Embed Size (px)

Citation preview

Internal Documents

INDUSTRY AND ENERGY DEPARTMENT WORKING PAENERGY SERIES PAPER No. 52

Electricity Pricing:Conventional Views and New Concepts

March 1992

ji,(r, .- 4 . .. . . .~~~ .- 0 .

The World Bank Industry and Energy Department, PRE

s SE g -o °ILE.COPY

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ELECTRICITY PRICING: CONVENTIONAL VIEWS AND NEW CONCEPTS

by

Witold Teplitz-Sembitzky

Energy Development DivisionIndustry and Energy Department

Sector and Operations Policy

March 1992

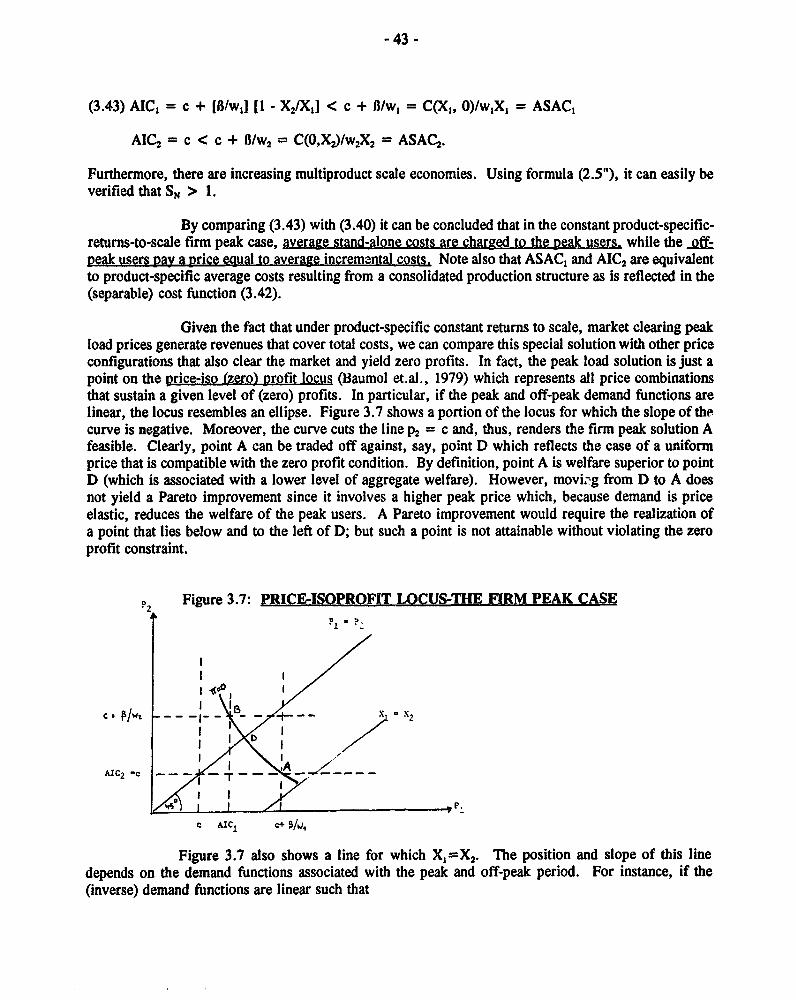

Copyright (c) 1992The World Bank1818 H Street, N.W.Washington, D.C. 20433U.S.A.

T. s report is one of a series issued by the Industry and Energy Departnent for theinformation and guidance of Bank staff. The report may not be published or quoted asrepresenting the views of the Bank Group, nor does the Bank Group accept responsibilityfor its accuracy or completeness.

The author is grateful to Mr. Amadou Cisse for valuable discussions, critique, andsuggestions. Helpful comments on an earlier draft of the paper were also provided byMr. John Besant-Jones.

Execufive Summary

Both in theory and practice, electricity pricing is a difficult and complex subject. This paperfocuses on the theoretical aspects of electricity pricing and thus neither resolves the manypractical problems of designing electricity tariffs nor offers an agenda for immediate action.Instead, it attempts to clarify the debate over conventional and new theories of electricitypricing by examining the rationales of some basic assumptions about pricing, includingmarginal cost (MC) pricing, Ramsey-pricing, sustainable pricing, axiomatic pricing, averagecost pricing, priority service pricing, and price capping. The analysis suggests thatdoctrinaire adherence to marginal cost and efficiency principles may be inappropriate andinsufficiendy responsive to the uneveiu, rapidly changing, and often financially shaky powersectors of developing countries.

Electricity pricing is fraught with a number of complications that reflectessential technical characteristics of the power sector. To simplify matters, this paperdisregards spatial aspects of power transmission and distribution (i.e., restricts its focus tothe generation end). This still leaves the analysis to cope with key features that distinguishe!ectricity pricing from putting a price tag on, say, office supplies:

1. Electricity is nonstorable; it is generated at different times to serve loads of differentsize at different priority levels. Thus, power generation is a multiproduct industry inwhich the outputs can be indexed by time of use and priority of service.

2. Power generation is an exarnple of joint production that exhibits economies of scopefrom horizontal integration and, thus, is cheaper than separate production. Putanother way, generating capacity qualifies as a public input (i.e., an input that canproduce several outputs or loads on a nonrival and nonexcludable basis).

3. Economies of scope entail multiproduct economies of scale (i.e., total costs exceedthe weighted average of marginal costs defined along a ray from the origin). By thesame token, the incremental costs of generating a particular load fall short of thecorresponding stand-alone generation costs. In addition, there may existproduct/load-specific scale economies.

4. Power sector investments are to a significant extent transaction-specific and,therefore, sunk (i.e., the worth of the sector's assets cannot be recovered entirelyupon exit.

These features have several implications:

1. Allocating costs and setting prices across different outputs becomes a complex taskthat eludes single-product reasoning.

2. In the presence of sunk costs, the mechanics of competition cannot be expected toimnplicitly .egulate or discipline the sector in an efficient and reliable manner. Someform of explicit regulation will be needed to ensure that sector performance ingeneral and tariff setting in particular live up to the standards ascribed to areasonably compeddve market.

3. Under economies of scope, the competitive ideal of independent, atomistic suppliersis at variance with the requirements of an efficient industry structure. At theminimum, efficiency calls for central coordination (merit order dispatch) of a limitednumber of suppliers. It may even warrant a structure based on a single supplier

- ii -

(natural monopoly). The latter case would apply if a monopoly enjoyed costadvantages with respect to any conceivable combination of outputs that the marketcan absorb.

The distinguishing features of the power sector notwithstanding, standardeconomic arguments suggest that in a multiproduct industry marginal costs (MC) are asvalid a benchmark for static efficiency pricing as in a single-product context. In fact,tailored to the characteristics of power generation, the ideal of multiproduct MC pricingassumes the form of time-of-use pricing, often referred to as peak-load pricing, or spotpricing, an upbeat variant of the MC principle that defines time in terms of instants.

The rationale for MC pricing is that it is necessary for an efficient allocationof resources that maximizes aggregate welfare. For that matter, efficient prices need to clearthe market and, as the notion of "spot pricing" emphasizes, should be based on short-runmarginal costs. Frequent disclaimers to the contrary, these requirements will not be met byprices based on long-run marginal cost (unless demand and supply are poised in a long-runeq"s'iium), let alone long-run average (incremental) costs. To make matters worse, inpractical applications the long-run approach to pricing of electricity usually is confined to ascalar measure of system costs that blurs the multiproduct nature of power generation.

MC pricing, however, is *n general not sufficient for economic efficiency. Itmay even be inefficient. For instance, if the electric -tility uses oublic funds that havepositive shadow costs, prices should exceed MC. Likewise, if MC pricing does not recovertotal costs, it may be better to charge financially viable prices iather than to balance theutility's accounts through indirect transfers.

Moreover, MC pricing can be rejected on equity grounds. Prices departingfrom MC may be justified as a substitute for imperfect taxation to redistribute income.Also, a switch to time-of-use pricing that improves on aggregate welfare but makes peak-load customers worse off may be considered unacceptable to the extent that it violates thePareto-principle.

Finally, the incentive framework may not be conducive to MC pricing, and aregulatory authority may not be in a position to successfully enforce MC prices. In fact, thelack of commitment on the part of the utility to charge efficient tariffs is pervasive in theabsence of disciplining market forces. Therefore, electric utility regulation is commonlydeemed a prerequisite for efficient pricing. Regulatory hierarchies, however, tend to beinefficient, too. In particular, utilities have an informational edge over the regulator and,thus, may evade agreed duties and covenants.

In short, although MC pricing is necessary for maximal welfare, real worldconditions rarely lend themselves to first-best solutions. If technical, institutional, oreconomic impediments spoil the decisionmakers' environment, a responsive pricing seategythat explicitly accounts for constraints is more likely to be efficient than is a doctrinaireadherence to the yardstick of marginal costs.

When MC pricing involves financial losses that the utility is required toavert, multiproduct Ramsey-pricing, which calls for markups over MC inverselyproportional to the elasticities of demand, ranks second from the viewpoint of economicefficiency. (In fact, it is first-rate with respect to the break-even constraint.) This is becauseit minimizes the partial equilibrium deadweight loss that financially viable prices departingfrom marginal costs tend to incur. Regrettably, however, the Ramsey rule-like the MCyardstick-only provides a necessary condition for second-best optimality. Whether or notRamsey pricing leads to a second-best outcome is an entirely different question. Applying

- iii -

the rule may be of no avail ir. the struggle for break-even constrained efficiency unlessdemand and supply are "well-behaved."

Another problem with Ramsey-pricing is that it may entail cross-subsidiesamong outputs and, thus, cross-subsidies among consumers. In this event, a utility acting asa second-best welfare maximizer is vulnerable to profitable, but inefficient entry (i.e., someconsumers have an incentive to defect to rival suppliers even though this would reduce thelevel of aggregate welfare). By the same token, Ramsey-pricing may be at odds withpolicies designed to instill competition in the power sector, because increased competitionreduces the scope for the large markups the Ramsey rule advocates in inelastic markets.

An alternative approach that counts on the merits ascribed to competitionwhile seeking to protect the incumbent udlity against inefficient entry has been suggested bythe "contestability" literature. The idea is that an efficient industry structure may besustainable with the aid of financially viable prices that keep customers satisfied and deterentry. By definition, sustainable prices must clear the market, recover costs, and rule outcross-subsidies. Unfortunately, such prices may be elusive that is, it may not be feasible tosafeguard an efficient industry structure with the help pricing policies alone. Apart fromthat, unsustainable Ramsey prices are welfare-superior to sustainable prices. Thus, one hasto trade off the virtues of sustainable prices against the potential welfare gains from strictRamsey-pricing.

Notwithstanding the doubts abo&. the feasibility and welfare properties ofsustainable pricing, the contestability literature h _ 4;Žawn attention to the crucial question ofwhe ther and to what extent a utility can be obliga ,- or impelled to put a particular pricingpolity into place. In this rega.d, the argument raised by the contestable market concept isthat the forces of potential entry bring prices on a path toward sustainability. Is there asimilar built-in mechanism that would induce a utility to adopt prices that are close toRamsey levels? The answer is no. Analogous to the case in which MC pricing is called forin the absence of reasonably competitive markets, there is no incentive mechanism thatwould prompt the utility to self-select Ramsey prices. Rather, Ramsey pricing, like MCpricing without competition, needs to be enforced through regulatory arrangements.Clearly, in practice, the disciplining forces behind sustainable prices may turn out to be asweak as is the incentive to implement Ramsey prices. The contestability literaturenevertheless made a strong point in highlighting the need to assess pricing rules in terms ofthe regulatory and incentive framework required for their implementation.

Interestingly enough, another line of argument, the axiomatic pricingapproach, does not focus on the contestability of markets, but reaches at a multiproduct costallocation procedure that may closely match the properties of sustainable prices. Theapproach hinges on the claim that prices, to be desirable, should satisfy a number ofconditions defined in terms of fairly plausible rules for cost accounting, including theprinciple of cost recovery. In the special case when costs are separable across outputs, theonly cost-based pricing mechanism that complies with this particular set of desiderata boilsdown to average cost (AC) pricing. In the context of power generation, this solution isequivalent to load-specific average cost pricing or time-of-use pricing, with the peak-loadprice based on average stand alone costs and off-peak prices set equal to the averageincremental costs of serving off-peak demand. Moreover, under economies of scope, load-specific average cost prices will be sustainable.

Apart from its affinity to the concept of sustainability, axiomatic pricing hasother appealing features. It "rationalizes" the debate over the desirability of pricing rules tothe extent that it can be derived as a conclusion from transparent premises. Its informationalrequirements are less demanding than are those of Ramsey-pricing. And if the

- lv -

decisionmaking process within the utility is decentralized along cost of profit centers, it isthe only mechanism that unambiguously rewards or penalizes good or bad performance.

On the other hand, axiomatic pricing has the disadvantage of forgoingpotential welfare gains that could be captured by discriminating across outputs/markets inthe style of Ramsey-pricing. And a weakness shared with MC, Ramsey-, and sustainablepricing is its lack of commitment. That is, there is no a priori reason why a utility should bekeen on axiomatic pricing (or AC-pricing) and at the same time pursue the goal of costminimization.

Ramsey-pricing, on the other hand, pinpoints a simple but pivotal pc' toolfor improvements on welfare that cost-based pricing strategies are unat ,o acco. .lish.By placing the focus on demand characteristics that may vary across markets -onsu- , o,both, the Ramsey approach increases the decisionmaker's degree of freedom in settir.,tariffs. Even though the inverse elasticity rule of Ramsey pricing is designed as a device forconstrained welfare-maximization, the logic underlying the approach can just as well beused to pursue the less zealous goal of making improvements in welfare feasible. In fact, inthe presence of consumers with diverse preferences, any uniform price charged per unit ofoutput and exceedir g marginal costs can be Pareto-dominated by an additional optionaltwo-part tariff, consisting of a fixed entry fee and a usage charge. This is because anincrease in the scope for choice, if properly designed, can make some consumers better offwithout making others, including the utility, worse off.

From a practical viewpoint, the main advantage of the optional pricingapproach to enhancing welfare is that it can be implemented without a comprehensiveknowledge of the consumers' demand functions. Clearly, the more information is availableto the decisionmaker, the better are the opportunities to fine-tune the options. In the extremecase, with perfect informnation, this strategy would result in the design of an optimalnonlinear tariff schedule that maximizes total welfare, subject to the utility's break-evenconstraint. By dint of discriminating continously across consumer classes in each market,such schedules Pareto-dominate linear Ramsey-pricing. Also, they will involve quantitydiscounts when (1) the elasticity of demand for an additional kWh (usage) increases withthe number of kWhs purchased, and (2) the excess willingness to pay for usage issufficiently large to justify the provision of additional capacity. Needless to say, theinformational requirements for achieving a constrained optimum with the help of nonlinearprices are even more forbidding than in the case of ordinary Ramsey-pricing. The principlemessage, though, remains valid: Flexibility, -that is, increasing the degree of freedom inpricing-is a means of improving both the consumers' well-being and the utility's accounts.

As it affects industry structure and sector performance, nonlinear pricing hasboth advantages and drawbacks. If the utility qualifies as a natural monopoly and ispermitted to charge nonlinear (discriminatory) tariffs, it may be able to foreclose entry andat the same time earn positive profits. Hence, it is conceivable that an inefficient utility willsurvive in contestable markets. By the same token, however, nonlinear pricing may help anotherwise unsustainable but efficient utility to withstand the threat of entry. This impliesthat even in the typical case in which the disciplining force of potential entry or intermodalcompetition is weak, nonlinear pricing may be ber,eficial rather than harmful or ruthless.

Priority service pricing is another example of how the mechL.aism of self-selection can improve on welfare and efficiency. Because outages at the generation end areunavoidable, even though the likelihood of their occurrence can be influenced through byproviding reserve capacity, the utility has to decide on reliability design targets and theallocation of shortfalls. By offering service contracts that charge a premium on electricity inlimited supply, the utility can encourage consumers to choose their preferred orders of

t ~~~~~~~~~~~~~~~~~~~- v -

priority in obtaining service. Moreover, by inducing consumers to reveal their willingnessto pay for "reliability," priority service pricing renders the separate calculation (estimatiop)of nutage costs-often tenuously derived-superfluous and thus eases tne task ofde m-rmining the optimal size of capacity. Again, because of informational and technical"0oA3-aints, optimal priority scrvice pricing will not be feasible hli practice. However, evenim,perfectly designed service conmacts are likely to improve welfare compared with theE .rnaave of random rationing.

In discerning and comparing the virtues of alternative pricing policies, oneshoulc not 1.,se sight of the fundamental dilemma mentioned before. In the power sectorthere is no "invisible hand," not even a workably efficient one. The analogy of a perfectlycompetitive r. .rket in which firms minimize costs and maximize welfare in the quest ofprofits is misplaced. On the other hand, regulatory authorities that are supposed to control,reward, or penalize sector performance more often than not have little or no knowledge ofthe sector's cost and demand functions. Thus, regulatory failures are likely to occur andmay cause as much grief as do market imperfections. This dilemma has prompted thequestion of whether and how utilities can be induced to adopt pricing strategies with animplicit commitment to cut costs and benefit consumers.

An interesting and promising answer to this problem is the price cappingapproach. The basic idea behind price capping is that utilities should be allowed tomaximize profits (and thus minimize costs) subject to a price constraint. Simply put, aslong as it does not raise prices above a fixed or indexed level, a utility with a money-makingspirit should do what it likes to do. Under ideal conditions, this would trigger an iterativeprocess with amazingly appealing convergence properties. It goes without saying that inpra_tical applications the prospects for price capping are less advantageous than in theory.The problems besetting the design and implementation of prices caps notwithstanding, theapproach is likely to score better on efficiency than clumsy price regulation-provided thatthe utility generally follows the line of conduct attributed to the profession of entrepreneurs.

What conclusions can be drawn with respect to electricity pricing indeveloping countries? The paper suggests the follow:ng:

Worshipping the principle of MC pricing may do as great a disservice to economicefficiency as does the politiciz .tion of pricing issues. In particular, when manyelectric utilities in developing countries are on the verge of a financial collapse,pricing policies guided by the first-order conditions of global welfare maximum aremisplaced. Rather than requiring the utilities to pine for an optimum optimorum,emphasis should be placed on strategies that help restore the solvency of the powersector. For that matter, pricing has to be relieved of sacrosant efficiency objectivesand should come to grips with more mundane and immediate commercial ends.

* The power sectors of developing countries are typified by lumpy investments incapacity required to meet rapidly growing demand accompanied by changes in boththe shape of the load duration curve and the merit order dispatch. Thus, pricinggenerally takes place in a system disequilibrium. Consequently, pricing rules tunedtoward conditions under which the supply mix matches the pattern of lemand willbeflawed.

* Long-run marginal costs (LRMC) are a misleading benchmark for electricitypricing. Unless the power sector invests and operates on a steady-state equilibrium,LRMC pricing cannot be justified on efficiency grounds. Frequent disclaimers tothe contrary, it would in fact be inefficient. For all practical purposes, LRMCs oftenare treated as a scalar measure defined as a ratio of annuities. This measure not only

- vi -

is a far cry from the concept of marginal costs but it aiso is useless for the design ofmultiproduct tariffs.

Generally speaking, responsive pricing or "profane yet intelligent pricing" tends torate better than strict or ro'itine use of inflexibie or unwieldy formulas that serveelusive efficiency goals or rest on ill-conceived arguments such as price stability. Inthe same vein, welfare-enhancing pricing policies often are more to the point thanprescriptions governed by the scholastcism of welfare maximization. For instance,load-specific average cost prices are apt to Pareto-dominate an arbitrary anagementof tariffs that are clustered around system average incremental costs and purport totake account of unknown demand characteristics. Likewise, in terns of welfare, amenu of optional discriminatory tariffs tends to gain more ground than doesRamsey pricing based on tedious but shaky estimates of price elasticities.

Finally, from a regulatory viewpoint, guidance, supervision, well-defined rules of thegame, and arm's-length obligations (which should not be confused with armchairregulation) make more sense than putting the utilitv into the straitjacket of aparticular pricing policy.

- vii -

ELECTRICITY PRICING: CON'VENTIQNAL VIEWS AND NEW CONCEPTS

Table of Contents

Executive Summary .............. , i

Table of Contents .vii

List of Figures .viii

1. Introduction. 1

2. Basic Cost Concepts ............. ........................ 42.1 Introduction ............. 42.2 The Single-Product Case ................................... 52.3 The Multiproduct Case .................................. 72.4 Cost Allocations ................................... 12

3. Marginal Cost Pricing ................................... 193.1 The Single Product Case .................................. 203.1.1 SRMC versus LRMC in a Static Setting ........ ................ 203.1.2 MC-Pricing in a Dynamic Setting ............................ 293.1.3 First-Best Optimality and Second-Best Fallacies .................... 333.1.4 Practical Approximations to Single Product MC-Pricing .... ........... 363.2 The Multiproduct Case . ................................... 393.2.1 Peak Load Pricing with Single Technology ....................... 393.2.2 Peak Load Pricing with Diverse Technology ...................... 463.2.3 Avoided Cost Pricing . ................................... 493.2.4 Capacity Cost Responsibility in the Face of LOLP .................. 563.2.5 Real Time Pricing ...................................... 59

4. Lir, Leak-Even Pricing . ................................. 614.1 W. Pricing ................ 614.2 Sl.. idnable Prices and Efficient Industry Structure ...... ............ 674.3 Sustainability and Financial Viability under Alternative

Linear Pricing Regimes ......................... 71

5. Nonlinear Pricing ......................... 745.1 Two-Part Tariffs ......................... 755.2 Optimal Nonlinear Tariffs ......... ................ 805.3 Priority Service Pricing ......................... 865.4 Sustainability and Nonlinear Pricing ......................... 89

6. Summary and Conclusions ......... ................ 91

References .. 99

- viii -

List of Figure

Page No.-

Figure 3.1 Demand and Supply Equilibrium under MC-Pricing .... ........ 20Figure 3.2 Welfare Improvement from MC-Pricing under

Decreasing AC ..................... 24Figure 3.3 LRMC under Constant Returns p.., qc3le............... 26Figure 3.4 LRMC under Increasing Rt... to Sale .27Figure 3.5 Capacity Additions and MC-Pricin ............ ............ 28Figure 3 6 The Shifting Peak Case . .............................. 41Figure 3.7 Price-Isoprofit Locus: The Firm Peak Case ..... ........... 43Figure 3.8 Price-Isoprofit Locus: The Shifting Peak Case ..... .......... 45Figure 3.9 Load Duration Curve with Given Rates of Usage ..... ......... 48Figure 3.10 Linear Load Duration Curve .51Figure 3.11 Base-Biased Load Shift .......... ............. 53Figure 3.12 Composite Load Duration Curves ....................... 57Figure 4.1 Single Product Monopoly Violating the Anonymous

Equity Condition . 69Figure 5.1 Welfare Improving Optional Two-Part Tariff with

Two Consumer Classes .............................. 77Figure 5.2 Declining Block Rates and Two-Part Tariffs ..... ............ 79Figure 5.3 Consumer Participation in a Differential Market ..... ......... 83Figure 5.4 Optimal Profit-Maximizing Tariff Schedule ..... ............ 85Figure 5.5 Sustainable Multiple Tariffs ............ ............... 90

i. Ainioauct:o

Ever since electric power was generated, pricing of electricity proved to be a thornyissue. thanks to the inputs of professionai economists who did not enter the debate until the 191(s(Hausmann and Neufeld, 1984), there are two lines of argument that have shaped the orthodox viewabout rate setting in the power sector. One 7s related to the categorical imperative that marginal cost(MC) pricing is first best on ecoiiomic effPciency grounds. The other hinges on the problem that ifa profit maximizing electric utility enjoys (rightly or wrongly) the status of a monopoly, it cannotbe expected to base prices on marginal costs.

In fact, economic analysis tells that %ader certain conditions MC-pricing is necessaryfor an optimal allocation of resources, whereby optimality is defined in the sense that relative to agiven initial distribution of resource endowments, no one can be made better off without makingsomeone worse off. Moreover, it has been shown that any MC-pricing equilibrium can be achievedby means of perfectly competitive markets, with profit maximizing firms and utility maximizinghouseholds as participants. Accordingly, if the competitive market paradigm is distorted by a naturalmonopoly, - an industry structure that electric utilities were considered to conform with -, thenecessary conditions for efficiency can only be fulfilled by requiring the monopoly to charge (marketclearing) MC-prices. This explains why MC-pricing of electricity often is discussed as a prescribedrule for conduct, rather dhan as a strategy that utilities would not hesitate to choose in the quest ofprofits. Put differently, in policy terms there is a correspondence between MC-pricing and (public)utility regulation.

The rationale for MC-pricing notwithstanding, fact is that there persists the tendencyto water down the principle of MC-pricing by blending it with other objectives. Strict adherence tothe ideal of MC-pricing has been and is being rejected on account of

- cost allocation procedures,- financial requirements,- fairness and equity considerations,- distortionary impacts stemming from the rest of the economy,- market imperfections, notably nonconvexities (e.g. increasing returns to scale),- informational impediments, measurements difficulties, and implementation

problems,- etc.

So the debate over electricity tariffs is kept alive not only by fervent proponents ofthe principle of MC-pricing; there continue to prevail divergent views, including the agnostic oneaccording to which there should be no committment to a particular pricing dogma.

A compromising stance has been advocated by the World Bank. In the OMS No. 2.25of March 1977, it is argued that in the power sector "efficiency pricing should normally be thestarting point, with financial objectives... an equally important consideration; income distributionis generally not an important factor ---, but there may well be scope for indirect taxation fallinglargely on higher income groups".

It seems that the above directive by and large has guided the Bank's policy towardselectricity pricing in practice. Based on a sample of tariff studies and appraisal reports, Blake (1990)

reckons that "financial requirements figure prominently", while (long-run) marginal costs play therole of a benchmark. In the same breath, he critisizes that marginal costs have not always beendefined in a way consistent with the efficiency objective, and asserts that the thrust of "economicanalysis of tariffs must be on efficiency first and foremost" (p. 44).

Thus, while a strong case can be made for MC-pricing, accomplishing th-. "first best"does not seem to be an overriding concern in practical applications. Furthermore, on the theoreticalfront, "public utility pricing" in general and MC-pricing in particular are far from being a doctrinalmatter. Rather, there is a wide spectrum of ideas and concepts, ranging from refined andsophisticated versions of MC-pricing to alternative approaches that depart from the MC-pricing ruleand/or deal with issues less fuzzy and less elusive than that of social welfare maximization.

The purpose of the present paper is to provide an outline of, and comment on bothstandard analytical problems and new concepts relevant to electricity pricing. To simplify matters,the focus is on the generation end, i.e., the emergent and highly controversial issue of transmissionpricing will be neglected. The paper maintains the view that on economic grounds pricing ofelectricity is essentially different from attaching price tags to, say, furniture. (If not it would befutile to agotfze over a pricing problem that may be distinctive in degree, but not in kind). A keyto the difference lies in cost characteristics. Power generation is an example of joint production witheconomies of scope (which can be captured through merit c:der dispatch); the power sector issaddled with substantial fixed costs, and there may exist scale and network economies. Thesefeatures, which are discussed in Chapter 2, have a strong bearing on the efficient industry structureand the way in which multiproduct pricing policies can sustain efficient production and investmentplans. Needless to say, single product reasoning is likely to preempt wrong judgements about pricingin this contexi.

Th7 above caveat notwithstanding, the paper makes use of the single-product-partial-equilibrium framework to highlight the subject matter of MC-pricing. The static short-run versuslong-run controversy is addressed in Section 3.1.1, while Section 3.1.2 presents a dynamic versionof single product MC-pricing, with due consideration given to the treatment of capacity costs.Practical approximations to MC-pricing as well as their shortcomings are discussed in Section 3.1.4.

However, pertinent to the power sector and analytically more interesting is the casewhere multiple outputs (loads) are produced jointly with the help of a "public input". A pivotalquestion that emerges in this connection is how to allocate costs and set prices across outputs andconsumer classes. Depending on the attributes that cost allocation schemes are desired to possessand contingent on the irformational and regulatory leeway for tariff setting, there are a number ofstrategies to choose from.

The standard peak-load (time-of-use) pricing solution is presented in the Sections3.2.1-3.2.2. Reconciling this solution with revenue requirements leads to second-best Ramseypricing that is dealt with in Section 4.1.

Peak-load and Ramsey pricing already enjoy the status of textbook wisdom, at leastamong interested experts. However, there is variety of arguments and concepts, most of themdeveloped during the 1980s, which are relevant or contribute to the debate over tariff setting, but

- 3 -

have received little or no attention so far (except among specialists). The paper attempts to closethis gap. Due regard is given to

- the axiomatic pricing approach (Section 2.4) which, if applied to power generation,may vindicate load-specific average cost pricing (Section 3.2.1), and which is the onlycost allocation procWture that is incentive compatible within a context of decentralizeddecision making (Section 2.4);

- the concept of sustainable pricing (Section 4.2) which became prominent in the wakeof the contestability literature and features tariff attributes that are not (necessarily)captured by MC or Ramsey pricing (Sections 4.3 and 5.4);

- the measurement of avoided costs (Section 3.2.3);

- the idea of real time pricing (Section 3.2.5), a "technocratic" extension of time-of-usepricing to spot markets, that has gained momentum in the discussion of deregulationpolicies in the US and UK power sector;

- reliability and priority service pricing (Sections 5.3 and 3.2.4);

- optimal nonlinear tariffs (Section 5.2) which can improve on linear Ramsey pric? -gby discriminating across consumers with different preferences;

- welfare improving pricing strategies with low-key informational and regulatoryrequirements such as price capping (Section 4.1) and optional two-part tariffs (Section5.1).

In addition, the paper draws attention to second best considerations that can beinferred from a general equilibrium framework (Section 3.1.3), with a special focus placed on scaleeconomies and their impact on the attainability of an optimum through MC-pricing, or, as the casemay be, a second-best outcome through Ramsey pricing.

In short, the paper puts the issue of electricity pricing into a broader perspective.While MC-pricing is necessary for an efficient (economy-wide) allocation of resources, it may notbe workable. It is difficult to design, enforce, or foist. Informational/financial/accountingconstraints, distortions in the incentive framework, regulatory puzzles or political/institutionalobstacles tend to thwart first best pricing strategies, let alone rules of thumb which allude to therespectable, albeit equivocal, goal of social welfare maximization. Stated differently, under second-best circumstances, allocative efficiency and, thus, strict MC-pricing may cease to be the bottomline. This does not justify the dismissal of efficiency considerations. Rather, the usefulness of aparticular pricing policy has to be evaluated with respect to the suitability and attainability of theobjectives it is supposed to serve. Also, the pruning of both objectives and policies becomes moreimportant than scholastic rule making. Economic analysis has a good deal to say on these matters,as will be shown in the following chapters.

-4 -

2. Basic Cost Concepts

2.1 Introduction

The structure and behavior of cost functions that typify power generation, transmissionand distribution systems have a strong bearing on sector organization and management in general andelectricity pricing in particular. First and foremost, cost properties decide upon whether sectorfacilities have a natural monopoly status and, consequently what is the most efficient industry/marketstructure. Secondly, the level and composition of costs play a crucial role in determining revenuerequirements and cost allocation rules. Thirdly, the way in which costs are shared or accounted forby prices not only effects economic efficiency in the large, but also creates incentives/disincentiveswithin the sector (utilities). Finally, the "fairness" properties of prices charged for utility servicesto a considerable degree depend on cost-related matters.

Understanding the cost characteristics, i.e. the "shape of the cost surface" of electricutilities therefore is at the heart of both sector management and pricing decisions. In this context,conceptual clarity and a bit of analytical rigor are needed to lay the groundwork for a number ofarguments which will be raised in the following chapters. To simplify matters, the focus is restrictedto the generation level (which typically accounts for more than 70% of total electricity supply costsin LDCs). Having in mind that power generation essentially is multiproduct, we begin with the moretractable single-product case and after that extend the analysis to cover various issues o' jointproduction (sections 2.2 and 2.3). Among other things, the focus will be on economies of scale andscope, the concepts of subadditive costs and cost complementarities, and on cost allocationprocedures. It should also be mentioned that the present chapter is confined to a static setting.Dynamic aspects of power generation will be addressed in Chapter 3 (Section 3.1.2).

Readers who are not interested in the technical details presented in the followingsections may skip Chapter 2 and continue with Chapter 3.

In the following lines a cost function, denoted by C(X), is defined -relative to giveninput prices - as the minimum cost of producing output X which can be a single product or a vectorof n products. A long-run cost function refers to a minimum cost figuration which can be achievedby (instantaneously) adjusting all inputs. In particular, we assume (unless otherwise stated) that inthe long-run there are no fixed costs in the sense that it is feasible to cease production at no cost,i.e. C(O) = 0. In the short-run, however, some of the costs tend to be fixed, i.e. do not change asoutput varies. This inflexibility may be due to contractual commitments or indivisibilities andirreversibilities of investments. In fact, some of the costs may prove sunk, i.e. cannot be recoveredeven in the long-run so that C(O) > 0.

Accordingly, a short-run cost function in general contains a fixed cost component andcoincides with the long-run cost schedule only if the actual output level is that associated with a long-run cost minimum. As a consequence, if, due to fixed costs, the short-run costs are above the levelthat would prevail in a long-run cost minimum, the fixed costs need to be allocated directly throughthe short-run cost function rather than under long-run cost considera.ions. On the other hand, if allinputs are free to vary (e.g. if investment in now capacity is required to produce output X), the long-run cost function will govern the allocation of short-run costs.

Also, a cost fiu ion is said to be additive if it can be broken down into differentcomponents, say labor (CI) and fuel (C2), such that

C(X) = C1(X) + C2(X)

On the other hand, a multiproduct cost function is said to be additively separable across outputs ifthe outputs, say, XI and X2 can be produced independently, say, at costs D(X,) and E(X2), such that

C(X) = D(Xj) + E(X2), with X = (XI, X2)

Separable cost functions have the advantage that each output can be held "responsible" for aparticular portion of the total costs (or, as the case may, net revenues). Unfortunately, though, costfunctions cannot in general be assumed to be separable. For instance, the function

C ,X 2) =X + X2 + (X + X2) 1/2

is non-separable across the outputs XI and X2. Another class of non-separable cost functions arethose which contain non-attributable fixed costs. The problem of apportioning non-separable costswill be discussed comprehensively in Section 2.4.

2.2 The Single-Product Case

Irrespective of whether decisions are made with a view towards the short-run or thelong-run, in the single-product case the properties of cost functions are typically discussed in termsof the behavior of average costs (AC) and marginal costs (MC). While the former measure the ostsper unit of output, the latter refer to the instantaneous rate of change in costs with respect to changesin output. In fact, marginal costs are equal to the incremental average costs evaluated at the limitwhere the change in output approaches zero, i.e.

MC = dC/dX = lim [C(X+ AX) - C(X)1/AXAX- O

(Note that we assume that there is no discontinuity in the cost function).

Clearly, the area under the average cost curve up to X measures the total costs ofproducing output X, while the area under the marginal cost curve is equivalent to the total variablecosts of producing output X.

Moreover, if average costs deviate from marginal costs there will be economies(diseconomies) of scale. The degree of single product scale economies can be defined as the ratioof AC to MC

(2.1) S6 = AC(X)/MC(X)P'1.

- 6 -

As can easily be verified, there will be increasing (decreasing) returns to scale if and only if averagecosts are decreasing (increasing). For instance, average costs are decreasing everywhere if and onlyif

(2.2) C(XX) <AC(X) , A > 1.

Differentiating (2.2) with respect to X for a given X yields (dC/dx)x < C which is equivalent to S.> 1 (increasing returns to scale).

In the single-product context, there are only two reasons why AC may decline: Inthe absence of fixed costs, decreasing variable unit costs will be sufficient for AC to decline; andwith nondecreasing variable unit costs, the presence of fixed costs is necessary for AC to decline.

The case of decreasing AC has gained prominence since traditionally it was considereda prerequisite for a monopoly to figure as a natural one. In fact, under decreasing AC or, whatcomes to the same thing, increasing returns to scale, a single producer enjoys a cost advantage overany group of two or more firms that produce the same quantity of a given product. Stateddifferently, declining AC imply strict subadditivity:

A single-product cost function is said to be strictly subadditive at output X if for anylist of outputs Xj > 0, i = 1,2, ... , k, that add up to X, the inequality(2.3) C(X) < E C(Xi)holds.

In fact, it is the concept of subadditive costs rather than scale economies that specifiesthe conditions a firm has to fulfill in order to qualify as a natural monopoly. That the requirementsof declining AC are much stronger than those implied in subadditivity can be shown with the aid ofthe cost function

C(X) = 1 +x 2 .

Obviously, with the above cost function, a single producer enjoys decreasing averagecosts (increasing returns to scale) up to output X = YPI = 1 at which the average cost minimum isachieved. Beyond this threshold average costs will increase. Now, if the output is shared betweentwo firms they must produce X/2 each, and their combined costs will exceed the costs of a singleproducer if

1 + X2 < 2 [1 + (X/2)21, which is equivalent to X < VFThus, there is an output range 1 < X < r2 where the single producer's cost function continues tobe subadditive even though average costs increase, reflecting the fact that in the single product casedeclining AC are sufficient, but not necessary for the cost function to be subadditive.

Unfortunately, though, the single product world bears little resemblance to the powersector. Power generation essentially is multiproduct. Outputs may differ in terms of reliability,generation technology, time of use, etc. Single product reasoning therefore blurs a variety of

features that distinguish the properties of multiproduct cost functions. The subsequent section showshow familiar concepts that readily apply to single product cost schedules can be extended to capturethe behavior of costs in a multiproduct industry. For a more thorough treatment of multiproduct costschedules the interested reader is referred to Baumol et.al. (1988), Chapter 4.

2.3 The Multiproduct Case

In what follows the focus is on a multiproduct firm (utility) that produces a vector ofn outputs, denoted by X = (XI, X2, ... , X.). Consequently, there no longer exists a scalar unit ofmeasurement in terms of which outputs can be expressed. However, what one can do is to fix outputproportions and let the size of a given output bundle, the "standard commodity", vary along a rayBX from the origin. This leads to the concept of ray average costs (RAC) which is the multiproductcounterpart of the single product average cost function.

Clearly, ray average costs C(BX)/B increase (decrease) as

(2.4) )[C(13X)/81l/B = [1B Xi MC, - C(BX)j/B2l,0,

where MC; = C/ IXY.

Accordingly, for a given output bundle X, with X = BX, the degree of multiproduct scale economiescan be defined as

C(X(2.5) SN (X) X 1, N = {1, 2, ... , n).

EX; MCj

Multiplying (2.4) by B/C(BX) and solving for SN yields

(2.5') SN (X) 1[+' eW 1 as e$O,

where e denotes the elasticity of RAC with respect to B, evaluated at X = BX. Thus, there areincreasing (decreasing) returns to scale at output X as the elasticity of RAC is negative (positive).

While RAC measure proportional changes in a set of outputs, they do not cope withchanges in the composition of the vector X. Changes in the output mix, however, can be addressedwith the concept of incremental costs (IC). The incremental costs of the i-th output measure thedifference between the total costs of producing the bundle X and the costs that would be incurredif the i-th output were deleted:

(2.6) ICj(X) m C(X) - C(XN.),

where XN.j is equal to the vector X, with a zero component in place of X,.

- 8 -

Likewise, the incremental costs of any subset of N, say T, are:

(2.6') ICT(X = C(X) - C(XN.T)

Also, average incremental costs (AIC) of output X; can be defined as

(2.7) AIC,(X) =: ICj/X;

Furthermore, the AIC of the i-th output are strictly decreasing (DAIC) up to Xi if

(2.8) IC; (X) < [ICi (BX)]/B, 0< 1 < 1.

By definition, under DAIC the right-hand side of (2.8) is a decreasing function of B on 0 < B <1. Thus

Y., MCi - ICj < O,

which means that in the presence of declining average incremental costs. marginal costs will fallshort of incremental costs.

Since product-specific returns to scale are defined as the ratio of average incremental costs tomarginal costs, i.e.

(2.9) Si (X) = AIC1/MC;C.1,

it can also be concluded that declining average incremental costs are equivalent to increasing product-specific returns to scale.

With the help of (2.9) and (2.7), definition (2.5) can be rewritten as

(2.5") SN = E aiS/t[[E ICJ/C(X)} 81

where the weights c; denote the ratios of Xi MC; to E X; MC;

Equation (2.5") states that the degree of multiproduct scale economies is equal to

the weighted average of product-specific economies of scale, divided by

the ratio of total incremental costs to total costs.

The denominator of (2.5") can be viewed as an indicator of the economies of joint productiondisplayed by a multiproduct technology. In fact, if the denominator were equal to unity, the costsof producing the output bundle X wouid amount to the sum of the stand alone costs of itscomponents. In this event, there would be no gains from producing the outputs XY, i = 1, 2, ....n, jointly, regardless of whether or not there are product specific returns to scale. Thus, theincremental costs must fall short of its stand-alone costs in order to justify joint production in terms

- 9 -

of cost savings. Otherwise, a multiproduct firm could be broken down into several specialized firmswithout any increase in costs.

Indeed, the rationale underlying the cost savings resulting from the simultaneousproduction of several (different) outputs can be captured with the concept of economies of scope.Strong economies of scope are said to exist with respect to a product set N = {1, 2, ... , n} if thecondition

(2.10) C(X) < E C(X)

is fulfilled. Hence, the degree of economies of scope at X relative to output Xi can be defined as

CM() - ICi(X)(2.11) SC; - __ 0.

C(X)

According to (2.11), the degree of economies of scope with respect to output X; is a measure of therelative increase in costs that would result from producing this output separately. (Note that wedisregard the case of a negative increase in costs).

Clearly, if all outputs have positive incremental costs, we obtain

SC,(X) < 1,

and

E ICi/C = 1-SCi.

lherefore, Equation (2.5") can be rewritten as

(2.5"') SN = [ E cvi SJ/[1-SC;J.

Equation (2.5"') reveals that economies of scope, i.e. the cost savings from joint production amplifythe impact which product-specific returns to scale have on the overall scale economies. In particular,economies of scope may generate overall scale economies even if the product-specific returns to scaleare non-increasing.

Basically, economies of scope are a result of cost complementarities and/or subadditiveftxed costs. A cost function that is twice differentiable exhibits (weak) cost complementarities overa given set of joint products if the increased production of one output does not raise the marginalcosts of the other outputs, but lowers the marginal costs of the other outputs over some output range.Formally this condition can be stated as

(2.12) tC/ baXa, % 0, i*+ j.

- 10 -

If the differentiability assumption does not hold, cost complementarity requires that the cost functionsatisfies the condition (Sharkey, 1981)

(2.12') C(X + XT + XR) - C(X + XT) < C(X + XR) - C(X)

for all outputs X, XT, and XR (where S, T, and R are disjoint subsets of N). Condition (2.12')means that the incremental costs of any subset of outputs (say, XR) do not increase with the numberof outputs to which the subset is added.

If all outputs are produced under cost complementarities the multiproduct cost functionis subadditive. Subadditivity in the multiproduct context requires that

(2.13) C( EX) < E C(X;)

for any set of vectors X', X2, ... , XI. For instance, if a two-product cost function C(X) is strictlysubadditive at output bundle X = (2,2), we must have

(i) C(2,2) < C(1,1) + C(1,1)

(ii) C(2,2) < C(2,1) + C(0,1)

(iii) C(2,2) < C(1,2) + C(1,0)

(iv) C(2,2) < C(2,0) + C(0,2)

Note that the last inequality (iv) states that there must be economies of scope. In fact,cost complementarities imply subadditivity, and subadditive costs imply the presence of economiesof scope. However, as the above example indicates, subadditivity is not necessary for economiesof scope to exist. Stated differently, a cost function that fails to be subadditive (and, consequently,does not exhibit cost complementarities) may nonetheless exhibit economies of scope.

When there are no cost complementarities, subadditive fixed costs will be necessaryfor economies of scope to prevail. Moreover, if the savings in fixed costs rendered feasible by jointproduction prove sufficiently large, economies of scope may occur even in the presence of (local)cost anticomplementarities. On the other hand, when there are no fixed costs, the absence of (weak)cost complementarities and anticomplementarities is both necessary and sufficient for the absence ofeconomies of scope (Gorman, 1985).

The pivotal role that economies of scope play in the multiproduct context is obvious:When there are cost savings from joint production, the efficient, cost-minimizing industry structurecannot be established on the basis of specialized, single-product firms. Stated differently, with(strict) economies of scope, the efficient industry structure requires, at the minimum, the presenceof some multiproduct firms. Consider, for instance, an industry in which n different outputs can beproduced by n+ 1 firm types; one diversified firm that produces all outputs jointly, and n specializedfirms that produce a particular output each. If there are economies of scope, then in an equilibriumthere will be at most n firm types supplying the market of which one must be the diversified firm

- II -

type (for a more detailed discussion see Baumol et.al. 1988, and Eaton and Lemche, 1991). Clearly,the limiting case is that of a single multiproduct monopoly which qualifies as the most efficientindustry structure if the industry's cost function proves to be subadditive.

In the same vein, with economies of scope, the impact of scale economies on coststends to be less crucial than in a single-product world: Product-specific scale economies are neithernecessary nor sufficient for economies of scope to exist. And while economies of scope arenecessary for subadditivity (and cost complementarities), subadditivity does not imply scaleeconomies, nor are scale economies sufficient for the cost function to be subadditive.

As an illustration consider first the cost function

(2.14) C(X1, X2) = XI + X2 + (XIX2 )"3.

By applying Equation (5), we obtain

SN = (XI + X2 + (XIX2)"3)/(XI + X2 + (2/3) (XIX2)1"3) > 1,

i.e. there are overall economies of scale (and, thus, decreasing RAC). In addition, the product-specific returns to scale are increasing for both outputs, as can be easily verified by applyingEquation (9). However, the cost function exhibits diseconomies of scope and, thus, fails to besubadditive. For instance, if X = (1,1), we have

C(1,1) = 3 > C(1,0) + C(O,1) = 2,

i.e. the costs of producing the two outputs separately are less than the costs of producing theproducts in combination.

On the other hand, consider a long-run (single-product) cost function of the type

(2.15) C(X) = , X + cX

where 6 denotes the constant (annuitized) unit capacity costs and c stands for the constant unitoperating costs (defined per unit of time, say, per month). Clearly, the above function exhibitsconstant returns to scale. Now, let X,, X2, and X3, with X, 2 X2 > X3, denote peak load,intermediate load and base load demand, and assume that the capacity can be adjusted to any levelof demand (e.g. investments in capacity are perfectly divisible). Moreover, let the load durationcycles be identically equal to one year (a more comprehensive discussion of this case is given inSection 3.2.1). Clearly, under these circumstances, a single firm that meets aggregate demand attotal costs

(2.16) C(XI, X2, X3) = (i XI + C[XI + X2 + X31

is placed at an advantage over three firms that provide the different loads separately with stand-alonecosts adding up to

- 12 -

C(XI) + C(X2) + C(X3 ) = [W + cl [XI + X2 + X3].

In other words, joint production of XI, X2 and X3 involves economies of scope at any load profilethat satisfies XI > X2 > X3 . Furthermore, as can easily be verified, the incremental costs of anysubset of outputs meet condition (2.12') without violating the weak inequality. In particular, theincremental costs of producing output 2 jointly with output 3 exceed the incremental costs ofproducing output 2 in combination with the outputs 3 and 1; i.e., we have

BX2 + cIX2+X3] - [c+B]X3 > BXI+c[XI+X2+X3 ] - BXI-c[X1+X3 ]

since B[X2-X3] > 0. Therefore, the case under consideration is one of joint production that exhibitsconstant returns to scale, yet enjoys cost complementarities.

In light of the above arguments it can be concluded that agonizing over the presenceor absence of scale economies may be entirely beside the point if the matter in dispute is the efficientstructure and regulatory outfit of a multiproduct industry that is blessed with economies of scope,let alone subadditive costs. At least, policy conclusions read into the (alleged) obsolence of scaleeconomies are prone to error in a multiproduct context.

A question that remains to be addressed is whether there are more general costcharacteristics from which subadditivity can be inferred. Unfortunately, analytically simpleconditions for subadditivity tend to be much stronger than necessary, while less rigid conditions aremore complex and difficult to interpret. To get an idea about the problems involved in detectingsubadditivity it suffices to mention that overall economies of scale in tandem wieh economies of scopedo not ensure that costs are subadditive (Baumol et.al., 1988, p. 173).

Among the conditions for subadditivity that are weaker than the assumption of costcomplementarities, two are of special interest (for details, see Baumol et.al., 1988):

- The multiproduct cost function C(X) will be subadditive if there are economies ofscope at X and if the AIC of each output decline up to X.

i [.y cost function that contains fixed costs and is linear in variable outputs will besubadditive if and only if the fixed costs are subadditive.

In summary, it has been argued that in the multiproduct context costwmplementarities, subadditivity and economies of scope are likely to prove pervasive features thatelude single-product reasoning. Moreover, these cost properties not only have an influence on theefficient industry structure, but also affect the way in which different pricing policies contribute tothe fulfillment of sector objectives such as financial viability, productive efficiency or the consumers'well being. In the subsequent chapters, these issues will be addressed in greater detail.

2.4 Cost Allocations

A legitimate approach to the problem of multiproduct pricing is to ask what are thespecific costs incurred by the different outputs under consideration. Another, closely related question

- 13 -

is what costs should be allocated to different outputs. Clearly, if each output could be held"responsible" for a distinct fraction of the costs, one might argue that the outputs should bearprecisely the costs they impose on the production program. From an accounting point of view,however, it may not be possible to fully attribute total costs to the outputs produced. And accoutingproblems aside, the reason why outputs should precisely bear the costs they incur is far fromobvious. Both issues will be addressed below.

Basically, cost apportioning turns out to be a problem when the cost function is non-separable. A case in point is the presence of common fixed costs. Unsurprisingly, the allocationof joint fixed costs has become a major concern of accountants and financial analysts. The problem,however, used to receive little attention among economists, for two reasons: Economists oftenmaintain that a -priori rules for cost apportioning are irrelevant. What matters is a system ofefficient prices. And once these prices have been determined, the allocation of costs becomes asecondary problem. The other argument is that rules for assigning non-separable costs are arbitrary.At least, it is a widespread belief that no economically convincing case can be made for ai yparticular cost allocation scheme.

The claim that the objective of efficient pricing should not be confused with the taskof allocating costs is in fact valid. However, a system of efficient prices may fail to share totalcosts. In this event the problem of cost accounting reappears in the form of the question of how toallocate losses. Moreover, if first-best pricing policies do not prove feasible, cost allocation rulesmay contribute to second-best solutions. At the minimum, concerns about the allocation of costs maybe a useful starting point for second-best pricing policies. Therefore, alluding to the ideal ofefficiency pricing does not necessarily remove the need to cope with the mercenary problem ofapportioning costs.

Nonetheless, the argument that there is no compelling economic reason to resort toa particular rule for assigning joint costs at first glance appears to be plausible, especially when thesecosts are fixed. Indeed, there are a number of rules for fully distributing costs (FDC) of which noneseems to be particularly desirable on economic grounds. Consider, for instance, the cost function

(2.17) C(X) = E Vi(X;) + F,

where Vi(Xj) stands for the variable costs associated with the i-th output and F denotes the common(fixed) costs. The problem with (2.17) is that, while the variable costs can be directly attributed tothe different outputs, there are various ways of apportioning fixed costs across outputs. Let C, bethe costs borne by the i-th *,utput, and let f, denote the share of common costs assigned to output isuch that

f. = 1.

Then any allocation of fixed costs satisfying the condition

(2.18) E C; = E V1 + E f,F = C(X)

- 14 -

will recover total costs. For instance, if the common fixed costs are allocated in proportion to therelative outputs, we have

(2.19) f; = X,/:X, i = 1, 2, ..., n.

Alternatively, one can assign the fixed costs in proportion the relative variable costs, i.e.

(2.20) f = V1 / s V1, i = 1, ,...,n.

Or one may charge a single output with total common costs. So it seems that if only the coststructure and the vtctor of outputs are known, there is no economic-illy convincing precept forchoosing among different procedures for allocating non-separable costs.

Nevertheless, the view (still widely held) that the so-called FDC rules are essentiallyarbitrary can be questioned. The challenge comes from a new branch of economic reasoning thatcan be lumped under the notion of ax.omatic pricing. The salient feature of the axiomatic pricingapproach is that it defines a set of "desiderata" cost allocation procedures should satisfy in order tobecome acceptable. The approach a!so shows that relative to the properties which are deemeddesirable for cost allocation schemes (or prices that replicate the cost allocation) and are laid out inthe form of axioms, there exists only a single procedure that is compatible with the predeterminedaxiomatic framework. In this context, a cost allocation procedure is a function which, on a per unitbasis, assigns to each outupt a share of costs. The properties which the allocation procedure isrequired to meet are usually specified in terms of the following five axioms:

(a) Cost Recovery Axiom: Outputs should share total costs.

This requirement is certainly desirable from the producer's point of view since itensures that the operations are financially viable. However, it rules out prices basedon marginal costs if MC fall short of AC or do not sum to total costs.

(b) Rescalin2 Axiom: The relative shares in costs should be independent of the units interms of which outputs are measured.

This property is intuitively plausible. It means, for instance, that the question ofwhether electricity is measu,red kWhs or MWhs should not affect the way in whichcosts are apportioned between peak load and base load.

(c) Consister. y Axiom: Outputs that play the same role in the cost function should sharethe same portion of costs.

Clearly, this axiom is desirable from a cost accounting point of view. It implies, forinstance, that time-of-day considerations should not guide the allocation of capacitycosts if unit capacity costs do not vary over time. However, one may object that inrestricting the focus to cost characteristics, the axiom pushes out potentially decisivefactors such as consumer preferences.

- 15 -

(d) Positiv!V Axigm: If increasing the production of an output results in higher costs,the share of costs assigned to this output should not be reduced.

There seems nothing wrong with this axiom. The following, apparently innocent,requirement pays special attention to the way in which accounts may typify costs:

(e) Additivity Axiom: If total costs can be decomposed into different categories, thiscategorization should not affect the allocation of costs across outputs.

New, if the cost function, is continuously differentiable and contains no fixed costs,it can be shown (Mirman and Tauman, 1982; Billera and Heath, 1982) that the only cost allocationprocedure which obeys the five axioms (a)-(e) is the Aumann-Shapley (AS) price mechanism definedas

IC(2.21) ASi(C,X) f I dax, i = 1, 2, ... , n, C = C(aX).

oJ X

The above result is equivalent to the Aumann-Shapley value for non-atomic gamnes (Aumann anciShapley, 1974). It states that the per-unit costs assigned to each output should be equal to theaverage of the output's marginal costs along the ray X. Obviously, in the special and easilytractable case of a separable cost function, the Aumann-Shapley procedure boils down to average costpricing; for separability implies

C(X) = CI(X,) + C2(X2) + ... + C (Xn)

so that dC,'!do = [aCi/aXjX;, i = 1, 2, ... , n.

Consequenitly,

XC dCi C(XASN= l - da = Xi' f1 da = _

oJ Yx. oJ doa Xi

Moreover, if there are constant returns to scale, marginal costs do not change along the ray aX.Thius

AS; = aC/bX1,

i.e., under constant returns to scale, the Aumann-Shapley mechanism is equivalent to marginal costpricing. B'it in general, MC-pricing which is compatible with the axioms (b)-(e) cannot be expectedto meet the cost recovery postulate (axiom (a)).

It is worth highlighting the significance of the above findings: For a large class ofcost functions, average cost pricing (in the presence of separable costs) or, as the case may be,

- 16-

marginal cost pricing (under constant returns to scale) can be justified in terms of cost-relatedallocative properties specified by the axioms (a)-(e). In other words, the axiomatic pricing approachdemonstrates that the allocation of costs among the outputs of a multiproduct firm may not bearbitrary; rather it will have to follow a well-defined procedure if the way in which costs are imputedis subjected to a set of fairly weak, yet plausible/acceptable "desiderata".

To illustrate how the Aumann-Shapley mechanism works in the case of non-separablecosts, conside- the function

E(X) = XI + X2 + (XI + X2)'8

Total costs can be broken down into components that are linear in each output, and a jointcomponent that reflects the common use of a facility.

Obviously,

lAS,X; = [1+(X1+X2 )-2'3 1X1 + ll+(X1+X2)-2'3]X2 = E(X).

Marginal cost pricing, on the other hand, will entail losses since

IEs:_ Xi = X,+X 2 +(1/3) (X,+X2)1/3 < E(X).

i )Xi

Clearly, cost recovery by allocating total costs in direct proportion to product-specificMC will be feasible. It can be accomplished through a mark-up over MC such that the costs per unitof output amount to

MC; [C(X))/ E MCj Xj].

The above cost allocation formula is referred to as "proportionally adjusted MC-pricing". However, the problem with proportionally adjusted MC-pricing is that it may not beincentive compatible. (Note that the argument applies to ; cost allocation rule that deviates fromthe Aumann-Shapley mechanism). Incentive compatibility means that decentralized decisions whichreduce (increase) the utility's total costs should be rewarded (penalized). Stated differently, if aparticular output is produced in a more cost efficient way - as measured by the MC of producing thisoutput -, the unit costs charged to the output should not increase.

For instance, let there be a cost-saving measure that changes the cost function E(X)used in the above example to

D(X) = XI + X2 + (O.5XI + X2)113.

Clearly, under D(X) total costs are lower than with E(X), and the savings areattributable to output XI. As can easily be verified, the AS-mechanism will impute lower unit coststo output XI. Assume that XI = X2 = 1.

- 17 -

Then

ASI(E,X) 1 1.630,

while

AS, (D,X) X 1.382.

On the other hand, marginal costs work out at

16E/AXI X 1.210 and aD1/ X1 X 1.382.

Consequently, proportionally adjusted MC pricing vill penalize output XI.

The above finding has important practical implications. If the multiproduct utilityrelies on decentralized decision making and for that reason fully distributes costs on the basis of unitcharges, then the Aumann-Shapley cost allocation procedure "is the only method that attaches nopenalty to diligence, and no reward to negligence" (Young, 1985, p. 764).

It is also worth noting that in the special case where the cost function is homogeneousof degree r>0 and thus

MC;(caX) = a"r MC;(X)

holds, we have

dC(X)(2.22) AS; = 1_ f1 arl da = [1/r] MCi.

ax oJ

Consequently,

(2 22') AS/MC; = 1/rjl1 for r i 1.

Equation (2.22'), which applies to homogenous cost functions only, is the multiproduct extension offormula (2.1) which - unlike formula (2.9) - defines scale economies in terms of the ratio of AC toMC.

However, a major shortcoming of the Aumann-Shapley solution is that it cannot bereadily applied to cost functions that include fixed costs. To show this, consider the cost function(2.17). Allocating the non-attributable fixed costs to a single output (or a subset of outputs) wouldviolate the consistency axiom. Setting the unit cost equal to marginal costs is compatible with theconsistency axiom, but contradicts the principle of cost recovery. Similar problems arise if oneapplies conventional FDC-rules. For instance, if the fixed costs are assigned in proportion to the

- 18 -

relative outputs (Equation 2.19), this runs counter to the consistency postulate. Thus, apportioningfixed costs requires the axioms (a)-(e) to be modified in some way.

Thus, altering or abandoning some of the axioms means that one has to trade-off thedesirability of allocative properties against the desirability of strict, cost-based allocation procedures.For instance, if the consistency axiom is given up, this opens the door for a variety of allocationsthat no longer depend on costs and outputs alone. In particular, characteristics of the demandfunction or socioeconomic considerations may become a decisive factor. So if one prefers the focusbe restricted to cost-based allocation procedures, the consistency axiom must be retained. On theother hand, the decision to weaken the cost recovery axiom would drastically change the axiomaticsetting by rendering losses at the firm level feasible. At least, cost recovery can be considered acrucial, if not essential requirement that should not be dismissed out of hand. Also, there is noreason to discard the rescaling and positivity axioms which are both weak and plausible. Therefore,it appears that the additivity axiom is the most appropriate candidate for a change. In fact, in orderto cope with fixed costs Mirman et.al. (1983) have proposed to replace the additivity postulate withthe following weaker version:

(f) Modified Additivity Axiom: If the cost function C(X) contains a fixed cost F and ifthe variable costs can be broken down into Vi(X), i = 1, ... , k, the fixed cost should be split amongthe variable cost components such that

C(X) = C(Vi+fiF) = V(X) + F, with V(X)= Vi,f. A

where f, denotes the relative share of the fixed cost that it added to Vj(X). Moreover, f; should beat least as large as fj, i*j, whenever V; is at least as large as Vi.

Mirman et.al. (1983) have shown that in the presence of fixed costs there exists aunique modified Aumann-Shapley (MAS) cost allocation procedures that satisfies the axioms (a), (b),(c), (d), and (f). The procedure is given by the formula

4aC(2.23) MAS; = [l+f(X)] f I da = [1 + f(X)] AS;,

oJ ax1

where f(X) = F/V(X) and C = C(coX).

Equation (2.23) states that the fixed costs should be allocated proportionally to the perunit variable costs that the AS-procedure assignes to the different outputs. Thus, the MAS-allocationof total costs is a scalar multiple of the AS-allocation imputed on the variable costs.

Clearly, if the variable costs are separable across outputs, the fixed cost should beallocated in direct proportion to the average variable costs. And if the latter are constant, the totalcosts to be borne by a unit of output will be a scalar multiple of the output's marginal costs.

Formula (2.23) completes the discussion of axiomatic cost allocation rules. Whatremains to be answered is whether there exist prices based on Aumann-Shapley cost allocations that

- 19 -

clear the market. Demand-compatible AS-allocations have a particularly appealing property: Theycan be derived without any knowledge about the individuals' demand curves. The only informationrequired for determining the equilibrium solution is the cost structure and aggregate demand.

Mirman and Tauman (1982) have shown for the no-fixed-cost case that in generalthere exist Aumann-Shapley prices relative to which supply is matched by demand. Withnonattributable fixed costs, the result also holds if variable costs are separable across outputs. Theexistence of demand-compatible AS prices notwithstanding, in ordinary practice it may prove difficultto strike such prices. But clearing the market is a problem that also applies to MC-pricing, let alonepricing formulas which rely on data about disaggregate demand.

In sum it can be stated that the axiomatic approach to allocating costs not only"solves" the problem of how to share costs, but also provides an alternative approach to calculatingcost-based prices. If pricing decisions are distorted because of politically motivated interference orshaky welfare reasoning so that a case can be made for greater reliance oni cost-based guidance inprice setting, the AS-procedure has something to tell.

3. Marginal Cost Pricing

Since Hotelling's (1938) seminal paper on the welfare implications of public utilityrates, much lip service has been paid to the principle of marginal cost pricing. But the praise ofmarginal cost pricing conveyed by the rhetoric of policy makers often goes hand in hand withtenuously derived arguments set forth to justify that in practical applications prices deviate frommarginal costs. Also, there is a continuing and sometimes confusing debate over the significanceof short-run and long-run marginal costs. Different views are being held with respect to theclassification of c0sts and, in particular, the treatment of capital costs. It has also been proposed toabandon measuring strict marginal costs and instead use marginal cost surrogates such as long-runincremental costs. And apart from the skepticism fueled by a number of practical difficulties withMC-pricing, general equilibrium second-best reasoning has been advanced to downplay theimportance of marginal optimality conditions.

In short, despite its prominence as a policy device, there is also an element of mysteryand scholasticism associated with the principle of marginal cost pricing. The subsequent sections aretherefore intended to outline the conceptual background of marginal cost pricing and to shed somelight on major issues that have become a matter of controversy. Starting with the single-productcase, Section 3.1.1 highlights the rationale underlying the marginal cost approach within a static,partial equilibrium setting. Section 3.1.2 extends the analysis to a dynamic context. While Section3.1.3 re-assesses the marginal cost principle from a general equilibriun point of view, practicalapproaches to measuring marginal costs are discussed in Section 3.1.4. Sections 3.2.1-3.2.3 dealwith problems of multiproduct marginal cost pricing. The analysis centers on the concept of peakload or time of use pricing (Sections 3.2.1 - 3.2.2), avoided cost pricing (Section 3.2.2), and itsmodification in the presence of loss-of-load probability (LOLP) design targets(Section 3.2.4). Anoutline of real time pricing is given in Section 3.2.5.

- 20 -

3.1 The Single Product Case

3.1.1 SRMC versus LRMC in a Static Setting

The rationale underlying marginal cost pricing is the maximization of social welfare.The reason why pricing at marginal costs maximizes social welfare is frequently set forth under anumber of simplifying assumptions. First, it has become common to argue in favor of MC-pricingfrom the perspective of a partial equilibrium framework, assuming that the rest of the economy hasalready adjusted to marginal cost prices. So the focus is on a single market with a single good(electricity). Second, welfare is measured in terms of the consumers' and producers' surplus.Third, the consumer surplus is equivalent to the area under the individuals' uncompensated(Marshallian) demand curve. In fact, as has been demonstrated by Willig (1976), this measure is"usually a very good approximation" to the consumers' welfare. Fourth, the producers' surplus isrepresented by the industry's profits. Fifth, for any output, profits are measured by the area to theleft of the industry's (increasing) marginal cost curve. This requires that there are no fixed costs andthat the industry's output is supplied along the marginal cost curve.

Given these assumptions, welfare, i.e. the sum of the consumers' and producers'surplus is maximized at a price that (i) equals marginal costs and (ii) clears the market. Figure 3.1illustrates the result. Obviously at MC = PI the aggregate surplus of the consumers (area ACB) andproducers (area BCD) is highest. On the other hand, if, for instance, the price were equal to P2 ($MC), there would be a deadweight loss equivalent to the area ECF.

Figure 3.1: Demand and Supply Equilibrium Under MC-Pricing

Price

A

Marg. Revenues

P2 1c

PI- Demand

0 X1 Output0 ~~~~xl

Several remarks are in order:

First, the reasoning behind Figure 3.1 is purely static, i.e. the focus is restricted to a single pointin time. Second, no distinction is made between long-run and short-run costs. Third, for pricing

- 21 -

at marginal costs to be welfare-optimal it has to clear the market. Fourth, marginal cost pricing doesnot maximize the consumers' surplus; nor does it enable the industry to maximize profits. Asregards the latter point, it is worth recalling that in a profit maximum marginal costs would be equalto marginal revenues. In Figure 3.1 such a configuration corresponds to price P2, and, thus involvesa welfare loss (area ECF). Fifth, both the market clearing condition and the concern for theconsumers' well-being require MC-pricing to explicitly take account of the demand side. In fact,as will be shown below, there may be conditions under which the entire demand curve needs to beknown in order to make a case for MC-pricing.

A simple example may help to illustrate some of the points raised in the lastparagraph. Consider the (single-product) short-run cost function

(3.1) C(X) = F + cX

where c denotes the (constant) unit operating costs which are equal to marginal costs, and F standsfor fixed capacity costs. Moreover, suppose that demand is given by the linear (inverse) demandfunction

(3.2) p = a - bX

where p denotes the unit price and a, b are parameters.

Now, at any output X, total welfare, i.e. the sum of the (net) consumers' and producers' surplus(total surplus = TS), is determined by

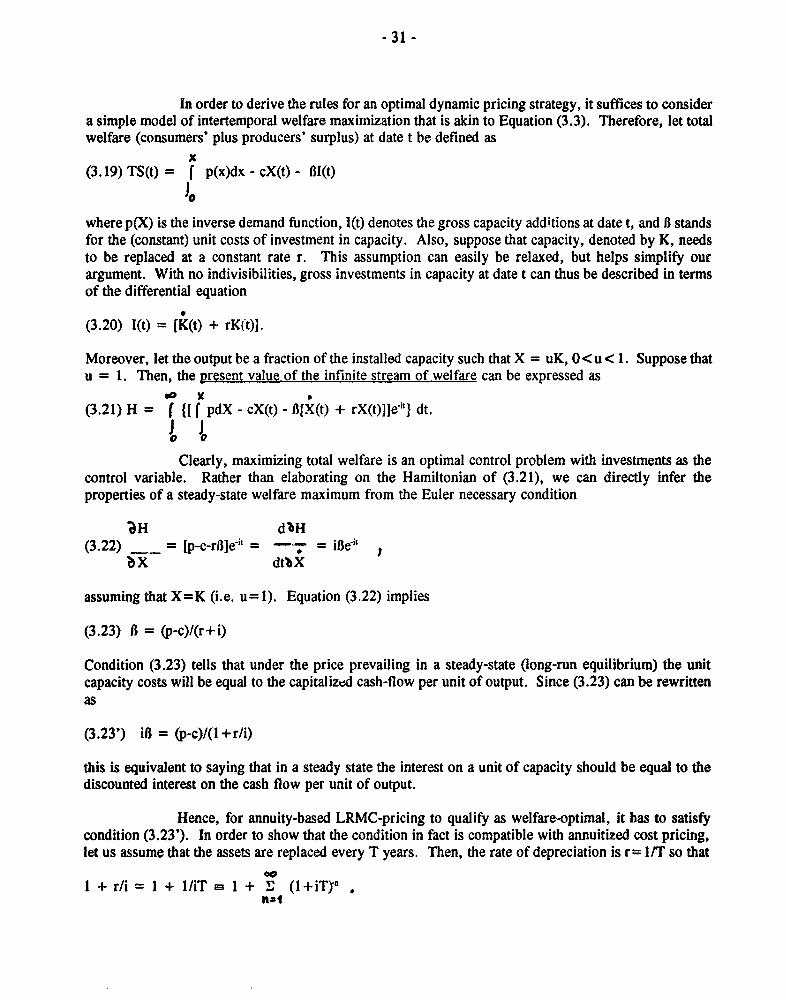

(3.3) TS = p(X)dx - px + px -C(X)

which, in view of (3.1) and (3.2), yields

(3.4) TS = aX - bX2/2 - cX - F.

While it is often taken for granted that the total surplus is positive, our example showsthat this may not be the case. Indeed, as can easily be verified, the quadratic equation (3.4) has twosolutions for X (i.e. two real roots) provided the condition

(3.5) (a-c)2 > F2b