor Sanat Kumar Saha

Banking and economic development thrives on the belief that deposits are safe and investments from bank loans are done judiciously

Lecture 14 Dr Amiya Kumar Bagchi

Following the tradition of pre-British India in colonial timersquos money lenders performing function of bank lending basically dispossessed cultivating farmers of their land despite many legal and institutional attempts to protect their interests Professor Bagchi says if peasants remain illiterate and poor because of exploitation lack of incentives and access to essential inputs such as irrigation and fertilizers and if creditors can dispossess them because of indebtedness then no amount of tinkering with terms of lending can provide a framework for ethical banking Credit market is essentially imperfect and fragmented offering different terms to different borrowers Morality comes into play in the role of the central bank supervising operations of the imperfect credit market Information asymmetry creates problem in lending which can be overcome by relationship banking which has aided development of SMEs in Germany and elsewhere

38

Annex 2 Profile of Selected Banking Scandals CrisesYear International

1997-1998 Asian financial crisis is attributable to (i) hot money flow into the banking system (ii) excessive short term private borrowing to finance long term projects and poor loan quality (iii) collapse of the fixed exchange rate regime under market pressure leading to devaluation and managed float (iv) crony capitalism and inefficient allocation of credit to politically favored parties (v) premature liberalization of capital markets (vi) unethical conduct of currency speculators (vii) severe problems in the banking and financial sectors (vii) weakening economic performance and balance of payments difficulties (viii) technological changes in the financial market (ix) lack of confidence in crisis ridden governmentsrsquo ability to solve problems (x) unusually high NPL ($400-$800 billion or 9-18 of GDP) and write off (close to $300 billion) in Japan (xi) lack of skilled manpower to regulate the rapidly growing financial sector (xii) the development of the financial systems not keeping pace with the development of the financial markets (xiii) more investment monies flowing into these economies than could be profitably employed at modest risk (Alan Greenspan Chairman of the US Federal Reserve) and (xiv) relatively high interest rate discouraging growth (Nanto Dick K 1998 The 1997-98 Asian Financial Crisis CRS Report for Congress httpfasorgmancrscrs-asia2htm)

Early Mid 2000s

In the earlymid 2000rsquos financial services firm Lehman Brothers borrowed significant amounts to fund its investing a process known as leveraging A significant portion of this investing was in housing-related assets making it vulnerable to a downturn in that market When that happened Lehman was forced

39

to file for bankruptcyndashit remains the largest bankruptcy filing in history with Lehman holding over $600 billion in assets (httpthoughtcatalogcombrad-winlsow2013 0915-recent-bank-scandals-that-show-just-how-powerless-rest-of-us-really-are)

2008 In December 2008 it was revealed that the Wall Street Firm Bernard L Madoff Investment Securities LLC was a massive Ponzi schemendashmeaning it paid back investments with money from other investors instead of actual profit Prosecutors estimated the size of the fraud to be $648 billion (httpthoughtcatalogcombrad-winlsow2013 0915-recent-bank-scandals-that-show-just-how-powerless-rest-of-us-really-are)

2009 In June 2009 the SEC charged Angelo Mozilo former executive of mortgage lender Countrywide Financial with fraud for allegedly misleading investors about the quality of Countrywidersquos loans Among other things this included tens and billions of dollars of risky subprime and adjustable-rate mortgages Before Countrywide was sold to Bank of America it had been the largest NY mortgage lender In 2010 Mozilo agreed to pay $675 million in fines and was hit with a lifetime ban from serving as an officerdirector of any public company (httpthoughtcatalogcombrad-winlsow2013 0915-recent-bank-scandals-that-show-just-how-powerless-rest-of-us-really-are)

2009 In 2009 a grand jury accused Raj Rajaratnam founder of one of the worldrsquos largest hedge funds called The Galleon Group of using a network of company insiders to tip him off to information that netted $20 million in illegal profits over a three year period He was found guilty in May 2011 and was

40

sentenced to 11 years in prison (httpthoughtcatalogcombrad-winlsow2013 0915-recent-bank-scandals-that-show-just-how-powerless-rest-of-us-really-are)

2010 In March 2010 a report from Anton R Valukas the Bankruptcy Examiner called attention to the use of Repo 105 transactions to boost Lehman Brotherrsquos apparent financial position around the date of the year-end balance sheet Attorney general Andrew Cuomo later filed charges against the bankrsquos auditors Ernst amp Young in December 2010 alleging that the firm ldquosubstantially assistedhellip a massive accounting fraudrdquo by approving the accounting treatment A month later a New York Times story revealed that Lehman had used a small company named Hudson Castle to move a number of transactions and assets off Lehmanrsquos books as a means of manipulating accounting numbers of Lehmanrsquos finances and risks httpthoughtcatalogcombrad-winlsow2013 0915-recent-bank-scandals-that-show-just-how-powerless-rest-of-us-really-are)

2010 In 2010 it was reported that a Kabul Bank took $861 million out of war-ravaged Afghanistan in a massive fraud centered on fake loans to 19 individuals and companies A bailout of the bank costs the equivalent of 5 percent of Afghanistanrsquos GDP ensuring this is one of the worldrsquos largest banking failures of all-time (httpthoughtcatalogcombrad-winlsow2013 0915-recent-bank-scandals-that-show-just-how-powerless-rest-of-us-really-are)

2012 First up is perhaps the biggest financial scandal this year It stemmed from the nationrsquos biggest and arguably safest bank JPMorgan Chase In May Chief Executive and Wall Street poster boy Jamie Dimon revealed that his bank had suffered a massive

41

trading loss initially reported to be $2 billion That $2 billion turned into roughly $58 billion loss (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2012 The Libor manipulation scandal was the yearrsquos most far-reaching hitting dozens of banks across the US and Europe This summer Barclays was the first bank to settle allegations that it manipulated the London Interbank Offered Ratendasha benchmark rate tied to hundreds of trillions of dollarsrsquo worth of financial contracts and derivatives (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2012 The UBS settlement amount was only outdone by the one paid by HSBC just a week prior The British bank paid a record $19 billion to UK and US regulators over money laundering More specifically HSBC settled charges that its lax money-laundering policies allowed billions in Mexican drug money and Iranian terrorist money to be transferred into the US financial system (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2012 Standard Chartered a UK bank paid $327 million to US regulators in December over alleged illegal transactions with Iran Sudan Libya and Burma (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2012 Back at UBS the scandals keep rolling Late last year UBS disclosed one of its traders had gone rogue and lost the bank over $2 billion as a result According to documents Kweku Adobolirsquos bets exposed the bank to $12 billion in losses even though his unit was only authorized to risk $100 million intra-day and $50 million overnight He was found guilty on two counts

42

of fraud in November after a 10-week trial (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2012 Not all scandals involved billions of dollars A small futures brokerage firm in Iowa went under after its CEO allegedly engaged in fraud losing over $215 million of client money CEO Russell Wasendorf Sr was indicted by federal prosecutors who said he submitted false information for his US futures and currency brokerage firm Wasendorf pleaded not guilty even though last month he confessed in a suicide note that he had been using fake bank statements to embezzle millions of dollars from customers (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2012 Insider trading has been a big focus for regulators over the last year The prosecution of former hedge fund titan Raj Rajaratnam over illicit profits he made on inside information also shined a spotlight on one of his informants Rajat Gupta a former Goldman Sachs director was fined $5 million and jailed for two years for sharing inside information with Rajaratnam Among the secret information was a $5 billion investment Warren Buffett would make in Goldman Sachs amid the 2008 financial crisis (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2012 Prosecutors have been circling billionaire hedge fund manager Steven Cohen and his firm SAC Capital for quite some time In recent weeks it appears theyrsquove been getting closer in their attempt to take him down

43

A former portfolio manager at an affiliate of SAC Capital Advisors was indicted this month for allegedly trading on inside information Mathew Martoma worked for a unit of SAC and according to documents his inside information was apparently used by Cohenndashthough he isnrsquot named in any of the prosecutionrsquos documents (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

2013 In September 2013 JP Morgan Chase announced they will pay $970 million in fines to US and British regulators and made a rare admission of wrongdoing over action involved in last yearrsquos ldquoLondon Whalerdquo trading scandal Additionally the Consumer Financial Protection Bureau announced that JPMorgan Chase and Chase Bank have agreed to pay refunds totaling $309 million to more than 21 million customers after the Office of Comptroller or Currency ldquofound that Chase engaged in unfair billing practices for certain credit card lsquoadd-on productsrsquo by charging consumers for credit monitoring services that they did not receiverdquo (httpwwwforbescomsiteshalahtouryalai2012122710-biggest-banking-scandals-of-2012)

Bangladesh

1992 The Bank of Commerce and Investment (BCI) established in 1985 attracted deposits on promise of high interest rates but it eventually collapsed in April 1992 with 200 crore taka ($25 million) vanishing including Taka 2 crore and 5 lac from the High Court The Bank had no authority from the Bangladesh Bank to do banking business yet carried on under the very nose of the Ministry of Finance and the Bangladesh Bank who blamed each other for the debacle (First Nurul Matin Memorial Lecture by Justice Shahabuddin Ahmed)

Year

44

2013 A government audit report has unearthed serious irregularities involving Tk 601 crore at the state-run BASIC Bank Ltd In most cases of irregularities a number of the bankrsquos branches lent money to clients beyond their credit limits and showed overvalued prices of mortgaged properties said the report of the commercial audit department On some occasions the bankrsquos headquarters breached its credit policy in approving loans And in other cases the branches acted on their own and even defied the headquartersrsquo instructions A branch even approved two loans of Tk 100 crore one month and four days before it opened the accounts of the loan applicant Going by newspaper reports BASIC bank has suffered a scam worth Tk3493 crore ($4366 million) Whereas the Board of Directors of Sonali Bank claimed they had no knowledge of what was going on with loans to Hall-Mark it is BASIC bankrsquos board that has enabled the siphoning off of funds The level of political influence in the state-owned banks has reached phenomenal proportions which open up the possibilities of improper sanctioning of loans Such lsquoappointeesrsquo inevitably find allies in a coterie of corrupt bank officials who play a key role in facilitating corrupt practices A similar situation exists in Agrani Bank that is suffering from bad loans amounting to approximately Tk2885 crore (The Daily Star Sunday July 14 2013)

2013 Bangladesh Bank (BB) has appointed an observer to BASIC Bank the first for a state-owned bank after it failed to fulfil major conditions put up by the central bank to improve its financial health On November 18 2015 Bangladesh Bank yesterday appointed observers to four state-owned banks -- Sonali Janata Rupali and Agrani -- after their key financial indicators such as capital adequacy and classified

45

loans took a turn for the worse (The Daily Star Friday November 29 2013)

2012 Hallmark Loan Scam August 27 2012 Sonali Bank asked to suspend 31 officials The central bank has directed Sonali Bank to suspend 31 of its officers including two deputy managing directors by Thursday for their involvement in the Tk 3547 crore loan scam In a letter Bangladesh Bank yesterday asked the managing director of the state-run commercial bank for taking action against those officials so that they could not affect the activities of the bank The officials have been held responsible following an audit which found unethical disbursement of loans to a little-known Hallmark Group and some other firms Quoting the audit report the central bank said around Tk 3547 crore ($4434 million) was embezzled through unauthorized means Sonali Bank has to take punitive measures against the officials in line with the service rules and after bringing specific allegations against them said the letter Criminal procedures if applicable and necessary steps mdash in line with the laws mdash have to be taken against those 31 officials said Bangladesh Bank Of the 31 officials AKM Azizur Rahman deputy general manager of the bankrsquos Ruposhi Bangla Hotel branch (formerly Sheraton Hotel branch) and Saiful Hasan assistant general manager of the same branch have already been suspended Another official the erstwhile managing director of the bank has his job term spent The central bank letter however did not name the official Sonali Bank has also been asked to inform the central bank about the measures it takes against the officials It will have to submit reports to Bangladesh Bank fortnightly about the progress in implementing the instructions said the letter

46

The central bank said Syful Shamsul Alam and Co a chartered accountant and consultancy firm has already conducted a functional audit on the Ruposhi Bangla Hotel branch of Sonali Bank to determine liability of the officials involved in the scam The audit report also found that the officials carried out activities beyond their authority at the branch level Moreover it said such embezzlement of crores of taka had taken place in collusion with the executives of the GM Office and the Principal Office who were responsible for monitoring and supervising branch-level activities or for their sheer negligence of duties -With The Daily Star input (Dhaka Mirror August 27 2012)

2012 Farashuddin Many wonder if but not all agree that the failure of Sonali Bank Ruposhi Bangla Branch to prevent the fraudulent misappropriation of Tk3607 crores by Hallmark Group (Tk2668 crores) and others is the biggest scandal in the banking industry In recent times several such frauds -- (a) misappropriation of Tk622 crores by one Nurunnabi in Chittagong in 2007 through a false local letter of credit (b) embezzlement of Tk596 crores withdrawn without cheque from Oriental Bank in 2006 (alleged Hawa Bhaban connection) and (c) transfer of Tk300 crores by forgery from five banks by one Om Prokash in 2002 -- were not as heinous as bank defrauding Perhaps more damaging has been the transfer in their personal accounts of more than Tk 4500 crores from the mother account of the infamous Destiny

Group before the eyes of the banking authorities several months into the first sighting of the alleged

fraudulent and illegal deposit taking from the members of the public

47

Two key recommendations 1Significant reforms are necessary in financial and banking management which have been long overdue A finance and banking reforms commission may be set up 2Bangladesh Banks capacity for effective objective transparent and accountable bank supervision may be enhanced including enlargement of professional staff extension of its authority over the NCBs and adoption of a separate pay scale (The Daily Star September 9 2012)

2012 Destiny Multipurpose Cooperative Society Ltd (DMSCL) Scam Fourteen Destiny Group officials including its chairman Rafiqul Amin were involvedin a Tk 1448-crore scam in the multilevel companyrsquos cooperative wing Destiny Multipurpose Cooperative Society Ltd Of the sum Rafiqul Amin misappropriated nearly Tk 130 crore a government investigation has found The grouprsquos former vice-president Gofranul Haque embezzled about Tk 128 crore and ex-treasure Akbar Hossain Sumon Tk 119 crore Nine other officials of the controversial cooperative firm including its former general secretary Zakir Hossain each pocketed Tk 1188 crore according to the inquiry carried out by the Department of Cooperatives (DoC) Syedur Rahman a director of Destiny Group has been blamed in the report over misappropriating Tk 215 crore while DMSCL Executive Director MA Muhith has been accused of misappropriating Tk 87 lakh The committee members spent the money in the name of business promotion and giving loans to some two dozen non-profitable entities the probe report says According to the cases the accused persons laundered Tk 328526 crore ($4782 million) Destiny Multipurpose Cooperative Society Ltd (DMCSL)

48

came under the spotlight after a central bank investigation in March found that the firm was involved in illegal banking The Anti-Corruption Commission and the National Board of Revenue are also investigating possible money laundering and tax dodging by the company (The Daily Star August 29 2012)

REFERENCES

Abdullah Sheikh 2015 Microfinance institutions borrow more banks in Bangladesh Bdnews24com 26 November 2015

Ahmed Sadiq Mohiuddin Alamgir and Mustafa Kamal Mujeri 2015 Strengthening Institutions to Accelerate Growth and Lower Poverty Paper presented at the Second Bangladesh Economistsrsquo Forum Dhaka 24 September 2015

Alo Jebun Nesa Deposit rate falls faster than lending rate to widen spread The Daily Star 16 February 2015 httpwwwdhakatri-bunecombusiness2015feb16deposit-rate- falls- faster- lending- rate- widen-spreadsthashkARTtfZ2dpuf

Business News 2015 httpbusinessnews-bdcombangladeshs-in-terest-rate-spread-rises-slightly-in-april

Dhaka Mirror August 27 2012

Dhaka Tribune February 8 2015 httpwwwdhakatribunecom b a n k s 2 0 1 5 f e b 0 8 m o s t - f o r t u n a t e - b o r r o w -ers-owe-banks-tk53000cr

Dr Akbar Ali Khan 2009 Ethics in Banking Ninth Nurul Matin Memorial Lecture BIBM Dhaka

Dr A B Mirza Md Azizul Islam 2011 Ethics in Banking Eleventh Nurul Matin Memorial Lecture BIBM Dhaka

49

Dr Amiya Kumar Bagchi 2014 Ethics in Banking Fourteenth Nurul Matin Memorial Lecture BIBM Dhaka

Dr Bimal Jalan 2007 Ethics in Banking Seventh Nurul Matin Memorial Lecture BIBM Dhaka

Dr Yaga Venugopal Reddy 2012 Ethics in Banking Twelfth Nurul Matin Memorial Lecture BIBM Dhaka

Hossain Monzur Monday February 1 2010 Determinants of interest rate spread The Daily Star Dhaka httparchivethedai-lystarnetnewDesignnews-detailsphpnid=124283

http thoughtcatalogcombrad-winlsow20130915-re-cent-bank-scandals-that-show-just-how-powerless-rest-of-us-really-are

h t t p w w w a u t h o r s t r e a m c o m P r e s e n t a t i o n r k g u p -ta1949-471451-business-ethics-and-values-Banking-industry

httpwwwforbescomsiteshalahtouryalai2012122710-bigg-est-banking-scandals-of-2012

Irwin Neil July 29 2014 Why Canrsquot the Banking Industry Solve its Ethics Problems The Upshot httpwwwnytimescom2014 0730upshotwhy-cant-the-banking-industry-solve-its-eth-ics-problemshtml_r=0

Justice Muhammad Habibur Rahman 1999 Ethics in Banking Second Nurul Matin Memorial Lecture BIBM Dhaka

Justice Shahabuddin Ahmed 1998 Ethics in Banking First Nurul Matin Memorial Lecture BIBM Dhaka

M Syeduzzaman 2002 Ethics in Banking Fourth Nurul Matin Memorial Lecture BIBM Dhaka

Malik Faiza 2015 NBP actions in Bangladesh ndash NA panel calls NAB to examine Rs185 billion loss httpwwwibexmagcom pakistan-economybanking-and-financenbp-actions-bangla-desh-na-panel-calls-nab-examine-rs-18-5-billion-loss

50

Nanto Dick K 1998 The 1997-98 Asian Financial Crisis CRS Report for Congress httpfasorgmancrscrs-asia2htm

Professor Muhammad Farashuddin 2011 Ethics in Banking Tenth Nurul Matin Memorial Lecture BIBM Dhaka

Professor Muzaffer Ahmed 2008 Ethics Banking and Professional Responsibility Eighth Nurul Matin Memorial Lecture BIBM Dhaka

Professor Nurul Islam 2006 Ethics in Banking Sixth Nurul Matin Memorial Lecture BIBM Dhaka

Professor Rehman Sobhan 2000 Restoring Justice to Banking Third Nurul Matin Memorial Lecture BIBM Dhaka

Professor Sanat Kumar Saha 2013 Banking and Ethics Thirteenth Nurul Matin Memorial Lecture BIBM Dhaka

Professor Wahiuddin Mahmud 2005 Ethics in Banking Fifth Nurul Matin Memorial Lecture BIBM Dhaka

RK Gupta 2010 Business Ethics and Values in Banking Industry

Serrano Ricardo Sanchez 2010 Ethical Issues facing the Banking Industry Fidelity International Institute httpfidelisinstituteorg articlephpse=13ampca=22

The Daily Star August 29 2012

The Daily Star Friday November 29 2013

The Daily Star September 9 2012

The Daily Star Sunday July 14 2013

Wehinger Gert 2013 Banking ethics and good principles OECD Economic Observer 294 Q1 httpwwwoecdobserverorg news-fullstoryphpaid4017Banking_ethics_and_good_princi-ples_html

51

Post Script Daily Bangladesh Pratidin ঢাকা শিনবার ২৮ ২০১৫

টেল বদল

ভয়া ও ঋেণ খািল হেয় সরকার ও বাংলােদশ

রনেসাশস কড়া িদেলও করা না খােতর এই টাপটল

ারেপ খােতই হেয় উেঠেছ ারটেল এই

নয় খািল হেয় এই রদোরটেল

ভয়া এফিডআর লেখ তা িদেয় ঋণ ভয়া

ও ভয়া নাম- িদেয় টাকা িনেয় বাংলােদশ

হেয় গত িতন বছের এমন িতন হাজার ৭০০ টাকা রাইট

অফ (অবেলাপন) কেরেছ অবেলাপনকত চাইেলও জিরমানা আর মানস

হওয়ার ভেয় তা সরবরাহ করেছ না রাঘব-

এই টোপটল মািলকরাও জিড়ত বেল জানা

মািলক ও িনেজরাই ভয়া এফিডআর

সনদ করেত এবং নােম- ঋণ িদেয় টাকা করেত

সহায়তা করেছন বেল এেসেছ বলেছন রাঘব-

আটকােত না পারেল অবেলাপেনর পিরমাণ বাড়েতই থাকেব গত

কেয়ক বছের অবেলাপনকত ঋেণর পিরমান কের বাড়েছ বাংলােদশ

জানা ইদ বছের খাত িতন হাজার ৭০০ টাকার

গােয়ব হেয় ঋেণর নােম এ টাকা অবেলাপন কেরেছ

খােত িহেসেব িণকত ঋেণর পিরমাণ ছেয়েড়িাদ ৩৮ হাজার

টাকা এর ঋণ ৩৬ হাজার টাকার

52

ভয়া এফিডআর

কের ঋণ ওই এফিডআর

িবপরীেত এফিডআর যাচাই-বাছাই না কের ঋণ নদামেনঅ

িদেয় ঋণ কেয়ক বছর পর িবপরীেত

ঋণ হেয়েছ স ণ ভয়া এ ছাড়া স ণ ভয়া গঠন কের জাল

দিলল জমা িনেয়ও ঋণ এসব ভয়া দিলল ঋণ পর

তখন যায় করা হেয়েছ ওই

থাকেলও দিলল হেয়েছ তা

রিপারেপ জাল এমনিক নাম ভল তখন তােদর

ভােলা ধের রাখেত হেয় ওই ঋণ সবই অবেলাপন কের একবার

অবেলাপন কের িদেল ঋণ আর কখেনাই পাওয়া যায় না

আদালেত মামলা কের আর তা বছেরর পর বছর চলেত থােক

ঋণ আর জেখ পায় না বাংলােদশ সব

কােছ ঋেণর চাইেল তারা নানাভােব িদেয়

তারা কােছও না অেনক সময় এড়ােত

সরবরাহ কের কােছ এসব অিনয়ম-

জািলয়ািতেত

জিড়ত এমনিক জিড়ত মািলকরা

একজন কের মািলক রেয়েছন যারা ভয়া এফিডআর কের ঋণ

জািলয়ািতর করেছন হাজার টাকা একজন মািলক

হেলও বাংলােদশ িনয়ম ীয়াযনঅ পিরবার পিরচালক িনেয়াগ

িদেত হয় তেব িনেজর অেনক িনেজর

পিরচালক িহেসেব হয় যারা ওই জিড়ত নন

বছেরর পর বছর িনজ মািলকানায় এই মািলকরা

AvZyenxq ^Rb

AvZyenmvr

53

জািলয়ািত-অিনয়ম কের বাংলােদশ

২০১২ সাল খােত অবেলাপন ঋণ িছল ৩৪ হাজার টাকার িকছ

িতন বছের ২০১৫ সােলর নজ অবেলাপন করা হেয়েছ আরও

িতন হাজার ৭০০ টাকা এর চার িবেশষািয়ত

এবং রেয়েছ এ জানেত চাইেল

বাংলােদশ সােবক ড আহেমদ বাংলােদশ

বেলন রাইট অফ বা অবেলাপন আমােদর এর

হয় তােদর রাখেত এ

এ অবেলাপন হয় আর

থােক না এক জায়গায় িদেয় হয় এর খােত

অিনয়ম- আরও উৎসািহত হয় বেল মেন কেরন সােবক এই এ ছাড়া

অভাব রাজৈনিতক

কারেণ খােত অেনক সময় ঋণ অবেলাপেনর হার বােড় যা এ খােত এক

ধরেনর এ আসেত হেল বাংলােদশ

ও তদারিক বাড়ােত হেব ঋণ আেগ তা যাচাই

করেত হেব তাহেলই খােত অবেলাপন ঋেণর পিরমাণ কিমেয় আনা

বাংলােদশ সােবক খােলদ বেলন ঋণ

িহেসেব হেলও তা আদায় করার কথা

অবেলাপন করেতই এর

জিড়ত গত কেয়ক বছের অবেলাপেনর হার বাড়েছ তা খিতেয়

উিচত একই আর এমনভােব অবেলাপন করা না হয় নজর

রাখা উিচত - See more at httpwwwbd-pratidincomfirst-

page20151126 111 8 19sthashnBQ1V2ozdpuf

wKšIacutey

Ethics in Banking A Human Folly or Systemic Failure

Governor Bangladesh Bank Dr Atiur RahmanDirector General Bangladesh Institute of Bank ManagementDistinguished GuestsLadies and GentlemenAssalamu Alaikum