Embed Size (px)

Citation preview

Effects of The New Pension Reform on your MTRS Benefits

Recent Changes in Pension Law Member Benefits & Creditable Service

Pension Options

Presented by:Peggy Dougherty

Financial Advisor, Lincoln Investment Planning, Inc.

Marie ArditoRetired Educator, Mass Retirees United

April 12, 2012Reading Public Schools

Peggy Dougherty offers advisory services and securities through Lincoln Investment Planning, Inc., Registered Investment Advisor, Broker Dealer, Member FINRA/SIPC. 51 Sawyer Road, Waltham, MA 02453 (71)647-3050 . Supervising office: 218 Glenside Avenue, Wyncote, PA 19095 (800)242-1421

Marie Ardito is associated with Lincoln Investment as a speaker and not as a financial representative. 04/12

Disclaimer

While the information presented is believed to be accurate and reliable as of seminar date, it is recommended that each individual confirmit's applicability to his/her own retirement variables and with a retirement consultant from his/her respective retirement board. Also, all legal matters should be discussed with an attorney and financial matters with a financial planner. The information presented is general in nature. The presenter assumes no obligations for failure to verify information at the time participant is retiring.

Part 1

Pension Reform III

Recent changes in pension law: “Pension Reform III”

“Pension Reform and Benefit Modernization,” Chapter 176 of the Acts of 2011, signed Nov. 18, 2011

• A complex and wide-reaching new law • Requires substantial changes to our internal computer

applications, and informational and educational materials • MTRS now working to develop the necessary policies and

procedures to implement these changes as quickly and smoothly as possible

• Watch for updates to employers and members in coming months

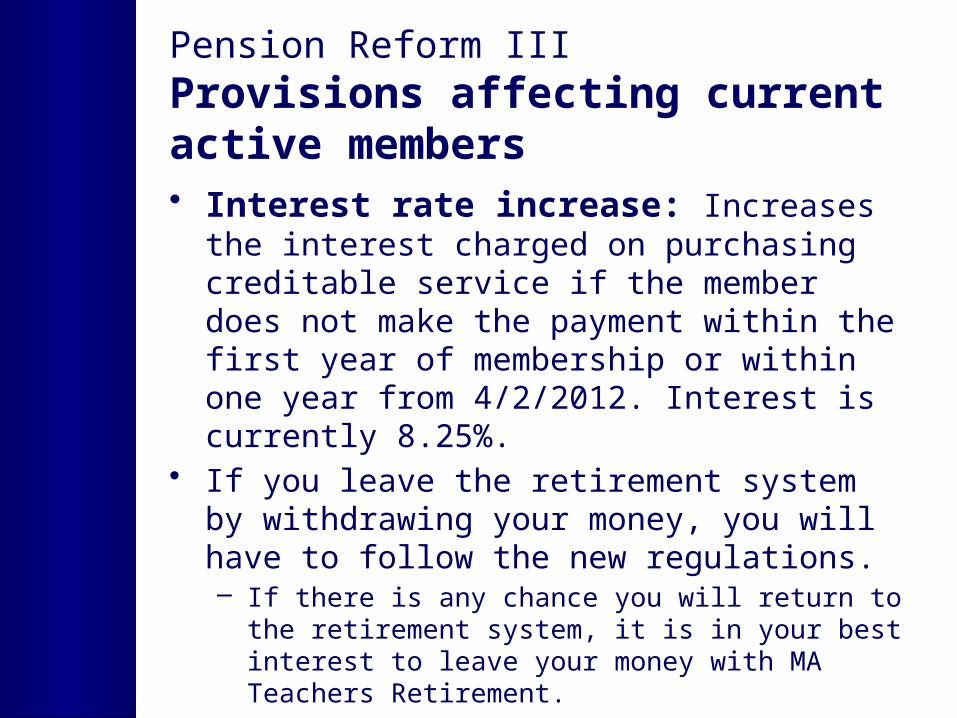

Pension Reform III Provisions affecting current active members• Interest rate increase: Increases the interest

charged on purchasing creditable service if the member does not make the payment within the first year of membership or within one year from 4/2/2012. Interest is currently 8.25%.

• If you leave the retirement system by withdrawing your money, you will have to follow the new regulations.– If there is any chance you will return to the retirement

system, it is in your best interest to leave your money with MA Teachers Retirement.

Pension Reform III Provisions affecting new members(those who enroll in a Massachusetts public retirement system, or re-enroll after taking a refund, on or after April 2, 2012)

• Overall retirement benefits reduced • Minimum retirement age is now 60 • Age factors reduced • Lengthens the salary average period used in the

retirement benefit calculation formula to 5 years • Reduces the contribution rate by 3% (e.g., from

11% to 8%) once a member has 30 years of creditable service

• Begins the additional 2% Retirement Plus add-on after the 23rd year of creditable service instead of the 24th year of creditable service

Part 2

Benefits,

creditable service

and resources

for MTRS members

Retirement Benefits

1)“Regular” • Any age, with 20 years of creditable

service, OR • Age 55 with 10 years of creditable service

…and…

Retirement Benefits

2) RetirementPlus • Any age, with 30 years of creditable

service, at least 20 years of which must be “teaching” service with the MTRS or Boston Retirement System

• Enhanced benefit: Additional 2% add on after 24th year of creditable service (upon reaching 30 years)

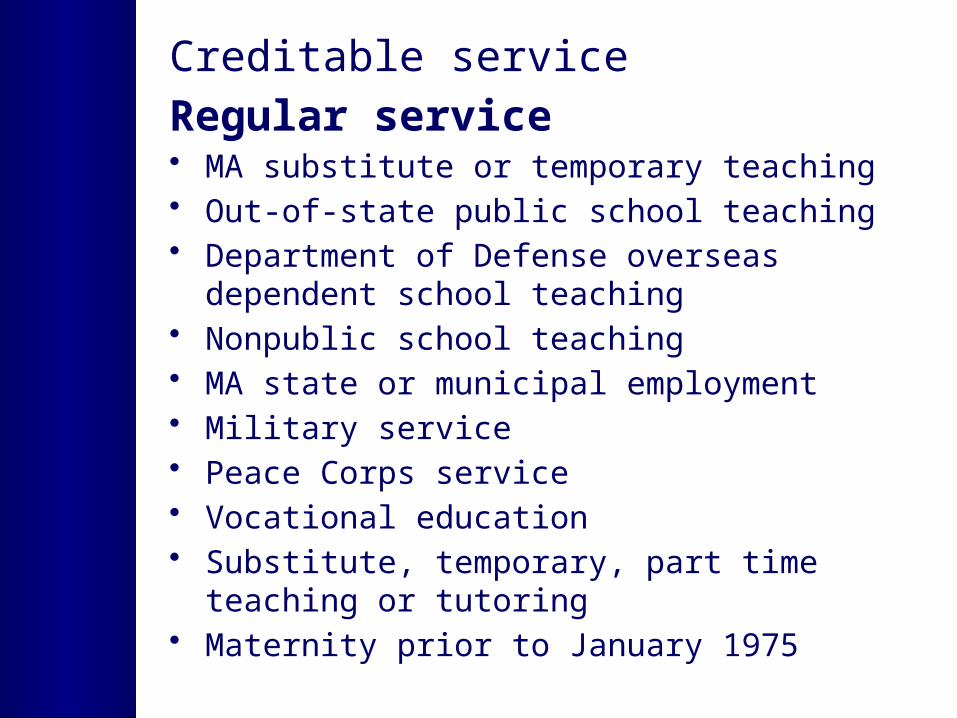

Creditable service

Regular service • MA substitute or temporary teaching • Out-of-state public school teaching • Department of Defense overseas dependent

school teaching • Nonpublic school teaching • MA state or municipal employment • Military service • Peace Corps service • Vocational education • Substitute, temporary, part time teaching or

tutoring• Maternity prior to January 1975

Creditable Service

• All Creditable Service must be purchased prior to effective date of retirement.

• Part of a year counts.• All forms may be downloaded from the MTRS

website (www.mass.gov/mtrs) or can be obtained by calling them at

• 1-617-679-6877 or 1-413-784-1711• MA Teachers' Retirement System

– 1 Charles Park, 2nd Floor– Cambridge, MA 02142-1254

Forms MTRS Provide

• Option Selection Form• Group Health Insurance• Federal Tax Withholding• Direct Deposit

Age Factor

• PART OF A YEAR DOES NOT COUNT HERE. Age as of last birthday. If you retire on your birthday, you are able to use that age factor.

• USE 1 BEFORE A DECIMAL POINT IF IN 50’S --2 IN FRONT OF DECIMAL POINT IF IN 60’s. Whatever the number is after the decimal point is the second number of your age.

Age Factors

• 1.0 = 50• 1.1 = 51• 1.2 = 52• 1.3 = 53• 1.4 = 54• 1.5 = 55• 1.6 = 56• 1.7 = 57

• 1.8 = 58• 1.9 = 59• 2.0 = 60• 2.1 = 61• 2.2 = 62• 2.3 = 63• 2.4 = 64• 2.5 = 65

65 is the largest age factor a person may use

New Age Factor for those hired after 4/2/12

With at least 30 years of service at time of retirement

2.50 67 or older 62 or older 57 or older

2.35 66 61 56 2.20 65 60 55 2.05 64 59 54 1.90 63 58 53 1.75 62 57 52 1.60 61 56 51 1.45 60 55 50

2.50 67 or older 62 or older 57 or older

2.375 66 61 56 2.250 65 60 55 2.125 64 59 54 2.0 63 58 53 1.875 62 57 52 1.750 61 56 51 1.625 60 55 50

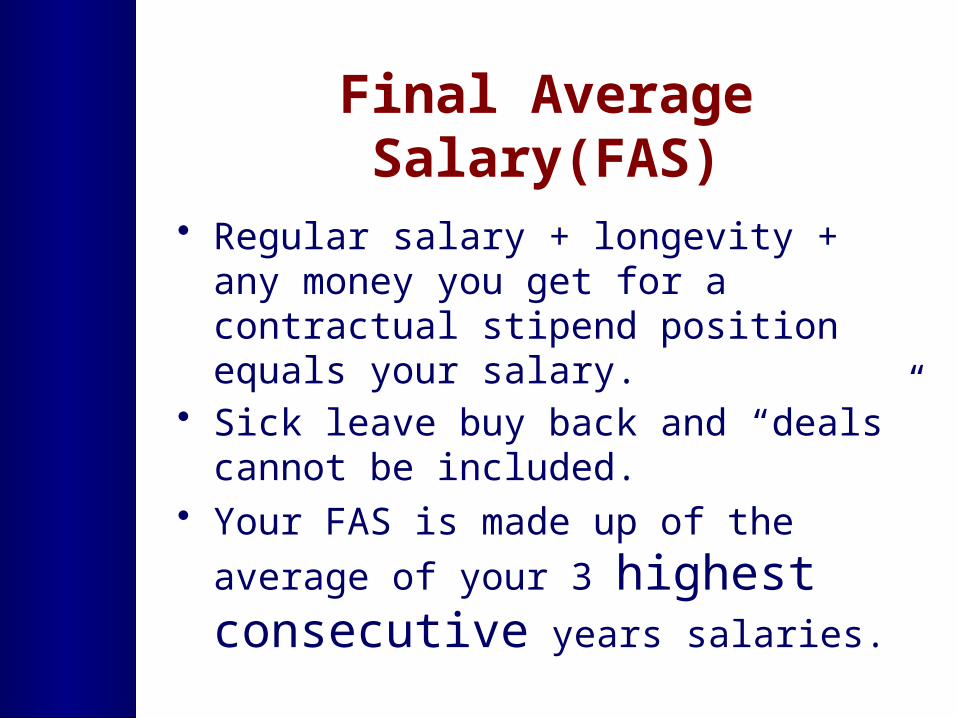

Final Average Salary(FAS)

• Regular salary + longevity + any money you get for a contractual stipend position equals your salary.

• Sick leave buy back and “deals” cannot be included.

• Your FAS is made up of the average of

your 3 highest consecutive years salaries.

Retirement Plus

• You add 2% for each year above 25 years but cannot count until 30 Y/S

• 30 Y= 12% 31 Y= 14% 32 Y= 16%

• 33 Y= 18% 34 Y= 20% 35 Y= 22%

• Two percent applied only to the whole number of your creditable service, not part of the year.

Formula for Option A• Person 56 years old • 34.3 years of service • Final Average Salary (FAS) = $56,787

• Age Factor X Yrs of Service = % of Salary1.6 X 34.3 = 54.88%(add 20% R+ factor = 74.88%)

• FAS X % of Salary = Annual Pension $56,787 X 74.88% = $42,522

For illustrative purposes only

Options

• There are 3 options: A, B, C

• Must submit Option Selection Form with your Application to Retire Form

• Irrevocable decision once effective date of retirement occurs

Understanding the Three Pension Options: A, B, C

• Option A-– Highest payout available

– For your lifetime only

– Payout ends when you die

– No beneficiary benefits

Option B

• 1-2% less than option A income for member

• Anyone can be your beneficiary• When you die, balance of your fund goes

to beneficiary• Account depletes itself in 10-11 years

Option C

• Lowest possible payout – approx. 9-11% less than Option A amount

• Provides survivor benefit equal to 2/3 of Option C

• Beneficiary must be parent, spouse, sibling, child, ex-spouse who has not remarried or a same sex marriage partner

• Pop-up provision available

Case Study• Your age: 60• Your Age Factor: 2.0• Final Average Salary: $60,000• Years of Service: 35• Retirement Plus Percentage: 22%• Beneficiary’s age: 59

• Option A Option B Option C$48,000 $47,520 $43,680Dies with you Any remaining $29,119

to beneficiary to survivor

($4,320 difference)

For illustrative purposes only

Which Option Should You Choose:

• Factors to consider:– Your Age– Your beneficiary’s age– Health of you and your Beneficiary – Is ability to change your beneficiary

important? – Cost differential between Options A and C

Pension Max

• Must be insurable

• Different types of insurance:– Term– Universal Life– Variable Life– Whole Life

$50,000 Pension

5 Yrs 10 Yrs 15 Yrs 20 Yrs 25 Yrs

Actual Pension

$51, 900 $53,900 $55,850 $57,800 $59,750w/ COLA

Income needed

$56,275 $65,236 $75,624 $87,666 $101,626 w/ 3%

inflation

Income needed

$60,775 $77,563 $98,990 $126,336 $161,238 w/ 5%

inflation

For illustrative purposes only.

COLACost of Living Adjustment

• Issued annually if voted on by Legislature

• If retired on June 30, 2011, eligible July of 2012

COLA Based On:

• 1971-------$6,000• 1981-------$7,000• 1985-------$8,000• 1986-------$9,000• 1997-------$12,000• 2012-------$13,000• MRU working to increase this base

to $16,000

Social Security

• Need 40 units for eligibility

• Receive Earning and Benefits Statement2 months before your birthday

• No matter what Social Security may tell you prior to your actually filing you will be penalized by the WEP/GPO unless:

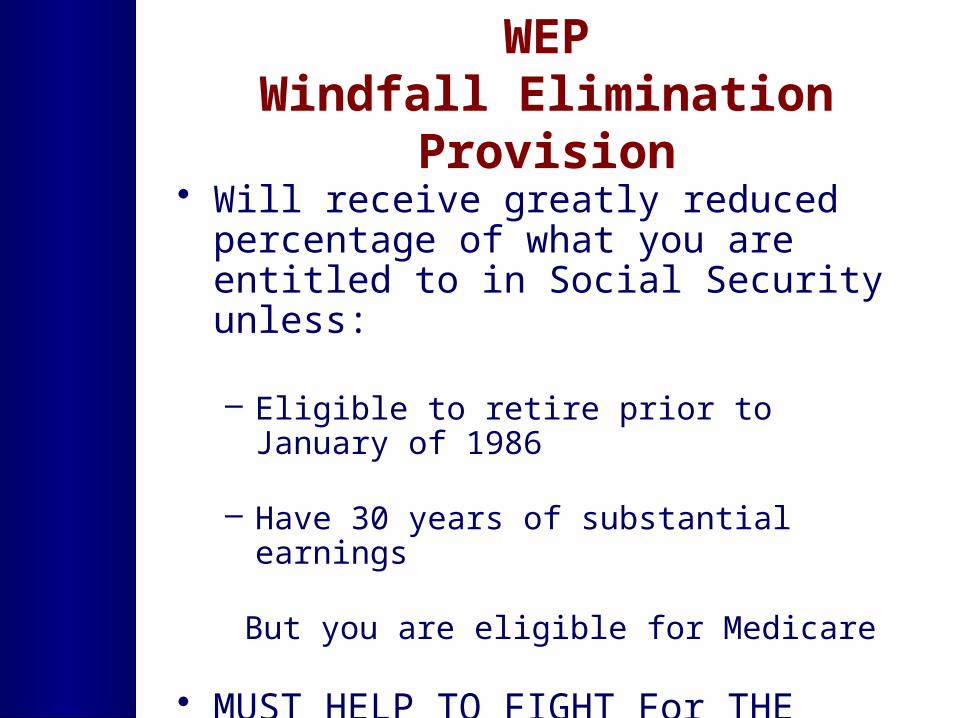

WEPWindfall Elimination Provision

• Will receive greatly reduced percentage of what you are entitled to in Social Security unless:

– Eligible to retire prior to January of 1986

– Have 30 years of substantial earnings

But you are eligible for Medicare

• MUST HELP TO FIGHT For THE REPEAL OF THE WEP/GPO