Embed Size (px)

Citation preview

Japanese Yen 010Taiwanese Dollar ndash010Canadian Dollar ndash022British Pound ndash024Swedish Krona ndash054Swiss Franc ndash061Brazilian Real ndash063Singapore Dollar ndash064Mexican Peso ndash065Danish Krone ndash067

TOP CURRENCY PERFORMERSOne day spot return in percent

top currency performers

-1994

-5029

-1211

00

-1413

-1677

-672

-120

-1727

-5083

-1486

-1013

-1579

-1768

-725

-249

-600 -500 -400 -300 -200 -100 0

Greece

Ireland

Italy

Portugal

Spain

Belgium

France

Europe10Y Spread Distance FromHighs (Yesterday)10Y Spread Distance FromHighs (Today)

data reports (new york time)

continued on next page

most read on bloomberg

economic-events calendarTIME

KEEnErsquosCornEr

TIME EVEnT surVEy PrIor

recent Decline in unemployment May reverse Come spring

930 EC ECB Calls for Bids in 7-Day Refinancing930 EC ECB Announces Bond Purchases1100 US Fed to Purchase $425-5bln Notes2245 JN Japan to Sell 2-Year NotesTBA CO Overnight Lending RateTBA US Treasury Releases Borrowing Estimates

830 US Personal Income 040 010

830 US Personal Spending 010 010

830 US PCE Deflator (YoY) - 250

830 US PCE Core (MoM) 010 010

830 US PCE Core (YoY) 170 170

1030 US Dallas Fed Manf Activity - -3

Greek Talks risk Derailing Eu summitrsquos Plan

sarkozy says France to Impose Transaction Tax

Portugal May Get Little relief From Greek Debt Deal

China Preserves Ammunition With rrr on Hold

Loonie reaches us Parity as Aussie overvalued

WHAT TO WATCH European Union leaders will meet in Brussels at 9 am for a summit on deficit reduction the regionrsquos bailout funds and a second rescue package for Greece final press conferences 1 pm US personal spending prob-ably rose 01 percent for a third consecutive month according

to estimates ahead of a report 830 am Portuguese credit-default swaps rose to a record 395 percent upfront signaling a 71 percent chance of default in five years said CMA Spainrsquos economy shrank 03 percent in the fourth quarter The countryrsquos wors-ening situation is ldquocredit negativerdquo and will complicate efforts to reduce the budget said Moodyrsquos

ECONOMICS France plans to sell up to 83 billion euros ($109 billion) of debt matur-ing in less than a year 9 am Dallas Fed manufacturing activity est 05 1030 am South Korean industrial production 6 pm Japanese manufacturing PMI 615 pm Italy sold 75 billion euros ($98 billion) of debt near its maximum borrowing costs on 2022 bonds fell to 608 percent from 698 percent on Dec 29

GOvErNMENT republican presidential candidates enter the last full day of campaigning before tomorrowrsquos Florida primary France will unilaterally impose a tax on financial transactions starting in August said President Nicolas Sarkozy

MArKETS Asian and European stocks declined The euro weakened Crude oil fell US Treasuries rose pushing five-year yields to a record low

FirSt WorD DAybook

Heather burke and brad Skillman

Gerard Lyons on the lsquofragile Westrsquo lsquoresilient Eastrsquo and Chinarsquos soft landing

10y spreads distance from HigHs

Big Picture GueSt CoMMeNtAry by JeFFrey GreeNberG AND AiCHi AMeMiyA NoMurA

at any other time since the survey began in 1946 We do not discount the improve-ment in the labor market but we find reasons to be wary of recent movements in the unemployment rate

Could recent history repeat itself be-tween November 2010 and March 2011 the unemployment rate (as reported) fell a full percentage point to 88 percent only to reverse to 92 percent by June 2011 We believe current unemployment data is likely to succumb to the same pattern

the unemployment rate fell to 85 per-cent in December declining for a fourth straight month and recording its lowest level since February 2009 While unem-ployment remains ldquostubbornly highrdquo as Cleveland Fed President Sandra Pianalto phrased it the recent improvement in labor market statistics has not gone unnoticed in Januaryrsquos preliminary release of the thomson reutersuniversity of Michigan Survey of Consumers more consumers re-ported hearing of employment gains than

Eu summit Personal spending spain Auctions

1 2 3 4 5 6 7 8 9 10 11 12

013012brief NEwS ANALYSIS amp COMMENTARY

Monday

wwwbloombergbriefscomEconomics

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

January 2009 -29mn

-3000

-2500

-2000

-1500

-1000

-500

0

500

Jan-49 Jan-55 Jan-61 Jan-67 Jan-73 Jan-79 Jan-85 Jan-91 Jan-97 Jan-03 Jan-09

Change in EmploymentJanuary month-to-month change in employed not seasonally-adjusted (Household survey)Median+- 2 standard deviations

000s

Source Nomura Securities

03

-02

-03

-02

-01

0

01

02

03Difference Between Official and Alternative Employment pp

Δ (Nov 10 - Jan 11) = 05pp

Source Nomura Securities

Why A sharp decline in labor market indica-tors caused by the financial crisis in late 2008-early 2009 has led to imperfect sea-sonal adjustments to detect the distortion we reconstructed the seasonally-adjusted unemployment rate from unadjusted data for the main constituents the bureau of Labor Statistics (bLS) uses in its unemployment rate calculation but excluded the critical months of the financial crisis for the purposes of seasonal adjustment

We consider the difference between the official data series and our alternative to represent the ldquoseasonal biasrdquo in the unem-ployment rate While the two series have the same trend the impact on month-to-month changes in unemployment can be material For instance the difference between the up-ward bias (where the reported unemployment rate is higher than underlying) in November 2010 and the downward bias in January 2011 accounted for 05 percent of the 07 percent-age point unemployment rate decline over that period

Likewise wersquove found that nearly the entire decline in the December 2011 unemployment rate to 85 percent from 87 percent can be explained by seasonal bias Furthermore we forecast the unemployment rate will decline further to 83 percent in January again helped by a downward seasonal bias Come April the seasonal bias should reverse and the unemployment rate may as well

Special factors driving the unemployment rate decline give little reason for celebration be-cause the unemployment rate falls when unem-ployed persons stop looking for work (and are no longer in the labor force) we calculate the unemployment rate including these labor force ldquoexitersrdquo After first adjusting for demographic trends in labor force participation we find this broader measure of the unemployment rate to be 103 percent in December as opposed to the reported 85 percent it has been greater than 10 percent since September 2009

FoMC participants still see considerable slack in the labor market even as the official unemployment rate has recently trended downward Chicago Fed President Charles evans commented that the decline ldquomay be transitoryrdquo and that an 85 percent unemploy-ment rate is ldquopossible at the end of 2012rdquo Chairman bernanke expressed his ongoing concern about employment conditions in his first press conference of 2012 by saying ldquoif the situation continues with inflation below target

Big Picturecontinued from page 1

JeFFrey GreeNberG AND AiCHi AMeMiyA

and unemployment declining at a rate which is very very slow then our frame-work the logic of our framework says we should be looking for ways to do morerdquo

the recent decline in the unemploy-ment rate does not change the fear that cyclical unemployment could become structural to be sure the share of long-term unemployed (more than 27 weeks) has risen from 174 percent of total unemployed at the start of the recession to 425 percent four years later While no FoMC participants estimated that the longer run (natural)

unemployment rate exceeded 6 percent just three years ago now nearly a third of participants do the FoMCrsquos latest economic projections reveal partici-pants forecast the unemployment rate to be 67-to-76 percent in the fourth quarter of 2014 We believe the concern that unemployment could become more entrenched if unaddressed will motivate more action and expect the FoMC to continue its Sisyphean task of reaching full employment by announcing further expansion of the balance sheet in the second quarter of this year

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 2

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

BUSINESS HAS SUFFERED A SERIOUS BLOW JOIN THE RECOVERY TEAM

In a world of financial risk organizations can never be too prepared Thatrsquos why more global companies are relying on Certified Financial Risk Managers As an FRMreg yoursquoll be recognized for mastering the complexities of credit market and operational risks Yoursquoll also play a critical role in the financial well-being of banks consultancies corporations and asset management firms If you want to be part of the solution take the first step by earning your FRM certification Visit the Global Association of Risk Professionals (GARP) at garporgfrm

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 3

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

2400120060030015007500ndash075ndash150ndash300ndash600ndash1200ndash2400

Daily Percentage Change of the Global Equity Markets

PoLITICAL WATCH by bLooMberG NeWS

annual growth the previous quarter

Polish consumer confidence fell to an index reading of minus 571 in January from minus 568 in December

Italian business confidence fell to an index reading of 921 in January the lowest since November 2009 from 925 in December economists predicted 923

Global Equity Performance

Gingrich Invokes GoldmanNewt Gingrich accusing republican

presidential primary opponent Mitt romney of being a ldquofundamentally dishonestrdquo tool of Wall Street pledged to stop banking firms such as Goldman Sachs Group from ldquorigging the gamerdquo Pressing his campaign into the last full day before Floridarsquos primary tomor-row Gingrich spoke of running a White House that would ldquochallenge the system head-onrdquo and disrupt the ldquoWall Street eliterdquo ldquoto the degree they survive by rig-ging the gamerdquo he said ldquothey have a lot more to fear to the degree that theyrsquore willing to be in a very investment-orient-ed high-tempo entrepreneurial world they have more to gainrdquo

States Lag on InsuranceStates with the most residents who

would benefit from expansion of medi-cal coverage have been the slowest to set up the insurance exchanges re-quired under the health-care overhaul a study found Fifteen states have made little progress on creating the markets in the almost two years since the law was signed according to the study by the robert Wood Johnson Foundation and the urban institute those same states could reduce the number of uninsured residents by an average of 53 percent compared with 42 percent for states that have already taken legislative steps to create exchanges and a national average of 48 percent the study found

New Zealandrsquos Bollard to QuitNew Zealand central bank Governor

Alan Bollard will quit in September ending a decade-long tenure in which he raised interest rates to a record high before cutting them last year to their lowest ever bollard wonrsquot seek another five years when his current term ends Sept 25 the reserve bank of New Zealand said the central bank said it will search in New Zealand and abroad for a successor the move leaves New Zealand searching for a new central bank chief during a period of slowing global growth and a sluggish domestic economy thatrsquos motivating young peo-ple to leave in search of higher-paying jobs in Australia and elsewhere

oVErnIGHT By BloomBerg News

euroPe

Euro-area confidence in the economic outlook improved to an index reading of 934 in January from a revised 928 in De-cember the median estimate was 938

Spainrsquos economy shrank 03 percent in the fourth quarter from the previous three months GDP grew 03 percent from the prior year compared with 08 percent

Lithuaniarsquos economy expanded 43 percent in the fourth quarter from the prior year after growing 67 percent the previ-ous three months the median estimate was an increase of 6 percent

AsiA

Taiwanrsquos unemployment rate declined to 422 percent in December from 432 percent in November the median esti-mate was 433 percent

The Philippine economy expanded 37 percent in the fourth quarter from a year earlier that compares with a revised 36 percent increase in GDP the previous three months economists forecast a 38 percent gain

South Korearsquos current-account sur-plus narrowed to $396 billion in Decem-ber a three-month low from a revised $456 billion in November

Thailandrsquos economy contracted 5 percent in the fourth quarter of 2011 the finance ministry said it grew 11 percent for the full year

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 4

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

10

11

12

13

14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source US Bureau of Labor Statistics

Union Membership ( of Employed)

Source Bureau of Labor Statistics

FACE OFFMArKET CALLsby bLooMberG NeWS

Far From its Peak union Membership Increased only slightly in 2011

Standard Chartered Plcrsquos Jaspal Bindra chief executive officer for Asia said the Fedrsquos pledge to keep interest rates low through at least late 2014 creates a risk of hyperinflation in Hong kong ldquoif you have near-zero interest rates when their inflation is at over 6 or 7 per-cent given the China effect and their growth is also thanks to China at 6 or 7 percent yoursquore looking for hyperinflationrdquo he said

richard Koo chief economist at Nomura research institute said Japan should limit intervention to weaken the yen because a strong currency keeps the cost of fuel imports low as the nationrsquos nuclear capac-ity dwindles ldquoright now irsquom not pushing loudly for interventionrdquo said koo

viktor Shvets a Hong kong-based strate-gist at Samsung Securities Co said uS economic growth ldquowill be stuck between 15

percent and 25 percent for years to comerdquo with occasional quarters of zero or near-zero growth

ronald Stoeferle a commodity analyst at erste Group bank AG said gold prices may rise 33 percent further to a record $2300 an ounce early next year accord-ing to technical analysis ldquoWe are seeing a momentum in goldrdquo Stoeferle said

Morgan Stanley economist Pasquale Diana said Hungaryrsquos benchmark inter-

est rate may have peaked at 7 percent after the central bank unexpectedly left the two-week deposit rate unchanged last week A ldquomodest rallyrdquo or a ldquostabilization of risk metricsrdquo may be sufficient to begin rate cuts Diana said

Goldman Sachs economist Ahmet Akarli said a reduction of turkeyrsquos current account deficit may have reversed leaving it the most vulnerable economy in the region Financial conditions in the country are too loose he said

According to the bureau of Labor Statistics the number of union members increased negligably in 2011 to 14764 million from 14715 million in 2010 As a percentage of total employment in the uS union membership in 2011 slipped to 118 percent from119 percent the prior year the bLS doesnrsquot have a complete set of union membership data compa-rable union enrollment figures date only back to 1983 when there were 177 mil-lion union workers and the membership rate was 201 percent

We do know that in 1950 roughly one out of every three workers was em-ployed in the manufacturing sector with the same percentage carrying a union card today with nearly 83 percent of private industry workers employed in the services sector the percentage and number of union workers have both de-clined Manufacturers comprise only 103 percent of all private workers while 50 percent are employed in the construction sector employment in the manufacturing sector today (1179 million) is at the same level as it was in 1941

Membership in the united Auto Workers

been furloughed at an elevated pace Current union membership is dominated by government workers As a percent of total union workers 1004 million (281 percent) were federal 1973 million (315 percent) state and 4947 million (317 percent) local

mdash Richard Yamarone Bloomberg economist

union peaked in 1979 at 15 million work-ers while according to its website the uAW today has only 390000 members there were roughly 600000 retirees on pension and medical care plans being supported by that level of membership

in addition to the Housing and Auto sectors government workers have also

Hiroki Shimazu of SMBC Nikko Securities forecasts a 04 increase in personal spending up from 01 percent previously

Ellen ZentnerDavid resler of Nomura Securities predict no change in per-sonal spending the median bloomberg survey forecast is 01 percent

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 5

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

0

25

50

75

100

125

-10

0

10

20

30

40

2003 2004 2005 2006 2007 2008 2009 2010 2011

difference (RHS)

exports to US amp EU (LHS)

exports to Asia ex Japan (LHS)

$bn

Source CEIC RBC

$bn

China South Korea Taiwan Hong Kong Singapore Export Destinations

17 17

15 -01

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2005 2006 2007 2008 2009 2010 2011 2012

US GDP growth - change in rate (pp)euro-area GDP growth - change in rate (pp)US GDP growth ()euro area GDP growth ()

Sources RBC Bloomberg

percent

RBC forecasts

US Euro-Area GDP Growth

rise in Intra-regional Exports to Help support Asia as us Eu Demand slows

Growth prospects for China and other emerging-market Asian countries in 2012 will depend on how their exports perform exports fell very sharply in late 2008 and early 2009 and the recent deterioration in the global outlook raises concerns about another slump in external demand

Asian export performance remains heav-ily dependent on growth in the uS and the euro-area in addition to direct trade with these economies much of Asiarsquos intra-regional trade consists of intermedi-ate goods for which the final demand is from the uS and the euro-area

Looking ahead further deteriora-tion in the regionrsquos export performance seems likely in coming months mainly reflecting the weaker euro area outlook recent exchange rate moves provide an additional reason to suspect that euro-area demand will remain weak over the last six months emerging-market Asian currencies have appreciated significantly against the euro most recording gains of 4 percent to 10 percent over this period with the Chinese yuan up around 12 per-cent emerging-market Asian exporters however have gained competitiveness with uS customers over this period with most regional currencies around 3 percent to 7 percent weaker against the dollar

Given that uS and euro-area growth is unlikely to weaken in 2012 as sharply as they did a few years ago Asian exports should perform better than they did a few years ago

exports remain near record levels in China and other parts of Asia suggesting that even modest growth rates in external demand will provide significant support to domestic activity across the region

in addition major Asian economies are now exporting significantly more to their own region than they are in aggregate terms to the uS and the european union with this amount averaging around $24 billion per month in 2011 this strongly suggests that much of the recent increase in intra-regional trade in Asia reflects stronger final demand from within the re-gion rather than from the uS and the eu

in other words Asia is still vulnerable to weaker growth in the uS and europe but this vulnerability is less pronounced

than previously in the case of China Asian economies excluding Japan is by far the most important market for Chinese exporters indeed China exports more to the rest of Asia excluding Japan than it does to the uS and the eu combined Chinese exports to Asia excluding Japan have soared since early 2009 and remain near record levels in recent months

this pattern is even more pronounced for South korea taiwan Hong kong and Singapore the exports they send to each other China and the rest of Asia excluding Japan far exceed those sent to other mar-kets indicative of growing final demand in the region as per capita incomes rise

the fact that the performance of Asian exports increasingly depends on final demand from within Asia itself highlights

the importance of policy moves to support domestic demand Fiscal policy is already supportive in much of Asia officials have in recent months halted and in some cases started to reverse tighter monetary policy settings put in place over 2010 and 2011 a trend that should support liquidity and activity in coming months this com-bined with optimism that external demand from the uS may stabilize or show signs of recovery suggests that exports and headline GDP growth in Asia will likely continue to moderate early in 2012 before picking up again later in the year

(Brian Jackson is the senior emerging markets strategist at RBC Capital Markets in Hong Kong He previously worked as an economist at the Bank of England and an analyst at the Federal Reserve Bank of New York)

AsIA WATCH BriaN jacksoN rBc capital markets guest columNist

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 6

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Perc

enta

ge C

hang

e

Stressed Consumers

Real Personal Disposable Income Real Spending

Source Bloomberg PIDSCWT PCE CHY INDEXltGOgt

-25

-20

-15

-10

-5

0

5

10

15

20

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Housing Market Contracts at Slower Pace

House Price Index Case-Shiller 20-City Home Price Index

Source Bloomberg HPIMYOY SPCS20Y INDEXltGOgt

30

35

40

45

50

55

60

65

70

75

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Manufacturing Remains StoutChicago PMI ISM Manufacturing

Source Bloomberg CHPMIND INDEXltGOgt NAPMPMI INDEXltGOgt

-1000

-800

-600

-400

-200

0

200

400

2007 2008 2009 2010 2011

ADP Private Job Creation

ADP Estimate of Private Payrolls BLS Estimate of Private Payrolls

Source Bloomberg ADP CHNG NFP PCH INDEXltGOgt

8

9

10

11

12

13

14

15

16

17

18

2006 2007 2008 2009 2010 2011

Total Vehicle Sales

Source Bloomberg SAARDTOT INDEXltGOgt

on an inflation-adjusted basis personal disposable income declined 01 percent and average hourly earnings 09 percent over the past year Consumers appeared to pull back on spending in December and may continue to slow in January

the bloomberg consensus forecast expects a gain of 150000 in total employment to kick off 2012 temporary retail and transportation jobs are expected to subtract from it the un-employment rate is forecast to hold steady at 85 percent

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400BLS Non-Farm Payroll Estimate

3-Month Average Change in Total Employment

S NFP TCH INDEXltGOgt

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400BLS Non-Farm Payroll Estimate

3-Month Average Change in Total Employment

S NFP TCH INDEXltGOgt

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

1989 1994 1999 2004 2009

BLS Non-Farm Payroll Estimate

3-Month Average Change in Total Employment

S NFP TCH INDEXltGOgt

Given widespread skepticism about the quality of job gains in December it would not be surprising to see a significant downward revision of last monthrsquos ADP estimate and job gains are barely enough to keep pace with demographic changes

regional manufacturing surveys and the 105 percentage point spread between new orders and inventories suggests conditions are ripe for a sustained increase in industrial production

the Case-Shiller home price index is likely to show the de-cline in home prices accelerated in November the CoreLogic data a solid forward-looking indicator for the Case-Shiller index fell 16 percent on the month

December retail sales data fell flat after a strong start to the holiday shopping season the December employment report indicated an increase in aggregate hours worked and average hourly earnings that should bolster nominal incomes

investors will in-tensely focus on an array of labor market and manufacturing data for the first month of 2012 following the weaker-than-anticipat-ed 28 percent pace of growth to close out 2011 Given that inven-tory building by firms accounted for roughly 62 percent of growth in the fourth quarter there is considerable risk to the consensus 2 percent forecast of growth in the cur-rent quarter there is a strong possibility after three months of improving economic numbers that the data flow will look quite pessimistic through mid-2012

Labor Market Manufacturing Data Provide First Look at 2012 Economy

EConoMICs PrEVIEW JoSePH bruSueLAS bLooMberG eCoNoMiSt

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 7

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

Non-commercial accounts have increased their net holdings of oil for the last five weeks most recently by 15199 contracts to 305249 contracts the position may continue to rise as political ten-sions in the Middle east escalate it is in line with the one-year average

Speculators have increased their holdings of gold for the last three consecutive weeks that may be a response to the intensification of the european sovereign debt crisis During the latest reporting period they purchased 9019 contracts on a net basis bringing the net long position to 155027 contracts

Energy ProductsGold

As uS stocks rallied non-commercial accounts sold uS treasury securities across the maturity spectrum creating a total reduction of 214893 contracts they unloaded two- (1023 contracts) five- (55989 contracts) 10- (137880 contracts) and 20- (20001 contracts) year instruments

Speculators boosted their net short position in the euro to a fresh high of 169740 contracts after sell-ing 11145 contracts on a net basis during the week ended Jan 24 the position remains overstretched it is 22 standard deviations below the one-year average and the ratio of net longs to open inter-est stands at 047 by contrast they bought 8919 contracts on the uS dollar increasing the net long position to 84270 contracts

US Treasury SecuritiesCurrencies

in the week that followed the SampP downgrade of several euro-area nations speculators continued to sell the euro and buy the uS dollar according to data from the Commodity Futures trading Commission though they dumped treasury securities as the SampP rallied they continued to slowly increase their exposure to gold and oil

CoMMITMEnTs oF TrADErs DaviD powell BloomBerg ecoNomist

-200000

-150000

-100000

-50000

0

50000

100000

150000

200000

2111 4111 6111 8111 10111 12111

EUR JPY GBP CHF

CAD AUD NZD USD

Contracts

Source Bloomberg Note 1 USD contract = $200000 Futures + Options

0

50000

100000

150000

200000

250000

300000

350000

2111 4111 6111 8111 10111 12111

Gold

Source Bloomberg Note Futures + Options

Contracts

-300000

-200000

-100000

0

100000

200000

300000

400000

2111 4111 6111 8111 10111 12111

2-Year 5-Year

10-Year 20-Year

Source Bloomberg Note Futures + Options

Contracts

-600000

-400000

-200000

0

200000

400000

600000

2111 4111 6111 8111 10111 12111

Crude Oil

Natural Gas

Contracts

Source Bloomberg Note Futures + Options

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 8

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

WEEK AHEAD CALEnDAr Dick schumacher greg miles aND jim mcDoNalD

HIGHLIGHTSeuropean union leaders hold a summit

to complete a deficit-reduction treaty uS employers probably added workers to pay-rolls for a 16th consecutive month

Florida republicans hold their presiden-tial primary exxon Mobil Amazoncom and Merck release results

Chinarsquos January manufacturing data will indicate whether the worldrsquos second-largest economy is headed for a so-called soft landing

MF Global Incrsquos customers face deadline for filing claims at the bankrupt commodity brokerage Customers may not get back all of $12 billion still missing ac-cording to trustee James Giddens About 72 percent of assets $38 billion have been distributed

Earnings Exxon Mobil Corprsquos fourth-quarter profit will probably rise at the slowest pace in two years according to a bloomberg Survey 800 am eSt Ama-zoncom Incrsquos profit probably plunged in the fourth quarter according to a bloom-berg survey after the company added 17 fulfillment centers and sold the kindle Fire tablet at prices near-production costs to gain share About 500 pm eSt

US Senate Banking Committee over-sight hearing on ldquoHolding the Consumer Financial Protection bureau Accountablerdquo Washington 1000 am eSt

Bloomberg Government (BGOv) publishes an exclusive survey showing how much it may cost uS companies to strengthen computer network defenses against cyber attacks 800 am eSt

BLOOMBErG LINK CONFErENCE ldquothe John C bogle Legacy Forumrdquo Speakers include Kenneth r Feinberg Paul volcker Gary Gensler

WEDNESDAY Feb 1

House Science Space and Technol-ogy Committee hearing on effect of natu-ral gas fracking on underground drinking water Washington 1000 am eSt

BLOOMBErG LINK CHINA CON-FErENCE Speakers include robert D Hormats David rubenstein Franciso G Blanch James Bacchus

THUrSDAY Feb 2

US House Transportation and Infrastructure Committee may vote to approve a five-year $260 billion trans-port bill to fund highway bridge and mass-transit projects setting the stage for support in the Senate and House it would

be the first long-term infrastructure fund-ing since 2009

Earnings MasterCard Inc may report that adjusted fourth-quarter profit jumped 24 percent according to a bloomberg survey 800 am eSt

FrIDAY Feb 3

Employers in the US probably added workers to payrolls for a 16th consecutive month in January as economic growth accelerated the unemployment rate is expected to be 85 percent according to bloomberg surveys of economists

Euro-area final servicescomposite PMI for January both measures likely rose above the 50 mark that divides con-traction and expansion according to the flash estimate on Jan 24 400 am eSt

Munich Security Conference US Secretary of Defense Leon Panetta and senior defense and security officials gather for an annual forum on the most pressing defense risks through Feb 5

SATUrDAY Feb 4

republican caucuses in Nevada and Maine may provide the first indications of support for Mitt romney and Newt Gingrich after the Florida primary

Anti-Putin protests in Moscow organizers have been granted permission by city officials for a demonstration of as many as 50000 people Presidential vot-ing is on March 4

Six Nations rugby tournament begins the annual competition includes england ireland italy Scotland Wales and France the defending champion

US Pro Football Hall of Fame selec-tions named 530 PM eSt

SUNDAY Feb 5

Super Bowl in indianapolis the game starts at 630 pm eSt

MONDAY Jan 30

European Union leadersrsquo summit Heads of government from the 27-mem-ber eu aim to wrap up a deficit-reduction treaty to fight the regionrsquos sovereign-debt crisis they also will discuss ways to boost the capacity of the regionrsquos bailout funds as well as the second rescue package for Greece 900 am eSt Final press conferences are scheduled for about 100 pm eSt

Kweku Adoboli the former UBS AG trader accused of causing a $23 billion loss to the Swiss bank through unauthor-ized activity enters a plea on the charges against him in Londonrsquos Southwark Crown Court 500 am eSt

Japanese lawmakers continue to question Prime Minister Yoshihiko Noda in parliament on policies he outlined in a Jan 24 speech including a plan to double the sales tax by 2015

Punjab state elections indians begin to vote in state elections that will be a test of Prime Minister Manmohan Singhrsquos government after a year of scandals

TUESDAY Jan 31

Florida republican presidential pri-mary Voting ends at 700 pm eSt

US presidential candidates release financial reports showing donors fund-ing levels how much candidates are contributing to their campaign

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 9

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

The Webrsquos best Economics Blogs are on Bloomberg Click STNI BESTEcoNomIcSBlogS ltgogt

nEWs oF noTE

banks and other lenders are becoming ldquoincreasingly liberalrdquo with mortgages and home-equity credit lines that donrsquot require individuals to prove their income accord-ing to 152 pages of documents obtained by bloomberg News under freedom of information law from the office of the Superintendent of Financial institutions the mortgages typically granted to the self-employed and recent immigrants ldquohave some similarities to non-prime loans in the uS retail lending marketrdquo the documents show Canadarsquos housing mar-ket has surged since the 2009 recession as near-record low mortgage rates fueled prices and home purchases unlike the uS where sales and values have fallen since 2007 bank of Canada Governor Mark Carney has said record consumer debts are the greatest domestic threat to the countryrsquos financial institutions even as the central bank has held the benchmark rate at 1 percent since September 2010

ndash Andrew Mayeda

Bernanke Beats obama for Mortgage-Bond Investors

Mortgage-bond investors have been bet-ting that Federal reserve Chairman Ben S Bernanke will do more to aid housing than President Barack Obama

Government-backed mortgage bonds are poised to return the most this month since october relative to treasuries with the Fed helping push yields on lower-cou-pon notes that guide loan rates to record lows even after obama said he wants to help more homeowners refinance higher-coupon debt that would be damaged in such a scenario outperformed uS notes and a rally in unguaranteed securities that would stand to benefit fizzled

bernankersquos Fed the biggest buyer of mortgage bonds since october as it reinvests proceeds from past pur-chases further bolstered the $54 trillion government-backed market last week by extending its commitment to hold short-term rates near zero and reiterating it may acquire more of the debt investors are wagering on additional purchases as gross domestic product trails economistsrsquo forecasts ldquoA lot of it is an expectation of more Qe which only becomes more validated when you look at the details of GDP that wersquove just seenrdquo said Jason Callan the head of structured products as Columbia Management investment Advisers LLC in Minneapolis

ndash Jody Shenn

Little relief for Portugalthe Greek debt swap negotiations that

may produce relief for Athens are fueling concerns in Lisbon where an agreement would make it more likely Portuguese investors would be next to accept a loss

european leaders have said a Greek accord where investors take a 50 percent writedown in the face value of their bonds is unique and wonrsquot be applied to other nations struggling to tame rising debts

Holders of Portuguese securities are skeptical with the yield on the nationrsquos 10-year bonds rising 42 basis points to a euro-era record of 1522 percent on Jan 27 Portuguese bonds have been the worst performers of the nine eu countries downgraded by Standard amp Poorrsquos on Jan 13 the increase in borrowing costs is dimming prospects in Portugalrsquos ability to sell longer-term bonds in the public markets by the end of next year as inves-tors may be forced to endure writedowns before rescue funds from the eu run out in June 2014

ndash Anabela Reis

Canadarsquos subprime WarningCanadian lenders are loosening stan-

dards offering mortgages similar to uS subprime loans that pose an ldquoemerging riskrdquo to financial institutions according to the countryrsquos banking regulator

Since 2005 european oil consumption has fallen by 15 million barrels a day and uS oil consumption has fallen by 2 million barrels a day Gregor Macdonald writes at the Gregorus blog that the failure of global oil production to grow over seven years in the face of a phase transition in oil prices is not suggestive of peak oil ldquorather itrsquos proof of oilrsquos imminent supply resurrectionrdquo httpgooglZxIcJ

Andrew Lo of MIT takes a look at some recent research from the neurosci-ences on fear and reward learning mirror neurons theory of mind and the link between emotion and rational behavior ldquoby exploring the neuroscientific basis of cognition and behaviorrdquo he writes ldquowe may be able to identify more fundamental drivers of financial crises and improve our models and methods for dealing with themrdquohttpgooglbGccT

According to Wired Science a new study on the neurobiology of moral decision-making finds dearly held values truly are sacred and not merely cost-benefit analyses masquerading as noble intent ldquoif itrsquos a sacred value to you then you canrsquot even conceive of it in a cost-benefit frameworkrdquo the studyrsquos author Greg berns says httpgooglmC2FZ

Around the weB New research and commentary on the Web

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 10

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

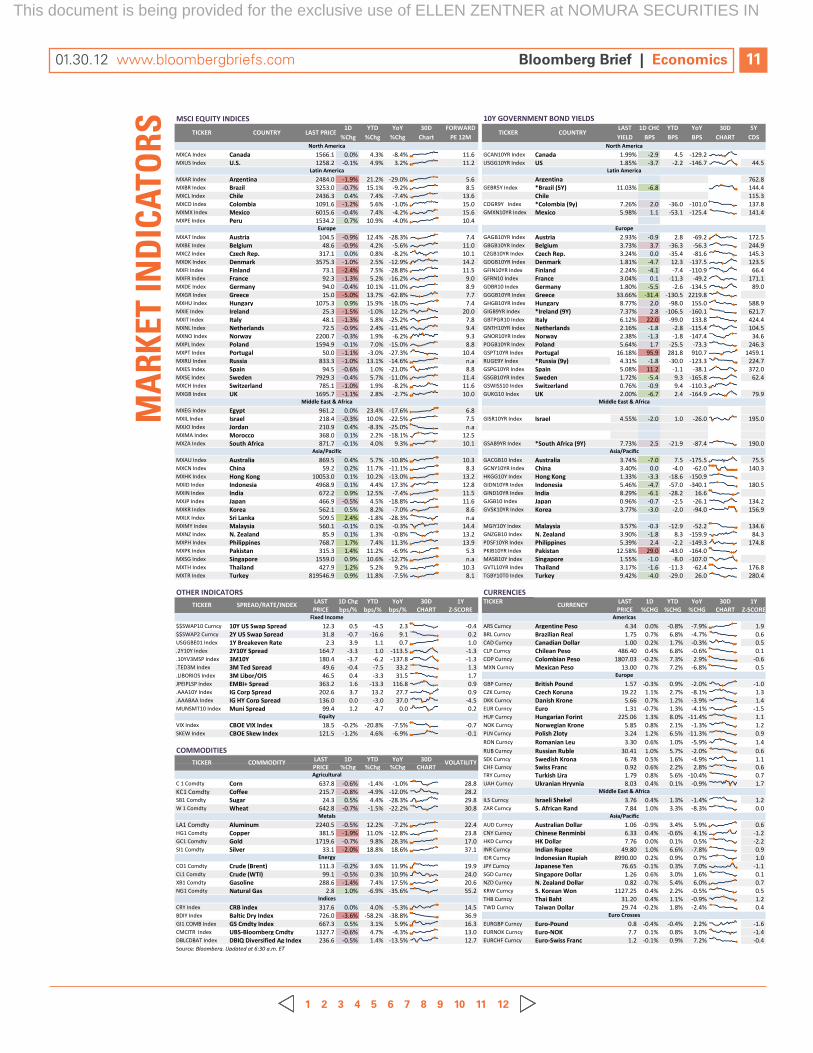

1D YTD YoY 30D FORWARD LAST 1D CHG YTD YoY 30D 5YChg Chg Chg Chart PE 12M YIELD BPS BPS BPS CHART CDS

MXCA Index Canada 15661 00 43 -84 116 GCAN10YR Index Canada 199 -29 45 -1292MXUS Index US 12582 -01 49 32 112 USGG10YR Index US 185 -37 -22 -1467 445

MXAR Index Argentina 24840 -19 212 -290 56 Argentina 7628MXBR Index Brazil 32530 -07 151 -92 85 GEBR5Y Index Brazil (5Y) 1103 -68 1444MXCL Index Chile 24363 04 74 -74 136 Chile 1153MXCO Index Colombia 10916 -12 56 -10 150 COGR9Y Index Colombia (9y) 726 20 -360 -1010 1378MXMX Index Mexico 60156 -04 74 -42 156 GMXN10YR Index Mexico 598 11 -531 -1254 1414MXPE Index Peru 15342 07 109 -40 104

MXAT Index Austria 1045 -09 124 -283 74 GAGB10YR Index Austria 293 -09 28 -692 1725MXBE Index Belgium 486 -09 42 -56 110 GBGB10YR Index Belgium 373 37 -363 -563 2449MXCZ Index Czech Rep 3171 00 08 -82 101 CZGB10YR Index Czech Rep 324 00 -354 -816 1453MXDK Index Denmark 35753 -10 25 -129 142 GDGB10YR Index Denmark 181 -47 123 -1375 1235MXFI Index Finland 731 -24 75 -288 115 GFIN10YR Index Finland 224 -41 -74 -1109 664MXFR Index France 923 -13 52 -162 90 GFRN10 Index France 304 01 -113 -492 1711MXDE Index Germany 940 -04 101 -110 89 GDBR10 Index Germany 180 -55 -26 -1345 890MXGR Index Greece 150 -50 137 -628 77 GGGB10YR Index Greece 3366 -314 -1305 22198MXHU Index Hungary 10753 09 159 -180 74 GHGB10YR Index Hungary 877 20 -980 1550 5889MXIE Index Ireland 253 -15 -10 122 200 GIGB9YR Index Ireland (9Y) 737 28 -1065 -1601 6217MXIT Index Italy 481 -13 58 -252 78 GBTPGR10 Index Italy 612 220 -990 1338 4244MXNL Index Netherlands 725 -09 24 -114 94 GNTH10YR Index Netherlands 216 -18 -28 -1154 1045MXNO Index Norway 22007 -03 19 -62 93 GNOR10YR Index Norway 238 -13 -18 -1474 346MXPL Index Poland 15949 -01 70 -150 88 POGB10YR Index Poland 564 17 -255 -733 2463MXPT Index Portugal 500 -11 -30 -273 104 GSPT10YR Index Portugal 1618 959 2818 9107 14591MXRU Index Russia 8333 -10 131 -146 na RUGE9Y Index Russia (9y) 431 -18 -300 -1233 2247MXES Index Spain 945 -06 10 -210 88 GSPG10YR Index Spain 508 112 -11 -381 3720MXSE Index Sweden 79293 -04 57 -110 114 GSGB10YR Index Sweden 172 -54 93 -1658 624MXCH Index Switzerland 7851 -10 19 -82 116 GSWISS10 Index Switzerland 076 -09 94 -1103MXGB Index UK 16957 -11 28 -27 100 GUKG10 Index UK 200 -67 24 -1649 799

MXEG Index Egypt 9612 00 234 -176 68 MXIL Index Israel 2184 -03 100 -225 75 GISR10YR Index Israel 455 -20 10 -260 1950MXJO Index Jordan 2109 04 -83 -250 naMXMA Index Morocco 3680 01 22 -181 125 MXZA Index South Africa 8717 -01 40 93 101 GSAB9YR Index South Africa (9Y) 773 25 -219 -874 1900

MXAU Index Australia 8695 04 57 -108 103 GACGB10 Index Australia 374 -70 75 -1755 755MXCN Index China 592 02 117 -111 83 GCNY10YR Index China 340 00 -40 -620 1403MXHK Index Hong Kong 100530 01 102 -130 132 HKGG10Y Index Hong Kong 133 -33 -186 -1509MXID Index Indonesia 49689 01 44 173 128 GIDN10YR Index Indonesia 546 -47 -570 -3401 1805MXIN Index India 6722 09 125 -74 115 GIND10YR Index India 829 -61 -282 166MXJP Index Japan 4669 -05 45 -188 116 GJGB10 Index Japan 096 -07 -25 -261 1342MXKR Index Korea 5621 05 82 -70 86 GVSK10YR Index Korea 377 -30 -20 -940 1569MXLK Index Sri Lanka 5095 24 -18 -283 naMXMY Index Malaysia 5601 -01 01 -03 144 MGIY10Y Index Malaysia 357 -03 -129 -522 1346MXNZ Index N Zealand 859 01 13 -08 132 GNZGB10 Index N Zealand 390 -18 83 -1599 843MXPH Index Philippines 7687 17 74 113 139 PDSF10YR Index Philippines 539 24 -22 -1493 1748MXPK Index Pakistan 3153 14 112 -69 53 PKIB10YR Index Pakistan 1258 290 -430 -1640MXSG Index Singapore 15590 09 106 -127 na MASB10Y Index Singapore 155 -10 -80 -1070MXTH Index Thailand 4279 12 52 92 103 GVTL10YR Index Thailand 317 -16 -113 -624 1768MXTR Index Turkey 8195469 09 118 -75 81 TGBY10T0 Index Turkey 942 -40 -290 260 2804

LAST 1D Chg YTD YoY 30D 1Y TICKER LAST 1D YTD YoY 30D 1YPRICE bps bps bps CHART Z-SCORE PRICE CHG CHG CHG CHART Z-SCORE

$$SWAP10 Curncy 10Y US Swap Spread 123 05 -45 23 -04 ARS Curncy Argentine Peso 434 00 -08 -79 19$$SWAP2 Curncy 2Y US Swap Spread 318 -07 -166 91 02 BRL Curncy Brazilian Real 175 07 68 -47 06USGGBE01 Index 1Y Breakeven Rate 23 39 11 07 10 CAD Curncy Canadian Dollar 100 02 17 -03 052Y10Y Index 2Y10Y Spread 1647 -33 10 -1135 -13 CLP Curncy Chilean Peso 48640 04 68 -06 0110YV3MSP Index 3M10Y 1804 -37 -62 -1378 -13 COP Curncy Colombian Peso 180703 -02 73 29 -06TED3M Index 3M Ted Spread 496 -04 -75 332 13 MXN Curncy Mexican Peso 1300 07 72 -68 05LIBORIOS Index 3M LiborOIS 465 04 -33 315 17JPEIPLSP Index EMBI+ Spread 3632 16 -133 1168 09 GBP Curncy British Pound 157 -03 09 -20 -10AAA10Y Index IG Corp Spread 2026 37 132 277 09 CZK Curncy Czech Koruna 1922 11 27 -81 13AAABAA Index IG HY Corp Spread 1360 00 -30 370 -45 DKK Curncy Danish Krone 566 07 12 -39 14MUNSMT10 Index Muni Spread 994 12 47 00 02 EUR Curncy Euro 131 -07 13 -41 -15

HUF Curncy Hungarian Forint 22506 13 80 -114 11VIX Index CBOE VIX Index 185 -02 -208 -75 -07 NOK Curncy Norwegian Krone 585 08 21 -13 12SKEW Index CBOE Skew Index 1215 -12 46 -69 -01 PLN Curncy Polish Zloty 324 12 65 -113 09

RON Curncy Romanian Leu 330 06 10 -59 14RUB Curncy Russian Ruble 3041 10 57 -20 06

LAST 1D YTD YoY 30D SEK Curncy Swedish Krona 678 05 16 -49 11PRICE Chg Chg Chg CHART CHF Curncy Swiss Franc 092 06 22 28 06

TRY Curncy Turkish Lira 179 08 56 -104 07C 1 Comdty Corn 6378 -06 -14 -10 288 UAH Curncy Ukranian Hryvnia 803 04 01 -09 17KC1 Comdty Coffee 2157 -08 -49 -120 282SB1 Comdty Sugar 243 05 44 -283 298 ILS Curncy Israeli Shekel 376 04 13 -14 12W 1 Comdty Wheat 6428 -07 -15 -222 308 ZAR Curncy S African Rand 784 10 33 -83 00

LA1 Comdty Aluminum 22405 -05 122 -72 224 AUD Curncy Australian Dollar 106 -09 34 59 06HG1 Comdty Copper 3815 -19 110 -128 238 CNY Curncy Chinese Renminbi 633 04 -06 41 -12GC1 Comdty Gold 17196 -07 98 283 170 HKD Curncy HK Dollar 776 00 01 05 -22SI1 Comdty Silver 331 -20 188 186 371 INR Curncy Indian Rupee 4980 10 66 -78 09

IDR Curncy Indonesian Rupiah 899000 02 09 07 10CO1 Comdty Crude (Brent) 1113 -02 36 119 199 JPY Curncy Japanese Yen 7665 -01 03 70 -11CL1 Comdty Crude (WTI) 991 -05 03 109 240 SGD Curncy Singapore Dollar 126 06 30 16 01XB1 Comdty Gasoline 2886 -14 74 175 206 NZD Curncy N Zealand Dollar 082 -07 54 60 07NG1 Comdty Natural Gas 28 10 -69 -356 552 KRW Curncy S Korean Won 112725 04 22 -05 05

THB Curncy Thai Baht 3120 04 11 -09 12CRY Index CRB index 3176 00 40 -53 145 TWD Curncy Taiwan Dollar 2974 -02 18 -24 04BDIY Index Baltic Dry Index 7260 -36 -582 -388 369GI1 COMB Index GS Cmdty Index 6673 05 31 59 163 EURGBP Curncy Euro-Pound 08 -04 -04 22 -16CMCITR Index UBS-Bloomberg Cmdty 13277 -06 47 -43 130 EURNOK Curncy Euro-NOK 77 01 08 30 -14DBLCDBAT Index DBIQ Diversified Ag Index 2366 -05 14 -135 127 EURCHF Curncy Euro-Swiss Franc 12 -01 09 72 -04Source Bloomberg Updated at 630 am ET

Americas

Europe

AsiaPacific

Euro Crosses

Middle East amp Africa

CURRENCY

North America

Europe

Latin America

Middle East amp Africa

AsiaPacific

CURRENCIES

Indices

Energy

Metals

Agricultural

MSCI EQUITY INDICES

Equity

Fixed Income

TICKER COMMODITY VOLATILITY

COMMODITIES

TICKER SPREADRATEINDEX

10Y GOVERNMENT BOND YIELDS

OTHER INDICATORS

North America

Middle East amp Africa

AsiaPacific

Latin America

Europe

TICKER COUNTRY LAST PRICE TICKER COUNTRY

MA

rKET

InD

ICAT

ors

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 11

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

KEEnErsquosCornEr

on Air Listen on the radio at these regularly scheduled times and dates

SurVeiLLANCeWeekdays 700 AM-1000 AM tom keene joins ken Prewitt for bloomberg Surveillance

bLooMberG oN tHe eCoNoMyMondayndashthursday 700-800 PM tom keene interviews high-profile guests and looks at the economy

PodCast Listen on the web at httpwwwbloombergcompodcastssurveillance

Also available on the bloomberg terminal bPoD ltGogt

twitter on Demand Full interviews are available at tom keene on Demand httpwwwbloombergcomtvradioradio and follow him on twitter tomkeene

Bloomberg Brief Economics

Newsletter Ted Merz Executive Editor tmerzbloombergnet 212-617-2309

Bloomberg News Dan Moss Executive Editor dmossbloombergnet 202-624-1881

Economics Kevin Depew Newsletter Editors kdepew2bloombergnet 212-617-3131

Chris Kirkham ckirkhambloombergnet +44-20-7673-2464 Staff Economists David Powell dpowell24bloombergnet +44-20-7073-3769 Richard Yamarone ryamaronebloombergnet 212-617-8737 Niraj Shah nshah185bloombergnet +44-171-330-7500

Newsletter Nick Ferris Business Manager nferris2bloombergnet 212-617-6975

Advertising bbriefbloombergnet 212-617-6975 reprints amp Permissions Lori Husted lorihustedtheygsgroupcom 717-505-9701

To subscribe via the Bloomberg Terminal type BRIEF ltGogt or on the web at wwwbloombergbriefscom To contact the editors econbriefbloombergnet

This newsletter and its contents may not be forwarded or redistributed without the prior consent of Bloomberg Please contact our reprints and permissions group listed above for more information

copy 2012 Bloomberg LP All rights reserved

Nipa Piboontanasawat npiboontanasbloombergnet +852-2977-6628

Joseph Brusuelas jbrusuelas3bloombergnet 212-617-7664

Michael McDonough mmcdonough10bloombergnet +852-2977-6733

Gerard Lyons chief economist and group head of global research Standard Chartered Bank talks to tom keene and ken Prewitt about two europes the lsquofragile eastrsquo and Chinarsquos soft landing

Todayrsquos guests Michael Cloherty RBC Capital John Ryding RDQ Economics Peter Hayes Blackrock Carl Weinberg HFE Doris Kearns Goodwin historianauthor Mark Gilman Benchmark Co

ics And the euro has been driven by poli-tics and theyrsquove overridden the economics in the good times these problems were kept beneath the surface Now those un-derlying economic flaws have come to the surface basically in its current form the euro canrsquot survive because of the severe austerity having to be felt in economies such as Greece and Spain

Q What do you see happening over the next 12 monthsA the likelihood is that Greece will leave italy Spain and others will put up with the pain the center will start to provide more help but maybe the big positive which buys us time is the fact that the european Central bank has added a lot of liquidity there are two shock absorbers in europe at the moment ndash one bad one good the bad shock absorber is youth unemploy-ment the good shock absorber is the european Central bank

Q You do so much good work in emerg-ing markets what are your thoughts on Chinarsquos GDP and would you please define what a hard landing would be if we saw thatA A hard landing would be something like 4 percent growth i think wersquore going to see Chinese economy slowing significantly in the next four months maybe down to around 6 percent growth thatrsquos a pretty soft landing in China the fundamentals are pretty good China will not be able to prevent cooling but theyrsquoll be able to ease policy if the economy does cool

Q How about the USA the uS is going to have a steady but not spectacular recovery Six months ago the market was pessimistic the uS did quite well the marketrsquos gone from that extreme to the other thinking the uS might do really well the big issue for me is whether corporate America has the con-fidence to go out and invest if it does the uS will really gather momentum

Q Invest abroad or invest in the USA After the last recession albeit a pretty mild recession by comparison with this one the uS corporate sector started to invest a lot more across the emerging world across Asia this time around big corporate America seems to be sitting on its balance sheets not sure what to do Normally at this stage of a recovery you would expect big firms to want to put their

Q You have called it a lsquofragile Westrsquo and a lsquoresilient Eastrsquo What is the distinction between East and West right nowA the east itself is cooling down but itrsquos still in pretty good shape the Western economies are still trying to get over the overhang of debt in America the big distinction is between the big firms who are in good shape and the small firms who donrsquot seem to be able to get access to liquidity Against all that one of the themes in Davos this year apart from the possible collapse of europe is the need to focus on income disparity income disparities have always been a big theme but in the West itrsquos more of an issue now than before

Q In your study of economics whatrsquos wrong with a more conservative eco-nomic view that says ldquoLet the success-ful be successful and pull up those who are strugglingrdquo versus another angle which would say ldquoredistribute what the successful have done to those down the food chainrdquoA the redistribution can actually sort of backfire make the cake actually smaller - the cake being the economic cake before Davos i spent two weeks in Asia and itrsquos interesting to note that both in China and in taiwan income disparity is becoming the big issue there but itrsquos not yet risen to the surface because the economic cake in those economies is getting much big-ger the challenge in the West is to make sure that we donrsquot actually have policies to correct this that make the actual outcome worse than the original situation

Q You made a big splash by saying that the euro is flawed and cannot survive Could you explain your reasoningA Well the reasoning is based on the fact that good economics is good politics but good politics is not always good econom-

cash to work if they do that then jobs will start to be more plentiful and confidence will start to pick up

(This interview was condensed and edited)

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 12

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

January 2009 -29mn

-3000

-2500

-2000

-1500

-1000

-500

0

500

Jan-49 Jan-55 Jan-61 Jan-67 Jan-73 Jan-79 Jan-85 Jan-91 Jan-97 Jan-03 Jan-09

Change in EmploymentJanuary month-to-month change in employed not seasonally-adjusted (Household survey)Median+- 2 standard deviations

000s

Source Nomura Securities

03

-02

-03

-02

-01

0

01

02

03Difference Between Official and Alternative Employment pp

Δ (Nov 10 - Jan 11) = 05pp

Source Nomura Securities

Why A sharp decline in labor market indica-tors caused by the financial crisis in late 2008-early 2009 has led to imperfect sea-sonal adjustments to detect the distortion we reconstructed the seasonally-adjusted unemployment rate from unadjusted data for the main constituents the bureau of Labor Statistics (bLS) uses in its unemployment rate calculation but excluded the critical months of the financial crisis for the purposes of seasonal adjustment

We consider the difference between the official data series and our alternative to represent the ldquoseasonal biasrdquo in the unem-ployment rate While the two series have the same trend the impact on month-to-month changes in unemployment can be material For instance the difference between the up-ward bias (where the reported unemployment rate is higher than underlying) in November 2010 and the downward bias in January 2011 accounted for 05 percent of the 07 percent-age point unemployment rate decline over that period

Likewise wersquove found that nearly the entire decline in the December 2011 unemployment rate to 85 percent from 87 percent can be explained by seasonal bias Furthermore we forecast the unemployment rate will decline further to 83 percent in January again helped by a downward seasonal bias Come April the seasonal bias should reverse and the unemployment rate may as well

Special factors driving the unemployment rate decline give little reason for celebration be-cause the unemployment rate falls when unem-ployed persons stop looking for work (and are no longer in the labor force) we calculate the unemployment rate including these labor force ldquoexitersrdquo After first adjusting for demographic trends in labor force participation we find this broader measure of the unemployment rate to be 103 percent in December as opposed to the reported 85 percent it has been greater than 10 percent since September 2009

FoMC participants still see considerable slack in the labor market even as the official unemployment rate has recently trended downward Chicago Fed President Charles evans commented that the decline ldquomay be transitoryrdquo and that an 85 percent unemploy-ment rate is ldquopossible at the end of 2012rdquo Chairman bernanke expressed his ongoing concern about employment conditions in his first press conference of 2012 by saying ldquoif the situation continues with inflation below target

Big Picturecontinued from page 1

JeFFrey GreeNberG AND AiCHi AMeMiyA

and unemployment declining at a rate which is very very slow then our frame-work the logic of our framework says we should be looking for ways to do morerdquo

the recent decline in the unemploy-ment rate does not change the fear that cyclical unemployment could become structural to be sure the share of long-term unemployed (more than 27 weeks) has risen from 174 percent of total unemployed at the start of the recession to 425 percent four years later While no FoMC participants estimated that the longer run (natural)

unemployment rate exceeded 6 percent just three years ago now nearly a third of participants do the FoMCrsquos latest economic projections reveal partici-pants forecast the unemployment rate to be 67-to-76 percent in the fourth quarter of 2014 We believe the concern that unemployment could become more entrenched if unaddressed will motivate more action and expect the FoMC to continue its Sisyphean task of reaching full employment by announcing further expansion of the balance sheet in the second quarter of this year

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 2

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

BUSINESS HAS SUFFERED A SERIOUS BLOW JOIN THE RECOVERY TEAM

In a world of financial risk organizations can never be too prepared Thatrsquos why more global companies are relying on Certified Financial Risk Managers As an FRMreg yoursquoll be recognized for mastering the complexities of credit market and operational risks Yoursquoll also play a critical role in the financial well-being of banks consultancies corporations and asset management firms If you want to be part of the solution take the first step by earning your FRM certification Visit the Global Association of Risk Professionals (GARP) at garporgfrm

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 3

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

2400120060030015007500ndash075ndash150ndash300ndash600ndash1200ndash2400

Daily Percentage Change of the Global Equity Markets

PoLITICAL WATCH by bLooMberG NeWS

annual growth the previous quarter

Polish consumer confidence fell to an index reading of minus 571 in January from minus 568 in December

Italian business confidence fell to an index reading of 921 in January the lowest since November 2009 from 925 in December economists predicted 923

Global Equity Performance

Gingrich Invokes GoldmanNewt Gingrich accusing republican

presidential primary opponent Mitt romney of being a ldquofundamentally dishonestrdquo tool of Wall Street pledged to stop banking firms such as Goldman Sachs Group from ldquorigging the gamerdquo Pressing his campaign into the last full day before Floridarsquos primary tomor-row Gingrich spoke of running a White House that would ldquochallenge the system head-onrdquo and disrupt the ldquoWall Street eliterdquo ldquoto the degree they survive by rig-ging the gamerdquo he said ldquothey have a lot more to fear to the degree that theyrsquore willing to be in a very investment-orient-ed high-tempo entrepreneurial world they have more to gainrdquo

States Lag on InsuranceStates with the most residents who

would benefit from expansion of medi-cal coverage have been the slowest to set up the insurance exchanges re-quired under the health-care overhaul a study found Fifteen states have made little progress on creating the markets in the almost two years since the law was signed according to the study by the robert Wood Johnson Foundation and the urban institute those same states could reduce the number of uninsured residents by an average of 53 percent compared with 42 percent for states that have already taken legislative steps to create exchanges and a national average of 48 percent the study found

New Zealandrsquos Bollard to QuitNew Zealand central bank Governor

Alan Bollard will quit in September ending a decade-long tenure in which he raised interest rates to a record high before cutting them last year to their lowest ever bollard wonrsquot seek another five years when his current term ends Sept 25 the reserve bank of New Zealand said the central bank said it will search in New Zealand and abroad for a successor the move leaves New Zealand searching for a new central bank chief during a period of slowing global growth and a sluggish domestic economy thatrsquos motivating young peo-ple to leave in search of higher-paying jobs in Australia and elsewhere

oVErnIGHT By BloomBerg News

euroPe

Euro-area confidence in the economic outlook improved to an index reading of 934 in January from a revised 928 in De-cember the median estimate was 938

Spainrsquos economy shrank 03 percent in the fourth quarter from the previous three months GDP grew 03 percent from the prior year compared with 08 percent

Lithuaniarsquos economy expanded 43 percent in the fourth quarter from the prior year after growing 67 percent the previ-ous three months the median estimate was an increase of 6 percent

AsiA

Taiwanrsquos unemployment rate declined to 422 percent in December from 432 percent in November the median esti-mate was 433 percent

The Philippine economy expanded 37 percent in the fourth quarter from a year earlier that compares with a revised 36 percent increase in GDP the previous three months economists forecast a 38 percent gain

South Korearsquos current-account sur-plus narrowed to $396 billion in Decem-ber a three-month low from a revised $456 billion in November

Thailandrsquos economy contracted 5 percent in the fourth quarter of 2011 the finance ministry said it grew 11 percent for the full year

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 4

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

10

11

12

13

14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source US Bureau of Labor Statistics

Union Membership ( of Employed)

Source Bureau of Labor Statistics

FACE OFFMArKET CALLsby bLooMberG NeWS

Far From its Peak union Membership Increased only slightly in 2011

Standard Chartered Plcrsquos Jaspal Bindra chief executive officer for Asia said the Fedrsquos pledge to keep interest rates low through at least late 2014 creates a risk of hyperinflation in Hong kong ldquoif you have near-zero interest rates when their inflation is at over 6 or 7 per-cent given the China effect and their growth is also thanks to China at 6 or 7 percent yoursquore looking for hyperinflationrdquo he said

richard Koo chief economist at Nomura research institute said Japan should limit intervention to weaken the yen because a strong currency keeps the cost of fuel imports low as the nationrsquos nuclear capac-ity dwindles ldquoright now irsquom not pushing loudly for interventionrdquo said koo

viktor Shvets a Hong kong-based strate-gist at Samsung Securities Co said uS economic growth ldquowill be stuck between 15

percent and 25 percent for years to comerdquo with occasional quarters of zero or near-zero growth

ronald Stoeferle a commodity analyst at erste Group bank AG said gold prices may rise 33 percent further to a record $2300 an ounce early next year accord-ing to technical analysis ldquoWe are seeing a momentum in goldrdquo Stoeferle said

Morgan Stanley economist Pasquale Diana said Hungaryrsquos benchmark inter-

est rate may have peaked at 7 percent after the central bank unexpectedly left the two-week deposit rate unchanged last week A ldquomodest rallyrdquo or a ldquostabilization of risk metricsrdquo may be sufficient to begin rate cuts Diana said

Goldman Sachs economist Ahmet Akarli said a reduction of turkeyrsquos current account deficit may have reversed leaving it the most vulnerable economy in the region Financial conditions in the country are too loose he said

According to the bureau of Labor Statistics the number of union members increased negligably in 2011 to 14764 million from 14715 million in 2010 As a percentage of total employment in the uS union membership in 2011 slipped to 118 percent from119 percent the prior year the bLS doesnrsquot have a complete set of union membership data compa-rable union enrollment figures date only back to 1983 when there were 177 mil-lion union workers and the membership rate was 201 percent

We do know that in 1950 roughly one out of every three workers was em-ployed in the manufacturing sector with the same percentage carrying a union card today with nearly 83 percent of private industry workers employed in the services sector the percentage and number of union workers have both de-clined Manufacturers comprise only 103 percent of all private workers while 50 percent are employed in the construction sector employment in the manufacturing sector today (1179 million) is at the same level as it was in 1941

Membership in the united Auto Workers

been furloughed at an elevated pace Current union membership is dominated by government workers As a percent of total union workers 1004 million (281 percent) were federal 1973 million (315 percent) state and 4947 million (317 percent) local

mdash Richard Yamarone Bloomberg economist

union peaked in 1979 at 15 million work-ers while according to its website the uAW today has only 390000 members there were roughly 600000 retirees on pension and medical care plans being supported by that level of membership

in addition to the Housing and Auto sectors government workers have also

Hiroki Shimazu of SMBC Nikko Securities forecasts a 04 increase in personal spending up from 01 percent previously

Ellen ZentnerDavid resler of Nomura Securities predict no change in per-sonal spending the median bloomberg survey forecast is 01 percent

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 5

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

0

25

50

75

100

125

-10

0

10

20

30

40

2003 2004 2005 2006 2007 2008 2009 2010 2011

difference (RHS)

exports to US amp EU (LHS)

exports to Asia ex Japan (LHS)

$bn

Source CEIC RBC

$bn

China South Korea Taiwan Hong Kong Singapore Export Destinations

17 17

15 -01

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2005 2006 2007 2008 2009 2010 2011 2012

US GDP growth - change in rate (pp)euro-area GDP growth - change in rate (pp)US GDP growth ()euro area GDP growth ()

Sources RBC Bloomberg

percent

RBC forecasts

US Euro-Area GDP Growth

rise in Intra-regional Exports to Help support Asia as us Eu Demand slows

Growth prospects for China and other emerging-market Asian countries in 2012 will depend on how their exports perform exports fell very sharply in late 2008 and early 2009 and the recent deterioration in the global outlook raises concerns about another slump in external demand

Asian export performance remains heav-ily dependent on growth in the uS and the euro-area in addition to direct trade with these economies much of Asiarsquos intra-regional trade consists of intermedi-ate goods for which the final demand is from the uS and the euro-area

Looking ahead further deteriora-tion in the regionrsquos export performance seems likely in coming months mainly reflecting the weaker euro area outlook recent exchange rate moves provide an additional reason to suspect that euro-area demand will remain weak over the last six months emerging-market Asian currencies have appreciated significantly against the euro most recording gains of 4 percent to 10 percent over this period with the Chinese yuan up around 12 per-cent emerging-market Asian exporters however have gained competitiveness with uS customers over this period with most regional currencies around 3 percent to 7 percent weaker against the dollar

Given that uS and euro-area growth is unlikely to weaken in 2012 as sharply as they did a few years ago Asian exports should perform better than they did a few years ago

exports remain near record levels in China and other parts of Asia suggesting that even modest growth rates in external demand will provide significant support to domestic activity across the region

in addition major Asian economies are now exporting significantly more to their own region than they are in aggregate terms to the uS and the european union with this amount averaging around $24 billion per month in 2011 this strongly suggests that much of the recent increase in intra-regional trade in Asia reflects stronger final demand from within the re-gion rather than from the uS and the eu

in other words Asia is still vulnerable to weaker growth in the uS and europe but this vulnerability is less pronounced

than previously in the case of China Asian economies excluding Japan is by far the most important market for Chinese exporters indeed China exports more to the rest of Asia excluding Japan than it does to the uS and the eu combined Chinese exports to Asia excluding Japan have soared since early 2009 and remain near record levels in recent months

this pattern is even more pronounced for South korea taiwan Hong kong and Singapore the exports they send to each other China and the rest of Asia excluding Japan far exceed those sent to other mar-kets indicative of growing final demand in the region as per capita incomes rise

the fact that the performance of Asian exports increasingly depends on final demand from within Asia itself highlights

the importance of policy moves to support domestic demand Fiscal policy is already supportive in much of Asia officials have in recent months halted and in some cases started to reverse tighter monetary policy settings put in place over 2010 and 2011 a trend that should support liquidity and activity in coming months this com-bined with optimism that external demand from the uS may stabilize or show signs of recovery suggests that exports and headline GDP growth in Asia will likely continue to moderate early in 2012 before picking up again later in the year

(Brian Jackson is the senior emerging markets strategist at RBC Capital Markets in Hong Kong He previously worked as an economist at the Bank of England and an analyst at the Federal Reserve Bank of New York)

AsIA WATCH BriaN jacksoN rBc capital markets guest columNist

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 6

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Perc

enta

ge C

hang

e

Stressed Consumers

Real Personal Disposable Income Real Spending

Source Bloomberg PIDSCWT PCE CHY INDEXltGOgt

-25

-20

-15

-10

-5

0

5

10

15

20

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Housing Market Contracts at Slower Pace

House Price Index Case-Shiller 20-City Home Price Index

Source Bloomberg HPIMYOY SPCS20Y INDEXltGOgt

30

35

40

45

50

55

60

65

70

75

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Manufacturing Remains StoutChicago PMI ISM Manufacturing

Source Bloomberg CHPMIND INDEXltGOgt NAPMPMI INDEXltGOgt

-1000

-800

-600

-400

-200

0

200

400

2007 2008 2009 2010 2011

ADP Private Job Creation

ADP Estimate of Private Payrolls BLS Estimate of Private Payrolls

Source Bloomberg ADP CHNG NFP PCH INDEXltGOgt

8

9

10

11

12

13

14

15

16

17

18

2006 2007 2008 2009 2010 2011

Total Vehicle Sales

Source Bloomberg SAARDTOT INDEXltGOgt

on an inflation-adjusted basis personal disposable income declined 01 percent and average hourly earnings 09 percent over the past year Consumers appeared to pull back on spending in December and may continue to slow in January

the bloomberg consensus forecast expects a gain of 150000 in total employment to kick off 2012 temporary retail and transportation jobs are expected to subtract from it the un-employment rate is forecast to hold steady at 85 percent

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400BLS Non-Farm Payroll Estimate

3-Month Average Change in Total Employment

S NFP TCH INDEXltGOgt

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400BLS Non-Farm Payroll Estimate

3-Month Average Change in Total Employment

S NFP TCH INDEXltGOgt

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

1989 1994 1999 2004 2009

BLS Non-Farm Payroll Estimate

3-Month Average Change in Total Employment

S NFP TCH INDEXltGOgt

Given widespread skepticism about the quality of job gains in December it would not be surprising to see a significant downward revision of last monthrsquos ADP estimate and job gains are barely enough to keep pace with demographic changes

regional manufacturing surveys and the 105 percentage point spread between new orders and inventories suggests conditions are ripe for a sustained increase in industrial production

the Case-Shiller home price index is likely to show the de-cline in home prices accelerated in November the CoreLogic data a solid forward-looking indicator for the Case-Shiller index fell 16 percent on the month

December retail sales data fell flat after a strong start to the holiday shopping season the December employment report indicated an increase in aggregate hours worked and average hourly earnings that should bolster nominal incomes

investors will in-tensely focus on an array of labor market and manufacturing data for the first month of 2012 following the weaker-than-anticipat-ed 28 percent pace of growth to close out 2011 Given that inven-tory building by firms accounted for roughly 62 percent of growth in the fourth quarter there is considerable risk to the consensus 2 percent forecast of growth in the cur-rent quarter there is a strong possibility after three months of improving economic numbers that the data flow will look quite pessimistic through mid-2012

Labor Market Manufacturing Data Provide First Look at 2012 Economy

EConoMICs PrEVIEW JoSePH bruSueLAS bLooMberG eCoNoMiSt

1 2 3 4 5 6 7 8 9 10 11 12

013012 wwwbloombergbriefscom bloomberg brief | economics 7

This document is being provided for the exclusive use of ELLEN ZENTNER at NOMURA SECURITIES IN

Non-commercial accounts have increased their net holdings of oil for the last five weeks most recently by 15199 contracts to 305249 contracts the position may continue to rise as political ten-sions in the Middle east escalate it is in line with the one-year average

Speculators have increased their holdings of gold for the last three consecutive weeks that may be a response to the intensification of the european sovereign debt crisis During the latest reporting period they purchased 9019 contracts on a net basis bringing the net long position to 155027 contracts

Energy ProductsGold

As uS stocks rallied non-commercial accounts sold uS treasury securities across the maturity spectrum creating a total reduction of 214893 contracts they unloaded two- (1023 contracts) five- (55989 contracts) 10- (137880 contracts) and 20- (20001 contracts) year instruments

Speculators boosted their net short position in the euro to a fresh high of 169740 contracts after sell-ing 11145 contracts on a net basis during the week ended Jan 24 the position remains overstretched it is 22 standard deviations below the one-year average and the ratio of net longs to open inter-est stands at 047 by contrast they bought 8919 contracts on the uS dollar increasing the net long position to 84270 contracts

US Treasury SecuritiesCurrencies

in the week that followed the SampP downgrade of several euro-area nations speculators continued to sell the euro and buy the uS dollar according to data from the Commodity Futures trading Commission though they dumped treasury securities as the SampP rallied they continued to slowly increase their exposure to gold and oil

CoMMITMEnTs oF TrADErs DaviD powell BloomBerg ecoNomist

-200000

-150000

-100000

-50000

0

50000

100000

150000

200000

2111 4111 6111 8111 10111 12111

EUR JPY GBP CHF

CAD AUD NZD USD

Contracts

Source Bloomberg Note 1 USD contract = $200000 Futures + Options

0

50000

100000

150000

200000

250000

300000

350000

2111 4111 6111 8111 10111 12111

Gold

Source Bloomberg Note Futures + Options

Contracts

-300000

-200000

-100000

0

100000

200000

300000

400000

2111 4111 6111 8111 10111 12111

2-Year 5-Year

10-Year 20-Year

Source Bloomberg Note Futures + Options

Contracts

-600000

-400000

-200000

0

200000

400000

600000