Embed Size (px)

DESCRIPTION

Our report EDC Market Update features market data in great detail on yields, rents, vacancy rates and an outlook on pricing in the following property sectors: office, retail, industrial & logistics and residential rental properties.

Citation preview

N O V E M B E R 2 0 1 5

Research

MARKET UPDATE

Erhverv Poul Erik Bech

EDC Research - November 2015 - page 2

MARKET UPDATE EDC

Contact us:Robert Neble LarsenCEOTel: +45 33 30 10 54 Mail: [email protected]

Copenhagen:Morten Westphal JensenRegional directorTel: + 45 38 77 05 22Mail: [email protected]

Aarhus:Søren Leth PedersenRegional Director, Partner, MSc.(f), Chartered Surveyor, MDETel: +45 58 58 78 76Mail: [email protected]

Aalborg:Frank Jensen Regional Director, Partner, CBATel: +45 58 58 75 72Mail: [email protected]

Kolding:Karsten L Jensen Regional Director, Partner, Tel: +45 58 58 74 07 Mail: [email protected]

Odense:Morten Nielsen Dept. Manager, Partner, Chartered Surveyor, MDETel: +45 58 58 78 56Mail: [email protected]

Research:Andreas BrandtAnalyst, MSc in EconomicsTel: +45 33 30 10 95Mail: [email protected]

edc.dk/erhverv

N O V E M B E R 2 0 1 5

REMARKS FOR OUR ESTIMATES:

The valuation of a property depends on various property specific attributes, including, but not limited to, the lease conditions, the tenant’s credit rating and the property’s condition. When valuing a property, the estimates should not be relied upon without seeking qualified, professional advice. However, the estimates can serve as useful in-put in the valuation process. Any reproduction of data in this report should be credited to EDC Erhverv Poul Erik Bech. Whilst data and estimates have been rigorously checked, EDC Erhverv Poul Erik Bech can take no responsibility for any inaccuracy within this report. Estimates and forecasts of rents and yields are as of 1. October 2015. Estimates are subject to change.

YIELDS, MARKET RENTS AND FORECASTS:

LOCATION: Yield and market rent estimates covers properties with prime, secondary and tertiary location.

FACILITY CLASS: Location aside, our estimates are based upon a segmentation of pro-perty facility classes; facility class A, B and C, where class A is the best facility class. Various variables for each property type have been taken into consideration with regards to deter-mine the facility classes, such as: size, floor plan structure, year of construction, lifts, climate control, cabling infrastructure, staff facilities, customer facilities, parking facilities, building energy rating, ceiling height, general accessibility, general condition of the property, etc. A property with prime location and class A facilities has the best possible location in an area, the highest standard when it comes to facilities, is modern and ready to move into. This type of property will typically be traded at the lowest yield for the area, have the highest market rent and have a short reletting process. Naturally, yield and market rent estimates are subject to certain deviations depending on the exact location and property specific facilities.

YIELD DEFINITION: All yields are net initial yields and is defined as the annualised rent generated by the property, after the deduction of estimated annual irrecoverable property outgoings, expressed as a percentage of the property valuation (property valuation is adjusted for the value of rental deposits and prepaid rent). For comparison purposes it is assumed that all properties are fully let at market-conform conditions.

MARKET RENT ESTIMATES: All rents are headline rents, in other words the con-tracted gross rent receivable which becomes payable after any tenant incentives have expired. Market rent estimates are expressed in €/sq m/year. Figures have been roun-ded when converting from DKK (Danish Kroner) to €. It is assumed that all properties are let at market-conform conditions.

FORECASTS: All forecasts reflect our expectations for the development over the next 3 to 6 months.

RESIDENTIAL RENTAL PROPERTIES: In this report estimates are included for “Newer residential rental properties”, “Fully developed older residential rental proper-ties” and “Older residential rental properties”. In Denmark residential rental levels cannot be determined freely and is subject to far reaching rent control. The major dif-ference between the before mentioned types of residential rental property is that older residential rental properties are regulated by the provisions in the Danish rent act (Le-jeloven) and the Housing Regulation Act (Boligreguleringsloven) concerning cost dri-ven rental levels. Newer residential rental properties taken in to use no earlier than 1 April 1992 are subject to the rules concerning free market rent, pursuant to the Housi-ng Regulation Act § 15 A and others.

DATA FOR VACANT COMMERCIAL SPACE ( VACANCY RATE)

Source: Oline ED-Statistikken (Oline-ED Statistics) as of 1. October 2015. For more information we refer to www.oline.dk/info/statistik. The forecasts of the vacancy rates have been made by EDC Erhverv Poul Erik Bech and reflect our expectations for the development over the next 3 to 6 months.

Forecasts

Increasing

Stable

Decreasing

EDC Research - November 2015 - page 3

MARKET UPDATE EDC

Regions of Denmark and selected market areas

N O V E M B E R 2 0 1 5

Capital Region of Denmark

Region Zealand

Southern Denmark Region

Central Jutland Region

Region North Jutland

Copenhagen

Odense

Aarhus

KoldingFredericia

Vejle

Aalborg

Triangle Area

EDC Research - November 2015 - page 4

MARKET UPDATE EDC

Facility class A Facility class B Facility class C Facility class A Facility class B Facility class C

Copenhagen Yield in % Yearly market rent in €/sq m

Prime 5.00 5.50 6.00 245 190 155

Secondary 5.50 6.00 6.75 190 150 130

Tertiary 6.75 7.25 7.75 150 130 110

Aarhus

Prime 5.25 5.75 6.25 185 145 120

Secondary 6.00 6.50 7.25 150 115 95

Tertiary 6.50 7.00 8.00 115 85 75

Aalborg

Prime 6.00 6.50 7.50 135 125 105

Secondary 6.25 7.25 8.00 125 110 95

Tertiary 7.25 8.00 8.50 110 90 75

Triangle area

Prime 6.75 7.00 7.25 145 105 75

Secondary 7.00 7.50 7.75 110 85 70

Tertiary 7.75 8.75 9.75 60 55 50

Odense

Prime 6.25 7.00 8.00 155 125 95

Secondary 7.00 8.00 9.00 135 110 90

Tertiary 8.00 9.00 10.00 90 85 70

Vacancy sq m As % of building stock Change % QoQ Change % YoY Forecast

Central Copenhagen 473,300 8.1 0.6 -0.4

East Jutland (including Aarhus) 282,800 9.3 -2.8 -3.2

North Jutland Region (including Aalborg) 153,600 7.9 -0.8 0.0

South Jutland (including the Triangle Area) 226,600 9.7 -0.6 -1.0

Funen (including Odense) 119,800 8.0 -0.8 -1.9

Yield in %, yearly market rent in €/sq m and forecast for the next 3-6 months

Vacant office space in sq m, in % of building stock and forecast for the next 3-6 months

Source: EDC Erhverv Poul Erik Bech. Data as of 1. October 2015.Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

Source: Oline ED-Statistikken (Oline ED-statistics), data as of 1. October 2015. Changes quarter on quarter and year on year. Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

O F F I C E - N O V E M B E R 2 0 1 5

Office

EDC Research - November 2015 - page 5

MARKET UPDATE EDC

Office Building stock Vacancy sq m Change sq m QoQ As % of building stock Change in % QoQ

Central Copenhagen 5,824,100 473,300 35,100 8.1% 0.6%

Copenhagen area 3,691,400 542,000 -21,100 14.7% -0.6%

North Zealand 1,585,500 151,900 -39,800 9.6% -2.5%

Bornholm 114,100 1,200 0 1.0% 0.0%

Capital Region of Denmark 11,215,200 1,168,400 -25,800 10.4% -0.2%

East Zealand 692,800 31,500 -2,800 4.5% -0.4%

West- and South Zealand 1,558,100 73,400 -300 4.7% 0.0%

Region Zealand 2,250,900 104,900 -3,000 4.7% -0.1%

Funen (including Odense) 1,493,200 119,800 -11,100 8.0% -0.8%

South Jutland 2,324,400 226,600 -12,200 9.7% -0.6%

Southern Denmark Region 3,817,600 346,400 -23,200 9.1% -0.6%

East Jutland 3,052,700 282,800 -86,200 9.3% -2.8%

West Jutland 1,396,300 71,200 -1,100 5.1% -0.1%

Central Jutland Region 4,449,100 354,000 -87,400 8.0% -1.9%

North Jutland 1,938,900 153,600 -15,200 7.9% -0.8%

Region North Jutland 1,938,900 153,600 -15,200 7.9% -0.8%

Denmark, total 23,671,700 2,127,300 -154,700 9.0% -0.6%

Vacant office space in sq m, in % of building stock and forecast for the next 3-6 months

Key vacancy figures from Oline ED-Statistikken (Oline ED-statistics)

Source: Oline ED-Statistikken (Oline ED-statistics), data as of 1. October 2015. "% of building stock" is the proportion of empty space in sq m relative to the total building stock.

Source: Vacancy data from Oline ED-Statistikken (Oline ED-statistics). Data as of 1. October 2015.Forecasts: EDC Erhverv Poul Erik Bech. All forecasts reflect our expectations for the development over the next 3 to 6 months.

Central East Jutland North Jutland Region South Jutland Funen Copenhagen (including Aarhus) (Including Aalborg) (including the (including Odense) Triangle Area)

O F F I C E - N O V E M B E R 2 0 1 5

0%

2%

4%

6%

8%

10%

12%

Central Copenhagen East Jutland(Including Aarhus)

Region North Jutland(Including Aalborg)

South Jutland(including theTriangle area)

Funen(including Odense)

473,300 sq m

282,800 sq m

153,600 sq m

226,600 sq m

119,800 sq m

EDC Research - November 2015 - page 6

MARKET UPDATE EDC

The map for office properties in Copenhagen/Aarhus illustrates a location segmentation in prime, secondary and tertiary locations, where the prime area typically has the best locations for office property in Copenhagen/Aarhus. The location segmentation has been made by EDC Erhverv Poul Erik Bech.

The location segmentation can change over time. The segmentation is our perception of general location segmenta-tion and should not be perceived as a definitive segmentation of the best, good and below average locations.

Copenhagen Aarhus

O F F I C E - N O V E M B E R 2 0 1 5

Location segmentation for offices

Copenhagen Aarhus

O2

O3

O2

O3

O4

151

151

E20

E20E20

E47

E47

156

201

21

2

1

22

23

20

4

3

8

18

21

1917

21

17

16 19

Frederiksberg

CPH airport

Orestad North

Orestad City

Orestad South

Norrebro

Outer Osterbro

Central Osterbro

Tuborg Harbour

VesterbroKalvebodBrygge

HavnefrontSouth

Nordhavn

CPH City

Vanlose

Bispebjerg

SoborgMorkhoj

UtterslevHusum

Hellerup

Valby

Vigerslev

Brondbyoster

Rodovre

Hvidovre

Avedore

Sundbyvester

Kastrup

Taarnby

GentofteGladsaxe

Amerika Square

Sydhavn

180

O1

O2

505

501

451

501

195

511

46

47

2

2019

18

E45

E45

15

15

26Tilst

Aarhus

Sotoften

Sabro

Lisbjerg

Lystrup

Egaa

Risskov

Olsted

Kasted

Skejby Vejby

Brendstrup

Geding

Kvottrup

Faarup

Skjoldelev

Borum

Yderup

True

LyngbyLabing

Brabrand

GellerupHasle

Marselisborg

Holme

Stavtrup

Aarslev

Aarslev Mark

Ormslev Stationsby

Ormslev Aabo

Lemming

Viby

BeringKolt

Kattrup

Horning Overballe

Jegstrup

Tranbjerg

Slet

Bjostrup

Skaade

Storhoj

HorretOsterby

Hasselager

Aaby

Aabyhoj

170

Location Facility class A Facility class B Facility class C

Prime 5.00 5.50 6.00

Secondary 5.50 6.00 6.75

Tertiary 6.75 7.25 7.75

Location Facility class A Facility class B Facility class C

Prime 245 190 155

Secondary 190 150 130

Tertiary 150 130 110

Yield in % and forecast for the next 3-6 months

Yearly market rent in €/sq m and forecast for the next 3-6 months

Location Facility class A Facility class B Facility class C

Prime 5.25 5.75 6.25

Secondary 6.00 6.50 7.25

Tertiary 6.50 7.00 8.00

Location Facility class A Facility class B Facility class C

Prime 185 145 120

Secondary 150 115 95

Tertiary 115 85 75

1 km1 km

Prime locations Secondary locations Tertiary locations

• Trains • Metro

Source: Vacancy data from Oline ED-Statistikken (Oline ED-statistics). Data as of 1. July 2015.

EDC Research - November 2015 - page 7

MARKET UPDATE EDCR E T A I L - N O V E M B E R 2 0 1 5

Facility class A Facility class B Facility class C Facility class A Facility class B Facility class C

Copenhagen Yield in % Yearly market rent in €/sq m

Prime 4.50 5.00 5.25 2,555 1,885 1,615

Secondary 5.75 6.00 6.50 500 340 270

Tertiary 7.00 7.50 7.75 150 130 110

Aarhus

Prime 5.00 5.25 5.50 740 605 475

Secondary 5.25 5.50 6.00 540 475 340

Tertiary 6.00 6.50 7.00 270 220 165

Aalborg

Prime 5.25 5.75 6.25 540 440 270

Secondary 6.25 6.50 7.00 175 145 95

Tertiary 7.00 7.50 8.00 85 70 60

Triangle area

Prime 5.75 6.00 6.25 405 325 190

Secondary 6.50 6.75 7.00 230 150 125

Tertiary 7.25 7.75 8.25 110 85 70

Odense

Prime 5.25 6.00 6.50 675 515 340

Secondary 6.00 6.75 7.50 405 270 175

Tertiary 8.00 9.00 10.00 110 85 55

Vacancy sq m As % of building stock Change % QoQ Change % YoY Forecast

Central Copenhagen 37,600 3.0 0.2 0.4

East Jutland (including Aarhus) 128,500 6.4 0.8 1.1

North Jutland Region (including Aalborg) 132,300 9.8 -0.2 0.8

South Jutland (including the Triangle Area) 150,200 8.9 -0.9 -0.8

Funen (including Odense) 71,200 5.6 0.1 0.5

Yield in %, yearly market rent in €/sq m and forecast for the next 3-6 months

Vacant retail space in sq m, in % of building stock and forecast for the next 3-6 months

Source: Oline ED-Statistikken (Oline ED-statistics), data as of 1. October 2015. Changes quarter on quarter and year on year. Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

Retail

Source: EDC Erhverv Poul Erik Bech. Data as of 1. October 2015.Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

EDC Research - November 2015 - page 8

MARKET UPDATE EDC

Retail Building stock Vacancy sq m Change sq m QoQ As % of building stock Change in % QoQ

Central Copenhagen 1,271,300 37,600 1,600 3.0% 0.2%

Copenhagen area 880,300 29,100 -2,400 3.3% -0.3%

North Zealand 1,081,900 59,700 -3,200 5.5% -0.3%

Bornholm 92,200 1,400 -1,000 1.5% -1.1%

Capital Region of Denmark 3,325,800 127,800 -5,100 3.8% -0.2%

East Zealand 437,000 30,900 800 7.1% 0.2%

West- and South Zealand 1,305,700 96,100 9,200 7.4% 0.7%

Region Zealand 1,742,700 127,000 10,000 7.3% 0.6%

Funen (including Odense) 1,277,000 71,200 900 5.6% 0.1%

South Jutland 1,688,400 150,200 -14,900 8.9% -0.9%

Southern Denmark Region 2,965,400 221,400 -14,100 7.5% -0.4%

East Jutland 2,008,700 128,500 15,400 6.4% 0.8%

West Jutland 1,029,200 77,200 3,200 7.5% 0.3%

Central Jutland Region 3,037,900 205,600 18,500 6.8% 0.6%

North Jutland 1,356,000 132,300 -2,900 9.8% -0.2%

Region North Jutland 1,356,000 132,300 -2,900 9.8% -0.2%

Denmark, total 12,427,700 814,100 6,400 6.6% 0.1%

Key vacancy figures from Oline ED-Statistikken (Oline ED-statistics)

Vacant retail space in sq m, in % of building stock and forecast for the next 3-6 months

Source: Oline ED-Statistikken (Oline ED-statistics), data as of 1. October 2015. "% of building stock" is the proportion of empty space in sq m relative to the total building stock.

R E T A I L - N O V E M B E R 2 0 1 5

Central East Jutland North Jutland Region South Jutland Funen Copenhagen (including Aarhus) (Including Aalborg) (including the (including Odense) Triangle Area)

Source: Vacancy data from Oline ED-Statistikken (Oline ED-statistics). Data as of 1. October 2015.Forecasts: EDC Erhverv Poul Erik Bech. All forecasts reflect our expectations for the development over the next 3 to 6 months.

0%

2%

4%

6%

8%

10%

Central Copenhagen East Jutland(Including Aarhus)

Region North Jutland(Including Aalborg)

South Jutland(including theTriangle area)

Funen(including Odense)

37,600 sq m

128,500 sq m

132,300 sq m

150,200 sq m

71,200 sq m

EDC Research - November 2015 - page 9

MARKET UPDATE EDC

Above Average Average Below Average Above Average Average Below Average

Capital Region of Denmark Yield in % Yearly market rent in €/sq m

Primary 6.50 7.00 7.50 150 135 125

Secondary 7.00 8.00 9.00 110 95 85

Region Zealand

Primary 7.00 8.00 9.00 125 110 95

Secondary 8.00 9.00 10.00 95 85 70

Central Jutland Region

Primary 7.00 7.25 7.50 150 135 125

Secondary 7.75 8.00 8.25 110 95 85

Region North Jutland

Primary 7.00 7.50 8.80 150 125 110

Secondary 7.50 8.00 8.50 125 110 95

South Jutland

Primary 7.25 7.50 8.00 150 135 125

Secondary 7.50 7.75 8.50 110 95 85

Tertiary 8.00 8.25 9.50 95 85 70

Funen

Primary 7.50 8.00 8.50 150 125 110

Secondary 8.25 9.00 9.50 125 110 90

Yield in %, yearly market rent in €/sq m and forecast for the next 3-6 months

Box retail

Source: EDC Erhverv Poul Erik Bech. Data as of 1. October 2015.Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

BOX RETAIL:

Box retail stores are typically located in external retail areas and selling goods that do not require unusually large quantities of floor space. In this publication, we do not include big box retailing with permission for selling items that require unusually large quantities of floor space according to the provisions in the Danish Planning Act (Planloven). Yield and rent estimates are stated as “above ave-rage”, “average”, “below average” for different areas (primary, secondary, tertiary).

B O X R E TA I L - N O V E M B E R 2 0 1 5

EDC Research - November 2015 - page 10

MARKET UPDATE EDCI N D U S T R I A L & L O G I S T I C S

N O V E M B E R 2 0 1 5

Facility class A Facility class B Facility class C Facility class A Facility class B Facility class C

Copenhagen Yield in % Yearly market rent in €/sq m

Prime 7.00 7.75 8.25 70 60 50

Secondary 7.50 8.25 8.75 60 55 45

Tertiary 8.00 9.00 9.50 50 45 35

Aarhus

Prime 7.50 8.25 9.00 55 45 35

Secondary 8.00 8.50 9.50 45 40 35

Aalborg

Prime 7.50 8.00 9.00 45 40 35

Secondary 8.75 9.25 10.25 35 35 25

Triangle area

Prime 7.75 8.25 8.50 45 40 35

Secondary 8.00 8.50 9.00 40 35 35

Odense

Prime 8.00 8.50 9.00 50 45 35

Secondary 8.50 9.50 10.50 45 35 25

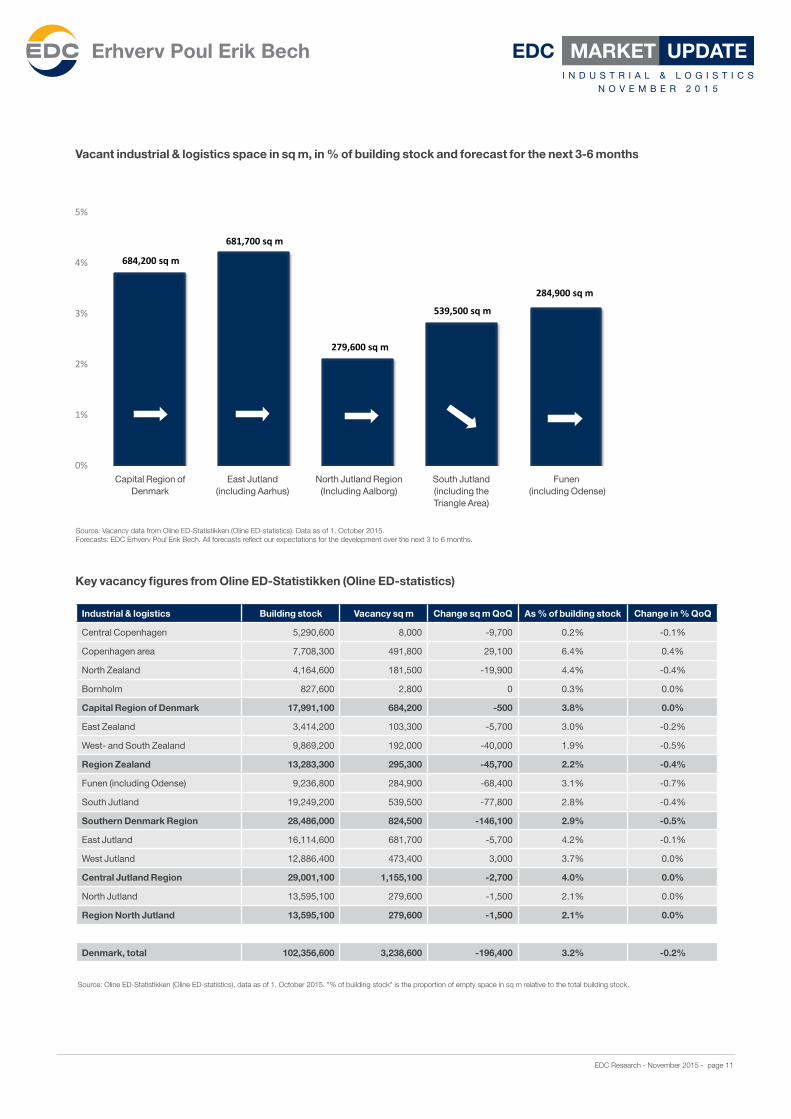

Vacancy sq m As % of building stock Change % QoQ Change % YoY Forecast

Capital Region of Denmark 684,200 3.8 0.0 -0.2

East Jutland (including Aarhus) 681,700 4.2 -0.1 0.0

North Jutland Region (including Aalborg) 279,600 2.1 0.0 0.1

South Jutland (including the Triangle Area) 539,500 2.8 -0.4 -0.9

Funen (including Odense) 284,900 3.1 -0.7 -0.2

Yield in %, yearly market rent in €/sq m and forecast for the next 3-6 months

Vacant industrial & logistics space in sq m, in % of building stock and forecast for the next 3-6 months

Source: Oline ED-Statistikken (Oline ED-statistics), data as of 1. October 2015. Changes quarter on quarter and year on year. Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

Industrial & Logistics

Source: EDC Erhverv Poul Erik Bech. Data as of 1. October 2015.Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

EDC Research - November 2015 - page 11

MARKET UPDATE EDCI N D U S T R I A L & L O G I S T I C S

N O V E M B E R 2 0 1 5

Industrial & logistics Building stock Vacancy sq m Change sq m QoQ As % of building stock Change in % QoQ

Central Copenhagen 5,290,600 8,000 -9,700 0.2% -0.1%

Copenhagen area 7,708,300 491,800 29,100 6.4% 0.4%

North Zealand 4,164,600 181,500 -19,900 4.4% -0.4%

Bornholm 827,600 2,800 0 0.3% 0.0%

Capital Region of Denmark 17,991,100 684,200 -500 3.8% 0.0%

East Zealand 3,414,200 103,300 -5,700 3.0% -0.2%

West- and South Zealand 9,869,200 192,000 -40,000 1.9% -0.5%

Region Zealand 13,283,300 295,300 -45,700 2.2% -0.4%

Funen (including Odense) 9,236,800 284,900 -68,400 3.1% -0.7%

South Jutland 19,249,200 539,500 -77,800 2.8% -0.4%

Southern Denmark Region 28,486,000 824,500 -146,100 2.9% -0.5%

East Jutland 16,114,600 681,700 -5,700 4.2% -0.1%

West Jutland 12,886,400 473,400 3,000 3.7% 0.0%

Central Jutland Region 29,001,100 1,155,100 -2,700 4.0% 0.0%

North Jutland 13,595,100 279,600 -1,500 2.1% 0.0%

Region North Jutland 13,595,100 279,600 -1,500 2.1% 0.0%

Denmark, total 102,356,600 3,238,600 -196,400 3.2% -0.2%

Key vacancy figures from Oline ED-Statistikken (Oline ED-statistics)

Vacant industrial & logistics space in sq m, in % of building stock and forecast for the next 3-6 months

Source: Oline ED-Statistikken (Oline ED-statistics), data as of 1. October 2015. "% of building stock" is the proportion of empty space in sq m relative to the total building stock.

Source: Vacancy data from Oline ED-Statistikken (Oline ED-statistics). Data as of 1. October 2015.Forecasts: EDC Erhverv Poul Erik Bech. All forecasts reflect our expectations for the development over the next 3 to 6 months.

Capital Region of East Jutland North Jutland Region South Jutland Funen Denmark (including Aarhus) (Including Aalborg) (including the (including Odense) Triangle Area)

0%

1%

2%

3%

4%

5%

Capital Region ofDenmark

East Jutland(Including Aarhus)

Region North Jutland(Including Aalborg)

South Jutland(including theTriangle area)

Funen(including Odense)

684,200 sq m

681,700 sq m

279,600 sq m

539,500 sq m

284,900 sq m

EDC Research - November 2015 - page 12

MARKET UPDATE EDCR E S I D E N T I A L R E N TA L P R O P E RT I E S

N O V E M B E R 2 0 1 5

Newer residential rental properties

Facility class A Facility class B Facility class A Facility class B

Copenhagen Yield in % Yearly market rent in €/sq m

Prime 4.25 4.75 265 230

Secondary 5.00 5.25 240 205

Tertiary 5.25 5.50 205 170

Aarhus

Prime 4.25 4.50 220 190

Secondary 4.50 4.75 185 150

Tertiary 5.00 5.25 165 135

Aalborg

Prime 4.50 4.75 150 130

Secondary 5.25 5.50 130 115

Tertiary 5.75 6.25 115 110

Triangle area

Prime 6.00 6.75 135 125

Secondary 6.75 7.00 110 95

Odense

Prime 5.00 5.50 170 130

Secondary 5.75 6.00 145 115

Older residential rental properties Fully developed older residential rental properties

Facility class A Facility class B Facility class C Facility class A Facility class B Facility class A Facility class B

Copenhagen Yield in % Yield in % Yearly market rent in €/sq m

Prime 3.00 3.25 4.00 4.50 4.75 205 185

Secondary 3.50 4.00 4.75 5.00 5.25 185 170

Tertiary 4.50 5.00 6.00 5.25 5.50 150 135

Aarhus

Prime 2.50 2.75 3.00 3.75 4.25 190 170

Secondary 3.00 3.25 3.50 4.25 5.00 155 145

Tertiary 4.00 4.25 4.50 5.00 5.50 135 115

Aalborg

Prime 3.75 4.50 5.00 4.75 5.00

Secondary 4.75 5.25 5.50 5.25 5.50

Tertiary 6.50 6.75 7.25 6.00 6.25

Triangle area

Prime 6.00 6.50 7.25 6.25 6.50

Secondary 7.00 7.25 8.00 6.75 7.00

Tertiary 7.75 8.00 8.50 7.75 8.00

Odense

Prime 4.50 5.00 5.75 5.00 5.50

Secondary 5.00 5.75 6.00 5.50 6.00

Yield in %, yearly market rent in €/sq m and forecast for the next 3-6 months

Note: ”Older residential rental properties” and “Fully developed older residential rental properties” are regulated by the provisions in the Danish Rent Act (Lejeloven) and the Housing Regu-lation Act (Boligreguleringsloven) concerning cost driven rental levels.

“Newer residential rental properties” taken in to use no earlier than 1 April 1992 are subject to the rules concerning free market rent, pursuant to the Housing Regulation Act § 15 A and others.

Residential rental properties

Source: EDC Erhverv Poul Erik Bech. Data as of 1. October 2015. Forecasts: All forecasts reflect our expectations for the development over the next 3 to 6 months.

EDC Research - November 2015 - page 13

MARKET UPDATE EDC

Hard work, ethics and a solid business sense

– were the three pillars on which I founded my company in 1978. These core values are still the same and their legitimacy has been confirmed by good results, solid growth and satisfied clients.

Hard work is part of our culture which is deeply rooted throughout the company. Every day our employees do their utmost to provide our clients with knowledge-based advice and first-class service and our phones are open from 7 a.m. to 9. p.m. - 365 days a year.

Our ethics mean you can have confidence in us; in our dedication and our business ethics, in our way of working together, and in our transparent processes that provide our clients with security and overview.

A solid business sense is your guarantee for a satisfactory and profitable business outcome. Our focus is representing our clients and their interests in the most optimal way possible. The performance of our experienced specialists is continuously assessed with regards to competence, performance and negotiating skills to ensure our clients always have confidence in the quality of our services.

Nationwide commercial real estate company – with local knowledge

Our commitment to our core values has turned EDC Poul Erik Bech in to a nationwide company with a strong presence in Denmark. Our 15 commercial offices ensure that we have in-depth knowledge of the local area and the market as a whole. We continuously work actively and highly focused to have the industry’s most powerful network in order to be up to date with the changing market and our clients’ needs.

We look forward to working with you.

Poul Erik BechChairman

N O V E M B E R 2 0 1 5

International division

Purchases

Letting services

Sale & Lease

BackAdvisory

Property & facilities

management

Developer advisory

Selling of development

projects

Selling

Valuations(RICS)

EDC Property Invest

– a complete solution for commercial property

EDC Research - November 2015 - page 14

MARKET UPDATE EDCN O V E M B E R 2 0 1 5

Why invest in Danish real estate?

• Low transaction costs

• High degree of market transparency and stability

• Low financing rates through Danish mortgage credit institutions

• Solid key economic indicators

• AAA/A-1+ credit rating and stable outlook** S&P as of 27 March 2015.

Low financing rates

• Low origination costs

• Low APR compared to the majority of European markets

• Highly transparent, stable and liquid mortgage bond market

• Flexible loans on conditions close to funding conditions of capital market players

Why invest in Denmark

The Danish mortgage system

Loan

Borrower InvestorMortgage institution

Repayment. interest and

marginRepayment and interest

Bonds

Investment

EDC Research - November 2015 - page 15

MARKET UPDATE EDCN O V E M B E R 2 0 1 5

• Low financing rate: Bond yield plus a small markup (margin) for the mortgage bank

• Debt/value ratio: Financing through the mortgage institutions, normally up to 60% of valuation

• Loan maturity: Min. 1 year (yearly refinancing), max. 20 years

• Payment structure: Floating or fixed rates, with or without quarterly principal repayments

• Each new loan is in principle funded by the issuance of new mortgage bonds of equal size and identical cash flow and maturity characteristics, called the Balance Principle. Proceeds from the sale of the bonds are passed on to the borrower and similarly, interest and principal payments are passed directly to investors holding mortgage bonds

• The Danish mortgage institutions have existed since 1850 and are considered very strong and very low risk financial instruments

• In terms of volume outstanding, Denmark has the second largest share of the mortgage bond market in Europe

• There has never been an incidence of default on a Danish mortgage bond

Low transaction costs

As buyer:

Deed registration: 0.6% of purchase price + € 190

Mortgage: 1.5% of the mortgage’s principal +€ 190

Costs for own advisor, lawyer, agent etc. are typically very low

As seller:

Agent, lawyer etc. varies, but typically between 1 - 4% of purchase price depending on deal size

Denmark is known to have some of the lowest roundtrip property transactions costs

2014 2015 2016

GDP growth (%), YOY

Denmark 1.1 1.8 2.1

EU 1.4 1.8 2.1

Unemployment rate (%)

Denmark 6.6 6.2 5.9

EU 10.2 9.6 9.2

Current account balance (% of GDP)

Denmark 6.2 6.1 6.2

EU 1.6 1.9 1.9

Inflation (%)

Denmark 0.3 0.6 1.7

EU 0.6 0.1 1.5

Source: The Economic forecast (Spring forecast 2015) from the European Commission.

Solid key economic indicatorsHigh degree of transparency

Denmark is among the most transparent markets in Euro-pe and worldwide*. The transparent Danish market provi-des the investor with a secure and low risk environment for foreign direct investment.

Investments in Denmark are conducted in a market which benefits from a highly transparent and stable legal and re-gulatory framework coupled with a simple transaction process.

*In the recent 2014 version of the Jones Lang LaSalle Global Real Estate Transparency Index ®,Denmark was rated a transparent market and ranked no. 16 worldwide, when it comes to market transparency.

Lease structure

• Rent adjustment, normally adjusted yearly with the rate of inflation or a fixed minimum rate

• Rent review every fourth year. Terms are flexible

• It is possible to agree on a threshold for the rent. Eg. the rent cannot drop further than the rent in force at the start of the tenancy

• The landlord and the tenant can freely agree on the rent amount as long as the rent is not unreasonable or contrary to sound business practices

• Lease length: There are no statutory restrictions on the duration of a commercial lease agreement. It is normal to have interminable leases in place

• The leading real estate agency in Denmark in the areas of selling, leasing, valuation and advisory

• Founded in 1978, operating nationwide across 15 commercial real estate branches, more than 45 residential real estate branches, and finally 3 residential real estate branches in France and Sweden.

• Owner of the property management company LEA Ejendomspartner

• More than 450 employees

Our greatest strength is our nationwide presence and local knowledge with 70 commercial specialists servicing our clients. We are chartered surveyors, valuers and certified members of RICS. We espe-cially deal with the following types of properties:

• Investment properties, properties for rent and owner-user properties

• Offices, high street retail, industrial & logistics and mixed-use properties

• Residential rental properties

• Land and development projects

• Hotels, restaurants and other properties in the leisure sector

We offer our clients a wide range of services:

• Execution of investment transactions of single assets. portfolios and on a company level

• Letting services

• Valuations (RICS)

• Sale and Lease Back

• Due diligence

• Project development consultancy

• Property and facilities management

• Capital structure advisory

• Tenant and landlord representation

• EDC Location Search

• EDC PropertySWAP®

• Research services

• Bespoke consultancy and market study services

CHARTERED SURVEYORS & INTERNATIONAL PROPERTY CONSULTANTS

Copenhagen Herlev Hillerod Roskilde +45 33 30 10 00 • [email protected] +45 44 57 03 37 • [email protected] +45 48 26 99 10 • [email protected] +45 46 33 33 33 • [email protected]

Koge Naestved Odense Kolding +45 55 35 55 53 • [email protected] +45 55 78 66 03 • [email protected] +45 58 58 82 00 • [email protected] +45 76 33 80 10 • [email protected]

Aabenraa Sonderborg Esbjerg Vejle +45 73 33 13 00 • [email protected] +45 58 58 80 20 • [email protected] +45 76 10 48 00 • [email protected] +45 75 83 13 11 • [email protected]

Holstebro Aarhus Aalborg +45 58 58 77 10 • [email protected] +45 87 30 99 30 • [email protected] +45 96 31 49 00 • [email protected]

Read more: edc.dk/erhverv

Office locations:

![[May2012] edc](https://img.dokumen.tips/doc/110x75/55cf881955034664618d5a8b/may2012-edc.jpg)