Embed Size (px)

Citation preview

Company Overview

12.4%

13.9%

392

247

173

18.4%

490

21.9%

2004 2005 2006 2007 2008

760

20.6%

2009

12.4%

25.2%

1,080

2010

25.6%

1,233

IPO

24.1%

Leadership

Foundation

Strengthening

10.6%

1983 1986 1989 1992 1995 1996 1997 1998 1999 2000 2001 2002

9.8%

10.0%

8.4% 6.5%

110 106 98

63

35 24 17

Proprietary Technology

Microsiga Startup

Franchise System

126

2003

Market Consolidation

TOTVS Brand

DNA

Integrated Systems for SMEs

1st IT IPO in Latin America

R$ 1 Billion of Sales in 2010

2011

1,343

Gro

ss R

eve

nu

es (

R$

Mill

ion

s) a

nd

EB

ITD

A M

argi

n (

%)

¹

(1) EBITDA Margin does not include extraordinary expenses 2

History

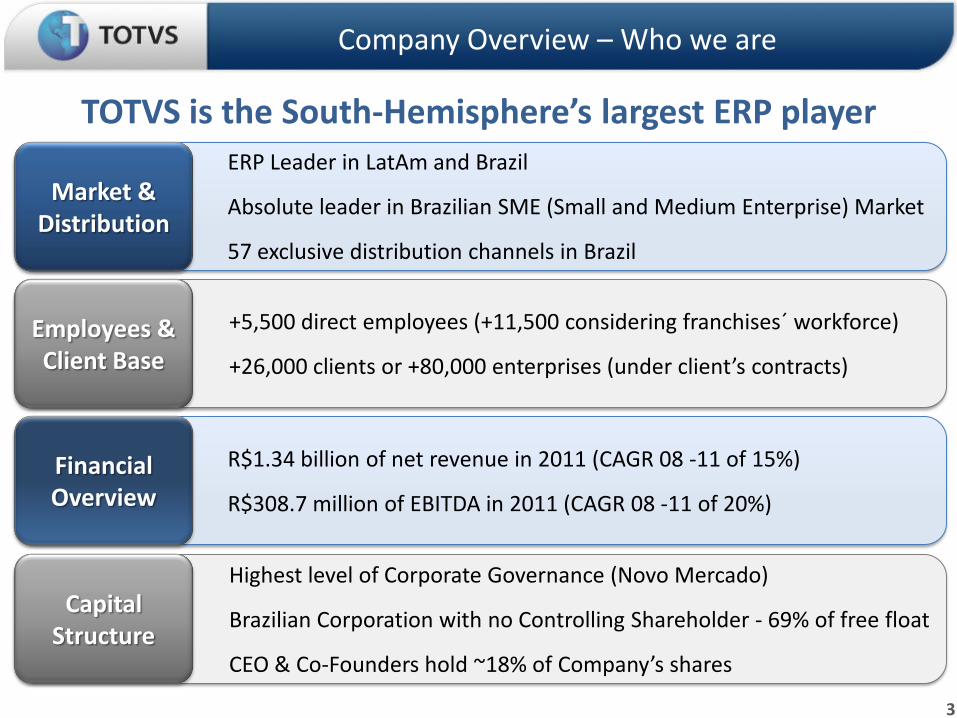

TOTVS is the South-Hemisphere’s largest ERP player

Company Overview – Who we are

Highest level of Corporate Governance (Novo Mercado)

Brazilian Corporation with no Controlling Shareholder - 69% of free float

CEO & Co-Founders hold ~18% of Company’s shares

ERP Leader in LatAm and Brazil

Absolute leader in Brazilian SME (Small and Medium Enterprise) Market

57 exclusive distribution channels in Brazil

R$1.34 billion of net revenue in 2011 (CAGR 08 -11 of 15%)

R$308.7 million of EBITDA in 2011 (CAGR 08 -11 of 20%)

+5,500 direct employees (+11,500 considering franchises´ workforce)

+26,000 clients or +80,000 enterprises (under client’s contracts)

Market & Distribution

Capital Structure

Employees & Client Base

Financial Overview

3

CEO, Co-founders and related persons and companies 17.9%

Fundação Petrobras de Seguridade Social – PETROS 10.0%

BNDES Participações S/A 3.2%

Free Float 68.9%

% of free float 2Q12 1Q12 4Q11 3Q11 2Q11

Non-Institutional Investors 6.2% 7.1% 5.9% 6.7% 6.5%

Institutional Investors 93.8% 92.9% 94.1% 93.3% 93.5%

Local Investors 12.2% 13.6% 12.4% 17.9% 14.9%

International Investors 87.8% 86.4% 87.6% 82.1% 85.1%

Company Overview – Who we are

Ownership Structure

Shareholders

4

6th worldwide in Revenue* and 1st in growth

5

Source: Gartner - ERP Software, Worldwide, 2011

*Licenses and Maintenance Revenues, in US$ million 2010 vs. 2011 Evolution

Global Ranking of ERP-Suite 2011

Company Overview – Who we are

Company Overview – Who we are

18th Most Valuable Brand in Brazil

• High value despite the brand´s young age

• Ranked ahead of major consumer brands

• Has become a synonym for Brazilian business software

Source: Brand Analytics/Millard Brown – Istoé Dinheiro ed.760 june 2012

http://www.istoedinheiro.com.br/noticias/82403_AS+MARCAS+MAIS+VALIOSAS+DO+BRASIL+EM+2012

18 TOTVS 56919 TAM 560

20 CIELO 555

21 MULTIPLUS 519

22 PORTO SEGURO 500

23 MAGAZINE LUIZA 479

24 GOL 450

25 REDECARD 439

26 NET 436

27 EXTRA 412

28 BM&FBOVESPA 386

29 BANRISUL 383

30 HERING 351

31 IGUATEMI 349

32 ODONTOPREV 342

33 PÃO DE AÇUCAR 332

34 UNIÃO 322

50 MOST VALUABLE BRAZILIAN BRANDS

Rank Brand Value (US$ MM)

1 PETROBRAS 10,560

2 BRADESCO 6,690

3 ITAÚ 6,606

4 SKOL 4,698

5 BANCO DO BRASIL 4,574

6 NATURA 3,307

7 BRAHMA 2,359

8 VALE 1,708

9 SADIA 1,496

10 ANTARTICA 851

11 VIVO 817

12 PERDIGÃO 778

13 LOJAS AMERICANAS 762

14 BOHEMIA 697

15 IPIRANGA 670

16 OI 600

17 CASAS BAHIA 589

6

Target Market

Strong Fundaments and Business Model

Company Overview – Who we are

Product & Technology Distribution Revenue model

Focus on SMB

• Low Penetration

• Leadership

• Fragmented

Competition

• Diversified Base

• Economy

Formalization

Flexibility

• Independence

• Agnostic

• Scalability

• Cloud Ready

• ERP by Industry and

by Size

• Social Network

Environment

• Mobile

Capillarity

• Franchise Model

• Regional

Entrepreneurship

• Exclusivity

• Client Ownership

• Aligned Interests

Full Control

• Growth Capturing

• Inflation Hedge

• Recurrence

• High retention rate

• Cyclic

7

Target Market – ERP in Brazil

(1)IBGE estimates about the Brazilian market. - http://www.sidra.ibge.gov.br/bda/pesquisas/cempre. Table 988. (2)”Valor 1000” Magazine, ed 2009. Companies with more than R$ 1Bi revenue. (3) Gartner “ SWOT: Totvs, Enterprise Application Software, Worldwide, 2010 ”

Employees

0 - 9

10 - 499

Revenue (R$)

Under R$1 Bi

Over R$1 Bi

4,620,905 (1)

618,486 (1)

288 (1)(2)

8,751(1)

# Companies

>= 500

Mega Large

Large

Medium

Small

Micro

ER

P M

ark

et P

en

etra

tion

8

Leadership in Brazil leverages the positioning in LatAm

Source: IDC - Latin America Software Tracker 2010

Target Market – Opportunity in Latin America

Brazil Market Size: USD 1.6 B

Rest of Latin America Market Size: USD 1.3 B

54% 46%

Latin America ERP Market in 2010: USD 2.9 Billion

Latam ERP Market Size Brazilian Transnational

Enterprise Activities

Source: FDC – Brazilian transnational enterprise ranking

9

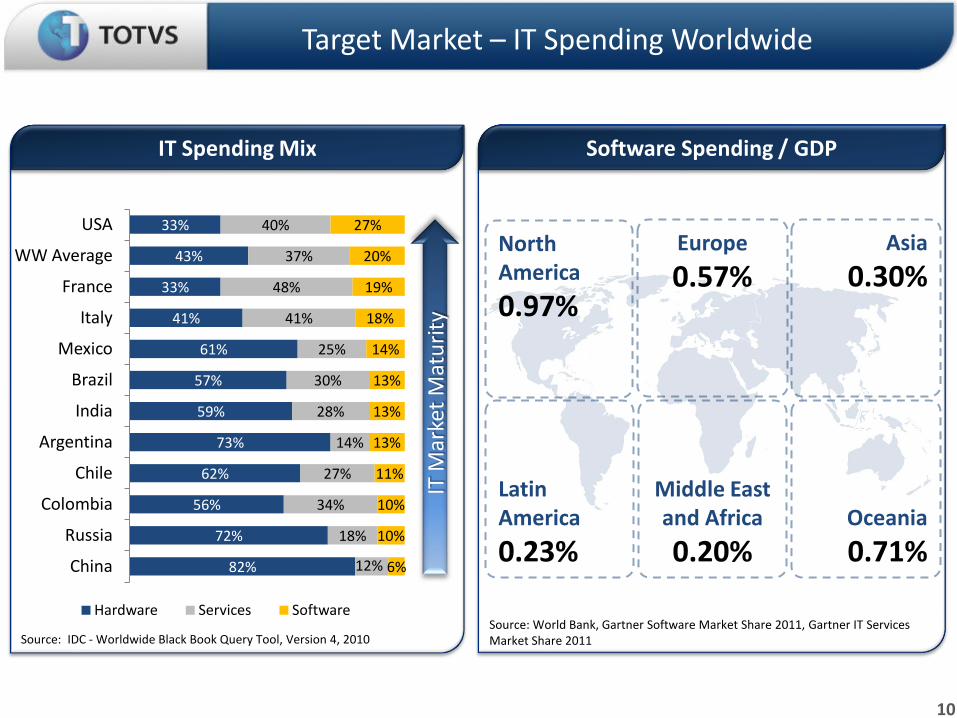

Target Market – IT Spending Worldwide

82%

72%

56%

62%

73%

59%

57%

61%

41%

33%

43%

33%

12%

18%

34%

27%

14%

28%

30%

25%

41%

48%

37%

40%

6%

10%

10%

11%

13%

13%

13%

14%

18%

19%

20%

27%

China

Russia

Colombia

Chile

Argentina

India

Brazil

Mexico

Italy

France

WW Average

USA

Hardware Services Software

Source: IDC - Worldwide Black Book Query Tool, Version 4, 2010

IT M

arke

t M

atu

rity

IT Spending Mix

Latin America

0.23%

North America

0.97%

Europe

0.57% Asia

0.30%

Oceania

0.71%

Middle East and Africa

0.20%

Software Spending / GDP

Source: World Bank, Gartner Software Market Share 2011, Gartner IT Services Market Share 2011

10

Product & Tech – Solution Overview

11

Decision Making Support • BI / DW / SGI / BSC / BA

Process, Content and Relationship

Management • Corporate Productivity

• Communication • Natural User Interface

Identity Management • Authenticated and

Certified Individuals and Companies

Enterprise Management • Back Office ERP • By Industry ERP

Human Capital Management • Enterprise Culture • Organization Development • Payroll

Consumer Management • Customized Attendant • Self-Service • Behavioral Analysis (Social CRM)

Anywhere • Smartphones / Tablets • Availability

Business Platform • Interaction, Share and

Collaboration • e-commerce (Store) • Supply Chain

TOTVS Arena

Product & Tech – Solution Overview

12

Collaboration among companies

• Single Sign-on • Information Ownership • SaaS (Software as a Service)

Available for posting on:

Product & Tech – Portfolio

Software Services

• TOTVS | Software Services Support / Implementation Technological Evolution Software Factory / SLA Training • TOTVS | Consulting Change Management / Processes Strategy Management / Performance PMO CSC • TOTVS | Outsourcing

e-Learning BPO Service Desk

• TOTVS | Marketplace

• TOTVS | Collaboration

Technology

• TOTVS | Cloud Computing

• TOTVS | Hardware

Series 1 | 3 | T

• TOTVS | Application Server

• TOTVS | DbAccess

• TOTVS | SmartClient

Standard HTML Mobile Social

• TOTVS | Developer Studio

• TOTVS | ECM

WCM BPM Content Management

• TOTVS | ESB

Corporate Management Infrastructure TOTVS | Platform

13

Product & Tech – ERP Core

ERP by Industries Functional adherence to the core business of each industry

Company Management • ERP by Industry Sector &

by Company Size

Agribusiness: Agricultural and Agribusiness Management | Cultivation, Cultural Procedures,

Harvest | Origination of Grains | Subcontracting | Fleet Maintenance | Automation in the Field

Construction and Projects: Work and Project Management | Merger Management | Viability

Analysis

Distribution & Logistics: Supply Chain | TMS | WMS | OMS | Fleet Maintenance |Shipper |

Harbor Customs Facilities

Education: Academic Management | Library | Distance Learning | Academic Portal | Selection

Process

Financial Services: Investment Management | Core Banking | Credit Management

Legal: Process Follow-up and Control | Schedule | Timesheet |Agreement, Customer and Team

Performance Management

Manufacturing: MPS | MRP | CRP | APS | Shop Floor Control | Industrial Automation | Asset

Maintenance | Environmental Management

Health: Health Plan and Affiliated Provider Management | Hospital Management | CCIH

Services: Service Agreement Management and SLA | Asset Maintenance

Retail: Store and POS | Magazine | Drugstore | OMS | Credit Management | Supply

Series 3

Series 1

Series T

14

Product & Tech – Facts by Industry

15

+1,110 extractive and processing customers, +1,000 metal and plastic, +1,400 capital goods

+900 department stores, +140 supermarkets, +280 building materials distributors

+2,300 services providers, +400 Utilities providers, +470 travel and passengers transportation

12 million lives, +9,700 beds, medical registers to 35 specialties

7 out of 10 top law firms, 10,000 lawyers

50 out of 100 Brazilian biggest companies

+20 international builders, +450 engineering and design customers

+200 sugarcane producers = 50% Brazilian harvest, +120 grain

producers, 1 million hectares

+1,600 wholesaler distributors, +600 freight companies

22k portfolios, 4k funds, 120k/day consumer credit transactions, R$1.5 trillion assets under custody, LatAm

Financial Market Top provider

+700 Brazilian institutions, +1.5 million students

Agribusiness

Construction and Projects

Distribution and Logistics

Educational

Financial Services

Legal

Health

Manufacturing

Retail

Services

Product & Tech – Software Implementation

To facilitate systems

deployment with

the highest return

Systems implementation

services according to the

size and complexity of

each TOTVS customer

16

Product & Tech – Consulting Services

To increase TOTVS

customers’ results Consulting service acts in

the core business and

administrative processes.

It promotes the

management maturity and

maximizes the investment

return.

17

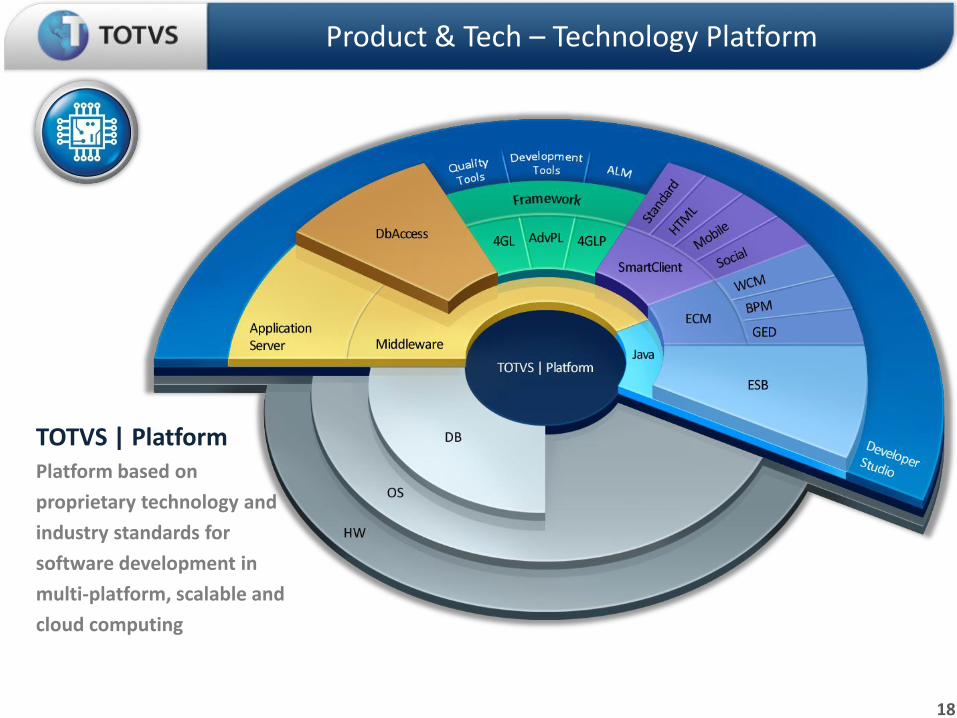

Product & Tech – Technology Platform

TOTVS | Platform Platform based on

proprietary technology and

industry standards for

software development in

multi-platform, scalable and

cloud computing

18

Native integration with TOTVS

Applications and Environment.

Advanced Cloud Computing, SOA and

BPM resources.

Integrated Development

Enjoinment, Tests and Life Cycle Manag.(*).

Technology by over 30 thousand

enterprises in the world.

TOTVS | Developer Studio: Customize, Create and Share Applications

(*) Supported Languages: Java / ADVPL++ / 4GL / 4GLP / .NET / NCL / LUA/ JavaTV / HTML5 Tools: Application Server, DbAcess e Ajax Server Interfaces: IT & TV Digital (Brazilian standard)

Product & Tech – Software Developer Kit (SDK)

TOTVS | Platform

19

Latin America

Brazil

►Distribution Channels: 5 Branches + 52 Franchisees

►~40 complementary channels working with TOTVS distribution network

►+5,200 Direct employees

Subsidiaries

Products

only

Franchises

►Products over 15 countries

►Excluding Brazil:

+300 direct employees

+13 Full TOTVS distribution channels

Distribution – Capillarity

Branch Franchise

Regional Presence and Entrepreneurship

20

Final Contact with Clients / Alignment of Interests

Franchise

Licenses

Services

Maintenance

Services

Licenses

Maintenance

Licenses Commissions

Maintenance Commissions

Proprietary Channel

Sales

Franchise Sales

Clients

Distribution – Channel Remuneration Model

21

Cyclical Model

New Customers

Base Customers

New Customers

Basic Implementation

Base Customers

New Licenses

New Modules

Consulting and

VAS+

Licenses

Services

Maintenance

New Licenses

Corporate Model Updates Upgrades

(New version) Help-desk

Y0 Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8

Traditional model

Corporate model

Recurring Fees by Metric

Entry Fee + Implementation

Y0 Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 … …

Revenue Model

22

23

Revenue Model

Net Revenue Breakdown (R$ million) ¹

Licenses Services Maintenance

High Recurrence and Predictability

(1) Pro forma figures for the year 2008 as the numbers include Datasul.

Consistent License Fee Revenue growth…

24

Financial Performance

Net License Fee Revenue (R$ million) 1

(1) Pro forma figures for the year 2008 as the numbers include Datasul.

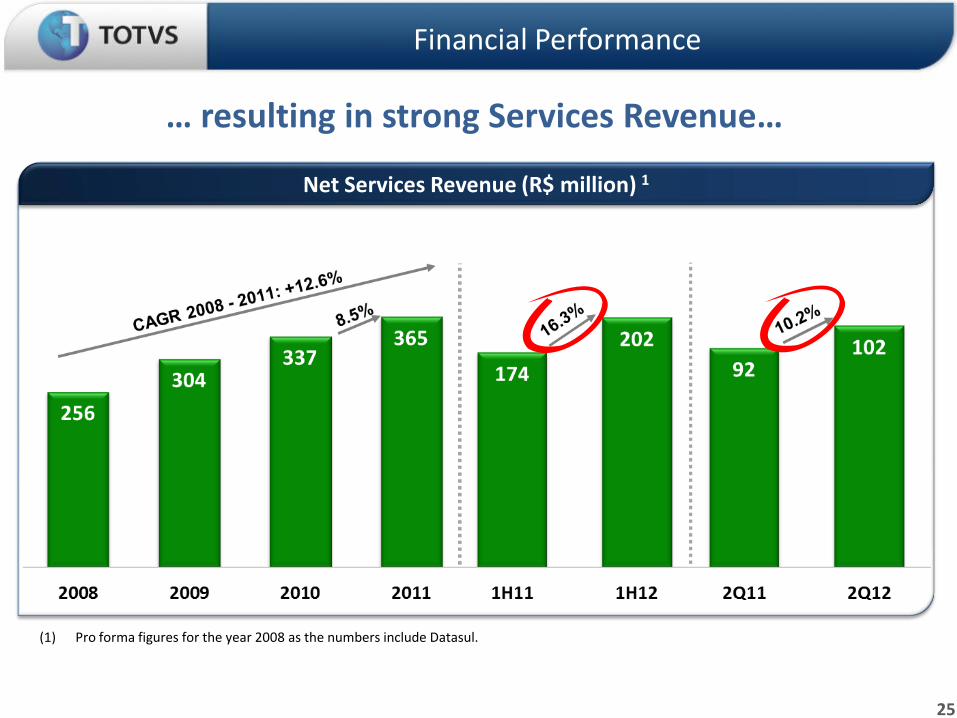

… resulting in strong Services Revenue…

25

Financial Performance

Net Services Revenue (R$ million) 1

(1) Pro forma figures for the year 2008 as the numbers include Datasul.

… and high levels of Maintenance Fee

26

Financial Performance

Net Maintenance Fee Revenue (R$ million) 1

(1) Pro forma figures for the year 2008 as the numbers include Datasul.

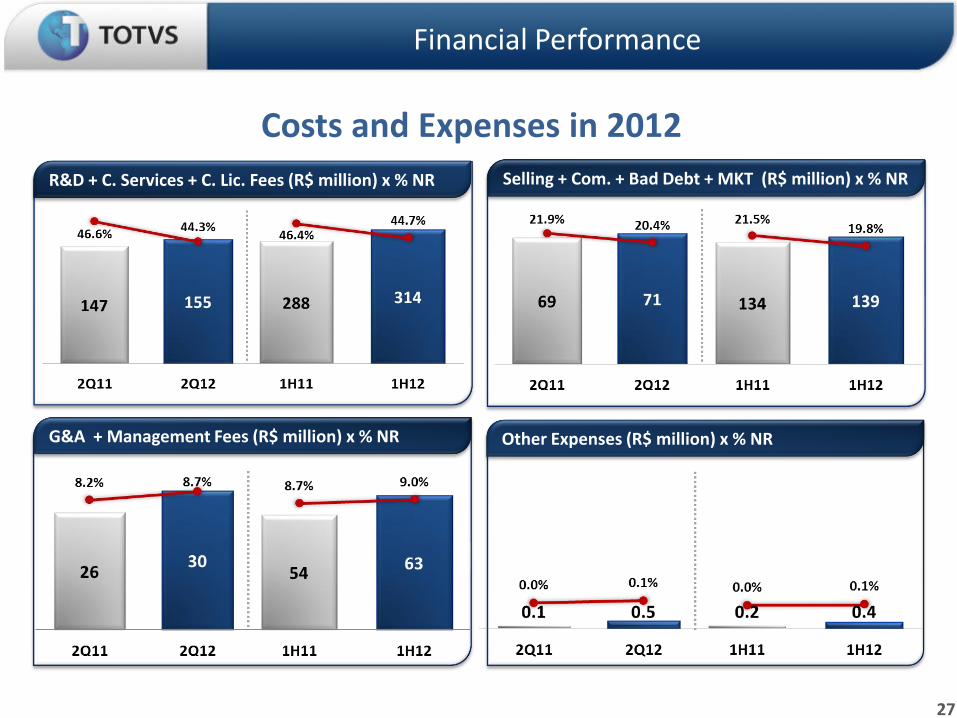

Costs and Expenses in 2012

27

Financial Performance

R&D + C. Services + C. Lic. Fees (R$ million) x % NR Selling + Com. + Bad Debt + MKT (R$ million) x % NR

G&A + Management Fees (R$ million) x % NR Other Expenses (R$ million) x % NR

EBITDA in 2012

28

2Q – Year over Year (R$ million) 1

Financial Performance

YTD – Year over Year (R$ million) 1

(1) Pro forma figures for the year 2008 as the numbers include Datasul.

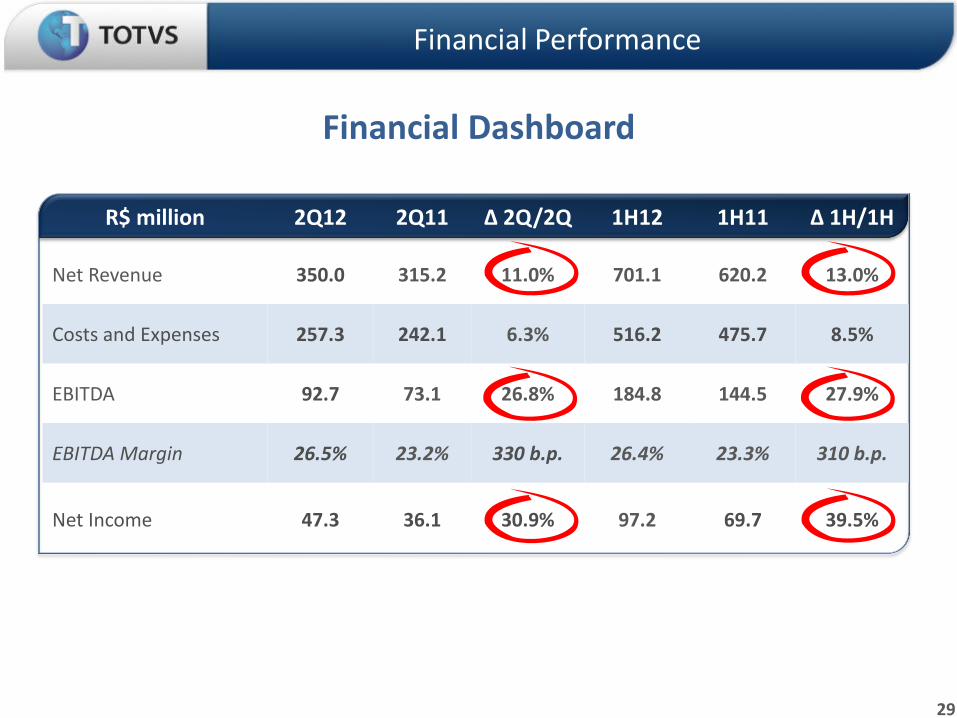

R$ million 2Q12 2Q11 Δ 2Q/2Q 1H12 1H11 Δ 1H/1H

Net Revenue 350.0 315.2 11.0% 701.1 620.2 13.0%

Costs and Expenses 257.3 242.1 6.3% 516.2 475.7 8.5%

EBITDA 92.7 73.1 26.8% 184.8 144.5 27.9%

EBITDA Margin 26.5% 23.2% 330 b.p. 26.4% 23.3% 310 b.p.

Net Income 47.3 36.1 30.9% 97.2 69.7 39.5%

Financial Dashboard

29

Financial Performance

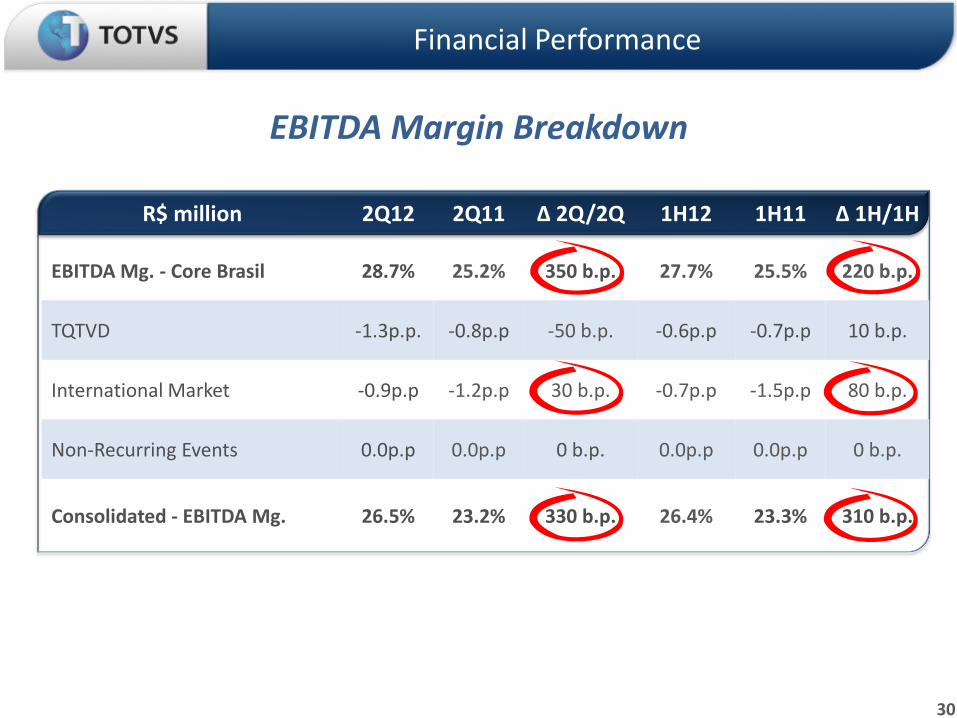

R$ million 2Q12 2Q11 Δ 2Q/2Q 1H12 1H11 Δ 1H/1H

EBITDA Mg. - Core Brasil 28.7% 25.2% 350 b.p. 27.7% 25.5% 220 b.p.

TQTVD -1.3p.p. -0.8p.p -50 b.p. -0.6p.p -0.7p.p 10 b.p.

International Market -0.9p.p -1.2p.p 30 b.p. -0.7p.p -1.5p.p 80 b.p.

Non-Recurring Events 0.0p.p 0.0p.p 0 b.p. 0.0p.p 0.0p.p 0 b.p.

Consolidated - EBITDA Mg. 26.5% 23.2% 330 b.p. 26.4% 23.3% 310 b.p.

EBITDA Margin Breakdown

30

Financial Performance

31

Financial Performance

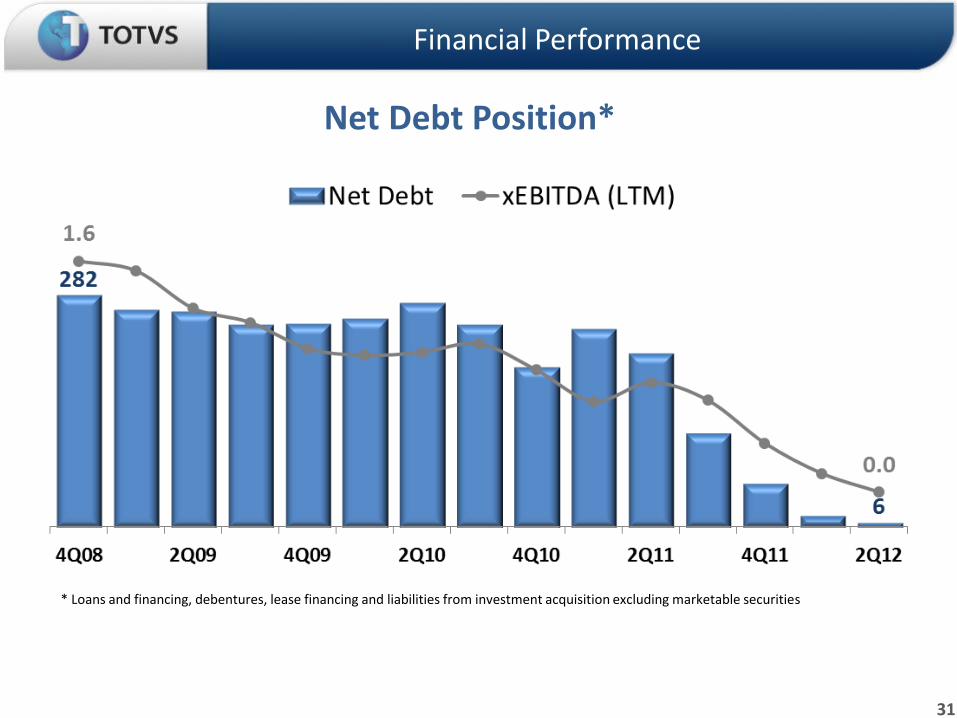

Net Debt Position*

* Loans and financing, debentures, lease financing and liabilities from investment acquisition excluding marketable securities

32

Financial Performance

Cash Flow and Debt

(*) The Debt informed comprehends (i) Loans and financing, (ii) Debentures, (iii) Current obligation under capital leases , (iv) Obligation relating to acquisitions and (v) Marketable securities.

TOTVS Vision

Company transformation into a global standard • Capturing internationalization of the Brazilian economy

• Geographical selectivity

• Brazil remains the cornerstone of our strategy

5th Phase

33

• by You • Branding • ECM • Private

• Specialization by Industry and Size • SaaS (Software as a Service) • Mobile • M&A

• Componentization & SW life cycle • Efficiency gains in Services & Development • International Market

Growth

Loyalty

Margin

Contacts

Safe harbor The material that follows is a presentation of general

background information about TOTVS activities as of the date of

the presentation in July 2012.

It is information given in summary form and does not purport to

be complete. It is not intended to be relied upon as advice to

potential investors.

This presentation may contain statements that express

management’s expectations and/or forecasts about future

events.

These expectations and/or forecasts involve risks and

uncertainties that could cause actual results to differ materially

from those projected in such forward-looking statements.

Therefore, the future results of the company may differ from

current expectations and readers must not base their

expectations exclusively on the information presented herein.

No representation or warranty, express or implied, is made

concerning, and no reliance should be placed on the accuracy,

fairness, or completeness of the information presented herein.

This document does not constitute an offer, or invitation, or

solicitation of an offer, to subscribe for or purchase any

securities. Neither this document nor anything contained herein

shall form the basis of any contract or commitment whatsoever.

QUESTIONS

www.totvs.com/ir

Year 2 Year 3 Year 4 Year 1 Year n ...

One solution for each stage of your company More than serving well, a better

understanding of your business