Embed Size (px)

Citation preview

THREL : Submission of the Opinion of Independent Financial Advisor regarding the sale of all shares of EMCS Thai Company Limited

September 7, 2017

Subject: Submission of the Opinion of Independent Financial Advisor regarding the Connected Transaction of the Company

To: The President The Stock Exchange of Thailand

Enclosure: 1. Opinion of Independent Financial Advisor regarding the Connected Transaction of the Company

The Board of Directors Meeting No. 4/2017 of Thaire Life Assurance Public Company Limited (the “Company”), held on July 26, 2017, resolved to propose to the Shareholders Meeting to consider and approve the sale of all shares of EMCS Thai Company Limited (“EMCS”) held by the Company in the number of 1,200,000 shares, equivalent to 20 percent of the total number of shares of EMCS, at the price of Baht 50 per share, totaling Baht 60,000,000 to Thai Reinsurance Public Company Limited (“THRE”) (the “Share Sale Transaction”).

In this respect, THRE is a major shareholder of the Company, as at August 10, 2017 (the latest book closing date of the Company) THRE holds 17.45 percent of the issued shares of the Company. Therefore, the Share Sale Transaction is considered as a connected transaction under the Notification of the Capital Market Supervisory Board No. TorChor.21/2551 Re: Rules on Connected Transactions and the Notification of the Board of Governor of the Stock Exchange of Thailand Re: Disclosure of Information and Other Acts of Listed Companies concerning Connected Transactions B.E. 2546 (2003) (as amended) (the “Connected Transaction Notifications”). The transaction size is equivalent to 4.5205 percent of the net tangible assets of the Company based on the consolidated financial statement of the Company as at March 31, 2017. In respect of the Share Sale transaction, the Company shall proceed as follows:

1) Disclose the information memorandum on the Share Sale Transaction to the Stock Exchange of Thailand (the “SET”) according to the Connected Transaction Notifications;

2) Convene the shareholder meeting of the Company to consider and approve the Share Sale Transaction with a vote of not less than three-fourths of the total votes of the shareholders attending the meeting and having the right to vote; and

3) Appoint an Independent Financial Advisor to provide the opinion on the Share Sale Transaction; the opinion shall be sent to the Securities and Exchange Commission (the “SEC”), the SET, and the Shareholders of the Company.

In this regard, the Company would like to submit the copies of Opinion of Independent Financial Advisor regarding the Connected Transaction of the Company to the Office of the Securities and Exchange Commission, the Stock Exchange of Thailand and shareholders of the Company for your consideration.

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 2

Please be informed accordingly

Yours sincerely,

(Mr. Sutti Rajitrangson)

President

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 3

- Translation -

Opinion of the Independent Financial Advisor regarding Disposition of Assets and Connected Transactions

of

Thaire Life Assurance Public Company Limited

Presented to the Shareholders of Thaire Life Assurance Public Company Limited

Prepared by

Wealthiest BCA Company Limited

29 August 2017

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 1

DISCLAIMERS

1) The results of the study conducted by Wealthiest BCA Company Limited (“WBCA” or “Independent Financial Advisor” or “IFA”) are based on information and assumptions provided by the management of Thaire Life Assurance Public Company Limited and the information disclosed to the public on the websites of the Securities and Exchange Commission (www.sec.or.th) and the Stock Exchange of Thailand (www.set.or.th).

2) IFA conducted the study with knowledge, skills, and reasonable professional care. 3) IFA shall not be responsible for the profits or the losses and any impacts resulting from this

transaction. 4) IFA considered and provided opinion based on prevailing conditions and information as perceived at

the time of the study. If market conditions change significantly in the future, the results of the study in this report may be affected. The shareholders shall then be careful in acknowledging the said information for further making decision.

5) The opinion provided by IFA is based on the assumptions that the information and documents received are true and correct without any essential changes; and that the economic conditions and information considered are only at the time of the study. If such factors are changed significantly from that present situation; the Company may be affected from the said changes and may consequently affect this transaction. Hence, the IFA opinion provided shall not assure future significant impact on the Company.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 2

Table of Contents ABBREVIATION ................................................................................................................................................. 4

Executive Summary ............................................................................................................................................. 11

1. NATURE AND DETAILS OF THE TRANSACTION ................................................................................. 14

1.1. Transaction Date ............................................................................................................................. 14

1.2. Contractual Parties and relationship with the Company ................................................................. 14

1.3. General Characteristics of the Transaction ..................................................................................... 14

1.4. Transaction Size ............................................................................................................................... 15

1.4.1. The Transaction Size Calculation under the Acquisition and Disposition Notifications ...... 15

1.4.2. The Transaction Size Calculation under the Connected Transaction Notifications ............ 16

1.5. Payment Terms and Conditions of the Transaction ........................................................................ 16

1.6. Details of the Relevant Assets ......................................................................................................... 17

1.6.1. Details of EMCS Thai Company Limited .............................................................................. 17

1.6.2. Background and Significant Changes and Development ..................................................... 17

1.6.3. Overview of Business Operation .......................................................................................... 17

1.6.4. Industry and Competitions .................................................................................................... 21

1.6.5. Market and Competition ........................................................................................................ 23

1.6.6. The Shareholding Structure .................................................................................................. 26

1.6.7. List of Shareholders of EMCS as at 31 March 2017 ........................................................... 27

1.6.8. List of Shareholders of EMCS after the Transaction ........................................................... 27

1.6.9. List of the Board of Directors of EMCS as at 31March 2017 .............................................. 27

1.6.10. List of the Board of Directors of EMCS after the Transaction ............................................. 27

1.6.11. Financial Summary ................................................................................................................ 28

1.7. Value of the Disposed Assets .......................................................................................................... 30

1.8. Basis Used to Determine the Value of Consideration ..................................................................... 30

1.9. Terms and Conditions of the Transactions ...................................................................................... 30

1.10. Characteristics and Scope of Interests of Connected Persons ...................................................... 31

1.11. Plans for utilizing Proceeds received from the Transaction ............................................................ 32

1.12. Directors Who have Interest and/or are Connected Persons in this Transaction .......................... 32

1.13. Opinion of the Board of Directors and the Audit Committee regarding the Transaction ............... 32

1.14. Opinion of the Audit Committee and/or the Director which is Different from the Board of Directors’ Opinion ............................................................................................................................................... 32

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 3

2. RATIONALE AND REASONABLENESS OF THE TRANSACTION ........................................................ 34

2.1. Objectives and Necessity of entering into the Transaction ............................................................. 34

2.1.1. Objectives and Necessity of THRE ...................................................................................... 34

2.1.2. Objectives and Necessity of THREL .................................................................................... 37

2.2. Advantages and Disadvantages of the entering and non-entering into the Transaction ............... 38

2.2.1. Advantages of the entering and Disadvantages of non-entering ........................................ 38

2.2.2. Disadvantages of the entering and advantages of non-entering ......................................... 40

2.3. Comparison of advantages and disadvantages of entering into the Transaction with connected person and with third person .................................................................................................................... 41

2.3.1. Advantages from entering the Transaction with connected person..................................... 41

2.3.2. Disadvantages from entering the Transaction with connected person ................................ 41

2.4. Risk factors from entering / not-entering / unable to entering the Transaction ............................. 43

3. REASONABLENESS OF THE OFFERING PRICE AND CONDITIONS OF THE TRANSACTION ...... 44

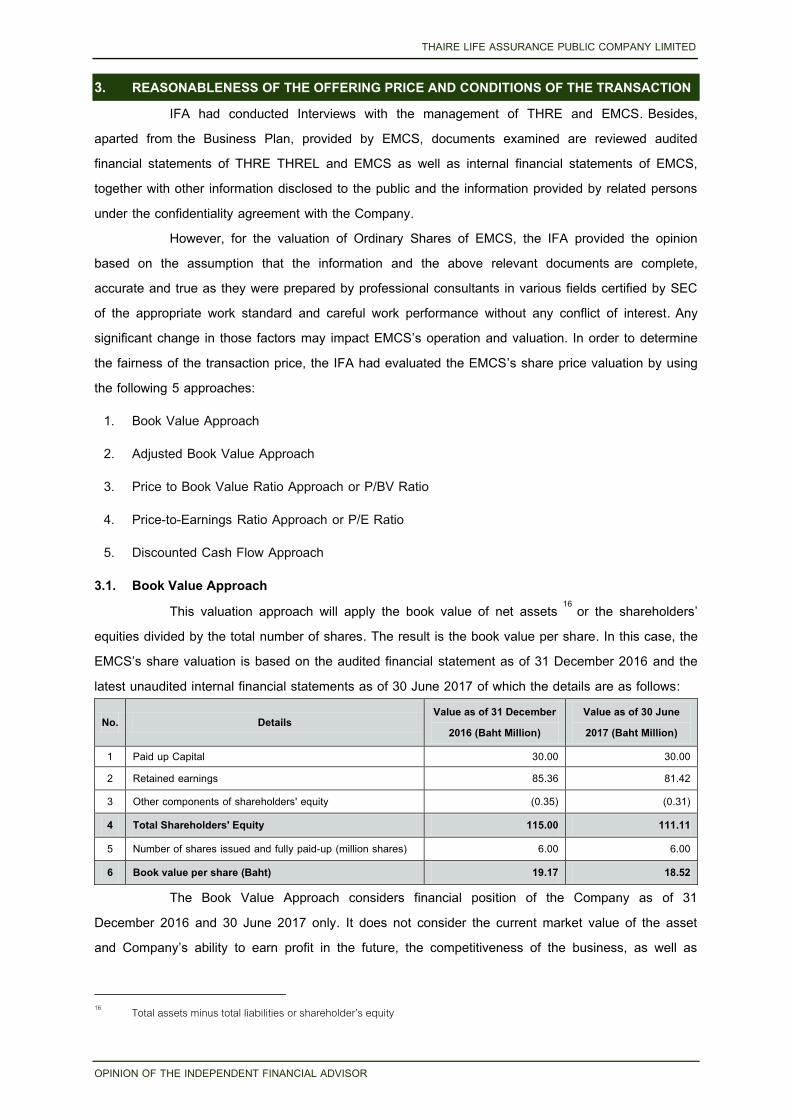

3.1. Book Value Approach....................................................................................................................... 44

3.2. Adjusted Book Value Approach ....................................................................................................... 45

3.3. Price to Book Value Ratio Approach or P/BV Ratio ....................................................................... 45

3.4. Price-to-Earnings Ratio Approach or P/E Ratio .............................................................................. 48

3.5. Discounted Cash Flow Approach ..................................................................................................... 49

3.6. Summary of the Appropriateness of the EMCS’s Ordinary Shares Offering Price ........................ 83

4. SUMMARY OF THE INDEPENDENT FINANCIAL ADVISOR OPINION ................................................ 85

Attachment 1 Investment plan of EMCS ............................................................................... Attachment 1 page 1

Attachment 2 Internal (unaudited) Financial statement of EMCS as of 30 June 2017 ....... Attachment 2 page 1

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 4

ABBREVIATION

Abbreviation Meaning Office or SEC The Office of the Securities and Exchange Commission Exchange or SET The Stock Exchange of Thailand MAI The Market for Alternative Investment OIC Office of Insurance Commission the Company or THREL or the Seller Thaire Life Assurance Public Company Limited THRE or the Major Shareholder or the Buyer

Thai Reinsurance Public Company Limited

EMCS or the Target EMCS Thai Company Limited THRES Thaire Services Company Limited THRET Thaire Training Company Limited BKI Bangkok Insurance Public Company Limited TP Mr. Thongchai Phanumaporn NW Mrs. Nawarat Wongthitirat Merimen Merimen Group and/or Merimen Technologies (Thailand) Company

Limited Independent Financial Advisor: IFA or WBCA

Wealthiest BCA Company Limited

The Group of Companies or the Group Thai Reinsurance Public Company Limited together with its subsidiaries, associated companies, and connected person, which including but not limited to THREL, EMCS, THRES, THRET, etc.

EGM Extraordinary General Meeting Connected person or Connected persons Thaire Life Assurance Public Company Limited and Thai

Reinsurance Public Company Limited as the Buyer and EMCS Thai Company Limited as the Target

Other shareholders Bangkok Insurance Public Company Limited, Mr. Thongchai Phanumaporn and Mrs. Nawarat Wongthitirat

Notification of Connected Transaction Rules

The Notification of the Capital Market Supervisory Board No. TorChor. 21/2551 Re: Rules on Connected Transactions and

Notification of Connected Transaction Disclosure

The Notification of the Board of Governor of the Stock Exchange of Thailand No. BorChor/Por 22-01 Re: Disclosure of Information and Other Acts of Listed Companies concerning Connected Transactions B.E. 2546 (2003)

IM 1 Information Memorandum on the Disposal of Assets and Connected Transaction of THREL dated 26th July 2017.

IM 2 Information Memorandum on the Disposal of Assets and Connected Transaction of THREL dated 29th August 2017.

Information Memorandum Both two issues of Information Memorandum on the Disposal of Assets and Connected Transaction of THREL.

SPA Share Purchase Agreement dated 26 July 2017 between Thai Reinsurance Public Company Limited as the Buyer and Thaire Life Assurance Public Company Limited as the Seller

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 5

Abbreviation Meaning The Selling Shares Common shares of EMCS Thai Company Limited (“EMCS”), a

company limited registered under Thai law with registration number 0105543108248, on the Transaction Date OF 1,200,000 shares, equivalent to 20 percent of the total shares of EMCS according to SPA.

Condition Precedent(s) Condition Precedents according to terms & conditions of SPA No. 3 The Completed Transaction Date The Comp Transaction Date according to terms & conditions of SPA

No. 4 BKI share purchase agreement Share Purchase Agreement dated 25 June 2017 between Thai

Reinsurance Public Company Limited as the Buyer and Bangkok Insurance Public Company Limited as the Seller

TP share purchase agreement Share Purchase Agreement dated 25 June 2017 between Thai Reinsurance Public Company Limited as the Buyer and Mr. Thongchai Phanumaporn as the Seller

NW share purchase agreement Share Purchase Agreement dated 25 June 2017 between Thai Reinsurance Public Company Limited as the Buyer and Mrs. Nawarat Wongthitirat as the Seller

BKI shares transfer forms Shares Transfer Forms dated 7 August 2017 between Thai Reinsurance Public Company Limited as the Transferee and Bangkok Insurance Public Company Limited as the Transferor

TP shares transfer forms Shares Transfer Forms dated 7 August 2017 between Thai Reinsurance Public Company Limited as the Transferee and Mr. Thongchai Phanumaporn as the Transferor

NW shares transfer forms Shares Transfer Forms dated 7 August 2017 between Thai Reinsurance Public Company Limited as the Transferee and Mrs. Nawarat Wongthitirat as the Transferor

Letter No. 1 Letter from THRE to THREL dated 26 April 2017, the offering letter to acquire shares of EMCS at Baht 40 per share with request of response from THREL within 31 May 2017

Letter No. 2 Letter from THRE to THREL dated 25 May 2017, to extend response date of the Transaction to 30 June 2017

Letter No. 3 Letter from THRE to THREL dated 28 June 2017, to inform THREL that other third parties agreed to sell shares to THRE at Baht 50 per share, as a result, THRE become super majority control at 80 percent shares

Letter No. 4

Letter from THRE to THREL dated 29 June 2017, to 2nd extend response date of the Transaction to 31 July 2017

Letter No. 5 Letter from THREL to THRE dated 19 July 2017, to response to the offer with the counter offer to sell shares at Baht 54 per share with request of response on 21 July 2017

Letter No. 6 Letter from THRE to THREL dated 20 July 2017, to confirm pricing at Bath 50 per share as appropriated price because THRE had already entered into same transactions other third parties

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 6

Abbreviation Meaning Letter No. 7 Letter from WBCA to THRE dated 1 August 2017, to request for

corporate restructuring plan after acquisition of EMCS shares Letter No. 8 Letter from THRE to WBCA dated 3 August 2017, regarding

corporate restructuring plan after acquisition of EMCS shares Letter No. 9 Letter from WBCA to THREL dated 4 August 2017, to confirm

relationship among the Group of Companies, together with response from THREL

Business Plan (1) Market Situations, Competition Abilities, Strategic Planning, and Business Plan of EMCS; and (2) Updated data on additional Business Plan and Strategic Plan as of 15th August 2017

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 7

29 August 2017 To: Board of Directors and Shareholders of Thaire Life Assurance Public Company Limited Subject: Opinion of the Independent Financial Advisor regarding Disposition of Assets and Connected

Transactions of Thaire Life Assurance Public Company Limited Reference:

1. Resolution of the Board of Directors Meeting of Thaire Life Assurance Public Company Limited No. 4/25017 on 26 July 2017

2. Information Memorandum on the Disposal of Assets and Connected Transaction of Thaire Life Assurance Public Company Limited

3. Financial Advisor Opinion regarding Share Valuation of EMCS Thai Company Limited (“EMCS”) presented to the Board of Directors Meeting of Thaire Life Assurance Public Company Limited No. 4/25017 on 26 July 2017

4. Share Purchase Agreement dated 26 July 2017 between Thai Reinsurance Public Company Limited and Thaire Life Assurance Public Company Limited

5. Letter from THRE to THREL dated 26 April 2017, the offering letter to acquire shares of EMCS at Baht 40 per share with request of response from THREL within 31 May 2017

6. Letter from THRE to THREL dated 25 May 2017, to extend response date of the Transaction to 30 June 2017

7. Letter from THRE to THREL dated 28 June 2017, to inform THREL that other third parties agreed to sell shares to THRE at Baht 50 per share, as a result, THRE become super majority control at 80 percent shares

8. Letter from THRE to THREL dated 29 June 2017, to 2nd extend response date of the Transaction to 31 July 2017

9. Letter from THREL to THRE dated 19 July 2017, to response to the offer with the counter offer to sell shares at Baht 54 per share with request of response on 21 July 2017

10. Letter from THRE to THREL dated 20 July 2017, to confirm pricing at Bath 50 per share as appropriated price because THRE had already entered into same transactions other third parties

11. Letter from WBCA to THRE dated 1 August 2017, to request for corporate restructuring plan after acquisition of EMCS shares

12. Letter from THRE to WBCA dated 3 August 2017, regarding corporate restructuring plan after acquisition of EMCS shares

13. Letter from WBCA to THREL dated 4 August 2017, to confirm relationship among the Group of Companies, together with response from THREL

14. Business Plan by Management of EMCS and THRE which had manament signature to confirm the accruracy of information provided.

15. Internal (unaudited) Financial Statements as of 30 June 2017.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 8

The Resolution of the Board of Directors Meeting of Thaire Life Assurance Public Company Limited (the “Company” or “THREL”) No. 4/2017, held on 26 July 2017 at 14.00 hours approved to propose to the Shareholders’ Meeting to consider the approval of the sale of all EMCS Thai Company Limited (“EMCS”) shares, held by the Company, to Thai Reinsurance Public Company Limited (“THRE”) in the amount of 1,200,000 shares, equivalent to 20 percent of the total shares of EMCS, at Baht 50 per share, totaling Baht 60,000,000 (the “Transaction”) according to the offer from THRE whose objectives were to restructure the group of companies under supervision of THRE as well as to increase its investment to improve business efficiency to cope with changes of technology during the past five years and in the future. Besides, EMCS especially requires modern technology and business model to better meet the demand of the market. As a result, THRE offered to buy shares from all shareholders of EMCS.

EMCS was founded on 22nd November 2000 to undertake key business as the leader in providing information technology services, as supplemental services, to manage motor claims for motor insurance, a part of Non-Life Insurance business, for key customers of THRE, which is a Group of Non-Life Insurance Companies. Hence, the customer who uses EMCS service shall benefit from saving the cost of claim, which shall have indirect impact on THRE, a reinsurance company, in reducing its cost of services. However, the Company is a Re-Life Insurance company with a group of Life Insurance Companies, who have no relationship with EMCS business, as customers. Therefore, the investment in EMCS is mainly for financial returns.

The major reason the Board of Directors agreed with the above proposal is that it is the disposal of non-core investment that has no relation with the core business of the Company, which shall not be affected by such disposal. In addition, the Board of Directors is also worried about future market uncertainty caused by International Competitors who show intentions to expand regionally.

In addition to the necessity to restructure the group of companies under supervision of THRE with higher investments and costs to maintain market shares and competitive edges in the future; the risk occurred as a result of the Company’s inability to participate in management decision since THRE has Super Majority Control (comprehensive control)1 over shares of EMCS. Hence, to further hold EMCS shares, the Company may face the risks resulted from (1) Continuous Capital Increase, which shall cause the Company to not be able to maintain benefits that used to receive in the past due to Dilution Effect; (2) Restructuring the group of companies under supervision of THRE might be for the maximum benefit of THRE rather than maintaining maximum benefit of each subsidiary company, which mainly cause THRE to acquire all shares from the shareholders for the flexibility of such restructuring processes.

1 Referred to Letter No. 3: Progress Notification Letter to inform THREL that other third parties agreed to sell shares to

THRE, as a result, THRE become super majority shareholder with 80 percent shares and comprehensive control over EMCS

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 9

In this respect, THRE is a major shareholder and a connected person of the Company, as THRE holds 17.47 percent of the issued shares of the Company on 2 May 2017 (the latest book closing date of the Company). Therefore, this Transaction is considered a connected transaction under the Notification of the Capital Market Supervisory Board No. TorChor. 21/2551 Re: Rules on Connected Transactions and the Notification of the Board of Governor of the Stock Exchange of Thailand No. BorChor/Por 22-01 Re: Disclosure of Information and Other Acts of Listed Companies concerning Connected Transactions B.E. 2546 (2003) (as amended) (the “Connected Transaction Notifications”). The Transaction Size is equivalent to 4.5205 percent of the net tangible assets (NTA) of the Company based on the consolidated financial statement of the Company as at 31 March 2017. In respect of the Transaction, the Company shall proceed as follows:

1) Disclose the Information Memorandum on the Transaction to the Stock Exchange of Thailand (the “SET”) according to the Connected Transaction Notifications of which the details are appeared in the Information Memorandum on the Disposal of Assets and Connected Transaction of Thaire Life Assurance Public Company Limited.

2) Organize the Shareholders’ Meeting to seek approval for a decision to enter into a connected transaction hereunder must consist of at least three-fourths of the total votes of shareholders attending the meeting and having voting right. But THRE, who is the shareholder with interest, shall not have voting right in the agendas relating to the Transaction. Besides, the Board of Directors of the Company also approved to hold the Extraordinary General Meeting of Shareholders No. 1/2017 on 22nd September 2017 at 14.00 hours at Victor Club, 8th Floor, Sathorn Square Office Tower, North Sathorn Road, Silom District, Bangkok 10500 with the following agendas: Agenda 1 To consider and adopt the Minutes of the Annual General Meeting of Shareholders

No. 6 Agenda 2 To consider and approve the sale of EMCS Thai Company Limited shares, which

is regarded as a connected transaction. Agenda 3 To consider other issues (if any)

3) Appoint an Independent Financial Advisor (IFA) to provide the IFA Opinion on the Transaction, including the delivery of such opinion to SEC, SET, and the Shareholders of the Company. In this regard, the Company had appointed Wealthiest BCA Company Limited as the Independent Financial Advisor to provide the IFA Opinion on, and conduct any matter relating to the Transaction as specified in the Connected Transaction Notifications.

Moreover, IFA is under the approved lists of SEC and having no relationship with the Company and other related parties on the Transaction.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 10

In preparing this report, IFA had studied and reviewed the documents received from (1) the Company; (2) the Entity whose shares should be sold in the Transaction; and (3) the Entities who should acquire such shares (altogether called “Related Parties”); as well as disclosed information and public information, including other data from public sources and the interviews of the management of the parties involved in the related transaction. However, to give opinion in this report, IFA could neither confirm the accuracy nor the completeness of the Information provided by the parties and/or the management of the parties involved in the related transaction. Besides, this report was developed to provide the opinion on this Transaction only and was based on existing data, at the time of the study, including various assumptions determined in consideration of the possibility of the situation based on actual event. Therefore, any significant changes in the future may affect the Company and its shareholders.

The IFA Opinion contained in this report is developed to provide the opinion on reasonableness of the Transaction to the shareholders. However, the approval of this Transaction is based primarily on each shareholder’s discretion. The shareholders, therefore, have to study all information appeared in this IFA report together with all documents attached with the Notice of EGM and make decision with prudence. In addition, the IFA Opinion may be summarized as follows:

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 11

Executive Summary

According to The Resolution of the Board of Directors Meeting of Thaire Life Assurance Public Company Limited (the “Company” or “THREL”) No. 4/2017, held on 26 July 2017 at 14.00 hours approved to propose to the Extraordinary General Meeting of Shareholders No. 1/2017 to consider the approval of the sale of all EMCS Thai Company Limited (“EMCS”) shares, held by the Company, in the amount of 1,200,000 shares, equivalent to 20 percent of the total shares of EMCS, at Baht 50 per share, totaling Baht 60,000,000 to Thai Reinsurance Public Company Limited (“THRE”).

However, THRE is the major shareholder and a connected party of the Company, as of 2 May 2017 (Latest Book Closing Date) on which THRE held 17.47 percent of the issued shares of the Company, therefore, the Transaction is considered as a connected transaction under the Notification of the Capital Market Supervisory Board No. TorChor. 21/2551 Re: Rules on Connected Transactions and the Notification of the Board of Governor of the Stock Exchange of Thailand No. BorChor/Por 22-01 Re: Disclosure of Information and Other Acts of Listed Companies concerning Connected Transactions B.E. 2546 (2003) (as amended) (the “Connected Transaction Notifications”) with the Transaction size equivalent to 4.5205 percent of the Net Tangible Assets (NTA) of the Company appeared in Consolidated Financial Statements as of 31 March 2017.

After consideration of the Transaction Size, it is found out that the Transaction Size is over Baht 20 Million and is over 3 percent of NTA, according to Consolidated Financial Statements of the Company; therefore, the Transaction is considered as a connected transaction of a listed company. Thus, the Company shall have the duty on Information Disclosure to SET, to which the Company already disclosed via ELCID on 26 July 2017. Besides, the Company shall seek approval from the shareholders’ meeting and must consist of at least three-fourths of the total votes of shareholders attending the meeting and having voting right, excluding interested shareholders’ equity.

The Board of Directors Meeting No. 4/2017 on 26th July 2017 granted resolution to call for EGM for the year 2017 to consider the approval of the sale of all EMCS shares, held by the Company to THRE as abovementioned and the approval of appointing Wealthiest BCA Company Limited to be IFA to provide the IFA Opinion on the Transaction to the Company’s shareholders regarding reasonableness and fairness of price and conditions of the connected transaction.

Furthermore, selling EMCS’s common shares, held by the Company, on Transaction Date shall reduce the risk as well as uncertainty that may arise from EMCS’ performance due to future market uncertainty caused by International Competitors who may take significant market shares from EMCS. Only if the Company sells all common shares of EMCS, there shall be no liability to realize the changing in performance of EMCS and no burden to increase capital when EMCS invests into new technology to increase its competitiveness.

However, to enter into the Transaction may cause the Company to lose opportunity to realize future profits from EMCS as related company; if, in the future, EMCS would be able to perform well and maintain profits as in the past and/or gain more profit after restructuring. But when compared

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 12

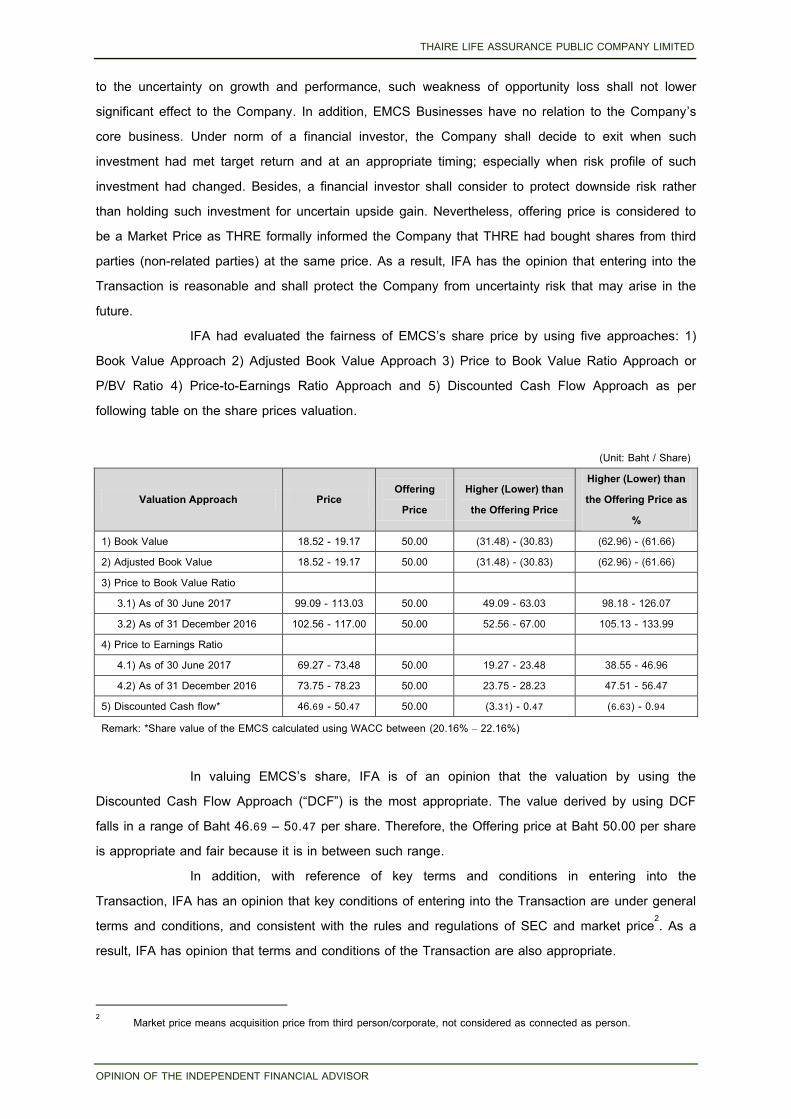

to the uncertainty on growth and performance, such weakness of opportunity loss shall not lower significant effect to the Company. In addition, EMCS Businesses have no relation to the Company’s core business. Under norm of a financial investor, the Company shall decide to exit when such investment had met target return and at an appropriate timing; especially when risk profile of such investment had changed. Besides, a financial investor shall consider to protect downside risk rather than holding such investment for uncertain upside gain. Nevertheless, offering price is considered to be a Market Price as THRE formally informed the Company that THRE had bought shares from third parties (non-related parties) at the same price. As a result, IFA has the opinion that entering into the Transaction is reasonable and shall protect the Company from uncertainty risk that may arise in the future.

IFA had evaluated the fairness of EMCS’s share price by using five approaches: 1) Book Value Approach 2) Adjusted Book Value Approach 3) Price to Book Value Ratio Approach or P/BV Ratio 4) Price-to-Earnings Ratio Approach and 5) Discounted Cash Flow Approach as per following table on the share prices valuation.

(Unit: Baht / Share)

Valuation Approach Price Offering

Price Higher (Lower) than the Offering Price

Higher (Lower) than the Offering Price as

% 1) Book Value 18.52 - 19.17 50.00 (31.48) - (30.83) (62.96) - (61.66) 2) Adjusted Book Value 18.52 - 19.17 50.00 (31.48) - (30.83) (62.96) - (61.66) 3) Price to Book Value Ratio

3.1) As of 30 June 2017 99.09 - 113.03 50.00 49.09 - 63.03 98.18 - 126.07 3.2) As of 31 December 2016 102.56 - 117.00 50.00 52.56 - 67.00 105.13 - 133.99

4) Price to Earnings Ratio 4.1) As of 30 June 2017 69.27 - 73.48 50.00 19.27 - 23.48 38.55 - 46.96 4.2) As of 31 December 2016 73.75 - 78.23 50.00 23.75 - 28.23 47.51 - 56.47

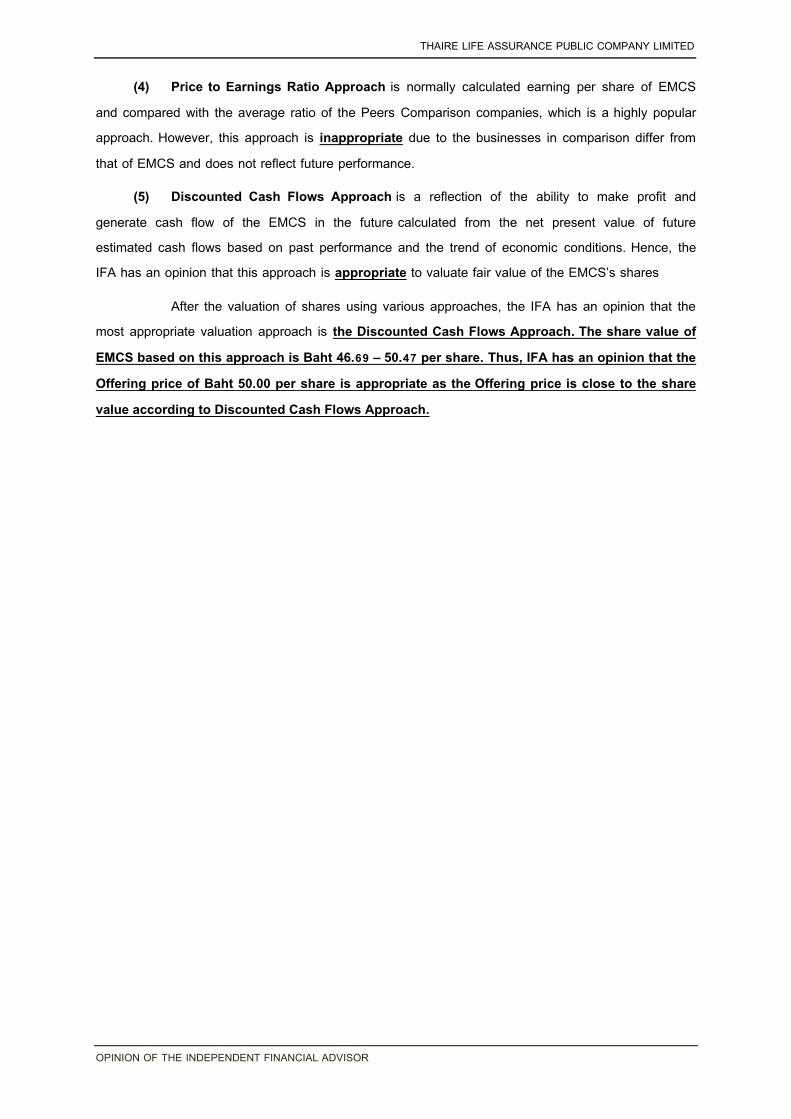

5) Discounted Cash flow* 46.69 - 50.47 50.00 (3.31) - 0.47 (6.63) - 0.94 Remark: *Share value of the EMCS calculated using WACC between (20.16% – 22.16%)

In valuing EMCS’s share, IFA is of an opinion that the valuation by using the

Discounted Cash Flow Approach (“DCF”) is the most appropriate. The value derived by using DCF falls in a range of Baht 46.69 – 50.47 per share. Therefore, the Offering price at Baht 50.00 per share is appropriate and fair because it is in between such range.

In addition, with reference of key terms and conditions in entering into the Transaction, IFA has an opinion that key conditions of entering into the Transaction are under general terms and conditions, and consistent with the rules and regulations of SEC and market price2. As a result, IFA has opinion that terms and conditions of the Transaction are also appropriate.

2 Market price means acquisition price from third person/corporate, not considered as connected as person.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 13

From the above considerations, which may have effects to the shareholders, the IFA is of an opinion that the shareholders should approve to enter into the Transaction. However, in considering the approval or disapproval of the transaction, the shareholders should also study the information and opinions provided in this report together with other information and documents attached to the invitation letter for the shareholders meeting before making a decision. The decision to approve or disapprove the Transaction is at the discretion of the shareholders.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 14

1. NATURE AND DETAILS OF THE TRANSACTION 1.1. Transaction Date 3

The Transaction is expected to be made within the 4th Quarter of 2017, after the approval from the Shareholders’ Extraordinary General Meeting No. 1/2017, to be held on 22 September 2017, under the condition that the Company will sell all of EMCS’ shares to THRE at 9.00 a.m. on the 10th business day after all condition precedents have been met, which is called “Completed Transaction Date,” according to the SPA. This date is expected to happen in late October 2017, under the following processes of Condition Precedents: September 2017 The Shareholders of THRE at the Sharehoders’ Extraordinary General

Meeting grant approval of entering into the Transaction as per Condition Precedents 3(kor) under SPA, which states that “The Seller receives approval from its Sharehoders’ Meeting to sell shares under terms and conditions specified in this SPA.”

October 2017 THRE obtains approval form Office of Insurance Commission (“OIC”) to buy EMCS shares from THREL as per Condition Precedents 3(ngor) under SPA, which states that “The Buyer receives approval from OIC to buy shares under terms and conditions specified in this SPA.”

However, in case the Buyer or Seller has been waived by the other authorized party(ies) at the Buyer’s venue or at any other date, time or the venue that both parties agree upon under such above condition precedents; it might affect the “Completed Transaction Date” to be postponed. 1.2. Contractual Parties and relationship with the Company Seller : Thaire Life Assurance Public Company Limited Purchaser : Thai Reinsurance Public Company Limited Relationship Between the Parties

THRE is a major shareholder of the Company, as at 2 May 2017 (the latest book closing date of the Company), THRE holds 104,790,630 shares, which is 17.47 percent of the issued shares and voting rights of the Company. However, there were no common board members and/or common management and/or common control between both parties, and policies are independent. 1.3. General Characteristics of the Transaction

The Resolution of the Board of Directors Meeting of Thaire Life Assurance Public Company Limited (the “Company” or “THREL”) No. 4/2017, held on 26th July 2017 approved to propose to the Extraordinary General Meeting of Shareholders No. 1/2017 to consider the approval of the sale of all shares of EMCS Thai Company Limited (“EMCS”), a company limited registered under Thai law with registration number 0105543108248, on the Transaction Date. The Company shall sale 1,200,000 shares, equivalent to 20 percent of the total shares of EMCS, at Baht 50 per

3 Data from SPA No. 3 and No. 4

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 15

share, totaling Baht 60,000,000, to Thai Reinsurance Public Company Limited (“THRE”); (the “Transaction”) according to offers from THRE who has an anobjective to acquire all common shares from all shareholders of EMCS. Besides, THRE and other shareholders comprise Bangkok Insurance Public Company Limited, Mr. Thongchai Phanumaporn and Mrs. Nawarat Wongthitirat had already signed the Shares Transfer Form on 7 August 2017. As a result, such abovementioned transaction, after completed all actions per condition precedents4 and shares payment, shall be regarded as Completed Transaction.5

However, THRE is the major shareholder and a connected party of the Company, therefore, the Transaction is considered as a connected transaction under the Notification of the Capital Market Supervisory Board No. TorChor. 21/2551 Re: Rules on Connected Transactions and the Notification of the Board of Governor of the Stock Exchange of Thailand No. BorChor/Por 22-01 Re: Disclosure of Information and Other Acts of Listed Companies concerning Connected Transactions B.E. 2546 (2003) (as amended) (the “Connected Transaction Notifications”) with the Transaction size equivalent to 4.5205 percent of NTA of the Company appeared in Consolidated Financial Statements as of 31 March 2017. 1.4. Transaction Size

The entering into this Transaction is the sale of common shares of EMCS to THRE, the connected person, with the Transaction Size of Baht 60 Million calculated from selling price of Baht 50 per share as of 31 March 2017.

1.4.1. The Transaction Size Calculation under the Acquisition and Disposition Notifications The Transaction Size calculation can be summarized as follows:

Calculation Criteria Calculation formula Transaction

Size

1. Net tangible asset (NTA) value NTA of EMCS x % of investment / NTA of the Company = (107,353,447.51 x 20%) / 1,327,280,313.00

1.6176%

2. Net profit from operating results net profit of EMCS x % of investment / net profit of the Company =(44,779,648.16 x 20%) / 327,986,445.00

2.7306%

3. Total value of consideration value of consideration received or paid / total assets of the Company =60,000,000.00 / 2,196,638,727.00

2.7314%

4. Value of equity issued as number of shares issued for payment / number of issued and paid-up shares Not applicable as no new share is issued for payment

4 In this context, the condition precedents indicated that “the Buyer obtains approval from Office of Insurance Commission

(OIC) to buy shares according to terms and conditions of this SPA.” 5 IFA has no document that clearly identified, at the date on which IFA issued this report, that the aforementioned

transaction was completed. However, as the parties already signed the SPA, it could be assured that the said transaction might really happened at the appropriate time, which might be before, at the time of, or after the Completed Transaction Date, according to the SPA between THRE and THREL (following the probability of the process, it should rather be before the Completed Transaction Date.)

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 16

Total Consideration Received

NTA of the Company1

60,000,000

1,327,280,313.00

Calculation Criteria Calculation formula Transaction

Size consideration for the assets

Remark: Based on the reviewed consolidated financial statements of the Company ended March 31, 2017 and the unaudited financial statements of EMCS ended March 31, 2017 .

The Transaction Size calculated based on the Total value of consideration criterion, which gives the highest Transaction Size, is equivalent to 2.7314 percent (based on the reviewed consolidated financial statements of the Company ended March 31, 2017). Since the Transaction Size is lower than 15 percent, the Company, therefore, has no obligations under the Acquisition and Disposition Notifications.

1.4.2. The Transaction Size Calculation under the Connected Transaction Notifications The Transaction is also considered as a connected transaction with the Transaction

Size exceeding 3 percent of NTA of the Company; the Transaction Size calculation of the connected transaction can be summarized as follows: The calculation of the net tangible assets NTA = total assets – total liabilities – net intangible assets – deferred tax assets – net deferred commission expenses = 2,196,638,727.00 – 748,244,871.00 – 25,575,841.00 – 33,348,341.00 – 62,189,361.00 = Baht 1,327,280,313.00

Transaction size = = = 4.5205 % Remark: 1The Net tangible assets of the Company (NTA) based on the reviewed consolidated financial statements of the Company ended March 31, 2017.

The transaction size calculated based on the total consideration received criterion, which gives the highest value, is equivalent to 4.5205 percent of the net tangible assets of the Company based on the reviewed consolidated financial statements of the Company ended 31 March 2017.

In this regard, the Company shall disclose the information memorandum on the Transaction to the SET and convene the shareholders’ meeting of the Company to consider and approve the Transaction with a vote of at least three-fourths of the total votes of the shareholders attending the meeting and having voting right, excluding the shareholders with interest. The notice of the shareholder meeting together with the opinion of the Independent Financial Advisor shall be sent to the shareholders not less than 14 days prior to the shareholders’ meeting. 1.5. Payment Terms and Conditions of the Transaction

THRE will make a full payment of Baht 60,000,000 in cash to the Company and the Company will transfer the shares of EMCS to THRE on the same day (“Completed Transaction Date”) 6.

6 The details appeared in Part 1, No. 1.1 of this report.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 17

1.6. Details of the Relevant Assets 1.6.1. Details of EMCS Thai Company Limited

Registration Number 0105543108248 Address 48/21 Soi Rajchadapisek 20, Rajchadapisek Road, Samsen Nok Sub-District,

Huaykwang District Bangkok Registered Capital Baht 30,000,000 Number of shares 6,000,000 shares Par value (per share) Baht 5 Paid-up capital Baht 30,000,000

1.6.2. Background and Significant Changes and Development EMCS Thai Company Limited (“EMCS”) was founded on 22nd November 2000 with

initial capital of Baht 20 Million to provide information technology products and services as tools to manage motor claims for motor insurance related businesses. EMCS was a joint venture between (1) Thai Reinsurance Public Company Limited with approximately 25 percent shares; (2) Thaire Life Assurance Public Company Limited with approximately 20 percent shares; (3) PAC Total Solutions Sdn. Bhd., an International Information Technological Company from Malaysia with approximately 45 percent shares; and (4) Mr. Thongchai Phanumaporn with approximately 10 percent shares. 2002 PAC Total Solutions Sdn. Bhd. sold half of its shares to Bangkok Insurance Public

Company Limited (“BKI”), thus, BKI became shareholder with 22.50 percent shares of EMCS

2003 EMCS capital increased to Baht 27 Million and increased again to Baht 30 Million with the same group of shareholders but different structure;

2004 EMCS capital increased to Baht 40 Million with new shareholder, Mr. Chai Sophonpanich

2009 EMCS capital reduced to Baht 30 Million whereas PAC Total Solutions Sdn. Bhd. exited from EMCS and at the end of year 2009, Mr. Chai Sophonpanich sold shares to Mrs. Nawarat Wongthitirat

2017 The Board of Directors of THRE resolved to buy shares of EMCS from other shareholders at Baht 50 per share.

1.6.3. Overview of Business Operation EMCS is the leader in Information Technology for Motor Claim Solutions for the Non-

Life Insurance Industry in Thailand who provides additional services to Non-Life Insurance Companies, core customers of THRE, who shall receive benefits from Claim Management Cost Saving, which used to be based upon lots of man-power. In addition, EMCS also has other clients including (1) Garage Repair Shops; (2) Authorized Car Dealers; (3) Parts Suppliers; (4) Windscreen Service Shops; (5) Survey Companies; and (6) Car Owners; whereas EMCS shall receive Service Fee Per Transaction or Other Services’ Fees.

Business Structure and Group of Customers

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 18

THRE’s main business is the reinsurance of all types of non-life insurance of which the key group of customers consists of 55 insurance companies. In order to provide integrated services, THRE had set up EMCS to provide services for the said key group of customers. At present, the total number of EMCS’ customers is 39 companies whose customers are insurers or car owners and authorized car dealers. When there are claims after car accidents, the customers of those non-life insurance companies have to use the services of survey companies, garage repair shops, windscreen service shops and part suppliers. However, EMCS’ IT Claim System covers all customer groups as shown in the following diagram.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 19

EMCS Business Model

*The total 39 key customers of EMCS, which are primary sources of revenue of the Company, are the customers of THRE.

Car Reparing BusinessCar Owners / Dealers (377)

The total 39 key customers of EMCS*

Non-Life Reinsurer Business Non-Life Insurer Business

80% of Car Insurer are EMCS’s customers

THREInternational

Insurers

Subsidiaries of

Banks

Others

Garage Repair 1,670 Shops

Parts Suppliers127 Shops

Windscreen Services171 Shops

Survey Companies

369 Shops

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 20

Vision “To formulate an industry standard of motor claim solutions in Thailand” Standard Systems for vehicle crash repair sphere include setting standard charges for

crash repairs that are accepted by all Garage Repair Shop Members for time saving in claim costs evaluation processes and also setting standard cost for Parts Supplies that are acceptable by both Insurance Companies and Garage Repair Shop Members as well as ensuring same quality and safety of repair by Garage Repair Shop Members. Besides, the standard of repair quality is also set to increase the standard level of the garage repair shop and the standard of Electronic Motor Claim Solutions for car insurance including related statistics preparation. Mission “To be the pioneer service provider of the electronic motor claim solutions to

insurer and repairers” The Mission is for achieving the major objectives of minimizing the cost of claims by

non-life insurance companies, including garage repair shops, with accepted standard costs agreed in advance; increasing the quality level and the efficiency of garage repair shops to maximum effectiveness by organizing correct cost data of labor and spare parts to ensure quick and accurate claim.

To accomplish such mission, EMCS was the first and only organization to develop E-Claim Solutions in Thailand and provide services for Non-Life Insurance Companies. (Other E-Claim Systems in Thailand might have been developed but for the use within large Non-Life Insurance Companies only, not for outside service.) E-Claim Systems shall enable fast, easy and accurate evaluation of damages and submission of repair price for approval. In addition, E-Claim Systems would help decrease the amount of unnecessary jobs and increase the accuracy as well as efficiency, resulting in less time consuming and lower costs.

E-Claim System Processing starts with Computerized Evaluating System which is the linkage between Non-Life Insurance Companies and Garage Repair Shop Members in Claims communication through internet. Under this system, the digital pictures of the damage that are sent shall be evaluated for repairing costs, using the set-in-advance standard costs that are developed from the cost of standard Garage Repair Shops. Moreover, most of the evaluation of spare parts cost in the market can be processed at once via the system; due to parts databases classifying car data by Types / Brand, which enable easy search. The system then is the center for collection of data and claim statistics. With said statistics, the system is able to not only calculate costs of labor and spare parts but also send claims at once via the internet for repair approval.

Such processes enable E-Claim Systems to increase efficiency and accuracy of motor insurance damages and claims, speed up repair approval system, reduce steps in price examined and eliminate the delay in waiting for the survey officers from the insurance companies to reexamine the damages at the repair garage. Hence, claims evaluation that are standardized shall eliminate issues on wrong parts supplied with easy cost estimation and control to reduce the costs and expenses of related corporations and increase customers’ satisfaction and trustworthiness.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 21

1.6.4. Industry and Competitions The Thai government is working hard to promote “Thailand 4.0” as a new gimmick

and economic model aimed at pulling Thailand out of (1) a middle-income trap; (2) an inequality trap; (3) an imbalanced trap as well as country revolution to gain sustainable wealth whereas Insurance Industry, which is a finance industry, shall have to adapt both organization strategies and embedded technological innovation called Fintech. The survey of PwC7 indicated that Thailand is the top social media shoppers who use more than 51 percent internet shopping, through which insurance industry has been one of the highest growth. Thus, as a result of industry analysis, there shall be several factors that affect EMCS businesses, which are as follows:

1) The New Standards issued by Office of Insurance Commission In order to increase confident and safety for consumers in purchasing insurance

policy through online channels, the Office of Insurance Commission (OIC) in Thailand announced that it had approved, in principle, notifications that set out the criteria, procedures, and conditions for issuing and offering for sale of both life and general insurance products through online channels B.E. 2560, which insurance companies and brokers shall have to improve their database standards as well as sharing systems or disclosure through electronic transactions or regulations or other standards according to OIC announcement.

Consequently, EMCS who is the leader in Information Technology for Motor Claim Solutions for Non-Life Insurance Industry in Thailand and having connecting systems as well as providing efficiency services to manage claims of Non-Life Insurance Companies, Survey Companies, Authorized Car Dealers, Garage Repair Shops, Windscreen Service Shops, and Parts Suppliers, shall require higher standard development of IT Systems especially IT Safety Systems according to OIC. EMCS then plans to develop Safety Systems including but not limited to ISO27001: Information Security Management System (ISMS); ISO20000: Information Technology Service Management Systems (SMS); and CMMI: Capability Maturity Model Integration.

2) Claims per Policy Trends As the Royal Thai Government explores ways to bolster political commitment on road

safety, improves effectiveness of road safety law enforcement, increases penalties, promotes safety drive using information technology to reduce accidents; the ratio of claims per insurance policy, therefore, continues to decrease of which the data from year B.E. 2549-2558 are shown in following table and graph, with 3.00 percent per annum in average. This is the key revenue driver of EMCS.

7 PwC indicated that Thais are top online shopper of the world in “Millennium Era”, the Leader of Mobile Shopping

https://thaipublica.org/2016/04/pwc-18-4-2559/

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 22

Table: Annual Claims per Policy

3) International Competitors

In 2017, in addition to Government Policy Challenge, there shall be challenges from International Competitors who enter into this region. One of the scariest for EMCS is Merimen Technology (Thailand) Company Limited, registered on 10th February 2017 and is a subsidiary company of Merimen Group (“Merimen”) who is the Marketing leader of Integrating System Platform that exchanges data through the same system for Insurance Industry and initiated the provision of software service for Motor Industry Insurance via website application (SaaS). Major Clients are Global Non-Life Insurance Companies who use Merimen systems that have more modules than those of EMCS, which are shown in the following picture:

59.41 55.65 54.06 52.23

48.69 48.43 48.68 48.09 45.42 44.06

2549 2550 2551 2552 2553 2554 2555 2556 2557 2558

Year Policy Count Claim Count Claim Count/Policy Count (%) % Change YoY 2549 3,463,197 2,057,336 59.41 2550 4,036,625 2,246,253 55.65 -6.33% 2551 4,229,538 2,286,627 54.06 -2.85% 2552 4,279,208 2,234,953 52.23 -3.39% 2553 5,127,698 2,496,891 48.69 -6.77% 2554 5,686,441 2,754,211 48.43 -0.53% 2555 6,824,608 3,322,403 48.68 0.51% 2556 7,361,708 3,540,237 48.09 -1.22% 2557 7,681,346 3,489,091 45.42 -5.55% 2558 8,171,249 3,600,431 44.06 -3.00%

Average Changes YoY -3.23%

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 23

In addition to numbers of modules, Merimen has very strong Clients’ Base, not only Global Non-Life Insurance Companies which are Merimen Group’s Clients, but also Finance Institutions (especially banks), who are clients base of Silverlake, the mother company of Merimen who has more than 25 years experiences with several industries including but not limited to banks, insurance, retails, and logistics. Currently, clients of Merimen have already used Merimen Systems overseas, while EMCS has only one module of Non-Life Insurance Systems. As a result, EMCS is required to adapt its system to International Standard or otherwise losing its clients to Merimen. Example There is a case of a non-life insurance company which has overseas mother company using GuideWire System of Merimen, and the mother company required its subsidiaries to change their systems to the same systems of GuideWire within the 4th Quarter of 2016. But Merimen Thailand is not yet ready to implement E-Claim System for Motor Industry, which is only 1 Module out of 5 Modules to be implemented in Thailand, whereas the other 4 are successfully adjusted to GuideWire. The Clients, therefore, requested EMCS to adjust its system with GuideWire in order to be able to continue using EMCS services, while EMCS had an opinion that without such system development, Merimen shall try harder to quickly set up its system in Thailand.

1.6.5. Market and Competition

1) Charateristics of Clients and Target Group EMCS’s Target Clients are (1) Non-Life Insurance Companies (2) Garage Repair

Shops; (3) Authorized Car Dealers; (4) Parts Suppliers; (5) Windscreen Service Shops; (6) Survey Companies; and (7) Car Owners.

Key Group of Clients are Non-Life Insurance Companies that received licenses from Minister of Finance to undertake Non-Life Insurance Businesses to reinsure various damages, such as damages from fire, car accident, marine and logistics. The latest data during January – December 2016,8 indicated that there are 55 Non-Life Insurance companies in total with 8,626,006 voluntary non-life insurance policies, of which 6,907,017 policies accounted for 80 percent of total insurance policies belonged to 39 companies, who are EMCS’s Clients. The 16 remaining companies with 1,718,989 insurance policies or 20 percent of the total policies may have used their own developed systems.

8 The data of all Non-Life Insurers, THRE’s clients in re-insurace business, from THRE base data that are sent to OIC via

electronic channel.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 24

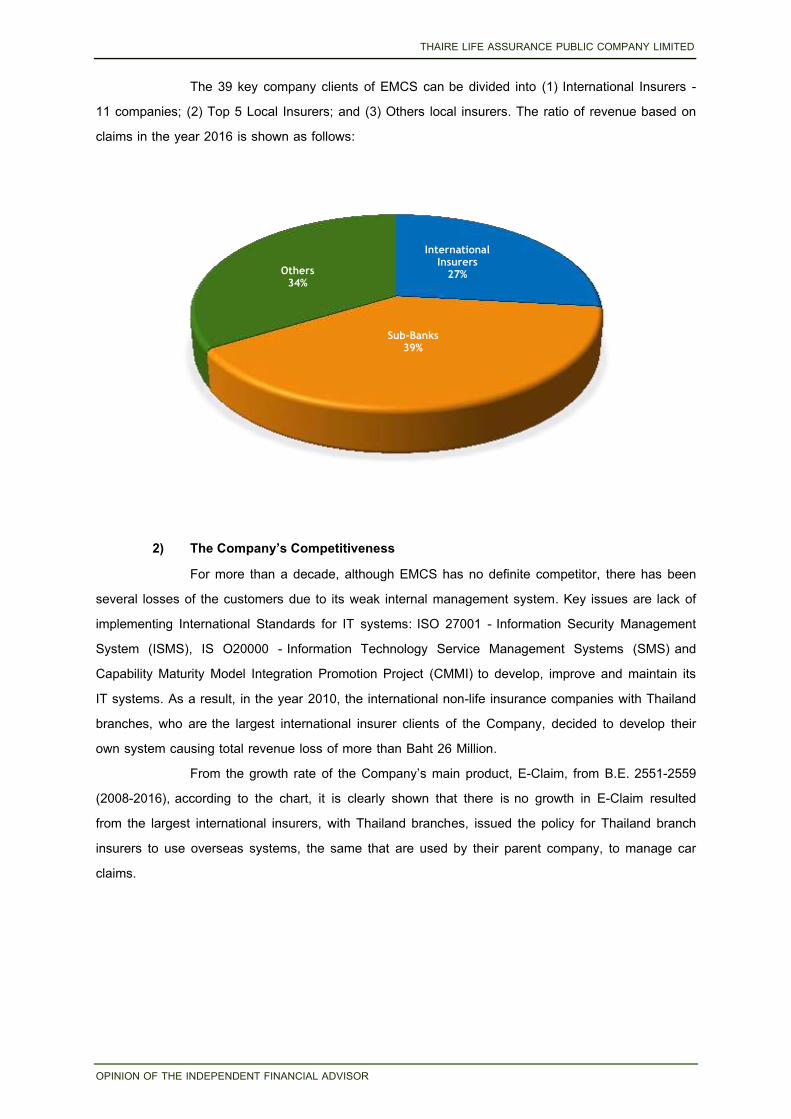

The 39 key company clients of EMCS can be divided into (1) International Insurers - 11 companies; (2) Top 5 Local Insurers; and (3) Others local insurers. The ratio of revenue based on claims in the year 2016 is shown as follows:

2) The Company’s Competitiveness

For more than a decade, although EMCS has no definite competitor, there has been several losses of the customers due to its weak internal management system. Key issues are lack of implementing International Standards for IT systems: ISO 27001 - Information Security Management System (ISMS), IS O20000 - Information Technology Service Management Systems (SMS) and Capability Maturity Model Integration Promotion Project (CMMI) to develop, improve and maintain its IT systems. As a result, in the year 2010, the international non-life insurance companies with Thailand branches, who are the largest international insurer clients of the Company, decided to develop their own system causing total revenue loss of more than Baht 26 Million.

From the growth rate of the Company’s main product, E-Claim, from B.E. 2551-2559 (2008-2016), according to the chart, it is clearly shown that there is no growth in E-Claim resulted from the largest international insurers, with Thailand branches, issued the policy for Thailand branch insurers to use overseas systems, the same that are used by their parent company, to manage car claims.

International Insurers

27%

Sub-Banks 39%

Others 34%

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 25

Effects on Growth of E-Claim

In case there is a strong competitor to take market shares, it is possible that the

Company shall lose its major clients to international competitors, especially Merimen who has major overseas clients as per following table:

Thus, if Merimen fully enters into Thai market and is successful; EMCS shall lose at

least 27 percent of its based clients, who are international insurers that have already used Merimen System. Besides, with the support of Silverlake, the parent company of the clients, the insurers who are subsidiaries of banks to Merimen (most of them using Silverlake systems) may have to use Merimen System. This group of 5 company clients’ accounts for approximately 40 percent of the client base. Hence, if EMCS does not change its strategy to compete with the competitor, it may lose 67 percent of its total base revenue from the past.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 26

1.6.6. The Shareholding Structure

Ad of 31 December 2016, the Shareholding Structure of THRE had 5 subsidiaries whose businesses were related to Insurance Business, having THREL as connected person in the Group as follows:

100% 51% 49%

100% 100% 17.47%

20% 31%

Thai Reinsurance Plc.

Thaire Actuarial Consulting Co., Ltd.

EMCS Thai Co., Ltd.

Thaire Services Co., Ltd.

Thaire Life Assurance Broker Co., Ltd.

Carpool Insurance Broker Co., Ltd.

Thaire Life Assurance Plc.Other Shareholders

(Third Person)

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 27

1.6.7. List of Shareholders of EMCS as at 31 March 2017 Name As at March 31, 2017

Number of Shares held

percentage

1. Thai Reinsurance Public Co., Ltd. 2,940,000 49.00% 2. Thaire Life Assurance Public Co., Ltd. 1,200,000 20.00% 3. Bangkok Insurance Public Co., Ltd. 1,159,950 19.33% 4. Mr. Thongchai Phanumaporn 660,000 11.00% 5 Mrs. Nawarat Wongthitirat 40,050 0.67%

Total 6,000,000 100.00%

1.6.8. List of Shareholders of EMCS after the Transaction Name After the Transaction9 After the Transaction 10

Number of

Shares held percentage Number of

Shares held percentage

1. Thai Reinsurance Public Co., Ltd. 4,140,000 69.00% 6,000,000 100.00% 2. Thaire Life Assurance Public Co., Ltd. - 0.00% - 0.00% 3. Bangkok Insurance Public Co., Ltd. 1,159,950 19.33% - 0.00% 4. Mr. Thongchai Phanumaporn 660,000 11.00% - 0.00% 5 Mrs. Nawarat Wongthitirat 40,050 0.67% - 0.00%

Total 6,000,000 100.00% 6,000,000 100.00%

1.6.9. List of the Board of Directors of EMCS as at 31March 2017 Name Position

1. Mr. Surachai Sirivallop Authorized Director 2. Mr. Oran Vongsuraphichet Authorized Director 3. Mrs. Thitaporn Tarakij Authorized Director 4. Mr. Chai Sophonpanich Authorized Director 5. Mr. Thongchai Phanumaporn Authorized Director

1.6.10. List of the Board of Directors of EMCS after the Transaction Name Position

1. Mr. Surachai Sirivallop Authorized Director 2. Mr. Oran Vongsuraphichet Authorized Director 3. Mrs. Thitaporn Tarakij Authorized Director 4. Mr. Chai Sophonpanich Authorized Director 5. Mr. Thongchai Phanumaporn Authorized Director

9 Based on the assumption that the Transaction of the Company shall be the first to be completed prior to the completion

of all other shareholders’ transactions, as per Information Memorandum on the Disposal of Assets and Connected Transaction of Thaire Life Assurance Public Company Limited (IM1) dated 26th July 2017.

10 Based on the assumption that the Transaction of the Company shall be the last to be completed after the completion of all other shareholders’ transactions, as per BKI TP and NW shares transfer forms dated 7th August 2017 (after THREL issued IM1 on 26th July 2017).

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 28

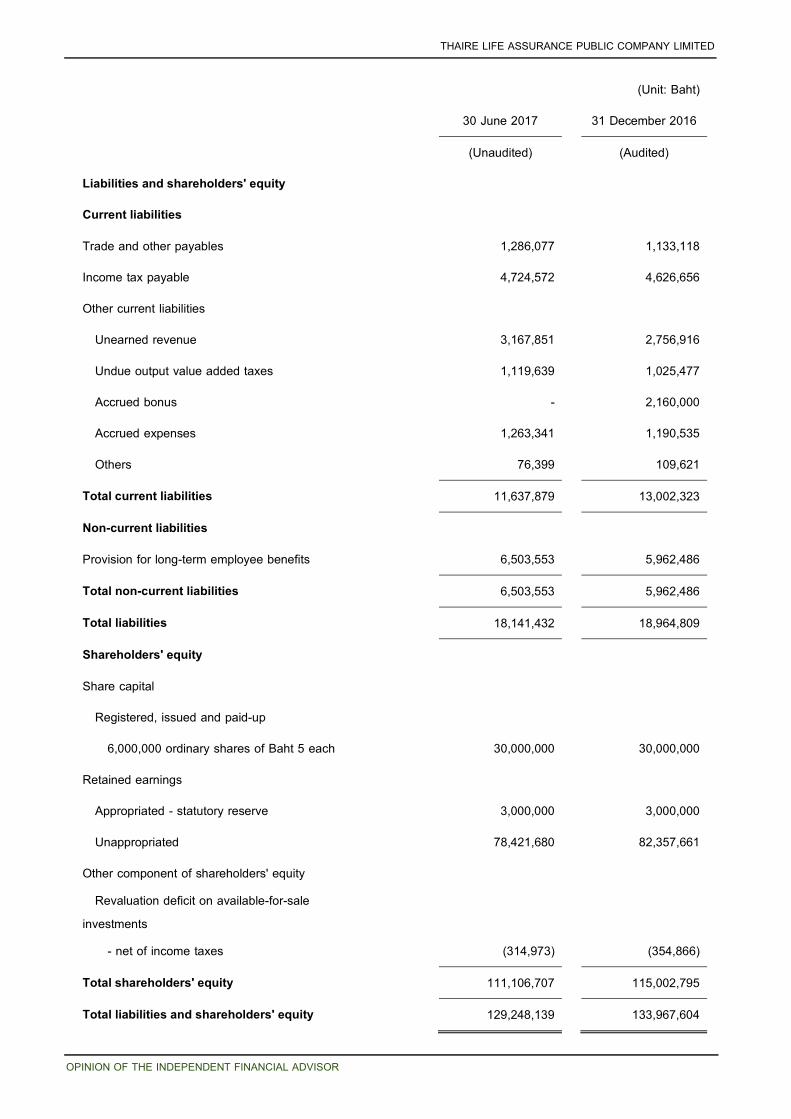

1.6.11. Financial Summary

The following summary is from Financial Statement as of 2014-2016, from Audited Financial Statements of EMCS, and Unaudited Financial Statement (Internal) as of 2nd Quarter of 2017.

Income Statement Jan - Dec Jan - Jun

2014 2015 2016 2017

Revenue Revenue from service 92.06 104.47 116.26 60.52

Revenue from interest and dividends 0.99 1.00 0.93 0.49

Other income 0.24 0.13 4.24 0.32

Total revenue 93.29 105.60 121.42 61.33

Expenses Cost of service 35.64 43.78 55.26 24.96

Administrative expenses 9.66 10.07 9.60 9.65

Total expenses 45.30 53.86 64.86 34.61

Profit before income tax expense 47.98 51.75 56.56 26.72

Income tax expense 9.59 10.35 11.28 5.46

Net profit 38.39 41.39 45.28 21.26

Financial Ratio 2012 2013 2014 2015 2016 Q2 2017

Profitability ratio Operating profit margin 49.85% 56.04% 51.44% 49.00% 46.58% 43.57%

Net profit margin 38.37% 44.97% 41.15% 39.20% 37.29% 34.67%

Return on equity 62.35% 49.60% 40.91% 43.67% 39.37% 19.14%

Efficiency ratio Return on assets 48.89% 42.98% 35.24% 35.81% 33.80% 16.45%

Assets Turnover 127.42% 95.59% 85.64% 91.35% 90.64% 47.45%

Financial policy ratio Debt to equity ratio 0.28 0.15 0.16 0.22 0.16 0.16

Dividend payout ratio 1.26 0.17 0.39 0.97 0.56 1.11

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 29

(Unit: Million Baht)

Statement of Financial Position 31-Dec 30-Jun

2014 2015 2016 2017

Asset Current asset

Cash and cash equivalents 14.44 28.12 17.63 72.06

Short-term investments - net 34.77 18.45 66.52 2.68

Trade receivables - net 13.37 13.63 15.19 16.54

Other current assets 1.62 0.43 0.80 0.74

Total current assets 64.21 60.64 100.14 92.03

Non-current assets Long-term investments - - - -

Property, plant and equipment - net 37.78 43.99 17.64 19.22

Intangible assets - net 5.30 9.05 14.23 16.49

Deferred tax assets 1.17 1.38 1.43 1.50

Other non-current assets 0.47 0.54 0.54 -

Total non-current assets 44.73 54.96 33.83 37.22

Total asset 108.93 115.60 133.97 129.25

Liabilities and shareholders' equity Total current liabilities

Accounts payable and other payables 1.13 0.79 1.13 1.29

Income tax payable 4.70 4.32 4.63 4.72

Accrued bonus - 6.44 2.16 -

Other current liabilities 4.38 3.63 5.08 5.63

Total current liabilities 10.20 15.18 13.00 11.64

Non-current liabilities Provision for long-term employee benefits 4.89 5.64 5.96 6.50

Total Non-Current Liabilities 4.89 5.64 5.96 6.50

Total Liabilities 15.09 20.82 18.96 18.14

Shareholders' Equity Share capital Registered and Paid up Capital 6,000,000 ordinary shares at 5 Baht 30.00 30.00 30.00 30.00

Retained earnings Allocated - Legal Reserve 3.00 3.00 3.00 3.00

Unallocated 61.09 62.28 82.36 78.42

Other components of shareholders' equity Loss on measurement of available-for-sale investments - net of income tax (0.24) (0.50) (0.35) (0.31)

Total Shareholders' Equity 93.85 94.78 115.00 111.11

Total liabilities and shareholders' equity 108.93 115.60 133.97 129.25

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 30

1.7. Value of the Disposed Assets The investment of Baht 24 ,833,497 in EMCS (the equity method investment as at

March 31, 2017) which consists of 1,200,000 ordinary shares at a par value of Baht 5 each, equivalent to 20 percent of the paid-up capital of EMCS. 1.8. Basis Used to Determine the Value of Consideration

The Company received a letter from THRE indicated that other third parties agreed to sell shares to THRE at Baht 50 per share, as a result, THRE become super majority Shareholder at 80 percent shares with comprehensive control over EMCS. Besides, THRE offered to acquire all EMCS shares held by the Company at Baht 50 per share (same as third person).

The Company, therefore, appointed a Financial Advisor11 to determine the fair value of the share sale price for the Board of Directors. Such report use the Discount Cash Flow basis calculated from the future cash flow of EMCS which is the Free Cash Flow to Equity assessment in order to find the fair value of EMCS. 1.9. Terms and Conditions of the Transactions

To enter into the Transaction with THRE, who is a major shareholder and a connected person of the Company, it is considered as a connected transaction under the Notification of the Capital Market Supervisory Board No. TorChor. 21/2551 Re: Rules on Connected Transactions and the Notification of the Board of Governor of the Stock Exchange of Thailand No. BorChor/Por 22-01 Re: Disclosure of Information and Other Acts of Listed Companies concerning Connected Transactions B.E. 2546 (2003) (as amended) (the “Connected Transaction Notifications”). The Transaction Size is equivalent to 4.5205 percent of the net tangible assets (NTA) of the Company based on the consolidated financial statement of the Company as at 31 March 2017. In respect of the Transaction, the Company shall proceed as follows:

1) Disclose the Information Memorandum on the Transaction to the Stock Exchange of Thailand (the “SET”) according to the Connected Transaction Notifications of which the details are appeared in the Information Memorandum on the Disposal of Assets and Connected Transaction of Thaire Life Assurance Public Company Limited.

2) Organize the Shareholders’ Meeting to seek approval for a decision to enter into a connected transaction hereunder, which must consist of at least three-fourths of the total votes of shareholders attending the meeting and having voting right. But THRE, who is the shareholder with interest, shall not have voting right in the agendas relating to the Transaction. Besides, the Board of Directors of the Company also approved to hold the Extraordinary General Meeting of Shareholders No. 1/2017 on 22nd September 2017 at 14.00 hours at Victor Club, 8th Floor, Sathorn Square Office Tower, North Sathorn Road, Silom District, Bangkok 10500 with the following agendas:

11 The Financial Advisor: FA is the financial advisor approved by the Office of the Securities and Exchange Commission.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 31

Agenda 1 To consider and adopt the Minutes of the Annual General Meeting of Shareholders No. 6 Agenda 2 To consider and approve the sale of EMCS Thai Company Limited shares, which is

regarded as a connected transaction. Agenda 3 To consider other issues (if any)

3) Appoint an Independent Financial Advisor (IFA) to provide the IFA Opinion on the Transaction, including the delivery of such opinion to SEC, SET, and the Shareholders of the Company. In this regard, the Company had appointed Wealthiest BCA Company Limited as the Independent Financial Advisor to provide the IFA Opinion on, and conduct any matter relating to the Transaction as specified in the Connected Transaction Notifications.

The Company will sell all shares of EMCS held by the Company by executing the Share Sale and Purchase Agreement on 26 July 2017, which contains significant condition precedents (“Condition Precedents”) as follows:

(A) Confirmation from the Buyer and the Seller are accurate and true on the date of SPA and still accurate and true until the Completed Transaction Date

(B) No change or event has occurred which may have a material adverse effect on EMCS; (C) The Seller received approval from its Shareholder Meeting to enter into the Transaction with

terms and conditions stated in SPA (according to the approval of Board of Directors of the Company, the Extraordinary General Meeting of Shareholders No. 1/2017 shall be held on 22nd September 2017 at 14.00 hours at Victor Club, 8th Floor, Sathorn Square Office Tower, North Sathorn Road, Silom District, Bangkok 10500)

(D) The Buyer obtained approval from the Office of Insurance Commission to purchase the shares of EMCS from the Company;

(E) The Seller and the Buyer obtained necessary approval for the acquisition or disposal of shares of EMCS (as the case may be) or to complete the transaction as agreed in SPA, and;

(F) There shall be no legal proceedings, claims, or any actions brought by the governmental authority or any persons to terminate the Transaction.

(G) There shall be no rules regulations and/or authorities which announce or become effective after the date of SPA that prevent and/or causing the Transaction to be illegal.

Hence, according to the conditions of Completed Transaction, it is indicated that the purchase and transfer of shares shall take place at 9.00 a.m. on the 10th business day after the condition precedents are completed or are waived by the authorized Party who has the right to waive (“Completed Transaction Date”). 1.10. Characteristics and Scope of Interests of Connected Persons

THRE is a major shareholder of the Company, holding 104,690,630 shares equivalent to 17.45 of the issued shares of the Company as at 2 May 2017 (the latest book closing date of the Company). Therefore, THRE is a connected person under the Connected Transaction Notifications. As a result, THRE will not have a voting right in the Extraordinary General Meeting of Shareholders No. 1/2017 in the agendas relating to the Transaction.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 32

1.11. Plans for utilizing Proceeds received from the Transaction

The Company will utilize the cash of Baht 60,000,000 as working capital in its operation.

1.12. Directors Who have Interest and/or are Connected Persons in this Transaction

None

1.13. Opinion of the Board of Directors and the Audit Committee regarding the Transaction

The Board of Directors has considered the Transaction, as described above, and views that it is a disposal of assets, which are not the Company’s main business, so as to enable the Company to fully focus on its life insurance business, as well as increasing liquidity and capital of the Company, which shall consequently create opportunities for the Company to expand its investment in the future.

The Transaction will help increase the Company’s capital, which will, in part, be utilized as reserve fund for future opportunity of joint venture with relevant businesses that could help support the Company in return. In this respect, the Company will invest in the businesses that have potential, steady growth, and are in the area of the Company’s expertise.

In addition, the Board of Directors has an opinion that THRE’s offering price is in the range of enterprise’s fair value as valuated by a Financial Advisor for the consideration of the Board of Directors in making decision. Besides, as of the date of receiving the confirmation on the offered price at Baht 50 per share; the Company has not much bargaining power and there is a possibility that THRE may cancel the offer. As a result, the Company shall be the only one remaining minority shareholder of EMCS under absolute control of THRE. The Board of Directors, therefore, has an opinion that this entering into the transaction shall be submitted at the meeting of shareholders for their approval. 1.14. Opinion of the Audit Committee and/or the Director which is Different from the Board of

Directors’ Opinion

After consideration on details of the necessity in entering into the said Disposition of

Assets and Connected Transaction at the meeting; the Audit Committee has an opinion that the

transaction is reasonable and shall be able to protect future risk of the Company due to the risk of

providing information technology service for non-life insurance companies, which has neither direct nor

indirect relation to the Company’s re-life insurance business. Besides, the Company is only a minority

shareholder who has no controlling power, and consequently has no opposing right and management

participation. In addition, the Company may not gain benefits from dividend, as it used to be, due to

high capital investment plan of EMCS, which completely differs from the one in the past and may have

an impact on cash flow of EMCS resulted in the inability to pay dividend for both short and long term..

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 33

From above reasons and necessity, the Audit Committee in its meeting No. 4/2560 on 8th August 2017 had an approval resolution of selling all of EMCS’s common shares held by the Company to THRE; and proposing the said transaction to the Shareholders’ meeting to further obtaining approval.

THAIRE LIFE ASSURANCE PUBLIC COMPANY LIMITED

OPINION OF THE INDEPENDENT FINANCIAL ADVISOR page 34

2. RATIONALE AND REASONABLENESS OF THE TRANSACTION 2.1. Objectives and Necessity of entering into the Transaction

2.1.1. Objectives and Necessity of THRE There was the necessity to restructure the group of companies under supervision of

THRE and increasing its investment to improve business efficiency to cope with 5-Year changes of technology and prevent the international competitor(s) from taking significant market shares, especially from global/international non-life insurers’ local branches in Thailand as well as utilizing tax benefits from retained losses.12 Especially EMCS, who requires modern corporate restructuring to respond to market demand13, and other parts as follow:

(1) Corporate Restructuring of Thaire Services Company Limited (“THRES”) Thaire Services Company Limited (“THRES”) was found in April 2006 with initial

capital of Baht 5 Million to provide supporting services to Non-Life Insurance Businesses under the name of Third Party Admin Company Limited, with its core business to provide services on Health Insurance Claims and Compensations, then changing the name to Thaire Services Company Limited and adding call center business at the end of 2006.

THRES had continued to increase its registered capital from Baht 5 to 10, 20, 60, and 100 Million at the end and had corporate restructured by transferring Information Technology Department of THRE, which shall consider to be cost center, to become part of profit center in THRES in 2009.