Embed Size (px)

Citation preview

Economics /Management 4 Financial Accounting

Spring 2016

Indirect Statement of Cash Flows [Ugly Puppy Agg 2nd]

Accrual v. Cash Flow

• Accrual is about matching the inflows & outflows of resources OR CLAIMS(OBLIGATIONS) in the Earnings process - regardless of when you paid/will pay for those resources.

• But since liquidity is important, we want to know about the concomitant sources(uses) of cash in the Earnings process.

Set-up

• Total cash flow is the aggregate Δ in cash b/w accounting periods:

Cash1 - Cash0

The SCF is simply a stylized format that separately reports Cash-basis accounting processes for:

1. Operating activities

2. Investing activities

3. Financing activities

Illustrating the Indirect Method

Look at the Ugly Puppy 2nd period Financials.

Look at Cash Flow and the changes in the Balance Sheet

• Cash is the unique item – isolate it on the RHS of the A = L + Eq “Balance Sheet”.

• Cash flow is the dependent variable in this Equation.

• Cash flow is the change in cash from one Balance Sheet to the next Balance Sheet.

• Thus, CF is the 1st derivative of all BS w.r.t. all “not” Cash accounts.

The 2nd Period - Aggressive Starting Rev 140 COGS (50) GP 90 G&A ( 10) EBITDA 80 DA ( 74) EBIT 6 I ( 7) EBT ( 1) T (0) NI ( 1)

120

10

( 0)

50

0

0

100

(33)

0

0

0

0

200

47

176

20

( 0)

40

0

40

224

(107)

0

40

7

100

200

46

Changes in the Balance Sheet - Period #2 minus #1

56 10 0

(10)

0

40

124

(74)

0

40

7

100

0

(1)

The Indirect SCF (1) = NI = the Δ RE 74 = DA = the -Δ Accum DA (10) = Less the Δ Receivables 10 = Less the Δ Inventory (40) = Less the Δ Supplies 40 = Plus the Δ Payables 7 = plus the Δ Accruals 80 CFOA (124) =less the Δ LLA is the CFIA 100 = plus the Δ IBD 0 = plus the ΔPinK 0 = less dividends 100 CFFA 56 Total CF

ΔBS/Δperiod = the derivative item-by-item

The S.C.F

• The SCF is a highly stylized financial statement.

• Illustrates the sources and uses of liquidity.

• Attributing cash flow to three activities:

Operating – a modified Cash Basis income statement

Investing – acquisition(disposition) of fixed assets, Net CAPEX

Financing – sources(uses) of cash through the

selling(repurchasing) claims, i.e. loans or stock.

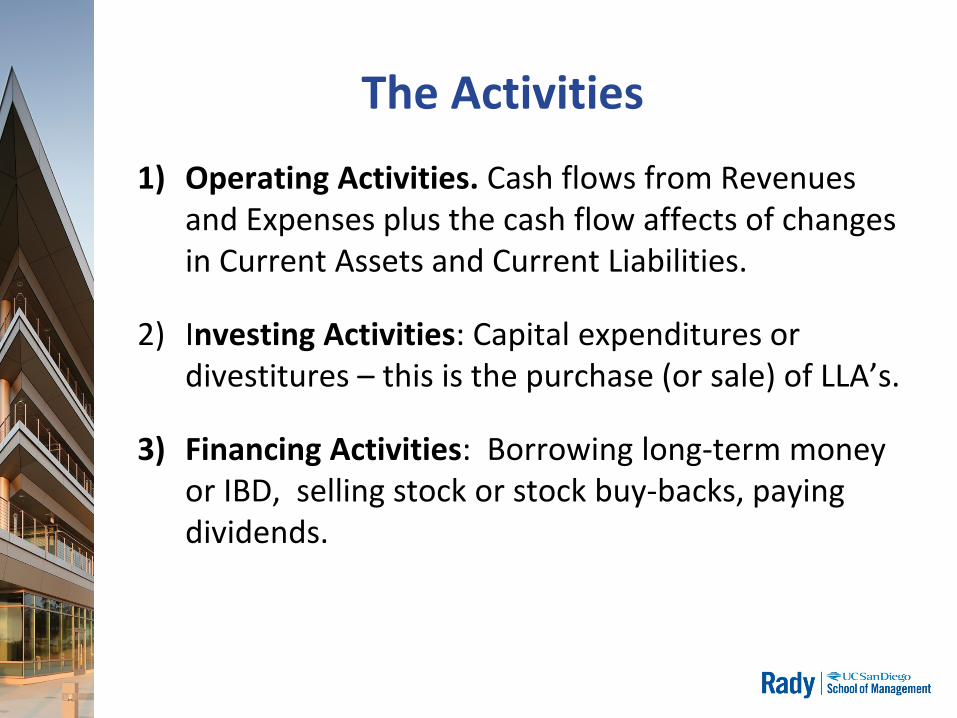

The Activities

1) Operating Activities. Cash flows from Revenues and Expenses plus the cash flow affects of changes in Current Assets and Current Liabilities.

2) Investing Activities: Capital expenditures or divestitures – this is the purchase (or sale) of LLA’s.

3) Financing Activities: Borrowing long-term money or IBD, selling stock or stock buy-backs, paying dividends.

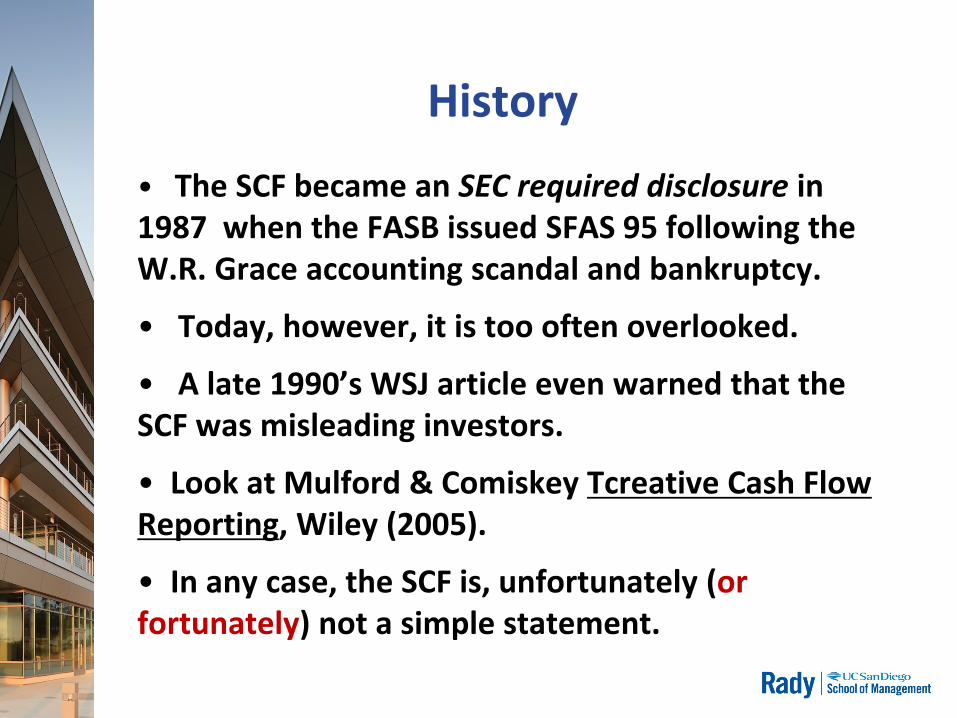

History

• The SCF became an SEC required disclosure in 1987 when the FASB issued SFAS 95 following the W.R. Grace accounting scandal and bankruptcy.

• Today, however, it is too often overlooked.

• A late 1990’s WSJ article even warned that the SCF was misleading investors.

• Look at Mulford & Comiskey Tcreative Cash Flow Reporting, Wiley (2005).

• In any case, the SCF is, unfortunately (or fortunately) not a simple statement.

Sell a man a fish – make a living.

You Idiot !

Fortunately, the SCF is not a simple. It takes work to learn it.

Teach a man to fish ..

The Statement of Cash Flows

• A stylized translation of the Accrual income statement into a three-part statement of the Sources and Uses of cash: CFOA, CFIA, and CFFA. • A firm’s accounting choices will shape its accrual income statement and its SCF accordingly.

• The SCF can be expressed two ways: 1) The Direct Method 2) The Indirect Method

The Methods

The methods only differ by the way Operating Activities are translated into cash flows.

• Indirect Method.

Starts at the bottom of the accrual income statement (w/ NI) then restates the accrual recognitions to their modified cash-basis effects.

• Direct Method.

Starts at the top of the accrual income statement and adjusts the 3 primary parts – Revenue, COGS, & SG&A – into a cash-basis..

Duci Accept a stipulation - the objective nature of cash flow

makes it a good point of reference, so call it the truth.

This stipulation makes accrual earnings a sort of non-truth, a kind of lie - maybe a white lie, maybe worse.

All lies are composed of commissions and/or omissions.

You can reconstitute the truth from a lie if

you systematically:

a) remove what was committed, and

b) include what was omitted.

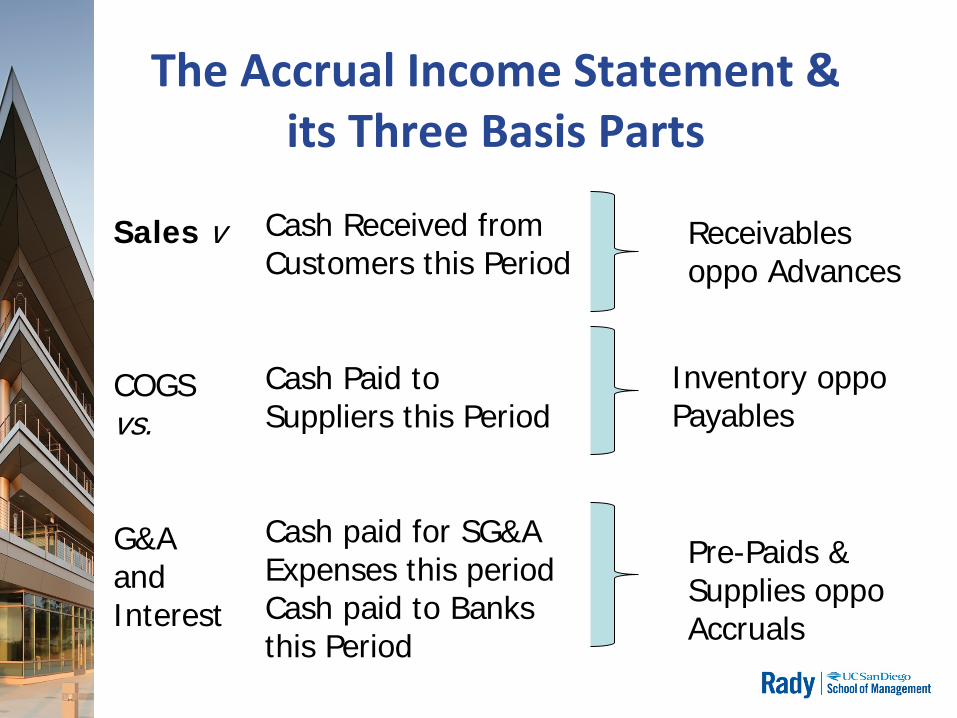

The Accrual Income Statement & its Three Basis Parts

Sales v COGS vs. G&A and Interest

Cash Received from Customers this Period Cash Paid to Suppliers this Period Cash paid for SG&A Expenses this period Cash paid to Banks this Period

Receivables oppo Advances

Inventory oppo Payables

Pre-Paids & Supplies oppo Accruals

The Working Capital “operating” Accounts The Working Capital Accounts

1. Receivables – when customers buy, but pay later 2. Inventory – stuff we buy to sell to customers later 3. Pre-paid Expenses – when we pay-for-it now, but use

it later 4. Supplies - when we pay-for-it now, but use it later. 5. Unearned Revenue – cash from customers before the

sale 6. Payables – when we purchase inventory but pay later 7. Accrued Expenses – when we use something but pay

for it later

The Current Asset/Liability Pairings

Cash Receivables

Inventory

Pre-Paids

LLA

(Accumulated DA)

Advances

Payables

Accruals

I.B.D.

Paid in Capital

Retained earnings

These accounts are merely memorializations of cash-to-be-collected and cash-to-be-paid

The SCF is the first derivative of the Balance Sheet wrt the Accounting period.

Assets

use cash Liabilities

& Equity

are sources of cash

Assets Liabilities

Increase USE SOURCE

Decrease SOURCE USE

Cash Flow