Embed Size (px)

Citation preview

Effect of Liberalization on Banking Competition

Gloria O. Pasadilla

Melanie S. Milo

27 June 2005

Philippine Institute for Development Studies

07/20/2005 Slide # 2Pasadilla-Milo

THE PROBLEM

GENERAL:

SPECIFIC:

1. evaluate impacts of reforms on concentration

2. evaluate impacts of profitability and margins

3. measure actual degree of competition: H-stat

assess the effects of competition policy reforms on bank competition

07/20/2005 Slide # 3Pasadilla-Milo

THE CONTEXTMajor reforms in 1990s

• Easing of restrictions on domestic bank entry and branching

• Foreign Entry (RA No. 7721)• Consolidation trend • Asian crisis

07/20/2005 Slide # 4Pasadilla-Milo

THE CONTEXTPast findings

• Foreign entry leads to:• greater efficiency • reduced interest margins• improved competitiveness• reduced profits

• Market concentration is positively (negatively) associated with profits (efficiency)

07/20/2005 Slide # 5Pasadilla-Milo

Effect on the Number of Banks

0

10

20

30

40

50

60

1985 1995 1996 1997 1998 1999 2000 2001 2002 2003

Total banks Foreign banks

8 domestic, 10 foreign

banks entered

6 bank mergers

07/20/2005 Slide # 6Pasadilla-Milo

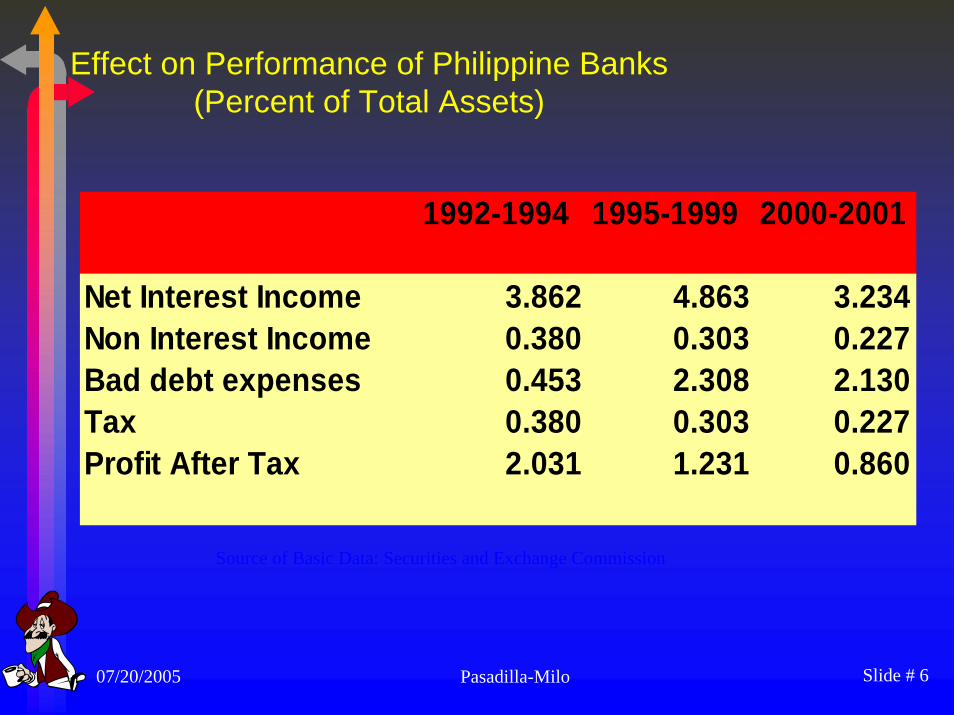

Effect on Performance of Philippine Banks(Percent of Total Assets)

Source of Basic Data: Securities and Exchange Commission

1992-1994 1995-1999 2000-2001

Net Interest Income 3.862 4.863 3.234Non Interest Income 0.380 0.303 0.227Bad debt expenses 0.453 2.308 2.130Tax 0.380 0.303 0.227Profit After Tax 2.031 1.231 0.860

07/20/2005 Slide # 7Pasadilla-Milo

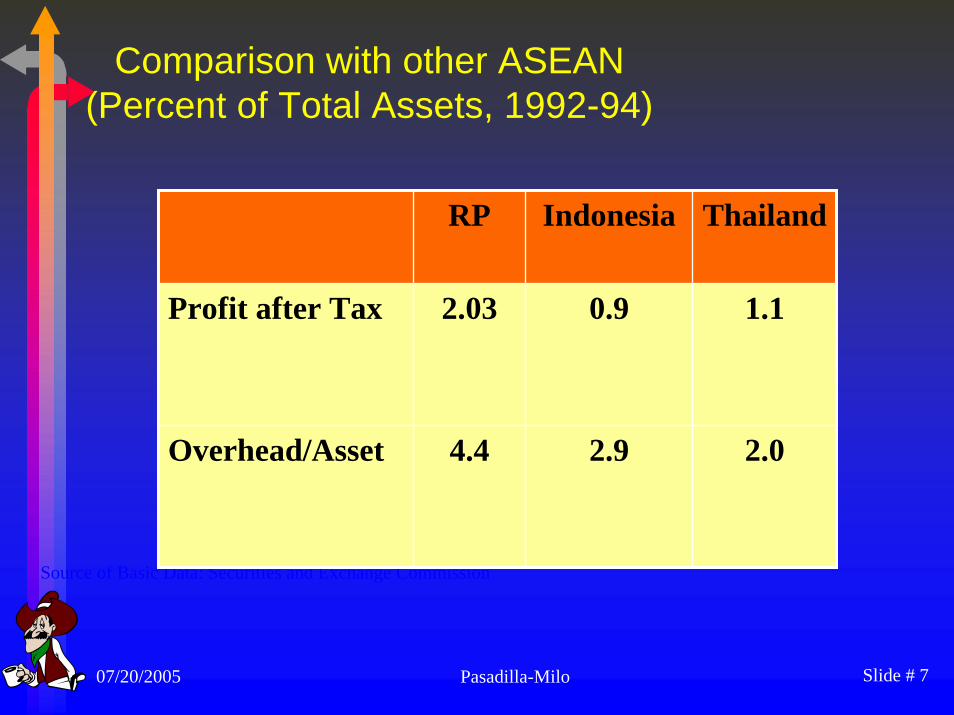

Comparison with other ASEAN(Percent of Total Assets, 1992-94)

Source of Basic Data: Securities and Exchange Commission

RP Indonesia Thailand

Profit after Tax 2.03 0.9 1.1

Overhead/Asset 4.4 2.9 2.0

07/20/2005 Slide # 8Pasadilla-Milo

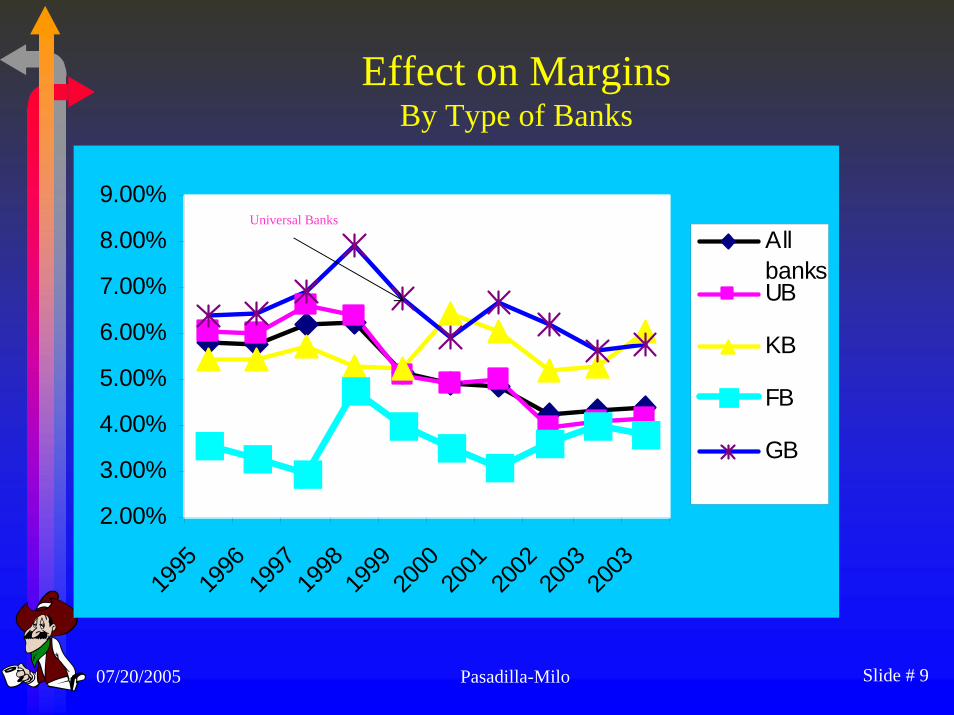

Effect on MarginsBank Average Lending Rates, Savings and Short-term Deposit Rates and Bank

Interest Spread

Bank Average Short-TermYEAR Lending Rate2 Savings1 Time Deposits

(1) (2) (3) (1-2) (1-3)

1990-94 19.36 9.73 14.67 9.63 4.691995-97 15.25 8.37 10.53 6.88 4.721998-99 15.07 9.14 10.92 5.93 4.162000-03 10.41 5.82 6.94 4.59 3.47

Bank Spread

Source: BSP SPEI, BSP Statistics online.

07/20/2005 Slide # 9Pasadilla-Milo

Effect on MarginsBy Type of Banks

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2003

AllbanksUB

KB

FB

GB

Universal Banks

07/20/2005 Slide # 10Pasadilla-Milo

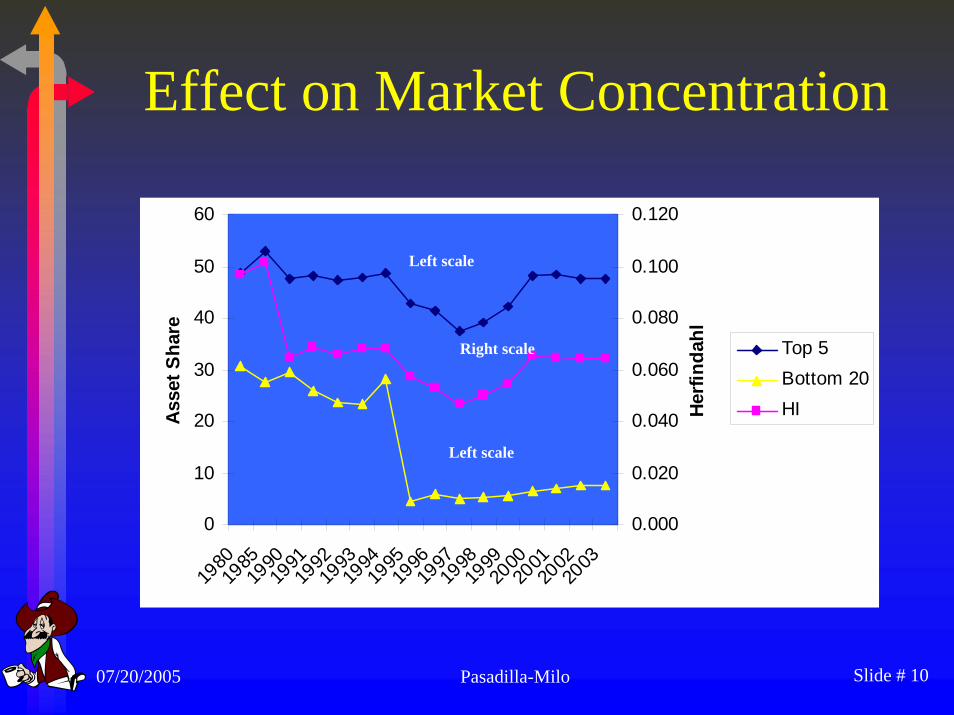

Effect on Market Concentration

0

10

20

30

40

50

60

1980

1985

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Ass

et S

hare

0.000

0.020

0.040

0.060

0.080

0.100

0.120

Herfi

ndah

l

Top 5Bottom 20HI

Left scale

Left scale

Right scale

07/20/2005 Slide # 11Pasadilla-Milo

Measuring Competitiveness- Problems with other methods

• margins – affected by many other factors• no exact benchmark for competitive returns

- Alternative Method- Structural or contestability approach e.g. Panzar-Rosse Method

07/20/2005 Slide # 12Pasadilla-Milo

Contestability Literature – short excursion

- S-C-P Paradigm does not always hold

• threat of entry can enforce competition despite degree of concentration

- e.g. US and Canadian Banking market

• conversely, collusive action can exist even when there are many firms

- e.g. small banks in EU countries

07/20/2005 Slide # 13Pasadilla-Milo

Contestability Literature – short excursion

- No definitive relationship between market concentration and degree of competition

• Some found evidence that concentration impairs competitiveness (Bikker and Haaf, 2001)

• degree of competition unrelated to market structure. Contestability and market openness affects competition more (Claessens and Laeven, 2003).

07/20/2005 Slide # 14Pasadilla-Milo

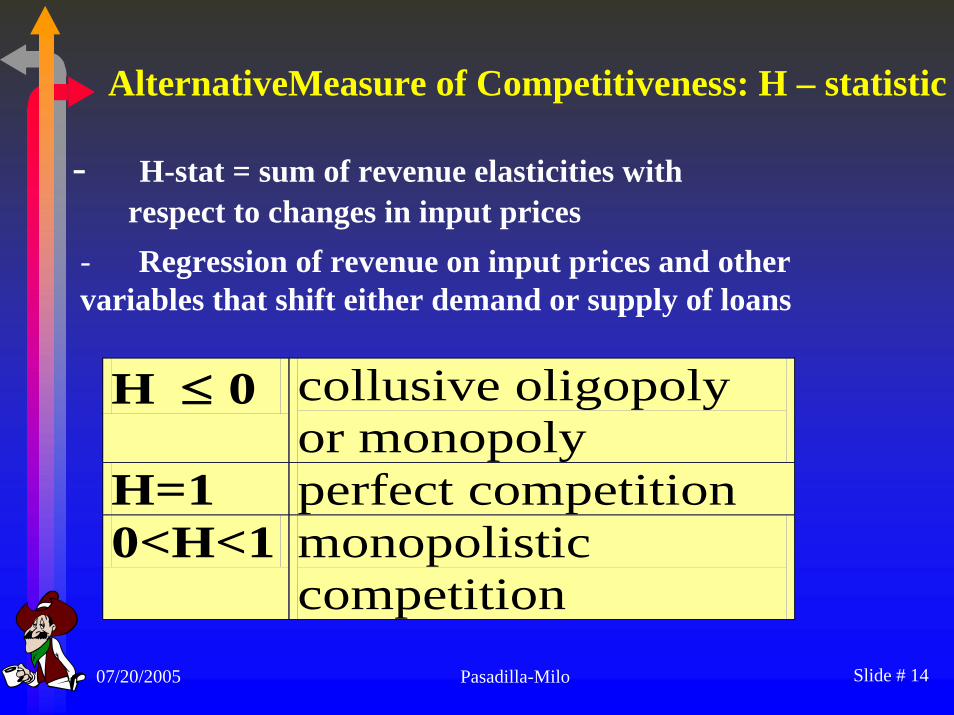

AlternativeMeasure of Competitiveness: H – statistic

- H-stat = sum of revenue elasticities with respect to changes in input prices

H ≤ 0 collusive oligopoly or monopoly

H=1 perfect competition 0<H<1 monopolistic

competition

- Regression of revenue on input prices and other variables that shift either demand or supply of loans

07/20/2005 Slide # 15Pasadilla-Milo

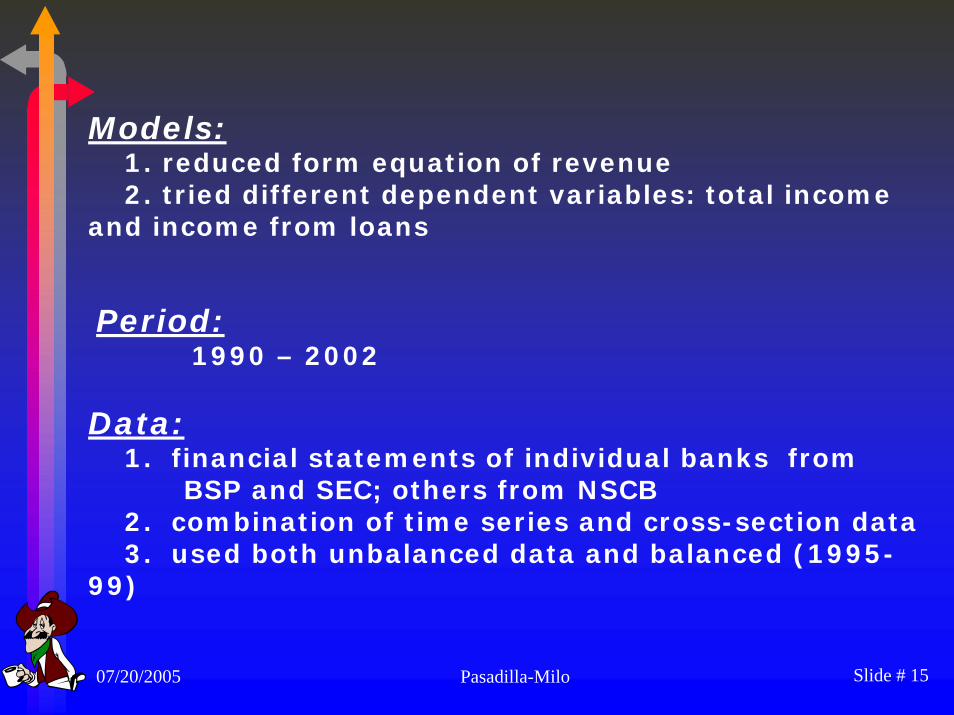

Period:1990 – 2002

Data: 1. financial statements of individual banks from

BSP and SEC; others from NSCB2. combination of time series and cross-section data3. used both unbalanced data and balanced (1995-

99)

Models:1. reduced form equation of revenue 2. tried different dependent variables: total income

and income from loans

07/20/2005 Slide # 16Pasadilla-Milo

MAJOR FINDINGS

1. Banking sector is fairly competitive

2. Competition in Loans business is more intensethan fee generating business

07/20/2005 Slide # 17Pasadilla-Milo

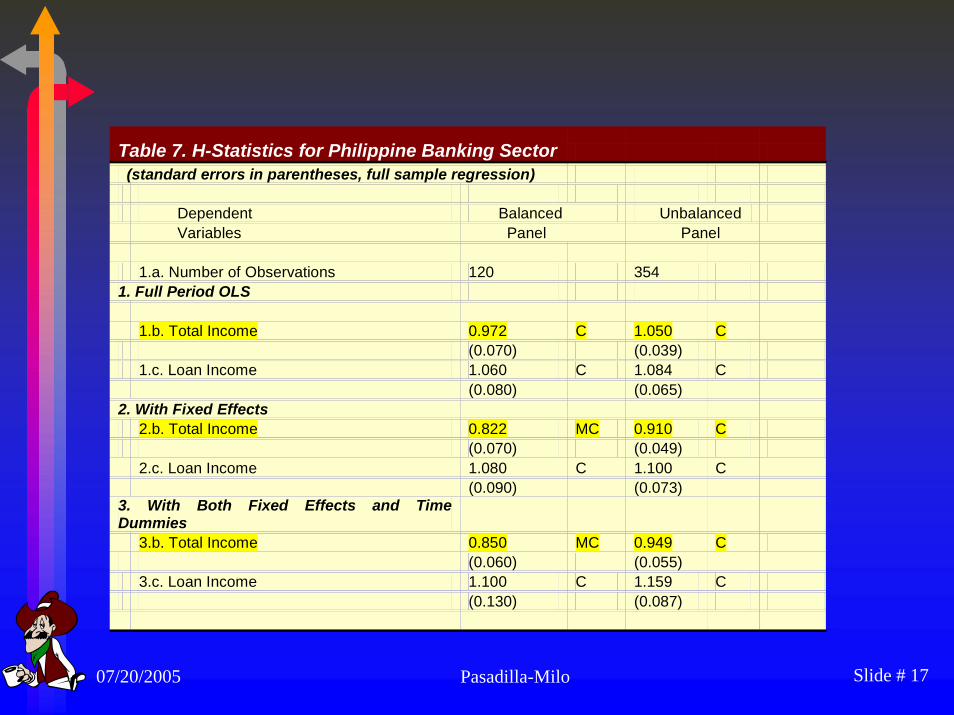

Table 7. H-Statistics for Philippine Banking Sector (standard errors in parentheses, full sample regression) Dependent Balanced Unbalanced Variables Panel Panel 1.a. Number of Observations 120 354 1. Full Period OLS 1.b. Total Income 0.972 C 1.050 C (0.070) (0.039) 1.c. Loan Income 1.060 C 1.084 C (0.080) (0.065) 2. With Fixed Effects 2.b. Total Income 0.822 MC 0.910 C (0.070) (0.049) 2.c. Loan Income 1.080 C 1.100 C (0.090) (0.073) 3. With Both Fixed Effects and Time Dummies 3.b. Total Income 0.850 MC 0.949 C (0.060) (0.055) 3.c. Loan Income 1.100 C 1.159 C (0.130) (0.087)

07/20/2005 Slide # 18Pasadilla-Milo

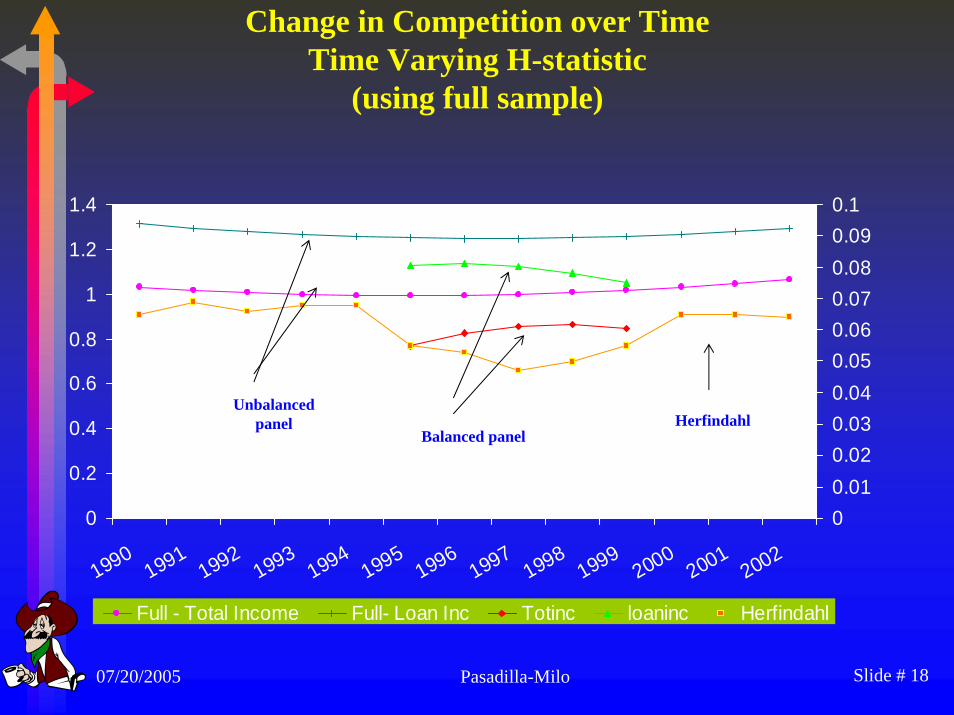

Change in Competition over TimeTime Varying H-statistic

(using full sample)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

19901991

19921993

19941995

19961997

19981999

20002001

2002

00.010.020.030.040.050.060.070.080.090.1

Full - Total Income Full- Loan Inc Totinc loaninc Herfindahl

HerfindahlBalanced panel

Unbalanced panel

07/20/2005 Slide # 19Pasadilla-Milo

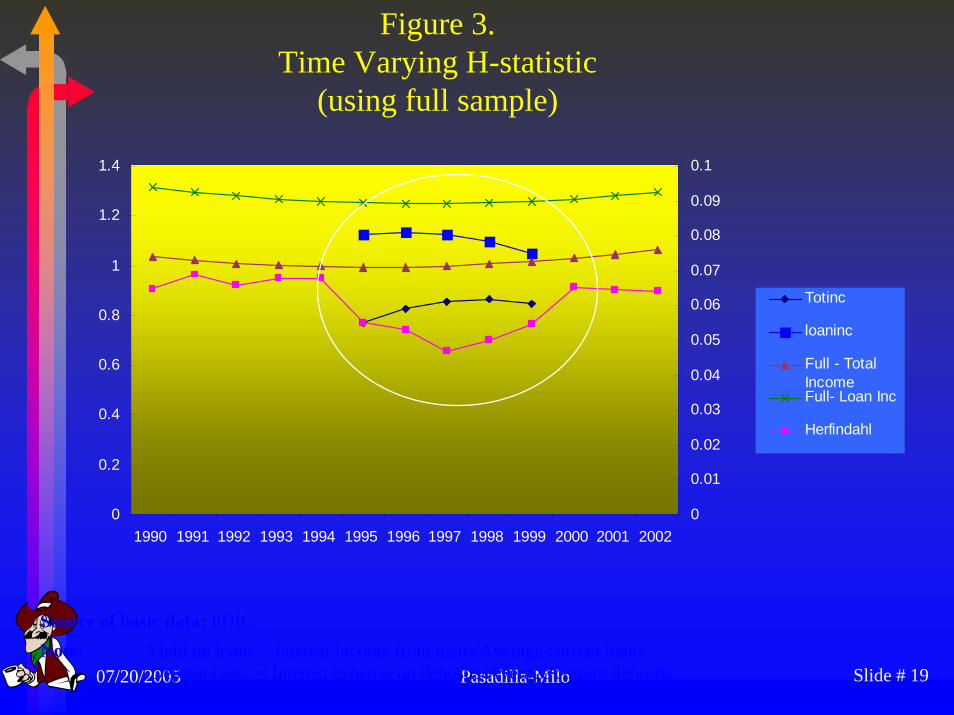

Figure 3.Time Varying H-statistic

(using full sample)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 20020

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.1

Totinc

loaninc

Full - TotalIncomeFull- Loan Inc

Herfindahl

Source of basic data: PDIC.Note: a Yield on loans = Interest income from loans/Average current loans

Deposit cost = Interest expense on deposits/Average current deposits

07/20/2005 Slide # 20Pasadilla-Milo

MAJOR FINDINGS

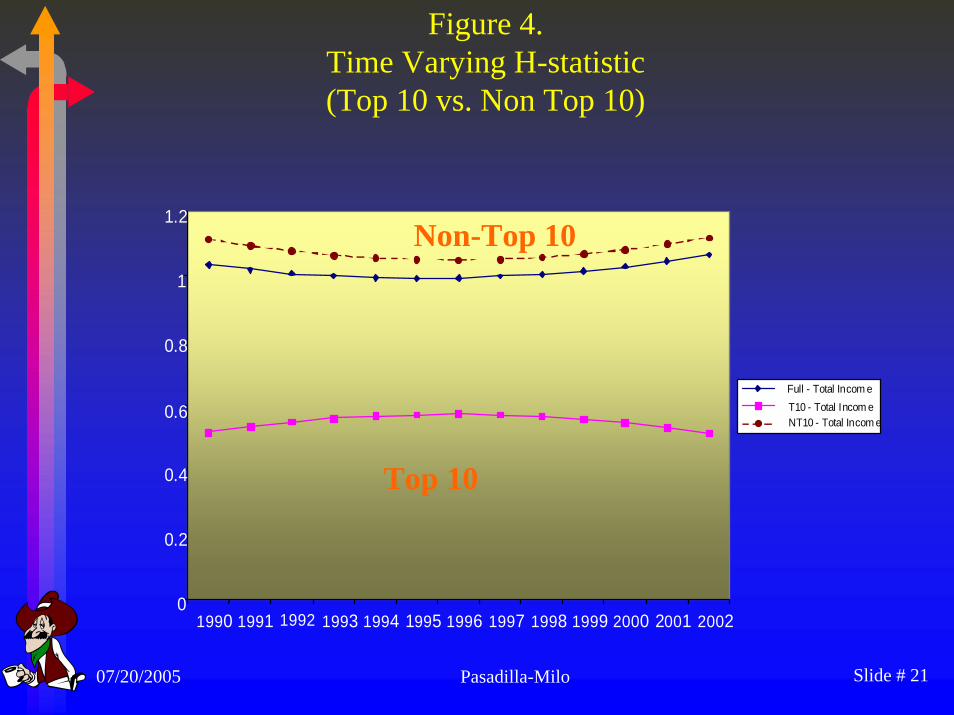

3. Increase in competition among small banks and decrease in competition among big banks

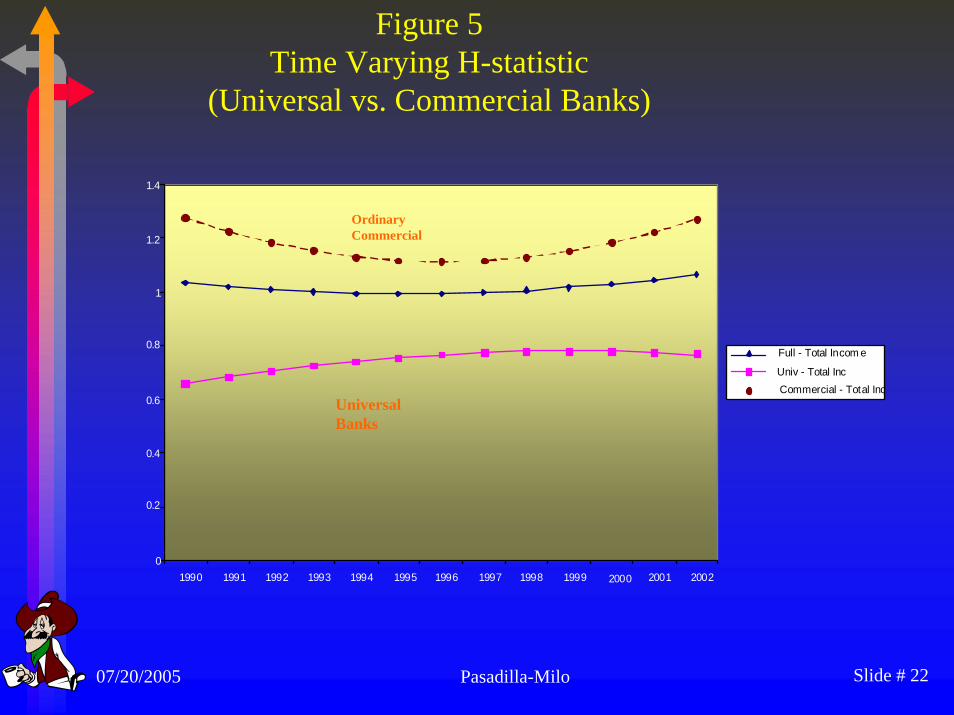

4. Increase in competition among commercial banks and decrease in competition among universal banks

5. Increase in competition among merged banks

07/20/2005 Slide # 21Pasadilla-Milo

Figure 4.Time Varying H-statistic(Top 10 vs. Non Top 10)

0

0.2

0.4

0.6

0.8

1

1.2

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Full - Total Incom e T10 - Total Incom e NT10 - Total Incom e

Top 10

Non-Top 10

07/20/2005 Slide # 22Pasadilla-Milo

Figure 5Time Varying H-statistic

(Universal vs. Commercial Banks)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Full - Total Incom e Univ - Total Inc Commercial - Total Inc

UniversalBanks

Ordinary Commercial

07/20/2005 Slide # 23Pasadilla-Milo

Figure 6Time Varying H-statistic

(Merged vs. Not Merged Banks)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Full - Total Incom e Merged - Total Inc Not - Total Inc

Merged Banks

Non-Merged Banks

07/20/2005 Slide # 24Pasadilla-Milo

Summary

Herfindahl index points to no undue concentration

Sector characterized by few large banks and many smallbanks on the fringe

Entry of more market players are correlated with drop in interest spread and profit, possibly due to dissipation of previous monopoly profits

07/20/2005 Slide # 25Pasadilla-Milo

Summary

H-stat disclose no monopoly or collusive behavior. Fairly competitive environment exists.

Trend shows increased banking competition in latter 1990s. Competition is more intense in loan business than in fee-generating services.

Big banks show competition decline and are more monopolisticcompetitors, small banks are more competitive. Much of the increase in competition was due to presence of small banks

07/20/2005 Slide # 26Pasadilla-Milo

PIDS Research Papers can be downloaded at:

www.pids.gov.ph