Embed Size (px)

Citation preview

EnterpriseRiskCaptives:Regulatory&LegislativeUpdate

DCIA2017SpringForum

RyanWork,VicePresident,GovernmentRelationsSelf-InsuranceInstituteofAmerica,Inc.

2016Presidential– BytheNumbersü 5xElectoralCollegewinnerlostthe

popularvoteü 14xWinnerreceivedlessthan50%LowerTurnout• Poolofeligiblevotersrose5.5%/#ballotsincreased1.5%

• Majorpartyvotesfell3million- 3rd party=5.5%/7.5millionvotes

2012vs.2016• Trumpreceived317,00moreballotsthanRomney

• Clintonreceived3.5millionfewerthanObama(3.4%)

SmallFactorsWon:

• Clintonwon3%lessthanObama

• Trumpwon10%ofObamasupport

• Trumpwonwhitefemalesby10points,53to43.

• TrumpwonlargerAfricanAmerican(8%)andHispanicvote(29%)thanRomney

Framing thePoliticalEnvironmentPresident:306R– 232D(270towin)• AntiWashingtonFrustration• Post-IdeologicalHouse:239R– 193D(218Majority)• 246Republicans- 188DemocratsSenate:52R– 48D(+2)• Republicansdefended24seats,comparedwithonly10forDemocrats

• OutpolledPresidential– Toomey,Rubio

States:

• Governors– 33R- 16Ds

• Rs Control33StateLegislatures,17vetoproof

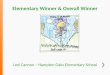

2016– BattlegroundStates2012

2016ElectionMap2012

PolicyPerspectives

RegulatoryViewofCaptives

AbusiveTaxShelters– IRS‘DirtyDozen’List• ‘Unscrupulouspromoterspersuadecloselyheldentitiestoparticipateinscheme…creatingand“selling”totheentitiesoftentimespoorlydrafted“insurance”bindersandpoliciestocoverordinarybusinessrisksoresoteric,implausiblerisksforexorbitant“premiums,”whilemaintainingtheireconomicalcommercialcoveragewithtraditionalinsurers.’

• ‘Promotersmanagetheentities’captiveinsurancecompaniesyearafteryearforheftyfees,assistingtaxpayersunsophisticatedininsurancetocontinuethecharade.’

ERCLegislativeEnvironment

CongressionalProposals• FarmMutuals:IncreasewrittenpremiumthresholdofIRC§ 831(b)from$1.2millionto$2.2.Million

831(b)LegislativePurpose

•Prohibituseofreinsurance• Limitto20%ofnetwrittenpremiumstoapolicyholderinataxableyear

SenateFinanceCommitteeOriginal

Restrictions

• Senate•Thresholdincrease/curbestateabuse

•U.S.Treasurystudyontheuseofcaptivesasanestateplanningtool

•House• Cleanthresholdincrease

IntroducedafterSIIAAdvocacy

Congressional– LawChangesIncorporatedin2015PATHAct

I.Premiumthresholdincreasefrom$1.2millionto$2.2million(indexedtoinflation).

II.Restrictionstoprohibitestateplanningandwealthtransfer.

üTest1:RiskDiversificationNomorethan20%ofnetwrittenordirectpremiumsfromanyonepolicyholder.

• RelatedinsuredsaretreatedasonepolicyholderOR

üTest2:OwnershipTestFamilyandlinealdescendantscannotownmoreintheinsurancecompanythantheoperatingentity.

• 2%deminimis

EffectiveDate:Dec.31,2016

WhereWeStandwithChanges

SIIA,joinedby15stateassociations,requestedthefollowingfromtheIRS/Treasury:

• AdministrativerelieffromcompliancewiththePATHAct

• InterimReasonableCompliance/SafeHarbors

• Guidance&Clarificationonkeyissues:• Defining“policyholder”• Clarificationofspecifiedandspousalownership• Calculationofspecifiedassetsrelatedtomultiplebusinessentities• Deminimis standardapplicationandexceptions.

PATHAct:SIIALegislativeClarificationProposals

JCTDiscussions&TaxTechnicalCorrections:

vTest1:Clarificationoflook-throughlanguage

vTest2:Calculationofthe“percentageofinterestsinthespecifiedassets”

vGuidancetoTreasurythatdeminimis standard(2%)cannotbelowered- providebrightlineexceptionsforsituationswherenoestatetaxavoidanceisinvolved

vSpousalOwnershipIntent

TaxTechnicalCorrectionsAct

1)Clarifylook-thoughforreinsuranceorfrontingarrangements2)Clarifyspecifiedassets( underTest2)tomeanaggregateamountofrelatedassetsownedbyspouse/relation.• Two-yeargraceperiodwhenacquiringownershipthroughinheritanceordeath.

JCTleavesuptoTreasuryDepartmentguidancerelatedtoownership,premiums,grossrevenue,andfactorstakenintoaccountunderapplicableStatelawforassessingrisk.

Captives&TaxReform

TaxReformReconciliationRoundTwo:ØCreateaseparate,lowerbusinesstaxrate

Ø Trump-15%Ø House- 20%

ØCuttaxesonsavingsandinvestmentbyallowingdeductionof50percentofthedividends,capitalgains,andinterestreceivedfromstocksandmutualfunds.

Ø Provideatax-freereturnonnewinvestmentbyallowingfullandimmediatewrite-offs.

ØEliminateDeathTaxØ Individualtaxdownto3brackets– 10/25/35

Ø Eliminatealldeductionswiththeexceptionofchild,home,charitableØ Doublestandarddeductions

Questions:qTreatmentof831(b)Captives

IRSNotice2016-66

17

Notice2016-66OverviewNovember1,2016• IRSissuesNotice2016-66designatingvastmajorityof831(b)

captivesas“TransactionsofInterest”• Triggersdisclosurerequirementsforowners,managersandmaterial

advisors.• Failuretoreportcanincurfinancialpenalties.

January30,2017• OriginalFilingDate• PostponementtoMay1(Notice2017-08)

18

IRSConcernsIsthecaptiveaninsurancecompany?Ø Inadequatecapitaltocoverassumedrisks.Ø LoansfromcaptivetoinsuredsoraffiliatesØ InsurednotfilingclaimsforlossesØ PooledpremiumsdonotreflecttheriskØ AmbiguousclaimsproceduresØ IssuanceofpoliciesandbindersØ CaptiveclaimsadministrationØ Investmentssolelybenefittingtheinsured

19

TransactionofInterestRequirements•Form8886FilingRequirements:• 831(b)Captivesinwhichtheinsuredcompanyowner(andaffiliates)ownatleast20%ofthecaptiveAND:

1.Thecaptives’lossesandlossexpensesarelessthan70%ofpremiumsearnedlesspolicyholderdividends,or

2.Captivehasmadeloans,guarantees,etc.benefitingaffiliates.

20

Form8886Filed,NowWhat?

• TheIRSwillreviewfilingsandtrytodistinguishbetweenabusiveandnon-abusivestructures.• IRSwilldeterminewhethercertain831(b)captiveswillbe:• DeletedfromTOIcategory;• DesignatedasListedTransactions;or• FurtherReview.

IRSNotice:ExecutiveOrderApril21– ‘IdentifyingandReducingTaxRegulatoryBurdens’§ TreasurytoreviewsignificanttaxregulationsissuedonorafterJanuary1,2016.

§ OfficeofInformationandRegulatoryAffairsandOMBidentifyinaninterimreportwithin60daysregulationsthat:

(i)imposeunduefinancialburdenontaxpayers;(ii)addunduecomplexitytotheFederaltaxlaws;or(iii)exceedthestatutoryauthorityoftheIRS.

üFinalreportdue150daysaftertheorder.üActionswillbepublishedintheFederalRegisternolaterthan180afterfinalreport.

SIIAAdvocacyMessages• ERCtaxpayerswillbeplacedunderundueregulatoryandreportingburdens.• Noticebroadlytargetedformajorityofparticipants,insteadofbeingnarrowlytailoredtowardsabusers.• MuchoftheinforequestedbytheIRSisalreadyprovidedtothemthroughvariousrequiredforms.• IRSisignoringrecentTaxCourtprecedent• PrematuretoissuesuchaNoticeconsideringtheimplicationsofcases– ie.Avrahami.• IRSisignoringCongressionalintent- PATHACT

SIIAActivitiesüMetwithIRS

üFormallyRequestExtensionforCompliance(GranteduntilMay1).

üExpressedConcerns

üEducate&MeetwithCongresstowardsgoalofIRSrescission.üCongressionalLettersüIndustryLetters

üFiledCommentsinJanuary.üInformingEOReport

CongressionalIntervention

IndustryTools

IndustryCoalitions• StateAssociations(DCIA)• IndividualMembers• Owners• DomicileAdvocates• DealerObligors

Self-InsuranceEducationalFoundation(SIEF)

• CapitolHillBriefings

Self-InsurancePoliticalActionCommittee

• Supportingfederalcandidates

MediaOutreachCapabilities

• Op-eds• ExpertInterviews