Embed Size (px)

Citation preview

Page 1 of 18

Empire Oil & Gas Ltd (EGO)

Conven

tiona

l O

il &

Gas: P

rodu

ce

r / E

xplo

rer

Brief Business Description:

Hartleys Brief Investment Conclusion

Chairman & CEO:

Antonino (Tony) Iannello Chairman

Ken Aitken CEO

Substantial Shareholders:

ERM Power 19%

Philip Garrat 6%

Company Address:

Valuation: $0.753

Issued Capital: 10,205

- fully diluted 10,377

Market Cap: $40.8m

- fully diluted $41.5m

Current Debt

Current Cash

FY14 FY15F FY16F

Prod (TJ) 1,855 2,876 3,060

Op Cash Flw -$6m $0m $13m

Free Cash Flw -$9m -$21m -$2m

NPAT* (A$m) -$2m $4m $5m

EPS ($, bas)* -0.02x 0.04x 0.05x

P/E (basic)* -18.3x 10.2x 7.6x

EV / EBIT -20.1x 11.0x 7.0x

EV / EBITDA 24.9x 4.0x 3.1x

N.D. / equity 2% 4% 7%

Net Cash End $1.9m -$1.6m -$3.8m

*normalised

Source: Hartleys Research

Authors:

Simon Andrew

Oil and Gas Analyst

Ph: +61 8 9268 3020

$14.4m

$12.9m

EGO is a gas producer and explorer with a core

focus on the Perth Basin. Key asset is the Red

Gully Gas plant

EGO should start generating cash flow from gas

sales for the first time since the start-up of the Red

Gully Gas plant. The drilling of the Red Gully North-

1 exploration well, expected before the end of

CY15, is the most significant near term catalyst for

the stock price.

229 Stirling Highway

Claremont

12mth Price Target: $0.0075

EGO.asxSpeculative Buy

16 Sep 2015

Share Price: $0.0040

EMPIRE OIL & GAS NL (EGO)

Ego is not a dirty word….. We initiate coverage of Empire Oil and Gas Ltd (EGO) with a Speculative

Buy recommendation and a 12-month target price of 0.75cps, 50% upside

from the current share price. EGO has started generating cash flow from

gas sales for the first time since the start-up of the Red Gully Gas plant. A

recent reserve upgrade ensures that EGO can deliver Tranche-2 of the

Alcoa GSA plus have an additional 2PJ of gas for sale. The drilling of the

Red Gully North-1 exploration well, expected before the end of CY15, is the

most significant near term catalyst for the stock price.

About to move from a producer to a cash generator EGO management has provided FY16 revenue guidance of A$23m. The

significant increase in net revenue will be generated by EGO entering

Tranche 2 of the Alcoa GSA. Tranche 2 of the GSA requires delivery of

10PJ of gas to Alcoa, for which EGO will receive a previously negotiated

gas price. The price has not been disclosed to the market however we

assume it to be A$6.5/Gj. We estimate that EGO will generate A$13m in

operating cash flow in FY16. During Tranche 1, EGO delivered circa 5PJ of

gas that had been prepaid (therefore EGO did not receive any cash flow).

Red Gully-1 reserve upgrade EGO recently announced a 64% increase in 1P reserves from the Red

Gully-1 B Sand to 12.2PJ. Upgraded reserves are now sufficient to cover

Tranche-2 of the Alcoa GSA (10 PJ) plus an additional 2PJ of uncontracted

gas. EGO has already identified potential customers for the excess gas.

Drilling the Red Gully North prospect in 4Q CY15 The Red Gully North prospect is expected to be drilled in 4Q CY15. The well

cost is estimated at A$10m (dry hole cost) with an additional A$2m required

to test and complete. We regard the well as relatively low risk, as it is testing

up-dip of a known gas discovery (Gingin-1), off modern seismic and using

modern drilling and completion techniques. EGO estimates that a successful

outcome from Red Gully North could add an additional 5TJ/d of production.

This would require the plant capacity to be increased above the current

10TJ/d.

Debt refinancing We expect EGO to refinance the A$15.1m in debt, currently outstanding

with ERM Power, before the end of this year. The current debt facility is

interest free and due in August 2016, but carries significant escalation

clause should the EGO share price appreciate above 0.8cps.

Valuation and recommendation We value EGO at 0.75cps. At the core of our valuation is the Red Gully gas

operation, valued at A$43m or 0.42cps. The remainder of our 0.75cps

valuation is made op from Red Gully North (0.11cps), Gin-Gin East and

other exploration (0.23cps). EGO’s net debt at the end of FY15 was

estimated to be A$2m. EGO management has indicated an intention to

consolidate the current shares on issue. The history of share consolidations

on the ASX suggests that there may be a period of share price weakness

immediately after the consolidation. In our view, consolidation is required if

the EGO share register is to mature. The major risk to our recommendation

is disappointing results from the Red-Gully North exploration well. EGO

does have commodity price exposure via condensate prices.

Hartleys Limited ABN 33 104 195 057 (AFSL 230052) 141 St Georges Terrace, Perth, Western Australia, 6000

Hartleys does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single

factor in making their investment decision. Further information concerning Hartleys’ regulatory disclosures can be found on Hartleys

website www.hartleys.com.au

0.00

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008

0.009

.

20.

40.

60.

80.

100.

120.

140.

Sep-15May-15Jan-15Oct-14

Volume - RHS

EGO Shareprice - LHS

Sector (S&P/ASX SMALL RESOURCES) - LHS

A$ M

Empire Oil & Gas

Source: IRESS

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 2 of 18

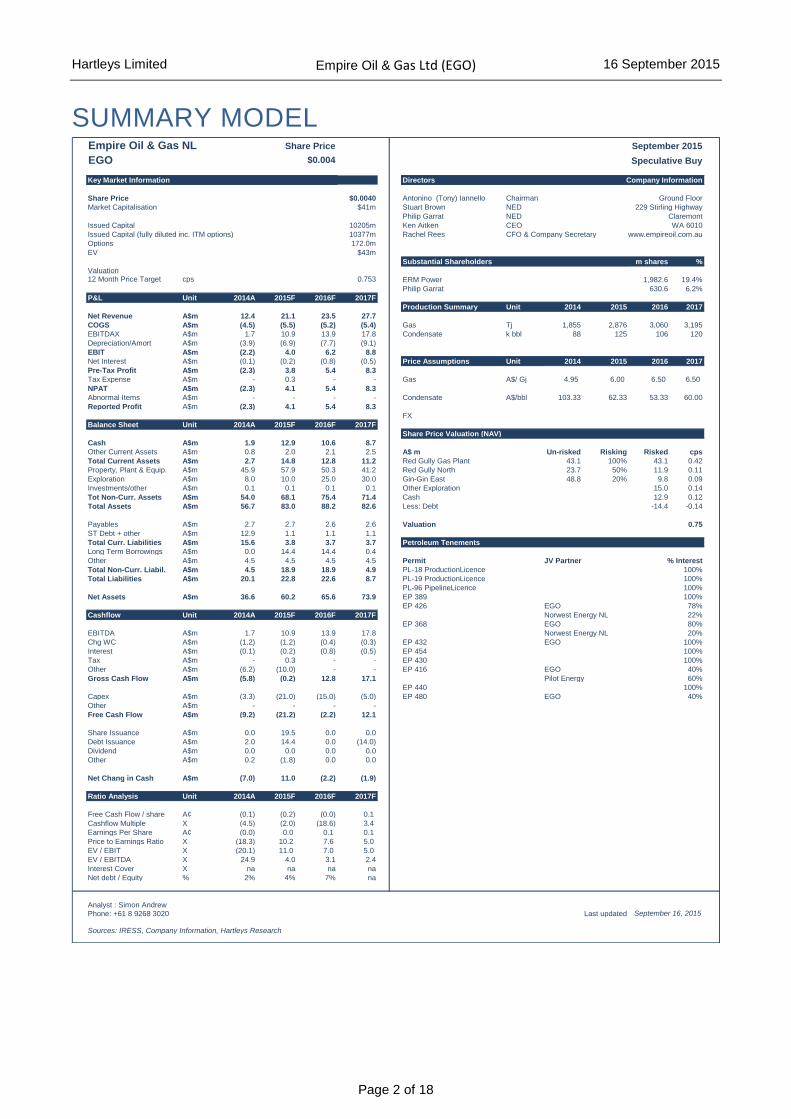

SUMMARY MODEL

Empire Oil & Gas NL Share Price

EGO $0.004 Speculative Buy

Key Market Information Directors Company Information

Share Price $0.0040 Antonino (Tony) Iannello Chairman Ground Floor

Market Capitalisation $41m Stuart Brown NED 229 Stirling Highway

Philip Garrat NED Claremont

Issued Capital 10205m Ken Aitken CEO WA 6010

Issued Capital (fully diluted inc. ITM options) 10377m Rachel Rees CFO & Company Secretary www.empireoil.com.au

Options 172.0m

EV $43m

Substantial Shareholders m shares %

Valuation 212 Month Price Target cps 0.753 3 ERM Power 1,982.6 19.4%

5 Philip Garrat 630.6 6.2%

P&L Unit 2014A 2015F 2016F 2017F 6

7 Production Summary Unit 2014 2015 2016 2017

Net Revenue A$m 12.4 21.1 23.5 27.7 8

COGS A$m (4.5) (5.5) (5.2) (5.4) 9 Gas Tj 1,855 2,876 3,060 3,195

EBITDAX A$m 1.7 10.9 13.9 17.8 10 Condensate k bbl 88 125 106 120

Depreciation/Amort A$m (3.9) (6.9) (7.7) (9.1)

EBIT A$m (2.2) 4.0 6.2 8.8

Net Interest A$m (0.1) (0.2) (0.8) (0.5) Price Assumptions Unit 2014 2015 2016 2017

Pre-Tax Profit A$m (2.3) 3.8 5.4 8.3

Tax Expense A$m - 0.3 - - Gas A$/ Gj 4.95 6.00 6.50 6.50

NPAT A$m (2.3) 4.1 5.4 8.3

Abnormal Items A$m - - - - Condensate A$/bbl 103.33 62.33 53.33 60.00

Reported Profit A$m (2.3) 4.1 5.4 8.3

FX

Balance Sheet Unit 2014A 2015F 2016F 2017F

Share Price Valuation (NAV)

Cash A$m 1.9 12.9 10.6 8.7

Other Current Assets A$m 0.8 2.0 2.1 2.5 A$ m Un-risked Risking Risked cps

Total Current Assets A$m 2.7 14.8 12.8 11.2 Red Gully Gas Plant 43.1 100% 43.1 0.42

Property, Plant & Equip. A$m 45.9 57.9 50.3 41.2 Red Gully North 23.7 50% 11.9 0.11

Exploration A$m 8.0 10.0 25.0 30.0 Gin-Gin East 48.8 20% 9.8 0.09

Investments/other A$m 0.1 0.1 0.1 0.1 Other Exploration 15.0 0.14

Tot Non-Curr. Assets A$m 54.0 68.1 75.4 71.4 Cash 12.9 0.12

Total Assets A$m 56.7 83.0 88.2 82.6 Less: Debt -14.4 -0.14

Payables A$m 2.7 2.7 2.6 2.6 Valuation 0.75

ST Debt + other A$m 12.9 1.1 1.1 1.1

Total Curr. Liabilities A$m 15.6 3.8 3.7 3.7 Petroleum Tenements

Long Term Borrowings A$m 0.0 14.4 14.4 0.4

Other A$m 4.5 4.5 4.5 4.5 Permit JV Partner % Interest

Total Non-Curr. Liabil. A$m 4.5 18.9 18.9 4.9 PL-18 Production Licence 100%

Total Liabilities A$m 20.1 22.8 22.6 8.7 PL-19 Production Licence 100%

PL-96 Pipeline Licence 100%

Net Assets A$m 36.6 60.2 65.6 73.9 EP 389 100%

EP 426 EGO 78%

Cashflow Unit 2014A 2015F 2016F 2017F Norwest Energy NL 22%

EP 368 EGO 80%

EBITDA A$m 1.7 10.9 13.9 17.8 Norwest Energy NL 20%

Chg WC A$m (1.2) (1.2) (0.4) (0.3) EP 432 EGO 100%

Interest A$m (0.1) (0.2) (0.8) (0.5) EP 454 100%

Tax A$m - 0.3 - - EP 430 100%

Other A$m (6.2) (10.0) - - EP 416 EGO 40%

Gross Cash Flow A$m (5.8) (0.2) 12.8 17.1 Pilot Energy 60%

EP 440 100%

Capex A$m (3.3) (21.0) (15.0) (5.0) EP 480 EGO 40%

Other A$m - - - -

Free Cash Flow A$m (9.2) (21.2) (2.2) 12.1

Share Issuance A$m 0.0 19.5 0.0 0.0

Debt Issuance A$m 2.0 14.4 0.0 (14.0)

Dividend A$m 0.0 0.0 0.0 0.0

Other A$m 0.2 (1.8) 0.0 0.0

Net Chang in Cash A$m (7.0) 11.0 (2.2) (1.9)

Ratio Analysis Unit 2014A 2015F 2016F 2017F

Free Cash Flow / share A¢ (0.1) (0.2) (0.0) 0.1

Cashflow Multiple X (4.5) (2.0) (18.6) 3.4

Earnings Per Share A¢ (0.0) 0.0 0.1 0.1

Price to Earnings Ratio X (18.3) 10.2 7.6 5.0

EV / EBIT X (20.1) 11.0 7.0 5.0

EV / EBITDA X 24.9 4.0 3.1 2.4

Interest Cover X na na na na

Net debt / Equity % 2% 4% 7% na

Analyst : Simon Andrew

Phone: +61 8 9268 3020 Last updated

Sources: IRESS, Company Information, Hartleys Research

September 2015

September 16, 2015

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 3 of 18

INVESTMENT THESIS We initiate coverage of Empire Oil and Gas Ltd (EGO) with a Speculative Buy

recommendation and a 12-month target price of 0.75cps, 50% upside from the

current share price. EGO has started generating cash flow from gas sales for the

first time since the start-up of the Red Gully Gas plant. A recent reserve upgrade

ensures that EGO can deliver Tranche-2 of the Alcoa GSA plus have an additional

2PJ of gas for sale. The drilling of the Red Gully North-1 exploration well, expected

before the end of CY15, is the most significant near term catalyst for the stock

price.

Significant increase in cash generation expected in FY16 and beyond. EGO

management has provided FY16 revenue guidance of A$23m. The significant

increase in net revenue will be generated by EGO entering Tranche 2 of the Alcoa

GSA. Tranche 2 of the GSA requires delivery of 10PJ of gas to Alcoa, for which

EGO will receive a previously negotiated gas price. The price has not been

disclosed to the market however we assume it to be A$6.5/Gj. We estimate that

EGO will generate A$13m in operating cash flow in FY16. During Tranche 1, EGO

delivered 5PJ of gas that had been prepaid (therefore EGO did not receive

associated cash flow).

EGO expects to drill the Red Gully North prospect in 4Q CY15. EGO expect

the well to cost A$10m (dry hole cost), with an additional estimate of A$2m to test

and complete. The well is regarded as low risk as it is testing the up-dip of a

known gas discovery (Gingin-1) using modern seismic and will employ modern

drilling and completion techniques. EGO estimates that a successful outcome from

Red Gully North could add an additional 5TJ/d of production, which would require

the plant capacity to be increased above the current 10TJ/d.

AWE – recent success in the Perth Basin. AWE’s recent exploration and

appraisal success has helped the market refocus on the Perth Basin. In 2014 AWE

discovered the Waitsia gas field located on permits L1/L2 (AWE 50% and operator

/ Origin 50%). Permits L1/L2 lie immediately the west of Block EP 368 and EP

426, both operated by EGO. Following completion of the Waitsia-1 and Waitsia-2

appraisal wells AWE was able to increase their estimate of total gross recoverable

gas (P50) from 290 Bcf to 484 Bcf.

Other events and catalysts

Debt refinancing. We expect EGO to refinance the A$15.1m in debt currently

outstanding with ERM Power (ERM). The current debt facility is interest free

and due in August 2016 but carries an escalation clause should the EGO share

price appreciate above 0.8cps (see page 17).

Share consolidation. EGO management has indicated an intention to

consolidate the current shares on issue. The history of share consolidations on

the ASX suggests that there may be a period of share price weakness

immediately after the consolidation. In our view, consolidation is required if the

EGO share register is to mature.

Valuation and Target Price. We value EGO at 0.75cps. At the core of our

valuation is the Red Gully gas operation, valued at A$43m or 0.42cps. The

remainder of our 0.75cps valuation is made op from Red Gully North (0.11cps),

Gin-Gin East and other exploration (0.23cps). EGO’s net debt at the end of FY15

was estimated to be A$2m.. EGO management has indicated an intention to

Init iate coverage of

EGO with a

Speculative Buy and

12-month target price

of 0.8cps – 60%

upside from the

current share pr ice

Dril l ing of Red Gul ly -

North prospect

expected before the

end of FY15

AWE’s recent success

has drawn at tent ion

back to the Perth

Basin

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 4 of 18

consolidate the current shares on issue. The history of share consolidations on the

ASX suggests that there may be a period of share price weakness immediately

after the consolidation. In our view, consolidation is required if the EGO share

register is to mature.

The major risk to our recommendation is disappointing results from the Red-Gully

North exploration well. Whilst EGO’s gas sales price is largely fixed, the Company

does have commodity price exposure via condensate prices.

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 5 of 18

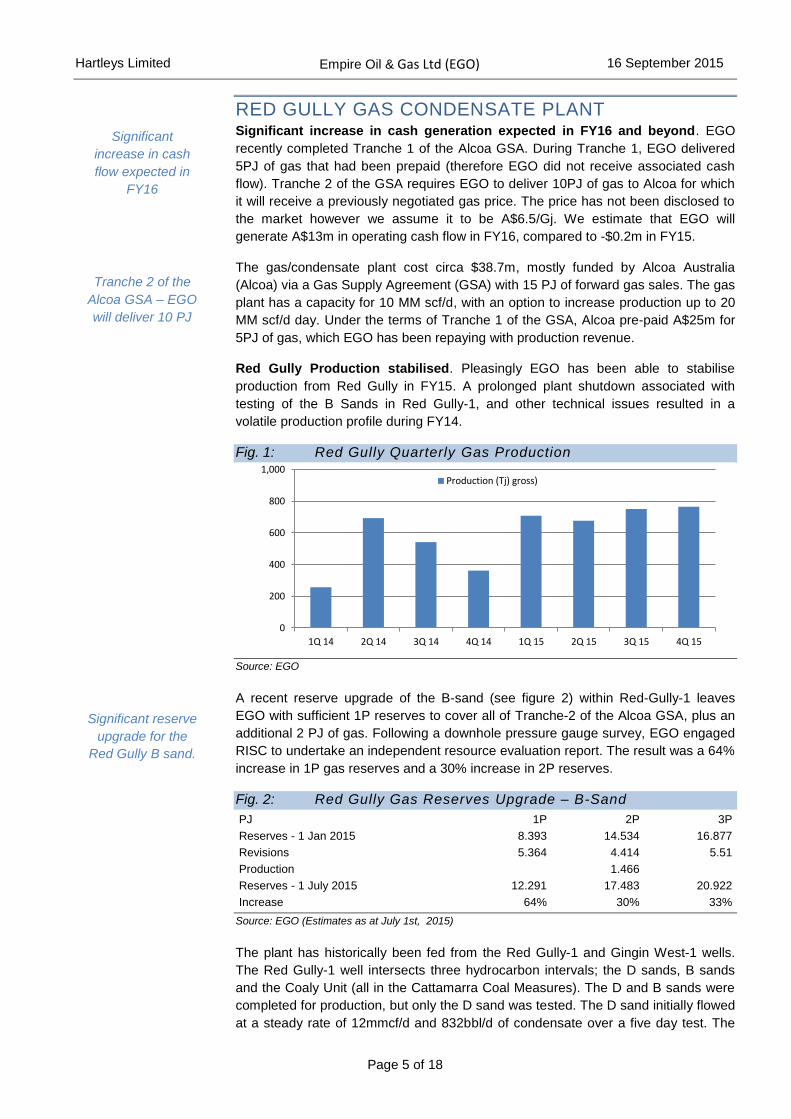

RED GULLY GAS CONDENSATE PLANT Significant increase in cash generation expected in FY16 and beyond. EGO

recently completed Tranche 1 of the Alcoa GSA. During Tranche 1, EGO delivered

5PJ of gas that had been prepaid (therefore EGO did not receive associated cash

flow). Tranche 2 of the GSA requires EGO to deliver 10PJ of gas to Alcoa for which

it will receive a previously negotiated gas price. The price has not been disclosed to

the market however we assume it to be A$6.5/Gj. We estimate that EGO will

generate A$13m in operating cash flow in FY16, compared to -$0.2m in FY15.

The gas/condensate plant cost circa $38.7m, mostly funded by Alcoa Australia

(Alcoa) via a Gas Supply Agreement (GSA) with 15 PJ of forward gas sales. The gas

plant has a capacity for 10 MM scf/d, with an option to increase production up to 20

MM scf/d day. Under the terms of Tranche 1 of the GSA, Alcoa pre-paid A$25m for

5PJ of gas, which EGO has been repaying with production revenue.

Red Gully Production stabilised. Pleasingly EGO has been able to stabilise

production from Red Gully in FY15. A prolonged plant shutdown associated with

testing of the B Sands in Red Gully-1, and other technical issues resulted in a

volatile production profile during FY14.

Fig. 1: Red Gully Quarterly Gas Production

Source: EGO

A recent reserve upgrade of the B-sand (see figure 2) within Red-Gully-1 leaves

EGO with sufficient 1P reserves to cover all of Tranche-2 of the Alcoa GSA, plus an

additional 2 PJ of gas. Following a downhole pressure gauge survey, EGO engaged

RISC to undertake an independent resource evaluation report. The result was a 64%

increase in 1P gas reserves and a 30% increase in 2P reserves.

Fig. 2: Red Gully Gas Reserves Upgrade – B-Sand

Source: EGO (Estimates as at July 1st, 2015)

The plant has historically been fed from the Red Gully-1 and Gingin West-1 wells.

The Red Gully-1 well intersects three hydrocarbon intervals; the D sands, B sands

and the Coaly Unit (all in the Cattamarra Coal Measures). The D and B sands were

completed for production, but only the D sand was tested. The D sand initially flowed

at a steady rate of 12mmcf/d and 832bbl/d of condensate over a five day test. The

0

200

400

600

800

1,000

1Q 14 2Q 14 3Q 14 4Q 14 1Q 15 2Q 15 3Q 15 4Q 15

Production (Tj) gross)

PJ 1P 2P 3P

Reserves - 1 Jan 2015 8.393 14.534 16.877

Revisions 5.364 4.414 5.51

Production 1.466

Reserves - 1 July 2015 12.291 17.483 20.922

Increase 64% 30% 33%

Significant

increase in cash

flow expected in

FY16

Tranche 2 of the

Alcoa GSA – EGO

will deliver 10 PJ

Significant reserve

upgrade for the

Red Gully B sand.

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 6 of 18

Gingin West-1 well tested the top D sand and flowed at a steady rate of 7.5mmcf/d

and 375bbl/d of condensate over a four day test.

The Company has also identified additional local potential of 205bcf of gas and

9.2mmbbl of condensate. This includes the gas/condensate discovered in the Gingin

field.

Fig. 3: EP389 Prospects

Source: Empire Oil and Gas Ltd

Historic exploration in the area includes the Gingin-1 and 2 wells and the Bootine

well. Gingin-1 was drilled in 1964 and initially flowed at a peak rate of 3.8mmcf/d.

Following a frac in 1971, the well was put onto production at a rate of 5mmcf/d.

However, the well declined quickly and production ceased after approximately 10

months. The well was brought back into production in 1975 at a lesser rate but only

produced for six months. Total production from Gingin-1 was 1.7bcf. Poor

permeability is blamed for the rapid decline. Gingin-2 and Bootine-1 both flowed

hydrocarbons in excess of 2mmcf/d, however, neither well was considered

commercial.

EGO commissioned RPS Energy Services Pty Ltd (RPS) to prepare a study on the

unconventional gas potential within EP389. The study found the potential for

undiscovered gas in place of 40 – 140Bcf per square kilometre. EGO has interpreted

the results to indicate approximately 24Tcf of gas in place within the permit.

Previous wells

in the area

produced

strongly but

declined rapidly

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 7 of 18

DRILLING OF RED GULLY NORTH EGO expects to drill the Red Gully North prospect in 4Q CY15. Together with

the start of Tranche 2 of the Alcoa GSA, this is the most significant catalyst

over the next 6 months. The well cost is estimated at A$10m (dry hole cost) with

an additional estimate of A$2m to test and complete. The well is regarded as low risk

as it is testing up-dip of a known gas discovery (Gingin-1) off modern seismic and

using modern drilling and completion techniques. EGO estimate that a successful

outcome from Red Gully North could add an additional 3TJ/d from the Red Gully

processing plant. The Gingin field is estimated to contain 2C Contingent Resource of

7.9PJ and Best Estimate Prospective Resource of 4.9PJ

The Red Gully North prospect lies within EP389 (EGO 100%) with the well location

sitting 470m from the Gingin-1 discovery. Importantly the well location is only

4km from the Red Gully processing plant. In March EGO signed a drilling contract

with Enderdrill. In addition to the Red Gully North well the drilling contract gives EGO

the option to drill a further four wells.

Gingin-1 discovery. The Gingin-1 well was drilled by WAPET in 1964-5 to test the

northerly trending Gingin anticline. Encouraging gas shows led to the drilling of

Gingin-2 by WAPET in 1965-66. Gingin-1 and Gingin-2 were drilled to depth of

4544m and 4482m respectively.

The results of Gingin-1 were encouraging enough for the operator to flow test the

well. The 6 most productive zones all occurred within the Cattamarra Coal Measures

(Early Jurassic). The most productive interval flowed 3.85 MMcf/d and small volumes

of 460API condensate. In 1971 the 3 most productive intervals flowed a

combined 13MMcf/d for a short period (GSWA Report 43, A. Crostella, 1995). A

longer term flow test in 1972 produced 5 MMcf/d, which was fed into the Dongara-

Perth pipeline. Gingin-2 was also flow tested but did not produce commercial

quantities of hydrocarbons.

Fig. 4: Red Gully North and Gingin East

Source: EGO

EGO expects to

drill the Red Gully

North prospect in

4Q CY15

Importantly the

well location is

only 4km from the

Red Gully

processing plant.

3 most productive

intervals were

fractured and

flowed a

combined 13

MMcf/d for a short

period

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 8 of 18

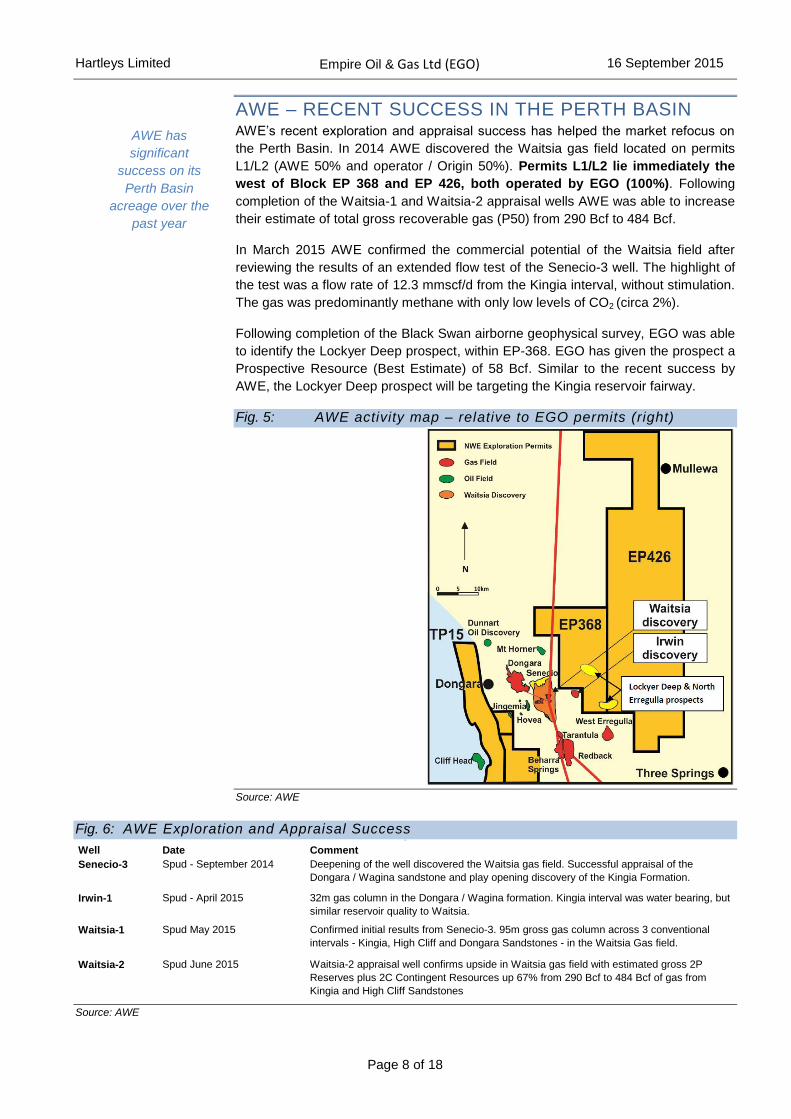

AWE – RECENT SUCCESS IN THE PERTH BASIN AWE’s recent exploration and appraisal success has helped the market refocus on

the Perth Basin. In 2014 AWE discovered the Waitsia gas field located on permits

L1/L2 (AWE 50% and operator / Origin 50%). Permits L1/L2 lie immediately the

west of Block EP 368 and EP 426, both operated by EGO (100%). Following

completion of the Waitsia-1 and Waitsia-2 appraisal wells AWE was able to increase

their estimate of total gross recoverable gas (P50) from 290 Bcf to 484 Bcf.

In March 2015 AWE confirmed the commercial potential of the Waitsia field after

reviewing the results of an extended flow test of the Senecio-3 well. The highlight of

the test was a flow rate of 12.3 mmscf/d from the Kingia interval, without stimulation.

The gas was predominantly methane with only low levels of CO2 (circa 2%).

Following completion of the Black Swan airborne geophysical survey, EGO was able

to identify the Lockyer Deep prospect, within EP-368. EGO has given the prospect a

Prospective Resource (Best Estimate) of 58 Bcf. Similar to the recent success by

AWE, the Lockyer Deep prospect will be targeting the Kingia reservoir fairway.

Fig. 5: AWE activity map – relative to EGO permits (right)

Source: AWE

Fig. 6: AWE Exploration and Appraisal Success xxx

Source: AWE

Well Date Comment

Senecio-3 Spud - September 2014 Deepening of the well discovered the Waitsia gas field. Successful appraisal of the

Dongara / Wagina sandstone and play opening discovery of the Kingia Formation.

Irwin-1 Spud - April 2015 32m gas column in the Dongara / Wagina formation. Kingia interval was water bearing, but

similar reservoir quality to Waitsia.

Waitsia-1 Spud May 2015 Confirmed initial results from Senecio-3. 95m gross gas column across 3 conventional

intervals - Kingia, High Cliff and Dongara Sandstones - in the Waitsia Gas field.

Waitsia-2 Spud June 2015 Waitsia-2 appraisal well confirms upside in Waitsia gas field with estimated gross 2P

Reserves plus 2C Contingent Resources up 67% from 290 Bcf to 484 Bcf of gas from

Kingia and High Cliff Sandstones

AWE has

significant

success on its

Perth Basin

acreage over the

past year

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 9 of 18

ASSET OVERVIEW EGO holds a large acreage position in the Perth Basin. Following the divestment by

ERM of their interest in joint ventured assets, EGO now has high equity interest in all

of its Perth basin acreage (see Figure 5). In 2014 ERM agreed to sell its interest in

EP389, including the Red Gully Gas plant plus other tenements to EGO for

A$15.1m. Part of this transaction included EGO raising $7.5m via a placement of

share to ERM after which ERM holds a 19.4% stake in EGO.

The Red Gully North and Gingin East prospects both sit within EP 389 (100% EGO).

Fig. 7: EGO – Perth Basin asset overview

Source: EGO

NORTH PERTH BASIN EXPLORATION

EP368 (80%), Operator & EP426 (78%), Operator The North Erregulla prospect straddles EP426 and EP368.

In early 2012, Origin Energy Ltd (ORG) agreed to farm into EP368 and EP426 for

40% by free carrying all parties, except Norwest Energy NL, on a 100km2 3D seismic

survey program over the North Erregulla prospect. However, Origin has since

terminated the farm-in agreement.

The North Erregulla prospect was originally drilled in 1967. Wireline logs and drill

stem tests proved there was a 3 metre column of live oil in the Wagina formation.

The prospect was drilled as a tilted fault block target following oil shows at the

Erregulla-1 well which encountered a seven metre oil column that showed a small

amount of oil in the Cockleshell Gully Formation.

West Erregulla-1 was drilled in 1990 as a follow up to North Erregulla-1. No oil was

encountered but a small flow of gas was measured in the Basal Triassic Sandstone.

Permit JV Partner % Interest

PL-18 Production Licence 100%

PL-19 Production Licence 100%

PL-96 Pipeline Licence 100%

EP 389 100%

EP 426 EGO 78%

Norwest Energy NL 22%

EP 368 EGO 80%

Norwest Energy NL 20%

EP 432 EGO 100%

EP 454 100%

EP 430 100%

EP 416 EGO 40%

Pilot Energy 60%

EP 440 100%

EP 480 EGO 40%

Pilot Energy 60%

Key focus on

Perth Basin

production and

exploration

Origin Energy

recently pulled

out of a farmin

agreement to

acquire 3D

seismic

EP368 and

EP426 also

prospective for

Kockatea and

Carynginia

shale

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 10 of 18

Fig. 8: EGO – Perth Basin Acreage

Source: EGO

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 11 of 18

In 2008 the Moriary-1 well was drilled approximately 4km south east of North

Erregulla-1. The target was a tilted fault block. The well was plugged and abandoned

after formation water was encountered along with non-commercial residual

hydrocarbons.

EGO believes North Erregulla-1 was drilled down dip from the crest of the reservoir.

The seismic will provide more clarity on the prospect and, if EGO’s interpretation is

correct, then EGO estimates the prospect could hold 22 million barrels of

recoverable oil in the Dongara Sandstone and 3 million barrels of recoverable oil in

the Arranoo Member. In addition to this, the HCSS could hold 100 billion cubic feet

of gas.

All of EP368 and the southern half of EP426 could be prospective for Kockatea and

Carynginia shale gas. In EP426, North Erregulla-1 intersected 35 metres of the

Kockatea Shale. The combined acreage of the two permits is 731,505 acres and we

estimate that approximately 400,000 (80,000 net) of these acres are prospective. By

our estimates, the permits contain the potential for 1.7Tcf of net recoverable gas.

EP432 (100%) Operator The Black Arrow prospect is another tilted fault block and will evaluate the potential

of the Arranoo Sandstone. The well is subject to approval from the DMP. There been

a number of dry wells in Block A and no discoveries. However, Gairdner-1 was

drilled in the permit immediately north of EP432 in 1990 and had oil shows but was

plugged and abandoned. EGO believes the Black Arrow prospect is an extension of

the Gairdner prospect.

Block B is the Southern portion of the EP and contains the Cataby-1 well, which had

oil shows, and the Mullering-1 well which was dry. EGO plans to drill a well to further

test the Cataby-1 discovery.

EP454 (100%) & EP430 (100%), Operator The permit contains the Charger prospect, which is a shallow anticlinal target. EGO

intends to drill Charger-1 after Black Arrow-1 in EP432 and is seeking a farminee

fund all or part of the well. EP454 has not had an exploration well drilled within its

boundaries.

EP430 contains two prospects, Launer and Winchester, each targeting the

Cattamarra Coal Measures. 2D seismic was acquired over the permit in August 2011

but further seismic will be required over the Winchester prospect before it could be

considered drill ready. No exploration wells have been drilled in EP430, though a

stratigraphic well was drilled on the eastern boundary.

SOUTH PERTH BASIN EXPLORATION

EP480 (100%) and EP416 (90%), Operator In order to focus on the core northern Perth Basin tenements, EGO recently farmed

down equity in the southern Perth Basin tenements. Under the terms of the farm-in

agreement Pilot Energy (PGY) will pay EGO $450,000 to earn a 60% interest in both

permits and become the operator. Payment will be made in two stages. $150,000

initially and a further $350,000 upon renegotiation of the permit terms with the

regulator (expected in early 2016). PGY will also free carry EGO on 24 months of

permit expenses, excluding seismic and drilling.

EP368 and

EP426 also

prospective for

Kockatea and

Carynginia

shale

Charger and

Black Arrow

prospects will

be drilled in

2013

No exploration

wells have been

drilled in EP454

or EP430

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 12 of 18

PERTH BASIN The historic exploration success rate in the northern part of the Basin was about one

in ten. Since then, improvements in seismic quality, including the application of

three-dimensional seismic surveys, have led to a higher success rate. Major play

types include Permian, Triassic and Jurassic anticlines as well as Permian and

Triassic tilted fault blocks and stratigraphic traps.

Although exploration activity in the Perth Basin commenced in 1935, the first wildcat

well wasn’t drilled until 1961. The majority of early stage exploration and drilling was

performed by WAPET (now Chevron). Exploration has concentrated on the North

Perth Basin around the Geraldton/Dongara area (and Norwest’s permits). Seismic

surveys have been acquired across all major areas of the Perth Basin.

Fig. 9: Perth Basin Stratigraphy

Source: Department of Mineral and Energy WA, Atlas of Petroleum Fields, Onshore Perth

Basin

Since the first well (Eneabba 1), more than 250 onshore wells and 40 offshore wells

have been drilled. Of the wells drilled, approximately 30 have produced oil and

approximately 40 have produced gas for a total of 13 commercial fields. Three-

quarters of wells drilled and the majority of accumulations are located in the northern

part of the Basin. The gas in the north of the Basin is mainly dry, with minimal

condensate production, and the oil is highly paraffinic. Whilst the southern Perth

Basin has proved prospective (Whicher Range), there have been no commercial

discoveries. It is a common belief that the southern region has poor sealing potential

and limited source rock.

Conventional oil

and gas explorer

and soon to be

producer

North Perth Basin

is considered most

prospective

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 13 of 18

LOCATION, LOCATION, LOCATION

When considering the prospects and economics of a gas field, location is crucial and

the Perth Basin is ideal.

There are two pipelines (the Dampier to Bunbury Natural Gas Pipeline and

the Parmelia Pipeline) running through the Basin.

There have been numerous discoveries and commercial fields in the Basin.

Total reserves produced to date are in excess of 30mmbbls oil and

condensate and 625 Bcf gas from 10 fields, all of which are located in the

northern part of the Basin.

The unconventional potential of the Basin has recently been improved by

exploration activities carried out by AWE, and NWE. In particular, the

program undertaken by the two companies targeted the tight sands of the

High Cliff Sandstone, the Irwin River Coal Measures, the Carrynginia Shale

and the Kockatea Shale. The program proved that each zone can be fracced

and will produce gas to surface. It is important to note that the Kockatea also

produced oil to surface.

Given the proximity to Perth and the level of historic exploration in the basin,

there are a number of oil and gas services companies close to the region.

However, there is an inadequate amount of companies to provide a

seamless and timely service. As such, exploring for oil and gas in the Perth

Basin can be expensive (due to long distance mobilisation and

demobilisation costs) and require careful planning to ensure all equipment is

available at the same time.

Fig. 10: EGO ’s Northern Perth Basin Acreage

Source: Hartleys

Perth Basin

accommodates a

number of existing

fields and is close

to market,

pipelines, services

and equipment

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 14 of 18

MANAGEMENT AND DIRECTORS From the EGO website

Antonino Mario (Tony) Iannello - Chairman

(Interest in 13.888m shares as at 26th March 2015)

Tony was appointed as a director on 22 November 2013 bringing to the business

more than 30 years of banking and energy experience. He is a director of the listed

companies shown below. He is the Non-Executive Chairman of HBF Health Ltd, MG

Kailis Group, and D’Orsogna Ltd. He is a director of the St Baker Wilkes Indigenous

Educational Foundation Limited, Water Corporation of Western Australia, and a

member of The Murdoch University Senate. Prior to embarking on a career as a

non-executive director, Tony was the Managing Director of Western Power

Corporation until its separation into four separate businesses.

Stuart Anthony Brown - Non-Executive Director

Mr Brown is a petroleum geologist with over 30 years experience in Australia and

internationally at the technical, managerial, executive and board levels. Mr Brown

held the position of Vice-President Strategic Planning at Woodside from 2007 until

2012. In this role he was responsible for the management of Woodside’s corporate

strategic planning, including the overview of the company’s investment decisions

and investment reviews and reported to the CEO and Board. Mr Brown is currently

Managing Director of his own privately-owned petroleum consultancy, International

Oil & Gas Strategies Pty Ltd.

Philip Garratt - Non-Executive Director

(Interest in 596.587m shares and 122.312m options as at 5th May 2015)

Phil was appointed as a director on 5 May 2015 bringing more than 30 years of

senior management experience in a range of industries including oil exploration,

development and distribution, mineral resource exploration and telecommunications.

Phil has worked extensively at a global level to help grow and develop businesses in

these fields in his capacity as a principal and investor. He offers skills with a

particular focus on business development and corporate governance.

Ken Aitken - Chief Executive Officer

Mr Aitken has extensive knowledge of WA’s oil and gas industry through his senior

roles with Origin, Mitsui, Apache and New Standard Energy as well as international

experience in Norway, UK and Indonesia. Mr Aitken was General Manager

Operations and Engineering with ASX-listed petroleum company New Standard

Energy with responsibility for managing all operated asset activities with joint venture

partners Conoco Phillips and Petrochina. Prior to this, Mr Aitken held the position of

WA Business Unit Manager/Asset Manager with Origin Energy for a total of seven

years, during which time he managed production of approximately three million

barrels of oil and 20PJ of gas. During his tenure, Origin discovered and developed

the significant Redback gas field, located in the onshore Perth Basin.

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 15 of 18

HARTLEYS FORECASTS

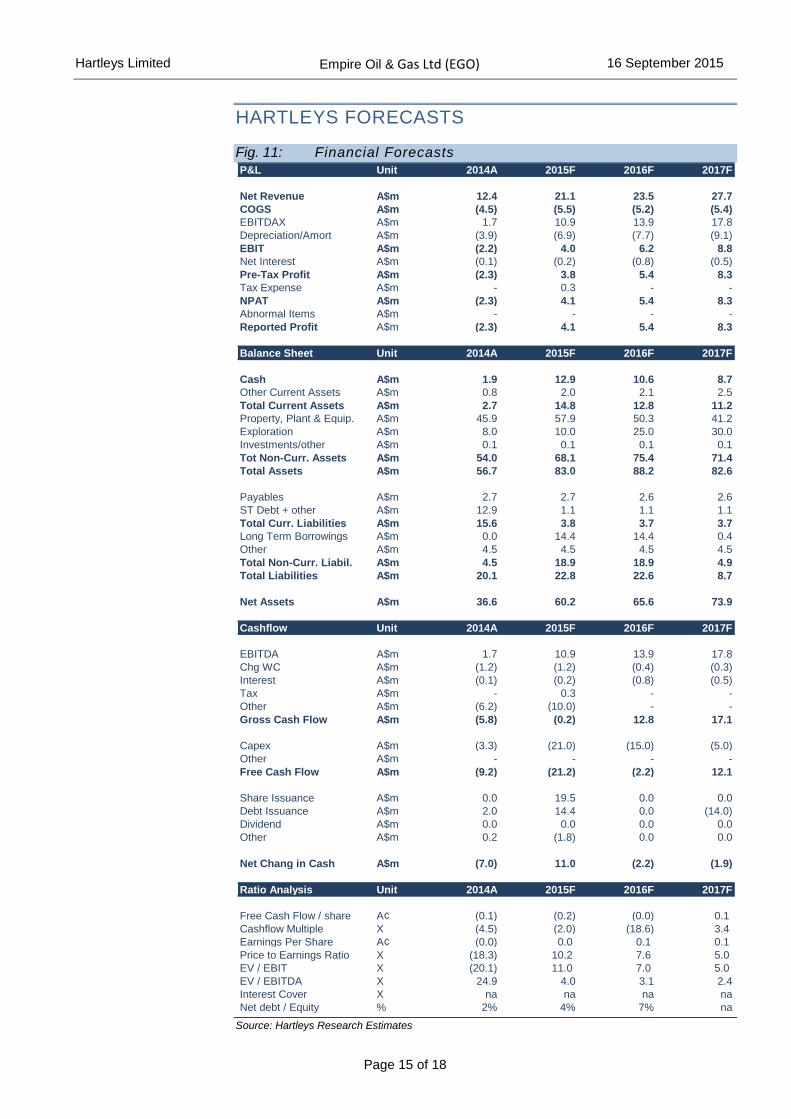

Fig. 11: Financial Forecasts

x

Source: Hartleys Research Estimates

P&L Unit 2014A 2015F 2016F 2017F

Net Revenue A$m 12.4 21.1 23.5 27.7

COGS A$m (4.5) (5.5) (5.2) (5.4)

EBITDAX A$m 1.7 10.9 13.9 17.8

Depreciation/Amort A$m (3.9) (6.9) (7.7) (9.1)

EBIT A$m (2.2) 4.0 6.2 8.8

Net Interest A$m (0.1) (0.2) (0.8) (0.5)

Pre-Tax Profit A$m (2.3) 3.8 5.4 8.3

Tax Expense A$m - 0.3 - -

NPAT A$m (2.3) 4.1 5.4 8.3

Abnormal Items A$m - - - -

Reported Profit A$m (2.3) 4.1 5.4 8.3

Balance Sheet Unit 2014A 2015F 2016F 2017F

Cash A$m 1.9 12.9 10.6 8.7

Other Current Assets A$m 0.8 2.0 2.1 2.5

Total Current Assets A$m 2.7 14.8 12.8 11.2

Property, Plant & Equip. A$m 45.9 57.9 50.3 41.2

Exploration A$m 8.0 10.0 25.0 30.0

Investments/other A$m 0.1 0.1 0.1 0.1

Tot Non-Curr. Assets A$m 54.0 68.1 75.4 71.4

Total Assets A$m 56.7 83.0 88.2 82.6

Payables A$m 2.7 2.7 2.6 2.6

ST Debt + other A$m 12.9 1.1 1.1 1.1

Total Curr. Liabilities A$m 15.6 3.8 3.7 3.7

Long Term Borrowings A$m 0.0 14.4 14.4 0.4

Other A$m 4.5 4.5 4.5 4.5

Total Non-Curr. Liabil. A$m 4.5 18.9 18.9 4.9

Total Liabilities A$m 20.1 22.8 22.6 8.7

Net Assets A$m 36.6 60.2 65.6 73.9

Cashflow Unit 2014A 2015F 2016F 2017F

EBITDA A$m 1.7 10.9 13.9 17.8

Chg WC A$m (1.2) (1.2) (0.4) (0.3)

Interest A$m (0.1) (0.2) (0.8) (0.5)

Tax A$m - 0.3 - -

Other A$m (6.2) (10.0) - -

Gross Cash Flow A$m (5.8) (0.2) 12.8 17.1

Capex A$m (3.3) (21.0) (15.0) (5.0)

Other A$m - - - -

Free Cash Flow A$m (9.2) (21.2) (2.2) 12.1

Share Issuance A$m 0.0 19.5 0.0 0.0

Debt Issuance A$m 2.0 14.4 0.0 (14.0)

Dividend A$m 0.0 0.0 0.0 0.0

Other A$m 0.2 (1.8) 0.0 0.0

Net Chang in Cash A$m (7.0) 11.0 (2.2) (1.9)

Ratio Analysis Unit 2014A 2015F 2016F 2017F

Free Cash Flow / share A¢ (0.1) (0.2) (0.0) 0.1

Cashflow Multiple X (4.5) (2.0) (18.6) 3.4

Earnings Per Share A¢ (0.0) 0.0 0.1 0.1

Price to Earnings Ratio X (18.3) 10.2 7.6 5.0

EV / EBIT X (20.1) 11.0 7.0 5.0

EV / EBITDA X 24.9 4.0 3.1 2.4

Interest Cover X na na na na

Net debt / Equity % 2% 4% 7% na

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 16 of 18

VALUATION We value EGO at 0.75cps. At the core of our valuation is the Red Gully gas

operations, worth A$43m or 0.42cps. The remainder of our 0.75cps valuation is

made op from Red Gully North (0.11cps), Gin-Gin East and other exploration

(0.23cps). EGO’s net debt at the end of FY15 was estimated to be A$2m.

EGO management has indicated an intention to consolidate the current shares on

issue. The history of share consolidations on the ASX suggests that there may be a

period of share price weakness immediately after the consolidation. We are however

of the view that a consolidation is required if the EGO share register is to mature.

Fig. 12: EGO valuation summary

Source: Hartleys Research

We expect EGO to refinance the A$15.1m in debt currently outstanding with ERM

Power (ERM). The current debt facility is interest free and due in August 2016 but

carries an escalation clause should the EGO share price appreciate above 0.8cps

“Under this mechanism, EGO will increase the amount it pays to ERM on top of the

$15.1 million by a percentage equal to 70 per cent of the percentage increase in

EGO’s share price. For example, if EGO’s share price increases by 50 per cent,

EGO will increase the amount it pays to ERM by 70 per cent of 50 per cent, or 35

per cent. This would result in an additional payment to ERM of $5.7 million. This

means that the final amount ERM receives from EGO for these assets is closely

aligned to EGO’s success.”

A$ m Un-risked Risking Risked cps

Red Gully Gas Plant 43.1 100% 43.1 0.42

Red Gully North 23.7 50% 11.9 0.11

Gin-Gin East 48.8 20% 9.8 0.09

Other Exploration 15.0 0.14

Cash 12.9 0.12

Less: Debt -14.4 -0.14

Valuation 0.75

We value EGO at

0.8cps - the Red

Gully gas

operation accounts

for 0.48cps

Fig. 1: \

Hartleys Limited Empire Oil & Gas Ltd (EGO) 16 September 2015

Page 17 of 18

RISKS Investment in the oil and gas sector should be considered high risk. There is no

guarantee of exploration success. Further to this, producing assets typically decline

without further exploration and development. Specific risks include exploration risk,

development risk and production risk.

Our exploration valuation includes a risked metric based on prospect size for permits or

wells held by the Company. In essence, exploration values assume that the market will

recognise a portion of potential value before the results of a well are known. In most

cases, we include just 10% of potential prospect value in our valuations. However, this

may increase or decrease depending on the type of well being drilled and confidence in

the prospect.

SIMPLE S.W.O.T. TABLE Strengths Experienced management team

Long history in Perth Basin Numerous prospects Near term cashflow Strong domestic gas market

Weaknesses Balance sheet debt Relatively short reserves life

Opportunities Red Gully gas plant improves commercial potential of any nearby discovery Other exploration success Continuing exploration and operational success could improve Company reputation

Threats Production issues Exploration failure Environmental concerns Board/shareholder disputes

Source: Hartleys Research

Perth Basin is very

prospective and

about to

commence

production

Page 18 of 18

HARTLEYS CORPORATE DIRECTORY Research Trent Barnett Head of Research +61 8 9268 3052

Mike Millikan Resources Analyst +61 8 9268 2805

Scott Williamson Resources Analyst +61 8 9268 3045

Simon Andrew Energy Analyst +61 8 9268 3020

Janine Bell Research Assistant +61 8 9268 2831

Corporate Finance Grey Egerton-

Warburton

Director & Head of

Corp Fin.

+61 8 9268 2851

Richard Simpson Director +61 8 9268 2824

Paul Fryer Director +61 8 9268 2819

Dale Bryan Director +61 8 9268 2829

Ben Wale Associate Director +61 8 9268 3055

Ben Crossing Associate Director +61 8 9268 3047

Stephen Kite Associate Director +61 8 9268 3050

Scott Weir Associate Director +61 8 9268 2821

Registered Office

Level 6, 141 St Georges TcePostal Address:

PerthWA 6000 GPO Box 2777

Australia Perth WA 6001

PH:+61 8 9268 2888 FX: +61 8 9268 2800

www.hartleys.com.au [email protected]

Note: personal email addresses of company employees are

structured in the following

manner:[email protected]

Hartleys Recommendation Categories

Buy Share price appreciation anticipated.

Accumulate Share price appreciation anticipated but the risk/reward is

not as attractive as a “Buy”. Alternatively, for the share

price to rise it may be contingent on the outcome of an

uncertain or distant event. Analyst will often indicate a

price level at which it may become a “Buy”.

Neutral Take no action. Upside & downside risk/reward is evenly

balanced.

Reduce /

Take profits

It is anticipated to be unlikely that there will be gains over

the investment time horizon but there is a possibility of

some price weakness over that period.

Sell Significant price depreciation anticipated.

No Rating No recommendation.

Speculative

Buy

Share price could be volatile. While it is anticipated that,

on a risk/reward basis, an investment is attractive, there

is at least one identifiable risk that has a meaningful

possibility of occurring, which, if it did occur, could lead to

significant share price reduction. Consequently, the

investment is considered high risk.

Institutional Sales Carrick Ryan +61 8 9268 2864

Justin Stewart +61 8 9268 3062

Simon van den Berg +61 8 9268 2867

Chris Chong +61 8 9268 2817

Digby Gilmour +61 8 9268 2814

Veronika Tkacova +61 8 9268 3053

Wealth Management Nicola Bond +61 8 9268 2840

Bradley Booth +61 8 9268 2873

Adrian Brant +61 8 9268 3065

Nathan Bray +61 8 9268 2874

Sven Burrell +61 8 9268 2847

Simon Casey +61 8 9268 2875

Tony Chien +61 8 9268 2850

Tim Cottee +61 8 9268 3064

David Cross +61 8 9268 2860

Nicholas Draper +61 8 9268 2883

John Featherby +61 8 9268 2811

Ben Fleay +61 8 9268 2844

James Gatti +61 8 9268 3025

John Goodlad +61 8 9268 2890

Andrew Gribble +61 8 9268 2842

David Hainsworth +61 8 9268 3040

Neil Inglis +61 8 9268 2894

Murray Jacob +61 8 9268 2892

Gavin Lehmann +61 8 9268 2895

Shane Lehmann +61 8 9268 2897

Steven Loxley +61 8 9268 2857

Andrew Macnaughtan +61 8 9268 2898

Scott Metcalf +61 8 9268 2807

David Michael +61 8 9268 2835

Jamie Moullin +61 8 9268 2856

Chris Munro +61 8 9268 2858

Michael Munro +61 8 9268 2820

Ian Parker +61 8 9268 2810

Charlie Ransom

(CEO)

+61 8 9268 2868

Brenton Reynolds +61 8 9268 2866

Conlie Salvemini +61 8 9268 2833

David Smyth +61 8 9268 2839

Greg Soudure +61 8 9268 2834

Sonya Soudure +61 8 9268 2865

Dirk Vanderstruyf +61 8 9268 2855

Jayme Walsh +61 8 9268 2828

Samuel Williams +61 8 9268 3041

Disclaimer/Disclosure

The author of this publication, Hartleys Limited ABN 33 104 195 057 (“Hartleys”), its Directors and their Associates from time to time may hold

shares in the security/securities mentioned in this Research document and therefore may benefit from any increase in the price of those

securities. Hartleys and its Advisers may earn brokerage, fees, commissions, other benefits or advantages as a result of a transaction arising

from any advice mentioned in publications to clients.

This report was prepared solely by Hartleys Ltd. ASX did not prepare any part of the report and has not contributed in any way to its content.

The role of ASX in relation to the preparation of the research reports is limited to funding their preparation, by Hartleys Ltd, in accordance with

the ASX Equity Research Scheme. ASX does not provide financial product advice. The views express in this research may not necessarily

reflect the views necessarily reflect the views of ASX. To the maximum extent permitted by law, no representation, warranty or undertaking,

express or implied, is made and no responsibility or liability is accepted by ASX as to the adequacy, accuracy, completeness or reasonableness

of the research reports.

Any financial product advice contained in this document is unsolicited general information only. Do not act on this advice without first consulting

your investment adviser to determine whether the advice is appropriate for your investment objectives, financial situation and particular needs.

Hartleys believes that any information or advice (including any financial product advice) contained in this document is accurate when issued.

Hartleys however, does not warrant its accuracy or reliability. Hartleys, its officers, agents and employees exclude all liability whatsoever, in

negligence or otherwise, for any loss or damage relating to this document to the full extent permitted by law.

![Corrigés du manuel - Dossier 0 et 1 [Alter Ego +]](https://img.dokumen.tips/doc/110x75/55cf91f1550346f57b91fd8e/corriges-du-manuel-dossier-0-et-1-alter-ego-.jpg)