Embed Size (px)

Citation preview

Edexcel Level 4 Diploma in Accounting (QCF)

Specification

Edexcel NVQ/competence-based qualifications For first registration 1 March 2012

Pearson Education Ltd is one of the UK’s largest awarding organisations, offering academic and vocational qualifications and testing to schools, colleges, employers and other places of learning, both in the UK and internationally. Qualifications offered include GCSE, AS and A Level, NVQ and our BTEC suite of vocational qualifications, ranging from Entry Level to BTEC Higher National Diplomas. Pearson Education Ltd administers Edexcel GCSE examinations.

Through initiatives such as onscreen marking and administration, Pearson is leading the way in using technology to modernise educational assessment, and to support teachers and learners.

References to third-party material made in this specification are made in good faith. We do not endorse, approve or accept responsibility for the content of materials, which may be subject to change, or any opinions expressed therein. (Material may include textbooks, journals, magazines and other publications and websites.)

Authorised by Martin Stretton Prepared by Roger Field

Publications code N031199

All the material in this publication is copyright © Pearson Education Limited 2012

Contents

Qualification title covered by this specification 1

Key features of the Edexcel Level 4 Diploma in Accounting (QCF) 2

What is the purpose of this qualification? 2

Who is this qualification for? 2

What are the benefits of this qualification to the learner and employer? 2

What are the potential job roles for those working towards this qualification? 3

What progression opportunities are available to learners who achieve this qualification? 3

What is the qualification structure for the Edexcel Level 4 Diploma in Accounting (QCF)? 4

Qualification structure 4

How is the qualification graded and assessed? 5

Assessment strategy 5

Types of evidence 6

Centre recognition and approval 7

Centre recognition 7

Approvals agreement 7

Quality assurance 7

What resources are required? 7

Unit format 8

Units 9

Unit 1: Principles of drafting financial statements 11

Unit 2: Drafting financial statements 15

Unit 3: Principles of budgeting 19

Unit 4: Drafting budgets 23

Unit 5: Principles of managing financial performance 27

Unit 6: Measuring financial performance 31

Unit 7: Principles of internal control 35

Unit 8: Evaluating accounting systems 39

Unit 9: Principles of credit management 43

Unit 10: Control of debt and credit 47

Unit 11: Principles of personal tax 51

Unit 12: Calculating personal tax 55

Unit 13: Principles of business tax 59

Unit 14: Calculating business tax 63

Unit 15: Principles of external audit 67

Unit 16: Auditing financial statements 71

Further information 75

Useful publications 75

How to obtain National Occupational Standards 75

Professional development and training 76

Annexe A: Progression pathways 77

Selected Edexcel qualifications available in accounting and finance 77

Annexe B: Quality assurance 79

Key principles of quality assurance 79

Quality assurance processes 79

Annexe C: Centre certification and registration 81

What are the access arrangements and special considerations for the qualifications in this specification? 81

Annexe D: Assessment strategy 83

Introduction and scope 83

A: Teaching and assessment 83

B: Workplace assessment and simulation 84

C: Quality assurance and quality control 84

D: Competence of assessors and verifiers 84

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

1

Qual

ific

atio

n t

itle

cov

ered

by

this

spec

ific

atio

n

This

spec

ific

atio

n g

ives

you t

he

info

rmation y

ou n

eed t

o o

ffer

the

Edex

cel Le

vel 4 D

iplo

ma in A

ccounting (

QCF)

:

Qu

alifi

cati

on

tit

le

Qu

alifi

cati

on

N

um

ber

(QN

) A

ccre

dit

ati

on

st

art

date

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

600/4

723/9

01/0

3/2

012

This

qual

ific

atio

n h

as

bee

n a

ppro

ved w

ithin

the

Qual

ific

ations

and C

redit F

ram

ework

(Q

CF)

and is

elig

ible

for

public

fundin

g a

s det

erm

ined

by

the

Dep

artm

ent

for

Educa

tion (

DfE

) under

Sec

tion 9

6 o

f th

e Le

arnin

g a

nd S

kills

Act

2000.

The

qual

ific

atio

n t

itle

lis

ted a

bove

fea

ture

s in

the

fundin

g lis

ts p

ublis

hed

annual

ly b

y th

e D

fE a

nd t

he

regula

rly

updat

ed w

ebsi

te.

It w

ill a

lso a

ppea

r on t

he

Learn

ing A

ims

Ref

eren

ce A

pplic

atio

n (

LARA),

wher

e re

leva

nt.

You s

hould

use

the

QCF

Qualif

icat

ion N

um

ber

(Q

N)

when

you w

ish t

o s

eek

public

fundin

g f

or

your

lear

ner

s. E

ach

unit w

ithin

a

qual

ific

ation w

ill a

lso h

ave

a u

niq

ue

QC

F unit r

efer

ence

num

ber

, w

hic

h a

re lis

ted in t

his

spec

ific

atio

n.

The

QCF

qual

ific

atio

n t

itle

and u

nit r

efer

ence

num

ber

s w

ill a

ppea

r on t

he

lear

ner

s’ f

inal

cer

tifica

tion d

ocu

men

ts.

Lear

ner

s nee

d t

o

be

made

aw

are

of th

is w

hen

they

are

rec

ruited

by

the

centr

e an

d r

egis

tere

d w

ith E

dex

cel.

For

furt

her

info

rmat

ion o

n t

he

fundin

g o

f 14-1

9 q

ual

ific

atio

ns

off

ered

in E

ngla

nd,

ple

ase

ref

er t

o t

he

DfE

Sec

tion 9

6 w

ebsi

te.

For

furt

her

info

rmat

ion o

n t

he

fundin

g o

f 19+

qualif

icat

ions

off

ered

in E

ngla

nd,

ple

ase

ref

er t

o t

he

SFA

web

site

.

For

furt

her

info

rmat

ion o

n f

undin

g in W

ales

, vi

sit

the

DAQ

W w

ebsi

te.

For

furt

her

info

rmat

ion o

n f

undin

g in N

ort

her

n I

rela

nd,

visi

t th

e D

ELN

I and D

EN

I w

ebsi

te.

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

2

Key features of the Edexcel Level 4 Diploma in Accounting (QCF)

This qualification:

is nationally recognised

is based on the National Occupational Standards (NOS) for Accounting.

Edexcel expects that the Edexcel Level 4 Diploma in Accounting will be approved as a component required for the Higher Apprenticeship in Accounting.

What is the purpose of this qualification?

This qualification is designed to recognise occupational competence in accounting at level 4 and thus provide opportunities for career and educational progression.

Who is this qualification for?

This qualification has been developed for those working, or wishing to work, in accounting. It is intended to provide progression from the Edexcel Level 3 Diploma in Accounting, allowing learners to further develop their accounting skills.

This qualification is for all learners aged 16 and above who are capable of reaching the required standards.

Edexcel’s policy is that its qualifications should:

be free from any barriers that restrict access and progression

ensure equality of opportunity for all wishing to access them.

What are the benefits of this qualification to the learner and employer?

For learners, the benefits of this qualification are that it:

allows them to develop skills that will be useful to them in their day-to-day job role

confirms their occupational competence, thus enhancing their employability

motivates them by giving the opportunity to gain a nationally-recognised level 4 qualification that demonstrates ongoing professional development.

For employers, the benefits of this qualification are that it:

helps identify training needs by benchmarking best practice

motivates staff to perform at a high standard, resulting in better customer satisfaction and improved staff retention

allows for increased confidence in the performance of staff who have achieved the qualification.

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

3

What are the potential job roles for those working towards this qualification?

Accounting technician – duties may include overall strategic responsibility for an accounts payable and receivable department, with wider credit management and people management duties.

Accounts manager – duties may include controlling budgets, assisting with the preparation of accounts and writing reports.

What progression opportunities are available to learners who achieve this qualification?

Learners who have successfully completed this qualification can progress on to foundation degrees in Accounting, and also to qualifications for chartered accountants.

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

4

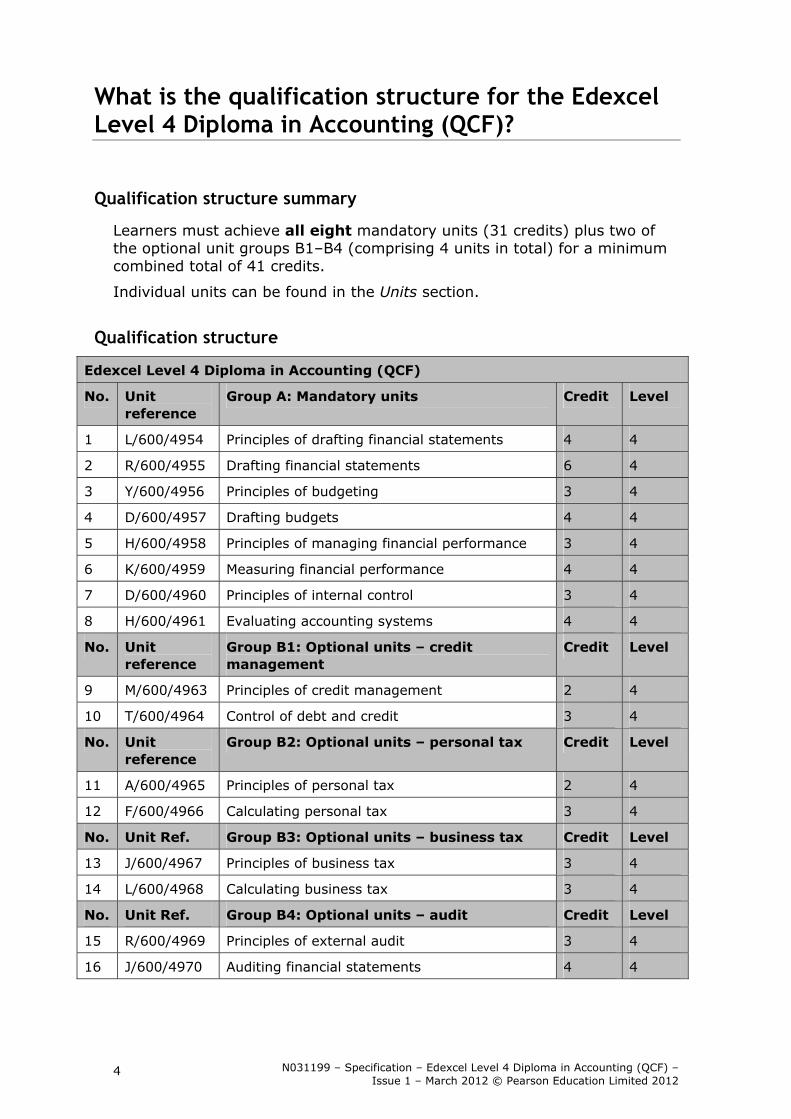

What is the qualification structure for the Edexcel Level 4 Diploma in Accounting (QCF)?

Qualification structure summary

Learners must achieve all eight mandatory units (31 credits) plus two of the optional unit groups B1–B4 (comprising 4 units in total) for a minimum combined total of 41 credits.

Individual units can be found in the Units section.

Qualification structure

Edexcel Level 4 Diploma in Accounting (QCF)

No. Unit reference

Group A: Mandatory units Credit Level

1 L/600/4954 Principles of drafting financial statements 4 4

2 R/600/4955 Drafting financial statements 6 4

3 Y/600/4956 Principles of budgeting 3 4

4 D/600/4957 Drafting budgets 4 4

5 H/600/4958 Principles of managing financial performance 3 4

6 K/600/4959 Measuring financial performance 4 4

7 D/600/4960 Principles of internal control 3 4

8 H/600/4961 Evaluating accounting systems 4 4

No. Unit reference

Group B1: Optional units – credit management

Credit Level

9 M/600/4963 Principles of credit management 2 4

10 T/600/4964 Control of debt and credit 3 4

No. Unit reference

Group B2: Optional units – personal tax Credit Level

11 A/600/4965 Principles of personal tax 2 4

12 F/600/4966 Calculating personal tax 3 4

No. Unit Ref. Group B3: Optional units – business tax Credit Level

13 J/600/4967 Principles of business tax 3 4

14 L/600/4968 Calculating business tax 3 4

No. Unit Ref. Group B4: Optional units – audit Credit Level

15 R/600/4969 Principles of external audit 3 4

16 J/600/4970 Auditing financial statements 4 4

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

5

How is the qualification graded and assessed?

The overall grade for this qualification is a ‘pass’. The learner must achieve all the required units within the specified qualification structure.

To pass a unit the learner must:

achieve all the specified learning outcomes

satisfy all the assessment criteria by providing sufficient and valid evidence for each criterion

show that the evidence is their own.

The qualification is designed to be assessed:

in the workplace or

in conditions resembling the workplace, as specified in the assessment strategy for the sector.

Assessment strategy

The assessment strategy for this qualification can be found in Annexe D. This includes details on:

teaching and assessment strategies

workplace assessment and simulation

quality control of assessment

competence of assessors and verifiers.

Evidence of competence may come from:

current practice where evidence is generated from a current job role

a programme of development where evidence comes from assessment opportunities built into a learning/training programme whether at or away from the workplace

the Recognition of Prior Learning (RPL) where a learner can demonstrate that they can meet the assessment criteria within a unit through knowledge, understanding or skills they already possess without undertaking a course of learning. They must submit sufficient, reliable and valid evidence for internal and standards verification purposes. RPL is acceptable for accrediting a unit, several units or a whole qualification

a combination of these.

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

6

It is important that the evidence is:

Valid relevant to the standards for which competence is claimed

Authentic produced by the learner

Current sufficiently recent to create confidence that the same skill, understanding or knowledge persist at the time of the claim

Reliable indicates that the learner can consistently perform at this level

Sufficient fully meets the requirements of the standards.

Types of evidence

To successfully achieve a unit, the learner must gather evidence which shows that they have met the required standard in the assessment criteria. Evidence can take a variety of forms, including the following:

products of work carried out in the workplace. This may include, for example, written documents, screen dumps, print-outs or electronic copies of accounting records, etc

simulation of real work, using case studies and assignments

oral presentation and questioning

written tests, including multiple choice papers

direct observation of workplace activities by the assessor

professional discussion between the assessor and the candidate

witness testimony from managers and others at the workplace.

Learners can use one piece of evidence to prove their knowledge, skills and understanding across different assessment criteria and/or across different units. It is, therefore, not necessary for learners to have each assessment criterion assessed separately. Learners should be encouraged to reference the assessment criteria to which the evidence relates.

Evidence must be made available to the assessor, internal verifier and Edexcel standards verifier. A range of recording documents is available on the Edexcel website www.edexcel.com. Alternatively, centres may develop their own.

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

7

Centre recognition and approval

Centre recognition

Centres that have not previously offered Edexcel qualifications need to apply for and be granted centre recognition as part of the process for approval to offer individual qualifications. New centres must complete both a centre recognition approval application and a qualification approval application.

Existing centres will be given ‘automatic approval’ for a new qualification if they are already approved for a qualification that is being replaced by the new qualification and the conditions for automatic approval are met. Centres already holding Edexcel approval are able to gain qualification approval for a different level or different sector via Edexcel Online.

Approvals agreement

All centres are required to enter into an approvals agreement which is a formal commitment by the head or principal of a centre to meet all the requirements of the specification and any linked codes or regulations. Edexcel will act to protect the integrity of the awarding of qualifications, if centres do not comply with the agreement. This could result in the suspension of certification or withdrawal of approval.

Quality assurance

Detailed information on Edexcel’s quality assurance processes is given in Annexe B.

What resources are required?

This qualification is designed to support learners working in the Accounting sector. Physical resources need to support the delivery of the qualification and the assessment of the learning outcomes and must be of industry standard. Staff assessing the learner must meet the requirements within the assessment strategy for the sector as shown in Annexe D.

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

8

Unit format

Each unit in this specification contains the following sections.

Unit title:

Unit reference number:

QCF level:

Credit value:

Guided learning hours:

Unit summary:

Evidence requirements:

Assessment methodology:

Recording of evidence:

Learning outcomes:

Assessment criteria:

Evidence type:

Portfolio reference:

Date:

The unit title is accredited on the QCF and this form of words will appear on the learner’s Notification of Performance (NOP).

This code is a unique reference number for the unit.

All units and qualifications within the QCF have a level assigned to them, which represents the level of achievement. There are nine levels of achievement, from Entry level to level 8. The level of the unit has been informed by the QCF level descriptors and, where appropriate, the NOS and/or other sector/professional.

All units have a credit value. The minimum credit value is one, and credits can only be awarded in whole numbers. Learners will be awarded credits when they achieve the unit.

A notional measure of the substance of a qualification. It includes an estimate of the time that might be allocated to direct teaching or instruction, together with other structured learning time, such as directed assignments, assessments on the job or supported individual study and practice. It excludes learner-initiated private study.

This provides a summary of the purpose of the unit.

Learners must provide evidence for each of the requirements stated in this section.

Learning outcomes state exactly what a learner should know, understand or be able to do as a result of completing a unit.

The assessment criteria of a unit specify the standard a learner is expected to meet to demonstrate that a learning outcome, or a set of learning outcomes, has been achieved.

Learners must reference the type of evidence they have and where it is available for quality assurance purposes. The learner can enter the relevant key and a reference. Alternatively, the learner and/or centre can devise their own referencing system.

This provides a summary of the how evidence should be recorded.

The learner should use this box to indicate where the evidence can be obtained eg portfolio page number.

The learner should give the date when the evidence has been provided.

Information about how the unit must be delivered and assessed.

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

9

Units

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

10

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

11

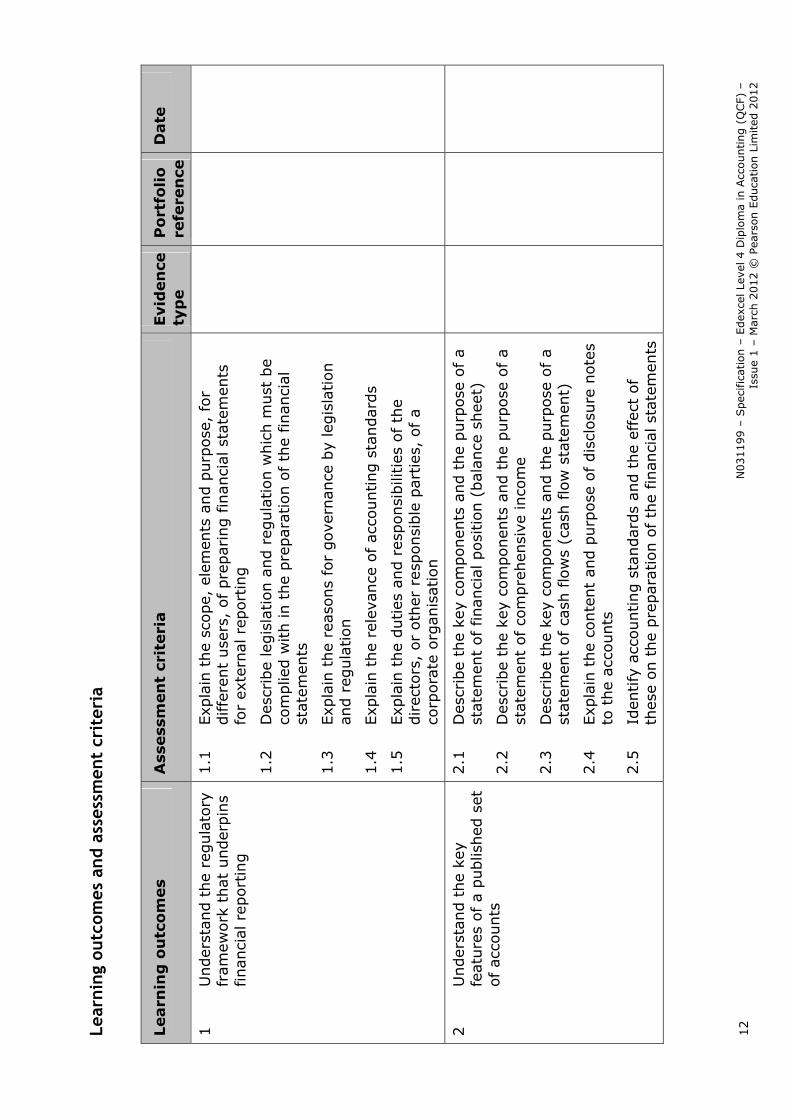

Unit 1: Principles of drafting financial statements

Unit reference number: L/600/4954

QCF level: 4

Credit value: 4

Guided learning hours: 35

Unit summary

Learners will develop knowledge and understanding of the external reporting environment for limited companies and for groups who are required to publish accounts. The principles of consolidated accounts and the analysis and interpretation of financial statements through ratio analysis are also covered.

Evidence requirements

Assessment must be carried out in a way that is consistent with the requirements outlined in Annexe D: Assessment strategy and the Assessment methodology below.

To pass the unit, learners must meet all of the assessment criteria.

Assessment methodology

This unit develops learners’ knowledge and understanding of preparing forecasts and budgets. In order for learners to be able to apply this knowledge and understanding effectively, this unit must be delivered and assessed alongside Unit 2: Drafting financial statements.

Recording of evidence

The type of evidence, portfolio reference and date should be entered against each assessment criterion in the table. Alternatively, centre documentation could be used to record this information. If evidence cannot be included in a portfolio, its location must be recorded in assessment documentation. All assessment evidence must be accessible for internal verifiers and Edexcel standards verifiers.

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

12

Lear

nin

g ou

tcom

es a

nd a

sses

smen

t cr

iter

ia

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

1

Under

stan

d t

he

regula

tory

fr

amew

ork

that

under

pin

s finan

cial

rep

ort

ing

1.1

Exp

lain

the

scope,

ele

men

ts a

nd p

urp

ose

, fo

r diffe

rent

use

rs,

of pre

par

ing fin

anci

al s

tate

men

ts

for

exte

rnal re

port

ing

1.2

D

escr

ibe

legis

lation a

nd r

egula

tion w

hic

h m

ust

be

com

plie

d w

ith in t

he

pre

para

tion o

f th

e finan

cial

st

atem

ents

1.3

Exp

lain

the

reaso

ns

for

gove

rnance

by

legis

lation

and r

egula

tion

1.4

Exp

lain

the

rele

vance

of

acco

unting s

tandar

ds

1.5

Exp

lain

the

duties

and r

esponsi

bili

ties

of th

e direc

tors

, or

oth

er r

esponsi

ble

par

ties

, of

a co

rpora

te o

rgan

isat

ion

2

Under

stan

d t

he

key

feat

ure

s of a

publis

hed

set

of ac

counts

2.1

D

escr

ibe

the

key

com

ponen

ts a

nd t

he

purp

ose

of a

stat

emen

t of

finan

cial

posi

tion (

bal

ance

shee

t)

2.2

D

escr

ibe

the

key

com

ponen

ts a

nd t

he

purp

ose

of a

stat

emen

t of

com

pre

hen

sive

inco

me

2.3

D

escr

ibe

the

key

com

ponen

ts a

nd t

he

purp

ose

of a

stat

emen

t of

cash

flo

ws

(cas

h f

low

sta

tem

ent)

2.4

Exp

lain

the

conte

nt

and p

urp

ose

of

dis

closu

re n

ote

s to

the

acco

unts

2.5

Id

entify

acc

ounting s

tandar

ds

and t

he

effe

ct o

f th

ese

on t

he

pre

par

ation o

f th

e finan

cial

sta

tem

ents

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

13

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

3

Under

stan

d b

asi

c princi

ple

s of

conso

lidat

ion

3.1

D

escr

ibe

the

key

com

ponen

ts o

f a s

et o

f co

nso

lidat

ed fin

anci

al st

atem

ents

: par

ent,

su

bsi

dia

ry,

non-c

ontr

olli

ng inte

rest

(m

inori

ty

inte

rest

), g

oodw

ill,

fair v

alues

, pre

- an

d p

ost

-ac

quis

itio

n p

rofits

, an

d e

quity

3.2

Exp

lain

the

pro

cess

of basi

c co

nso

lidat

ion for

a par

ent

and s

ubsi

dia

ry

3.3

D

escr

ibe

the

effe

ct o

f co

nso

lidation o

n e

ach

of th

e ke

y el

emen

ts:

par

ent,

subsi

dia

ry,

non-c

ontr

olli

ng

inte

rest

(m

inori

ty inte

rest

), g

oodw

ill,

fair

val

ues

, pre

- an

d p

ost

-acq

uis

itio

n p

rofits

, an

d e

quity

3.4

Exp

lain

the

key

feat

ure

s of

a par

ent/

ass

oci

ate

rela

tionsh

ip

4

Appre

ciat

e th

e an

alys

is

and inte

rpre

tation o

f finan

cial

sta

tem

ents

4.1

D

emonst

rate

an u

nder

stan

din

g o

f th

e re

lationsh

ip

bet

wee

n t

he

elem

ents

of

the

finan

cial

sta

tem

ents

: as

sets

, lia

bili

ties

, eq

uity,

inco

me,

exp

ense

s,

contr

ibutions

from

ow

ner

s, a

nd d

istr

ibutions

to

ow

ner

s

4.2

Exp

lain

how

to c

alcu

late

acc

ounting r

atio

s:

pro

fita

bili

ty,

liquid

ity,

eff

icie

ncy

, finan

cial

posi

tion

4.3

Exp

lain

the

inte

r-re

lationsh

ips

bet

wee

n r

atio

s

4.4

Exp

lain

the

purp

ose

of th

e in

terp

reta

tion o

f ra

tios

4.5

D

escr

ibe

how

the

inte

rpre

tation a

nd a

naly

sis

of

acco

unting r

atio

s is

use

d in a

busi

nes

s en

viro

nm

ent

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

14

Lear

ner

nam

e:__________________________________________

D

ate:

___________________________

Lear

ner

sig

nat

ure

:_______________________________________

D

ate:

___________________________

Ass

esso

r si

gnat

ure

:______________________________________

D

ate:

___________________________

Inte

rnal

ver

ifie

r si

gnatu

re:

________________________________

(i

f sa

mple

d)

Dat

e:___________________________

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

15

Unit 2: Drafting financial statements

Unit reference number: R/600/4955

QCF level: 4

Credit value: 6

Guided learning hours: 55

Unit summary

Learners will be able to prepare a full range of financial statements for a limited company including consolidated accounts for a simple group. They will also be able to use the information they have collated to identify the financial position of the business in terms of profitability, liquidity and how they use their resources.

Evidence requirements

Assessment must be carried out in a way that is consistent with the requirements outlined in Annexe D: Assessment strategy and the Assessment methodology below.

To pass the unit, learners must meet all of the assessment criteria.

Assessment methodology

This unit develops learners’ skills in preparing financial statements. In order for them to do this successfully, this unit must be delivered and assessed alongside Unit 1: Principles of drafting financial statements, which will provide them with the necessary underpinning knowledge and understanding.

Recording of evidence

The type of evidence, portfolio reference and date should be entered against each assessment criterion in the table. Alternatively, centre documentation could be used to record this information. If evidence cannot be included in a portfolio, its location must be recorded in assessment documentation. All assessment evidence must be accessible for internal verifiers and Edexcel standards verifiers.

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

16

Lear

nin

g ou

tcom

es a

nd a

sses

smen

t cr

iter

ia

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

1

Dra

ft s

tatu

tory

fin

anci

al

stat

emen

ts for

a lim

ited

co

mpan

y

1.1

Apply

acc

ounting s

tandar

ds

and r

elev

ant

legis

lation

to c

orr

ectly

iden

tify

, an

d a

ccura

tely

adju

st,

acco

unting info

rmat

ion

1.2

U

se a

ppro

priat

e in

form

atio

n t

o a

ccura

tely

dra

ft a

st

atem

ent

of

com

pre

hen

sive

inco

me

1.3

U

se a

ppro

priat

e in

form

atio

n t

o a

ccura

tely

dra

ft a

st

atem

ent

of

finan

cial

posi

tion (

bal

ance

shee

t)

1.4

Pr

epare

note

s to

the

acco

unts

whic

h s

atis

fy

stat

uto

ry c

urr

ent

dis

closu

re r

equirem

ents

in r

espec

t of acc

ounting p

olic

ies,

fix

ed a

sset

s, c

urr

ent

and

long-t

erm

lia

bili

ties

, eq

uity

1.5

D

raft

an a

ccura

te s

tate

men

t of

cash

flo

ws

(cas

h

flow

sta

tem

ent)

2

Dra

ft s

imple

conso

lidat

ed

finan

cial

sta

tem

ents

2.1

D

raft

a c

onso

lidat

ed inco

me

state

men

t fo

r a

pare

nt

com

pany

with o

ne

part

ly-o

wned

subsi

dia

ry

2.2

D

raft

a c

onso

lidat

ed s

tate

men

t of

finan

cial

posi

tion

(bal

ance

shee

t) f

or

a p

aren

t co

mpan

y w

ith o

ne

par

tly-

ow

ned

subsi

dia

ry

2.3

Apply

curr

ent

stan

dard

s to

acc

ura

tely

cal

cula

te a

nd

appro

priat

ely

dea

l w

ith t

he

acco

unting t

reat

men

t of

goodw

ill,

non-c

ontr

olli

ng inte

rest

(m

inori

ty inte

rest

) an

d p

ost

-acq

uis

itio

n p

rofits

, in

the

gro

up f

inan

cial

st

atem

ents

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

17

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

3

Inte

rpre

t finan

cial

st

atem

ents

usi

ng r

atio

an

alys

is

3.1

Cal

cula

te a

nd inte

rpre

t th

e re

lationsh

ip b

etw

een t

he

elem

ents

of th

e finan

cial

sta

tem

ents

with r

egar

d t

o

pro

fita

bili

ty,

liquid

ity,

eff

icie

nt

use

of

reso

urc

es a

nd

finan

cial

posi

tion

3.2

D

raw

val

id c

oncl

usi

ons

from

the

info

rmat

ion

conta

ined

within

the

finan

cial

sta

tem

ents

3.3

Pr

esen

t cl

early

and c

onci

sely

iss

ues

, an

alys

is a

nd

concl

usi

ons

to t

he

appro

pri

ate

peo

ple

Lear

ner

nam

e:__________________________________________

D

ate:

___________________________

Lear

ner

sig

nat

ure

:_______________________________________

D

ate:

___________________________

Ass

esso

r si

gnat

ure

:______________________________________

D

ate:

___________________________

Inte

rnal

ver

ifie

r si

gnatu

re:

________________________________

(i

f sa

mple

d)

Dat

e:___________________________

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

18

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

19

Unit 3: Principles of budgeting

Unit reference number: Y/600/4956

QCF level: 4

Credit value: 3

Guided learning hours: 25

Unit summary

This unit is about understanding how and why budgets are prepared. The learner will develop the necessary knowledge to allow them to prepare revenue forecasts and a range of budgets for different circumstances and be able to tailor them to meet organisational requirements. They will be able to understand the components parts of budgetary procedure to aid organisational planning and control.

Evidence requirements

Assessment must be carried out in a way that is consistent with the requirements outlined in Annexe D: Assessment strategy and the Assessment methodology below.

To pass the unit, learners must meet all of the assessment criteria.

Assessment methodology

This unit develops learners’ knowledge and understanding of preparing forecasts and budgets. In order for learners to be able to apply this knowledge and understanding effectively, this unit must be delivered and assessed alongside Unit 4: Preparing budgets.

Recording of evidence

The type of evidence, portfolio reference and date should be entered against each assessment criterion in the table. Alternatively, centre documentation could be used to record this information. If evidence cannot be included in a portfolio, its location must be recorded in assessment documentation. All assessment evidence must be accessible for internal verifiers and Edexcel standards verifiers.

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

20

Lear

nin

g ou

tcom

es a

nd a

sses

smen

t cr

iter

ia

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

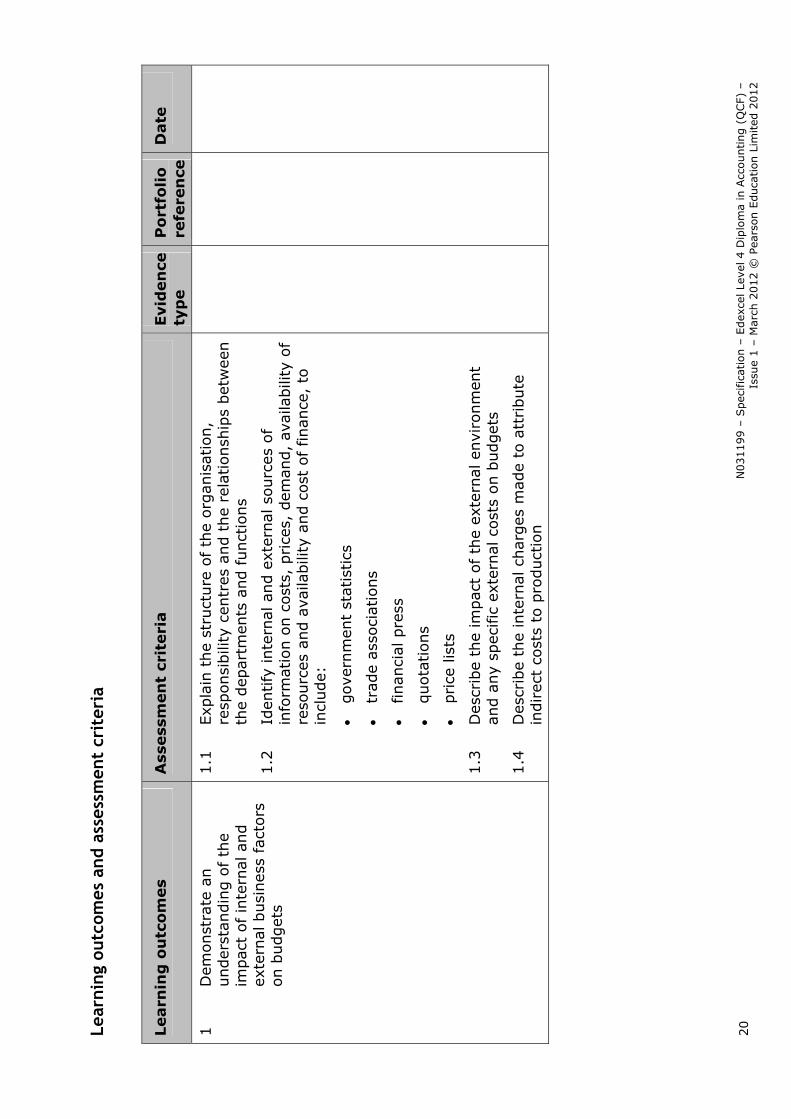

1

Dem

onst

rate

an

under

stan

din

g o

f th

e im

pac

t of

inte

rnal

and

exte

rnal busi

nes

s fa

ctors

on b

udget

s

1.1

Exp

lain

the

stru

cture

of

the

org

anis

atio

n,

resp

onsi

bili

ty c

entr

es a

nd t

he

rela

tionsh

ips

bet

wee

n

the

dep

artm

ents

and funct

ions

1.2

Id

entify

inte

rnal

and e

xter

nal so

urc

es o

f in

form

atio

n o

n c

ost

s, p

rice

s, d

eman

d,

availa

bili

ty o

f re

sourc

es a

nd a

vaila

bili

ty a

nd c

ost

of finance

, to

in

clude:

gove

rnm

ent

stat

istics

tr

ade

asso

ciat

ions

finan

cial

pre

ss

quota

tions

price

lis

ts

1.3

D

escr

ibe

the

impac

t of th

e ex

tern

al e

nvi

ronm

ent

and a

ny

spec

ific

ext

ernal

cost

s on b

udget

s

1.4

D

escr

ibe

the

inte

rnal

char

ges

mad

e to

att

ribute

in

direc

t co

sts

to p

roduct

ion

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

21

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

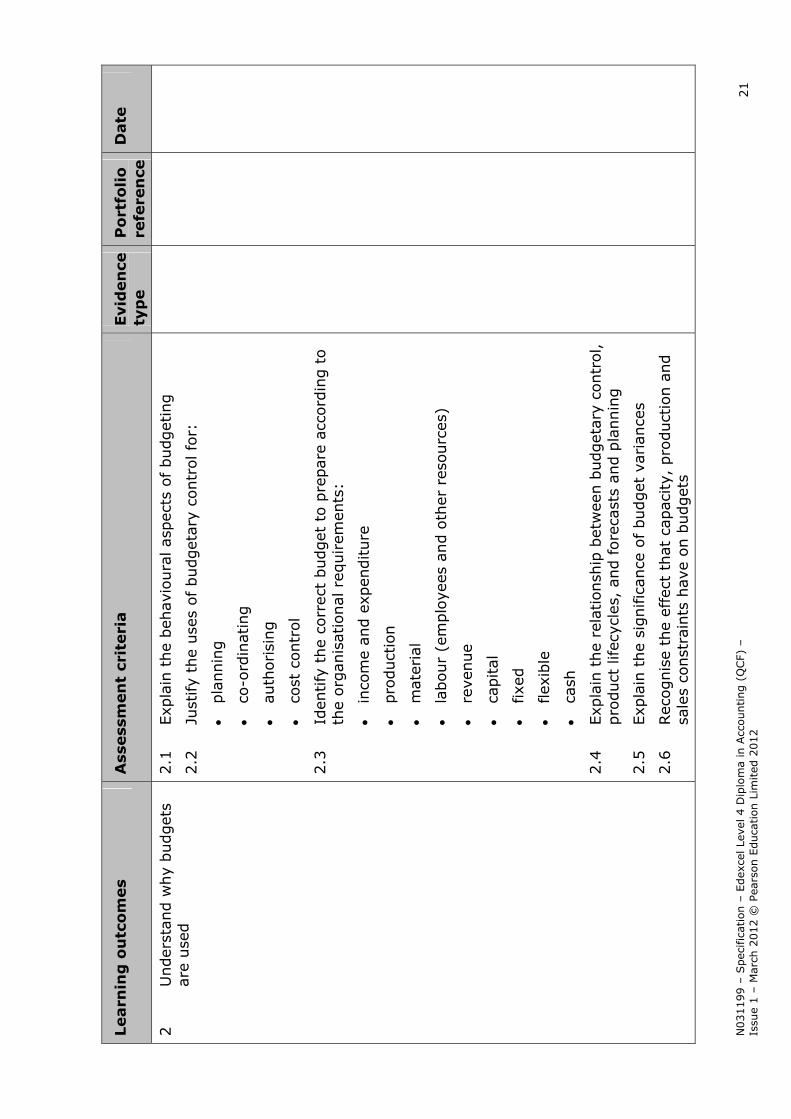

2

Under

stan

d w

hy

budget

s ar

e use

d

2.1

Exp

lain

the

beh

avi

oura

l asp

ects

of budget

ing

2.2

Ju

stify

the

use

s of budget

ary

contr

ol fo

r:

pla

nnin

g

co

-ord

inat

ing

au

thorisi

ng

co

st c

ontr

ol

2.3

Id

entify

the

corr

ect

budget

to p

repar

e ac

cord

ing t

o

the

org

anis

atio

nal

req

uirem

ents

:

in

com

e an

d e

xpen

diture

pro

duct

ion

m

ater

ial

la

bour

(em

plo

yees

and o

ther

res

ourc

es)

re

venue

ca

pital

fixe

d

flex

ible

ca

sh

2.4

Exp

lain

the

rela

tionsh

ip b

etw

een b

udget

ary

contr

ol,

pro

duct

lifec

ycle

s, a

nd fore

cast

s an

d p

lannin

g

2.5

Exp

lain

the

signific

ance

of

budget

var

iance

s

2.6

Rec

ognis

e th

e ef

fect

that

capac

ity,

pro

duct

ion a

nd

sale

s co

nst

rain

ts h

ave

on b

udget

s

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

22

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

3

Under

stan

d t

he

skill

s nee

ded

in b

udget

pre

par

ation

3.1

Exp

lain

the

princi

ple

s of

stan

dard

cost

ing

3.2

D

escr

ibe

the

purp

ose

of

reve

nue

and c

ost

fore

cast

s an

d h

ow

they

lin

k to

budget

s

3.3

Id

entify

when

to u

se t

he

follo

win

g t

echniq

ues

:

in

dex

ing

sa

mplin

g

m

ovi

ng a

vera

ges

lin

ear

regre

ssio

n

se

asonal

tre

nds

3.4

Rec

ognis

e ex

pen

ses

as d

iffe

rent

types

of

cost

s, t

o

incl

ude:

direc

t or

indirec

t (o

verh

ead)

fixe

d,

variab

le,

sem

i-va

riable

or

step

ped

3.5

Id

entify

the

sourc

es o

f re

leva

nt

dat

a u

sed in b

udget

pro

posa

ls

Lear

ner

nam

e:__________________________________________

D

ate:

___________________________

Lear

ner

sig

nat

ure

:_______________________________________

D

ate:

___________________________

Ass

esso

r si

gnat

ure

:______________________________________

D

ate:

___________________________

Inte

rnal

ver

ifie

r si

gnatu

re:

________________________________

(i

f sa

mple

d)

Dat

e:___________________________

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

23

Unit 4: Drafting budgets

Unit reference number: D/600/4957

QCF level: 4

Credit value: 4

Guided learning hours: 35

Unit summary

This unit is about preparing forecasts and budgets. The learner will develop the necessary skills to allow them to prepare budgets, analyse variances and make recommendations for improving organisational performance. They will be able to guide managers in planning and control.

Evidence requirements

Assessment must be carried out in a way that is consistent with the requirements outlined in Annexe D: Assessment strategy and the Assessment methodology below.

To pass the unit, learners must meet all of the assessment criteria.

Assessment methodology

This unit develops learners’ skills in preparing forecasts and budgets. In order for them to do this, this unit must be delivered and assessed alongside Unit 3: Principles of budgeting, which will provide them with the necessary underpinning knowledge and understanding.

Recording of evidence

The type of evidence, portfolio reference and date should be entered against each assessment criterion in the table. Alternatively, centre documentation could be used to record this information. If evidence cannot be included in a portfolio, its location must be recorded in assessment documentation. All assessment evidence must be accessible for internal verifiers and Edexcel standards verifiers.

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

24

Lear

nin

g ou

tcom

es a

nd a

sses

smen

t cr

iter

ia

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

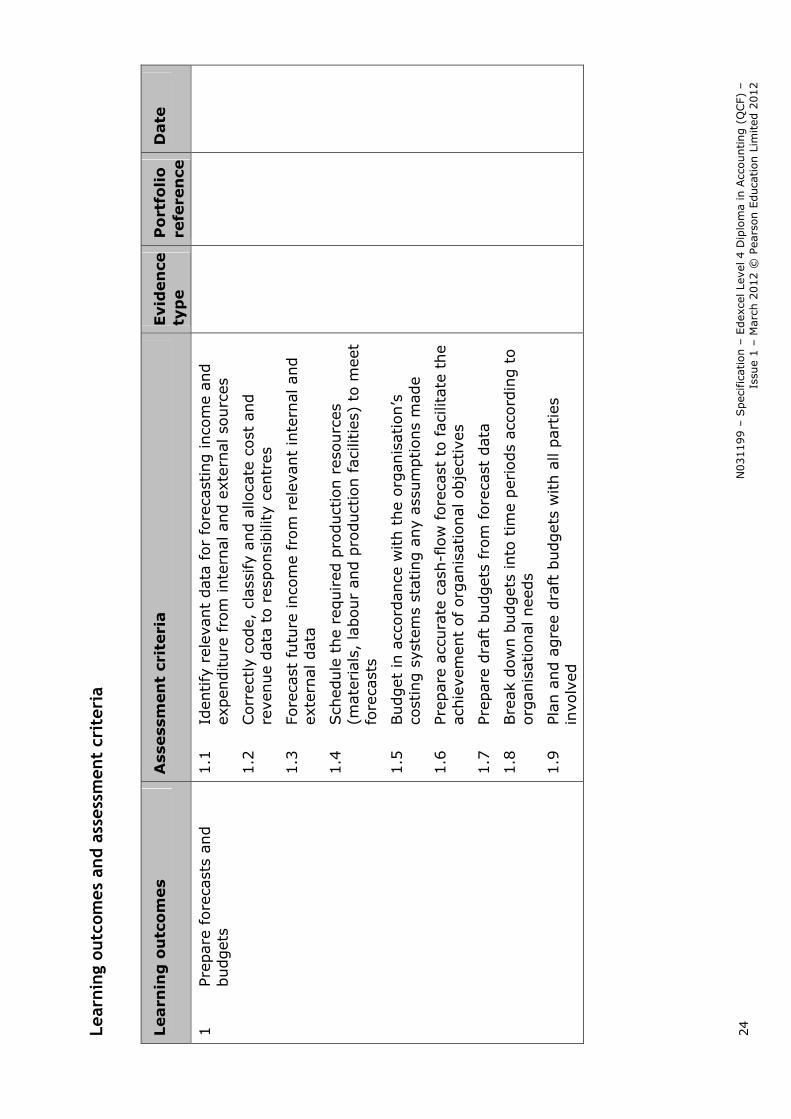

1

Prep

are

fore

cast

s an

d

budget

s 1.1

Id

entify

rel

evan

t dat

a for

fore

cast

ing inco

me

and

expen

diture

fro

m inte

rnal and e

xter

nal so

urc

es

1.2

Corr

ectly

code,

cla

ssify

and a

lloca

te c

ost

and

reve

nue

dat

a to

res

ponsi

bili

ty c

entr

es

1.3

Fo

reca

st futu

re inco

me

from

rel

evan

t in

tern

al a

nd

exte

rnal dat

a

1.4

Sch

edule

the

required

pro

duct

ion r

esourc

es

(mat

eria

ls,

labour

and p

roduct

ion faci

litie

s) t

o m

eet

fore

cast

s

1.5

Budget

in a

ccord

ance

with t

he

org

anis

atio

n’s

co

stin

g s

yste

ms

stat

ing a

ny

assu

mptions

mad

e

1.6

Pr

epare

acc

ura

te c

ash

-flo

w fore

cast

to faci

litat

e th

e ac

hie

vem

ent

of org

anis

atio

nal

obje

ctiv

es

1.7

Pr

epare

dra

ft b

udget

s fr

om

fore

cast

dat

a

1.8

Bre

ak

dow

n b

udget

s in

to t

ime

per

iods

acc

ord

ing t

o

org

anis

atio

nal

nee

ds

1.9

Pl

an a

nd a

gre

e dra

ft b

udget

s w

ith a

ll par

ties

in

volv

ed

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

25

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

2

Under

stan

d t

he

impact

th

at c

han

ges

in t

he

econom

ic e

nvi

ronm

ent

will

hav

e on t

he

budget

2.1

Cal

cula

te t

he

effe

ct t

hat

variat

ions

in c

apac

ity

on

cost

s, p

roduct

ion a

nd s

ales

will

hav

e on b

udget

ed

cost

s an

d r

even

ues

2.2

Pr

epare

an a

ccura

tely

fle

xed b

udget

2.3

Anal

yse

critic

al fact

ors

affec

ting c

ost

s an

d r

even

ues

an

d d

raw

cle

ar c

oncl

usi

ons

2.4

Id

entify

and e

valu

ate

options

and s

olu

tions

to

incr

ease

pro

fita

bili

ty o

r re

duce

fin

anci

al lo

sses

or

exposu

re t

o r

isk

3

Use

budget

ary

contr

ol to

en

sure

org

anis

atio

nal

ta

rget

s are

met

3.1

Set

cle

ar

targ

ets

and p

erfo

rmance

indic

ators

to

enab

le t

he

budget

s to

be

monitore

d

3.2

Chec

k an

d r

econci

le b

udget

fig

ure

s on a

n o

ngoin

g

bas

is

3.3

Rev

iew

and r

evis

e th

e va

lidity

of budget

s in

the

light

of an

y si

gnific

ant

antici

pate

d c

han

ges

3.4

Id

entify

varian

ces

bet

wee

n b

udget

and a

ctual

in

com

e/ex

pen

diture

3.5

Anal

yse

the

vari

ance

s an

d e

xpla

in t

he

impac

t th

at

this

will

have

on t

he

org

anis

atio

n

3.6

In

form

manag

emen

t of an

y si

gnific

ant

issu

es

aris

ing f

rom

budget

ary

contr

ol

3.7

Pr

esen

t an

y re

com

men

dat

ions

with a

cle

ar

rational

e to

appro

priat

e peo

ple

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

26

Lear

ner

nam

e:__________________________________________

D

ate:

___________________________

Lear

ner

sig

nat

ure

:_______________________________________

D

ate:

___________________________

Ass

esso

r si

gnat

ure

:______________________________________

D

ate:

___________________________

Inte

rnal

ver

ifie

r si

gnatu

re:

________________________________

(i

f sa

mple

d)

Dat

e:___________________________

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

27

Unit 5: Principles of managing financial performance

Unit reference number: H/600/4958

QCF level: 4

Credit value: 3

Guided learning hours: 25

Unit summary

This unit is about understanding the principles of managing financial performance. Learners will have the knowledge to be able to use a range of techniques to analyse information on expenditure. They will be able to make judgements to support decision making, planning and control by managers.

Evidence requirements

Assessment must be carried out in a way that is consistent with the requirements outlined in Annexe D: Assessment strategy and the Assessment methodology below.

To pass the unit, learners must meet all of the assessment criteria.

Assessment methodology

This unit develops learners’ knowledge and understanding of managing financial performance. In order for learners to be able to apply this knowledge and understanding effectively, this unit must be delivered and assessed alongside Unit 6: Measuring financial performance.

Recording of evidence

The type of evidence, portfolio reference and date should be entered against each assessment criterion in the table. Alternatively, centre documentation could be used to record this information. If evidence cannot be included in a portfolio, its location must be recorded in assessment documentation. All assessment evidence must be accessible for internal verifiers and Edexcel standards verifiers.

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

28

Lear

nin

g ou

tcom

es a

nd a

sses

smen

t cr

iter

ia

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

1

Dem

onst

rate

an a

ccura

te

under

stan

din

g o

f th

e in

tern

al a

nd e

xter

nal

fa

ctors

that

affe

ct

org

anis

atio

ns

1.1

Exp

lain

the

purp

ose

and s

truct

ure

of re

port

ing

syst

ems

within

the

org

anis

atio

n

1.2

D

escr

ibe

the

contr

ibution o

f an

org

anis

atio

n’s

fu

nct

ional

spec

ialis

ts t

o c

ost

red

uct

ion a

nd v

alue

enhan

cem

ent

1.3

Exp

lain

the

org

anis

ation's

ext

ernal

envi

ronm

ent

and t

he

spec

ific

ext

ernal

cost

s

1.4

Id

entify

cost

s co

rrec

tly

(mat

eria

ls,

labour

and

expen

ses)

and t

he

sourc

es o

f in

form

ation a

bout

thes

e co

sts,

incl

udin

g:

gove

rnm

ent

stat

istics

pro

fess

ional

or

trade

asso

ciat

ions

quota

tions

price

lis

ts

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

29

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

2

Be

awar

e of th

e co

st

acco

unting t

echniq

ues

nee

ded

in m

onitoring

finan

cial

per

form

ance

2.1

Exp

lain

the

types

of

cost

cen

tres

, pro

fit

centr

es a

nd

inve

stm

ent

centr

es

2.2

D

escr

ibe

the

use

of

stan

dar

d u

nits

of in

puts

and

outp

uts

2.3

Rec

ognis

e th

e diffe

rence

s bet

wee

n s

tandard

, m

argin

al and a

bso

rption c

ost

ing in t

erm

s of co

st

reco

rdin

g,

cost

rep

ort

ing a

nd c

ost

beh

avio

ur

2.4

Exp

lain

the

use

of

varian

ce a

nal

ysis

in labour,

m

ater

ials

and o

verh

ead c

ost

ing

2.5

Acc

ura

tely

iden

tify

fix

ed,

variable

, se

mi-

variab

le

and s

tepped

cost

s an

d e

xpla

in t

hei

r use

in c

ost

re

cord

ing,

cost

rep

ort

ing a

nd c

ost

analy

sis

3

Under

stan

d t

he

tech

niq

ues

nec

essa

ry f

or

mea

suring

per

form

ance

and

man

agin

g c

ost

s

3.1

Id

entify

the

rele

vant

per

form

ance

and q

ualit

y m

easu

res

to u

se t

o m

onitor

finan

cial

per

form

ance

3.2

Exp

lain

the

princi

ple

s of dis

counte

d c

ash f

low

3.3

Id

entify

appro

priat

e per

form

ance

indic

ators

to u

se

for:

ef

fici

ency

ef

fect

iven

ess

pro

duct

ivity

co

st p

er u

nit

bal

ance

d s

core

card

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

30

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

ben

chm

ark

ing

co

ntr

ol ra

tios

(effic

iency

, ca

paci

ty a

nd a

ctiv

ity)

sc

enar

io p

lannin

g (

‘what

-if’ a

nal

ysis

)

3.4

Exp

lain

the

use

and p

urp

ose

of

tech

niq

ues

:

in

dex

ing

sa

mplin

g

tim

e se

ries

(eg

movi

ng a

vera

ges

, lin

ear

regre

ssio

n a

nd s

easo

nal

tre

nds)

3.5

Id

entify

the

corr

ect

ratios

use

d t

o m

onitor

finan

cial

per

form

ance

3.6

D

escr

ibe

a ra

nge

of co

st m

anag

emen

t te

chniq

ues

an

d r

ecognis

e w

hen

thes

e sh

ould

be

use

d

lif

e cy

cle

cost

ing

ta

rget

cost

ing (

incl

udin

g v

alu

e en

gin

eering)

ac

tivi

ty-b

ase

d c

ost

ing

Lear

ner

nam

e:__________________________________________

D

ate:

___________________________

Lear

ner

sig

nat

ure

:_______________________________________

D

ate:

___________________________

Ass

esso

r si

gnat

ure

:______________________________________

D

ate:

___________________________

Inte

rnal

ver

ifie

r si

gnatu

re:

________________________________

(i

f sa

mple

d)

Dat

e:___________________________

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

31

Unit 6: Measuring financial performance

Unit reference number: K/600/4959

QCF level: 4

Credit value: 4

Guided learning hours: 35

Unit summary

This unit is about measuring financial performance. Learners will have the skills to collect and analyse information, monitor performance, and present reports to management.

Evidence requirements

Assessment must be carried out in a way that is consistent with the requirements outlined in Annexe D: Assessment strategy and the Assessment methodology below.

To pass the unit, learners must meet all of the assessment criteria.

Assessment methodology

This unit develops learners’ skills in measuring financial performance. In order for them to do this, this unit must be delivered and assessed alongside Unit 5: Principles of managing financial performance, which will provide them with the necessary underpinning knowledge and understanding.

Recording of evidence

The type of evidence, portfolio reference and date should be entered against each assessment criterion in the table. Alternatively, centre documentation could be used to record this information. If evidence cannot be included in a portfolio, its location must be recorded in assessment documentation. All assessment evidence must be accessible for internal verifiers and Edexcel standards verifiers.

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

32

Lear

nin

g ou

tcom

es a

nd a

sses

smen

t cr

iter

ia

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

1

Colla

te info

rmat

ion f

rom

va

rious

sourc

es a

nd

pre

par

e ro

utine

cost

re

port

s

1.1

O

bta

in inco

me

and e

xpen

diture

info

rmat

ion fro

m

diffe

rent

units

within

the

org

anis

atio

n a

nd

conso

lidat

e in

an a

ppro

priat

e fo

rm

1.2

Rec

onci

le inco

me

and e

xpen

diture

info

rmation

colle

cted

fro

m v

ario

us

dep

artm

ents

or

info

rmat

ion

syst

ems

within

the

org

anis

atio

n

1.3

Acc

ount

for

transa

ctio

ns

bet

wee

n t

he

separa

te u

nits

of th

e org

anis

atio

n,

in a

ccord

ance

with t

he

org

anis

atio

n’s

pro

cedure

s

1.4

Id

entify

oth

er v

alid

rel

evan

t in

form

atio

n f

rom

in

tern

al a

nd e

xter

nal

sourc

es

1.5

Pr

epare

routine

cost

rep

ort

s

1.6

Anal

yse

routine

cost

rep

ort

s an

d c

om

par

e w

ith

budget

and s

tandar

d c

ost

s to

acc

ura

tely

iden

tify

an

y diffe

rence

s an

d t

he

implic

atio

ns

of th

ese

1.7

Corr

ectly

iden

tify

var

iance

s an

d p

repare

rel

evan

t re

port

s fo

r m

anag

emen

t

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

33

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

2

Mak

e su

gges

tions

for

impro

ving f

inan

cial

per

form

ance

by

monitoring a

nd a

nal

ysin

g

info

rmat

ion

2.1

Com

par

e re

sults

ove

r tim

e usi

ng m

ethods

that

al

low

for

chan

gin

g p

rice

lev

els

2.2

M

onitor

and a

nal

yse

curr

ent

and fore

cast

tre

nds

in

price

s an

d m

arke

t co

nditio

ns

on a

reg

ula

r bas

is

2.3

Com

par

e tr

ends

with p

revi

ous

dat

a an

d iden

tify

pote

ntial

im

plic

atio

ns

2.4

Consu

lt r

elev

ant

staf

f in

the

org

anis

atio

n a

bout

the

anal

ysis

of tr

ends

and v

arian

ces

2.5

Cal

cula

te r

atio

s, p

erfo

rman

ce indic

ators

and

mea

sure

s of

valu

e ad

ded

in a

ccord

ance

with t

he

org

anis

atio

n’s

pro

cedure

s

2.6

Pr

epare

rel

evan

t per

form

ance

indic

ators

2.7

In

terp

ret

the

resu

lts

of re

leva

nt

per

form

ance

in

dic

ato

rs,

iden

tify

pote

ntial im

pro

vem

ents

and

estim

ate

the

valu

e of su

ch im

pro

vem

ents

2.8

Id

entify

way

s to

red

uce

cost

s an

d e

nhan

ce v

alues

, co

nsu

ltin

g s

pec

ialis

ts a

s nec

essa

ry

2.9

Pr

epare

est

imat

es o

f ca

pital in

vest

men

t pro

ject

s usi

ng d

isco

unte

d c

ash flo

w t

echniq

ues

N031199 –

Spec

ific

atio

n –

Edex

cel Le

vel 4 D

iplo

ma

in A

ccounting (

QCF)

–

Issu

e 1 –

Mar

ch 2

012 ©

Pea

rson E

duca

tion L

imited

2012

34

Learn

ing

ou

tco

mes

Ass

ess

men

t cr

iteri

a

Evid

en

ce

typ

e

Po

rtfo

lio

re

fere

nce

D

ate

3

Prep

are

per

form

ance

re

port

s fo

r m

anag

emen

t 3.1

Pr

epare

rep

ort

s in

the

most

appro

priat

e fo

rmat

and

pre

sent

them

to m

anag

emen

t w

ithin

the

required

tim

esca

les

3.2

Pr

epare

exc

eption r

eport

s to

iden

tify

mat

ters

whic

h

require

furt

her

inve

stig

atio

n

3.3

M

ake

spec

ific

rec

om

men

dat

ions

to m

anagem

ent

in

a cl

ear

and a

ppro

priate

form

Lear

ner

nam

e:__________________________________________

D

ate:

___________________________

Lear

ner

sig

nat

ure

:_______________________________________

D

ate:

___________________________

Ass

esso

r si

gnat

ure

:______________________________________

D

ate:

___________________________

Inte

rnal

ver

ifie

r si

gnatu

re:

________________________________

(i

f sa

mple

d)

Dat

e:___________________________

N031199 – Specification – Edexcel Level 4 Diploma in Accounting (QCF) – Issue 1 – March 2012 © Pearson Education Limited 2012

35

Unit 7: Principles of internal control

Unit reference number: D/600/4960

QCF level: 4

Credit value: 3

Guided learning hours: 25

Unit summary

This unit is about understanding principles of internal control. Learners will be able to identify the role of internal control within an organisation, and be able to recognise different approaches and make informed reasoned judgements to inform management on how to implement or improve systems within an organisation.

Evidence requirements

Assessment must be carried out in a way that is consistent with the requirements outlined in Annexe D: Assessment strategy and the Assessment methodology below.

To pass the unit, learners must meet all of the assessment criteria.

Assessment methodology

This unit develops learners’ knowledge and understanding of internal control. In order for learners to be able to apply this knowledge and understanding effectively, this unit must be delivered and assessed alongside Unit 8: Evaluating accounting systems.

Recording of evidence