Embed Size (px)

Citation preview

Empowerment & Choice: Asset Building for People with

Disabilities

Jennifer L. NugentEmployment Specialist

Truman Employment Services

Real Voices Real Choices

August 20141

Asset Building

Asset building is a series of strategies that has the potential to help people with

disabilities improve their economic status, expand opportunities for community

participation, and positively impact quality of life.

2

Poverty Statistics for People with Disabilities

• 65% of disabled are unemployed– vs. 25% of non-disabled

• 3 times as many people with disabilities live in poverty• 39% of people with disabilities say lack of financial

resources is their biggest problem• People with disabilities earn 72% of nondisabled

earnings• Less than 10% of disabled own their own homes

– Vs. 70% of non-disabled

• 80% of disabled have no assets or in debt– vs. 33% of all Americans

3

Americans with Disabilities Act

“The nation’s proper goals regarding individuals with disabilities are to assure equality of opportunity, full participation, independent living, and economic self-sufficiency for such individuals.”

[42 U.S.C. 1201(a)(8) (2005)]

4

Barriers to Asset Development for People with Disabilities

• Eligibility requirements for many public benefit programs preclude individuals with disabilities from developing assets.

• You have to be poor to remain eligible– SSI– Medicaid– Food Stamps– Housing Subsidies

5

The American dream

What is your American dream?

6

Assets

• Assets are resources that retain value over time• Tangible Assets

– House– Stocks– Land

• Intangible Assets– Resilience– Education– Attitude– Spirituality/faith

7

People with Disabilities and Assets: Three Myths

• People with disabilities can’t work.– Work produces income which is the first step towards saving

and building assets.

• People with disabilities have all their needs met by their special programs.– People with disabilities want to reduce their reliance on

government benefits and have more freedom and independence.

• People with disabilities can’t be expected to save and build assets.– People with disabilities want a better economic future. They are

starting businesses and becoming homeowners.

8

Asset Development Cycle

9

Change the Paradigm!

• Shift focus from employment to financial stability

• There is no one simple solution to asset poverty

• Asset building is a series of strategies that can be used to support economic empowerment of people with disabilities

Start the conversation

• ASK:– Do you have a bank account?– Do you have a budget?

• American dream exercise

• Vision Board project– Help participant brainstorm on goals– Create a visual expression of dreams/goals

for the future

7 strategies

• Financial literacy and access to financial services

• Utilization of the Earned Income Tax Credit (EITC) and free tax preparation

• Individual Development Accounts• Homeownership• Microenterprise Development• SSA Work Incentives/ Benefits Planning• Pooled Trust

I. Financial Literacy & Access to Financial Services

• Financial education is about creating a budget and setting savings and asset goals.

Learn to Understand Money

• 2001 FDIC financial education program called “Money Smart”

• Goal is to provide money management skill-building and create positive relationships with banks

• Ten modules that take 1-2 hours to complete

• Interactive computer based curriculum available

Get Banked!

• Families with incomes under $20,000 per year spend an average of $500 per year to get a check cashed or pay bills

• 50% of people with disabilities do not have a savings or checking account

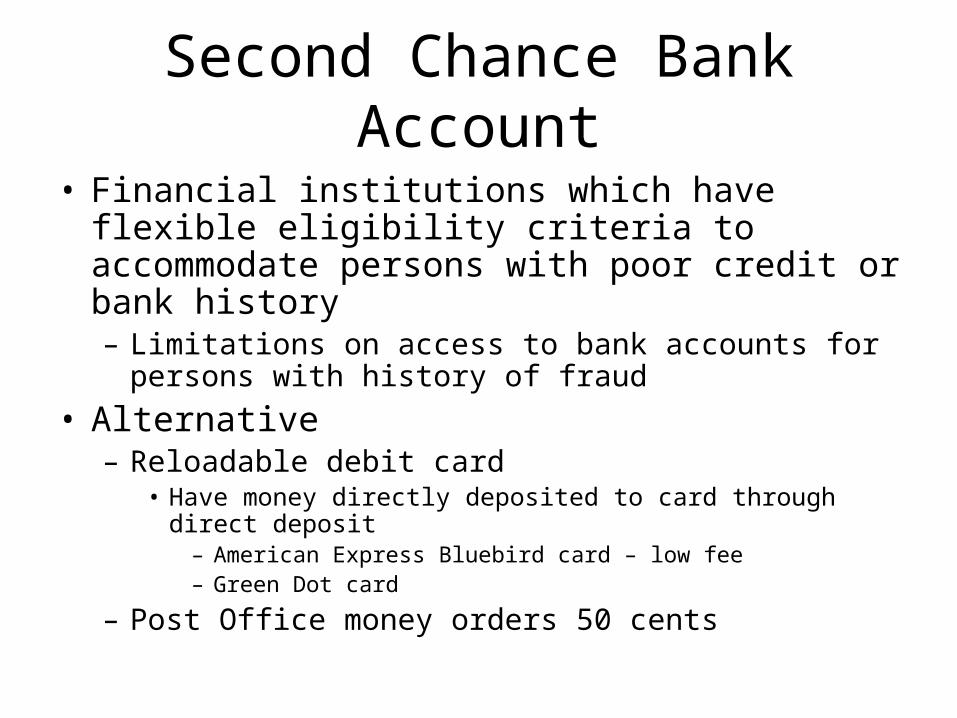

Second Chance Bank Account

• Financial institutions which have flexible eligibility criteria to accommodate persons with poor credit or bank history– Limitations on access to bank accounts for persons

with history of fraud

• Alternative– Reloadable debit card

• Have money directly deposited to card through direct deposit– American Express Bluebird card – low fee– Green Dot card

– Post Office money orders 50 cents

What can we do?

• Incorporate “Rate your financial behavior” worksheet into case management tools

• Assist participant to check credit report– Annualcreditreport.com – 3 free reports

• Include asset development goals in every treatment plan• Support a participant in developing a budget• Facilitate a Money Smart or other financial education

class• Support a participant in obtaining a bank account• Start a “money group” and provide access to trained

mentors

Resources for Strategy One• National Foundation for Credit Counseling (phone, online, or in

person credit counseling)– www.nfcc.org

• Bank On (second chance bank accounts)– www.joinbankon.org

• FDIC Money Smart (financial education)– www.fdic.gov/consumers/moneysmart/index.html

• Practical Money Skills for Life (financial education)– www.practicalmoneyskills.com/games

• Tomorrow’s Money– www.tomorrowsmoney.org

• Financial Entertainment– www.financialentertainment.org

• VISA Financial Soccer– www.realeconomicimpact.org

II. Utilize Earned Income Tax and Free Tax Preparation

• The EITC is the largest federal support program for low income individuals and families

• EITC helps over 15 million low-income wage earners each year

• It is estimated that over 1 million people with disabilities are not filing for the EITC

• 2013 IRS/NDI Real Economic Impact Tour – Assisted 500,000 people with disabilities with free tax

preparation– $400 million in tax refunds were received

• SSI recipients have 12 months to spendown tax refund

EITC facts

• Must have a valid SSN used for employment• Must have earned income• Age 25 – 65• 2013 Individual income limit $14,340

– Family limit $19,680 with no children

• Less than $3,300 in investment income• Single individual with no children 25-65

– Credit between $2 - $487

• Additional income guidelines for families with children

EITC Impact on Other Benefits

• EITC does not count as earned income and therefore does not impact eligibility for SSI

• EITC does not count as earned income for purposes of eligibility for Medicaid

• If you are filing for EITC for the first time, may file to claim the credit for a three-year period

Free Tax Preparation Resources

• VITA (Volunteer Income Tax Assistance)

• Call 2-1-1 to find nearest free prep site

• Call IRS 1-800-906-9887– www.irs.gov/individuals/Find-a-location-for-

FreeTax-Prep

• http://unitedwaygkc.org/Downloads/tax/2014_VITA_Sites.pdf

What can we do?

• ASK:– Have you worked during the past 3 years?– Did you file a tax return?– Did you know you may qualify to get money

back as a tax credit?

• Explain: EITC does not impact resource eligibility for SSI or Medicaid

• Publicize: Information on free tax clinics• Organize a shuttle to a VITA tax site

III: Individual Development Account (IDA)

• A matched savings program to support 3 goals– Home Ownership, Education, Starting a Business

• Must save from earnings (wages)• Federal vs. local programs:

– Federal: savings not counted as resources for eligibility purposes

– Local: a good source of savings but will count as resources for eligibility purposes; more useful for SSDI recipients

• Financial Education requirements

Eligibility

• 100-200% of FPL

• Net worth < $10,000– Excludes value of car or home

• May qualify if receive Earned Income Tax Credit (EITC)

Kansas City IDA Programs

• Federal: United Way/Catholic Charities– Youth 18-26– Savings for education– Wyandotte County– 1:8 match

• Local: Family Conservancy – 2:1 match – Maximum contribution $2,000

• New programs may be under development

III: Additional Resources

• Assets for Independence Resource Center– www.ida.resources.org

• Corporation for Enterprise Development– www.cfed.org/programs/idas

What can we do?

• Read about IDA’s and research new funding opportunities

• Review the American dream exercise with participants and explore possible goals & the appropriate IDA programs

• Host an IDA speaker to discuss their program

IV & V: Microenterprise Development and Homeownership

• Home ownership and business Development have been key asset building strategies for generations of Americans

• These goals require careful planning and bring new responsibilities

• People with disabilities can and do own homes and run businesses

Family Self-Sufficiency Program (FSS)

• HUD program

• Eligibility: recipients of Housing Choice vouchers (formerly Section 8)

• Participants set employment and self-sufficiency goals

• FSS coordinator enters into a 5 year contract with participant

FSS savings

• Currently, HUD residents pay 30% of their income as rent

• Ordinarily increases in income result in increases in rent

• Under FSS, participants may instead set aside that money in a special account

FSS program services

• FSS program services may include but are not limited to:– Childcare– Counseling– Transportation– Household Skill Training– Education– Job training– Homeownership Counseling

Use of escrow account

• There are no restrictions on the use of the funds in the escrow account

• Potential uses:– Capitalize a business– Purchase a home– Transportation– education

Housing Choice Homeownership Program

• HUD recipients may participate in a first-time homeownership program

• Participants with a disability must have annual income of at least $8,520 in 2013– Income may include SSI/SSDI

• Participants use their subsidy to pay mortgage, insurance, maintenance, insurance and utilities instead of paying rent to a landlord

• Voucher is good for 30 years• 3% down payment required

– 1% from voucher holder– 2% from outside sources such as IDA

IV & V: Resources

• Small Business Administration– www.sba.gov

• HUD– www.hud.gov/offices/pih/pha/contacts/states

What can we do?

• Identify participants with potential for self-employment– Work from home/accessibility issues– Opportunity for more independence in work environment– Transportation limitations

• Share case examples with participants• Advocate with VR for funding for self-employment

opportunities• Ongoing development of self-employment resource

guide• Learn more about SSA work incentives for self-

employment• Host a speaker from the SBA and/or HUD

VI: SSA Work incentives

SSA Work incentives are provisions which support individuals receiving SSI or SSDI to transition to work or to work while maintaining some benefits and health insurance coverage.

Plan to Achieve Self-Support (PASS)

• SSI beneficiary may set aside countable unearned income, countable income and resources to reach a specific work-related goal

• Funds in PASS are excluded for eligibility determination of SSI,HUD, and food stamps

• Must be approved by SSA• SSDI recipients are also eligible under certain

circumstances• Goal: to earn at least SGA and likelihood to

graduate off benefits

PASS Statistics

• In 2006 SSA stated that 1.5 million (37%) of SSI recipients had sufficient wages to set aside in a PASS– Nationwide there are only 1500 with a PASS

Property Essential for Self-Support

• PESS is property needed for self-support– Property owned and used in a business(farm)– Personal property used for work (tools)– Property used to produce goods or services

(loom)

• Up to $6,000 equity of non-business property is excluded as a resource

VI. Resources

• Social Security Administration– www.socialsecurity.gov

• Social Security Administration’s Red Book– www.socialsecurity.gov/redbook

What can you do?

• ASK:– Have you ever met with a benefits specialist?– Have you discussed the options of PASS or PESS?– What ideas do you have for starting your own

business?– What type of assistance would you need?

• Complete the American dream checklist with a participant

• Attend a “lunch and learn” session about SSA work incentives

• Identify your Truman benefits specialists and learn how to make a referral for participants

VII. Pooled Trusts

• Midwest Special Needs Trust provides a way for people to shelter/exclude extra savings and preserve eligibility for benefits

• Revocable and Irrevocable Trusts• For some trusts, funds may revert to the fund

upon death of participant• Expenditure of funds must be approved and may

only be used for reasonable extra expenses, not food, shelter or clothing which is provided for through SSI/SSDI payments

VII. Resources

• MO Special Needs Trust– http://www.midwestspecialneedstrust.org

What can we do?

• ASK– What are your wishes for your loved one’s

future?– Have you planned for their future financial

security?– Do you have resources you would like to save

for your future needs?

• Visit the Midwest Special Needs Trust website to learn more about pooled trusts in Missouri