Embed Size (px)

Citation preview

Environmental Life Cycle Criteria for Making Decisions about

Green versus Toxic Propellant Selections

by Christyl C. Johnson

B.S. in Physics, May 1987

M.S. in Electrical Engineering, August 1990

A Dissertation Submitted to the Faculty of

The School of Engineering and Applied Science

of The George Washington University

in partial satisfaction of the requirements

for the degree of Doctor of Philosophy

January 31, 2012

Dissertation directed by

Michael Duffey

Associate Professor of Engineering Management and Systems Engineering

ii

The School of Engineering and Applied Science of The George Washington University

certifies that Christyl Chamblee Johnson has passed the Final Examination for the degree

of Doctor of Science as of December 9, 2011. This is the final and approved form of the

dissertation.

Environmental Life Cycle Criteria for Making Decisions about Green

Versus Toxic Propellant Selections

Christyl C. Johnson

Dissertation Research Committee:

Michael Duffey, Professor of Engineering and Applied Science, Dissertation Director

E. Lyle Murphree, Professor of Engineering Management and Systems Engineering,

Examining Committee Chair

Jonathan Deason, Professor of Engineering and Applied Science, Committee Member

Gregory Shaw, Associate Professor of Engineering Management and Systems

Engineering, Committee Member

Woodrow Whitlow, Associate Administrator, Mission Support Directorate, NASA

Headquarters, Committee Member

Michael Ryschkewitsch, NASA Chief Engineer, NASA Headquarters, Committee

Member

iii

ACKNOWLEDGEMENTS

I would first like to thank Dr. Michael Duffey for his invaluable guidance, direction, and

assistance throughout this process. Dr. Duffey, you are the best advisor that I could have

ever had for this research, and all of your efforts are much appreciated!

Next, I would like to say a heartfelt thanks to Shanessa Jackson for her many invaluable

contributions in many areas along the way. Your countless hours spent and tireless

support has meant the world to me!! Along these same lines, I must thank Dr. Michael

Griffin and Dr. Woodrow Whitlow, who have been supporting me on this research and in

my career for many years now. Thank you again for all that you have done!!

I wish to say a heartfelt thanks to my colleagues at ECAPS (Mathias Persson, Aaron

Dinardi, and Kjell Anflo), who were instrumental in providing important pieces of the

data set used in this research. I also wish to thank my colleagues at FOI in Sweden

(Helena Bergman, Niklas Wingborg, and John de Flon) for our collaborative efforts in

this area over the years. This research would not have been possible without their

contributions.

I would also like to say thank you to my wonderful team at Goddard Space Flight Center

for their support and contributions. Kris Romig, Caitlyn Bacha, Nona Cheeks, Rich

Barney, and Dennis Andruczyk. A special thanks goes to Kris Romig for his

contributions in gathering critical pieces of data for this research. From Goddard’s

iv

Wallops Flight Facility I would like to thank Jay Pittman, Joel Simpson, and Steve

Nelson for their contributions from a range and operations perspective. I would also like

to thank Kimberly Guodace and Richard Keinath for hosting my visit to Kennedy Space

Flight Center, and for providing valuable data used in this research.

I would like to say a special thank you to Jim Farrugia of the Gelman Library at George

Washington University for his enthusiastic and helpful assistance during the literature

search phase of my research. I would also like to thank Michelle Mazzuchi for all of her

help in getting all of the department requirements cleared for this dissertation.

Last, but certainly not least, I would like to thank my family and close friends for all of

their love and support throughout this process. Special thanks go to my husband, Darryl

Johnson; my son, Jerrin Johnson; my father, Sannie Chamblee; my mother, Martha

Chamblee; my brother, Tony Chamblee; my father-in-law, Howard Johnson; my mother-

in-law, Fraitus Johnson; and my close friend, Antoinette Bishop, who never let me slow

down for a minute. Having this support network throughout this journey has been

invaluable to me. Thank you all!! I love you all!!

v

ABSTRACT

Environmental Life Cycle Criteria for Making Decisions about Green versus Toxic

Propellant Selections

Large uncertainties of performance and expense have been an on-going deterrent to

serious consideration of less-toxic green propellants as alternatives to hydrazine for

aerospace propulsion systems. Although candidate propellants may equal or even surpass

the performance of current propellants, with environmental benefits that have been

documented, life cycle trade analyses performed to date have not provided a sufficient

business case for investment in such a significant infrastructural change. These analyses

have been incomplete - typically focused on broad cost, performance, and risk

characteristics, and have not taken into account the comparative costs associated with the

environmental impacts of the alternatives. Environmental life cycle costs must be

included in the analyses in order to understand the true costs incurred.

This research defines a set of environmental components to serve as criteria in life cycle

cost analyses for propellant selection decisions. Based upon information gathered during

visits to facilities responsible for each phase of the propellant life cycle, a detailed

compilation of the environmental life cycle processes and related costs was constructed,

including manufacturing and storage; general safety considerations; site control and

access; air monitoring; personal protective equipment (PPE); decontamination

procedures; transportation by rail, sea, air, and public highway; operations and

maintenance; and end of life disposal.

vi

Lending credence to the significance of the identified costs, a case study approach was

implemented as a way to examine these environmental cost factors using real data. The

case study for this effort was the PRISMA mission, which provided a one-to-one

comparison between the baseline hydrazine to a High Performance Green Propellant

(HPGP) system. This case study revealed a significant reduction in costs (~$500K)

during only one phase of the mission life cycle (a 2/3 reduction from the baseline

hydrazine system).

This analysis resulted in a sample model utilizing the significant cost factors previously

identified that should be included in future total life cycle cost analyses. These cost

categories (broken into operational cost and capital cost) should be identified for both the

baseline option and the alternative option over the expected life of the propellant. The

methodology best suited for incorporation of these identified environmental costs for

decision-making is a customized cost-benefit analysis (CBA). This research has indicated

that the biggest environmental cost drivers over the life cycle of the propellant are facility

operations and maintenance, end of life disposal, and transportation. The costs associated

with health and human safety protection while operating with hazardous materials are

major cost drivers for propellant selection and present significant direct, indirect, and

capital costs over the life of the propellant. These costs are critical, and must be included

in the analyses for informed decision-making.

When environmental costs are included in the analysis, one can potentially bridge the gap

between traditional investment and return on investment models in a timeframe that can

be acceptable to investment decision-makers.

vii

TABLE OF CONTENTS

ACKNOWLEDGEMENTS ............................................................................................... iii

ABSTRACT ........................................................................................................................ v

LIST OF FIGURES ............................................................................................................ x

LIST OF TABLES ............................................................................................................ xii

INTRODUCTION .............................................................................................................. 1

1.1. Background and Statement of the Problem .......................................................... 1

1.2. Objective of the Proposed Research ..................................................................... 4

1.3. Significance of the Proposed Research ................................................................ 4

1.4. Scope and Limitations .......................................................................................... 5

LITERATURE REVIEW ................................................................................................... 6

2.1. Life Cycle Cost Analysis...................................................................................... 6

2.2. Basic Tools Currently in Use ............................................................................... 8

2.2.1 Life Cycle Cost (LCC) Expanded .................................................................9

2.2.2 Cost Benefit Analysis (CBA) Expanded .....................................................12

2.2.3 Life Cycle Assessment (LCA) Expanded ...................................................15

2.3. Current Guidelines, Regulations, and Policies ................................................... 17

2.4. Current Industry Approaches for Incorporating Environmental Costs into Life

Cycle Cost Analysis ........................................................................................... 21

2.4.1 Transportation Industries .............................................................................21

2.4.2 Sustainable Buildings Industry ....................................................................29

2.4.3 Space Industry for Launch Systems ............................................................34

METHODOLOGY ........................................................................................................... 38

3.1. Proposed Methodology for Identifying Environmental Unaccounted for Costs

that Should be Included in Life Cycle Cost Analysis for Propellant Selection

Decisions ............................................................................................................ 38

viii

3.2. Proposed Methodology for Future Life Cycle Cost Analyses ........................... 40

3.3. Research Methodology ....................................................................................... 42

OBSERVATIONS, FINDINGS AND RESULTS ........................................................... 45

4.1. Site Visit Observations ....................................................................................... 45

4.2. Summary of Environmental Unaccounted for Cost Factors Over all Phases of

the Life Cycle of the Propellants Under Consideration ..................................... 48

4.2.1 Manufacturing and Storage .........................................................................56

4.2.1.1 General Safety Considerations ................................................................ 56

4.2.1.2 Site Control and Access .......................................................................... 59

4.2.1.3 Air Monitoring ........................................................................................ 60

4.2.1.4 Personal Protective Equipment (PPE) ..................................................... 62

4.2.1.5 Decontamination Procedures................................................................... 63

4.2.1.6 Storage ..................................................................................................... 64

4.2.2 Transportation .............................................................................................65

4.2.2.1 Land: Rail ................................................................................................ 68

4.2.2.2 Sea ........................................................................................................... 70

4.2.2.3 Air............................................................................................................ 71

4.2.2.4 Land: Public Highways ........................................................................... 72

4.2.3 Operations and Maintenance .......................................................................72

4.2.4 End of Life Disposal ....................................................................................74

4.3. Identification of Significant Cost Drivers .......................................................... 77

4.4. Application of Cost Factors to Life Cycle Analysis Tools ................................ 78

CASE STUDY – PRISMA MISSION .............................................................................. 81

5.1. Test Case Study Comparing Actual Flight of Hydrazine System versus a

―Green‖ Ammonium Dinitramide System ......................................................... 81

5.1.1 Background and Mission Description .........................................................82

5.1.2 Transportation of Propellant ........................................................................84

5.1.3 Handling and Operations During Launch Campaign ..................................85

ix

5.1.4 Assessment of Quantifiable Internal Costs: Comparison of

Hydrazine to HPGP .....................................................................................88

CONCLUSIONS............................................................................................................... 90

6.1. Summary of Findings ......................................................................................... 90

6.2. Recommendations and Future Work .................................................................. 92

Bibliography ..................................................................................................................... 97

x

LIST OF FIGURES

Figure 2.1-1: Life Cycle Analysis Phases: Each phase is evaluated in terms of safety

implications, environmental impacts, and economic development .................................... 7

Figure 2.1-2: Inputs and Outputs to be considered in Life Cycle Cost Analysis

(Environmental Protection Agency (EPA) 2006) ............................................................... 8

Figure 2.4.1-1: Impact Pathway Approach, (European Commission, 2003) ................... 24

Figure 2.4.1-2: Costs of Air Pollution Associated with Urban Passenger Transportation

........................................................................................................................................... 25

Figure 2.4.1-3: Costs of Air Pollution Associated with Rural Passenger Transportation,

(European Commission, 2003) ......................................................................................... 26

Figure 2.4.1-4: Quantifiable Costs Associated with 4 Modes of Transportation in

Germany, (European Commission, 2003) ........................................................................ 26

Figure 2.4.1-5: Life Cycle Stages for Transportation Fuels (Xiaoyu Yan, 2009) ........... 27

Figure 2.4.1-6: Global Greenhouse Gas Emissions in 2004, (International Civil Aviation

Organization, Air Transport Bureau (ATB) 2009) ........................................................... 29

Figure 2.4.2-1: Financial Benefits of Green Buildings, (Kats, et. al., 2003) ................... 31

Figure 2.4.2-2: Relational Costs of Employees to Other Building Costs in California

(Kats, et. al., 2003) ............................................................................................................ 32

Figure 2.4.2-3: Potential Productivity Gains from Enhanced Indoor Environments (Kats,

et. al., 2003) ...................................................................................................................... 34

Figure 4.1-1: Hot-Fire Ground Test Facility Site Visit in Gindsjon, Sweden ................. 47

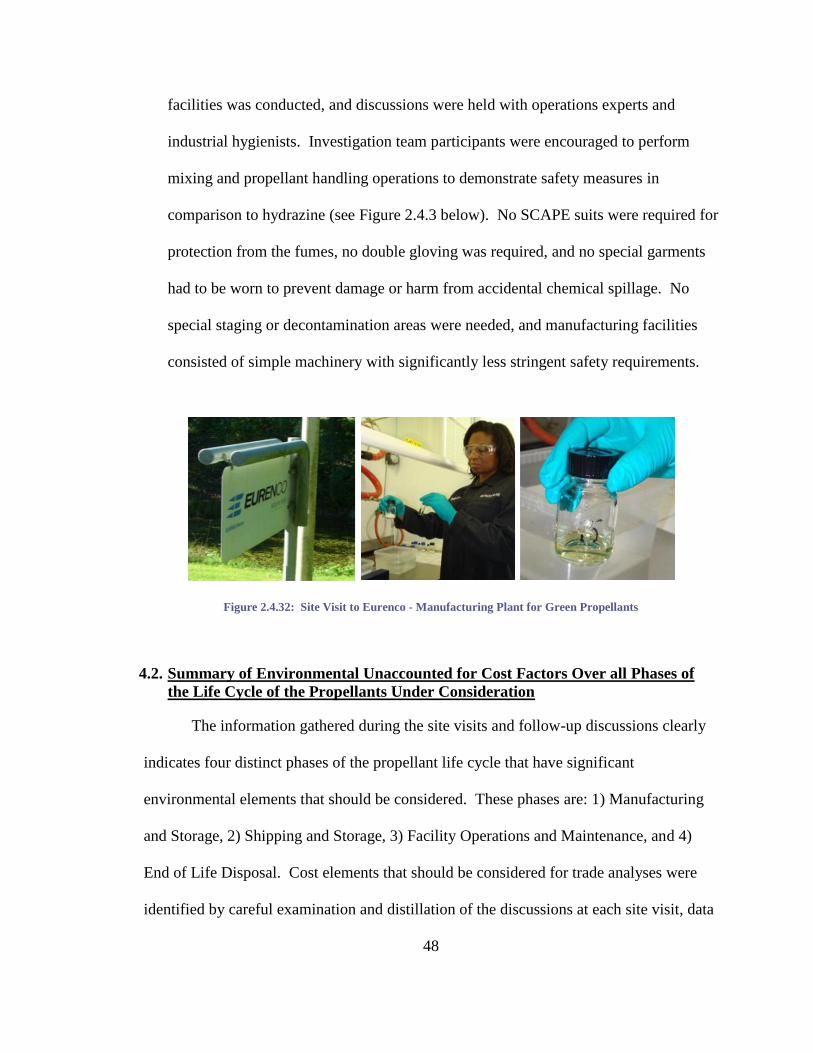

Figure 4.1-2: Site Visit to Eurenco - Manufacturing Plant for Green Propellants .......... 48

Figure 5.1.1-1: PRISMA Mission Logo and Launch Vehicle (Dinardi, High Performance

Green Propulsion (HPGP) On-Oribit Validation & Ongoing Development 2011) .......... 83

Figure 5.1.1-2: Prisma Main Spacecraft Propulsion System with a Hydrazine Tank ..... 83

Figure 5.1.2-1: PRISMA HPGP Transportation .............................................................. 84

xi

Figure 5.1.3-1: Personal Protection Equipment - HPGP vs Hydrazine (Dinardi, High

Performance Green Propulsion (HPGP) On-Oribit Validation & Ongoing Development

2011) ................................................................................................................................. 86

Figure 5.1.3-2: Launch Campaign Fueling Timeline (ECAPS Corporation 2011) ......... 87

Figure 5.1.3-3 Environmental Wastes from the Launch Campaign (ECAPS Corporation

2011) ................................................................................................................................. 88

Figure 6.2-1: Logic Model Discussion for Selection of Future Propellants .................... 93

xii

LIST OF TABLES

Table 2.4.1-1: Health and Environmental Effects (European Commission, 2003) ......... 23

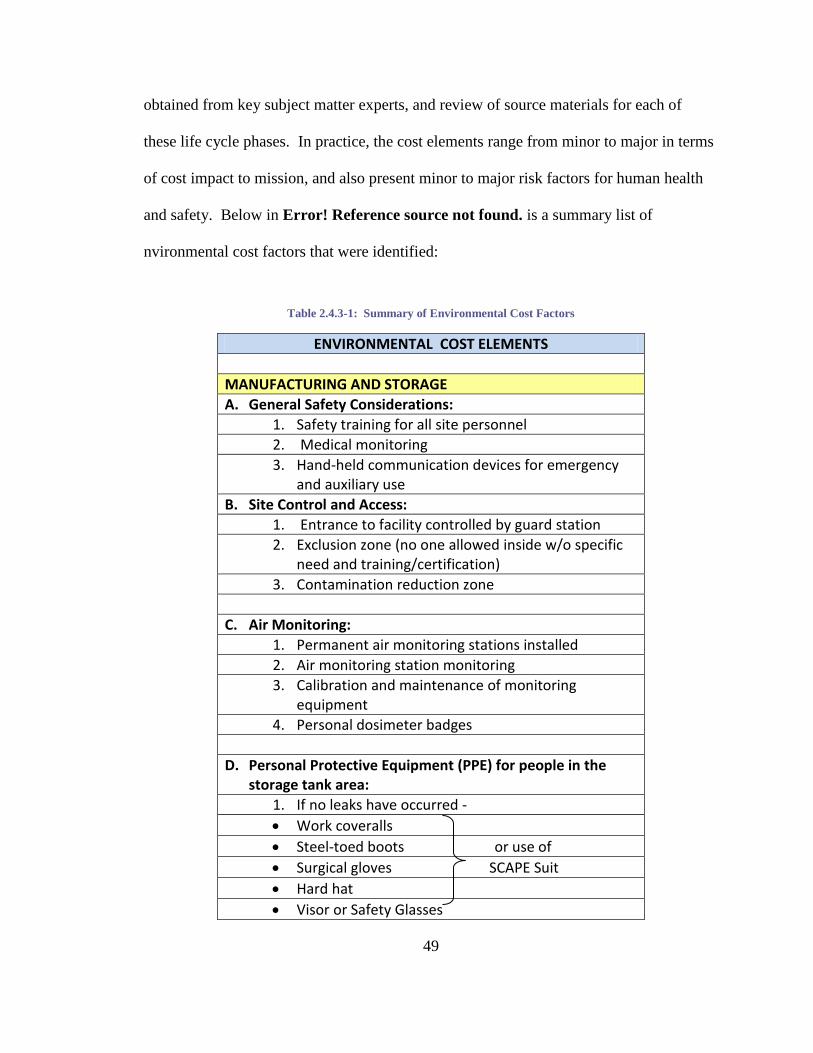

Table 4.2-1: Summary of Environmental Cost Factors ................................................... 49

Table 4.2-2: Environmental Unaccounted for Life Cycle Cost Element Comparison of

Hydrazine to HPGP........................................................................................................... 53

Table 4.2.2-1: CFR for Transportation of Hazardous Materials (Hydrazine and ADN) . 66

Table 4.4-1: Template for Application of Environmental Cost Factors in Analysis ....... 79

Table 5.1.4-1: Comparison for Prisma HPGP vs Hydrazine (Dinardi and ECAPS

Corporation, Site Visit Interviews and Data Provided by ECAPS Subject Matter Experts

2011) ................................................................................................................................. 89

1

INTRODUCTION

1.1. Background and Statement of the Problem

In an environment where budgets are becoming more and more

constrained, it has become increasingly important for federal agencies to find

efficient ways to reduce the costs associated with every aspect of achieving their

missions. In order for entities (both public and private) within the space

community to deliver technologies required to reach the destinations of the future

(like near-earth asteroids, Mars, and other celestial bodies), our nation must find

creative ways to deliver innovative technologies with a watchful eye on

minimizing costs along the way. Decision-makers must evaluate costs over the

full life cycle of the options under consideration in order to make informed

decisions about whether or not to introduce new technologies, systems, or

approaches.

Over the past 50 years, the U.S. and foreign launch systems in the public

domain have used ammonium perchlorate (AP) and hydrazine as the preferred

propellants for their solid and liquid propulsion systems. These propellants have

been known to provide outstanding performance and reliability. Unfortunately,

this remarkable performance comes with a significant trade-off in risk and

―hidden‖ costs as it relates to hazards to humans and the environment in the

manufacturing, storage, transportation, operations, and disposal of these toxic

materials. Many of these ―hidden‖ costs stem from the strict regulations that

govern safe handling of hazardous and carcinogenic materials. As the space

2

community develops new technologies to meet the needs of the next generation of

launch vehicles and spacecraft, the international community and government

entities are demanding that the environmental impact of industrial processes,

including launch vehicle and spacecraft processes be included in the overall cost

analyses.

Since AP contains chlorine, for example, it produces significant amounts

of hydrochloric acid during the combustion process. This hydrochloric acid,

when released into the atmosphere, has been known to have negative effects on

the environment (U.S. Environmental Protection Agency 2007). In addition, a

hypergolic propellant like hydrazine can present a serious danger to humans in the

event of a catastrophic failure, as witnessed during the Columbia accident in 2003

when the presence of this hazardous material impeded the debris recovery efforts,

and could have caused harm to citizens who may have come into contact with it.

(NASA CAIB 2003). In addition to the hazards associated with these toxic

propellants, their use precludes the kind of extended missions that are anticipated

to be prominent features of the nation’s future space exploration policy. Since

one cannot design a propulsion system large enough to store adequate amounts of

propellant to launch, perform exploration and rendezvous missions, and return

safely to Earth, the propellant of choice must be one that can be replenished while

on the surface of the Moon, Mars, an asteroid, or other destination. It must be

naturally occurring in that habitat, like oxygen or hydrogen.

With these anticipated requirements mandated for future missions,

decision-makers must decide when and how to make a wholesale investment in

3

―green‖ propellant technologies. For the purpose of this research, ―green‖

propellants are defined as those exhibiting the following characteristics: 1) low

toxicity, 2) non-carcinogenic, and 3) environmentally benign. Many candidate

―green‖ propellants have been investigated for potential replacement of the

hazardous propellants. One such propellant that has shown great promise is

ammonium dinitramide, or ADN. Its chemical composition is NH4N(NO2)2,

which has as base elements hydrogen, nitrogen, and oxygen. ADN contains no

chlorine, therefore hydrochloric acid is not produced during combustion, and its

Swedish manufacturers have claimed that ADN production does not require any

toxic materials. Other attractive features include its ability to easily be extracted

into water, which makes it suitable for water washout and easy ingredient

recovery; simple venues for destruction, as it is easily converted to the fertilizer

ammonium nitrate; and very attractive performance and ballistic characteristics

(Thiokol Chemical Corp Brigham City, UT 1998).

As the space industry performs trade studies to evaluate these new green

propellants in comparison to the current toxic ones, and aims to propose these

new technologies for new missions or flights of opportunity, they are required to

provide the costs associated with implementing these technologies over their

entire life. Unfortunately, to date, life cycle cost analyses have omitted the costs

associated with the environmental impacts for both the current propellants and the

proposed green propellants. The omission of these costs discounts significant

costs incurred in all phases of the life cycle, and has made the introduction of new

propellants prohibitive, as the business case has not been closed to transition to

4

the new green propellants. Decision-makers in this area have been put in the

position to make decisions based upon incomplete, and thus inaccurate, data.

1.2. Objective of the Proposed Research

The purpose of this research is to define a set of environmental factors that

could be added to the decision criteria used to perform trade analysis for propellant

selection decisions. Past studies that explored transitioning from toxic propellants

like AP and hydrazine to green propellants typically focused on economic,

performance, and risk characteristics, and did not account for many of the ―hidden‖

costs incurred. Because of this incomplete methodology, the National Aeronautics

and Space Administration (NASA) has previously been unable to close the business

case for committing to large-scale investments in green propellant technologies. It is

the intent of this research to bring many of these ―hidden‖ costs to light, and provide

the space research and development community with decision criteria that will reflect

a more accurate account of the costs that must be considered throughout the life

cycle. When environmental costs are included in the analysis, one can potentially

bridge the gap between traditional investment and return on investment models in a

timeframe that can be acceptable to the investment decision-makers.

1.3. Significance of the Proposed Research

There is significant interest by the United States Department of Defense,

NASA and their industry partners in technologies that open the door for future

capabilities for our nation. The research being proposed here can have a significant

5

impact on the US capability to develop lower cost green launch systems. In order for

the community to take advantage of new technologies and capabilities, it must use a

research methodology that accurately reflects life cycle costs to guide these important

decisions. Without a more comprehensive cost accounting methodology to judge

propellant scenarios, it is difficult to demonstrate the holistic benefit of green

propellants. Since the assessment of the costs associated with a transition to those

new technologies has been a deterrent in past studies, the light shed upon the analysis

from this different vantage point may support and perhaps even spur innovation in

this area. When environmental costs are coupled with the economic and risk costs,

one can more easily identify and address environmental constraints that prohibit

growth and development, and allow for the development of sustainable propulsion

systems for the future.

1.4. Scope and Limitations

The research conducted here focuses strictly on liquid propellants, assuming

the use of Anhydrous Hydrazine monopropellant as a baseline, and provides no

comparison consideration for Monomethyl Hydrazine (MMH) for bipropellant use.

This research was conducted with careful consideration of the fact that

generally in the space community, trade studies must be conducted with limited

resources in a relatively short period of time (on an average completed within 90

days). In order for environmental elements to be included in the studies, there must

be a set of criteria that can be readily documented and quantified. With this in mind,

those environmental cost elements that are difficult to quantify, and require exercises

to value impacts like health risks via surveys, etc. were not considered when

6

establishing the baseline environmental cost factors to be included in future

propellant trade analyses.

Costs associated with the identified environmental cost factors were included

when available, but many of these costs were not identified during this investigation.

These remaining unidentified costs can and should be requested from those

performing future trade studies; the current academic investigation was unable to

provide financial resources for the data to be mined and included in this research.

LITERATURE REVIEW

2.1. Life Cycle Cost Analysis

The term ―life cycle‖ refers to the major activities over the course of the

product’s life-span from its manufacture, including the raw material acquisition, use,

maintenance, and its final disposal. The life cycle analysis performed in this research

provides a means for one to understand the cumulative effect of all of the impacts of

each stage in the material’s life cycle, and includes environmental impacts that are

often not addressed in traditional life cycle estimations (i.e. environmental effects,

―hidden‖ operational costs, and end-of –life disposal), but represent an actual cost that

must be accounted for (Environmental Protection Agency (EPA) 2006). This type of

analysis can provide a more accurate representation of the true human health and

environmental impacts associated with a product, system, or process, and will better

inform the decision-maker of the cost trade-offs in product and process selection.

7

Life cycle analysis is often called a ―cradle-to-grave‖ approach for assessing

any system or its components. Cradle-to-grave begins with the gathering of raw

materials from the earth to create the product and ends at the point when all materials

are completely consumed or returned to the earth (See Figure 2.1-1 below)

(Environmental Protection Agency (EPA) 2006).

Figure 2.2.1-1: Life Cycle Analysis Phases: Each phase is evaluated in terms of safety implications,

environmental impacts, and economic development

It is important to recognize and understand how each choice influences what

happens during these stages so that a decision-maker can balance trade-offs and

positively impact the environment, the economy, and society. Each decision will have

input requirements and associated outputs that must be accounted for in the cost analysis

(See Figure 2.2.1-2 below).

Raw Material Production

Manufacturing Distribution Use/OperationsEnd of Life Recovery

Management

Life Cycle Analysis Phases

8

Figure 2.2.1-2: Inputs and Outputs to be considered in Life Cycle Cost Analysis (Environmental Protection

Agency (EPA) 2006)

2.2. Basic Tools Currently in Use

The public body of literature contains large volumes of information about the

topics of life cycle costing and life cycle analysis. In general, when conducting an

analysis of the cost over the life of a product or system, life cycle costing (LCC), cost

benefit analysis (CBA), and life cycle assessment (LCA) are the tools most

commonly used. LCC models generally have an economic focus, with budget

allocation and business performance as key indicators. A CBA model also has an

economic focus, but it includes the social benefits of the proposed options in

monetary terms, and provides a means to weigh those benefits against the costs. An

LCA model is a methodology used to evaluate the detailed cumulative environmental

performance or effects of a system (Huppes 2004).

LCCs are used broadly across the federal government, and are required for

military and other federal government acquisitions, software development, materials

9

systems, flight systems, energy management systems, and a large array of other

applications. LCCs are also used broadly in public industry during green building

design, automobile and other vehicle production, fuel production, and many other

areas. Although LCCs have been broadly used to understand conventional costs, the

application of environmental components to elements of cost is not advanced enough

for the community to have a commonly accepted methodology for estimating these

values to be included in the models (Steen 2005). This makes extending the LCC

analysis to a CBA more difficult because one must not only determine the

conventional and environmental elements of cost for the model; but also include

social benefits in monetary terms, and then aggregate the costs in a meaningful way.

LCAs can be much more complex than LCCs and CBAs, as they require the

modeler to take inventory of the entire system to quantify as much as is feasible,

including burdens (i.e. individual pollutant emissions), impacts, and their monetized

values; and to use multi-criteria analysis to quantify those impacts that are too

uncertain or do not easily allow quantification by monetization (Rabl 2008).

2.2.1 Life Cycle Cost (LCC) Expanded

Life cycle cost has historically been, and continues to be, the methodology

by which Federal agencies normalize the cost of procurements throughout the

usable life of the product. The intent behind this methodology is to ensure that

operating costs of new acquisitions are clearly identified to assist agencies in

optimizing procurement strategies and choosing the option that provides the

lowest cost of ownership over the life cycle. Typically, an analysis of life cycle

cost accounts for all the costs associated with the acquisition, operation,

10

maintenance and repair, replacement, and retiring/salvage of a particular product,

whether it is a building, machinery, or an operating system such as a hydro-

electric power plant. To conduct a complete life cycle cost analysis requires that

the variables and inputs are normalized to a common point, usually in present

value of money, with out-year cost returned to present value via a predetermined

discount rate. A good LCC model would then demonstrate values in present

value with the capability to demonstrate future value and cost.

As stated in a 2007 update of life cycle cost models and processes for the

State of Washington, as part of the process of making capital investment

decisions, a commonly recognized component is a present value life cycle cost

analysis. For assets like facilities, a ―same-year dollar basis‖ comparison of all

costs related to quantifiable capital and operations as well as an estimation of

those costs over the life of the facility can be addressed in the life cycle cost

analysis. The costs included in the analysis are for planning (the purchase of land,

existing facilities, or leasing agreements), development (construction), operations

(maintenance, equipment and staffing), and management (project management,

staffing). When considering the development of a new facility and/or the adaption

of existing facilities in part or full, accounting for all potential costs and benefits

in the analysis will allow decision-makers to determine the most economical

choice among various possibilities (Joint Legislative Audit and Review

Committee 2007). In order to calculate the total life cycle cost of a project, one

must sum each of the identified costs, and then subtract any elements that would

constitute a positive cash flow such as a salvage or resale value:

11

Life-cycle cost = first cost + maintenance and repair + energy + water

+ replacement - salvage value (Fuller 2005)

In practice, the following formula is frequently used:

LCC = C + Mpw + E pw + R pw - S pw , where the subscript, pw, denotes the present

worth using a preapproved discount rate (Hestermannm n.d.). The discount rate is

sensitive and therefore set prior to calculation to prevent manipulation of the

outcome. Depending on project complexity, additional parameters can be added

to the calculation to increase fidelity.

a. (C) is the capital cost, which would include the initial expenses for the

system design, engineering, equipment, and installation. This cost is

always considered as a single payment occurring in the initial year of the

project, regardless of how the project is financed (Hestermannm n.d.).

b. (M) is the sum of all yearly scheduled operation and maintenance (O&M)

costs. O&M costs include such items as an operator's salary, inspections,

insurance, property tax, and all scheduled maintenance (Hestermannm

n.d.).

c. (E) is the energy cost, which is simply the sum of the annual fuel costs.

Energy cost is calculated separately from operation and maintenance costs,

so that differential fuel inflation rates may be used (Hestermannm n.d.).

d. (R) captures the replacement costs, and is the sum of all anticipated repair

and equipment replacement costs over the life of the system

(Hestermannm n.d.).

e. (S) is the salvage value of the system, which is its value at the end of its

usable life (Hestermannm n.d.).

Future costs must be discounted so that they take into consideration the

time value of money. In many business decisions, a selection is made primarily

12

based upon the procurement costs. When an LCC analysis is conducted, the

decision-maker is provided with the additional benefit of knowing whether or not

the potential operational savings are enough to justify the initial investment costs.

Life cycle cost models are viable tools for accounting for actual or conventional

budgetary and economic costs, but do not function well when additional or non-

traditional activities are being evaluated (H. Paul Barringer 2003).

2.2.2 Cost Benefit Analysis (CBA) Expanded

Cost-benefit analysis (CBA) is a method for quantifying costs and

benefits of a course of action, program, or project, and those of its alternatives, to

provide a procedure for a single scale of comparison for unbiased evaluation.

Though primarily used in financial analysis, CBAs are not limited to monetary

considerations like LCCs. They often include those environmental and social

costs and benefits that can be reasonably quantified. CBAs provide an analytical

way to make decisions about issues that are more difficult to quantify such as

education, health care, transportation, or the environment. The key component

for developing a CBA is quantifying the status quo (current actual cost over the

evaluated time) of a particular action. All other alternatives are then evaluated

against the existing action. After one defines what is considered to be a ―benefit‖

for the analysis, and the relevant time is established, benefits and costs can be

estimated and modeled. For example, in some studies a benefit is defined as

something that promotes or adds to human well-being, whereas a cost is

considered to be something that diminishes it. As described above for life cycle

cost analysis, the present value of both current and future costs and benefits must

13

be considered. One must consider that the money spent today will not have the

same value in the future, as inflation will decrease the value if expressed in future

terms. In order to compensate for these changes in value, one must discount the

future costs and benefits. The determination of the value for the discount rates

and future values used for CBA must be based on a coherent set of circumstances

that are established from the beginning, or the outcome can be significantly

skewed (Environmental Literacy Council 2008).

In many policy considerations, decision-makers may determine that they

will measure as benefits parameters like increased personal income, improved

quality of life, or improvements in the quality of air that we breathe. On the other

hand, costs may be identified as missed opportunities; costs that are easily

identified and explained (internal costs); and external costs that are typically hard

to quantify – i.e. end of life disposal; environmental impact due to wastes,

emissions, and pollutants; or the cost of health problems that result from

hazardous or toxic products. Although these external costs are not typically

included in the prices that are paid for products, the cost is still paid by society in

taxes, compensation dispensed for accidents, payments for insurance and medical

fees, and even through reduced environmental quality for future generations

(Econation 2010). These external costs (and sometimes benefits) are considered

to be externalities, and they are usually imposed upon parties that did not

contribute to the action causing the benefit or cost (Ozkan 2008) (tutor2u n.d.).

In practice, a CBA is performed in stages: 1) definition of the project, 2)

identification of the project impacts, 3) determination of which impacts are

14

economically relevant, 4) quantification of the relevant impacts, 5) monetization

of relevant effects, and 6) determination of discounting for cost and benefit flows

(Hanley and Splash 2003). In any CBA, there must be a common measurement

unit established for costs and benefits. The most convenient unit is money, so

benefits and costs of alternatives must be expressed in terms of equivalent

monetary value and must account for the time value of money (including

inflation) (Watkins n.d.). Once the common measure has been established, one

can compare and evaluate options to find an optimal solution. In economics, the

ideal solution would be what is called a Pareto improvement, in which a change

from the baseline scenario to an alternative scenario would make at least one

improvement to an individual or a system without negatively affecting another

individual or diminishing another part of the system. While the ideal solution is

desirable, it is often impractical or impossible. A more commonly applied

measure of economic efficiency is the Kaldor-Hicks efficiency (Reckon, LLP

2009) Utilizing the Kaldor-Hicks theory, there will be individuals/systems that

are both made better and worse by going from the baseline to an alternate

scenario; however, the ones that are improved would in theory compensate those

that are diminished (Environmental Literacy Council 2008). An example of such

a scenario would be a new air transportation vehicle that permits customers to

travel from Washington, DC to Los Angeles in two hours instead of the typical

five-hour flight. This new capability would provide improvements for both the

provider and the customers, but it would release toxic pollutants into the air.

Under the Kaldor-Hicks theory, the producers and customers would still be

15

willing to proceed with this new capability even if it required compensation to the

victims of that pollution. A Kaldor-Hicks solution only provides a mechanism for

possible compensation, but does not require that the parties carry it out.

Therefore, in contrast to the Pareto improvement, a Kaldor-Hicks improvement

may result in a scenario where not every party is better off – in fact, some parties

could be affected negatively (Stringham 2001)

2.2.3 Life Cycle Assessment (LCA) Expanded

As society becomes increasingly aware and concerned about the

environment and the depletion of natural resources, businesses and industries are

increasingly motivated to assess the effects that their activities are having on the

environment. In many industries, businesses are committing to developing and

using more environmentally friendly products and processes. With the wealth of

current legislation that sets expectations in this area, many businesses seek to

exceed the compliance expectations, and are implementing pollution prevention

strategies and environmental management systems. The life cycle assessment is

one such environmental management system tool (Environmental Protection

Agency (EPA) 2006).

Life cycle assessments first address the capture and collection of the raw

materials required to create a product, and conclude with analysis of the

consumption of the product or its return to the earth. Each stage in the LCA is

dependent upon the others, so the LCA must estimate a cumulative environmental

impact – including those impacts that are generally not included in traditional life

16

cycle cost analyses (i.e. extraction of the raw materials, transportation of the

product materials, and end of life disposal). The LCA technique, which can be

very effective in assessing the environmental effects and potential impacts of a

product, system, process or service, is a systematic process with four components.

The first step is to define the goal and scope of the product, system, process or

service. This step enables the assessor to establish the context for the analysis,

clearly identify which environmental effects are to be reviewed, and establish the

boundaries for the assessment. The second step is to perform an inventory

analysis, which develops a compilation of material and energy inputs and

environmental releases that are relevant to the assessment. This compilation

would include things like solid waste disposal, airborne emissions, waste effluents

that are discharged into water, and other inputs. The third step is to perform an

impact assessment, which would determine the potential ecological and human

effects of the inputs and releases identified in the inventory analysis. The fourth

step is to interpret the results of the inventory and impact assessment to determine

the preferred product, system, process or service, clearly understanding the

assumptions incorporated into the assessments of the previous steps

(Environmental Protection Agency (EPA) 2006).

An LCA provides the decision-maker with the information necessary to

determine which product, system, process or service has the least effect on the

environment. LCAs are instrumental in preventing a decision that shifts

environmental problems from one part of the system to another or from one stage

in the life cycle to another. Since an LCA does not provide a solution regarding

17

the most cost-effective or best-performing product, system, process or service, it

should be combined with cost and performance data to reach a final conclusion.

Although LCAs are effective, they are costly in terms of time and resources. The

data required to perform a comprehensive LCA can be difficult to obtain, as

multiple business practices from diverse industries must be evaluated. The

availability and accuracy of the data can significantly affect the final results.

Because of these constraints and complexities, LCAs are conducted in one of

three levels. A comprehensive LCA is considered to be a Level 1 LCA, in which

the data quality requirements, complexity of system boundaries, and completeness

of the inventory analysis components meet the most stringent requirements of

strict legislation, like the Energy Independence and Security Act of 2007. A level

2 LCA, which is also called a standard LCA, evaluates all of the major component

operations, but with a less comprehensive inventory analysis and lower data

quality requirements. The level 3 LCA, or the screening LCA, has the least

degree of analysis complexity, data quality, and completeness of the inventory

analysis, but it can be very useful for taking a ―quick look‖ or preliminary

assessment of one or more technology alternatives being considered, or to inform

research funding decisions (Allen, et al. 2009).

2.3. Current Guidelines, Regulations, and Policies

There are dozens of guidelines and policies that require federal agencies to

perform life cycle cost analysis in order to make well-informed decisions about the

efficient allocation of resources. Executive Order 13514, Federal Leadership in

Environmental, Energy, and Economic Performance, was created to encourage

18

federal government agencies to lead by example with regards to promoting energy

security, protecting the environment, and protecting the interests of taxpayers. This

Executive Order outlines the United States policy that ―Federal agencies shall

increase energy efficiency; measure, report, and reduce their greenhouse gas

emissions from direct and indirect activities; conserve and protect water resources

through efficiency, reuse, and storm-water management; eliminate waste, recycle,

and prevent pollution; leverage agency acquisitions to foster markets for sustainable

technologies and environmentally preferable materials, products, and services;

design, construct, maintain, and operate high performance sustainable buildings in

sustainable locations; strengthen the vitality and livability of the communities in

which Federal facilities are located; and inform Federal employees about and

involve them in the achievement of these goals.‖ In order to achieve this objective,

agencies are expected to prioritize their decisions and actions based upon a complete

accounting of the economic, social and environmental benefits and costs, resulting

from a life cycle return on investment analysis. This Executive Order only requires

that a life cycle calculation be performed – it does not provide guidance regarding the

mechanism or methodology for the calculations (The President of the United States

2009).

Similarly, the Code of Federal Regulations (CFR), 10 CFR Part 436: ―Federal

Energy Management and Planning Programs‖ establishes rules and standards to

promote a reduction in energy consumption for energy management and planning

programs, and to promote the most cost effective investments in energy and water

systems for buildings and water conservation measures for federal buildings. This

19

document requires agencies to determine the cost-effectiveness of a project over its

life cycle, provides guidance regarding the methodology and procedures for

calculating and comparing the life cycle costs of Federal buildings, presents a

mechanism for determining the cost effectiveness of energy and water conservation

methods, and establishes a method for ranking alternatives for designing new

buildings or retrofitting existing buildings based upon life cycle costs. 10 CFR 436

makes reference to the ―Life Cycle Costing Manual for the Federal Energy

Management Program” (NIST 85-3273), which expands on the life cycle cost criteria

and techniques described in 10 CFR 436. This manual defines how economic

performance can be measured, outlines how assumptions should be handled, and

describes which procedures should be followed in performing life cycle cost

evaluations (GPO Home Page n.d.).

As a companion to 10 CFR 436, and NIST 8-3273, President William Clinton

released ―Executive Order 13123: Greening the Government through Efficient

Energy Management,‖ which required that ―Agencies shall use life-cycle cost analysis

in making decisions about investments in products, services, construction, and other

projects to lower the Federal Government’s costs and to reduce energy and water

consumption…‖ The Office of Energy Efficiency and Renewable Energy in the U.S.

Department of Energy subsequently published guidance documents for federal

agencies to facilitate implementation of this Executive Order. The implementation

guidance provides clarification on how federal agencies should determine life cycle

costs for the investments required by the Executive Order, including guidelines for

comparing different energy and fuel alternatives and assessing the current tools for

20

performing this analysis. Executive Order 13123 also specifically recommends the

use of life cycle cost analysis (LCCA), which evaluates all costs of ownership,

operations, maintenance, and disposal over the life of the product or system (U.S.

Department of Energy; Office of Energy Efficiency and Renewable Energy; Federal

Energy Management Program 2003).

Another piece of important legislation is the ―Energy Independence and Security

Act of 2007”. This act was established with the intent to facilitate the United States’

movement toward greater energy independence and security by encouraging the

production of more clean, renewable fuels, by increasing the efficiency of U.S.

products, buildings, and vehicles, and by promoting more research and development

on greenhouse gas capture and storage technologies. This legislation specifically

calls for life-cycle assessments and life-cycle costing, with some specific guidelines,

to be performed for investment decisions (Congress 2007).

A number of the guidelines require specific agencies to develop a

methodology to determine the life cycle costs and cost benefits. However, when

different agencies perform this analysis using different inputs, parameters, and

assumptions, it is nearly impossible to compare projects or systems among the

agencies. In order to address the need for uniform guidance, the White House Office

of Management and Budget (OMB) released OMB Circular No. A-94, ―Guidelines

and Discount Rates for Benefit-Cost Analysis of Federal Programs.‖ This circular

provides a general roadmap for federal agencies to conduct the cost-benefit and cost-

effectiveness analyses. Although it does specifically exempt decisions concerning

things like water resource projects, the acquisition of commercial services, or energy

21

management programs (guidance for these is provided in the ―Economic and

Environmental Principles and Guidelines for Water and Related Land Resources

Implementation Studies,‖ OMB Circular No. A-76, and the Federal Register of

January 25, 1990 respectively), the circular does provide baseline guidance and can

serve as a checklist for agencies to ensure adequate inclusion of all elements required

for sound cost-benefit analyses (The White House 1992).

Circular A-94 makes a distinction between performing a benefit-cost analysis

and a cost-effectiveness analysis. The benefit-cost analysis is the recommended

technique for formal economic analysis. A cost-effectiveness analysis is permitted

when it has been determined that the benefits of competing options are the same,

when a policy requires that the benefits must be provided, or when it is not necessary

or practical to consider the monetary value of the benefits under consideration. The

circular establishes the net present value as the standard criterion that agencies should

use to determine whether a program can be justified based upon economic principles.

It also provides guidance on outcome measures, elements that should be added into

the benefit-cost analysis, identification and measurement of the benefits and costs to

be considered, treatment of inflation in the analysis, establishment of the discount

rate, and treatment of uncertainties (The White House 1992).

2.4. Current Industry Approaches for Incorporating Environmental Costs into

Life Cycle Cost Analysis

2.4.1 Transportation Industries

The European Commission has sponsored a series of research activities to

evaluate the social-environmental damages resulting from the transport of goods

22

and people. The European Research Network has been working to develop and

adopt a common methodology and conduct case studies to quantify the external

and other unaccounted for costs associated with energy production and

consumption. It was their intent to improve energy and transport policies by

establishing a mechanism to either tax the most damaging fuels and technologies

or incentivize the fuels and technologies with the lowest socio-environmental

cost. This can only be successful once a robust methodology for monetary

quantification of the socio-environmental damages is in place (European

Commission 2003). In Europe, hundreds of technology research projects are

combined with socio-economic research to provide a scientific basis for policy

formulation related to energy and the environment. The European Commission

has sponsored this research in order to determine the consequences of specific

CO2 targets and the cost effectiveness of technologies developed to address

meeting these targets; to address climate change issues by determining the least

expensive option to achieve Kyoto, while identifying the effects of greenhouse

gas emission trading; and to provide a mechanism to measure the socio-

environmental damages resulting from energy production and consumption –

identify which damages should be included in the external cost evaluation, and

what methodology should be used. The Commission’s External Cost report uses

cost benefit analysis as a principal tool to compare the costs required to reduce

environmental burdens. Table 2.4.1-1 below provides an overview of the

categories, burdens, and their associated effects that were included in this

23

analysis. Building material, crops, global warming, and ecosystem effects were

considered in addition to human health effects (European Commission 2003).

Table 2.4.1-1: Health and Environmental Effects (European Commission, 2003)

The Commission studies used an impact pathway approach, which follows a

pathway from its source by evaluating changes in the quality of the air, soil, and water,

and considering physical impacts before translating them to monetary costs and benefits.

24

The following diagram (Figure 2.4.1-1) illustrates the main components of this impact

pathway approach (European Commission 2003).

Figure 2.4.1-1: Impact Pathway Approach, (European Commission, 2003)

Using the impact pathway categories presented in Figure 2.4.1-1, researchers

found that when comparing the costs associated with vehicle use, vehicle production, fuel

25

production, and infrastructure, the most dominant air pollution cost is associated with

vehicle use, which varies by city due to fluctuations in the number of people who can be

affected by airborne pollutants and the climate (See Figure 2.4.1-2 below).

Figure 2.4.1-2: Costs of Air Pollution Associated with Urban Passenger Transportation

In areas that are not considered to be urban (rural areas), fewer people are

impacted by tail pipe emissions, so other processes like vehicle and fuel production and

infrastructure provision become increasingly more significant and important relative to

the costs associated with vehicle use (Figure 2.4.1-3).

The researchers who conducted the European Commission study then estimated

the total quantifiable damage costs that could be attributed to accidents, noise, global

warming, and air pollution. In 1998, the quantifiable total costs were approximately $33

26

billion for the entire transportation sector. As seen in Figure 2.4.1-4 below, the biggest

driver for high external costs for transportation in Germany is road transportation.

Figure 2.4.1-3: Costs of Air Pollution Associated with Rural Passenger Transportation, (European

Commission, 2003)

Figure 2.4.1-4: Quantifiable Costs Associated with 4 Modes of Transportation in Germany, (European

Commission, 2003)

27

Rail, aircraft, and inland waterway modes of transportation have external costs that are

―insignificant‖ relative to the costs associated with road transportation. It is also worth

noting here that for the aircraft mode of transportation, the largest contributor to external

costs is increases in the atmosphere of green-house gases like CO2. For air pollution, the

data presented takes into consideration direct emissions and those from fuel and

electricity production.

Another study conducted by Yan and Crookes presents a ―Life Cycle Analysis of

Energy Use and Greenhouse Gas Emissions for Road Transportation Fuels in China.‖

The life cycle stages that were assessed for transportation fuels in this study included

feedstock recovery and transport, fuel production and transport, and fuel consumption

(See Figure 2.4.1-5 below) (Xiaoyu Yan 2009).

Figure 2.4.1-5: Life Cycle Stages for Transportation Fuels (Xiaoyu Yan, 2009)

The Yan and Crookes report also identifies the road transport sector as the

dominant contributor to the external costs being considered. Road transportation was

named as the dominant oil consumer and the most significant source of greenhouse gas

emission in China, due to the steady increase in use of private vehicles over the past few

28

years. Again, the focus in their life cycle analysis is on CO2 emissions, and promotion of

alternative fuels to reduce the greenhouse gas effects (Xiaoyu Yan 2009).

Another report, published by the Aviation Fuel Life Cycle Assessment Group for

the Air Force, provides insight into how life cycle assessments are performed for their

aviation fuels. The interim report under the Advanced Propulsion Fuels Research and

Development contract provides a framework and specific guidelines for estimating the

greenhouse gas footprints for transportation fuels – aviation fuels in particular. This set

of guidelines instructs the reader in great detail on how to perform the life cycle analysis,

with the focus on reducing fuel consumption and greenhouse gas emissions (Allen, et al.

2009).

The International Civil Aviation Organization’s Air Transportation Bureau (ATB)

is addressing the effects of international aviation greenhouse gas emissions on the global

climate. In order to find effective solutions to protect the environment, they are

encouraging technology improvements, providing operational measurement tools,

pursuing market-based measures, and working toward the movement to sustainable fuels.

Figure 2.4.1-6 below shows that in 2004, transportation modes accounted for only 13% of

the global greenhouse gas emissions. Of that 13%, only 2% was attributed to aviation

CO2 emissions. As reported in the European Commission study, road transportation was

the dominant contributor to greenhouse gas emissions, with aviation contributing only

13% (International Civil Aviation Organization, Air Transport Bureau (ATB) 2009).

29

Figure 2.4.1-6: Global Greenhouse Gas Emissions in 2004, (International Civil Aviation Organization, Air

Transport Bureau (ATB) 2009)

2.4.2 Sustainable Buildings Industry

In the sustainable buildings industry, the prevailing theme throughout the

literature, especially for federal facilities, is to reduce the energy consumption and

costs, to improve the work environment of the facilities, and to minimize the

environmental impact of facility operations. In order for these facilities to be

―sustainable‖, managers and designers must perform their duties with the

following goals in mind: 1) Minimize waste and make the most efficient use of all

resources, including water, energy, land, and materials, 2) protect the natural

environment, from which all other resources are produced, and 3) create a healthy

facility environment for current and future generations (BuildingGreen, Inc.

2001).

As described in section 2.3 above (Current Guidelines, Policies, and

Regulations), 10 CFR 436 includes a requirement for federal managers to make

decisions based upon information resulting from a Life Cycle Cost analysis, so

the majority of published literature regarding sustainable buildings makes

30

mention of or provides data to evaluate the life cycle costs. Those costs include

initial investment costs, planned maintenance costs, repair and replacement costs,

costs for utilities like water and energy, and other costs that would be incurred

over the life of the facility. Additionally, managers and designers of sustainable

buildings are more often taking extra steps to perform environmental life cycle

assessments in order to understand the potential environmental impacts over the

life of the facility or its products (BuildingGreen, Inc. 2001).

A report published by California’s Sustainable Building Task Force, ―The

Cost and Financial Benefits of Green Buildings‖ presents a comprehensive cost

benefit analysis for ―building green‖. In the sustainable building industry,

environmental and human health benefits are commonly acknowledged in their

green building discussions, but this report claims that ―minimal increases in

upfront costs of about 2% to support green design would, on average, result in

life cycle savings of 20% of total construction costs – more than ten times the

initial investment…… an investment of up to $100,000 to incorporate green

building features into a $5 million project would result in a savings of $1 million

in today’s dollars over the life of the building. (Kats, et al. 2003)‖ In addition to

the typical financial benefits examined in building cost benefit analyses, this

report identifies and includes financial benefits from increased productivity and

health for people exposed to the environment of the building. The task force

found an apparent consensus both inside and outside of the sustainable building

community about the environmental and social benefits of building green.

However, there is consistent concern regarding the lack of accurate and

31

comprehensive economic and financial information regarding these benefits; thus,

the task force funded an Economic Analysis Project to develop a more accurate

and comprehensive cost benefit analysis of a sustainable building. The findings

from this report show cost savings in energy, emissions, water, waste, operations

and maintenance, and an enhancement in worker/occupant health and productivity

(Figure 2.4.2-1). The report states that they observed such a large effect on

productivity and health because both direct and indirect costs for employees are

significantly larger than the cost of construction or energy. Therefore, one will

see large financial benefits even from small changes in health and productivity

(Kats, et al. 2003).

Figure 2.4.2-1: Financial Benefits of Green Buildings, (Kats, et. al., 2003)

32

Although health and productivity components are typically addressed

separately, this report combines them as they both attribute directly to worker

well-being and comfort. Worker well-being and comfort are measured by their

impact on productivity. The report acknowledges the very complicated

relationship or correlation between building design/operation and worker comfort

and/or productivity, and utilizes recent meta-studies that have screened and

synthesized the thousands of studies, reports, and articles published on the subject

matter. As shown in Figure 2.4.2-2 below, the cost to the state of California that

is attributed to worker/employee costs is ten times the combined costs attributed

to property costs (Kats, et al. 2003).

Figure 2.4.2-2: Relational Costs of Employees to Other Building Costs in California (Kats, et. al., 2003)

33

It is very difficult to measure the exact cost benefits associated with

healthier, greener buildings, because those costs associated with poor air quality

and poor environmental conditions result in more employees taking days off, and

more employees experiencing allergies, asthma, and other respiratory illnesses.

These effects on the employees are typically hidden in paid sick leave days,

insurance and medical costs, and lower productivity while at work. William Fisk

and his colleagues conducted a comprehensive study that quantified potential

health and productivity benefits from enhanced indoor environments (Figure

2.4.2-3). His study found a potential savings or productivity gain in 2002 dollars

that ranged from $43 billion to $235 billion (Kats, et al. 2003). When these kinds

of elements are introduced into a life cycle analysis, they can help the decision-

maker have a significantly more informed view of the trade space, and can

significantly impact the final decision whether to invest a green building.

34

Figure 2.4.2-3: Potential Productivity Gains from Enhanced Indoor Environments (Kats, et. al., 2003)

2.4.3 Space Industry for Launch Systems

Several trade studies regarding propellant options for future architectures

have been performed across NASA in recent history, including the Explorations

System Architecture Study (ESAS), the Crew Exploration Vehicle (CEV) Smart

Buyer Study, the CEV Green Propellant Study, the Propulsion Architecture

Study, and more.

Analysis conducted by NASA to determine the affordability of exploration

architecture options did not use a budgetary approach as is typically done for

smaller systems or even complex systems when more time is allotted for model

development and analysis. Instead, NASA used a combination of cost-estimation

methods as described in the quote below:

35

“ESAS (Exploration System Architecture Study) operations analysis

of affordability used a combination of cost-estimation methods

including analogy, historical data, subject matter expertise, and

previous studies with contracted engineering firms for construction cost

estimates. The operations affordability analysis relied on cost-

estimating approaches and was not budgetary in nature, as budgetary

approaches generally have extensive processes associated with the

generation of costs, and these budgetary processes cannot easily scale

to either architecture-level study trades in a broad decision-making

space or to trading large quantities of flight and ground systems design

details in a short time frame. The operations cost-estimating methods

used in the ESAS are attempts at fair and consistent comparisons of

levels of effort for varying concepts based on their unique operations

cost drivers.” (NASA 2005)

Most cost estimates were calculated using parametric cost estimating tools,

which utilize historical data to predict the development or production costs of related new

space programs/instruments. The tool most commonly used was the NASA/Air Force

Cost Model (NAFCOM), which has an expansive database of about 122 historical

projects including spacecraft and launch vehicles.

No environmental cost-benefit analysis was included in their life cycle

cost model, although some of the costs associated with using toxic fuel are

included in the operations costs (Prince 2010). The study indicates that switching

to nontoxic, green propellants could ―enable safe/efficient launch operations,

infrastructure reduction, performance improvement, logistics reduction, and

potential commonality between main and auxiliary propellants” (NASA 2005).

In the cost chapter of the published ESAS report, the statement was made that the

estimates developed for the study did not consider ―opportunities for significant

improvements in operations costs‖. Their recommendation to decision-makers is

quoted below:

36

“Hypergols should be eliminated at an architectural level across the

CEV and LV elements. The need is to create highly operable systems that

improve over current systems operations in regard to costs, safety of ground

personnel, and overall responsiveness of the system to flight rate demands. A

generation of systems has evolved that has deferred such an evolution to nontoxic

systems. The elimination of hypergols would begin with newer elements such as

the CEV and the upper stage, and would continue as upgrades to SRB- and

SSME-related systems (power systems). Then, eventual elimination of hydraulic

systems and the implementation of simpler electric actuated systems would

become possible, leading to further operability improvements.” (NASA 2005)

While NASA’s internal trade analysis did not include environmental costs

over the life cycle, an extensive search of the literature was conducted to survey

other efforts to assess environmental impacts over the life cycle. Researchers at

ATK Thiokol Propulsion published research on understanding and mitigating the

environmental effects of rocket exhaust. This work was focused on examining

the terrestrial effects on the local launch site (determining the path and

concentration of chemicals found in the ground cloud that is formed during the

launch) and possible effects that the chlorine in the cloud could have on the

stratospheric ozone. This study resulted in a finding that the toxicity threat from

launch effluents was not likely to evoke range safety cancellation of a scheduled

launch. This study referenced several other independent reviews over the past

decade that investigated the atmospheric impact of rocket motors. Their findings

were similar – the local impacts from the exhaust are minor and manageable, and

the more global impact to the atmosphere is minimal (Bennett 2001).

Fick et. al. have published work on the industrial benefits of using a green

propellant, Hydrazinium Nitroformate (HNF), for satellite propulsion systems.

This work focused on operational and performance aspects – the handling

37

capability resulting from the less-toxic nature of the propellant, and the

envisioned reductions in cost that could result in manufacturing, testing and

operating with this propellant. This article states that considerable cost savings

will be realized due to more relaxed handling constraints than were required with

hydrazine--for example, because of its non-toxic nature, no special garments must

be worn during fueling. As much in many of the published articles, mention is

made of the cost savings in general that should be realized, but they do not

attempt to quantify those costs, and they point out that further work must be done

to understand these issues before these innovations can become a reality. Fick’s

article also identified the fact that parallel processing operations will be able to

continue in the same building where fueling operations are occurring (M. Fick

2001). This is an important point because traditionally all activities are shut down

in the surrounding area until fueling is complete when hazardous fuels like

hydrazine are being loaded.

Bombelli, et. al. have published work on the economic benefits of using

non-toxic fuels in spacecraft applications. This paper states that the European

Space Agency and others have pointed out that the use of green propellants can

provide cost saving opportunities in ground operations and in manufacturing. It

also states that while most publications provide results for a specific propellant

being tested at the thruster or component level, it was focused on quantifying cost

reduction potential resulting from ground operations and simplification of

hardware. It also identified areas ripe for cost reduction with ground support

equipment and Self-Contained Atmospheric Protective Ensemble (SCAPE) suit

38

requirements, but again does not attempt to examine the needs and requirements

over the full life cycle (Vittorio Bombelli 2003).

The community has identified a clear need for an understanding of the

environmental impacts and costs associated with propulsion systems. Only with

this understanding can truly informed decisions be made about significant

technologies of the future that have the potential to revolutionize the spacecraft

and launch industry.

METHODOLOGY

3.1. Proposed Methodology for Identifying Environmental Unaccounted for

Costs that Should be Included in Life Cycle Cost Analysis for Propellant

Selection Decisions

While there is a clear need for increased knowledge of the environmental

impacts and costs associated with propulsion systems, and it is widely understood

that some benefit should be expected from inclusion of this information in the life

cycle analysis, there is currently no guidance on which elements of environmental

cost impacts should be evaluated and included. Where should one begin? Which

elements can be quantified, and are significant enough to influence the outcome

of an analysis? The key theme that pervades all of the life cycle analyses

conducted in the transportation industry is an emphasis on the measurement and

reduction of greenhouse gas emissions, and the reduction of fuel consumption.

Environmentally-conscious life cycle automotive design engineers tend to focus

their research in areas like recyclability, ease of disassembly, and reusability in

39

conjunction with the typical emission reduction concerns (Tmiyama, Umeda and

Wallace June, 1997). Pioneers in the sustainable buildings industry consider

human health and productivity in addition to typical life cycle assessment

elements (initial investment costs, planned maintenance costs, repair and