Embed Size (px)

DESCRIPTION

Donald Rissmiller Chief Economist Strategas Research Partners

Citation preview

1 of 28

ECONOMICS HIGHLIGHTS

What Will Muddle-Through Growth Do To Profits?

Don Rissmiller Chief Economist

Strategas Research Partners

March 1, 2013

(212) 906-0134 [email protected]

2011 2012 2013 2014

4Q 1Q 2Q 3Q 4Q 1QF 2QF 3QF 4QF 1QF 2QF 3QF 4QF

Real GDP Q/Q % AR 4.1% 2.0% 1.3% 3.1% 0.1% 2.0% 2.0% 2.3% 3.0% 2.5% 2.0% 2.0% 1.0%

Core CPI Q/Q % AR 1.9% 2.1% 2.4% 1.6% 1.7% 1.0% 1.0% 1.5% 1.5% 2.0% 2.0% 2.0% 2.0%

Fed Funds EOP 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%

F = Forecast; EOP = End of Period

www.strategasrp.com 2

STRATEGAS BASE CASE

4 Macro Issues: 1) U.S. Fiscal policy, 2) Euro-area uncertainty, 3) China slowing, 4) Oil price Volatility.

Most are better (for now). U.S. fiscal sequester still an issue.

U.S. fiscal cliff was a big punt: “kicking-the-can” again. o Fiscal Cliff becomes a Fiscal Slope

Divergences: o Business confidence vs. Consumer confidence o Capital Spending vs. Employment

Fed and other central banks likely to remain easy (not close to 6.5% U.S. unemployment)

With the output gap, inflation is not a problem, for now. “Reflation” comes before inflation.

U.S. pent-up demand in 1H: household formation, capex (down already).

PMIs suggest some economic momentum as we start 2013.

As business cycle matures, profit margins likely peaking.

Question of sustainability: still looking at only 4% nominal growth. A Mid-Cycle slowdown, or an “Intra-cycle slowdown”?

www.strategasrp.com 3

WHERE ARE WE IN THIS BUSINESS CYCLE?

What Puts the “Mid” in Mid-cycle Slowdown?

Real Gross Domestic Product

% Change - Year to Year SAAR, Bil.Chn.2005$

10050095908580757065605550

Source: Bureau of Economic Analysis

15

10

5

0

-5

15

10

5

0

-5

More frequent recessions on the

left hand side of this chart… WHY?

www.strategasrp.com 4

GDP = C + I + G + NX

Real PCE: Contribution to Real GDP Change4-qtr MovingAverage SAAR, %

Real Gross Pvt Dom Investmnt: Contribution to Real GDP Chg4-qtr MovingAverage SAAR, %

10050095908580

Source: Bureau of Economic Analysis

7.5

5.0

2.5

0.0

-2.5

-5.0

7.5

5.0

2.5

0.0

-2.5

-5.0

Consumption = 71% (still !)

Investment = 13%

Govt = 19%

Net Exports = -3%

Investment

Consumption

www.strategasrp.com 5

IMPACTS OF THE FISCAL CLIFF: PENT-UP DEMAND

CAPEX (10% OF THE U.S. ECONOMY): DOWN

CONSUMER SPENDING (71% ECONOMY): NOT DOWN

Mfrs' New Orders: Nondefense Capital Goods ex Aircraft

SA, Mil.$

10050095Source: Census Bureau

75000

67500

60000

52500

45000

37500

75000

67500

60000

52500

45000

37500

CAPEX EQP PROXY

www.strategasrp.com 6

BOTH CEOs & CFOs HAVE BEEN MORE CAUTIOUS

Duke/CFO Outlook: Expected Growth in Capital Spending in Next 12 Months

%

131211100908070605040302

Source: Duke Fuqua School of Business/CFO Magazine

15

10

5

0

-5

-10

-15

15

10

5

0

-5

-10

-15

CEO Economic Outlook Survey Diffusion Index

50+=Expansion

131211100908070605040302

Source: Business Roundtable

125

100

75

50

25

0

-25

125

100

75

50

25

0

-25

www.strategasrp.com 7

HOW WILL THIS DIVERGENCE END?

Mfrs' New Orders: Nondefense Capital Goods ex Aircraft% Change - Year to Year SA, Mil.$

All Employees: Total Nonfarm% Change - Year to Year SA, Thous

10050095Sources: Census Bureau, Bureau of Labor Statistics

40

20

0

-20

-40

4

2

0

-2

-4

-6

This gap has to narrow between the employment

of capital and the employment of

labor.

Capex proxy

Jobs

www.strategasrp.com 8

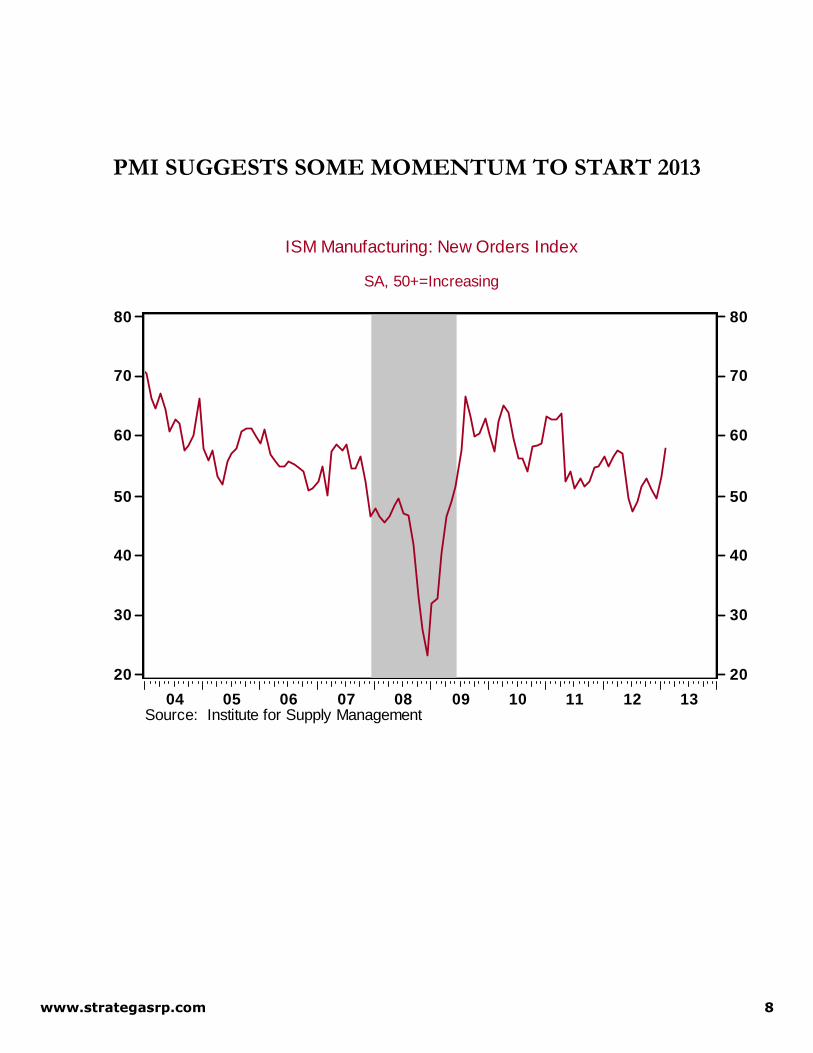

PMI SUGGESTS SOME MOMENTUM TO START 2013

ISM Manufacturing: New Orders Index

SA, 50+=Increasing

13121110090807060504Source: Institute for Supply Management

80

70

60

50

40

30

20

80

70

60

50

40

30

20

www.strategasrp.com 9

ECONOMIC SYMMETRY: It Wasn’t a “V” or a “U” Recovery …

1) SQUARE-ROOT SHAPED RECOVERY.

2) REVERSE SQUARE-ROOT SHAPED EXPANSION?

Disposable Personal Income

% Change - Year to Year SAAR, Bil.$

1312111009080706050403020100

Source: Bureau of Economic Analysis

10.0

7.5

5.0

2.5

0.0

-2.5

-5.0

10.0

7.5

5.0

2.5

0.0

-2.5

-5.0

www.strategasrp.com 10

A RETURN OF HOUSEHOLD FORMATION WILL BE KEY

Total Number of Households, Break-adjusted

% Change - Year to Year Thous

10050095

Source: Census Bureau/Haver Analytics

2.4

2.0

1.6

1.2

0.8

0.4

0.0

2.4

2.0

1.6

1.2

0.8

0.4

0.0

www.strategasrp.com 11

SYMMETRY:

1) SQUARE-ROOT SHAPED RECOVERY.

2) REVERSE SQUARE-ROOT SHAPED EXPANSION?

2012 Muddle

Through

(Deleveraging)

Late-2012, early

2013 Slowdown

(Fiscal Cliff /

Sequester

Uncertainty)

2013-14

Recovery

(We get housing

& capex back)

2011 Muddle

Through

(Deleveraging) 2009-2010

Moderate

Recovery

(Missing

housing)

2007-2009 Deep

Recession

www.strategasrp.com 12

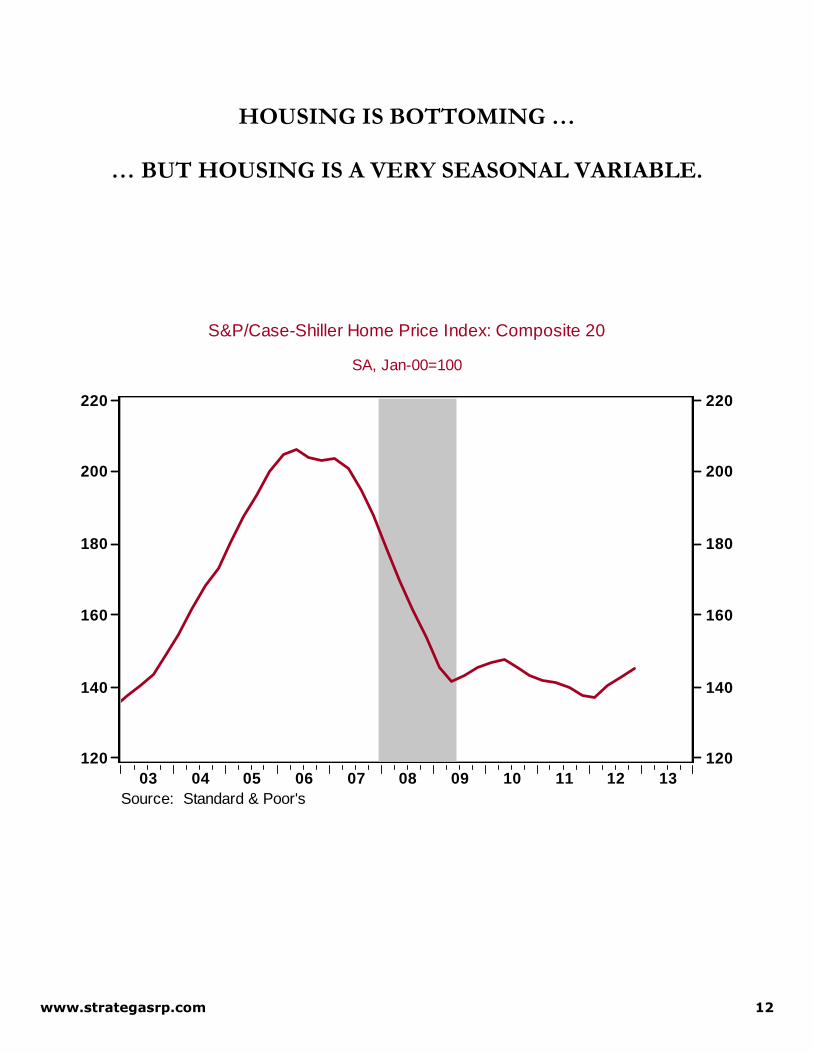

HOUSING IS BOTTOMING …

… BUT HOUSING IS A VERY SEASONAL VARIABLE.

S&P/Case-Shiller Home Price Index: Composite 20

SA, Jan-00=100

1312111009080706050403

Source: Standard & Poor's

220

200

180

160

140

120

220

200

180

160

140

120

www.strategasrp.com 13

HOUSING SEASONALITY MATTERS …

www.strategasrp.com 14

WHY IS U.S. FISCAL POLICY SO DIFFICULT TO FINISH?

There’s no market reason for a problem (Treasury rates low).

Debate not on deficits/crowding out, but on size of govt.

Federal Receipts as a Percentage of GDP

FY, %

1005009590858075706560555045403530

Source: Office of Management and Budget

24

20

16

12

8

4

0

24

20

16

12

8

4

0

Federal Outlays as a Percentage of GDP

FY, %

1005009590858075706560555045403530

Source: Office of Management and Budget

45.0

37.5

30.0

22.5

15.0

7.5

0.0

45.0

37.5

30.0

22.5

15.0

7.5

0.0

“Hauser’s Law”

www.strategasrp.com 15

3 TYPES OF TAXES:

1) INCOME

2) WEALTH

3) TRANSACTION

U.S. DEBT/GDP MUST GO SIDEWAYS AS A DEFINITION OF FISCAL SUSTAINABILITY

Debt

Nominal GDP

Taxes

Spending

Real GDP

Inflation

This ratio needs to go sideways long-term as a definition of fiscal sustainability (otherwise, interest costs would eventually consume the entire federal budget).

Population Productivity

www.strategasrp.com 16

WITH THE SLOWDOWN, INFLATION IS NOT A WORRY (FOR NOW).

REFLATION COMES BEFORE INFLATION.

Nonfarm Business Sector: Compensation Per Hour% Change - Year to Year SA, 2005=100

CPI-U: All Items% Change - Year to Year SA, 1982-84=100

1005009590858075706560

Source: Bureau of Labor Statistics

16

12

8

4

0

-4

16

12

8

4

0

-4

Compensation

www.strategasrp.com 17

INFLATION IS A LAGGING INDICATOR

Real GDP

CPI

www.strategasrp.com 18

MODEL OF CORE CPI STILL TAME.

TREND PRICE GROWTH SHOULD REMAIN NEAR THE FED’S FORECAST.

Model Equation: Core CPI Y/Y = -0.2 + 0.9x [Core CPI Y/Y, Lagged 1 Yr] + 0.2 x [U.S. Output Gap, Lagged 1YR] + 0.1 x [Import Price Deflator Y/Y – Core CPI Y/Y, Lagged 1 Yr]. Estimated 1962-2012 with an R2 of 84%.

www.strategasrp.com 19

THERE’S LITTLE EVIDENCE OF EITHER SUBSTANTIAL

INFLATION OR DEFLATION IN THE PIPELINE

CPI: All Items

Core CPI

Core Finished

Core Crude

www.strategasrp.com 20

THE SEQUESTERED FED RATE HIKES?

BY THE FOMC’S OWN METRICS, THE FED IS NOT DONE.

Civilian Unemployment Rate: 16 yr +

SA, %

1005009590858075706560Source: Bureau of Labor Statistics

12

10

8

6

4

2

12

10

8

6

4

2

www.strategasrp.com 21

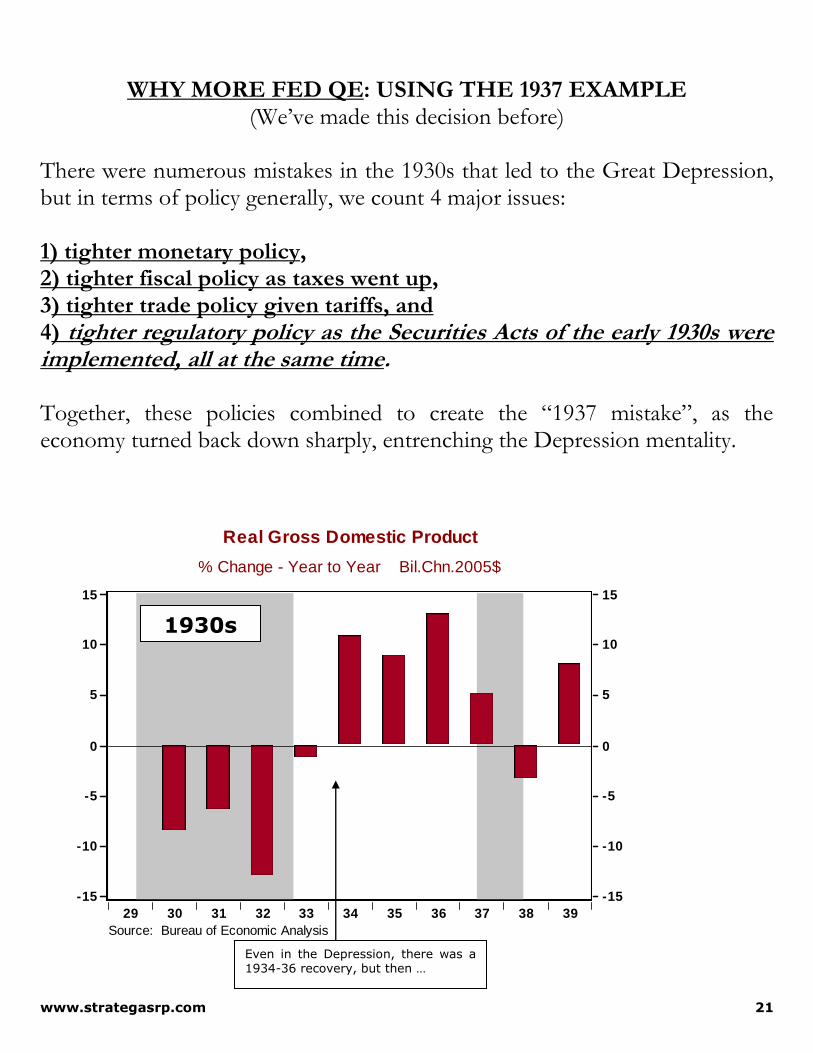

WHY MORE FED QE: USING THE 1937 EXAMPLE (We’ve made this decision before)

There were numerous mistakes in the 1930s that led to the Great Depression, but in terms of policy generally, we count 4 major issues: 1) tighter monetary policy, 2) tighter fiscal policy as taxes went up, 3) tighter trade policy given tariffs, and 4) tighter regulatory policy as the Securities Acts of the early 1930s were implemented, all at the same time. Together, these policies combined to create the “1937 mistake”, as the economy turned back down sharply, entrenching the Depression mentality.

Real Gross Domestic Product

% Change - Year to Year Bil.Chn.2005$

3938373635343332313029

Source: Bureau of Economic Analysis

15

10

5

0

-5

-10

-15

15

10

5

0

-5

-10

-15

1930s

Even in the Depression, there was a 1934-36 recovery, but then …

www.strategasrp.com 22

WHAT DOES FED QE DO?

1) Avoid Deflation (Inflation back to 2%) 2) Help unemployment come down ??

QE PRICE EFFECT RATHER THAN REAL ECONOMIC IMPACT

CPI-U: All Items

% Change - Year to Year SA, 1982-84=100

1312111009080706050403Source: Bureau of Labor Statistics

6

4

2

0

-2

6

4

2

0

-2

Civilian Unemployment Rate: 16 yr +

SA, %

1312111009080706050403Source: Bureau of Labor Statistics

10

9

8

7

6

5

4

10

9

8

7

6

5

4

Target

Target

Hit

Miss

www.strategasrp.com 23

MUDDLE-THROUGH?

HISTORICALLY, IT HAS TAKEN ROUGHLY 2% U.S. REAL GDP FOR PROFITS TO GO FLAT

Real Gross Domestic Product% Change - Year to Year SAAR, Bil.Chn.2005$

S&P 500 Composite: Operating Earnings per share% Change - Year to Year $/share

05009590

Sources: Bureau of Economic Analysis, Standard & Poor's

6

4

2

0

-2

40

20

0

-20

-40

GDP

www.strategasrp.com 24

ARE PROFIT MARGINS PEAKING?

GAP CURRENTLY BETWEEN GDP AND EMPLOYMENT.

Real Gross Domestic ProductSAAR, Bil.Chn.2005$

All Employees: Total NonfarmSA, Thous

1312111009080706050403020100

Sources: Bureau of Economic Analysis, Bureau of Labor Statistics

14000

13500

13000

12500

12000

11500

11000

138000

136000

134000

132000

130000

128000

PRODUCTIVITY (MORE OUTPUT PER WORKER) CAN GO TO:

1) RAISE WAGES

2) LOWER PRICES

3) HAVE MORE PROFIT

GDP, LHS

Employment

www.strategasrp.com 25

WATCHING LABOR’S SHARE OF INCOME FOR AN INDICATION OF PROFIT MARGINS.

U.S. Corporate Compensation % Corporate GDP

10050095908580757065605550

Source: Haver Analytics

70

68

66

64

62

60

58

70

68

66

64

62

60

58

LABOR DOWN, PROFITS UP.

www.strategasrp.com 26

U.S. UNEMPLOYMENT BY EDUCATIONAL DISTRIBUTION SHOWS CYCLICAL & STRUCTURAL UNEMPLOYMENT

Unemployment Rate: < HS Diploma: 25+ Years (SA, %)

Unemployment Rate: HS Diploma, No College: 25+ Years (SA, %)

Unemployment Rate: < Bachelor's Degree: 25+ Years (SA, %)

Unemployment Rate: College Graduates: 25+ Years (SA, %)

1312111009080706050403Source: BLS

16

12

8

4

0

16

12

8

4

0

www.strategasrp.com 27

HOLD THE BANKING SYSTEM TOGETHER, AND “FRACK” OUR WAY OUT OF THE CURRENT SITUATION?

NATURAL GAS PRICES HAVE ALREADY FALLEN, AND

EXPECTATIONS ARE BUILDING THEY WILL STAY LOW.

Natural Gas Price, Henry Hub, LA

$/mmbtu

10050095Source: Wall Street Journal

15.0

12.5

10.0

7.5

5.0

2.5

0.0

15.0

12.5

10.0

7.5

5.0

2.5

0.0

A study, funded by the nonpartisan Alfred P. Sloan Foundation and performed by the University

of Texas, examined 15,000 wells drilled in the Barnett Shale formation in northern Texas, mostly

over the past decade. It is among the first to study the geology and economics of shale drilling.

Looking at data from actual wells rather than relying on estimates and extrapolations, the study

broadly confirms conclusions by the energy industry and the U.S. government, which in December

forecast rising gas production.

WSJ, 2/27/2013

www.strategasrp.com 28