Embed Size (px)

Citation preview

Electrocomponents plc

ANNOUNCEMENT OF PRELIMINARY RESULTS

YEAR ENDED 31 MARCH 2013 23 May 2013

2 2

Agenda

Overview and current trading Ian Mason

Financial performance Simon Boddie

Business performance Simon Boddie

Strategy update Ian Mason

Q&A All

3 3

Key themes

Challenging market conditions during FY13

Significant improvement in gross margin and cost performance in H2

Global operating model implemented to enable global strategy delivery

Evolved to common global strategy comprising seven strategic priorities

New performance framework, targeting improved medium-term financial performance

Common global strategy to drive improved performance

4 4

Financial highlights

1% underlying sales growth UK +4%, International -1%

Headline PBT decline -19%, 8% pts due to fewer days and fx

Stronger H2 headline PBT H2 £57.2m versus H1 £41.5m

Headline free cash flow growth +6%, £56.1m

Maintained final dividend 6.75p, full year 11.75p

Strong balance sheet 1.2x net debt:EBITDA

Headline free cash flow up, stronger H2

5 5

Current trading

(1) underlying sales growth adjusted for currency and trading days

(2) seven weeks to 17 May 2013

Group sales growth maintained at H2 level

Sales Growth (1)

Region H1

FY13 H2

FY13 Apr & May (2)

FY14 Continental Europe 0% 1% 2%

North America (5)% (1)% 1%

Asia Pacific 0% 0% (1)%

International (2)% 0% 1%

UK 5% 2% 0%

Group 0% 1% 1%

6 6

Agenda

Overview and current trading Ian Mason

Financial performance Simon Boddie

Business performance Simon Boddie

Strategy update Ian Mason

Q&A All

7 7

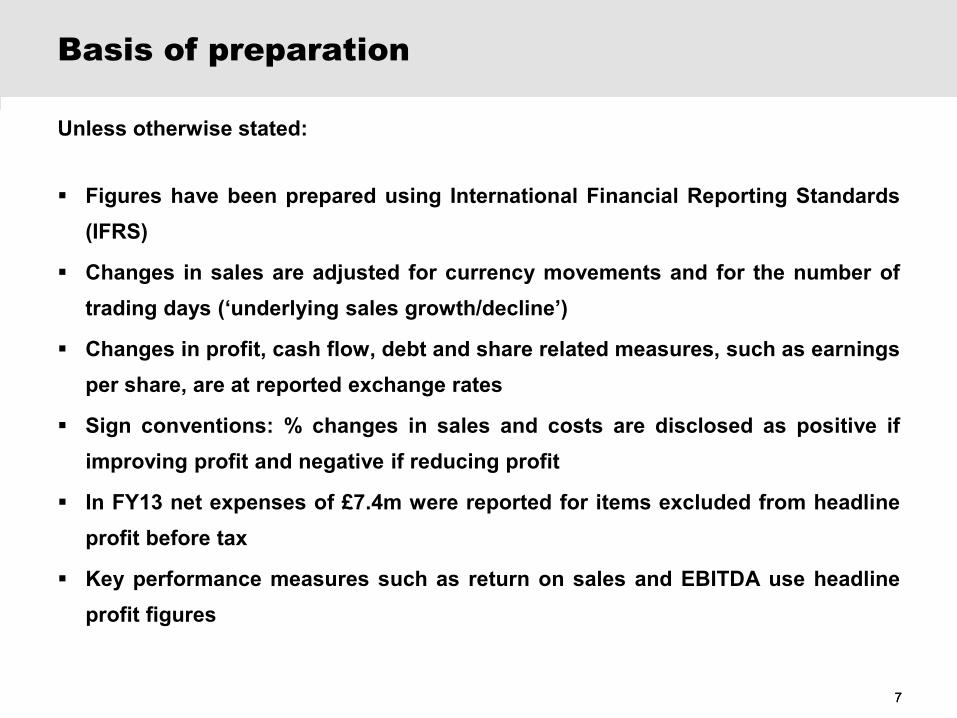

Basis of preparation

Unless otherwise stated: Figures have been prepared using International Financial Reporting Standards

(IFRS)

Changes in sales are adjusted for currency movements and for the number of trading days (‘underlying sales growth/decline’)

Changes in profit, cash flow, debt and share related measures, such as earnings per share, are at reported exchange rates

Sign conventions: % changes in sales and costs are disclosed as positive if improving profit and negative if reducing profit

In FY13 net expenses of £7.4m were reported for items excluded from headline profit before tax

Key performance measures such as return on sales and EBITDA use headline profit figures

8 8

Profit and loss account

(1) Adjusted for currency; sales also adjusted for trading days (2) Headline operating profit expressed as a percentage of sales

Headline return on sales of 8.4% (2)

£m 2013 2012 Change

Sales 1,235.6 1,267.4 0.5% (1)

Gross margin 46.0% 46.8% (0.8)% pointsHeadline operating costs (464.1) (464.6) (1.7)% (1)

Headline operating profit 104.3 128.1 (18.6)%Interest (5.6) (5.8) 3.4%Headline profit before tax 98.7 122.3 (19.3)%

Headline return on sales (2) 8.4% 10.1% (1.7)% points

Group sales growth by technology:

• Maintenance sales growth of 3% (1)

• Electronics sales decline of 2% (1)

Headline profit before tax movement

Components of % change:

(1) Adjusted for currency; sales also adjusted for trading days

(8)% 1% (6)%

9

(6)% (19)%

Gross margin and operating costs equal impact

£122m £99m

£3m £(8)m

£(10)m

FY12 Fewer trading days & fx

Underlying sales growth (1)

Gross margin Operating costs (1) FY13

£(8)m

10 10

Significant H2 improvement

(1) Adjusted for currency; sales also adjusted for trading days (2) Headline operating profit expressed as a percentage of sales

H2 benefitting from management actions

H1 H2 FY

Underlying sales growth (1) 0% 1% 1%

Gross margin change (points) (1.2)% (0.3)% (0.8)%

Headline operating costs growth (1) (3.1)% (0.3)% (1.7)%

Headline PBT 41.5 57.2 98.7

Headline return on sales (points) (2) 7.3% 9.5% 8.4%

11 11

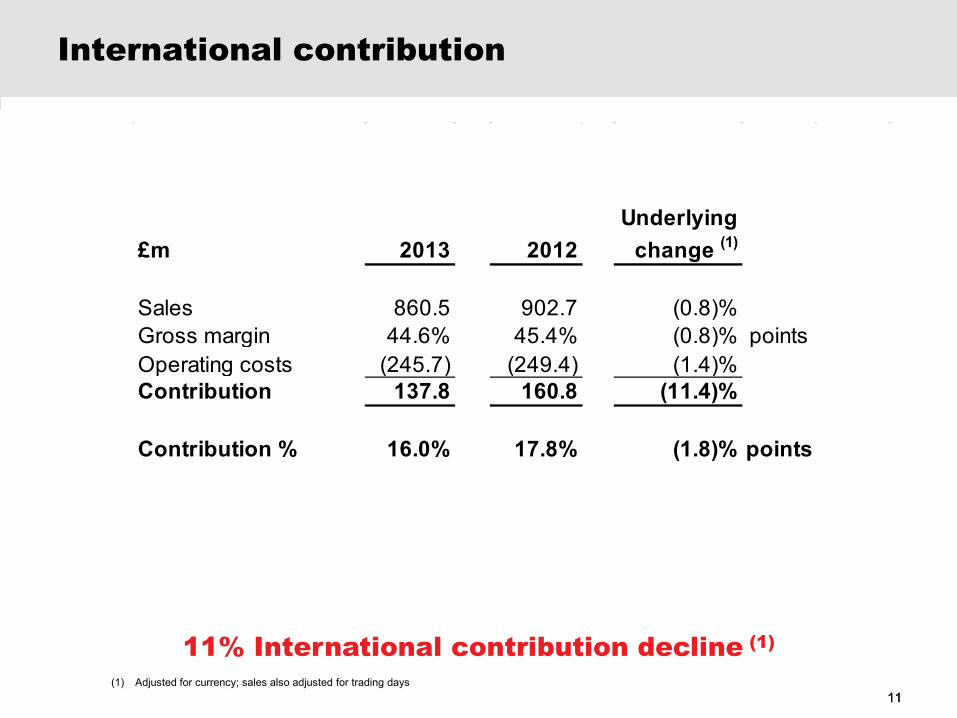

International contribution

£m 2013 2012Underlying

change (1)

Sales 860.5 902.7 (0.8)%Gross margin 44.6% 45.4% (0.8)% pointsOperating costs (245.7) (249.4) (1.4)%Contribution 137.8 160.8 (11.4)%

Contribution % 16.0% 17.8% (1.8)% points

(1) Adjusted for currency; sales also adjusted for trading days

11% International contribution decline (1)

12 12

International contribution components

Change (1)

(1) Adjusted for currency

Resilient Europe performance

(3)% (20)% (32)% (11)%

£161m

£138m

£(9)m£(8)m

£(6)m

FY12 Continental Europe

North America Asia Pacific FY13

13 13

UK contribution

£m 2013 2012Underlying

change (1)

Sales 375.1 364.7 3.7%Gross margin 49.3% 50.0% (0.7)% pointsOperating costs (79.0) (76.5) (3.2)%Contribution 105.9 106.0 (0.1)%

Contribution % 28.2% 29.1% (0.9)% points

(1) Sales adjusted for trading days

Strong UK contribution margin above 28%

14 14

Headline earnings per share

£m 2013 2012 Change

Headline profit before tax 98.7 122.3 (19)%Headline effective tax rate 30% 31% 1% points

Per share amounts:Headline earnings 15.7p 19.5p (19)%

Full year dividend (1) 11.75p 11.75p -

(1) 2013: comprises 5p interim dividend, 6.75p proposed final dividend

Full year dividend maintained

Reorganisation: impact on profit

15

Annualised cost savings of £7m achieved

Reconciliation from headline to reported profit before tax:

Recurring cost savings: FY13 savings c.£4m, annualised c. £7m

Net reduction of 140 roles

£m 2013 2012 Change

Headline profit before tax 98.7 122.3 (19)%Reorganisation costs (7.4) - -Reported profit before tax 91.3 122.3 (25)%

16 16

Cash flow

Headline free cash flow up 6%

£m 2013 2012

Profit before tax 91.3 122.3Depreciation 25.9 27.9Employee share options / non-cash mvts 2.0 3.0Finance expense (net) 5.6 5.8Working capital (16.9) (35.8)Cash generated from operations 107.9 123.2Interest paid (net) (5.6) (5.8)Tax paid (25.6) (26.9)Net capital expenditure (27.4) (37.8)Reported free cash flow 49.3 52.7Add back: reorganisation cash flows 6.8 -Headline free cash flow 56.1 52.7

17 17

Net debt

£m 2013Net debt as at 1 April 2012 (154.2)Free cash flow 49.3Dividends paid (51.3)New shares / finance loans (2.6)Translation differences (0.9)Net debt as at 31 March 2013 (159.7)

Strong balance sheet

Pension net deficit £19.0m (2012: £8.3m) FY14 non-cash P&L pension cost considerations: • c. £5m impact from adoption of IAS19 amendments (FY13 to be restated)

• c. £1m impact from lower discount rates

2013 Covenant Net debt : EBITDA 1.2x <3.25x

Interest cover 21x >3x

£m 2013Committed facilities 305.3Used facilities (156.1)Unused facilities 149.2

Movement in net debt Facilities & covenants

18 18

Agenda

Overview and current trading Ian Mason

Financial performance Simon Boddie

Business performance Simon Boddie

Strategy update Ian Mason

Q&A All

19 19

Business portfolio

Significant opportunity to improve International margin

FY13 £m

Underlying sales

growth% of Group

revenueContribution % of revenue

Market position

Continental Europe 1% 35% 21% No. 1

North America (3)% 22% 13% No. 3

Asia Pacific 0% 13% 7% No. 1

International -1% 70% 16% No. 1

UK 4% 30% 28% No. 1

Group 1% 100% 20% No.1

20 20

Continental Europe

1% sales growth (1)

France flat, smaller markets performing well

10% eCommerce growth, 66% share

Strengthened automation and control offer

10% sales CAGR (1) since regionalisation

Good performance in challenging markets (1) Adjusted for trading days and currency

Continental Europe eCommerce share

0%

10%

20%

30%

40%

50%

60%

70%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

21 21

North America

3% sales decline (1)

c. 70% electronics exposure

H2 improvement, adapted to new system

16% eCommerce decline, 34% share

30k products introduced

H2 improvement after tough H1 (1) Adjusted for trading days and currency

22 22

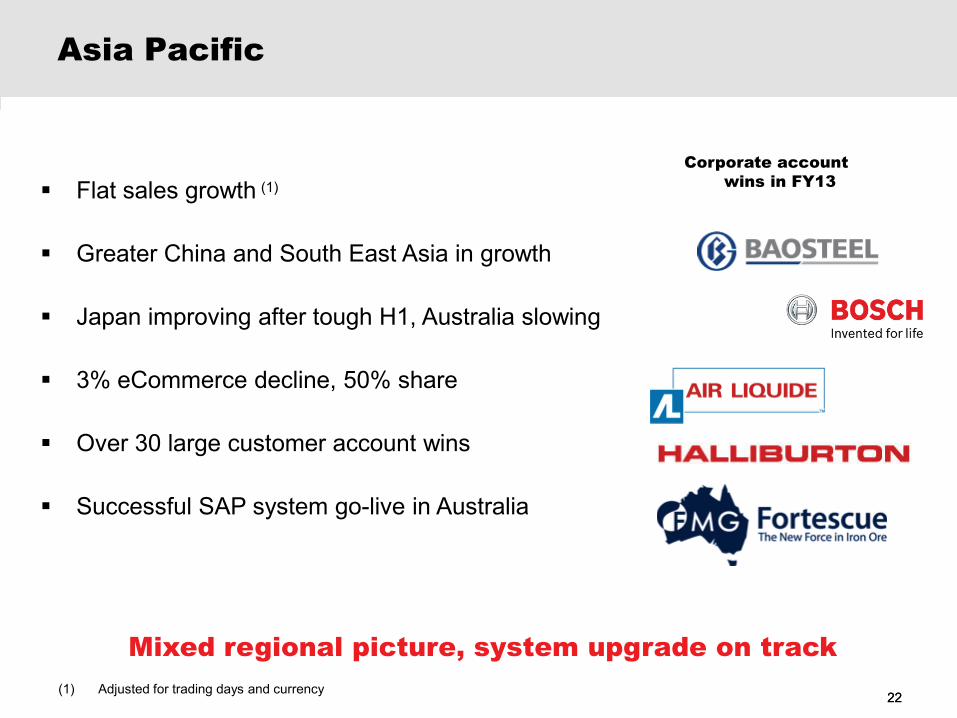

Asia Pacific

Flat sales growth (1)

Greater China and South East Asia in growth

Japan improving after tough H1, Australia slowing

3% eCommerce decline, 50% share

Over 30 large customer account wins

Successful SAP system go-live in Australia

Mixed regional picture, system upgrade on track (1) Adjusted for trading days and currency

Corporate account wins in FY13

To help protect your privacy, PowerPoint prevented this external picture from being automatically downloaded. To download and display this picture, click Options in the Message Bar, and then click Enable external content.

23 23

UK

4% sales growth (1), 1% ex-Raspberry Pi

c. 75% maintenance exposure

Strong sales of Raspberry Pi

10% eCommerce growth, 62% share

Corporate accounts performing well

Benefitting from maintenance and Raspberry Pi (1) Adjusted for trading days

Raspberry Pi Model B

24 24

Agenda

Overview and current trading Ian Mason

Financial performance Simon Boddie

Business performance Simon Boddie

Strategy update Ian Mason

Q&A All

• International growth• Electronics and Maintenance• eCommerce• Operating leverage• UK profitability

“The world’s distributor of choice”Vision

Strategy

Priorities

25 25

Successful delivery of strategy set in 2006

New opportunities identified

26 26

Delivered International growth, UK profitability

Opportunity for both International and UK to grow faster

0

100

200

300

400

500

600

700

800

900

1000

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

£m International Sales

APAC

US

Europe

CAGR

8%

8%

5%

International Growth UK Contribution

International 6%

Opportunity

Gain market share at faster rate

Opportunity

Grow in line with market, maintain profitability

27 27

Delivered two strong offers

Single global offer driving growth

Higher Electronics Growth balanced by Higher Maintenance Returns

Opportunities:

Grow faster and more efficiently with single global offer

Global pricing strategy to improve value for money perception, partially mitigate gross margin pressure

Customers Suppliers Cross-sell

Electronics Maintenance >100k new products

& technical marketing Automation & Control emerged

as leading technology

28 28

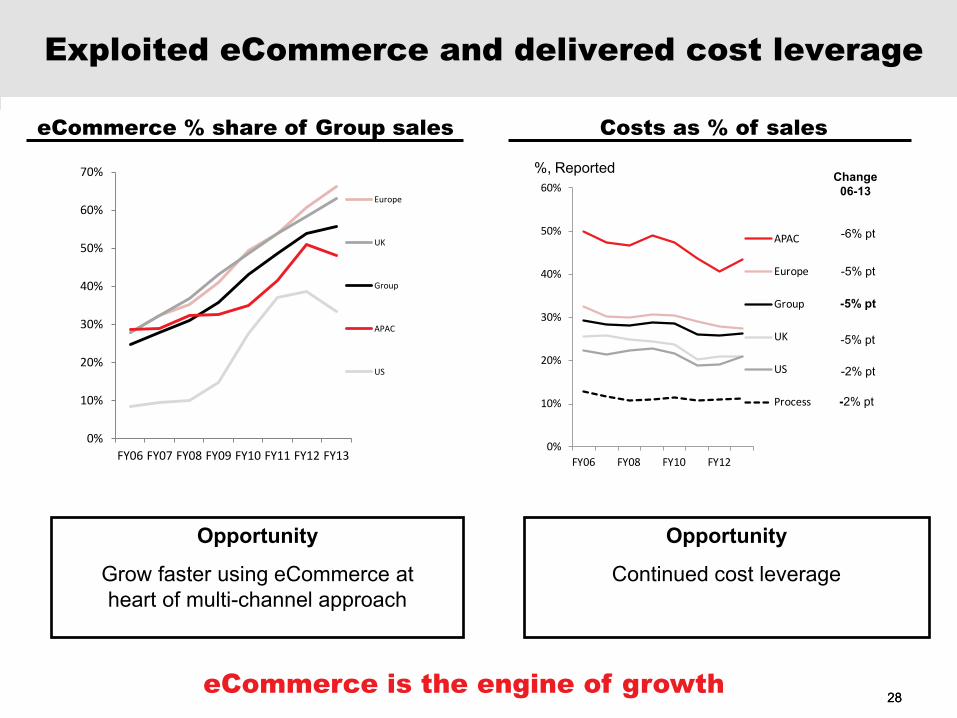

Exploited eCommerce and delivered cost leverage

eCommerce is the engine of growth

eCommerce % share of Group sales Costs as % of sales

0%

10%

20%

30%

40%

50%

60%

70%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Europe

UK

Group

APAC

US

0%

10%

20%

30%

40%

50%

60%

FY06 FY08 FY10 FY12

APAC

Europe

Group

UK

US

Process

Change 06-13

-6% pt

-5% pt

-5% pt

-5% pt

-2% pt

-2% pt

%, Reported

Opportunity

Grow faster using eCommerce at heart of multi-channel approach

Opportunity

Continued cost leverage

29 29

New global operating model implemented

Customer needs are similar everywhere

Leading suppliers are global

Internet enables faster customer acquisition

Organisation in place to capture benefits

Europe experience endorses common strategy

Enable global strategy delivery

IT FINANCE HR

SALES OFFER MARKETING

STRATEGY

Global Operating Model

30 30

Evolved to common global strategy

7 strategic priorities, integrated business plan

31 31

Grow target customers

Integrated strategy to service and grow each customer group

Focus on our four key contact types and their needs

One global offer

32

Key initiatives

More products, more efficiently

Global range

Global inventory management

Reliable 1,2,3 day service

Clear, distinct category strategies

Semiconductors

Automation & Control

Support

Electrical, Test & Measurement

SemiconductorsSemiconductors

Interconnect, Passives & Electromechanical

Automation & Control

Electrical, Test & Measurement

Support

,

eCommerce with a human touch

More customers, buying more 33

Key initiatives

Lifecycle management

Digital marketing

eCommerce functionality

Sales capability

eCommerce engine

Fuel eCommerce

Machine

Supporting

Infrastructure

Human Touch

34 34

Value for money

Key initiatives

Better price perception, improved value

Global pricing strategy

Value for money communication

Dynamic pricing

Improving our value proposition

Service

Price perception

Ease of doing business

Broad range of leading products

35 35

Strategic enablers

Strong platform for growth

• High-performing team

• Business insight

• World-class systems and supply chain

Global network of hubs

36 36

Increasing investment in strategic initiatives

Funded from existing cash flows

Capital expenditure investment Key strategic initiatives • Global inventory planning tools

• Systems enabling global range

• Develop APAC network

• Website functionality

• Search engine marketing, optimisation

• Global automated nursery programme

• SAP across APAC

• Enterprise architecture

• Global pricing tools

0

5

10

15

20

25

30

35

40

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

£m• Target average run-rate £40m pa

• Historic average run-rate £25m pa

0%

2%

4%

6%

8%

10%

12%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Return on sales adjusted to reflect 75:25 International:UK sales mix

37 37

Performance metrics

Focused on growth, profitability and cash flow (1) Underlying sales growth, adjusting for trading days and currency movements. Target range includes estimated market growth of 3.5%, historic includes market growth of 2.5%

-10%

-5%

0%

5%

10%

15%

20%

25%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Group sales growth (1)

• Target 5% - 8% pa

• Historic 4% pa

Group return on sales

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Free cash flow as a % of sales

• Target 4% - 6%

• Historic 3% - 8%

0%

5%

10%

15%

20%

25%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Return on capital employed

• Target 20% - 30%

• Historic 15% - 25%

• Target 9% - 11%

• Historic 7% - 10%

38 38

New medium-term performance framework

Targeting improved medium-term financial performance

(1) Performance between 2006 and 2013 (2) Underlying sales growth, adjusted for trading days and currency movements (3) Includes historic market growth of 2.5% (4) Includes estimated market growth of 3.5% (5) These are headline measures of profitability and cash flow which are defined as the relevant reported profit / cash flow before reorganisation costs / cash flows (6) Historical reported operating margin adjusted to reflect 75:25 International:UK sales mix (7) Operating profit as a percentage of net assets (including goodwill) plus net debt

Key Performance Indicator Historic Performance (1) Medium-term Target

Group sales growth (2) 4% pa (3) 5% - 8% pa (4)

Group return on sales (5) 7% - 10% (6) 9% - 11%

Return on capital employed (5) (7) 15% - 25% 20% - 30%

Free cash flow as % of sales (5) 3% - 8% 4% - 6%

39 39

Key themes

Challenging market conditions during FY13

Significant improvement in gross margin and cost performance in H2

Global operating model implemented to enable global strategy delivery

Evolved to common global strategy comprising seven strategic priorities

New performance framework, targeting improved medium-term financial performance

Common global strategy to drive improved performance

40 40

Agenda

Overview and current trading Ian Mason

Financial performance Simon Boddie

Business performance Simon Boddie

Strategy update Ian Mason

Q&A All

Electrocomponents plc

ANNOUNCEMENT OF PRELIMINARY RESULTS

YEAR ENDED 31 MARCH 2013 23 May 2013

42 42

Financial appendices

43 43

Impact of foreign exchange

Foreign exchange operating profit sensitivities: A 10 cent weakening of the Euro against Sterling reduces Group operating profit by c. £6m

A 10 cent weakening of the US Dollar against Sterling reduces Group operating profit by c. £2m

2013 2012 2012 Growth GrowthForeign exchange reported Foreign exchang

impact adjusted£m £m % %

International contribution

Continental Europe 90.9 99.8 (5.8) (8.9)% (3.3)%

North America 34.9 43.3 0.5 (19.4)% (20.3)%

Asia Pacific 12.0 17.7 0.1 (32.2)% (32.4)%

International 137.8 160.8 (5.3) (14.3)% (11.4)%

UK contribution 105.9 106.0 (0.0) (0.1)% (0.1)%

Group contribution 243.7 266.8 (5.3) (8.7)% (6.8)%

Process costs (139.4) (138.7) 1.3 (0.5)% (1.5)%

Headline operating profit 104.3 128.1 (4.0) (18.6)% (16.0)%

Reported

44 44

800K Catalogues 56% e Commerce

44,000 Parcels Daily

> 1m Customers

Strong Brands

2,500 Major Suppliers > 550,000 Products

17 Distribution Centres 90+% of World GDP

Electrocomponents: what we do

The World’s distributor of choice