Embed Size (px)

Citation preview

InfoTrack for

Unified Communications

Impact of Microsoft Lync on the

Enterprise Voice Market—2014

June 2014

A T3i Group Market Intelligence Program

Focused on Unified Communications

Enterprise and SMB Markets

IP Telephony

Systems

UC

Applications

Converged

Services

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 2 of 85

InfoTrack for Unified Communications: Impact of Microsoft Lync on the Enterprise Voice Market—2014

A T3i Group Series of Primary Research Studies on the Market Demand for Unified Communications Infrastructure and Applications

T3i Group LLC 210 Malapardis Road

Cedar Knolls, New Jersey 07927

USA

www.InfoTrackResearch.com

T3i Group provides market research, analysis and advisory services to the business communications

industry. It has clients in every global region and operates three lines of business:

InfoTrack monitors and analyzes shipment, revenue and market share data for global

enterprise telephony, unified communications, messaging and contact center shipments.

InfoTrack provides a comprehensive view of market sizing and installed base by technology and

manufacturer. InfoTrack for Unified Communications provides a demand based view of

customer adoption of unified communications applications over time.

Tactics provides easy access to detailed feature comparisons for business communications

products and services. Tactics’ databases enable users to review product and service feature

descriptions and information for over 1,000 telephony, collaboration and unified

communications products. The product profiles are presented in an easy-to-use, side-by-side

comparison tool.

Tarifica is the global leader in Telecom competitive pricing intelligence. Covering 450

operators in 130 countries, Tarifica’s database of PSTN, Leased Line, Ethernet and Wireless

voice and data service tariffs is the largest in the world.

Each of these programs is backed by a staff of expert industry consultants who provide clients with

insightful analysis, market briefings and advisory services.

For information on this report, or other T3iGroup products and services, please contact: Ken Dolsky at

[email protected], 973-602-0109.

Copyright ©1999-2014. All rights reserved. No part of this publication may be reproduced in any material form (including

photocopying) or stored in any medium by electronic means and whether or not transiently or incidentally to some other use of

this publication without the written prior permission of the copyright owner. Application for the copyright owner’s permission to

reproduce any part of this publication should be addressed to the contact and address referenced above.

Every effort has been taken to ensure the accuracy and completeness of information presented in this report. However, T3i

Group cannot accept liability for the consequences of action taken based on the information provided.

Copyright 2014 T3i Group All rights reserved June 2014 Page 3 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

TABLE of Contents

Page

LIST of EXHIBITS .............................................................................................................................................. 5

1. EXECUTIVE SUMMARY .............................................................................................................................. 8 How Have Plans to Trial Microsoft Lync Changed Since A Year Ago? ........................................................ 8 Do the Trials of Microsoft Lync Include Enterprise Voice? ........................................................................... 9 What Is the Anticipated Adoption Rate of Lync Enterprise Voice? ............................................................ 10 Why are Businesses Deploying Lync with Enterprise Voice? ..................................................................... 11 How Did Actual Costs Compare with Expectations for Implementation of Lync EV? .............................. 13 How Extensively Are Firms Planning to Deploy Lync Enterprise Voice? .................................................. 13 What is the Actual Penetration of Lync EV Licenses Within Employees of U.S. Enterprises? ................ 14 What is the Actual Penetration of Lync EV Licenses Within Employees of U.S. SMBs? ......................... 13 What is the Projected Penetration of Lync EV Licenses Over the Next Few Years? ................................ 11 Where Does Microsoft Rate Among Preferred Vendors for IP-PBXs? ........................................................ 15 Where Does Microsoft Rate Among Preferred Vendors for UC Apps? ........................................................ 18

2. INTRODUCTION AND METHODOLOGY .............................................................................................. 19 Scope of InfoTrack for Unified Communications (IUC) ............................................................................... 19 Program Leadership ....................................................................................................................................... 19 Primary Research Methodology .................................................................................................................... 19

3. ANALYSIS OF ENTERPRISE PLANS FOR MICROSOFT LYNC ENTERPRISE VOICE ............ 20 Demographics of Enterprise Survey Participants ........................................................................................ 20 Distribution of Participating Enterprises by Type of Decision Maker ....................................................... 21 Distribution of Participtaing Enterprises by Type of Industry ................................................................... 22 Enterprise Position on Microsoft Software Products and Services ............................................................. 23 Enterprise Status on Trialing Microsoft Lync .............................................................................................. 24 Percent of Enterprise Microsoft Lync Trials that Include Enterprise Voice .............................................. 25 Enterprise Perception of Microsoft Capabilities for Enterprise Voice ........................................................ 26 Performance of Enterprise Voice during Microsoft Lync Trials .................................................................. 27 Enterprise Perspective on Startup Costs of Implementing Lync with Enterprise Voice .......................... 28 Enterprise Perspective on Ongoing Costs of Implementing Lync with Enterprise Voice ......................... 29

Enterprise Plans for Deploying Lync with Enterprise Voice Beyond Trials .............................................. 30

Enterprises' Top Reasons for Deploying Lync with Enterprise Voice Beyond Trials ................................ 31

Factors that Fell Short of Enterprises’ Expectations in Deploying Lync with Enterprise Voice ............. 32

Enterprise Problems in Scaling Lync with Enterprise Voice ...................................................................... 33

Current Status of Licenses for Lync with Enterprise Voice—Medium Enterprise ................................... 34

Current Status of Licenses for Lync with Enterprise Voice—Large Enterprise ....................................... 35

Enterprise Projected Deployment of Licenses for Microsoft Lync with Enterprise Voice ......................... 36

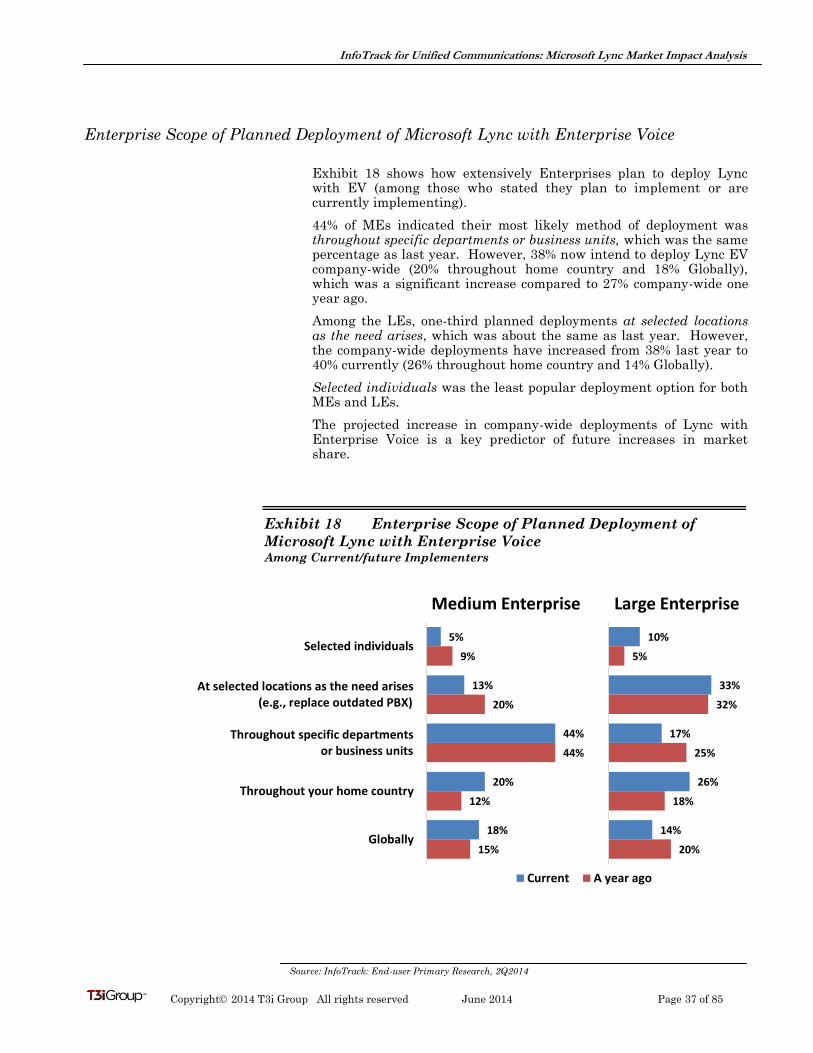

Enterprise Scope of Planned Deployment of Microsoft Lync with Enterprise Voice ................................. 37

Enterprise Organization Responsible for Decision to Deploy Lync with Enterprise Voice ....................... 38

Enterprise Ratings of Microsoft Dealers in Terms of Voice Expertise ....................................................... 39

Resources Used Extensively During Deployment of Lync with Enterprise Voice ..................................... 40

Enterprise Familiarity with Enhancements to Microsoft Lync .................................................................. 41

Perception of Whether Enhancements Meet Enterprise Needs .................................................................. 42

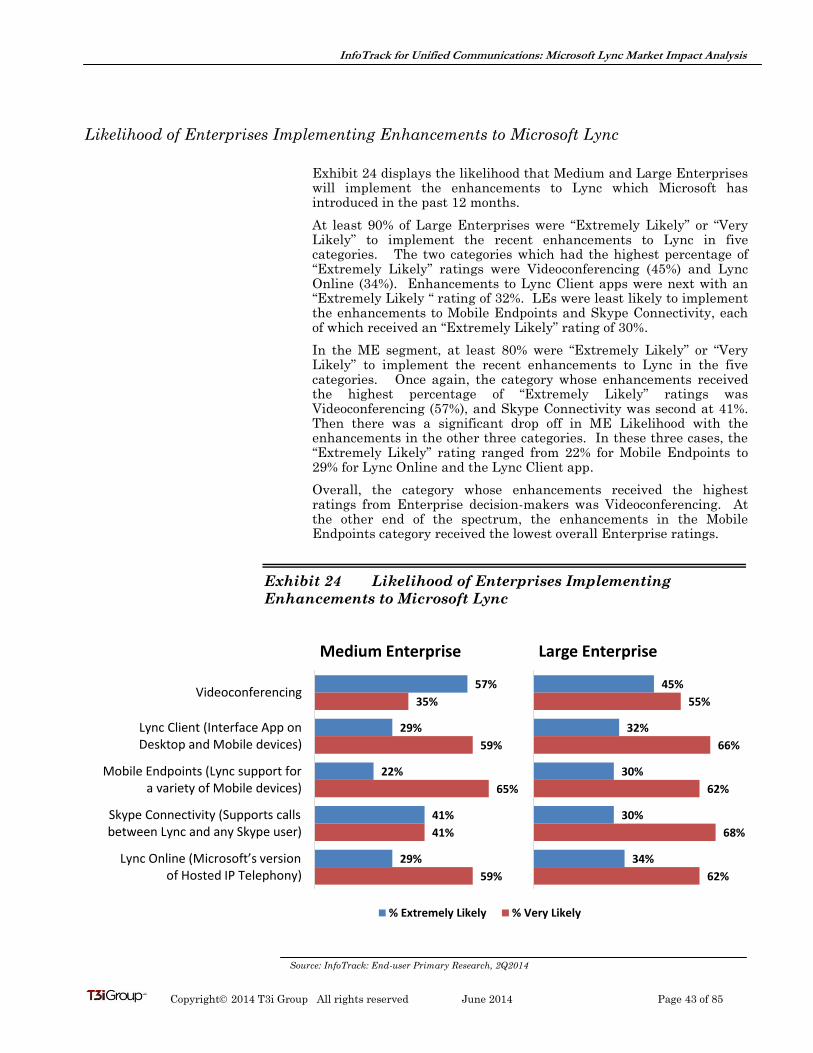

Likelihood of Enterprises Implementing Enhancements to Microsoft Lync .............................................. 43

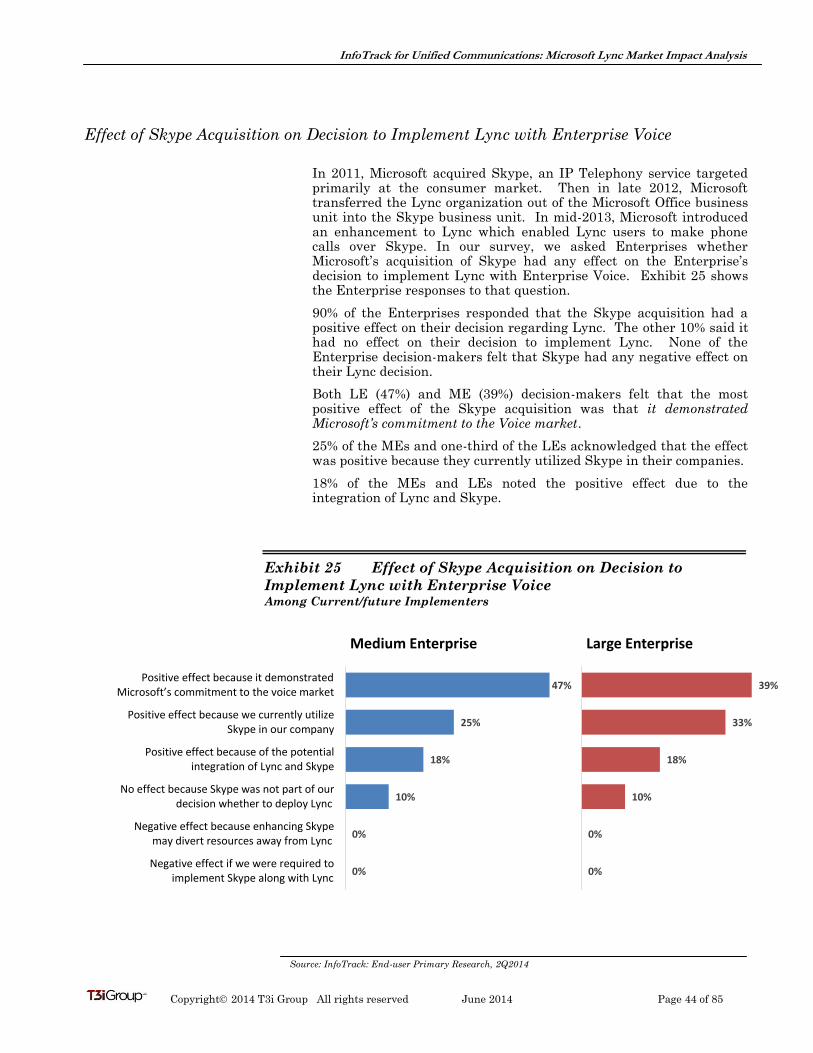

Effect of Skype Acquisition on Decision to Implement Lync with Enterprise Voice ................................. 44

Likelihood of Implementing Skype Functions during Next Few Years ...................................................... 45

Enterprise Plans for Replacing/Retaining Existing Telephony Systems During Lync Deployment ........ 46

Enterprise Distribution of Endpoints on Deployed Lync Systems with Enterprise Voice ........................ 47

Copyright 2014 T3i Group All rights reserved June 2014 Page 4 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

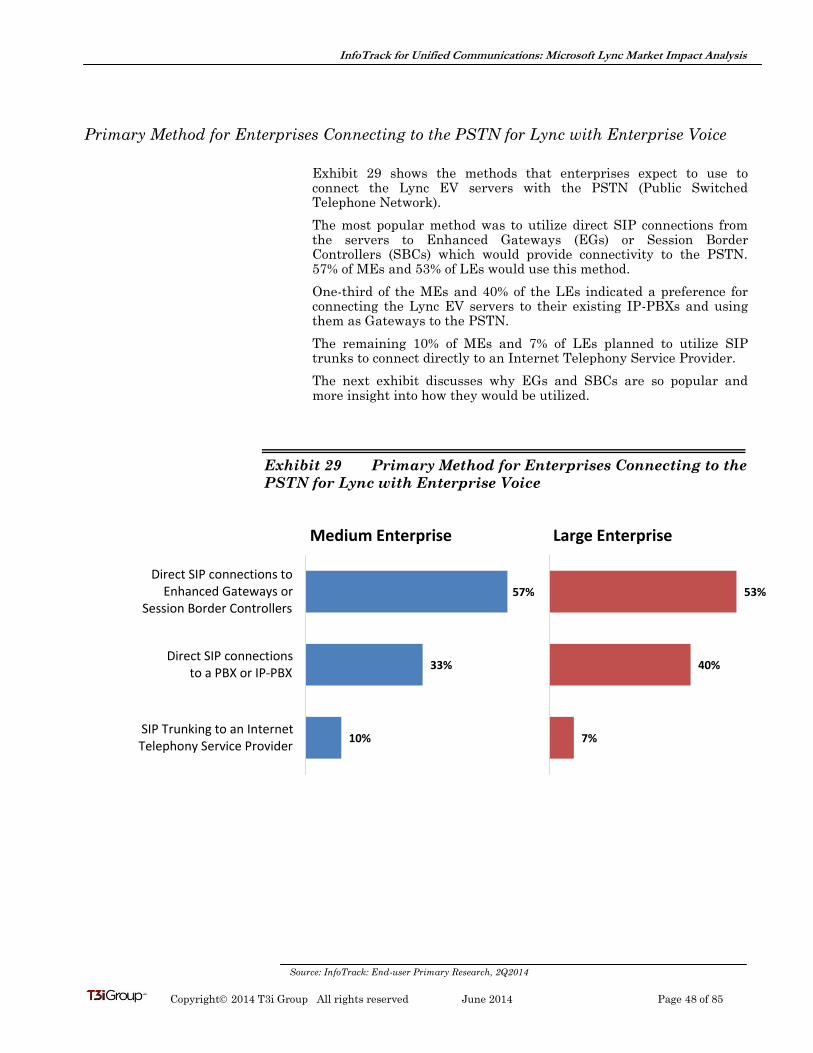

Primary Method for Enterprises Connecting to the PSTN for Lync with Enterprise Voice ..................... 48

Agreement Regarding Use of 3rd Party Session Border Controllers/Enhanced Gateways ........................ 49

Enterprise Plans for Voicemail on Lync with Enterprise Voice .................................................................. 50

Enterprise Preferred Vendors for IP-PBXs—Before Microsoft Entered the Enterprise Voice Market

vs. Currently ................................................................................................................................................... 51

Enterprise Preferred Vendors for UC Apps—Before Microsoft Entered the Enterprise Voice Market

vs. Currently ................................................................................................................................................... 52

4. ANALYSIS OF SMB PLANS FOR MICROSOFT LYNC ENTERPRISE VOICE .............................. 53 Demographics of SMB Survey Participants ................................................................................................. 53 Distribution of Participating SMBs by Type of Decision-Maker ................................................................. 54 Distribution of Participating SMBs by Industry .......................................................................................... 55 SMB Position on Microsoft Software Products and Services ...................................................................... 56 SMB Status on Trialing Microsoft Lync ....................................................................................................... 57 Percent of SMB Microsoft Lync Trials that Include Enterprise Voice ....................................................... 58 SMB Perception of Microsoft Capabilities for Enterprise Voice ................................................................. 59 Performance of Enterprise Voice during SMB Trial of Microsoft Lync ...................................................... 60 SMB Perspective on Startup Costs of Implementing Lync with Enterprise Voice .................................... 61 SMB Perspective on Ongoing Costs of Implementing Lync with Enterprise Voice ................................... 62 SMB Plans for Deploying Microsoft Lync with Enterprise Voice Beyond Trials ....................................... 63

SMB Top Reasons for Deploying Lync with Enterprise Voice Beyond Trials ............................................ 64

Factors that Fell Short of SMBs’ Expectations in Deploying Lync with Enterprise Voice ....................... 65

SMB Problems in Scaling Lync with Enterprise Voice ................................................................................ 66

Current Status of Licenses for Lync with Enterprise Voice—Small Business .......................................... 67

Current Status of Licenses for Lync with Enterprise Voice—Medium Busines ........................................ 68

Projected SMB Deployment of Licenses for Microsoft Lync with Enterprise Voice .................................. 69

Scope of Planned SMB Deployment of Microsoft Lync with Enterprise Voice ........................................... 70

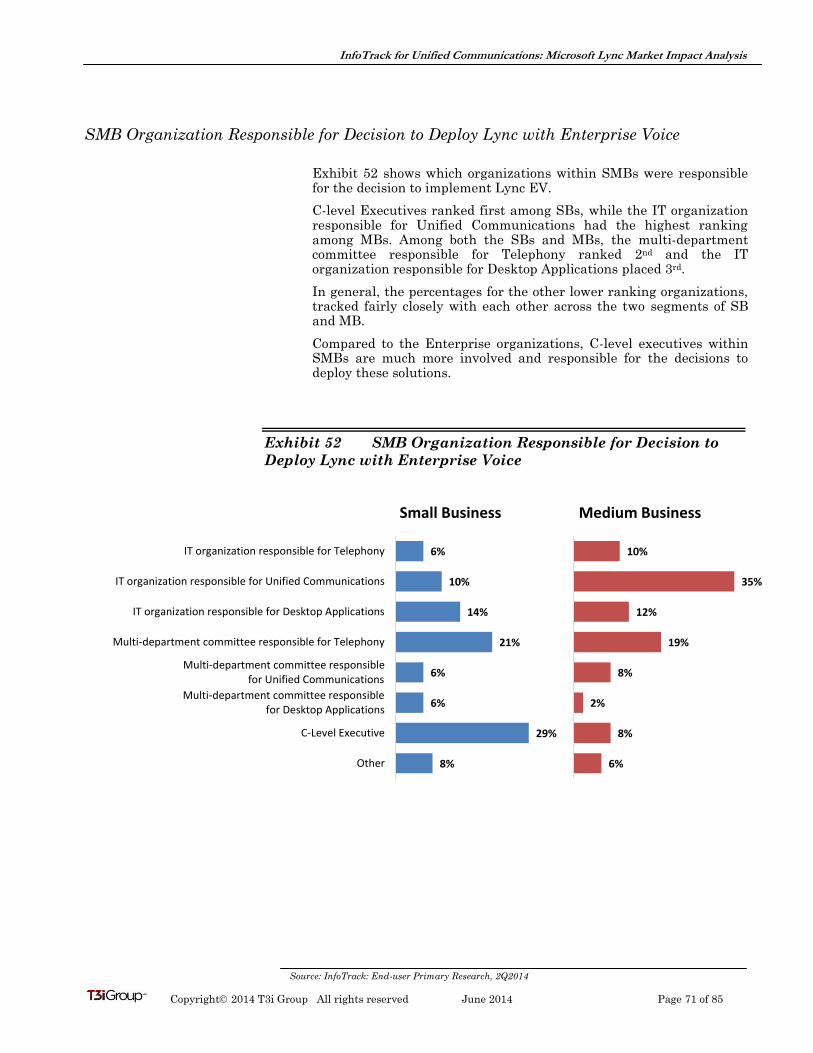

SMB Organization Responsible for Decision to Deploy Lync with Enterprise Voice ................................ 71

SMB Ratings of Microsoft Dealers in Terms of Voice Expertise ................................................................. 72

Resources Used Extensively During Deployment of Lync with Enterprise Voice ..................................... 73

SMB Familiarity with Enhancements to Microsoft Lync ............................................................................ 74

Perception of Whether Enhancements Meet SMB Needs ........................................................................... 75

Likelihood of SMBs Implementing Enhancements to Microsoft Lync ........................................................ 76

Effect of Skype Acquisition on SMB Decision to Implement Lync with Enterprise Voice ........................ 77

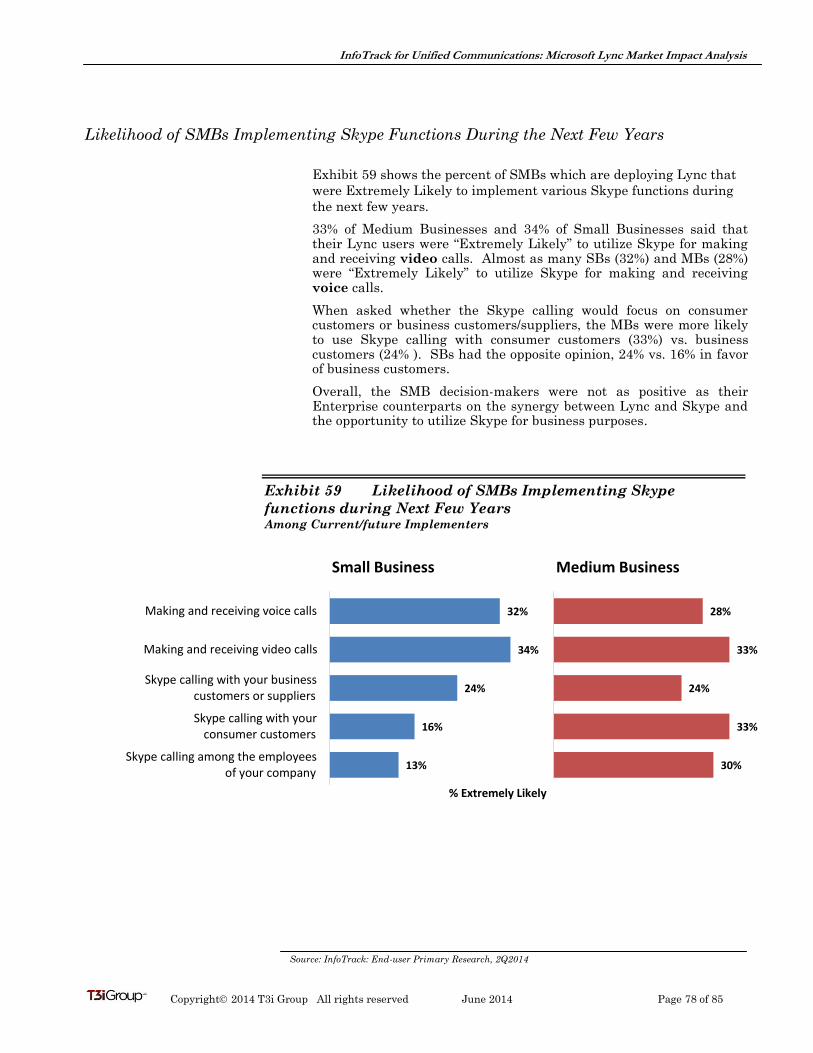

Likelihood of SMBs Implementing Skype functions during Next Few Years ............................................ 78

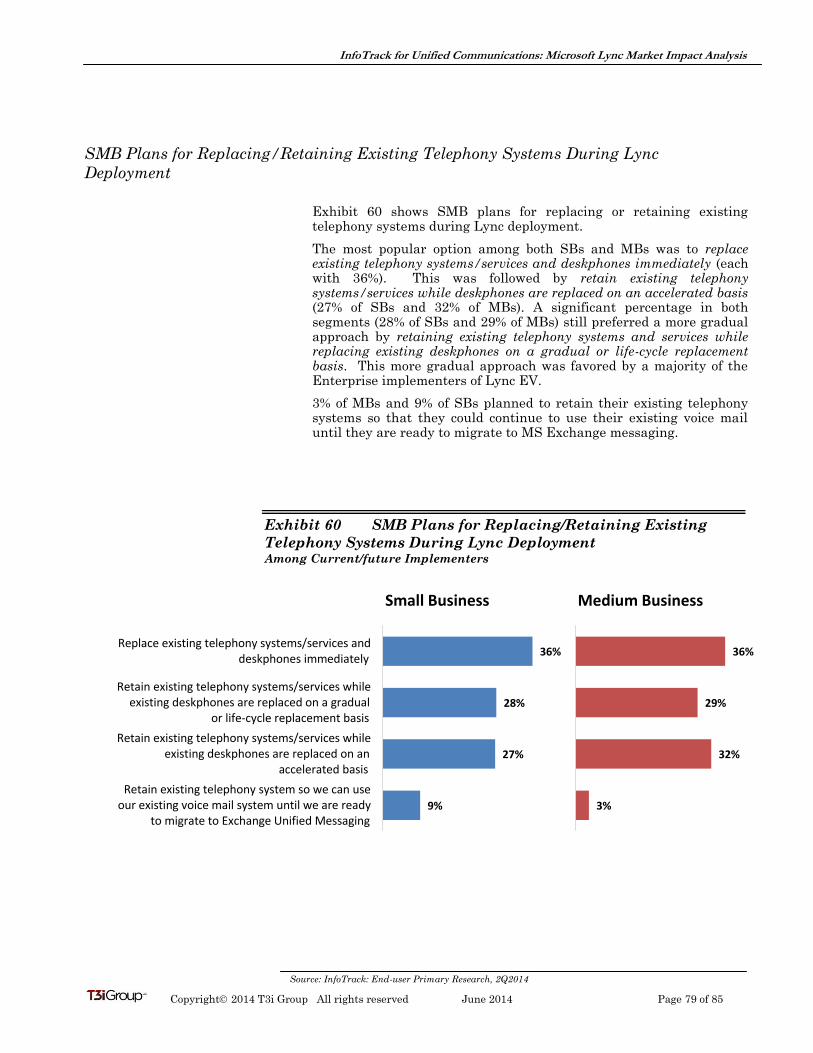

SMB Plans for Replacing/Retaining Existing Telephony Systems During Lync Deployment .................. 79

Distribution of Endpoints on SMB Deployed Lync Systems with Enterprise Voice .................................. 80

Primary Method for SMBs Connecting to the PSTN for Lync with Enterprise Voice ............................... 81

SMB Agreement on Use of 3rd Party Session Border Controllers/Enhanced Gateways ............................ 82

SMB Plans for Voicemail on Lync with Enterprise Voice ........................................................................... 83

SMB Preferred Vendor for IP-PBXs—Before Microsoft Entered the Enterprise Voice Market

vs. Currently ................................................................................................................................................... 84

SMB Preferred Vendor for UC Apps—Before Microsoft Entered the Enterprise Voice Market

vs. Currently ................................................................................................................................................... 85

Copyright 2014 T3i Group All rights reserved June 2014 Page 5 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

LIST of EXHIBITS

Page

Exhibit ES-1 Current Status of Microsoft Lync Trials vs. a Year Ago ............................................................ 8

Exhibit ES-2 Microsoft Lync Trials that Include Enterprise Voice vs. a Year Ago ........................................ 9

Exhibit ES-3 Current Plans for Deploying Lync with Enterprise Voice Beyond Trials vs. a Year Ago ...... 10

Exhibit ES-4 Top Reasons for Deploying Lync with Enterprise Voice Beyond Trials .................................. 11

Exhibit ES-5 Perspective on the Costs of Implementing Lync with Enterprise Voice ................................. 12

Exhibit ES-6 Scope of Planned Deployment of Lync Enterprise Voice vs. a Year Ago ................................. 13

Exhibit ES-7 Penetration of Lync EV Licenses in the Enterprise Market vs. a Year Ago ........................... 14

Exhibit ES-8 Penetration of Lync EV Licenses in the SMB Market vs. a Year Ago ..................................... 15

Exhibit ES-9 Projected Penetration of Lync EV Licenses ............................................................................... 16

Exhibit ES-10 Preferred Vendor for IP-PBXs – Before Microsoft Entered the Market

vs. Currently ................................................................................................................................ 17

Exhibit ES-11 Preferred Vendor for UC Apps – Before Microsoft Entered the Market

vs. Currently ................................................................................................................................ 18

Exhibit 1 Distribution of Participating Enterprises by Size..................................................................... 20

Exhibit 2 Distribution of Participating Enterprises by Type of Decision-Maker .................................... 21

Exhibit 3 Distribution of Participating Enterprises by Type of Industry ................................................ 22

Exhibit 4 Enterprise Position on Microsoft Software Products and Services.......................................... 23

Exhibit 5 Current Status of Enterprise Trials of Microsoft Lync ............................................................ 24

Exhibit 6 Percent of Enterprise Microsoft Lync Trials that Include Enterprise Voice........................... 25

Exhibit 7 Enterprise Perception of Microsoft Capabilities for Enterprise Voice .................................... 26

Exhibit 8 Performance of Enterprise Voice during Microsoft Lync Trials .............................................. 27

Exhibit 9 Enterprise Perspective on Startup Costs of Implementing Lync with Enterprise Voice ....... 28

Exhibit 10 Enterprise Perspective on Ongoing Costs of Implementing Lync with Enterprise Voice ...... 29

Exhibit 11 Enterprise Plans for Deploying Lync with Enterprise Voice Beyond Trials ........................... 30

Exhibit 12 Enterprises’ Top Reasons for Deploying Lync with Enterprise Voice Beyond Trials ............. 31

Exhibit 13 Factors that Fell Short of Enterprises’ Expectations in Deploying Lync with EV ................. 32

Exhibit 14 Enterprise Problems in Scaling Lync with Enterprise Voice ................................................... 33

Exhibit 15 Current Status of Licenses for Lync with Enterprise Voice—Medium Enterprise ................ 34

Exhibit 16 Current Status of Licenses for Lync with Enterprise Voice—Large Enterprise .................... 35

Exhibit 17 Enterprise Projected Deployment of Licenses for Microsoft Lync with Enterprise Voice ...... 36

Exhibit 18 Enterprise Scope of Planned Deployment of Microsoft Lync with Enterprise Voice .............. 37

Exhibit 19 Enterprise Scope of Planned Deployment of Microsoft Lync with Enterprise Voice .............. 38

Exhibit 20 Enterprise Ratings of Microsoft Dealers in Terms of Voice Expertise .................................... 39

Exhibit 21 Resources Used Extensively During Deployment of Lync with Enterprise Voice .................. 40

Exhibit 22 Enterprise Familiarity with Enhancements to Microsoft Lync ............................................... 41

Exhibit 23 Perception of Whether Enhancements Meet Enterprise Needs ............................................... 42

Copyright 2014 T3i Group All rights reserved June 2014 Page 6 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Exhibit 24 Likelihood of Enterprises Implementing Enhancements to Microsoft Lync ........................... 43

Exhibit 25 Effect of Skype Acquisition on Decision to Implement Lync with Enterprise Voice .............. 44

Exhibit 26 Likelihood of Implementing Skype functions during Next Few Years .................................... 45

Exhibit 27 Enterprise Plans for Replacing/Retaining Existing Telephony Systems During Lync

Deployment .................................................................................................................................. 46

Exhibit 28 Enterprise Distribution of Endpoints on Deployed Lync Systems with Enterprise Voice ..... 47

Exhibit 29 Primary Method for Enterprises Connecting to the PSTN for Lync with Enterprise Voice .. 48

Exhibit 30 Agreement Regarding Use of 3rd Party Session Border Controllers/Enhanced Gateways .... 49

Exhibit 31 Enterprise Plans for Voicemail on Lync with Enterprise Voice............................................... 50

Exhibit 32 Enterprise Preferred Vendors for IP-PBXs—Before Microsoft Entered the Enterprise

Voice Market vs. Currently ........................................................................................................ 51

Exhibit 33 Enterprise Preferred Vendors for UC Apps—Before Microsoft Entered the Enterprise

Voice Market vs. Currently ........................................................................................................ 52

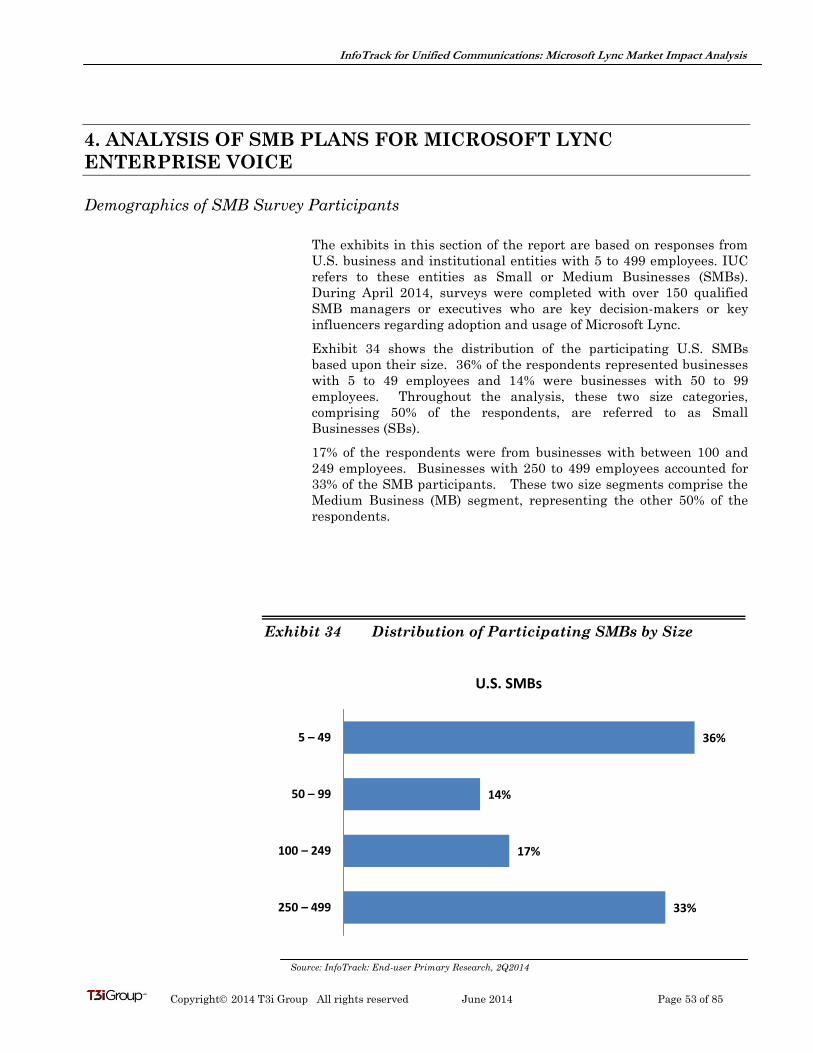

Exhibit 34 Distribution of Participating SMBs by Size .............................................................................. 53

Exhibit 35 Distribution of Participating SMBs by Type of Decision-Maker ............................................. 54

Exhibit 36 Distribution of Participating SMBs by Industry....................................................................... 55

Exhibit 37 SMB Position on Microsoft Software Products and Services ................................................... 56

Exhibit 38 SMB Status on Trialing Microsoft Lync .................................................................................... 57

Exhibit 39 Percent of SMB Microsoft Lync Trials that Include Enterprise Voice .................................... 58

Exhibit 40 SMB Perception of Microsoft Capabilities for Enterprise Voice .............................................. 59

Exhibit 41 Performance of Enterprise Voice during SMB Trial of Microsoft Lync ................................... 60

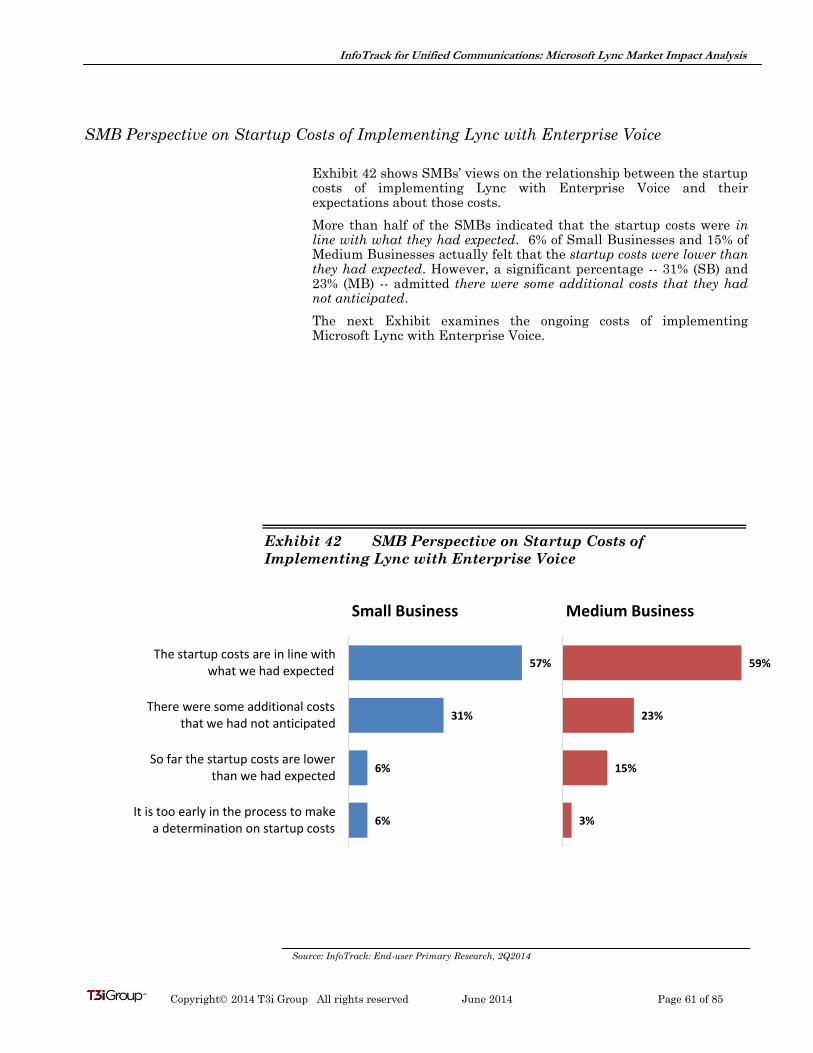

Exhibit 42 SMB Perspective on Startup Costs of Implementing Lync with Enterprise Voice ................ 61

Exhibit 43 SMB Perspective on Ongoing Costs of Implementing Lync with Enterprise Voice ............... 62

Exhibit 44 SMB Plans for Deploying Microsoft Lync with Enterprise Voice Beyond Trials ................... 63

Exhibit 45 SMB Top Reasons for Deploying Lync with Enterprise Voice Beyond Trials ......................... 64

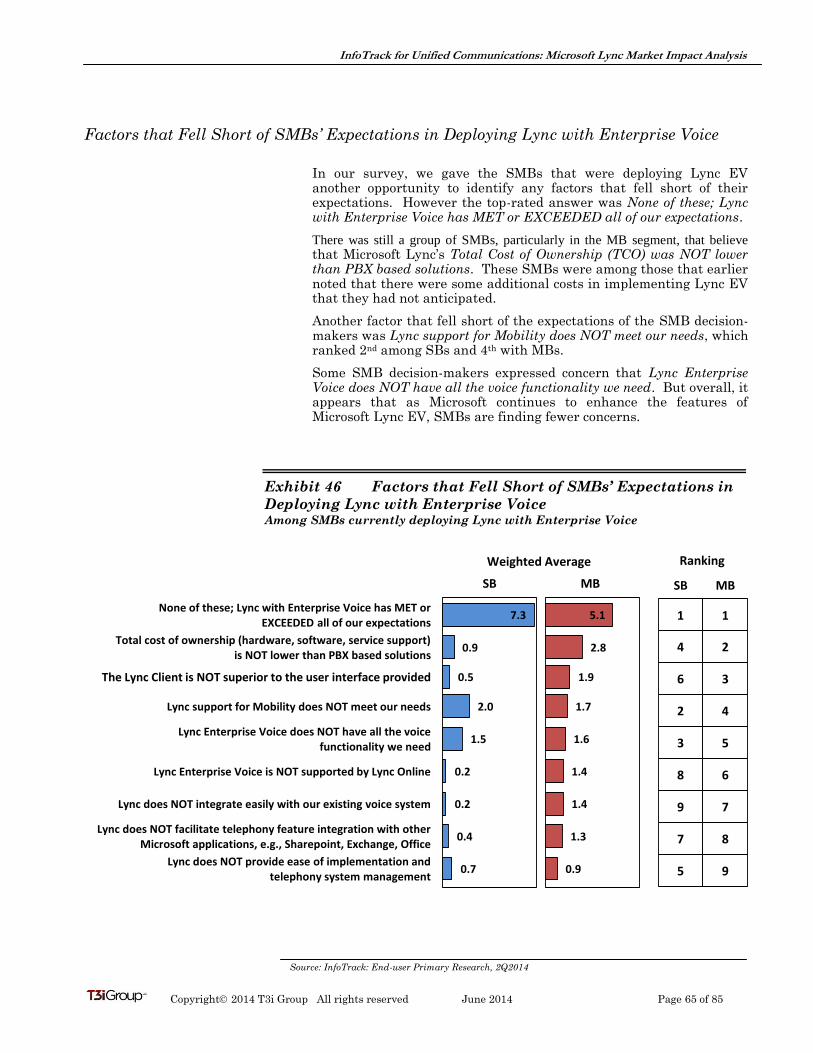

Exhibit 46 Factors that Fell Short of SMBs’ Expectations in Deploying Lync with Enterprise Voice .... 65

Exhibit 47 SMB Problems in Scaling Lync with Enterprise Voice ............................................................ 66

Exhibit 48 Current Status of Licenses for Lync with Enterprise Voice—Small Business ....................... 67

Exhibit 49 Current Status of Licenses for Lync with Enterprise Voice—Medium Business ................... 68

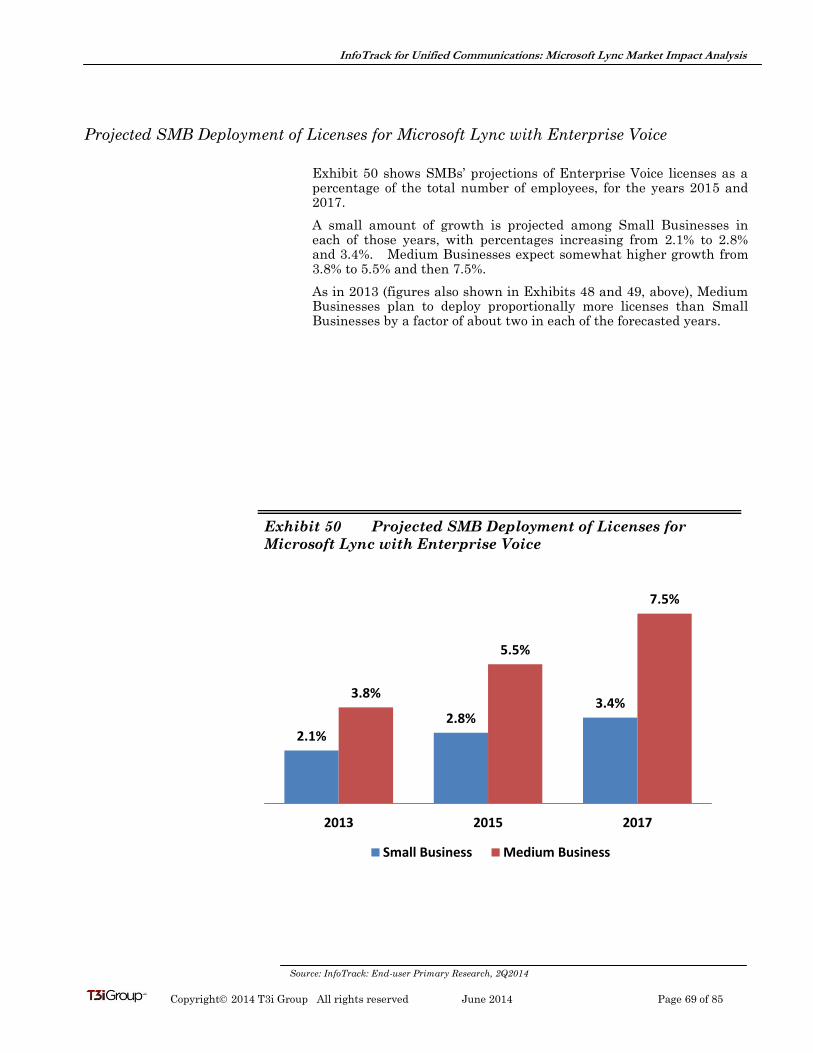

Exhibit 50 Projected SMB Deployment of Licenses for Microsoft Lync with Enterprise Voice ............... 69

Exhibit 51 Scope of Planned SMB Deployment of Microsoft Lync with Enterprise Voice ....................... 70

Exhibit 52 SMB Organization Responsible for Decision to Deploy Lync with Enterprise Voice ............. 71

Exhibit 53 SMB Ratings of Microsoft Dealers in Terms of Voice Expertise .............................................. 72

Exhibit 54 Resources Used Extensively During Deployment of Lync with Enterprise Voice .................. 73

Exhibit 55 SMB Familiarity with Enhancements to Microsoft Lync ......................................................... 74

Exhibit 56 Perception of Whether Enhancements Meet SMB Needs ........................................................ 75

Exhibit 57 Likelihood of SMBs Implementing Enhancements to Microsoft Lync .................................... 76

Exhibit 58 Effect of Skype Acquisition on SMB Decision to Implement Lync with Enterprise Voice ..... 77

Exhibit 59 Likelihood of SMBs Implementing Skype functions during Next Few Years ......................... 78

Exhibit 60 SMB Plans for Replacing/Retaining Existing Telephony Systems During Lync Deployment79

Copyright 2014 T3i Group All rights reserved June 2014 Page 7 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Exhibit 61 Distribution of Endpoints on SMB Deployed Lync Systems with Enterprise Voice .............. 80

Exhibit 62 Primary Method for SMBs Connecting to the PSTN for Lync with Enterprise Voice ........... 81

Exhibit 63 SMB Agreement on Use of 3rd Party Session Border Controllers/Enhanced Gateways ........ 82

Exhibit 64 SMB Plans for Voicemail on Lync with Enterprise Voice ........................................................ 83

Exhibit 65 SMB Preferred Vendor for IP-PBXs—Before Microsoft Entered the

Enterprise Voice Market vs. Currently ..................................................................................... 84

Exhibit 66 SMB Preferred Vendor for UC Apps—Before Microsoft Entered the

Enterprise Voice Market vs. Currently ..................................................................................... 85

Copyright 2014 T3i Group All rights reserved June 2014 Page 8 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

38%

34%

23%

5%

14%

28%

52%

6%

Have completed trial

Currently conducting trial

Planning to conduct trial

No plans to conduct trial

Enterprise

Current A year ago

16%

18%

46%

20%

8%

21%

52%

19%

Have completed trial

Currently conducting trial

Planning to conduct trial

No plans to conduct trial

SMB

Current A year ago

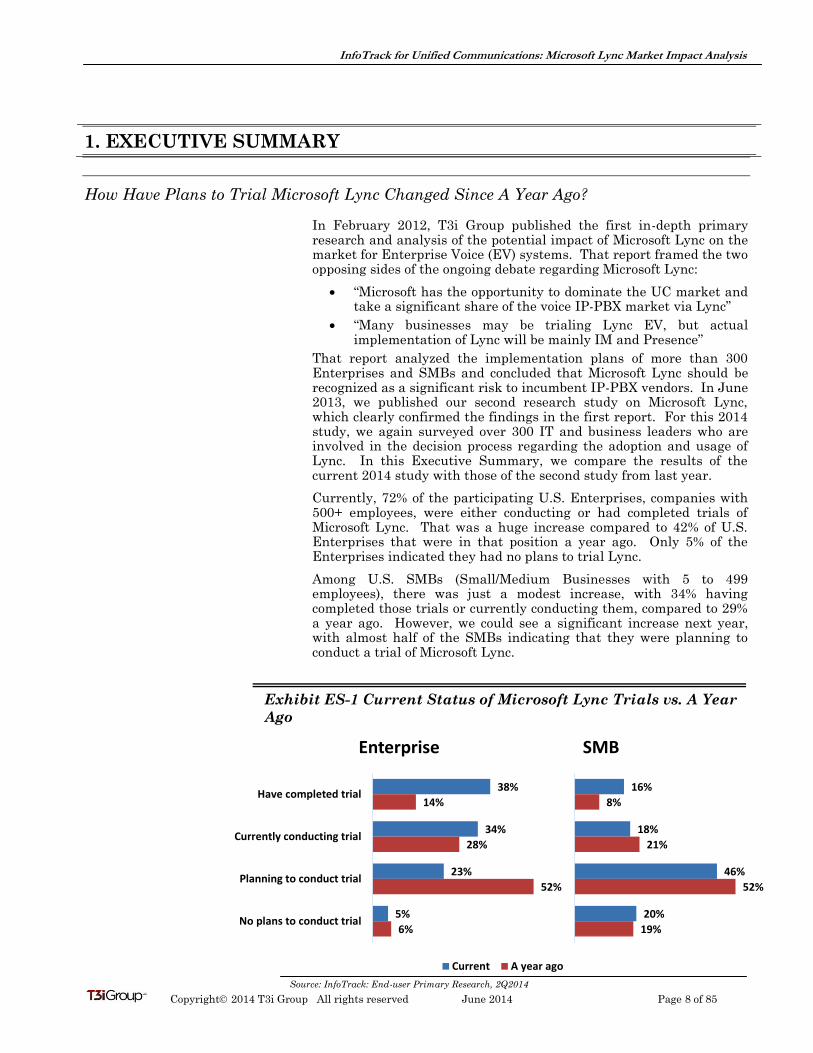

1. EXECUTIVE SUMMARY

How Have Plans to Trial Microsoft Lync Changed Since A Year Ago? In February 2012, T3i Group published the first in-depth primary research and analysis of the potential impact of Microsoft Lync on the market for Enterprise Voice (EV) systems. That report framed the two opposing sides of the ongoing debate regarding Microsoft Lync:

“Microsoft has the opportunity to dominate the UC market and take a significant share of the voice IP-PBX market via Lync”

“Many businesses may be trialing Lync EV, but actual implementation of Lync will be mainly IM and Presence”

That report analyzed the implementation plans of more than 300 Enterprises and SMBs and concluded that Microsoft Lync should be recognized as a significant risk to incumbent IP-PBX vendors. In June 2013, we published our second research study on Microsoft Lync, which clearly confirmed the findings in the first report. For this 2014 study, we again surveyed over 300 IT and business leaders who are involved in the decision process regarding the adoption and usage of Lync. In this Executive Summary, we compare the results of the current 2014 study with those of the second study from last year.

Currently, 72% of the participating U.S. Enterprises, companies with 500+ employees, were either conducting or had completed trials of Microsoft Lync. That was a huge increase compared to 42% of U.S. Enterprises that were in that position a year ago. Only 5% of the Enterprises indicated they had no plans to trial Lync.

Among U.S. SMBs (Small/Medium Businesses with 5 to 499 employees), there was just a modest increase, with 34% having completed those trials or currently conducting them, compared to 29% a year ago. However, we could see a significant increase next year, with almost half of the SMBs indicating that they were planning to conduct a trial of Microsoft Lync.

Exhibit ES-1 Current Status of Microsoft Lync Trials vs. A Year

Ago

Source: InfoTrack: End-user Primary Research, 2Q2014

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 9 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

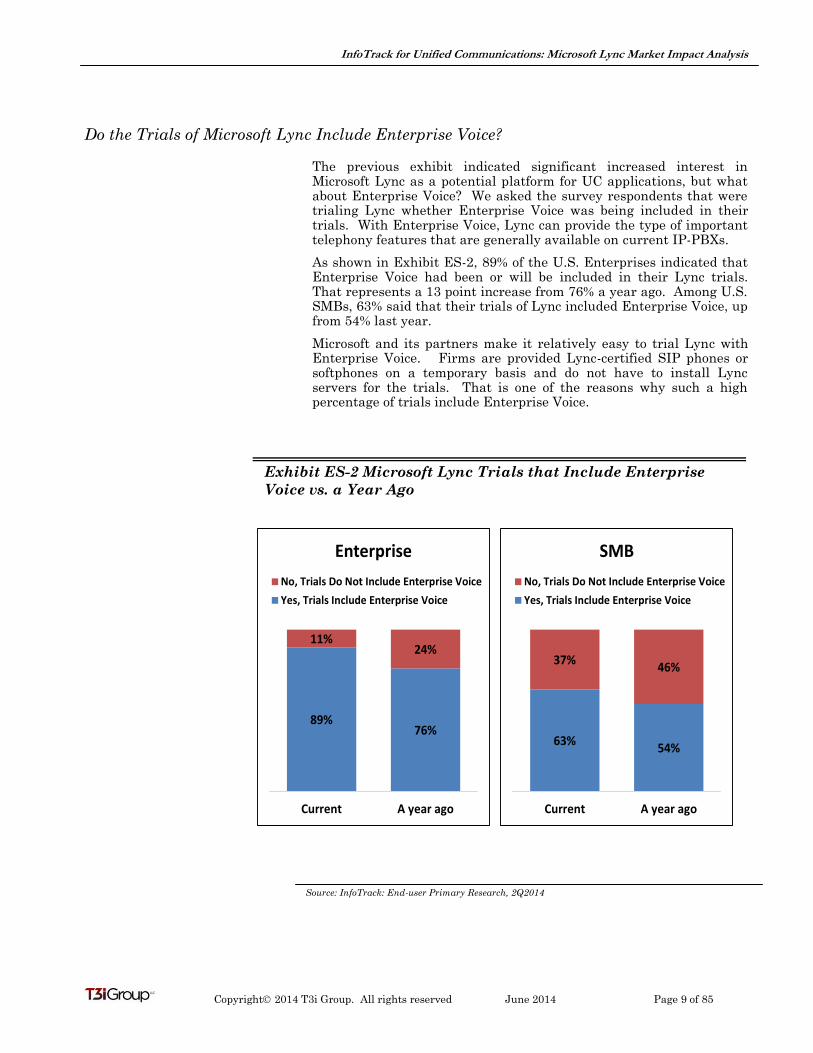

Do the Trials of Microsoft Lync Include Enterprise Voice?

The previous exhibit indicated significant increased interest in Microsoft Lync as a potential platform for UC applications, but what about Enterprise Voice? We asked the survey respondents that were trialing Lync whether Enterprise Voice was being included in their trials. With Enterprise Voice, Lync can provide the type of important telephony features that are generally available on current IP-PBXs.

As shown in Exhibit ES-2, 89% of the U.S. Enterprises indicated that Enterprise Voice had been or will be included in their Lync trials. That represents a 13 point increase from 76% a year ago. Among U.S. SMBs, 63% said that their trials of Lync included Enterprise Voice, up from 54% last year.

Microsoft and its partners make it relatively easy to trial Lync with Enterprise Voice. Firms are provided Lync-certified SIP phones or softphones on a temporary basis and do not have to install Lync servers for the trials. That is one of the reasons why such a high percentage of trials include Enterprise Voice.

Exhibit ES-2 Microsoft Lync Trials that Include Enterprise

Voice vs. a Year Ago

89%76%

11%24%

Current A year ago

Enterprise

No, Trials Do Not Include Enterprise Voice

Yes, Trials Include Enterprise Voice

63%54%

37%46%

Current A year ago

SMB

No, Trials Do Not Include Enterprise Voice

Yes, Trials Include Enterprise Voice

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 10 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

What Is the Anticipated Adoption Rate of Lync Enterprise Voice?

The decision-makers in this research were also asked about their plans for actually deploying Lync with Enterprise Voice (EV). Exhibit ES-3 depicts their responses.

Last year, 15% of U.S. Enterprises had begun to deploy Lync with Enterprise Voice beyond the trial stage, and another 44% were in the planning stages of deployment. It appears that more than half of those that were in the planning stages last year have actually begun their deployment, thus increasing the current total to 44%, tripling the 15% from a year ago. Only 21% of the Enterprises were either waiting for the results of their trials before deciding whether to deploy Lync EV or had no plans to deploy. That represents a 20 point reduction in the percent of “Undecideds” or “No Plans” from last year. Only 4% of the U.S. Enterprises we surveyed indicated that they had no plans to implement Microsoft Lync Enterprise Voice.

The percent of SMBs that were actually deploying Lync EV beyond trials also increased in the past year, but only from 9% to 12%. 31% of SMBs were currently planning to deploy Lync with Enterprise Voice, up from 27% last year. 57% were either undecided awaiting trial results, or don’t plan to deploy, compared to 64% a year ago.

It is extremely significant that almost half of U.S. Enterprises have begun to deploy Lync EV. This is the market segment in which Microsoft has traditionally developed the strongest relationships with IT decision-makers. These results show that those relationships are paying off.

Exhibit ES-3 Current Plans for Deploying Lync with Enterprise

Voice Beyond Trials vs. A Year Ago

44%

35%

17%

4%

15%

44%

34%

7%

Currently deploying

Planning to deploy

Undecided; depends on results of trial

No plans to deploy Microsoft Lync for Enterprise Voice

Enterprise

Current A year ago

12%

31%

43%

14%

9%

27%

48%

16%

Currently deploying

Planning to deploy

Undecided; depends on results of trial

No plans to deploy Microsoft Lync for Enterprise Voice

SMB

Current A year ago

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 11 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

Why are Businesses Deploying Lync with Enterprise Voice? We asked the decision-makers who were currently deploying Lync EV or planning to deploy, to rank the top reasons for that decision. The results are shown in Exhibit ES-4.

The number one reason among both Enterprises and SMBs was that Lync Enterprise Voice’s total cost of ownership (TCO) is lower than PBX based solutions. This was also the top reason provided in last year’s survey responses. Microsoft prices Lync very attractively for firms that use other Microsoft applications. Licenses for access to Lync are bundled in the Enterprise CAL Suite with licenses of other popular Microsoft applications including Exchange, SharePoint and Windows. Firms who want to add Enterprise Voice can upgrade for an additional incremental charge. Microsoft’s Enterprise Agreement offers volume pricing discounts for licenses, as well.

The effectiveness of Microsoft’s bundling strategy is reflected in the second reason both Enterprises and SMBs gave for moving to Lync Enterprise Voice -- Facilitates voice feature integration with other Microsoft applications.

The next three reasons demonstrate the effectiveness of Microsoft’s incremental pricing strategy: We have already adopted Microsoft Lync for IM and Presence We have already adopted Microsoft Lync for Web Conferencing Lync EV is a natural extension of our commitment to Lync for UC

The Microsoft IP-PBX competitors may argue that Enterprises are mainly implementing Microsoft Lync just as a platform for UC, simply because they were already using Microsoft for IM or web conferencing. But IP-PBX vendors face an even greater risk if Enterprises adopt Lync for UC, because Exhibit ES-4 shows that Enterprises will implement Microsoft Lync as a platform for Enterprise Voice, largely because they had already begun using Microsoft Lync for UC.

Exhibit ES-4 Top Reasons for Deploying Lync with Enterprise

Voice Beyond Trials Among Enterprises & SMBs Deploying/Planning to Deploy Lync with Enterprise Voice

Top Reasons ENT SMB

Total cost of ownership (hardware, software, service support) is lower than

PBX based solutions1 1

Facilitates voice feature integration with other Microsoft applications, e.g.,

Sharepoint, Exchange, Office2 2

We have already adopted Microsoft Lync for IM and Presence 3 4

We have already adopted Microsoft Lync for Web Conferencing 4 3

Lync Enterprise Voice is a natural extension of our commitment to Microsoft

Lync for UC5 5

The Lync Client is superior to the user interface provided by other UC vendors 6 6

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 12 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

How Did Actual Costs Compare with Expectations for Implementation of Lync EV?

In the preceding Exhibit, Enterprises and SMBs both indicated that their number one reason for implementing Microsoft Lync for Enterprise Voice was because its Total Cost of Ownership (TCO) was lower than PBX based solutions. But were they really considering all of the costs or were they focused primarily on start-up costs? In the early stages, the costs may be lower because much of the initial cost of Lync EV was an incremental extension to the investment that they had already made in implementing a broader suite of Microsoft applications.

In this year’s survey we asked the respondents to distinguish between start-up costs and ongoing costs. Half of the Enterprises that were currently deploying Lync EV or preparing to deploy it indicated that the start-up costs were in line with what they had expected. Almost as many, 42%, said the same thing about ongoing costs. One-third of the Enterprises admitted that there were some additional ongoing costs that they had not anticipated. But that was only slightly more than the 28% who said the same thing about the start-up costs. 19% of Enterprises felt that the ongoing costs were actually lower than they had expected, versus 15% who felt that way about start-up costs.

A significant percentage of Enterprises encountered some surprises with both the ongoing costs of deploying Lync EV and the start-up costs. Interestingly, the attitude of SMBs toward ongoing costs vs. start-up costs was almost identical to that of their Enterprise counterparts. However, despite these unanticipated additional costs, the scope of deployment of Microsoft Lync with Enterprise Voice is continuing to increase, as shown in the next exhibit.

Exhibit ES-5 Perspective on the Costs of Implementing Lync

with Enterprise Voice

50%

28%

15%

7%

42%

32%

19%

7%

The costs are in line with what we had expected

There were some additional costs that we had not anticipated

So far the costs are lower than we had expected

It is too early in the process to make a determination on costs

Enterprise

Startup Costs Ongoing costs

58%

26%

12%

4%

55%

31%

14%

0%

The costs are in line with what we had expected

There were some additional costs that we had not anticipated

So far the costs are lower than we had expected

It is too early in the process to make a determination on costs

SMB

Startup Costs Ongoing costs

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 13 of 85

7%

24%

29%

24%

16%

7%

27%

34%

15%

17%

Selected individuals

At selected locations as the need arises (e.g., replace outdated PBX)

Throughout specific departments or business units

Throughout your home country

Globally

Enterprise

Current A year ago

14%

22%

31%

33%

0%

23%

17%

28%

25%

7%

Selected individuals

At selected locations as the need arises (e.g., replace outdated PBX)

Throughout specific departments or business units

Throughout your home country

Globally

SMB

Current A year ago

How Extensively Are Firms Planning to Deploy Lync Enterprise Voice?

We asked the firms that were deploying or planned to deploy Lync Enterprise Voice to characterize the scope of their deployment from an array of five approaches that range from enabling selected individuals to full-scale global deployment. Among the current/future implementers in last year’s study, 32% of those Enterprises were planning a company-wide deployment of Lync Enterprise Voice that would cover either their U.S. operations (15%) or their entire global Enterprise (17%). That represented 19% of all Enterprises that took part in last year’s study. Certainly, that could have a substantial impact on the PBX market both within the U.S. and globally.

Since then, Enterprises have begun to deploy Lync 2013 which offered significant improvements over Lync 2010. As a result, the percent of projected company-wide deployments among the current/future implementers has jumped to 40% (24% nationwide and 16% globally). Measured against a base of 79% of Enterprises which are currently deploying or planning to deploy, that represented 32% of all Enterprises that participated in this year’s study.

33% of U.S. SMBs that are currently deploying or plan to deploy Lync Enterprise Voice expect nation-wide or global deployment. That is just one point higher than the 32% of the SMBs in last year’s study. These SMBs planning company-wide deployment represent 14% of all SMBs that participated in this study, up slightly from 12% of SMBs last year.

In the 2013 InfoTrack for Unified Communications (IUC) forecast report, we estimated that Microsoft had achieved a 14.9% market share of IP Telephony shipments to U.S. Enterprises in 2012 and 3.6% share for SMBs. Based on the results of this study, we can expect to see a significant increase in Microsoft’s Enterprise market share for 2013, with perhaps a flat or declining share in the SMB market.

Exhibit ES-6 Scope of Planned Deployment of Lync EV vs. A

Year Ago Among Current/Future Implementers

Source: InfoTrack: End-user Primary Research, 2Q2014

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 14 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

What is the Actual Penetration of Lync EV Licenses Within All Employees of U.S.

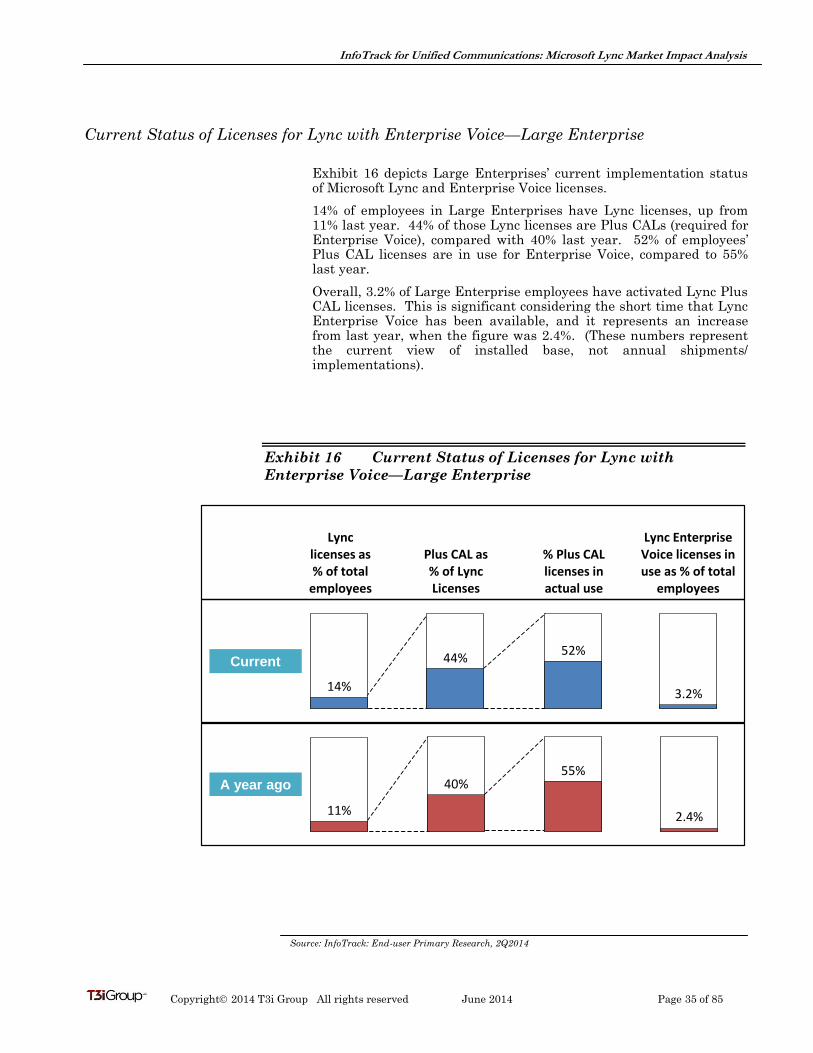

Enterprises? To measure the penetration of Lync Enterprise Voice licenses that are actually in use in the U.S. Enterprise segment of the market, we asked the decision-makers the following series of questions about the number and status of their Lync licenses in the U.S.:

How many total Lync licenses does your company have? Of those, how many are Plus CAL for Enterprise Voice? What % of those are in actual use by employees? What is your company’s total number of employees in the U.S.?

As noted earlier, Enterprises may have a number of Lync licenses that were bundled as part of Microsoft’s Enterprise CAL Suite of licenses. In this year’s study, the total Lync licenses represented 15% of their employees in the U.S., up sharply from 11% a year ago. 45% of those licenses were Plus CAL for Enterprise Voice, somewhat more than last year. The percent of Plus CAL licenses that had been activated for actual use was also about the same as last year, 51% vs. 54%. These active Plus CAL licenses represent 3.4% of total U.S. Enterprise employees, a significant increase from 2.5% in last year’s study.

Exhibit ES-7 Penetration of Lync EV Licenses in the Enterprise

Market vs. a Year Ago

Current

15%

45% 51%

3.4%

11%

42%54%

2.5%

A year ago

Lync licenses as % of total

employees

Plus CAL as % of Lync Licenses

% Plus CAL licenses in actual use

Lync Enterprise Voice licenses in use as % of total

employees

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 15 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

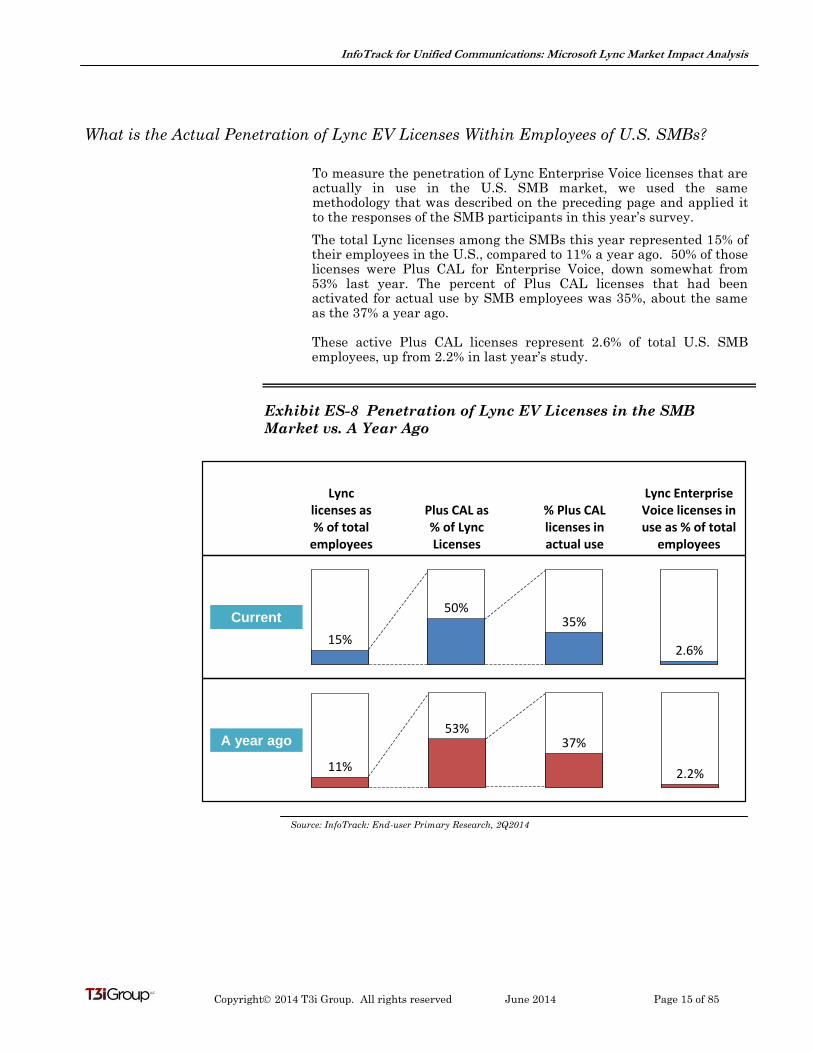

What is the Actual Penetration of Lync EV Licenses Within Employees of U.S. SMBs?

To measure the penetration of Lync Enterprise Voice licenses that are actually in use in the U.S. SMB market, we used the same methodology that was described on the preceding page and applied it to the responses of the SMB participants in this year’s survey.

The total Lync licenses among the SMBs this year represented 15% of their employees in the U.S., compared to 11% a year ago. 50% of those licenses were Plus CAL for Enterprise Voice, down somewhat from 53% last year. The percent of Plus CAL licenses that had been activated for actual use by SMB employees was 35%, about the same as the 37% a year ago. These active Plus CAL licenses represent 2.6% of total U.S. SMB employees, up from 2.2% in last year’s study.

Exhibit ES-8 Penetration of Lync EV Licenses in the SMB

Market vs. A Year Ago

Current

15%

50%35%

2.6%

11%

53%37%

2.2%

A year ago

Lync licenses as % of total

employees

Plus CAL as % of Lync Licenses

% Plus CAL licenses in actual use

Lync Enterprise Voice licenses in use as % of total

employees

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 16 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

What is the Projected Penetration of Lync EV Licenses Over the Next Few Years? We asked the study participants a similar set of questions about their future deployment plans in order to calculate the projected penetration of Lync EV Licenses.

Among U.S. Enterprises, the projected penetration of active plus CAL licenses was 5.7% by the end of 2015. That was up significantly from the 3.4% penetration at the end of 2013, as presented in Exhibit ES-7. By the end of 2017, the penetration of active Plus CAL licenses was projected to reach 8.3% of U.S. Enterprise employees. Penetration of Lync EV licenses in the U.S. SMB market was projected to lag that of the U.S. Enterprise market. By the end of 2015, the projected penetration of active plus CAL licenses was 3.6% of U.S. SMB employees. That was a significant increase from the 2.6% penetration computed for the end of 2013. The rate of SMB penetration was expected to accelerate over the following two years, reaching 4.6% of SMB employees by the end of 2017.

Exhibit ES-9 Projected Penetration of Lync EV Licenses

3.4%

5.7%

8.3%

2.6%

3.6%

4.6%

2013 2015 2017

Enterprise SMB

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 17 of 85

27%

52%

0%

4%

17%

15%

34%

38%

4%

9%

Avaya

Cisco

Microsoft

Cloud-based Hosted Service Provider

Other

Vendors

Enterprise

Before Currently

30%

20%

0%

6%

44%

26%

16%

15%

6%

37%

Avaya

Cisco

Microsoft

Cloud-based Hosted Service Provider

Other

Vendors

SMB

Before Currently

Source: InfoTrack: End-user Primary Research, 2Q2014

Where Does Microsoft Rate Among Preferred Vendors for IP-PBXs? Participants in this study were asked to identify the one company that was currently their preferred vendor for IP-PBXs or the functionality of IP-PBXs. They were also asked to identify who that preferred vendor was before Microsoft entered the Enterprise Voice market. The responses to these questions have been summarized in Exhibit ES-10.

About half of the U.S. Enterprises indicated that Cisco was their Preferred Vendor for IP-PBXs before Microsoft entered the Enterprise Voice market. This was followed by Avaya with 27%. 17% of the Enterprises preferred one of the other telephony systems vendors.

In response to the question regarding their current Preferred Vendor for IP-PBXs, 38% of the Enterprises selected Microsoft. This was substantially higher than the 25% in last year’s study. It was somewhat surprising that the percentage of Enterprises that picked Microsoft was higher than Cisco. On the other hand, we noted in Exhibit ES-3 that 44% of the Enterprises were currently deploying Microsoft Lync with Enterprise Voice. And in Exhibit ES-6, we saw that 40% of Enterprises expected company-wide deployment of Microsoft Lync EV. We should note that the format of this question in the survey limited Enterprises to one selection for Preferred Vendor currently. So of the Enterprises that had begun to deploy Microsoft Lync but still had mostly Cisco IP-PBXs, some could have decided to pick Microsoft as their one response to this question. As a result, Cisco dropped from 52% to 34%, while preferences for Avaya declined 12 points to 15%.

Among SMBs, 15% selected Microsoft as their currently preferred IP-PBX vendor. SMBs that preferred Avaya declined from 30% to 26%, while preferences for other telephony systems vendors went from 44% to 37%. Cisco dropped from 20% to 16% among these SMB decision-makers.

Exhibit ES-10 Preferred Vendor for IP-PBXs – Before Microsoft

Entered the Market vs. Currently

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 18 of 85

Source: InfoTrack: End-user Primary Research, 2Q2014

Where Does Microsoft Rate Among Preferred Vendors for UC Apps? Participants in this study were also asked to identify the one company that is currently their preferred vendor for UC applications. In addition, they were asked to identify who that preferred vendor was before Microsoft entered the Enterprise Voice market. The responses to these questions have been summarized in Exhibit ES-11.

43% of the U.S. Enterprises indicated that Cisco was their Preferred Vendor for UC Apps before Microsoft entered the Enterprise Voice market. At that point in time, Microsoft was already considered to be the Preferred Vendor for UC Apps by 27% of the Enterprises, followed by Avaya at 15%.

In response to the question regarding their current Preferred Vendor for UC Apps, 40% of the Enterprises selected Microsoft. This was a gain of 13 points for Microsoft, while Cisco dropped 7 points to 36%, which put them in 2nd place behind Microsoft. Avaya declined 6 points to 9%.

Among SMBs, before Microsoft entered the Enterprise Voice market they were the 3rd most popular vendor for UC apps. But currently, 29% of the SMBs chose Microsoft as their Preferred Vendor for UC Apps, a gain of 17 points. That put them ahead of Avaya which declined from 23% to 17%, and Cisco which dropped from 20% to 17% among these SMB decision-makers.

The bottom line here is that Microsoft is now the highest rated vendor for both UC Apps (40%) and IP-PBXs (38%) among U.S. Enterprises that participated in this survey. They have also moved into the top spot as Preferred Vendor for UC Apps among SMBs (29%).

Exhibit ES-11 Preferred Vendor for UC-Apps – Before Microsoft

Entered the Market vs. Currently

15%

43%

27%

2%

13%

9%

36%

40%

3%

12%

Avaya

Cisco

Microsoft

Cloud-based Hosted Service Provider

Other

Vendors

Enterprise

Before Currently

23%

20%

12%

9%

36%

17%

17%

29%

11%

26%

Avaya

Cisco

Microsoft

Cloud-based Hosted Service Provider

Other

Vendors

SMB

Before Currently

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Copyright 2014 T3i Group. All rights reserved June 2014 Page 19 of 85

2. INTRODUCTION AND METHODOLOGY

Scope of InfoTrack for Unified Communications (IUC)

InfoTrack for Unified Communications is a research program that addresses demand for evolving communications technologies and the impact of significant market shifts. Our analysis focuses on understanding decision-makers’ perceptions of the solutions being marketed to them, and their resulting buyer behaviors.

In the first half of 2014 we published reports on 1) New Trends and Changes in Customers’ UC Buying Behavior and 2) Transformative Technologies – Enterprise and SMB Outlook on how UC can Transform how they do Business. This current report is the 3rd annual report on the Market Impact of Microsoft Lync.

In June 2014 we will publish our annual in-depth forecast of the IP Telephony and Unified Communications (UC) application markets.

Program Leadership

The program directors for IUC are Ken Dolsky ([email protected]) and Terry White ([email protected]). They are responsible for all primary research involving the market demand for unified communications among U.S. and international businesses and institutions. To support these primary research efforts, T3i Group has established two research panels, one consisting of more than 7,000 Enterprise decision-makers and a second panel with more than 6,000 SMB decision-makers.

Primary Research Methodology

Analyses presented in this study were driven by comprehensive primary research, which was conducted specifically for this report. This primary research included a mix of web-based surveys and telephone interviews, with key industry players, including:

Decision-makers for both IP Telephony and UC applications

Leading suppliers of IP Telephony systems and UC apps.

The research covered both Enterprises (entities with 500 or more employees) and SMBs (entities with 5 to 499 employees). Results for each group are provided in separate sections.

Copyright 2014 T3i Group All rights reserved June 2014 Page 20 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

3. ANALYSIS OF ENTERPRISE PLANS FOR MICROSOFT LYNC

ENTERPRISE VOICE

Demographics of Enterprise Survey Participants

The exhibits in this section of the report are based on responses from U.S. business and institutional entities with 500 or more employees. IUC refers to these entities as Enterprises. During April 2014, surveys were completed with over 150 qualified Enterprise managers who are key decision-makers or key influencers regarding adoption and usage of Microsoft Lync. The same survey also received responses from 150 managers at SMB sized companies (499 employees or less) with the same responsibilities. The results from the SMB managers are described later in Section 4.

Exhibit 1 below shows the distribution of the participating U.S. Enterprises based upon their size. 23% of the respondents represented Enterprises with 500 to 999 employees, and 27% were Enterprises with 1,000 to 2,499 employees. Throughout the analysis, these two size categories, comprising 50% of the respondents, are referred to as Medium Enterprises (ME).

36% of the respondents were from Enterprises with between 2,500 and 9,999 employees. Enterprises with 10,000 or more employees accounted for 14% of the Enterprise participants. These two size segments comprise the Large Enterprise (LE) segment, representing 50% of the respondents.

Exhibit 1 Distribution of Participating Enterprises

by Size

23%

27%

36%

14%

500 – 999

1,000 – 2,499

2,500 – 9,999

10,000 +

U.S. Enterprises

Copyright 2014 T3i Group All rights reserved June 2014 Page 21 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Distribution of Participating Enterprises by Type of Decision Maker

Exhibit 2 contains two graphs that show the distribution of titles and decision-making responsibilities among the Enterprise decision-makers who participated in this study.

44% were Executives who are responsible for business decisions, including CEOs, CFOs, COOs and Line of Business Managers. These executives are becoming more involved in the UC decision process, which justified their significantly higher representation in this year’s survey.

CIOs, Information Systems Managers and Applications Managers, who are responsible for IT (information technology) decision-making, accounted for 49% of the participants in this study.

The remaining 7% were Telecom Managers and Data Network Managers whose primary decision-making responsibilities involve communications systems and networks.

Exhibit 2 Distribution of Participating Enterprises

by Type of Decision Maker

44%

49%

7%

Business

Information

Communications1%

6%

1%

33%

15%

12%

13%

19%

Telecom Manager

Data Network Manager

Applications Manager

Info Systems Manager

CIO

LoB Manager

CFO or COO

CEO

Copyright 2014 T3i Group All rights reserved June 2014 Page 22 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Distribution of Participating Enterprises by Type of Industry

Exhibit 3 shows the industry segment distribution of the Enterprise decision-makers who participated in this study. The participants represented 10 different industries.

The top three industries accounted for almost half of the Enterprise respondents, led by Manufacturing with 20%, Retail/Wholesale at 15% and Professional Services at 10%.

The next five industries represented roughly 40%of the total, including Healthcare, Telecommunications, Business Services, Financial Services/Insurance and Education.

Exhibit 3 Distribution of Participating Enterprises

by Type of Industry

20%

15%

10%

9%

9%

8%

7%

6%

5%

2%

9%

Manufacturing

Retail/Wholesale

Professional Services

Healthcare

Telecommunications

Business Services

Financial Services/Insurance

Education

Government

Utilities

Other

Copyright 2014 T3i Group All rights reserved June 2014 Page 23 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Enterprise Position on Microsoft Software Products and Services

Exhibit 4 shows the position taken by Enterprises toward Microsoft as a provider of products and services. Enterprises surveyed were strongly inclined toward reliance on the company, with 96% of Large Enterprises and 94% of Medium Enterprises describing themselves as “Microsoft shops” for at least some software.

Of those, MEs were more likely to depend primarily on Microsoft for key products and services (72% of MEs versus 63% of LEs), while LEs were more likely to buy only selected products and services from Microsoft (33% of LEs versus 22% of MEs). Among those few that characterized themselves as not a Microsoft shop were 4% of LEs and 6% of MEs.

Exhibit 4 Enterprise Position on Microsoft Software

Products and Services

72%

22%

6%

63%

33%

4%

Our company is primarily a “Microsoft shop” for key software products

and services

Our company is a “Microsoft shop” for

selected software products and services

Our company is NOT a “Microsoft shop” for key software products and

services

Medium Enterprise Large Enterprise

Copyright 2014 T3i Group All rights reserved June 2014 Page 24 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

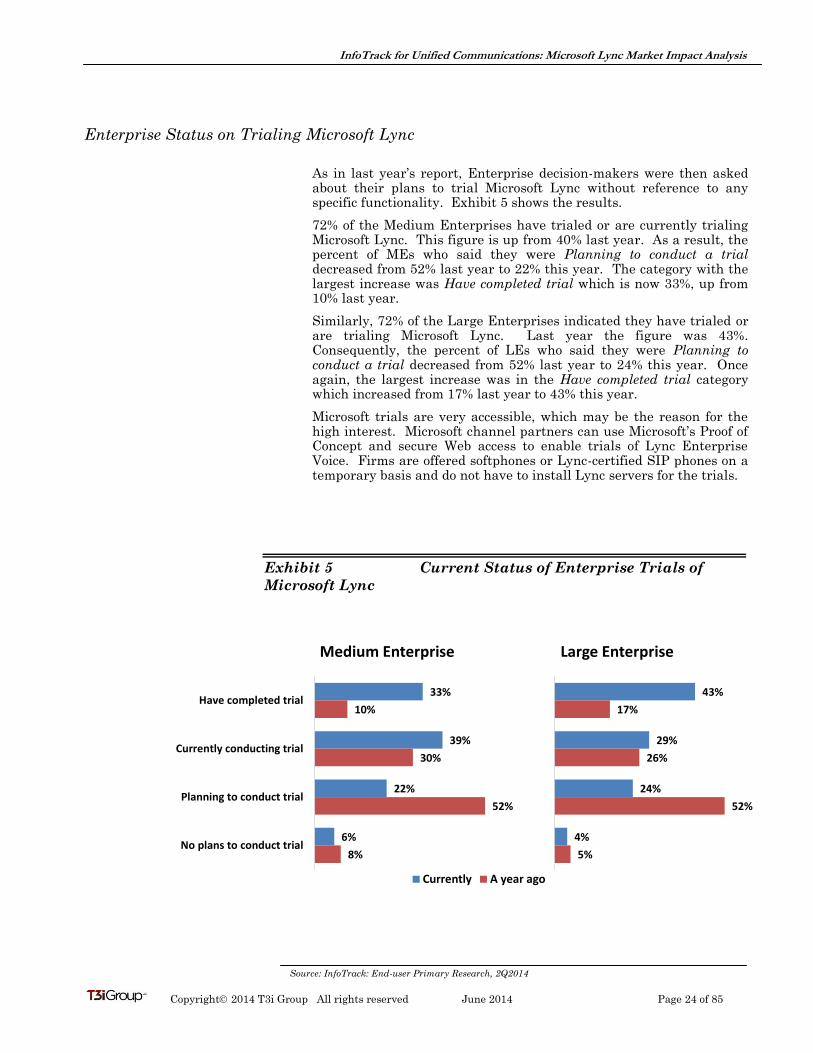

Enterprise Status on Trialing Microsoft Lync

As in last year’s report, Enterprise decision-makers were then asked about their plans to trial Microsoft Lync without reference to any specific functionality. Exhibit 5 shows the results.

72% of the Medium Enterprises have trialed or are currently trialing Microsoft Lync. This figure is up from 40% last year. As a result, the percent of MEs who said they were Planning to conduct a trial decreased from 52% last year to 22% this year. The category with the largest increase was Have completed trial which is now 33%, up from 10% last year.

Similarly, 72% of the Large Enterprises indicated they have trialed or are trialing Microsoft Lync. Last year the figure was 43%. Consequently, the percent of LEs who said they were Planning to conduct a trial decreased from 52% last year to 24% this year. Once again, the largest increase was in the Have completed trial category which increased from 17% last year to 43% this year.

Microsoft trials are very accessible, which may be the reason for the high interest. Microsoft channel partners can use Microsoft’s Proof of Concept and secure Web access to enable trials of Lync Enterprise Voice. Firms are offered softphones or Lync-certified SIP phones on a temporary basis and do not have to install Lync servers for the trials.

Exhibit 5 Current Status of Enterprise Trials of

Microsoft Lync

33%

39%

22%

6%

10%

30%

52%

8%

Have completed trial

Currently conducting trial

Planning to conduct trial

No plans to conduct trial

Medium Enterprise

Currently A year ago

43%

29%

24%

4%

17%

26%

52%

5%

Have completed trial

Currently conducting trial

Planning to conduct trial

No plans to conduct trial

Large Enterprise

Currently A year ago

Copyright 2014 T3i Group All rights reserved June 2014 Page 25 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Percent of Enterprise Microsoft Lync Trials that Include Enterprise Voice

Exhibit 6 shows the percentages of completed, current and planned Enterprise Microsoft Lync trials that included Enterprise Voice. As shown previously in Exhibit ES-2, 89% of the U.S. Enterprises who have trialed or are currently conducting trials or plan to trial indicated that Enterprise Voice had been, is or will be included in their Lync trials. That represents a 13 point increase from 76% a year ago.

88% of MEs said their trials include or will include Enterprise Voice. This compares with 68% who said this in last year’s report.

Similarly, 90% of LEs said they have trialed or will trial Enterprise Voice. This compares with 84% who said this in last year’s report.

Both segments of Enterprises have shown a significant increase in their interest in trialing Lync Enterprise Voice, especially among MEs.

Microsoft and its partners make it relatively easy to trial Lync with Enterprise Voice. Firms are provided Lync-certified SIP phones or softphones on a temporary basis and do not have to install Lync servers for the trials.

Exhibit 6 Percent of Enterprise Microsoft Lync Trials

that Include Enterprise Voice Among those who have completed, are currently trialing or plan to trial

88%68%

12%32%

Current A year ago

Medium Enterprise

No, Trials Do Not Include Enterprise Voice

Yes, Trials Include Enterprise Voice

90% 84%

10% 16%

Current A year ago

Large Enterprise

No, Trials Do Not Include Enterprise Voice

Yes, Trials Include Enterprise Voice

Copyright 2014 T3i Group All rights reserved June 2014 Page 26 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

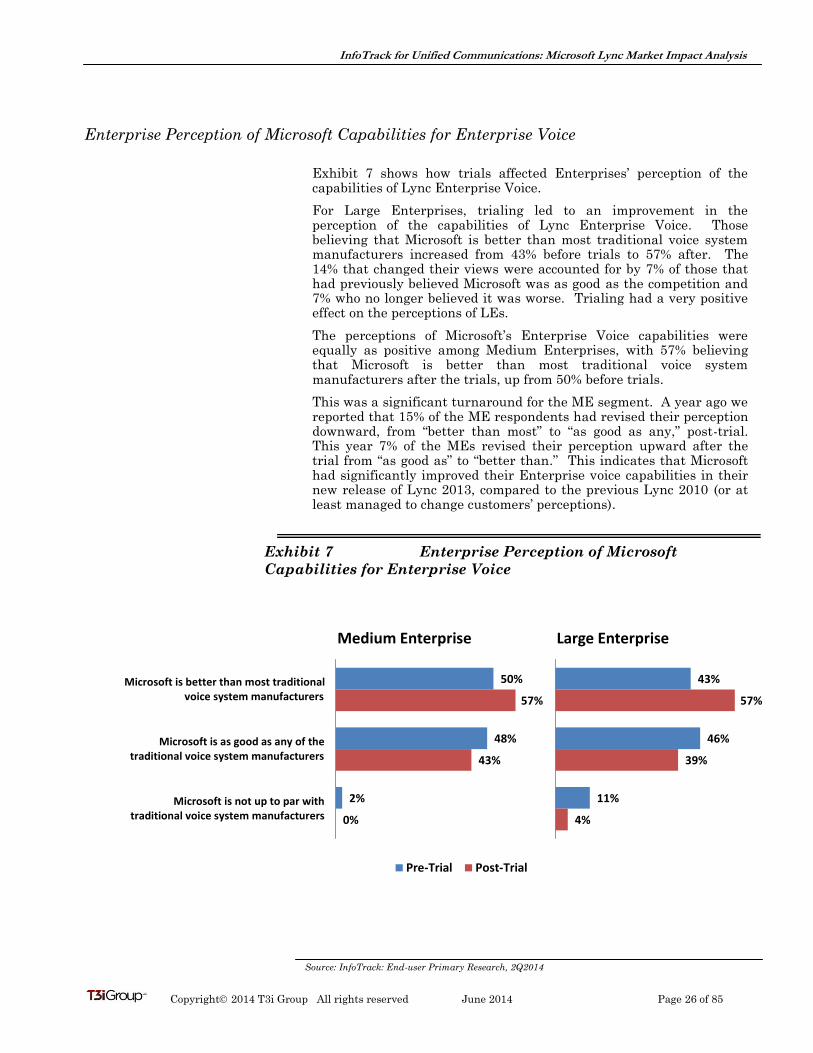

Enterprise Perception of Microsoft Capabilities for Enterprise Voice

Exhibit 7 shows how trials affected Enterprises’ perception of the capabilities of Lync Enterprise Voice.

For Large Enterprises, trialing led to an improvement in the perception of the capabilities of Lync Enterprise Voice. Those believing that Microsoft is better than most traditional voice system manufacturers increased from 43% before trials to 57% after. The 14% that changed their views were accounted for by 7% of those that had previously believed Microsoft was as good as the competition and 7% who no longer believed it was worse. Trialing had a very positive effect on the perceptions of LEs.

The perceptions of Microsoft’s Enterprise Voice capabilities were equally as positive among Medium Enterprises, with 57% believing that Microsoft is better than most traditional voice system manufacturers after the trials, up from 50% before trials.

This was a significant turnaround for the ME segment. A year ago we reported that 15% of the ME respondents had revised their perception downward, from “better than most” to “as good as any,” post-trial. This year 7% of the MEs revised their perception upward after the trial from “as good as” to “better than.” This indicates that Microsoft had significantly improved their Enterprise voice capabilities in their new release of Lync 2013, compared to the previous Lync 2010 (or at least managed to change customers’ perceptions).

Exhibit 7 Enterprise Perception of Microsoft

Capabilities for Enterprise Voice

50%

48%

2%

57%

43%

0%

Microsoft is better than most traditional voice system manufacturers

Microsoft is as good as any of thetraditional voice system manufacturers

Microsoft is not up to par withtraditional voice system manufacturers

Medium Enterprise

Pre-Trial Post-Trial

43%

46%

11%

57%

39%

4%

Microsoft is better than most traditional voice system manufacturers

Microsoft is as good as any of thetraditional voice system manufacturers

Microsoft is not up to par withtraditional voice system manufacturers

Large Enterprise

Pre-Trial Post-Trial

Copyright 2014 T3i Group All rights reserved June 2014 Page 27 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

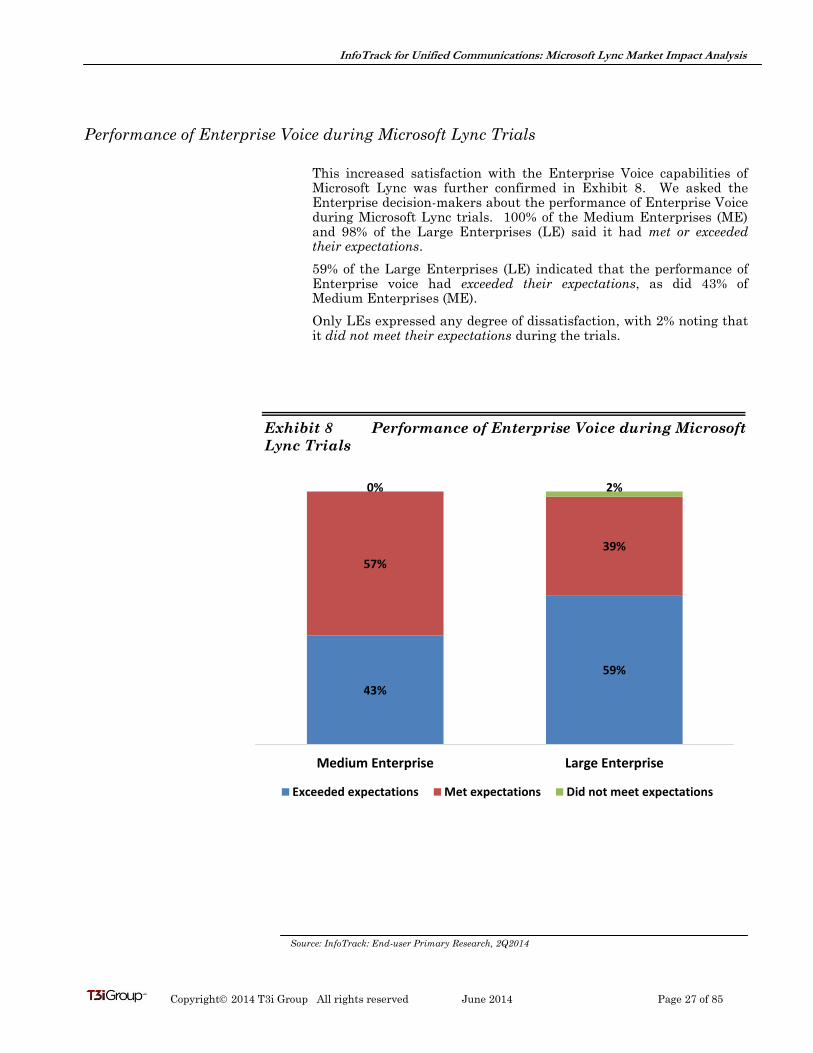

Performance of Enterprise Voice during Microsoft Lync Trials

This increased satisfaction with the Enterprise Voice capabilities of Microsoft Lync was further confirmed in Exhibit 8. We asked the Enterprise decision-makers about the performance of Enterprise Voice during Microsoft Lync trials. 100% of the Medium Enterprises (ME) and 98% of the Large Enterprises (LE) said it had met or exceeded their expectations.

59% of the Large Enterprises (LE) indicated that the performance of Enterprise voice had exceeded their expectations, as did 43% of Medium Enterprises (ME).

Only LEs expressed any degree of dissatisfaction, with 2% noting that it did not meet their expectations during the trials.

Exhibit 8 Performance of Enterprise Voice during Microsoft

Lync Trials

43%

59%

57%

39%

0% 2%

Medium Enterprise Large Enterprise

Exceeded expectations Met expectations Did not meet expectations

Copyright 2014 T3i Group All rights reserved June 2014 Page 28 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Enterprise Perspective on Startup Costs of Implementing Lync with Enterprise Voice

Exhibit 9 shows enterprises’ views on the relationship between the startup costs of implementing Lync with Enterprise Voice and their expectations about those costs.

Roughly half of the Enterprises indicated that the startup costs were in line with what they had expected. 14% of Medium Enterprises and 16% of Large Enterprises actually felt that the startup costs were lower than they had expected. However, approximately twice that many -- 29% (ME) and 27% (LE) -- admitted there were some additional costs that they had not anticipated.

The next Exhibit examines the ongoing costs of implementing Microsoft Lync with Enterprise Voice.

Exhibit 9 Enterprise Perspective on Startup Costs of

Implementing Lync with Enterprise Voice

5%

14%

29%

52%

It is too early in the process to make a determination on startup costs

So far the startup costs are lower than we had expected

There were some additional costs that we had not anticipated

The startup costs are in line with what we had expected

Medium Enterprise

9%

16%

27%

48%

It is too early in the process to make a determination on startup costs

So far the startup costs are lower than we had expected

There were some additional costs that we had not anticipated

The startup costs are in line with what we had expected

Large Enterprise

Copyright 2014 T3i Group All rights reserved June 2014 Page 29 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Enterprise Perspective on Ongoing Costs of Implementing Lync with Enterprise Voice

We also asked the Enterprise decision-makers about the ongoing costs of operating and managing Lync with Enterprise Voice. Exhibit 10 provides a view of their responses.

A little over 40% of the Enterprises indicated that the ongoing costs were in line with what they had expected. But almost as many Large Enterprises (38%) revealed there were some additional costs that they had not anticipated. 26% of Medium Enterprises agreed that there were additional ongoing costs, but that was only slightly more than the 23% of MEs that actually felt the ongoing costs were lower than they had expected. 14% of LEs also said they had encountered lower ongoing costs than they had expected.

The results in Exhibits 9 and 10 indicate some improvements regarding the Enterprise perspective on costs compared to the results of the study we conducted a year ago. In that study, only 10% of MEs and none of the LEs experienced lower total costs than expected. While 42% of LEs and 25% of MEs expressed concerns that there were additional costs that they had not anticipated. In that study, the vast majority of MEs (65%) and LEs (58%) felt that the total costs were in line with what they had expected.

Exhibit 10 Enterprise Perspective on Ongoing Costs of

Implementing Lync with Enterprise Voice

10%

23%

26%

41%

It is too early in the process to make a determination on ongoing costs

So far the ongoing costs are lower than we had expected

There were some additional costs that we had not anticipated

The ongoing costs are in line with what we had expected

Medium Enterprise

5%

14%

38%

43%

It is too early in the process to make a determination on ongoing costs

So far the ongoing costs are lower than we had expected

There were some additional costs that we had not anticipated

The ongoing costs are in line with what we had expected

Large Enterprise

Copyright 2014 T3i Group All rights reserved June 2014 Page 30 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Enterprise Plans for Deploying Lync with Enterprise Voice Beyond Trials

Exhibit 11 shows the plans of all Enterprises surveyed regarding the deployment of Lync with Enterprise Voice currently compared to a year ago.

In last year’s study, almost equal percentages of LEs (43%) and MEs (44%) were planning to deploy Lync EV. But this year, those are the type of percentage of LEs (49%) and MEs (39%) who are actually deploying Lync EV. Last year, only 18% of LEs and 11% of MEs had started deploying Microsoft Lync with Enterprise voice. Thus, there has been a huge increase in the percent of U.S. Enterprises that are now deploying Lync EV.

In addition, 37% of MEs and 33% of LEs indicated that they were currently in the planning stages of deploying Lync with Enterprise Voice and had proceeded beyond the trial stage.

24% of the Enterprises and 18% of the Large Enterprises were either waiting for the results of their trials before deciding whether to deploy Lync EV or had no plans to deploy. This represents a 21 point reduction in the percent of “Undecideds” or “No Plans” from last year.

It appears that the positive results that Enterprises are experiencing during their trials of Lync EV have had a significant impact on their plans to move forward with deployment.

Exhibit 11 Enterprise Plans for Deploying Lync with

Enterprise Voice Beyond Trials (Among all Enterprises)

39%

37%

20%

4%

11%

44%

38%

7%

Currently deploying

Planning to deploy

Undecided; depends on results of trial

No plans to deploy Microsoft Lync for Enterprise Voice

Medium Enterprise

Current A year ago

49%

33%

14%

4%

18%

43%

31%

8%

Currently deploying

Planning to deploy

Undecided; depends on results of trial

No plans to deploy Microsoft Lync for Enterprise Voice

Large Enterprise

Current A year ago

Copyright 2014 T3i Group All rights reserved June 2014 Page 31 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

ME LE

Ranking

1

2

3

4

8

5

7

1

2

3

4

5

6

7

10 8

6 9

11 10

9 11

ME LE

Weighted Average

Total cost of ownership (hardware, software, service support) is lower than PBX based solutions

6.1 5.5

4.6 4.6Facilitates voice feature integration with other Microsoft

applications, e.g., Sharepoint, Exchange, Office

3.3 4.1We have already adopted Microsoft Lync for IM and Presence

1.2 1.9Lync is available as both a premises system and a hosted service

3.0 2.6Lync Enterprise Voice is a natural extension of our

commitment to Microsoft Lync for UC

1.6 2.8The Lync Client is superior to the user interface

provided by other UC vendors

3.3 3.0We have already adopted Microsoft Lync for Web Conferencing

2.4 2.6We have already invested in the Enterprise CAL Suite

1.6 0.7Ease of implementation and telephony system management

1.2 1.1Connectivity with Skype

2.5 1.6Lync Enterprise Voice has all the voice functionality we need

Enterprises’ Top Reasons for Deploying Lync with Enterprise Voice Beyond Trials

The Enterprises implementing Microsoft Lync for Enterprise Voice were asked why they decided to implement Lync. Exhibit 12 ranks their responses.

Both Medium and Large Enterprises most frequently cited lower total cost of ownership with Microsoft Lync Enterprise Voice than with PBX-based solutions. Microsoft’s pricing structure bundles access to Lync in the Enterprise CAL Suite with access to popular applications, including Windows, Exchange and Sharepoint, so the incremental cost to add Lync functionality from a license standpoint is attractive. This is a key point because the second most important reason for both MEs and LEs was Facilitates voice feature integration with other Microsoft applications.

We have already adopted Microsoft Lync for IM and Presence was third most important for both Enterprise segments, followed by we have already adopted Microsoft Lync for web conferencing.

Lync Enterprise Voice is a natural extension of our commitment to Microsoft Lync for UC was cited as the fifth most important reasons for MEs, and the 6th most important for LEs.

The majority of the top-rated reasons indicate that once MEs and LEs adopt Microsoft Lync as their preferred platform for UC Apps, such as IM & presence and web conferencing, they are very likely to take the next step and implement Lync Enterprise Voice.

Exhibit 12 Enterprises’ Top Reasons for Deploying Lync with

Enterprise Voice Beyond Trials Among Enterprises Deploying or Planning to Deploy Lync with Enterprise

Voice

Copyright 2014 T3i Group All rights reserved June 2014 Page 32 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Factors that Fell Short of Enterprises’ Expectations in Deploying Lync with Enterprise

Voice

In our survey, we gave the Enterprises that were deploying Lync EV another opportunity to identify any factors that fell short of their expectations. However, the top-rated answer was None of these; Lync with Enterprise Voice has MET or EXCEEDED all of our expectations.

There was still a group of Enterprises, particularly in the LE segment, that believe that Microsoft Lync’s Total Cost of Ownership (TCO) was NOT lower than PBX based solutions. These Enterprises were among those that earlier noted that there were some additional costs in implementing Lync EV that they had not anticipated.

Another factor that fell short of the expectations of the LE decision-makers was Lync Enterprise Voice is NOT supported by Lync Online, which is Microsoft’s hosted version of Lync. This did not rate as a major determent among MEs, perhaps because there are several Microsoft partners that offer a hosted Lync service that does include the full Enterprise Voice capability.

Some ME decision-makers expressed concern that Lync does NOT integrate easily with our existing voice system. Others had some concerns about the Lync support for Mobility. But overall, it appears that as Microsoft continues to enhance the features of Microsoft Lync EV, Enterprises are finding fewer concerns.

Exhibit 13 Factors that Fell Short of Enterprises’

Expectations in Deploying Lync with Enterprise Voice Among Enterprises Currently Deploying Lync with Enterprise Voice

ME LE

Ranking

1

2

4

6

9

3

8

1

2

3

4

5

6

7

7 8

5 9

ME LE

Weighted Average

None of these; Lync with Enterprise Voice has MET or EXCEEDED all of our expectations

3.9 4.1

2.2 4.1Total cost of ownership (hardware, software, service support)

is NOT lower than PBX based solutions

0.9 1.9Lync Enterprise Voice is NOT supported by Lync Online

1.8 0.6Lync does NOT provide ease of implementation and

telephony system management

2.0 1.0Lync does NOT integrate easily with our existing voice system

1.8 1.4Lync support for Mobility does NOT meet our needs

1.0 1.5Lync does NOT facilitate telephony feature integration with other

Microsoft applications, e.g., Sharepoint, Exchange, Office

1.7 0.7Lync Enterprise Voice does NOT have all the voice

functionality we need

0.8 0.3The Lync Client is NOT superior to the user interface

provided by other UC vendors

Copyright 2014 T3i Group All rights reserved June 2014 Page 33 of 85

InfoTrack for Unified Communications: Microsoft Lync Market Impact Analysis

Source: InfoTrack: End-user Primary Research, 2Q2014

Enterprise Problems in Scaling Lync with Enterprise Voice

Exhibit 14 shows the degree to which enterprises saw or anticipated problems in scaling Lync with Enterprise Voice. The population answering this question included those who had deployed, are currently deploying and those that plan to deploy Lync with Enterprise Voice.

About half (51% of MEs and 52% of LEs) found some problems but nothing major, while a somewhat smaller group (38% for MEs and 40% for LEs) found no problems scaling. More serious concerns expressing considerable problems were more prevalent among MEs than LEs (8% versus 5%), while only 3% of MEs and LEs were not able to scale as necessary.

Overall, more than half of the enterprises had some degree of scaling difficulty while deploying or their planning efforts indicated they were likely to have some problem with scaling. However, the percentage that indicated that scaling was a significant problem was about a third less than in last year’s study

Exhibit 14 Enterprise Problems in Scaling Lync with

Enterprise Voice

3%

8%

51%

38%

Have not been able to scale as necessary

Considerable problems