Embed Size (px)

Citation preview

rbs.com/ukautopilotindex

Business areaEquity Structured Retail

RBS Emerging Markets

(BRIC) Deposit Growth Plan 4

Contents

Key dates 2

Important terms 3

Key Features of the RBS Emerging Markets (BRIC) Deposit Growth Plan 4 5

Is the Plan right for me? 6

How is the return calculated? 7

RBS VC BRIC Index desciption 8

Considerations when placing a deposit linked to the RBS VC BRIC Index 10

What are the risks? 11

Questions 12

Contacts 17

Terms and Conditions 19

2

Key dates

Plan available for sale 5 March 2012 to 4 May 2012

ISA transfer deadline 20 April 2012

2011/2012 ISA deadline 5 April 2012

2012/2013 ISA deadline 4 May 2012

Direct Account deadline 4 May 2012

SIPP/SSAS deadline 4 May 2012

Initial Valuation Date 1 June 2012

Start Date 12 June 2012

Final Valuation Date 1 December 2017

Maturity Date 8 December 2017

3

Account – The deposit account opened by RBS plc for your Deposit. An Account may be either a Direct Account or an ISA Account.

Application Form – The application form to invest in the Plan, either via an ISA or Direct Account, and can include a Transfer Application Form.

Business Day – Any day (other than Saturday or Sunday) on which banks are open for business in the UK.

Cash ISA – An Account established in accordance with the ISA Regulations and consists of a cash component only.

Client Money – Money held in accordance with the provisions of the FSA’s Client Assets Sourcebook relating to client money.

Deposit – The initial deposit or the amount transferred from another Cash ISA deposited in the Account.

Deposit Taker – In this case RBS plc is the licensed deposit taker.

Direct Account – Any part of the Deposit that is not part of an ISA.

Final Index Level – The average of the closing levels of the Index on the 1st of each month in the last year of the Plan (13 monthly observations in total), or the next Business Day when not a Business Day.

Final Valuation Date – The date when we calculate the Final Index Level and the Maturity Value.

FSA – The Financial Services Authority, or any successor organisation.

FSCS – The Financial Services Compensation Scheme.

Index - The RBS VC BRIC Index.

Initial Index Level - The closing level of the Index on the Initial Valuation Date.

Initial Valuation Date - The date when we calculate the Initial Index Level.

ISA – An Individual Savings Account.

ISA Account – An Account opened by RBS plc in accordance with the ISA Regulations.

ISA Manager – The person who is approved to administer an ISA, and in respect of an ISA related to the Plan, means The Royal Bank of Scotland plc.

ISA Regulations – The Individual Savings Account Regulations 1998, as amended or replaced from time to time.

Maturity Date – The date on which your Deposit and any additional return due to you is paid into a Client Money account, pending your further instructions.

Maturity Value – The final value of the Deposit (together with any interest), calculated as set out in the Plan brochure.

Plan – RBS Emerging Markets (BRIC) Deposit Growth Plan 4, comprising the deposits placed through your ISA and/or your Direct Account, as specified in your Application Form(s).

Plan Manager – The company which is responsible for the administration of the Plan, which in this case is The Royal Bank of Scotland plc.

Start Date – The date on which the Deposit is placed with RBS plc.

Transfer Application Form – An application form to transfer your investment in an existing ISA to an ISA Account under the Plan.

Valuation Date – The two days per month when you can withdraw money from the Plan and which will be the 8th and the 21st of each month (or the next Business Day when not a Business Day).

We, us, our and RBS plc – The Royal Bank of Scotland plc. We are a member of The Royal Bank of Scotland Group plc (the ‘RBS Group’). For information about our group of companies, please visit www.rbs.com and click on “About Us”.

Important termsHere is a short description of some of the important terms used in this Plan brochure. See the Terms and Conditions for the full definition of all terms used.

What are indices?Indices are tools for measuring the performance of a collection of financial assets. An index may, for example, be composed of shares in companies from a specific industry sector or a particular country or it may contain a range of commodities such as oil, gold or wheat. An index is therefore often useful as a benchmark which can be used to represent the performance of a particular market sector.

What are emerging markets?Emerging markets are those countries that are typically experiencing rapid growth in their social, political and economic development. These markets are generally compared to the developed markets, such as the UK and the US, which typically have more mature, well developed economies.

What are the BRIC countries?The term “BRIC” is an acronym that stands for Brazil, Russia, India and China. These four countries represent the largest economies in the emerging markets.

What is market capitalisation?Market capitalisation is a measure of the size of a company. It is calculated by multiplying the number of shares in a company by the current share price.

4

The RBS Emerging Markets (BRIC) Deposit Growth Plan 4 is only available via your financial adviser.

Before you invest in the Plan you should ensure that you read and understand this brochure, including the Terms and Conditions.

You can only invest in this Plan if a financial adviser has confirmed it is suitable for you.

Official Index nameThe official name of the Index is the RBS VC BRIC Index (EUR) ER 16%.

Key Features of the RBS Emerging Markets (BRIC) Deposit Growth Plan 4The RBS Emerging Markets (BRIC) Deposit Growth Plan 4 (the ‘Plan’) is a five and a half year deposit where the return is dependent on the performance of the RBS VC BRIC Index (the ‘Index’).

5

Please see the fold out pages 3 and 4 for useful explanations of the important terms used in this brochure.

The PlanThe Plan is designed to repay your original Deposit in full at maturity plus a return equal to any rise in the Index after averaging, as explained on page 7.

When you invest in the Plan, your money will be placed on deposit with The Royal Bank of Scotland plc (‘RBS plc’). This means that, although the Plan is designed to repay your Deposit at maturity, this is dependent on the ability of RBS plc to pay what it owes you. Therefore, if RBS plc were to default or go bankrupt you could lose some or all of your money. If that occurs you may be entitled to compensation from the Financial Services Compensation Scheme (`FSCS’). See page 16 for further information.

The Financial Services Authority is the independent financial services regulator. It requires us, The Royal Bank of Scotland plc, to give you this important information to help you to decide whether the RBS Emerging Markets (BRIC) Deposit Growth Plan 4 is right for you. You should read this document carefully so that you understand what you are buying, and then keep it safe for future reference.

The RBS VC BRIC IndexThe RBS VC BRIC Index is designed to provide exposure to the performance of the shares of some of the largest companies in four of the fastest growing emerging market economies: Brazil, Russia, India and China (‘BRIC’). As the value of the shares of these companies rise or fall, so too should the value of the Index.

More detailed information on the Index, including its additional features, is provided later in this brochure on pages 8 and 9.

6

Is the Plan right for me?

The points below highlight some of the factors you should consider with your financial adviser when deciding whether to invest in the Plan.

The Plan may be right for you if: The Plan may not be right for you if:

You have a minimum £5,000 to invest. You may need access to your money in the next five and a half years.

You have enough money to cover any emergencies and are happy to keep your money invested for five and a half years.

You do not have any funds set aside for an emergency.

You want to know that your original Deposit will be repaid to you at the end of five and a half years (subject to the risk that RBS plc defaults or goes bankrupt and is unable to pay what it owes you).

You are looking for a regular income or dividends for your investment.

You accept the risk that you may not receive any return on your deposit.

You definitely want to receive a return on your deposit.

You are happy for your money to be deposited with RBS plc for five and a half years.

You are not willing to take the risk that RBS plc may default or go bankrupt during the life of the Plan.

It suits you that any returns on this deposit which are placed outside an ISA may be subject to income tax at your marginal rate.

You want to add to your deposit on a regular basis.

You want the opportunity to make a tax efficient return by investing in a Cash ISA.

You are not sure how the Plan works or have not understood this brochure.

You would like a deposit linked to the RBS VC BRIC Index. You do not want a deposit linked to the RBS VC BRIC Index.

7

On the Final Valuation Date we will calculate whether the Index has risen and whether any return is due on your original Deposit.

To do this we will compare the Final Index Level with the Initial Index Level. If the Final Index Level is greater than the Initial Index Level, you will receive a return at maturity that is equal to the percentage by which the Final Index Level is greater than the Initial Index Level. If the Final Index Level is equal to or less than the Initial Index Level, you will not receive a return at maturity. You will receive only your original Deposit.

Initial Index Level This is the closing level of the RBS VC BRIC Index on the Initial Valuation Date.

Final Index LevelThis is calculated as the average of the closing levels of the Index on the 1st of each month over the last year of the Plan (13 monthly observations), or the next Business Day when not a Business Day. To calculate the average, we will add the 13 monthly Index levels and divide that result by 13.

AveragingThe process of averaging may benefit the performance of the Plan if the Index falls over the averaging period. However, if the opposite occurs, this will constrain the Plan’s performance when compared to a calculation method which does not use averaging.

Examples of returnBelow is a table which illustrates some possible outcomes at maturity. Any return is dependent on the performance of the Index and these figures are given as examples only, in order to illustrate how the Plan works.

Original Deposit

Change in the RBS VC BRIC Index (comparing the Final

Index Level against the Initial Index Level)

Total amount received back (including your original

Deposit) at maturity (gross)

£ 10,000 +50% £ 15,000£ 10,000 +10% £ 11,000£ 10,000 0% £ 10,000£ 10,000 -10% £ 10,000£ 10,000 -50% £ 10,000

The returns stated are gross of any tax. It is expected that returns outside of an ISA may be subject to income tax. See ‘Types of investment’ on page 12.

How is the return calculated?

8

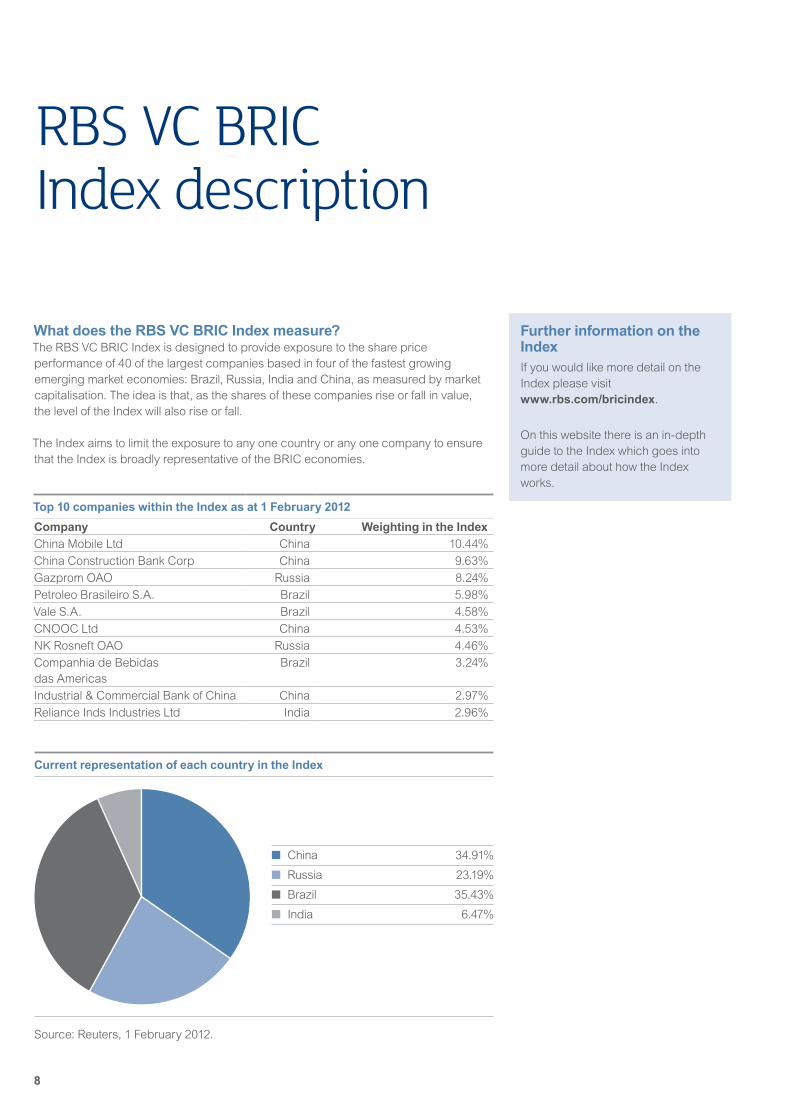

What does the RBS VC BRIC Index measure?The RBS VC BRIC Index is designed to provide exposure to the share price performance of 40 of the largest companies based in four of the fastest growing emerging market economies: Brazil, Russia, India and China, as measured by market capitalisation. The idea is that, as the shares of these companies rise or fall in value, the level of the Index will also rise or fall.

The Index aims to limit the exposure to any one country or any one company to ensure that the Index is broadly representative of the BRIC economies.

RBS VC BRIC Index description

Further information on the IndexIf you would like more detail on the Index please visit www.rbs.com/bricindex.

On this website there is an in-depth guide to the Index which goes into more detail about how the Index works.

Top 10 companies within the Index as at 1 February 2012Company Country Weighting in the IndexChina Mobile Ltd China 10.44%China Construction Bank Corp China 9.63%Gazprom OAO Russia 8.24%Petroleo Brasileiro S.A. Brazil 5.98%Vale S.A. Brazil 4.58%CNOOC Ltd China 4.53%NK Rosneft OAO Russia 4.46%Companhia de Bebidas das Americas

Brazil 3.24%

Industrial & Commercial Bank of China China 2.97%Reliance Inds Industries Ltd India 2.96%

Current representation of each country in the Index

Source: Reuters, 1 February 2012.

n China 34.91%

n Russia 23.19%

n Brazil 35.43%

n India 6.47%

9

How does the Index aim to limit the impact of volatile share price movements?Volatility Control Overlay On a short term basis, markets can behave unexpectedly and this is particularly true of emerging market shares which can experience large movements in their price level.

Volatility is one measure of these price movements, or of the amount by which the price level of a financial asset moves from its average price level over a set period of time.

In order to potentially limit the impact of this volatility, an automatic feature called a Volatility Control Overlay is applied. This will cause the Index to have increased exposure to the underlying company shares during periods of low volatility but will proportionally reduce exposure as volatility increases. The exposure to the underlying company shares is adjusted daily and can vary from 0% to 100%.

If the underlying company shares rise in a volatile manner then the Volatility Control Overlay may limit the effect of this rise.

Circuit BreakerBecause volatility in emerging market shares can be significantly greater than the volatility in developed market shares, the RBS VC BRIC Index applies a second feature called a Circuit Breaker. The Circuit Breaker aims to protect the level of the Index from crashes in the underlying company shares.

The Circuit Breaker aims to completely remove exposure to the underlying company shares when there is a sudden spike in volatility combined with a downward movement in the shares. If the Circuit Breaker is triggered, the exposure to the underlying company shares will be maintained at 0% for five days.

The performance graph on the next page illustrates how these two automatic features impact the performance of the Index.

10

Simulated and historical performance of the Index

Source: Bloomberg, 1 February 2012.

Please note: past performance should not be used as an indicator of future performance.

Ind

ex le

vels

re-

bas

ed a

t 100

(as

at 1

Feb

ruar

y 20

07)

DAXGlobal BRIC TR (EUR) Index

40

60

80

100

120

140

160

180

FTSE 100 Index

01 Feb 2007 01 Feb 2008 01 Feb 2009 01 Feb 2010 01 Feb 2011 01 Feb 2012

RBS VC BRIC Index

This information refers to simulated past performance and actual past performance, neither of which should be used as an indicator of future performance. Simulated performance indicates how the Index would have performed if it had been active during the set period. Actual performance shows how the Index actually performed from the date it went live. The performance shown in the graph opposite is net of all costs, adjustments and fees. Actual performance of the RBS VC BRIC Index started on 9 October 2010. The Royal Bank of Scotland plc has retrospectively calculated the Index levels based on the Index rules and historical data from sources the Index sponsor deems reliable.

Considerations when investing in products linked to the RBS VC BRIC Index You are not investing directly in the underlying company shares to which the Index provides exposure and therefore you will not receive dividends.

The Index operates on the basis of pre-determined rules set by RBS plc. No assurance can be given that the strategy will be successful, generate positive returns or perform better than any benchmark or other indices.

RBS plc has discretion in making certain decisions, calculations and corrections which may apply retrospectively or from the relevant date forward, for example, following the occurrence of market disruption events or index adjustment events. The exercise of this discretion may adversely affect the performance

of the Index, though RBS plc must always act in good faith when making any decisions, calculations or corrections.

Occasions can arise where RBS plc, or any member of the RBS Group, may have some form of conflict of interest in relation to the structure and operation of the Index. RBS plc maintains a Conflicts of Interest policy as required by the Financial Services Authority to manage any such conflict.

The Index rules may be amended by RBS plc acting in a commercially reasonable manner. Any such amendment may be made without the consent of, or notice to, investors in products linked to the Index and may have an adverse effect on the level of the Index, though RBS plc must always act in good faith when making any amendments.

The Index may be postponed or terminated if the prices of the underlying company shares are not published, or where, for example, the relevant stock exchanges fail to open or suspend or stop trading.

The level of the Index may not be published or, in the event that it is not possible or practicable to continue, the Index may be terminated by RBS plc. Should the Index cease to exist, any product linked to this Index may be restructured or may terminate early. This may have a negative impact on the return on any investment in such a product.

If any of these events occur, RBS plc may, as Deposit Taker, adjust the calculation of payments or defer payments on the deposit.

11

• Because your money will be placed on deposit with RBS plc, in the unlikely event that RBS plc were to default or go bankrupt, you could lose some or all of your original Deposit and any potential interest. If this occurs you may be entitled to compensation from the FSCS. See page 16 for more information.

• Whether or not you receive any interest on your deposit is dependent on the performance of the RBS VC BRIC Index. Therefore, if the Final Index Level is less than or equal to the Initial Index Level you will only receive back your original Deposit (subject to the risk described above).

• The Index is linked to a collection of underlying company shares in the BRIC countries. Prices of these shares can move up and down very quickly and may be negatively affected by global economic, financial and political developments. In particular:

– companies in emerging markets may be subject to certain risks and special considerations not typically associated with investing in other more established economies or securities markets. Examples of these risks include greater political and economic uncertainty, different accounting and reporting standards and a higher degree of government involvement in the economy.

• We will use averaging in the final year of the Plan to calculate the Final Index Level. Averaging may benefit the performance of the Plan if the Index falls over the averaging period. However, if the opposite occurs, this will constrain the Plan’s performance when compared to a calculation method which does not use averaging.

• The Volatility Control Overlay and the Circuit Breaker may have the effect of limiting gains in the Index.

• If you decide to terminate the Plan before maturity, the amount you receive back will be dependent on the early withdrawal value of the deposit. This means that you could get back significantly less than you originally deposited.

• If the return is not equal to or above the rate of inflation over the life of the Plan, the real value of your deposit will fall, as your money will buy you less than it would have done when you deposited it.

• Tax rules may change during the life of the Plan, which may affect the tax treatment of any return you receive.

What are the risks?

12

Questions

Qualifying investorsWho can invest?You must be aged 18 or over to apply.

You must be UK resident for tax purposes.

The Plan is not available for US persons.

How much can I invest?The minimum deposit is £5,000. There is no maximum for Direct Account deposits, ISA transfers or SIPP/SSAS deposits. The total 2011/2012 Cash ISA allowance is £5,340. The total 2012/2013 Cash ISA allowance is £5,640. You can use both your 2011/2012 and 2012/2013 Cash ISA allowance for this Plan.

Charges What are the charges?All charges applicable to the Plan have already been built into the Plan structure and so have been accounted for in the returns described in this brochure. This means that, if you hold the Plan to maturity, any return will be based on the whole of your original Deposit. These charges will be no more than 5.25% of your original Deposit and they incorporate all costs including any commissions payable to your adviser.

How much will any advice cost?Out of the charges described above, we will pay a commission, of up to 3% of your original Deposit, to the adviser who arranged your investment in the Plan on your behalf. You will be given details of the amount paid to your adviser in our confirmation of your investment.

Types of investmentDirect AccountYou can place a deposit direct into the Plan as an individual or a joint account holder and also as a corporate body, a trust or a charity.

ISAIf you are ordinarily resident in the UK for tax purposes, you can invest up to a maximum of £5,340 via the Plan into a 2011/2012 Cash ISA and a maximum of £5,640 into a 2012/2013 Cash ISA. The total annual ISA allowance with all providers is £10,680 for the tax year 2011/2012. The total annual ISA allowance for the tax year 2012/2013 is £11,280. This includes any amount you may invest in a Stocks and Shares ISA during the same year. This Plan is only available as a Cash ISA. Another version of the Plan is available if you wish to invest in a Stocks and Shares ISA. You can use both your 2011/2012 and 2012/2013 tax year Cash ISA allowance for this Plan (provided you do not have any other Cash ISA for the relevant tax year).

You can transfer all or part of any existing Cash ISA above £5,000 into this Plan. If you transfer a Cash ISA you opened in this tax year then you must transfer the full amount.

Your existing provider may make a charge for transferring your ISA.

It is important that we receive your ISA transfer funds by the 16 May 2012. If we receive your ISA transfer funds after this date we will return the cheque to your original ISA Manager.

13

SIPP/SSASYou can invest pension monies via a Self Invested Personal Pension (SIPP) or Small Self Administered Scheme (SSAS). RBS plc places no limit on the maximum investment amount.

TaxHow will my investment be treated for tax purposes in the UK?Tax treatment depends on individual circumstances and may be subject to change in the future. These statements are not intended to be, nor should they be, regarded as legal or tax advice and you should consult your tax adviser to obtain advice about the particular tax treatment in relation to this Plan, particularly if you may be subject to tax in other jurisdictions.

Direct AccountIt is expected, based on our understanding of current tax regulations, that any returns from the Plan for individuals and joint account holders will be treated as interest and may be subject to income tax. Any returns from the Plan for individuals and joint account holders will be paid net of basic rate income tax as required by law. Higher rate or additional rate taxpayers will have further tax to pay. Any returns from the Plan will generally be paid gross if you place a deposit as a corporate body or charity and trusts will be paid gross or net of basic rate income tax, depending on the terms of the trust.

ISAAny returns from the Plan will be paid gross. Under current legislation, the proceeds of deposits held within an ISA are not subject to either UK income tax or UK capital gains tax, and any gains or losses on your deposit will be disregarded for the purposes of the calculation of UK taxes.

SIPP/SSASAny returns from the Plan will be paid gross.

Making an investmentHow do I apply?The Plan is only available via your financial adviser and they will explain how to apply for the Plan. Before you invest in the RBS Emerging Markets (BRIC) Deposit Growth Plan 4, it is important that you read and understand this brochure, including the Terms and Conditions. You can only invest in this Plan if your financial adviser has confirmed it is suitable for you.

What confirmation of my investment will I receive? Within five Business Days of our receipt of your money and a correctly completed Application Form, we will send you a confirmation that your application has been accepted, though such acceptance is still subject to your financial adviser having satisfied certain conditions before the Initial Valuation Date. If your financial adviser does not satisfy these conditions before the Initial Valuation Date, then we may reject your application after we have initially indicated acceptance to you. In the event of an application being rejected, we will provide notice of rejection and we will notify you and your financial adviser as soon as practicably possible and return your Deposit to you without any interest.

We will also enclose details of your right to cancel within 14 days of us accepting your application.

What happens to my money before the Start Date?We will place your money in a Client Money account with Lloyds TSB Bank plc. No interest will be paid. Where an application is made to open a 2012/2013 Cash ISA, any subscription monies for that 2012/2013 Cash ISA will be held outside the ISA until on or after 6 April 2012.

If Lloyds TSB Bank plc were to default or go bankrupt before the Start Date and you suffered a loss as a result of this, you may be eligible to claim compensation from the UK Financial Services Compensation Scheme (‘FSCS’). See ‘What are the compensation arrangements?’ on page 16.

14

What happens to my money on the Start Date? Your money will be placed on deposit with RBS plc with a fixed Maturity Date. The deposit has been structured to give the Plan return described earlier in this brochure. The return depends on the ability of RBS plc to pay what it owes you at maturity.

Credit ratingsWhat are credit ratings?Credit ratings can be a useful way to compare the credit risk associated with different product providers and related investments. Ratings are assigned by independent companies known as ratings agencies and they are reviewed regularly and are subject to change if the company’s circumstances change significantly and the agency considers it necessary.

Fitch’s ratings range from AAA (Most Secure/Best) to D (Most Risky/Worst), Moody’s ratings of these companies range from Aaa (Most Secure/Best) to C (Most Risky/Worst) and Standard & Poor’s ratings range from AAA (Most Secure/Best) to D (Most Risky/Worst).

A rating outlook indicates the likely rating trend over a one to two-year period. It reflects financial or other trends that have not yet reached the level that would trigger a rating change, but which may do so if such trends continue. A stable outlook means that the rating is unlikely to change in the short term. A negative outlook means that the rating may be lowered in the near future.

The credit rating is not investment advice and should not be seen as a recommendation to purchase, sell, or hold a financial obligation from a particular financial institution. Credit ratings are simply one factor that you can look at when making a decision on whether to make a particular investment. A rating is not a guarantee that a particular institution cannot fail.

What are the current RBS plc credit ratings? On 1 February 2012 RBS plc is rated ‘A’, with a stable outlook, by Fitch, ‘A2’, with a negative outlook, by Moody’s and ‘A’, with a stable outlook, by Standard & Poor’s. For the latest information on the RBS plc credit rating please visit: www.investors.rbs.com/credit_ratings.

After making an investment How will you keep me up-to-date with my Plan?We will send a statement twice a year in April and October to the address you have given us.

Information on the performance of the Index is available on our website at: www.rbs.com/bricindex

Should you wish to find out any other information regarding your Plan, please contact your financial adviser or contact us, see ‘Contacts’ on page 17.

Can I change my mind before the Start Date?You can change your mind within 14 days of the day you receive confirmation that your application has been accepted. To do this you must complete and return the cancellation form which is enclosed with your confirmation.

If you do choose to cancel your investment in the Plan, simply fill out the cancellation form and return it to us at the address under ‘Contacts’.

If you cancel the Plan and we receive your cancellation form before the Start Date we will return your original Deposit without any interest. If we receive your cancellation form on or after the Start Date we will return the early withdrawal value of the Plan, which may be significantly less than your original Deposit, as described more fully in ‘Can I withdraw my money before maturity?’.

If you cancel an ISA or ISA transfer there is a risk that the ISA status of your deposit will be lost. In our cancellation form we will ask you what you would like us to do with the funds.

If you do not cancel your money will remain invested in the Plan.

The credit rating is not investment advice and should

not be seen as a recommendation to purchase,

sell, or hold a financial obligation from a particular

financial institution, they are simply one factor that you can

look at when making a decision on whether to make a particular investment. A rating

is not a guarantee that a particular institution cannot fail.

15

Can I withdraw my money before maturity?The Plan is designed to be held for the full five and a half year period until the Maturity Date, however you can withdraw all or part of your deposit early if you need to. There will be two Valuation Dates each month, on the 8th and 21st, when you can withdraw money from the Plan. In order to meet these dates we must receive your request by 12 noon on the Business Day immediately before the Valuation Date.

Although you will not be charged any fee by RBS plc for withdrawing your investment before the Maturity Date, if you do withdraw early, you should be aware that we shall need to terminate contracts that we have entered into. Early termination of these contracts, which we put in place for each investment, will mean that, if you withdraw all or part of your investment before the Maturity Date, it is likely you will receive less than the value at maturity and you may well receive less than your original Deposit. You should be aware before making a withdrawal request that this shortfall could be significant.

The amount you receive on any withdrawal (all or part) will be based on the early withdrawal value of the Plan on the Valuation Date we process your request and not on the early withdrawal value of the Plan on the day we receive your withdrawal request.RBS plc must always act in good faith when calculating the early withdrawal value of the Plan and will take into account relevant factors including, amongst others, how long there is to the Maturity Date, the market conditions prevailing on the relevant Valuation Date, for example, what the current level of the Index is and what current interest rates are, and the costs we incur in terminating the contracts.

You can withdraw amounts equal to £500 or more but, if you do want to keep the Plan open, you must leave at least £500 deposited in it. If you want to transfer your ISA to another provider, the full ISA amount must be transferred, but such amount will be subject to the adjustments described above. Partial transfers are not permitted.

What happens if I die before the Plan matures?If you die before the Maturity Date, the Plan will become part of your estate. Your personal representatives will need to contact us in order to let us know how they wish to proceed with the Plan as part of probate/administration.

If you made a Direct Account deposit, your Plan will remain open until we have received instruction from your personal representatives.

If you made an ISA deposit, your ISA will lose its ISA tax status and will be closed automatically. The Plan will be continued as a Direct Account deposit until we receive instructions from your personal representatives.

Your representatives will have two options:• Close the Plan with the proceeds paid to your representatives. The value they receive

will be subject to the current early withdrawal value of the deposit so they may receive back less than you originally deposited.

• Keep the Plan open and transfer it to a named beneficiary(ies) to continue the deposit until maturity. If your representatives choose this option, the beneficiary(ies) must read and agree to the Terms and Conditions as detailed in this brochure.

What happens at Maturity?On the Final Valuation Date we will calculate the total return due to you. Prior to the Maturity Date, we will write and inform you of the options that are available to you. After we receive your instructions, we will process them and endeavour to meet your request within 5 Business Days of the Maturity Date or receipt of your instructions if later.

Until we receive your instructions, we will hold your money in a Client Money account with Lloyds TSB Bank plc. No interest will be paid.

If we do not receive your instructions within a reasonable time we may return your money to your nominated bank or building society account.

16

Further questionsDo you provide additional support to advisers?We may provide advisers with support to help improve their service to you. This could include training, seminars and/or marketing materials. For specific details on any support provided, please contact your adviser or us.

What are the compensation arrangements?The compensation arrangements will differ depending on which of the two time frames headed in the table below applies. Please be sure to read both sections carefully.

Before the Start Date and after the Maturity Date

From the Start Date to the Maturity Date

During these periods your money will be held in a Client Money account at Lloyds TSB Bank plc. If during these times, Lloyds TSB Bank plc defaults or becomes bankrupt and you suffered a loss as a result of this, you may be eligible to claim compensation from the Financial Services Compensation Scheme (the ‘FSCS’), up to £85,000.

In the event that RBS plc itself defaults or becomes bankrupt during these periods your money will be returned to you as it is being held as protected Client Money segregated from RBS plc assets.

On and after the Start Date and for the duration of the five and a half year period until the Maturity Date, your money will be held on deposit with RBS plc. If RBS plc defaults or becomes bankrupt during this period you may be eligible to claim compensation from the FSCS, up to £85,000.

The Financial Services Compensation Scheme The FSCS can pay compensation to depositors if a bank or building society is unable to meet its financial obligations. Most depositors, including most individuals and small businesses are covered by the scheme. In respect of deposits, an eligible depositor is entitled to claim up to £85,000. For joint accounts each account holder is treated as having a claim in respect of their share so, for a joint account held by two eligible depositors, the maximum amount that could be claimed would be £85,000 each. The £85,000 limit relates to the combined amount of all the eligible depositor’s accounts with a bank or building society, including their share of any joint account, and not to each separate account.

You can find more information about the FSCS (including eligibility to claim) on their website, www.fscs.org.uk or by calling 0800 678 1100.

What if I want to complain?If your complaint relates to the advice you received when purchasing the Plan, please contact your financial adviser. If you have a complaint about any aspect of the service we have provided, please contact us at: The Royal Bank of Scotland plc, BNY Mellon House, Ingrave Road, Brentwood, Essex CM15 8TG, or call us on 0800 032 4902.

Copies of our complaint handling procedure are available, from the above contact details, on request.

If you are unhappy with the way we have handled your complaint you can contact the Financial Ombudsman Service who may take the matter up on your behalf: Financial Ombudsman Service, South Quay Plaza, 183 Marsh Wall, London E14 9SR.

17

The Royal Bank of Scotland plcIf you have any queries please contact us at:

The Royal Bank of Scotland plc BNY Mellon House Ingrave Road Brentwood Essex CM15 8TG Tel: 0800 032 4902

Lines are open between 9am and 5pm Monday to Friday. Calls may be recorded for training and monitoring purposes.

RegulatorRBS plc is authorised and regulated by The Financial Services Authority. Its address is:

The Financial Services Authority 25 The North Colonnade Canary Wharf London E14 5HS

We are entered on their register under number 121882. You can check this at: www.fsa.gov.uk/register or by contacting them on 0845 606 1234.

About The Royal Bank of Scotland plcThe Royal Bank of Scotland plc is a subsidiary of The Royal Bank of Scotland Group plc.

The Royal Bank of Scotland Group plc is one of the world’s foremost financial services companies. We work closely with our personal, commercial and large corporate and institutional customers to address their financial needs. Internationally, the RBS Group’s brands include The Royal Bank of Scotland and RBS Coutts and NatWest in the UK, Citizens and Charter One in the United States and other well known financial services providers.

This item can be provided in Braille or large print, please call us on 0800 032 4902 to request this. For general queries, text phone users can contact us (using the Typetalk service) by prefixing our number with 18001.

Contacts

18

The RBS VC BRIC Index is one of an exclusive range of indices

that are created, owned and maintained by RBS plc

18

Definitions ‘Account’ The deposit account opened by RBS plc for your Deposit. An Account may be either a Direct Account or an ISA Account.

‘Application Form’ The application form to invest in the Plan, either via an ISA or Direct Account, and can include a Transfer Application Form.

‘Business Day’ Any day (other than Saturday or Sunday) on which banks are open for business in the UK.

‘Cash ISA’ An Account established in accordance with the ISA Regulations and consists of a cash component only.

‘Client Money’ Money held in accordance with the provisions of the FSA’s Client Assets Sourcebook relating to client money.

‘Deposit’ The initial deposit or the amount transferred from another Cash ISA deposited in the Account.

‘Deposit Taker’ In this case RBS plc is the licensed deposit taker.

‘Direct Account’ Any part of the Deposit that is not part of an ISA.

‘Final Index Level’ The average of the closing levels of the Index on the 1st of each month from, and including, 1 December 2016 to, and including, 1 December 2017 (13 monthly observations in total), or the next Business Day when not a Business Day, subject to adjustment in accordance with the provisions of the deposit programme as set out on page 10 of this Plan brochure.

‘Final Valuation Date’ The date when we calculate the Final Index Level and the Maturity Value, which will be 1 December 2017, subject to adjustment in accordance with the provisions of the deposit programme as set out on page 10 of this Plan brochure.

‘FSA’ The Financial Services Authority, or any successor organisation.

‘FSA Rules’ The FSA’s Handbook of Rules and Guidance, as amended from time to time.

‘FSCS’ The Financial Services Compensation Scheme, or any successor organisation.

‘HMRC’ Her Majesty’s Revenue & Customs.

‘Index’ The RBS VC BRIC Index.

‘Initial Index Level’ The closing level of the Index on the Initial Valuation Date.

‘Initial Valuation Date’ The date when we calculate the Initial Index Level, which will be 1 June 2012, subject to adjustment in accordance with the provisions of the deposit programme as set out on page 10 of this Plan brochure.

‘ISA’ An Individual Savings Account, which is a scheme of investment managed in accordance with the ISA Regulations by the ISA Manager under terms agreed between the ISA Manager and the investor.

‘ISA Account’ An Account opened by RBS plc in accordance with the ISA Regulations.

‘ISA Investments’ Any assets, including the Deposit, within the ISA at any time.

‘ISA Manager’ The person who is approved to administer an ISA, and in respect of an ISA related to the Plan, means The Royal Bank of Scotland plc.

‘ISA Regulations’ The Individual Savings Account Regulations 1998, as amended or replaced from time to time.

‘Maturity Date’ The date on which your original Deposit and any additional return due to you is paid into a Client Money account, pending your further instructions, and which will be 8 December 2017, subject to adjustment in accordance with the provisions of the deposit programme as set out on page 10 of this Plan brochure.

‘Maturity Value’ The final value of the Deposit (together with any interest), calculated as set out in the Plan brochure.

‘Plan’ The RBS Emerging Markets (BRIC) Deposit Growth Plan 4, comprising the deposits placed through your ISA and/or your Direct Account, as specified in your Application Form(s).

‘Plan Manager’ The company which is responsible for the administration of the Plan, which in this case is The Royal Bank of Scotland plc.

‘Start Date’ The date on which the Deposit is placed with RBS plc, which will be 12 June 2012.

‘Transfer Application Form’ An application form to transfer your investment in an existing ISA to an ISA Account under the Plan.

‘Valuation Date’ The two days per month when you can withdraw money from the Plan and which will be the 8th and the 21st of each month (or the next Business Day when not a Business Day).

‘We’, ‘us’, ‘our’ and ‘RBS plc’ The Royal Bank of Scotland plc. We are a member of The Royal Bank of Scotland Group plc (the ‘RBS Group’). For information about our group of companies, please visit www.rbs.com and click on “About Us”.

Terms and ConditionsPlease read these Terms and Conditions carefully and keep them for future reference. They provide you with important information about the Plan and together with the Plan brochure and the deposit programme, they form the agreement between you and us. When you sign the Application Form you are agreeing to these Terms and Conditions. The law which we take as the basis for establishing relations with you prior to the conclusion of the agreement is also the law of England. If you open a Plan via a wrapper platform (where permitted by RBS plc) then certain references to ‘you’ in these Terms and Conditions, will be references to, ‘you or the platform as your nominated agent’, where applicable.

19

1. Application1.1 The Royal Bank of Scotland plc is authorised and regulated by

the FSA. Under these Terms and Conditions, we act as both Plan Manager (which means that we are responsible for the administration of your Plan) and as ISA Manager (which means that, where you invest via an ISA, we administer your ISA).

1.2 You may open a Plan on the terms of the Plan brochure, the deposit programme and these Terms and Conditions. To open a Plan, you should complete the relevant Application Form (either ISA or (non-ISA) Direct Account) and send it to the address on the relevant Application Form.

1.3 Upon receipt of a duly completed Application Form and cheque (where required), the Plan Manager may accept your application subject to these Terms and Conditions, and subject to your financial adviser having satisfied various procedural requirements relating to the Plan. Completed Application Forms and payments must be received by the deadlines specified in the Plan brochure. We reserve the right to reject an application for any reason, including, specifically, a failure by your financial adviser to meet our requirements before the Initial Valuation Date. Since this failure may take place after the deadlines relating to the receipt of your completed Application Form and payments specified in the Plan brochure, we will provide notice of rejection after such deadlines and therefore after we have initially indicated acceptance to you. In the event of an application being rejected, will notify you and your financial adviser as soon as practicably possible and return your Deposit to you without any interest.

1.4 Within 5 Business Days of accepting your application, we will confirm your application to open a Plan and confirm the date on which the Deposit was made.

1.5 Money held by RBS plc prior to the Start Date AND then, between either early termination or final redemption at the Maturity Date and final settlement with you, will be held by RBS plc as Client Money in an account with a third party bank appointed by RBS plc for these purposes. No interest will be payable on such Client Money balances held by the third party bank. The third party bank for the Plan will be Lloyds TSB Bank plc.

2. ISA Accounts2.1 You must subscribe to your ISA with either your own money or by

the transfer of the proceeds of an existing ISA already held by you. Where an application is made to open a 2012/2013 ISA Account, any subscription monies for that 2012/2013 ISA Account will not be held within the ISA until on or after 6 April 2012. Transfers of existing ISAs will normally be arranged by us with the existing Cash ISA manager(s) following our receipt of a Transfer Application Form from you, at which point we will contact your existing ISA manager(s) to arrange the transfer for you. Once the proceeds from the existing ISA have been transferred, your ISA will be subject to these Terms and Conditions.

2.2 To effect an ISA transfer you should complete a Transfer Application Form and send it to the address on the form. A cancellation notice will be sent to you upon our acceptance of your Transfer Application Form.

2.3 You may instruct RBS plc to transfer to another approved ISA Manager the whole of your ISA, subject to and in accordance with the ISA Regulations. Transfers will be processed by RBS plc in accordance with clause 12 within 5 Business Days of the relevant Valuation Date so long as valid instructions have been received by 12 noon on the Business Day prior to that Valuation Date.

2.4 You will immediately inform us in writing if you cease to be a qualifying individual for the purposes of the ISA Regulations. We will notify you if, by reason of any failure to satisfy the provisions of the ISA Regulations, an ISA has, or will, become void. Where an ISA becomes void for any reason, in the absence of instructions otherwise from you, we will continue to hold the Deposit, but in a Direct Account and you will lose any favourable tax treatment applicable.

2.5 We shall not accept any further amounts into an ISA if the ISA Regulations no longer give you the right to invest in that ISA.

2.6 Any ISA Investments shall be in, and must remain in, your beneficial ownership and must not be used as security for a loan.

3. Taxation3.1 Under current legislation, a Deposit held within an ISA is not

subject to UK Income Tax and any income on your Deposit will be disregarded for the purposes of the calculation of UK taxes.

3.2 Where, however, your Deposit is held through the Direct Account (and therefore not subject to the ISA tax shelter) you may be subject, depending on your personal circumstances, to UK tax on any income received. These statements are based on current legislation, regulations and practice, all of which may change.

3.3 Where any deduction or withholding for or on account of tax is required by law (a “Tax Deduction”) from any amount otherwise payable, we shall be entitled to make such Tax Deduction and shall not be required to make any increased payment to compensate you for such Tax Deduction.

3.4 If you are an individual ordinarily resident in the UK, eligible to be paid interest gross of tax, and wish to be paid interest gross of tax on a Direct Account, you can download an R85 form from HM Revenue & Custom’s website at www.hmrc.gov.uk and send us your completed R85 form at: RBS Administration, BNY Mellon House, Ingrave Road, Brentwood, Essex CM15 8TG, together with a covering letter stating your customer reference.

20

4. Death In the event of your death, your ISA will lose its ISA status

immediately, and any income after that date will not benefit from the ISA tax shelter. The Deposit forms part of your estate for Inheritance Tax purposes and, accordingly, we shall act on the instructions of your personal representatives.

Your personal representatives can close the Plan or, subject to these Terms and Conditions, transfer your deposit to your beneficiary(ies).

5. Maturity Under the terms of the Plan, the final value of the Plan will be

calculated on the Final Valuation Date. Prior to the Maturity Date, we will contact you to inform you of your options at maturity and any action required by you. Upon receipt of your valid instructions, we will process them and endeavour to meet your request within 5 Business Days of the Maturity Date or receipt of your instructions, if later. Payment(s) will be made in accordance with clause 12 and subject to any requirements under clause 17. Any sums owing to you, that are not immediately paid, will be held by us as Client Money. Interest will not be paid on such sums. We may return the funds to you if we don’t receive your instructions.

6. Conflicts of Interest6.1 RBS plc is a multi-service financial institution, and occasions

can arise where we, one of our clients or another member of the RBS Group, may have some form of conflict of interest in relation to the business which is being transacted for you. RBS plc maintains a Conflicts of Interest policy as required by the FSA Rules to manage any such conflict to ensure that customers are not affected by any conflict. In the event that it is not possible to properly manage any conflict, we shall inform you as soon as possible and obtain your instructions.

6.2 For the avoidance of doubt, nothing in this clause will restrict us from providing services to other customers.

7. Compensation7.1 RBS plc is a member of the FSCS, which means that you may

be entitled to compensation in the event of our default. Further information is available on request, but in broad terms, your rights are as follows:

(a) Money held by us as Client Money will be returned to you and will not be affected by our default.

(b) The third party bank that will hold Client Money is also a member of the FSCS; on its default, if you are an eligible claimant under the compensation scheme rules, you may be entitled to compensation, currently of up to £85,000.

(c) If you are an eligible claimant under the compensation scheme rules, you may be entitled to compensation of up to £85,000 on our default when we hold the deposit.

7.2 Deposits with RBS plc, Direct Line, the One Account, Child & Co, Drummonds and Holts are all covered by a single FSA authorisation. This means the total deposits with these firms will count to one compensation limit. For further information on the conditions governing compensation and details on how to apply, please refer to the FSCS at www.fscs.org.uk.

8. Complaints8.1 If you wish to complain about the Plan or the service we provide

to you as the Plan Manager or as the ISA Manager, we have procedures designed to resolve your complaint effectively. Initially you should write to: RBS Administration, BNY Mellon House, Ingrave Road, Brentwood, Essex CM15 8TG.

8.2 You may have a right to complain to the Financial Ombudsman Service if you are not satisfied with our resolution of your complaint. Further details are available on request.

9. Cancellation Rights 9.1 RBS plc will give you the right to cancel your Plan within 14 days

of our acceptance of your Application Form in accordance with the requirements of the FSA Rules. You will also be informed of your right to cancel in the information that we send you on receipt of your Application Form. Alternatively you can write to us at RBS Administration, BNY Mellon House, Ingrave Road, Brentwood, Essex CM15 8TG. If you do so, please provide your name, address and the reference number with clear instructions to cancel your investment.

9.2 If you exercise your right to cancel (or if your application is rejected) within 14 days and we receive such cancellation notice before the Start Date, we will return your cash subscriptions without any interest.

Valid cancellation notices received five calendar days or less before the Start Date will be processed at the next available Valuation Date after the Start Date (see clause 11.7), and you will receive your cash subscriptions, without any interest, after such Valuation Date.

9.3 If we receive your cancellation notice on or after the Start Date, we will return to you, without any interest, your cash subscriptions, but the amount repaid to you may be subject to a market value adjustment.

9.4 All cancellations will require full clearance of your original subscription (minimum 15 Business Days) and any requirements under clause 17 to be satisfied before we can issue payment to you. Interest will not be payable on such sums.

9.5 When cancelling an ISA investment, including ISA transfers, you may lose any favourable tax treatment applicable.

9.6 Where you do not exercise your cancellation rights, the Plan will continue in line with the Terms and Conditions.

21

10. Record Keeping10.1 At all times you or your nominated agent may request a copy of

entries in our records relating to your investments in accordance with the FSA Rules and the Data Protection Act 1998, as may be amended from time to time.

10.2 We will prepare a statement twice a year to report on the value of your Deposit held through your ISA and/or your Direct Account. These will be prepared as at the 31 March and 30 September (or the next Business Day when not a Business Day) and then issued within 25 Business Days of being prepared.

10.3 We may employ agents in connection with the services we are to provide and may delegate any or all of our powers or duties to any delegate(s) of its choice in accordance with the ISA Regulations. We will satisfy ourselves that any person or entity to whom any functions or responsibilities are delegated under these Terms and Conditions is competent to carry out those functions and responsibilities. We shall not be liable for the fraud, negligence or wilful default of any such agent or delegate. This shall not exclude or restrict any liability towards you to which, by virtue of the ISA Regulations, the Financial Services and Markets Act 2000, or the FSA Rules, we may be subject to.

11. Termination/early withdrawal11.1 The Plan or any Account comprised in it may be terminated by

us by giving written notice to you if in our reasonable opinion it is impossible to administer the Plan or that account in accordance with the ISA Regulations, the FSA Rules or under general law or if you are in material breach of the ISA Regulations or these Terms and Conditions, which either cannot be rectified or has not been rectified following requests by us for you to do so. Where it is reasonably practical, we shall give you advance notice of such termination, but we may, in certain circumstances, be obliged to terminate immediately.

11.2 The ISA will terminate automatically with immediate effect if it becomes void under the ISA Regulations. We will notify you in writing if the ISA becomes void outlining the options available.

11.3 We may terminate the Plan at any time for reasons beyond our reasonable control, such as the termination of the Index if the components of the Index are not published or, if applicable, a relevant stock exchange suspends or stops trading. Where this happens, and we are unable to resolve the issue causing the problem, we shall give you a reasonable period of written notice.

11.4 We may terminate the Plan at any time should you fail to pay any money due.

11.5 You may terminate the Plan or any Account comprised in it at any time by giving us written notice to that effect. At our discretion you may also choose to maintain your Plan, but withdraw a specified amount from your Deposit (e.g. if you are a nominee). However, in the case of ISA transfers to another provider, only full transfers are possible, partial transfers are not permitted. You should be aware that if you terminate the Plan before the Maturity Date you may not get back the whole amount you originally deposited.

11.6 After the Start Date we value the Plan on the 8th and 21st of each month (or the next Business Day when not a Business Day). The deadline for receipt of written instructions is 12 noon on the Business Day immediately before the specified Valuation Dates.

11.7 Terminations/early withdrawals (of all or part of the Deposit) or outward ISA transfer requests received five calendar days or less before the Start Date, or on or after the Start Date, will be carried forward to the next available Valuation Date after the Start Date (see clause 11.6). At this point RBS plc will terminate any part of the Deposit pursuant to your instructions. We wish to remind you that early termination may result in a loss of capital and, if your Plan is an ISA, it may lose its ISA status in accordance with the ISA Regulations. The amount you receive on any withdrawal (all or part) or outward ISA transfer request will be based on the early withdrawal value of the Plan on the Valuation Date we process your request and not on the early withdrawal value of the Plan on the day we receive your withdrawal request.RBS plc must always act in good faith when calculating the early withdrawal value of the Plan and will take into account relevant factors including, amongst others, how long there is to the Maturity Date, the market conditions prevailing on the relevant Valuation Date, for example, what the current level of the Index is and what current interest rates are, and the costs we incur in terminating the contracts which we put in place for each investment.

11.8 Termination of the Plan or any Account comprised in it will not affect any legal rights or obligations which may have already arisen. On termination, we will promptly account to you for the proceeds of the Deposit held through your Plans in accordance with clause 12, save that we will be entitled to retain any funds required to pay any outstanding tax or other amounts payable from the Plan.

11.9 For any termination, we will require full clearance of your original subscription (minimum 15 Business Days) and any requirements under clause 17 to be satisfied before we can issue payment to you. Interest will not be payable on such sums.

11.10 Notwithstanding any other term hereof, on any termination of an ISA or early withdrawal from an ISA, we will pay you the relevant amounts in accordance with clause 12 as soon as we are reasonably able but in any event within 30 days of receipt of a valid instruction.

22

12. Payments We may, at our discretion, send proceeds to you (e.g. upon

termination or maturity etc.) by cheque or by transferring the funds into the bank or building society account from where the initial Plan investment originated. If any payment is requested to an account other than the account from where the initial Plan investment originated, you agree to us carrying out any necessary verification checks as per clause 17 prior to us releasing payment, during which time money will be held by us as per clause 1.5.

13. Commissions and Charges13.1 All charges are taken into account when the Plan is opened and

are reflected in the terms of the Plan and in the calculated return. These charges will amount to no more than 5.25% of your original Deposit. There will be no additional charges for you to pay to RBS plc.

13.2 We do, however, pay commissions to third party distributors and advisers on the sale of the Plan. It is the responsibility of such person to inform you how much it receives from RBS plc for each sale, but it will be up to 3% of your original Deposit.

13.3 Please be aware that there may be other taxes or costs that you are liable for that are not paid via or imposed by us.

14. Variation of Terms14.1 We may vary these Terms and Conditions by giving you

reasonable written notice: (a) to comply with any changes to the ISA Regulations, other

relevant legislation, HMRC practice and the FSA Rules (or the way they are applied);

(b) to make them fairer to you or to correct a mistake (provided this correction would not adversely affect your rights); or

(c) in order to manage your Plan more effectively, or to introduce additional facilities or options within your Plan.

14.2 We will notify you of any such change as soon as is reasonably practicable after the change has been made, if you have not been given prior notice.

15. Exclusion of Liability We will exercise due care and diligence in managing your Plan,

however we will not be liable to you: (a) for any fluctuation in the value of any interest to be paid on

your Deposit, except as a result of our fraud, negligence or wilful default;

(b) if we cannot carry out our responsibilities because of circumstances beyond our reasonable control; or

(c) for the acts or omissions of any financial adviser who arranged your investment in the Plan.

16. Communications16.1 We will always write and speak to you in English.

16.2 Telephone conversations may be recorded for training and monitoring purposes and to ensure that we provide a good service.

16.3 If you contact us electronically, we may collect your electronic identifier (e.g. Internet Protocol (IP) address or telephone number) supplied by your service provider.

17. Money Laundering17.1 All transactions relating to this Plan are covered by the Proceeds

of Crime Act 2002 and the Money Laundering Regulations 2007 (as amended from time to time) and the guidance notes provided by the Joint Money Laundering Steering Group. We are responsible for compliance with these Regulations. You may be asked for proof of identity and evidence of address at any time. Our checks may include verification of bank accounts connected to any transaction. Checks may include electronic verification through a third party provider. We may also make checks of third parties in verifying identity.

17.2 If we are unable to complete the required anti-money laundering verification checks on your investment, for example, due to outstanding information and/or documentation, restrictions will apply. For example, we will be unable to accept any further monies, process transfer requests, or allow any outbound monies to be released. These restrictions may affect all parties associated with the investment until the satisfactory resolution of any outstanding checks.

18. Corporate, trustee and joint account planholders (Direct Accounts)

18.1 Corporate persons, trustees and joint account holders may make investments in the Plan subject to the following conditions.

18.2 If you are body corporate, you confirm:- (a) you are duly incorporated and validly existing in the United

Kingdom; (b) you have the necessary corporate power to make the

Deposit; (c) you have duly authorised, executed and delivered the

Application Form in respect of the Deposit; (d) this Agreement constitutes valid and legally binding

obligations, enforceable under English law; and (e) by making the investment you will not violate any of your

constitutional documents.

18.3 If you are a trustee, you confirm:- (a) you have been duly appointed as trustee of the relevant

trust; (b) you have all necessary power, authority and consents to

make the Deposit; (c) in respect of the Deposit, you will comply with all internal

management procedures of the trust and any other procedural requirement; and

(d) by making the Deposit, you will not violate the relevant constituting trust document(s).

23

18.4 If the Account is to be held by more than one persons jointly, you all confirm:-

(a) your obligations and liabilities under these Terms and Conditions are joint and several;

(b) you each have authority (as full as if you were the only person entering into these Terms and Conditions) on behalf of the others to give or receive any instructions, notice, request or acknowledgement without notice to the others, including any instruction to withdraw the Deposit;

(c) where separate instructions are given by two or more holders and they are in conflict, RBS plc is entitled to act on those instructions or delay acting on those instructions until the conflict has been resolved;

(d) any such person may give RBS plc an effective and final discharge in respect of any of its obligations under these Terms and Conditions; and

(e) on the death (or, as applicable, dissolution) of any one or more of them, the Terms and Conditions and the Plan will not terminate and RBS plc may treat the survivor(s) as the only party(ies) to these Terms and Conditions as entitled to the Plan.

18.5 RBS plc may:- (a) contact and otherwise deal only with the account holder

named first in RBS plc’s records subject to any legal requirements or unless RBS plc requests otherwise; and

(b) in RBS plc’s sole discretion require an instruction to be given by all or a number of the persons entering these Terms and Conditions before RBS plc take any action under these Terms and Conditions.

18.6 You agree to provide us with any documents we reasonably request to confirm the above, or any other information and or documentation that we need in order to complete anti money laundering verification checks.

19. Data Protection19.1 In order to perform these Terms and Conditions, to process any

Application Form you submit and to administer the Plan, we, and persons working for us, will process personal data relating to you. Without limiting these purposes, we, and persons working for us, may use and share your personal data with other members of the RBS Group or other third parties to help us and them:

(a) assess financial and insurance risks; (b) recover debt; (c) prevent and detect crime; (d) understand our customers’ requirements; and (e) develop and test products and services.

19.2 We, and those persons working for us, may also transfer your personal data to other countries, including outside the European Economic Area, on the basis that anyone to whom we pass it provides an adequate level of protection. However, such personal data may be accessed by law enforcement agencies and other authorities to prevent and detect crime and comply with legal and regulatory obligations to which members of the RBS Group or third parties acting on our behalf may be subject.

19.3 You have the right to access the personal data we hold about you and to have any inaccuracies in that data erased or corrected. In accordance with applicable data protection legislation we reserve the right to charge a small fee for such access. Any enquiries or requests should be directed to The Royal Bank of Scotland plc, BNY Mellon House, Ingrave Road, Brentwood, Essex CM15 8TG.

20. HMRC and fraud prevention agencies20.1 You authorise us to provide HMRC with all relevant particulars

of the Account, which HMRC may request at any time.

20.2 If false or inaccurate information is provided and fraud is identified or suspected, details may be passed to fraud prevention agencies. Law enforcement agencies may access and use this information. We and other organisations may also access and use this information to prevent fraud and money laundering.

21. Severability If any of these Terms and Conditions are or become invalid or

unenforceable, the remainder of these Terms and Conditions shall remain valid and binding.

22. Governing Law These Terms and Conditions shall be governed by English law

and will become effective on acceptance by us of your signed Application Form. The courts of England and Wales shall have non-exclusive jurisdiction over any disputes arising between you and us that are not resolved by other means.

24

To find out more about RBS Emerging Markets (BRIC) Deposit Growth Plan 4, or to order literature IFAs may call 0800 032 4902. Private investors should contact their IFA.

To find out more about RBS Emerging Markets (BRIC) Deposit Growth Plan 4, or to order literature IFAs may call 0800 032 4902. Private investors should contact their IFA.

This document is issued and approved by RBS plc for the purposes of Section 21 of the Financial Services and Markets Act 2000.

This document is intended for your sole use on the basis that before entering into this, or any related transaction, you will ensure that you fully understand the potential risks and return of this, and/or any related transaction and determine it is appropriate for you given your objectives, experience, financial and operational resources, and other relevant circumstances. You should consult with such advisers as you deem necessary to assist you in making these determinations. The Royal Bank of Scotland plc (“RBS plc”) will not act and has not acted as your legal, tax, accounting or investment adviser nor does it owe any fiduciary duties to you in connection with this, or any related transaction and no reliance may be placed on RBS plc for advice or recommendations of any sort.

RBS plc disclaims all liability for any use your advisers make of the contents of this document when providing advice to you. Where the document is connected to financial instruments you should be aware that such instruments can provide significant benefits but may also involve a variety of significant risks. All financial instruments involve risks which include (amongst other risks) the risk of adverse or unanticipated market, financial or political developments, risks relating to the counterparty, liquidity risk and other risks of a complex character. In the event that such risks arise, substantial costs and/or losses may be incurred and operational risks may arise in the event that appropriate internal systems and controls are not in place to manage such risks.

RBS plc and its affiliates, connected companies, employees or clients may have an interest in financial instruments of the type described in this document and/or in related financial instruments. Such interest may include dealing, trading, holding, acting as market-makers in such instruments and may include providing banking, credit and other financial services to any company or issuer of securities or financial instruments referred to herein.

RBS plc is authorised and regulated by the Financial Services Authority. The Royal Bank of Scotland plc is an authorised agent of The Royal Bank of Scotland N.V. in certain jurisdictions. © The Royal Bank of Scotland plc. All rights, save as expressly granted, are reserved. The Daisy Device logo, RBS, THE ROYAL BANK OF SCOTLAND and BUILDING TOMORROW are trade marks of The Royal Bank of Scotland Group plc. Reproduction in any form of any part of the contents of this brochure without our prior written consent is prohibited unless for personal use only. Registered address: The Royal Bank of Scotland plc, 36 St Andrew Square, Edinburgh EH2 2YB. Registered in Scotland No. 90312.