Embed Size (px)

Citation preview

EKO FAKTORİNG A.Ş.

FINANCIAL STATEMENTSAT 31 DECEMBER 2013 TOGETHER WITHINDEPENDENT AUDITOR’S REPORT

EKO FAKTORİNG A.Ş.

FINANCIAL STATEMENTS AT 31 DECEMBER 2013

CONTENTS PAGES

BALANCE SHEET (STATEMENT OF FINANCIAL POSITION)........................................ 1

STATEMENT OF COMPREHENSIVE INCOME................................................................... 2

STATEMENT OF CHANGES IN EQUITY .............................................................................. 3

STATEMENT OF CASH FLOWS.............................................................................................. 4

NOTES TO THE FINANCIAL STATEMENTS ....................................................................... 5-36

NOTE 1 ORGANISATION AND NATURE OF OPERATIONS…….................................................... 5NOTE 2 BASIS OF PRESENTATION OF FINANCIAL STATEMENTS............................................. 5-17NOTE 3 CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS ........................................... 17-18NOTE 4 FINANCIAL RISK MANAGEMENT....................................................................................... 18-23NOTE 5 CASH AND CASH EQUIVALENTS ....................................................................................... 23NOTE 6 FACTORING RECEIVABLES, NET........................................................................................ 23-25NOTE 7 ASSET HELD FOR SALE......................................................................................................... 25-26NOTE 8 BORROWINGS ......................................................................................................................... 26NOTE 9 FINANCIAL LEASE PAYABLES............................................................................................ 27NOTE 10 ISSUED DEBT SECURITIES ................................................................................................... 27NOTE 11 OTHER ASSETS AND PREPAID EXPENSES........................................................................ 27NOTE 12 PROPERTY AND EQUIPMENT .............................................................................................. 28-29NOTE 13 INTANGIBLE ASSETS............................................................................................................. 29NOTE 14 TAXES ON INCOME................................................................................................................ 30-31NOTE 15 EMPLOYMENT BENEFIT OBLIGATIONS............................................................................ 32NOTE 16 OTHER LIABILITIES AND ACCRUED EXPENSES............................................................. 33NOTE 17 SHARE CAPITAL .................................................................................................................... 33-34NOTE 18 RETAINED EARNINGS AND LEGAL RESERVES .............................................................. 34NOTE 19 OTHER OPERATING INCOME/(EXPENSES), NET.............................................................. 34NOTE 20 OPERATING EXPENSES......................................................................................................... 35NOTE 21 FACTORING REVENUES........................................................................................................ 35NOTE 22 FOREIGN EXCHANGE GAINS/(LOSSES), NET ................................................................... 35NOTE 23 TRANSACTIONS AND BALANCES WITH RELATED PARTIES ...................................... 36NOTE 24 COMMITMENTS AND CONTINGENT LIABILITIES ......................................................... 36NOTE 25 SUBSEQUENT EVENTS ......................................................................................................... 36

EKO FAKTORİNG A.Ş.

BALANCE SHEET (STATEMENT OF FINANCIAL POSITION)AT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish lira (“TL”) unless otherwise indicated.)

1

Notes 2013 2012

ASSETS

Cash and cash equivalents 5 14,972 19,363Factoring receivables, net 6 371,550 296,639Assets held for sale 7 116 116Other assets and prepaid expenses 11 1,957 1,246Property and equipment, net 12 3,152 7,829Intangible assets, net 13 245 135Deferred tax asset, net 14 6,427 5,598

Total assets 398,419 330,926

LIABILITIES AND EQUITY

Bank borrowings 8 203,639 193,306Lease payables, net 9 165 226Issued debt securities 10 101,697 50,466Factoring payables 517 520Current income taxes payable, net 14 690 663Other liabilities and accrued expenses 16 1,447 1,035Employment benefit obligations 15 578 824

Total liabilities 308,733 247,040

EQUITY

Share capital 17 55,000 21,026Adjustment to share capital 17 424 424

Total paid-in share capital 17 55,442 21,450Share premiums - 16,410Revaluation fund - 1,337Remeasurements of employee

termination benefits, net of tax 18 -Retained earnings 34,244 44,689

Total equity 89,686 83,886

Total liabilities and equity 398,419 330,926

The accompanying notes set out on pages 5 to 36 form an integral part of these financial statements.

EKO FAKTORİNG A.Ş.

STATEMENT OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

2

Notes 2013 2012

Factoring interest income 21 63,686 67,149Factoring commissions 21 7,927 7,335

Income from factoring operations 71,613 74,484

Interest expenses (25,780) (28,271)Foreign exchange gains and losses, net 22 70 (132)Impairment loss on factoring receivables 6 (13,129) (7,771)Recoveries from impaired factoring receivables 6 478 1,050

Income after foreign exchange gains and losses, netand provision for impaired factoring receivables 33,252 39,360

Interest income other than factoring 186 33Other income/(expense), net 19 5,082 (315)

Operating profit 38,520 39,078

Operating expenses 20 (25,674) (18,201)

Income before taxes from operations 12,846 20,877

Taxation on income- Current year tax expense 14 (3,563) (4,976)- Deferred tax income 14 835 710

Net profit for the year 10,118 16,611

Remeasurements of employeetermination benefits, net of tax 23 -

Revaluation differences of tangible assets 12 - 716Deferred tax effect 14 (5) (80)

Total comprehensive income for the year 10,136 17,247

The accompanying notes set out on pages 5 to 36 form an integral part of these financial statements

EKO FAKTORİNG A.Ş.

STATEMENT OF CHANGES IN EQUITYAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

3

Adjustment ActuarialShare to share Share gain / (losses), Revaluation Retained Total

capital capital premium net of tax fund earnings equity

1 January 2012 21,026 424 16,410 - 701 30,368 68,929

Capital increase from internal resource - - - - - - -Dividend paid - - - - - (2,290) (2,290)Revaluation fund - - - - 636 - 636Net profit for the year - - - - - 16,611 16,611

31 December 2012 21,026 424 16,410 - 1,337 44,689 83,886

1 January 2013 21,026 424 16,410 - 1,337 44,689 83,886

Capital increase from internal resource 33,974 - (16,410) - - (17,564) -Dividend paid - - - - - (2,999) (2,999)Revaluation fund - - - - (1,337) - (1,337)Net profit for the year - - - - - 10,118 10,118Other comprehensive income - - - 18 - - 18

31 December 2013 55,000 424 - 18 - 34,244 89,686

The accompanying notes set out on pages 5 to 36 form an integral part of these financial statements.

EKO FAKTORİNG A.Ş.

STATEMENT OF CASH FLOWSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

4

Notes 2013 2012

Cash flows from operating activities

Net profit for the year 10,118 16,611

Adjustments to reconcile net income for the year to netcash provided from operating activities:

Depreciation of property and equipment 12 818 437Amortization of intangible assets 13 96 30Reserve for employment benefit obligations 15 213 455Provision for impaired factoring receivables 6 13,129 7,771Interest income, net (38,092) (38,909)Interest paid (22,303) (26,338)Interest received 63,872 67,180Current year taxation expense 14 2,728 4,266Other - 72

Cash flows from operating profit beforechanges in operating assets and liabilities 30,579 31,576

Net decrease/ (increase) in restricted cash 5 - 50Net increase in factoring receivables (91,439) (64,340)Net increase/ (decrease) in other assets and prepaid expenses (717) (984)Net decrease in asset held for sale - 36Net increase/ (decrease) in other liabilities and accrued expenses (1,335) 188Income taxes paid 14 (2,884) (4,729)Employment termination benefit paid 15 (36) (95)

Net cash used in operating activities (65,832) (38,298)

Cash flows from investing activities:Purchase of property, plant and equipment 12 (2,514) (1,343)Purchases of intangible assets-net of disposals 13 (206) (85)Proceeds from sale of property, plant and equipment 12,041 2

Net cash used in investing activities 9,321 (1,426)

Cash flows from financing activities:Proceeds/ (payments) of borrowings 6,856 5,039Issuance of debt securities 48,262 48,840Increase in finance lease payables (3) 226Dividends paid (2,999) (2,290)

Net cash provided from financing activities 52,116 51,815

Net increase in cash and cash equivalents (4,395) 12,091

Effect of foreign exchange rate changeson cash and cash equivalents - -

Cash and cash equivalents at beginning of the year 5 19,361 7,270

Cash and cash equivalents at end of the year 5 14,966 19,361

The accompanying notes set out on pages 5 to 36 form an integral part of these financial statements.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

5

NOTE 1 - ORGANISATION AND NATURE OF OPERATIONS

Eko Faktoring A.Ş. (“the Company”) was established in 1994. The Company provides domestic factoring services. The company has 114 employees at 31 December 2013 (2012: 99). The registeredoffice address of the Company is Eski Büyükdere Asfaltı, Ayazağa Yolu Cad., No: 9 Kat: 4 İz Plaza Giz Maslak, Istanbul/Turkey.

The financial statements as of and for the year ended 31 December 2013 have been approved for issueby the Board of Directors on 19 March 2014.

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS

The principal accounting policies adopted in the preparation of the financial statements at31 December 2013 are set out below. These policies have been consistently applied to the yearpresented, unless otherwise stated.

Accounting standards

The Company maintains its books of account and prepares its financial statements in Turkish Lira(“TL”) in accordance with the Communiqué on the Uniform Chart of Accounts, Disclosures and Formand Nature of Financial Statements to be Issued By Leasing, Factoring and Consumer FinanceCompanies (“Financial Statement’s Communiqué”) issued by the Banking Regulation and SupervisionAgency (“BRSA”) in Official Gazette No. 28861, dated 24 December 2013, and in accordance withTurkish Accounting Standards/Turkish Financial Reporting Standards (“TAS/TFRS”) and theiradditions and comments issued by the Turkish Accounting Standards Board (“TASB”) and with theCommuniqué: on Procedures Regarding Provisions to be Provided for Loans of Leasing, Factoringand Consumer Finance Companies (“Provisions Communiqué”) issued by the BRSA in OfficialGazette No. 28861, dated 24 December 2013.

These financial statements are derived from statutory financial statements with adjustments andreclassifications and the financial statements have been prepared in accordance with InternationalFinancial Reporting Standards (“IFRS”). IFRS comprise accounting standards issued by the InternationalAccounting Standards Board (“IASB”) and its predecessor body and interpretations issued by theInternational Financial Reporting Interpretations Committee (“IFRIC”) and its predecessor body.

The financial statements have been prepared on the historical cost basis except for, if applicable, certainfinancial instruments which are measured at fair value. Historical cost is generally based on the fair valueof the consideration given in exchange for assets.

The preparation of financial statements in conformity with IFRS requires the use of certain criticalaccounting estimates. It also requires management to exercise its judgment in the process of applyingthe Company’s accounting policies. The areas involving a higher degree of judgment or complexity, orareas where assumptions and estimates are significant to the financial statements are disclosed in therespective accounting policy disclosures. Although the estimations and assumptions are based on thebest estimates of the management’s existing incidents and operations, they may differ from the actualresults

Company’s going concern

The Company has prepared the financial statements according to the going concern assumption.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

6

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

Accounting for the effects of hyperinflation

Prior to 1 January 2006, International Accounting Standard 29 (“IAS29”), “Financial Reporting inHyperinflationary Economies”, requires that the financial statements prepared in the currency of ahyperinflationary economy be stated in terms of the purchasing power of this currency at balance sheetdate and restatement of the financial statements of the comparative periods within same terms. As thecharacteristics of the economic environment of Turkey indicate that hyperinflation has ceased,effective from 1 January 2006, the Company has no longer applied IAS 29. Accordingly, themeasuring unit current at 31 December 2005 is treated as the basis for the valuation of the amounts inthese financial statements.

Amendments in standards and interpretations

The Company adopted the standards, amendments and interpretations published by the InternationalAccounting Standards Board (“IASB”) and International Financial Reporting InterpretationCommittee (“IFRIC”) and which are mandatory for the accounting periods beginning on or after1 January 2013 which are related to the Company’s operations.

Standards, amendments and IFRICs applicable to 31 December 2013 year ends

- Amendment to IAS 1, ‘Financial statement presentation’, regarding other comprehensiveincome; is effective for annual periods beginning on or after 1 July 2012. The main changeresulting from these amendments is a requirement for entities to group items presented in ‘othercomprehensive income’ (OCI) on the basis of whether they are potentially reclassifiable toprofit or loss subsequently (reclassification adjustments). The amendments do not address whichitems are presented in OCI.

- Amendment to IAS 19, ‘Employee benefits’; is effective for annual periods beginning on orafter 1 January 2013. These amendments eliminate the corridor approach and calculate financecosts on a net funding basis.

- Amendment to IFRS 1, ‘First time adoption’, on government loans; ; is effective for annualperiods beginning on or after 1 January 2013. This amendment addresses how a first-timeadopter would account for a government loan with a below-market rate of interest whentransitioning to IFRS. It also adds an exception to the retrospective application of IFRS, whichprovides the same relief to first-time adopters granted to existing preparers of IFRS financialstatements when the requirement was incorporated into IAS 20 in 2008.

- Amendment to TFRS 7, ”Financial instruments: Disclosures” on asset and liability offsetting iseffective for annual periods beginning on or after 1 January 2013. This amendment includesnew disclosures to facilitate comparison between those entities that prepare TFRS financialstatements to those that prepare financial statements in accordance with US GAAP.

- Amendment to TFRS 10, 11 and 12 on transition guidance is effective for annual periodsbeginning on or after 1 January 2013. These amendments provide additional transition relief toTFRSs 10, 11 and 12, limiting the requirement to provide adjusted comparative information toonly the preceding comparative period. For disclosures related to unconsolidated structuredentities, the amendments will remove the requirement to present comparative information forperiods before TFRS 12 is first applied.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

7

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

- Annual Improvements 2011: It is effective for annual reporting periods beginning from 1January 2013 or after this period. These annual improvements include five titles in reportingperiod of 2009-2011. These amendments are:

• IFRS 1, “First-time Adoption of International Financial Reporting Standards”• IAS 1, “Presentation of Financial Statements”• IAS 16, “Tangible Assets”• IAS 32, “Financial instruments: Presentation”• IAS 34, “Interim Period Financial Reporting”

- IFRS 10, “Consolidated financial statements”, is effective for annual periods beginning on orafter 1 January 2013. The standard builds on existing principles by identifying the concept ofcontrol as the determining factor in whether an entity should be included within the consolidatedfinancial statements of the parent company. The standard provides additional guidance to assistin the determination of control where this is difficult to assess. This new standard might impactthe entities that a group consolidates as its subsidiaries.

- IFRS 11, ‘Joint arrangements’ is effective for annual periods beginning on or after 1 January2013. IFRS 11 is a more realistic reflection of joint arrangements by focusing on the rights andobligations of the arrangement rather than its legal form. There are two types of jointarrangement: joint operations and joint ventures. Joint operations arise where a joint operatorhas rights to the assets and obligations relating to the arrangement and therefore accounts for itsinterest in assets, liabilities, revenue and expenses. Joint ventures arise where the joint operatorhas rights to the net assets of the arrangement and therefore equity accounts for its interest.Proportional consolidation of joint ventures is no longer allowed.

- IFRS 12, “Disclosures of interests in other entities”, is effective for annual periods beginning onor after 1 January 2013. The standard includes the disclosure requirements for all forms ofinterests in other entities, including joint arrangements, associates, special purpose vehicles andother off balance sheet vehicles.

- IFRS 13, ‘Fair value measurement’; is effective for annual periods beginning on or after1 January 2013. IFRS 13 aims to improve consistency and reduce complexity by providing aprecise definition of fair value and a single source of fair value measurement and disclosurerequirements for use across IFRSs. The requirements, which are largely aligned between IFRSand US GAAP, do not extend the use of fair value accounting but provide guidance on how itshould be applied where its use is already required or permitted by other standards within IFRSsor US GAAP.

- IAS 27 (revised 2011), ‘Separate financial statements’; is effective for annual periodsbeginning on or after 1 January 2013. IAS 27 (revised 2011) includes the provisions on separatefinancial statements that are left after the control provisions of IAS 27 have been included in thenew IFRS 10.

- IAS 28 (revised 2011), ‘Associates and joint ventures’; is effective for annual periods beginningon or after 1 January 2013. IAS 28 (revised 2011) includes the requirements for joint ventures,as well as associates, to be equity accounted following the issue of IFRS 11.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

8

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

New IFRS standards, amendments and IFRICs effective after 1 January 2014

- Amendment to IAS 32, ”Financial instruments: Presentation on asset and liability offsetting” iseffective for annual periods beginning on or after 1 January 2014. These amendments are to theapplication guidance in IAS 32 ”Financial instruments: Presentation”, and the clarification ofsome of the requirements for offsetting financial assets and financial liabilities on the balancesheet.

- Amendments to “IFRS 10, 12 and IAS 27 on consolidation for investment entities” is effectivefor annual periods beginning on or after 1 January 2014. These amendments mean that manyfunds and similar entities will be exempt from consolidating most of their subsidiaries. Instead,they will measure them at fair value through profit or loss. The amendments give an exceptionto entities that meet an ”investment entity” definition and which display particularcharacteristics. Changes have also been made in IFRS 12 to introduce disclosures that aninvestment entity needs to make.

- Amendment to IAS 36, “Impairment of assets on recoverable amount disclosures” is effectivefor annual periods beginning on or after 1 January 2014. This amendment addresses thedisclosure of information about the recoverable amount of impaired assets if that amount isbased on fair value less costs of disposal.

- Amendment to IAS 39 ‘Financial Instruments: Recognition and Measurement’ - ‘Novation ofderivatives is effective for annual periods beginning on or after 1 January 2014. Thisamendment provides relief from discontinuing hedge accounting when novation of a hedginginstrument to a central counterparty meets specified criteria.

- IFRIC 21, “Levies” is effective for annual periods beginning on or after 1 January 2014. This isan interpretation of IAS 37 ”Provisions, contingent liabilities and contingent assets”. IAS 37sets out criteria for the recognition of a liability, one of which is the requirement for the entity tohave a present obligation as a result of a past event (known as an obligating event).The interpretation clarifies that the obligating event that gives rise to a liability to pay a levy isthe activity described in the relevant legislation that triggers the payment of the levy.

- IFRS 9 ”Financial instruments” - classification and measurement; is effective for annual periodsbeginning on or after 1 January 2015. This standard on classification and measurement offinancial assets and financial liabilities will replace IAS 39 ”Financial instruments: Recognitionand measurement”. IFRS 9 has two measurement categories: amortised cost and fair value.All equity instruments are measured at fair value. A debt instrument is measured at amortisedcost only if the entity is holding it to collect contractual cash flows and the cash flows representprincipal and interest. For liabilities, the standard retains most of the IAS 39 requirements.These include amortised-cost accounting for most financial liabilities, with bifurcation ofembedded derivatives. The main change is that, in cases where the fair value option is taken forfinancial liabilities, the part of a fair value change due to an entity’s own credit risk is recordedin other comprehensive income rather than the income statement, unless this creates anaccounting mismatch. This change will mainly affect financial institutions.

The main change is that, in cases where the fair value option is taken for financial liabilities, thepart of a fair value change due to an entity’s own credit risk is recorded in other comprehensiveincome rather than the income statement, unless this creates an accounting mismatch.This change will mainly affect financial institutions.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

9

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

New IFRS standards, amendments and IFRICs effective after 1 January 2014 (continued)

- Amendments to IFRS 9 ”Financial instruments regarding general hedge”. These amendments toTFRS 9 “Financial instruments” bring into effect a substantial overhaul of hedge accountingthat will allow entities to better reflect their risk management activities in the financialstatements.

- Amendment to IAS 19 regarding defined benefit plans; is effective for annual periods beginningon or after 1 July 2014. These narrow scope amendments apply to contributions from employeesor third parties to defined benefit plans. The objective of the amendments is to simplify theaccounting for contributions that are independent of the number of years of employee service,for example, employee contributions that are calculated according to a fixed percentage ofsalary.

- Annual Improvements 2012: It is effective for annual reporting periods beginning from 1 July2013 or after this period. This annual improvements include six titles in reporting period of2010-2012. These amendments are:

• IFRS 2, Share Based Payment• IFRS 3, Business Combinations• IFRS 8, Operating Segments• IAS 16, Tangible Fixed Assets and IAS 38, Intangible Fixed Assets• IFRS 9, Financial Instruments: IAS 37, Provisions, Contingent Assets and Liabilities• IAS 39, Financial Instruments - Recognition and Measurement”

- Annual Improvements 2013: It is effective for annual reporting periods beginning from 1 July2014 or after this period. This annual improvements include four titles in reporting period of2011-12-13. These amendments:

• IFRS 1, First time adoption, on government loans• IFRS 3 Joint arrangements,• IFRS 13, Fair value measurement• IAS 40, Investment Property Standards

Except IFRS 9, changes shown above does not have a serious impact on company’s financialcondition and performance.

Early adoption of standards

The Company did not early-adopt new or amended standards at 31 December 2013. Considering thefinancial statement items of the Company, it is deemed that the prospective changes would have nosignificant effect to over the financial position and performance of the Company.

Cash and cash equivalents

Cash and cash equivalents are initially recognised at cost in the balance sheet. Cash and cashequivalents consist of cash on hand, deposits at banks, defined amounts those are convertible to cashand highly liquid investments not significantly exposed to revaluation risk with maturities threemonths or less than three months (Note 5).

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

10

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

Related parties

In these financial statements, major shareholders of the Company, the organizations directly orindirectly financially related to the Company, key management personnel, board members of theCompany and their families, in each case together with, companies controlled by or affiliated withthem are considered and referred to as related parties (Note 23).

Financial instruments

Financial assets and liabilities are included in the balance sheet of the Company in case the Companyis a legal party to those financial instruments.

Financial assets

a. Effective interest rate method

Effective interest rate method is the validation of the financial asset through amortized cost and thedistribution of the related interest income to the related period. Effective interest ratio is the rate thatreduces the estimated cash total to be collected during the expected life of the financial instrument orwithin a shorter period of time, when applicable, to the current net value of the financial instrument.

The incomes related to the financial assets classified apart from the financial assets at fair valuethrough profit or loss, and available-for-sale equity instruments are calculated using the effectiveinterest method.

The financial assets other than the ones classified as financial assets at fair value through profit or lossand recorded on the fair value are recognized over the total amount of expenditures that can be directlylinked to the call transaction. The related assets are quoted or unquoted on the trading date dependingon the result of the trading of the financial assets based on a contract which stipulates that theinvestment instruments are delivered in line with the time set by the related market. The financialassets are classified into "financial assets at fair value through profit or loss” , "held-to-maturityinvestments", "available-for-sale financial assets" and loans and receivables". Classification is basedon the quality and purpose of the financial assets and determined during the first recognition.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

11

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

b. Financial assets at fair value through profit or loss

In the event that the Company acquires the financial assets primarily in order to sell them in the nearterm, the financial assets are a part of a financial instrument portfolio defined and managed by theCompany, and as in all the derivative products not designated as effective hedging instruments, theshort-term profits of the financial assets are realized, the stated financial assets are classified as thefinancial assets at fair value through profit or loss. Losses or profits arising from the fair valuevalidation of the financial assets at fair value through profit or loss are recognized in profit/loss. Netgains or losses recognized in profit or loss include the interest and/or dividend amount acquired fromthe stated financial asset.

c. Held-to-maturity investments

They are classified as the held-to-maturity investments that have either fixed or determinablepayments, or fixed-term debt instruments and for which an entity has both the ability and the intentionto hold to maturity. The held-to-maturity investments are recognized deducting the impairmentamount from the amortized cost based on the effective interest model and the related incomes arecalculated using the effective interest method.

The Company has no held-to-maturity investments as of the balance sheet date.

d. Available-for-sale financial assets

They are classified as the publicly quoted equity instruments held by the Company and traded in anactive market and the financial assets some of the debt securities of which are ready to be sold andthey are shown at fair value. The Company has equity instruments classified as the financial assets notpublicly quoted and not traded in an active market but ready to be sold; and their fair values cannot bemeasured reliably; therefore, they are shown at amortized costs. Impairments on the statement ofincome and the gains and losses arising from the changes in the fair value, except for the exchangedifference profit/loss amount regarding the interest and monetary instruments calculated using theeffective interest method are recognized within the other comprehensive income and accumulated inthe financial assets appreciation fund. In case the investment is sold or subjected to impairment, thetotal profit/loss accumulated in the financial assets appreciation fund are classified in the statement ofincome.

Dividends associated with the available-for-sale equity instruments are recognized in profit/loss whenthe Company is vested to receive the related payments.

The fair value of the available-for-sale financial assets in foreign currency is calculated by convertingthe current value in the related foreign currency to the reported currency using the conversion ratevalid on the reporting date. The changes in the fair value of the asset that arise from the conversionrate are recognized in profit/loss, while other changes are recognized under equity.

The Company does not have any available-for-sale investments as of the balance sheet date.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

12

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

e. Impairment in financial assets

The financial assets other than the ones at fair value through profit or loss are evaluated to find someindicators on whether a financial asset or a group of financial assets is impaired or not on each balancesheet date. In the event that one or more than one incidents happen after the first recognition of thefinancial assets and there is an objective indicator showing that the stated loss having an impact on theestimated cash flows of the related financial asset or the financial asset group, which can be reliablyestimated, has caused the financial asset to be impaired, the impairment occurs and the impairmentloss arises. The impairment amount for the loans and receivables is the difference between the currentvalue of the anticipated cash flows calculated discounting over the basic interest rate of the financialasset and the book value.

Except the trade receivables the book value of which is decreased using an allowance account, theimpairment in all the financial assets is deducted from the quoted value of the asset directly. In casethe trade receivable cannot be collected, this amount is written off by being deducted from theallowance account. The changes in the allowance account are recognized in profit or loss.

Except the available-for-sale equity instruments, if the impairment loss decreases in the next term andcan be associated with an event that happens after the recognition of the impairment loss, theimpairment loss recognized before is cancelled in profit / loss not to exceed the amortized cost to reachin the event that the impairment of the investments is never recognized on the date of cancellation forthe impairment.

The increase in the fair value of the available-for-sale equity instruments after the impairment isrecognized directly in equities.

f. Financial liabilities

The financial liabilities and equity instruments of the Company are classified based on contractualarrangements and the definition basis of a financial liability and equity-based instrument. The contractrepresenting the right in the remaining assets after deducting all the debt of the Company is the equityfinancial instrument.

The financial liabilities are classified as the financial liabilities at fair value through profit or loss or asother financial liabilities.

g. Financial liabilities at fair value through profit or loss

Financial liabilities at fair value through profit or loss, is recognized in their fair values and in eachreporting term, revaluated in their fair values on the balance sheet date. A change in the fair values isrecognized in the statement of income. Net gains or losses recognized in the statement of incomeinclude the interest rate paid for the stated financial liability.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

13

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

h. Derivative financial instruments

The operations of the Company mainly establish the entity and expose it to the financial risks based onthe changes in the interest rates. Derivative financial instruments (basically foreign exchange swapcontracts) are used sometimes in order to manage the financial risks associated with the exchange ratefluctuations based on the future foreign exchange and loan transactions.

Derivative financial instruments are calculated at the fair value on the contract date and thenrecalculated at their fair value in the next reporting terms. The Company does not indicate thederivative financial instruments as hedging and therefore, the change in the current values of thesederivative transactions is associated with the income and expenditure of the current year.

As on 31 December 2013 and 31 December 2012, the Company does not have any ongoing derivativetransactions.

Factoring receivables and provision for impaired factoring receivables

Factoring receivables originated by the Company by providing money directly to the borrower areconsidered as factoring receivables and are carried at amortised cost. All factoring receivables arerecognised when cash is advanced to borrowers against their domestic and foreign receivables.

A credit risk provision for impairment of the factoring receivables is established if there is objectiveevidence that the Company will not be able to collect all amounts due as a result of one or more eventsthat occurred after the initial recognition of the asset (a “loss event”) and that loss event(or events) has an impact on the estimated future cash flows of the receivables. The amount of theprovision for impaired factoring receivables is the difference between the carrying amount andrecoverable amount, being the present value of expected cash flows, including the amount recoverablefrom guarantees and collateral, discounted based on the interest rate at inception. For restructuredreceivables, the Company initially determines as to whether there has been an impairment as a resultof the restructuring, and if so, a provision for impairment is recorded representing the differencebetween the recoverable amount, being the present value of expected cash flows from restructuredreceivables discounted using the interest rate of the original receivables, and the carrying amount.

The provision also covers losses where there is objective evidence that probable losses are present incomponents of the portfolio at the balance sheet date. These have been estimated based upon historicalloss experience which is adjusted on the basis of current observable data to reflect the effects ofcurrent conditions that did not affect the period on which the historical loss experience is based and toremove the effects of conditions in the historical period that do not currently exist. The provision madeduring the year is charged against the income for the period.

Receivables that cannot be recovered are written off and charged against the provision for impairedfactoring receivables. These receivables are written off after all the necessary legal procedures havebeen completed and the amount of the loss is finally determined. Recoveries of amounts previouslyprovided for are treated as a reduction of the charge for provision for impaired factoring receivablesfor the period (Note 6).

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

14

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

Property and equipment

The Company has chosen the “revaluation method” as defined in (IAS 16) “Plant, property andequipment” in subsequent measurement of its buildings stated in its properties. The Company presentsthe buildings at the fair value based on valuation report of an independent licensed valuation company.Valuations are performed with sufficient regularity to ensure that fair value of buildings does notdiffer materially from its carrying amounts. Accumulated depreciation concerning the buildings isrestated proportionate to the change in the gross carrying amount of the asset such that the net bookvalue of the asset after revaluation equals its revaluated amount. All other property and equipment isstated at their net value which is their historical costs less any accumulated depreciation andimpairment (Note 12).

If a revaluation results in an increase in value, it should be credited to as “other comprehensiveincome” under the “Statement of Comprehensive Income” and accumulated in equity under theheading “revaluation funds” unless it represents the reversal of a revaluation decrease of the sameasset previously recognised as an expense, in which case it should be recognised as income.

Property and equipment are presented at recorded amount after the deduction of impairment andaccumulated depreciation (Note 12).

Depreciation is calculated on the booked amounts of property and equipment using the straight-linemethod. The ranges of estimated useful lives are as follows:

Buildings 50 yearsOffice equipment, furniture and fixtures 4-5 yearsLeasehold improvements 4-5 years

Estimated useful life and depreciation method is checked for every year in order to determine theprobable effects of the changes in estimation and these changes are recorded. Where the carryingamount of an asset is greater than its estimated recoverable amount, it is written down to itsrecoverable amount and the impairment provision is accounted for related to the income statement.

Gains or losses on disposal of property and equipment are determined with the comparison of restatedamounts and sales amounts and recorded to the related income or expense accounts.

Intangible assets

Intangible assets are comprised of software expenses and amortized over their estimated useful lives offive years. Expenses for the repair and maintenance of computer software are accounted for in theincome statement. However, the expenses are capitalized if they result in an enlargement or substantialimprovement of the respective assets (Note 13).

Impairment of assets

At each reporting date, the Company evaluates whether there is any impairment indication on theasset. When an indication of impairment exists, the Company estimates the recoverable values of suchassets. Impairment exists if the carrying value of an asset or a cash generating unit is greater than itsrecoverable amount which is the higher of value in use or fair value less costs to sell.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

15

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

Assets held for sale

A tangible asset (or a disposal Company of tangible assets) classified as “asset held for sale” ismeasured at lower of carrying value or fair value less costs to sell. An asset (or a disposal group ofassets) is regarded as “asset held for sale” only when the sale is highly probable and the asset (disposalgroup) is available for immediate sale in the frame of the common conditions for sale of assets.

Financial liabilities and issued debt securities

Financial liabilities are recognized initially at fair value, including the transaction costs incurred.Subsequently, financial liabilities are measured at amortized cost using the effective yield method.Any difference between initial amount after transaction costs and the amortized value is recognized inthe income statement as finance cost over the redemption period of the financial liability.

Accounting for finance lease (where the Company is “lessee”)

Under the finance leases, the Company recognizes the assets, with the fair value of the leased asset or,if lower, the present value of the minimum lease payments each determined at the inception of thelease. The assets that are obtained with finance lease agreements are classified as property andequipment. The useful life of an asset leased under a finance lease is considered equal to the lease termand leased assets are depreciated over the period of lease term. The finance lease liabilities arepresented in the balance sheet as “Finance lease payables” and related interest expenses and exchangegains and losses are charged to the income statement in the period that they occur (Note 9).

Income taxes

a. Income taxes currently payable

Income taxes (“corporation tax”) currently payable are calculated based in accordance with theTurkish tax legislation (Note 14).

Taxes other than on income are recorded within operating expenses (Note 20).

b. Deferred income taxes

Deferred income tax is provided in full, using the liability method, on temporary differences arisingbetween the tax bases of assets and liabilities and their carrying amounts in the financial statements.The rates enacted, or substantively enacted, at the balance sheet date are used to determine deferredincome tax.

The principal temporary differences arise from the provision for impaired factoring receivables,property and equipment, reserve for annual leave and provision for employment termination benefits(Note 14).

Deferred tax liabilities and assets are recognised when it is probable that the future economic benefitresulting from the reversal of temporary differences will flow to or from the Company. Deferred taxassets resulting from temporary differences in the recognition of expense for income tax, and forfinancial reporting purposes are recognised to the extent that it is probable that future taxable profitwill be available against which the deferred tax asset can be utilised.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

16

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

Provisions

Provisions are recognised when the Company has a present legal or constructive obligation as a resultof past events and it is probable that an outflow of resources will be required to settle the obligationand a reliable estimate of the amount can be made. If mentioned criteria are not formed, then theCompany presents these cases in the related financial notes. Where the effect of the time value ofmoney is material, the amount of a provision shall be the present value of the expenditures expected tobe required to settle the obligation. The discount rate reflects current market assessments of the timevalue of money and the risks specific to the liability.

The contingent assets are not accounted for in the financial statements unless they are realized anddisclosed in the related notes to the financial statements.

Employment termination benefits

Provision for employment termination benefits represents the present value of the future probableobligation of the Company. According to the labour laws and regulations in Turkey, the Company isrequired to provide compensation payments to employees who retires, leaves or is dismissed due toany inappropriate act defined in Turkish Labour Law. In this context, provision for employmenttermination benefits that represents the present value of the future probable obligation of theCompany, is calculated with defined actuarial estimations which arise from the changes in theactuarial assumptions or the differences between actuarial assumptions and outturns and accrued to thefinancial statements (Note 15).

Revenue recognition

Factoring service revenues are the interest income collected from the customers and accrued on thecash advances paid to these customers. Commission income is composed of a percentage of theamounts on invoices subject to factoring. All income and expenses are recognised on the accrual basis.

In finance leasing, the asset subject to leasing is accounted for in financial statements at a receivableamount equal to the net leasing investment. Finance income under finance lease is identified byapplying a constant rate of return to the net investment subject to lease. Received lease payments arededucted from the gross lease investment by decreasing the cost and unearned finance income. Theunearned finance income represents the difference between the gross amount of the leasing investmentand the present value of the investment calculated by a rate of return used in leasing. Rate of returnrepresents the rate that equalizes the sum of the minimum lease payments and the non-guaranteedremaining balance to the sum of the fair value and initial cost of the leased asset.

Commissions and fees, resulted from factoring and finance lease operations, are accrued on a timebasis.

Foreign currency transactions

Foreign currency transactions are translated into Turkish Lira using the exchange rates prevailing atthe dates of the transactions. Foreign exchange gains and losses resulting from the settlement of suchtransactions and from the translation at year-end exchange rates of monetary assets and liabilitiesdenominated in foreign currencies are accounted for in the income statement. Translation of thosebalances is performed with the year-end exchange rates.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

17

NOTE 2 - BASIS OF PRESENTATION OF FINANCIAL STATEMENTS (Continued)

Comparatives

Financial statements of the Company have been prepared comparatively with the prior period in orderto give information about financial position and performance. If the presentation or classification ofthe financial information is changed, in order to maintain consistency, financial information of theprior periods is also reclassified in line with the related changes.

No material reclassification has been made in the prior period financial statements of the Company.

Reporting of cash flows

For the purposes of statement of cash flows, cash and cash equivalents include cash and due frombanks with original maturity periods of less than three months, excluding the interest income accrualsaccrued over time deposits (Note 5).

Changes in accounting policies

Material changes in accounting policies are applied retrospectively and previous period financialstatements are rearranged. There is no material change in Company’s accounting policies in currentyear.

Changes in accounting estimates and errors

Significant changes in accounting policies or significant errors are corrected, retrospectively; byrestating the prior period consolidated financial statements. The effect of changes in accountingestimates affecting the current period is recognised in the current period; the effect of changes inaccounting estimates affecting current and future periods is recognised in the current and futureperiods.

Shareholders’ equity and dividends

The ordinary shares are classified as share capital. The dividends distributed over the ordinary sharesare recognized in the period when they are declared. The necessary expenses that incur directly fromthe increase in share capital are recognized under total paid-in share capital.

Subsequent events

Certain subsequent events that require an adjustment are provided with additional informationregarding the position of Company as of the balance sheet date are recognised in the financialstatements. Events that do not require an adjustment are presented at the notes to these financialstatements, if they meet a certain level of importance (Note 25).

NOTE 3 - CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

The Company makes estimates and assumptions that affect the reported amounts of assets andliabilities within the next financial year. Estimates and judgements are continually evaluated and arebased on Management’s experience and other factors, including expectations of future events that arebelieved to be reasonable under the circumstances. Management also makes certain judgements, apartfrom those involving estimations, in the process of applying the accounting policies. Judgements thathave the most significant effect on the amounts recognised in the financial statements and estimatesthat can cause a significant adjustment to the carrying amount of assets and liabilities within the nextfinancial year include.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

18

NOTE 3 - CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS (Continued)

Recognition of deferred tax assets:

Deferred tax assets can be recorded as much as the said tax benefit is probable. Amount of taxableprofits and possible tax benefits in the future is based on medium term business plan and expectationsprepared by the Company. The business plan is based on rational expectations of the Company undercurrent circumstances.

Allowance for impairment of factoring receivables:

A credit risk provision for impairment of factoring receivables is established if there is objectiveevidence that the Company will not be able to collect all amounts due. The estimates used inevaluating the adequacy of the provision for impairment of factoring receivables are based on value ofcollaterals in hand.

The Company intends to not to distribute capital gains which may arise in next periods out of the saleof tangible fixed assets that the Company has accounted with fair value, for 5 years period subsequentto such transactions, in order to benefit from the tax exemptions specified in relevant legislation.Consequently, deferred tax liabilities which have been calculated from temporary differences derivedbetween cost and fair value of the asset are calculated by taking into consideration of relevantexemptions (Note 14).

NOTE 4 - FINANCIAL RISK MANAGEMENT

Credit risk

Credit risk is the risk that one party to a financial instrument will fail to meet the terms of theiragreements as foreseen and cause the Company to incur a financial loss. The Company is subject torisks as a result of factoring activities. Credit risk is controlled by allocating specific limits to partiesthat create the credit risk and following the anticipated collections from customers. Credit risk is fullyconcentrated in Turkey where the Company mainly operates. Serving many customers from differentsectors allows the company to spread the credit risk.

The carrying amount of financial asset s recorded in the financial statements, grossed up for anyallowances for losses, represents the Company’s maximum exposure to credit risk without takingaccount of the value of any collateral obtained. As at the date of the financial statements the maximumexposure to credit risk of the Company’s financial assets is equal to their carrying values.

Geographical distribution of Company’s assets and liabilities are as follows:

Total Total31 December 2013 assets % liabilities %

Turkey 398,419 100 308,733 100European countries - - - -

398,419 100 308,733 100

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

19

NOTE 4 - FINANCIAL RISK MANAGEMENT (Continued)

Total Total31 December 2012 assets % liabilities %

Turkey 330,926 100 237,529 96European countries - - 9,511 4

330,926 100 247,040 100

Market risk

Market risk is the risk of negative effect of fluctuations in interest rates, exchange rates, inflation rates,and market prices on the Company’s share capital, income and ability to reach their objectives. TheCompany follows market risk under the headings, liquidity risk, exchange rate risk and interest raterisk.

Interest rate risk

The table below analyses assets and liabilities of the Company into relevant maturity buckets based onthe remaining period at balance sheet date to the contractual repricing dates.

Up to 3 3 to12 Over Non-interest31 December 2013 months months 1 year bearing Total

AssetsCash and cash equivalents 13,000 - - 1,972 14,972Factoring receivables, net 35,111 299,187 37,252 - 371,550Assets held for sale - - - 116 -Other assets and prepaid expenses - - - 1,957 1,957Property and equipment, net - - - 3,152 3,152Intangible assets, net - - - 245 245Deferred tax asset, net - - - 6,427 6,427

Total assets 37,530 299,187 37,252 26,869 398,419

LiabilitiesBank borrowings 145,849 57,790 - - 203,639Issued debt securities 2,904 53,931 44,862 - 101,697Factoring payable - - - 517 517Current income taxes payable, net - - - 690 690Financial lease payable 28 87 50 - 165Other liabilities and accrued expenses - - - 1,447 1,447Employment benefit obligations - - - 578 578

Total liabilities 148,781 111,808 44,912 5,651 308,733

Net repricing gap (111,251) 187,379 (7,660) 21,218 89,686

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

20

NOTE 4 - FINANCIAL RISK MANAGEMENT (Continued)

Up to 3 3 to12 Over Non-interest31 December 2012 months months 1 year bearing Total

AssetsCash and cash equivalents - - - 19,363 19,363Factoring receivables, net 187,927 66,103 42,609 - 296,639Assets held for sale - - - 116 116Other assets and prepaid expenses - - - 1,246 1,246Property and equipment, net - - - 7,829 7,829Intangible assets, net - - - 135 135Deferred tax asset, net - - - 5,598 5,598

Total assets 187,927 66,103 42,609 34,287 330,926

LiabilitiesBank borrowings 150,874 40,432 2,000 - 193,306Issued debt securities 1,319 3,786 45,361 - 50,466Factoring payable - - - 520 520Current income taxes payable, net - - - 663 663Financial lease payable 22 67 137 - 226Other liabilities and accrued expenses - - - 1,035 1,035Employment benefit obligations - - - 824 824

Total liabilities 152,215 44,285 47,498 3,042 247,040

Net repricing gap 35,712 21,818 (4,889) 31,245 83,886

Currency risk

The exchange rate risk originates from the foreign currency denominated assets and liabilities. TheCompany holds certain amount of foreign exchange position result of its operations.

The table below shows the Company’s sensitivity to 10% change in USD, EUR and CHF rates. Thetable below presents the effect of 10% increase in USD, EUR and CHF rates against TL on incomestatement. In this analysis, all other variables, in particular the interest rates are assumed to remainconstant.

Profit/(Loss) Profit/(Loss)2013 2012

USD (22) (14)EUR - -CHF - -

In case of 10% decrease in exchange rates against TL, there will be a negative effect on the incomestatement same as the amounts above.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

21

NOTE 4 - FINANCIAL RISK MANAGEMENT (Continued)

The Company’s assets and liabilities denominated in foreign currencies are as follows:

31 December 2013 USD EUR Total

AssetsCash and cash equivalents - 4 4Other assets and prepaid expenses 2 - 2

Total assets 2 4 6

LiabilitiesFinancial lease payable 165 - 165

Total liabilities 165 - 165

Net balance sheet position (163) 4 (159)

31 December 2012 USD EUR Total

AssetsCash and cash equivalents 89 4 93Other assets and prepaid expenses 2 - 2

Total assets 91 4 95

LiabilitiesFinancial lease payable 226 - 226

Total liabilities 226 - 226

Net balance sheet position (135) 4 (131)

As of 31 December 2013 and 2012, exchange rates of the foreign currencies used by the Company areas follows:

2013 2012

USD 2.1343 1.7826EUR 2.9365 2.3517

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

22

NOTE 4 - FINANCIAL RISK MANAGEMENT (Continued)

Liquidity risk

Liquidity risk is the possibility that the Company will be unable to fund its net funding requirements.Liquidity risk can be caused by market disruptions or credit downgrades, which may cause certainsources of funding to dry up immediately. To hedge against this risk, management has diversifiedfunding sources, and assets are managed with liquidity in mind, maintaining a proper balance of cashand cash equivalents.

The table below analyses liabilities of the Company into relevant maturity buckets as at31 December 2013 and 2012, based on the remaining period to the contractual maturity dates.Additionally, the interests that will be collected based on the assets and liabilities of the Company, areincluded in the table below. The amounts disclosed in the table are the contractual undiscounted cashflows.

Up to 3 3 to12 Over No definite31 December 2013 months months 1 year maturity Total

Bank borrowings 141,851 61,788 - - 203,639Factoring payables - - - 517 517Financial lease payables 31 95 51 - 177Issued debt securities 2,941 57,422 53,083 - 113,446

Total liabilities 144,823 119,305 53,134 517 317,779

Up to 3 3 to12 Over No definite31 December 2012 months months 1 year maturity Total

Bank borrowings 142,159 53,975 2,202 - 198,336Factoring payables - - - 520 520Financial lease payables 26 79 147 - 252Issued debt securities 1,329 4,035 54,035 - 59,399

Total liabilities 143,514 58,089 56,384 520 258,507

Fair value of financial instruments

Fair value is the amount at which a financial instrument could be exchanged in a current transactionbetween willing parties, other than in a forced sale or liquidation. The fair value is best evidenced by aquoted market price, if one exists.

The estimated fair values of financial instruments have been determined by the Company usingavailable market information and appropriate valuation methodologies. However, judgement isnecessarily required to interpret market data to develop the estimated fair value. Accordingly, theestimates presented herein are not necessarily indicators of the amounts the Company could realise ina current market exchange.

The fair values of current financial assets and short term borrowings are considered to approximatetheir respective carrying values due to their short term nature and the insignificant discount effect.

The carrying value of factoring receivables including the provision for doubtful receivables is alsoconsidered to approximate the fair value due to their short-term nature.

Since the Company does not have any financial assets carried at fair value, no additional disclosure offair value measurements by level of fair value hierarchy has been presented.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

23

NOTE 4 - FINANCIAL RISK MANAGEMENT (Continued)

Capital risk management

According to the regulation's 12th article, published in Official Gazette on 24 April 2013, for financiallease, factoring and finance companies’ foundation and operation bases, factoring companies arerequired to achieve and maintain a minimum of 3 per cent equities to total assets ratio. The Company’stotal equity exceeds 3 per cent of its total assets in the calculation which is made as of31 December 2013 (2012: Exceeds).

NOTE 5 - CASH AND CASH EQUIVALENTS

2013 2012

Cash on hand 41 17Banks:- Demand deposits 1,931 4,444- Time deposits 13,000 14,902

14,972 19,363

As of 31 December 2013, time deposits are shorter than 3 months and also as of 31 December 2013,there is no blockage over bank deposits (2012: there is no blockage over bank deposits).

For the purposes of the cash flow statement, cash and cash equivalents amounting to TL 14,966(2012: TL 19,361) as of 31 December 2013 comprised from cash and due from banks excludingaccrued interest and blocked deposits.

NOTE 6 - FACTORING RECEIVABLES, NET

2013 2012

Domestic transactions 391,958 312,209Impaired factoring receivables 29,418 42,282

Gross factoring receivables 421,376 354,491

Less: allowance for specific provision (29,418) (42,282)Less: allowance for additional provision (6,145) (2,099)Less: unearned revenue (*) (14,263) (13,471)

Factoring receivables, net 371,550 296,639

(*) Unearned revenue represents advance collections of factoring fees, recognised on pro-rata basis over theterm of the collection of factoring receivables.

At 31 December 2013 and 2012, factoring receivables are fixed interest rated.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

24

NOTE 6 - FACTORING RECEIVABLES, NET (Continued)

Factoring receivables can be analysed as below;

2013 2012

Neither past due nor impaired (*) 377,695 297,521Past due but not impaired - 1,217Impaired 29,418 42,282

Gross factoring receivables 407,113 341,020

Less: allowance for impairment (35,563) (44,381)

Net factoring receivables 371,550 296,639

(*) TL 27,362 of the relevant amount consists of the restructured receivables.

The aging analysis of the factoring receivables past due but not impaired is as follows:

2013 2012

1 - 3 months - 1,217

Prospective aging analysis of the net factoring receivables is as follows. The balances have been statedexcluding impaired factoring receivables and the general portfolio provision.

2013 2012

Up to 3 month 41,256 190,0263 month to 1 year 299,187 66,1031 year more 34,833 42,609

371,550 298,738

Movements in the provision for impaired factoring receivables during the year are as follows:

2013 2012

1 January 44,381 37,660

Charge for the year 13,129 7,771Recoveries of amounts previously provided (478) (1,050)Derecognized through sales (1) (21,469) -

35,563 44,381

(1) At the Board of Directors meeting held on 25 December 2013, it has been decided to sell out a non-performing loan portfolio included in non-performing loan accounts at a price of TL 20 thousand. Thistransaction has affected the financial statements as TL 20 thousand of pretax income.

As of 31 December 2013, the total of post-dated cheques and notes for the factoring receivables of theCompany is TL 379,553 (2012: TL 315,383) (Note 24). These cheques and notes are followed upunder off-balance sheet accounts.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

25

NOTE 6 - FACTORING RECEIVABLES, NET (Continued)

Economic sector risk concentrations of gross factoring receivables are shown in the table below. Thebalances have been stated excluding impaired factoring receivables and the general portfolioprovision.

2013 % 2012 %

Construction 62,391 17.83 51,889 17.37Consultancy, entertainment, advertising and media 28,875 8.25 45,216 15.14Textile and textile products 28,819 8.24 30,118 10.08Mining industry 24,400 6.97 25,371 8.49Transportation, warehousing and communication 21,365 6.11 14,784 4.95Food, beverage and tobacco industry 20,230 5.78 17,573 5.88Sport activities 18,844 5.39 33,603 11.25Wholesale and retail trade 17,132 4.90 5,508 1.84Transportation Vehicles Industry 15,244 4.36 10,787 3.61Metal industry and processed material production 14,026 4.01 4,028 1.35Agriculture, farming and forestry 11,178 3.20 1,993 0.67Electrical and optical equipment 10,493 3.00 12,164 4.07Paper and printing industry 9,884 2.83 2,728 0.91Nuclear energy, oil and coal products manufacturing 7,634 2.18 6,057 2.03Wood and wooden products industry 7,455 2.13 2,730 0.91Machinery and equipment 7,235 2.07 4,775 1.60Health 7,195 2.06 10,005 3.35Leather industry 5,893 1.68 3,284 1.10Chemical products industry 4,602 1.32 1,393 0.47Rubber and plastic products industry 4,096 1.17 1,106 0.37Tourism 3,579 1.02 10,421 3.49Electric, gas and water resources 2,354 0.67 552 0.18Other 38,626 4.80 2,653 0.89

371,550 100.00 298,738 100.00

NOTE 7 - ASSETS HELD FOR SALE2013 2012

Assets held for sale 116 116

116 116

At 31 December 2013 and 2012 asset held for sale comprised of the tangible assets obtained againstdelinquent receivables.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

26

NOTE 7 - ASSETS HELD FOR SALE (Continued)

Movement for assets held for sale for the period ended 31 December 2013 and 2012 is as follows:

1 January 31 December2013 Additions Disposals 2013

Cost:

Buildings 114 - - 114Securities 2 - - 2

116 - - 116

1 January 31 December2012 Additions Disposals 2012

Cost:

Buildings 114 - - 114Securities 38 - (36) 2

152 - (36) 116

NOTE 8 - BORROWINGS

Borrowings at 31 December 2013 and 2012 are set out below according to their currencies:

2013 2012Effective Original Effective Original

interest rate currency TL interest rate currency TL

Domestic banks (*)

Fixed rate borrowings:TL 11.31 185,113 185,113 10.86 183,795 183,795

Total domestic bank borrowings 185,113 183,795

(*) The effective interest rates of borrowings from domestic banks have been calculated together with the Banking andInsurance Transactions Tax (“BITT”) rate.

2013 2012Effective Original Effective Original

interest rate currency TL interest rate currency TL

Foreign banks

Fixed rate borrowings:TL 10.77 18,526 18,526 12.39 9,511 9,511

Total foreign bank borrowings 18,526 9,511

Total borrowings 203,639 193,306

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

27

NOTE 9 - FINANCIAL LEASE PAYABLES

Net and gross financial lease liabilities that the Company have leased tangible fixed assets withfinancial leasing agreements are as follows:

Gross leasing liabilities2013 2012

Up to 1 year 125 1041 - 4 years 52 148

Gross leasing payables 177 252

Deferred finance lease expenses (-) (12) (26)

Net leasing payables 165 226

NOTE 10 - ISSUED DEBT SECURITIES

2013 2012

Bonds issued 101,697 50,466

101,697 50,466

The Company has bonds those were issued through private placement. The details of those bonds areas follows:

ISIN CODE Issue Date Issued Amount Redemption date Coupon period

TRSEKOF71415 26 July 2012 TL 51,042 24 July 2014 Coupon payment per three monthTRSEKOF51516 24 May 2013 TL 50,655 22 May 2015 Coupon payment per three month

The coupons of the issued bonds are floating interest rates. For each coupon payment, the nominalinterest rates are calculated with respect to the rates of related government debt securities issued by theundersecretaries of Treasury with the methods defined in the circulars for those bonds.

NOTE 11 - OTHER ASSETS AND PREPAID EXPENSES

2013 2012

Prepaid expenses 1,042 277Advances given to courts 804 525Deposits and guarantees given 75 64Receivable from personnel 36 32Advances given to suppliers - 291Advances given to personnel - 47Other - 10

1,957 1,246

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

28

NOTE 12 - PROPERTY AND EQUIPMENT

1 January 31 December2013 Additions Disposals 2013

Cost:

Buildings (**) 6,447 - (6,447) -Machinery and equipments (*) 2,266 560 (104) 2,722Furniture and fixtures 472 583 - 1,055Leasehold improvements 536 1,371 (33) 1,874

9,721 2,514 (6,584) 5,651

Accumulated depreciation:

Buildings (71) (3) 74 -Machinery and equipments (1,516) (502) 104 (1,914)Furniture and fixtures (226) (107) - (333)Leasehold improvements (79) (206) 33 (252)

(1,892) (818) 211 (2,499)

Net book value 7,829 1,696 (6,373) 3,152

1 January 31 December2012 Additions Disposals 2012

Cost:

Buildings (**) 6,283 - - 6,447Machinery and equipments (*) 1,654 695 (83) 2,266Furniture and fixtures 283 217 (28) 472Leasehold improvements 105 431 - 536

8,325 1,343 (111) 9,721

Accumulated depreciation:

Buildings (498) (125) - (71)Machinery and equipments (1,350) (249) 83 (1,516)Furniture and fixtures (211) (41) 26 (226)Leasehold improvements (57) (22) - (79)

(2,116) (437) 109 (1,892)

Net book value 6,209 906 (2) 7,829

The amount of insurance on tangible fixed assets is TL 3,475 as of 31 December 2013 (31 December2012: TL 2,891)

(*) Machinery and equipment acquired through leasing assets are not available in 2013 (31 December 2012:Machinery and equipment items in 2012 through leasing of additional amounts of tangible fixed assets arecapitalized for TL 280).

(**) There are no pledge on tangible fixed assets as of 31 December 2013 (2012: Buildings are pledged to thecounterparty banks as collateral against the funds borrowed).

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

29

NOTE 12 - PROPERTY AND EQUIPMENT (Continued)

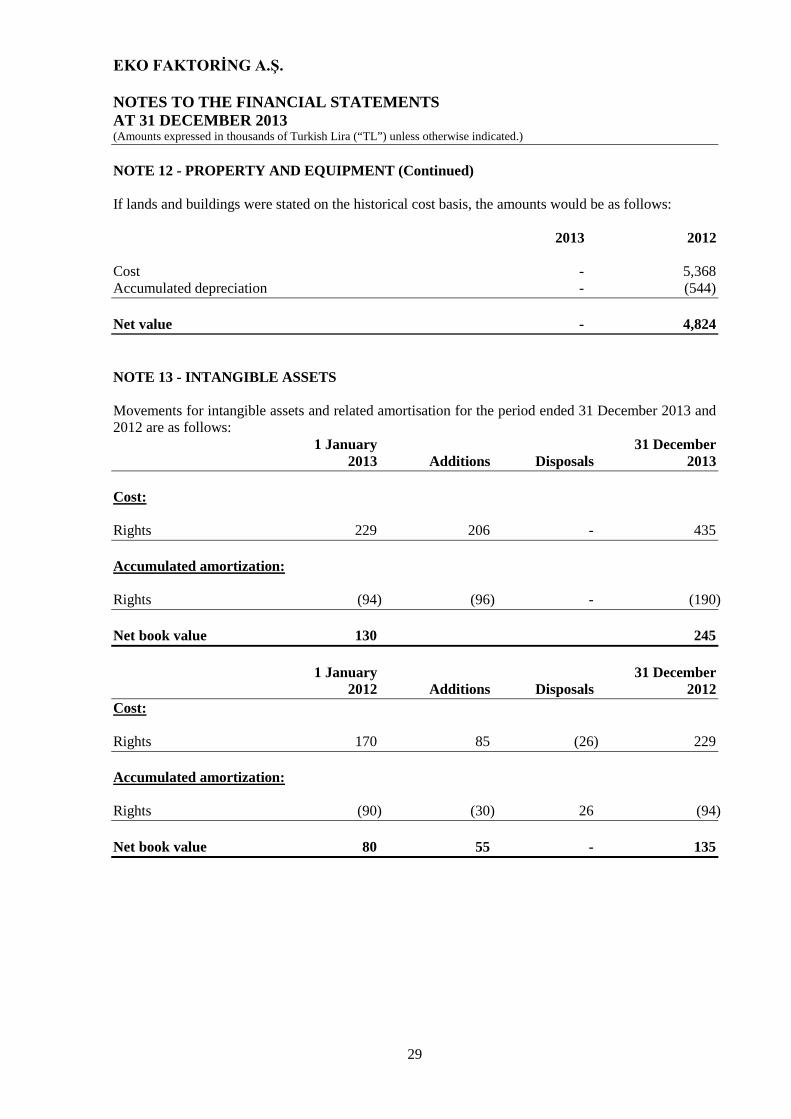

If lands and buildings were stated on the historical cost basis, the amounts would be as follows:

2013 2012

Cost - 5,368Accumulated depreciation - (544)

Net value - 4,824

NOTE 13 - INTANGIBLE ASSETS

Movements for intangible assets and related amortisation for the period ended 31 December 2013 and2012 are as follows:

1 January 31 December2013 Additions Disposals 2013

Cost:

Rights 229 206 - 435

Accumulated amortization:

Rights (94) (96) - (190)

Net book value 130 245

1 January 31 December2012 Additions Disposals 2012

Cost:

Rights 170 85 (26) 229

Accumulated amortization:

Rights (90) (30) 26 (94)

Net book value 80 55 - 135

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

30

NOTE 14 - TAXES ON INCOME

2013 2012

Corporate tax provision 690 663

690 663

2013 2012

Corporate tax payable 3,563 4,976Less: prepaid taxes (2,873) (4,313)

Corporate tax payable, net 690 663

Current year tax expense (3,563) (4,976)Deferred tax income 835 710

Total tax expense (2,728) (4,266)

The Corporate Tax Law was amended by Law No. 5520 dated 13 September 2006. Most of thearticles of the new Corporate Tax Law in No. 5520, have come into force effective from 1 January2006. Corporation tax is payable at a rate of 20% (2010: 20%) on the total income of the Companyregistered in Turkey after adjusting for certain disallowable expenses, tax exempt income (e.g. incomefrom subsidiaries and investment incentive) and other allowances (e.g. research and developmentallowance). No further tax is payable unless the profit is distributed (except for withholding tax at therate of 19.8%, calculated on an exemption amount if an investment allowance is granted in the scopeof Income Tax Law temporary article 61).

Dividends paid to non-resident corporations, which have a place of business in Turkey, or residentcorporations are not subject to withholding tax. Otherwise, dividends paid are subject to withholdingtax at the rate of 10% according to the Income Tax Law No, 94. An increase in capital via issuingbonus shares is not considered as a profit distribution.

Corporations are required to pay advance corporation tax quarterly at the rate of 20% on theircorporate income. Advance tax is declared to the tax authority by the 14th day and payable by the 17th

day of the second month following each calendar quarter end. Advance tax paid by corporations isdeducted from the annual corporation tax liability. If, despite offsetting, there remains an amount foradvance tax amount paid, it may be refunded or offset against other liabilities to the government.

In Turkey, there is no procedure for a final and definitive agreement on tax assessments. Companiesfile their tax returns by the 25th of the fourth month following the close of the financial year to whichthey relate.

In tax reviews, authorized bodies can review the accounting records for the past five years and if errorsare detected, tax amounts may change due to tax assessment.

Under the Turkish taxation system, tax losses can be carried forward to be offset against future taxableincome for up to 5 years. Tax losses cannot be carried back to offset profits from previous periods.

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

31

NOTE 14 - TAXES ON INCOME (Continued)

There exist many exemptions in Corporate Income Tax Law for corporations. Therefore, theexceptional incomes in the commercial income/profit have been considered during the corporateincome tax calculations.

The reconciliation between the expected and the actual taxation charge is as follows:

2013 2012

Profit before tax 12,846 20,877

Theoretical tax charge at the applicable tax rate of 20% 2,569 4,176Disallowable expenses and other additions 159 90Tax-exempt income - -

Current year tax charge 2,728 4,266

The temporary differences giving rise to the deferred income tax assets and the deferred tax liabilitiesare as follows:

2013 2012Cumulative Deferred tax Cumulative Deferred taxtemporary assets/ temporary assets /differences (liabilities) differences (liabilities)

Provision for impairedfactoring receivables 17,891 3,578 14,616 2,923

Unearned factoring income 14,263 2,853 13,471 2,694Provision for employment benefit

obligations 578 116 424 85Other provisions 25 5 23 6

Deferred tax assets 6,552 5,708

Difference between the carryingvalue and tax base ofproperty and equipment (632) (124) (114) (23)

Discount difference of loans andsecurities issued (8) (1) (35) (7)

Revaluation difference of building - - (1,592) (80)

Deferred tax liabilities (125) (110)

Deferred tax assets, (net) 6,427 5,598

Deferred tax assets/(liabilities) movement table as follows:

Net2013 2012

Deferred tax credit related with the net income for the period 835 710Deferred tax charge related with components of

other comprehensive income - (80)

835 630

EKO FAKTORİNG A.Ş.

NOTES TO THE FINANCIAL STATEMENTSAT 31 DECEMBER 2013(Amounts expressed in thousands of Turkish Lira (“TL”) unless otherwise indicated.)

32

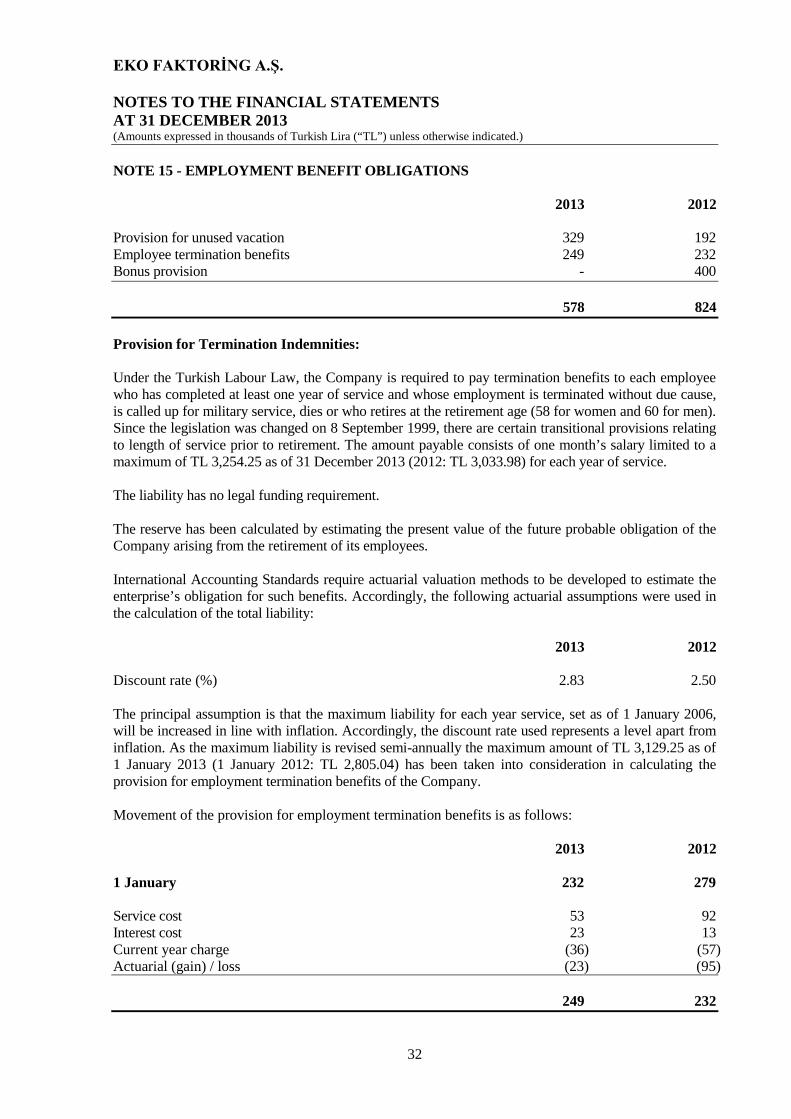

NOTE 15 - EMPLOYMENT BENEFIT OBLIGATIONS

2013 2012

Provision for unused vacation 329 192Employee termination benefits 249 232Bonus provision - 400

578 824