Embed Size (px)

Citation preview

Equity Valuation and Analysis

Leanna Dennard: [email protected]

Gavin Heckman: [email protected]

Kristin King: [email protected]

Michael Perrien: [email protected]

Jason Sibley: [email protected]

2

Table of Contents Executive Summary……………………………………………………………………………………………….4

Business and Industry Analysis……………………………………………………………………….……..9

Company Overview……………………………………………………………………………………..9

Industry Overview………………………………………………………………………….………….11

Five Forces Model…………………………………………………………………………………………….…12

Rivalry Among Existing Firms………………………………………………………………….….13

Threat of New Entrants………………………………………………………………………………19

Threat of Substitute Products……………………………………………………………………..22

Bargaining Power of Customers…………………………………………………………………..23

Bargaining Power of Suppliers…………………………………………………………………….25

Value Chain Analysis…………………………………….……………………………………………………..27

Firm Competitive Advantage Analysis…………………………………………………………………….30

Accounting Analysis ……………………………………………………………………………………………33

Key Accounting Policies …………………………………………………………………….………34

Accounting Flexibility …………………………………………………………………………………40

Actual Accounting Strategy ….…………………………………………………………………….41

Quality of Disclosure …………………………………………………………………………………42

Qualitative Analysis …………………………………………………………………………42

Quantitative Analysis ………………………………………………………….……………44

Sales Manipulation Diagnostic ……………………………………………..…44

Expense Manipulation Diagnostic …………………………………..….……50

Potential Red Flags ……………………………………………………..……………………………57

Undo Accounting Distortion ……………………………………………………………………….60

Financial Analysis, Forecast Financials, and Cost of Capital Estimation………………………61

Financial Analysis………………………………………………………………………………………61

Liquidity Analysis……………………………………………………………………………………….61

Profitability Analysis…………………………………………………………………………………..70

Capital Structure Analysis……………………………………………………………………………75

3

IGR/SGR Analysis………………………………………………………………………………………78

Financial Statement Forecasting………………………………………………………………….81

Analysis of Valuations………………………………………………………………………………………….88

Methods of Comparables……………………………………………………………………………89

Cost of Equity……………………………………………………………………………………………95

Cost of Debt……………………………………………………………………………………………..98

Weighted Average Cost of Capital……………………………………………………………….98

Intrinsic Valuations………………………………………………………………………………………………99

Discount Dividends Model…………………………………………………………………………..99

Free Cash Flows Model…………………………………………………………………………….101

Residual Income Model…………………………………………………………………………….103

Long Run Return on Equity Residual Income Model…………………………………….104

Abnormal Earnings Growth Model……………………………………………………………..106

Credit Analysis…………………………………………………………………………………………………..108

Analyst Recommendation……………………………………………………………………………………109

Appendix………………………………………………………………………………………………………….111

Heinz’s Ratios…..……………………………………………………………………………………..111

Campbell’s Ratios…………………………………………………………………………………….111

Sara Lee’s Ratios……………………………………………………………………………………..112

ConAgra’sRatios………………………………………………………………………………………112

Regression…..…………………………………………………………………………………………114

Cost of Debt……………………………………………………………………………………………131

Weighted Average Cost of Capital……………………………………………………………..131

Discount Dividends Model…………………………………………………………………………132

Free Cash Flows Model…………………………………………………………………………….133

Residual Income Model……………………………………………………………………………134

Long Run Return on Equity Residual Income Model……………………………………135

Abnormal Earnings Growth Model……………………………………………………………..137

Method of Comparables……………………………………………………………………………138

Reference Page…………………………………………………………………………………………………139

4

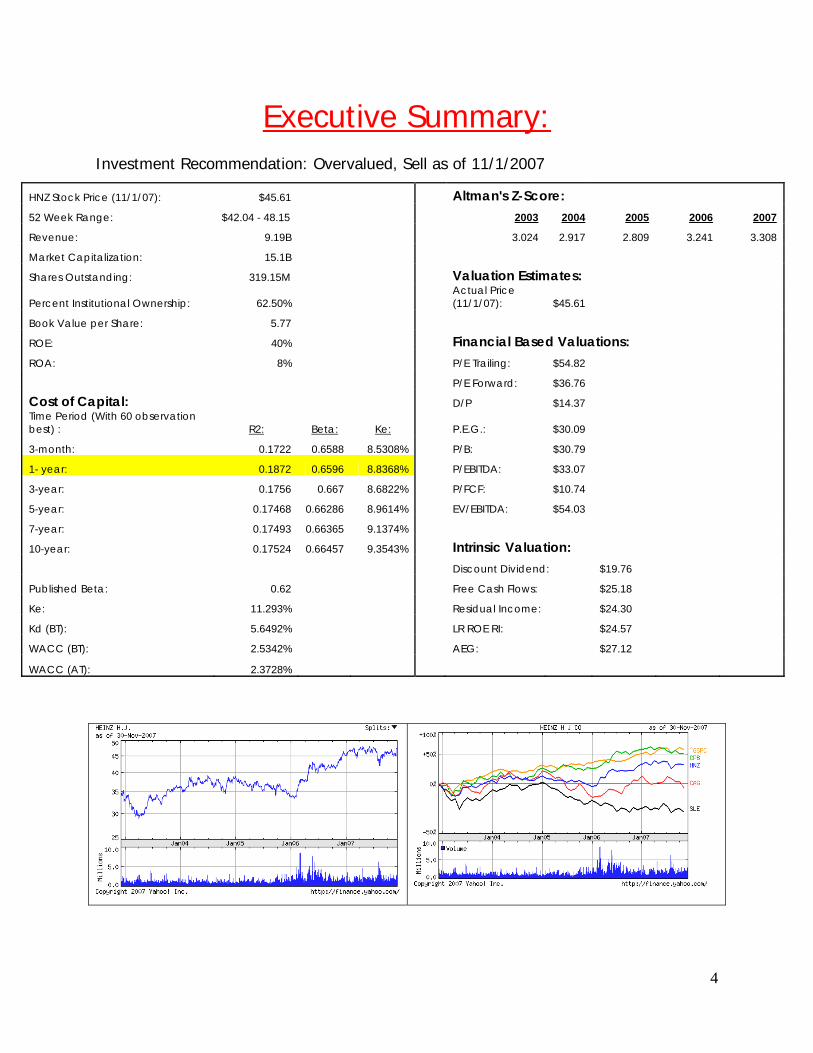

Executive Summary: Investment Recommendation: Overvalued, Sell as of 11/1/2007

HNZ Stock Price (11/1/07): $45.61 Altman's Z-Score: 52 Week Range: $42.04 - 48.15 2003 2004 2005 2006 2007

Revenue: 9.19B 3.024 2.917 2.809 3.241 3.308

Market Capitalization: 15.1B Shares Outstanding: 319.15M Valuation Estimates:

Percent Institutional Ownership: 62.50% Actual Price (11/1/07): $45.61

Book Value per Share: 5.77 ROE: 40% Financial Based Valuations: ROA: 8% P/E Trailing: $54.82 P/E Forward: $36.76 Cost of Capital: D/P $14.37 Time Period (With 60 observation best) : R2: Beta: Ke: P.E.G.: $30.09 3-month: 0.1722 0.6588 8.5308% P/B: $30.79 1- year: 0.1872 0.6596 8.8368% P/EBITDA: $33.07 3-year: 0.1756 0.667 8.6822% P/FCF: $10.74 5-year: 0.17468 0.66286 8.9614% EV/EBITDA: $54.03 7-year: 0.17493 0.66365 9.1374% 10-year: 0.17524 0.66457 9.3543% Intrinsic Valuation: Discount Dividend: $19.76 Published Beta: 0.62 Free Cash Flows: $25.18 Ke: 11.293% Residual Income: $24.30 Kd (BT): 5.6492% LR ROE RI: $24.57 WACC (BT): 2.5342% AEG: $27.12 WACC (AT): 2.3728%

5

Industry Analysis:

Heinz is a producer in the food industry and has many competitors that have

great effects on their decisions and products. They are a leading processed foods

manufacturer and own more than 68 factories world-wide and employing over 33,000

people. Heinz produces in Europe, Asia, and Australia. Food processing factories are

scattered in order to keep shipping and distribution costs low.

Some major competitors for Heinz include Sara Lee, ConAgra, and Campbell’s.

These existing firms battle for more and more market share since the food industry

mostly competes on quantity, not necessarily quality. Based on this high level of

rivalry, the threat of new entrants are very moderate. Since most of the products

produced in the food industry are very simple to recreate, the threat of substitute

products is high, giving the buyer moderate power. Also, since there are a lot of places

to receive the goods needed in the food industry, at least in the United States, the

suppliers have a little power in demanding higher prices from such large companies.

In order to gain a competitive advantage against their competition, firms in the

food industry must continually find ways to save more and more money compared to

the others. Efficient production, economies of scale, low-cost distribution, and product

variety are all key success factors in the industry that a firm must achieve to have a

chance at increasing its market share. Without these major success factors, the firm

would not have the cost saving and product variation needed to stay ahead or even

keep up with the rest of the industry.

Accounting Analysis:

It is very important that companies disclose proper financial statements. Their

information not only portrays how their company is doing but is also shows investors

how the company is doing. This is important for the companies to get loans. It is also

important for the companies to disclose correct information so they do not get in

trouble with GAAP. Heinz’s key success factors are economies of scale, cost leadership,

and low-cost distribution. Economies of scale are used to measure its wealth and size

relative to its competitors, and observe its relationships with its buyers. As the level of

6

disclosure continues to increase the level of transparency will also increase to provide

solid information.

Cost leadership is important in the food industry in order to get a position with

buyers to supply the company’s products. The food industry is very price competitive

and having a better priced substitutable product can increase sales versus having fewer

sales due to the cheaper replaceable good. Heinz strives to have competitive prices

and offer promotions on their products, such as coupons. This gives the buyer

incentives over other substitute products.

Low-cost distribution is the last of the key success factors. Since Heinz and the

food industry have to compete on price, they have to make up costs some where. One

way to decrease this risk is to go into long term contract with not only supplier, but also

buyers. This will provide more stability for Heinz and less worry of the future. It will

allow for them to allocate prices more effectively if they know their set price of

transportation.

Heinz strives to be cost effective, continue with a high level of research and

development, price sensitivity, and product variety. They also disclose information in

their 10-K’s that let shareholders and investors know where the numbers came from

and what methods they used. Heinz does a good job of disclosing this information. We

did not find any “red flags” through this process, but we did adjust for goodwill. This

shows that Heinz has a fairly high level of transparency in their disclosures.

Financial Analysis, Forecast Financials, and Cost of Capital Estimation:

We have put together a number of ratios that compare Heinz with three

competitors. We then used different financial information to project what Heinz’s share

price should be and compared it to Heinz’s share price at November 1, 2007. Liquidity,

profitability, and capital structure are the categories of the ratios we ran. We then used

these ratios to construct a forecast for Heinz’s three financial statements. Then we ran

regressions to see which beta was the best to use. Having this beta allowed us to

calculate our cost of debt, cost of equity, and weighted average cost of capital all of

which we would use to value Heinz.

7

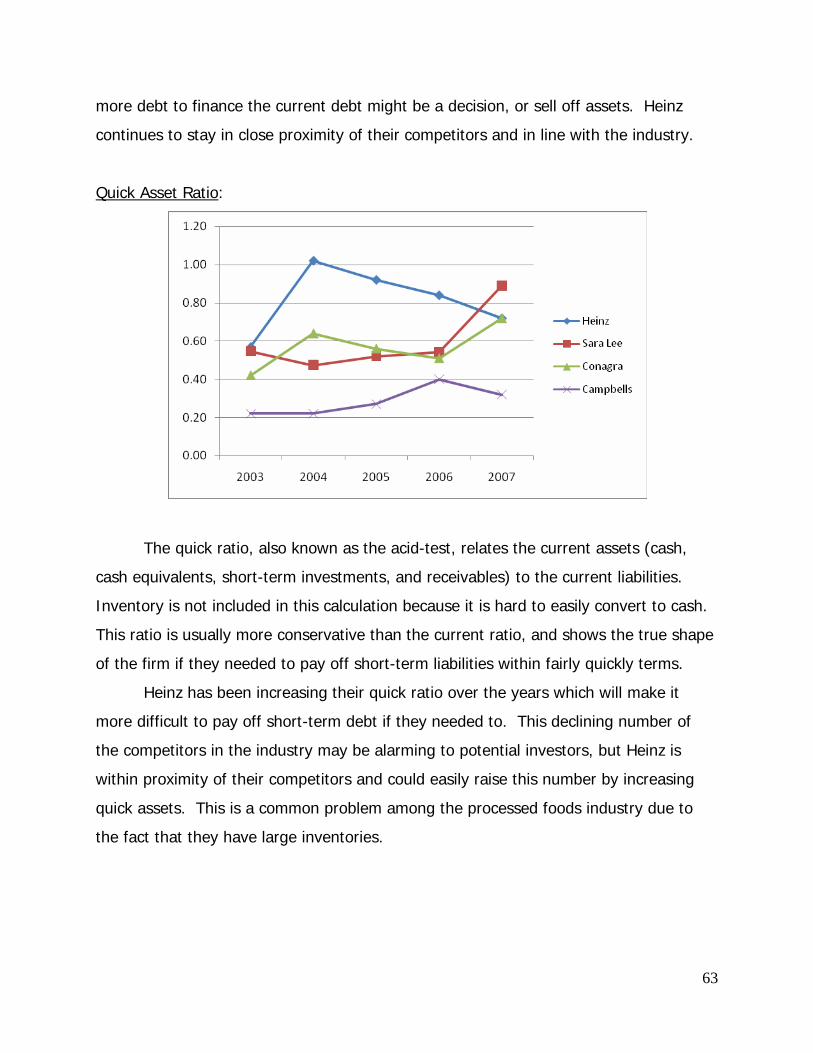

The liquidity analysis shows that Heinz is a liquid firm. The quick asset ratio,

inventory turnover, and working capital turn over all show this. Heinz is doing well

when looking at the industry especially in the current ratio and days supply of

inventory. The only concern we had with the liquidity analysis for Heinz was the days

sales outstanding. This number is currently in 2007 ok with consideration of the

industry but has come down from the highest number in the industry from the last four

years. This shows that they are aware of the problem and trying to fix it.

The profitability analysis shows that doing well in the food industry and most of

the time at the top of the industry. This is with the exception of Heinz’s ROE. They

have had a very unstable ROE over the past five years and have shown signs of

improvement, but not consistency. The ratios that we ran were gross profit margin,

operating profit margin, net profit margin, asset turnover ratio, ROA, and ROE.

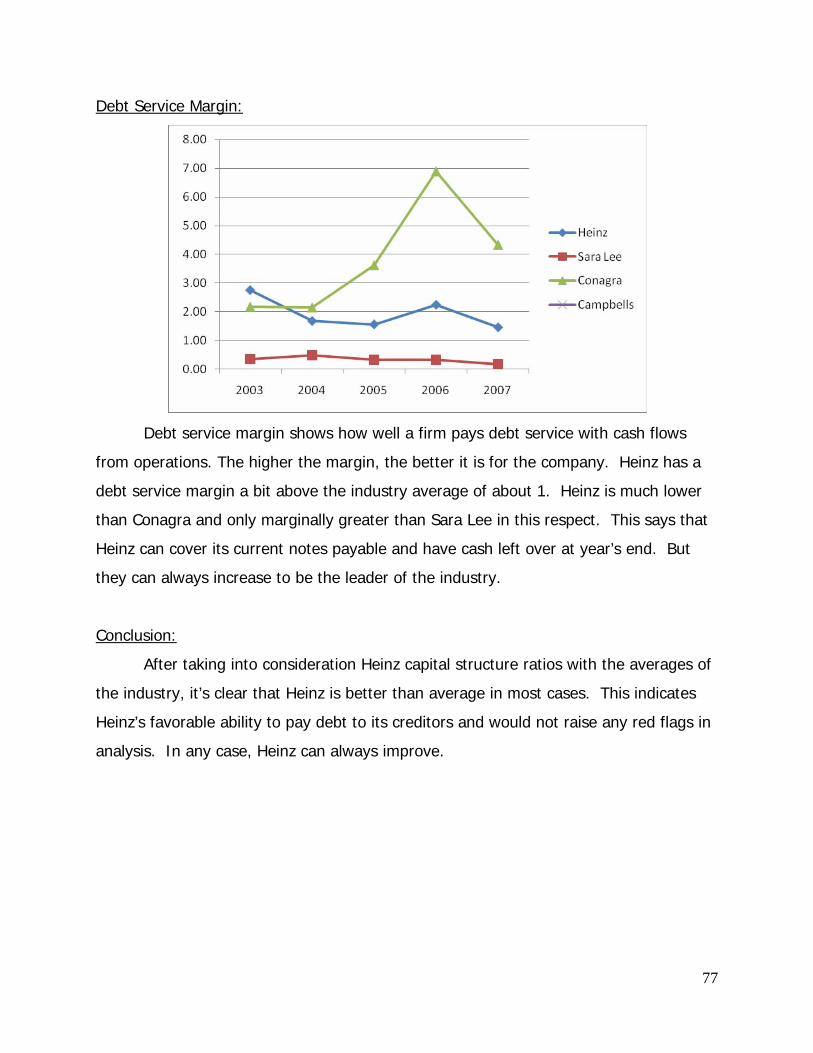

The last analysis was the capital structure analysis. Heinz showed good debt to

equity, times interest earned, and debt service margin. They are in line or at the top of

their industry. Although, Heinz can always improve on their ratios.

We then forecasted Heinz’s financial statements for ten years, starting in 2008

using the last five years of statement information. After analysis of all financial

information, we predicted an average growth rate of 5.4% of net income. We then

forecasted out the balance sheet, income statement, and cash flows statement which

will all help when we do our valuations of the firm.

Valuations:

The next step is to value the firm. We did this by first computing the cost of

equity, cost of debt, and the weighted average cost of capital. To solve the cost of

equity we used the CAPM model. We found the risk free rate and market risk premium

and used the best beta we found during our regression analysis. After finding the cost

of equity, we then found the cost of debt by taking all the liabilities on Heinz’s balance

sheet for 2007 and multiplied them by their corresponding rates. We then added up all

these numbers to get Heinz’s cost of debt. With these two numbers we found the

weighted average cost of capital. We used the WACC equation with the value of

8

liabilities over the value of the firm times the cost of debt plus the value of equity over

the value of the firm times the cost of equity.

Then, we computed our method of comparables. This method would show what

Heinz’s stock price should be. Each ratio gave us a different stock price. We ran P/E

forward and trailing, D/P, P/B, P.E.G., P/EBITDA, P/FCF, and EV/EBITDA. We found a

wide range of price from $10.74 from the P/FCF to $54.82 from the P/E trailing. These

wide ranges show that these methods vary in efficiency and effectiveness.

Our final valuation was the intrinsic valuation. This was made up of the discount

dividend model, free cash flows model, residual income model, long run return on

equity residual income model, and the abnormal earnings growth model. Heinz’s share

price will be valued at each of these valuation models and compared to their actual

share price from 11-1-07 which was $45.61. The discounted dividends model and free

cash flows models are both inaccurate in their valuations. They valued Heinz at $19.76

and $25.18 respectively. These both showed large fluctuations where there was a

change in variables. The residual income model valued Heinz at $24.30 and is a more

stable model along with abnormal earnings growth model. And the long run return on

equity residual income model comes up with $24.57 which is also a stable valuation.

Over all, these valuations show that Heinz is an overvalued firm.

9

Business and Industry Analysis:

Company Overview:

H.J. Heinz Company, a multi-national corporation, is a major processed foods

manufacturer. In 1869, Henry John Heinz and partner L.C. Noble started selling their

first product, horseradish, to local grocers in Pittsburgh, Pennsylvania. After 31 years of

selling condiments to local grocery stores, the H.J. Heinz Company became a legal

corporation on July 27, 1900. Today, Heinz is a leading processed foods manufacturer

owning more than 68 factories world-wide and employing over 33,000 people. “The

company also owns and leases office space, warehouses, distribution centers and

research and other facilities throughout the world (Heinz 2007 10K).” Food processing

factories are located sporadically throughout the world to make distribution more

efficient. The headquarters for the company still resides in Pittsburgh.

Food Processing

Factories

Owned Leased

North America 23 4

Europe 22 0

Asia/Pacific 14 2

Rest of World 9 3

Total 68 9

*Heinz 2007 10K

10

Heinz is included in the food sector of the major-diversified food industry. “Heinz

Company and its subsidiaries manufacture and market an extensive line of processed

food products throughout out the world including the following principal products:

ketchup, condiments and sauces, frozen food, soups, beans and pasta meals, infant

food and other processed food products” (Heinz 2007 10K). Heinz ketchup and Heinz

57 are the two leading products in the condiments sector. Acquiring new companies

around the world helps the company to grow their product line and increase the shelf

space allotted to them. Food processing plants dispersed throughout the world produce

the ingredients needed to manufacture their products. Having plants in numerous

major distribution areas help to keep shipping and processing costs low. Raw materials

that cannot be made in the factories are either bought through contracts with farmers,

or purchased in local markets.

The consumer goods industry contains a large number of companies, but the

main competitors of Heinz include the following: Sara Lee (SLE), Campbell Soup Co.

(CPB), and ConAgra Foods Inc. (CAG). With a market cap of $14.77 billion, Heinz leads

all of their major competitors. Heinz stock performance from 2003 to 2005 was

relatively stable around $46. Although the stock performance of Heinz is not as great

as that of Campbell Soup Co., Heinz net sales are far higher. Heinz stock price has

improved from $33.87 in 2003 to $46.81 today (www.finance.yahoo.com). The S&P

500 has historically been higher than Heinz and their competitors, but Heinz continues

to close the gap more and more every year.

*www.Heinz.com

11

“The H.J. Heinz Company has been a pioneer in the food industry for 138 years

and possesses one of the world’s best and most recognizable brands-Heinz. While the

Company has prospered for a long time, we are constantly finding new ways to

capitalize on emerging consumer trends and better methods of doing business (Heinz

2007 10K).” Heinz is constantly looking for ways to improve their current operations

and expand into new factories as needed. With increasing net sales and overall

company growth, Heinz will be incorporating more factories and distribution centers as

they are needed. The increase in revenues and operations allows Heinz to grow their

business all over the world. Also, over 100 new products were introduced within the

past year and many more continue to be developed. A 24% increase in marketing and

a 20% increase in research and development are both helping Heinz to grow their core

portfolio.

2003 2004 2005 2006 2007

Total Assets 9,224,751 9,877,189 10,577,718 9,737,767 10,033,026

Net Sales 8,236,836 7,625,831 8,103,456 8,643,438 9,001,630

Sales Growth (8.5%) (7.42%) 6.26% 6.66% 4.14%

*Numbers from Heinz 2003-2007 10K.

Industry Overview:

The consumer goods sector contains 32 different industries within its sector,

including the Foods-major diversified industry, the industry which Heinz is classified.

Heinz is placed in the major diversified food industry because not just one specialty

item is produced; instead they manufacture numerous different types of processed

foods. Having a wide variety of different products is beneficial to companies due to the

fact that consumers have more to choose from and are more likely to pick one of their

products versus one of their competitors.

12

Heinz relies on price competition to be able to keep up with their competitors.

“The Company operates in the highly competitive food industry across its product lines

competing with other companies that have varying abilities to withstand changing

market conditions (Heinz 2007 10K).” Being able to consistently update products and

development strategies is crucial for a company to remain competitive in their industry.

Using a cost leadership strategy will help Heinz to sell their products over other

companies. By having the lowest price for the highest quality good Heinz will be able to

attract and keep more customers.

Risk factors affect the percent of shares Heinz has in the market, and also their

financial analysis. Heinz is a multi-national company and faces the challenge of

currency exchange when totaling their sales and financial statements. Exchanging the

currency to U.S. dollars can cause accounting and numerical errors that will have to be

fixed on the financial statements.

Five Forces Model:

The five forces model is an analysis mechanism to help identify industry

competition, power, and profitability. The degree of actual and potential competition is

the first issue that the five forces model addresses. This competition among firms is a

determinant for prices in the industry. It ranges from the perfect competition state,

where a company’s prices are equal to the marginal costs, to a monopolistic state.

Monopolies can charge any price for any item, hurting the buyer. The five forces model

then examines rivalry amongst existing firms, threat of new entrants, and the threat of

substitute products. These competitive forces are tied closely to firm prices, costs,

products, and competitive moves with industrial firms. The second issue is the

bargaining power of the firm. This is important to firms because it can be an insight to

growth, income, or problems. It allows firm analysts to understand the position of the

firm over the bargaining power to buyers and suppliers.

13

Food Industry:

Competitive Force Level

Rivalry Among Existing Firms High

Threat of New Entrants Moderate

Threat of Substitute Products High

Power of Buyers Moderate

Power of Suppliers Low

Rivalry Among Existing Firms:

Problems that firms encounter in the food industry are unpredictable growth,

high industry competition, minimal differentiation, high fixed costs, and exit barriers. In

this industry, there are very high competitive products and pricing pressures due to the

large number of firms. Changes in business factors like pricing, product, or quantity

could lead to major changes in a firm’s profit. As the retail grocery trade continues to

consolidate, the food industry has to modify prices in relation to other firms and

increase buyer relations to be able to remain profitable.

Industry Growth Rate:

A main factor in industrial growth is competition. Having a flat growth industry

creates competition between firms for shelf space in a buyer’s store. A high growing

industry would lead firms to compete highly where price equals marginal cost to stay in

business. Being in a slow growth industry could possibly lead to the expectation of

price wars between competing firms. Having a negative growth would lead to lowering

prices below production costs which would cause a decrease in income. Each growth

14

scenario is directly affecting a firm’s income either positively or negatively. This is why

it is important for an analyst to track and predict the growth of industries. Shown in

the chart below, Heinz went from a negative growth to a positive and has steady sales

growth since 2004. The industry shows volatile sales growth. Sara Lee and Conagra

had major problems with their sales in a couple of years.

Sales Growth:

*Numbers from annual sales of each firm.

Concentration of Competitors:

The number of firms in an industry strongly influences how a company is run.

With a high number of firms at any given level, a company will have to aggressively

compete to get business and market share over competitors. Lowering prices, cutting

costs, and changing product lines are possible actions that could be taken in a high

concentration industry. Just the opposite is a low concentration industry where there

are few companies that can agree to charge a high price and receive higher profits

without advertising. This is called collusion. It can be very beneficial to firms and

quickly increase profits and keep them high. It is also important that there is a high

demand for products. The food industry has many firms that compete for the

15

customers’ needs or wants. The size of the firm is also very important in the

competition. The smaller companies cannot compare to the larger companies with

numerous product lines and international products. The chart below shows a range

from 15% to 35% market share per firm. The greater a firm’s market share increases,

the more it takes from others in the industry.

Industry Market Share:

Heinz percent of the market has been relatively stable for the past five years.

Although, Heinz net sales have been higher than its competitors for every year.

Having more diversified products than the other companies may reduce the percent of

the market shares because consumers do not realize which products are all made by

Heinz.

*Percentages are from annual sales compared with total industry sales for each year.

Differentiation and Switching Costs:

Businesses in the food industry strive to differentiate themselves from their

competitors by diversifying their product lines. However, there are many food

substitutes for the consumer. Firms appropriate this issue and pursue innovative ideas

to appeal to the customer’s desires. Competing companies fielding similar products

compete primarily on price and shelf space. Having similar products and prices creates

% Market Share

0% 5%

10% 15% 20% 25% 30% 35% 40%

2003 2004 2005 2006 2007

Heinz Campbells Sara Lee Conagra

16

low switching costs for consumers. Switching cost is the price that consumers are

willing to pay to switch from one product to a similar product, usually to a cheaper

substitute. Most consumers are indifferent between products and are quickly moved to

switch their buying behavior. Since switching costs are low in this industry, businesses

engage in greater price competition. Companies can also appeal to consumers by

offering new, diversified, healthy products that catch the consumer’s attention.

Economies of Scale:

An economy of scale is a process where a firm increases their size of production

and reducing long run average costs. Any size firm can experience economies of

scales. Introducing businesses outside of the United States is one example of an

economy of scale. Companies would increase the demand for their products and create

more revenue while spreading out their costs. While going international, firms keep in

mind diversity. Diversity is realizing and understanding the differences in multicultural

life. Being diverse with products, advertising, tastes, and values will increase this

success for a company.

Industry Diversity- Gross Profit:

U.S. Europe Asia/Pacific Rest of World

Heinz $1,140,000 $1,240,000 $386,800 $610,722

Campbells $2,657,000 --- --- --- --- --- --- --- $150,000

Sara Lee $6,602,000 $5,458,000 $2,042,000 $3,728,000

Conagra $3,138,500 --- --- --- --- --- --- --- $179,000 * Numbers in thousands from 2007 annual reports. Gross Profit = Net Sales – COGS

The Food Industry has a large market share outside of the United States. Heinz

has shown that selling domestically can be profitable as well as foreign sales. Heinz’s

percentage sold in the U.S. is about 34%, in Europe is 37%, in Asia/Pacific is 11%, and

17

the rest of the world is 18%. The major problems that comes up when selling outside

of the U.S. is dealing with exchange rates which are unexpected and can be very

unpredictable. Another major problem is that there are major cultural changes that

have to be made when looking at other countries. People from different cultures might

like a different type of spice in their food or lack of spice. Heinz would have to change

their recipes in order to sell any of their products.

Fixed and Variable Costs:

Costs play a large role in all firms’ success in earning a profit. The larger the

costs are, the less the company receives at the end of the year. Costs also provided

analysts with insight into the future of a company in projecting profit/loss outcomes. A

company ideally would like to have a small fixed to variable cost ratio. Firms should

have incentives to lower prices to increase the capacity of their products. The chart

below shows the food industry’s cost ratios. The average of Heinz fixed cost to variable

cost ratio is about .44, which is the average of 2003 through 2007. This means

companies have about double the variable costs to their fixed costs. This is not

profitable, especially in a price competitive industry.

Fixed Cost to Variable Cost Ratios:

2003 2004 2005 2006 2007

Heinz 0.4235 0.4635 0.4746 0.3645 0.4754

Campbells 0.3023 0.1952 0.1304 0.2769 0.1359

Sara Lee 0.4096 0.4124 0.4355 0.6756 0.4626

Conagra 0.3389 0.4412 0.4450 0.4337 0.4992 *Numbers from annual costs. Capacity:

When considering the capacity of an industry, the optimal goal is to have

demand greater than the company’s product supply. In the food industry, this is not

18

the case. Supply is greater than demand which is said to have excess capacity causing

the firm to lower already low prices in order to increase demand. This creates a

decrease in profits while costs are staying the same and the end outcome is less than

expected. From 2005 to 2006, Heinz had an increase in investing which showed an

effect on net income in 2007 which increase from 2006. Excess capacity in the food

industry is just another indicator that new entrant firms will fail before they even get

started.

Exit Barriers:

Exit barriers are anything that holds a company back from shutting down and

leaving its industry. Regulations can be assigned to an industry that companies have to

comply with before leaving. This is important for the company to consider if the

regulations or barriers cost more than the companies fixed costs. It would not be

reasonable to shut down if the company would have to pay more than could be earned

staying in the industry. That is why exit barriers are important factors in a business’

life. The food industry has few exit barriers to none. Since they would not hold a lot of

food in inventory, this would not take a long time. The most important issue would be

to disperse or sell the entire company’s disposable inventory. Then, it would sell off the

rest of the assets to pay off all costs and close books.

Conclusion:

The food industry is a highly competitive market. The competitiveness stems

from the similarities between company’s products and prices. The industry has a

gradual increasing growth rate, mostly concentrates on prices, competes on gaining

market share domestically and internationally, and has minimal exit barriers. Because

of high price competition, companies switch attention to the financials of costs and

liabilities. By decreasing costs and liabilities, the company will increase its net income.

19

Threat of New Entrants:

The threat of new entrants into the food industry is moderate. This industry has

low prices because of competition, which would not attract many new entrants. It is

comprised of many different types of firms ranging from large multi-product companies

to single product small companies. The threat of new entrants depends greatly on the

firm’s size. A billion dollar company would not have to be worried about new firm entry

because of their sheer size, while a small company would suffer from the switching

costs of customers. Economies of scale, first mover advantage, and barriers help

determine new entries into an industry.

Economies of Scale:

When deciding to enter into any industry, there are many important factors to

analyze and consider. The new entering company should compare its capital to the

firms that have the greatest market share. By looking at competitor’s operations, what

it buys and sells, how it invests, and other financial information, a new entrant can

determine if entering would even be worth it. The entrant would start off at a

disadvantage to the older companies. This is due not only to experience, but

economies of scale. The older firms have a positive income, relations with customers

and suppliers, innovations that took years to create, and the research to create new

products. The chart on the next page shows one of the important parts of the balance

sheet a new entrant should look at. Assets take a long time to posses and can add

great value to the company. A lender looks at assets to see if the company can back

up loans and the greater the assets, the greater the loans can be. If the assets are not

large enough, the company would struggle to keep up with other big dogs in the

industry.

20

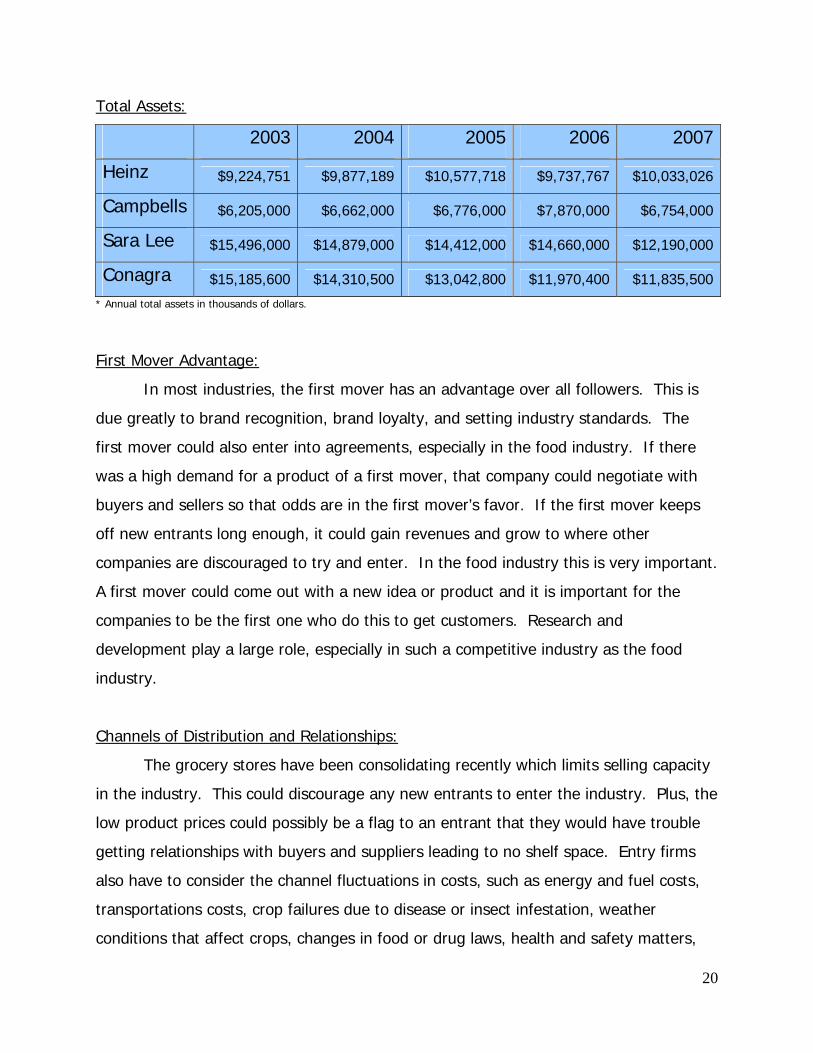

Total Assets:

2003 2004 2005 2006 2007

Heinz $9,224,751 $9,877,189 $10,577,718 $9,737,767 $10,033,026

Campbells $6,205,000 $6,662,000 $6,776,000 $7,870,000 $6,754,000

Sara Lee $15,496,000 $14,879,000 $14,412,000 $14,660,000 $12,190,000

Conagra $15,185,600 $14,310,500 $13,042,800 $11,970,400 $11,835,500

* Annual total assets in thousands of dollars.

First Mover Advantage:

In most industries, the first mover has an advantage over all followers. This is

due greatly to brand recognition, brand loyalty, and setting industry standards. The

first mover could also enter into agreements, especially in the food industry. If there

was a high demand for a product of a first mover, that company could negotiate with

buyers and sellers so that odds are in the first mover’s favor. If the first mover keeps

off new entrants long enough, it could gain revenues and grow to where other

companies are discouraged to try and enter. In the food industry this is very important.

A first mover could come out with a new idea or product and it is important for the

companies to be the first one who do this to get customers. Research and

development play a large role, especially in such a competitive industry as the food

industry.

Channels of Distribution and Relationships:

The grocery stores have been consolidating recently which limits selling capacity

in the industry. This could discourage any new entrants to enter the industry. Plus, the

low product prices could possibly be a flag to an entrant that they would have trouble

getting relationships with buyers and suppliers leading to no shelf space. Entry firms

also have to consider the channel fluctuations in costs, such as energy and fuel costs,

transportations costs, crop failures due to disease or insect infestation, weather

conditions that affect crops, changes in food or drug laws, health and safety matters,

21

export and import restrictions, and currency exchange rates. These would all lead to a

direct effect to the costs of production, transportation, and to an increase or decrease

of profits.

Barriers:

In the food industry, there are strict barriers dealing with obtaining, creating,

and selling a product that consumers put in their body. There is a strict health code

that each firm has to follow throughout its productions process. These barriers

differentiate healthy foods that consumers can trust and foods that could contain

harmful ingredients. Also in the food industry, sometimes there is a recall on food due

to ingredients or the production process. This is very costly to the companies who

produce these defected goods. These companies lose production costs along with the

profit loss and the cost of recalling all the products and disposing of them. These legal

rules could discourage new firms from entering the market due to the threat of major

capital lost.

Conclusion:

The foods industry has a low to moderate threat of new entrants. This is mainly

due to the large number of aged firms already in the industry. Their economies of scale

would be incomparable to a fresh firm. New firms would find difficulty if entered into

the food industry for three main reasons. The first is the first mover advantage. The

industry advantage usually always goes to the initial firm in any industry. The second

reason is the capacity of shrinking distribution channels of suppliers and especially

buyers. This makes it hard for entering firms to start out at equal to experienced firms

already in the industry. The final reason is the high responsibility of legal barriers.

These issues pose high income loss in extreme situations, but minimal in consideration

that people will be consuming the products. All this information listed above points to

limited entry into the foods industry in the near future.

22

Threat of Substitute Products:

There will always be a high degree of competition between substitutes in the

food products market. Due to the fact that there are many relevant substitutes for

industry products in this market targeting the same customers, there is a serious threat

of consumers switching to a competitively priced comparable product. The similarity

between product lines with others on the market directly correlates with a low switching

cost for consumers.

Buyers’ Willingness to Substitute:

Since many industry products are functionally as well as economically the same

as many competitor products, buyers have an exceedingly low switching cost for most

industry products. This further emphasizes the fact that the food products industry is a

highly competitive industry. The one exception to this rule is when a particular company

negotiates exclusive contracts with high visibility like restaurants, hotels, or hospitals. In

this case, the respective company may only carry company specific condiments or food

products. Presumably, these contracts are renegotiated on a routine basis, emphasizing

the importance of maintaining solid business relationships with buyers.

Relative Price and Performance:

In light of the fact that in certain instances industry products have superior

branding and name recognition, in some cases they do have a distinct competitive

advantage. However, the industry is flooded with many large and small competitors,

and substitute products remain a considerable threat directly affecting the company’s

bottom line. Therefore, it is important for competitors to charge a similar amount for

their products despite this competitive advantage. The industry’s business strategy is to

continue to reduce costs to increase company profit margins. Industry competitors can

also gain an advantage by having its various brokers and agents initiate new as well as

23

maintain existing relationships with its customers (www.finance.yahoo.com).

Maintaining a loyal base of customers is of the utmost importance to the company.

Conclusion:

There are plenty of substitutes readily available and in close proximity in the food

products industry. In this competitive environment, companies are concerned with

losing market share to competitors. Combine these aspects with extremely low

switching costs and it is easy to see why industry insiders focus their efforts on

reducing costs and selling as much product as possible. These efforts coupled with

sufficient brand recognition enable companies to stay ahead of the curve and maintain

increasing profit margins.

Bargaining Power of Customers:

The amount of bargaining power consumers have greatly affects how a firm runs

its operations. The main determinants of this are price sensitivity and relative

bargaining power. Price sensitivity directly affects the amount of bargaining between

buyers and sellers. Relative bargaining power directly affects the ends buyers’ decisions

in which product they end up buying. Major retail supermarket chains, large scale

grocers, hotels, and still smaller local stores are a sampling of the customers industry

competitors sell their products to. Some companies in the industry also have a highly

diverse international customer base, selling products to various food serving entities like

sports stadiums or airlines.

Price Sensitivity:

Price sensitivity is essentially the price customers are willing to pay for the value

they perceive in an item. The value for industry competitors in the food product

industry is largely based upon consumer taste preferences and competitor pricing. This

is mainly evidenced in products like steak sauce, where the recipe is unique and taste is

24

a vitally important factor. On the flip side, industry competitors have many products

such as ketchup and mustard that contain the same basic ingredients as competing

products. Due to the fact that these are also very popular items, there are a substantial

number of imitators in the industry trying to chip away at various competitors’ market

share. For these products in particular, brand recognition and price play more of a key

role in sales. To have their products offered in places like Wal-Mart, companies have to

compete on price. This is mainly due to outside pressure from Wal-Mart to maintain a

cheap and affordable price for its customers. This is a double edged sword because

keeping prices for buyers like Wal-Mart low means that companies must also fight to

keep their costs of production low.

Bargaining Power:

Relative bargaining power relates back to an earlier discussion of switching costs.

With low consumer switching costs, companies within the industry must advertise

creatively to set themselves apart with things like television commercials, placing

coupons in newspapers and other local periodicals, and setting up point of sale displays

to further gain brand recognition. The effects to individual companies of potentially

losing customers are also taken into account when discussing bargaining power. As was

previously stated, customers in the food products industry generally have a low

switching cost because the competition’s product can generally be found in the same

store on the same shelf. Companies also must worry about their other set of buyers,

stores they directly sell their products to. These are important negotiations because

they determine in-store shelf space and prices as discussed in the previous section.

Conclusion:

The two most important factors determining customer bargaining power are

price sensitivity and relative bargaining power. To a very large extent, companies

construct their appropriate business strategies in accordance with these factors.

25

Bargaining Power of Suppliers:

Relative bargaining power of suppliers is also a key component to companies

maintaining their past success. This is relatively the same as the discussion above on

bargaining power of buyers, except the focus is flipped around the other way now. If

suppliers are highly leveraged with bargaining power, companies may be forced to

comply with that supplier’s stipulations. This could potentially have the effect of

increasing input costs and lowering profit margins. In this case, the firm is at the mercy

of its suppliers. On the other hand, if there are many different suppliers to the

company, then that organization has the more powerful position. With this power they

can force suppliers to decrease their prices and perhaps even dictate more demanding

shipping standards.

Price Sensitivity:

With the food products industry being so large, it has a position of power over its

suppliers because there are a large number of commodities growers. Suppliers must

adapt to the demands made by large companies within the industry because if they do

not, other suppliers would be more than happy to take their place. There is generally a

market rate for the raw materials that companies purchase for their products. In certain

instances however, the company can be held hostage to the commodities markets it

purchases supplies from. Companies buy commodities such as tomatoes, potatoes,

dairy products, and meat to use in its food products. The availability or cost of such

commodities may fluctuate widely due to government policy and regulation, crop

failures or shortages due to plant disease or insect and other pest infestation, weather

conditions, or other unforeseen circumstances (Heinz 2007 10K). These fluctuations in

price and supply could have a detrimental effect on a company’s business. As an

example, Heinz raised its prices this year to offset higher costs of dairy sweeteners and

oils. “This was in response to the rising popularity of ethanol, which drove the price of

corn to record high prices earlier this year (www.forbes.com).”

26

Bargaining Power:

Due to the industry’s significant size, there is quite a bit of bargaining power with

suppliers in the industry. The supply chain is still a critical part of the operations

though. Any problem with the manufacturing or distribution sectors of a companies

supply chain could inhibit a company’s ability to make and distribute its products.

Keeping this in mind, it is important for companies to maintain a supply chain that can

consistently and economically purchase raw materials, manufacture, distribute, and sell

its products to customers in a timely manner.

Conclusion:

The bargaining power of suppliers to a very large extent determines how

competitive a company is able to be within a given industry. Maintaining relationships

conducive to consistent and cost effective means of production and delivery is essential

to the survival of any firm in the food products industry. Companies must continue to

find the right balance in maintaining relationships with its buyers and suppliers to stay

relevant within its industry and fully utilize its production capacities in hopes of

maximizing shareholder wealth.

27

Value Chain Analysis:

In summary, the food industry in which Heinz is a primary competitor is

characterized by high rivalry among existing firms, a moderate threat of new entrants

into the market, a high threat of substitute products, moderate bargaining power of

buyers, and low bargaining power of suppliers. The factors that contributed to these

conclusions were unpredictable growth, high industry competition, minimal

differentiation, high fixed costs, and exit barriers in the industry. For a firm seeking to

be competitive in the industry, focus must be maintained on various success factors.

Primary concern in the highly competitive food industry, with the variety of

substitutes available to consumers, should be placed on cost leadership, rather than

differentiation. It should be noted that no firm concentrates purely on cost leadership

or differentiation, so a successful competitor will have a combination of both, but

emphasis should be placed on cost leadership.

Competitive Strategies:

In an industry with high competition, many substitute products available, and

little consumer loyalty, a firm competes by becoming a cost leader. Factors involved

with becoming a cost leader include efficient production, low input costs, economies of

scale, and low-cost distribution. However, as mentioned earlier, no firm should be

purely cost-competitive, and in the food industry, firms who offer a great deal of

product variety also prosper.

Efficient Production:

Efficiency is important for any firm in any industry. Getting maximum output at

minimum cost is arguably the most important factor to meet in being competitive. In

the food industry, however, it is very important. Many of the input costs are highly

volatile for the firms in this industry, as they are based on agricultural commodities.

This leads two primary dilemmas for a firm in the industry, the first being that a firm

28

must be able to keep costs down when commodity prices are high. This requires

maintaining low costs for other inputs, and an efficient production set-up. The second

dilemma is that all of the firms in the industry are typically getting their agricultural

inputs at the same or very similar prices. For a firm to be competitive in this type of

environment, it must be efficient in its production. To determine whether or not a firm

is an efficient producer, one must monitor the costs of the firm. All costs should be

minimized, and those not directly related to the production process should virtually be

eliminated.

Economies of Scale:

Size matters in the food industry. In order for a firm to be competitive, it must

be large enough to market its product to a wide range of customers. To do this it must

be able to produce its products on a large scale, and distribute those products to many

different locations, in many cases world-wide, while keeping costs as low as possible.

This is difficult for smaller, younger firms to achieve, as it requires good relationships

with buyers, and large amounts of capital. Therefore, in this particular industry, it pays

to be big, wealthy, and established. Obviously, to measure an efficient economy of

scale would be to measure its wealth and size relative to its competitors, and observe

its relationships with its buyers. In this industry, the efficient economies of scale come

from the bigger companies.

Low-cost Distribution:

Another way for a firm to be competitive is to keep its distribution costs down.

This allows for higher profit margins down the line, which is critical in a cost-competitive

industry. In this instance, it helps to be large and experienced, again. Firms that have

the capital and the relationships with distributors have a better bargaining position than

smaller, less wealthy firms and can better keep the costs low. To get a good

measurement of this, one should measure how much the firm is spending on

distribution relative to what its competitors are spending.

29

Product Variety:

Product variety is not typically associated with a cost competitive market, as it is

usually more expensive for a firm to produce a multitude of products. In the food

industry, however, there are many different, closely-related products for a consumer to

choose from, and since there is less customer loyalty in this market, it is easy for a

consumer to choose one firm’s product over another’s. Therefore, the more products a

firm can offer a consumer to choose from, the more likely a consumer is to purchase

one of that firm’s products. Many firms in the industry do this either through various

brands, or by using a spin-off product, and in order for a firm to compete, it must do

the same. Efficiency in product variety can be measured the number of products

produced by a firm and the amount generated by each of those products.

Conclusion:

This is a highly competitive industry, as demonstrated by the wide availability of

substitute products, large number of competing firms, and volatility of inputs.

Maintaining a competitive advantage requires that a firm keep its costs as low as

possible. It must maintain efficient production, lowering as many of its input costs as it

can down, keep its distribution costs down, and market to as many consumers as

possible. It must also supply what the consumer is looking for, which requires offering

many different types of products, and yet maintaining low prices. Consumer loyalty is

extremely difficult to come by in this industry, so a firm seeking to be competitive must

cater to whatever a consumer may want.

30

Firm Competitive Advantage Analysis:

Heinz has been implementing a two year plan primarily to increase shareholder

value, but has also, helped increase net sales and operating income. This plan aims to

execute several key objectives in order to produce efficiently, grow economies of scale,

lower the cost of distribution, and increase the company’s product variety. These are

necessary for all companies in the food industry, and Heinz has made it a goal to lead

the industry in these aspects in order to stay ahead of the competition in the food

industry. According to Heinz’s most recent 10-K, thanks to the current two year plan,

“The Company achieved its targets for Fiscal 2007 and is well positioned for continued

growth in Fiscal 2008.”

Efficient Production:

In the food industry, it is essential to produce your product very efficiently to

increase profit by reducing cost of goods sold. Heinz in the past year has closed or

divested 16 plants in order to help lower production costs (www.heinz.com). This can

be seen as a precursor to “reducing cost of goods sold by 90 basis points as a

percentage of sales, and total gross profit exceeding the company’s expectations.” The

recent development of a “Global Supply Chain Task force” by Heinz has reduced the

cost of production in the recent fiscal year, and is expected to continue to help drive

production cost down. Since inputs such as agricultural inputs are hard to judge and

usually cost all companies in the food industry practically the same, Heinz is willing to

discard unproductive plants in order to help drive costs that they can more easily

control downwards, according to their most recent annual report.

Economies of Scale:

In this industry, being a large company is very important if you want to have

bargaining power over your suppliers. As stated earlier, the power of the suppliers in

this industry is low since most of the companies are large. For being one of the largest

31

companies in a large industry, Heinz is able to, for the most part, negotiate easily with

suppliers (www.finance.yahoo.com). Since Heinz produces so many of so many

different products, they can easily buy in massive quantities, which reduce the cost per

item significantly. By doing this, the company greatly reduces costs, and receives a

great, loyal supplier foundation. Staying with the same suppliers and signing long term

contracts can easily keep costs down as long as they are able to trust these suppliers.

Along with being a large company being able to “strong-arm” suppliers, Heinz, with its

two year plan which includes increasing cash flow and capital, has the ability to buy

certain suppliers so they can even supply some of their own necessities. In addition,

with an acquisition such as of IDF Corp., they can pick up suppliers through acquisitions

of competitors (www.heinz.com).

Low-cost Distribution:

In an industry that almost everyone receives the same products for the same

price, cost reduction is a key component in order to maximize profit margins. Another

way that Heinz is trying to achieve cost reduction is by lowering the cost of distributing

their products. This is a daunting task for a company who sells hundreds of products in

over 200 countries, but they understand they need to lower these costs in order to stay

as profitable as possible. One major way that Heinz has been able to control

distribution costs was by entering into “long-term agreement with ES3, LLC, a leading

national third-party logistics and distribution company, to be its lead logistics provider of

warehousing and distribution services for Heinz's ketchup, condiments and sauces

businesses” (www.es3.com). By signing this agreement, Heinz effectively has given the

task of distributing its goods to a large distribution company that has more distribution

centers in the United States that Heinz products can leave from and find their ways to

stores nationwide.

Product Variety:

In the food industry, firms must go beyond a simple one product in order to be

competitive. Heinz is no different in that they sell not only items such as ketchup and

32

mustard, but also meals, snacks, and infant foods. Though their top 15 brands grew

8.5% on the year, nearly 100 new products were launched (Heinz 10-K 2007). Heinz’s

current research and development teams are working on over 200 new products across

these several markets. In order to continue at varying the products that they produce,

Heinz has increased research and development nearly 20% in innovation and consumer

insight. By increasing consumer insight, the company will be able to continue to

research products that consumers actually want or need, making the whole innovation

process less expensive in the long run. The company is looking into “incremental

improvements in… convenience products like portable hand-held snacks… and

microwavable soups in the UK, Australia and New Zealand.”

Conclusion:

Heinz has positioned itself to increase market share by continuing growth

worldwide. By continuing to find ways to produce efficiently, increase economies of

scale by growing at a safe rate, lower the costs of distribution, and research and

develop new products, the company has established its future and put themselves in a

great situation to continue to lower costs and increase profits. Halfway through the

most recent two year plan, the numbers of the past year prove that Heinz has

implemented a great plan in order to stay competitive.

33

Accounting Analysis:

The balance sheet, income statement, and the statement of cash flows all show

the current standings of the firm and what it plans to do in the future. The

Management Discussions and Analysis section of the annual report provides insight into

the company’s performances, business conditions, and decisions. Financial statements

are important for numerous reasons. The main reason for presenting all necessary

financial statements is to provide information to investors. Investors are an important

part of any business. Without enough funding for operations, a company would be

forced to leave the industry. Investors fuel the firms operations leading directly to

profits. Another important reason to disclose financial statements is for shareholders.

A firm’s optimal goal is to maximize profits for the shareholders. The statements give

valuable insight to shareholders possibly creating a higher value for the company stock.

These financial statements must be prepared very diligently and properly. There

are many rules put into place so that firms cannot alter numbers or policies to make

their company look better. Firms must follow General Accepted Accounting Practices

(GAAP) that is put in place by the Securities and Exchange Commission (SEC). GAAP

sets the standards, conventions, rules, and procedures that firms must follow when

creating their financial statements. These rules also help investors to understand all of

the financial statements of the company so that they can know what they are investing

in.

Accounting allows managers to have room to modify their firm’s financial

statements to better fit the company. Having the ability to choose their own policies

creates the opportunity for managers to adjust the correct numbers to different

numbers that would make the company appear better off and have higher profits. An

accounting analysis is necessary to look at the financial statements to see if there is

purposeful wrong doings and correct them.

Accounting analysis evaluates the degree to which a company’s financial

statements capture its business principles. Analysts can follow these rules to evaluate

34

the firm’s financial statements and undo the mistakes. The first step is to identify key

accounting policies. A company’s industry characteristics and strategies help to

determine their key success factors. “One of the goals of financial statement analysis is

to evaluate how well these success factors and risks are being managed by the firm

(Palepu & Healy 3-7). The second step is to assess the degree of potential accounting

flexibility. This step connects key accounting policies to potential accounting flexibility

to see where the company can separate from the general structuring of financial

statements. The third step is to evaluate actual accounting strategies. This is where

the analysts can determine true performance from mistakes or changes in financial

statements. The fourth step is to evaluate the quality of disclosure with a qualitative

and quantitative analysis. This step shows how well the financial statements were put

together and how close they are to the actual numbers. The fifth step is to identify

potential red flags. A red flag is anything that the analysis cannot explain and is

directly related to what was found in step four. Any red flags that are found are good

indicators that the manager changed the numbers indicating no explanation. And the

last step in accounting analysis is to undo the accounting distortions that were found in

the previous steps. This is important so firms are transparent and not misleading to

their investors or stockholders. When firms do unknowingly make mistakes they would

be brought to the company’s attention and corrected at this point.

Key Accounting Principles:

When evaluating a company’s key accounting principles it is important to know

the key success factors. Understanding these factors can help the company to decide

which accounting principles to use to keep a competitive edge over their competition.

As stated earlier in the five forces model, the key success factors of Heinz are

economies of scale, cost leadership, and low-cost distribution. Heinz is in an industry

with a large amount of product substitutes, and must go the extra distance to keep

them ahead of their competitors. Setting the costs low will persuade consumers to

purchase their product instead of a higher priced alternative. In order to keep the costs

35

low and maintain cost leadership, Heinz must be efficient in their production and

purchasing of raw materials. When trying to keep the inputs as inexpensive as possible

it allows Heinz to keep their prices low. Product variety is also very important for Heinz

to be able to beat their competition. With so many different products to choose from in

this industry, Heinz must have as many products on the shelves as possible to ensure

success. The more products that Heinz can distribute the more likely the consumer is

to purchase from their line of products. The key success factors help to establish the

following key accounting policies used by Heinz.

Sales Growth:

Due to the highly competitive food processing industry, Heinz has to remain a

cost leader to continue the growth of both the company and net sales. Through

acquisitions and mergers, Heinz continues to expand their operations throughout the

world, and better manage fixed costs. With larger companies it is easier to mass

produce and distribute which keeps costs low. Since Heinz has food processing

factories and distribution centers world-wide, distribution costs are lower. “Gross profit

increased $299.8 million, or 9.7%, to $3.39 billion. These improvements reflect higher

volume, productivity improvements and favorable foreign exchange, partially offset by

commodity cost increases (Heinz 2007 10K).” Heinz is constantly trying to find ways to

increase productivity and decrease costs to raise the gross profit. Over the past five

years net sales of Heinz has been rising except for in 2006 where the sales were

comparable with that of 2005. The net sales growth is shown in the table on the

following page.

36

*Heinz 2007 10K

Heinz continues to look forward to new mergers and expansions that will

increase the net sales of the company. “In fiscal 2008, the Company will continue to

invest in improved business systems in order to boost the efficiency of its promotional

programs, particularly in Europe (Heinz 2007 10K).”

Post-Retirement Benefit Plans:

Heinz offers post-retirement health care and benefit plans for those employees

that are eligible. Benefit plans make it difficult for any cost leadership company to keep

their costs low while still following the key success factors. Heinz has to try to

accurately estimate the liabilities and discount rates that will be utilized by their

employees at a future date. It does become hard trying to keep the pension rates

competitive with other companies while still keeping overheads low for the cost

competition in the industry. Heinz has stated in the 2007 10K that “Several statistical

and other factors that attempt to anticipate future events are used in calculation the

expense and obligations related to the plans including assumptions about the discount

rate, expected return on plan assets, turnover rates and rate of future compensation

increases as determined by the Company, within certain guidelines.” Often times this

37

type of aggressiveness in accounting strategies can make it hard for the investor to see

what is really true about the company.

Pension Discount Rates

2003 2004 2005 2006 2007

Heinz 5.90% 5.80% 5.50% 5.30% 5.50%

Campbell’s 6.39% 6.19% 5.44% 6.05% N/A*

Sara Lee N/A* N/A* N/A* N/A* N/A*

Conagra 7.25% 6.50% 6.00% 5.75% 5.75%

*Numbers from 10K’s of companies

The table above shows the pension discount rates of Heinz and their

competitors. Decreasing rates means that the numbers are becoming more transparent

to the company and investors. Keeping the discount rates relatively consistent shows

that Heinz is confident in their key success factors. The key success factors are often

used when setting these rates to help keep the costs low.

Operating and Capital Leases:

An operating lease is “A lease for which the lessee acquires the property for only

a small portion of its useful life (www.investorwords.com).” Operating leases are not

recorded on the balance sheet because they are not owned by Heinz, but are usually

included in the income statement as an expense. This can cause the financial reports

to not be transparent as it makes liabilities seem lower than they really are. Operating

leases are utilized by Heinz to gain access to production and office facilities,

warehouses, and equipment that are necessary in production and distribution of

products. These lease obligations “amounted to approximately $104.3 million in 2007,

$97.6 million in 2006, and $101.2 million in 2005 (Heinz 2007 10K).” This is a relatively

small amount compared to the total liabilities.

Capital leases are defined by www.investorwords.com as “A lease that meets one

or more of the following criteria, meaning it is classified as a purchase by the lessee:

the lease term is greater than 75% of the property's estimated economic life; the lease

contains an option to purchase the property for less than fair market value; ownership

38

of the property is transferred to the lessee at the end of the lease term; or the present

value of the lease payments exceeds 90% of the fair market value of the property.”

Capital leases are used by Heinz, but not as often as operational leases. This type of

lease is stated on the balance sheet and is amortized over the asset’s useful life. The

table below illustrates the total long term debt versus operational and capital leases.

< 1 year 1-3 years 3-5 years > 5 years Total

Long Term Debt $538,236 $1,521,200 $1,873,122 $3,259,179 $7,191,737

Capital Leases $10,046 $19,423 $54,391 $33,581 $117,441

Operating Leases $67,002 $108,994 $71,476 $188,163 $435,635

*Heinz 2007 10 K (amounts in thousands)

Operating and capital leases are important in a cost leadership industry. Most

firms will want to keep most of their obligations classified as operating leases to make

the financials more appealing to investors.

Currency Rate Risk:

International companies face numerous market risk factors due to the conversion

of currency into U.S. dollars. Market risk numbers are not included on the balance

sheet because they are not believed to have an affect on the financial situation of the

company. The risks can be somewhat diversified since Heinz owns factories throughout

the world and not just in one market. “The Company may attempt to limit its exposure

to changing foreign exchange rates through both operational and financial market

actions including entering into forward contracts, option contracts, or cross currency

swaps to hedge existing exposures, firm commitments and forecasted transactions

(Heinz 2007 10k).” Maintaining low costs is vital in following the key success factors.

Although some market risks cannot be avoided, it is necessary for Heinz to try and

decrease whatever risks they can.

39

Research and Development:

Heinz is constantly looking for new and innovative products that can increase

company value. This requires that a large amount of money be spent on research and

development. R&D is reported in the income statement under the selling, general, and

administrative expenses and not as an asset. Expensing this out ensures that the net

income level is not temporarily higher than the real number.

Recently, Heinz has set out a goal for the company to grow the core portfolio

including the largest brands. The Heinz 2007 10K states that, “This strategy

established targets for increased marketing spending of $50 million and double digit

increases in research and development costs.” This was almost a 20% increase in

research and development in 2007 alone. Continually increasing R&D costs can make it

difficult to remain a cost leader, but Heinz expenses them which help to keep their fixed

costs low.

Heinz is very reliable about following the proper accounting methods of

expensing these costs, and not recording them as an asset. Although this might not be

the best option for cost leadership competition, it is the correct way to report R&D.

This keeps the company in stride with the key success factors and investors.

Conclusion:

With the accounting policies constantly changing, it is important for any company

to keep up with them and make sure that they are following their own key success

factors. Having clear, transparent financial reports is the best way to achieve this.

Heinz does a good job of disclosing all of the information necessary in reporting the

firm’s position. The accounting policies above followed the Heinz’s key success factors

of economies of scale, cost leadership, and low-cost distribution. As the level of

disclosure continues to increase the level of transparency will also increase to provide

solid information.

40

Accounting Flexibility:

Firms provide financial statements so that investors can have an accurate

assessment of the firm’s financial position when making investment decisions. The

information provided should be dependable and consistent over time in accordance with

Generally Accepted Accounting Principles (GAAP). The accounting flexibility given by

GAAP allows firms to either accurately depict their current financial position or to

disguise certain shortcomings.

Operating & Capital Leases:

Capital and operating leases are a major area where Heinz has accounting

flexibility. With its operating leases, Heinz leases the right to use a particular property

for operating its business. When the lease is up, Heinz then has the option to either

renew the lease for an additional term or abandon the premises. “The monthly rent

expenses associated with operating leases only show up on the income statement and

not the balance sheet (http://pages.stern.nyu.edu).” This alludes to the fact that

assets and liabilities can be understated by the company when using operating leases.

This does not necessarily reflect the true financial state of the company. This is

problematic because investors will be more inclined to invest if they perceive a company

to be more profitable than it is in reality.

“In a capital lease, the lessee assumes some of the risks of ownership and

enjoys some of the benefits. In this case, the leases are listed as both an asset and

liability on the balance sheet (http://pages.stern.nyu.edu).” Firms usually choose

operating leases over capital leases since capital leases recognize expenses sooner.

Since both lease type amounts are relatively small for Heinz, they maintain accounting

flexibility when choosing which lease style to apply.

Post-Retirement Benefits:

Post-retirement benefits can be very large liabilities for firms. Heinz must

determine the present value of future cash flows they will have to pay out to employees

41

with benefits through careful calculations based on employee base, the discount rate,

expected asset returns, and future compensation rates. “The lower the discount rate,

the more conservative the pension accounting; the higher the discount rate, the more

aggressive (http://beginnersinvest.about.com).” Lower discount rates obviously

represent higher assets for a company because expenses associated with pensions

would be less. Lower discount rates will also cause higher rates of return, thus

increasing the attractiveness of investment within a given company. Heinz has

consistently maintained a lower discount rate than that of its competitors. This

conservative style illustrates Heinz’ supreme confidence in the performance of their core

portfolio of products and acquired businesses enables them to have the flexibility of

lower pension discount rates.

Conclusion:

Accounting flexibility, as provided by GAAP, enables firms to best display their

financial realities in a way they see relevant to their line of business. This power can

also be used to disguise investors into thinking a firm is more valuable than it is in

actuality. Heinz relays helpful insider information on its company in a way that

contributes to the ability of investors to get a fair picture of its financial position.

Actual Accounting Strategy:

The leeway provided by GAAP will cause companies to resort to either aggressive

or conservative accounting styles when making their financial statements. The style

chosen depends upon whether the company wants to give a realistic or unfairly

optimistic view of their current business setting. Heinz appears to have chosen a mix of

conservative and aggressive accounting in formulating its financial statements.

Heinz had $104.3 million worth of operating leases in fiscal 2007. While this

number may seem high, it is a relatively small amount when compared with the

company’s total liabilities. Treating this lease expense as an operating expense on the

income statement enables Heinz to leave these leases off the balance sheet. This could

42

appear to be an aggressive accounting technique when considered on its own, but the

amount is small relative to total liabilities and Heinz’s direct competitors within the

industry use similar accounting methods. This bit of aggressiveness is also offset by the

disclosure of these facts in the financials.

Heinz has pension plans available to eligible employees. “The company sponsors

pension and other retirement plans in various forms covering substantially all

employees who meet eligibility requirements. Several statistical and other factors that

attempt to anticipate future events are used in calculating the expense and obligations

related to the plans (Heinz 2007 10K).” This is used with estimated pension withdrawal

and mortality rates to estimate the company’s future benefits expenses. Heinz has

used a discount rate consistently lower than its competitors, though competitor rates

are essentially in the same ballpark. Heinz has kept its discount rate consistent

between 5.3 and 5.9% for the last 5 fiscal years. This along with an overall lowering of

industry rates when information is available can be seen in the pension discount rates

chart above. “These lowering rates in the industry are viewed as a conservative

accounting measure by respective firms because these lower discount rates will in effect

cause pension costs to rise (http://beginnersinvest.about.com).”

Quality of Disclosure:

A firm’s management can make an outside analyst’s job more or less difficult

when deciding to put together the financials. Managers have a certain amount of

wiggle room in disclosing accounting policies. This makes management’s quality of

disclosure in the financial statements an important part of the firm’s accounting policies.

Qualitative Analysis of Disclosure:

The quality of disclosure provided by the company should be adequate in giving

a realistic view of the current business position without giving away information that

could deplete a firm’s competitive advantage within its industry. The quality of the

disclosed information is crucial for outside analysts to maintain their confidence in the

43

credibility of the company’s management. Misrepresented information, if discovered,

can do unknown amounts of harm to the company in all undertaken future business

endeavors. Heinz makes an effort to disclose and explain much of the information in its

annual reports. Some things like the goodwill mentioned above, however, are not

explained in a concise way that would give the average person a true understanding of

Heinz’s financial reality.

Post-Retirement Benefits:

Heinz does a fairly good job of informing investors about the affairs of both

existing and upcoming product lines and how these will directly affect the financials.