Embed Size (px)

DESCRIPTION

Citation preview

Sterkere USD

Erik Bruce

August 2012

Renter fortsatt viktig for valutaen

2 •

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

2Jun10 2Dec10 2Jun11 2Dec11 2Jun12

USD 2 å swap(venstre akse)

EUR 2 å swap(venstre akse)

1.16

1.2

1.24

1.28

1.32

1.36

1.4

1.44

1.48

1.52

-0.5

-0.2

0.1

0.4

0.7

1

1.3

1.6

2Jun10 2Jun11 2Jun12

2 år rentedif(venstre akse)

EURUSD(høyre akse)

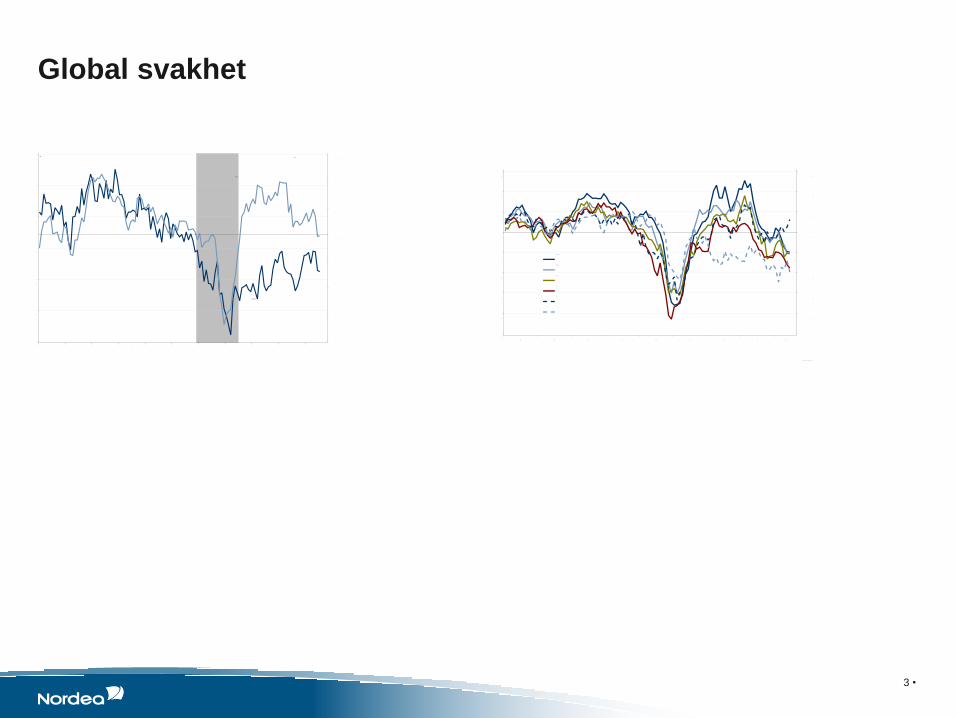

Global svakhet

3 •

Men det er i ferd med å snu i USA

4

Banksystemet fungerer

Bankene er mye bedre stilt i dag. Og nå får også småbedriftene låne

Balanse tilpasningen tatt

Nivå på sparing ikke gjeld som teller for vekst.

Oppsamlet behov for nyinvesteringer

Politisk risk må fjernes- potensiell enorm instrammning

Ikke behov for QE 3- Fed sier de vil holde renten lav lenge

Johnny Bo Jakobsen • 14/08/2012

8 •

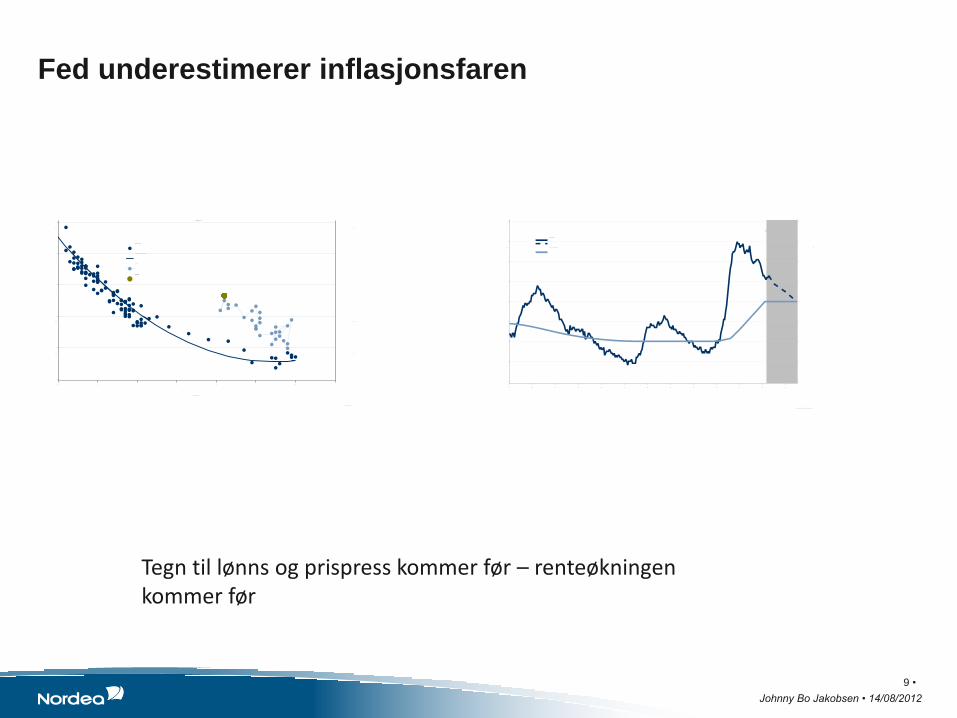

Fed underestimerer inflasjonsfaren

Johnny Bo Jakobsen • 14/08/2012

9 •

Tegn til lønns og prispress kommer før – renteøkningen kommer før

Pengene har strømmet fra Nord til Sør

10 •

Lenge finansiert av privat sektor i Nord

Nye krisetiltak - krisen avverget forhåpentligvis

10 år statsobligasjon – spread til Tyskland

Men veksten blir svak – fortsatt fall i sør

12

Men ikke allt er svakt

En ytterligere svekkelse av euroen vil hjelpe euroomådet

NOK har styrket seg mot EUR

14 •

7.00

7.20

7.40

7.60

7.80

8.00

8.20

8.40

23Aug10 29Mar11 02Nov11 07Jun12 11Jan13 17Aug13

EURNOK Forw ard Nordea Consensus

Mind the gap!

Italia

Hellas

Irland

Belgia

Portugal

Frankrike

Tyskland

ØsterrikeMalta

Nederland

Spania

Kypros

Finland

Slovenia

Slovakia

Luxembourg

Euro snitt

UKUSA

Norge

-12

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

-175 -150 -125 -100 -75 -50 -25 0 25 50 75 100 125 150 175 200

Statsgjeld (% av BNP)

Budsje

ttunders

kudd (

% a

v B

NP

)

Ikke tegn til høyere inflasjon

16 •

Industrien gjør det bra

17 •

Men det er forbrukern som er drivkraften

18 •

Norgrs Bank vil gå forsiktig fram og argumentene for kronekjøp

svekkes

Johnny Bo Jakobsen • 22/02/2012

19 •

5.0

5.5

6.0

6.5

7.0

7.5

8.0

23Aug10 29Mar11 02Nov11 07Jun12 11Jan13 17Aug13

USDNOK Forw ard Nordea Consensus

20

Takk for oppmerksomheten Les mer i vår rapport Økonomisk Oversikt 2/12 på www.nordea.com

som kommer 4 september

Nordea Markets is the name of the Markets departments of Nordea Bank Norge ASA, Nordea Bank AB (publ), Nordea Bank Finland Plc and

Nordea Bank Danmark A/S.

The information provided herein is intended for background information only and for the sole use of the intended recipient. The views and other

information provided herein are the current views of Nordea Markets as of the date of this document and are subject to change without notice.

This notice is not an exhaustive description of the described product or the risks related to it, and it should not be relied on as such, nor is it a

substitute for the judgement of the recipient.

The information provided herein is not intended to constitute and does not constitute investment advice nor is the information intended as an

offer or solicitation for the purchase or sale of any financial instrument. The information contained herein has no regard to the specific investment

objectives, the financial situation or particular needs of any particular recipient. Relevant and specific professional advice should always be

obtained before making any investment or credit decision. It is important to note that past performance is not indicative of future results.

Nordea Markets is not and does not purport to be an adviser as to legal, taxation, accounting or regulatory matters in any jurisdiction.

This document may not be reproduced, distributed or published for any purpose without the prior written consent from Nordea Markets.

Erik Bruce

Sjefsanalytiker

Tlf. 22484449